Edward D. Burmeister Baker & McKenzie Two Embarcadero Center, Suite 2400

27

Global Stock Plan Design and Global Stock Plan Design and Redesign: Redesign: Issues Relating to Broad- Issues Relating to Broad- Based Plans Based Plans 2001 Global Equity Compensation 2001 Global Equity Compensation Forum Forum San Francisco, California San Francisco, California November 5, 2001 November 5, 2001 Edward D. Burmeister Baker & McKenzie Two Embarcadero Center, Suite 2400 San Francisco, California 94111 (415) 576-3029 [email protected]

-

Upload

chanda-kim -

Category

Documents

-

view

30 -

download

0

description

Global Stock Plan Design and Redesign: Issues Relating to Broad-Based Plans 2001 Global Equity Compensation Forum San Francisco, California November 5, 2001. Edward D. Burmeister Baker & McKenzie Two Embarcadero Center, Suite 2400 San Francisco, California 94111 (415) 576-3029 - PowerPoint PPT Presentation

Transcript of Edward D. Burmeister Baker & McKenzie Two Embarcadero Center, Suite 2400

Global Stock Plan Design and Redesign:Global Stock Plan Design and Redesign:Issues Relating to Broad-Based PlansIssues Relating to Broad-Based Plans

2001 Global Equity Compensation Forum2001 Global Equity Compensation Forum

San Francisco, CaliforniaSan Francisco, CaliforniaNovember 5, 2001November 5, 2001

Edward D. BurmeisterBaker & McKenzie

Two Embarcadero Center, Suite 2400San Francisco, California 94111

(415) [email protected]

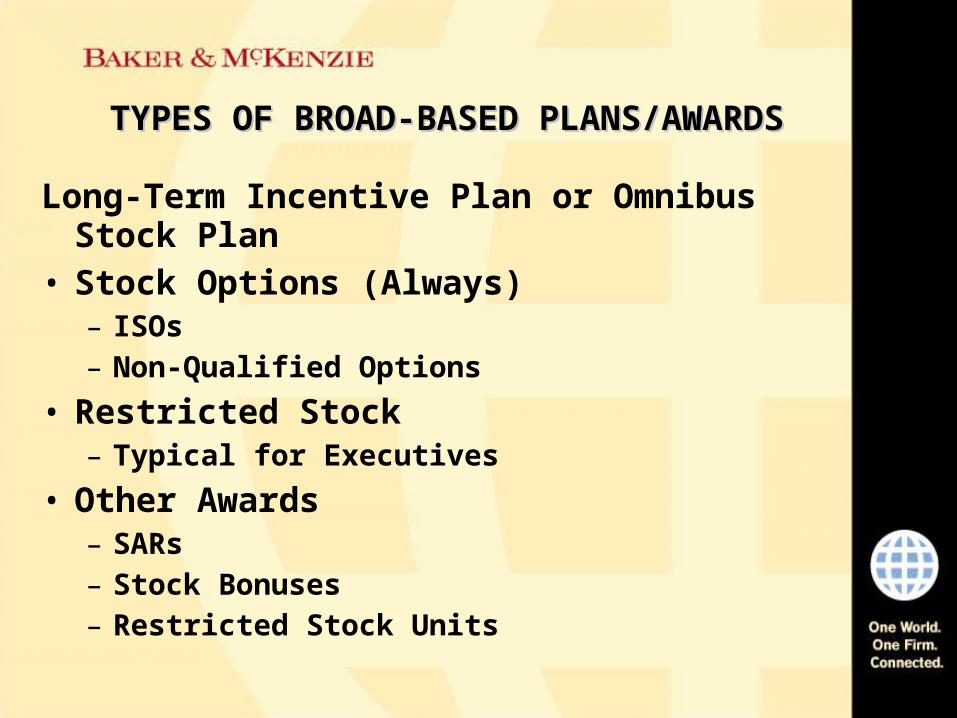

TYPES OF BROAD-BASED PLANS/AWARDSTYPES OF BROAD-BASED PLANS/AWARDS

Long-Term Incentive Plan or Omnibus Stock Plan• Stock Options (Always)

– ISOs– Non-Qualified Options

• Restricted Stock– Typical for Executives

• Other Awards– SARs– Stock Bonuses– Restricted Stock Units

BROAD-BASED AWARDSBROAD-BASED AWARDS

Hire Grants (Silicon Valley Model)

• All-Employee, “One”-Time Grant

• Ongoing Broad-Based Grants

STOCK PURCHASE PLANSSTOCK PURCHASE PLANS

• 423 Design

• Non-423 Design– Open Market– No Discount Plans– Other

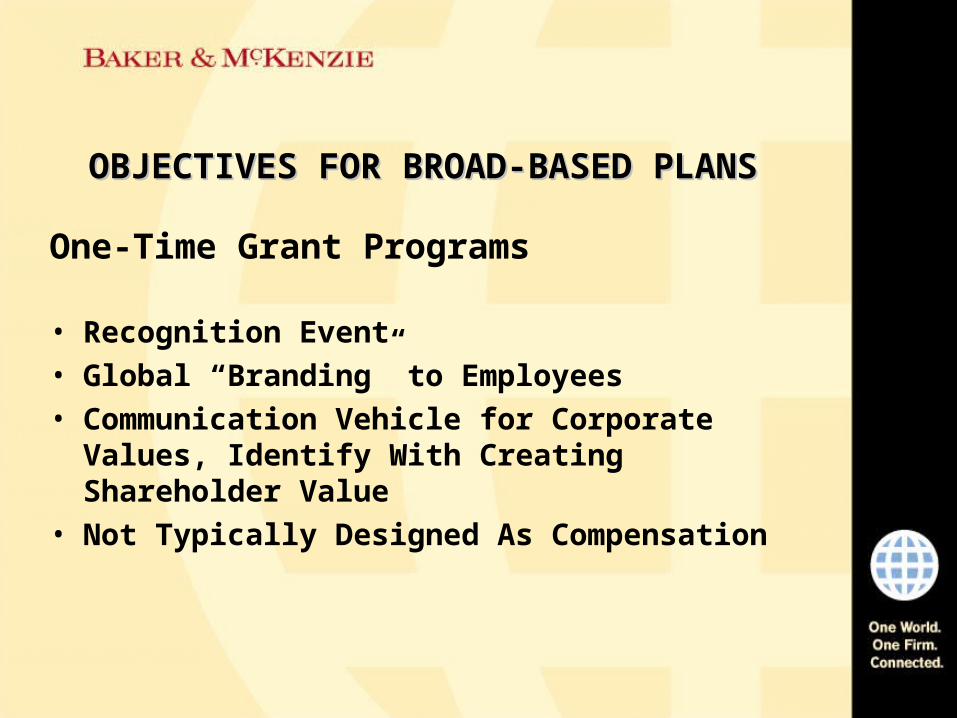

OBJECTIVES FOR BROAD-BASED PLANSOBJECTIVES FOR BROAD-BASED PLANS

One-Time Grant Programs

• Recognition Event

• Global “Branding” to Employees

• Communication Vehicle for Corporate Values, Identify With Creating Shareholder Value

• Not Typically Designed As Compensation

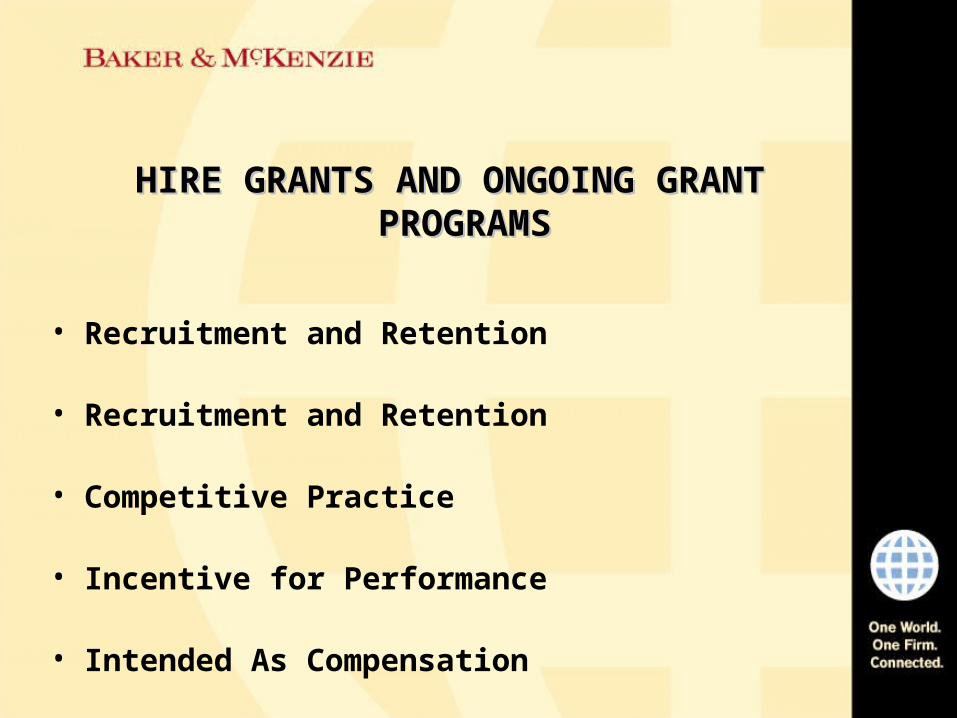

HIRE GRANTS AND ONGOING GRANT HIRE GRANTS AND ONGOING GRANT PROGRAMSPROGRAMS

• Recruitment and Retention

• Recruitment and Retention

• Competitive Practice

• Incentive for Performance

• Intended As Compensation

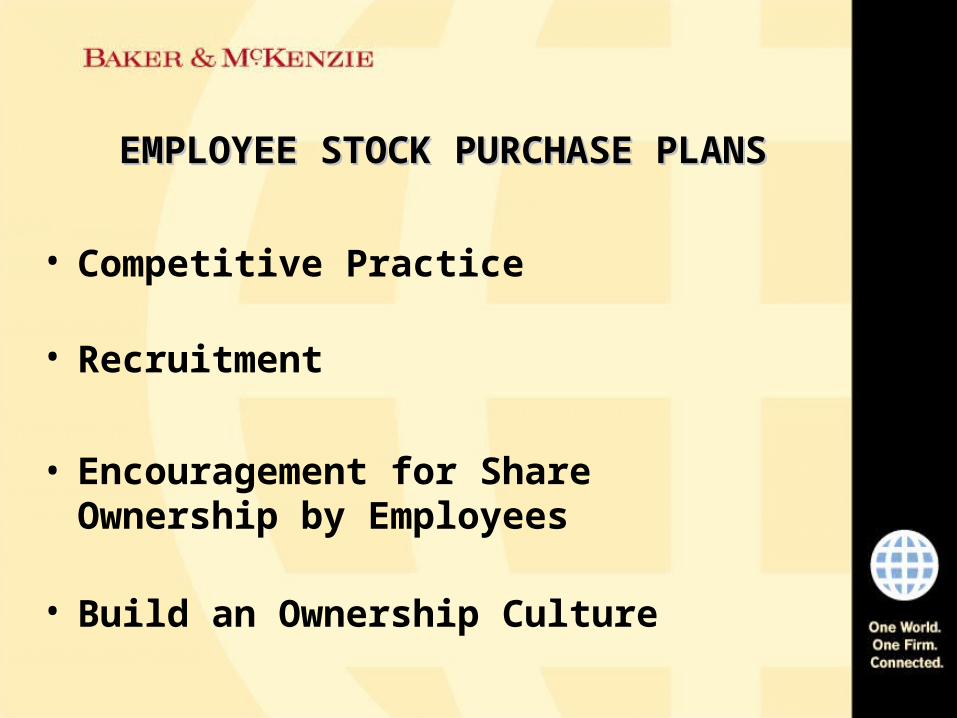

EMPLOYEE STOCK PURCHASE PLANSEMPLOYEE STOCK PURCHASE PLANS

• Competitive Practice

• Recruitment

• Encouragement for Share Ownership by Employees

• Build an Ownership Culture

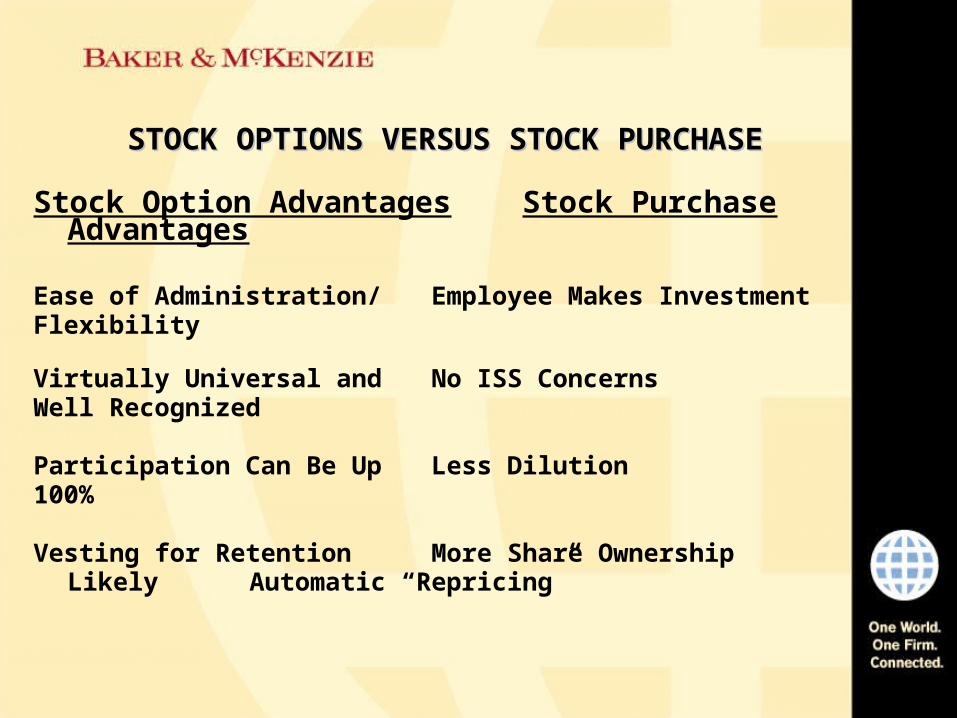

STOCK OPTIONS VERSUS STOCK PURCHASESTOCK OPTIONS VERSUS STOCK PURCHASE

Stock Option Advantages Stock Purchase Advantages

Ease of Administration/ Employee Makes InvestmentFlexibility

Virtually Universal and No ISS ConcernsWell Recognized

Participation Can Be Up Less Dilution100%

Vesting for Retention More Share Ownership Likely Automatic “Repricing”

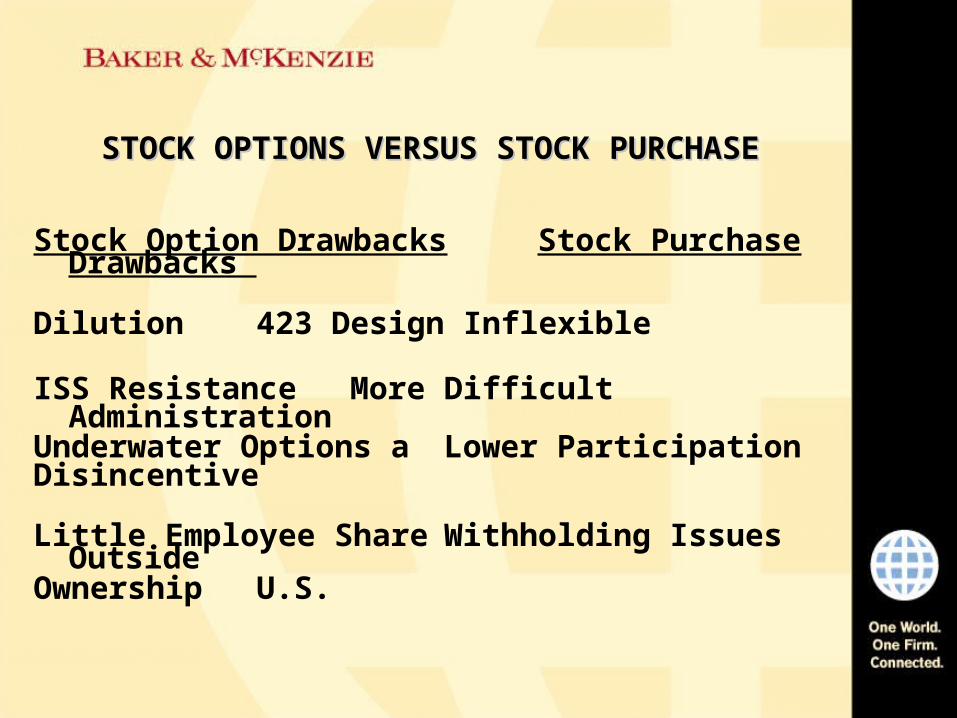

STOCK OPTIONS VERSUS STOCK PURCHASESTOCK OPTIONS VERSUS STOCK PURCHASE

Stock Option Drawbacks Stock Purchase Drawbacks

Dilution 423 Design Inflexible

ISS Resistance More Difficult Administration

Underwater Options a Lower ParticipationDisincentive

Little Employee Share Withholding Issues Outside Ownership U.S.

STOCK OPTION PLAN DESIGNSTOCK OPTION PLAN DESIGN

• Global One Size Fits All Design

• Global Design With Limited Local Variations

• Global Plan With Significant Local Customization

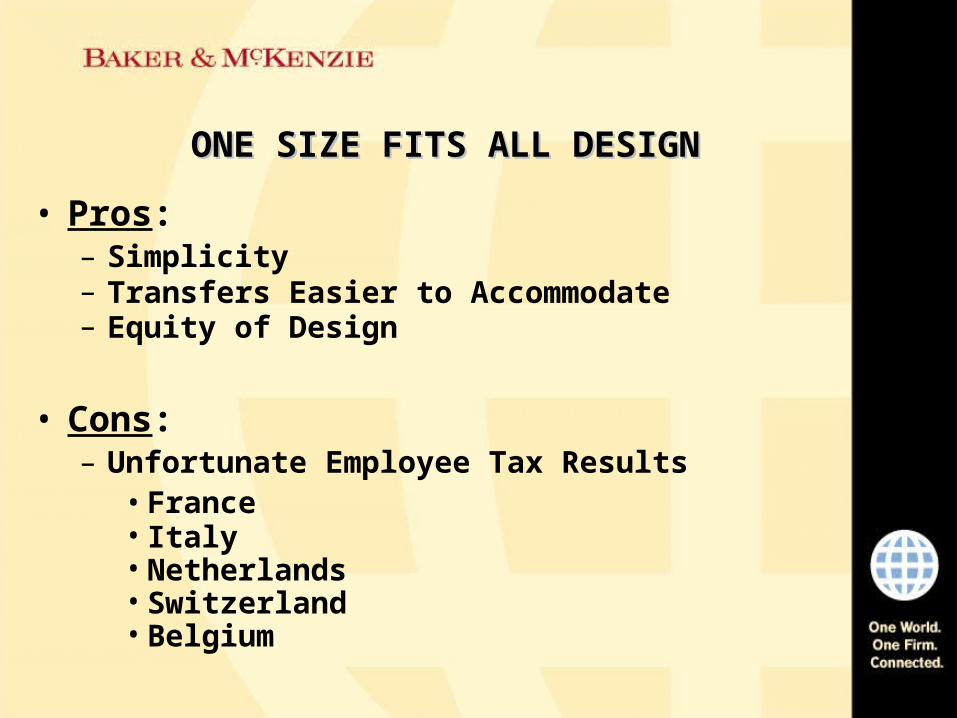

ONE SIZE FITS ALL DESIGNONE SIZE FITS ALL DESIGN

• Pros:– Simplicity– Transfers Easier to Accommodate– Equity of Design

• Cons:– Unfortunate Employee Tax Results

• France• Italy• Netherlands• Switzerland• Belgium

ONE SIZE FITS ALL DESIGNONE SIZE FITS ALL DESIGN (Con’t) (Con’t)

• Cons:– Unfortunate Company Social Taxes

• France• U. K.• Italy• Sweden• Norway

– Failure to Take Advantage of Local Tax Advantages• U. K.• Ireland• Israel• Austria• Singapore• Italy

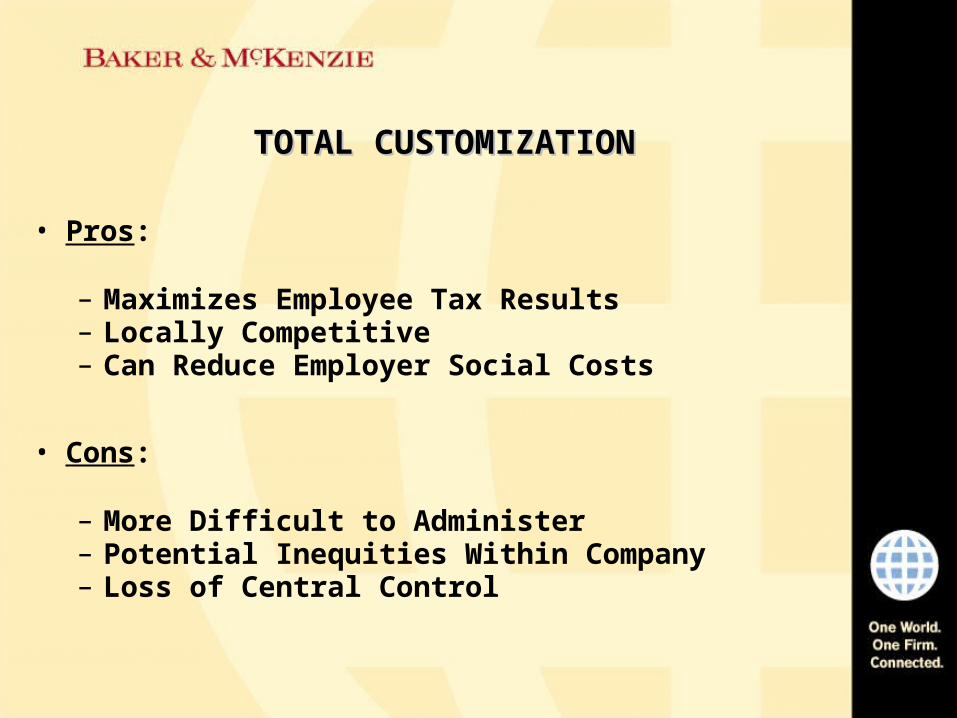

TOTAL CUSTOMIZATIONTOTAL CUSTOMIZATION

• Pros:

– Maximizes Employee Tax Results– Locally Competitive– Can Reduce Employer Social Costs

• Cons:

– More Difficult to Administer– Potential Inequities Within Company– Loss of Central Control

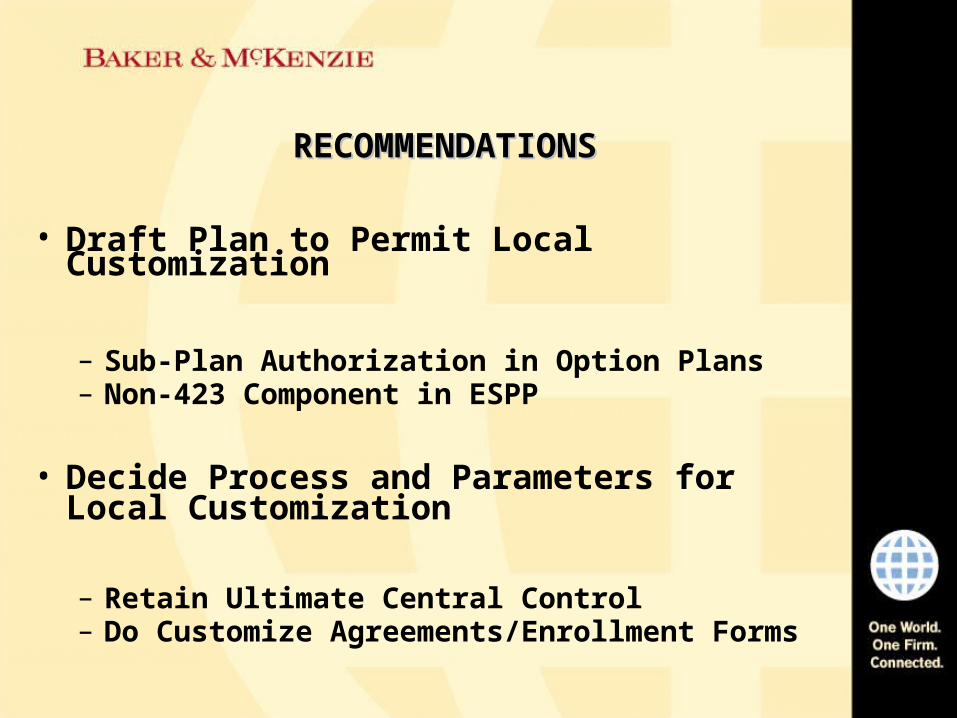

RECOMMENDATIONSRECOMMENDATIONS

• Draft Plan to Permit Local Customization

– Sub-Plan Authorization in Option Plans– Non-423 Component in ESPP

• Decide Process and Parameters for Local Customization

– Retain Ultimate Central Control– Do Customize Agreements/Enrollment Forms

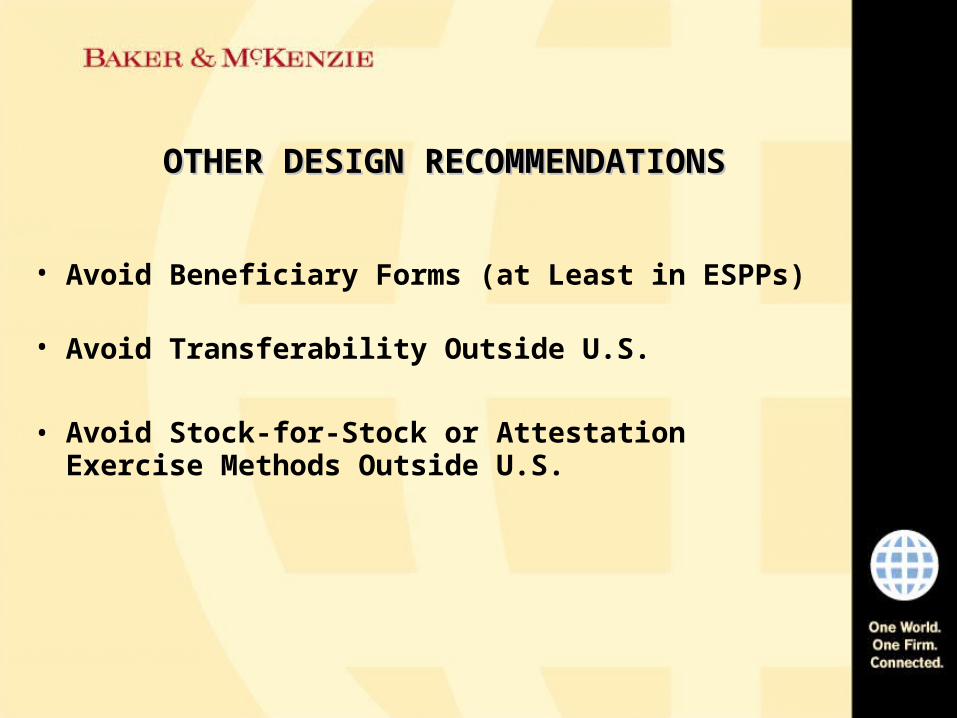

OTHER DESIGN RECOMMENDATIONSOTHER DESIGN RECOMMENDATIONS

• Avoid Beneficiary Forms (at Least in ESPPs)

• Avoid Transferability Outside U.S.

• Avoid Stock-for-Stock or Attestation Exercise Methods Outside U.S.

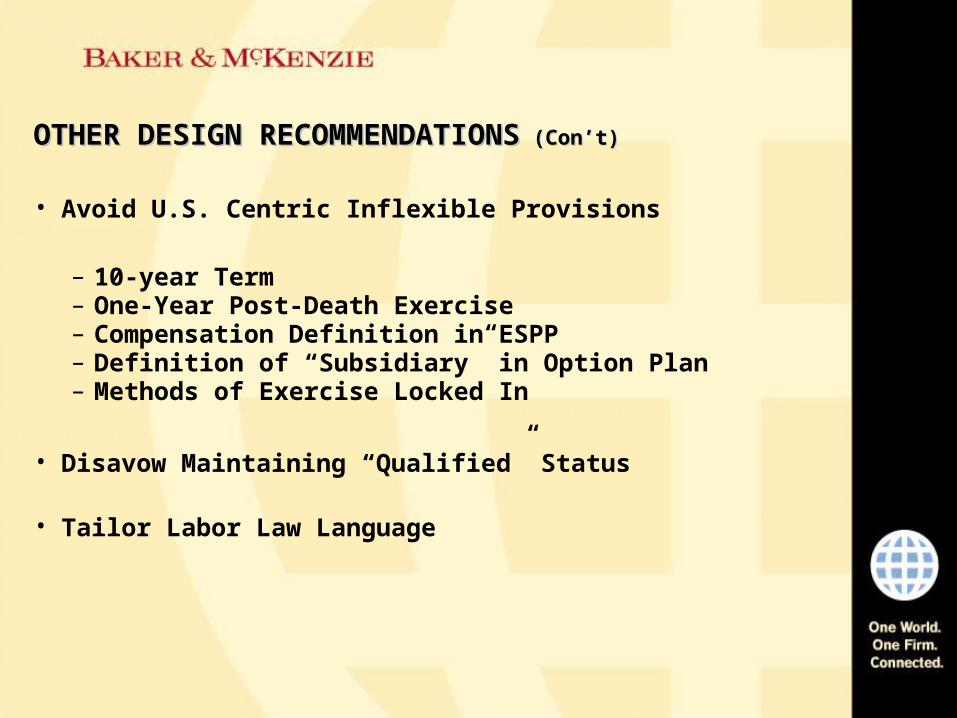

OTHER DESIGN RECOMMENDATIONSOTHER DESIGN RECOMMENDATIONS (Con’t) (Con’t)

• Avoid U.S. Centric Inflexible Provisions

– 10-year Term– One-Year Post-Death Exercise– Compensation Definition in ESPP– Definition of “Subsidiary” in Option Plan– Methods of Exercise Locked In

• Disavow Maintaining “Qualified” Status

• Tailor Labor Law Language

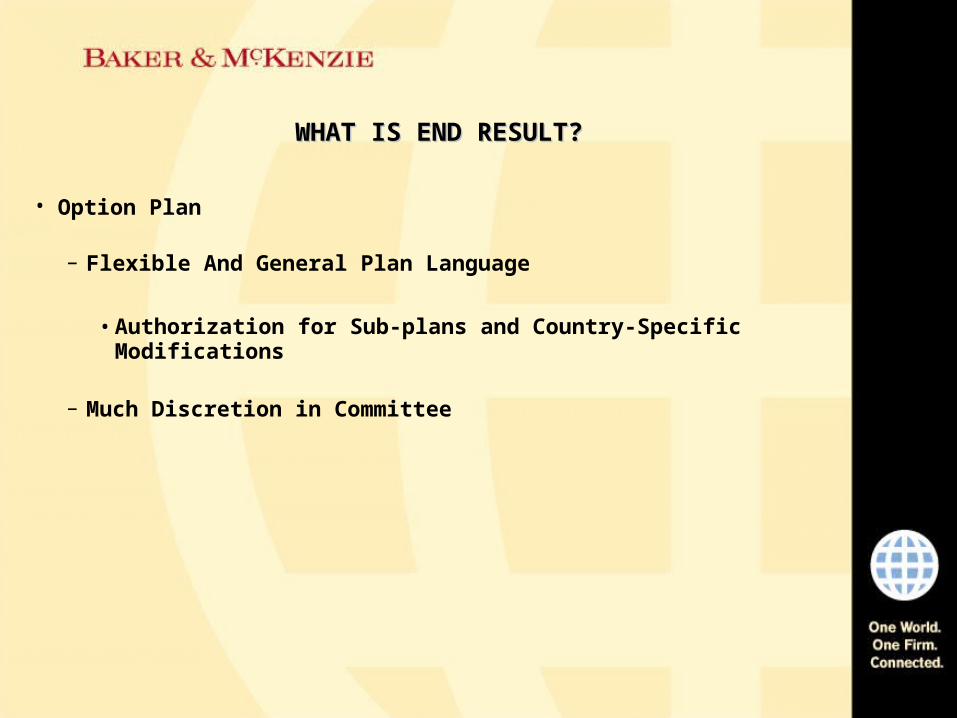

WHAT IS END RESULT?WHAT IS END RESULT?

• Option Plan

– Flexible And General Plan Language

• Authorization for Sub-plans and Country-Specific Modifications

– Much Discretion in Committee

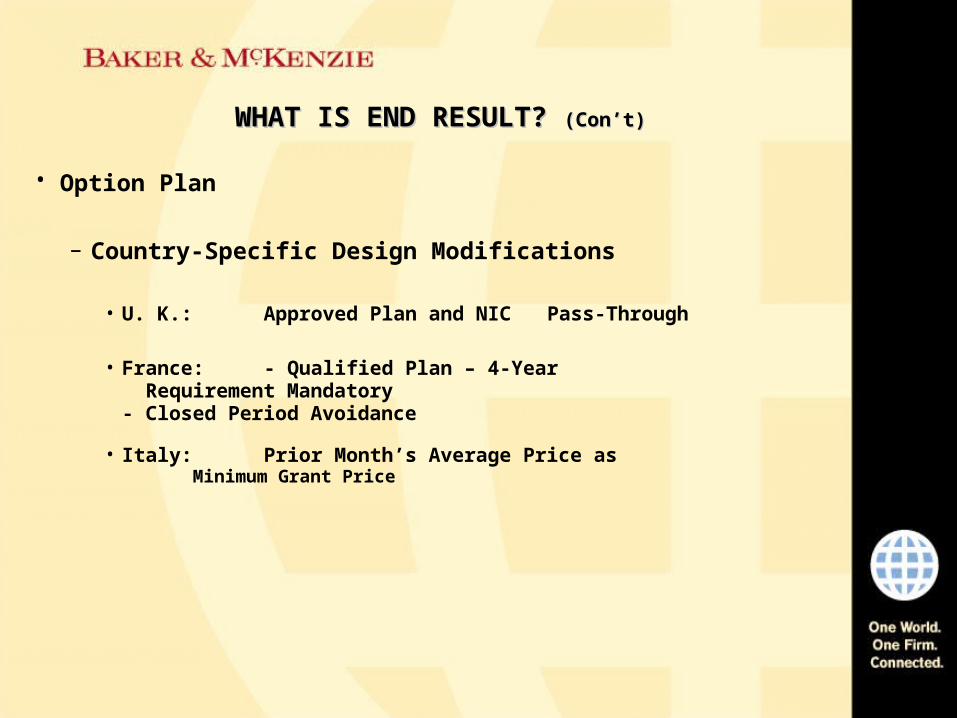

WHAT IS END RESULT? WHAT IS END RESULT? (Con’t)(Con’t)

• Option Plan

– Country-Specific Design Modifications

• U. K.: Approved Plan and NICPass-Through

• France: - Qualified Plan – 4-Year Requirement Mandatory- Closed Period Avoidance

• Italy: Prior Month’s Average Price as Minimum Grant Price

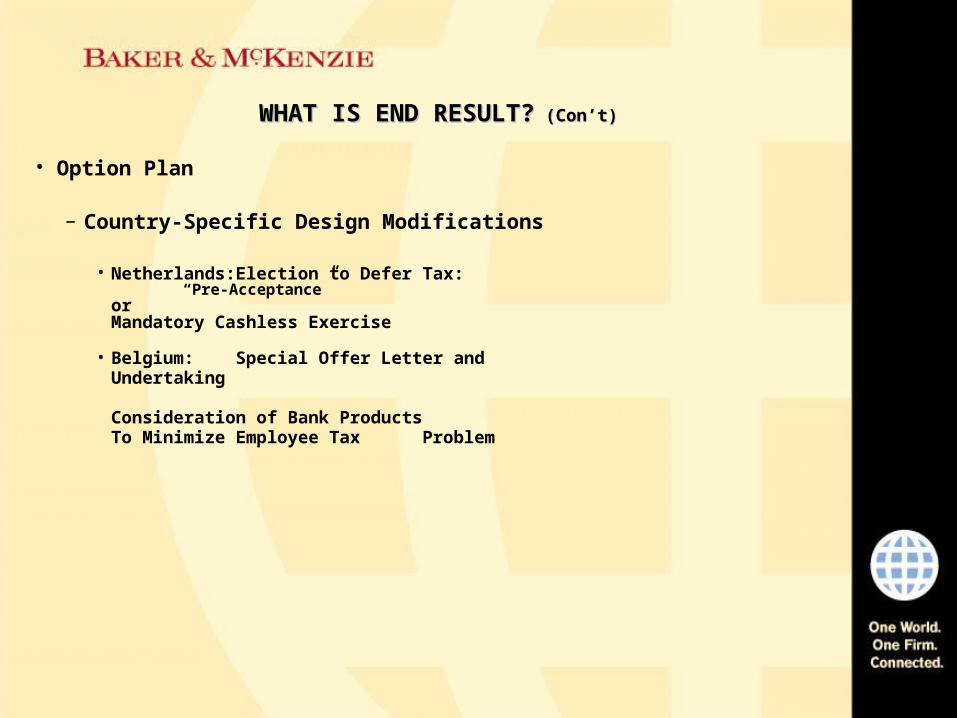

WHAT IS END RESULT?WHAT IS END RESULT? (Con’t) (Con’t)

• Option Plan

– Country-Specific Design Modifications

• Netherlands: Election to Defer Tax: “Pre-Acceptance”

orMandatory Cashless Exercise

• Belgium: Special Offer Letter andUndertaking

Consideration of Bank ProductsTo Minimize Employee Tax Problem

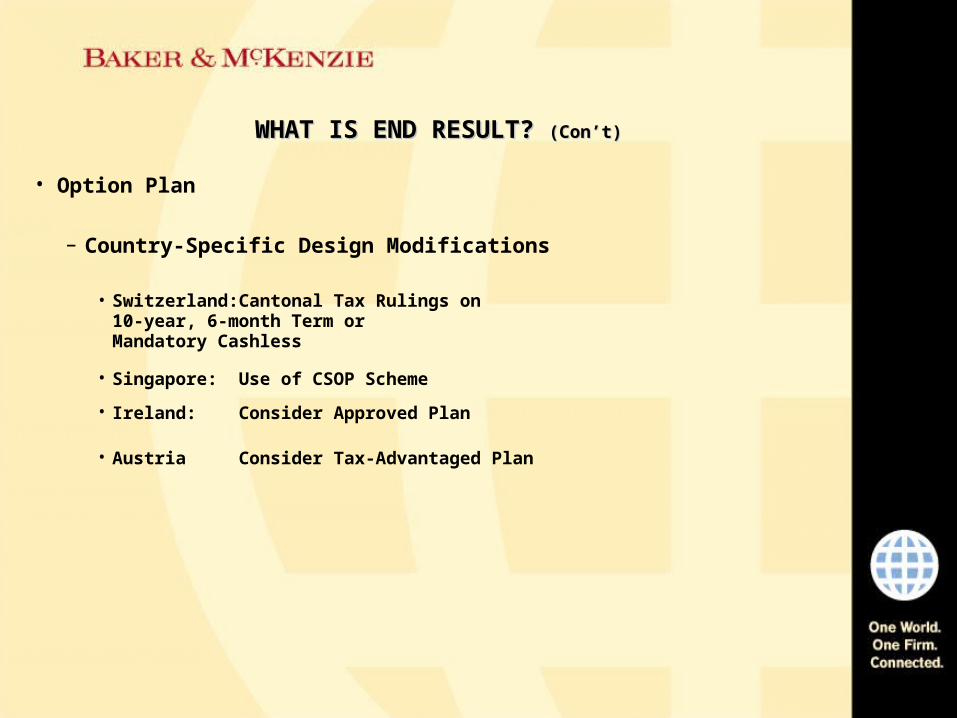

WHAT IS END RESULT? WHAT IS END RESULT? (Con’t)(Con’t)

• Option Plan

– Country-Specific Design Modifications

• Switzerland: Cantonal Tax Rulings on10-year, 6-month Term orMandatory Cashless

• Singapore: Use of CSOP Scheme

• Ireland: Consider Approved Plan

• Austria Consider Tax-Advantaged Plan

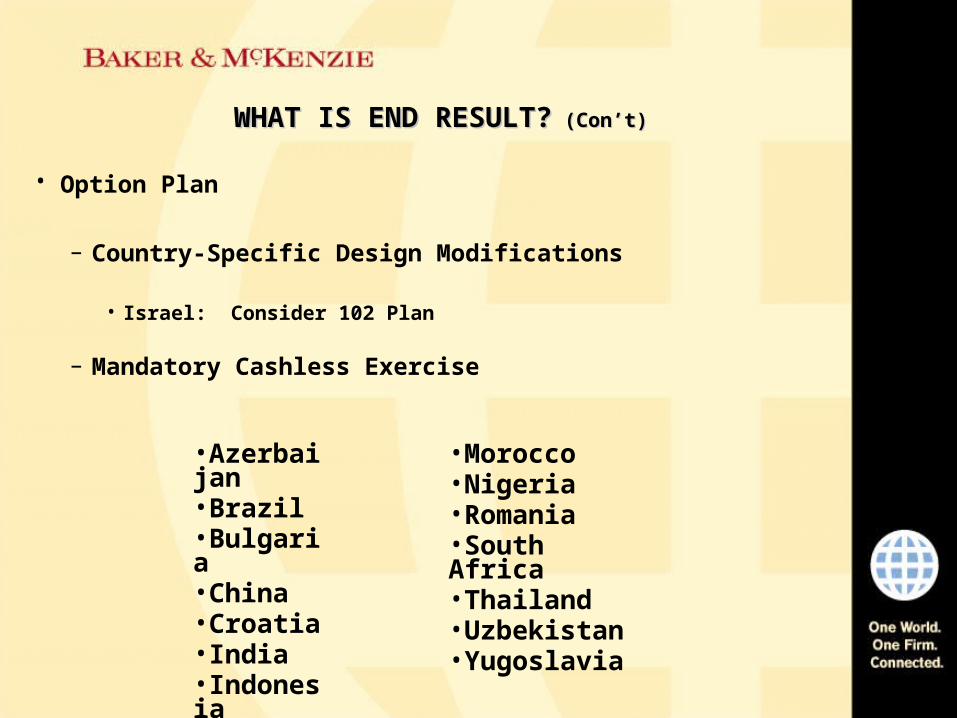

WHAT IS END RESULT?WHAT IS END RESULT? (Con’t) (Con’t)

• Option Plan

– Country-Specific Design Modifications

• Israel: Consider 102 Plan

– Mandatory Cashless Exercise

•Azerbaijan•Brazil•Bulgaria•China•Croatia•India•Indonesia

•Morocco•Nigeria•Romania•South Africa•Thailand•Uzbekistan•Yugoslavia

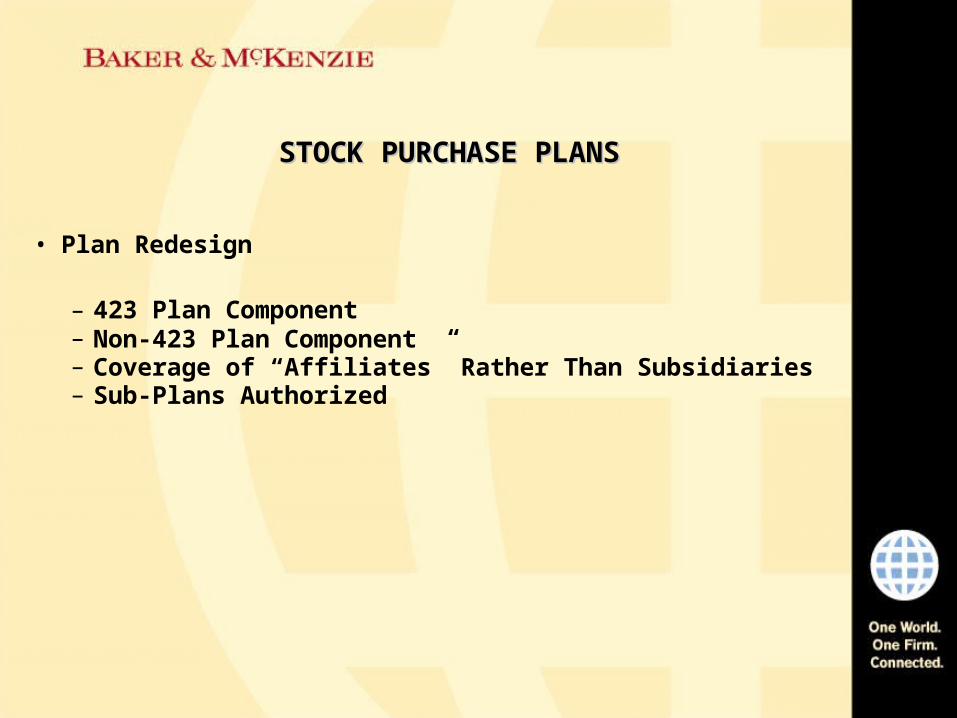

STOCK PURCHASE PLANSSTOCK PURCHASE PLANS

• Plan Redesign

– 423 Plan Component– Non-423 Plan Component– Coverage of “Affiliates” Rather Than Subsidiaries– Sub-Plans Authorized

STOCK PURCHASE PLANSTOCK PURCHASE PLAN (Con’t) (Con’t)

• Country Modifications – No Payroll Deductions (Alternatives: Direct Deposit, Checks)

• Hong Kong, Argentina, Mexico (Documentation May be Structured to Permit)

– Separate Accounts• Australia• Japan (if held by local sub)• Korea

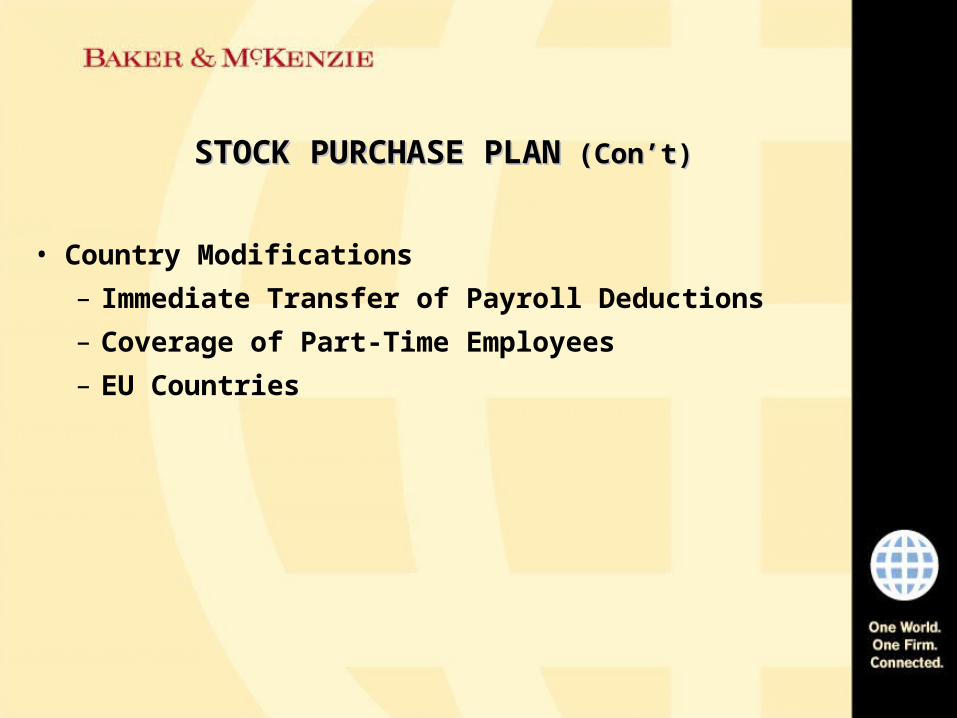

STOCK PURCHASE PLANSTOCK PURCHASE PLAN (Con’t) (Con’t)

• Country Modifications

– Immediate Transfer of Payroll Deductions

– Coverage of Part-Time Employees

– EU Countries

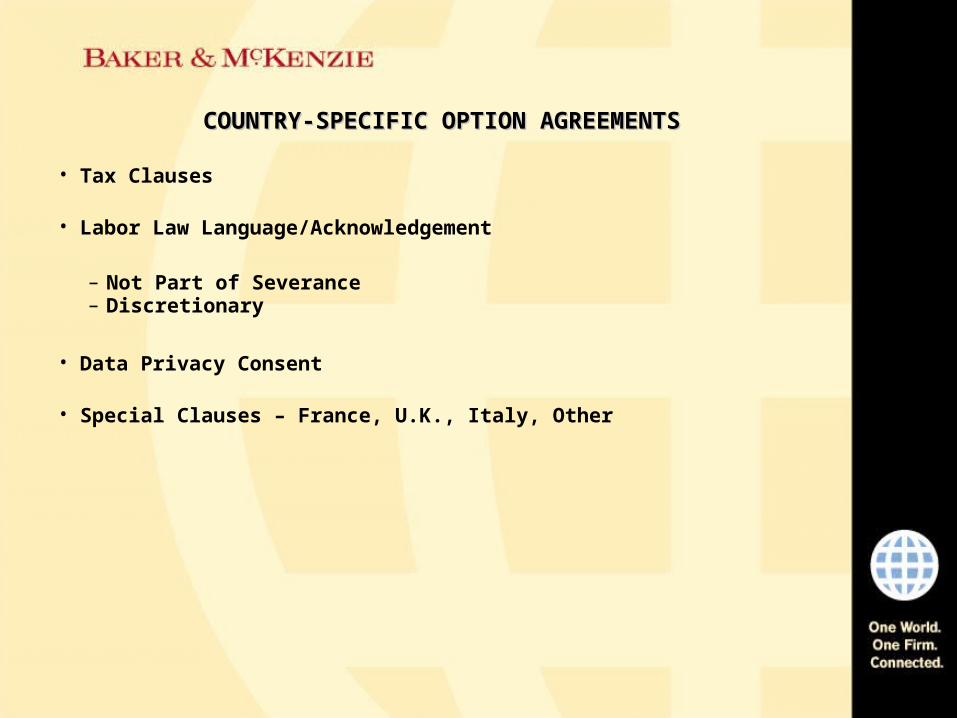

COUNTRY-SPECIFIC OPTION AGREEMENTSCOUNTRY-SPECIFIC OPTION AGREEMENTS

• Tax Clauses

• Labor Law Language/Acknowledgement

– Not Part of Severance– Discretionary

• Data Privacy Consent

• Special Clauses – France, U.K., Italy, Other

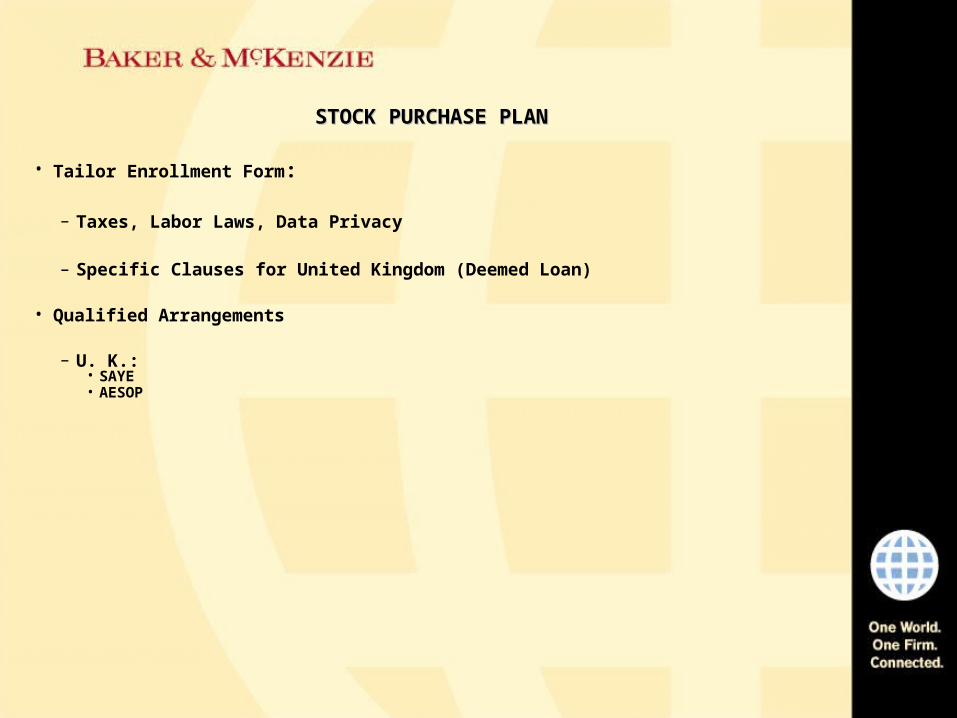

STOCK PURCHASE PLANSTOCK PURCHASE PLAN

• Tailor Enrollment Form:

– Taxes, Labor Laws, Data Privacy

– Specific Clauses for United Kingdom (Deemed Loan)

• Qualified Arrangements

– U. K.:• SAYE• AESOP

STOCK PURCHASE PLANSTOCK PURCHASE PLAN (Con’t) (Con’t)

• Qualified Arrangements

– Ireland:• SAYE

– France• P.E.E.

– Japan• Employee Association

• Company Structure Issues

– Check-The-Box Issues– Branch Issues