Dürr AG Conference Call Q1 2015

21

www.durr.com www.durr.com CONFERENCE CALL RESULTS JANUARY – MARCH 2015 DÜRR AKTIENGESELLSCHAFT Hanover, May 12, 2015 WELCOME Ralf W. Dieter, CEO Ralph Heuwing, CFO

-

Upload

duerr-ag -

Category

Investor Relations

-

view

229 -

download

0

Transcript of Dürr AG Conference Call Q1 2015

www.durr.comwww.durr.com

CONFERENCE CALLRESULTS JANUARY – MARCH 2015

DÜRR AKTIENGESELLSCHAFT

Hanover, May 12, 2015

WELCOME

Ralf W. Dieter, CEORalph Heuwing, CFO

DISCLAIMER

This presentation has been prepared independently by Dürr AG (“Dürr”).

The presentation contains statements which address such key issues as Dürr´s strategy, future financial

results, market positions and product development. Such statements should be carefully considered,

and it should be understood that many factors might cause forecast and actual results to differ from

these statements. These factors include, but are not limited to, price fluctuations, currency fluctuations,

developments in raw material and personnel costs, physical and environmental risks, legal and

legislative issues, fiscal, and other regulatory measures. Stated competitive positions are based on

management estimates supported by information provided by specialized external agencies.

2© Dürr Aktiengesellschaft, CCI, Conference Call – Q1, May 12, 2015

HIGHLIGHTS Q1 2015

© Dürr Aktiengesellschaft, CCI, Conference Call – Q1, May 12, 2015 3

Strong performance in sales (+14%) and incoming orders (+9%) on a like-for-like basis

EBIT +7%; before PPA-effects +33%; EBIT-margin before PPA: 6.9%

Q1 disproportionately influenced by special effects, normalization during the next quarters

HOMAG`s contribution to operating EBIT:€ +12.4 m; to net profit: € -14.7 m

Ongoing high cash generation despite increase of NWC

STRONG INCREASE IN BUSINESS VOLUME

4

Catch up effects in sales realization; FX with positive effects on business volume

Orders on hand at record level, securing utilization until first half of 2016

Project pipeline continues to be strong

© Dürr Aktiengesellschaft, CCI, Conference Call – Q1, May 12, 2015

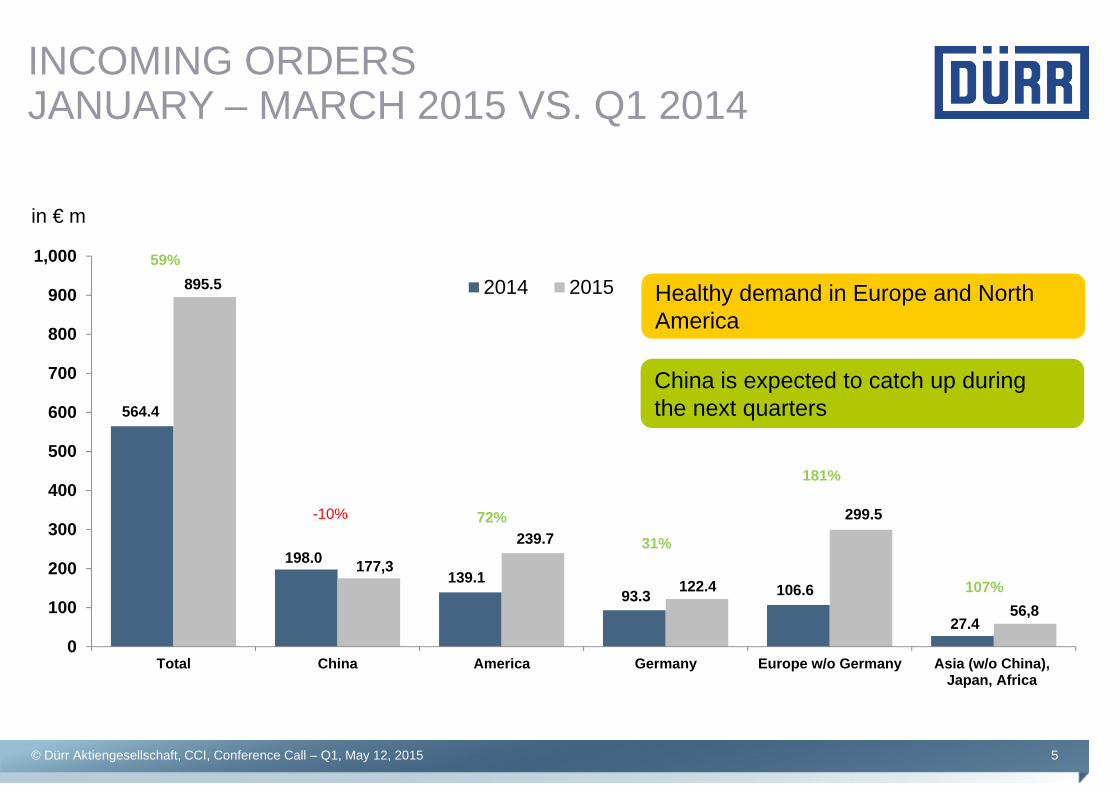

in € m Q1 2015 Q1 2014 ∆

Incoming orders 895.5 564.4 58.7%

Sales revenues 849.2 538.2 57.8%

Orders on hand (03/31) 2,904.7 2,160.8 34.4%

564.4

198.0139.1

93.3 106.6

27.4

895.5

177,3

239.7

122.4

299.5

56,8

0

100

200

300

400

500

600

700

800

900

1,000

Total China America Germany Europe w/o Germany Asia (w/o China),Japan, Africa

2014 2015

5

INCOMING ORDERS JANUARY – MARCH 2015 VS. Q1 2014

© Dürr Aktiengesellschaft, CCI, Conference Call – Q1, May 12, 2015

in € m

Healthy demand in Europe and North America

China is expected to catch up duringthe next quarters

59%

-10% 72%

31%

181%

107%

OPERATING EBIT +33% IN Q1 2015

6© Dürr Aktiengesellschaft, CCI, Conference Call – Q1, May 12, 2015

Gross margin unchanged at 21.4%, higher overhead costs due to HOMAG consolidation

EBIT margin in Q1 at 5.6% due to: PPA costs € 11.5 m, weaker HOMAG margin compared to Dürr, different sales mix

HOMAG integration impacted financial result by more than € -9 m; tax ratio increased to 53% due to domination and profit/loss transfer agreement

in € m Q1 2015 Q1 2014 ∆

Gross profit on sales 181.5 115.7 56.9%

EBITDA 70.8 50.8 39.6%

EBIT 47.4 44.2 7.3%

Net income 17.0 29.2 -41.8%

IMPROVEMENT IN NET FINANCIAL STATUS DESPITE INCREASE IN NWC

7© Dürr Aktiengesellschaft, CCI, Conference Call – Q1, May 12, 2015

in € m Q1 2015 Q1 2014

EBT 35.9 40.4

Depreciation and amortization of non-current assets 23.4 6.6

Interest result 11.9 3.9

Income taxes paid -18.7 -10.0

∆ Provisions 13.3 -7.6

∆ Net working capital -24.4 0.7

Other -1.8 8.7

Cash flow from operating activities 39.6 42.7

Interest paid (net) 0.0 -0.6

Capital expenditures -17.3 -8.3

Free cash flow 22.3 33.8

Others (e.g. currency effects) 30.1 -2.3

Change net financial status +52.4 +31.5

WIP BALANCE: SLIGHT DECLINE, BUT STILL SIGNIFICANTLY ABOVE USUAL LEVEL

© Dürr Aktiengesellschaft, CCI, Conference Call – Q1, May 12, 2015 8

in € m 03/31/2015 12/31/2014 03/31/2014

Assets

WIP in excess of billings 387.7 366.3 290.5

Liabilities

Billings in excess of WIP 657.8 675.2 565.9

Machinery business

Progress billings 112.5 88.1 23.6

Billings in excess of WIP 18.6 7.3 -12.1

Balance

Total WIP less total progress billings -288.8 -316.2 - 263.3

Prepayments (liabilities) 770.3 763.3 589.52 3+

4

1

2

3

1 2 4- -

SOLID FINANCIAL RATIOS

9© Dürr Aktiengesellschaft, CCI, Conference Call – Q1, May 12, 2015

ROCE on a high level despite low EBIT contribution at Woodworking Machinery and Systems (PPA)

Equity ratio at 21% due to changed profit entitlement of HOMAG´s free shareholders ( guarantee dividend)

Equity ratio should reach 25% at year end 2015 1 annualized

03/31/2015 12/31/2014 03/31/2014

Equity in € m 646.2 725.8 537.5

Equity ratio in % 20.9 24.4 26.8

Net financial status in € m 220.2 167.8 312.0

Cash in € m 576.9 522.0 482.2

Gearing in % -51.7 -30.1 -138.4

ROCE1 in % 42.8 38.7 70.5

PAINT AND FINAL ASSEMBLY SYSTEMS

Numerous midsize orders in Q1

Strong sales increase after project delays in the last year

Slight decline in margins due to a changed sales mix

10© Dürr Aktiengesellschaft, CCI, Conference Call – Q1, May 12, 2015

Improved order intake in Q1

in € m Q1 2015 Q1 2014 ∆

Incoming orders 278.9 254.0 9.8%

Sales revenues 297.9 251.6 18.4%

EBIT 23.1 21.0 9.8%

Stable development

Incoming orders unchanged, but promising project pipeline

New Industrial Products business with small sales contribution

EBIT margin impacted by start up costs for the new Industrial Products business

11© Dürr Aktiengesellschaft, CCI, Conference Call – Q1, May 12, 2015

APPLICATION TECHNOLOGY

in € m Q1 2015 Q1 2014 ∆

Incoming orders 133.6 135.3 -1.3%

Sales revenues 130.1 127.4 2.1%

EBIT 13.0 12.8 1.8%

MEASURING AND PROCESS SYSTEMS

Double digit order intake growth in balancing and cleaning business; book-to-bill at 1.2

Ongoing good margin situation in balancing business, cleaning business with further potential

Strong service business

12© Dürr Aktiengesellschaft, CCI, Conference Call – Q1, May 12, 2015

Earnings up 7%

in € m Q1 2015 Q1 2014 ∆

Incoming orders 161.9 138.6 16.8%

Sales revenues 136.6 128.3 6.4%

EBIT 12.5 11.7 6.9%

CLEAN TECHNOLOGY SYSTEMS

Slow start into the year; weak European market conditions

Full project pipeline in US and China

Full year expectations unchanged

13© Dürr Aktiengesellschaft, CCI, Conference Call – Q1, May 12, 2015

Book-to-bill at 1.1

in € m Q1 2015 Q1 2014 ∆

Incoming orders 33.6 36.5 -7.9%

Sales revenues 29.9 30.9 -3.2%

EBIT 0.5 0.9 -46.2%

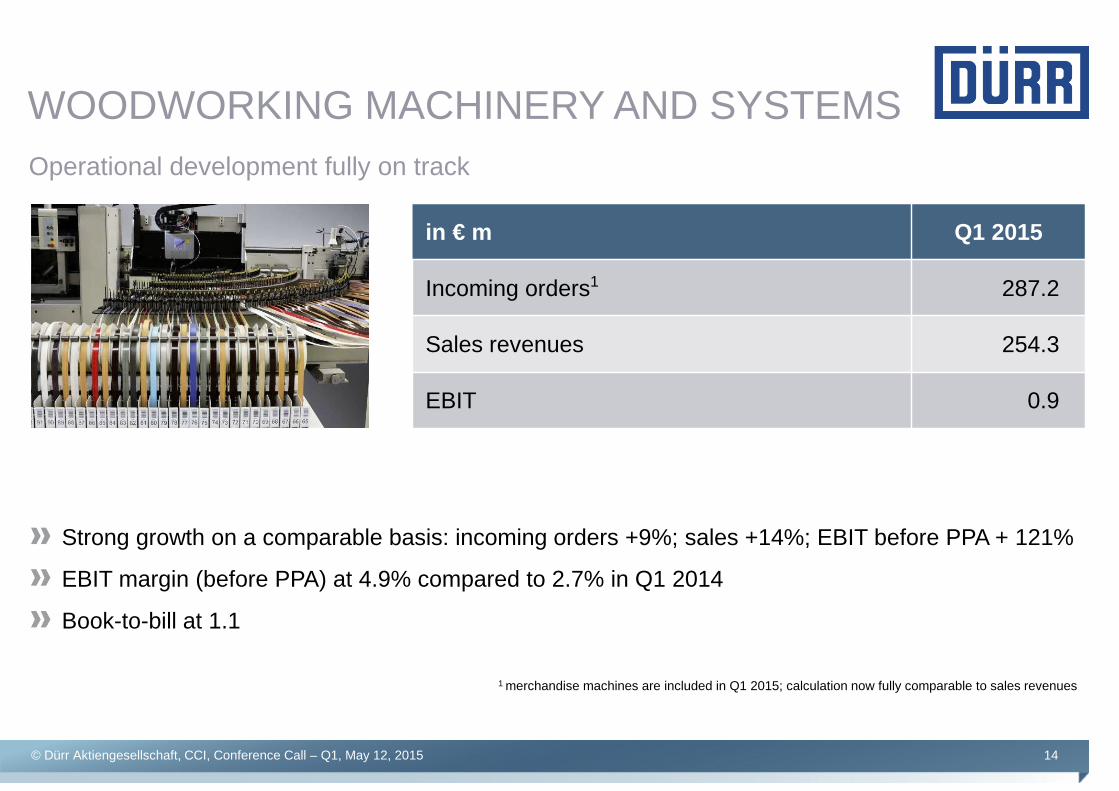

WOODWORKING MACHINERY AND SYSTEMS

© Dürr Aktiengesellschaft, CCI, Conference Call – Q1, May 12, 2015 14

Operational development fully on track

in € m Q1 2015

Incoming orders1 287.2

Sales revenues 254.3

EBIT 0.9

Strong growth on a comparable basis: incoming orders +9%; sales +14%; EBIT before PPA + 121%

EBIT margin (before PPA) at 4.9% compared to 2.7% in Q1 2014

Book-to-bill at 1.1

1 merchandise machines are included in Q1 2015; calculation now fully comparable to sales revenues

SERVICE BUSINESS

15

Positive effects from group initiative CustomerExcellence@Dürrlaunched in 2013

Sales revenues up 20% even without HOMAG

HOMAG`s service margins are on the same level as at Dürr´s machinery companies

Service growth outpaces new business again

41%

41%

18%

Modifications and upgrades

Spare parts and repair

Maintenance, assessments, seminars

Service mix Q1 2015

© Dürr Aktiengesellschaft, CCI, Conference Call – Q1, May 12, 2015

in € m Q1 2015 Q1 2014 ∆

Sales revenues (in € m) 213.8 130.0 64.5%

In % of group sales 25.2 24.2 +1.0 ppt

SALES DEVELOPMENT PASSENGER CARS JANUARY-MARCH 2015/14

© Dürr Aktiengesellschaft, CCI, Conference Call – Q1, May 12, 2015 16

Change year-on-year in %

-36

-16

-16

5

5

6

6

9

11

-40 -35 -30 -25 -20 -15 -10 -5 0 5 10 15 20

Russia

Brazil

Japan

India

New EU countries

USA

Germany

Western Europe

China

Source: German Association of the Automotive Industry (VDA); April 2015

20.9 20.8 21.9 23.1 24.0 24.9

20.0 21.0 21.1 22.6 23.7 23.9

21.4 22.0 23.3 24.0 24.9 25.3

22.1 24.3 26.027.9 29.1 30.11.8

2.0 2.02.2

2.4 2.7

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

100.0

110.0

2014 2015 2016 2017 2018 2019

Americas Europe Asia (w/o China) China Others

STRONGEST GROWTH IN THE EMERGING MARKETS

17

China, India, South East Asia & Brazil with expected automotive production growth > 6%

Emerging markets will contribute 2/3 of global growth between 2014 and 2019 CAGR in %

Source: own estimates, PwCLast update: April 2015

in m units

4

8

6

3

4

86.2 90.1 94.399.8 104.1 106.9

© Dürr Aktiengesellschaft, CCI, Conference Call – Q1, May 12, 2015

4

1,261

1,9222,400 2,407

2,575

3,400-3,500

2010 2011 2012 2013 2014 2015e

1,642

2,685 2,597 2,3872,793

3,200-3,500

2010 2011 2012 2013 2014 2015e

2.9

5.5

7.48.4

8.6 7.0-7.5%

2010 2011 2012 2013 2014 2015e

EBIT margin in %

3. OUTLOOK CONFIRMEDEBIT margin between 7.0-7.5% due to HOMAG

Incoming orders in € mSales in € m

18© Dürr Aktiengesellschaft, CCI, Conference Call – Q1, May 12, 2015

SUMMARY

© Dürr Aktiengesellschaft, CCI, Conference Call – Q1, May 12, 2015 19

Q1 with strong underlying growth in order intake and sales revenues

Earnings development in line with expectations, slight margin decline

Good cash flow situation despite increase in NWC

Impact from accounting treatment of domination and profit/loss transfer agreement and PPA mostly concentrated on Q1; normalization in the following quarters

2015 is a year of transition, 2016 is a year to harvest

FINANCIAL CALENDAR

© Dürr Aktiengesellschaft, CCI, Conference Call – Q1, May 12, 2015 20

05/15/2015 Annual general meeting, Bietigheim-Bissingen05/19/2015 UBS Pan European Small and Midcap Conference, London05/20/2015 Commerzbank German Mid Cap Investment Conf. 2015, Boston/NY05/28/2015 Societe Generale Nice Conference, Nice08/06/2015 Interim financial report for the first half of 201511/11/2015 Interim report for the first nine months of 2015

Contact Dürr AktiengesellschaftCorporate Communications & Investor RelationsGünter Dielmann / Stefan Burkhardt / Mathias ChristenCarl-Benz-Str. 3474321 Bietigheim-BissingenGermany

Phone: +49 7142 78-1785 /-3558Telefax: +49 7142 78-1716E-mail: [email protected]

www.durr.comwww.durr.com

CONFERENCE CALLRESULTS JANUARY – MARCH 2015

DÜRR AKTIENGESELLSCHAFT

Hanover, May 12, 2015

Ralf W. Dieter, CEORalph Heuwing, CFO