Economic Trends and Florida’s Competitive Position of Life and Quality Places Monthly Foreclosures...

36

Economic Trends and Florida’s Competitive Position presented by John Kaliski Cambridge Systematics, Inc. presented to Florida Department of Economic Opportunity Strategic Plan Regional Stakeholder Forum March 5, 2012

Transcript of Economic Trends and Florida’s Competitive Position of Life and Quality Places Monthly Foreclosures...

Economic Trends and Florida’s Competitive Position

presented by

John KaliskiCambridge Systematics, Inc.

presented to

Florida Department of Economic OpportunityStrategic Plan Regional Stakeholder Forum

March 5, 2012

Presentation Outline

• Current realities

• Future trends

• How do we compete?

• Where do we stand?

2

Source: Florida Trend.

Treasure Coast Region

• Indian River

• Martin

• Palm Beach

• St. Lucie

3

Recession Erased Job Gainsof the Past Decade

Employment, Index 2000 = 1.0

1.10

1.15

1.20

0.95

1.00

1.05

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

U.S. Florida

Source: U.S. Bureau of Labor Statistics, “Current Employment Statistics.”

4

Unemployment Rate Easing Downward

8.0

10.0

12.0

14.0

Unemployment Rate (in Percent)

Source: U.S. Bureau of Labor Statistics, “Local Area Unemployment Statistics.”

5

0.0

2.0

4.0

6.0

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

US FLORIDAU.S. FLORIDA

Employment Growth in Treasure Coast

Year-Over-Year Percent Change

2%

4%

6%

8%

6

Source: U.S. Bureau of Labor Statistics, “Current Employment Statistics.”

-8%

-6%

-4%

-2%

0%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Treasure Coast Florida United States

Per Capita Income Much Higher than U.S. but Eroding

Per Capita Income (in Thousands of $2010)

$50

$55

$60

7

Source: U.S. Bureau of Economic Analysis.

$35

$40

$45

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Treasure Coast Florida United States

Net Domestic Migration Has Resumed

50

100

150

200

Source: U.S. Census Bureau, American Community Survey (for the 2005-2010 data) and Population Estimates Program (for the 2011 data).

-100

-50

0

2005 2006 2007 2008 2009 2010 2011

8

A New EconomyGlobal Markets

2010

9

2010

Source: Goldman Sachs, 2008.

A New EconomyGlobal Markets

20102020203020402050

10

2010

Source: Goldman Sachs, 2008.

A New EconomyGlobal Activity Centers

Global Population Centers

11

Global Population Centers

Global Economic CentersSource: WhosYourCity.com.

A New EconomyCompeting as Regions… and Megaregions

12

Source: America 2050.

12

A New Economy7 County Area Ranks 11th Among U.S. Regions

Region 2010 GMP $B

New York City NY/NJ/CT 1,460

Los Angeles 881

Washington DC/Baltimore 575

San Francisco Bay Area 545

Chicago IL/IN/WI 539

13

Chicago IL/IN/WI 539

Boston MA/NH/RI 430

Houston 384

Dallas/Fort Worth 378

Philadelphia PA/NJ 367

Atlanta 279

SOUTHEAST FLORIDA (7 counties) 275

Seattle/Tacoma 254

Tampa Bay/Central Florida 235

How Do We Compete?Florida then… Florida Now…

• Talent

• Innovation

• Infrastructure

• Low costs

• Climate

• Land and natural

14 14

• Infrastructure

• Business climate

• Civic and governance systems

• Quality of life and quality places

• Land and natural resources

Talent Supply and EducationEducational Attainment Key Driver of Jobs and Income

11.5%

6.5%

$30,092

$46,632

Bachelor’s Degree or Higher

Unemployment Rate Median Earnings2010

20.5%

14.5%

$16,904

$23,936

Less than High School Graduate

High School Diploma Only

Associate’s Degree or Some College

Source: U.S. Census Bureau, American Community Survey.

15

Talent Supply and EducationCan We Provide the Workforce for the Future?

10…10… 6…6… 3…3… 2…2…

16

…students in a 9th grade class

2002

Source: Florida Board of Education 2011.

…graduate from high school

2005

…continue to college within two years

2007

…earn college credit within two years

2009

Talent Supply and EducationEducational Attainment 2006-2010

14%14%

Population over 25...

57%57% 29%29%

Treasure Coast

…with less than a High School degree …with a Bachelor’s Degree, or higher…with HS, Associate’s Degree, or some college

17

Source: U.S. Census Bureau, American Community Survey 2006-2010 five-year estimates.

15%15% 59%59% 26%26%

15%15% 57%57% 28%28%

Florida

United States

19%19% 54%54% 28%28%

South Florida

Emerging

Technologies

Innovation and Economic Development Changing Industry Composition

ConstructionAgriculture

Manufacturing

Global Trade

& Logistics

18

ConstructionAgriculture

Tourism

Past

Future?

Agriculture

TourismHealth Care

Construction

Finance &

Professional

Services

Innovation and Economic DevelopmentCan We Strengthen Our Innovation Pipeline?

2% of total U.S. R&D spending (2007)Discoveries

Start-Ups

Licenses

Patents

19

1% of total U.S. venture capital deals (2010)

2% of total U.S. university licensing activity (2008)

Success

3% of total U.S. patents issued (2010)

Innovation and Economic Development Florida’s Innovation Hubs

20

Source: InfoUSA; Florida Division of Colleges and Universities; Foundationffor Independent Higher Education.

Innovation and Economic DevelopmentCan We Expand Our Global Role?

$60

$70

$80

$90

$100 Florida Share of Total U.S. Export Value

3.4%

4.4%

$65 B

$94 B

21

Source: U.S. Census Bureau, Foreign Trade Division.

$-

$10

$20

$30

$40

$50

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2015

Florida Origin Export Value

$27 B

2011

Infrastructure and Growth LeadershipAre We Globally Connected?

22

19601960 20092009

Opportunity: Community of ChoiceInfrastructure and Growth LeadershipCan We Meet the Needs of a Growing Region?

23

Infrastructure and Growth LeadershipCan We Provide for Future Demand?

24

Source: Florida Department of Transportation.

Infrastructure and Growth LeadershipCan We Provide for Future Demand?

25

Source: Florida Department of Transportation.

Business Climate and CompetitivenessIs Florida Competitive?

Fourth ranked in net new business relocations, 2010

26

Source: Dun & Bradstreet.

Business Climate and CompetitivenessNo Longer a Low-Cost State

41st • Highest cost of doing business (CNBC, 2011)11th

• Growth in average health insurance

27

97%

6.3%• Effective business tax rate as percent

of GDP in 2010, up from 4.9% in 2007 (Council on State Taxation)

• Growth in average health insurance premium per enrolled employee, 2000-2010(Kaiser Family Foundation)

Civic and Governance SystemsAre We Able to Invest in the Future?

41st• Lowest per capita state and local

government employment per capita (U.S. Census, 2010)

5th

• Tax supported debt as percentage of

28

8%

53%• Increase in number of nonprofit

organizations, 2000-2010 (National Center for Charitable Statistics)

• Tax supported debt as percentage of revenues in 2009, up from 5% in 2006 (Florida Division of Bond Finance)

Civic and Governance SystemsCan the Public Sector Match the Scale of Business?

• 411 Municipalities• 67 Counties• ~ 112 Economic development organizations • ~ 52 Convention and visitors bureaus• 28 Fixed route transit systems• 28 Fixed route transit systems• 26 Metropolitan planning organizations• 24 Regional workforce boards• 11 Regional planning councils• 8 Economic regions• 5 Water management districts• 781 Community development special districts

29

Quality of Life and Quality PlacesIs Florida a Destination?

30

Third ranked in net domestic migration, 2010Source: U.S. Census Bureau, American Community Survey.

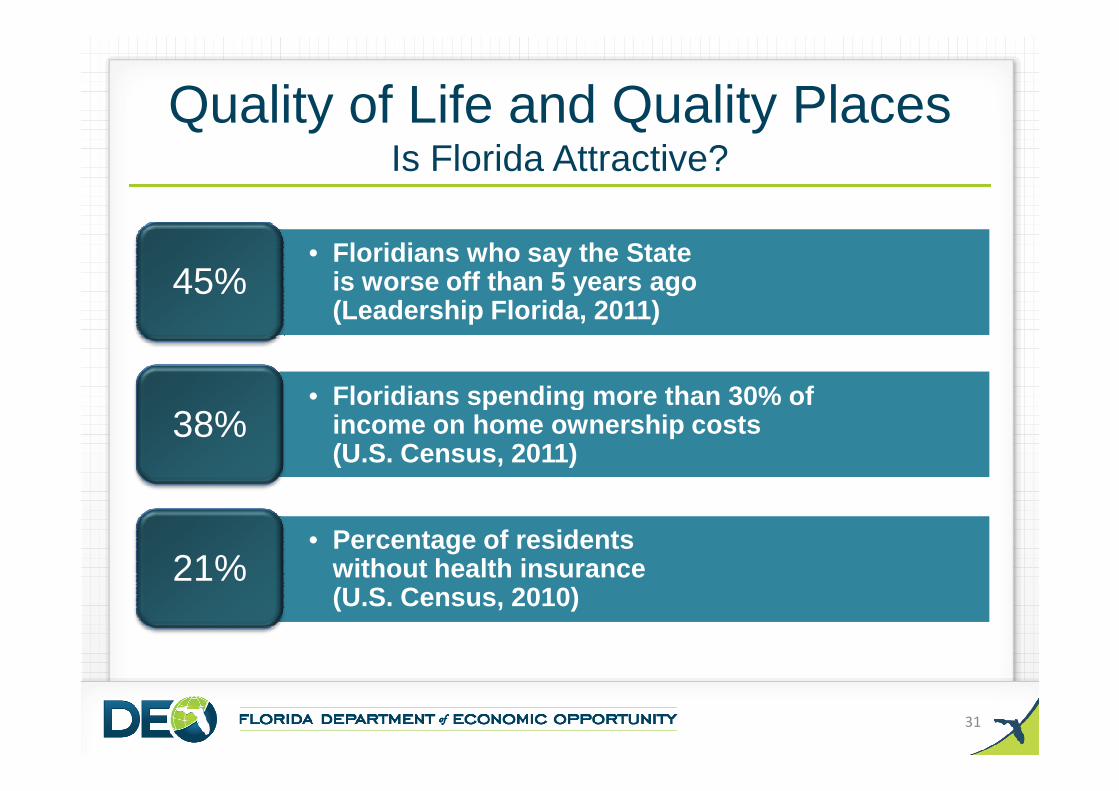

Quality of Life and Quality PlacesIs Florida Attractive?

41st• Floridians who say the State

is worse off than 5 years ago (Leadership Florida, 2011)

45%

• Floridians spending more than 30% of

31

38%

21%• Percentage of residents

without health insurance (U.S. Census, 2010)

• Floridians spending more than 30% of income on home ownership costs (U.S. Census, 2011)

Quality of Life and Quality Places Monthly Foreclosures in Treasure Coast, 2006-2011

40,000

50,000

60,000

70,000

80,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

Source: Florida Dept of Economic Opportunity, compiled from RealtyTrac, Inc. Total housing units receiving a filing notice, per month.

32

0

10,000

20,000

30,000

0

1,000

2,000

3,000

4,000

5,000

TREASURE COAST Florida - Right Scale

Quality of Life and Quality PlacesPoverty Rate Is Rising in Treasure Coast

13%

14%

15%

16%

17%

33

Source: U.S. Census Bureau Small Area Income and Poverty Estimates (SAIPE).

9%

10%

11%

12%

13%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Treasure Coast Florida United States

Quality of Life and Quality PlacesCan We Preserve What Makes Florida Special?

34

How Do We Get Started?

• Adopt common framework

• Create 5 year action plans – 2 integrated Comprehensive

Economic Development StrategiesEconomic Development Strategies– DEO Strategic Plan

• Move toward a 50-year vision– Regional Vision and Blueprint

for Economic Prosperity– Statewide vision

35

Questions?

Barbara FosterFlorida Department of Economic Opportunity

850-717-8966 | [email protected]

36

John KaliskiCambridge Systematics, Inc.

617-354-0167 | [email protected]

![¿Cuáles son los contaminantes de interés?10 July] Keynote...4! 110,000 100,000 90,000 80,000 70,000 60,000 50,000 40,000 30,000 20,000 10,000 0 Early deaths Best Practice China](https://static.fdocuments.us/doc/165x107/5e8c093603a7df31093d85fc/cules-son-los-contaminantes-de-inters-10-july-keynote-4-110000-100000.jpg)

![Welcome [] · 2019-06-07 · 8 Sensitivity: Confidential Compliance 8 0 1000 2000 3000 4000 0 10,000 20,000 30,000 40,000 50,000 60,000 70,000 80,000 Number of Ships • 80,000 ships](https://static.fdocuments.us/doc/165x107/5f8995659f796a4b9327f76e/welcome-2019-06-07-8-sensitivity-confidential-compliance-8-0-1000-2000-3000.jpg)