DYNAMICS OF CHANGE IN THE SUGAR INDUSTRY … Dubb - small scale cane growers2...DYNAMICS OF CHANGE...

30

Alex Dubb (PLAAS Mphil student) DYNAMICS OF CHANGE IN THE SUGAR INDUSTRY AND IMPLICATIONS FOR LAND AND AGRARIAN REFORM: THE RISE AND FALL OF SMALL-SCALE GROWER PRODUCTION

Transcript of DYNAMICS OF CHANGE IN THE SUGAR INDUSTRY … Dubb - small scale cane growers2...DYNAMICS OF CHANGE...

Alex Dubb (PLAAS Mphil student)

DYNAMICS OF CHANGE IN THE SUGAR INDUSTRY AND IMPLICATIONS FOR LAND AND AGRARIAN REFORM:

THE RISE AND FALL OF SMALL-SCALE GROWER PRODUCTION

Outline

Relocate the political-economy of the rise (and fall)

of Small Scale Grower (SSG) production

Results from fieldwork

Socio-economic survey data

Different trajectories

Implications For Policy

The Rise and Fall of SSG Production

Pictured: A local short-haul tractor team unloading cane

The Rise and Fall of SSG Production

From 1974-2000s, rapid rise of SSGs farming in newly consolidated Bantustans, supplying centralized miller-processors.

3,455 in 1973 to near 50,000 in early 2000s

‘Success’ of commercial production, private sector led-development etc.

Conventional story centred on Financial Aid Fund (FAF) providing small scale credit from 1974

From mid-2000s, rapid decline

30,000 registered SSGs, of which less than 14,000 delivered cane in 2011

End of FAF/UAF in mid 2000s – high defaults, cheating, write offs

Attributed to:

Widespread drought

High costs of production, labour, transport etc.

Small land sizes constrained by customary tenure

Low levels of education, training, numeracy, literacy, book-keeping etc.

The Rise and Fall of SSG Production

Certainly all factors but:

Droughts in 1980s….

High fuel and transport costs in 1970s…

Small (but unequal) land sizes an enduring feature of

former Bantustans….

Low levels of education, training, numeracy, literacy too

So what changed?

Must problematize the story of the rise of SSGs production

Industry promotion of FAF as a ‘development agency’

obscured its actual functioning

The Rise and Fall of SSG Production

The KwaZulu connection:

Institutional: Authority over land held by KwaZulu state, thus effectively holds

sugar quotas. Requires close political cooperation with KwaZulu state and local

inkosi.

Material:

KwaZulu provides over 60 extension officers

‘Development Corporations (BIC/CED/KFC) provide soft loans to millers for on-

lending to small-growers, contractors and infrastructure (roads, loading zones etc)

SASA chairman 1981: “It is estimated that the infrastructure provided by KwaZulu

has to date matched in value the loans advanced by the Fund.’’

Political: Validation of ‘separate development’ e.g: failure to expand would ‘’cause

scepticism among the KwaZulu people regarding statements by leaders of the sugar

industry that it is in the interests of the country to ensure positive economic development for

Black people’’

The Rise and Fall of SSG Production

Hidden Subsidies/Benefits to Milling Capital

Cost-Based Division of Proceeds (DoP): In order to ensure an equitable

split of proceeds between millers and growers, the total average costs

of each section would be deducted from total industry proceeds (with

the balance allocated according to ‘Return on Capital’).

The costs of administration and implementation of FAF and miller subsidiary

‘development companies’ were accounted as ‘milling costs’, thus effectively

deductible from total industry proceeds through the DoP.

All SSG production categorically receives higher A-pool prices for their

cane.

millers could thus increase their claim on the (higher priced) domestic market

proceeds by increasing the SSG proportion of their cane supply.

The Rise and Fall of SSG Production

Rahman (1997): Development companies enjoy 3 bonuses:

‘’The first involved political and financial backing by state agencies,

the second concerned the operation of the FAF credit system which came tied with their services;

the third is the attribution of their overheads and variable costs as milling costs by their miller parents. As milling costs, though they are in reality sugar growing costs, they went towards the cost based division of proceeds’! These development companies not only did profitable business with smallholders, they recouped their overheads and variable costs in the division of proceeds’’

The Rise and Fall of SSG Production

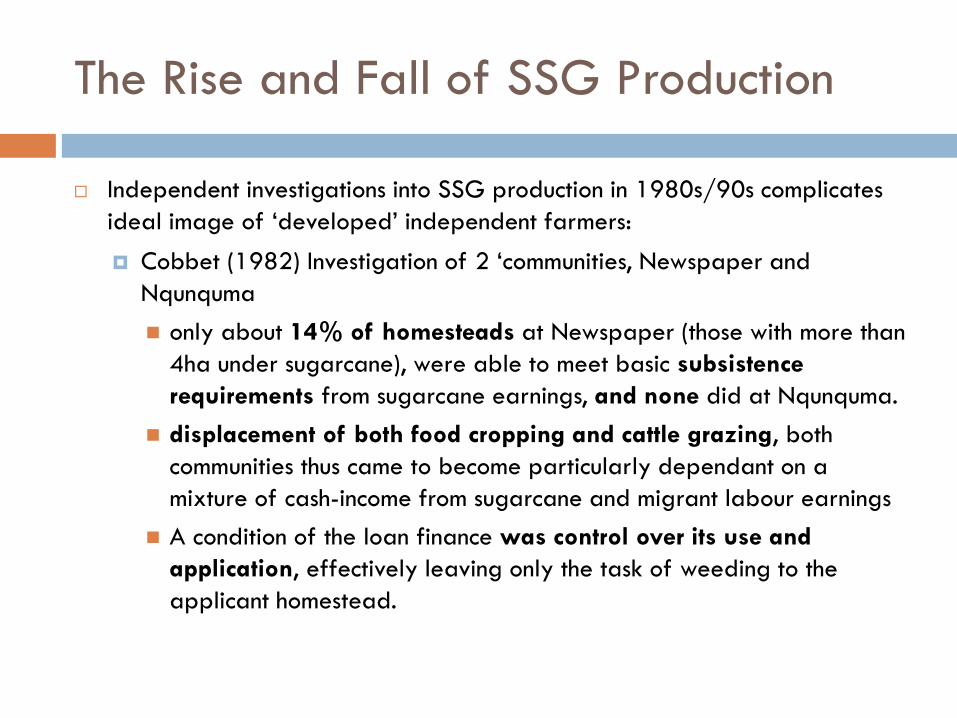

Independent investigations into SSG production in 1980s/90s complicates

ideal image of ‘developed’ independent farmers:

Cobbet (1982) Investigation of 2 ‘communities, Newspaper and

Nqunquma

only about 14% of homesteads at Newspaper (those with more than

4ha under sugarcane), were able to meet basic subsistence

requirements from sugarcane earnings, and none did at Nqunquma.

displacement of both food cropping and cattle grazing, both

communities thus came to become particularly dependant on a

mixture of cash-income from sugarcane and migrant labour earnings

A condition of the loan finance was control over its use and

application, effectively leaving only the task of weeding to the

applicant homestead.

The Rise and Fall of SSG Production

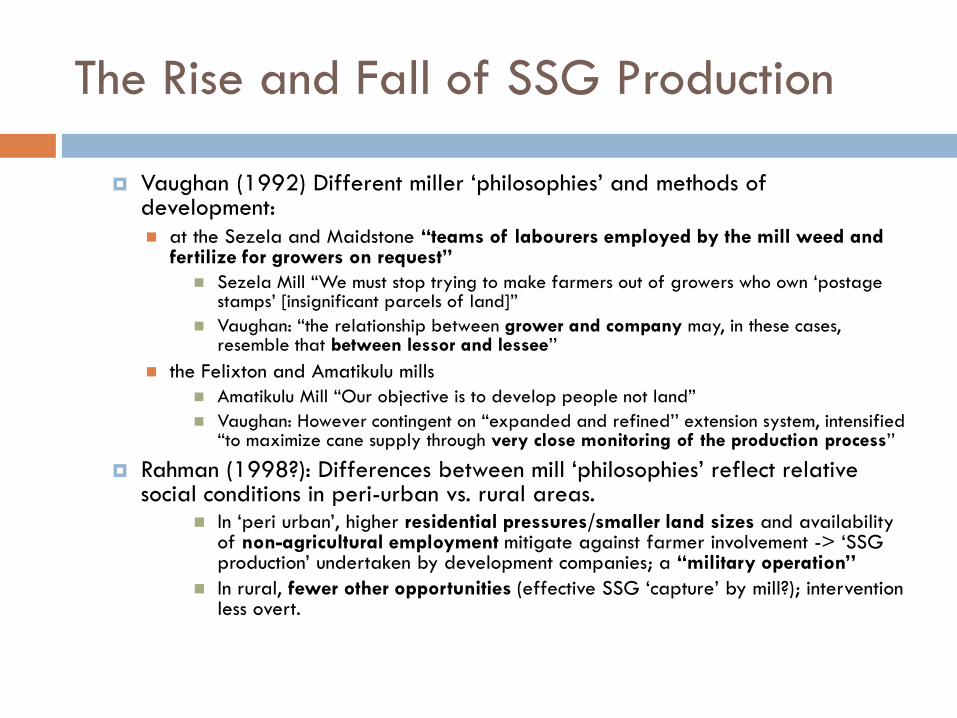

Vaughan (1992) Different miller ‘philosophies’ and methods of development:

at the Sezela and Maidstone “teams of labourers employed by the mill weed and fertilize for growers on request”

Sezela Mill “We must stop trying to make farmers out of growers who own ‘postage stamps’ [insignificant parcels of land]”

Vaughan: “the relationship between grower and company may, in these cases, resemble that between lessor and lessee’’

the Felixton and Amatikulu mills

Amatikulu Mill “Our objective is to develop people not land”

Vaughan: However contingent on “expanded and refined’’ extension system, intensified “to maximize cane supply through very close monitoring of the production process’’

Rahman (1998?): Differences between mill ‘philosophies’ reflect relative social conditions in peri-urban vs. rural areas.

In ‘peri urban’, higher residential pressures/smaller land sizes and availability of non-agricultural employment mitigate against farmer involvement -> ‘SSG production’ undertaken by development companies; a “military operation’’

In rural, fewer other opportunities (effective SSG ‘capture’ by mill?); intervention less overt.

The Rise and Fall of SSG Production

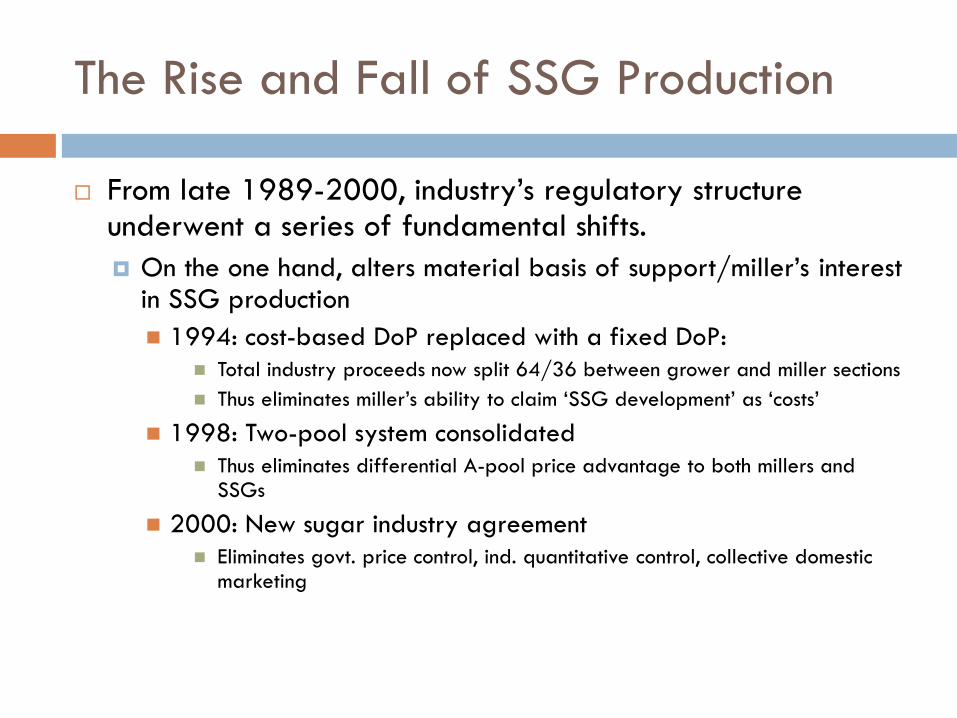

From late 1989-2000, industry’s regulatory structure underwent a series of fundamental shifts.

On the one hand, alters material basis of support/miller’s interest in SSG production

1994: cost-based DoP replaced with a fixed DoP:

Total industry proceeds now split 64/36 between grower and miller sections

Thus eliminates miller’s ability to claim ‘SSG development’ as ‘costs’

1998: Two-pool system consolidated

Thus eliminates differential A-pool price advantage to both millers and SSGs

2000: New sugar industry agreement

Eliminates govt. price control, ind. quantitative control, collective domestic marketing

The Rise and Fall of SSG Production

On the other hand: from 1989 quota restrictions lifted and

ultimately abolished.

7,500 previously illegal growers incorporated, bringing the total number

of registered SSGs to over 30,000, which by 1992 had grown to 42,313

By 2000 estimates of growers in the range of 50,000

Sokhela and Bates (2003) 50% of total production originated from

only 20% of growers

Munro (1996) under-resourced/capacitated/willing growers entering into

a number of, often ultimately conflictual, lease-hold arrangements with

other better resourced growers

Thus paradox of rising SSG registration in tandem with

decline of close monitoring/control over production

The Rise and Fall of SSG Production

Basis of support to SSGs similarly began process of considerable change.

Without direct financial incentive for oversight by millers, new attempts aimed at entrenching new levels of independence and self-representation:

1992: Small Grower Development Trust

instituted to ‘’promote economic empowerment of SSGs and also to develop viable and independent cane growing communities’’.

Has trained 20,000 SSGs, but has not become financially self sustaining.

1996: Joint Venture between SASRI and DAEA to provide extension services.

SACGA posts Grower Support Officers in each mill supply area for administrative assistance, esp i.r.t more inclusive representational structures.

Insufficient replacement for the teams of mill extension and administrative staff

2001: FAF re-launched as Umthombo Agricultural Finance (UAF), with stricter screening criteria.

Compelled to rely on a total staff of 35; 18 of which would be stationed in mill areas, and 8 who operated as loan officers.

By mid-2000s, however had discontinued its credit services

New attempts to re-introduce credit via MAFISA programme

Thus massive increase in SSG numbers quickly followed by complete restructuring of original (rather draconian) production systems.

Decline represents a ‘bubble’ popped by the ‘needle’ of drought

Evidence from Umfolozi

Pictured: The Umfolozi Sugar Mill (USM)

Evidence from Umfolozi

Two adjacent wards of Madwaleni and Shikishela within the Mpukunyoni tribal authority; approximately 30+ km from Mtubatuba and the Umfolozi Sugar Mill (USM)

‘extensive’ phase of administering a survey of 70 registered sugarcane-growers in distinct homesteads,

‘intensive’ phase of conducting supplementary ‘life history’ interviews with a selected 20 sugarcane grower homesteads; attending 3 Development Committee Meetings, 2 Local Association meetings, 1 MCC meeting, 1 Pest and Disease meeting, and associated interviews with mill and grower support staff.

USM has a peculiar history:

cooperatively owned by its large-scale white commercial cane suppliers (UCOSP)

purchased by Illovo in 1992 ->sold to Patrick Sokhela in 2005 -> unwillingly re-purchased by Illovo but sold in 2009 to a consortium including UCOSP; UVS; Charles Senekal and NCP Alcohols. Currently a scheme is underway to facilitate SSG purchase of a 7% interest in USM as well

Evidence from Umfolozi

2010 SACGA recorded 7,494 registered SSGs supplying USM, of which 2,779 delivered that year

Witnessed a sharp decline in SSG production, which has since decreased from a peak of about 400,000 tons in 2000 to about 100,000 tons in 2010

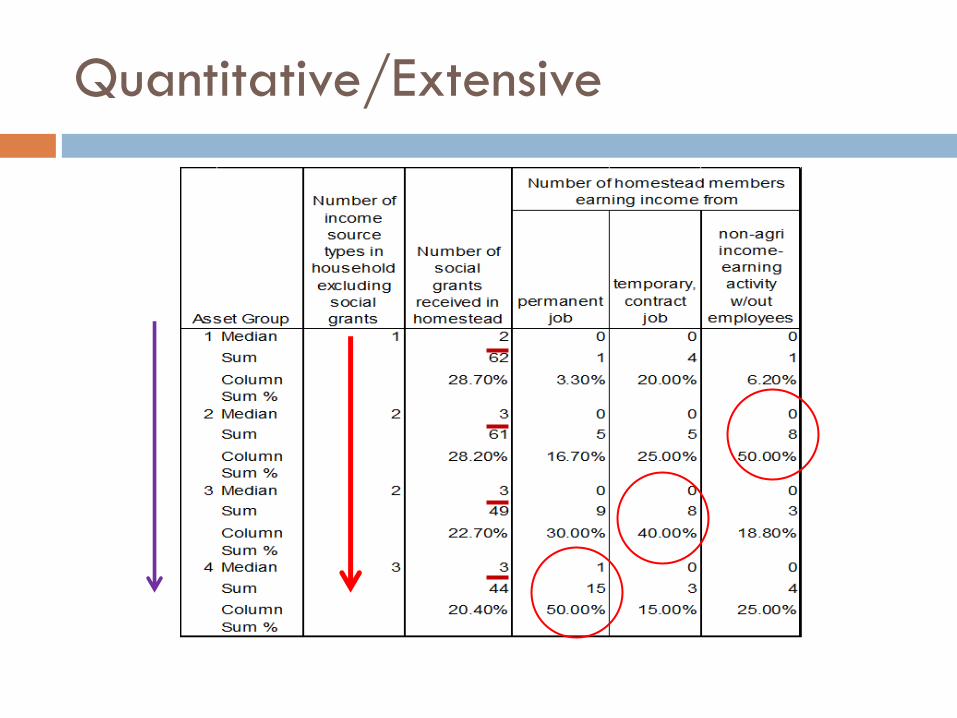

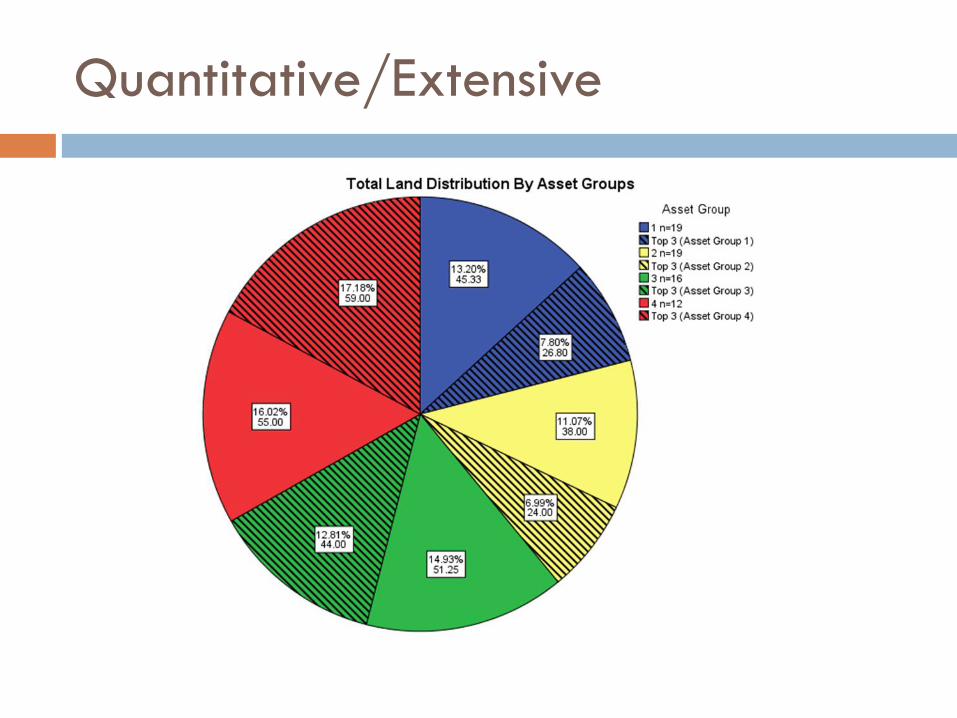

Quantitative/Extensive: Distributions By Asset Groups

Pictured: Ma Magwaza & resident homestead family

Quantitative/Extensive

Quantitative/Extensive

Quantitative/Extensive

Pictured: Mr Mngenge and Ma Buthelezi

QUALITATIVE/INTENSIVE: SSG TRAJECTORIES

Qualitative/Intensive

Grower Trajectories

Borrow typology from Scoones et al (2011)

Stepping Up (4 homesteads)

All own tractors and perform transport and/or ploughing services (‘contractors’)

All have significant land endowments, have purchased land at some point, and are expanding their area under production

All attribute their success to effective cross-subsidization of their contracting/sugarcane operations

But bulk of income from ‘contracting’ rather than sugarcane (R30-80,000 vs R10-40,000)

Hanging In (2 homesteads)

1: a female SSG and HH in asset group 3, has maintained full production on 6ha. She claims to have done so despite not hiring any outside labour, subsisting from social grants and selling reed mats, and reinvesting cane proceeds in inputs. Profits have largely been directed towards the now completed college education of her children, and who now require cattle for lobola purposes.

2: a male grower and contractor in asset group 4, has maintained full production on 12ha. There are no forms of direct employment in the homestead, although 4 homestead members engage in casual agricultural labour, and also run a small local tuck shop. Despite maintaining full cane production, his 3 tractors are currently in a state of disrepair, and he relies on loans with up to 30% interest from a local money lender to refurbish them annually.

Qualitative/Intensive

Stepping Out (2 homesteads) & Stepping Down (3 homesteads)

In all cases, the significant drops in production were conventionally explained as due to a cycle of declining returns and input/labour purchases in a context of drought.

‘Stepping Out’ both in highest asset quartile have access to significant land holdings (8ha & 6ha) but cane only on 1 & 2ha. Both have access to significant off-farm income from permanent employment, seeking

‘Stepping Down’:

Polygamous wife, asset group 2, husband ceased to support her, employed son helps to purchase inputs for 1ha of cane(of 2ha)

Induna, asset group 1, 8ha -> 1ha

Former wage labourer turn PCP, asset group 1; 11 ha -> 4ha. Survived only from cane after years of wage labour, used FAF when hit 11ha. Tractor now broken, applied for social grants for first time in 2010.

Dropping/Dropped Out (7 homesteads)

All female growers, 5 also homestead heads.

5/7 cases cane was started by male partner or with wages from a male partner since deceased/incapacitated

2/7 cane was started by renting land to a neighbour

falling out of cane production has had differential impact:

Those with pensions/access to permanent employment stabilized consumption

Those without = only homesteads reliant chiefly on wages from casual agricultural labourer

Both renting land to a neighbour to re-start production

Qualitative/Intensive

Creeping back? (2 homesteads)

Both in lowest asset quartile with no access to employment income but with 5ha of land

Attempting to expand production by incrementally expand production proportionate with marginal reinvestment from cane submissions.

The essential strategy entails utilizing a portion of annual cuttings as seedcane and using proceeds from submitted balance of the harvest to finance input purchases, whilst relying exclusively on social grants to maintain consumption.

Implications For Policy

Pictured: A casual sugarcane labourer after harvest

Implications for Policy

Not ‘independent’ or ‘yeoman farmers’

Relatively subordinate role of sugarcane production to simple reproduction/survival

Focal tension between using vs. re-investing cane-proceeds Re-investment premised on stabilized homestead consumption fund

(largely by by social grants),

And expanded investment fund premised on contributions from non-cane income (varying grades of employment; contracting)

Cane remains a relatively accessible potential site of investment But decreasing returns, making less attractive.

Diversification for survival/basic reproduction vs. diversification for accumulation

Implications for Policy

Labour Intensive? Labour expensive and difficult to mobilize, particularly at peak periods, such as harvesting

Prevalence of social grants mitigate ‘desperation’ and raise wage premium (monetization of relations of reciprocity?). Need immediate payment.

Family labour similarly difficult to discipline; children at school, seeking work etc. Also demand pay.

Labour-saving inputs (e.g chemicals) often preferred, but also expensive.

Expensive/Inadequate services No regular contact with extension officers

Ploughing a big initial cost

Transport:

Two points of transport: from field to LZ (black tractor owners) LZ to mill (private haulier company trucks)

Remaining black contractors (the ‘big winners’) few, overstretched, substandard services (also in ploughing) engage in price-fixing

Contributes to compounding logistical problems (incl. harvesting, ticket allocation, trucks) resulting in long delays

Grower pays twice for transport: first direct payment (avg 33% of revenue); second in lost sucrose content

Implications for Policy

Current initiatives to support SSGs not insubstantial, but insufficient:

Focus on adapting SSGs to prevailing commercial conditions with market-friendly institutional mechanisms, not necessarily well adapted to SSG’s own productive conditions

E.g MAFISA

Frustrated by SSG characteristics (illiteracy, small land sizes etc.) and failure to ‘develop’ (despite 40+ years of ‘development’!)

The origins of SSG production, however, lies equally in adapting commercial conditions to SSG production i.e. through regulatory interventions

Should consolidate gains since 2000s, e.g greater levels of representation at mill level.

Implications for Policy

Three proposals:

1. Differential pricing for SSG production

Increase SSG cane prices, miller sugar prices from SSG production

Increase miller incentive to increase SSG proportion of production/ extend services, increase SSG bargaining power

Effectively a transfer from LSCF and millers w/out SSG

2. Sharing Transportation Burden

Reliant on increased returns to SSG production

a) Increase miller capacity to employ personnel to oversee logistics

b) Phase-in a miller stake in transportation costs to incentivize more efficient transportation measures

Possibly absorb contractor services for better/cheaper services (comes at expense of existing black contractors)

c) de-centralize initial processing (Open Pan Sulphication?)

3. Re-registration for services

Currently, millers appear to prefer to extend number of SSGs (hedging against non-deliveries)

Increase in numbers of registered SSGs would preclude immediately re-extending services to SSGs.

Phase re-extension via re-registration, but likely won’t reach all

Peripheral ‘second-class’ grower without all services (limit of SSG production?)

END