Eazy-E Life Story

57

VCE Accounting, Units 3&4 Study Design 2013-2016 Notes by Yakir Havin Class of 2014 Contents (control + click to jump to chapter) Chapter 1 – The nature of accounting...............................5 Chapter 2 – Balance sheets.........................................7 Chapter 3 – Analysing and designing accounting systems.............9 Chapter 4 – The double entry recording process....................12 Chapter 5 – Special journals: cash transactions...................14 Chapter 6 – credit sales and credit purchases journals............15 Chapter 7 – The general journal...................................17 Chapter 9 – The perpetual inventory system........................18 Chapter 10 – Closing the general ledger...........................20 Chapter 11 – Income statements....................................21 Chapter 12 – Cash flow statements.................................22 Chapter 13 – Depreciation of non-current assets...................23 Chapter 14 – Profit determination and balance day adjustments.....24 Chapter 15 – Sales returns and purchases returns..................25 Chapter 16 – The reducing balance methods of depreciation.........27 Chapter 17 – Buying and selling non-current assets................28 Chapter 18 – Inventory valuation..................................29 Chapter 19 – Balance day adjustments: repaid revenue and accrued revenue...........................................................30 Chapter 20 – Managing and controlling debtors, creditors and stock 31 Chapter 21 – Budgeting: planning for the future...................34 Chapter 22 – Analysis and interpretation of accounting reports....36

description

Eazy-E

Transcript of Eazy-E Life Story

VCE Accounting, Units 3&4Study Design 2013-2016

Notes by Yakir HavinClass of 2014

Contents (control + click to jump to chapter)

Chapter 1 – The nature of accounting...................................................................................................5

Chapter 2 – Balance sheets...................................................................................................................7

Chapter 3 – Analysing and designing accounting systems.....................................................................9

Chapter 4 – The double entry recording process.................................................................................12

Chapter 5 – Special journals: cash transactions...................................................................................14

Chapter 6 – credit sales and credit purchases journals.......................................................................15

Chapter 7 – The general journal..........................................................................................................17

Chapter 9 – The perpetual inventory system......................................................................................18

Chapter 10 – Closing the general ledger..............................................................................................20

Chapter 11 – Income statements........................................................................................................21

Chapter 12 – Cash flow statements.....................................................................................................22

Chapter 13 – Depreciation of non-current assets................................................................................23

Chapter 14 – Profit determination and balance day adjustments.......................................................24

Chapter 15 – Sales returns and purchases returns..............................................................................25

Chapter 16 – The reducing balance methods of depreciation.............................................................27

Chapter 17 – Buying and selling non-current assets............................................................................28

Chapter 18 – Inventory valuation........................................................................................................29

Chapter 19 – Balance day adjustments: repaid revenue and accrued revenue...................................30

Chapter 20 – Managing and controlling debtors, creditors and stock.................................................31

Chapter 21 – Budgeting: planning for the future.................................................................................34

Chapter 22 – Analysis and interpretation of accounting reports.........................................................36

Yakir Havin

Chapter 1 – The nature of accounting

The uses of financial information

Main users of accounting information and their areas of interest: Owner/manager: profit, liquidity, stability, sales, growth, budgets, stock management,

debtors, creditors, rates of return. Prospective owners: budgets, future earnings, predicted returns, stability, prospects of

growth. Banks/ledgers: liquidity, stability, budgets. Suppliers of good or materials: credit rating, reliability, stability. Government departments: e.g. Taxation Department, Bureau of Statistics, Small Business

Victoria (needs are specific according to their own specialist areas). Employees/unions: stability of employment, profits, likelihood of wage increases. Customers: pricing, credit facilities, future trading opportunities.

Statements of accounting concepts

SAC1: Definition of the reporting entitySAC2: Objective of general purpose financial reporting

SAC2: Objective of general purpose financial reportingQualitative characteristics

Relevance: all information that may influence the users of a report must be disclosed so that decision-makers are fully informed.- Materiality is the test of whether something is worth reporting or not. If the item has no

or little effect on decision-making, it is not considered an asset, and its purchase is rather written off as an expense.

Reliability: the need to be able to check and verify accounting information against business documents to improve accuracy and prevent bias.

Comparability: financial reports are prepared in a consistent manner so that they may be compared from one reporting period to the next.

Understandability: accounting information is presented in a simplified, understandable fashion so that those without accounting training may be able to understand reports.

Assets are resources controlled by the entity as a result of past events and from which future economic benefits are expected to flow to the entity.

Liabilities are present obligations of the entity arising from past events, the settlement of which is expected to result in an outflow from the entity of resources embodying economic benefits.

2

Yakir Havin

Owner’s equity is the residual interest in the assets of the entity after deduction of its liabilities.

Revenues are increases in economic benefits during the reporting period in the form of inflows or enhancements of assets or decreases in liabilities that result in increases in equity, other than those relating to contributions from the owner.

Expenses are decreases in economic benefits during the reporting period in the form of outflows or depletions of assets or incurrences of liabilities that result in decreases in equity, other than those relating to distributions to equity participants.

Accounting principles

Consistency: accounting methods used must be applied consistently from one reporting period to another.

Historical cost: transactions are recorded at their original cost price, as verified by source documents.

Entity: the personal transactions of the owner(s) should be kept separate from those of the business, to ensure easy evaluation of business performance.

Reporting period: the continuous life of the business is divided into equal periods of time for the purpose of the preparation of reports in order to show the performance of the business (e.g. profit and loss).

Monetary unit: the unit of currency used in all accounting reports must be that of the country in which the report is being prepared.

Conservatism: a tendency to be cautious when preparing reports. Losses should be recorded when probable and profits when they are earned.

Going concern: deems that a business will continue as a going concern for an indefinite period.

Relevance is supported by the Entity and Reporting Period principles.Comparability is supported by the Consistency principle.

3

Yakir Havin

Chapter 2 – Balance sheets

Balance sheet

Assets are the resources controlled by an entity that have future economic benefits as a result of past transactions.

Liabilities are present obligations of an entity that will result in an outflow of resources in the future.

Owner’s equity is the residual interest in the assets of the entity after deduction of its liabilities. Also referred to as the net worth of the business.

Assets = Liabilities + Owner’s equity Owner’s equity = Assets – Liabilities

Equities describe anyone who has a legal claim on assets of the business. Liabilities include all external equities, as these are obligations to outsiders of the business. The internal equity is the owner’s claim on the firm. This is the net worth of the business of the proprietor.

There are two formats of a Balance Sheet: T-form presentation Narrative presentation

Classification in the balance sheet

Current assets are economic resources controlled by the entity, which are normally expected or intended to be turned into cash or used up in the next 12 months. E.g. cash on hand, cash at bank, short-term investments, the goods held for re-sale, stocks of supplies and amounts owing by credit customers.

Non-current assets are usually acquired with the intention of controlling them for a period of time greater than 12 months for the purpose of generating income for business. E.g. computers, vehicles, machinery, furniture, equipment, property and long-term investments.

Current liabilities include obligations of economic sacrifices due for payment within the next 12 months. E.g. bank overdrafts, short-term loans and amount owing to suppliers who have extended credit to the business.

Non-current liabilities are debts for which payment has been deferred over a period greater than 12 months. E.g. long-term loans.

4

Yakir Havin

Classification of loans

Interest-only loans do not require the principal of the loan to be repaid until the loan period has expired. That is, only the interest due is paid to the lender each year until the loan period has expired.

Characteristics: Gives owner time to accumulate the amount borrowed before having to make the single

repayment of the principal. Requires excellent planning skills, as the total amount borrowed has to be available on the

day the loan period expires. Classification is non-current liability as they do not involve an obligation for payment within

the next 12 months.

Instalment loans require the borrower to make scheduled repayments throughout the life of the loan. These amounts are usually stated as a dollar amount per month or per quarter.

Characteristics: Allows a business owner to avoid having to make one lump sum payment. Must be repaid constantly throughout the loan period and may therefore put a business

under steady pressure for several reporting periods. Classification is current liability for the instalment amounts owing within the next 12 months

and non-current liability for the remainder that is due at a time after 12 months.

Financial transactions and balance sheets

Revenues are the increases in economic benefit in the form of inflows of assets or reductions in liabilities that result in an increase in equity, other than contribution of capital by the owner.

Expenses are the decreases in economic benefits in the form of reduction in assets or increases in liabilities that result in a decrease in equity, other than distributions of equity (drawings).

Under the accrual accounting method of determining profit, revenue earned less expenses incurred equals the net profit for a period.

GST liability is an obligation owing of a business to the taxation office because the business has collected (charged) more GST than it has paid to its suppliers.

GST refund is an amount owing to a business from the taxation office because the business has paid (been charged) more GST than it has collected from its customers.

5

Yakir Havin

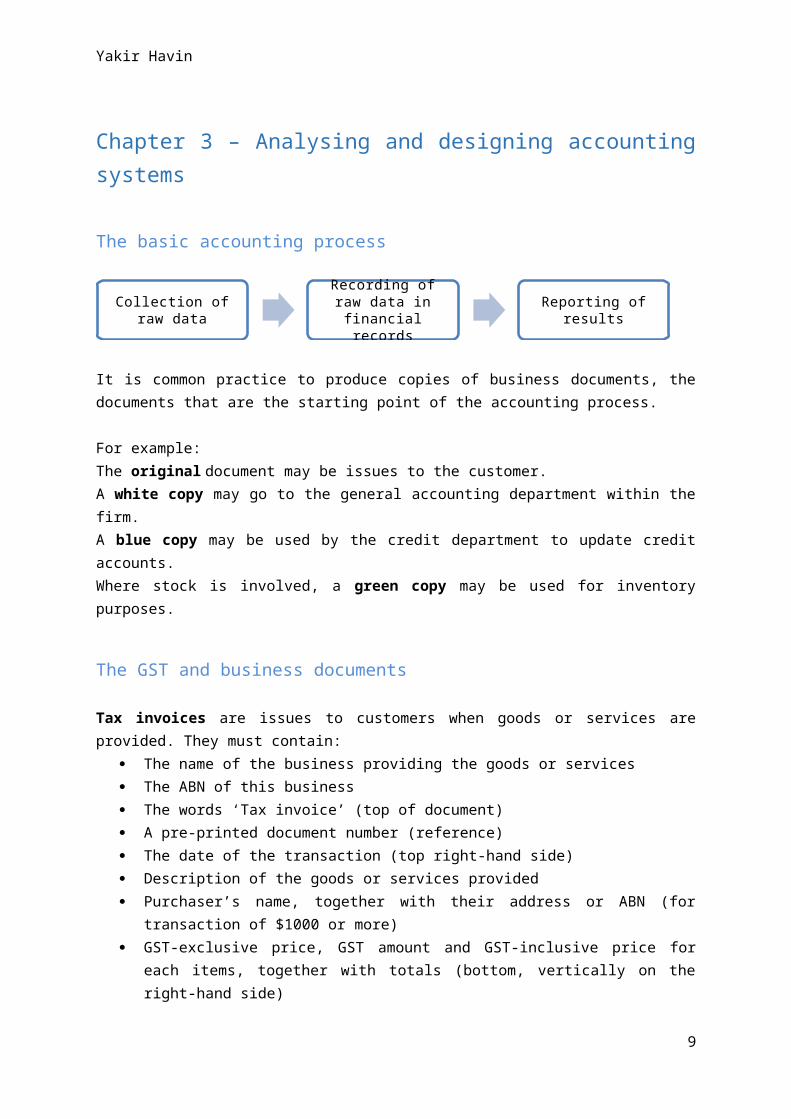

Chapter 3 – Analysing and designing accounting systems

The basic accounting process

It is common practice to produce copies of business documents, the documents that are the starting point of the accounting process.

For example:The original document may be issues to the customer.A white copy may go to the general accounting department within the firm.A blue copy may be used by the credit department to update credit accounts.Where stock is involved, a green copy may be used for inventory purposes.

The GST and business documents

Tax invoices are issues to customers when goods or services are provided. They must contain: The name of the business providing the goods or services The ABN of this business The words ‘Tax invoice’ (top of document) A pre-printed document number (reference) The date of the transaction (top right-hand side) Description of the goods or services provided Purchaser’s name, together with their address or ABN (for transaction of $1000 or more) GST-exclusive price, GST amount and GST-inclusive price for each items, together with totals

(bottom, vertically on the right-hand side)

For cash sales or transactions, the words ‘Cash receipt’ can be printed next to ‘Tax invoice’, and the credit terms are removed. The inclusion of the words ‘Tax invoice’ do not guarantee that the transaction was of a credit nature.

General business documents: cash transactions

For cash inflows, a cash receipt is used to evidence the transaction. A receipt should be issued to the customer and a copy kept by the firm.

6

Collection of raw data Recording of raw data in financial records Reporting of results

Yakir Havin

It is common practice to make all cash payments by cheque. The details of the cheque should be copied on to the cheque butt, which acts as a copy of the original cheque.

Business documents: credit transactions

When goods are purchased on credit an invoice is used to communicate the cost of the good supplied. Therefore invoices can be both received and issued by firms dealing on credit. The business/customer making the purchase always receives the original document while the supplier keeps a copy.

Memorandums for internal transactions

Internal transactions are transactions that only affect the business and its owner, not involving another business entity or individual. E.g. capital and drawings (receipt and cashed cheque).

However, for withdrawals of stock (as donations for advertising purposes), memorandums, or memos are used. Memos must also suit the needs of the reliability characteristic.

Statements of account

A statement of account is used to summarise the transactions involving a credit customer over a given period. Common practice is to issue these monthly. A statement of account includes a running balance after each transaction, as well as other basic transactional details (i.e. date, description etc.).

Other business documents

Order forms for requests from suppliers (not a financial transaction yet) Cash registers rolls Delivery dockets Employee pay slips Bank statements

Information flows: an overview of the accounting system

1) Source documents are the original documents of accounting data.2) Journals are used on a daily basis to record the details of the data in the source documents.3) Ledgers are used to record the details of a particular item/account (this is where double

entry occurs).4) Trial balance is a summary of the closed/footed ledgers listed in debit and credit total

columns. The purpose is to check that the double entry procedure has been carried out correctly.

7

Yakir Havin

5) Balance day adjustments adjust revenue and expense accounts so that they equal revenue earned and expenses incurred (under the accrual accounting method).

6) Accounting reports provide the owner/s with the results of the period’s activities.7) Evaluations of reports include profitability, liquidity, efficiency and financial stability.8) Planning for the future involves decision-making in response to the current period’s results.

This may include cash budgets and budgeted income statements.

Manual versus computerised accounting systems

The accounting process (computerised system)

Advantages: Computer systems can process data at more rapid rates. Information is free from human error (input and calculation).

Disadvantages: Computer systems cost money and their purchase must be calculated before being

undertaken. Employees are required to have specific skills before using computer systems.

8

source documents journals ledgers trial balance

planning for the future

evaluation of reports

accounting reports

balance day adjustments

Collection of raw data Data input

Processing of data by

computer package

Output of information

(reports)

Yakir Havin

Chapter 4 – The double entry recording process

Double entry accounting: an introduction

A ledger account is a financial record that relates to a particular item within the business. There are three parts to an entry in a ledger account: the date, a cross-reference, and an amount.

Assets appear on the left side of the ledger and are debit in nature. Liabilities and owner’s equity are on the right side of the ledger and are credit in nature. Therefore, assets are decreased with credits, while liabilities and owner’s equity are decreased with debits.

Double entry for revenue and expenses

As revenue increases owner’s equity, a revenue ledger account will be the same in nature as owner’s equity (credit in nature). Expenses have the opposite effect on owner’s equity and are therefore debit in their nature.

The role of the trial balance

A trial balance is a summary of the closed/footed ledgers listed in debit and credit total columns. The purpose is to check that the double entry procedure has been carried out correctly and accurately, and to detect input errors made in the ledgers.

Undetectable errors: Entering an incorrect amount for both the debit and credit Entering a debit or credit in the wrong account The debit and credit entries are reversed Omitting a transaction completely Compensating errors

None of the above errors will be detected in the trial balance as the debit and credit figures will balance, albeit with the wrong amounts.

Detecting errors through a trial balance

Detectable errors: Debit or credit omitted Duplication of a debit or credit Transposing errors

9

Yakir Havin

Accounting for drawings

Drawings occur when the proprietor of the business withdraws assets for personal use. Classification is owner’s equity but is the opposite of capital. As capital is credit in its nature, drawings, is debit in nature.

10

Yakir Havin

Chapter 5 – Special journals: cash transactions

The role of special journals

Journals provide the first form of classification in a double entry accounting system. Special journals are used to group transactions of a similar nature to make posting to ledger accounts easier.

Recording in the cash receipts journal

Advantage of multi-column cash receipts journal: A cross check may be made of the entries in a CRJ to ensure that recording errors have not

been made. Excluding Cost of Sales, the columns are totalled and checked that they equal the total Bank figure. If Discount expense applies, this is deducted. This is usually done before posting to a ledger account.

Recording cash discounts for debtors and creditors

Credit terms ‘2/7: n/30’ indicate that a 2% discount is available as a cash discount if the invoice is settled within 7 days. If the customer does not take advantage of this cash discount period, the net amount is due for payment within 30 days.

Credit customers are offered a cash discount as an incentive for early payment because: If debtors pay early the likelihood of bad debts is reduced. The early receipt of cash allows a business to pay for inventory purchases at an earlier time,

thus taking advantage of any cash discounts available from suppliers. It helps a business reduce time taken by debtors to settle their accounts, thus improving the

firm’s liquidity. Cash received earlier may be used to reduce other debts of the business.

11

Source documents Journals Ledger accounts

Yakir Havin

Chapter 6 – credit sales and credit purchases journals

Credit transactions

Characteristics: Applies to supplier–business and business–customer. Used to attract more customers and increase revenue. May be necessary when dealing with other businesses. Stock can be bought on credit and then sold while the business hasn’t paid the supplier.

The need for control accounts

Control accounts are used to summarise all the debtors and creditors subsidiary accounts (as well as transactions of stock). The control account saves time as one does not need to add all the subsidiary accounts when finding the total. Also, the control account acts as a checking mechanism, to ensure that it equals all the subsidiary accounts. Control accounts reduce the bulky detail contained in subsidiary ledgers and help reduce the threat of fraud (when recording duties are separated). Control accounts help maintain accuracy of debtors and creditors transactions. Control accounts are not relevant for all businesses as it depends on the firm’s needs. If a business does not trade on a credit basis, debtor and creditor control accounts are deemed unnecessary, as are subsidiary accounts, as the business will possess no debtors or creditors. Also, control accounts may need additional staff and new computer systems, thus their use needs to be weighed up.

Debtors schedules

A debtors schedule is a listing of the balances of individual debtors’ account in the subsidiary ledger. The total of this listing is then checked against the balance of the debtors control account in the general ledger. The purpose of this is to identify recording errors in one or both ledgers.

Creditors schedules

To reconcile the creditors’ subsidiary ledgers, a creditors schedule is made, listing all creditors with the amount owing to them at a particular date.

Advantages and disadvantages of control accounts

Advantages: Bulky details is removed from the general ledger. Trial balance figures provide a summary of total figures, rather than individual accounts. In larger businesses, accounting departments can be set up to cater for specific areas.

12

Yakir Havin

Control accounts provide a checking mechanism to detect recording errors. Control accounts assist in enforcing internal control procedures over staff and may therefore

reduce the likelihood of fraud.

Disadvantages: Control accounts are not suited to all business and can create unnecessary work in terms of

accounting records. Additional staff may have to be hired. A computerised system may be introduced.

13

Yakir Havin

Chapter 7 – The general journal

The need for a general journal

Contributions and drawings of stock or non-current assets by the owner are not covered by the special journals and are instead entered into the general journal. The general journal is also used for error corrections. An additional entry is made instead of removing the erroneous entry to reduce the chance of fraud.

Recording the contribution or withdrawal of assets by an owner

Whenever an owner puts an asset into a business, the particular asset must be debited and capital credited. For a withdrawal, the opposite occurs.

Using agreed value for assets

When an owner contributes a non-current asset to the business, an estimate of the asset’s worth based on current market value is made – as the asset has depreciated since its original purchase – and this figure becomes the agreed value henceforth. The original amount that the owner paid has no relevance to the business. This system does not satisfy the demands of reliability (no source document). However, relevance takes precedence here for the estimation of the asset’s worth to the business at the time of contribution, as this is the amount that affects decision making. Historical cost of the asset is not used here and conservatism is applied as to the worth of the contributed asset.

Donations of stock and business advertising

When a business donates stock for advertising purposes, this transaction is not recorded as drawings but rather as an advertising expense. However, there is no cash flow involved. Rather, the business has suffered a loss of economic resources, leading to a decrease in equity.

Accounting for bad debts

When a debtor cannot complete a payment, the outstanding debt is written off as a bad debt, resulting in a credit to debtor control and a debit to a new account, bad debts. Debtors may sometimes may be forced to pay [xx] cents in the dollar instead of the full amount.

14

Yakir Havin

Chapter 9 – The perpetual inventory system

What is inventory?

Inventory is defined as stock or merchandise that has been purchased for the purpose of resale to generate a profit. This does not include non-current assets.

What is perpetual inventory?

Control and monitoring of stock is vital towards business success. The perpetual inventory system helps to accurately record the inflows and outflows of stock. It record the stock item, quantity, cost price and balance of a type of stock.

Advantages: Greater control over stock is possible as up-to-date information is available throughout the

reporting period. Slow-moving and fast-moving lines of inventory can be identified. Reordering of inventory is more efficient. Interim profit reports can be prepared without doing a stocktake. The level of stock losses or gains is measured.

Disadvantages: Additional record keeping is involved because inventory balances must be continuously

updated. Additional costs may be incurred due to the additional record keeping. The need for a physical stocktake at the end of a reporting period is not eliminated.

Fixed mark-up systems

Cost price = selling price × 100100 + mark up

First in, first out stock valuation

FIFO is the assumption that the oldest cost price of inventory on hand is the cost price for inventory sold at any given time. This assumption also applies to stock losses. FIFO is used as it can be impossible to identify the cost price of each stock item, and to satisfy the demands of perpetual inventory, it is more a more efficient method of cost allocation than identified cost.

15

Yakir Havin

The role of stock cards

Stock cards include: Name (or description) of an item Product code number (if applicable) Name of the supplier Location of the item Minimum or maximum to be in stock (for reordering purposes) Valuation method used (e.g. FIFO) All purchases and sales in relation to the particular product

Stock cards and the general ledger

The stock control ledger account and the stock cards can be checked against each other at the end of a reporting period as a control mechanism.

Stock losses and stock gains

Stock losses are caused by: Undersupply by suppliers. Oversupply to customers. Theft. Recording errors in stock cards. Duplicate invoices issued by a supplier. Stocktaking errors.

Stock gains are caused by: Oversupply by suppliers. Undersupply to customers. Recording errors in stock cards. Stocktaking errors.

Adjusting for a stock gain

When an adjustment is made in a stock card to account for a stock gain, the lowest cost price of inventory on hand is used to comply with conservatism.

16

Yakir Havin

Chapter 10 – Closing the general ledger

The closing of the general ledger

Revenue, expense and drawings accounts are closed off at the end of reporting periods: To determine profit earned in the period. To prepare the ledger accounts for the new period (zero balances).

The profit and loss (P&L) summary account

The P&L summary account is a temporary ledger account used to find the net profit or loss of a firm during a reporting period and to close off revenue and expense accounts. The differential is posted to the capital account as a net profit or loss.

The general journal and closing entries

Before closing off accounts in the general ledger, the ‘particulars’ should be recorded in the general journal for:

Closing entries (for revenue and expenses separately). Transfer of net profit. Transfer of owner’s drawings.

17

Yakir Havin

Chapter 11 – Income statements

The income statement

The income statement reports the revenues and expenses of a firm during a reporting period to determine a net profit or loss figure. This report is produced to satisfy the needs of understandability as many would not be familiar with the workings of a double entry system (i.e. seeing the net profit/loss figure in the general journal).

Evaluating a net profit figure

Comparing the profit earned in the current period with that earned in previous periods. Checking that the profit earned in the current period meets with budgeted expectations. Comparing the profit earned in the current period against industry averages. Evaluating using analytical ratios (gross profit ratio, net profit ratio, etc.).

Cost of goods sold and gross profit

Cost of goods sold includes any expenses incurred in the purchasing of stock and preparing it for sale. This may include, but are not limited to:

Cost of sales Cartage inwards Buying expenses Customs duty Import expenses Packaging expenses

Reporting discounts

Discount revenue, interest revenue, commission revenue and other forms of non-sales revenue fall under the category of other revenues in the Income Statement. Discount expenses and the like fall under other expenses.

18

Yakir Havin

Chapter 12 – Cash flow statements

The role of the cash flow statement

The Cash Flow Statement (CFS) completes a set of the important accounting reports along with the Income Statement and Balance Sheet. It provides streamlined information relating to cash flows in and out of the business during a given reporting period.

Classification of cash flows

Operating activities: cash sales, collections from debtors, GST paid/collected, etc. Investing activities: purchase or sale of non-current assets (for cash). Financing activities: capital contribution, loans, loan repayments and drawings.

Cash flows and decision-making

Cash Flow Statements provide management with information that demonstrates the effects of its decision-making on the cash resources of the firm. Therefore, statements for consecutive reporting periods are often prepared within the one report to highlight changes that have occurred.

Cash versus profit

Cash and profit are not necessarily the same thing. Cash movements are reported in the cash flow statement in order to determine the firm’s net cash position, while revenues and expenses are reported in the income statement to determine an accurate profit figure. While some revenues and expenses may be earned or incurred in the form of cash movements, this is not always true. For example, while credit sales may be a contributing factor to a net profit, there is no cash inflow involved which may leave the cash flow statement in a net cash decrease. Conversely, capital contributions improve the firm’s cash position but have no effect on the net profit. Thus it is evident that a firm can have a net cash decrease/increase while also having a net profit/loss.

19

Yakir Havin

Chapter 13 – Depreciation of non-current assets

The meaning of depreciation

Depreciation is the allocation of the cost of a non-current asset over its effective working life (when it makes revenue for the firm). The revenue earned by an asset should be considered in the same period as depreciation expense is recognised to satisfy accrual accounting’s method of profit determination.

The meaning of cost

The historical cost of the asset All other once-off costs incurred to get the asset into a revenue-earning capacity

Straight-line method of depreciation

Depreciation expense=Cost of asset−Scrap valueUseful life( years)

The adjusting entry for depreciation

Debit: Depreciation of [asset] accountCredit: Accumulated depreciation of [asset]Narration: Adjusting entry for depreciation of [asset] at [rate/amount] per annum

Depreciation and the balance sheet

Accumulated depreciation is reported as a negative asset and detracts from the asset’s value to create a book value or carrying value. This is the worth of the asset to the firm after depreciation has been allocated and accumulated (or not yet depreciated), and is not a market value estimate.

Depreciation: relevance and reliability

Depreciation must be recorded as it is relevant to decision making as it decreases an asset’s worth, and increases the accumulated depreciation negative asset. However, depreciation value is based on estimates and therefore does not satisfy reliability. Relevance takes precedence here.

20

Yakir Havin

Chapter 14 – Profit determination and balance day adjustments

Profit determination: underlying assumptions

The going concern principle assumes that the business will continue to operate as a going concern for an indefinite period into the future. This allows for reporting of non-current elements that are expected to have a future effect on the business.

The reporting period principle divides the indefinite life of the business into arbitrary periods of time for the preparation of reports, determination of profit and evaluation of the business.

The relevance characteristic demands that accounting information relevant to decision making be included in business reports in order to calculate an accurate profit or loss figure. Based on accrual accounting, profit is determined by deducting expenses incurred from revenues earned in a given reporting period, not taking into account when payments are actually made.

Accrual accounting and balance day adjustments

Balance day adjustments have the function of adjusting the balances of revenue and expense accounts to match revenue earned and expenses incurred in the reporting period. Adjusting entries make revenue and expense accounts equal respective earned and incurred amounts. Closing entries close off the adjusted revenue and expense accounts to the P&L summary account.

Prepaid expenses

Prepaid expenses are expenses that are paid for in a period prior to the benefit thereof being consumed. Prepaid expenses are current assets and are adjusted to become expenses when the benefit is consumed by the business.

Accrued expenses

Accrued expenses are expenses whose benefit has been consumed before payment has been made. Accrued expenses are current liabilities and the (consumed) expense components are adjusted to respective expense accounts on balance day.

21

Yakir Havin

Chapter 15 – Sales returns and purchases returns

Credit notes for returns

A firm that purchases and sells stock on credit may have good retuned to the supplier or the customer because:

Goods and damaged or faulty Wrong size, type, brand or colour Late delivery and no longer required

When good are returned, a credit note may be issued as acknowledgement of a return. Credit notes are considered a form of source document. They typically include:

The firm that issued the credit note The firm that received the credit note Description, quantity, total and GST Date and credit note number

Purchases returns

When a firm returns goods that were bought on credit to its supplier, this is a purchases return. When a purchases return occurs, four accounts in the books of the firm are affected:

Creditors control (debit) Subsidiary creditor (debit) Stock control (credit) GST clearing (credit)

This transaction is recorded in the general journal and it does not fit into any of the special journals.

Sales returns

When a customer returns goods that were bought on credit to a firm, this is a sales returns from the perspective of the firm. The following six accounts are affected:

Sales returns (debit) GST clearing (debit) Debtor control (credit) Subsidiary debtor (credit) Stock control (debit) Cost of sales (credit)

Sales returns totals at the end of the period are deducted from sales in the income statement. Sales returns have their own account so that management can analyse trends in goods that have been returned which may indicate poor stock quality. A firm may choose a new supplier for this line of stock or remove it altogether.

22

Yakir Havin

Recording purchases returns in stock cards

Purchases returns have nothing to do with the FIFO assumption. This is because the supplier will always determine what credit will be allowed for the returned goods. Therefore, the actual value of any value of credit allowed will be identified by the supplier and evidenced by the credit note issued.

Recording sales returns in stock cards

The value of a sales return is the value of the sale that was originally made. However, the cost of sales for the return may not always be easily identified. Here, the cost price of the most recent sale of that item is considered the cost price of the goods being returned. This is, in effect, a reverse of the FIFO assumption.

23

Yakir Havin

Chapter 16 – The reducing balance methods of depreciation

The need for an alternative method of depreciation

Depreciation is the allocation of a cost of a non-current asset over its useful working life. This is an expense charged against the revenue earning capacity of the asset, so as to satisfy the demands of relevance and the reporting period principle. This is because matching all revenues earned with all expenses incurred will result in an accurate profit figure.

As some assets are not expected to earn a fixed amount of revenue throughout their working lives, depreciation must be allocated accordingly. This is where the reducing balance method (RBM) comes in.

The reducing balance method of depreciation

Assets that typically earn more revenue in the earlier years of their working lives than in the later years. This may be because certain assets require maintenance after a time or because they get superseded by newer models. Reducing balance depreciation allocates increasingly less depreciation throughout the asset’s life. The depreciation is calculated from the carrying value, as opposed to its historical cost, and as the carrying value decreases with each depreciation, so too does each depreciation amount.

Depreciation methods: which one to use?

To satisfy relevance and reporting period, depreciation allocated must match the asset’s revenue earning capacity. In this way, the asset’s carrying value decreases at a similar rate as the revenue that it is expected to earn, and accrual accounting is thus followed. Under the stipulations of relevance, depreciation should always be allocated as it will affect decision making.

While there are no clear cut rules to selecting a depreciation method, assets that typically earn a fixed revenue (furniture, shop fittings, etc.) should be depreciated using the straight-line method (SLM). Conversely, assets that generally earn more revenue earlier on should be depreciated using the reducing balance method.

Whichever method is chosen, it is important that the method remains the same in order that consistency be followed, and to maintain comparability between reports.

24

Yakir Havin

Chapter 17 – Buying and selling non-current assets

Recording credit purchases on non-current assets

These purchases are recorded in the general journal, as the credit purchases journal is designated for stock. If an asset is bought for cash, this should be recorded in the cash payments journal. Credit purchases, however, do not affect creditors control or creditors’ subsidiary ledgers whatsoever, as no stock purchase is involved. Rather, a sundry creditor account is made for the supplier of the asset.

Disposal of non-current assets

The four necessary steps to records to disposal of an asset for cash:1. Transfer the historical cost to the disposal of asset account.2. Transfer the accumulated depreciation to the disposal of asset account.3. Record the proceeds from the sale in the disposal of asset account.4. Close off disposal of asset account by recording profit/loss on the sale of the asset.

If a profit was made on the disposal of an asset, this means that the depreciation was too high, over-depreciation. If there was a loss made, this means that the depreciation was too low, under-depreciation. Other factors may include incorrect residual value or useful life, the asset is no longer popular or in demand, the asset has become technologically obsolete, or it may be damaged. These mistakes are expected as depreciation is based on estimates and does not satisfy reliability.

Profit on disposal of an asset is reported under other revenue as it is not earned in the normal course of business trading, while a loss is simply reported under other expenses.

Trading in non-current assets

Instead of being disposed of for cash, assets can be traded in on newer models. This reduces the amount owing to the sundry creditor for the new asset being purchased. Recording this is the same as disposing of an asset, except that instead of making a cash receipts entry, the trade-in allowance for the old asset is deducted from the sundry creditor account, and this is first recorded in the general journal.

25

Yakir Havin

Chapter 18 – Inventory valuation

Product costs versus period costs

The cost of inventory refers to the purchase price plus other costs involved in getting the inventory into a selling position. If costs related to the stock can be divided equally/directly related per stock item, then we check if the amount per item is considered material – of enough value to affect decision making and therefore warrant reporting (part of relevance). If the amount is indeed material, then this cost is a product cost and is added to the cost of the stock itself.

However, if the cost cannot be directly attributed to each stock item, or does not divide equally (e.g. $100 delivery cost for 10 chairs, 20 tables, 25 stools) and/or is not material, then this cost is written off as a period cost and is reported in that period’s income statement under other expenses.

Lower of cost and net realisable value

While inventory is generally recorded at cost price, there is an exception when the expected selling price of an item is less than its cost price. Net realisable value (NRV) is defined as the selling price less any costs incurred in the marketing, selling, and distribution of the item. The lower option of cost price or NRV is selected and recorded as the value of the inventory. This is due to conservatism, which calls on accountants to be prudent in recognising losses when they are expected, and gains only when realised, and as the stock sale will incur a loss, this is recorded in the stock write-down.

Possible reasons that an NRV will be lower than cost prices: Item has been superseder by a newer model Item has become obsolete, possibly through technological advancements Out of season or fashion Damaged Shop-soiled Being deliberately sold below cost to attract customers

If the value of stock is written down due to recording at NRV, a stock write-down must be recorded in the general journal and stock card, before being transferred to the general ledger and so on. The disclosure of stock write-downs are necessary under relevance, as lowering the value of stock will affect decision making.

26

Yakir Havin

Chapter 19 – Balance day adjustments: repaid revenue and accrued revenue

What is revenue earned for a period?

Under accrual accounting, revenues earned and expenses incurred are matched per period to determine profit. Besides for prepaid and accrued expenses, there are times when a firm will be paid for a service/goods it has not yet provided (prepaid revenue), or earns revenue before being paid (accrued revenue). These also fall under the category of balance day adjustments, and accrual accounting demands that these be reported for the period in which they were earned.

Prepaid revenue (the liability approach)

If a firm is paid and has not yet earned the revenue, this should be recorded as a prepaid revenue which is classified as a current liability as it is a resource controlled by the business as a result of past transaction (the receipt of cash) and is expected to result in an outflow of economic resources (the service/goods) within the next 12 months. In this way, the revenue will only be reported during the period in which the expenses relating to earning the revenue are incurred, thus making the match as stipulated by accrual accounting.

Accrued revenue (revenue owing)

If the revenue earning process has been completed, this revenue must be recorded during the period as it has been earned, even if it has not necessarily been paid for. Accrued revenue is classified as a current liability as it is a resource controlled by the business as a result of a past transaction (provision of service/goods) that is expected to result in an inflow of economic resources (cash) within the next 12 months. Sometimes when a firm is owed cash for a provision of service or goods, it will be paid a larger amount including payment for new service or goods in the new period. Here, the cash receipt should be split up as payment for the accrued revenue and as new revenue.

27

Yakir Havin

Chapter 20 – Managing and controlling debtors, creditors and stock

Controlling inventory

Buying and selling of stock is the lifeblood of the firm. Questions management may face daily are: What goods should be buy? How many and which size should we purchase? What brand and colour should be stocked?

Steps to take to ensure enhanced control of stock:1. Setting minimum and maximum levels of inventory

In a perfect situation, the minimum quantity should be just enough to satisfy sales until the new order is delivered. This is called just in time ordering.

2. Physically rotating stock by hand to avoid damages and shop-soiling3. Identifying and removing slow-moving lines

The definition of slow-moving is on a per item basis, and typically depends on the amount of revenue being brought in per item and nature of the business.

4. Monitoring seasonal products to avoid dead stock5. Monitoring products subject to technological obsolescence6. Introducing complementary products7. Changing with the times8. Monitoring selling prices9. Ensuring that adequate stock security is in place

- Security guards- Undercover security personnel- Video surveillance- Security tags on products- Random checks on staff- Check deliveries against invoices- Document files in an organised fashion to avoid ‘double invoicing’ by suppliers- Place cash from cash sales securely in registers

Evaluating stock turnover

Stock turnover ratio measures how long it takes to turn stock into sales. This can be determined in times per year or days.

Stock turnover ratio (¿ )= Cost of goods soldAveragelevel of stock

28

Yakir Havin

Stock turnover ratio (days )= Average stock ×365Cost of goods sold

Stock turnover should be evaluated against: Turnover rates in previous reporting periods Comparisons with expectations of management Consideration of the type of inventory sold

Action that can be taken if a problem is detected with a slow stock turnover: Reducing the selling price of slow-moving items Relocating stock within the store to highlight particular goods Running special promotions of targeted stock lines Item combinations for promotion

Controlling debtors

Before granting credit to a customer, a credit check should be performed and may include: Banking history Loans and/or credit card history References from other businesses References from financial institutions Cash forecasts and/or budgets Income statements and balance sheets

If receipt for a credit sale is overdue, management may undertake the following action: Offering discounts for prompt payment Charging interest on overdue accounts (if detailed in original contract) Sending reminders via email Reminding debtors via telephone (for personal contact) Sending monthly statements including coloured stickers Threatening not to provide credit in future Threatening clients with legal action

An age analysis of debtors provides a snapshot look at debtors’ due payments and apportions them according to days since sale has occurred.

Evaluating debtors turnover

Debtors turnover ratio measure how long it takes to turn debtors into cash.

Debtors turnover ratio (¿)= Credit salesAverage debtors

29

Yakir Havin

Debtors turnover ratio (days)= Average debtors×365Credit sales

Evaluating the cash cycle

Cash cycle measures how long it takes to turn stock into cash. This is determined by the sum of the stock turnover and debtors turnover ratios in days. It is possible for changes in either stock or debtors turnover ratio to occur without cash cycle changing, as these may offset one another.

Evaluating creditors turnover

Creditors turnover ratio measures how long it takes for the firm to pay off its creditors.

Creditors turnover ratio (¿)= Credit purchasesAveragecreditors

Creditors turnover ratio (days )= Average creditors×365Credit purchases

Unlike the stock and debtors turnover ratios, it is not always favourable to have a low creditors turnover. If the firm is repaying its creditors too quickly, issues of liquidity will arise where the firm may not have sufficient funds to pay off other debts. Conversely, creditors turnover should also not be too slow as this may force legal action from creditors or they may decide to cut off all supply.

30

Yakir Havin

Chapter 21 – Budgeting: planning for the future

The need for budgeting

Budgeting is a means of planning and controlling the future financial transactions of a business. All business have a need for budgeting because all managers should have a basic financial plan. This is preferred to not having a plan at all, whereby the business would be allowed to run haphazardly without control or interference.

It is crucial that the budgeting process remains flexible, as they are simply a tool for planning future events. Budgets should be reviewed and updated as required.

The sales budget

Perhaps considered the cornerstone of budgeting, the sales budget is crucial to overall budgeting. A sales budget predicts the future sales revenue expected to be earned by the business. A sales budget usually includes quantities expected to be sold and the anticipated selling prices.

Cash sales link to inflows of cash (cash flow statement). Credit sales link to debtor balances (balance sheet). Sales is revenue (income statement). Sales estimates leads to predictions such as stock requirements, estimated purchases and staffing needs.

Cash budgeting

A budgeted cash flow statement looks at future cash inflows and outflows of a business.

When making predictions, take into account the follow possible factors: Is the business likely to continue trading as successfully as before? Will the business sell the same products? Are there new competitors? Has the demand for products changed? Will technology affect the business?

Decisions that may be made as a result of cash budgeting include: Additional capital contributions Cut backs on personal cash drawings Reductions or postponement of payments of expenses Borrowing required cash Leasing assets rather than owning

31

Yakir Havin

Budgeted income statements

A budgeted income statement is used to examine the predicted revenues and expenses of a business over a given period of time.

If the budgeted income statement predicts management’s overall objectives, the budget should be adopted and put into action. If not, the budget should be reviewed and changes introduced until management is happy with the budget’s goals.

The budgeted balance sheet

The budgeted balance sheet predicts the firm’s financial position at a particular date in the future.

This can be used for: Reporting on the future situation of a firm’s non-current assets Examining the future liquidity Evaluating the gearing Showing future details of owner’s equity

Budget variance reports

Variance reports are where management analyses the differences between budgeted and actual results. If the variances are favourable, these should be maximised to further aid the firm’s performance in these respective areas. If not, management should examine the areas of unfavourable variance and attempt to take corrective action to rectify them. This is part of the perpetual budgeting system whereby budgets are continually reviewed and used to make decisions.

32

Yakir Havin

Chapter 22 – Analysis and interpretation of accounting reports

The role of analysis and interpretation

Analysis and interpretation should be seen as a tool that can assist management to make better decisions.

Distinguishing between analysis and interpretation

Analysis is the process of breaking down something complex into simpler, smaller portions.Interpretation is the process of explaining the meaning of the completed analysis.

When dollar figures on a report are converted to percentages, this is known as vertical analysis because the information is analysed in a vertical fashion. On an income statement, this allows management to interpret in terms of percentages of sales consumed by each expense, and how much remained for gross/net profit.

Horizontal analysis is reports that have been converted to percentages (common size statements) are analysed across different periods to detect trends. Trend analysis involves measuring changes in an item from period to period.

Analytical ratios

An analytical ratio is simply the comparison of two items that have a particular relationship to each other.

Ratio benchmarks

Previous reporting periods (trend analysis) Industry averages, or comparison with other similar businesses Budget estimates, or predicted results Alternative investments in the money market

Ratios should always be compared to at least one benchmark to give the ratio some sort of meaning.

33

Yakir Havin

Types of analytical ratios

1. Profitability ratios: comparing profit with investment2. Operating efficiency ratios: how efficiently assets have been used by management3. Liquidity ratios: the business’s ability to meet its short term debts as they fall due4. Stability ratios: the financial stability of the business and financial risk undertaken

Profitability ratios

Profit is simply a dollar figure of revenue earned less expenses incurred for a period. Profitability measures the comparison between the profit earned and the investment made.

1. Gross profit ratio=Gross profitSales

Increases due to: Decreases due to: Cost prices decreased, sales remained Cost prices remained, selling prices

increased Cost price and selling price decreased,

but cost price decreased at a greater rate

Cost prices increased, sales remained Cost prices remained, selling prices

decreased Cost price and selling price increased,

but cost price increased at a greater rate

2. Net profit ratio= Net profitSales

This will deviate from the gross profit ratio according to the firm’s operating expenses.

3. Expense ratio=[Expense item ]

Sales

Informs management about the percentage of sales consumed by each expense.

4. Returnon assets= Net profitAveragetotal assets

Compares net profit with the amount invested in the firm’s assets. The assets value is averaged across the period to preclude fluctuations at the beginning or end of the period from offsetting this ratio.

34

Yakir Havin

5. Returnon owne r ' s investment= Net profitAverage capital

This may diverge significantly from ROA as many firms fund their assets through liabilities instead of capital.

Operating efficiency ratios

A trading business purchases assets for the purpose of generating revenue. If these assets are used to maximum operating efficiency, the result should be maximum profit. Operating efficiency ratios are related to profitability ratios in the sense that they measure how well the assets generate revenue, which ultimately determines the level of profit earned.

1. Asset turnover ratio= SalesAverage totalassets

Compares sales revenue with the average investment in the firm’s total assets.

2. Stock turnover rate= Average stock×365Cost of goods sold

Measures the number of days it takes for a business to turn stock into sales.

ConsiderType of stock being sold Previous periods’ results Budget objectives

3. Debtors turnover rate= Average debtors×365Credit sales

Examines the performance of management in collecting debts from debtors. The days figure shows the average time it takes for debtors to settle their accounts.

ConsiderCredit terms Debtors age analysis Previous results Budget objectives

4. Debtors ageanalysis

Provides management with a breakdown of debtors’ accounts in relation to the age of their debts.

ConsiderCredit terms Previous results Budget objectives

5. Cashcycle=Stock turnover+Debtorsturnover

Evaluates the time taken to turn stock into sales, and then sales into cash.

35

Yakir Havin

ConsiderIndividual turnover rates Previous results Budget objectives Creditors turnover rate

6. Creditors turnover rate= Average creditors×365Credit purchases

Measures the time taken to repay creditors. It is important to balance the time to complete the cash cycle and the time taken to settle creditors’ account.

ConsiderCash cycle results Credit terms from suppliers Previous results Budget objectives

Efficiency ratios and profitability

The way management uses its asset has a direct impact on profitability.

Returnon assets= Net profitAverage assets

= SalesAverage assets

×Net profitSales

The return on assets reports on two aspects of a firm’s performance. First, how efficiently the assets have been used to generate revenue. Second, the return on assets is affected by the percentage of sales revenue consumed by the firm’s expenses, which determines net profit.

Liquidity analysis

Liquidity is the ability of a business to meet its short term debts as they fall due, which usually refers to debts within the next 12 months. For a firm to survive, it needs cash to meet needs such as expenses, creditors, loan repayments, and drawings.

1. Working capital ratio= Current assetsCurrent liabilities

Gives a percentage or dollar figure of current assets that the firm possesses relative to each dollar of its liabilities. Businesses may be able to survive on a low working capital if they have fast cash cycles. If WCR is too high, this may mean the firm has invested too much in current assets, meaning there is too much cash tied up in bank, inventory or debtors.

2. Quick asset ratio=Current assets−stock−prepaid expensesCurrent liabilities−bank overdraft

36

Yakir Havin

Measures liquidity of a much more immediate form than WCR, as only quick assets are being compared to urgent debts. In essence, the comparison becomes bank and debtors compared to creditors. Again, a quick cash cycle may allow a firm to operate on a low quick asset ratio, but this this not be encouraged, and may signal liquidity problems in the immediate future.

Liquidity analysis and cash flows

There is a logical connection between the cash flow statement and liquidity as this statement reports all inflows and outflows of cash, thus providing a summary of what has happened to cash resources over time. A cash flow statement should be read in conjunction with analytical ratios. A profitable business may cease trading if it cannot control cash, as bills and wages must be promptly paid.

3. Cash flows ratio=Net cash flows ¿operatingactivities ¿Average current liabilities

Shows the amount of times net cash flows from operations is equal to currently owing liabilities. If this is high, the business is unlikely to experience difficulty in meeting short term debts.

ConsiderPrevious results Budget objectives

Gearing and financial stability

Financial stability looks at the long term structure of a business entity. Gearing is the dependence of a firm on outside funds (as opposed to capital). A highly geared business is one that is funded majorly by external funds i.e. liabilities. This creates higher financial risk as there is pressure to meet repayments of debts. Consequences may include legal action threatened, or cut-off of supply by creditors.

Debt ratio=Total liabilitiesTotal assets

Determines the percentage of assets funded by borrowed finances.

Gearing and the rate of return on owner’s investment

Reasons an owner might borrow money: Necessity: the firm does not have sufficient wealth to finance business operations Optional: funds are borrowed and used to increase personal return

37

Yakir Havin

High gearing also affects business in the form of interest expense which will reduce net profit. A highly geared firm may achieve high ROIs, as the level of capital is very low, and simultaneously may achieve low ROAs, as the level of assets (funded by liabilities) is very high. Certain owners may choose a high risk – high return strategy of funding their business, while others may opt for a more conservative approach.

Other analysis tools

Non-financial key performance indicators give management information about the business’s performance in non-financial forms, such as:

Customer satisfaction surveys

Salesreturns ratio=Sales returnsTotal sales

Quality assurance

Purchases returns ratio= Purchases returnsTotal purchases

Quality of management- Communication skills- Management skills (controlling stock, debtors, creditors)- Adapting to change- Developing new products- Flexibility in response to customers- Recognising one’s weaknesses

Profit compared to hours worked

Profit earned= Net profitHoursworked

Economic climate- Consumer confidence- Market competitions- Wage demands by unions- Market trends- Technological change

Limitations of ratio analysis

1. Ratios are based on historical data and there is no guarantee these will correspond to future results

2. Historical cost accounting (changes due to inflation)3. Changes in accounting methods

38

Yakir Havin

4. Inter-firm comparisons5. Frequency of reporting6. Limited information

39