EFFECT OF SMALL AND MEDIUM SCALE ENTERPRISES ON …transcampus.org/JORINDV15Jun2017/2.pdf · EFFECT...

13

JORIND 15(1)June, 2017. ISSN 1596-8303. www.transcampus.org/journal; www.ajol.info/journals/jorind 8 EFFECT OF SMALL AND MEDIUM SCALE ENTERPRISES ON ECONOMIC GROWTH IN NIGERIA Omonigho Tonia Okhankhuele Department of Business Administration, Federal University of Technology, Akure, Nigeria E-mail: [email protected] +234-806-2824-074 Abstract This paper recognised SMEs as source of economic growth in Nigeria. The paper identified SMEs’ contribution to Nigeria’s Gross Domestic Product (GDP) from 1982 to 2012, and carried out analysis on the effect of SMEs on economic growth in Nigeria, within the same period. Secondary data were collected from CBN Statistical Bulletin (2002, 2013, 2015), Central Bank of Nigeria, Annual Report and Statement of Accounts (2011; 2012), and National Bureau of Statistics –Job Creation and Employment Surveys (2012). Data were analyzed using Pearson Product-Moment Correlation Coefficient (PPMCC). The study disclosed that there is a significant and positive relationship between SME’s contribution to Nigeria’s Gross Domestic Product (GDP) and Nigeria’s GDP from 1982 to 2012. The paper recommended that Government should make good policies and carry out concerted effort towards the development of SMEs in order to make them serve as the source of economic growth in Nigeria. Keywords: SMEs, economy, growth, effect Introduction There is a general consensus by several authors that Small and Medium Scale Enterprises (SMEs) are cornerstones for growth, industrialization and development in numerous countries around the globe. The importance of SMEs to nations is overwhelming. SMEs have been identified as the source of development for the developed nations, especially the newly industrialized countries like, Thailand, China, Taiwan, Indonesia, Malaysia, South Korea, Singapore, among others. They make up the major percentage of businesses in the globe and play extraordinary roles in delivery of goods and services, generating employment, enhancing standard of living, and significantly contribute to the Gross Domestic Products (GDPs) of several countries (Organization for Economic Cooperation and Development (OECD), 2000). Ofoegbu, Akanbi and Joseph (2013) affirmed that SMEs are the solution to economic development of several developing countries, including Nigeria. SMEs are regarded as the seed of big businesses, the energy that propels national economic engine and assiduous creator of jobs (Abor and Quartey, 2010). They serve as a source of economic growth and development (Ojeka, 2011; Lawal, 2014; Basil; 2005; Aruwa, 2006; Mensah, 2004; Ariyo, 2005; Ashamu, 2014). SMEs comprise 97% of the entire economy (Oke and Aluko, 2015), and aid as a base for creating innovation, employment, competition and economic vitality which in the long run results into poverty alleviation and national growth (Ojeka, 2011). The importance of SMEs has propelled several nations including Nigeria, to initiate several policies to aid the development of SMEs. Some of these efforts as identified by some scholars such as: Terungwa (2012); Aladekomo (2003); Lawal, (2014); Ayeni- Agbaje and Osho (2015) among others include: the establishment of financial institutions and initiation of several funding programmes to aid the development of SMEs in Nigeria, and initiation of specialized banks and other credit agencies/schemes to make funding available to the sub-sector. These specialized banks and institutions include among others: The Nigerian Industrial Development Bank (NIDB) which was established in 1964, to make available, medium and long term funds, to medium and large – scale enterprises, Nigeria Bank for Commerce and Industry (NBCID) in 1973, which was created to make financial services and other allied services available to indigenous enterprises especially SMEs, and the Small and Medium Industries Equity Investment Scheme (SMIEIS) which was established in 2001, to make financial and technical services available to SMEs. SMIEIS made it a prerequisite for all banks to set aside ten percent of their Profit after Tax (PAT) for equity investment and promotion of SMEs. The established banks were to link up with the Small and Medium Scale Enterprises Development Agencies in Nigeria (SMEDAN) in implementing SMIEIS scheme (Ayeni-Agbaje and Osho, 2015). Yet, the rate of mortality of Small firms in Nigeria is still very high (Ojeka, 2011; Onugu, 2005). There is no universally acceptable definition of SMEs over the globe because the categorization of businesses into small, medium or large scale is founded on qualitative and subjective judgment (Ogboru, 2007). Therefore, the numerical definition of SMEs differs from one country to another and commonly depends on assets’ value or number of employees (Ahiawodzi and Adade, 2012). The

Transcript of EFFECT OF SMALL AND MEDIUM SCALE ENTERPRISES ON …transcampus.org/JORINDV15Jun2017/2.pdf · EFFECT...

JORIND 15(1)June, 2017. ISSN 1596-8303. www.transcampus.org/journal; www.ajol.info/journals/jorind

8

EFFECT OF SMALL AND MEDIUM SCALE ENTERPRISES ON ECONOMIC GROWTH IN NIGERIA

Omonigho Tonia Okhankhuele Department of Business Administration, Federal University of Technology, Akure, Nigeria

E-mail: [email protected] +234-806-2824-074 Abstract This paper recognised SMEs as source of economic growth in Nigeria. The paper identified SMEs’ contribution to Nigeria’s Gross Domestic Product (GDP) from 1982 to 2012, and carried out analysis on the effect of SMEs on economic growth in Nigeria, within the same period. Secondary data were collected from CBN Statistical Bulletin (2002, 2013, 2015), Central Bank of Nigeria, Annual Report and Statement of Accounts (2011; 2012), and National Bureau of Statistics –Job Creation and Employment Surveys (2012). Data were analyzed using Pearson Product-Moment Correlation Coefficient (PPMCC). The study disclosed that there is a significant and positive relationship between SME’s contribution to Nigeria’s Gross Domestic Product (GDP) and Nigeria’s GDP from 1982 to 2012. The paper recommended that Government should make good policies and carry out concerted effort towards the development of SMEs in order to make them serve as the source of economic growth in Nigeria. Keywords: SMEs, economy, growth, effect Introduction There is a general consensus by several authors that Small and Medium Scale Enterprises (SMEs) are cornerstones for growth, industrialization and development in numerous countries around the globe. The importance of SMEs to nations is overwhelming. SMEs have been identified as the source of development for the developed nations, especially the newly industrialized countries like, Thailand, China, Taiwan, Indonesia, Malaysia, South Korea, Singapore, among others. They make up the major percentage of businesses in the globe and play extraordinary roles in delivery of goods and services, generating employment, enhancing standard of living, and significantly contribute to the Gross Domestic Products (GDPs) of several countries (Organization for Economic Cooperation and Development (OECD), 2000). Ofoegbu, Akanbi and Joseph (2013) affirmed that SMEs are the solution to economic development of several developing countries, including Nigeria. SMEs are regarded as the seed of big businesses, the energy that propels national economic engine and assiduous creator of jobs (Abor and Quartey, 2010). They serve as a source of economic growth and development (Ojeka, 2011; Lawal, 2014; Basil; 2005; Aruwa, 2006; Mensah, 2004; Ariyo, 2005; Ashamu, 2014). SMEs comprise 97% of the entire economy (Oke and Aluko, 2015), and aid as a base for creating innovation, employment, competition and economic vitality which in the long run results into poverty alleviation and national growth (Ojeka, 2011). The importance of SMEs has propelled several nations including Nigeria, to initiate several policies to aid the development of SMEs. Some of these efforts as identified by some scholars such as: Terungwa

(2012); Aladekomo (2003); Lawal, (2014); Ayeni-Agbaje and Osho (2015) among others include: the establishment of financial institutions and initiation of several funding programmes to aid the development of SMEs in Nigeria, and initiation of specialized banks and other credit agencies/schemes to make funding available to the sub-sector. These specialized banks and institutions include among others: The Nigerian Industrial Development Bank (NIDB) which was established in 1964, to make available, medium and long term funds, to medium and large – scale enterprises, Nigeria Bank for Commerce and Industry (NBCID) in 1973, which was created to make financial services and other allied services available to indigenous enterprises especially SMEs, and the Small and Medium Industries Equity Investment Scheme (SMIEIS) which was established in 2001, to make financial and technical services available to SMEs. SMIEIS made it a prerequisite for all banks to set aside ten percent of their Profit after Tax (PAT) for equity investment and promotion of SMEs. The established banks were to link up with the Small and Medium Scale Enterprises Development Agencies in Nigeria (SMEDAN) in implementing SMIEIS scheme (Ayeni-Agbaje and Osho, 2015). Yet, the rate of mortality of Small firms in Nigeria is still very high (Ojeka, 2011; Onugu, 2005). There is no universally acceptable definition of SMEs over the globe because the categorization of businesses into small, medium or large scale is founded on qualitative and subjective judgment (Ogboru, 2007). Therefore, the numerical definition of SMEs differs from one country to another and commonly depends on assets’ value or number of employees (Ahiawodzi and Adade, 2012). The

JORIND 15(1)June, 2017. ISSN 1596-8303. www.transcampus.org/journal; www.ajol.info/journals/jorind

9

National Council of Industry defined a medium scale enterprise as any company with operating assets less than ₦200 million, and employing less than 300 persons. A small-scale enterprise is one that has total assets less than ₦50 million, with less than 10 employees. Annual turnover was not considered in its definition of an SME. The National Economic Reconstruction Fund (NERFUND) defined a SSE as one whose total assets is less than ₦10 million, but made no reference either to its annual turnover or the number of employees. The Central Bank of Nigeria

(CBN), also defined medium scale enterprise as any company with operating assets less than ₦150 million, annual turnover less than ₦150 million employing less than 100 persons. A small-scale enterprise, on the hand, is one that has total assets less than ₦1 million, annual turnover less than ₦1 million with less than 50 employees (World Bank, 2001). However, the National Policy on Micro, Small and Medium Scale Enterprises (MSMEs) (2012), classified MSMEs in the table 1 below:

Table 1: Classification of SMEs by Assets and Employment S/N Size Category Employment Assets (N Million), (excl. land and buildings)

1 Micro Enterprises Less than 10 Less than 5 2 Small Enterprises 10 to 49 5 to less than 50 3 Medium Enterprises 50 to 199 50 to less than 500 Source: National Policy on MSMEs (2012) Simon Kuznets defined economic growth of a country as “a long-term rise in the capacity to supply increasingly diverse economic goods to its population, this growing capacity is based on advanced technology and the institutional and ideological adjustments that it demands”. Growth is thus objective, measurable and describes advancement in income, consumption, output, capital, labour force, among others (Todaro, 1885). Economic growth takes place when the productive capacity of a nation rises, and this is used to produce additional goods and services (Jhingan, 1997). Economic growth is therefore measured by the increase in the amount of goods and services that are produced in a country.

In spite of the roles being played by SMEs in economic development of nations, SMEs in Nigeria appear to be saddled with multitudes of problems including: financial, technological, among others which have hindered the progress of the sector and its contribution to the development of Nigeria. The main objective of this study is to evaluate the effect of SMEs on the growth of Nigeria’s economy, from 1982 to 2012. The specific objectives are to: identify SMEs contribution to Nigeria’s Gross Domestic Product (GDP) from 1982 to 2012, and examine the effect of SMEs on the growth of Nigeria’s economy, within the same period. Statement of the problem Small and Medium Enterprises (SMEs) have been acknowledged as a source of growth, industrialization and development in numerous countries in the globe. Several scholars including: Basil (2005), Ariyo (2005), Ojeka (2011), Abor and Quartey (2010), Oke and

Aluko (2015) among others have admitted that SMEs play energetic roles in the industrialization, growth, development of several nation, propels the national economic engine and serves as proficient productive job creator. Despite the establishment of specialized banks and other credit agencies/schemes to make funding available to SMEs, their situation has barely changed in terms of improving their performances. SMEs are still trying to access both financial and non-financial services provided by commercial and development banks. In Nigeria, SME sector has remained rather small in terms of its contribution to GDP and gainful employment, and has remained stagnant (Lawal, 2014). Although a lot of scholars from the field of Business Administration, Economics, Accounting, among others, have carried out research on the effect of SMEs on Economic Development in Nigeria (Onyeiwu, 2012; Akingunola, 2011). Their focus was majorly on the effect of the loan/credit granted by banks to SMEs in Nigeria on Nigeria’s Gross Domestic Product (GDP). Therefore, they compared the total loan/credit granted by banks to SMEs in Nigeria with Nigeria’s Gross Domestic Product (GDP) over a period of time, without comparing SMEs’ contribution (which depicts SMEs’ output), with GDP over the years. This is the gap that this study intends to fill. While some of the authors who carried out related studies (Akingunola, 2011; Onyeiwu, 2012; among others) concluded that there is a significant and positive relationship between SMEs financing (which was used to represent SMEs growth) and economic growth in Nigeria (represented by GDP), other authors (Abiola, Iyoha and Joseph, 2011; Basil, 2005) stated that the SMEs’ sector’s contribution to GDP has been somewhat small, SMEs has

JORIND 15(1)June, 2017. ISSN 1596-8303. www.transcampus.org/journal; www.ajol.info/journals/jorind

10

performed below expectation and is still far from attaining its targeted standards. There is therefore the need to evaluate the effect of SMEs on the growth of Nigeria’s economy by comparing SMEs’ share in GDP with Nigeria’s GDP from 1982 to 2012, in order to establish the relationship between the two variables. Hence the need for this study. Previous research Percentage of SMEs to total firms, employment and gross domestic product in African countries The Federal Office of Statistics carried out a study which showed that in Nigeria, Small and Medium Enterprises comprise 97% of the economy (Ariyo, 2005; Ogbuanu, Kabuoh and Okwu, 2014). MSMEs presently contribute about 50% to the nation’s Gross Domestic Product (Evbuomwan, Ikpi, Okoruwa, and Akinyosoye, 2013; Odeyemi, 2003). There are submissions that the SMEs sub-sector may perhaps encompass about 87 per cent of the total firms operating in Nigeria, excluding informal – enterprises (Ayeni-Agbaje and Osho, 2015). Averagely, SMEs represent above 90% of the enterprises and make up 50 to 60% of employment in lots of African countries. According to Abor and Quartey, (2010), SMEs in Ghana have been acknowledged to have made available about 85% of manufacturing employment in Ghana. They are also believed to contribute around 70% to Ghana’s Gross Domestic Product (GDP) and comprise around 92% of businesses in Ghana. SMEs have been known to offer about 85% of manufacturing employment in Ghana (Aryeetey, 2001). In South Africa, SMEs represent 91% of the formal business entities, contribute between 52% and 57% to GDP and offer about 61% of employment (Central Statistical Services (CSS) (1998); Ntsika, 1999; Gumede, 2000; Berry, Von Blottnitz, Cassim, Kesper, Rajaratnam, and Van Seventer, 2002). Okpara and Wynn, (2007) affirmed that SMEs contribute about 20% to 45% full employment and equally contribute about 30% to 50% to rural income which are mostly house-holds. Nigeria SMEs make available around 50% of all the jobs and enable our natural resources to be utilized due to their high innovativeness. This helps to raise the wealth of the nation via higher productivity (Ogbuanu et al., 2014). They have also aided in enhancing the standard of living of a lot of people, particularly those leaving in the rural areas. Data presented by the Registrar General’s Department specifies that 90% of the registered companies are micro, small and medium enterprises in Ghana (Mensah, 2004). Small scale businesses comprise over ten percent of the total registered

companies in Nigeria (Ayeni-Agbaje and Osho, 2015). About 50% of the total jobs in Nigeria are made available by SMEs (Ojeka, 2011). SMEs comprised around 70 percent of industrial employment in Nigeria in 1987 and this has basically been the same situation over the years (Omwumere, 2000). It other developing countries, the same situation occurs. In these countries, it is projected that SMEs employ 22 percent of the adult population. Precisely, around 15.5 percent and 13.9 per cent of the labour force is employed by the SMEs’ sector which is greater employment growth in comparison with micro and large scale enterprises which employ 5 percent and 11 percent in Ghana and Malawi respectively (Kayanula and Qaurtey, 2000). SMEs comprises above 60 percent of Gross Domestic Product (GDP) and 70 percent of over-all employment. Income countries of middle income, SMEs produced close to 70 percent of GDP and 95 percent of the entire employment, and in Organization for Economic Cooperation and Development (OECD) countries, SMEs make up the bulk of firms, contribute over 55 percent to GDP and makes up 65 percent of the entire employment (Basu, Blavy and Yulck, 2005). Importance and contributions of SMEs to nations Numerous importance and contributions have been adduced to SMEs in several parts of the world, by various authors. Ayeni-Agbaje and Osho, stated that Small and Medium Enterprises perform an essential role in both developed and developing countries in the globe. SMEs encompass the key majority of the world’s economies (Ojeka, 2011). They expedite economic growth and national development (Lawal, 2014). Some authors including Ayeni-Agbaje and Osho (2015), Adjei, (2012), Oke and Aluko (2015), Owualah (1987), Cook and Nixon (2000), Beck, Demirguc-Kunt and Levine (2005), Ojo (1992), Mensah (2004). Omwumere (2000), Ojeka (2011), Ahiawodzi and Adade (2012), World Bank (1995), Terungwa (2012), Olowe, Moradeyo and Babalola (2013), among others, agreed that SMEs are real apparatuses for realizing national objectives, with reference to the generation of employment at little investment cost, development of entrepreneurial capabilities, inspiring indigenous entrepreneurship and technology, economic growth, decreasing people’s migration from rural to urban areas, immense contribution to Gross Domestic Product (GDP), economic growth and development. SMEs acts as a source of generating employment for numerous citizens, assists in the process of industrialization, import substitution and export earnings of all countries. It also helps to stabilize income, lessen poverty and unemployment in numerous developing countries, requires least possible skill to be

JORIND 15(1)June, 2017. ISSN 1596-8303. www.transcampus.org/journal; www.ajol.info/journals/jorind

11

established, upturns productivity and aids in the utilization of human and capital resources that would have been left idle if they had to wait for huge sum of money to start large scale businesses.

In addition to the above contributions, Ayeni-Agbaje and Osho (2015) reported that, the Bolton committee of inquiry that was instituted in the United Kingdom in 1968 to assess the role of Small Scale Enterprise in the British economy, stated that these enterprises carry out two significant roles as: breeding ground for novel industries and source of vigorous competition. In the United states of America, SMEs have played an essential part in the changeover of the country from industrial era to the post-industrial technology period (Lawal, 2014; Ayeni-Agbaje and Osho, 2015). It is commendable to recognize that a massive percentage of Nigerians directly or indirectly depend on SMEs for subsistence (Ojeka, 2011). Interestingly, Stiglitz and Uy (1996) revealed that the East Asian countries’ phenomenon was occasioned by the zeal ascribed to the SMEs sub-sector, that engendered the upsurge in exports and resultant advancement of the industrial sector. Indeed, the newly industrialized countries like China, South Korea, Indonesia, Singapore, Malaysia, Taiwan, among others, achieved economic growth through SMEs’ activities that later led to the transformation of Large-Scale enterprises (Aruwa, 2006). They are capable of withstanding hostile economic conditions due to their flexible nature (Kayanula and Quartey, 2000). Panitchpakdi (2006) views SMEs as a source of competition, economic dynamism, employment and innovation which arouses the spirit of entrepreneur and skills’ diffusion.

In contrast to the findings above, Abiola et al. (2011) stated that SMEs’ sector has been stagnated and remains somewhat small with regards to its contribution to GDP or lucrative employment in Nigeria. Even though there are indications that the sector has improved considerably since 1999, it is still far from attaining its targeted standards as the sector is confronted with numerous limitations which include inadequate credit availability that hampers its growth. Basil (2005) submitted that, in the case of Nigeria, SMEs have performed below anticipation as a result of a mixture of problems, including their attitude and habits, instability of governments, environmental related factors, and repeated changes in government policy. He further asserted that SMEs in Nigeria have not performed plausibly well and therefore have not played the anticipated essential and vivacious role in Nigeria’s economic growth and development. Problems militating against the SMEs

SMEs sector’s development in developing countries has been hampered by a lot of factors which contribute to the rate of SMEs failure (Arinaitwe, 2006). Numerous authors including Oke and Aluko (2015), Ayeni-Agbaje and Osho (2015), Ogechuku (2006), Basil (2005), Levy (1993), Okpara, 2000, Cook and Nixson (2000), and Parker et al. (1995), recognized many factors that lead to ill-timed demise of SME in Nigeria. Key among these factors is inadequate capital occasioned by difficulties in accessing funds from banks. SMEs seem to be deficiency in both equity financing and debt (Ahiawodzi and Adade, 2012). Commercial banks are usually hesitant to give loan to SMEs due to the presumed risky nature of SMEs (Onugu, 2005; Ashamu, 2014). Liedholm, MacPherson and Chuta (1994) concluded that SMEs perish owing to non-financial reasons, while Green et al. (2002) concluded that difficulties in obtaining required property rights or licenses, and keeping proper records are in some ways more necessary to running a small enterprise, than finance. Oguntoye (1984) concluded that Small-Scale Enterprises have no financial departments at all, a small number of them that have, keep ill and ineffectively managed ones. A lot of them depend on one-year annual financial report patched together by external financial analyst when many things have already gone wrong. Also, Oyefuga, Siyanbola, Afolabi, Dada, and Egbetokun, (2010)’s study identified uncoordinated business plans and poorly packaged projects as the most significant reasons for SMEs’ inability to access funds from the scheme. Again, Kayanula and Quartey, (2000) affirmed that Lack of antitrust legislation favours larger firms, while lack of protection for property rights limits SMEs’ access to foreign technologies. Ayeni-Agbaje and Osho (2015) postulated that SMEs tend to be deficient in management and organizational structure, which exist in large-scale entrepreneur. Ayeni-Agbaje and Osho (2015), Afolabi (2013), World Bank (2001), Aruwa (2004), Steel and Webster, (1991), Aryeetey et al. (1994), Sowa et al., (1992) Parker et al. (1995), Kayanula and Quartey (2000), among others, enumerated numerous factors that pose as barriers to financing SMEs in Nigeria. Some of these factors include: lack of collateral, cost of capital, unsuitable bank loans terms and lack of equity capital, unwillingness of banks, particularly commercial banks, to lend to SME sector. A lot of SMEs’ entrepreneurs live in their own houses in rural communities or in hired properties in towns. Unfortunately, houses or estates in rural areas may perhaps not be qualified to be accepted as collateral security (Iniodu and Udomesiet, 2004) in (Ayeni-

JORIND 15(1)June, 2017. ISSN 1596-8303. www.transcampus.org/journal; www.ajol.info/journals/jorind

12

Agbaje and Osho, 2015). Borrowing from the commercial banks is herculean to the SMEs. Besides the interest rates of between 22 and 35 percent, there are other charges which include administrative/management fee, concession fee, processing fee, and too many others (Owenvbiugie and Igbinedion, 2015). The deposit money banks whose duty it is to assist SMEs financially, could just be characterized as generally unstable and unreliable, in meeting the needs of these medium and small scale enterprises (Uzonwanne, 2015). Meanwhile, Mago and Toro (2013), World Bank (1995), Opara (2000), World Bank (2001), Ogechukwu (2006), Basil (2005), Oboh (2002), Onugu (2005), Evbuomwan, Ikpi, Okoruwa, and Akinyosoye, (2013), Ayeni-Agbaje and Osho (2015), Adjei (2012), Aryeetey et al. (1994), Aderemi (2003) Areetey and Ahene (2004), Abor and Quartey (2010), among others, outlined some other factors that inhibit the success of SMEs to include: high costs of start-up for firms, as well as licensing and registration requirements, lack of entrepreneurial spirit and drive, high cost of resolving legal claims and too much delays in court proceedings, insufficient market research, overconcentration on one or two markets for finished products, corruption and absence of transparency, absence of succession plans, incapability of producing or paying for a feasibility study or business plan, absence. Other factors include: poor interpersonal skills, untrustworthy employees, economic downturn, narrow thinking and quick-fix anticipations and poor corporate governance, multiple taxation and levies, absence of contemporary technology for processing and preserving products, policy reversals, data insufficiencies and epileptic power supply, insufficiencies occasioned from high decrepit state of infrastructural facilities (roads, water, among others).

Aryeetey et al., (1994) opined that poor quality control and standardization of product, inadequate international marketing experience and limited access to international partners, consistently hinder the expansion of SMEs’ into international markets. Also,

SMEs do not have the necessary information about foreign markets. Steel and Webster (1992) stated that sequel to price liberalization the high cost of local raw materials, together with agricultural goods, was confirmed to be extortionate for smaller enterprises engaging between 10-29 employees in Ghana. Interestingly, Ayeni-Agbaje and Osho (2015) reported that some of the small-scale industrialist come up to bankers with vague projects which banks find no degree of confidence in. Usually, SMEs find it difficult to gain access to suitable technologies and information on techniques which are available. A lot of cases, SMEs employ foreign technology with a limited percentage of joint ownership or leasing, and acquire foreign licenses, since local patents are hard to obtain (Aryeetey, Baah-Nuakoh, Duggleby, Hetting, and Steel, 1994). There still exists a gap in skills in the entire SME sector (Kayanula and Quartey, 2000). This can be adduced to the inability of entrepreneurs to afford the cost of training and advisory services which is high, while some SMEs see no need in upgrading their skills owing to smugness. Several potential entrepreneurs have no clear vision and mission of what they wish to do (Onugu, 2005).

Method Since the broad objective of this study is to examine the effect of SMEs on the growth of Nigeria’s economy, from 1982 to 2012, secondary data on the yearly share of all manufacturing SMEs (independent variable) in Nigeria, in GDP (N Billion) from 1982-2012 and the GDP (N Billion) (dependent variable) were selected from CBN Statistical Bulletin (2002, 2013, 2015), Central Bank of Nigeria, Annual Report and Statement of Accounts (2011; 2012), and National Bureau of Statistics–Job Creation and Employment Surveys (2012). Pearson Product-Moment Correlation Coefficient (PPMCC) was used to measure the strength and direction of the linear relationship between the two variables. Results and discussion

JORIND 15(1)June, 2017. ISSN 1596-8303. www.transcampus.org/journal; www.ajol.info/journals/jorind

13

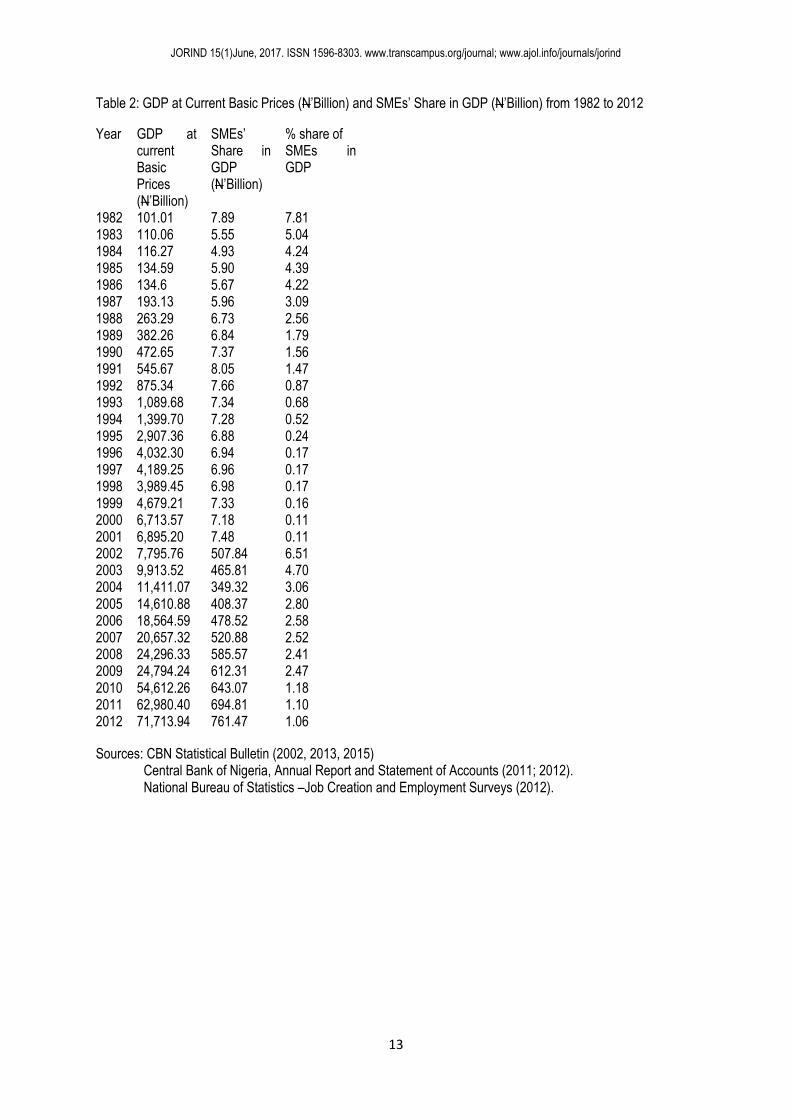

Table 2: GDP at Current Basic Prices (N’Billion) and SMEs’ Share in GDP (N’Billion) from 1982 to 2012

Sources: CBN Statistical Bulletin (2002, 2013, 2015) Central Bank of Nigeria, Annual Report and Statement of Accounts (2011; 2012). National Bureau of Statistics –Job Creation and Employment Surveys (2012).

Year

GDP at current Basic Prices (N’Billion)

SMEs’ Share in GDP (N’Billion)

% share of SMEs in GDP

1982 101.01 7.89 7.81 1983 110.06 5.55 5.04 1984 116.27 4.93 4.24 1985 134.59 5.90 4.39 1986 134.6 5.67 4.22 1987 193.13 5.96 3.09 1988 263.29 6.73 2.56 1989 382.26 6.84 1.79 1990 472.65 7.37 1.56 1991 545.67 8.05 1.47 1992 875.34 7.66 0.87 1993 1,089.68 7.34 0.68 1994 1,399.70 7.28 0.52 1995 2,907.36 6.88 0.24 1996 4,032.30 6.94 0.17 1997 4,189.25 6.96 0.17 1998 3,989.45 6.98 0.17 1999 4,679.21 7.33 0.16 2000 6,713.57 7.18 0.11 2001 6,895.20 7.48 0.11 2002 7,795.76 507.84 6.51 2003 9,913.52 465.81 4.70 2004 11,411.07 349.32 3.06 2005 14,610.88 408.37 2.80 2006 18,564.59 478.52 2.58 2007 20,657.32 520.88 2.52 2008 24,296.33 585.57 2.41 2009 24,794.24 612.31 2.47 2010 54,612.26 643.07 1.18 2011 62,980.40 694.81 1.10 2012 71,713.94 761.47 1.06

JORIND 15(1)June, 2017. ISSN 1596-8303. www.transcampus.org/journal; www.ajol.info/journals/jorind

14

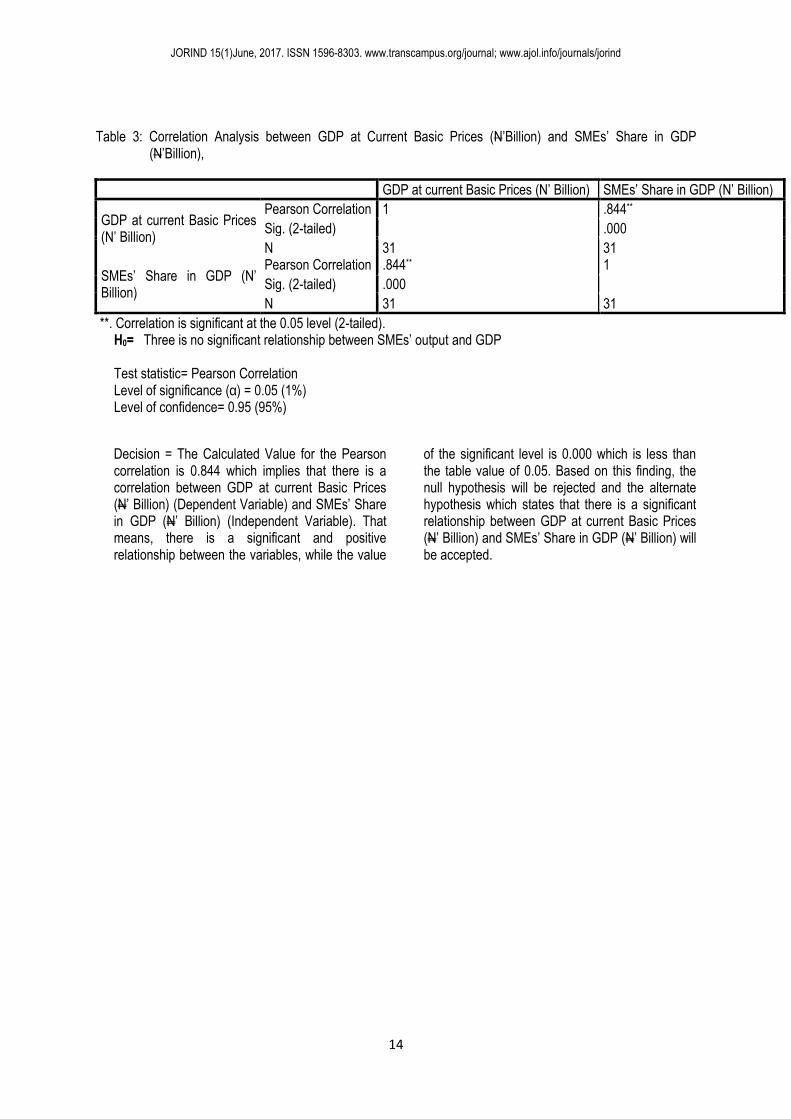

Table 3: Correlation Analysis between GDP at Current Basic Prices (N’Billion) and SMEs’ Share in GDP

(N’Billion),

GDP at current Basic Prices (N’ Billion) SMEs’ Share in GDP (N’ Billion)

GDP at current Basic Prices (N’ Billion)

Pearson Correlation 1 .844**

Sig. (2-tailed) .000

N 31 31

SMEs’ Share in GDP (N’ Billion)

Pearson Correlation .844** 1

Sig. (2-tailed) .000

N 31 31

**. Correlation is significant at the 0.05 level (2-tailed). H0= Three is no significant relationship between SMEs’ output and GDP Test statistic= Pearson Correlation Level of significance (α) = 0.05 (1%) Level of confidence= 0.95 (95%)

Decision = The Calculated Value for the Pearson correlation is 0.844 which implies that there is a correlation between GDP at current Basic Prices (N’ Billion) (Dependent Variable) and SMEs’ Share in GDP (N’ Billion) (Independent Variable). That means, there is a significant and positive relationship between the variables, while the value

of the significant level is 0.000 which is less than the table value of 0.05. Based on this finding, the null hypothesis will be rejected and the alternate hypothesis which states that there is a significant relationship between GDP at current Basic Prices (N’ Billion) and SMEs’ Share in GDP (N’ Billion) will be accepted.

JORIND 15(1)June, 2017. ISSN 1596-8303. www.transcampus.org/journal; www.ajol.info/journals/jorind

15

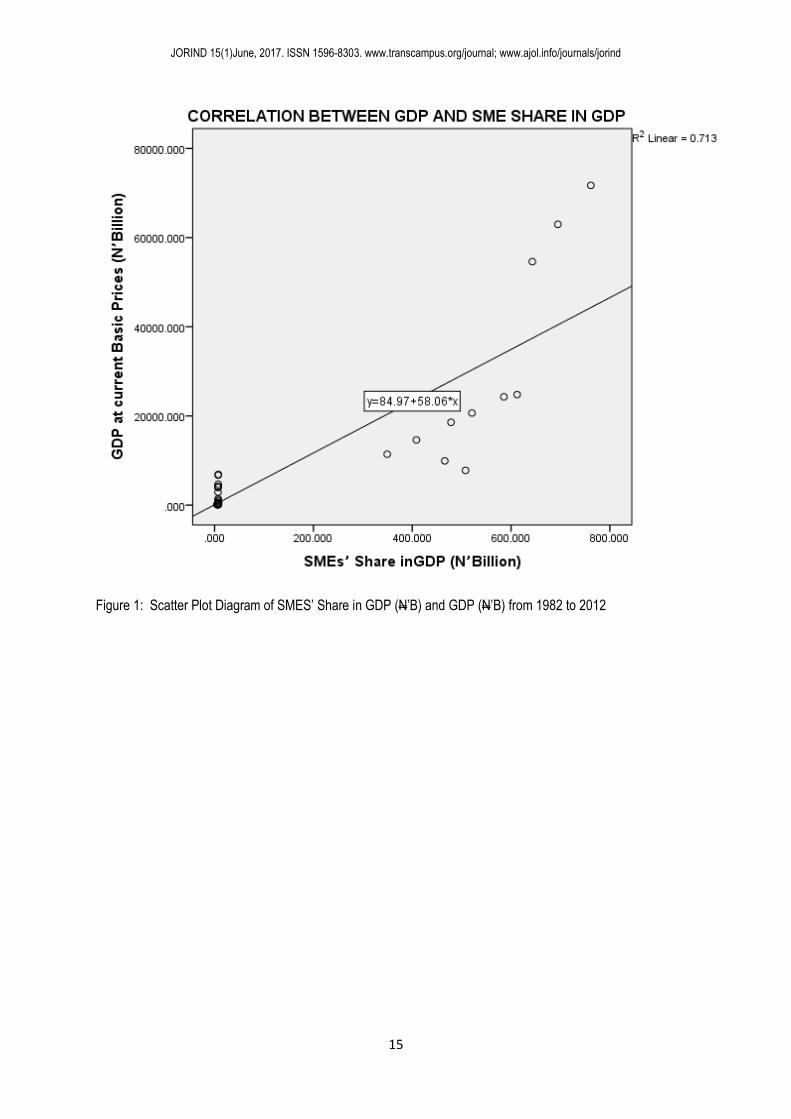

Figure 1: Scatter Plot Diagram of SMES’ Share in GDP (N’B) and GDP (N’B) from 1982 to 2012

JORIND 15(1)June, 2017. ISSN 1596-8303. www.transcampus.org/journal; www.ajol.info/journals/jorind

16

Goodness of Fit Test (R2): From the result obtained in the scatter plot, R2 is 0.713 showing a goodness of fit of 71.3%, on the grounds that the explanatory variable explains 71.3% of the explained or dependent variable (GDP). Coefficient of determination (R2) From the result, the coefficient of determination R2 which is 0.713 shows that the explanatory variables adequately explained the behaviour of the dependent variable (GDP). The result shows that approximately 71.3% of the variation in the dependent variable is explained by the explanatory variables.

Conclusion It can be inferred from the result above that there is a significant and positive relationship between SMEs’ growth and GDP in Nigeria, from 1982 to 2005. The Calculated Value for the Pearson correlation is 0.844 which means that there is a correlation between GDP at current Basic Prices (N’ Billion) (Dependent Variable) and SMEs’ Share in GDP (N’ Billion) (Independent Variable). This shows that there is a significant and positive relationship between the variables. Also, the value of the significant level is 0.000 which is less than the table value of 0.05. The study concluded that, there is a significant and positive relationship between SME’s contribution to Nigeria’s Gross Domestic Product (GDP) and Nigeria’s GDP from 1982 to 2012. The paper therefore recommended that Government should make more policies and carry out concerted effort towards the development of SMEs in order to make them further serve as the source of economic growth in Nigeria. References Abiola, B., Iyoha, F., and Joseph, T. (2011).

Microfinance and Micro, Small and Medium Enterprises Development in Nigeria. Unpublished Article, Covenant University, Ota, Ogun State, Nigeria.

Abor, J and Quartey, P. (2010). Issues in SMEs in

Ghana and South Africa. International Research, Journal of Finance and Economics. Issue 39. http://www.eurojournals.com/irjfe_39_15.pdf pp. 218-228.

Aderemi, A. (2003). Small and Medium Scale Enterprises: The Nigerian Situation. [Power Point Slides] Capital Partners Limited. Retrieved from www.capitalpartnersltd.com/Small%20Medium%20Scale.ppt

Adjei, D. S. (2012). Micro, Small and Medium Scale

Enterprises in Ghana: Challenges and Prospects. A Case Study of Sekondi-Takoradi Metropolis. A Thesis submitted to the Institute of Distance Learning, Kwame Nkrumah University of Science and Technology in partial fulfillment of the requirements for the degree of Commonwealth Executive Masters in Business Administration February 2012. pp. 15-40.

Afolabi, M. O. (2013). Growth Effect of Small and

Medium Enterprises (SMEs) Financing in Nigeria. Journal of African Macroeconomic Review. Vol. 3(1). pp. 193-205.

Ahiawodzi, A. K. and Adade, T. C. (2012). Access

to Credit and Growth of Small and Medium Scale Enterprises in the Ho Municipality of Ghana. British Journal of Economics, Finance and Management Sciences. November 2012. ISSN 2048-125X. Vol. 6 (2). pp. 34-51.

Akingunola, R. O. (2011). Small and Medium Scale

Enterprises and Economic Growth in Nigeria: An Assessment of Financing Options. Pakistan Journal of Business and Economic Review. Vol. 2, No1. pp. 78-97.

Akingunola, R. O. (2011). “Small and Medium Scale

Enterprises and Economic Growth in Nigeria: An Assessment of Financing Options”. Pakistan Journal of Business and Economic Review, 2(1,

Aladekomo, F. O. (2003). The Small and Medium

Enterprises’ (SME) Landscape: Environment, Government Policies, Programmes, and Institutional Support”, A paper delivered at the two-day workshop on “Strategies for Operationalizing Small and Medium Industries Equity Investment Scheme (SMIES) in Nigeria. On 23-24 August, 2003, at WEMA Bank Training School, Oba Akran Avenue, Ikeja, Lagos, Nigeria.

JORIND 15(1)June, 2017. ISSN 1596-8303. www.transcampus.org/journal; www.ajol.info/journals/jorind

17

Arinaitwe, S. K. (2006). Factors Constraining the

Growth and Survival of Small Scale Businesses. A Developing Countries Analysis. Journal of American Academy of Business, Cambridge. Vol. 8(2). pp. 167-179.

Ariyo, D. (2005). Small Firms are the Backbone of

the Nigerian Economy. http//www.africaeconomicanalysis.org/articles/gen/smallhtm.htm

Aruwa, S. A. S (2006). The Business Entrepreneur:

Entrepreneurial Development, Small and Medium Enterprises. Kaduna: Entrepreneurship Academy Publishing. 351 pp.

Aryeetey, E. (2001). Priority Research Issues

Relating to Regulation and Competition in Ghana. Centre for Regulation and Competition. Working Paper Series. Paper No.10.

Aryeetey, E, Baah-Nuakoh, A., Duggleby, T.,

Hetting, H. and Steel, W. F. (1994). Supply and Demand for Finance of Small Scale Enterprises in Ghana. Discussion Paper No.251. World Bank, Washington, DC.

Aryeetey, E. and Ahene, A. (2004). Changing

Regulatory Environment for Small-Medium Size Enterprises and their Performance in Ghana (CRC Working Paper No. 30594), Centre on Regulation and Competition (CRC). Retrieved from http://ageconsearch.umn.edu/bitstream/30594/1/cr050103.pdf

Ashamu, S. O. (2014). The Impact of Micro-finance

on Small Scale Business in Nigeria. Journal of Policy and Development Studies. Vol. 9. No. 1. November 2014. ISSN: 157-9385. www.arabianjbmr.com/JPDS_index.php. pp. 179-193.

Ayeni-Agbaje, A. R. and Osho, A. E. (2015).

Commercial Banks Role in Financing Small Scale Industries in Nigeria (A Study of First Bank, Ado-Ekiti, Ekiti State). European Journal of Accounting, Auditing and Finance Research. Vol. 3, No. 8. August 2015. ISSN 2053-4086(Print),

ISSN 2053-4094(Online) www.eajournals.org. pp.52-69.

Basil, O. (2005). Small and Medium Enterprises

(SMEs) in Nigeria. Problems and Prospects. A Dissertation Submitted to St. Clement University in partial fulfillment of the Award of the Degree of Doctor of Philosophy in Management. pp. 1-10.

Basu, A., Blavy, R. and Yulck, M. (2005).

Microfinance in Africa: Experience and Lessons from Selected African Countries. IMF Working Paper 04/1 7 4, Washington.

Beck, T., Demirgue-kunt, A. and Levine, R. (2005). SMEs, Growth and Poverty: Cross Country Evidence. NBER Working Paper 11224. National Bureau of Economic Research. Retrieved from http://www.nber.org/pepers/w11224pdf

Berry. A., Von Blottnitz, M., Cassim, R., Kesper, A.,

Rajaratnam, B. and. Van Seventer, D. E. (2002). The Economics of SMEs in South Africa, Trade and Industrial Policy Strategies. Johannesburg, South Africa.

Central Bank of Nigeria (CBN) (1988). Monetary Policies Circular No. 22, 1988.

Central Statistical Services (CSS) (1998). Employment and Unemployment in South Africa 1994-1997.

Cook P. and Nixon, F. (2000). Finance and

Medium- Sized Enterprise Development. IDPM, University of Manchester, Finance and Development Research Programme. Working Paper. No 14.

Evbuomwan, G. O., Ikpi A. E., Okoruwa, V. O. and

Akinyosoye, V. O. (2012). Preferences of Micro, Small and Medium Scale enterprises to Financial Products in Nigeria. Journal of Agricultural Economics and Development. Vol. 1(4). October 2012. Available online at http://academeresearchjournals.org/journal/jaed. pp. 80-98.

Green, C. J., Kimuyu, P., Manos, R. and Murinde,

V. (2002). How do Small Firms in Developing Countries Raise Capital? Evidence from a Large-Scale Survey of 16

JORIND 15(1)June, 2017. ISSN 1596-8303. www.transcampus.org/journal; www.ajol.info/journals/jorind

18

Kenyan Micro and Small Scale Enterprises. Economic Research Paper No. 02/6. Centre for International, Financial and Economics Research, Department of Economics, Loughborough University.

Gumede, V. (2000). Growth and Exporting of Small

and Medium Enterprises in South Africa. Some thoughts on Policy and Scope for Further Research. Trade and Industrial Policy Strategies. South Africa.

Jhingan, M. L (1997). Macroeconomic Theory. Delhi: Vrinda publishing. Levy, B. (1993). Obstacles to Developing

Indigenous Small and Medium Enterprises: An Empirical Assessment. World Bank Economic Review. Vol. 7 (1). pp. 65–83.

Kayanula, D. and Quartey, P. (2000). The Policy

Environment for Promoting Small and Medium Enterprise in Ghana and Malawi. Finance and Development Research Programme. Working Paper Series. No. 15.

Lawal, B. A. (2014). Banking Sector and the

Development of SMEs in Osun State. Research Journal of Finance and Accounting. ISSN 2222-1697 (Paper) ISSN 2222-2847 (Online). Vol.5. No.4, 2014. www.iiste.org pp. 21-32.

Liedholm, C., MacPherson, M. and Chuta, E.

(1994). Small Enterprise Employment Growth in Rural Africa. American Journal of Agricultural Economics. Vol. 76. pp. 1177-1182.

Mago, S and Toro, B. (2013). South African

Government’s Support to Small, Medium Micro-Enterprise (SMMEs): The Case of King William’s Town Area. J Economics. Kamla-Raj 2013. Vol. 4(1). pp. 19-28.

Mensah, S. (2004). A review of SME financing

schemes in Ghana. A Paper Presented at the UNIDO Regional Workshop of Financing Small and Medium Scale Enterprises, Accra, Ghana, 15th to 16th March, 2004.

Ntsika, (1999). State of Small Business in South

Africa. SARB Quarterly Bulletins and Stats SA Releases, South Africa.

Oboh, G. A. T. (2002). Banks Participation in the

Promotion of Small and Mediu-Scale Enterprises. Being a Pater Presented at the 6th Fellows and Associate Forumn of CIBN on 13th April.

Odeyemi, J. A. (2003). An Overview of the Current State of SMEs in Nigeria and the Need for Intervention. A Paper Presented at the National Summit on SMIEIS Organized by the Bankers’ Committee and Lagos Chambers of Commerce and Industry (LCCI), Lagos. 10th June, 2003.

Ofoegbu, E. O., Akanbi, P. A. and Joseph, A. T. (2013). Effect of Contextual Factors on the Performance of SMEs in Nigeria: A Case Study of Ilorin Metropolis. Advances in Management and Applied Economics. ISSN: 1792-7544 (print version), 1792-7552 (online). Vol. 3(1). pp. 95-114.

Ogboru, L. P. (2007). An Evaluation of Funding Arrangement for Small and Medium Scale Enterprises (SMEs) in Nigeria. A study of St Clements University, British, West Indies.

Ogbuanu, B. K., Kabuoh, M. N and Okwu, A. T.

(2014). Relevance of Small and Medium Enterprises in the Growth of the Nigerian Economy: A Study of Manufacturing SMEs. International Journal of Research in Statistics, Management and Finance. Vol. 2. No. 1. October 2014. ISSN PRINT: 2315-8409, ONLINE: 2354-1644. pp. 180-191.

Ogechukwu, A. (2006). The Role of Small Scale

Industry in National Development in Nigeria. Texas Corpus Christi, Texas, United State. November 1-3, 2006.

Oguntoye P. A. (1984), Bank and Small – Scale

Business, Role of Small- Scale Enterprises in National Development, Nigeria Experience; Lagos, F. A. Publishers Ltd.

Oyefuga, I. O., Siyanbola, W. O., Afolabi, O. D., Dada, A. D. and Egbetokun, A. A. (2010). SMEs funding: An Assessment of an

JORIND 15(1)June, 2017. ISSN 1596-8303. www.transcampus.org/journal; www.ajol.info/journals/jorind

19

Intervention Scheme in Nigeria” World Bank Review of Entrepreneurship, Management and Sustainable Development. Vol. 2, No. 5.

Ojeka, S. A. (2011). Tax Policy and Growth of

SMEs: Implications for the Nigerian Economy. Research Journal of Finance and Accounting. ISSN 2222-1697 (Paper) ISSN 2222-2847 (Online). Vol. 2. No. 2. 2011. www.iiste.org. 12 pp.

Ojo, A. T. (1992). Bank and Small Business. Lagos:

F and T Publisher LTD.

Oke and Aluko (2015). Impact of Commercial

Banks on Small and Medium Enterprises Financing in Nigeria. IOSR Journal of Business and Management (IOSR-JBM) e-ISSN: 2278-487X, p-ISSN: 2319-7668. Volume 17, Issue 4.Ver. I (Apr. 2015). www.iosrjournals.org. pp. 23-26.

Okpara F. O. (2000). Entrepreneurship (Text and

Cases). Enugu Nigeria: Precision Printers and Publishers.

Okpara, J. O., and Wynn, P. (2007). Determinants

of Small Business Growth Constraints in a Sub-Saharan African Economy. SAM Advanced Management Journal. Vol. 72(2). pp. 24-35.

Olowe, F. T., Moradeyo, O. A. and Babalola. O.A.

(2013). Empirical Study of the Impact of Microfinance Bank on Small and Medium Growth in Nigeria. International Journal of Academic Research in Economics and Management Sciences. Vol. 2(6). pp. 116-124.

Onugu, B. A. N. (2005). Small and Medium

Enterprises (SMES) in Nigeria: Problems and Prospects. Being a Dissertation Submitted to St. Clements University in Partial Fulfilment of the Requirements for the Award of the Degree of Doctor of Philosophy (Ph.D.) in Management. pp. 1-114.

Onwumere, J. (2000). The Nature and Relevance of

SMEs in Economic Development. Journal of the Chartered Institute of Bankers of Nigeria. pp.14-19.

Onyeiwu, C. (2012). Small and Medium Enterprises

Finance and Economic Development of Nigeria. An unpublished Article. University of Lagos. Lagos State, Nigeria.

Organisation for Economic Co-operation and

Development (OECD) (2000). Small and Medium Sized Enterprises: Local Strength, Global Reach OECD. Policy Review. pp. 1-8.

Owenvbiugie, R. O. and Igbinedion, V. I. (2015). Role of Finance on the Growth of Small and Medium Scale Enterprises in Edo State of Nigeria. Journal of Educational and Social Research. MCSER Publishing, Rome-Italy. Vol. 5. No.1. January 2015. ISSN 2239-978X. ISSN 2240-0524. pp. 241- 248.

Owualah, S. I. (1987). Providing Necessary Economic Infrastructure for Small Business: Whose

Responsibility? International Small Business Journal. Vol. 6(1). pp. 10-30.

Panitchpakdi, S. (2006): Statements at the 10 Session of the Commission on Enterprise, Business Facilitation and Development. 21 February 2006. Geneva. Retrieved from http://www.unctad.org/template s/webfl ye r.asp?docid= 6825HYPERLINK "http://www.unctad.org/templates/webflyer.asp?docid=%206825&intItemID=4843&lang=1"

Parker, R., Riopelle, R. and Steel, W. (1995). Small

Enterprises Adjusting to Liberalisation in Five African Countries. World Bank Discussion Paper. No 271. African Technical Department Series. The World Bank. Washington DC.

Sowa, N. K., Baah-Nuakoh, A., Tutu, K. A. and Osei, B. (1992). Small Enterprise and Adjustment. The Impact of Ghana’s Economic Recovery Programme on Small-Scale Industrial Enterprises. Research Reports. Overseas Development Institute, 111 Westminster Bridge Road, London SE1 7JD.

Steel, W. F. and Webster, L. M. (1991). Small

Enterprises in Ghana: Responses to

JORIND 15(1)June, 2017. ISSN 1596-8303. www.transcampus.org/journal; www.ajol.info/journals/jorind

20

Adjustment Industry. Series Paper, No. 33, The World Bank Industry and Energy Department, Washington DC.

Steel, W. F. and Webster, L. M. (1992). How Small Enterprises in Ghana have responded to Adjustment. The World Bank Economic Review. Vol. 6 (3). pp. 423-438.

Stiglitz, J. E. and Uy, M. (1996). Financial Markets, Public Policy and the East Asian Miracle. World Research Observer. Vol. 11(2). August, 1996. pp. 249-276.

Terungwa, A. (2012). Risk Management and Insurance of Small and Medium Scale Enterprises (SMEs) in Nigeria. International Journal of Finance and Accounting. Vol. 1(1). pp. 8-17.

Todaro, M. P. (1985). Economic Development in the Third World. Third Edition. London: Longman.

Uzonwanne, M. C. (2015). Deposit Money Banks and Financing of Small and Medium Scale Enterprises in Nigeria. Journal of Economics and Sustainable Development. ISSN 2222-1700 (Paper) ISSN 2222-2855 (Online). Vol.6. No.8. www.iiste.org pp. 185-195.

World bank, (2001). Small and Medium Scale

Enterprises Country Mapping. World Bank (1995). Private Sector Development in

Low Income Countries. Washington, D.C.

![A.I. Enterprises Ltd. and A.I. Enterprises Ltd. et …...[2014] 1 R.C.S. A.I. ENTERPRISES c. BRAM ENTERPRISES 177 A.I. Enterprises Ltd. et Alan Schelew Appelants c. Bram Enterprises](https://static.fdocuments.us/doc/165x107/5e918dac94e60f42b949e30a/ai-enterprises-ltd-and-ai-enterprises-ltd-et-2014-1-rcs-ai-enterprises.jpg)