Economics Chapter 1 Lesson 3. Bell Ringer (same bell ringer paper from Chapter 1) Briefly explain a...

12

Economics Chapter 1 Lesson 3

Transcript of Economics Chapter 1 Lesson 3. Bell Ringer (same bell ringer paper from Chapter 1) Briefly explain a...

EconomicsChapter 1 Lesson 3

Bell Ringer(same bell ringer paper from Chapter 1)

• Briefly explain a time when you or someone you know went to the store to buy something you/they wanted but it was sold out. Perhaps the store did not have the size, color, or style you wanted. Perhaps it was a video game that sold out on the first day! Why do you think this happened?

Remember:

• Use the SAME Chapter 1 Notes paper to continue to right your notes on

• You only need write what is written in RED.

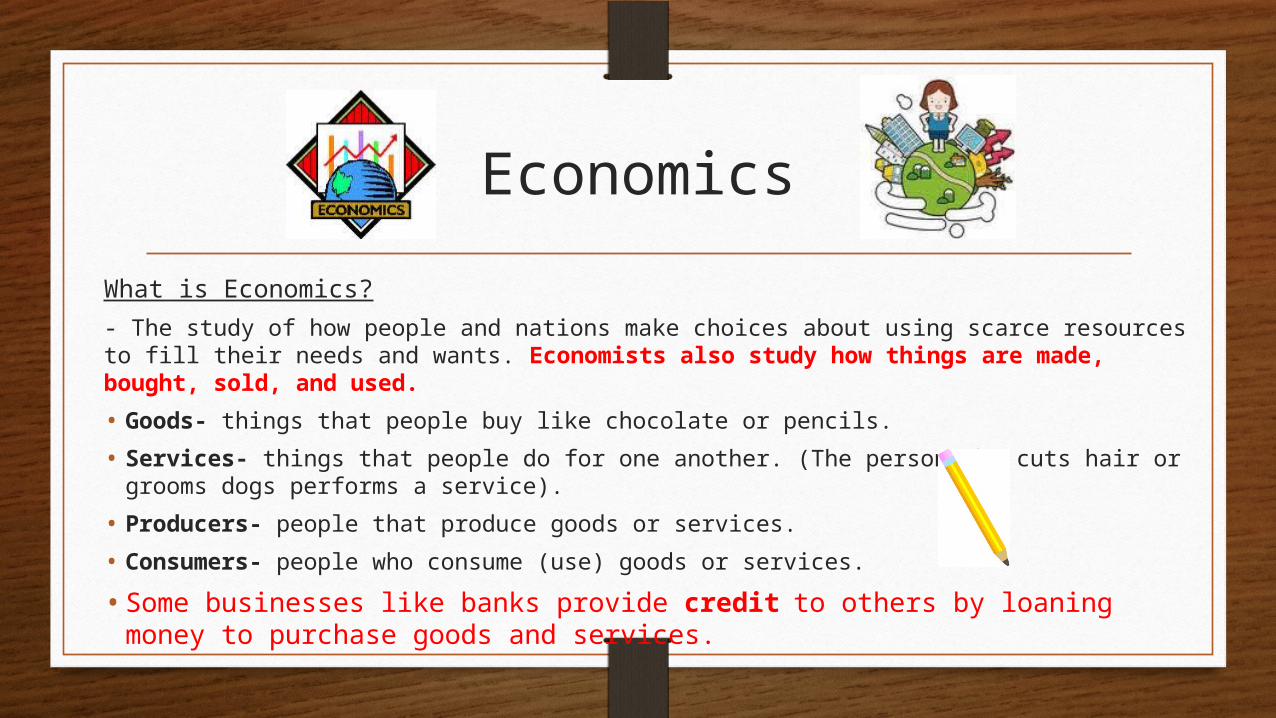

Economics

What is Economics?

- The study of how people and nations make choices about using scarce resources to fill their needs and wants. Economists also study how things are made, bought, sold, and used.

• Goods- things that people buy like chocolate or pencils.

• Services- things that people do for one another. (The person who cuts hair or grooms dogs performs a service).

• Producers- people that produce goods or services.

• Consumers- people who consume (use) goods or services.

• Some businesses like banks provide credit to others by loaning money to purchase goods and services.

Scarcity and Choice• Scarcity- when there is not enough resources to

produce everything people want and need.

• Choice- because of scarcity, people and societies must make choices about how to use resources.

• Scarcity of resources make Choices necessary.

Scarcity and Choice

• Example: Seinfeld Scarcity Example (1 min)

Scarcity is a challenge all societies face. The choices people make in response to it play a key role in how people live and how societies interact with each other.

The challenge that Elaine goes through in the stall is an example of how her want for toilet paper is greater than the availablity of the resource. Scarcity, forces you to make a choice; the new girlfriend refuses to share the toilet paper because she has a scarce supply of it. She makes a choice to use the limited resource ( toilet paper) and not share it with Elaine.

Opportunity Cost

• Remember: Scarcity forces us to make choices.

• Opportunity Cost is the chance you pass up when you make a choice.

> Example- Buying a song online is making a choice. You are choosing to spend money on buying a song instead of saving your money. Your decision to buy the song is the lost chance to save your money. The opportunity cost in this scenario would be not having the song you want if you instead decided to save your money.

Factors of Production

• Factors of Production are the resources needed to produce goods and services.

•Land-natural resources

•Labor- human resources

•Capital- human-made goods that people use to produce other goods and services (machines, buildings, tools). Sometimes money is considered a capital.

• Entrepreneurs are sometimes considered a factor of production. They organize and manage a business and bring together other factors of production. They take economis risks to make a profit.

Market and CommandEconomy

• Market Economy• Buyers and Sellers freely

choose to buy or make whatever they want.

• Customers seek the best deal.

• Little government involvement.

• This freedom leads to competition.

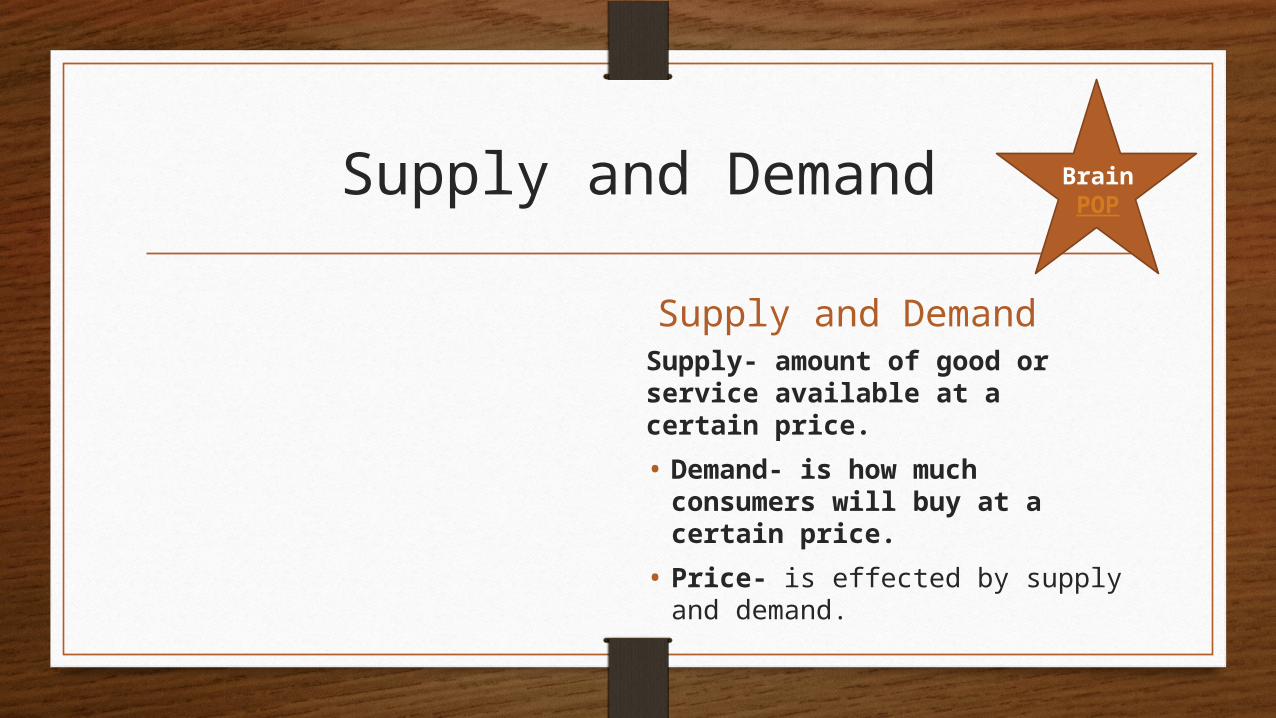

Supply and Demand

Supply and Demand Supply- amount of good or service available at a certain price.

• Demand- is how much consumers will buy at a certain price.

• Price- is effected by supply and demand.

BrainPOP

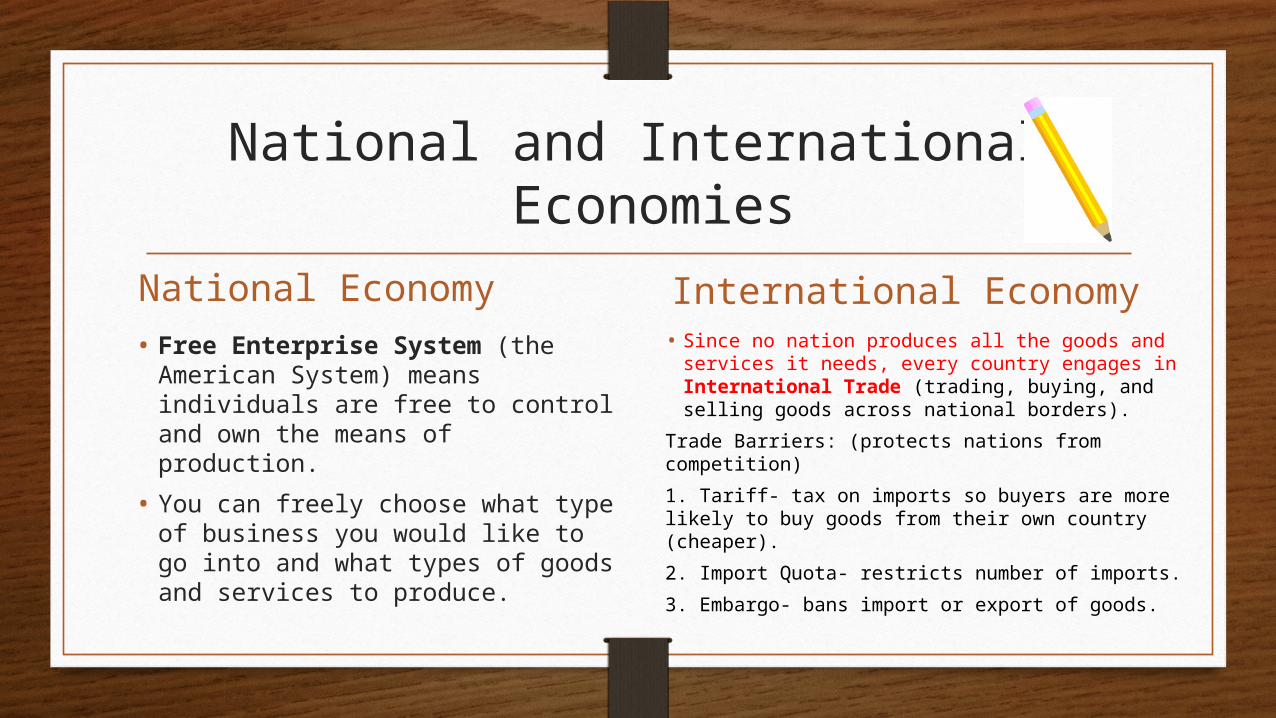

National and International Economies

National Economy

• Free Enterprise System (the American System) means individuals are free to control and own the means of production.

• You can freely choose what type of business you would like to go into and what types of goods and services to produce.

International Economy• Since no nation produces all the goods and

services it needs, every country engages in International Trade (trading, buying, and selling goods across national borders).

Trade Barriers: (protects nations from competition)

1. Tariff- tax on imports so buyers are more likely to buy goods from their own country (cheaper).

2. Import Quota- restricts number of imports.

3. Embargo- bans import or export of goods.

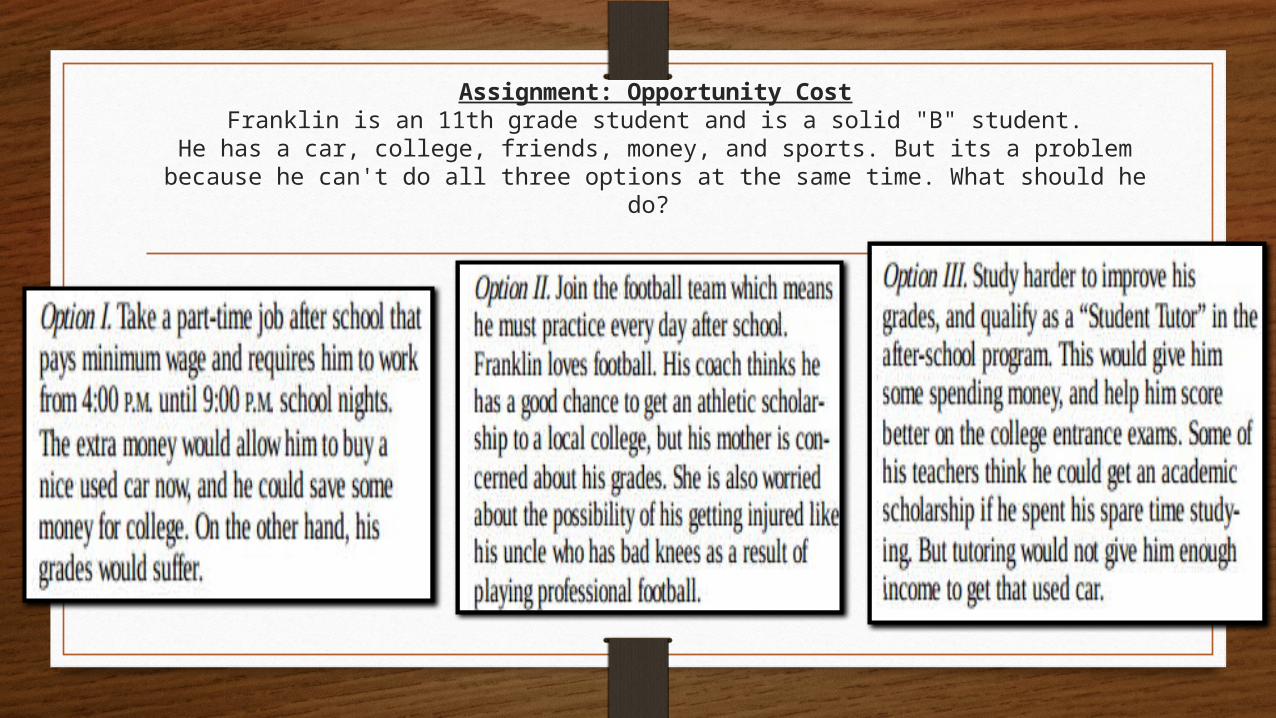

Assignment: Opportunity CostFranklin is an 11th grade student and is a solid "B" student.

He has a car, college, friends, money, and sports. But its a problem because he can't do all three options at the same time. What should he do?