Economic Trends in Israel Macroeconomic Review General data General data General data General data...

74

Economic Trends in Economic Trends in Israel Israel Macroeconomic Review Macroeconomic Review General data Product and employment Balance of payments and externa l stability Fiscal policy Monetary policy and inflation r ate Economics and Research Department / Ministry of Finance January 2007 contacts for comments and questions contacts for comments and questions : : [email protected]

-

Upload

derick-burke -

Category

Documents

-

view

219 -

download

1

Transcript of Economic Trends in Israel Macroeconomic Review General data General data General data General data...

Economic Trends in IsraelEconomic Trends in IsraelMacroeconomic ReviewMacroeconomic Review

General dataProduct and employmentBalance of payments and external stabilityFiscal policyMonetary policy and inflation rate

Economics and Research Department / Ministry of FinanceJanuary 2007

contacts for comments and questionscontacts for comments and questions : :[email protected]

Economic Trends in IsraelEconomic Trends in Israel

General dataGeneral dataProduct and employmentProduct and employmentBalance of payments and external stabilityBalance of payments and external stabilityFiscal policyFiscal policyMonetary policy and inflation rateMonetary policy and inflation rate

General dataGeneral data

1. Level of technology

2. Level of education

General dataGeneral data

1. Level of technology

2. Level of education

Expenditure on Civilian R&D as percent of the GDP in Israel and in OECD Countries, 2003

Israel ranks first in R&D investment (as percent of GDP).

4.74.5

3.73.5

3.12.9

2.62.6 2.52.2 2.2 2.2

2.0 2.0 1.9 1.9 1.91.7 1.7 1.7 1.6 1.61.6

1.31.1 1.1 1.01.0 0.9 0.8 0.7 0.60.6 0.6

0.4

0

1

2

3

4

5

Isra

el (2

005)

Isra

el (2

003)

Sweden

Finla

nd

Japan

Icela

nd

Korea

Switzer

land (2

000)

Germ

any

United

Sta

tes

Denm

ark (2

002)

Austri

a

Total

OECD

EU15

Belgiu

m

France

EU25

Luxem

bourg

(200

0)

United

Kin

gdom

Nether

land

s (20

02)

Austra

lia (2

002)

Canad

a

Norway

Czech

Rep

ublic

Irela

nd (200

2)Ita

ly

New Z

eala

nd

Hungary

Spain

Portu

gal (2

002)

Turkey

(200

2)

Greec

e (20

01)

Slovak

Rep

ublic

Poland

Mex

ico (2

001)

* Average of 30 OECD countries.

ICT Product as percent of total business sector product, 2001

16.416.2 16.1

13.112.2

11.411.210.0 9.8 9.6 9.6 9.3 9.0 8.7 8.7 8.6 8.4 8.4 8.1 8.1 8.1 7.8 7.8 7.4 7.0 6.8

6.35.4

0

5

10

15

20

Finlan

d

Israe

l (20

05)

Israe

l (20

01)

Irela

nd

Korea

USA UK

New Z

ealan

d

Honga

ry

OECD aver

age

Nether

lands

Sweden

Czech

Rep

ublic

Denm

ark

Austria

EU aver

age

France

Norway

Australi

a

Spain

Portu

gal

Canad

a

Japan

Italy

Belgiu

m

Germ

any

Greec

e

Mex

ico

Israel ranks second in its proportion of ICT production in total business sector product.

General dataGeneral data

1. Level of technology

2. Level of education

Percent of Population that attained at least upper secondary education, ages 25-64, 2003

One measure of the country’s level of education is the percent of its population that has at least twelve years of schooling. By this measure, Israel ranks rather high by international standards.

21 23

43 4448

59 59 62 62 62 65 65 66 6670 73 74 76 78 79 81 82 82 83 84 84 87 87 88

0

10

20

30

40

50

60

70

80

90

100

Mex

ico

Portu

gal

Spain

Italy

2002

Poland

Icela

nd 2002

Luxem

burg

Austral

ia

Belgiu

m

Irela

nd

Franc

eUK

Nethe

rlands 2

002

OECD aver

age

Switzer

land

Korea

Greec

e

Finla

nd

New Z

ealan

d

Austria

Denm

arkIsr

ael

Sweden

Germ

any

Canad

a

Japan

Norway

Slovak

Rep

ublicUSA

Economic Trends in IsraelEconomic Trends in Israel

General dataGeneral dataProduct and employmentProduct and employmentBalance of payments and external stabilityBalance of payments and external stabilityFiscal policyFiscal policyMonetary policy and inflation rateMonetary policy and inflation rate

Product and EmploymentProduct and Employment

1. GDP Growth Rate2. GDP per-capita – international comparison3. Factors affecting growth4. Characteristics of growth5. Unemployment and the labor market

Product and EmploymentProduct and Employment

1. GDP Growth Rate2. GDP per-capita – international comparison3. Factors affecting growth4. Characteristics of growth5. Unemployment and the labor market

GDP GrowthGDP Growth((quarter-on-quarter at annual rate, 1995Q2-2006Q3quarter-on-quarter at annual rate, 1995Q2-2006Q3))

The growth rates are expressed as the rate of quarter-on-quarter change in annual terms. In 1999–2000, Israel experienced high growth rates relative to the economy’s past performance and by international standards. Since October 2000, the growth rate has been declining due to the global economic slowdown (mainly with respect to demand for high-tech products which are the mainstay of Israeli exports), the decline on the Nasdaq index, which reduced investments in Israeli start-up companies and in high-tech industry in general, and due to the adverse effects of Palestinian terrorism on tourism, construction, agriculture as well as on exports to the Palestinian Authority areas. Contractionary monetary policy was a further impediment to growth. A rebound began in the second half of 2003 and gained momentum during 2004, 2005 and the first half of 2006. The slowdown in the third quarter was only temporary and resulted from the war in the north and especially from the drop in exports during that period. Real indicators published after the end of the war show a rapid rebound in the economy, with the result that in the fourth quarter the economy will revert to the rate of growth characteristic of the first half of 2006. Factors contributing to the upsurge in growth since the second half of 2003 include the global economic recovery, which was reflected by an expansion in world trade and the amount of activity in the high-tech industries, the structural reforms that were implemented in the Israeli economy, reduced uncertainty and the increased confidence resulting from the adoption of a decisive fiscal policy, a relatively calm security situation (excepting the period of the war in the north) and a less restrictive monetary policy.

8.0%

5.9%

-0.6%

2.3%

0.6%

7.4%

6.1%5.7%

4.3%

5.9%5.6%6.4%

-1.1%

3.4

4.4%

5.0%

-3.0%

1.7%

1.0%

0.6%

6.7%5.9%

10.2%

2.1%

-2.6%

1.0%

3.8%

-1.5%

10.1%

6.1%

5.1%

1.8%

4.8%

11.3%

0.4%

4.3%

0.9%

14.5%

-4.1%

-6.7%

4.2%

14.6%

1.6%1.4%

-5.1%

3.7%

-10%

-5%

0%

5%

10%

15%

20%

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

GDP Per Capita Growthannual percent change

GDP per capita is an indication of a country’s standard of living. Israel’s per-capita GDP declined in 2001-2003 by 6.0 percent in cumulative terms. This is an unprecedented decline in the standard of living. In 2005, due to the economic recovery, GDP per-capita climbed by 3.4 percent. This trend is expected to continue and to reach GDP per-capita growth of 3.1 percent in 2006 and 2.4 percent in 2007.

2.4%3.1%

3.4%3.0%

-0.3%

-2.9%-2.9%

4.4%

1.9%

-0.3%

3.4%

0.0%

3.4%

1.1%

4.3%3.7%

3.0%

0.3%1.7%

0.3%

5.9%

-5%

-3%

-1%

1%

3%

5%

7%

1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006CBSest.

2007proj.

Average 1987-2000: 2.4%

Average 2001-2003: -2.1%

Average 2004-2007:3.0%

Product and EmploymentProduct and Employment

1. Domestic growth rate2. GDP per-capita – international comparison3. Factors affecting growth4. Characteristics of growth5. Unemployment and the labor market

GDP per capita (PPP-adjusted), index (USA = 100), 2005

In 2005, GDP per-capita was lower in Israel than in the U.S. and most Western European countries, but higher than in many OECD countries. Israel’s GDP per-capita in 2005 was 72 percent of the weighted average in the OECD countries and 56 percent of GDP per-capita in the U.S.

8985

7872 71 69 68

58 58 56

48

38 3632 29 28

24 2420 19 18 16

134

10090

8881

75 73 70727383 80

595254

47

35

29

4541

24

74

0

20

40

60

80

100

120

140

160

OECD other countries

Product and EmploymentProduct and Employment

1. Domestic growth rate2. GDP per-capita – international comparison3. Factors affecting growth4. Characteristics of growth5. Unemployment and the labor market

The U.S. Economy, 1995-2006real growth rates of GDP and business investment

The domestic slowdown in 2001 and 2002 was affected by the growth slowdown in the U.S. and by the change in GDP composition, which was focused on business investment decline. This downturn in investments by American firms led to a decrease in demand for Israeli exports, which are heavily tilted in the direction of these products. U.S. GDP growth and American corporate investments began to recover in 2003. This trend, foremost in investments by American firms, became much stronger in 2004, 2005 and the first quarter of 2006. Since the second quarter of 2006 the GDP growth rate in the USA has slowed, although the level of American firms’ investment in the third quarter was relatively high.

3.7%

0.8%1.6%

3.9%3.2%

5.6%

2.6% 2.0%

9.3%

12.1%11.1%

9.2% 8.7%

-4.2%

5.9%4.4%

10.0%

3.1%

4.4%4.2%4.5%3.7%

2.5%

13.7%

-9.2%

1.0%

10.5%

6.8%

-15%

-10%

-5%

0%

5%

10%

15%

GDP

Private Nonresidential Fixed Investment

* *compared to previous quarter, at annual rate, s.acompared to previous quarter, at annual rate, s.a..

Growth in Advanced EconomiesGrowth in Advanced Economies(weighted average: US - 44%, Euro area - 37%,(weighted average: US - 44%, Euro area - 37%,

Japan - 4%, UK - 8%, Asian NIEs - 7%)Japan - 4%, UK - 8%, Asian NIEs - 7%)

The growth rate of GDP in advanced economies was calculated as a weighted average in terms of its share in Israeli exports. The global growth rate recovered in 2004 (relative to 2001–2003). This trend continued through 2005 and 2006 and thus supported Israeli exports. The global rate of growth in 2007 is expected to be lower than in 2006 but still high in comparison with the years 2001-2003.

3.22.9 2.9 3.0

3.6

2.9

3.84.0

1.31.6

2.0

3.4

2.6

3.1

2.3

3.6

0

1

2

3

4

5

1984-1993

1994-2003

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 est2006

Proj2007

The Nasdaq Index and Investment of VCs in Start Ups in Israel

The steep decline in the Nasdaq index in 2000–2002 had a severe downward effect on capital raised by VC funds. This in turn, dampened investments in Israeli start-up companies (as well as in American companies). The decline was harmful to the high-tech industry and affected the economic downturn in Israel that began in late 2000. Since the end of 2002, the Nasdaq exchange has staged a recovery that helped to increase investments in Israeli start-up companies during 2003-2005, although the level is still lower than the peak of 2000.

1000

1500

2000

2500

3000

3500

4000

4500

5000

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Nas

daq

Inde

x

0

200

400

600

800

1000

1200

US$ M

illions

Nasdaq Israel

Tourist Arrivalsthousands per month

The security situation in Israel and abroad led to a 63% decrease in the number of tourists arriving in Israel during the first half of 2006 compared with the first half of 2000. From the second half of 2003 until the outbreak of the war in the north, incoming tourism increased to a considerable extent as a result of the improvement in the security situation in Israel, the positive effects of the end of the war in Iraq and the global economic recovery. The war in the north badly affected incoming tourism. The monthly average number of tourists arriving by air from the time the war started (during July-December 2006) was 33% less than the monthly average for the second quarter of 2006.

0

50

100

150

200

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

Attack on the Achille Lauro

Intifada

Gulf War

Terrorist Attacks

War in Iraq

Pope visit

Sep 11th

Terrorist attack in Netanya, March 2002

Start OfPalestinianTerrorist Attacks, Sep 2000

War in Lebanon

Person-Nights at Hotelsthousands per month

The stability in local tourism slightly softened the adverse impact of inbound tourism due to the war in the north.

0

200

400

600

800

1,000

1,200

1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

TouristsIsraelis

The Short-Term Real Interest RateThe Short-Term Real Interest Rate(Derived from the Bank of Israel’s key lending rate)(Derived from the Bank of Israel’s key lending rate)

5.8%

2.7%

1.7%

3.4%

2.3%

1.6%1.5%1.7%

2.0%1.8%

1.5%1.5%1.1%

1.5%1.9%

3.3%3.7%

4.2%3.8%

3.9%

2.7% 2.6%2.8%2.8%

3.2%

3.7%

3.5%3.5%

5.9%

7.8%8.0%

3.1%

4.4%

5.9%

5.4%

3.4%3.4%

0%

2%

4%

6%

8%

10%

Annual averages

Contractionary monetary interest rates in 2001–2003 contributed to the deceleration of GDP growth and delayed recovery from the recession. A decrease in the interest rate took place in the beginning of 2005, as it decreased gradually to 3.5 percent until February 2005 and stayed at this level until September 2005. As a result, the real interest rate was lower in 2004 and 2005 than in previous years. From September 2005, the Bank of Israel’s interest rate rose gradually from 3.5% to a level of 5.5% in August 2006, remained unchanged in September and October 2006 and decreased from November 2006 to a level of 4.5% in January 2007. The rise in the interest rate during the first eight months of the year reflected the global rise in interest rates, the increase in fuel prices, and the publication of data showing continued rapid growth in the economy and a decline in the unemployment rate. The interest rate in Israel was also raised because o BOI concern over the adverse impact on stability of the war in the north. The reduction in the interest rate during recent months reflects mainly the strength of the NIS and the decrease in fuel prices.

3

4

5

6

long term (11 years, excluding first year)

Real Long-Term Interest Rate in View of the Improvement in Fiscal Credibility

The favorable turnaround in domestic activity in 2003-2006 was supported by firm government measures to restrain public expenditure. This is an essential step in returning the budget deficit and the public debt to a downward trajectory, and by structural reforms that bolstered the recovery and reinforced sustainable growth. An economic program to cope with the steep increase in the rate of the budget deficit was applied in the middle of 2003. The tough fiscal policy that was part of the program, coupled with policy measures incorporated into the 2004-2006 budgets, did much to enhance fiscal credibility. This, coupled with the receipt of the U.S. Government guarantees, made the financial markets more confident and brought down the real interest rate on long-term indexed bonds.

receiving loan guarantees

Support Israel’s international credit rating, calm the foreign exchange market, and stabilize inflation expectations

Reduce the pressure on domestic financial markets and lower domestic long-term interest rates

Lower the short-term interest rate

Increase aggregate demand

Higher growth rate

Growth in investments

Enhance Government’s ability to meet deficit targets

Maintain macro-economic stability

The Macroeconomic Effects ofThe Macroeconomic Effects ofLoan GuaranteesLoan Guarantees

Product and EmploymentProduct and Employment

1. Domestic growth rate2. GDP per-capita – international comparison3. Factors affecting growth4. Characteristics of growth5. Unemployment and the labor market

Industrial Production Index

The economic slowdown was reflected in a decline in industrial production from late 2000 to the end of 2001. From 2002 until the first half of 2003, industrial output was stable at a lower level. A recovery began in the second half of 2003. This trend became much stronger in 2006.

80

85

90

95

100

105

110

115

120

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

annual averages

Private consumption expenditure

In 2001, despite the economic slowdown, private consumption increased in absolute terms and as a share of GDP. In 2002, on the other hand, private consumption declined moderately as the duration of the recession prompted households to adjust their estimates of permanent income downward. This trend gathered strength in the first quarter of 2003 in view of the war in Iraq. Private consumption advanced briskly from the second quarter of 2003. The main factors contributing to the growth in private consumption are the rebound in the economy, the increase in real wages, the reduction in tax rates, the increase in the value of the public’s asset portfolio and the decline in the real interest rate. Expenditure on private consumption rose by 4.2% during the first three quarters of 2006 compared with the same period of 2005.

50

55

60

65

70

75

80

85

1999 2000 2001 2002 2003 2004 2005 2006

PRIVATE CONSUMPTION EXPENDITURE (NIS BILLIONS, 2005 PRICES, s.a.)

AS PERCENT OF GDP, AT CURRENT PRICES, ANNUAL AVERAGES

The revenue of the commerce and service industries, which reflects developments in private consumption, fell in 2002 and in the first half of 2003 after remaining stable during the years 2000 and 2001. The revenues data have been pointing to recovery since the second half of 2003.

Commerce and Services Sectors real monthly revenue index

60

70

80

90

100

110

120

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Fixed Investment

Fixed investment decreased in the last few years. The contraction in 2001–2003 affected most industries in the business sector and reflected the security and economic uncertainty, the global slowdown, and domestic monetary restraint. The decline in 2004, in contrast, traced mainly to a decrease in construction investment, a field in which rather large surpluses relative to demand had built up during the recent recession years. Net of the effects of dwelling stocks, investments in machinery, equipment, and transport vehicles increased. Total investments in fixed assets increased by 2.9 percent in 2005. The recovery process continued and even gained strength in the first three quarters of 2006. During that period, investment in fixed assets expanded by 5.1% compared with the same period of 2005.

14

16

18

20

22

24

26

28

30

32

1999 2000 2001 2002 2003 2004 2005 2006

FIXED INVESTMENT (NIS BILLIONS, 2005 PRICES, s.a.)

AS PERCENT OF GDP, AT CURRENT PRICES, ANNUAL AVERAGES

Housing Starts and Fixed InvestmentHousing Starts and Fixed Investmentin residential constructionin residential construction

Housing starts attest to the trend of future activity, since homebuilding lasts about a year and a half. The decrease in homebuilding starts has continued with variations since 1997, although the number of starts seems to have leveled off in 2004. An upturn in the number of building starts was recorded in the first quarter of 2006, although this trend was not maintained in the second and third quarters of the year.

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

hous

ing

unit

s pe

r qu

arte

r

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

NIS

mill

ion

s p

er

qu

art

er

(20

00

pri

ce

s)

Housing starts, housing units per quarter

Fixed investment in residential consruction, seasonaly adjusted

Structure of Industrial Exports

The recession in 2001–2002 was also reflected in a decrease in exports. Exports recovered slightly in 2003. This trend gathered strength in 2004, 2005 and the first eleven months of 2006, and reflects the effect of the real depreciation of the NIS in 2002-2004, the global economic recovery, the expansion of global trade and high-tech activity, the rapid recovery in the area of incoming tourism, the decrease in real domestic wages in 2002-2003, and corporate efficiency measures. Both high-tech and traditional industries took part in the upturn in exports.

15,962 14,862 13,525 14,16617,308 18,789

21,845

7,895

5,1884,731

4,7304,836

4,277

6,321

6,693

7,188

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

1995 2000 2001 2002 2003 2004 2005 2006 *Jan-Nov at

annual rate

US

$ m

illio

ns

traditional industrieshi-tech industries

35%

65%

23% 24%

76%77%27%

74%

26%27%

75%74%

26%

73%

25%

73%

Net Inflows of Foreign InvestmentUS $ billions

Foreign investment in Israel (direct investments in Israeli enterprises, portfolio investments and other investments) fell from $ 12.3 billion in 2000 to $ 3.2 billion in 2002 as a result of the global slowdown, the NASDAQ crisis and the security situation. From 2003, foreign investment increased and totaled $ 11.6 billion in 2005 and estimated at $ 16.0 billion in 2006 .

16.0

12.3

5.4

3.21.8

2.0 2.3

6.3

4.9

6.5

8.6

4.5

9.6

4.1

8.1

3.4

11.6

-2

0

2

4

6

8

10

12

14

16

18

20

22

24

26

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 *2006est.

FDI

Portfolio Investment

Other Investment

Total

*Portfolio Investments do not include Teva/Ivax deal completed in January 2006.

Product and EmploymentProduct and Employment

1. Domestic growth rate2. GDP per-capita – international comparison3. Factors affecting growth4. Characteristics of growth5. Unemployment and the labor market

The Unemployment RateThe Unemployment Rateand the Participation Rateand the Participation Rate

One reflection of the recession that began in 2000 was, among other things, an increase in the unemployment rate from 8.8% in 2000 to 10.3% in 2002. Despite the economic recovery that began in 2003, the unemployment rate continued to climb that year and peaked at 10.9% in the second half. In 2004, the unemployment rate fell to 10.4% on annual average. This trend continued in 2005 and in the third quarter of 2006, when the unemployment rate fell to 9.0% and 8.3% respectively. The large increase in the labor force participation rate is a direct result of the government’s policy of reducing transfer payments, cutting back on the number of foreign workers, encouraging a move from welfare to work and the recovery in the economy. The growth in the participation rate (which is low in Israel by international comparison), although it delays a more rapid decline in the unemployment rate in the short run, improves the economic situation.

6.9%6.7%

7.7%

8.6%8.9% 8.8%

9.4%

10.3% 10.4%10.7%

9.0%

8.6% 8.2%

4%

6%

8%

10%

12%

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006est.

2007proj.

52%

53%

54%

55%

56%

Participation rateright axis

Employment of Israelis(Thousands)

Despite the still high unemployment rate, the labor market took a turn for the better as Israelis returned to the employment cycle and new jobs were created. The number of Israelis employed increased markedly since the first quarter of 2003 until the end of the third quarter of 2006 (by 262 thousands), reflecting the economy recovery and the successful implementation of Government policies that aimed to downsize the population of foreign workers and reduce transfer payments.

2,579

1,800

1,900

2,000

2,100

2,200

2,300

2,400

2,500

2,600

2,700

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

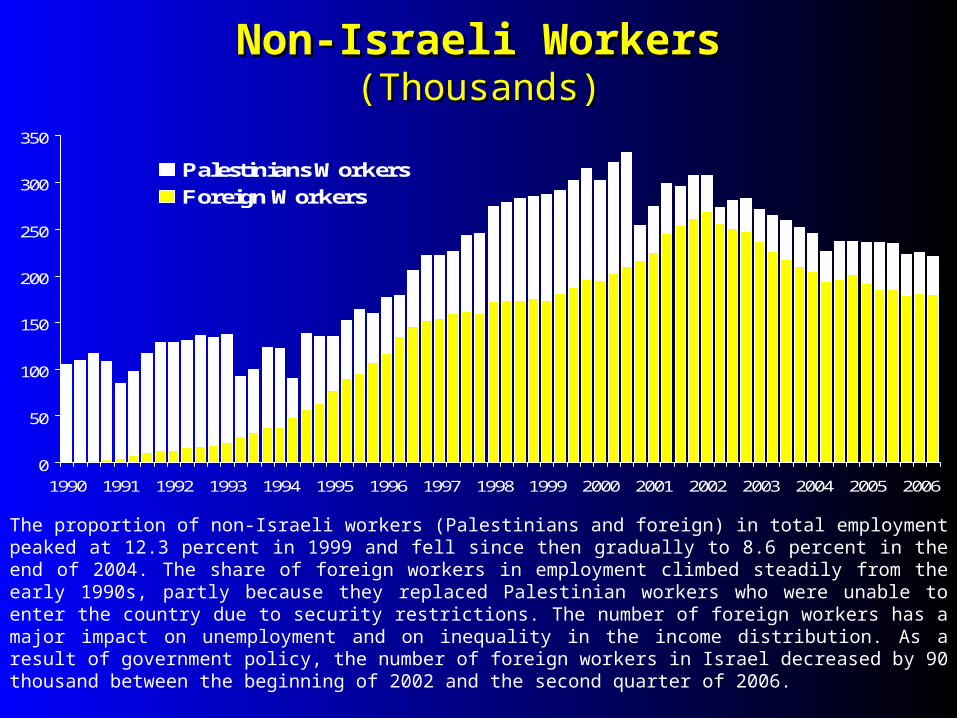

The proportion of non-Israeli workers (Palestinians and foreign) in total employment peaked at 12.3 percent in 1999 and fell since then gradually to 8.6 percent in the end of 2004. The share of foreign workers in employment climbed steadily from the early 1990s, partly because they replaced Palestinian workers who were unable to enter the country due to security restrictions. The number of foreign workers has a major impact on unemployment and on inequality in the income distribution. As a result of government policy, the number of foreign workers in Israel decreased by 90 thousand between the beginning of 2002 and the second quarter of 2006.

Non-Israeli WorkersNon-Israeli Workers(Thousands)(Thousands)

0

50

100

150

200

250

300

350

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Palestinians Workers

Foreign Workers

Real Wages Real Wages ((CPI-adjusted 2004 pricesCPI-adjusted 2004 prices))

6,908

7,366

6,805

7,1526,971

6,613 6,521

6,825 6,821

7,7197,747

7,503

7,038 7,0567,160

7,268

6,000

6,500

7,000

7,500

8,000

1999 2000 2001 2002 2003 2004 2005 2006Jan-Oct

Real wages - public sector

Real wages - business sector

Real wages per employee post in the business sector have risen since 2003 and was 4.4% higher in Real wages per employee post in the business sector have risen since 2003 and was 4.4% higher in the first ten months of 2006 (monthly average) than the average wage in 2003. Concurrently, real the first ten months of 2006 (monthly average) than the average wage in 2003. Concurrently, real wages in the public sector increased by 5.9%wages in the public sector increased by 5.9%..

Participation rate of Men, Ages 25-54, 2004

83

85

8889 89

90 90 90 91 91 91 91 91 91 92 92 92 92 92 92 9393 94 94 94

94 95 9595

96 96 96

82

84

86

88

90

92

94

96

98

100

One reason for the lower standard of living in Israel than in Western Europe and the U.S. is that Israel has a low labor-force participation rate, especially among men. This is due to a low participation rate among the ultra-Orthodox, to the large population of foreign workers who depress wage levels in industries such as construction and agriculture, making them unattractive to Israelis, and to the level of transfer payments. The purpose of the economic policy of using fewer foreign workers and reducing transfer payments is to boost the labor-force participation rate.

* Average of 30 OECD countries.

Economic Trends in IsraelEconomic Trends in Israel

General dataGeneral dataProduct and employmentProduct and employmentBalance of payments and external stabilityBalance of payments and external stabilityFiscal policyFiscal policyMonetary policy and inflation rateMonetary policy and inflation rate

Balance of Payments and External Balance of Payments and External StabilityStability

1. Balance-of-payments2. Foreign reserves3. External Debt

The Current Accountmillions of dollars & percent of GDP

The current account of the balance of payments is the net balance of total export receipts less total payments for imports of goods, services, and factors, and unilateral transfers (including the American grant in aid). This is the most important indicator of the state of the economy vis-a-vis the rest of the world in terms of imports and exports. In 2003-2005 and in the year ending in the third quarter of 2006, the current account was in a surplus. The surplus attests to high external stability both by international standards and relative to the deficits that were observed in the mid-1990s.

4.9%

2.9%

0.5%

-2.1%

-4.3%-5.1% -5.1%

-3.2%

-1.2%-1.5%

-1.2% -1.3%-0.6%

1.4%

2.5%

-3.5%-1.3%

0.3%

-6000

-4000

-2000

0

2000

4000

6000

8000

10000

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

Percent of GDP

\

Official Reserve Assets

The reserves include foreign currency held by the Bank of Israel in short-term accounts abroad (mainly U.S. Treasury bills). Israel’s reserves are high, both by international standards and in terms of months of imports. This assures Israel’s ability to finance its liabilities in the short term and to meet its import needs, and it corroborates the assessment of the low probability of a balance-of-payments crisis.

0

10,000

20,000

30,000

0

1

2

3

4

5

6

7

8

In Millions of US Dollars

In Months of Imports(of goods and nonfactor services)

External Debt, Gross and NetExternal Debt, Gross and Net(percent of GDP, end-period)(percent of GDP, end-period)

80.8

58.7

-22.0

-40

-20

0

20

40

60

80

100

1990 1995 1998 1999 2000 2001 2002 2003 2004 2005 Spt'2006

gross debtforeigners liabilities to Israelisnet debt

The net external debt (total external liabilities less external assets) was minus 22.0 percent of GDP at the end of the third quarter of 2006. These figures reflect that Israel’s external assets are greater than its external liabilities as opposed to previous years, where liabilities were greater than assets. This gives further indication that there is no significant risk of a balance-of-payments crisis.

Economic Trends in IsraelEconomic Trends in Israel

General dataGeneral dataProduct and employmentProduct and employmentBalance of payments and external stabilityBalance of payments and external stabilityFiscal policyFiscal policyMonetary policy and inflation rateMonetary policy and inflation rate

Fiscal PolicyFiscal Policy1. Public expenditure

2. Public expenditure – international comparison

3. The public sector burden

4. Budget deficit

5. Public debt

6. Public debt – international comparison

7. Tax burden

8. Tax reform

General Government Expenditure(as percent of GDP)

Government expenditure as percent of GDP increased in 2001 and 2002 due to the recession (which reduced GDP) and the need to increase the defense budget despite cutbacks in other public expenditure. Government expenditure as a percent of GDP declined in 2003. The reasons for the decrease include cuts in the government budget, a decline in real wages in the government sector, and a halt to the rapid increase in the public sector employment. A further decline occurred in 2004, as a result of a decrease of about 2 percent in public consumption in real terms, coupled with a real increase in GDP. In 2005 and 2006, due to the economic recovery, governmental expenditure as a percent of GDP declined and is estimated at 46.4% in 2006, despite a real growth in public consumption.

52.3% 52.1%51.4% 50.7%

50.0%48.4%

51.1%52.2%

51.5%

49.2%

47.4%46.6%

41.8%41.5%

43.5%44.1%

43.4%

40.8%42.0%42.6%

43.4%44.3%44.1%

40.1%

35%

40%

45%

50%

55%

60%

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 est. OECDweightedavg. 2005

Total Excl. interest, defense imports, and capital transfers abroad

Fiscal PolicyFiscal Policy1. Public expenditure

2. Public expenditure – international comparison

3. The public sector burden

4. Budget deficit

5. Public debt

6. Public debt – international comparison

7. Tax burden

8. Tax reform

General Government Expenditure, 2005General Government Expenditure, 2005 percent of GDPpercent of GDP

41.6

47.4

39.2 39.436.1

34.1

0

5

10

15

20

25

30

35

40

45

50

OECD* Israel OECD* Israel OECD* Israel *Average of 23 countries, weighted by population size.

*For the OECD countries, data on defense consumption and interest payments are for the most recent available year.

Total Net of Defense and Interest payments

Public expenditure relative to GPD is high in Israel by international standards, and reflects a high level of defense spending and interest payments on the public debt.

Net of Defense

General Government ExpenditureGeneral Government Expenditurepercent of GDP, 2005percent of GDP, 2005

Although public spending as a ratio of GDP fell from 2004 to 2005, it is still high by international standards.

*Average of 23 countries, weighted by population.

5754

49 48 48 48 48 4745

4239 38 37 37 36 36

49.443

55

41.7

51 49

4141

51

20

25

30

35

40

45

50

55

60

Fiscal PolicyFiscal Policy1. Public expenditure

2. Public expenditure – international comparison

3. The public sector burden

4. Budget deficit

5. Public debt

6. Public debt – international comparison

7. Tax burden

8. Tax reform

Average Growth Rate of OECD Economies (percent per year)During 1998-2007, based on the World Economic Outlook of the IMF, April 2006

2.5 2.6

3.3

0

5

The ten OECD countrieswith the higher public

expenditure

The ten OECD countrieswith the medium public

expenditure

The ten OECD countrieswith the lower public

expenditureMost empirical studies point to a negative correlation between the level of government expenditure and the rate of economic growth. This negative relationship reflects the effect of an increase in government expenditure on the interest rate and, accordingly, the downward effect on investments, the creation of pressure in the labor market that pushes wages up and reduces corporate profits, and the increase in the tax burden, which is adverse to growth. Furthermore, companies in the public sector sometimes operate less efficiently than those in the private sector.

Fiscal PolicyFiscal Policy1. Public expenditure

2. Public expenditure – international comparison

3. The public sector burden

4. Budget deficit

5. Public debt

6. Public debt – international comparison

7. Tax burden

8. Tax reform

Budget DeficitBudget Deficit(as percent of GDP)(as percent of GDP)

The large deficit in 2003 reflected the effects of the recession on economic activity, which was accompanied by a large decrease in government spending. The reduction in government expenditure in 2004 and a moderate increase in spending during 2005 and 2006 concurrent with a higher rate of growth contributed to a reduction in the rate of the fiscal deficit. The deficit in 2006 is estimated at 0.9% of GDP.

3.1% 3.2%

5.4%

4.2%

0.7%

3.6%

1.9%

2.9%

0.9%

3.7%4.0%

3.2%

4.2%

0.00%1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

est.2007

BudgetProposa

l

Fiscal PolicyFiscal Policy1. Public expenditure

2. Public expenditure – international comparison

3. The public sector burden

4. Budget deficit

5. Public debt

6. Public debt – international comparison

7. Tax burden

8. Tax reform

Gross Public Debtas percent of GDP, 1986-2006

The public debt is a result of budget deficits in the past. After the mid-1980s, when the Economic Stabilization Program was applied, the public debt as a percent of GDP declined steadily and came to 87 percent of GDP in 2000. In 2001–2003, due to the deceleration in the economy and the decline in revenue taxes on one hand, and the difficulty to decrease government expenditure on the other hand, the gross public debt rose to 102 percent of GDP in 2003. As a result of the economy recovery and the withstanding of the deficit target, the gross public debt decreased to 96.9 percent of GDP in 2005 and is estimated to reach 88 percent of GDP in 2006.

159.8

141.6146.2 148.1

138.8

123.4119.0 118.3

110.5104.5

101.6 100.0102.3

86.791.9

99.6 102.0 100.796.9

88.0

100.7

50

70

90

110

130

150

170

1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006est.

Fiscal PolicyFiscal Policy1. Public expenditure

2. Public expenditure – international comparison

3. The public sector burden

4. Budget deficit

5. Public debt

6. Public debt – international comparison

7. Tax burden

8. Tax reform

Gross Public Debtpercent of GDP, 2005

159

125

81 77 7769 69 68 64 62

53 52 50 49 47

30 2615

108

64

99

70

9788

0

20

40

60

80

100

120

140

160

180

JAPAN

ITALY

GREECE

BELGIUM

ISRAEL

ISRAEL 20

06

OECD*

FRANCE

PORTUGAL

GERMANY

CANADA

AUSTRIA

OECD avera

geUSA

NETHERLANDS

SWEDEN

FINLAND

NORWAY

DENMARK

SPAIN UK

IRELAND

NEW Z

EALAND

AUSTRALIA

8

Israel’s public debt (as percent of GDP) is larger than that in most OECD countries. The decrease in the debt will reduce the government’s interest payments and will make it possible to direct resources to social issues, to increase economic stability and to adopt an anti-cyclical policy.

*Average of 23 countries, weighted by population.

Fiscal PolicyFiscal Policy1. Public expenditure

2. Public expenditure – international comparison

3. The public sector burden

4. Budget deficit

5. Public debt

6. Public debt – international comparison

7. Tax burden

8. Tax reform

The Gross Tax Burdenas percent of GDP

The tax burden declined in 2003, mainly due to a steep decrease in collection of income tax that reflected the effects of the recession (especially the wage decrease) and, to a lesser extent, the effects of the direct-tax reform. Indirect-tax collection also slipped, mostly due to a steep decline in imports of consumption goods in the first half of the year and a price level that was much lower than a level that would be consistent with the inflation targets. In contrast, the stability in the tax burden in 2004 and 2005, relative to 2003, is a reflection of the effects of the tax reform on one hand, and the recovery of tax collection caused by the economic growth on the other hand.

Includes direct, indirect, and capital taxes, social security and health fees;

data before 1995 include an adjustment of 1 percent of GDP to account for a change in definitions.

38.7%

38.2%37.9%

38.2%

38.6%

39.1%

38.1%

36.8%

37.8%

36.8%37.0%

38.1%38.2%

37.5%

36.6%36.7%36.8%

36%

38%

40%

1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

36.7 36.3

30.4

Israel OECD economies - simpleaverage

OECD economies - weightedaverage (by population)

Tax burden as percent of GDP - international comparison2004

Israel’s tax burden resembles the average tax burden (simple arithmetic mean) in the twentieth wealthiest countries—the United States, Canada, Japan, and seventeen Western European countries that have relatively high tax burdens. The tax burden in the total class of OECD countries, a more appropriate reference group for Israel in standard-of-living terms than the affluent Western European countries, is 36.3 percent of GDP. The comparison of the average tax burden is more relevant if the OECD countries are weighted by population size. By this standard, the average tax burden in the OECD countries is only 30.4 percent of GDP. Thus, average Israelis shouldered in 2004 a burden that was 6.2 percent of GDP heavier than that endured by average citizens in the OECD countries. This discrepancy, in terms of the size of Israel’s GDP in 2004, means NIS 5,020 per resident or NIS 34.0 billion for the public at large.

The tax burden and the growth rate in The tax burden and the growth rate in OECD economiesOECD economies

Tax Burden In 2004

0

1

2

3

4

5

6

7

10 15 20 25 30 35 40 45 50 55

Gro

wth

Rat

e 19

98-2

007

Most empirical studies point to a negative correlation between the tax burden and the growth rate. A high tax burden slows growth by dampening investment, distorting business decisions, reducing labor supply, weakening incentives for the accumulation of human capital, inducing greater tax evasion, and causing labor and capital to flow to countries that have lower tax rates. In the long run, a high tax burden also correlates with a high level of public expenditure, which also slows the growth rate.

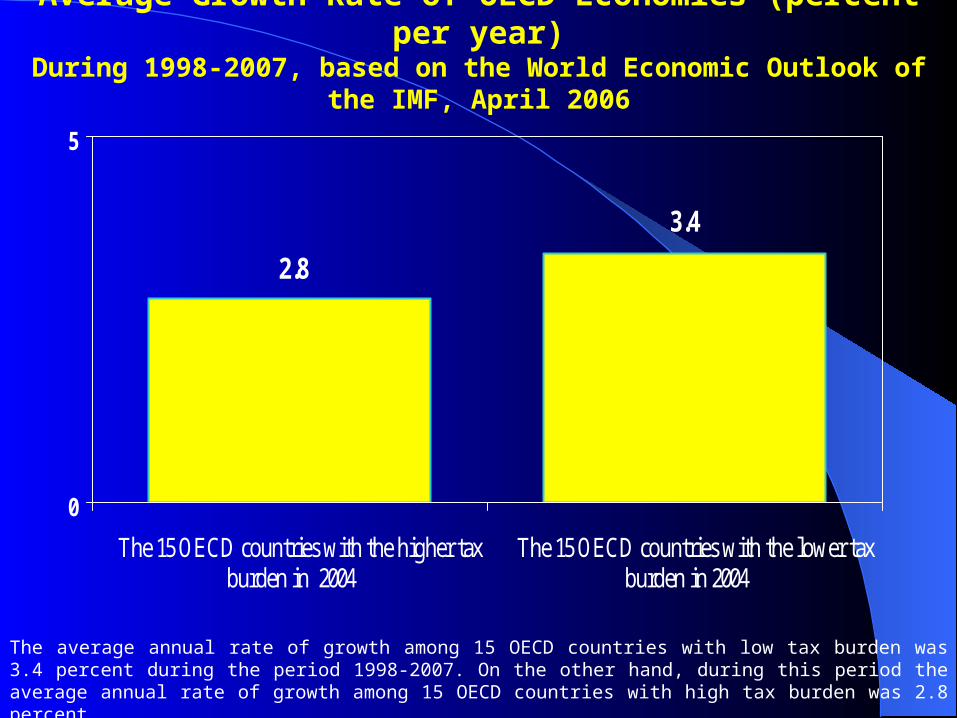

Average Growth Rate of OECD Economies (percent per year)During 1998-2007, based on the World Economic Outlook of the IMF, April 2006

2.8

3.4

0

5

The 15 OECD countries with the higher taxburden in 2004

The 15 OECD countries with the lower taxburden in 2004

The average annual rate of growth among 15 OECD countries with low tax burden was 3.4 percent during the period 1998-2007. On the other hand, during this period the average annual rate of growth among 15 OECD countries with high tax burden was 2.8 percent.

Fiscal PolicyFiscal Policy1. Public expenditure

2. Public expenditure – international comparison

3. The public sector burden

4. Budget deficit

5. Public debt

6. Public debt – international comparison

7. Tax burden

8. Tax reform

0%

10%

20%

30%

40%

50%

60%

70%

Monthly income, NIS, constant 2007 prices

2010

20072002

Marginal tax rate on labor income, before and after Marginal tax rate on labor income, before and after the tax reformthe tax reform

((including income tax, employee's social security tax, and health taxincluding income tax, employee's social security tax, and health tax))

Due to the tax reform, the marginal tax rate on labor income (including income tax, National Insurance contributions by employees, and health tax) declined gradually from 2003. The March 2003 economic plan moved up the phases of the planned reform while a second plan in July 2005 expanded and deepened the reform. The reform will come to an end in 2010, when the marginal tax rate on employee’s income be 44 percent.

Economic Trends in IsraelEconomic Trends in Israel

General dataGeneral dataProduct and employmentProduct and employmentBalance of payments and external stabilityBalance of payments and external stabilityFiscal policyFiscal policyMonetary policy and inflation rateMonetary policy and inflation rate

Monetary Policy and Inflation RateMonetary Policy and Inflation Rate

1. Inflation process2. Inflation targets3. BOI real interest rate4. Real effective exchange rate

Monetary Policy and Inflation RateMonetary Policy and Inflation Rate

1. Inflation process2. Inflation targets3. BOI real interest rate4. Real effective exchange rate

Annual inflation, 1986-2006Annual inflation, 1986-2006(end-of-period)(end-of-period)

Inflation since 1999 has been close to zero. The inflation rate in 2002 reflected a non-recurrent increase in prices due to currency depreciation after several years of high interest rates that had delayed the exchange-rate adjustment. During 2003, the Consumer Price Index declined by 1.9 percent, missing the inflation target of 1–3 percent by a large margin. The consumer price index rose by 2.4% in 2005 and fell by 0.1% in 2006. The fall in the CPI index resulted mainly from the strengthening of the shekel and the decrease in fuel prices during the second half of 2006, as well as from the contractionary policy which the Bank of Israel adopted during the period of the war in the north due to concern over the adverse impact on stability.

17.6%

14.5%

1.3%0.0%

1.4% 1.2%2.4%

-0.1%

20.7%

-1.9%

6.5%

9.4%

16.4%16.1%

8.1%7.0%

8.6%

10.6%11.2%

18.0%

19.7%

-5%

0%

5%

10%

15%

20%

25%

1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Monetary Policy and Inflation RateMonetary Policy and Inflation Rate

1. Inflation process2. Inflation targets3. BOI real interest rate4. Real effective exchange rate

12–month Rate of Change in the CPI and Annual Inflation Targets

The year 2006 ended with a negative inflation rate of 0.1%, which constitutes downward deviation from the inflation target, mainly due to the strengthening of the NIS and the decrease in fuel prices.

-0.1%

-4%

0%

4%

8%

12%

Dec. 1

996

Dec. 1

997

Dec. 1

998

Dec. 1

999

Dec. 2

000

Dec. 2

001

Dec. 2

002

Dec. 2

003

Dec. 2

004

Dec. 2

005

Dec. 2

006

Monetary Policy and Inflation RateMonetary Policy and Inflation Rate

1. Inflation process2. Inflation targets3. BOI real interest rate4. Real effective exchange rate

Short-Term Real Interest Rate,Short-Term Real Interest Rate,Derived from the Bank of Israel’s key lending rateDerived from the Bank of Israel’s key lending rate

2.8%

1.7% 1.5%

2.7%3.2%

3.5%

4.2%3.9%

1.5%

7.3%

7.8%

6.3%

1.0%

2.1%

7.0%

6.0%

4.8%5.0%

2.7%

4.1%

4.6%

5.3%

7.2%

6.5%6.5%

7.6%

2.3%2.2%

0%

2%

4%

6%

8%

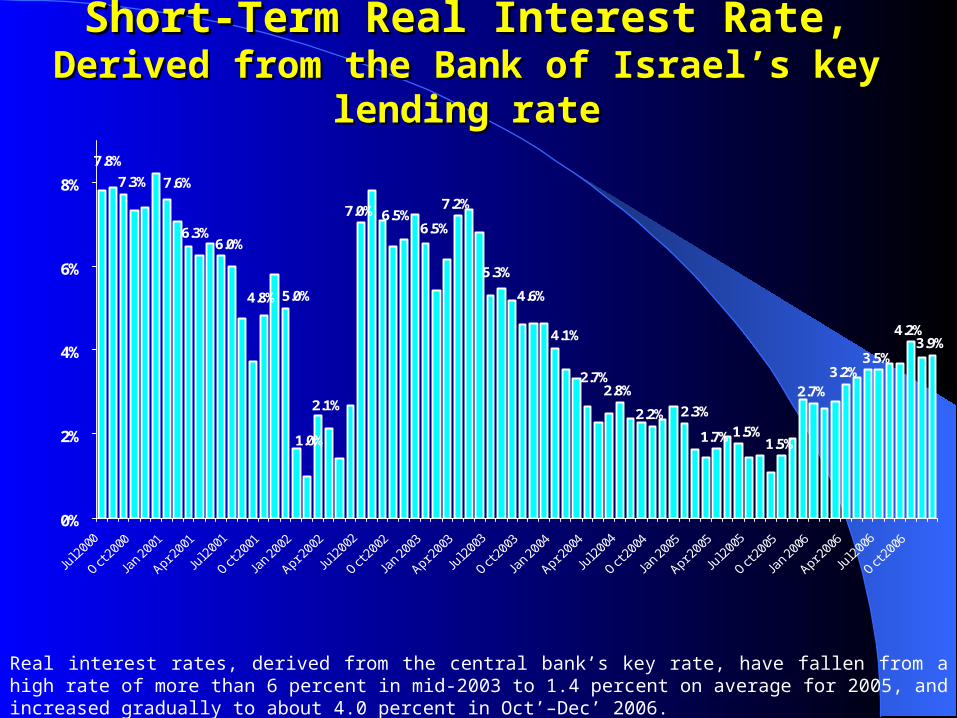

Real interest rates, derived from the central bank’s key rate, have fallen from a high rate of more than 6 percent in mid-2003 to 1.4 percent on average for 2005, and increased gradually to about 4.0 percent in Oct’–Dec’ 2006.

Monetary Policy and Inflation RateMonetary Policy and Inflation Rate

1. Inflation process2. Inflation targets3. BOI real interest rate4. Real effective exchange rate

Real Effective Exchange RateReal Effective Exchange Rate(index, Jan. 1990 = 100)(index, Jan. 1990 = 100)

Basket: US 50%, Euro 25%, UK 5%, Japan 5%, others 15% Basket: US 50%, Euro 25%, UK 5%, Japan 5%, others 15% increase means real appreciation, decrease means real depreciationincrease means real appreciation, decrease means real depreciation

The real depreciation during 2002-2004 reflected an adjustment of the exchange rate due to real shocks that struck the economy from October 2000. The adjustment was delayed because the Bank of Israel kept real interest rates high in 1999–2001. The adjustment became possible only after a steep interest rate cut in late 2001 that led to steep depreciation in the first half of 2002. Real depreciation continued in 2003–2004, as Israel had lower inflation rates than the other advanced countries. The real depreciation helped to make export industries more competitive and supported the economic-recovery process. During 2005 and the first half of 2006, there was almost no change in real effective exchange rate. However during 2006, the real effective exchange rate appreciated by about 5.0%.

96.998.3

100.6

104.5

107.7

104.1

98.9

102.8101.1

91.7

88.4

84.082.2 82.7 83.1

84.4 84.3

81.681.280.5 81.580.6

79.8

82.3

98.999.4

101.2

75

85

95

105

115