Economic Crises and The Twin Balance Sheet Problem in India · Economic Crises and The Twin Balance...

41

Economic Crises and The Twin Balance Sheet Problem in India Module 6 Contemporary Themes in India’s Economic Development and the Economic Survey Arvind Subramanian Chief Economic Adviser MINISTRY OF FINANCE GOVERNMENT OF INDIA

Transcript of Economic Crises and The Twin Balance Sheet Problem in India · Economic Crises and The Twin Balance...

Economic Crises and The Twin Balance Sheet Problem in India

Module 6

Contemporary Themes in India’s

Economic Development and the Economic Survey

Arvind Subramanian

Chief Economic Adviser

MINISTRY OF FINANCE

GOVERNMENT OF INDIA

Overview

• Financionomic (Financial-Economic) Crises and Indian

Experience

• Effects of the Twin Balance Sheet Crisis.

• Successful and Unsuccessful Central Banking Experiences.

2

Crises, Crises, Crises: A Rough Time-Line

Early 1980's 1991 1994-95 1997-98 1999 2007 2008 2009-10 2013-14 2016

Latin

American

Debt Crisis

BOP

Crisis

India

Tequila

Crisis

Argentina

Mexico

Asian

Financial

Crisis +

Russia

BrazilEast

Europe

Global

Financial

Crisis

Greece,

Ireland,

Spain,

Iceland

Taper Tantrum

Brazil, India,

Indonesia, South

Africa, Turkey

Tremors

in China

Financionomic (Financial-Economic)

Crises and Indian Experience

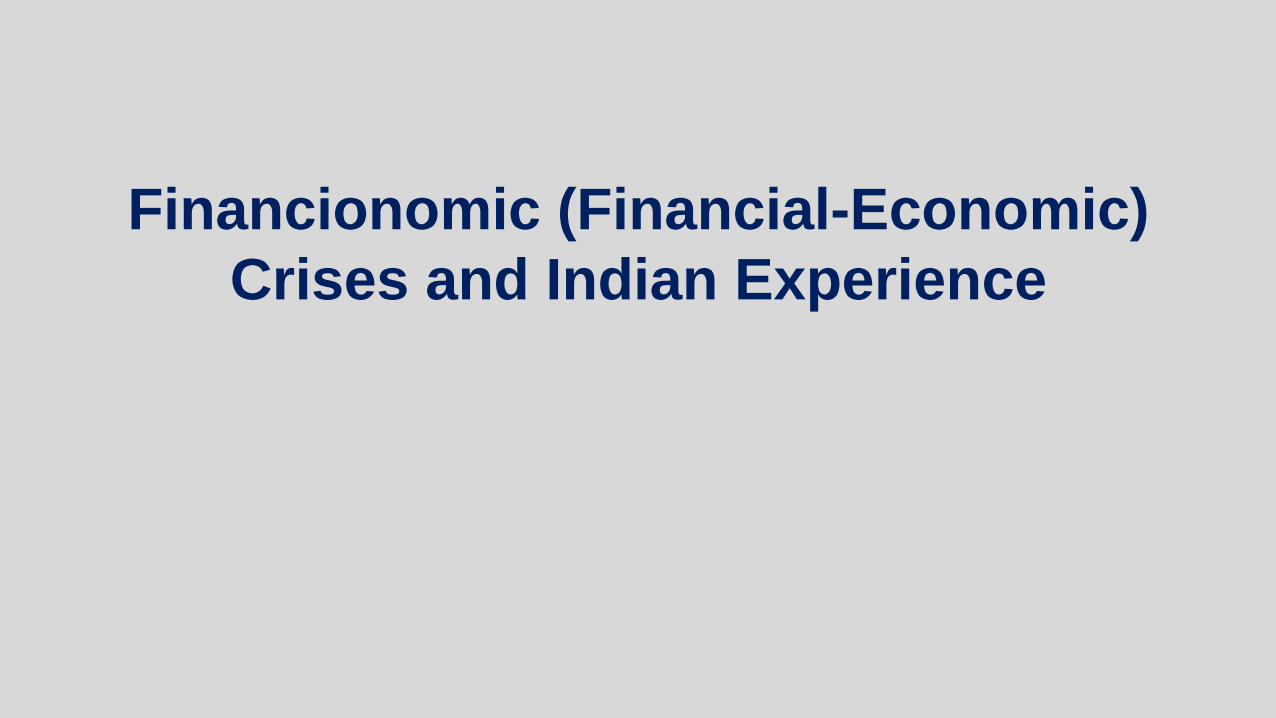

Debt Crises Not Uncommon (Reinhart & Rogoff, 2009)

5

What is a Financionomic Crisis?• Broadly defined as phenomena associated with substantial loss in

value of assets with a sharp negative impact on growth. These

assets can be:

1. Currency (exchange rate)

[Example: Thailand during Asian Financial Crisis late 1990s]

2. Equity

[Example: Argentina ‘Tequila Crisis’, 1994-95, AFC].

3. Real Estate

[Example: Japan late 1980s, USA post-Global Financial Crisis 2008-09].

6

Economic Crises Manifestations

7

Thailand during Asian Financial Crisis Argentina during ‘Tequila’ Crisis

Japan during the Balance Sheet Crisis

1. Bakker, Bas B. & Leslie Lipchitz, 2014, “Conventional and Insidious Macroeconomic Balance-Sheet Crises”, IMF working paper WP/14/160.

2. Dabós, M. and Laura Gómez Mera, 1998, “The Tequila Banking Crisis in Argentina”.

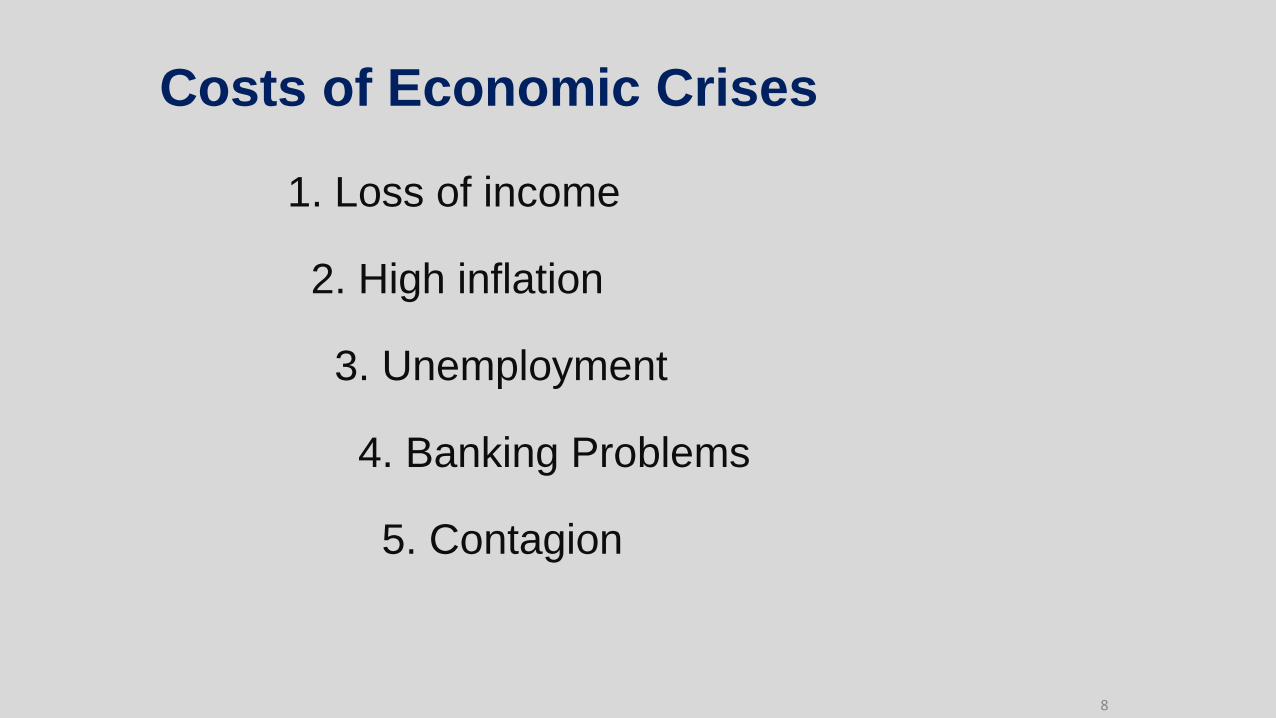

Costs of Economic Crises

1. Loss of income

2. High inflation

3. Unemployment

4. Banking Problems

5. Contagion

8

9

Source: Reuters and the Wall Street Journal

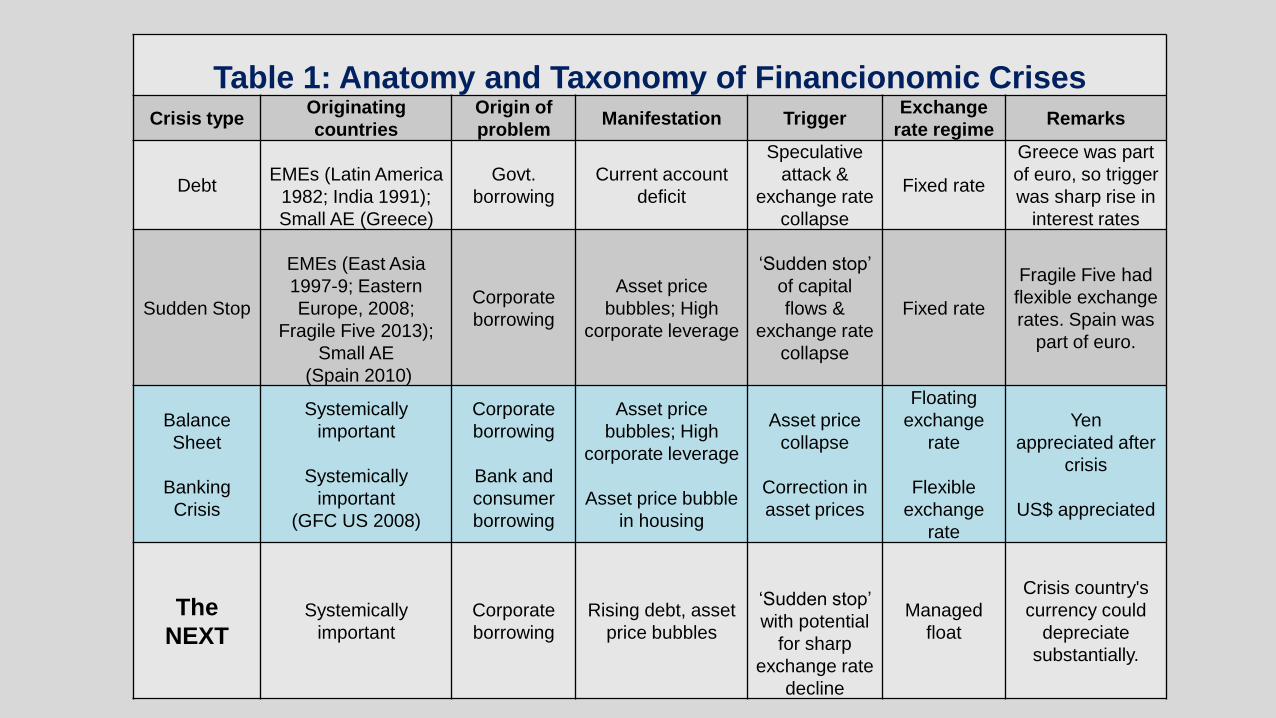

Table 1: Anatomy and Taxonomy of Financionomic CrisesCrisis type

Originating

countries

Origin of

problemManifestation Trigger

Exchange

rate regimeRemarks

DebtEMEs (Latin America

1982; India 1991);

Small AE (Greece)

Govt.

borrowing

Current account

deficit

Speculative

attack &

exchange rate

collapse

Fixed rate

Greece was part

of euro, so trigger

was sharp rise in

interest rates

Sudden Stop

EMEs (East Asia

1997-9; Eastern

Europe, 2008;

Fragile Five 2013);

Small AE

(Spain 2010)

Corporate

borrowing

Asset price

bubbles; High

corporate leverage

‘Sudden stop’

of capital

flows &

exchange rate

collapse

Fixed rate

Fragile Five had

flexible exchange

rates. Spain was

part of euro.

Balance

Sheet

Banking

Crisis

Systemically

important

Systemically

important

(GFC US 2008)

Corporate

borrowing

Bank and

consumer

borrowing

Asset price

bubbles; High

corporate leverage

Asset price bubble

in housing

Asset price

collapse

Correction in

asset prices

Floating

exchange

rate

Flexible

exchange

rate

Yen

appreciated after

crisis

US$ appreciated

The

NEXTSystemically

important

Corporate

borrowing

Rising debt, asset

price bubbles

‘Sudden stop’

with potential

for sharp

exchange rate

decline

Managed

float

Crisis country's

currency could

depreciate

substantially.

6/13/2017 MOOC Module 10: Twin Balance Sheet Problem 11

Historically Periods of High International Capital Mobility Have

Led to Banking Crises (R&R 2009)

12

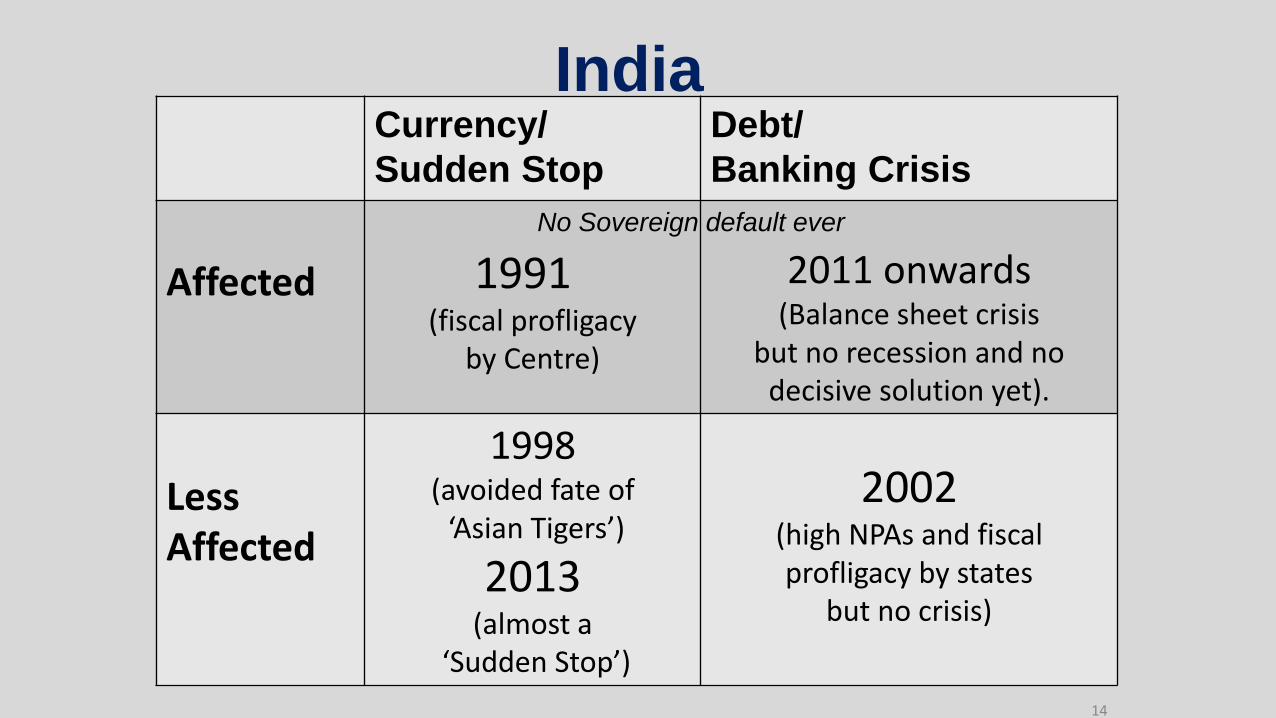

13

IndiaCurrency/

Sudden Stop

Debt/

Banking Crisis

Affected 1991(fiscal profligacy

by Centre)

2011 onwards (Balance sheet crisis

but no recession and no decisive solution yet).

Less Affected

1998(avoided fate of

‘Asian Tigers’)

2013(almost a

‘Sudden Stop’)

2002(high NPAs and fiscal profligacy by states

but no crisis)

14

No Sovereign default ever

The Twin Balance Sheet Problem in India: Banks and

Corporates Stressed

*:Per cent of debt owed by companies with Interest Coverage Ratio <1 based on sample of 3700 listed companies

(Credit Suisse).

15

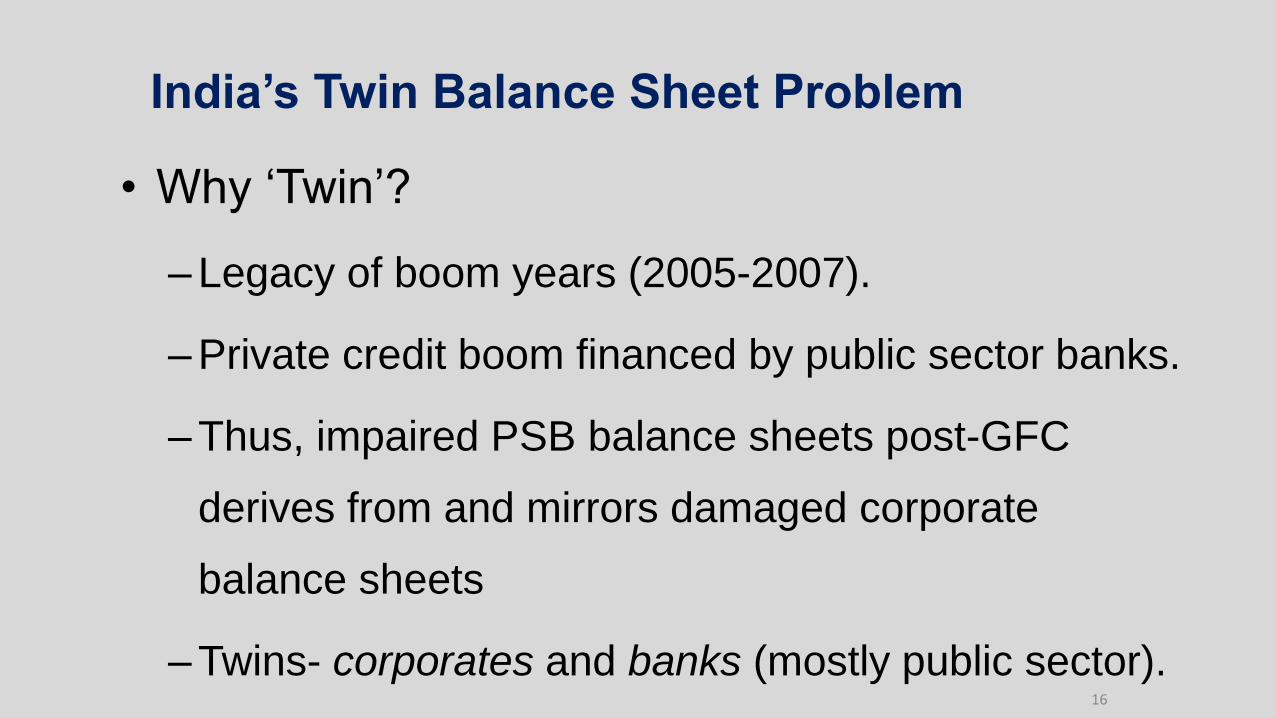

India’s Twin Balance Sheet Problem

• Why ‘Twin’?

– Legacy of boom years (2005-2007).

– Private credit boom financed by public sector banks.

– Thus, impaired PSB balance sheets post-GFC

derives from and mirrors damaged corporate

balance sheets

– Twins- corporates and banks (mostly public sector).16

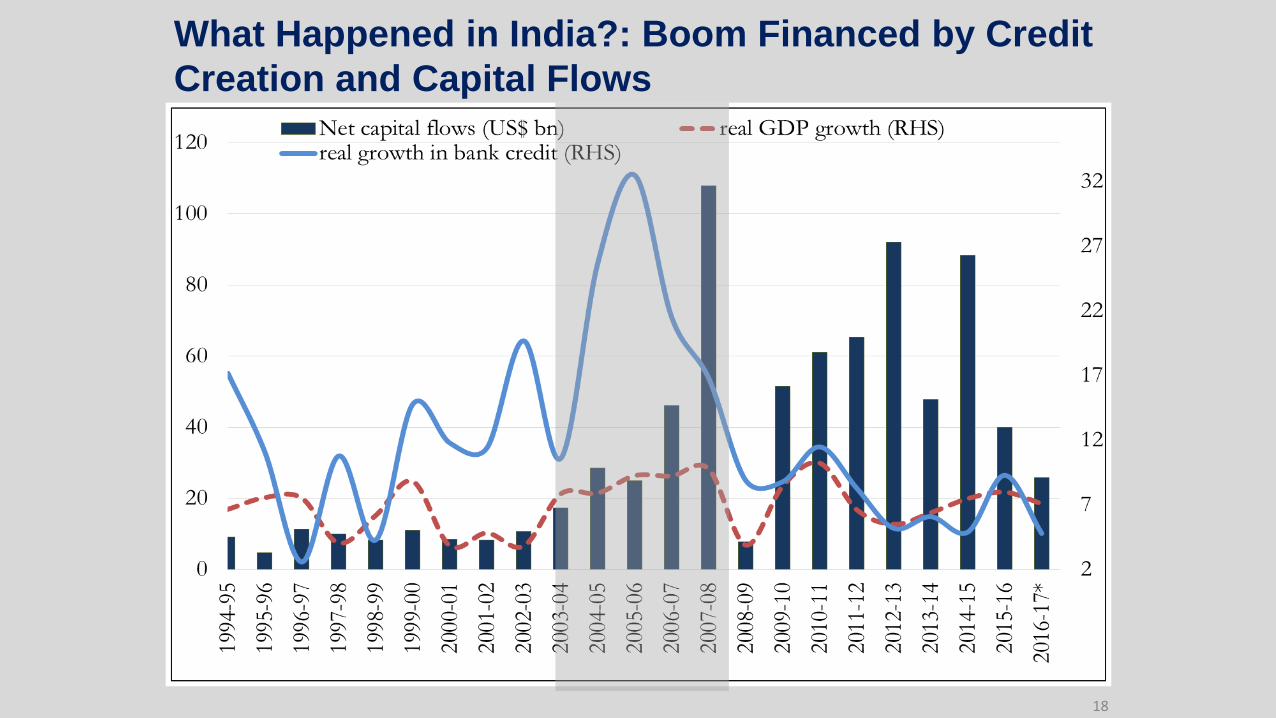

What Happened in India?Boom in Gross Capital Formation (Per cent of GDP)

17

What Happened in India?: Boom Financed by Credit

Creation and Capital Flows

18

19

30

35

40

45

50

55

60

65

70

Mar

-1992

Dec

-1992

Sep

-1993

Jun

-1994

Mar

-1995

Dec

-1995

Sep

-1996

Jun

-1997

Mar

-1998

Dec

-1998

Sep

-1999

Jun

-2000

Mar

-2001

Dec

-2001

Sep

-2002

Jun

-2003

Mar

-2004

Dec

-2004

Sep

-2005

Jun

-2006

Mar

-2007

Dec

-2007

Sep

-2008

Jun

-2009

Mar

-2010

Dec

-2010

Sep

-2011

Jun

-2012

Mar

-2013

Dec

-2013

Sep

-2014

Jun

-2015

Mar

-2016

Dec

-2016

Rupee per US$Market

Determined

Exchange Rate

Sharp Currency Declines Worsened Balance Sheets of Companies with

Foreign Borrowing

In February 2016 as PSB financial results came in

investors fled PSB shares..

0

0.5

1

1.5

2

2.5

3

3.5

4

12-Feb-15 12-Feb-16 12-Feb-15 12-Feb-16

Public Sector Banks HDFC

20

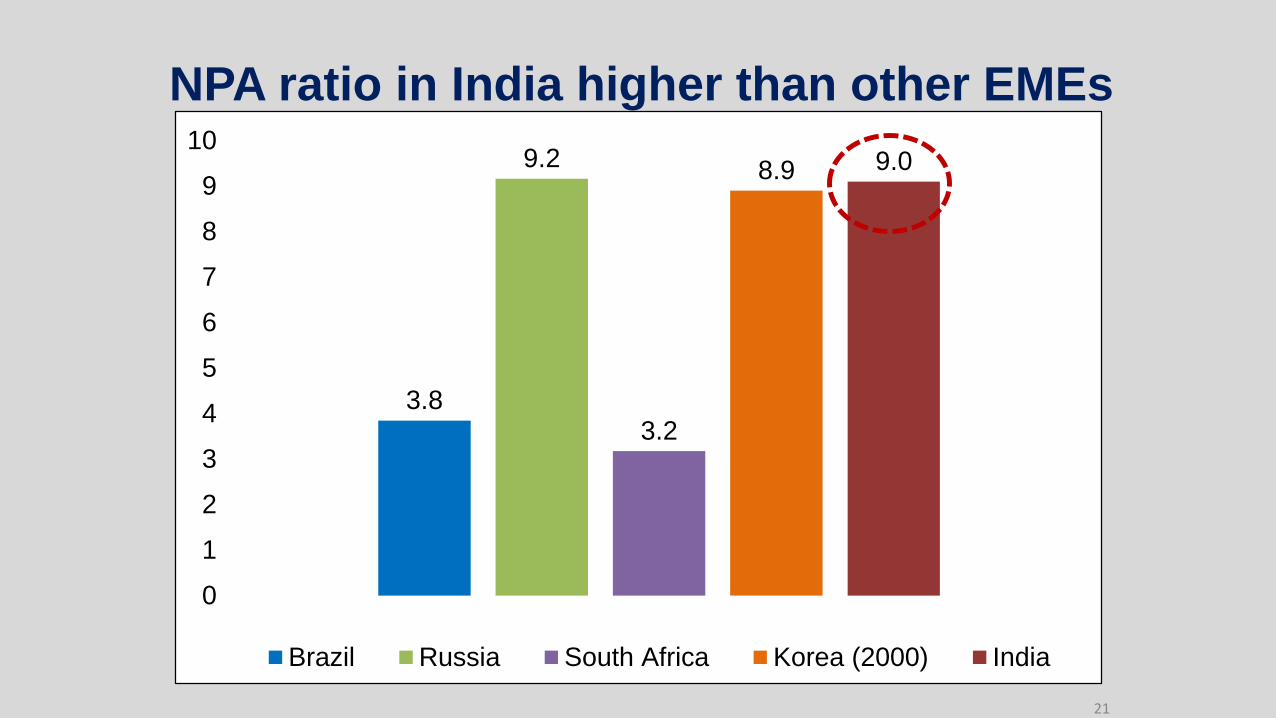

NPA ratio in India higher than other EMEs

3.8

9.2

3.2

8.9 9.0

0

1

2

3

4

5

6

7

8

9

10

Brazil Russia South Africa Korea (2000) India

21

But, not as bad as China’s..

22

Why hasn’t growth suffered in India?

Unique structure of financial system: Public Sector

dominated.

• Increase investment and supply capacity

• No sharp adjustments

• ‘Give time to time’ strategy (that worked in early 2000s)

• Allow companies time to turnaround ( high growth improving

cash flows) by postponing principal payments

• ‘Evergreening’

23

India: Real GDP growth

24

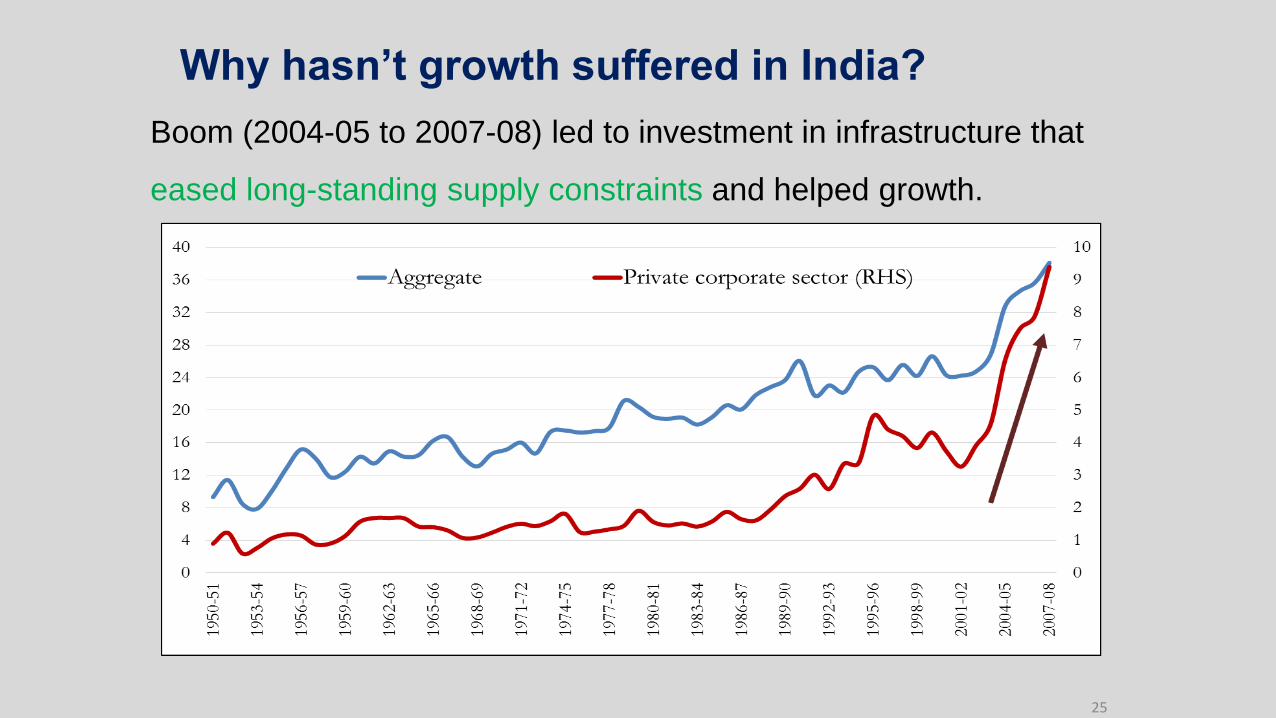

Why hasn’t growth suffered in India?

Boom (2004-05 to 2007-08) led to investment in infrastructure that

eased long-standing supply constraints and helped growth.

25

Strategy so far:

‘Giving Time to Time’ and EvergreeningAbout 6.5 % of loans outstanding of

stressed Companies were

restructured by 2014-15

With little improvements in cash flow

stressed Co.s* have borrowed

significantly to continue operations

454

990

1,372

2,101

2,675

3,572

5,349

6,298

6,689

7,083

7,519

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

FY

06

FY

07

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

Source: Credit Suisse database. * Top 10 stressed Groups. Includes bank debt, bonds, ECBs, and other debt.

27

Picture from CartoonStock, Andrew Toos.

Effects of the Twin Balance

Sheet Crisis

Health of Public Sector Banks in the Red

(Return on Assets)

International Norm

29

Return on Assets is obtained by dividing net profits by average total assets. The dotted

red line indicates the international norm.

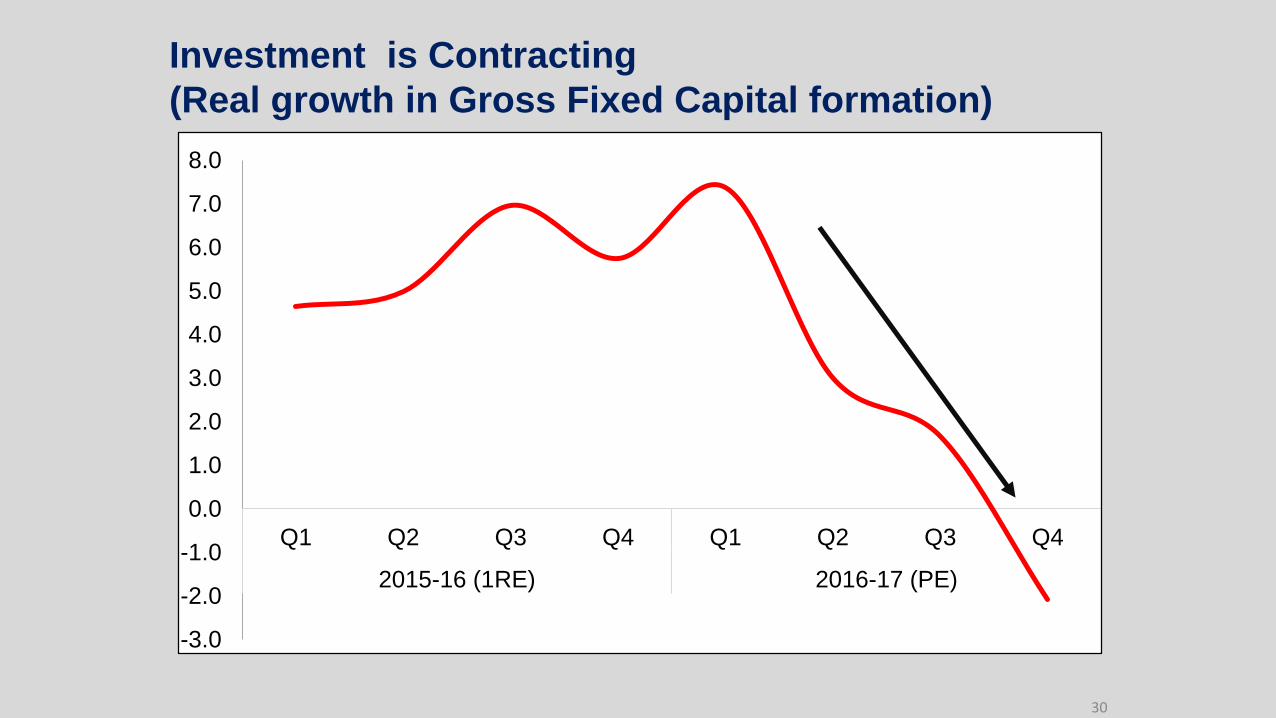

Investment is Contracting

(Real growth in Gross Fixed Capital formation)

30

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2015-16 (1RE) 2016-17 (PE)

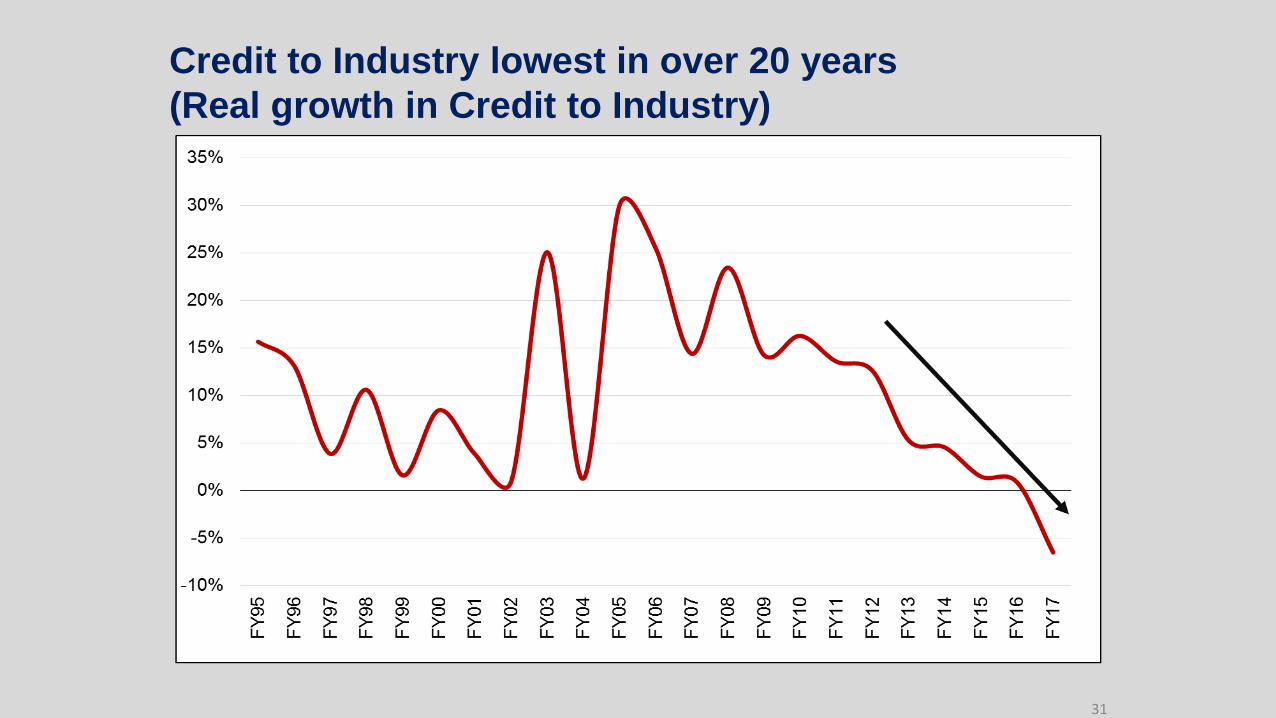

Credit to Industry lowest in over 20 years

(Real growth in Credit to Industry)

31

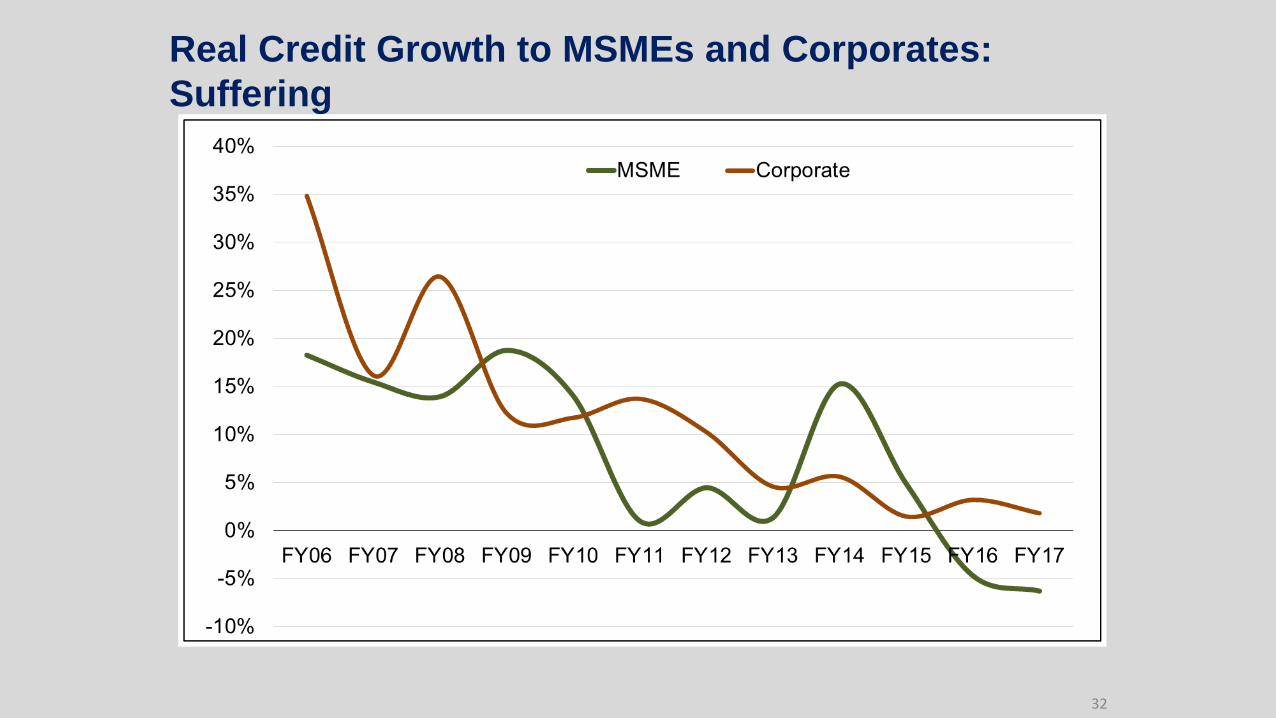

Real Credit Growth to MSMEs and Corporates:

Suffering

32

Monetary Policy Transmission 1A: Interest Rate and Borrowing

Channel, Transmission of Recent Rate Cuts Impeded by Rising NPAs

6.0

6.5

7.0

7.5

8.0

8.5

9.0

9.5

10.0

10.5

Apr.

21,

201

7M

ar.

10

, 20

17

Ja

n.

27

, 20

17

De

c. 1

6, 2

016

Nov. 4

, 20

16

Sep

. 23

, 2

016

Aug

. 12

, 2

016

Ju

l. 1

, 20

16

Ma

y 2

0,

20

16

Apr.

8, 2

016

Fe

b.

19,

20

16

Ja

n.

1,

201

6N

ov. 2

0, 2

015

Oct. 9

, 2

015

Aug

. 28

, 2

015

Ju

l. 1

7, 2

015

Ju

n.

5,

201

5A

pr.

24,

201

5M

ar.

6,

201

5Ja

n.

23

, 20

15

De

c. 1

2, 2

014

Oct. 3

1,

201

4S

ep

. 19

, 2

014

Aug

. 8,

20

14

Ju

n.

27

, 20

14

Ma

y 1

6,

20

14

Apr.

4, 2

014

Fe

b.

21,

20

14

Ja

n.

10

, 20

14

No

v. 2

9, 2

013

Oct. 1

8,

201

3S

ep

. 6,

20

13

Ju

l. 2

6, 2

013

Ju

n.

7,

201

3A

pr.

26,

201

3M

ar.

15

, 20

13

Fe

b.

1, 2

01

3D

ec. 2

1, 2

012

Nov. 9

, 20

12

Sep

. 28

, 2

012

Aug

. 17

, 2

012

Ju

n.

29

, 20

12

Ma

y 1

8,

20

12

Apr.

6, 2

012

Fe

b.

24,

20

12

Ja

n.

13

, 20

12

Dec. 2

, 20

11

Policy Repo Rate

Base Rate Mean

Term Deposit Rate Mean

33

How does India fit in the Balance Sheet Crisis Model?• Similarities with other cases (Japan)

• High NPAs

• Decisive resolution time-consuming.

• Weak (private) investment.

• But unique due to

• Relatively robust growth.

• Moderately high inflation.

• Key: In Japan and India fixing of balance sheets has taken time unlike

in US (after GFC) and Thailand (after AFC). So for the latter recovery

have been quicker.

34

June 2014:

5:25 Flexible

Refinancing

Mar-

14

Dec-14 Mar-16

June 16:

Scheme for

Sustainable

Structuring of

Stressed Assets

August

2014:

Change in

ARC Fee

Structure

June 2015:

SDR

Scheme

October

2015:

AQR

Scheme

May-17

Timeline of RBI/Government Actions

Banking

Regulation

(Amendment)

Ordinance

2017

Core Problems• It’s not just about banks, it’s a lot about companies. Public discussion has focused on bank

capital which is the easiest part. More problematic is to resolve the bad debts in the first place.

• It is an economic problem, not a morality play. Several of the problems have been caused by

unexpected changes in the economic environment: timetables, exchange rates, and growth rate

assumptions.

• The stressed debt is heavily concentrated in large companies. Concentration is an

opportunity, because TBS could be overcome by solving a relatively small number of cases. But

large cases are also more difficult to resolve.

• Many of these companies are unviable at current levels of debt requiring debt write-downs

in many cases. Cash flows in the large stressed companies have been deteriorating over the past

few years. The only alternative would be to convert debt to equity, take over the companies, and

then sell them at a loss.

42

Core Problems• Banks are finding it difficult to resolve these cases, despite a proliferation of schemes to

help them. They face severe coordination problems, since large debtors have many creditors. If

PSU banks grant large debt reductions, this could attract the attention of the investigative agencies.

But taking over large companies will be politically difficult, as well.

• Delay is costly. Since banks can’t resolve the big cases, they have simply refinanced the debtors.

But this is costly for the government, because it means the bad debts keep rising, increasing the

ultimate recapitalization bill for the government. Delay is also costly for the economy.

• Progress may require a Public Sector Asset Rehabilitation Agency (PARA). Private ARCs

haven’t proved more successful than banks. But international experience shows that a

professionally run central agency with government backing – while not without its own problems --

can overcome these difficulties.

37

38

Stressed Companies in Difficult Situation

Example: PowerGiven large cost over-runs, break even tariff is well above current merchant rates*

*: Tariffs are in Rs./KwH and on shown in RHS. Costs are in Rs. Million.

0

1

2

3

4

5

6

7

8

9

0

20

40

60

80

100

120

140

160Original Cost per MW (Rs mn) Cost overrun per MW (Rs mn)

Required Tariff (Rs/KwH) (RHS) Current Merchant tariff (Rs/KwH) (RHS)

The 4 Rs for Progress

39

• Recognition

• Resolution

• Recapitalization

• Reform

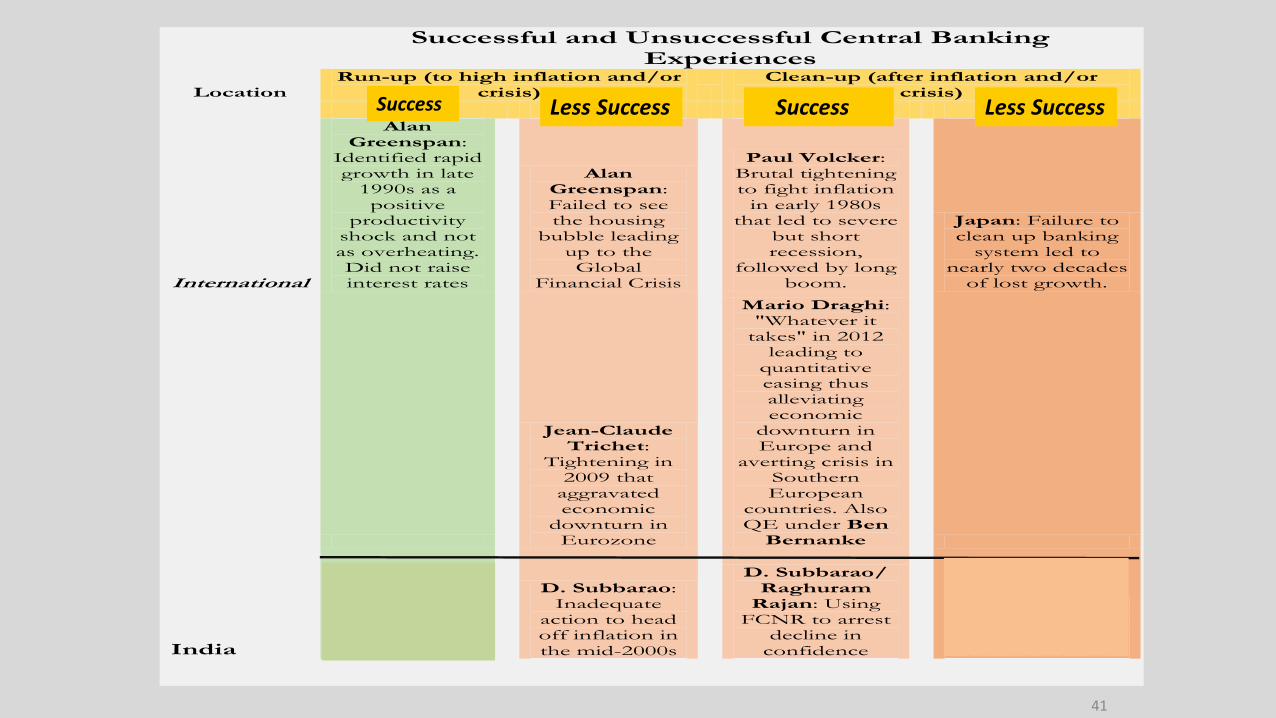

Successful and Unsuccessful Central Banking Experiences

Location Run-up (to high inflation and/or

crisis) Clean-up (after inflation and/or

crisis)

Success Less Success Less Success Failure

International

Alan Greenspan:

Identified rapid growth in late

1990s as a positive

productivity shock and not as overheating. Did not raise interest rates

Alan Greenspan: Failed to see the housing

bubble leading up to the Global

Financial Crisis

Paul Volcker: Brutal tightening to fight inflation

in early 1980s that led to severe

but short recession,

followed by long boom.

Japan: Failure to clean up banking

system led to nearly two decades

of lost growth.

Jean-Claude Trichet:

Tightening in 2009 that

aggravated economic

downturn in Eurozone

Mario Draghi: "Whatever it

takes" in 2012 leading to

quantitative easing thus alleviating economic

downturn in Europe and

averting crisis in Southern European

countries. Also QE under Ben

Bernanke

India

Y.V. Reddy: Anticipating

asset price rise and taking pre-emptive action

D. Subbarao: Inadequate

action to head off inflation in the mid-2000s

D. Subbarao/ Raghuram

Rajan: Using FCNR to arrest

decline in confidence

Post-2011 India: Twin Balance

Sheet challenge still unresolved

41

Less SuccessSuccessLess SuccessSuccess

Recommended Readings*1. Claessens, Stijn and M. Ayhan Kose, 2013, “Financial Crises Explanations,

Types, and Implications”, IMF working paper WP/13/28.

2. Economic Survey 2016-17, Chapter 4.

3. Reinhart, C. M. & K. S. Rogoff, 2008, “This Time is Different: A Panoramic

View of Eight Centuries of Financial Crises”, National Bureau of Economic

Research working paper 13882.

4. Subramanian, A., Josh Felman, Rangeet Ghosh & Zubair Noqvi, 2017,

“Rehab for the Balance Sheet”, The Indian Express.

*: The video clips used in this presentation from the movie ”The Big Short” have been

taken from YouTube.

42