ECON 202: Principles of Microeconomics Chapter 13 Oligopoly.

Econ 101: Principles of MicroeconomicsChapter 9: Making Decisions

Fall 2010

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 1 / 37

Outline

1 Opportunity Cost and Decisions

2 The Role of Marginal AnalysisMarginal CostMarginal Benefits

3 Sunk Cost

4 The Concept of Present Value

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 2 / 37

The Focus of This Chapter

In the remainder of the course, we will look in detail about thedecisions made by firms and consumers.

While the issues will vary from case to case, there are severalconcepts that will arise over and over again.

This chapter highlights four key concepts to keep in mind whenstudying the decision-making process:

1 Opportunity Costs: what you give up in making a choice.2 Marginal Analysis: studying the impact of small changes in the

“how-much” decision.3 Sunk Costs: costs that have already been incurred and cannot be

recovered.4 Present Value: The value today of a future cost or benefit.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 3 / 37

The Focus of This Chapter

In the remainder of the course, we will look in detail about thedecisions made by firms and consumers.

While the issues will vary from case to case, there are severalconcepts that will arise over and over again.

This chapter highlights four key concepts to keep in mind whenstudying the decision-making process:

1 Opportunity Costs: what you give up in making a choice.2 Marginal Analysis: studying the impact of small changes in the

“how-much” decision.3 Sunk Costs: costs that have already been incurred and cannot be

recovered.4 Present Value: The value today of a future cost or benefit.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 3 / 37

The Focus of This Chapter

In the remainder of the course, we will look in detail about thedecisions made by firms and consumers.

While the issues will vary from case to case, there are severalconcepts that will arise over and over again.

This chapter highlights four key concepts to keep in mind whenstudying the decision-making process:

1 Opportunity Costs: what you give up in making a choice.2 Marginal Analysis: studying the impact of small changes in the

“how-much” decision.3 Sunk Costs: costs that have already been incurred and cannot be

recovered.4 Present Value: The value today of a future cost or benefit.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 3 / 37

The Focus of This Chapter

In the remainder of the course, we will look in detail about thedecisions made by firms and consumers.

While the issues will vary from case to case, there are severalconcepts that will arise over and over again.

This chapter highlights four key concepts to keep in mind whenstudying the decision-making process:

1 Opportunity Costs: what you give up in making a choice.

2 Marginal Analysis: studying the impact of small changes in the“how-much” decision.

3 Sunk Costs: costs that have already been incurred and cannot berecovered.

4 Present Value: The value today of a future cost or benefit.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 3 / 37

The Focus of This Chapter

In the remainder of the course, we will look in detail about thedecisions made by firms and consumers.

While the issues will vary from case to case, there are severalconcepts that will arise over and over again.

This chapter highlights four key concepts to keep in mind whenstudying the decision-making process:

1 Opportunity Costs: what you give up in making a choice.2 Marginal Analysis: studying the impact of small changes in the

“how-much” decision.

3 Sunk Costs: costs that have already been incurred and cannot berecovered.

4 Present Value: The value today of a future cost or benefit.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 3 / 37

The Focus of This Chapter

In the remainder of the course, we will look in detail about thedecisions made by firms and consumers.

While the issues will vary from case to case, there are severalconcepts that will arise over and over again.

This chapter highlights four key concepts to keep in mind whenstudying the decision-making process:

1 Opportunity Costs: what you give up in making a choice.2 Marginal Analysis: studying the impact of small changes in the

“how-much” decision.3 Sunk Costs: costs that have already been incurred and cannot be

recovered.

4 Present Value: The value today of a future cost or benefit.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 3 / 37

The Focus of This Chapter

In the remainder of the course, we will look in detail about thedecisions made by firms and consumers.

While the issues will vary from case to case, there are severalconcepts that will arise over and over again.

This chapter highlights four key concepts to keep in mind whenstudying the decision-making process:

1 Opportunity Costs: what you give up in making a choice.2 Marginal Analysis: studying the impact of small changes in the

“how-much” decision.3 Sunk Costs: costs that have already been incurred and cannot be

recovered.4 Present Value: The value today of a future cost or benefit.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 3 / 37

Opportunity Cost and Decisions

Opportunity Cost and Decisions

We have already talked about the notion of opportunity cost

- In considering whether to make a fancy breakfast before class.- In considering the cost of attending college.

The opportunity cost of an action is the value of what we give up bytaking that action.

These costs can be broken down into two main components:1 The explicit cost; i.e., the actual money spent as a result of the action.2 The implicit costs; i.e., the non-monetary costs (opportunities

foregone) by the action.

In many cases, the implicit costs can be substantial.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 4 / 37

Opportunity Cost and Decisions

Opportunity Cost and Decisions

We have already talked about the notion of opportunity cost

- In considering whether to make a fancy breakfast before class.

- In considering the cost of attending college.

The opportunity cost of an action is the value of what we give up bytaking that action.

These costs can be broken down into two main components:1 The explicit cost; i.e., the actual money spent as a result of the action.2 The implicit costs; i.e., the non-monetary costs (opportunities

foregone) by the action.

In many cases, the implicit costs can be substantial.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 4 / 37

Opportunity Cost and Decisions

Opportunity Cost and Decisions

We have already talked about the notion of opportunity cost

- In considering whether to make a fancy breakfast before class.- In considering the cost of attending college.

The opportunity cost of an action is the value of what we give up bytaking that action.

These costs can be broken down into two main components:1 The explicit cost; i.e., the actual money spent as a result of the action.2 The implicit costs; i.e., the non-monetary costs (opportunities

foregone) by the action.

In many cases, the implicit costs can be substantial.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 4 / 37

Opportunity Cost and Decisions

Opportunity Cost and Decisions

We have already talked about the notion of opportunity cost

- In considering whether to make a fancy breakfast before class.- In considering the cost of attending college.

The opportunity cost of an action is the value of what we give up bytaking that action.

These costs can be broken down into two main components:1 The explicit cost; i.e., the actual money spent as a result of the action.2 The implicit costs; i.e., the non-monetary costs (opportunities

foregone) by the action.

In many cases, the implicit costs can be substantial.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 4 / 37

Opportunity Cost and Decisions

Opportunity Cost and Decisions

We have already talked about the notion of opportunity cost

- In considering whether to make a fancy breakfast before class.- In considering the cost of attending college.

The opportunity cost of an action is the value of what we give up bytaking that action.

These costs can be broken down into two main components:

1 The explicit cost; i.e., the actual money spent as a result of the action.2 The implicit costs; i.e., the non-monetary costs (opportunities

foregone) by the action.

In many cases, the implicit costs can be substantial.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 4 / 37

Opportunity Cost and Decisions

Opportunity Cost and Decisions

We have already talked about the notion of opportunity cost

- In considering whether to make a fancy breakfast before class.- In considering the cost of attending college.

The opportunity cost of an action is the value of what we give up bytaking that action.

These costs can be broken down into two main components:1 The explicit cost; i.e., the actual money spent as a result of the action.

2 The implicit costs; i.e., the non-monetary costs (opportunitiesforegone) by the action.

In many cases, the implicit costs can be substantial.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 4 / 37

Opportunity Cost and Decisions

Opportunity Cost and Decisions

We have already talked about the notion of opportunity cost

- In considering whether to make a fancy breakfast before class.- In considering the cost of attending college.

The opportunity cost of an action is the value of what we give up bytaking that action.

These costs can be broken down into two main components:1 The explicit cost; i.e., the actual money spent as a result of the action.2 The implicit costs; i.e., the non-monetary costs (opportunities

foregone) by the action.

In many cases, the implicit costs can be substantial.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 4 / 37

Opportunity Cost and Decisions

Opportunity Cost and Decisions

We have already talked about the notion of opportunity cost

- In considering whether to make a fancy breakfast before class.- In considering the cost of attending college.

The opportunity cost of an action is the value of what we give up bytaking that action.

These costs can be broken down into two main components:1 The explicit cost; i.e., the actual money spent as a result of the action.2 The implicit costs; i.e., the non-monetary costs (opportunities

foregone) by the action.

In many cases, the implicit costs can be substantial.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 4 / 37

Opportunity Cost and Decisions

The Cost of Raising a Child

What is the cost of raising a child, excluding college?

The estimates vary substantially, but figures close to $250-300,000are typical

The site http://www.babycenter.com/cost-of-raising-child-calculatorprovides estimates that vary by region, whether it is a single- ortwo-parent household, and the region in which you live.

Some of the categories they consider are:- Housing- Food- Transportation- Clothing- Healthcare- Childcare and Education

What other costs might we be missing here?

Is the cost of raising children less if one parent decides to stay athome?

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 5 / 37

Opportunity Cost and Decisions

The Cost of Raising a Child

What is the cost of raising a child, excluding college?

The estimates vary substantially, but figures close to $250-300,000are typical

The site http://www.babycenter.com/cost-of-raising-child-calculatorprovides estimates that vary by region, whether it is a single- ortwo-parent household, and the region in which you live.

Some of the categories they consider are:- Housing- Food- Transportation- Clothing- Healthcare- Childcare and Education

What other costs might we be missing here?

Is the cost of raising children less if one parent decides to stay athome?

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 5 / 37

Opportunity Cost and Decisions

The Cost of Raising a Child

What is the cost of raising a child, excluding college?

The estimates vary substantially, but figures close to $250-300,000are typical

The site http://www.babycenter.com/cost-of-raising-child-calculatorprovides estimates that vary by region, whether it is a single- ortwo-parent household, and the region in which you live.

Some of the categories they consider are:- Housing- Food- Transportation- Clothing- Healthcare- Childcare and Education

What other costs might we be missing here?

Is the cost of raising children less if one parent decides to stay athome?

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 5 / 37

Opportunity Cost and Decisions

The Cost of Raising a Child

What is the cost of raising a child, excluding college?

The estimates vary substantially, but figures close to $250-300,000are typical

The site http://www.babycenter.com/cost-of-raising-child-calculatorprovides estimates that vary by region, whether it is a single- ortwo-parent household, and the region in which you live.

Some of the categories they consider are:

- Housing- Food- Transportation- Clothing- Healthcare- Childcare and Education

What other costs might we be missing here?

Is the cost of raising children less if one parent decides to stay athome?

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 5 / 37

Opportunity Cost and Decisions

The Cost of Raising a Child

What is the cost of raising a child, excluding college?

The estimates vary substantially, but figures close to $250-300,000are typical

The site http://www.babycenter.com/cost-of-raising-child-calculatorprovides estimates that vary by region, whether it is a single- ortwo-parent household, and the region in which you live.

Some of the categories they consider are:- Housing

- Food- Transportation- Clothing- Healthcare- Childcare and Education

What other costs might we be missing here?

Is the cost of raising children less if one parent decides to stay athome?

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 5 / 37

Opportunity Cost and Decisions

The Cost of Raising a Child

What is the cost of raising a child, excluding college?

The estimates vary substantially, but figures close to $250-300,000are typical

The site http://www.babycenter.com/cost-of-raising-child-calculatorprovides estimates that vary by region, whether it is a single- ortwo-parent household, and the region in which you live.

Some of the categories they consider are:- Housing- Food

- Transportation- Clothing- Healthcare- Childcare and Education

What other costs might we be missing here?

Is the cost of raising children less if one parent decides to stay athome?

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 5 / 37

Opportunity Cost and Decisions

The Cost of Raising a Child

What is the cost of raising a child, excluding college?

The estimates vary substantially, but figures close to $250-300,000are typical

The site http://www.babycenter.com/cost-of-raising-child-calculatorprovides estimates that vary by region, whether it is a single- ortwo-parent household, and the region in which you live.

Some of the categories they consider are:- Housing- Food- Transportation

- Clothing- Healthcare- Childcare and Education

What other costs might we be missing here?

Is the cost of raising children less if one parent decides to stay athome?

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 5 / 37

Opportunity Cost and Decisions

The Cost of Raising a Child

What is the cost of raising a child, excluding college?

The estimates vary substantially, but figures close to $250-300,000are typical

The site http://www.babycenter.com/cost-of-raising-child-calculatorprovides estimates that vary by region, whether it is a single- ortwo-parent household, and the region in which you live.

Some of the categories they consider are:- Housing- Food- Transportation- Clothing

- Healthcare- Childcare and Education

What other costs might we be missing here?

Is the cost of raising children less if one parent decides to stay athome?

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 5 / 37

Opportunity Cost and Decisions

The Cost of Raising a Child

What is the cost of raising a child, excluding college?

The estimates vary substantially, but figures close to $250-300,000are typical

The site http://www.babycenter.com/cost-of-raising-child-calculatorprovides estimates that vary by region, whether it is a single- ortwo-parent household, and the region in which you live.

Some of the categories they consider are:- Housing- Food- Transportation- Clothing- Healthcare

- Childcare and Education

What other costs might we be missing here?

Is the cost of raising children less if one parent decides to stay athome?

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 5 / 37

Opportunity Cost and Decisions

The Cost of Raising a Child

What is the cost of raising a child, excluding college?

The estimates vary substantially, but figures close to $250-300,000are typical

The site http://www.babycenter.com/cost-of-raising-child-calculatorprovides estimates that vary by region, whether it is a single- ortwo-parent household, and the region in which you live.

Some of the categories they consider are:- Housing- Food- Transportation- Clothing- Healthcare- Childcare and Education

What other costs might we be missing here?

Is the cost of raising children less if one parent decides to stay athome?

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 5 / 37

Opportunity Cost and Decisions

The Cost of Raising a Child

What is the cost of raising a child, excluding college?

The estimates vary substantially, but figures close to $250-300,000are typical

The site http://www.babycenter.com/cost-of-raising-child-calculatorprovides estimates that vary by region, whether it is a single- ortwo-parent household, and the region in which you live.

Some of the categories they consider are:- Housing- Food- Transportation- Clothing- Healthcare- Childcare and Education

What other costs might we be missing here?

Is the cost of raising children less if one parent decides to stay athome?

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 5 / 37

Opportunity Cost and Decisions

The Cost of Raising a Child

What is the cost of raising a child, excluding college?

The estimates vary substantially, but figures close to $250-300,000are typical

The site http://www.babycenter.com/cost-of-raising-child-calculatorprovides estimates that vary by region, whether it is a single- ortwo-parent household, and the region in which you live.

Some of the categories they consider are:- Housing- Food- Transportation- Clothing- Healthcare- Childcare and Education

What other costs might we be missing here?

Is the cost of raising children less if one parent decides to stay athome?

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 5 / 37

Opportunity Cost and Decisions

Accounting Profit versus Economic Profit

These same issues arise when economists talk about profit.

Economists distinguish between1 Accounting profit: The total revenues of the firm minus the firm’s

explicit costs and capital depreciation.2 Economic profit: The total revenues of the firm minus the opportunity

costs of the resources it uses.

Accounting profits are important, particularly for tax purposes.

However, economic profits are more important in terms of guiding thedecisions made by firms.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 6 / 37

Opportunity Cost and Decisions

Accounting Profit versus Economic Profit

These same issues arise when economists talk about profit.

Economists distinguish between

1 Accounting profit: The total revenues of the firm minus the firm’sexplicit costs and capital depreciation.

2 Economic profit: The total revenues of the firm minus the opportunitycosts of the resources it uses.

Accounting profits are important, particularly for tax purposes.

However, economic profits are more important in terms of guiding thedecisions made by firms.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 6 / 37

Opportunity Cost and Decisions

Accounting Profit versus Economic Profit

These same issues arise when economists talk about profit.

Economists distinguish between1 Accounting profit: The total revenues of the firm minus the firm’s

explicit costs and capital depreciation.

2 Economic profit: The total revenues of the firm minus the opportunitycosts of the resources it uses.

Accounting profits are important, particularly for tax purposes.

However, economic profits are more important in terms of guiding thedecisions made by firms.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 6 / 37

Opportunity Cost and Decisions

Accounting Profit versus Economic Profit

These same issues arise when economists talk about profit.

Economists distinguish between1 Accounting profit: The total revenues of the firm minus the firm’s

explicit costs and capital depreciation.2 Economic profit: The total revenues of the firm minus the opportunity

costs of the resources it uses.

Accounting profits are important, particularly for tax purposes.

However, economic profits are more important in terms of guiding thedecisions made by firms.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 6 / 37

Opportunity Cost and Decisions

Accounting Profit versus Economic Profit

These same issues arise when economists talk about profit.

Economists distinguish between1 Accounting profit: The total revenues of the firm minus the firm’s

explicit costs and capital depreciation.2 Economic profit: The total revenues of the firm minus the opportunity

costs of the resources it uses.

Accounting profits are important, particularly for tax purposes.

However, economic profits are more important in terms of guiding thedecisions made by firms.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 6 / 37

Opportunity Cost and Decisions

Accounting Profit versus Economic Profit

These same issues arise when economists talk about profit.

Economists distinguish between1 Accounting profit: The total revenues of the firm minus the firm’s

explicit costs and capital depreciation.2 Economic profit: The total revenues of the firm minus the opportunity

costs of the resources it uses.

Accounting profits are important, particularly for tax purposes.

However, economic profits are more important in terms of guiding thedecisions made by firms.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 6 / 37

Opportunity Cost and Decisions

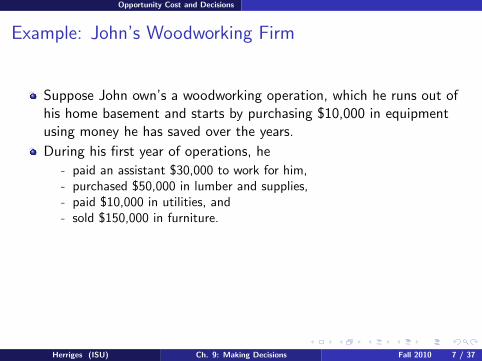

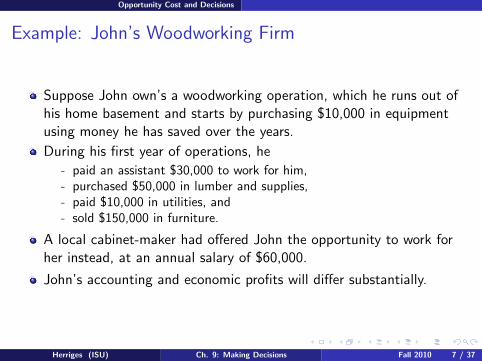

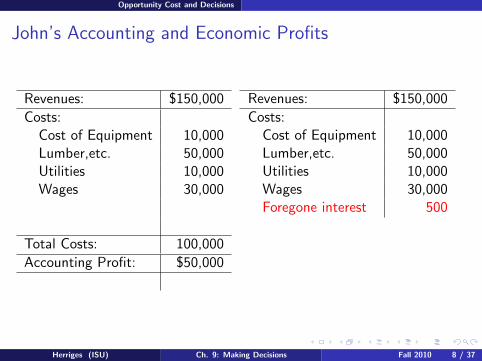

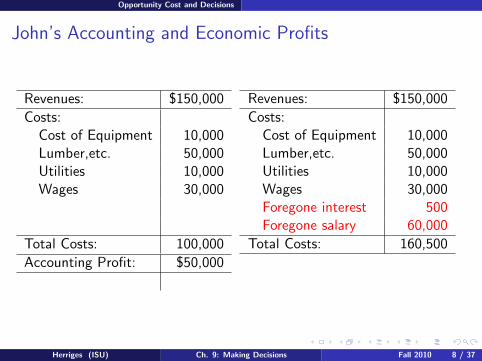

Example: John’s Woodworking Firm

Suppose John own’s a woodworking operation, which he runs out ofhis home basement and starts by purchasing $10,000 in equipmentusing money he has saved over the years.

During his first year of operations, he

- paid an assistant $30,000 to work for him,- purchased $50,000 in lumber and supplies,- paid $10,000 in utilities, and- sold $150,000 in furniture.

A local cabinet-maker had offered John the opportunity to work forher instead, at an annual salary of $60,000.

John’s accounting and economic profits will differ substantially.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 7 / 37

Opportunity Cost and Decisions

Example: John’s Woodworking Firm

Suppose John own’s a woodworking operation, which he runs out ofhis home basement and starts by purchasing $10,000 in equipmentusing money he has saved over the years.

During his first year of operations, he

- paid an assistant $30,000 to work for him,- purchased $50,000 in lumber and supplies,- paid $10,000 in utilities, and- sold $150,000 in furniture.

A local cabinet-maker had offered John the opportunity to work forher instead, at an annual salary of $60,000.

John’s accounting and economic profits will differ substantially.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 7 / 37

Opportunity Cost and Decisions

Example: John’s Woodworking Firm

Suppose John own’s a woodworking operation, which he runs out ofhis home basement and starts by purchasing $10,000 in equipmentusing money he has saved over the years.

During his first year of operations, he

- paid an assistant $30,000 to work for him,

- purchased $50,000 in lumber and supplies,- paid $10,000 in utilities, and- sold $150,000 in furniture.

A local cabinet-maker had offered John the opportunity to work forher instead, at an annual salary of $60,000.

John’s accounting and economic profits will differ substantially.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 7 / 37

Opportunity Cost and Decisions

Example: John’s Woodworking Firm

Suppose John own’s a woodworking operation, which he runs out ofhis home basement and starts by purchasing $10,000 in equipmentusing money he has saved over the years.

During his first year of operations, he

- paid an assistant $30,000 to work for him,- purchased $50,000 in lumber and supplies,

- paid $10,000 in utilities, and- sold $150,000 in furniture.

A local cabinet-maker had offered John the opportunity to work forher instead, at an annual salary of $60,000.

John’s accounting and economic profits will differ substantially.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 7 / 37

Opportunity Cost and Decisions

Example: John’s Woodworking Firm

Suppose John own’s a woodworking operation, which he runs out ofhis home basement and starts by purchasing $10,000 in equipmentusing money he has saved over the years.

During his first year of operations, he

- paid an assistant $30,000 to work for him,- purchased $50,000 in lumber and supplies,- paid $10,000 in utilities, and

- sold $150,000 in furniture.

A local cabinet-maker had offered John the opportunity to work forher instead, at an annual salary of $60,000.

John’s accounting and economic profits will differ substantially.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 7 / 37

Opportunity Cost and Decisions

Example: John’s Woodworking Firm

Suppose John own’s a woodworking operation, which he runs out ofhis home basement and starts by purchasing $10,000 in equipmentusing money he has saved over the years.

During his first year of operations, he

- paid an assistant $30,000 to work for him,- purchased $50,000 in lumber and supplies,- paid $10,000 in utilities, and- sold $150,000 in furniture.

A local cabinet-maker had offered John the opportunity to work forher instead, at an annual salary of $60,000.

John’s accounting and economic profits will differ substantially.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 7 / 37

Opportunity Cost and Decisions

Example: John’s Woodworking Firm

Suppose John own’s a woodworking operation, which he runs out ofhis home basement and starts by purchasing $10,000 in equipmentusing money he has saved over the years.

During his first year of operations, he

- paid an assistant $30,000 to work for him,- purchased $50,000 in lumber and supplies,- paid $10,000 in utilities, and- sold $150,000 in furniture.

A local cabinet-maker had offered John the opportunity to work forher instead, at an annual salary of $60,000.

John’s accounting and economic profits will differ substantially.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 7 / 37

Opportunity Cost and Decisions

Example: John’s Woodworking Firm

Suppose John own’s a woodworking operation, which he runs out ofhis home basement and starts by purchasing $10,000 in equipmentusing money he has saved over the years.

During his first year of operations, he

- paid an assistant $30,000 to work for him,- purchased $50,000 in lumber and supplies,- paid $10,000 in utilities, and- sold $150,000 in furniture.

A local cabinet-maker had offered John the opportunity to work forher instead, at an annual salary of $60,000.

John’s accounting and economic profits will differ substantially.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 7 / 37

Opportunity Cost and Decisions

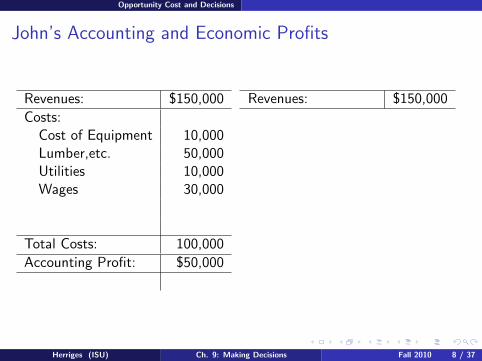

John’s Accounting and Economic Profits

Revenues: $150,000

Costs:Cost of Equipment 10,000Lumber,etc. 50,000Utilities 10,000Wages 30,000

Total Costs: 100,000

Accounting Profit: $50,000

Revenues: $150,000

Costs:Cost of Equipment 10,000Lumber,etc. 50,000Utilities 10,000Wages 30,000Foregone interest 500Foregone salary 60,000

Total Costs: 160,500

Economic Profit: -$10,500

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 8 / 37

Opportunity Cost and Decisions

John’s Accounting and Economic Profits

Revenues: $150,000

Costs:Cost of Equipment 10,000

Lumber,etc. 50,000Utilities 10,000Wages 30,000

Total Costs: 100,000

Accounting Profit: $50,000

Revenues: $150,000

Costs:Cost of Equipment 10,000Lumber,etc. 50,000Utilities 10,000Wages 30,000Foregone interest 500Foregone salary 60,000

Total Costs: 160,500

Economic Profit: -$10,500

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 8 / 37

Opportunity Cost and Decisions

John’s Accounting and Economic Profits

Revenues: $150,000

Costs:Cost of Equipment 10,000Lumber,etc. 50,000

Utilities 10,000Wages 30,000

Total Costs: 100,000

Accounting Profit: $50,000

Revenues: $150,000

Costs:Cost of Equipment 10,000Lumber,etc. 50,000Utilities 10,000Wages 30,000Foregone interest 500Foregone salary 60,000

Total Costs: 160,500

Economic Profit: -$10,500

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 8 / 37

Opportunity Cost and Decisions

John’s Accounting and Economic Profits

Revenues: $150,000

Costs:Cost of Equipment 10,000Lumber,etc. 50,000Utilities 10,000

Wages 30,000

Total Costs: 100,000

Accounting Profit: $50,000

Revenues: $150,000

Costs:Cost of Equipment 10,000Lumber,etc. 50,000Utilities 10,000Wages 30,000Foregone interest 500Foregone salary 60,000

Total Costs: 160,500

Economic Profit: -$10,500

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 8 / 37

Opportunity Cost and Decisions

John’s Accounting and Economic Profits

Revenues: $150,000

Costs:Cost of Equipment 10,000Lumber,etc. 50,000Utilities 10,000Wages 30,000

Total Costs: 100,000

Accounting Profit: $50,000

Revenues: $150,000

Costs:Cost of Equipment 10,000Lumber,etc. 50,000Utilities 10,000Wages 30,000Foregone interest 500Foregone salary 60,000

Total Costs: 160,500

Economic Profit: -$10,500

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 8 / 37

Opportunity Cost and Decisions

John’s Accounting and Economic Profits

Revenues: $150,000

Costs:Cost of Equipment 10,000Lumber,etc. 50,000Utilities 10,000Wages 30,000

Total Costs: 100,000

Accounting Profit: $50,000

Revenues: $150,000

Costs:Cost of Equipment 10,000Lumber,etc. 50,000Utilities 10,000Wages 30,000Foregone interest 500Foregone salary 60,000

Total Costs: 160,500

Economic Profit: -$10,500

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 8 / 37

Opportunity Cost and Decisions

John’s Accounting and Economic Profits

Revenues: $150,000

Costs:Cost of Equipment 10,000Lumber,etc. 50,000Utilities 10,000Wages 30,000

Total Costs: 100,000

Accounting Profit: $50,000

Revenues: $150,000

Costs:Cost of Equipment 10,000Lumber,etc. 50,000Utilities 10,000Wages 30,000Foregone interest 500Foregone salary 60,000

Total Costs: 160,500

Economic Profit: -$10,500

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 8 / 37

Opportunity Cost and Decisions

John’s Accounting and Economic Profits

Revenues: $150,000

Costs:Cost of Equipment 10,000Lumber,etc. 50,000Utilities 10,000Wages 30,000

Total Costs: 100,000

Accounting Profit: $50,000

Revenues: $150,000

Costs:Cost of Equipment 10,000Lumber,etc. 50,000Utilities 10,000Wages 30,000Foregone interest 500Foregone salary 60,000

Total Costs: 160,500

Economic Profit: -$10,500

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 8 / 37

Opportunity Cost and Decisions

John’s Accounting and Economic Profits

Revenues: $150,000

Costs:Cost of Equipment 10,000Lumber,etc. 50,000Utilities 10,000Wages 30,000

Total Costs: 100,000

Accounting Profit: $50,000

Revenues: $150,000

Costs:Cost of Equipment 10,000

Lumber,etc. 50,000Utilities 10,000Wages 30,000Foregone interest 500Foregone salary 60,000

Total Costs: 160,500

Economic Profit: -$10,500

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 8 / 37

Opportunity Cost and Decisions

John’s Accounting and Economic Profits

Revenues: $150,000

Costs:Cost of Equipment 10,000Lumber,etc. 50,000Utilities 10,000Wages 30,000

Total Costs: 100,000

Accounting Profit: $50,000

Revenues: $150,000

Costs:Cost of Equipment 10,000Lumber,etc. 50,000

Utilities 10,000Wages 30,000Foregone interest 500Foregone salary 60,000

Total Costs: 160,500

Economic Profit: -$10,500

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 8 / 37

Opportunity Cost and Decisions

John’s Accounting and Economic Profits

Revenues: $150,000

Costs:Cost of Equipment 10,000Lumber,etc. 50,000Utilities 10,000Wages 30,000

Total Costs: 100,000

Accounting Profit: $50,000

Revenues: $150,000

Costs:Cost of Equipment 10,000Lumber,etc. 50,000Utilities 10,000

Wages 30,000Foregone interest 500Foregone salary 60,000

Total Costs: 160,500

Economic Profit: -$10,500

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 8 / 37

Opportunity Cost and Decisions

John’s Accounting and Economic Profits

Revenues: $150,000

Costs:Cost of Equipment 10,000Lumber,etc. 50,000Utilities 10,000Wages 30,000

Total Costs: 100,000

Accounting Profit: $50,000

Revenues: $150,000

Costs:Cost of Equipment 10,000Lumber,etc. 50,000Utilities 10,000Wages 30,000

Foregone interest 500Foregone salary 60,000

Total Costs: 160,500

Economic Profit: -$10,500

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 8 / 37

Opportunity Cost and Decisions

John’s Accounting and Economic Profits

Revenues: $150,000

Costs:Cost of Equipment 10,000Lumber,etc. 50,000Utilities 10,000Wages 30,000

Total Costs: 100,000

Accounting Profit: $50,000

Revenues: $150,000

Costs:Cost of Equipment 10,000Lumber,etc. 50,000Utilities 10,000Wages 30,000Foregone interest 500

Foregone salary 60,000

Total Costs: 160,500

Economic Profit: -$10,500

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 8 / 37

Opportunity Cost and Decisions

John’s Accounting and Economic Profits

Revenues: $150,000

Costs:Cost of Equipment 10,000Lumber,etc. 50,000Utilities 10,000Wages 30,000

Total Costs: 100,000

Accounting Profit: $50,000

Revenues: $150,000

Costs:Cost of Equipment 10,000Lumber,etc. 50,000Utilities 10,000Wages 30,000Foregone interest 500Foregone salary 60,000

Total Costs: 160,500

Economic Profit: -$10,500

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 8 / 37

Opportunity Cost and Decisions

John’s Accounting and Economic Profits

Revenues: $150,000

Costs:Cost of Equipment 10,000Lumber,etc. 50,000Utilities 10,000Wages 30,000

Total Costs: 100,000

Accounting Profit: $50,000

Revenues: $150,000

Costs:Cost of Equipment 10,000Lumber,etc. 50,000Utilities 10,000Wages 30,000Foregone interest 500Foregone salary 60,000

Total Costs: 160,500

Economic Profit: -$10,500

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 8 / 37

Opportunity Cost and Decisions

John’s Accounting and Economic Profits

Revenues: $150,000

Costs:Cost of Equipment 10,000Lumber,etc. 50,000Utilities 10,000Wages 30,000

Total Costs: 100,000

Accounting Profit: $50,000

Revenues: $150,000

Costs:Cost of Equipment 10,000Lumber,etc. 50,000Utilities 10,000Wages 30,000Foregone interest 500Foregone salary 60,000

Total Costs: 160,500

Economic Profit: -$10,500

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 8 / 37

Opportunity Cost and Decisions

The Difference in Profits

In John’s case, while he made an accounting profit, economists wouldsay he had an economic loss.

The difference between his accounting profits and his economic profitslies in the “implicit costs” of his capital

Capital includes his

- Physical capital: the equipment, buildings, tools, inventory, andfinancial assets used by the firm.

- Human capital: the education and knowledge embodied in theworkforce.

For John, there are two implicit costs of his capital that are ignoredwhen computing accounting profits:

- The foregone interest John could have earned on the money he used tobuy the equipment.

- The foregone salary he could have earned working for the othercabinetmaker.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 9 / 37

Opportunity Cost and Decisions

The Difference in Profits

In John’s case, while he made an accounting profit, economists wouldsay he had an economic loss.

The difference between his accounting profits and his economic profitslies in the “implicit costs” of his capital

Capital includes his

- Physical capital: the equipment, buildings, tools, inventory, andfinancial assets used by the firm.

- Human capital: the education and knowledge embodied in theworkforce.

For John, there are two implicit costs of his capital that are ignoredwhen computing accounting profits:

- The foregone interest John could have earned on the money he used tobuy the equipment.

- The foregone salary he could have earned working for the othercabinetmaker.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 9 / 37

Opportunity Cost and Decisions

The Difference in Profits

In John’s case, while he made an accounting profit, economists wouldsay he had an economic loss.

The difference between his accounting profits and his economic profitslies in the “implicit costs” of his capital

Capital includes his

- Physical capital: the equipment, buildings, tools, inventory, andfinancial assets used by the firm.

- Human capital: the education and knowledge embodied in theworkforce.

For John, there are two implicit costs of his capital that are ignoredwhen computing accounting profits:

- The foregone interest John could have earned on the money he used tobuy the equipment.

- The foregone salary he could have earned working for the othercabinetmaker.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 9 / 37

Opportunity Cost and Decisions

The Difference in Profits

In John’s case, while he made an accounting profit, economists wouldsay he had an economic loss.

The difference between his accounting profits and his economic profitslies in the “implicit costs” of his capital

Capital includes his

- Physical capital: the equipment, buildings, tools, inventory, andfinancial assets used by the firm.

- Human capital: the education and knowledge embodied in theworkforce.

For John, there are two implicit costs of his capital that are ignoredwhen computing accounting profits:

- The foregone interest John could have earned on the money he used tobuy the equipment.

- The foregone salary he could have earned working for the othercabinetmaker.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 9 / 37

Opportunity Cost and Decisions

The Difference in Profits

In John’s case, while he made an accounting profit, economists wouldsay he had an economic loss.

The difference between his accounting profits and his economic profitslies in the “implicit costs” of his capital

Capital includes his

- Physical capital: the equipment, buildings, tools, inventory, andfinancial assets used by the firm.

- Human capital: the education and knowledge embodied in theworkforce.

For John, there are two implicit costs of his capital that are ignoredwhen computing accounting profits:

- The foregone interest John could have earned on the money he used tobuy the equipment.

- The foregone salary he could have earned working for the othercabinetmaker.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 9 / 37

Opportunity Cost and Decisions

The Difference in Profits

In John’s case, while he made an accounting profit, economists wouldsay he had an economic loss.

The difference between his accounting profits and his economic profitslies in the “implicit costs” of his capital

Capital includes his

- Physical capital: the equipment, buildings, tools, inventory, andfinancial assets used by the firm.

- Human capital: the education and knowledge embodied in theworkforce.

For John, there are two implicit costs of his capital that are ignoredwhen computing accounting profits:

- The foregone interest John could have earned on the money he used tobuy the equipment.

- The foregone salary he could have earned working for the othercabinetmaker.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 9 / 37

Opportunity Cost and Decisions

The Difference in Profits

In John’s case, while he made an accounting profit, economists wouldsay he had an economic loss.

The difference between his accounting profits and his economic profitslies in the “implicit costs” of his capital

Capital includes his

- Physical capital: the equipment, buildings, tools, inventory, andfinancial assets used by the firm.

- Human capital: the education and knowledge embodied in theworkforce.

For John, there are two implicit costs of his capital that are ignoredwhen computing accounting profits:

- The foregone interest John could have earned on the money he used tobuy the equipment.

- The foregone salary he could have earned working for the othercabinetmaker.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 9 / 37

Opportunity Cost and Decisions

The Difference in Profits

In John’s case, while he made an accounting profit, economists wouldsay he had an economic loss.

The difference between his accounting profits and his economic profitslies in the “implicit costs” of his capital

Capital includes his

- Physical capital: the equipment, buildings, tools, inventory, andfinancial assets used by the firm.

- Human capital: the education and knowledge embodied in theworkforce.

For John, there are two implicit costs of his capital that are ignoredwhen computing accounting profits:

- The foregone interest John could have earned on the money he used tobuy the equipment.

- The foregone salary he could have earned working for the othercabinetmaker.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 9 / 37

The Role of Marginal Analysis

Marginal Analysis

A second important economic concept is that of marginal analysis

:the comparison of the benefit of doing a little more of some activitywith the cost of doing a little more of that activity.

While we do often make “either or decisions,”such as whether to

buy a car or not,attend to college or not,take a vacation or not,. . .

. . . many of our decisions involve “how much” decisions (or whateconomists often refer to as “decisions at the margins”)

For example, we have to decide

How many packages of Ramen noodles to buy,How large a house to buy,How many hours to study for an examHow much money the government should allocate to the“Cash-for-clunkers” program.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 10 / 37

The Role of Marginal Analysis

Marginal Analysis

A second important economic concept is that of marginal analysis:the comparison of the benefit of doing a little more of some activitywith the cost of doing a little more of that activity.

While we do often make “either or decisions,”such as whether to

buy a car or not,attend to college or not,take a vacation or not,. . .

. . . many of our decisions involve “how much” decisions (or whateconomists often refer to as “decisions at the margins”)

For example, we have to decide

How many packages of Ramen noodles to buy,How large a house to buy,How many hours to study for an examHow much money the government should allocate to the“Cash-for-clunkers” program.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 10 / 37

The Role of Marginal Analysis

Marginal Analysis

A second important economic concept is that of marginal analysis:the comparison of the benefit of doing a little more of some activitywith the cost of doing a little more of that activity.

While we do often make “either or decisions,”

such as whether to

buy a car or not,attend to college or not,take a vacation or not,. . .

. . . many of our decisions involve “how much” decisions (or whateconomists often refer to as “decisions at the margins”)

For example, we have to decide

How many packages of Ramen noodles to buy,How large a house to buy,How many hours to study for an examHow much money the government should allocate to the“Cash-for-clunkers” program.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 10 / 37

The Role of Marginal Analysis

Marginal Analysis

A second important economic concept is that of marginal analysis:the comparison of the benefit of doing a little more of some activitywith the cost of doing a little more of that activity.

While we do often make “either or decisions,”such as whether to

buy a car or not,

attend to college or not,take a vacation or not,. . .

. . . many of our decisions involve “how much” decisions (or whateconomists often refer to as “decisions at the margins”)

For example, we have to decide

How many packages of Ramen noodles to buy,How large a house to buy,How many hours to study for an examHow much money the government should allocate to the“Cash-for-clunkers” program.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 10 / 37

The Role of Marginal Analysis

Marginal Analysis

A second important economic concept is that of marginal analysis:the comparison of the benefit of doing a little more of some activitywith the cost of doing a little more of that activity.

While we do often make “either or decisions,”such as whether to

buy a car or not,attend to college or not,

take a vacation or not,. . .

. . . many of our decisions involve “how much” decisions (or whateconomists often refer to as “decisions at the margins”)

For example, we have to decide

How many packages of Ramen noodles to buy,How large a house to buy,How many hours to study for an examHow much money the government should allocate to the“Cash-for-clunkers” program.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 10 / 37

The Role of Marginal Analysis

Marginal Analysis

A second important economic concept is that of marginal analysis:the comparison of the benefit of doing a little more of some activitywith the cost of doing a little more of that activity.

While we do often make “either or decisions,”such as whether to

buy a car or not,attend to college or not,take a vacation or not,. . .

. . . many of our decisions involve “how much” decisions (or whateconomists often refer to as “decisions at the margins”)

For example, we have to decide

How many packages of Ramen noodles to buy,How large a house to buy,How many hours to study for an examHow much money the government should allocate to the“Cash-for-clunkers” program.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 10 / 37

The Role of Marginal Analysis

Marginal Analysis

A second important economic concept is that of marginal analysis:the comparison of the benefit of doing a little more of some activitywith the cost of doing a little more of that activity.

While we do often make “either or decisions,”such as whether to

buy a car or not,attend to college or not,take a vacation or not,. . .

. . . many of our decisions involve “how much” decisions (or whateconomists often refer to as “decisions at the margins”)

For example, we have to decide

How many packages of Ramen noodles to buy,How large a house to buy,How many hours to study for an examHow much money the government should allocate to the“Cash-for-clunkers” program.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 10 / 37

The Role of Marginal Analysis

Marginal Analysis

A second important economic concept is that of marginal analysis:the comparison of the benefit of doing a little more of some activitywith the cost of doing a little more of that activity.

While we do often make “either or decisions,”such as whether to

buy a car or not,attend to college or not,take a vacation or not,. . .

. . . many of our decisions involve “how much” decisions (or whateconomists often refer to as “decisions at the margins”)

For example, we have to decide

How many packages of Ramen noodles to buy,

How large a house to buy,How many hours to study for an examHow much money the government should allocate to the“Cash-for-clunkers” program.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 10 / 37

The Role of Marginal Analysis

Marginal Analysis

A second important economic concept is that of marginal analysis:the comparison of the benefit of doing a little more of some activitywith the cost of doing a little more of that activity.

While we do often make “either or decisions,”such as whether to

buy a car or not,attend to college or not,take a vacation or not,. . .

. . . many of our decisions involve “how much” decisions (or whateconomists often refer to as “decisions at the margins”)

For example, we have to decide

How many packages of Ramen noodles to buy,How large a house to buy,

How many hours to study for an examHow much money the government should allocate to the“Cash-for-clunkers” program.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 10 / 37

The Role of Marginal Analysis

Marginal Analysis

A second important economic concept is that of marginal analysis:the comparison of the benefit of doing a little more of some activitywith the cost of doing a little more of that activity.

While we do often make “either or decisions,”such as whether to

buy a car or not,attend to college or not,take a vacation or not,. . .

. . . many of our decisions involve “how much” decisions (or whateconomists often refer to as “decisions at the margins”)

For example, we have to decide

How many packages of Ramen noodles to buy,How large a house to buy,How many hours to study for an exam

How much money the government should allocate to the“Cash-for-clunkers” program.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 10 / 37

The Role of Marginal Analysis

Marginal Analysis

A second important economic concept is that of marginal analysis:the comparison of the benefit of doing a little more of some activitywith the cost of doing a little more of that activity.

While we do often make “either or decisions,”such as whether to

buy a car or not,attend to college or not,take a vacation or not,. . .

. . . many of our decisions involve “how much” decisions (or whateconomists often refer to as “decisions at the margins”)

For example, we have to decide

How many packages of Ramen noodles to buy,How large a house to buy,How many hours to study for an examHow much money the government should allocate to the“Cash-for-clunkers” program.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 10 / 37

The Role of Marginal Analysis

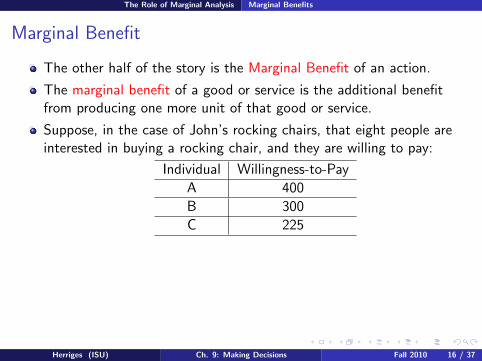

Choosing How Many Rocking Chairs to Build

Let’s revisit John’s woodworking shop.

For simplicity, suppose that

- John only builds rocking chairs.- He already owns all his equipment and has decided to work alone.- He no longer has a job offer from any other firm.

If we know that John could make $500 in profit by building 10rocking chairs, does that mean

- that he should build those 10 rocking chairs?- that he should build more rocking chairs?

We can’t tell.

What we need to be able to compare is the

- Marginal cost (i.e., the additional cost) of building each chair to- Marginal benefit (i.e., the additional benefit) from building each chair.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 11 / 37

The Role of Marginal Analysis

Choosing How Many Rocking Chairs to Build

Let’s revisit John’s woodworking shop.

For simplicity, suppose that

- John only builds rocking chairs.- He already owns all his equipment and has decided to work alone.- He no longer has a job offer from any other firm.

If we know that John could make $500 in profit by building 10rocking chairs, does that mean

- that he should build those 10 rocking chairs?- that he should build more rocking chairs?

We can’t tell.

What we need to be able to compare is the

- Marginal cost (i.e., the additional cost) of building each chair to- Marginal benefit (i.e., the additional benefit) from building each chair.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 11 / 37

The Role of Marginal Analysis

Choosing How Many Rocking Chairs to Build

Let’s revisit John’s woodworking shop.

For simplicity, suppose that

- John only builds rocking chairs.

- He already owns all his equipment and has decided to work alone.- He no longer has a job offer from any other firm.

If we know that John could make $500 in profit by building 10rocking chairs, does that mean

- that he should build those 10 rocking chairs?- that he should build more rocking chairs?

We can’t tell.

What we need to be able to compare is the

- Marginal cost (i.e., the additional cost) of building each chair to- Marginal benefit (i.e., the additional benefit) from building each chair.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 11 / 37

The Role of Marginal Analysis

Choosing How Many Rocking Chairs to Build

Let’s revisit John’s woodworking shop.

For simplicity, suppose that

- John only builds rocking chairs.- He already owns all his equipment and has decided to work alone.

- He no longer has a job offer from any other firm.

If we know that John could make $500 in profit by building 10rocking chairs, does that mean

- that he should build those 10 rocking chairs?- that he should build more rocking chairs?

We can’t tell.

What we need to be able to compare is the

- Marginal cost (i.e., the additional cost) of building each chair to- Marginal benefit (i.e., the additional benefit) from building each chair.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 11 / 37

The Role of Marginal Analysis

Choosing How Many Rocking Chairs to Build

Let’s revisit John’s woodworking shop.

For simplicity, suppose that

- John only builds rocking chairs.- He already owns all his equipment and has decided to work alone.- He no longer has a job offer from any other firm.

If we know that John could make $500 in profit by building 10rocking chairs, does that mean

- that he should build those 10 rocking chairs?- that he should build more rocking chairs?

We can’t tell.

What we need to be able to compare is the

- Marginal cost (i.e., the additional cost) of building each chair to- Marginal benefit (i.e., the additional benefit) from building each chair.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 11 / 37

The Role of Marginal Analysis

Choosing How Many Rocking Chairs to Build

Let’s revisit John’s woodworking shop.

For simplicity, suppose that

- John only builds rocking chairs.- He already owns all his equipment and has decided to work alone.- He no longer has a job offer from any other firm.

If we know that John could make $500 in profit by building 10rocking chairs, does that mean

- that he should build those 10 rocking chairs?- that he should build more rocking chairs?

We can’t tell.

What we need to be able to compare is the

- Marginal cost (i.e., the additional cost) of building each chair to- Marginal benefit (i.e., the additional benefit) from building each chair.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 11 / 37

The Role of Marginal Analysis

Choosing How Many Rocking Chairs to Build

Let’s revisit John’s woodworking shop.

For simplicity, suppose that

- John only builds rocking chairs.- He already owns all his equipment and has decided to work alone.- He no longer has a job offer from any other firm.

If we know that John could make $500 in profit by building 10rocking chairs, does that mean

- that he should build those 10 rocking chairs?

- that he should build more rocking chairs?

We can’t tell.

What we need to be able to compare is the

- Marginal cost (i.e., the additional cost) of building each chair to- Marginal benefit (i.e., the additional benefit) from building each chair.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 11 / 37

The Role of Marginal Analysis

Choosing How Many Rocking Chairs to Build

Let’s revisit John’s woodworking shop.

For simplicity, suppose that

- John only builds rocking chairs.- He already owns all his equipment and has decided to work alone.- He no longer has a job offer from any other firm.

If we know that John could make $500 in profit by building 10rocking chairs, does that mean

- that he should build those 10 rocking chairs?- that he should build more rocking chairs?

We can’t tell.

What we need to be able to compare is the

- Marginal cost (i.e., the additional cost) of building each chair to- Marginal benefit (i.e., the additional benefit) from building each chair.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 11 / 37

The Role of Marginal Analysis

Choosing How Many Rocking Chairs to Build

Let’s revisit John’s woodworking shop.

For simplicity, suppose that

- John only builds rocking chairs.- He already owns all his equipment and has decided to work alone.- He no longer has a job offer from any other firm.

If we know that John could make $500 in profit by building 10rocking chairs, does that mean

- that he should build those 10 rocking chairs?- that he should build more rocking chairs?

We can’t tell.

What we need to be able to compare is the

- Marginal cost (i.e., the additional cost) of building each chair to- Marginal benefit (i.e., the additional benefit) from building each chair.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 11 / 37

The Role of Marginal Analysis

Choosing How Many Rocking Chairs to Build

Let’s revisit John’s woodworking shop.

For simplicity, suppose that

- John only builds rocking chairs.- He already owns all his equipment and has decided to work alone.- He no longer has a job offer from any other firm.

If we know that John could make $500 in profit by building 10rocking chairs, does that mean

- that he should build those 10 rocking chairs?- that he should build more rocking chairs?

We can’t tell.

What we need to be able to compare is the

- Marginal cost (i.e., the additional cost) of building each chair

to- Marginal benefit (i.e., the additional benefit) from building each chair.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 11 / 37

The Role of Marginal Analysis

Choosing How Many Rocking Chairs to Build

Let’s revisit John’s woodworking shop.

For simplicity, suppose that

- John only builds rocking chairs.- He already owns all his equipment and has decided to work alone.- He no longer has a job offer from any other firm.

If we know that John could make $500 in profit by building 10rocking chairs, does that mean

- that he should build those 10 rocking chairs?- that he should build more rocking chairs?

We can’t tell.

What we need to be able to compare is the

- Marginal cost (i.e., the additional cost) of building each chair to- Marginal benefit (i.e., the additional benefit) from building each chair.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 11 / 37

The Role of Marginal Analysis Marginal Cost

Marginal Costs

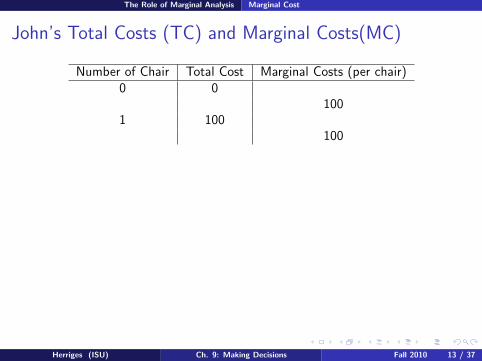

In general, the marginal cost of producing a good is the additionalcost of producing one more unit of the good.

For John, suppose the marginal cost of building a rocking chair is$100, regardless of how many chairs he builds.

This includes the cost of lumber and the electricity used in production.

This is an example of constant marginal cost

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 12 / 37

The Role of Marginal Analysis Marginal Cost

Marginal Costs

In general, the marginal cost of producing a good is the additionalcost of producing one more unit of the good.

For John, suppose the marginal cost of building a rocking chair is$100, regardless of how many chairs he builds.

This includes the cost of lumber and the electricity used in production.

This is an example of constant marginal cost

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 12 / 37

The Role of Marginal Analysis Marginal Cost

Marginal Costs

In general, the marginal cost of producing a good is the additionalcost of producing one more unit of the good.

For John, suppose the marginal cost of building a rocking chair is$100, regardless of how many chairs he builds.

This includes the cost of lumber and the electricity used in production.

This is an example of constant marginal cost

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 12 / 37

The Role of Marginal Analysis Marginal Cost

Marginal Costs

In general, the marginal cost of producing a good is the additionalcost of producing one more unit of the good.

For John, suppose the marginal cost of building a rocking chair is$100, regardless of how many chairs he builds.

This includes the cost of lumber and the electricity used in production.

This is an example of constant marginal cost

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 12 / 37

The Role of Marginal Analysis Marginal Cost

John’s Total Costs (TC) and Marginal Costs(MC)

Number of Chair Total Cost Marginal Costs (per chair)0 0

1001 100

1002 200

1003 300

1004 400

1005 500

1006 600

1007 700

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 13 / 37

The Role of Marginal Analysis Marginal Cost

John’s Total Costs (TC) and Marginal Costs(MC)

Number of Chair Total Cost Marginal Costs (per chair)0 0

100

1 100100

2 200100

3 300100

4 400100

5 500100

6 600100

7 700

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 13 / 37

The Role of Marginal Analysis Marginal Cost

John’s Total Costs (TC) and Marginal Costs(MC)

Number of Chair Total Cost Marginal Costs (per chair)0 0

1001 100

1002 200

1003 300

1004 400

1005 500

1006 600

1007 700

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 13 / 37

The Role of Marginal Analysis Marginal Cost

John’s Total Costs (TC) and Marginal Costs(MC)

Number of Chair Total Cost Marginal Costs (per chair)0 0

1001 100

100

2 200100

3 300100

4 400100

5 500100

6 600100

7 700

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 13 / 37

The Role of Marginal Analysis Marginal Cost

John’s Total Costs (TC) and Marginal Costs(MC)

Number of Chair Total Cost Marginal Costs (per chair)0 0

1001 100

1002 200

1003 300

1004 400

1005 500

1006 600

1007 700

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 13 / 37

The Role of Marginal Analysis Marginal Cost

John’s Total Costs (TC) and Marginal Costs(MC)

Number of Chair Total Cost Marginal Costs (per chair)0 0

1001 100

1002 200

100

3 300100

4 400100

5 500100

6 600100

7 700

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 13 / 37

The Role of Marginal Analysis Marginal Cost

John’s Total Costs (TC) and Marginal Costs(MC)

Number of Chair Total Cost Marginal Costs (per chair)0 0

1001 100

1002 200

1003 300

1004 400

1005 500

1006 600

1007 700

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 13 / 37

The Role of Marginal Analysis Marginal Cost

John’s Total Costs (TC) and Marginal Costs(MC)

Number of Chair Total Cost Marginal Costs (per chair)0 0

1001 100

1002 200

1003 300

100

4 400100

5 500100

6 600100

7 700

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 13 / 37

The Role of Marginal Analysis Marginal Cost

John’s Total Costs (TC) and Marginal Costs(MC)

Number of Chair Total Cost Marginal Costs (per chair)0 0

1001 100

1002 200

1003 300

1004 400

1005 500

1006 600

1007 700

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 13 / 37

The Role of Marginal Analysis Marginal Cost

John’s Total Costs (TC) and Marginal Costs(MC)

Number of Chair Total Cost Marginal Costs (per chair)0 0

1001 100

1002 200

1003 300

1004 400

100

5 500100

6 600100

7 700

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 13 / 37

The Role of Marginal Analysis Marginal Cost

John’s Total Costs (TC) and Marginal Costs(MC)

Number of Chair Total Cost Marginal Costs (per chair)0 0

1001 100

1002 200

1003 300

1004 400

1005 500

1006 600

1007 700

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 13 / 37

The Role of Marginal Analysis Marginal Cost

John’s Total Costs (TC) and Marginal Costs(MC)

Number of Chair Total Cost Marginal Costs (per chair)0 0

1001 100

1002 200

1003 300

1004 400

1005 500

100

6 600100

7 700

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 13 / 37

The Role of Marginal Analysis Marginal Cost

John’s Total Costs (TC) and Marginal Costs(MC)

Number of Chair Total Cost Marginal Costs (per chair)0 0

1001 100

1002 200

1003 300

1004 400

1005 500

1006 600

1007 700

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 13 / 37

The Role of Marginal Analysis Marginal Cost

John’s Total Costs (TC) and Marginal Costs(MC)

Number of Chair Total Cost Marginal Costs (per chair)0 0

1001 100

1002 200

1003 300

1004 400

1005 500

1006 600

100

7 700

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 13 / 37

The Role of Marginal Analysis Marginal Cost

John’s Total Costs (TC) and Marginal Costs(MC)

Number of Chair Total Cost Marginal Costs (per chair)0 0

1001 100

1002 200

1003 300

1004 400

1005 500

1006 600

1007 700

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 13 / 37

The Role of Marginal Analysis Marginal Cost

Marginal Cost Curve

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 14 / 37

The Role of Marginal Analysis Marginal Cost

Marginal Cost Curve

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 14 / 37

The Role of Marginal Analysis Marginal Cost

Marginal Cost Curve

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 14 / 37

The Role of Marginal Analysis Marginal Cost

Marginal Cost Curve

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 14 / 37

The Role of Marginal Analysis Marginal Cost

Marginal Cost Curve

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 14 / 37

The Role of Marginal Analysis Marginal Cost

Marginal Cost Curve

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 14 / 37

The Role of Marginal Analysis Marginal Cost

Marginal Cost Curve

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 14 / 37

The Role of Marginal Analysis Marginal Cost

Marginal Cost Curve

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 14 / 37

The Role of Marginal Analysis Marginal Cost

Marginal Cost Curve

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 14 / 37

The Role of Marginal Analysis Marginal Cost

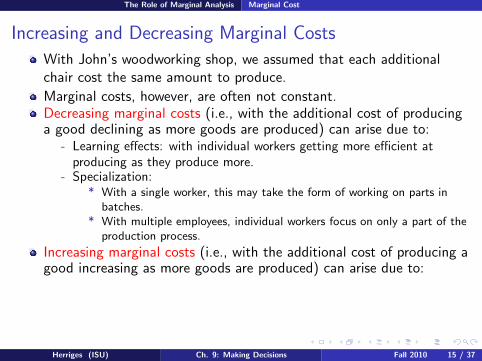

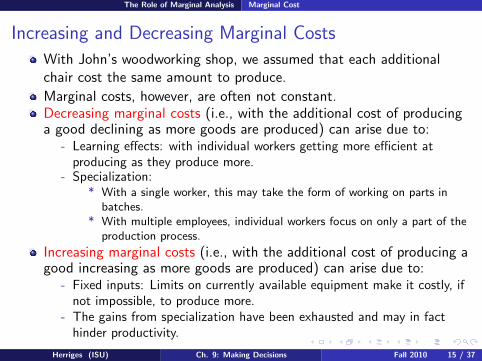

Increasing and Decreasing Marginal Costs

With John’s woodworking shop, we assumed that each additionalchair cost the same amount to produce.

Marginal costs, however, are often not constant.Decreasing marginal costs (i.e., with the additional cost of producinga good declining as more goods are produced) can arise due to:

- Learning effects: with individual workers getting more efficient atproducing as they produce more.

- Specialization:* With a single worker, this may take the form of working on parts in

batches.* With multiple employees, individual workers focus on only a part of the

production process.

Increasing marginal costs (i.e., with the additional cost of producing agood increasing as more goods are produced) can arise due to:

- Fixed inputs: Limits on currently available equipment make it costly, ifnot impossible, to produce more.

- The gains from specialization have been exhausted and may in facthinder productivity.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 15 / 37

The Role of Marginal Analysis Marginal Cost

Increasing and Decreasing Marginal Costs

With John’s woodworking shop, we assumed that each additionalchair cost the same amount to produce.

Marginal costs, however, are often not constant.

Decreasing marginal costs (i.e., with the additional cost of producinga good declining as more goods are produced) can arise due to:

- Learning effects: with individual workers getting more efficient atproducing as they produce more.

- Specialization:* With a single worker, this may take the form of working on parts in

batches.* With multiple employees, individual workers focus on only a part of the

production process.

Increasing marginal costs (i.e., with the additional cost of producing agood increasing as more goods are produced) can arise due to:

- Fixed inputs: Limits on currently available equipment make it costly, ifnot impossible, to produce more.

- The gains from specialization have been exhausted and may in facthinder productivity.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 15 / 37

The Role of Marginal Analysis Marginal Cost

Increasing and Decreasing Marginal Costs

With John’s woodworking shop, we assumed that each additionalchair cost the same amount to produce.

Marginal costs, however, are often not constant.Decreasing marginal costs (i.e., with the additional cost of producinga good declining as more goods are produced) can arise due to:

- Learning effects: with individual workers getting more efficient atproducing as they produce more.

- Specialization:* With a single worker, this may take the form of working on parts in

batches.* With multiple employees, individual workers focus on only a part of the

production process.

Increasing marginal costs (i.e., with the additional cost of producing agood increasing as more goods are produced) can arise due to:

- Fixed inputs: Limits on currently available equipment make it costly, ifnot impossible, to produce more.

- The gains from specialization have been exhausted and may in facthinder productivity.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 15 / 37

The Role of Marginal Analysis Marginal Cost

Increasing and Decreasing Marginal Costs

With John’s woodworking shop, we assumed that each additionalchair cost the same amount to produce.

Marginal costs, however, are often not constant.Decreasing marginal costs (i.e., with the additional cost of producinga good declining as more goods are produced) can arise due to:

- Learning effects: with individual workers getting more efficient atproducing as they produce more.

- Specialization:* With a single worker, this may take the form of working on parts in

batches.* With multiple employees, individual workers focus on only a part of the

production process.

Increasing marginal costs (i.e., with the additional cost of producing agood increasing as more goods are produced) can arise due to:

- Fixed inputs: Limits on currently available equipment make it costly, ifnot impossible, to produce more.

- The gains from specialization have been exhausted and may in facthinder productivity.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 15 / 37

The Role of Marginal Analysis Marginal Cost

Increasing and Decreasing Marginal Costs

With John’s woodworking shop, we assumed that each additionalchair cost the same amount to produce.

Marginal costs, however, are often not constant.Decreasing marginal costs (i.e., with the additional cost of producinga good declining as more goods are produced) can arise due to:

- Learning effects: with individual workers getting more efficient atproducing as they produce more.

- Specialization:

* With a single worker, this may take the form of working on parts inbatches.

* With multiple employees, individual workers focus on only a part of theproduction process.

Increasing marginal costs (i.e., with the additional cost of producing agood increasing as more goods are produced) can arise due to:

- Fixed inputs: Limits on currently available equipment make it costly, ifnot impossible, to produce more.

- The gains from specialization have been exhausted and may in facthinder productivity.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 15 / 37

The Role of Marginal Analysis Marginal Cost

Increasing and Decreasing Marginal Costs

With John’s woodworking shop, we assumed that each additionalchair cost the same amount to produce.

Marginal costs, however, are often not constant.Decreasing marginal costs (i.e., with the additional cost of producinga good declining as more goods are produced) can arise due to:

- Learning effects: with individual workers getting more efficient atproducing as they produce more.

- Specialization:* With a single worker, this may take the form of working on parts in

batches.

* With multiple employees, individual workers focus on only a part of theproduction process.

Increasing marginal costs (i.e., with the additional cost of producing agood increasing as more goods are produced) can arise due to:

- Fixed inputs: Limits on currently available equipment make it costly, ifnot impossible, to produce more.

- The gains from specialization have been exhausted and may in facthinder productivity.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 15 / 37

The Role of Marginal Analysis Marginal Cost

Increasing and Decreasing Marginal Costs

With John’s woodworking shop, we assumed that each additionalchair cost the same amount to produce.

Marginal costs, however, are often not constant.Decreasing marginal costs (i.e., with the additional cost of producinga good declining as more goods are produced) can arise due to:

- Learning effects: with individual workers getting more efficient atproducing as they produce more.

- Specialization:* With a single worker, this may take the form of working on parts in

batches.* With multiple employees, individual workers focus on only a part of the

production process.

Increasing marginal costs (i.e., with the additional cost of producing agood increasing as more goods are produced) can arise due to:

- Fixed inputs: Limits on currently available equipment make it costly, ifnot impossible, to produce more.

- The gains from specialization have been exhausted and may in facthinder productivity.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 15 / 37

The Role of Marginal Analysis Marginal Cost

Increasing and Decreasing Marginal Costs

With John’s woodworking shop, we assumed that each additionalchair cost the same amount to produce.

Marginal costs, however, are often not constant.Decreasing marginal costs (i.e., with the additional cost of producinga good declining as more goods are produced) can arise due to:

- Learning effects: with individual workers getting more efficient atproducing as they produce more.

- Specialization:* With a single worker, this may take the form of working on parts in

batches.* With multiple employees, individual workers focus on only a part of the

production process.

Increasing marginal costs (i.e., with the additional cost of producing agood increasing as more goods are produced) can arise due to:

- Fixed inputs: Limits on currently available equipment make it costly, ifnot impossible, to produce more.

- The gains from specialization have been exhausted and may in facthinder productivity.

Herriges (ISU) Ch. 9: Making Decisions Fall 2010 15 / 37