Economics 2010 Lecture 11 Organizing Production (I) Production and Costs (The short run)

31

Economics 2010 Economics 2010 Lecture 11 Organizing Production (I) Production and Costs (The short run)

-

Upload

grant-dalton -

Category

Documents

-

view

216 -

download

2

Transcript of Economics 2010 Lecture 11 Organizing Production (I) Production and Costs (The short run)

Economics 2010Economics 2010

Lecture 11

Organizing Production (I)

Production and Costs

(The short run)

Output and CostsOutput and Costs

Product Concepts and DefinitionsProduct CurvesCost Concepts and DefinitionsShort-Run Cost Curves

Product Concepts and DefinitionsProduct Concepts and DefinitionsTotal product (TP) is the number of

units of output produced in a given time period.

Marginal product (MP) is the increase in total product, TP, resulting from a one-unit increase in the amount of the variable factor (labor) employed.

Average product (AP) is total product per unit of the variable factor (labor) employed.

Total Product CurveTotal Product CurveFigure shows

the total product (TP) curve for sweaters

The curve separates what is attainable from what is unattainable

Marginal Product CurveMarginal Product CurveWe show here

the total product (TP) curve for sweaters again

But now, we emphasize the idea of marginal product

Marginal Product CurveMarginal Product CurveThe marginal

product (MP) curve for sweaters

Marginal product in this case increases and then diminishes

This is to be expected

Average Product CurveAverage Product Curve

average product (AP) curve for sweaters (purple)

and the marginal product curve (pink)

Average Product CurveAverage Product Curve

Average product equals marginal product at the maximum of average product

Average Product CurveAverage Product Curve

When marginal product exceeds average product, average product is increasing

Average Product CurveAverage Product Curve

When marginal product is less than average product, average product is decreasing

Average Product CurveAverage Product Curve

When marginal product equals average product, average product is at its maximum

Marginal-Average RelationsMarginal-Average Relations

The relationship between a marginal value and an average value that you’ve just seen is universal (it is a mathematical certainty!)

Initial Increasing ReturnsInitial Increasing ReturnsWe know that as a firm uses more of a

variable input, with the quantity of fixed inputs held constant, the marginal product of the variable input at first increases

The Law of Diminishing The Law of Diminishing ReturnsReturns

As a firm uses more of a variable input, with the quantity of fixed inputs held constant, the marginal product of the variable input eventually diminishes

Intuition on product curvesIntuition on product curvesMarginal product and average product

at first increase because of specialization and the division of labor

Marginal product and average product eventually diminish because the gains from specialization and the division of labor are limited and the plant eventually becomes congested

Too many people in the kitchen will spoil the broth!

Cost Concepts and DefinitionsCost Concepts and DefinitionsTotal cost (TC) is the sum of the costs

of all the inputs used in production. Total cost is divided into two parts:

Total fixed cost (TFC) is cost of all fixed inputs. Total fixed cost is independent of the level of output

Total variable cost (TVC) is cost of all variable inputs. Total variable cost varies with the level of output

TC = TFC + TVC

Cost Concepts and DefinitionsCost Concepts and Definitions

Marginal cost is the increase in TC resulting from a one-unit increase in output. It is calculated as the change in total cost divided by the change in total output

Cost Concepts and DefinitionsCost Concepts and Definitions

Average cost is cost per unit of outputAverage fixed cost (AFC) is total fixed

cost per unit of output.Average variable cost (AVC) is total

variable cost per unit of output.Average total cost (ATC) is total cost

per unit of output.ATC = AFC + AVC

Cost Concepts and DefinitionsCost Concepts and Definitions

Short-run Cost CurvesShort-run Cost Curves

Total cost curvesAverage cost curvesMarginal cost curve

They apply when at least some of our inputs are fixed

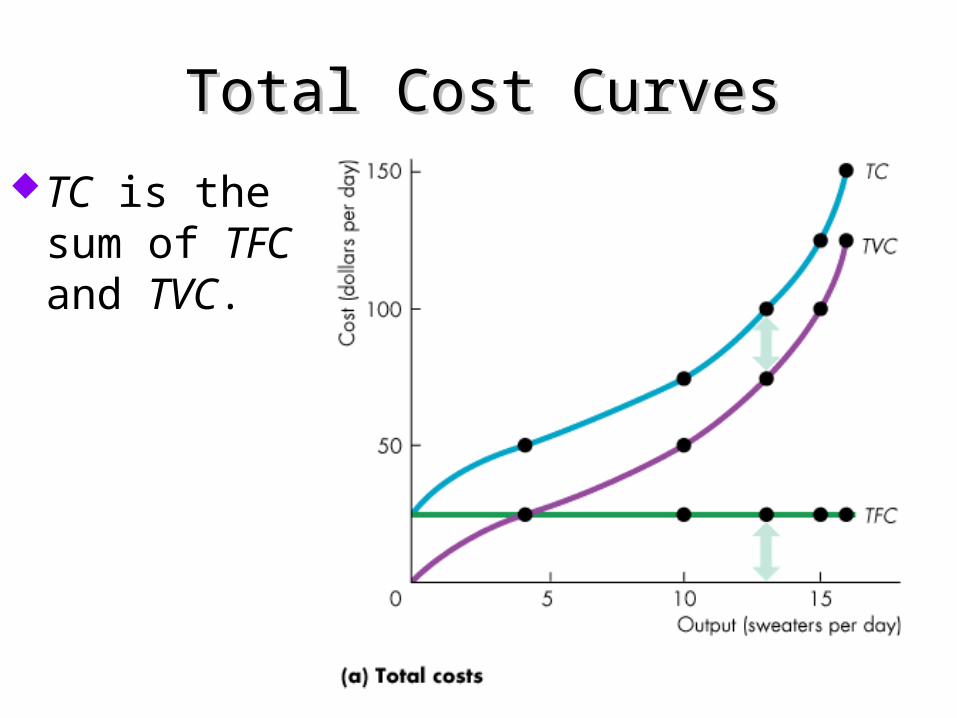

Total Cost CurvesTotal Cost Curves

Look at the total cost curves for sweaters

TFC is constant at $25, remember?

TVC is based on the TP curve.

Total Cost CurvesTotal Cost Curves

TC is the sum of TFC and TVC.

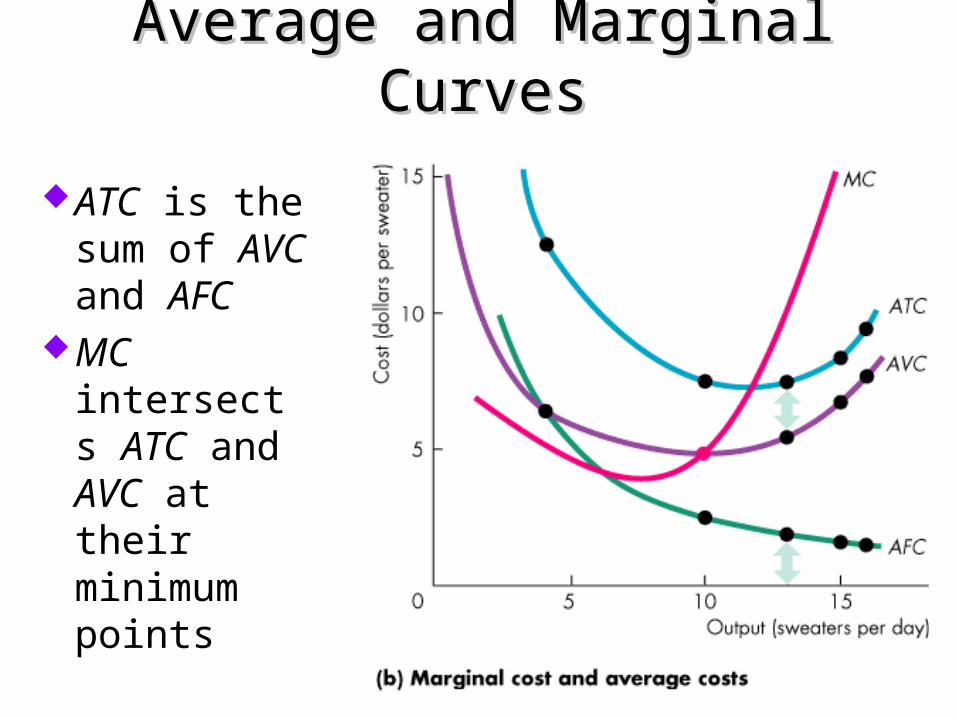

Average and Marginal CurvesAverage and Marginal Curves

We show here the average cost curves and the marginal cost curve

Average and Marginal CurvesAverage and Marginal Curves

ATC is the sum of AVC and AFC

MC intersects ATC and AVC at their minimum points

Average and Marginal CurvesAverage and Marginal Curves

When marginal cost is less than average cost, average cost is decreasing

Average and Marginal CurvesAverage and Marginal Curves

When marginal cost exceeds average cost, average cost is increasing.

Average and Marginal CurvesAverage and Marginal Curves

When marginal cost equals average cost, average cost is at its minimum

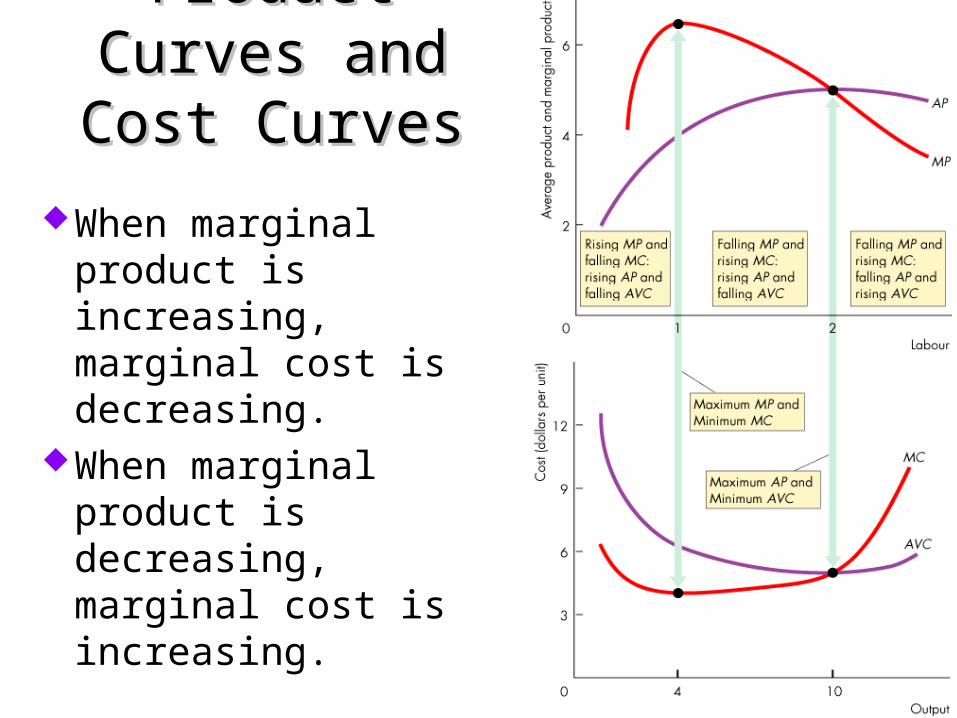

Product Curves Product Curves and Cost Curvesand Cost Curves

When marginal product is increasing, marginal cost is decreasing.

When marginal product is decreasing, marginal cost is increasing.

Product Curves Product Curves and Cost Curvesand Cost Curves

When average product is increasing, average cost is decreasing

When average product is decreasing, average cost is increasing

Product Curves Product Curves and Cost Curvesand Cost Curves

When average product is at its maximum, average variable cost is at its minimum

Relate the ideas of cost and product curves

Product curves are using only information from the technological cookbook

Cost curves add the information on prices too

![[3] Production and Costs](https://static.fdocuments.us/doc/165x107/55cf949c550346f57ba329fa/3-production-and-costs.jpg)