Economy clustering as a new MRAI reality: obstacles and opportunities 12 maggio 2015 Luca Penna...

18

Economy clustering as a new MRAI reality: obstacles and opportunities 12 maggio 2015 Luca Penna Azienda Speciale ConCentro Camera di Commercio di Pordenone

-

Upload

francis-young -

Category

Documents

-

view

217 -

download

1

Transcript of Economy clustering as a new MRAI reality: obstacles and opportunities 12 maggio 2015 Luca Penna...

Economy clustering as a new MRAI reality: obstacles and opportunities

12 maggio 2015 Luca Penna

Azienda Speciale ConCentroCamera di Commercio di Pordenone

CLUSTER / DISTRICTS: Geographic concentration of inteconnected business, suppliers and associated institutions in a specific field

INDUSTRY CLUSTER

TECHNOLOGY CLUSTER

Traditional industrial sectors

High technology sectors

Enterprises, Institutions, Agencies,…

Enterprises, Institutions, Universities, Technology

Parks,…Infrastructures and research&innovation

policies

CREATIVE CLUSTER

CULTURAL CLUSTER

Creativity and non technology innovation

Cultural resources

Enterprises, Institutions, Creative centers,

Fundations, ..

Enterprises, Institutions, Universities, Cultural

bodies,…

LIVING LABImprese, Istituzioni,

Enti di ricerca, “end users”

Rete ENoLL: European Network of Living Labs

A living lab is a user-centred, open-innovation ecosystem, often operating in a territorial context, integrating concurrent research and innovation processes within a public-private-people partnership

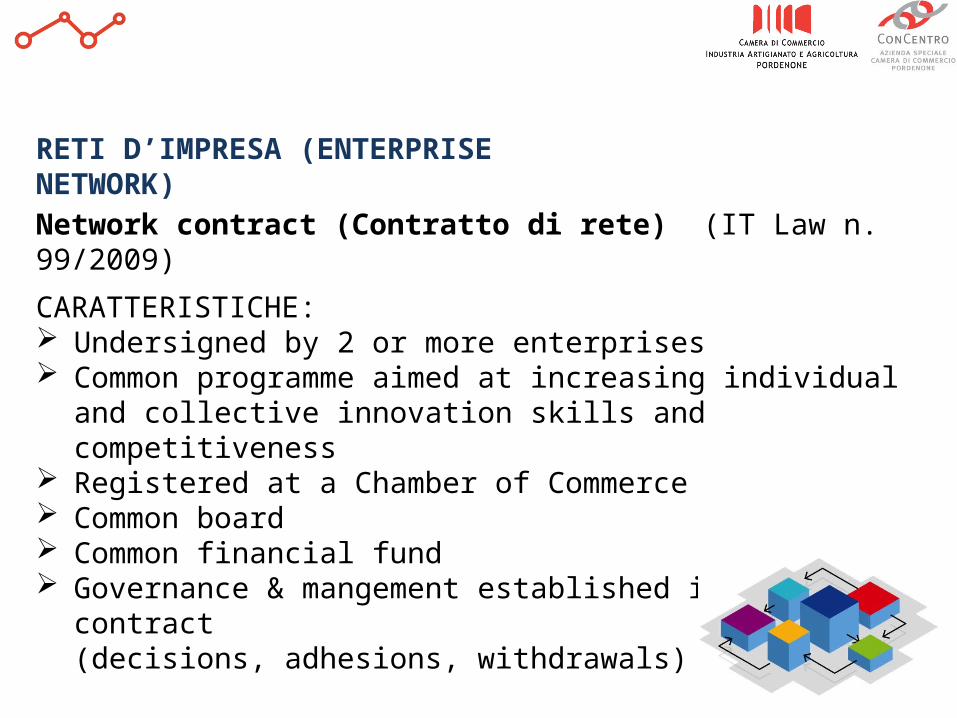

RETI D’IMPRESA (ENTERPRISE NETWORK)

Network contract (Contratto di rete) (IT Law n. 99/2009)

CARATTERISTICHE: Undersigned by 2 or more enterprises Common programme aimed at increasing individual and collective

innovation skills and competitiveness Registered at a Chamber of Commerce Common board Common financial fund Governance & mangement established in the contract

(decisions, adhesions, withdrawals)

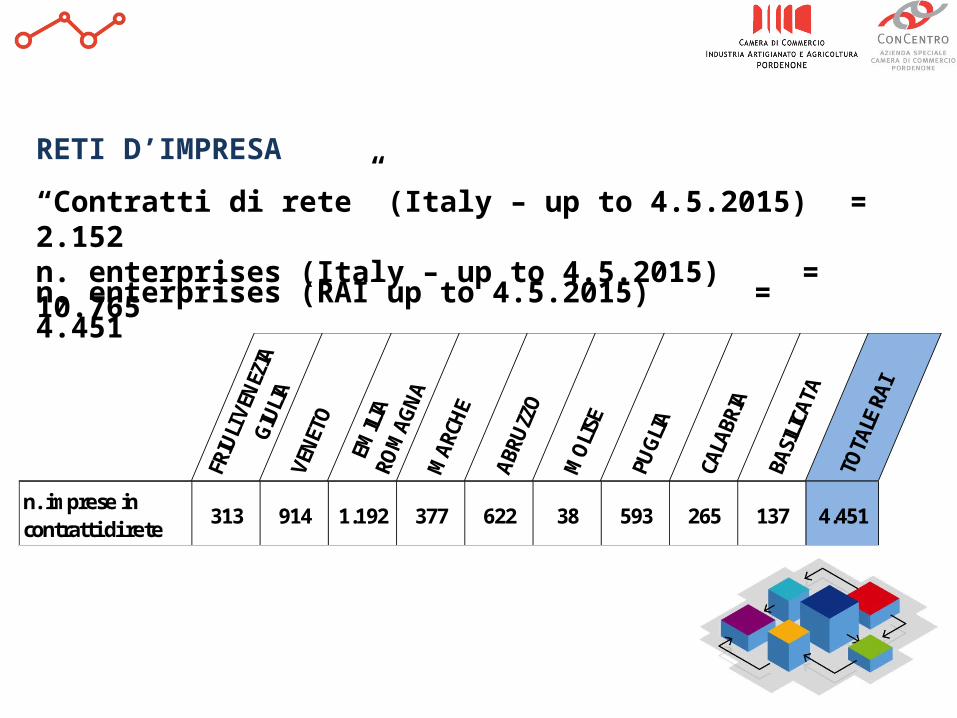

RETI D’IMPRESA

“Contratti di rete” (Italy – up to 4.5.2015) = 2.152n. enterprises (Italy – up to 4.5.2015) = 10.765

n. enterprises (RAI up to 4.5.2015) = 4.451

FRIU

LI V

ENEZ

IA

GIUL

IAVE

NETO

EMIL

IA

ROM

AGNA

MAR

CHE

ABRU

ZZO

MO

LISE

PUGL

IA

CALA

BRIA

BASI

LICA

TA

TOTA

LE R

AI

n. imprese in contratti di rete

313 914 1.192 377 622 38 593 265 137 4.451

PROVINCIALI31%

REGIONALI20%

NAZIONALI49%

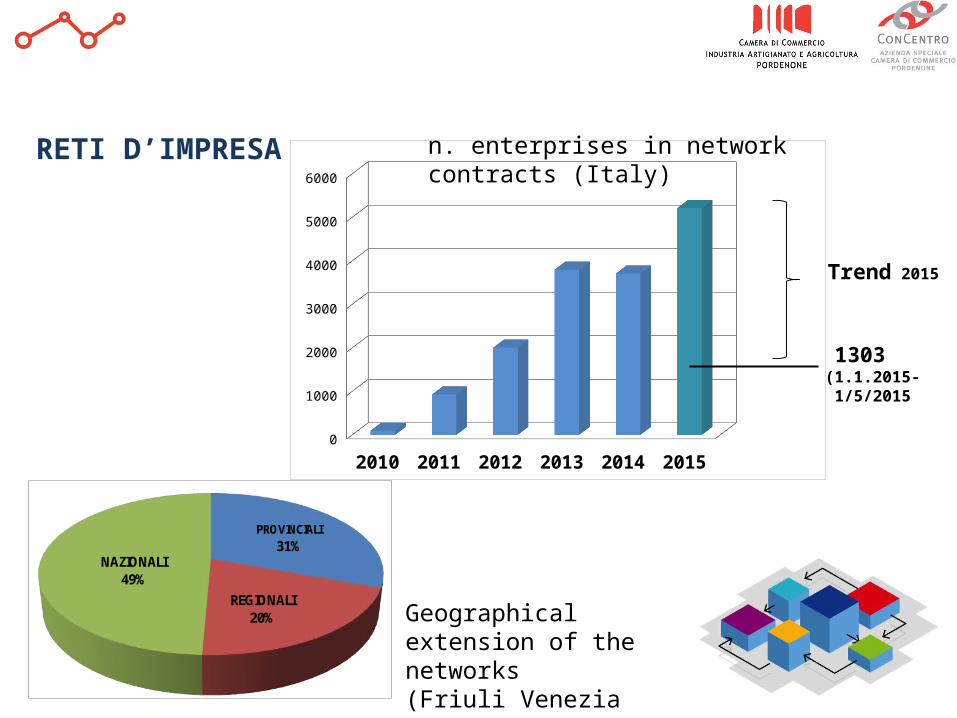

RETI D’IMPRESA

2010 2011 2012 2013 2014 20150

1000

2000

3000

4000

5000

6000

1303 (1.1.2015-1/5/2015

Trend 2015

n. enterprises in network contracts (Italy)

Geographical extension of the networks(Friuli Venezia Giulia)

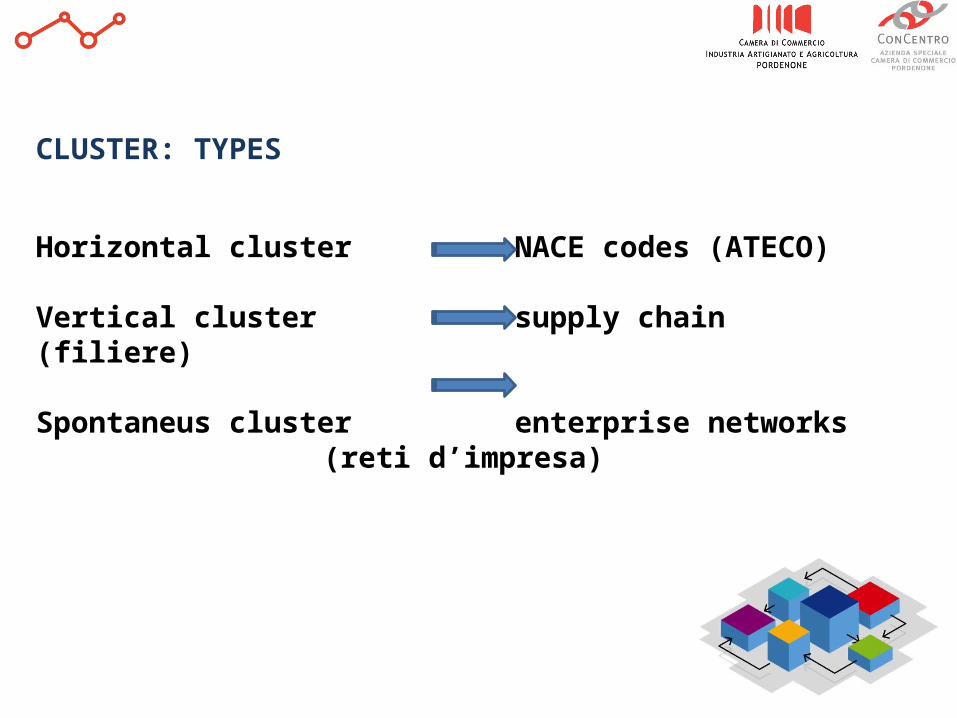

CLUSTER: TYPES

Horizontal cluster NACE codes (ATECO)

Vertical cluster supply chain (filiere)

Spontaneus cluster enterprise networks (reti d’impresa)

CLUSTER PARTICIPANTSConsortiatemporary association among enterprisescompaniesenterprise networks (contratti di rete)

Research & innovation centresLaboratoriesScience and Technology ParksIncubators (BIC, etc.)

Universities

Training organizations

Cultural bodies & institutionsCultural & creative associations, foundations, etc.

Chambers of Commerce & IndustryEnterpreneurs Associations

National, regional and local institutionsAgencies

Consumer associationsGroups

END USERS GROUPS

ENTERPRISES

RESEARCH & INNOVATION ORGANIZATIONS

TRAINING CENTRES

SECTORIAL BODIES

ENTERPRENEURS BODIES

GOVERNMENT BODIES

CLUSTER: POLICIES

Smart Specialization Strategy (S3)

Technologies clusters

Emerging industries Clusters

Creative & Cultural Clusters (Tourism)

SMART SPECIALIZATION STRATEGY (S3)

Com(2010)553: Regional policy contributing to smart growth in Europe 2020

Regulation (EU) n. 1303/2013: common provisions on the new structural funds 2014-2020

SMART SPECIALIZATION STRATEGY (S3)

FRIU

LI V

ENEZ

IA

GIU

LIA

VEN

ETO

EMIL

IA

ROM

AGNA

MAR

CHE

ABRU

ZZO

MO

LISE

PUGL

IA

CALA

BRIA

BASI

LICA

TASL

OVE

NIA

CRO

AZIA

IPEI

ROS

ION

IA N

ISIA

DYTI

KI E

LLAD

APE

LOPO

NN

ISO

S

Agrifood 12

Blue economy (acquacolture, etc)

3

Tobacco 1

Smart manufacturing / Mechatronics

8

Sustainable living & Construction

9

ICT & smart communities 3

Transport (Automotive, maritime, etc.)

7

Energy 6

Environment 4

Waste management 3

Smart health & Life sciences

10

Culture & creativity 10

Tourism 10

ITALIAN TECHNOLOGY CLUSTERS

FRIU

LI V

ENEZ

IA

GIU

LIA

VEN

ETO

EMIL

IA

ROM

AGNA

MAR

CHE

ABRU

ZZO

MO

LISE

PUGL

IA

CALA

BRIA

BASI

LICA

TA

Green Chemistry 3

Agrifood 4

Smart Living Technologies 2

Life Sciences 5

Smart Communities Technologies 3

Transport and Systems for Shipping by Land and Sea

4

Aerospace 2

Energy 1

Smart factory 4

CLUSTERS AND EMERGING INDUSTRIES

CLUSTER: OBSTACLES & OPPORTUNITIES

common cluster definition, identification, criteria, monitoring activities

implementation of a AI Cluster observatory (European Cluster Observatory)

cluster cooperation iniziatives (B2B, Cluster2Cluster, etc.)

common research & innovation initiativesaccess to credit (B2Finance)

best practice exchangecluster management & governance qualification

policy practices exchange (capacity bulding initiatives)new enterprise network models (for instance "reti d'impresa")

LACK OF DATA ABOUT CLUSTERS IN ADRIATIC & IONIAN REGION

EU & NATIONAL STRATEGY ENDORSMENT (S3, NATIONAL & REGIONAL CLUSTER, EMERGING & CREATIVE/CULTURAL SECTORS)

CLUSTER QUALIFICATION

FOSTER THE ENTERPRISE NETWORKS

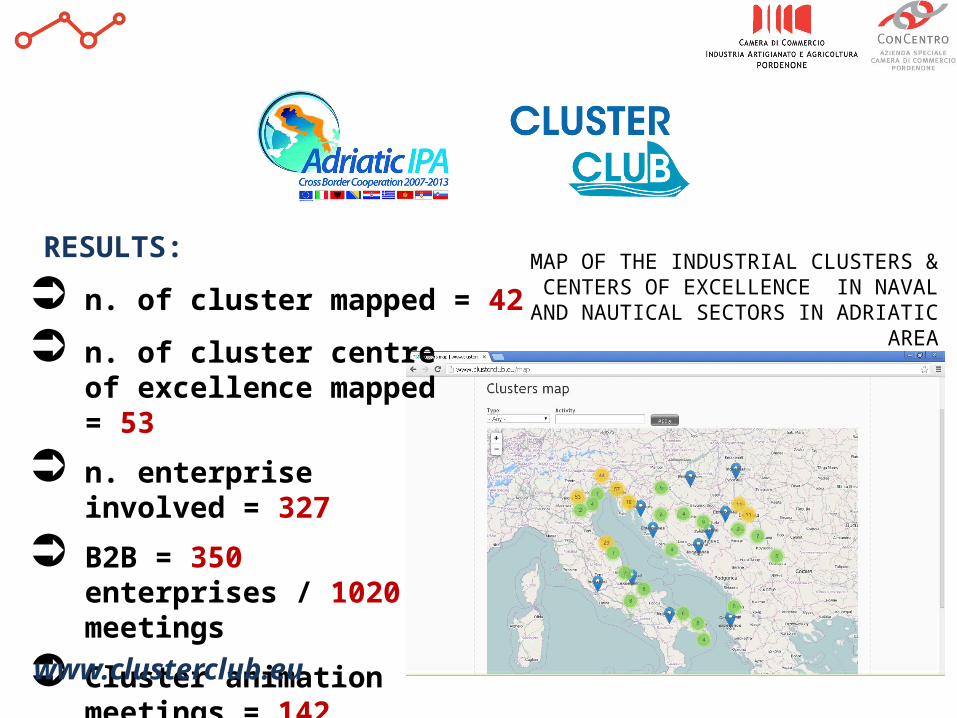

MAP OF THE INDUSTRIAL CLUSTERS & CENTERS OF EXCELLENCE IN NAVAL AND NAUTICAL SECTORS IN

ADRIATIC AREA

RESULTS:

n. of cluster mapped = 42

n. of cluster centre of excellence mapped = 53

n. enterprise involved = 327

B2B = 350 enterprises / 1020 meetings

Cluster animation meetings = 142 participants / 42 cluster

www.clusterclub.eu

GRAZIE!THANK YOU!

FALEMINDERIT!

Luca PennaAzienda Speciale ConCentro – CCIAA Pordenone