Economic Dynamics and Integration in Eastern … · Economic Dynamics and Integration in Eastern...

38

Economic Dynamics and Integration in Eastern Europe and Asia Lecture Winter semester 2017/18 Chair for Macroeconomic Theory and Politics Schumpeter School of Business and Economics Bergische Universität Wuppertal

Transcript of Economic Dynamics and Integration in Eastern … · Economic Dynamics and Integration in Eastern...

Economic Dynamics and Integration in Eastern Europe and

Asia

LectureWinter semester 2017/18

Chair for Macroeconomic Theory and PoliticsSchumpeter School of Business and Economics

Bergische Universität Wuppertal

Prof. Paul J.J. Welfens

• Office: M-12.08

• Email: [email protected]

• Office hours: Monday 12:00-13:00 (During Semester)

Thursday 11:00-12:00 (During Semester break) at EIIW

• Chair for Macroeconomic Theory and Politics:

https://welfens.wiwi.uni-wuppertal.de/index.php?id=3314&L=0

11. 12. 2017 2

David Hanrahan

• Office: M-12.10

• Email: [email protected]

• Office hours: by appointment

• Chair for Macroeconomic Theory and Politics:

https://welfens.wiwi.uni-wuppertal.de/index.php?id=6194

311. 12. 2017

Tian Xiong

• Office: M-12.11

• Email: [email protected]

• Office hours: Tuesday 14:00-15:00

• Chair for Macroeconomic Theory and Politics:

https://welfens.wiwi.uni-wuppertal.de/index.php?id=6011

11. 12. 2017 4

• Introduction of Asia

•Economic Dynamics of Asia

Content

11. 12. 2017 5

611. 12. 2017 Source: geology.com

Asia

711. 12. 2017 Source: https://en.wikipedia.org/wiki/Asia

Global shares of income, 2015

811. 12. 2017Notes: Weights are based on gross national income in current US dollars, Atlasmethod.

Source: ADB estimates using data from World Development Indicators online database

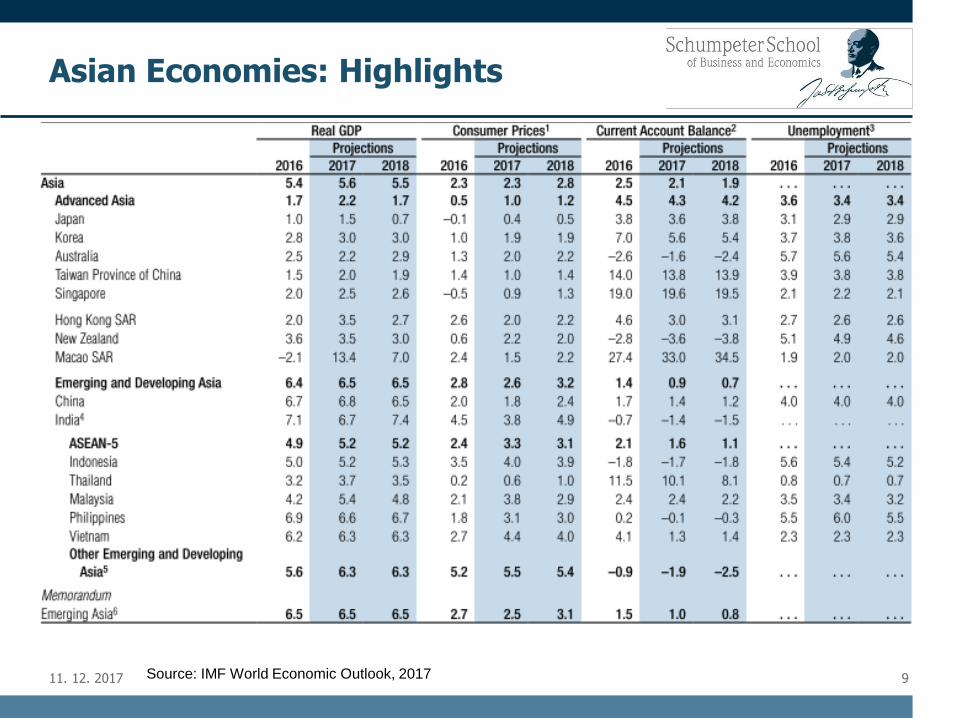

Asian Economies: Highlights

911. 12. 2017 Source: IMF World Economic Outlook, 2017

Real GDP Growth

1011. 12. 2017 Source: IMF World Economic Outlook, 2017

Real GDP Growth

1111. 12. 2017 Source: IMF World Economic Outlook, 2017

Demand-side contributions to growth

1211. 12. 2017 Source: Haver Analytics; CEIC Data Company (accessed 26 August 2017).

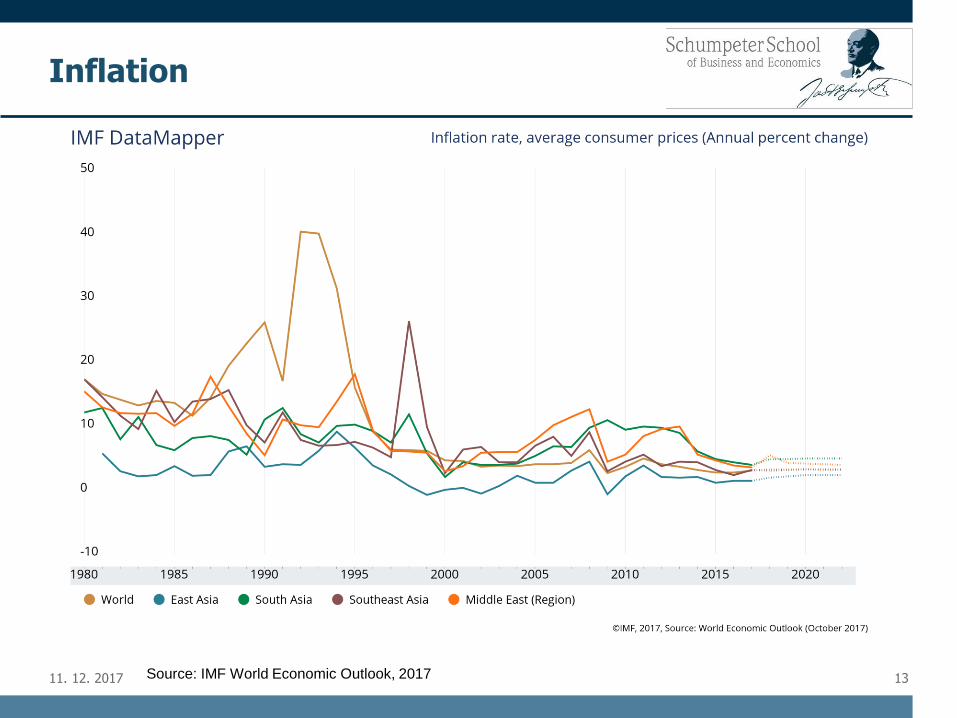

Inflation

1311. 12. 2017 Source: IMF World Economic Outlook, 2017

Unemployment

1411. 12. 2017 Source: IMF World Economic Outlook, 2017

Current Account Balance, Developing Asia

1511. 12. 2017 Source: Asian Development Outlook database.

Foreign Direct InvestmentFDI inflows, global and by group of economies, 2005-2016 (Billions of dollars and percent)

1611. 12. 2017 Source: UNCTAD, FDI/MNE database

Foreign Direct InvestmentFDI inflows, top 20 host economies, 2015-2016 (Billions of dollars)

1711. 12. 2017 Source: UNCTAD, FDI/MNE database

Foreign Direct InvestmentFDI outflows, top 20 home economies, 2015-2016 (Billions of dollars)

1811. 12. 2017 Source: UNCTAD, FDI/MNE database

Foreign Direct Investment

1911. 12. 2017 Source: FDI Markets. The Financial Times; ADB estimates

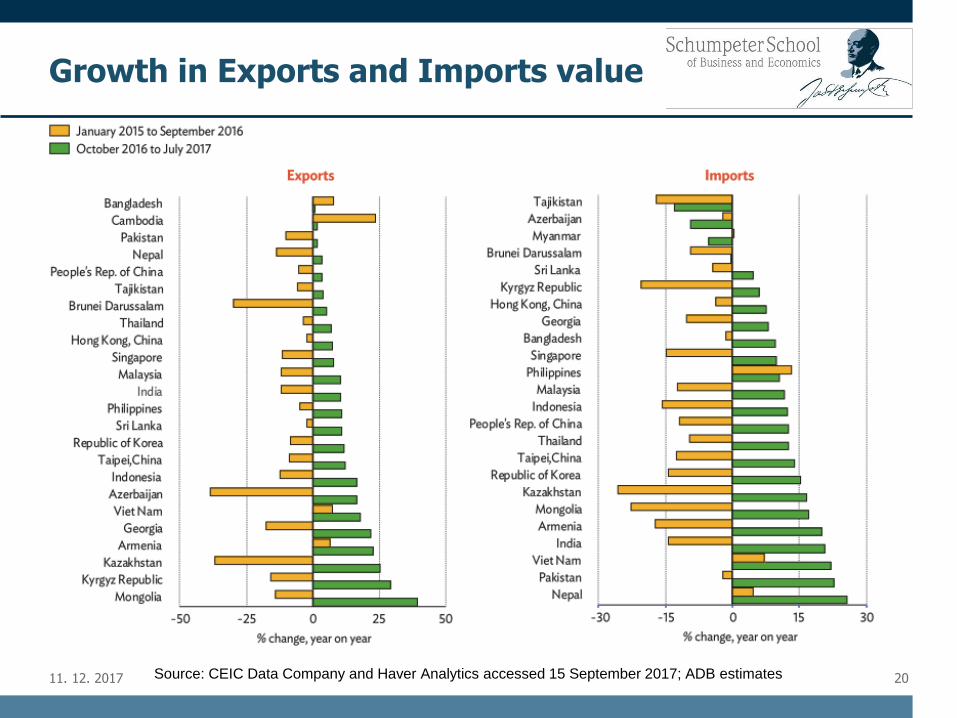

Growth in Exports and Imports value

2011. 12. 2017 Source: CEIC Data Company and Haver Analytics accessed 15 September 2017; ADB estimates

Trade Openness indicator

2111. 12. 2017

Note: Note: Major industrial economies refer to US, euro area, and Japan. Trade openness is defined as the sum of

exports and imports of goods and services in US dollars.

Source: Haver Analytics and Netherlands Bureau for Economic Policy Analysis, accessed 15 September 2017; ADB

estimates

• Japan first adopted export-oriented manufacturing as a growthstrategy in the 1960s.

• Japan itself recorded double-digit real rates of growth from 1960 upuntil the first oil shock of 1973.

• During this period of rapid growth, industrial structure also changed asexports shifted away from labour-intensive to more sophisticatedproducts.

• Japan’s movement into higher technology exports opened the way forthe NIEs to themselves adopt an export-oriented manufacturinggrowth strategy.

• These economies were able to expand production and exports inlabour-intensive industries such as apparel and footwear in the 1960sand then to develop more capital-intensive industries following Japanin the 1970s and 1980s.

International Trade pattern

2211. 12. 2017

• A third wave of trade-led industrial growth then began to take hold asSoutheast Asian economies adopted export-oriented policies in themid-1970s and early 1980s, with rapid growth in exports of labour-intensive manufactures.

• By the mid-1980s, the ASEAN countries started exporting electrical andnonelectrical machinery and other more sophisticated products.

• Finally, the PRC and Viet Nam emerged as fast-growing exporters oflabour-intensive manufactures in the late 1980s and early 1990s.

• International trade provided an environment conducive to rapidindustrial growth and transformation of the predominantly agriculturaleconomies of East and Southeast Asia into modern industrialeconomies in a remarkably short period of time by historical standards.

• The East and Southeast Asian region shows a remarkableconcentration in machinery sectors over 1995–2004.

International Trade pattern

2311. 12. 2017

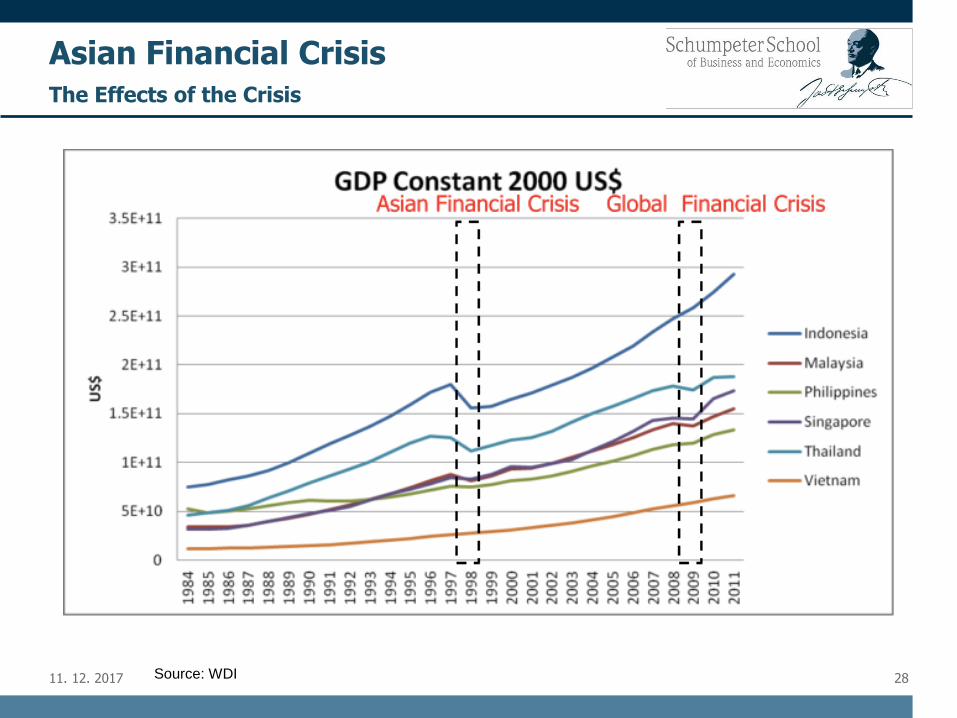

• It was started by the collapse of the Thai baht in July 1997 due to speculative attacks.

• Thailand was forced to let its currency float on 2nd July 1997.

• Months later, the problem spread throughout Southeast Asia including Republic of Korea mainly on equity markets and currencies.

• Indonesia, Korea, Malaysia, Philippines, and Thailand suffered the most severe adverse impacts as a result of the Asian Financial Crisis.

Asian Financial Crisis

2411. 12. 2017

Asian Financial Crisis

2511. 12. 2017 Source: Radelet and Sachs, 1998

A huge, sudden reversal of capital flows

Private net capital

flows to Indonesia,

Korea, Malaysia,

Philippines, and

Thailand increased

from USD 40.5 billion

in 1994 to USD 93

billion in 1996.

In 1997, suddenly

reversed to minus

USD 12.1 billion.

External Financing of Five Asian Countries, 1994-98a

• The crisis forced sharp depreciation of all major Southeast Asian currencies in the short term.

• The collapse of the monetary system and stock markets in Southeast Asia and the heavy losses suffered by investors all forecasted their stop-loss.

• A large number of foreign capital withdrawal and domestic inflation suffered tremendous stress.

• A large number of enterprises in Asian countries went bankrupt, bank failures, stock market collapses, real estate falls, the exchange rate depreciation, the unemployment rate rise, people's lives are seriously affected.

• The economy suffered a serious blow, causing economic recession, social unrest and political instability, and as a result, some countries have plunged into long-term chaos.

Asian Financial CrisisThe Effects of the Crisis

2611. 12. 2017

Asian Financial CrisisThe Effects of the Crisis

2711. 12. 2017 Source: WDI

Asian Financial CrisisThe Effects of the Crisis

2811. 12. 2017 Source: WDI

• Radelet and Sachs (1998):

▪ Macroeconomic policy-induced crisis: A BOP crisis (currencydepreciation; loss of foreign exchange reserves; collapse of apegged exchange rate) arises when domestic credit expansion bythe central bank is inconsistent with the pegged exchange rate.Often, the credit expansion results from the monetisation of budgetdeficits.

▪ Financial panic: A financial panic is a case of multiple equilibria inthe financial markets. A panic is an adverse equilibrium outcome inwhich short-term creditors suddenly withdraw their loans from thesolvent borrower.

Asian Financial CrisisThe Causes of the Crisis

2911. 12. 2017

• Radelet and Sachs (1998):

▪ Bubble collapse: A stochastic financial bubble occurs whenspeculators purchase a financial asset at a price above itsfundamental value in the expectation of a subsequent capital gain.

▪ Moral-Hazard crisis: A moral hazard crisis arises because banksare able to borrow funds on the basis of implicit or explicit publicguarantees of bank liabilities. If banks are undercapitalized orunder-regulated, they may use these funds for overly risky or evencriminal activities.

Asian Financial CrisisThe Causes of the Crisis

3011. 12. 2017

• Lane (1999) - Financial fragility:

▪ Many financial institutions and corporations in the countries affectedhad borrowed in foreign currencies without adequate hedging,making them vulnerable to currency depreciation.

▪ Much of the debt was short-term while assets were longer-term,creating the possibility of a liquidity attack, the effect of whichwould be similar to that of a bank run.

▪ Prices in these countries’ equity and real estate markets had risensubstantially before the crisis, increasing the likelihood of a sharpdeflation in asset prices.

▪ Credit was often poorly allocated, contributing to increasingly visibleproblems at banks and other financial institutions before the crisishit

3111. 12. 2017

Asian Financial CrisisThe Causes of the Crisis

• The East Asian crisis differs from previous crises in several key respects(Rana and Lim, 2000)

• It is a crisis of confidence, a capital-account crisis, not a traditionalcurrent-account crisis.

• Unlike other previous crises of confidence of the 1980s and 1990s, itsroot causes are structural-premature financial liberalization(liberalization of financial markets without adequate supervision andregulation), crony capitalism, and policy mistakes in managing privatecapital flows,

• it is a liquidity risk (currency crises are the outcome of self- fulfillingprophecies and financial panic, and include bank runs, fickle investors,and hot money), not a solvency risk (a currency crisis results fromweak macroeconomic fundamental)

3211. 12. 2017

Asian Financial CrisisThe Causes of the Crisis

•Weisbrot (2007):

1.IMF failed to act as a lender of the last resort, when such a lender wasmost needed.

▪ Financial liberalization which was strongly promoted by the IMFwas the main cause of the crisis.

▪ In South Korea: the removal of a number of restrictions on foreignownership of domestic stocks and bonds, residents' ownership offoreign assets, and overseas borrowing by domestic financial andnon-financial institutions.

▪ Korea's foreign debt nearly tripled from $44 billion in 1993 to $120billion in September 1997. This was not a very large debt burdenfor an economy of Korea's size, but the short-term percentagewas high at 67.9 percent by mid-1997.

3311. 12. 2017

Asian Financial CrisisThe Causes of the Crisis

•Weisbrot (2007):

▪ For comparison, the average ratio of short-term to total debt fornon-OPEC less developed countries at the time of the 1980s debtcrisis (1980-82) was 20 percent.

▪ Thailand created the Bangkok International Banking Facility in1992, which greatly expanded both the number and scope offinancial institutions that could borrow and lend in internationalmarkets.

▪ Indonesian non-financial corporations borrowed directly fromforeign capital markets, pilling up $39.7 billion of debt by mid 1997,87 percent of which was short-term.

3411. 12. 2017

Asian Financial CrisisThe Causes of the Crisis

•Weisbrot (2007):

2.The IMF recommended a series of policies that appear to haveworsened the crisis:

▪ high interest rates and a tightening of domestic credit to sloweconomic growth;

▪ fiscal tightening, including cuts in food and energy subsidies inIndonesia (later rescinded there after rioting broke out);

▪ further liberalization of international capital flows.

▪ the closing of sixteen Indonesian banks, a move that the IMFthought would help restore confidence in the banking system.Instead it led to panic withdrawals by depositors at remainingbanks, further destabilizing the financial system.

3511. 12. 2017

Asian Financial CrisisThe Causes of the Crisis

•Weisbrot (2007):

3. The amounts of funds dispersed were too little and too late to slowthe damage

▪ In Indonesia, only $3 billion had been disbursed by March 1998, ascompared to a $40 billion commitment.

▪ The IMF Letter of Intent (LoI) was signed in January 1998 by theGovernment of Indonesia.

3611. 12. 2017

Asian Financial CrisisThe Causes of the Crisis

Lane, T. (1999). The Asian financial crisis: what have we learned?. Finance and

Development, 36(3), 44.

Radelet, S., & Sachs, J. (1998). The onset of the East Asian financial crisis (No. w6680).

National bureau of economic research.

Rana, P. B., & Lim, J. A. Y. (2000). The East Asian crisis: Macroeconomic policy design and

sequencing issues. Rising to the Challenge in Asia: A Study of Financial Markets, 1.

Sally, R. (2010). Regional economic integration in Asia: the track record and prospects.

ECIPE Occasional paper, 2, 2010.

Weisbrot, M. (2007). Ten years after: the lasting impact of the Asian financial crisis. Center

for Economic and Policy Research, 2.

References

11. 12. 2017 37

Thank You

for

Your Attention!

11. 12. 2017 38