e-MITRA - NetHope Solutions Centersolutionscenter.nethope.org/assets/collaterals/Panel_1.1...4...

8

e - MITRA Agent Network Models: Lessons from Other Countries Agent Network Strategy Workshop December 6 th 2012

Transcript of e-MITRA - NetHope Solutions Centersolutionscenter.nethope.org/assets/collaterals/Panel_1.1...4...

e-MITRA

Agent Network Models: Lessons from Other Countries Agent Network Strategy Workshop December 6th 2012

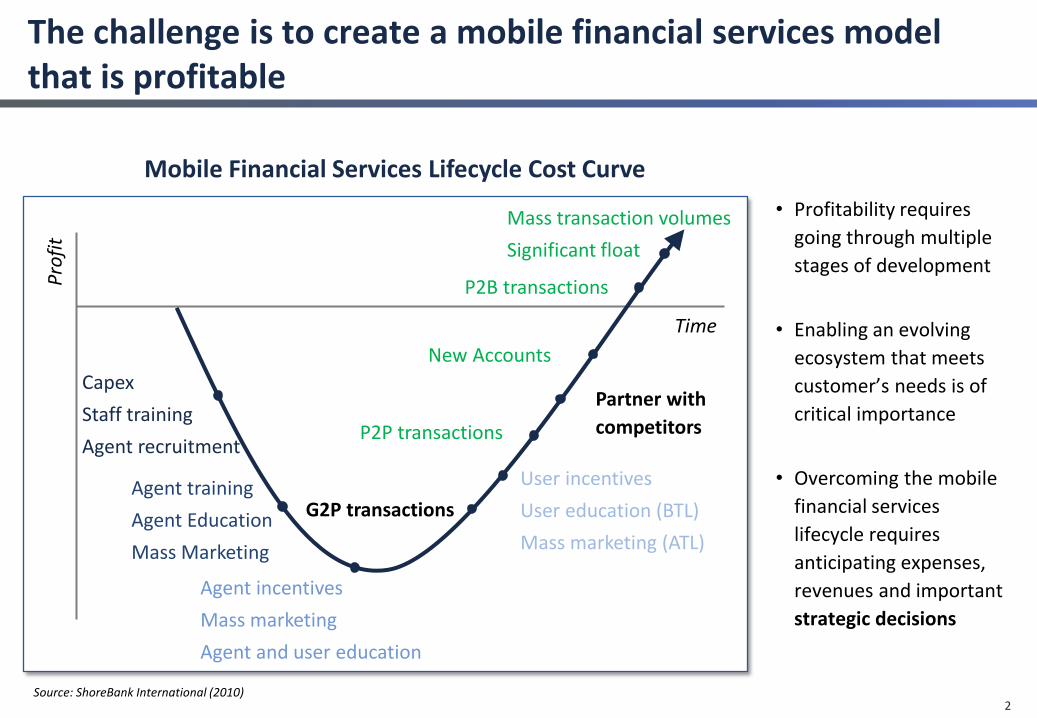

The challenge is to create a mobile financial services model that is profitable

Mobile Financial Services Lifecycle Cost Curve

Capex

Staff training

Agent recruitment

Agent training

Agent Education

Mass Marketing

Agent incentives

Mass marketing

Agent and user education

User incentives

User education (BTL)

Mass marketing (ATL)

Partner with

competitors

G2P transactions

P2P transactions

New Accounts

P2B transactions

Mass transaction volumes

Significant float

• Profitability requires

going through multiple

stages of development

• Enabling an evolving

ecosystem that meets

customer’s needs is of

critical importance

• Overcoming the mobile

financial services

lifecycle requires

anticipating expenses,

revenues and important

strategic decisions

Source: ShoreBank International (2010) 2

Pro

fit

Time

3

Pakistan: UBL Omni

• Leveraging government contracts (G2P) to

roll out agents

• Appropriate agent selection

• Offering services to both walk in and

account holding users

• Appropriate products for target market

Best practices

• ~14% of Pakistanis hold formal bank accounts (~25 mln.)

• However, mobile phone ownership is high: 98 mln. mobile phone connection across 6 mobile

network operators

• UBL is the second largest private bank with assets of $7.5 bln, and operates a networks of over

1,121 branches across the country, with 17 overseas branches and nearly 14,000 employees

• UBL built their mobile banking platform internally

• Creating a new business line within a

commercial bank

• Rapid scaling and customer uptake

• Building an agent network in remote or

conflict areas

• Understanding a new market segment

Challenges

4

Pakistan: Easypaisa

• Easy to use service aimed at low literacy

levels

• Good relation with regulator

• Online real-time KYC validation with

centralized national ID authority

Best practices

• Telenor Pakistan, a major MNO, bought Tameer Microfinance Bank to enter the mobile financial

services market in Pakistan, as the regulator did not allow MNOs to offer these services

• Regulator (State Bank of Pakistan) allowed a flexible approach to launch, now “bank-led” model

• Focused on Over-The-Counter (non-account based) remittance and bill payment transactions.

Now trying to find ways to move from Over-The-Counter to account-based transactions

• 20,000 agents, 160,000 transactions per day, 4 million users per month

• Licensed an internationally recognized mobile financial services software platform to offer

services (Fundamo)

• Moving from over-the-counter to account

based to offer full financial services

Challenges

Source: www.easypaisa.com.pk (November 2012); CGAP (2011)

5

Bangladesh: bKash

• Creating an enabling regulatory

environment

• Strategy partnership with Banks and

NGOs to build business case

• Leveraging networks of partners (e.g.

Telcos, NGOs) to expand agent network

Best practices

• In Bangladesh: 83% of the population lives under $2 a day; less than 15% is formerly “banked”.

• bKash is a join venture of BRAC Bank and Money in Motion.

• Mobile network cover 99% of Bangladesh and mobile phone ownership rates as high as 83% for

urban Bangladeshis and almost 60% of the rural populations.

• bKash was set up as a separate company to provide mobile financial services, giving it more

flexibility and autonomy than a traditional division of a bank.

• Striking the right deal with a vendor and

customizing technology

• Negotiating an agreements with Telcos

• Developing a go to market strategy that

ensures customer uptake

• Developing a robust agent network

Challenges

6

Mobile financial services business models

Role

Account provider Safaricom/M-PESA State Bank of India and other banks

Transaction provider Safaricom/M-PESA FINO

MNO Safaricom Any company

Third-party operators

Banks ATM networks Utility companies

Government, insurance companies

ANMs Aggregators, superagents, and Top Image all play an agent management role

FINO

Agents Independent cash merchants

Trusted community members

Source: CGAP (2011)

7

Key takeaways

• Local delivery is essential for extending the outreach of the bank

• Convincing customers that local/ agent banking is credible requires appropriate targeted marketing

• Designing appropriate products customized for the delivery channels and for the low income market is key

• Costs are very much lower with agent banking initial experience shows that costs are about 80% less than

branch based banking

• However, profits for agents/ intermediaries are through the transaction volumes. Hence, scaling the

number of accounts fast becomes necessary in order to reach profitability – to scale, technology is the

solution

• However, technology in and of itself is not a panacea for branchless banking

– its value to the bank and customer is directly related to trust and functionality

• Training of the agents that deliver services to:

– Serve the customer properly/respectful

– Provide consistent experience to customers through out agent network

– Cross sell to add value and keep the account/customer "sticky"

• Creating awareness among the target market about the available services and products is an important

cornerstone for success Source: ShoreBank International (2011)

8

A profitable mobile financial services model requires thorough strategic planning

Source: ShoreBank International (2010)

Review Landscape

• Who are the competitors and other market players?

• What are the options for an agent network?

Market research

• What is the market demand and need?

• What is the value add of the proposed services? For customers?

Internal Capacity

• What internal capabilities should be built?

• What internal systems are necessary?

Investment & resources

• What are the required investments and who will provide it?

Technology • What technology is required for the

strategy? • Who are the available vendors?

Market strategy

• What type of platform is required? • What are key risk and challenges in

implementing the strategy?

Business case • What type of partnership or

implementation structure is most sustainable and scalable?

Products • Which products are demanded? • Which products should be offered?

Marketing and awareness

• How can you generate awareness rapid scale among customers?