E 4101/5101 Lecture 7: The VAR and econometric models of the VAR · PDF filesimultaneous...

62

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Ragnar Nymoen Department of Economics, University of Oslo 10 March 2011 E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Transcript of E 4101/5101 Lecture 7: The VAR and econometric models of the VAR · PDF filesimultaneous...

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

E 4101/5101Lecture 7: The VAR and econometric models of

the VARRagnar Nymoen

Department of Economics, University of Oslo

10 March 2011

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

Introduction I

I Main references:

I Hamilton Ch 10 and 11.I Davidson and MacKinnon, Ch 13 (note their reference back to

Ch 12.2 on Seemingly Unrelated Regressions, known from e.g.E-4160, and the unrestricted reduced form (URF) of thesimultaneous equations model (also known from E-4160)

I Vector autoregressions, VARs has become widely adopted inmacroeconomics due to the so called Sims’ critique, in Sims(1980).

I In line with this,Hamilton motivates the VAR by its“convenience for estimation and forecasting”: meaning thatVARs are easy to estimate and are useful for forecasting.

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

Introduction II

I The VAR has another very important role as well, as astatistical model that underlies identified structuraleconometric models.

I This role is important both for the stationary case and for thecase with unit-roots and (potential) co-integration. Threetext-books that develop this viewpoint are: Hendry (1955),Johansen (1995) and also Davidson and MacKinnon (2004).

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

The bivariate case—the final equation I

The simplest example is a vector autoregressive process (VAR)with two variables and first order dynamics as in:(

ytxt

)=

(a11 a12a21 a22

)(yt−1xt−1

)+

(εy ,tεx ,t

), (1)

where εy ,t and εx ,t are two white-noise variables (correlated oruncorrelated).

I Notation: Follow H and use yt for both stochastic variableand realization.

I To simplify we have dropped the intercept, (interpret yt andxt as deviations from their respective means)

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

The bivariate case—the final equation II

I White noise disturbances can be replaced by the weakerassumption of innovations with conditional mean zero andconstant conditional covariance matrix. The conditioning ison yt−1 and xt−1.

We now express yt as a function of yt−1 and εy ,t and εx ,t .Solve the first equation for xt−1:

xt−1 = (1/a12)yt − (a11/a12)yt−1 − (1/a12)εy ,t (2)

Substitution in the second equation of the VAR gives

xt =a22a12

yt + (a21 − a22a11a12

)yt−1 −a22a12

εy ,t + εx ,t , a12 6= 0 (3)

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

The bivariate case—the final equation III

Finally: Replace t by t + 1 in the first equation in (1), and replacext by the left hand side of (3):

yt+1 = a11yt + a12a22a12

yt + (a21 − a22a11a12

)yt−1

− a22a12

εy ,t + εx ,t+ εy ,t+1 (4)

(4) is called a final equation. It shows that yt given by the VAR(1) follows the 2 order stochastic difference equation:

yt = (a11 + a22)︸ ︷︷ ︸φ1

yt−1 + (a12a21 − a22a11)︸ ︷︷ ︸φ2

yt−2 + εt . (5)

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

The bivariate case—the final equation IVThe disturbance in the final equation is:

εt = εy ,t − a22εy ,t−1 + a12εx ,t−1

Write the final equation more compactly

φ(L)yt = εt , where (6)

φ(L) = 1− φ1L− φ2L2,

φ1 = (a11 + a22) and φ2 = (a12a21 − a22a11).

The associated characteristic polynomial:

p(λ) = λ2 − φ1λ− φ2. (7)

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

The bivariate case—the final equation VFrom before we know that if the two roots of p(λ) = 0 are bothdifferent from one in magnitude:

1. yt has a stationary solution and

2. yt is weakly stationary (since the stationary solution defines ytas a well defined filter of the stationary input series εt).

If the roots are inside the unit circle: The backward solution isglobally asymptotically stable, and yt is a causal process.The same conclusion follows for xt , if you derive the final equationfor the xt variable.Have found: The stationarity of the vector time series [yt , xt ]

′can

be investigated by deriving the final equations for one of thevariables

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

The bivariate case—the final equation VI

Dynamic multipliers and impulse response functionsNote that the dynamic multipliers for yt

∂yt+s

∂εy ,t

can be found by solving the final equation for yt (5).But from the same final equation we also find the cross-derivatives:

∂yt+s

∂εx ,t

The full set of multipliers is called impulse-response functions inthe VAR terminology.

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

The bivariate case—the companion form I

Let zt denote the vector time series made up of yt and xt . Define

zt = [yt , xt ]′ and εt = [εy ,t , εx ,t ]

′ ,

(1) can be expressed as

zt = Fzt−1 + εt , (8)

where F is the matrix with VAR coefficients, i.e.,

F =

(a11 a12a21 a22

).

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

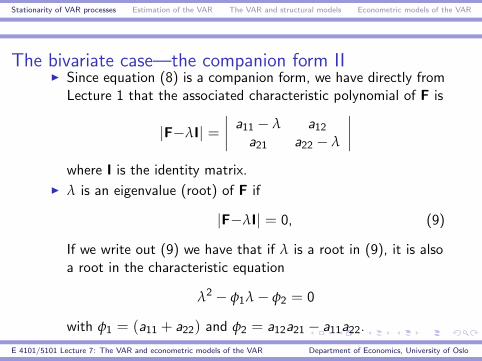

The bivariate case—the companion form III Since equation (8) is a companion form, we have directly from

Lecture 1 that the associated characteristic polynomial of F is

|F−λI| =∣∣∣∣ a11 − λ a12

a21 a22 − λ

∣∣∣∣where I is the identity matrix.

I λ is an eigenvalue (root) of F if

|F−λI| = 0, (9)

If we write out (9) we have that if λ is a root in (9), it is alsoa root in the characteristic equation

λ2 − φ1λ− φ2 = 0

with φ1 = (a11 + a22) and φ2 = a12a21 − a11a22.

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

The bivariate case—the companion form III

F is an example of a companion matrix.Since (9) is the same equation as the characteristic equation forthe final equation for yt , we have that [yt , xt ]′ is a stable processiff the eigenvalues of F have moduli different from 1.

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

The general case: Companion form I

The companion form is well suited for generalizations.Let yt be the n× 1 vector.

yt = [y1t , y2, . . . , ynt ]′

The VAR of or order p is:

yt = φ1yt−1 + φ2yt−2+...+φpyt−p + εt (10)

where φi is a n× n matrix with coefficients and εt is a vector withwhite-noise disturbances that may be correlated

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

The general case: Companion form II

Write (10) in companion form:

ytyt−1...yt−p+1

︸ ︷︷ ︸

ξt n×p

=

φ1 φ2 · · · φp−1 φp

I 0 0 · · · 00 I 0 · · · 0...

......

......

0 0 0 I 0

︸ ︷︷ ︸

Fnp×np

yt−1yt−2

...yt−p

︸ ︷︷ ︸

ξt−1

+

εt

0...0

︸ ︷︷ ︸

vt

,

(11)

ξt = Fξt−1 + vt , (12)

with the symbols in H equation (10.1.11) p 259.

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

The general case: Companion form III

I This VAR (called covariance stationary vector process in Ch10) is stationarity if all the eigenvalues of the companionmatrix F have moduli from

|F−λI| = 0

that are different from zero. See H page 259.

I The VAR is causal if the moduli of all roots are less than 1.

I Note that the number of roots is increasing in both p and n(the length and the size of the VAR).

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

Impulse-response functions I

The vector variable ξt+sabove can be written as

ξt+s =s−1∑i=0

Fivt+s−i + Fsξt (13)

I and for ξt :

ξt =t−1∑i=0

Fivt−i + Ftξ0. (14)

In the maintained stationary case we also have

Ft →t→∞

0

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

Impulse-response functions II

so

ξt =∞

∑i=0

Fivt−i (15)

These expressions are multivariate generalization of thecorresponding from Lecture 1.

I By writing out the first n rows of ξt the solution of vectorvariable yt is seen to be an infinite sum of εt−j with decliningweight, i.e., a convergent sum of the history of εt .

I “The infinite MA representation”

I See H p 260 for the details, which are matrix generalizationsof the expressions we had in Lecture 1 for a single variable.

I The weights are determined by the companion matrix F.

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

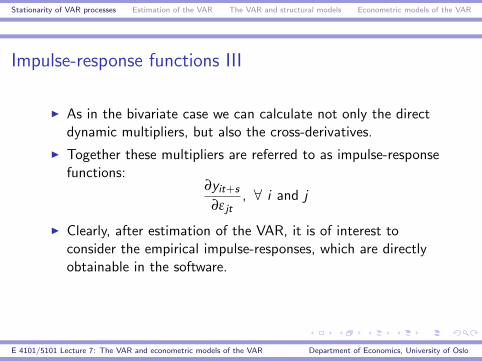

Impulse-response functions III

I As in the bivariate case we can calculate not only the directdynamic multipliers, but also the cross-derivatives.

I Together these multipliers are referred to as impulse-responsefunctions:

∂yit+s

∂εjt, ∀ i and j

I Clearly, after estimation of the VAR, it is of interest toconsider the empirical impulse-responses, which are directlyobtainable in the software.

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

Estimation of the VAR I

I Let the disturbance vector εtbe independent and identicallydistributed with mean zero and covariance Ω,In particularconsider the Gaussian VAR εt ∼ i .i .d N(0, Ω), as inHamilton, p 291.

I For the Gaussian VAR, the OLS estimators of φi ,i = 1, 2, . . . , p, are the Maximum-Likelihood estimators.

I This is a direct extension of the ML theory for the AR-modelof a single time series

I The ML estimators are obtained by OLS on each of the nequations in the VAR—also when Ω contains non-zeroelements off the main diagonal. Why?

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

Estimation of the VAR II

I For the weaker assumption εt ∼ i .i .d with mean zero andcovariance Ω,the OLS estimators have the same asymptoticdistribution as the ML estimators of the Gaussian VAR.

I Note that if the disturbances in one equation are for exampleautocorrelated, the theory does not apply. We then have asituation represented by the models in EBs lecture note 4, 5and 6:

I Then need IV estimators, including GMM

I Hence εt ∼ i .i .d N(0, Ω) with mean zero and covariance Ωis a defining characteristic of the Gaussian VAR, as well as alimitation.

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

How do we test the VAR assumptions? IIn practice we need to

1. Determine the lag length p of the VAR (because it is seldomknown a priori)

2. Check the assumption about the disturbances.

Seldom the case that these two issues can regarded in isolation:Under-specification of p might result in residuals that areautocorrelated. However, we mention the main tools for eachproblem in turn:

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

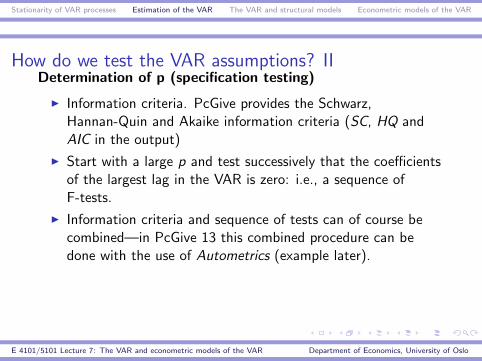

How do we test the VAR assumptions? IIDetermination of p (specification testing)

I Information criteria. PcGive provides the Schwarz,Hannan-Quin and Akaike information criteria (SC, HQ andAIC in the output)

I Start with a large p and test successively that the coefficientsof the largest lag in the VAR is zero: i.e., a sequence ofF-tests.

I Information criteria and sequence of tests can of course becombined—in PcGive 13 this combined procedure can bedone with the use of Autometrics (example later).

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

How do we test the VAR assumptions? IIITesting assumptions about ε it (mis-specifiation testing)

I Since each equation is estimated by OLS, we can use(E-4160) test-battery: autoregresive autocorrelation, ARCHdisturbance, White tests of heteroskedasticity, non-normalitytests.

I PcGive also has vector versions of these mis-specificationtests.

I Note the degrees of freedom tend to be very large for thesetests, so even if the size of the test is OK, mis-specificationmay be hidden (due to low power of test).

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

How do we test the VAR assumptions? IV

Significant departures from the hypothesis of Gaussiandisturbances can often be resolved by

I Larger p

I Increase the dimension (n) of the VAR: more variables in theyt vector.

I Introduce exogenous stochastic explanatory variables: VAR-Xmodel, conditional or partial model.

I Introduce deterministic variables in the VAR.

NOTE:

I The economic relevance of the statistically well specified VARis a matter in itself.

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

How do we test the VAR assumptions? V

I Little help if p is set so large that there are no degrees offreedom left,

I or if VAR-X introduce variables that are difficult to rationalizeor interpret theoretically or historically.

I May then want to estimate simpler model with GMM for eachequation instead.

I However, in this part of the lecture we follow the VARapproach and assume that a congruent (not mis-specified)and relevant VAR can be established.

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

Building flexibility into the VAR IOne natural way to obtain a congruent VAR is (in addition toincrease p and n which are subject to the above caveats) is toinclude deterministic terms.Specifically, the Maximum-Likelihood interpretation of OLSestimators is also valid for the augmented VAR

yt = cdt + φ1yt−1 + φ2yt−2+...+φpyt−p + fixt + εt (16)

where dt is a vector with deterministic variables. For example:

dt = (1, Trendt , dum1t , . . . , dumKt)

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

Building flexibility into the VAR II

dumkt is a dummy variable representing

I Seasonal dummy

I Dummy for structural break (change in mean of yt), or outlier

xt is a vector of conditioning economic variables, and fi is a matrixof coefficients for these variables.

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

The VAR interpreted as a unrestricted reduced form IConsider again the bivariate case of, Xt and Yt and dynamics ofthe first order:The simultaneous equations representation of this dynamic systemis[

1 b12,0

b21,0 1

] [ytxt

]=

[b11,1 b12,1

b21,1 b22,1

] [yt−1xt−1

]+

[εy ,tεy ,t

](17)

where εy ,t are εy ,t uncorrelated Gaussian disturbances.If we start from (17), the VAR in (1) is seen to be a reduced formof the simultaneous equations model:[

a11 a12a21 a22

]︸ ︷︷ ︸

in (1)

=

[1 b12,0

b21,0 1

]−1 [b11,1 b12,1

b21,1 b22,1

]

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

The VAR interpreted as a unrestricted reduced form II

and [εy ,tεx ,t

]︸ ︷︷ ︸

in (1)

=

[1 b12,0

b21,0 1

]−1 [εy ,tεx ,t

].

I Since the simultaneous equation model (17) is “unrestricted”,in fact it is not identified, we call the reduced form of thatmodel the unrestricted reduced form, URF, see Davidson andMacKinnon page 596.

I The VAR disturbances εy ,t and εx ,t are correlated even if (ashere) εy ,t and εx ,t are uncorrelated ( b12,0 6= 0, or b21,0 6= 0).

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

The VAR interpreted as a unrestricted reduced form IIII This removes the interpretability of the impulse responses

since for example∂yt+s

∂εy ,t

is in general not interpretable as the effect on yt+s of a shockto y in period t.

I This shows that the unrestricted VAR is not a structuralmodel.

I It would not help to estimate (17) in this case, since neitherequation is identified on the order condition.

I In fact, the under-identification of the simultaneous equationmodel (17) and the non-structural VAR is one and the samething: It is all about lack of identification.

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

The VAR interpreted as a unrestricted reduced form IV

I The VAR has unidentified impulse-responsesI The simultaneous equations model (17) is not identified on the

rank and order conditions for a simultaneous equation model.

I “Fork in the road”:

I “Sim’s followers to the left”.I “Those who want to keep the systems of equations model,

SEM, to the right”

I We will take the SEM route in this course.

I Our programme will be to regard the VAR as the statisticalmodel of the system and try to specify structural econometricmodels that do not “throw away information”, but insteadencompass the VAR.

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

SVARs and identified SEMs I

I One popular way to identify the impulse-response, thusobtaining a structural VAR, a SVAR, is to replace εy ,t andεx ,t by a pair of uncorrelated disturbances (orthogonalizedinnovations in Hamilton’s terminology).

I This is called the Cholesky decomposition/factorization (thetheorem is in H Ch 4.4 p 91-91), while the application to ourcase is on page 320 (orthogonalization) and 327-330(identification of impulse-responses)

I The Cholesky factorization is equivalent to choosing arecursive system of equations model.

I “xt causally prior to yt” ⇐⇒ b21,0 = 0

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

SVARs and identified SEMs III So could estimate the recursive SEM in the first place. (There

is nothing saying that a structural economic model cannot berecursive!)

I Other ways to identify the VAR impulse-responses involvesmore complicated operations on the VAR covariance matrix.See the last sections of Hamilton’s Ch 11.

I The main, and general, message are that these restrictions areequivalent to restrictions on the contemporaneous and/orlagged coefficients of the SEM representation of the system.

I There is no way around solving identification with reference toa theoretical framework.

I The difference between the SVAR route and the SEM routemay not be as large as one may think

I A choice of “how to” express one’s theory?

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

Confidence intervals for impulse-respones I

I Hypotheses that can be formulated as linear restrictions onthe VAR are easy to test: t-test and F-tests.

I Inference about the significance of the impulse-responses isanother matter

I Apart from the simplest case (AR(1)) the standard errorsneeded to construct confidence intervals are complicated, asHamilton Ch 11.7 shows.

I In addition, difficult to interpret the relevance of a significantbut unidentified dynamic multiplier.

I For (identified) SVARs, an given the increased computationpower, the current practice is to use Monte-Carlo simulationto construct confidence intervals.

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

Confidence intervals for impulse-respones II

I Regard the estimated VAR as the true DGP (may want torelax assumption about exact Gaussian distribution perhaps).

I Generate many thousand data sets.I Estimate and calculate the impulse-response functions for each

replication.I The confidence interval can be constructed as the intervall

that excludes the lowest 2.5 percent and the highest 2.5percent for example

I The simulation based method can also be used for (largescale) SEM, which is one way of obtaining identified VARs.

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

Why are confidence intervals so wide? I

I As noted by Hamilton, p 339, the practical experience withconfidence intervals from VARs are that they are“disappointingly wide”. H gives two interpretations and cures:

I Impose more restrictions on the estimated VAR beforecalculating impulse-responses (their insignificance is due toinefficient estimation)

I Impose more restriction on the system dynamics from theoutset (do Bayesian economtrics instead, See Ch 12)

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

Why are confidence intervals so wide? II

I There is third interpretation as well: The information set (thevariables in the VAR and whether exogenous explanatoryvariables are included or not) may have little relevance for thetask of estimating the dynamic multipliers with any precision.

I Dynamic multipliers are like other partial derivatives: They areextremely responsive to omitted variables bias.

I This suggest that more modeling, rather than less, may thesolution in some cases.

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

Open and closed systems I

I The extended VAR in (16) contained a vector of endogenousvariables yt and a vector of unmodeled variables xt . Thereforethis kind of system is called an open VAR.

I Open systems impose untested exogeneity assumptions.

I This does not mean that they are “suspect” or “inferior” toother systems.

I Not obvious that it is interesting test the exogeneity of worldGDP for a small open economy for example. But more aboutthat later.

I We consider closed systems at this stage because they make iteasier to show how certain popular econometric model can bedeveloped from the VAR, as the statistical model of thesystem.

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

Open and closed systems II

I We will use the bivariate VAR in (17) since the lowdimensionally of the VAR and the short lag length easeexposition without (much) loss of generality.

I For simplicity we also assume Gaussian errors.

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

Simultaneous equation and recursive models

I The first model class, which is the simultaneous equationsmodel representation of the VAR has already been mentioned.

I Relevance of this model hinges on identification.I Estimation of identified model structures can be done by

familiar system methods: 2SLSL, 3SLS and FIML. We will seeexamples

I Recursive system

I As we have seen, a special form of identificationI Estimation by OLS, equation by equation

I Combinations are possible: We then speak of block-recursivesystems. Operational macro models are often of thiscombined type. Will also combine several estimation methods

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

Conditional and marginal model I

I A VAR can always be re-parameterized in terms of aconditional model and a marginal model.

I The relevance of the conditional model stems from the factthat it can often, but not always, contain parameters ofinterest (i.e., in terms of economic theory or for the purposeof the analysis).

Write the VAR (1), the URF relative to the SEM (17), as

yt = µy ,t−1 + εy ,t (18)

xt = µx ,t−1 + εx ,t (19)

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

Conditional and marginal model IIwhere (

εx ,tεy ,t

)∼ N

(0,

(σ2x ωxy

ωxy σ2y

)| xt−1, yt−1

). (20)

The conditional distribution of εx ,t and εy ,t is bi-variate normal(with expectation zero and covariance(

σ2x ωxy

ωxy σ2y

).

The conditioning is on xt−1 and yt−1.The correlation coefficient between εx ,t and εy ,t is

ρxy =ωxy

σxσy.

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

Conditional and marginal model III

µx ,t−1 and µx ,t−1 are the expectations of Xt and Yt conditional onthe pre-history, xt−1 and yt−1:

µy ,t−1 = E[yt | xt−1, yt−1] = a11yt−1 + a12xt−1 (21)

µx ,t−1 = E[xt | xt−1, yt−1] = a21yt−1 + a22xt−1 (22)

yt and xt in (18) and (19) are also bi-variate normally distributed.

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

Conditional and marginal model IVThe distribution of yt conditional on xt , xt−1, yt−1 is also normal,with expectation

E[Yt | xt , xt−1, yt−1] = µy ,t−1 − ρxyσyσx

µx ,t−1 + ρxyσyσx

xt

=ωx y

σ2x

xt + (a12 −ωx y

σ2x

a22)xt−1

+ (a11 −ωx y

σ2x

a21)yt−1.

If we defineεt = yt − E[yt | xt , xt−1, yt−1] (23)

we obtain the first order autoregressive distributed lag model,ARDL:

yt = φ1yt−1 + β0xt + β1xt−1 + εt . (24)

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

Conditional and marginal model V

The disturbance εt can alternatively be written εt

εt = εy ,t −ωx y

σ2x

εx ,t (25)

because

E[εy ,t | εx ,t , xt−1, yt−1] =ωx y

σ2x

εx ,t

from the properties of the normal distribution. Sinceεx ,t = [xt − E[xt | xt−1, yt−1], we can write the conditioning on xt ,hence.

E[εy ,t | xt , xt−1, yt−1] =ωx y

σ2x

εx ,t .

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

Conditional and marginal model VIThe disturbance εt in the ARDL model for yt is conditionallynormal with mean 0, and variance σ2

εt ∼ N(0, σ2 | xt , xt−1, xt−1).

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

Conditional and marginal model VIIIn sum the VAR is modelled by the ARDL equation

yt = φ1yt−1 + β0xt + β1xt−1 + εt . (26)

E[εt | xt , xt−1, yt−1] = 0

Var[εt | xt , xt−1, yt−1] ≡ σ2 = σ2y (1− ρ2xy ), (show)

φ1 = a11 −ωx y

σ2x

a21, β0 =ωx y

σ2x

,

β1 = a12 −ωx y

σ2x

a22.

and the marginal equation for xt :

xt = a21yt−1 + a22xt−1 + εx ,t (27)

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

Conditional and marginal model VIII

(26) can be estimated by OLS which is conditional FIML for thecase of Gaussian disturbances.

I If our purpose is to test hypotheses about the parameters inthe conditional model , we do not need to estimate themarginal model (27).

I If the purpose is forecasting, or policy analysis (what happensif there is a change in the marginal model?), the marginalmodel must also be estimated.

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

Sequential conditioning—the general case I

I The derivation of the ARDL(1, 1) was by sequentialconditioning: First we conditioned on the history (yt−1 andxt−1), and then we conditioned on current xt .

I This approach is general and can be used to derive, from alarge joint distribution (many variables and long lags), aconditional model.

I For example, the ARDL(p, p)

yt −φ1yt−1− . . .−φpyt−p = β0xt + β1xt−1+ . . .+ βpxt−p + εt ,(28)

can be derived from a pth order Gaussian in yt and xt .

I By the same token: Can also have n− 1 different x variablesin the conditional model, if the initial VAR is of dimension n.

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

Equilibrium correction model I

The conditional ARDL can be re-parameterized as an equilibriumcorrection model, ECM.For the first order model (with intercept φ0 added):

∆yt = φ0 + β0∆xt + (φ1 − 1)yt−1 + (β0 + β1)xt−1 + εt

∆yt = β0∆xt

+ (φ1 − 1)

yt−1 −φ0

(1− φ1)− (β0 + β1)

(1− φ1)xt−1︸ ︷︷ ︸

y ∗t−1

+ εt

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

Equilibrium correction model IIDefine

y ∗t =φ0

(1− φ1)− (β0 + β1)

(1− φ1)xt−1

as the conditional equilibrium path for yt , thenequilibrium-correction is seen to be the obvious name for thisparameterization of the model.Recall from the first lecture that equilibrium correction is inherentfor stationary variables. For β0 = β1 = 0, the solution can bewritten:

yt =φ0

1− φ1︸ ︷︷ ︸y ∗

+

y0 −φ0

1− φ1︸ ︷︷ ︸y ∗

φt1 +

t−1∑i=0

φi1εt−i .

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

Equilibrium correction model III

For p = 4 (with intercept φ0 added)

yt −4

∑i=1

φi yt−i = φ0 +4

∑i=0

βixt−i + εt , (29)

one possibility is to put the levels term at the fourth lag

∆yt = φ0 +3

∑i=1

φ†i∆yt−i +

3

∑i=0

β†i ∆xt−i (30)

+ (φ(1)− 1)yt−4 + β(1)xt−4 + εt

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

Equilibrium correction model IV

where φ(1) is φ(L) with L = 1, β(1) is the same for β(L).

φ†i =

i

∑j=1

φj − 1, i = 1, 2, 3, (31)

β†i =

i

∑j=0

βj , i = 1, 2, 3.

Alternatively,put the level-terms at the first-lag

∆yt = φ0 +3

∑i=1

φ‡i∆yt−i +

3

∑i=0

β‡i ∆xt−i (32)

+ (φ(1)− 1)yt−1 + β(1)xt−1 + εt

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

Equilibrium correction model V

φ‡i= −

4

∑j=i+1

φj , i = 1, 2, 3,

β‡0 = β0 (33)

β‡i = −

4

∑j=i+1

βj , i = 1, 2, 3.

In both cases the long-run multiplier with respect to xt is

K1 =β(1)

1− φ1(1)=

∑4j=0 βj

(1−∑4j=1 φj )

(34)

β†0 = β

‡0 = β0, (35)

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

Equilibrium correction model VI

but the other parameters are not the same in the two versions.

φ†i 6= φ‡

i, i = 1, 2, 3, (36)

β†i 6= β

‡i , i = 1, 2, 3. (37)

I ECMs are more flexible than this.

I The AR lag length and the DL lag length need not be thesame.

I The levels of y and x can be on different lags.

I The long run multiplier K1 is invariant to the different ways ofwriting the ECM.

I But the interim multipliers are affected (as illustrated)

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

Matrix notation for ECM IMatrix-notation for the ECM with one xt variable (m lags):

∆yt = z′1tb1 + z′2tb2 + εt (38)

z′1t = (1, ∆yt−1, ∆yt−2, . . . , ∆yt−p+1, ∆xt , ∆xt−1, . . . , ∆xt−m+1),

z′2t = (yt−p,xt−m),

b1 =

φ0

φ†1...

φ†p−1β†0...

β†m−1

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

Matrix notation for ECM II

b2 =

((φ(1)− 1)

β(1)

)=

(φ∗

β∗

).

(38) is a 1-1 linear transform of the ARDL(p, m) and therefore allresults for the OLS estimators also holds for b1and b2.The estimate of the long-run multiplier K1 is non-linear

K1 =β(1)

− (φ(1)− 1)≡ β∗

−φ∗,

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

Matrix notation for ECM IIIHowever,

√Var[K1]can be obtained by the so called

Delta-method, see Bardsen (1989) :

Var[K1] ≈(

1

−φ∗

)2

Var(β∗) +

(β∗

(−φ∗)2

)2

Var(φ∗) (39)

+ 2

(1

−φ∗

)(β∗

(−φ∗)2

)Cov(β∗, φ∗).

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

Matrix notation for ECM IV

This also applies to an ECM with k explanatory variables xjt (withlag order mj), i.e. the approximate variance of

Kj =βj (1)

− (φ(1)− 1)≡

β∗j−φ∗

,

is given by (39), with an obvious change in notation.

I

√Var[Kj ] is available directly in PcGive.

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

A potential misundertanding—and looking ahead I

Although we have derived the ECM as a single equation model,estimateable by OLS, this does not mean that ECMs aresynonymous with single equations and OLS estimation

I We derived our ECM from a bi-variate VAR.

I Already with three variables in the VAR , yt , xt , zt ,newpossibilities for model formulation by sequential conditioningemerges:

I Can for example condition on xt (and the history of xt).

I This replaces the 3-variable VAR by a bi-variate VARX whichis conditional on xt .

I With Gaussian disturbances both the VAR and the VARX areGaussian statistiscal models.

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

A potential misundertanding—and looking ahead II

I The VARX can be modelled in its turn, for example:

I Simultaneous equation modelI Recursive system and conditional system

I If the order of dynamics of the VARX is 2 or higher, all thesemodels can be put in “ECM form”.

I In the simultaneous equation model, the ECM structuralequations are estimated by 2SLS or FIML

I We will return to these point after the co-integration theory

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo

Stationarity of VAR processes Estimation of the VAR The VAR and structural models Econometric models of the VAR

References

Bardsen, G.: “Estimation of Long-Run Coefficients inError-Correction Models” Oxford Bulletin of Economics andStatistics, 51, 345-350.Hendry, D. F. (1995) Dynamic Econometrics, Oxford UniversityPressJohansen, S. (1995) Likelihood-based Inference in CointegratedVector Autoregressive Models, Oxford University Press.Sims, C. A. (1980) Macroeconomics and Reality, Econometrica48,1—48

E 4101/5101 Lecture 7: The VAR and econometric models of the VAR Department of Economics, University of Oslo