Eastpoint Water and Sewer District Financial Statement.pdf · Eastpoint Water and Sewer District...

30

Eastpoint Water and Sewer District Financial Statements September 30, 2013 and 2012

Transcript of Eastpoint Water and Sewer District Financial Statement.pdf · Eastpoint Water and Sewer District...

Eastpoint Water and Sewer District

Financial Statements

September 30, 2013 and 2012

Eastpoint Water and Sewer District Table of Contents

September 30, 2013 and 2012

Independent Auditor’s Report 1 Management’s Discussion and Analysis Basic Financial Statements

3

Statements of Net Position 7 Statements of Revenues, Expenses, and Changes in Net Position 9 Statements of Cash Flows 10 Notes to the Basic Financial Statements 12

Compliance Section

Independent Auditor’s Management Letter 22

Independent Auditor’s Report on Internal Control over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance with Government Auditing Standards

24

Carr, Riggs & Ingram, LLC

14101 Panama City Beach Parkway

Suite 200

Panama City Beach, FL 32413

(850) 784-6733

(850) 784-4866 (fax)

www.cricpa.com

INDEPENDENT AUDITOR’S REPORT

Board of Commissioners Eastpoint Water and Sewer District Eastpoint, Florida

Report on the Financial Statements

We have audited the accompanying financial statements of the business-type activities of Eastpoint Water and Sewer District (the District), as of and for the years ended September 30, 2013 and 2012, which collectively comprise the District’s basic financial statements as listed in the table of contents.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditor’s Responsibility

Our responsibility is to express opinions on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinions.

- 2 -

Opinions

In our opinion, the financial statements referred to above present fairly, in all material respects, the respective financial positions of the business-type activities of Eastpoint Water and Sewer District as of September 30, 2013 and 2012, and the respective changes in financial position, and, where applicable, cash flows thereof for the year then ended in accordance with accounting principles generally accepted in the United States of America.

Other Matters

Required Supplementary Information

Accounting principles generally accepted in the United States of America require that the management’s discussion and analysis on pages 3 through 6 be presented to supplement the basic financial statements. Such information, although not a part of the basic financial statements, is required by the Governmental Accounting Standards Board, who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic, or historical context. We have applied certain limited procedures to the required supplementary information in accordance with auditing standards generally accepted in the United States of America, which consisted of inquiries of management about the methods of preparing the information and comparing the information for consistency with management’s responses to our inquiries, the basic financial statements, and other knowledge we obtained during our audit of the basic financial statements. We do not express an opinion or provide any assurance on the information because the limited procedures do not provide us with sufficient evidence to express an opinion or provide any assurance.

Other Reporting Required by Government Auditing Standards

In accordance with Government Auditing Standards, we have also issued our report dated February 20, 2015, on our consideration of the Eastpoint Water and Sewer District’s internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering Eastpoint Water and Sewer District’s internal control over financial reporting and compliance.

Certified Public Accountants Panama City Beach, Florida February 20, 2015

Management’s Discussion & Analysis

- 3 -

MANAGEMENT’S DISCUSSION AND ANALYSIS Management of Eastpoint Water and Sewer District, an independent special district, offers readers of the District’s financial statements this narrative overview and analysis of the District’s financial performance during the fiscal years ending September 30, 2013 and 2012. This information is designed in a manner to enhance the readers understanding of the District’s financial position and activities in conjunction with the audited basic financial statements which follow. FINANCIAL HIGHLIGHTS The total assets of the District exceeded its liabilities at the close of the fiscal year.

- The District’s net position increased by 4% from the prior year. - The District’s operating revenue increased by 3% from the prior year. - The District’s operating expenses decreased by 3% from the prior year.

OVERVIEW OF THE FINANCIAL STATEMENTS This discussion and analysis is intended to serve as an introduction to the District’s basic financial statements. The District’s basic financial statements are comprised of the following: 1) statement of net position, 2) statement of revenues, expenses, and changes in net position, 3) statement of cash flows, and 4) notes to the financial statements. This report also contains other essential information to assist the reader to better understand the data supplied in the basic financial statement. REQUIRED FINANCIAL STATEMENTS The District reports information in the financial statements that conforms to U.S. generally accepted accounting principles using the accrual methods similar to those used by private companies. The revenues are reported when earned and expenses are recorded when a liability is incurred. The operating revenues are the result of charges to customers for water and sewer services, intergovernmental revenues, miscellaneous income, and connection fees. These statements offer short and long-term financial information about its activities. The statement of net position includes all of the District’s assets and liabilities and provides information about the nature and amounts of investments in resources (assets) and the obligations to District’s creditors (liabilities). The financial statements also provide the basis for evaluating the capital structure of the District and assessing its liquidity and financial flexibility. Revenues and expenses are accounted for in the statement of revenues, expenses, and changes in net position. This statement measures the financial success of the operation of the District and can be used to determine whether it has successfully recovered all its costs through its user fees and other charges, profitability and credit worthiness. FINANCIAL ANALYSIS OF THE DISTRICT The financial analysis of the District provides the foundation for sound financial management. It translates the conceptual relationship into a numerical language useful for practical interpretation. The statement of net position presents information on all the District’s assets and liabilities noting differences between the two reported as net position. Over time, these increases or decreases in net position may serve as a useful indicator of whether the financial position of the District is improving or weakening.

- 4 -

The statement of revenues, expenses, and changes in net position presents information indicating how the District’s net position changed during the year. NET POSITION A summary of the District’s statement of net position is presented below:

Condensed Statements of Net Position

September 30, 2013 2012

Current assets $ 1,207,956 $ 1,327,396

Noncurrent assets 10,590,042 10,458,726

Total assets 11,797,998 11,786,122

Current liabilities 10,960 126,484

Noncurrent liabilities 3,847,174 4,033,065

Total liabilities 3,858,134 4,159,549

Net investment in capital assets 6,694,880 6,232,406

Restricted net position 58,255 211,146

Unrestricted net position 1,186,729 1,183,021

Total net position $ 7,939,864 $ 7,626,573

Condensed Statements of Revenues, Expenses, and Changes in Net Position

Year ended September 30, 2013 2012

Operating revenues $ 775,295 $ 754,433

Nonoperating revenues 662,907 1,310,021

Total revenues 1,438,202 2,064,454

Operating expenses 776,185 797,277

Depreciation 217,849 219,417

Nonoperating expenses 130,877 112,756

Total expenses 1,124,911 1,129,450

Net income 313,291 935,004

Beginning net position 7,626,573 6,691,569

Ending net position $ 7,939,864 $ 7,626,573

The statement of revenues, expenses, and changes in net position identifies the various revenue and expense items which impacted the change in net position. The statement provides answers as to the nature and source of these changes. The operating revenues had an increase due to an increase in connections fees in the current year. The nonoperating revenue decrease was primarily due to a decrease in grant revenue. Total expenses were fairly consistent with prior year.

- 5 -

CAPITAL ASSETS At September 30, 2013, the District has invested $10,418,880 in capital assets. This represents 88% of total assets. A summary of the Districts capital assets follows.

Capital Assets

September 30, 2013 2012

Land $ 602,729 $ 602,729

Water and sewer system 13,206,710 7,387,550

Equipment and furniture 307,104 307,104

Construction in progress 836,594 6,158,431

Total 14,953,137 14,455,814

Less accumulated depreciation 4,534,257 4,316,408

Net capital assets $ 10,418,880 $ 10,139,406

Well construction began in 2008 in response to the need for resource protection as mandated by permitting agencies, water quality, safety and the necessary reconstruction of a failing delivery system. Since the wells have not yet been put into service, pending the delayed water plant construction, they are categorized as construction in progress at year end. During 2012, the District continued working on upgrading water lines to under-served areas while continuing its efforts through engineering, permitting and design to begin the rebuilding of its water plant and vacuum sewer pumping stations. Construction of these upgrades was completed in 2013. DEBT ADMINISTRATION

As of September 30, 2013, the Eastpoint Water and Sewer District had total bonded debt outstanding of $3,724,000, which is a decrease of $183,000 from the previous year. ECONOMIC FACTORS AND NEXT YEAR’S BUDGET AND RATES

The District's Commissioners and managers utilized the same factors for establishing the 2013-2014 budget as were used for setting the 2012-2013 budget. Among those factors considered were: user fees, service charges, declining ad valorem taxes, aging infrastructure repair costs, manpower, and existing debt. In addition, the continued decline in the seafood industry, and the fact that the District is comprised of the largest population of lower income families in Franklin County, weighed heavily in overall budget considerations. Necessary rate increases were again balanced with budget cuts to meet the Districts immediate needs. Special consideration was given to anticipated need for future construction planning and financing. Given the strained economic conditions in the community focus was placed on securing grant funding for those necessary projects. The Commissioners and managers are constantly reviewing ways to lower operating costs while meeting the increasing demands of an aging system while balancing the community's ability to pay for these services during continued economic challenge and a decreasing customer base.

- 6 -

CONTACTING THE DISTRICT’S FINANCIAL MANAGER

This financial report is designed to provide a general overview of the Eastpoint Water and Sewer District’s finances for all those with an interest in the District’s finances. Questions concerning any of the information provided in this report or requests for additional financial information may be addressed to the Management at Eastpoint Water and Sewer District, 40 Island Drive, Eastpoint, Florida 32328.

Eastpoint Water and Sewer District Statements of Net Position – Proprietary Fund

See accompanying notes. - 7 -

September 30, 2013 2012

Assets

Current assets

Cash and cash equivalents 1,017,357$ 956,504$

Accounts receivable, net 98,187 150,286

Grants receivable 10,609 108,226

Other receivable - 8,444

Inventory 69,225 99,961

Prepaid expenses 12,578 3,975

Total current assets 1,207,956 1,327,396

Noncurrent assets

Restricted cash and cash equivalents 171,162 319,320

Capital assets

Land 602,729 602,729

Water and sewer system 13,206,710 7,387,550

Equipment and furniture 307,104 307,104

Construction in progress 836,594 6,158,431

Total capital assets 14,953,137 14,455,814

Less accumulated depreciation (4,534,257) (4,316,408)

Net capital assets (net of

accumulated depreciation) 10,418,880 10,139,406

Total noncurrent assets 10,590,042 10,458,726

Total assets 11,797,998 11,786,122

(Continued)

Eastpoint Water and Sewer District Statements of Net Position – Proprietary Fund (continued)

See accompanying notes. - 8 -

September 30, 2013 2012

Liabilities

Current liabilities

Accounts payable 10,960$ 126,484$

Total current liabilities 10,960 126,484

Noncurrent liabilities

Customer deposits 112,907 108,174

Due within a year

Bonds payable 50,000 59,000

Accrued interest 10,267 17,891

Due in more than one year

Bonds payable 3,674,000 3,848,000

Total noncurrent liabilities 3,847,174 4,033,065

Total liabilities 3,858,134 4,159,549

Net position

Net investment in capital assets 6,694,880 6,232,406

Restricted for

Debt service 14,433 70,058

Renewal and replacement 23,555 51,082

Short lived asset reserves 20,267 5,067

Bond reserve - 84,939

Unrestricted 1,186,729 1,183,021

Total net position 7,939,864$ 7,626,573$

Eastpoint Water and Sewer District Statements of Revenues, Expenses, and Changes in Net

Position – Proprietary Fund

See accompanying notes. - 9 -

2013 2012

Operating revenues

Water services 283,944$ 283,517$

Sewer services 231,131 227,304

Impact fees - 1,250

Connection fees 45,831 10,300

Miscellaneous revenues 214,389 232,062

Total operating revenues 775,295 754,433

Operating expenses

Personnel services 327,153 301,213

Contractual services 61,906 100,343

Repairs and maintenance 24,235 20,886

Utilities 93,239 91,395

Insurance 22,849 37,656

Office 19,036 17,554

Other operating 110,860 40,724

Training 337 250

Bad debts 108,194 178,649

Miscellaneous 8,376 8,607

Depreciation 217,849 219,417

Total operating expenses 994,034 1,016,694

Operating loss (218,739) (262,261)

Nonoperating revenues (expenses)

Property taxes 132,200 143,202

Grant revenues 510,951 1,139,197

Interest income 19,756 27,622

Interest expense (130,877) (112,756)

Total nonoperating revenues (expenses) 532,030 1,197,265

Net income 313,291 935,004

Net position, beginning 7,626,573 6,691,569

Net position, ending 7,939,864$ 7,626,573$

Year ended September 30,

Eastpoint Water and Sewer District Statements of Cash Flows – Proprietary Fund

See accompanying notes. - 10 -

2013 2012

Operating activities

Receipts from customers 968,924$ 1,112,550$

Payments to suppliers and others (580,783) (738,036)

Payments to employees (327,153) (301,213)

Net cash provided by operating activities 60,988 73,301

Noncapital financing activities

Cash received for property taxes 132,200 143,202

Grant revenues 510,951 1,139,197

Net cash provided by noncapital financing activities 643,151 1,282,399

Capital and related financing activities

Acquisition of capital assets (497,323) (3,828,297)

Proceeds from bonds payable - 3,724,000

Principal repayment of bonds payable (183,000) (57,000)

Proceeds from short-term debt - 2,567,520

Repayment of short-term debt - (3,574,995)

Interest paid on long-term debt (130,877) (112,756)

Net cash used in capital and related financing activities (811,200) (1,281,528)

Investing activities

Interest received 19,756 27,622

Net cash provided by investing activities 19,756 27,622

Net change in cash and cash equivalents (87,305) 101,794

Cash and cash equivalents, beginning 1,275,824 1,174,030

Cash and cash equivalents, ending 1,188,519$ 1,275,824$

Classified as cash

Current assets - cash and cash equivalents 1,017,357$ 956,504$

Restricted assets - cash and cash equivalents 171,162 319,320

Cash and cash equivalents, ending 1,188,519$ 1,275,824$

(Continued)

Year ended September 30,

Eastpoint Water and Sewer District Statements of Cash Flows – Proprietary Fund (continued)

See accompanying notes. - 11 -

Year ended September 30, 2013 2012

Reconciliation of operating loss to net

cash provided by operating activities

Operating loss (218,739)$ (262,261)$

Adjustments to reconcile operating loss to net

cash provided by operating activities

Depreciation 217,849 219,417

(Increase) decrease in

Accounts receivable, net 52,099 128,051

Grants receivable 97,617 260,173

Other receivable 8,444 (8,444)

Inventory 30,736 (28,972)

Prepaid expenses (8,603) 254

Increase (decrease) in

Accounts payable (115,524) (225,539)

Customer deposits 4,733 7,309

Accrued interest (7,624) (16,687)

Due from other governmental units Total adjustments 279,727 335,562

Net cash provided by operating activities 60,988$ 73,301$

Eastpoint Water and Sewer District Notes to the Basic Financial Statements

- 12 -

NOTE 1: SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES Reporting Entity The Eastpoint Water and Sewer District (the District) is an independent special district created under Chapter 67-1399, Laws of Florida, Acts of 1967 in the unincorporated community of Eastpoint, Florida. The District has the powers granted to Water and Sewer Districts under the provisions of Chapter 153, Florida Statutes. The governing body of the District is the Eastpoint Board of Commissioners. The District provides water services and sewer disposal as authorized by Statutes. Basis of Presentation The District operates as a proprietary fund and applies all applicable Governmental Accounting Standards Board (GASB) pronouncements. A proprietary type fund is used to account for operations that are financed and operated in a manner similar to private business enterprises, where the intent of the governing body is that the costs (expenses, including depreciation) of providing goods of services to the general public on a continuing basis are financed or recovered primarily through user charges. The District exercises oversight responsibility through designation of management and budgetary review and approval. Measurement Focus, Basis of Accounting, and Financial Statement Presentation The accompanying financial statements are reported using the “economic resources measurement focus,” and the “accrual basis of accounting.” Revenues are reported when earned and expenses are recorded when a liability is incurred, regardless of the timing of related cash flows. There were no entities that required inclusion as component units within the District’s financial statements. Proprietary funds distinguish operating revenues and expenses from nonoperating items. Operating revenues and expenses generally result from providing services and producing and delivering goods in connection with a proprietary fund’s principal ongoing operations. The principal operating revenue of the District is charges to customers for water and sewer services. Operating expenses include the cost of sales and services, administrative expenses, and depreciation on capital assets. All revenues and expenses not meeting this definition are reported as nonoperating revenues and expenses. Governmental Accounting Standards Board (GASB) Pronouncements The District follows the provisions of GASB Statement No. 34, Basic Financial Statements-and Management’s Discussion and Analysis-for State and Local Governments and GASB Statement No. 37, Basic Financial Statements-and Management’s Discussion and Analysis-for State and Local Governments: Omnibus. Statement 34 establishes standards for external financial reporting for all state and local governmental entities.

Eastpoint Water and Sewer District Notes to the Basic Financial Statements

- 13 -

NOTE 1: SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED) Use of Estimates The preparation of financial statements in conformity with U.S. generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts and disclosures. Accordingly, actual results could differ from those estimates. Cash and Cash Equivalents The District considers demand deposits, certificates of deposit and other highly liquid debt instruments to be cash equivalents. Investments

Investments of the District are reported at fair value unless otherwise disclosed. Accounts Receivable Accounts receivable are shown at their net realizable value and reduced by an allowance for uncollectible accounts. The allowance is based on accounts that are past due at year end which are final bills or are over $1,000. Inventory The District’s inventory, which consists primarily of supplies, is stated at the lower of cost or market value with cost determined using the first-in, first-out method. Capital Assets It is the District’s policy to capitalize property and equipment with a cost of over $500 with an estimated useful life in excess of one year. Lesser amounts are expensed. Property and equipment is valued at historical cost or estimated historical cost if actual historical cost is not available. Donated fixed assets are valued at their estimated fair value on the date donated. Depreciation of fixed assets other than land and construction in process is charged as an expense against operations. Depreciation has been provided over the estimated useful lives of the assets using the straight-line method. The useful lives are generally as follows:

Utility plant in service 40 Years Equipment and furniture 3-10 Years

Compensated Absences The District follows GASB 16 entitled, Accounting for compensated absences. Enterprise funds accrue sick leave and vacation benefits in the period in which they are earned.

Eastpoint Water and Sewer District Notes to the Basic Financial Statements

- 14 -

NOTE 1: SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED) Net position

GASB Statement No. 63, Financial Reporting of Deferred Outflows of Resources, Deferred Inflows of Resources, and Net Position, was implemented in the current year. This standard provides financial reporting guidance for deferred outflows of resources and deferred inflows of resources and this standard renames the components of net position which were previously considered net assets. Net position is classified in three categories. The general meaning of each is as follows:

Net investment in capital assets - represents the cost of capital assets, less accumulated depreciation reduced by the outstanding balances of any borrowings used for the acquisition, construction or improvement of those assets. Restricted - This category includes resources restricted by creditors, grantors, contributors, laws or regulations of other governments, constitutional provisions, or enabling legislation. Unrestricted - indicates that portion of net position that is available for future periods.

Use of Restricted Assets It is generally the practice of the District to utilize restricted assets before unrestricted when possible. Subsequent Events Management of the District has evaluated subsequent events through February 20, 2015, the date the financial statements were available to be issued.

NOTE 2: CASH AND INVESTMENTS Deposits All cash resources of Eastpoint Water and Sewer District are placed in banks that are qualified public depositories, as required by law (Florida Security for Public Deposits Act). Every qualified public depository is required by this law to deposit with the State Treasurer eligible collateral equal to, or in excess of, an amount to be determined by the State Treasurer. The State Treasurer is required by this law to ensure that the District’s funds are entirely collateralized throughout the fiscal year. In the event of a failure by a qualified public depository, losses, in excess of federal depository insurance and proceeds from the sale of the securities pledged by the defaulting depository, are assessed against the other qualified public depositories of the same type as the depository in default. When other qualified public depositories are assessed additional amounts, they are assessed on a pro-rata basis. All District cash consists of demand deposits and interest-bearing certificates of deposit in a local bank.

Eastpoint Water and Sewer District Notes to the Basic Financial Statements

- 15 -

NOTE 2: CASH AND INVESTMENTS (CONTINUED) Investments Florida Statutes, Section 218.415, authorizes the City to invest surplus funds in the following:

The Local Government Surplus Funds Trust Fund, or any intergovernmental investment pool authorized pursuant to the Florida Interlocal Cooperation Act of 1969, as provided in Section 163.01.

Securities and Exchange Commission registered money market funds with the highest credit quality rating from a nationally recognized rating agency.

Interest-bearing time deposits or savings accounts in qualified public depositories, as defined in Section 280.02.

Direct obligations of the U.S. Treasury.

The District had no investments at September 30, 2013. Interest Rate Risk

At September 30, 2013, the District did not hold any investments that were considered to be an interest rate risk. Credit Risk

At September 30, 2013, the District did not hold any investments that were considered to be a credit risk. Custodial Credit Risk

At September 30, 2013, the District did not hold any investments that were considered to be a custodial risk. Concentration of Credit Risk

At September 30, 2013, the District did not hold any investments that were considered to be a concentration of credit risk. Restricted cash and investments consisted of the following:

September 30, 2013 2012

Customer deposits $ 112,907 $ 108,174

Bond principal and interest 14,433 70,058

Bond renewal and replacement 23,555 51,082

Short lived asset reserve 20,267 5,067

Bond reserve - 84,939

Total restricted cash and investments $ 171,162 $ 319,320

Eastpoint Water and Sewer District Notes to the Basic Financial Statements

- 16 -

NOTE 3: ACCOUNTS RECEIVABLE Accounts receivable includes amounts due from customers for water and sewer services provided by the District. Accounts receivable at their net realizable value are as follows:

September 30, 2013 2012

Customers utility billings $ 378,440 $ 322,345

Tap fees 178 178

Total accounts receivable 378,618 322,523

Less allowance for doubtful accounts (280,431) (172,237)

Accounts receivable, net $ 98,187 $ 150,286

Accounts receivable are recorded based upon reading meters indicating customers’ usage of water. An allowance for doubtful accounts is established for estimated amounts not expected to be collected. NOTE 4: UNBILLED REVENUE There are no significant amounts of unbilled revenue at September 30, 2013. NOTE 5: RISK MANAGEMENT The District is exposed to various risks of loss related to torts; theft of, damage to and destruction of assets; errors or omissions; and natural disasters for which the government carries commercial insurance. Insurance against losses are provided for the following types of risk:

Workers’ compensation and employer’s liability

General and automobile liability

Real and personal property damage

Public officials’ liability The District’s coverage for workers’ compensation is under a retrospectively rated policy. Premiums are accrued based on the ultimate cost to the date of the District’s experience for this type of risk.

NOTE 6: EMPLOYEE BENEFITS – RETIREMENT PLAN Defined Benefit Pension Plan The District participates in the Florida Retirement System (FRS) which is a multiple-employer; cost-sharing retirement system established by Chapter 121, Florida Statutes. The Florida Retirement System

Eastpoint Water and Sewer District Notes to the Basic Financial Statements

- 17 -

NOTE 6: EMPLOYEE BENEFITS – RETIREMENT PLAN (CONTINUED) is administered by the Division of Retirement of the State of Florida Department of Administration. The District’s payroll for employees covered by the system for the years ended September 30, 2013, 2012 and 2011 was $226,961, $238,526 and $211,291, respectively. FRS issues a publicly available financial report that includes financial statements and required supplementary information. That report may be obtained by contacting the State of Florida Department of Management Services, Division of Retirement, Bureau of Research, Education and Policy, 2639 North Monroe Street, Building C, Tallahassee, Florida 32399-1650. The system provides vesting of benefits after 6 years of creditable service. Members are eligible for normal retirement after attaining age 62 or 30 years of service. Generally, membership is compulsory for all full-time and part-time employees. Employees contribute 3% to the plan. The District’s contributory rates for the year ended September 30, 2013 were as follows:

October 1, 2012 Through

June 30, 2013 July 1, 2013 Through September 30, 2013

Regular employees 5.18% 6.95% Special risk employees 14.90% 19.06%

The District’s contributions to the Plan for the years ended September 30, 2013, 2012 and 2011 were $14,068, $12,333 and $20,399 respectively, which equal the required contributions. For the year ended September 30, 2013 retirement contributions represent 6% of District’s total covered payroll.

Three Year Trend Information

Year Ended September 30,

Annual Pension

Cost (APC)

Percent of APC

Contribution

Net Pension

Obligation

2011 $ 20,399 100% - 2012 12,333 100% - 2013 14,068 100% -

Defined Contribution Plan Pursuant to Chapter 121, Florida Statutes, the Florida Legislature created the Florida Retirement Investment Plan (“FRS Investment Plan”), a cost-sharing multiple-employer defined contribution pension plan qualified under Section 401(a) of the Internal Revenue Code. This FRS Investment Plan is an alternative available to members of the Florida Retirement System in lieu of the defined benefit plan. Changes to the law can only occur through an act of the Florida Legislature. The FRS Investment Plan is administered by the Florida State Board of Administration. Information about this plan can be obtained by writing to FRS Plan Administrator, P.O. Box 56290, Jacksonville, Florida 32241-6290 or by calling 866-377-2121.

Eastpoint Water and Sewer District Notes to the Basic Financial Statements

- 18 -

NOTE 6: EMPLOYEE BENEFITS – RETIREMENT PLAN (CONTINUED) FRS Investment Plan is funded through employee and employer contributions. Employees contribute 3% to the plan. The District’s contributory rates for the year ended September 30, 2013 were as follows:

October 1, 2012 Through June 30, 2013

July 1, 2013 Through September 30, 2013

Regular employees 5.18% 6.95% Special risk employees 14.90% 19.06%

Required employer and employee contributions made to the plan totaled $1,617 and $862, respectively.

NOTE 7: OTHER POSTEMPLOYMENT BENEFITS (OPEB) The District provides health insurance to its active and retired employees (the OPEB Plan). Pursuant to Section 112.0801, Florida Statutes, the District is required to permit participation in the health insurance program by retirees and their eligible dependents at a cost to the retiree that is no greater than the cost at which coverage is available for active employees. Currently, the District funds the OPEB Plan on a pay-as-you-go basis as a current operating expense, and reflects the expense in its financial statements in the fiscal year in which the payments are made. Pursuant to the provisions of GASB 43, Financial Reporting for Postemployment Benefits Other Than Pensions, and GASB 45, Accounting and Financial Reporting by Employers for Postemployment Benefits Other Than Pensions, governments who provide postemployment benefits other than pensions are required to begin showing all or a portion of the liabilities associated with their OPEB Plans in their financial statements and whether, and to what extent, progress is being made in funding those liabilities. NOTE 8: PROPERTY TAXES

Property taxes consist of ad valorem taxes on real and personal property within the District. Property values are determined by the Franklin County Property Appraiser. Property taxes are collected by the Franklin County Tax Collector. State law provides for enforcement of collection of personal property taxes by seizure of the property to satisfy unpaid taxes and for enforcement of collection of real property taxes by the sale of interest-bearing tax certificates. Property tax revenues are recognized when taxes are received by the District. Because any delinquent taxes collected after September 30 would not be material, delinquent taxes due are not accrued at year end. The District’s millage rate for the year ended September 30, 2013, was 2.0 mils. The tax levy of the District is established by the Districts’ Board prior to October 1 of each year.

Eastpoint Water and Sewer District Notes to the Basic Financial Statements

- 19 -

NOTE 8: PROPERTY TAXES (CONTINUED)

The District’s tax calendar is as follows:

Tax Lien Date: January 1 Tax Levy Date: Not later than October 1 Delinquent Date: April 1 of year following assessment Payment Period: November through March (up to 4% discount for early

payment) Tax Delinquent Date: April 1 Tax Certificates Sold: May 31

NOTE 9: CAPITAL ASSETS Capital assets activity for the year ended September 30, 2013, was as follows:

September 30, September 30,

2012 Increases (Decreases) 2013

Capital assets not being

depreciated

Land 602,729$ -$ -$ 602,729$

Construction in progress 6,158,431 497,323 (5,819,160) 836,594

Total capital assets,

not being depreciated 6,761,160 497,323 (5,819,160) 1,439,323

Capital assets being

depreciated

Water and sewer system 7,387,550 5,819,160 - 13,206,710

Equipment and furniture 307,104 - - 307,104

Total capital assets

being depreciated 7,694,654 5,819,160 - 13,513,814

Less accumulated

depreciation 4,316,408 217,849 - 4,534,257

Total capital assets

being depreciated, net 3,378,246 5,601,311 - 8,979,557

Total capital assets, net 10,139,406$ 6,098,634$ (5,819,160)$ 10,418,880$

Eastpoint Water and Sewer District Notes to the Basic Financial Statements

- 20 -

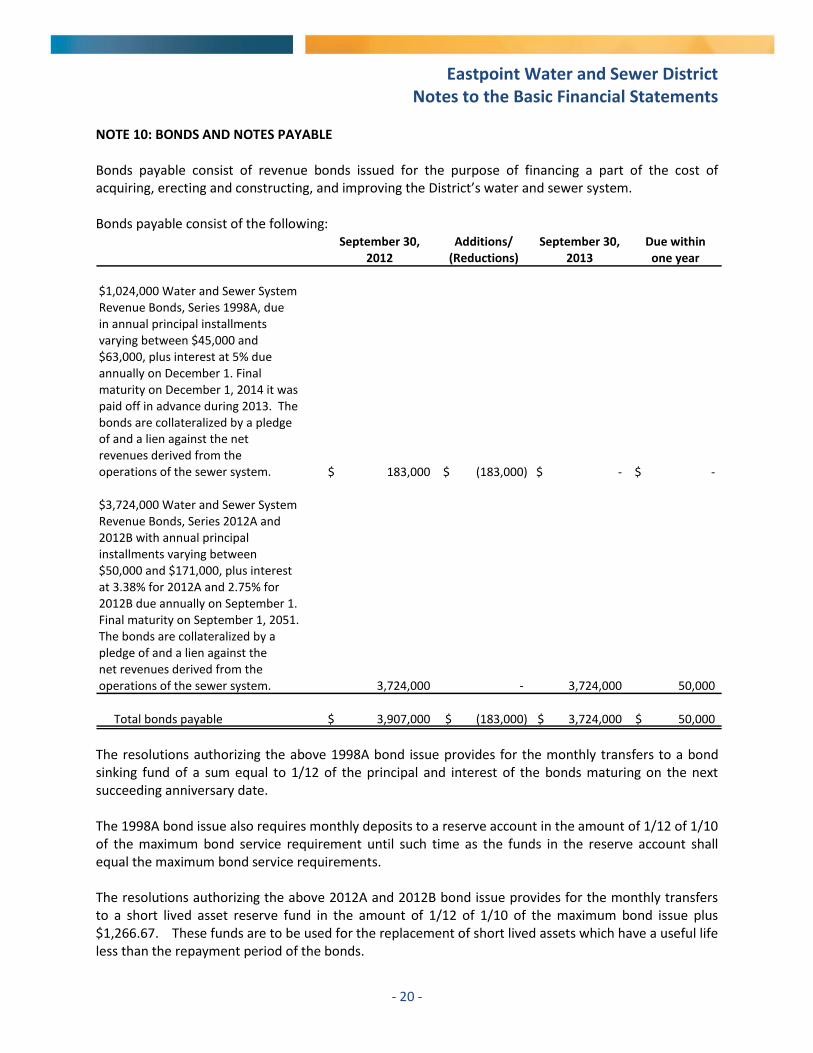

NOTE 10: BONDS AND NOTES PAYABLE

Bonds payable consist of revenue bonds issued for the purpose of financing a part of the cost of acquiring, erecting and constructing, and improving the District’s water and sewer system. Bonds payable consist of the following:

September 30, Additions/ September 30, Due within2012 (Reductions) 2013 one year

$1,024,000 Water and Sewer System Revenue Bonds, Series 1998A, due in annual principal installments varying between $45,000 and $63,000, plus interest at 5% due annually on December 1. Final maturity on December 1, 2014 it was paid off in advance during 2013. The bonds are collateralized by a pledge of and a lien against the net revenues derived from the operations of the sewer system. 183,000$ (183,000)$ -$ -$

$3,724,000 Water and Sewer System Revenue Bonds, Series 2012A and 2012B with annual principal installments varying between $50,000 and $171,000, plus interest at 3.38% for 2012A and 2.75% for 2012B due annually on September 1. Final maturity on September 1, 2051. The bonds are collateralized by a pledge of and a lien against the net revenues derived from the operations of the sewer system. 3,724,000 - 3,724,000 50,000

Total bonds payable 3,907,000$ (183,000)$ 3,724,000$ 50,000$

The resolutions authorizing the above 1998A bond issue provides for the monthly transfers to a bond sinking fund of a sum equal to 1/12 of the principal and interest of the bonds maturing on the next succeeding anniversary date.

The 1998A bond issue also requires monthly deposits to a reserve account in the amount of 1/12 of 1/10 of the maximum bond service requirement until such time as the funds in the reserve account shall equal the maximum bond service requirements. The resolutions authorizing the above 2012A and 2012B bond issue provides for the monthly transfers to a short lived asset reserve fund in the amount of 1/12 of 1/10 of the maximum bond issue plus $1,266.67. These funds are to be used for the replacement of short lived assets which have a useful life less than the repayment period of the bonds.

Eastpoint Water and Sewer District Notes to the Basic Financial Statements

- 21 -

NOTE 10: BONDS AND NOTES PAYABLE (CONTINUED) The 2012A and 2012B bond issue also requires annual deposits to a reserve account in the amount of 1/10 of the maximum bond service requirement until such time as the funds in the reserve account shall equal the maximum bond service requirements. The bond issue also requires the monthly deposits to a sinking fund of a sum equal to 1/12 of the principal and interest of the bonds maturing on the next succeeding anniversary date. Future debt service requirements on long-term debt are summarized below:

Year ending

September 30, Principal Interest Principal Interest Total

2014 $ 44,000 $ 112,219 $ 6,000 $ 10,973 $ 173,192

2015 46,000 110,734 6,000 10,808 173,542

2016 47,000 109,181 6,000 10,643 172,824

2017 49,000 107,595 7,000 10,478 174,073

2018 51,000 105,941 7,000 10,285 174,226

2019 - 2023 280,000 502,876 37,000 48,511 868,387

2024 - 2028 331,000 452,251 42,000 43,148 868,399

2029 - 2033 390,000 392,547 48,000 37,043 867,590

2034 - 2038 460,000 322,144 55,000 30,086 867,230

2039 - 2043 544,000 239,017 63,000 22,057 868,074

2044 - 2048 642,000 140,872 72,000 12,898 867,770

2049 - 2051 441,000 30,139 50,000 2,805 523,944

Total $ 3,325,000 $ 2,625,516 $ 399,000 $ 249,735 $ 6,599,251

Series 2012 A Series 2012 B

The series 1998A water and sewer revenue bonds are secured by a first lien on the net water and sewer system revenues. Annual principal and interest payments on the bonds are 957 percent of pledged revenues. The total principal and interest remaining to be paid on the bonds is $0 as the bonds were paid in full during 2013. Principal and interest paid for the current year and total pledged revenues were $193,255 and $20,189, respectively. The series 2012A water and sewer revenue bonds are secured by a first lien on the net water and sewer system revenues. Annual principal and interest payments on the bonds are 556 percent of pledged revenues. The total principal and interest remaining to be paid on the bonds is $5,950,516. Principal and interest paid for the current year and total pledged revenues were $112,219 and $20,189, respectively. The series 2012B water and sewer revenue bonds are secured by a first lien on the net water and sewer system revenues. Annual principal and interest payments on the bonds are 54 percent of pledged revenues. The total principal and interest remaining to be paid on the bonds is $648,735. Principal and interest paid for the current year and total pledged revenues were $10,973 and $20,189, respectively.

Compliance Section

Carr, Riggs & Ingram, LLC

14101 Panama City Beach Parkway

Suite 200

Panama City Beach, FL 32413

(850) 784-6733

(850) 784-4866 (fax)

www.cricpa.com

- 22 -

INDEPENDENT AUDITOR’S MANAGEMENT LETTER Board of Commissioners Eastpoint Water and Sewer District Eastpoint, Florida We have audited the financial statements of Eastpoint Water and Sewer District (the District), as of and for the fiscal year ended September 30, 2013, and have issued our report thereon dated February 20, 2015. We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. We have issued our Independent Auditor’s Report on Internal Control over Financial Reporting and on Compliance and Other Matters Based on an Audit of the Financial Statements Performed in Accordance with Government Auditing Standards. Disclosures in this report, which is dated February 20, 2015, should be considered in conjunction with this management letter. Additionally, our audit was conducted in accordance with Chapter 10.550, Rules of the Auditor General, which governs the conduct of local governmental entity audits performed in the State of Florida. This letter includes the following information, which is not included in the aforementioned auditor’s report. Section 10.554(1)(i)1., Rules of the Auditor General, requires that we determine whether or not corrective actions have been taken to address findings and recommendations made in the preceding

annual financial audit report. Corrective actions have been taken to the extent considered necessary, other than for those comments repeated in the Independent Auditor’s Report on Internal Control Over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance with Government Auditing Standards.

Findings reported the two previous years include 13-01, 13-02, and 13-03. Section 10.554(1)(i)2., Rules of the Auditor General, requires our audit to include a review of the provisions of Section 218.415, Florida Statutes, regarding the investment of public funds. In connection with our audit, we determined that the District complied with Section 218.415, Florida Statutes. Section 10.554(1)(i)3., Rules of the Auditor General, requires that we address in the management letter any recommendations to improve financial management. In connection with our audit, we did not have any such recommendations. Section 10.554(1)(i)4., Rules of the Auditor General, requires that we address noncompliance with provisions of contracts or grant agreements, or abuse, that have occurred, or are likely to have occurred, that have an effect on the financial statements that is less than material but which warrants the attention of those charged with governance. In connection with our audit, we did not have any such findings.

- 23 -

Section 10.554(1)(i)5., Rules of the Auditor General, requires that the name or official title and legal authority for the primary government and each component unit of the reporting entity be disclosed in this management letter, unless disclosed in the notes to the financial statements. The Eastpoint Water and Sewer District was established in 1967, under a Charter in accordance with the laws of Florida 67-1717. There are no component units of the District.

Section 10.554(1)(i)6.a., Rules of the Auditor General, requires a statement be included as to whether or not the local governmental entity has met one or more of the conditions described in Section 218.503(1), Florida Statutes, and identification of the specific condition(s) met. In connection with our audit, we determined that the District did not meet any of the conditions described in Section 218.503(1), Florida Statutes. Section 10.554(1)(i)6.b., Rules of the Auditor General, requires that we determine whether the annual financial report for the District for the fiscal year ended September 30, 2013, filed with the Florida Department of Financial Services pursuant to Section 218.32(1)(a), Florida Statutes, is in agreement with the annual financial audit report for the fiscal year ended September 30, 2013. In connection with our audit, we determined that these two reports were in agreement. Pursuant to Sections 10.554(1)(i)6.c. and 10.556(7), Rules of the Auditor General, we applied financial condition assessment procedures. It is management’s responsibility to monitor the District’s financial condition, and our financial condition assessment was based in part on representations made by management and the review of financial information provided by same. Our management letter is intended solely for the information and use of the Legislative Auditing Committee, members of the Florida Senate and the Florida House of Representatives, the Florida Auditor General, Federal and other granting agencies, and applicable management, and is not intended to be and should not be used by anyone other than these specified parties.

Certified Public Accountants Panama City Beach, Florida February 20, 2015

Carr, Riggs & Ingram, LLC

14101 Panama City Beach Parkway

Suite 200

Panama City Beach, FL 32413

(850) 784-6733

(850) 784-4866 (fax)

www.cricpa.com

- 24 -

INDEPENDENT AUDITOR’S REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING AND ON COMPLIANCE AND OTHER MATTERS BASED ON AN AUDIT OF FINANCIAL STATEMENTS PERFORMED IN ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS Board of Commissioners Eastpoint Water and Sewer District Eastpoint, Florida

We have audited, in accordance with the auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards issued by the Comptroller General of the United States, the financial statements of the business-type activities of Eastpoint Water and Sewer District, as of and for the year ended September 30, 2013, and the related notes to the financial statements, which collectively comprise the District’s basic financial statements and have issued our report thereon dated February 20, 2015.

Internal Control over Financial Reporting

In planning and performing our audit of the financial statements, we considered Eastpoint Water and Sewer District’s internal control over financial reporting to determine the audit procedures that are appropriate in the circumstances for the purpose of expressing our opinions on the financial statements, but not for the purpose of expressing an opinion on the effectiveness of Eastpoint Water and Sewer District’s internal control. Accordingly, we do not express an opinion on the effectiveness of Eastpoint Water and Sewer District’s internal control.

Our consideration of internal control was for the limited purpose described in the preceding paragraph and was not designed to identify all deficiencies in internal control that might be material weaknesses or significant deficiencies and therefore, material weaknesses or significant deficiencies may exist that were not identified. However, as described below, we identified certain deficiencies in internal control that we consider to be material weaknesses and significant deficiencies.

A deficiency in internal control exists when the design or operation of a control does not allow management or employees, in the normal course of performing their assigned functions, to prevent, or detect and correct, misstatements on a timely basis. A material weakness is a deficiency, or a combination of deficiencies, in internal control such that there is a reasonable possibility that a material misstatement of the entity’s financial statements will not be prevented, or detected and corrected on a timely basis. We consider the deficiencies described below to be material weaknesses.

13-01 (Prior years 12-01 and 11-01) (initially reported in 2005) Separation of certain accounting and administrative duties among employees, which is recommended as an effective internal control procedure, was inadequate at the District. The District should separate duties so that no one

- 25 -

individual has control over all phases of a transaction. Additional oversight by management and the Board should be implemented in cases where proper segregation of incompatible duties is not considered feasible.

Management’s response - Separation of duties is not considered feasible by the District because of its size and limited number of employees. The Board will continue to closely monitor the District’s activities.

13-02 (Prior years 12-02 and 11-02) (initially reported in 2007) Significant adjustments to the financial records were made in order for the financial statements to conform to U.S. generally accepted accounting principles.

Management’s response - We realize that ideally our internal control system should be designed in a manner that ensures the accuracy of the financial statements and that the auditors should not have to recommend journal entries to see that they conform to generally accepted accounting principles. We don’t feel that in the near future the benefits derived from investing in the resources necessary for us to implement an effective internal control system would outweigh the cost of those resources.

13-03 (Prior years 12-03 and 11-03) (initially reported in 2008) Inadequate design of internal control over the preparation of the financial statements being audited gives rise to a significant deficiency in internal control.

Management’s response - Our auditors assist us with the preparation of our financial statements. We don’t feel that in the near future the benefits derived from investing in the resources necessary for us to prepare our own financial statements would outweigh the cost of those resources.

A significant deficiency is a deficiency, or a combination of deficiencies, in internal control that is less severe than a material weakness, yet important enough to merit attention by those charged with governance. We consider the deficiencies described below to be significant deficiencies.

13-04 (Prior year 12-04) (initially reported in 2012) During the audit we noted that bank reconciliations, while in agreement with year end balances, were not be prepared accurately originally and were not prepared in a timely manner. Inadequate procedures and controls over reconciliation procedures gives rise to a significant deficiency in internal controls.

Management’s response - Due to the changeover in management, there has been a period of adjustment needed by the District's Office Manager. This process has been improving since last year’s audit was completed. We will continue to review the current procedures and controls and adjust them as considered necessary to continue improving in this area.

13-05 (Prior year 12-05) (initially reported in 2012) During the audit, it was noted that the client does not have appropriate bank accounts set up and funded per their bond documents and the resolution approving the bonds. The District should have a reserve fund, a sinking fund, and a short lived asset reserve fund. This gives rise to a significant deficiency in internal control.

Management’s response - We were aware that a reserve fund and a sinking fund were required. These were set up in October of 2012 and appropriately funded. We were unaware of the short lived asset reserve fund until it was brought to our attention by the auditors. We set up the short lived asset reserve fund and appropriately funded it in March of 2014.

- 26 -

Compliance and Other Matters

As part of obtaining reasonable assurance about whether the District’s financial statements are free from material misstatement, we performed tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements, noncompliance with which could have a direct and material effect on the determination of financial statement amounts. However, providing an opinion on compliance with those provisions was not an objective of our audit, and accordingly, we do not express such an opinion. The results of our tests disclosed no instances of noncompliance or other matters that are required to be reported under Government Auditing Standards.

Purpose of this Report

The purpose of this report is solely to describe the scope of our testing of internal control and compliance and the results of that testing, and not to provide an opinion on the effectiveness of the entity’s internal control or on compliance. This report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the entity’s internal control and compliance. Accordingly, this communication is not suitable for any other purpose.

Certified Public Accountants Panama City Beach, Florida February 20, 2015