DUAS 1 31 18 EF - DealerCONNECT Login · The Dealer Uniform Accounting System (DUAS) ... books of...

508

FORWARD TO ALL DEALERS: There is an ever-increasing demand and emphasis placed upon sound business management practices. Good management depends upon prompt and accurate facts to satisfactorily control capital and assure a satisfactory return on investment. The Dealer Uniform Accounting System (DUAS) has been designed to make these facts available to every dealer in an orderly and usable pattern, and also provide management information for quick review and comparison. The System incorporates the latest techniques for accumulation of vital capital and management factors. It also incorporates the actual experiences of dealer accountants in dealerships with varying levels of sales volume. The Dealer Uniform Accounting System has been developed on a “Profit Center” concept. The Profit Center concept provides a measurement of the profit contribution by each center (department) as related to the total operation. The Profit Center concept evolves from the latest accounting techniques used by many successful retail dealers throughout the United States. In recognizing each center (department) as a profit contributor, the DUAS provides specific expense accounts which are directly applicable to the five basic profit centers. These expenses are known as selling expenses for the New and Used Vehicle Departments; and, direct expenses for the Service and Parts Departments. For those dealerships that wish further distribution of expenses down to a departmental operating profit, the DUAS provides for the departmentalization of fixed expenses to the various profit centers. In recognizing the Service and Parts Centers as profit contributors, rather than expense absorbing areas, the Profit Center concept also recognizes the recovery of direct expenses, as well as prime costs, for internal work performed by these two departments. In summary, the Dealer Uniform Accounting System and Profit Center concept provide for: 1. Improved Profit Planning 2. Proper Measurement of Profit 3. Improved Expense Control FCA recognizes that the manufacturer and dealer have a mutual responsibility in assuring maximum volume and profits for both parties. It further recognizes that factual information is required to make decisions and establish policies. The Dealer Financial Statement provides these facts when input via the Dial System on a timely basis each month. Your cooperation in following the recommended Dealer Uniform Accounting System will enable FCA to assist you in attaining a higher return on your investment and contribute toward the strengthening of the dealer organization. F-1 DEALER UNIFORM ACCOUNTING SYSTEM FCA (2/18)

Transcript of DUAS 1 31 18 EF - DealerCONNECT Login · The Dealer Uniform Accounting System (DUAS) ... books of...

FORWARD

TO ALL DEALERS: There is an ever-increasing demand and emphasis placed upon sound business management practices. Good management depends upon prompt and accurate facts to satisfactorily control capital and assure a satisfactory return on investment. The Dealer Uniform Accounting System (DUAS) has been designed to make these facts available to every dealer in an orderly and usable pattern, and also provide management information for quick review and comparison. The System incorporates the latest techniques for accumulation of vital capital and management factors. It also incorporates the actual experiences of dealer accountants in dealerships with varying levels of sales volume. The Dealer Uniform Accounting System has been developed on a “Profit Center” concept. The Profit Center concept provides a measurement of the profit contribution by each center (department) as related to the total operation. The Profit Center concept evolves from the latest accounting techniques used by many successful retail dealers throughout the United States. In recognizing each center (department) as a profit contributor, the DUAS provides specific expense accounts which are directly applicable to the five basic profit centers. These expenses are known as selling expenses for the New and Used Vehicle Departments; and, direct expenses for the Service and Parts Departments. For those dealerships that wish further distribution of expenses down to a departmental operating profit, the DUAS provides for the departmentalization of fixed expenses to the various profit centers. In recognizing the Service and Parts Centers as profit contributors, rather than expense absorbing areas, the Profit Center concept also recognizes the recovery of direct expenses, as well as prime costs, for internal work performed by these two departments.

In summary, the Dealer Uniform Accounting System and Profit Center concept provide for:

1. Improved Profit Planning 2. Proper Measurement of Profit 3. Improved Expense Control

FCA recognizes that the manufacturer and dealer have a mutual responsibility in assuring maximum volume and profits for both parties. It further recognizes that factual information is required to make decisions and establish policies. The Dealer Financial Statement provides these facts when input via the Dial System on a timely basis each month. Your cooperation in following the recommended Dealer Uniform Accounting System will enable FCA to assist you in attaining a higher return on your investment and contribute toward the strengthening of the dealer organization.

F-1 DEALER UNIFORM ACCOUNTING SYSTEM

FCA

(2/18)

TO ALL ACCOUNTANTS – BUSINESS MANAGERS:

An accounting system comprises not only the chart of accounts, books of original entry, and allied forms, but also includes routines and procedures by which all of the records are coordinated and utilized.

An effective accounting system must adequately reflect the various operations and financial position of a business. It must also be sufficiently flexible to meet the requirements of a changing and developing organization.

The Dealer Uniform Accounting System is primarily designed to apply these principles to the business activities of an automobile dealership. However, it also makes provision for inclusion of other business activities with which the dealer may be associated. This manual will explain the application of fundamentals to each particular type of transaction.

Several innovations are now included in the Dealer Uniform Accounting system. These are:

a. Profit Center Concept. b. Redesigned journals to facilitate posting for daily operating control purposes and monthly closing to

the general ledger. c. Redesigned general ledger pages to facilitate compilation and transfer of general ledger date to the

financial statement. d. Separation of the financial statement into carbon multi-leaved sets to eliminate time-consuming

reproduction procedures. e. Separation of financial statement into four separate pages to allow for delegation of final statement

preparation to more than one individual.

The Dealer Uniform Accounting System Manual is not intended to be a text on the principles of accounting or bookkeeping from which a beginner can learn the fundamentals. Basic Accounting or Bookkeeping training is necessary to properly interpret the principles of the Dealer Uniform Accounting System and to maintain the records of the dealership in such a manner that an accurate financial statement can be easily prepared for presentation to the dealer and submission to the Zone Office/Business Center on a timely basis.

The journals of this system, or of any system, are books of original entry and utilize what is known as “one line entry forms.” Special columns with account titles are provided for debit and credit entries, and to facilitate cross- footing for proof of balance.

The Dealer Uniform Accounting System Manual is composed of 12 original entry journals:

Cash Receipts Journal Cash Disbursement and Purchase Journal New Vehicle Purchase Journal New Vehicle Department-Sales Journal Used Vehicle Department-Sales Journal Service and Parts Journal-Repair Order Sales

(2/18)

DEALER UNIFORM ACCOUNTING SYSTEM

FCA F-2

(2/18)

ACCOUNTANTS & BUSINESS MANAGERS – Cont’d.

Parts & Accessories Journal-Counter Sales Warranty Sales Journal & Claims Register Internal Sales Journal Payroll Journal General Journal Standard Entries Journal

The General Ledger is the permanent record in which the transactions, summarized in the journals, are entered in accounts which group together related transactions. Each account in the General Ledger has an account name and number for identification and reference purposes.

The Chart of Accounts is a list of the names and numbers of the accounts that should be used in the General Ledger. Some dealers will not require all of the accounts provided. However, subsidiary ledgers are necessary to record additional detail as to the various items representing the balance of a specific General Ledger Account. An example of this is the recording of amounts due from individual customers.

The following table will assist in analyzing a transaction and in determining the proper entries:

Classification To Increase To Decrease Normal Account of Accounts Account Account Balance Should Show

Assets Debit Credit Debit Liabilities Credit Debit Credit Net Worth Credit Debit Credit Dividend and

Drawing Accounts Debit Credit Debit Expenses Debit Credit Debit Sales Credit Debit Credit Cost of Sales Debit Credit Debit Other Income Credit Debit Credit Other Deductions Debit Credit Debit

Your conscientious adherence to the procedures outlined in this manual will substantially increase your value as an accountant. Properly maintained and utilized, the Dealer Uniform Accounting System and the resultant Dealer Financial Statement become the Dealer’s prime source for appraising the results of his/her planned objectives. The end product of good accounting is Informed Management.

F-3 DEALER UNIFORM ACCOUNTING SYSTEM

FCA

(2/18)

FORWARD

INTRODUCTION

This Chart of Accounts has been designed for the use of all FCA Dealers. It has been prepared in conformity with currently accepted accounting practices for operating and analyzing an automobile dealership.

Sufficient accounts have been provided to meet all conditions which dealers are likely to encounter. The Accounts have been grouped by classifications with the following numbering scheme:

ACCOUNT CLASSIFICATION NUMBERS Assets 100 thru 199 Liabilities and Net Worth 200 thru 299 Expenses 300 thru 399

(New Vehicle 300-319) (Parts & Access. 350-359) (Used Vehicle 320-339) (Fixed Expenses 360-399) (Service Dept. 340-349)

Sales and Cost of Sales 400 thru 599 Other Income 600 thru 699 Other Deductions 700 thru 799 Leasing Operations:

Income: Control Account 615 Sub-Accounts 800-8 thru 899-8

Expenses: Control Account 715 Sub-Accounts 900-8 thru 999-8

Seven letter suffix designations (A thru G) are used in the Sales and Cost of Sales numbering system to distinguish the various types of sales and cost factors. They are:

1 (A) Gross sales price 2 (B) Discount and over allowances (reduction in sales) 3 (C) Base cost 4 (D) Special vehicle income (reduction in cost)

(D) Reconditioning used vehicles (addition in cost) (D) Unapplied time (addition in cost)

5 (E) Repossession losses (addition in cost) (E) Customer Repossession Refund (addition in cost) (E) Quantity purchase discounts (reduction in cost)

6 (F) Finance and insurance income (reduction in cost) (F) Wholesale compensation (reduction in cost)

7 (G) Inventory write down (addition in cost)

Bracketed letters represent normal credit balance accounts and unbracketed letters represent normal debit balance accounts.

Pages should be opened in the ledgers only for such accounts as are required, for example: a dealer selling only car lines would not require inventory, sales, and cost of sales accounts for truck lines, nor would a sole proprietorship require all the net worth accounts necessary for a corporation.

The Chart provides specific accounts for investments in subsidiary companies and separate corporations. Records for these organizations should be maintained separately from records of the automobile dealership. However, other activities, that may or may not be located elsewhere, having a direct relationship to the dealership should be combined on the Dealer Financial Statement.

(2/18)

DEALER UNIFORM ACCOUNTING SYSTEM

FCA 1-1

ASSETS

ACCOUNT PAGE ACCOUNT PAGE NUMBER NUMBER NUMBER NUMBER

CASH AND EQUIVALENT Other Services & Parts Inventories: 101 Petty Cash Fund..............................................................2-1 136-A Gas, Oil & Lubricants....................................................2-41 102 Undeposited Cash...........................................................2-2 136-B Body and Paint Shop Materials....................................2-42 103 Cash in Bank...................................................................2-3 136-C Sublet Work..................................................................2-43 104 Cash on Deposit..............................................................2-4 137 Non-Automotive Inventories.........................................2-44 106 Contracts in Transit.........................................................2-5

RECEIVABLES OTHER CURRENT ASSETS

110 Service and Parts Accounts Receivable..........................2-6 140 Marketable Securities...................................................2-45 111 Vehicle Accounts Receivable..........................................2-7 Prepaid Expenses: 112 Customer Notes Receivable............................................2-8 145-A Advertising...............................................................2-46 114 Other Receivables...........................................................2-9 145-B Insurance.................................................................2-47 Factory Receivables 145-C Interest.....................................................................2-48 116-A Warranty Service Claims/ 145-D Rent.........................................................................2-49 Road Ready Claims..................................................2-10 145-E Taxes and Licenses.................................................2-50 116-A1 WSC – Advance Payment........................................2-11 145-F Other........................................................................2-51 116-B Holdback – New Cars and Trucks............................2-12 116-C Special Vehicle Income.......................................2-13/14 OTHER ASSETS 116-D Floor Plan Allowance................................................2-15 151 Officers’ and Employees’ Accounts..............................2-52 116-E Wholesale Compensation – Parts............................2-16 152 Due from Finance & Insurance 116-F Inventory Rebates...............................................2-17/18 Companies – Deferred............................................2-53 116-G Other.........................................................................2-19 153 Deposits on Contracts..................................................2-54 116-H Dealer Cash/Consumer Rebates..............................2-20 154 Cash Value of Life Insurance.......................................2-55 117 Cash Sales.....................................................................2-21 155-A Driver Education Vehicles............................................2-56 118 Allowance for Doubtful Accounts...................................2-22 155-B Depreciation and Program Allowances - 119 Due from Finance and Insurance Driver Education Vehicles.......................................2-57 Companies – Current................................................2-23 156-A Lease/Rental Vehicles.................................................2-58 156-B Depreciation and Program Allowances -

INVENTORIES Lease/Rental Vehicles............................................2-59 120 Cars – CDJR/Fiat......................................................2-24/25 157 Other Assets and Investments.....................................2-60 123 Trucks – CDJR/Fiat...................................................2-24/25 124 Recreational Vehicles....................................................2-27 LAND, BUILDINGS AND EQUIPMENT 125 Other New Cars and Trucks – Competitive..............2-24/25 160 Land..............................................................................2-61 126 Demonstrators...............................................................2-29 161-A Buildings and Building Equipment................................2-62 127 Used Cars.................................................................2-30/31 161-B Depreciation of Buildings and 128 Used Trucks...................................................................2-32 Building Equipment................................................2-63 129 Certified Pre-owned Vehicle (CPOV).......................2-33A/B 162-A Service Equipment........................................................2-64 130 Parts and Accessories – CDJR/Fiat...............................2-34 162-B Depreciation of Service Equipment..........................2-65 131 Parts and Accessories – Other MFG.............................2-35 163-A Parts and Accessories Equipment................................2-66 132 Inventory Adjustment - Parts & Accessories..................2-36 163-B Depreciation of Parts and 133 Tires and Tubes.............................................................2-37 Accessories Equipment.........................................2-67 134 Other Automobile Inventories........................................2-38 164-A Company Cars and Service Vehicles............................2-68 135-A Labor in Process – Mechanical......................................2-39 164-B Depreciation of Company Cars 135-B Labor in Process – Body and Paint...............................2-40 and Service Vehicles.............................................2-69 165-A Furniture, Signs, and Equipment...................................2-70 165-B Depreciation of Furniture, Signs, and Equipment......................................................2-71 166-A Leaseholds....................................................................2-72 166-B Amortization of Leasehold........................................2-73

DEALER UNIFORM ACCOUNTING SYSTEM

1-2 FCA (2/18)

CHART OF ACCOUNTS LIABILITIES AND NET WORTH

ACCOUNT PAGE ACCOUNT PAGE

NUMBER NUMBER NUMBER NUMBER

PAYABLES 217-D Miscellaneous...............................................................3-29 Accounts Payable: 201-A Trade Creditors..........................................................3-1 WHOLESALE FINANCE LIABILITY 201-C Miscellaneous Employee Deductions........................3-2 220 New Cars and Trucks...................................................3-30 201-D Other..........................................................................3-3 226 Demonstrators..............................................................3-31 202 Customer Refunds – Payable.........................................3-4 227 Used Cars and Trucks..................................................3-32 203 Notes Payable................................................................3-5 228-B Used Cars and Trucks CPOV.......................................3-33 205 Dividends Payable..........................................................3-6 230 Other Inventory Finance Liability..................................3-34 206 Vehicle Lien Payoffs.......................................................3-7 207 Vehicle Protection/Extended Warranty – Payable..........3-2 OTHER LIABILITIES 240 Security Deposits: Lease Vehicles...........................3-35

ACCRUED EXPENSES 250 Reserve for Repossession Losses...........................3-36 Payroll and Equivalent: 255 Driver Education Vehicle Liability.............................3-37 210-A Salaries, Wages, Commissions, 256 Lease/Rental Vehicle Liability..................................3-38 Bonuses and Profit Sharing....................................3-9 258 Company Cars and Service Liability........................3-39 210-B Vacation and Time Off Pay......................................3-10 212 Interest..........................................................................3-11 LONG TERM DEBT 213 Insurance......................................................................3-12 260 Notes Payable – Capital Loans.................................3-40 Taxes – Payroll: 262 Subordinated Notes..................................................3-41 214-A F.I.C.A. Withheld and Accrued.................................3-13 263 Mortgages Payable...................................................3-42 214-B Federal Income Tax Withheld..................................3-14 265 Other Notes and Contracts.......................................3-43 214-C Federal Unemployment Taxes.................................3-15 268 LIFO Reserve – Inventory Adjustment......................3-44 214-D State Income Tax Withheld......................................3-16 214-E Local (City & County) Income Tax Withheld............3-17 NET WORTH 214-F State Unemployment Tax........................................3-18 270 Capital Stock – Preferred...............................................3-45 Taxes – Other Than Payroll and Income: 271 Capital Stock – Common...............................................3-46 215-A Sales Tax – Vehicles...............................................3-19 272 Additional Paid in Capital...............................................3-47 215-B Sales and Use Tax – Other Than Vehicles..............3-20 275 Retained Earnings.........................................................3-48 215-C Vehicle License and Title Fees................................3-21 277 Dividends.......................................................................3-49 215-D Real and Personal Property....................................3-22 280 Investments – Proprietor or Partners.............................3-50 215-E State and Local Taxes – Other................................3-23 285 Withdrawals...................................................................3-51 216 Income Taxes...............................................................3-34 290 Adjustments...................................................................3-52 Other Accrued Expenses: 296 Estimated Income Tax – Current Year..........................3-53 217-A Utilities.....................................................................3-25 299 Profit or (Loss) – Current...............................................3-54 217-B Legal and Audit........................................................3-26 217-C Employer’s Pension Contributions......................3-27/28

DEALER UNIFORM ACCOUNTING SYSTEM

(2/18) FCA 1-3

CHART OF ACCOUNTS EXPENSE

ACCOUNT PAGE ACCOUNT PAGE

NUMBER NUMBER NUMBER NUMBER NEW VEHICLE – SALES EXPENSE PARTS AND ACCESSORIES DEPARTMENT -

301 Salespersons’ Commissions & Incentives - New............4-1 SALES EXPENSE 302 Sales Managers’ Commissions & 350 Salaries, Wages & Incentives........................................4-41 Incentives – New........................................................4-2 352 Personnel Training........................................................4-42 303 Vehicle Inventory Maintenance.......................................4-3 353 Advertising.....................................................................4-43 304 Policy Service – New......................................................4-4 354 Supplies, Tools and Laundry.........................................4-44 306 Salesperson’s Salaries – New........................................4-5 355 Freight, Express and Shipping......................................4-45 307 Sales Manager’s Salaries – New....................................4-6 356 Policy Adjustments........................................................4-46 308 Other Salaries – New......................................................4-7 357 Vehicle Expense............................................................4-47 309 Advertising – Print, TV, Other – New..............................4-8 358 Depreciation – Equipment.............................................4-48 309-A Advertising – Print, TV, Other Credits – New...............4-8A 359 Maintenance, Repair and 310 Sales Personnel Training – New....................................4-9 Rental – Equipment..................................................4-49 312 Demonstration Expense – New....................................4-10 315 Floor Plan Interest – New.............................................4-11 FIXED EXPENSES 315-A Floor Plan Interest Credits – New..............................4-11A 362 Salaries and Wages – Administrative 316 F & I Managers’ Commissions – New........................4-11B and General..............................................................4-50 317 F & I Managers’ Salaries – New.................................4-11D 363 Employee Benefits.........................................................4-51 318 Advertising – Internet Only – New..............................4-11F 365 Payroll Taxes.................................................................4-52 367 Advertising – General and Institutional..........................4-53

USED VEHICLE – SALES EXPENSE 368 Stationery, Office Supplies and Postage.......................4-54 321 Salespersons’ Commissions & Incentives – Used........4-12 370 Legal, Auditing and Collection Expense........................4-55 322 Sales Managers’ Commissions – Used.........................4-13 371 Other Outside Services.................................................4-56 323 Vehicle Inventory Maintenance – Used.........................4-14 372 Company Car Expense.................................................4-57 324 Policy & Warranty Service – Used.................................4-15 373 Dues, Subscriptions and Contributions.........................4-58 326 Salesperson’s Salaries – Used......................................4-16 374 Data Processing Service...............................................4-59 327 Sales Managers’ Salaries – Used.................................4-17 377 Travel and Entertainment..............................................4-60 328 Other Salaries – Used...................................................4-18 378 Bad Debts......................................................................4-61 329 Advertising – Print, TV, Other – Used...........................4-19 380 Miscellaneous................................................................4-62 330 Sales Personnel Training – Used..................................4-20 381 Interest on Mortgage.....................................................4-63 332 Demonstration Expense – Used....................................4-21 382 Rent...............................................................................4-64 335 Interest on Floor Plan – Used........................................4-22 383 Amortization of Leaseholds...........................................4-65 336 F & I Managers’ Commissions – Used........................4-22A 384 Depreciation Buildings and 337 F & I Managers’ Salaries – Used.................................4-22C Building Equipment...................................................4-66 338 Advertising – Internet Only – Used..............................4-22E 385 Taxes – Real Estate......................................................4-67 386 Insurance – Real Estate................................................4-68

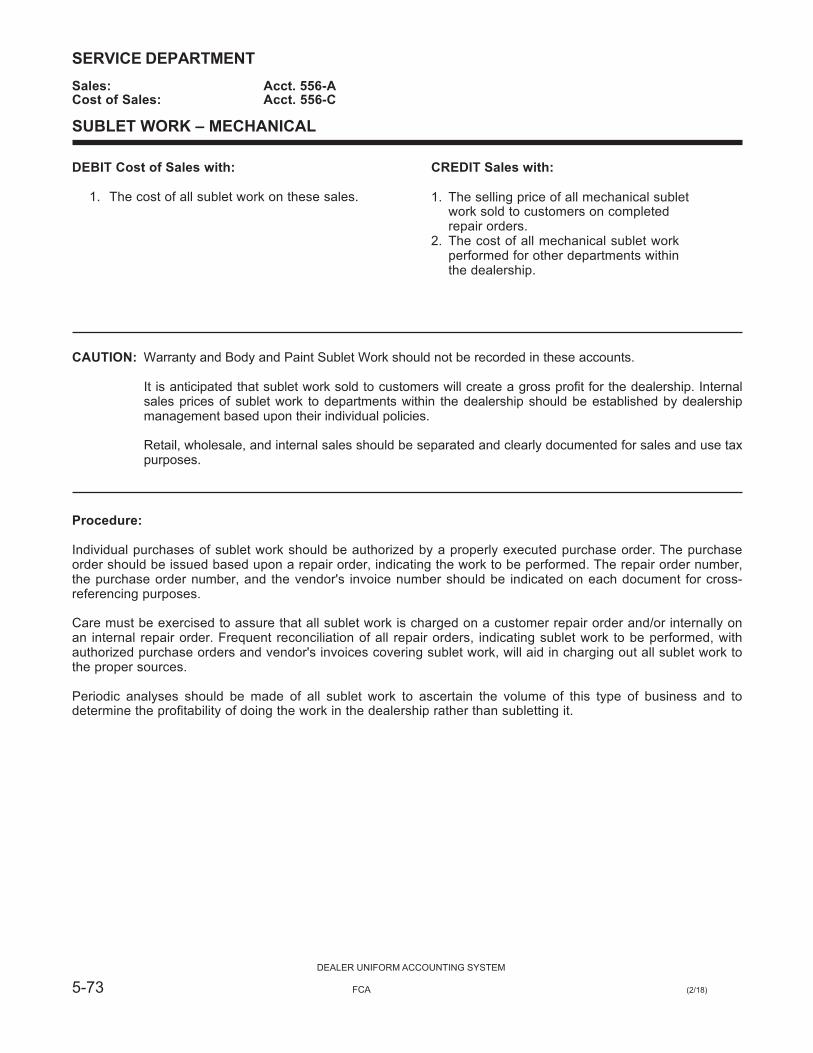

SERVICE DEPARTMENT – SALES EXPENSE 387 Maintenance and Repairs – Real Estate.......................4-69 340-A Salaries, Wages and 388 Interest – (Other than Floor Plan Incentives – Mechanical...........................................4-23 and Mortgage)..........................................................4-70 340-B Salaries, Wages and 389 Insurance – (Other than Real Estate)............................4-71 Incentives – Body & Paint.........................................4-24 390 Taxes and Licenses (Other than 341-A Vacation & Time-Off Pay – Mechanical.........................4-25 Payroll & Real Estate................................................4-72 341-B Vacation & Time-Off Pay – Body & Paint.......................4-26 391 Depreciation – (Other than Buildings 342-A Personnel Training – Mechanical...................................4-27 & Building Equipment)..............................................4-73 342-B Personnel Training – Body & Paint................................4-28 392 Maintenance and Repairs (Other than 343-A Advertising – Mechanical...............................................4-29 Buildings & Building Equipment)..............................4-74 343-B Advertising – Body & Paint............................................4-30 393 Equipment Rental – (Other than 344-A Supplies, Tools & Laundry – Mechanical.......................4-31 Service and Parts Equipment)..................................4-75 344-B Supplies, Tools & Laundry – Body & Paint....................4-32 395 Heat, Light, Power and Water.......................................4-76 345-A Vehicle Expense – Mechanical......................................4-33 396 Telephone......................................................................4-77 345-B Vehicle Expense – Body & Paint...................................4-34 399 Salaries – Owners and Officers.....................................4-78 346-A Policy Adjustments – Mechanical..................................4-35 346-B Policy Adjustments – Body & Paint...............................4-36 348-A Depreciation of Equipment – Mechanical......................4-37 348-B Depreciation of Equipment – Body & Paint...................4-38 349-A Maintenance, Repair & Rental of Equipment – Mechanical..........................................4-39 349-B Maintenance, Repair & Rental of Equipment – Body & Paint.......................................4-40

DEALER UNIFORM ACCOUNTING SYSTEM

1-4 FCA (2/18)

CHART OF ACCOUNTS SALES AND COST OF SALES

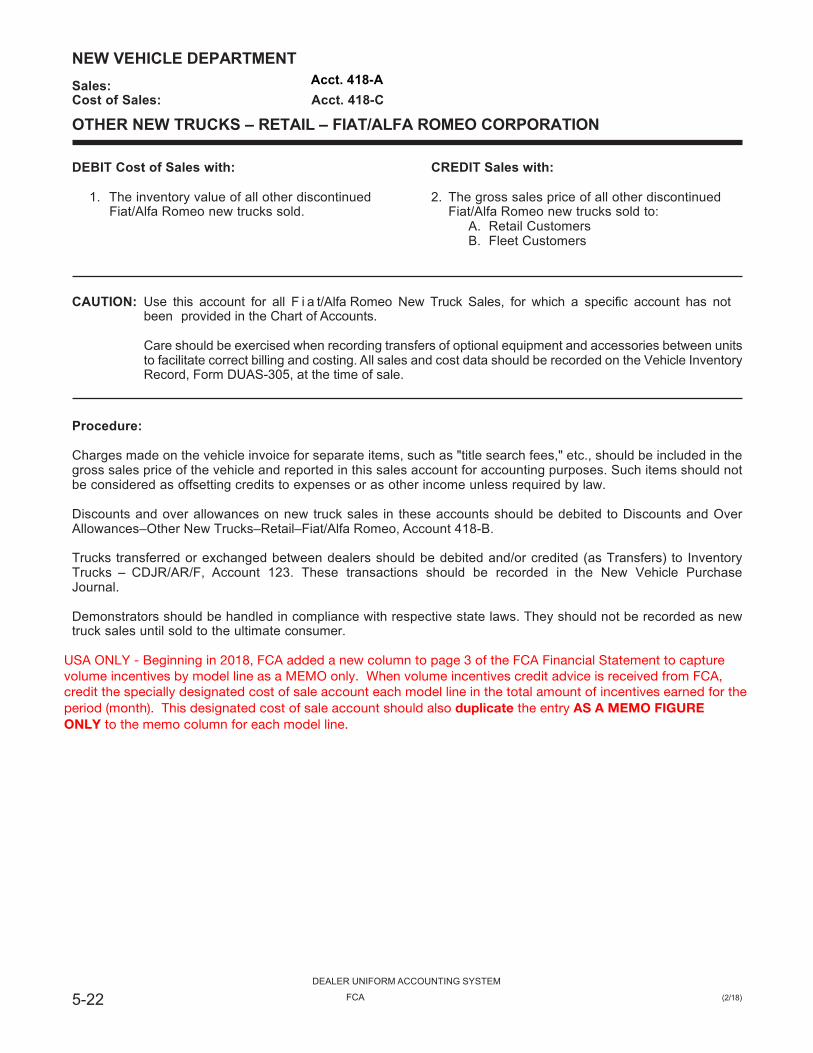

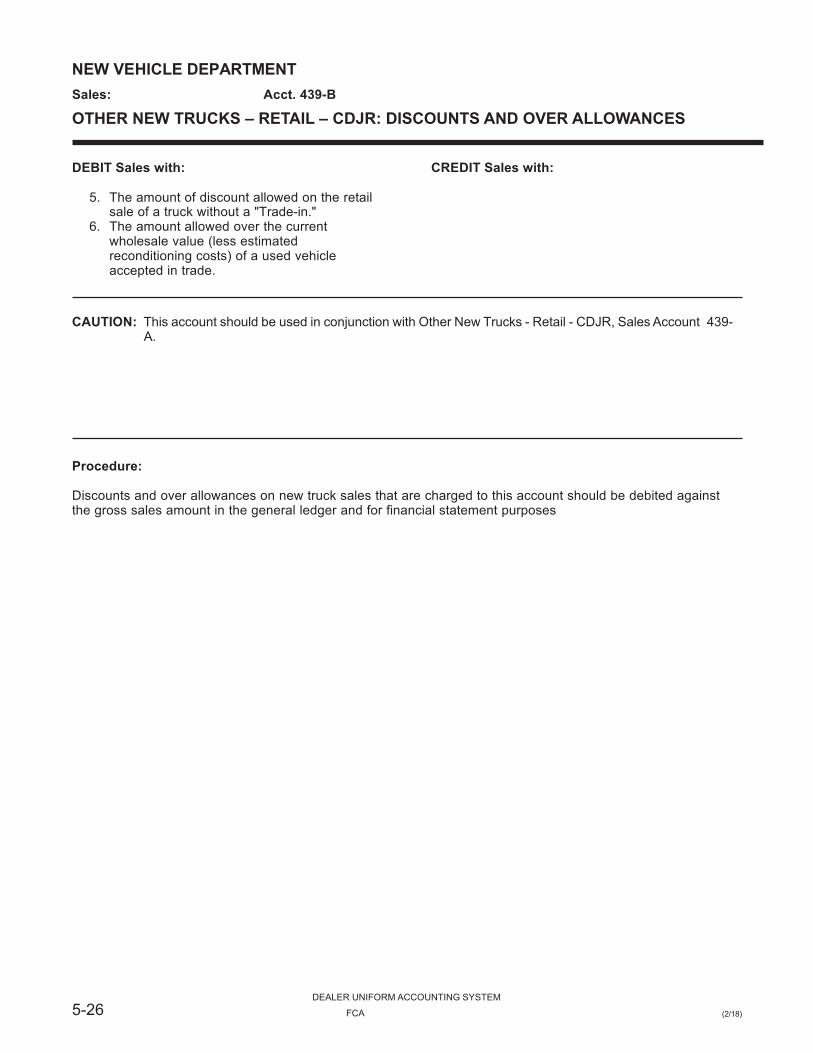

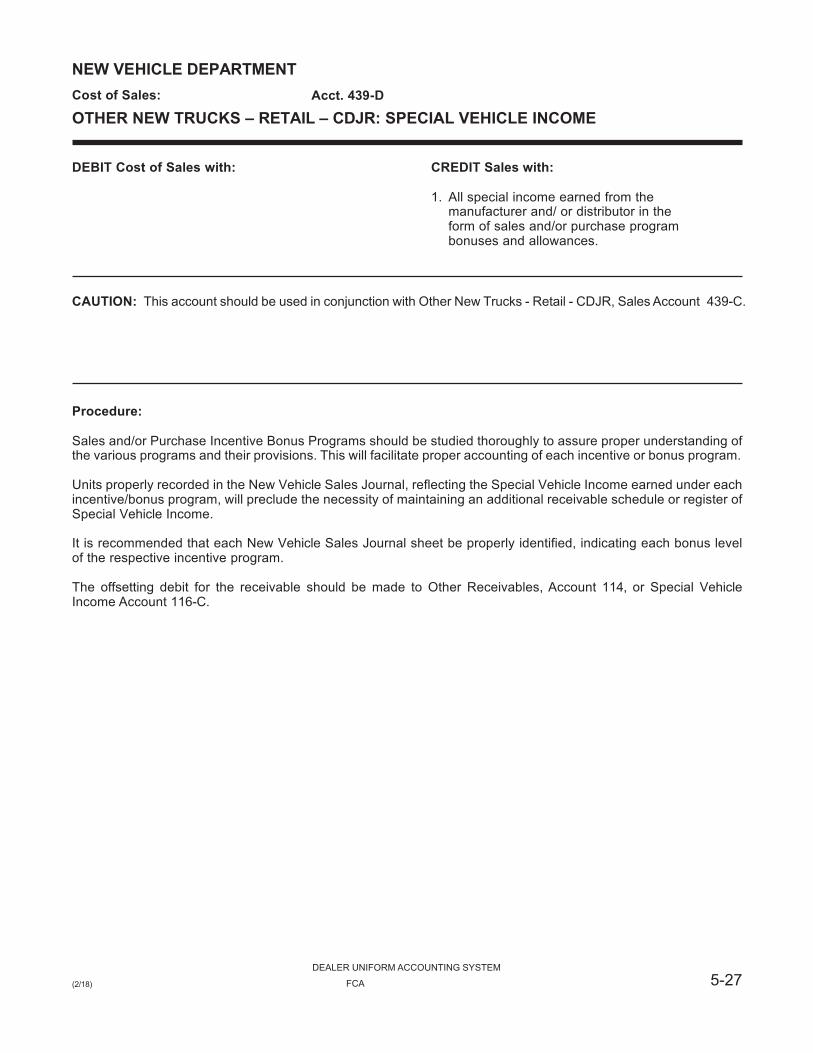

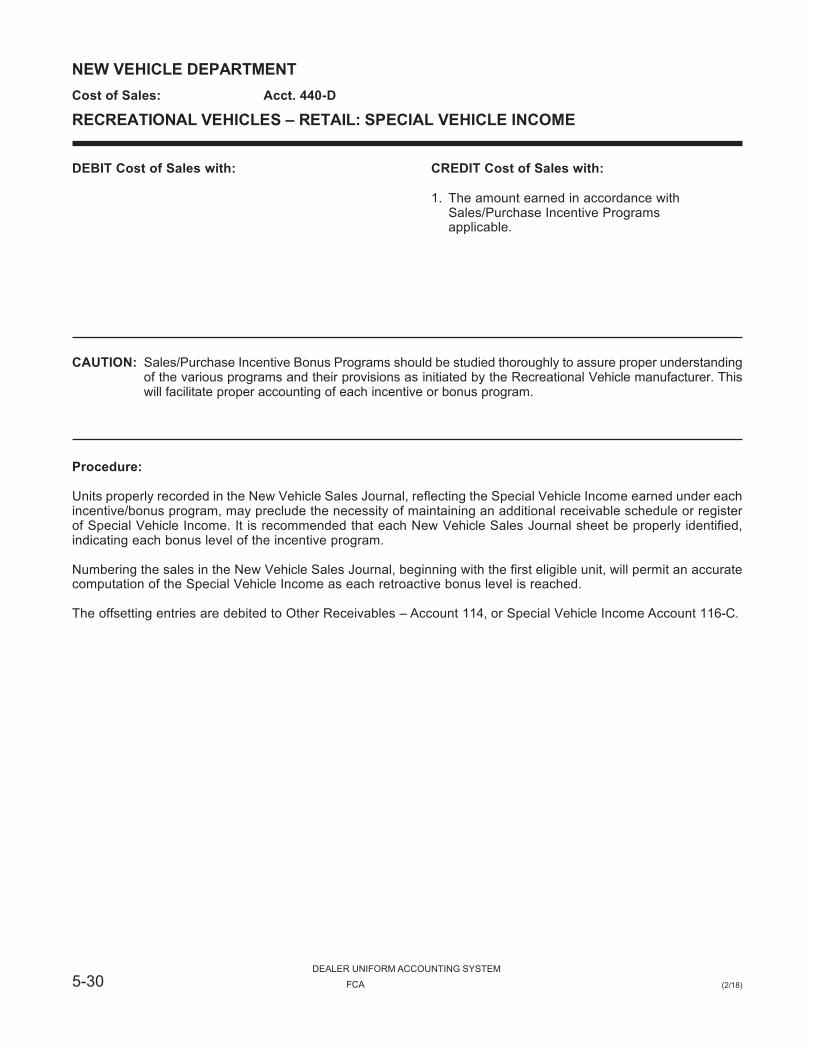

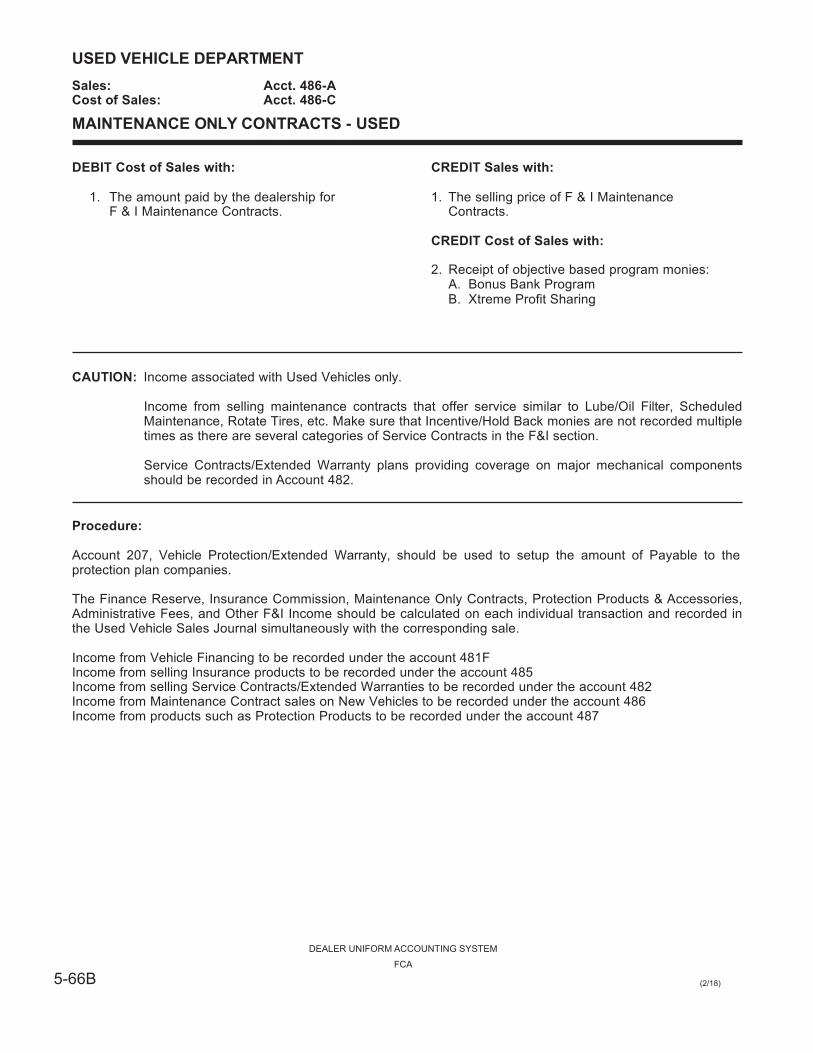

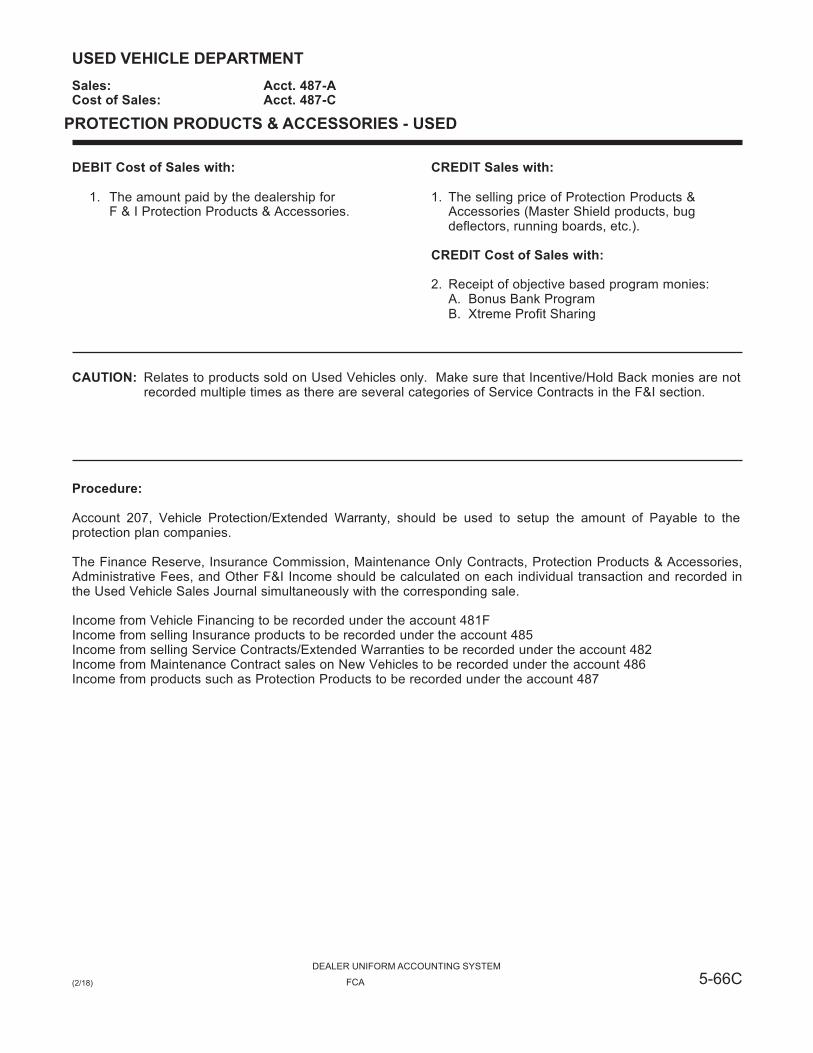

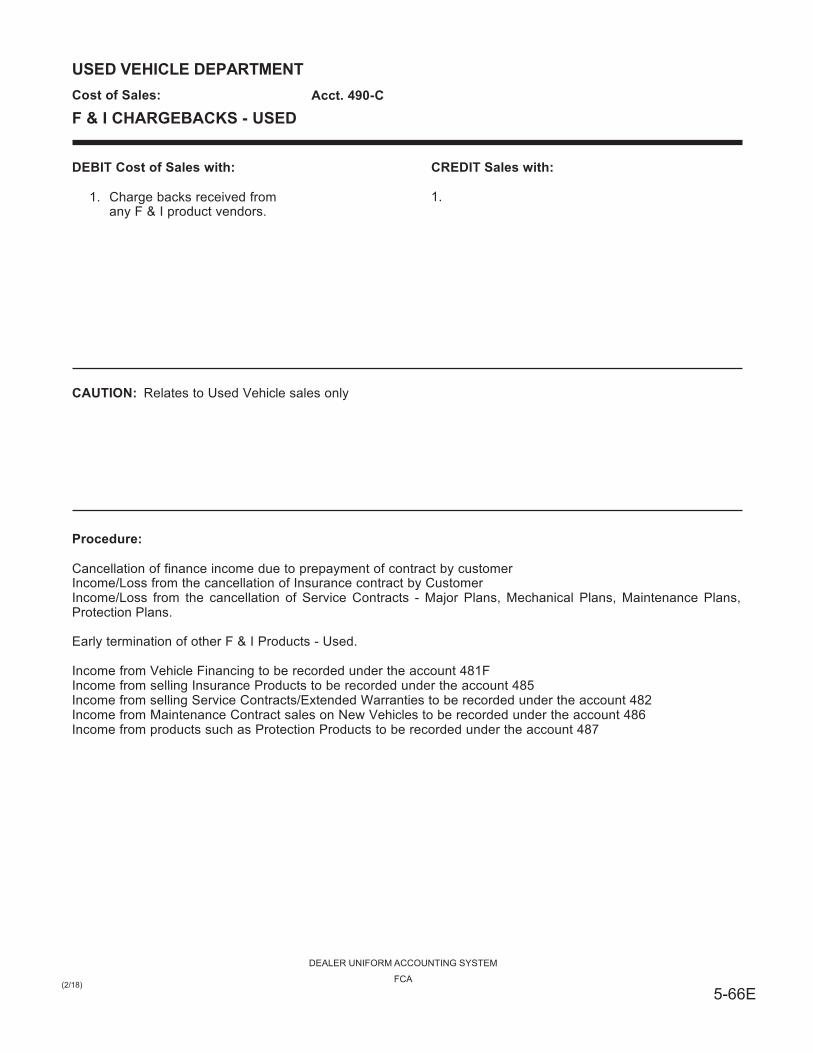

ACCOUNT PAGE ACCOUNT PAGE NUMBER NUMBER NUMBER NUMBER SALES COST NEW VEHICLE DEPARTMENT SALES COST 401-A 401-C Other New Cars – Retail: Maserati……………….5-4 474-A 474-C Used Trucks – Wholesale..............................5-49 402-A 402-C New Cars – Retail: Fiat – 124 Spider...................5-1 475-A 475-C Used CPOV Cars Retail.................................5-50 403-A 403-C Other New Cars – Retail: Fiat/Alfa Romeo………5-7 476-G Used Car Inventory – Writedown....................5-56 404-A 404-C New Cars – Retail: Fiat 500..................................5-1 477-G Used Truck Inventory – Writedown................5-57 405-A 405-C New Cars – Retail: Alfa Romeo Stelvio................5-1 478-E Customer Repossession Refund....................5-58 406-A 406-C New Cars – Retail: Fiat 500 Cabrio......................5-1 479-A 479-C Non-Automotive – Used……………………….5-59 407-A 407-C New Cars – Retail: Challenger.............................5-1 480-E Repossessed Vehicle Losses – Used…….…5-60 408-A 408-C New Cars – Retail: 200 Series 4 Dr. Sedan.........5-1 482-A 482-C Service Contracts – Used...............................5-63 409-A 409-C New Cars – Retail: Charger..................................5-1 483-A 483-C CPOV Finance and Insurance..........................5-64 410-A 410-C Other New Trucks – Retail: Maserati……………5-19 411-A 411-C New Cars – Retail: Alfa Romeo – 4C…...............5-1 484-A 484-C CPOV Service Contracts..................................5-65 412-A 412-C New Cars – Retail: TBD 2.................…...............5-1 485-C Insurance Contracts – Used..........................5-66A 413-A 413-C New Cars – Retail: Fiat 500E – USA Only...........5-1 486-A 486-C Maintenance Only Contracts – Used.............5-66B 417-A 417-C New Cars – Retail: Alfa Romeo Giulia…..............5-1 487-A 487-C Protection Products & Accessories – Used...5-66C 418-A 418-C Other New Trucks – Retail: Fiat/Alfa Romeo…..5-22 489-A 489-C Other F & I – Used.........................................5-66D 419-A 419-C New Cars – Retail: Alfa Romeo – TBD................5-1 490-C F & I Chargebacks – Used.............................5-66E 420-A 420-C New Cars – Retail: 300 Series.............................5-1 491-A 491-C CPOV Non-Automotive & Other – Used.......5-66F 423-A 423-C New Cars – Retail: Viper......................................5-1 492-A 492-C CPOV Insurance Contracts – Used.............5-66G 425-A 425-C Other New Cars – Retail – CDJR………..............5-10 426-A 426-C Other New Cars – Retail – Competitive..............5-13 SERVICE DEPARTMENT 427-A 427-C New Trucks – Retail: Grand Caravan.................5-16 550-A 550-C Customer Labor – Mechanical..........................5-67 428-A 428-C New Trucks – Retail: Pacifica…………………….5-16 551-A 551-C Service Contract Labor – Mechanical...............5-68 429-A 429-C New Trucks – Retail: RAM HD (2500/3500).......5-16 552-A 552-C Warranty Labor – Material................................5-69 430-A 430-C New Trucks – Retail: Cherokee..........................5-16 553-A 553-C Road Ready Labor...........................................5-70 431-A 431-C New Trucks – Retail: Wrangler 4-DR..................5-16 554-A 554-C Labor Internal – Mechanical.............................5-71 432-A 432-C New Trucks – Retail: Wrangler...........................5-16 555-A 555-C Customer Labor – Non-Automotive..................5-72 433-A 433-C New Trucks – Retail: Compass...........................5-16 556-A 556-C Sublet Work – Mechanical................................5-73 435-A 435-C New Trucks – Retail: Durango............................5-16 557-A 557-C Sublet Work – Warranty – Mechanical.............5-74 436-A 436-C New Trucks – Retail: Ram ProMaster City……..5-16 558-A 558-C Quick Service Labor Mechanical......................5-75 437-A 437-C New Trucks – Retail: Ram 1500.........................5-16 559-D Unapplied/Variance Labor – Mechanical..........5-76 438-A 438-C New Trucks – Retail: Grand Cherokee...............5-16 560-A 560-C Customer Labor – Body & Paint.......................5-77 439-A 439-C Other New Trucks – Retail – CDJR……………..5-25 562-A 562-C Warranty Labor – Body & Paint........................5-78 440-A 440-C New Recreational Vehicles – Retail....................5-28 563-A 563-C Labor Internal – Body & Paint...........................5-79 441-A 441-C Other New Trucks – Retail – Competitive...........5-31 564-A 564-C Sublet Work – Body & Paint.............................5-80 442-A 442-C New Trucks – Retail: Renegade…………………5-16 565-A 565-C Sublet Work – Warranty – Body & Paint..........5-81 443-A 443-C New Trucks – Retail: Fiat 500X………………….5-16 566-A 566-C Body and Paint Stop Materials.........................5-82 444-A 444-C New Trucks – Retail: Patriot...............................5-16 567-D Unapplied/Variance Labor – Body & Paint.....5-83A 445-A 445-C New Cars – Fleet................................................5-34 568-A 568-C Service Contracts Sold on Serv. Lane...........5-83B 446-A 446-C New Trucks – Fleet.............................................5-35 448-A 448-C New Trucks – Retail: Ram Chassis Cab 3500....5-16 PARTS AND ACCESSORIES 450-A 450-C Non-Automotive – New.......................................5-36 570-A 570-C P & A – Repair Orders – Mechanical...............5-84 451-A 451-C New Trucks – Retail: Journey.............................5-16 571-A 571-C P & A – Service Contracts – Mechanical.........5-85 452-A 452-C New Trucks – Retail: Ram Chassis Cab 4500....5-16 572-A 572-C P & A – Warranty – Mechanical.......................5-86 453-A 453-C New Trucks – Retail: Ram Chassis Cab 5500....5-16 573-A 573-C P & A – Retail..................................................5-87 454-A 454-C Volume Incentives (New Vehicle).......................5-38 574-A 574-C P & A – Wholesale...........................................5-88

455-E Repossessed Vehicle Losses – New....................5-39 575-A 575-C P & A – Internal – Mechanical..........................5-89 457-F Finance Contract Reserve – New.........................5-40 576-A 576-C P & A – Quick Service – Oil – Lubricants.......5-90A

458-A 458-C Service Contracts – New....................................5-41A 577-A 577-C Service Contracts Sold at Parts Counter.......5-90B 460 Dealer Transfers – Special Income....................5-41B 580-A 580-C P & A – Repair Orders – Body & Paint.............5-91

461-A 461-C New Trucks – Retail: Fiat 500L..........................5-16 582-A 582-C P & A – Warranty – Body & Paint.....................5-92 462-A 462-C New Trucks – Retail: Ram ProMaster................5-16 583-A 583-C P & A – Internal – Body & Paint........................5-93

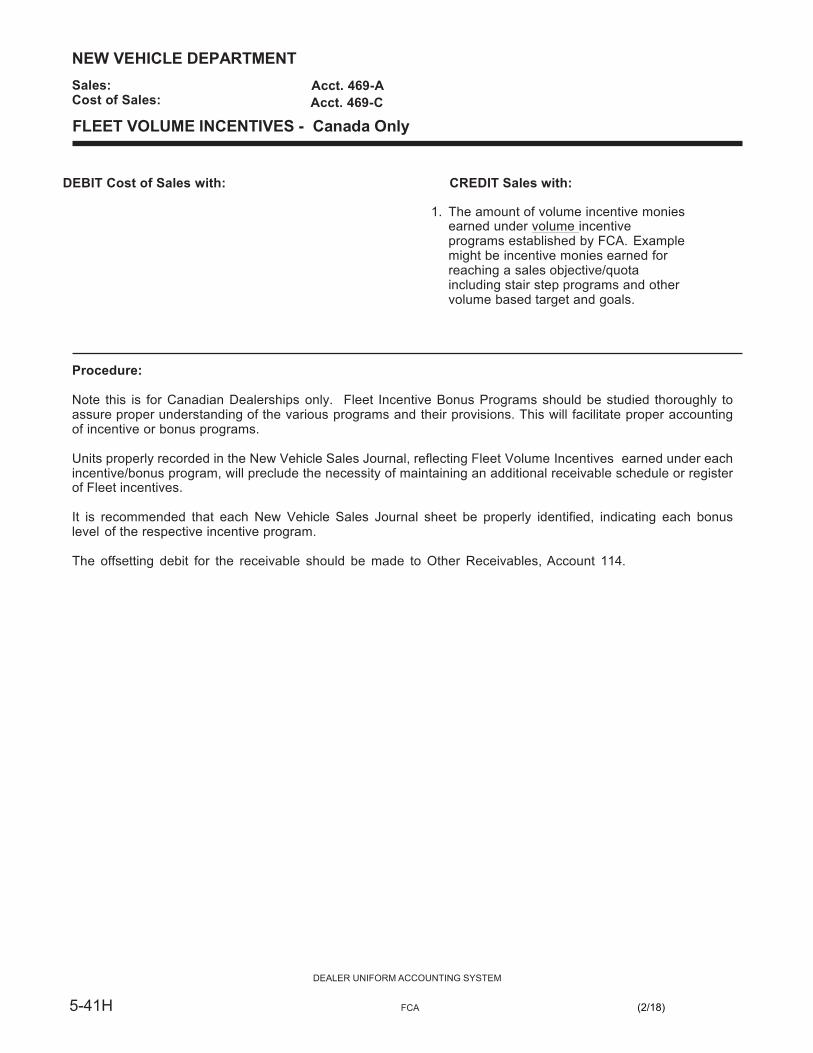

463-C Insurance Contracts – New................................5-41C 585-E Purchase Discounts – P & A............................5-94 464-A 464-C Maintenance Only Contracts – New...................5-41D 586-F Wholesale Allowance.......................................5-95 465-A 465-C Protection Products & Accessories – New.........5-41E 587-G P & A – Inventory Adjustments.........................5-96 467-A 467-C Other F & I – New...............................................5-41F 590-A 590-C Tires and Tubes................................................5-97 468-C F & I Chargebacks – New………………………..5-41F 591-A 591-C Mopar Express Lane CP Parts.......................5-98A 469-A 469-C Fleet Volume Incentives – Canada Only……..…5-41H 592-A 592-C Mopar Express Lane Svc. Contracts Parts..5-98B

593-A 593-C Mopar Express Lane – Warranty – Parts.......5-98C USED VEHICLE DEPARTMENT 594-A 594-C Mopar Express Lane – Internal – Parts.........5-98D

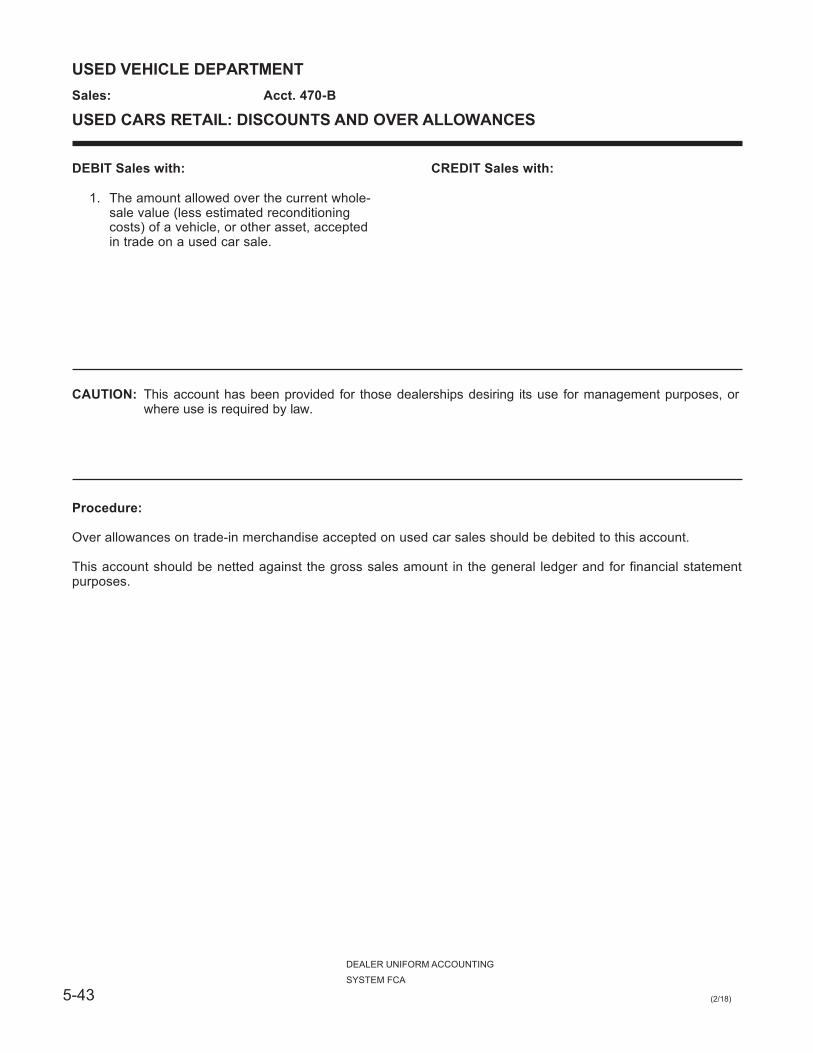

470-A 470-C Used Cars – Retail................................................5-42 595-A 595-C Non-Automotive and Miscellaneous.................5-99 470-D Reconditioning – Used Cars – Retail..................5-44 596-A 596-C Mopar Express Lane CP Labor....................5-100A

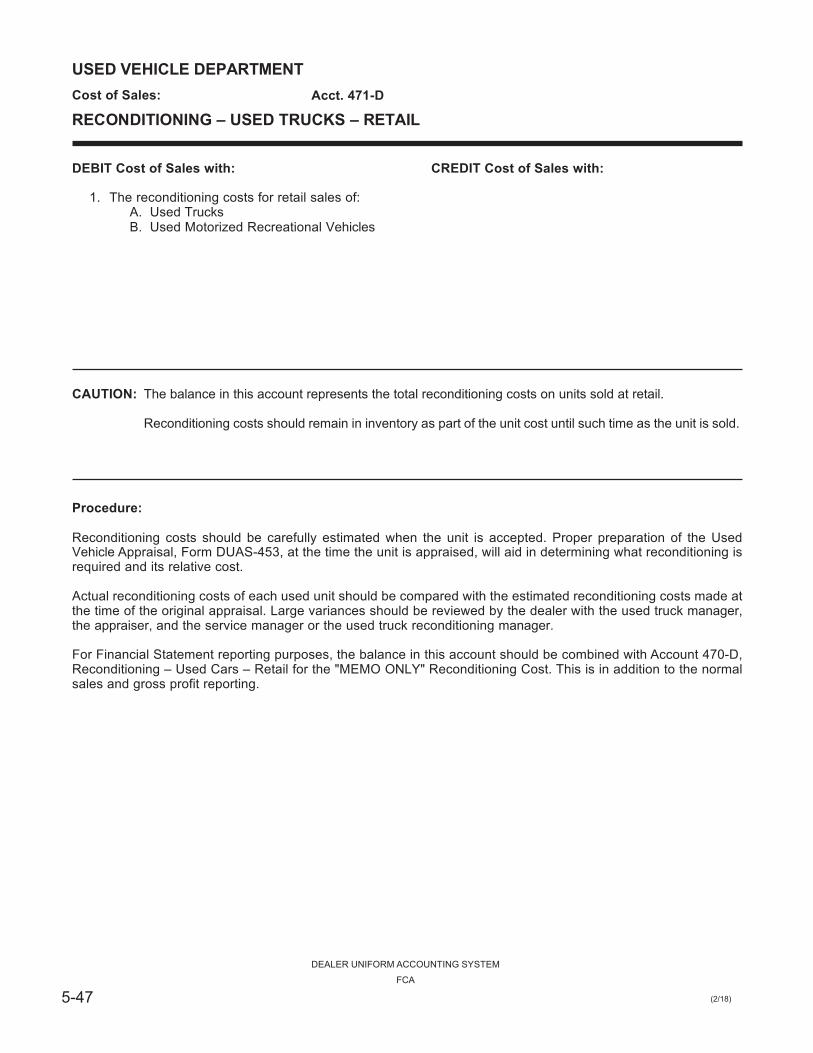

471-A 471-C Used Trucks – Retail.............................................5-45 597-A 597-C Mopar Express Lane Svc. Contracts Labor.5-100B 471-D Reconditioning – Used Trucks – Retail...............5-47 598-A 598-C Mopar Express Lane Warranty Labor..........5-100C

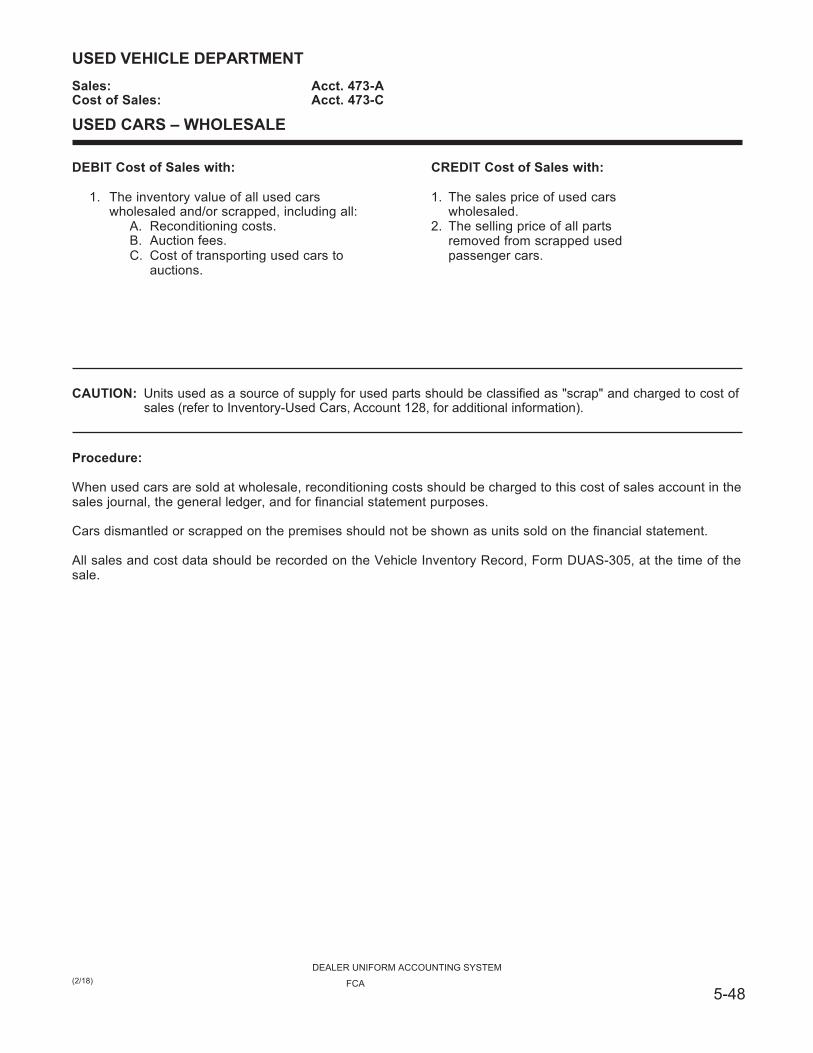

473-A 473-C Used Cars – Wholesale......................................5-48 599-A 599-C Mopar Express Lane Labor Internal.............5-100D DEALER UNIFORM ACCOUNTING SYSTEM

(2/18) FCA 1-5

OTHER INCOME AND OTHER DEDUCTIONS LEASING

ACCOUNT PAGE NUMBER NUMBER

OTHER INCOME

466-C Doc Fee/Administrative Fee – New………………………6-1 488-C Doc Fee/Administrative Fee – Used……………………..6-2 601 Cash Discounts Earned...................................................6-3 603 Interest Earned................................................................6-4 608 Gain on Disposal of Capital Assets.................................6-5 609 Miscellaneous Income.....................................................6-6 610 LIFO Adjustments............................................................6-7 615 Vehicle Lease and Rental Income...................................6-8

OTHER DEDUCTIONS 701 Cash Discounts Allowed..................................................6-9 704 Bonuses.........................................................................6-10 708 Loss on Disposal of Capital Assets...............................6-11 709 Miscellaneous Deductions.............................................6-12 710 LIFO Adjustments..........................................................6-13 715 Vehicle Lease and Rental Expense...............................6-14

LEASE AND RENTAL INCOME 803-8 Lease Income...................................................................7-3 807-8 Rental Income..................................................................7-4 809-8 Gain or Loss on (L&R) Vehicles…...................................7-5

EXPENSES DIRECT 920-8 Gasoline...........................................................................7-6 922-8 Maintenance and Repairs................................................7-7 927-8 Licenses, Titles and Taxes...............................................7-8 928-8 Depreciation.....................................................................7-9 929-8 Insurance.......................................................................7-10 930-8 Interest...........................................................................7-11

SELLING 940-8 Salaries, Wages and Commissions...............................7-12 945-8 Company Cars...............................................................7-13 947-8 Pick-up and Delivery......................................................7-14 949-8 Advertising & Promotion................................................7-15 951-8 Bad Debts......................................................................7-16 955-8 Miscellaneous................................................................7-17

1-6

DEALER UNIFORM ACCOUNTING SYSTEM

FCA

(2/18)

CURRENT ASSETS Account 101

PETTY CASH FUND

DEBIT with:

1. The amount set aside when the Petty Cash

Fund is established, and for any increase in the amount of the fund.

CREDIT with:

1. Any decrease in the amount of the fund, or when the fund is eliminated.

CAUTION: The amount of the Petty Cash Fund should be held to minimum requirements. Large sums should not be paid out of the Petty Cash Fund. Payroll or payroll advances should not be made from the Petty Cash Fund. Cash received in the regular course of business should not be commingled with Petty Cash. All Petty Cash Vouchers should be controlled and accounted for numerically.

Procedure:

This is a fund set aside for use (1) to pay small purchases that cannot conveniently be paid by check, and (2) as a change fund.

The Petty Cash Fund should be divided to establish:

1. A Petty Cash Fund used only to pay small bills. 2. A change or Cashier Fund(s).

Disbursements from the Petty Cash Fund should be recorded and explained on a Petty Cash Voucher, form DUAS- 123. Petty Cash Vouchers should be pre-numbered. They should be issued and accounted for in numerical sequence. No Petty Cash Vouchers should be destroyed. If, for any reason, a voucher is spoiled, it should be marked "VOID" and filed in proper numerical order with the other vouchers.

The voucher serves as a receipt from the person receiving the money. Vouchers should be prepared in ink, signed by recipient, and approved by the proper person(s). Paid invoices should be attached to the related voucher supporting the disbursement of funds. At the end of each month, or at more frequent intervals, if necessary, all vouchers should be summarized on a Petty Cash Summary Envelope, Form DUAS-331, for reimbursement to the fund. All Petty Cash Vouchers, paid bills, and Petty Cash Summary Envelopes should be properly cancelled when paid.

The sum of all Petty Cash Vouchers on hand, plus actual cash, should always equal the amount of the Petty Cash Fund. It is recommended that checks issued to reimburse the fund be made payable to the custodian of the fund, i.e., J. H. Doe - Petty Cash.

(2/18)

DEALER UNIFORM ACCOUNTING SYSTEM

FCA 2-1

CURRENT ASSETS Account 102

UNDEPOSITED CASH

DEBIT with:

1. All cash received. 2. Cash overages.

CREDIT with:

1. All daily bank deposits.

CAUTION: The balance exceeding the amount of the Cashier Fund represents undeposited receipts. All cash received should be deposited each banking day, intact as received. No money should be paid out of the Undeposited Cash Account.

Procedure:

This is a clearing account for all cash received in the ordinary course of business and not yet deposited in the bank.

All cash received, regardless of the source, should pass through the hands of the Cashier, or other responsible person, for proper recording. It is recommended that individual, pre-numbered Cash Receipts, Form DUAS-101, be used.

NOTE: Customer finance company payments should be in the form of cash or money order only, and should

be recorded in a separate receipt book. Such payments should be remitted to the finance company daily. (Refer to Account 201-D for additional information.)

Receipts that are voided should carry an explanation thereon and all copies kept intact. It is recommended that voided receipts be recorded in the Cash Receipts Journal in numerical sequence with other receipts for accountability.

Receipts from a third party (one party making payment of another's account) or endorsed checks (where a third party is the maker) should indicate the names of both parties. For legal reasons, all receipts should bear the full signature of the Cashier rather than being merely initialed.

It is recommended that all checks received, be endorsed immediately with the dealership bank deposit stamp. This practice will serve to safeguard both the dealership and the customer in the event a check is lost or stolen.

Cash overages and shortages should be recorded daily. Overages should be recorded in the Cash Receipt Book and included in the bank deposit. Shortages in the daily deposit should be charged/debited to Account 709, not taken out of the petty cash box.

2-2 DEALER UNIFORM ACCOUNTING SYSTEM

FCA

(2/18)

CURRENT ASSETS Account

CASH IN BANK 103

DEBIT with:

1. The total of all cash deposited. 2. Stop payment orders on issued checks

that may be: A. Lost B. Incorrect

3. Contracts and Drafts deposited by a third party, i.e., sight drafts.

4. Bank Credit Memorandums issued.

CREDIT with:

1. The amount of all checks issued. 2. Bank Debit Memorandums issued. 3. Customer checks returned for:

A. Insufficient Funds B. Stop Payment

CAUTION: Daily receipts should be deposited intact each day. Night depository facilities should be used on business days when banks are closed and when sizable amounts of cash are received after office hours. The check protector/writer and all unused checks should be properly safeguarded to minimize the possibility of being stolen, lost, or misused. E.F.T. Electronic Funds Transfer must be arranged in order to process payments to DAAs. Dealer must be on E.F.T. to receive funds electronically. Dealer must also pay FCA with E.F.T.

Procedure:

Whenever separate bank accounts are maintained (general, payroll, trust, etc.) the basic Cash In Bank account number (103) may be sub-accounted by adding a letter suffix, e.g., Cash In Bank–General, Account 103-A; Cash In Bank–Bank Credit Cards, Account 103-B; Cash in Bank-Payroll Account 103-C; etc. If more than one bank account is maintained, a separate general ledger sheet, properly identified, should be provided for each account. The balances in these accounts should be combined into one total for financial statement purposes.

Deposit slips should be prepared in duplicate, but preferably in triplicate, with copies distributed as follows:

Original–retained by bank Duplicate–authenticated by bank and returned to dealership Triplicate–authenticated by bank and returned directly to dealer's attention by bank

All checks should be listed on the deposit slip indicating the name of the maker and the name of the endorser when applicable. This procedure will facilitate identification of all receipts being deposited.

Voided dealership checks should remain intact and the signature area punched or removed to preclude possible future use. Voided checks should be recorded in the Cash Disbursements Journal in their proper numerical sequence with other checks for accountability.

Bank service charges, charge backs, and other bank debit memorandums should be properly and promptly recorded in the Cash Disbursement and Purchase Journal so that the "Bank" balance can be accurately and readily ascertained.

The month-end general ledger balance should be reconciled with the balance shown on the bank's statement. Any variances should be promptly investigated and resolved. Bank Reconciliation, Form DUAS-379, should be used for this purpose.

(2/18)

DEALER UNIFORM ACCOUNTING SYSTEM

FCA 2-3

CURRENT ASSETS Account 104

CASH ON DEPOSIT

DEBIT with:

1. The total amount of cash deposited with a

finance institution in an interest bearing account.

2. The amount of cash that is on deposit in certificates of deposit, high interest yield savings accounts, CMA, etc.

CREDIT with:

1. The amount of "Cash On Deposit" which financing institution applies against outstanding floor plan liability.

2. The amount of "Cash on Deposit" returned to dealership by financing institution.

CAUTION: The balance in this account should represent the amount of excess cash deposited with financing institution(s) in interest bearing accounts.

Procedure:

Finance institution statements should be reconciled immediately upon receipt.

The amount of interest earned on the monies deposited should be recorded as follows: 1. Interest earned on cash deposited in certificates of deposit, high interest yield savings accounts, etc., should

be a credit to Account 603, Interest Earned. 2. Interest earned on cash deposited to reduce the monthly interest charges on floor plan liability, should be a

credit to Account 315, Interest On Floor Plan Expense-New.

2-4 DEALER UNIFORM ACCOUNTING SYSTEM

FCA

(2/18)

CURRENT ASSETS Account 106

CONTRACTS IN TRANSIT

DEBIT with:

1. The net amount (unpaid balance) of

customer finance contracts offered and/or submitted to financing institutions.

CREDIT with:

1. The amount(s) received from finance institutions on customer finance contracts accepted.

CAUTION: The customer's purchase order, the vehicle sales invoice, and the finance contract should correspond in details; discrepancies may lead to legal complications.

Contracts in Transit should not be construed as Vehicle Receivables (Account 111).

Procedure:

Finance contracts should be reviewed daily to determine that remittances are received promptly. Any contracts or balances outstanding more than two or three days should be investigated to determine the cause of the delay and to ascertain when payment may be received.

At each month-end, a list of contracts for which payments have not been received should be prepared on Monthly Analysis Summary, Form DUAS-373, or a Computer generated schedule with a list of outstanding contracts by name and customer number.

To improve control of this account and facilitate collection follow up, the month-end schedule should be prepared as follows:

Finance Customer Contract Date Amount Date Paid Company Name Date Submitted

(2/18)

DEALER UNIFORM ACCOUNTING SYSTEM

FCA 2-5

CURRENT ASSETS Account 110

SERVICE AND PARTS ACCOUNTS RECEIVABLE

DEBIT with:

1. The amount of service, parts, and accessory items sold to customers on open account.

2. C.O.D. shipments of parts and accessories sold to customers.

3. Customers' checks returned by the bank. (Separate account for NSF Checks)

CREDIT with:

1. Payments received from customers on service and parts accounts.

2. Cash discounts allowed for prompt payment.

3. Credit Memoranda issued to customers for service and parts adjustments.

4. Accounts determined to be uncollectible. Separate allowance for doubtful accounts should be used for the reserve.

CAUTION: This is a control account. The account balance represents the total of all unpaid balances in the Accounts Receivable Subsidiary Ledger, for all open account sales (including Non-Automotive and Other Automotive merchandise) by the Service and Parts Departments.

The responsibility of extending credit and collection activities should be delegated to one person. New accounts should be added only after a complete credit investigation has been made.

Procedure:

Credit once established should be continued only as long as the customer maintains his account on a current basis. Collection follow-up action should be taken as soon as the account becomes past due. Collection follow-up information should be recorded on the individual customer's ledger sheet, and on the accounts receivable aged analysis prepared each month-end.

Each month-end this account balance should be in agreement with the subsidiary ledger. The subsidiary ledger balances should be scheduled. A Trial Balance and Analysis of Receivables with Collection Follow-Up sheet should be used.

Credit balances in this account should be shown on Line 7 under Current Liabilities on the financial statement.

A diligent, systematic collection effort of all accounts will lessen bad debt losses.

A separate sub account could be maintained for all NSF checks. (Sub account 110-A)

See Account 378, Bad Debts, for handling of write-offs, before uncollectible accounts are written off, authorization of Management should be obtained.

2-6 DEALER UNIFORM ACCOUNTING SYSTEM

FCA

(2/18)

CURRENT ASSETS Account 111

VEHICLE ACCOUNTS RECEIVABLE

DEBIT with:

1. All vehicle deposits applied against

customer purchases. 2. The amounts of vehicle sales to customers

on open account. 3. Vehicle customers' checks returned by the

bank uncollected, (Separate account for NSF Checks should be scheduled).

CREDIT with:

1. Customer deposits received on future vehicle sales.

2. The amount of vehicle account payments received.

3. Appraised value of used vehicles taken in trade (See NOTE).

4. Accounts ascertained to be uncollectible.

CAUTION: This is a controlled account of all unpaid balances in the Vehicle Accounts Receivable Subsidiary Ledger, for all open account sales (including Non-Automotive and Other Automotive merchandise) sold by the New and Used Vehicle Departments. This account should be scheduled and controlled by Customer number, or vehicle VIN number.

Contracts in Transit and Cash Sales should not be recorded in this account.

To minimize collection problems each open account balance should be secured by a contract (discountable at a finance company or bank), or by a properly executed purchase order for fleet accounts.

Procedure:

The Sales Manager, or other authorized person, should check to verify that all vehicle documents are in order and that all cash due on each vehicle sale has been received before the vehicle is released to the customer.

Each month-end, individual customer's account balances should be scheduled. A Trial Balance and Analysis of Receivables with Collection Follow-Up sheet should be used. The total of the amounts listed should agree with the balance in this account.

Credit balances in this account should be shown on Line 7 under Current Liabilities of the financial statement.

Collection follow-up information should be recorded on the accounts receivable schedule prepared each month-end.

A diligent, systematic collection effort of accounts will lessen bad debt losses.

NOTE: When a used vehicle is taken in trade prior to the delivery of the new vehicle, it is recommended that

a journal entry be made charging the used vehicle inventory with the appraised value of the unit. The offsetting credit should be to this account for the same amount. The customer's receivable account card should show the amount of the deposit as equal to the appraised value of the used vehicle, with a memo amount equal to the overallowance. At the time the new vehicle order is written the appraised value, or the amount the customer would receive in cash if the order were cancelled, should be noted on both copies of the new vehicle order. This procedure should be followed to avoid any misunderstanding as to the amount due the customer if the order is cancelled. At the time of the retail delivery of the new vehicle, the Vehicle Accounts Receivable in the sales journal should be debited for the net amount of the deposit, and the overallowance column debited for actual overallowance as shown on the customer's receivable account card.

(2/18)

DEALER UNIFORM ACCOUNTING SYSTEM

FCA 2-7

CURRENT ASSETS Account 112

CUSTOMER NOTES RECEIVABLE

DEBIT with:

1. The face value of notes received on

vehicle sales. 2. The face value of notes accepted on

service and parts sales. 3. Deferred Certificates from finance

companies. 4. Other notes received.

CREDIT with:

1. Collections from customers on notes. 2. Payments received from finance

companies on Deferred Certificates. 3. The unpaid balance of note(s), when the

collateral securing the note(s) has been repossessed.

4. Notes and Deferred Certificates ascertained to be uncollectible.

CAUTION: This is a control account and the account balance represents the total of the unpaid balances of all notes in the Subsidiary Ledger.

"Side Notes" accepted in lieu of cash on vehicle sales should be discouraged and avoided.

All notes, regardless of their source, should be recorded on the dealership's books.

Procedure:

Deferred Certificates are instruments issued to dealerships by finance institutions for amounts withheld from the principal sum of the contracts when they are discounted. They become collectible at a specified future date, usually on or before the final maturity date of the contract.

The total amount of Deferred Certificates and "Side Notes" (notes accepted in lieu of cash) on vehicle sales that are financed should be reserved 100% as doubtful accounts.

Notes Receivable represent dealership cash funds that are invested in previous sales, and prudence should be exercised to insure that such funds are profitably converted back to the cash position.

Each month-end, this account balance should be in agreement with a detailed schedule. Prepare a Trial Balance and Analysis of Receivables with Collection Follow-Up sheet.

NOTE: Interest income derived from notes should be taken into earnings, as installments are paid. At such

time, the portion representing interest earned should be credited to Interest Earned, Account 603, or, in the case of vehicle notes, the applicable Finance and Insurance, Accounts 457-F or 481-F, in accordance with existing tax regulations. The application of interest to Finance and Insurance Income will help defray any repossession losses.

2-8 DEALER UNIFORM ACCOUNTING SYSTEM

FCA

(2/18)

CURRENT ASSETS Account 114

OTHER RECEIVABLES

DEBIT with:

1. Amount of vehicles, service, parts, and

accessories sold to a leasing subsidiary company on open account.

2. Direct leasing receivables resulting from leases written by the dealership.

3. All amounts due resulting from retail leasing sales to financial institutions.

4. Amounts due from Dealer Group (advertising) Funds. i.e., PPA, DAA Monies.

5. All other receivables, including manufacturers other than FCA, not provided in the Chart of Accounts.

CREDIT with:

1. Payments received on accounts. 2. Cash discounts allowed for prompt payment. 3. Adjustments in accounts. 4. Accounts determined to be uncollectible.

CAUTION: This is a control account and the account balance represents the total of the unpaid balances of all individual accounts as detailed in the subsidiary ledger. Each sub account should be scheduled.

Use this account for all factory receivables due from manufacturers other than FCA.

Procedure:

This account may represent numerous types of receivables. Individual subsidiary ledgers schedule should reflect all pertinent information to document the various receivables.

The PPA amount on the factory invoice should be setup as a receivable from the DAA in this account. These amounts are included on the direct factory invoices together with the EB/PF charges (if elected). The PPA monies are an offset to the vehicle inventory cost at time of stocking into the dealership inventory.

All amounts due in settlement of retail leasing sales to financial institutions should be handled through this account for better internal control.

This account should NOT be used to record security deposits on lease agreements held by the dealership. See Security Deposits: Lease Vehicles, Account 240.

Lease vehicle agreements normally stipulate payment in advance on a monthly basis by the lessee. That is to say, billings made on the 25th of the current month, are due and payable on the 1st of the following month. Income is taken in the month in which earned (whether or not payment is received); therefore, billings are not recorded until the 1st of the month following the billing date. NOTE: This means that billings are considered PAST DUE if not paid by the 1st of the month following the billing date.

Each month-end the individual account balances should be scheduled. A Trial Balance and Analysis of Receivables-with Collection Follow-Up sheet should be used.

Collection follow-up information should be recorded on the individual account ledger sheets and on the schedule prepared each month-end.

Credit balances in this account should be shown on Line 7 of the financial statement under Current Liabilities.

(2/18)

DEALER UNIFORM ACCOUNTING SYSTEM

FCA 2-9

CURRENT ASSETS Account 116-A

FACTORY RECEIVABLES: WARRANTY SERVICE CLAIMS/ROAD READY CLAIMS

DEBIT with:

A. The amount of warranty repairs submitted

to the factory (less any deductible charges) covering:

1. Labor 2. Replaced parts and accessories 3. Sublet work

B. The amount of transportation claims filed

and submitted to the factory.

C. The amount of road ready/full tank of gas reimbursement authorized by the factory.

CREDIT with:

1. All cash and/or credits received from the factory applicable to such claims.

2. The amount of all disallowed claims.

3. Any variance between the amount

claimed and the actual amount paid by the factory.

CAUTION: Warranty service records must be maintained in accordance with instructions in the Dealer Warranty and Policy Procedure Manual.

All claims will be processed and paid under existing policies and procedures without regard to the WSC-Advance Payment.

This account should be used for receivables due from FCA only.

Procedure:

This is a control account and the total of the individual open claims listed in the Warranty Sales Journal and Claims Register should agree with this general ledger account balance each month-end.

The offsetting entry for variances (overages, shortages, or denials) between the amount claimed and the amount paid by the factory should be made to Policy Adjustments, Accounts 346A, 346B and 356.

Road ready/full tank of gas reimbursements will be automatically credited to the dealership when notified by the carrier that the vehicle has been delivered.

2-10 DEALER UNIFORM ACCOUNTING SYSTEM

FCA

(2/18)

CURRENT ASSETS Account

Article 1. 116-A1

FACTORY RECEIVABLES: WSC – ADVANCE PAYMENT

DEBIT with:

1. Any reductions in the amount of the

advance, or upon termination of the program.

CREDIT with:

1. The amount of the original advance payment received.

2. Any subsequent increases in the amount of the advance.

CAUTION: This sub-account is established solely for the purpose of accounting for advance payments made to dealers by FCA in accordance with the Advance Warranty Payment Program.

Procedure:

This is a sub-account of Warranty Service Claims, Account 116-A. This WSC-Advance Payment account should reflect a credit balance at all times. The balance in this account should agree with the monthly amount indicated on the dealer's (parts) statement furnished by FCA.

For Financial Statement Reporting: Account 116-A1 should be recorded on Line 8, Page 1 under Liabilities.

Warranty Claims will continue to be processed and paid under existing policies and procedures without regard to the advance.

(2/18)

DEALER UNIFORM ACCOUNTING SYSTEM

FCA 2-11

CURRENT ASSETS Account 116-B

FACTORY RECEIVABLES: HOLDBACK - NEW CARS AND TRUCKS

DEBIT with:

1. The amount of holdback indicated on

the factory invoice, or as computed from the Confidential Price Bulletin, for the specific vehicle.

CREDIT with:

1. All cash and/or credits received applicable

to this account.

CAUTION: The Holdback amount should be recorded by individual unit in a separate schedule. The account balance represents all open items recorded in the New Vehicle Purchases Journal for which payment has not been received.

This account should be used for receivables due from FCA only.

Procedure:

A subsidiary schedule or ledger is required, as the detail entry will adequately identify each unit and the applicable holdback. When payment is received from FCA, a supporting schedule of units will be enclosed, furnishing adequate information applicable to each unit. The date the payment is received should be recorded in the appropriate Journal opposite the amount due. Any variances between the amount due and the amount received should be located, their source determined, and proper disposition made. The individual unit amounts remaining unpaid should always equal the account balance in the general ledger.

New vehicles purchased from FCA should be recorded at cost less the vehicle holdback and the PPA funds reflected on the invoice.

In all instances where new vehicles are purchased from, sold to, or traded with other direct dealers, they are considered TRANSFERS and should, therefore, be recorded in a separate Dealer Trade Journal.

When new vehicles are transferred between direct dealers and the Holdback is included in the price of the new vehicles being transferred, the Dealer Uniform Accounting Procedure is as follows:

1. New Vehicles Sold to Another Direct Dealer The Holdback received from the direct dealer purchasing the new vehicle should be credited to Miscellaneous Income, Account 609.

2. New Vehicles Purchased From Another Direct Dealer The Holdback paid to the direct dealer selling the new vehicle should be debited to Miscellaneous Deductions, Account 709.

3. New Vehicles Traded Between Direct Dealers The Holdback applicable to new vehicles traded between direct dealers should be handled as outlined in Items 1 and 2 above.

Income resulting from the sale of new vehicles to other direct dealers should be considered as Miscellaneous Income; and losses resulting from the purchase of new vehicles from other direct dealers should be considered as Miscellaneous Deductions. (It is suggested that sub-accounts be used to permit a closer control and reconciliation of the income and losses sustained from these types of transactions.)

2-12 DEALER UNIFORM ACCOUNTING SYSTEM

FCA

(2/18)

CURRENT ASSETS Account 116-C

FACTORY RECEIVABLES: SPECIAL VEHICLE INCOME

DEBIT with:

1. The amount due from the factory in accordance with Sales/Purchase Incentive Programs applicable to the respective vehicle lines.

2. The amount of the Delivery Allowance due from the factory in accordance with the FCA Management Employee New Vehicle Purchase Plan.

CREDIT with:

1. All cash received and/or credit allowed applicable to the various programs identified in this account.

CAUTION: Sales/Purchase Incentive Programs should be studied thoroughly to assure proper understanding of the specific programs and all provisions. To do so will facilitate proper accounting whereby earnings are recorded in the current period. If more than one Incentive Program is in effect during a specific model year, it is recommended that each program be separately identified and controlled. A Distribution Sheet should be used for this purpose. This account should be used for receivables due from FCA only.

Procedure:

Units properly recorded in the New Vehicle Department-Sales Journal, reflecting the Special Vehicle Income earned under each incentive program, you may consider maintaining an additional receivable schedule or register.

The following accounting procedure provides a uniform method of recording the Special Vehicle Income regardless of the amount and program variations.

BONUS PROGRAM EXAMPLE

1-5 units $25.00 each 6-10 units $50.00 each-retroactive to 1st unit

11 or more units $75.00 each-retroactive to 1st unit

It is recommended that each sales journal sheet, and the general ledger account sheet, be properly identified indicating each bonus level of the incentive program (in this example, the above levels would be recorded):

Step A. When recording each of the first 5 unit sales in the New Vehicle Department-Sales Journal, enter

$25.00 in the Special Vehicle Income column applicable to the make of vehicle to which the bonus applies. This Special Vehicle Income column provides for a dual-posted entry.

Step B. When the sixth unit is sold and before the sale for that unit is recorded in the New Vehicle Department–Sales Journal, the following journal entry should be made in the Special Vehicle Income column: "Retroactive on Units 1 thru 5 (CONTEST NAME)" $125.00

Step C. When recording each of the next 5 unit (6-10) sales, enter $50.00 (next plateau) in the Special Vehicle Income column applicable to the make of vehicle to which the bonus applies.

(2/18)

DEALER UNIFORM ACCOUNTING SYSTEM

FCA 2-13

CURRENT ASSETS Account 116-C

FACTORY RECEIVABLES: SPECIAL VEHICLE INCOME (Cont’d)

Procedure:

As each plateau, or retroactive base, is attained repeat Steps B. and C. above. This method will furnish a continuous schedule of Special Vehicle Income, and may be repeated under each incentive program. Numbering the sales within each car line in the New Vehicle Department-Sales Journal, beginning with the first eligible unit, will permit an accurate computation of the Special Vehicle Income as each retroactive bonus level is reached.

The following provides a uniform method of recording Market Performance Allowance Program, each dealership is assigned a unit number that must be obtained. 100% of this goal must be met before any monies are due. FCA sets the dollar amount. This amount will vary depending upon the percentage over and above the 100% goal. A complete record must be kept. Dealership can verify MPA attainment through the NVDR system. Before month end-closing dealership must make the necessary entries to set up the receivable and entry to cost of sales 401-D thru 449-D.

The schedules should be set up controlled by program number with sales invoice or VIN. Computation of amounts due and Maintenance of subsidiary records should be in accordance with instructions on individual programs. At month end, the total of open and unpaid items should be reconciled to the balance in each account.

The following is a list of FCA Programs that should be in this account.

1. Market Performance Allowance Program 2. Regional Market Allowance Program 3. Stock and Promote 4. Bonus Bank Program 5. Xtreme Profit Sharing

The above programs should all be scheduled separately. FCA will issue a supporting schedule to show each unit. This may be applied to the proper account. This account must be controlled.

2-14 DEALER UNIFORM ACCOUNTING SYSTEM

FCA

1/09

CURRENT ASSETS Account 116-D

FACTORY RECEIVABLES: FLOOR PLAN ALLOWANCE

DEBIT with:

1. The amount of all Floor Plan Allowance due from the factory.

CREDIT with:

1. The cash received and/or credits allowed applicable to this account.

CAUTION: Any variance between the amount due and the amount received should be investigated, resolved, and proper disposition made.

This account should be used for receivables due from FCA only.

Procedure:

Floor Plan Assistance Program, all domestic vehicles will be eligible for Floor Plan Assistance that reflects the actual in transit time from the date of collection to the date of delivery to a specific site or to dealership. Only eligible fleet Units will receive 15 day Floor Plan Assistance allowance in addition to the in transit Floor Plan Assistance.

The Supplemental Floor Plan Assistance Program (SFPAP) allowances may necessitate an additional schedule. The SFPAP payment will be made on a weekly basis to the factory invoiced dealer of record, following the reporting of the vehicle sale through the sales of reporting system (NVDR), or 120 days after shipment, whichever occurs first.

The object of these programs is to help reduce the floor plan interest expense, therefore the offsetting credit should be to interest on Floor Plan–New, Account 315-A. In the event the dealership does not floor plan new vehicles, the credit offsetting the receivable should be made to Miscellaneous Income, Account 609.

(2/18)

DEALER UNIFORM ACCOUNTING SYSTEM

FCA 2-15

CURRENT ASSETS Account 116-E

FACTORY RECEIVABLES: WHOLESALE COMPENSATION – PARTS

DEBIT with:

1. The amount of Wholesale Allowance earned on applicable parts sales.

CREDIT with:

1. The amount of all cash received

from the factory applicable to this account.

2. The amount of all credits issued by the factory applicable to this account.

CAUTION: Reference is made to the Parts Division's current Schedule of Discounts and Terms of Purchase and reporting forms for policies and procedures governing Wholesale Allowance. To participate in the Wholesale Allowance Plan and take advantage of the additional revenue available, the Dealer, Parts Manager, and Office Manager/Accountant must be thoroughly familiar with the information and conditions outlined in the referenced publications.

This account should be used for receivables due from FCA only.

Procedure:

The following procedures provide a uniform method of maintaining records and recording income, and are therefore recommended:

1. The Price Symbol (A, B, etc.) should be recorded on each parts counter invoice and repair order directly

following the part number (Example: 2070 158-A). Each qualified wholesale part listed on the invoice or repair order should reflect the allowance amount as published in the Master Parts Price List.

2. When posting parts invoices and repair orders to their respective sales journals, the wholesale allowance amount should be posted at the same time. The blank columns provided in the parts counter sales journal and repair order sales journal may be used as a double-posting column for this purpose. Caption the column Wholesale Compensation-Parts, Account 116-E; at the bottom of the column insert Debit A/C 116-E and Credit A/C 586-F.

3. The Wholesale Allowance Plan's reporting forms should be prepared and maintained on a daily basis. At month-end the forms should be totaled and compared with the total posted to the general ledger account to assure that the amount claimed on the reporting forms is the same as the amount recorded as earned.

2-16 DEALER UNIFORM ACCOUNTING SYSTEM

FCA

(2/18)

CURRENT ASSETS Account 116-F

FACTORY RECEIVABLES: INVENTORY REBATES

DEBIT with:

1. Amounts due from the factory for: A. Model year-end rebates on new

vehicles in inventory.

CREDIT with:

1. The cash and/or credits received applicable to this account.

CAUTION: Inventory rebates applicable to each vehicle line may be authorized each model year-end by Divisional General Sales Letters. The Parts Return Allowance Plan is described in the Parts Division's current Schedule of Discounts and Terms of Purchase. Compliance with this publication is mandatory to obtain the return credit allowance.

This account should be used for receivables due from FCA only.

Procedure:

MODEL YEAR REBATES The General Journal entry to record vehicle inventory rebates at model year-end, as evidenced by affidavit submitted to the Car Division, should be as follows:

Factory Receivables–Inventory Rebates Debit 116-F (total amount for qualified units per affidavit)

New Vehicle Inventories Credit 120, etc. (credit to affidavit units still in stock as of date of this entry) and/or Cost of Sales–New Vehicles Credit 401-C, etc. (credit for affidavit units sold from the effective date indicated in the Divisional General Sales Letters to the date of this entry)

Any variances between the original receivable amount and the remittance received should be adjusted through the appropriate cost of sale account if the unit has been sold, or the inventory account if the unit is still in stock. In the event the rebate payment is to be paid to the bank, or finance company, special handling may be required.

(2/18)

DEALER UNIFORM ACCOUNTING SYSTEM

FCA 2-17

CURRENT ASSETS Account 116-F

FACTORY RECEIVABLES: INVENTORY REBATES (Cont’d)

Procedure:

1. Dealerships will receive notification of the return allowance earnings applicable to eligible purchases by a

computed and printed "RA" amount on each invoice. Dealerships should provide for the accumulation of such earnings on a MEMO Basis. This may be accomplished at the same time the invoices are recorded on the Accounts Payable Voucher Envelope (or other subsidiary record) and the Cash Disbursements and Purchase Journal. A blank column should be captioned "MEMO-RA" on each document to designate the accumulated return allowance earned. These amounts may then be posted to the Memo Column of the General Ledger page used for the Parts Inventory, Account 130.

2. After the required forms are submitted and parts return shipment has been authorized, the following entry

should be made and thoroughly explained in the General Journal:

Factory Receivables–Inventory Rebates Dr 116-F (Net amount of return allowance for parts returned.)

Purchase Discounts Dr 585-E (Applicable discounts deducted from the return allowance.)

Inventory–Parts Cr 130 (Gross amount of parts returned.)

This entry will be made throughout the year as each cycled parts return is completed.

NOTE: Inasmuch as the final parts return will be made after December 31, the above Debit to Account

585-E should be made to Adjustments, Account 290, so as to eliminate any distortion in the operating account balances during the subsequent year.

3. When the Credit Memorandum for the return is received, the following entry should be recorded on the

Accounts Payable Voucher Envelope for FCA: Accounts Payable–FCA Dr 201-A

Factory Receivables–Inventory Rebates Cr 116-F