ECO2704 Lecture Notes: Melitz Model - University of...

22

Introduction Closed Economy Model Open Economy Model Subsequent literature ECO2704 Lecture Notes: Melitz Model Xiaodong Zhu University of Toronto October 15, 2010 1 / 22

Transcript of ECO2704 Lecture Notes: Melitz Model - University of...

Introduction Closed Economy Model Open Economy Model Subsequent literature

ECO2704 Lecture Notes: Melitz Model

Xiaodong Zhu

University of Toronto

October 15, 2010

1 / 22

Introduction Closed Economy Model Open Economy Model Subsequent literature

• Dynamic Industry Model with heterogeneous firms whereopening to trade leads to reallocations of resources within anindustry

• Opening to trade leads to

• Reallocations of resources across firms• Low productivity firms exit• High productivity firms expand so there is a change in industry

composition• High productivity firms enter export markets• Improvements in aggregate industry productivity• No change in firm productivity

• Consistent with empirical evidence from trade liberalizations?

2 / 22

Introduction Closed Economy Model Open Economy Model Subsequent literature

The theoretical model is consistent with a variety of other stylizedfacts about industries

• Heterogeneous firm productivity

• Ongoing entry and exit

• Co-movement in (gross) entry and exit due to sunk entry costs• Exiting firms are low productivity (selection effect)

• Explains why some firms export within industries and others donot

• Contrast with traditional theories of comparative advantage• Exporting firms are high productivity (selection effect)• No feedback from exporting to productivity

3 / 22

Introduction Closed Economy Model Open Economy Model Subsequent literature

• Single factor: labor, numeraire, wage normalized to 1

• Firms enter market by paying sunk entry cost (fe )

• Firms observe their productivity (ϕ) from distribution G (ϕ)

• Productivity is fixed thereafter

• Once productivity is observed, firms decide whether to produceor exit

• Firms produce horizontally-dierentiated varieties, with a fixedproduction cost (fd ) and a variable cost that depends on theirproductivity

• Firms face an exogenous probability of death (δ) per perioddue to force majeure events

4 / 22

Introduction Closed Economy Model Open Economy Model Subsequent literature

Preferences and demand

Q =

[ˆ

k∈Ωq(k)

σ−1σ dk

]σ

σ−1

, σ > 1

Let R be the total expenditures of the representative consumer.Then,

q(k) =

(

p(k)

P

)

−σ

Q

r(k) = p(k)q(k) =

(

p(k)

P

)1−σ

R

Here p(k) is the price of variety k and P is the price index faced bythe consumer,

P =

[ˆ

k∈Ωp(k)1−σdk

]1

1−σ

5 / 22

Introduction Closed Economy Model Open Economy Model Subsequent literature

Technology

The amount of labour needed for a firm to produce q(k) units ofvariety k is

fd + q(k)/ϕ(k)

So the total cost of production is

fd + q(k)/ϕ(k)

and the marginal cost is1/ϕ(k)

All firms with the same productivity behave in exactly the sameway. So we will use productivity ϕ rather than variety k to identifya firm.

6 / 22

Introduction Closed Economy Model Open Economy Model Subsequent literature

Profit maximization

Each firm produces a differentiated variety (monopolisticcompetition):

π(ϕ) = maxq(ϕ) p(ϕ)q(ϕ) − fd + q(ϕ)/ϕ

Constant markup pricing:

p(ϕ) =σ

σ − 1ϕ−1 = (ρϕ)−1 (1)

which implies the following:

r(ϕ) = (ϕ)σ−1 Pσ−1R , q(ϕ) = [ϕ]σ Pσ−1R (2)

π(ϕ) =r(ϕ)

σ− fd (3)

7 / 22

Introduction Closed Economy Model Open Economy Model Subsequent literature

Entry and exitPrior to entry, a firm incurs a sunk cost of entry, fe .Upon entry, it draws a productivity ϕ randomly from a distributionG (.). The firm will stay in the market only if

π(ϕ) ≥ 0 or r(ϕ) ≥ σfd

Current value of firm ϕ is

v(ϕ) =

∞∑

t=0

(1 − δ)tmax π(ϕ), 0 = max

π(ϕ)

δ, 0

Let ϕ∗ be the cutoff productivity such that π(ϕ∗) = 0 andpin(ϕ

∗) = 1 − G (ϕ∗) the probability that a firm will stay. Then,productivity distribution of producing firms is given by the followingdensity function:

µ(ϕ) =

g(ϕ)pin(ϕ∗) if ϕ ≥ ϕ∗

0 otherwise(4)

8 / 22

Introduction Closed Economy Model Open Economy Model Subsequent literature

Equilibrium in a closed economy

A stationary equilibrium is a vector (ϕ∗,M ,Me,P ,R) of cutoffproductivity, mass of producing firms, mass of entrants, price level andaggregate expenditures such that price, revenue, quantity and profit foreach firm ϕ are given by equation (1) to (3), the distribution of producingfirms is given by µ(ϕ) in equation (4), and the following conditions hold:Zero profit condition:

π(ϕ∗) = 0

Free entry condition:

pin (ϕ∗)

ˆ

π(ϕ)

δµ(ϕ)dϕ = fe

Stationarity condition:pin (ϕ

∗)Me = δM

Market clearing condition:R = L

9 / 22

Introduction Closed Economy Model Open Economy Model Subsequent literature

Price index

P =

[ˆ

p(ϕ)1−σµ(ϕ)Mdϕ

]1

1−σ

P = M1/(1−σ)ρ−1

[ˆ

ϕσ−1µ(ϕ)dϕ

]

= M1/(1−σ) (ρϕ)−1 (5)

Here

ϕ =

[ˆ

ϕσ−1µ(ϕ)dϕ

]1

σ−1

is a weighted average of firm productivities.

10 / 22

Introduction Closed Economy Model Open Economy Model Subsequent literature

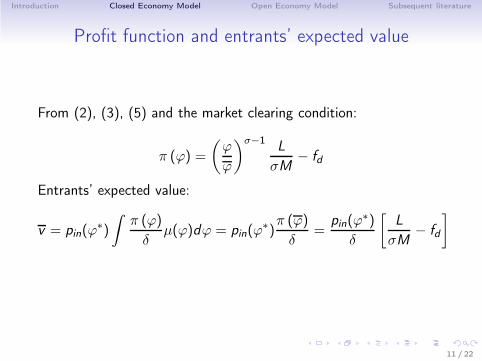

Profit function and entrants’ expected value

From (2), (3), (5) and the market clearing condition:

π (ϕ) =

(

ϕ

ϕ

)σ−1L

σM− fd

Entrants’ expected value:

v = pin(ϕ∗)

ˆ

π (ϕ)

δµ(ϕ)dϕ = pin(ϕ

∗)π (ϕ)

δ=

pin(ϕ∗)

δ

[

L

σM− fd

]

11 / 22

Introduction Closed Economy Model Open Economy Model Subsequent literature

Mass of producing firms

Zero profit condition=⇒

(

ϕ∗

ϕ

)σ−1L

σM= fd

Free entry condition =⇒

pin(ϕ∗)

δ

[

L

σM− fd

]

= fe (6)

Thus,[

(

ϕ∗

ϕ

)1−σ

− 1

]

fd =δfe

pin(ϕ∗)

12 / 22

Introduction Closed Economy Model Open Economy Model Subsequent literature

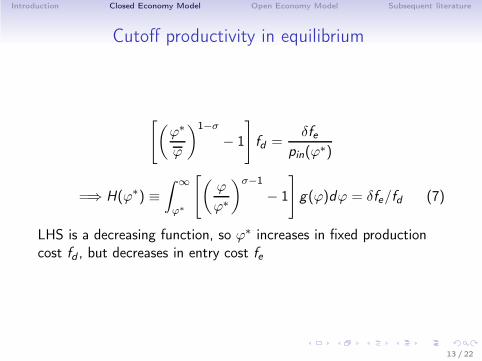

Cutoff productivity in equilibrium

[

(

ϕ∗

ϕ

)1−σ

− 1

]

fd =δfe

pin(ϕ∗)

=⇒ H(ϕ∗) ≡

ˆ

∞

ϕ∗

[

(

ϕ

ϕ∗

)σ−1

− 1

]

g(ϕ)dϕ = δfe/fd (7)

LHS is a decreasing function, so ϕ∗ increases in fixed productioncost fd , but decreases in entry cost fe

13 / 22

Introduction Closed Economy Model Open Economy Model Subsequent literature

Number of firms in equilibrium

From equation (6),

M =L

σ [fd + δfe/pin(ϕ∗)]

14 / 22

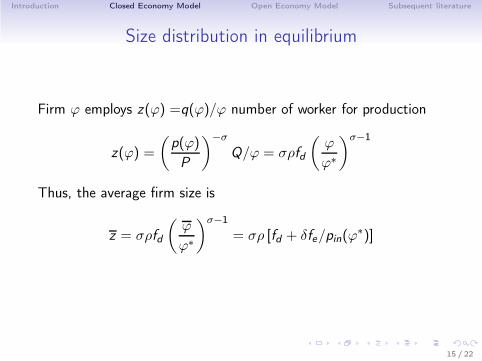

Introduction Closed Economy Model Open Economy Model Subsequent literature

Size distribution in equilibrium

Firm ϕ employs z(ϕ) =q(ϕ)/ϕ number of worker for production

z(ϕ) =

(

p(ϕ)

P

)

−σ

Q/ϕ = σρfd

(

ϕ

ϕ∗

)σ−1

Thus, the average firm size is

z = σρfd

(

ϕ

ϕ∗

)σ−1

= σρ [fd + δfe/pin(ϕ∗)]

15 / 22

Introduction Closed Economy Model Open Economy Model Subsequent literature

Properties of Closed Economy Equilibrium

• Increasing fixed production cost fd will

• raise average productivity• raise average firm size• but lower the number of producing firms

• Increasing sunk entry cost fe will

• lower average productivity• lower average firm size• and lower the number of producing firms

16 / 22

Introduction Closed Economy Model Open Economy Model Subsequent literature

• n + 1 identical countries, so identical wage, price level andincome across countries

• wage is normalized to 1

• To produce, a firm will first incur a fixed production cost fd

• If the firm decides to export, it will also incur a fixed exportcost fx

• Iceberg trade cost τ

17 / 22

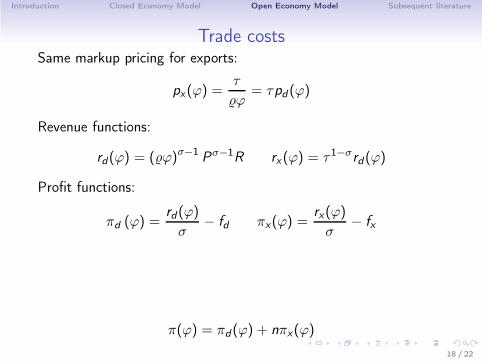

Introduction Closed Economy Model Open Economy Model Subsequent literature

Trade costsSame markup pricing for exports:

px(ϕ) =τ

ϕ= τpd (ϕ)

Revenue functions:

rd(ϕ) = (ϕ)σ−1 Pσ−1R rx(ϕ) = τ1−σrd (ϕ)

Profit functions:

πd (ϕ) =rd (ϕ)

σ− fd πx(ϕ) =

rx(ϕ)

σ− fx

π(ϕ) = πd (ϕ) + nπx(ϕ)

18 / 22

Introduction Closed Economy Model Open Economy Model Subsequent literature

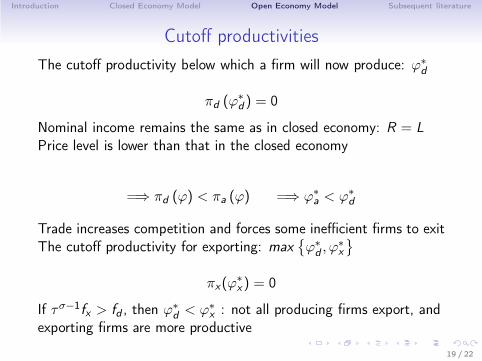

Cutoff productivities

The cutoff productivity below which a firm will now produce: ϕ∗

d

πd (ϕ∗

d ) = 0

Nominal income remains the same as in closed economy: R = L

Price level is lower than that in the closed economy

=⇒ πd (ϕ) < πa (ϕ) =⇒ ϕ∗

a < ϕ∗

d

Trade increases competition and forces some inefficient firms to exitThe cutoff productivity for exporting: max

ϕ∗

d , ϕ∗

x

πx(ϕ∗

x ) = 0

If τσ−1fx > fd , then ϕ∗

d < ϕ∗

x : not all producing firms export, andexporting firms are more productive

19 / 22

Introduction Closed Economy Model Open Economy Model Subsequent literature

Open economy results

• The opening of trade leads to:

• Rise in the zero profit cutoff productivity• Rise in average firm revenue and profit

• Low productivity firms between ϕ∗

a and ϕ∗

d exit

• Intermediate productivity firms betwen ϕ∗

d and ϕ∗

x contract

• Only firms with productivities greater than ϕ∗

x enter exportmarkets and expand

• All of the above lead to a change in industry composition thatraises aggregate industry productivity

20 / 22

Introduction Closed Economy Model Open Economy Model Subsequent literature

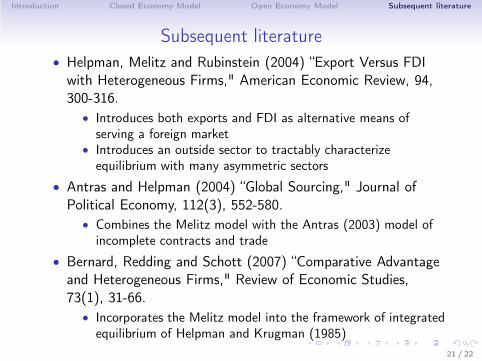

Subsequent literature

• Helpman, Melitz and Rubinstein (2004) “Export Versus FDIwith Heterogeneous Firms," American Economic Review, 94,300-316.

• Introduces both exports and FDI as alternative means ofserving a foreign market

• Introduces an outside sector to tractably characterizeequilibrium with many asymmetric sectors

• Antras and Helpman (2004) “Global Sourcing," Journal ofPolitical Economy, 112(3), 552-580.

• Combines the Melitz model with the Antras (2003) model ofincomplete contracts and trade

• Bernard, Redding and Schott (2007) “Comparative Advantageand Heterogeneous Firms," Review of Economic Studies,73(1), 31-66.

• Incorporates the Melitz model into the framework of integratedequilibrium of Helpman and Krugman (1985)

21 / 22

Introduction Closed Economy Model Open Economy Model Subsequent literature

Subsequent literature

• Chaney, Thomas (2008) “Distorted Gravity: the Intensive andExtensive Margins of International Trade," AmericanEconomic Review, September.

• Provides a simplified static version of the Melitz model withoutongoing firm entry and with an outside sector

• Examines the model’s implications for the extensive andintensive margins of international trade

• Arkolakis, Costas, Klenow, Peter, Demidova, Svetlana andAndres Rodriguez-Clare (2009) “The Gains from Trade withEndogenous Variety," American Economic Review, Papers andProceedings, 98 (4), 444-450.

• Solves the Chaney version of the model without an outsidesector

• Derives a sufficient statistic for welfare of the same form asthat in Eaton and Kortum (2002)

22 / 22