Drop Shipping: Who’s on the - … · Drop Shipping: Who’s on the Hook for Sales Tax? Scott...

28

Drop Shipping: Who’s on the Hook for Sales Tax? Scott Peterson, VP of U.S. Tax Policy and Government Affairs, Avalara

Transcript of Drop Shipping: Who’s on the - … · Drop Shipping: Who’s on the Hook for Sales Tax? Scott...

Drop Shipping: Who’s on the

Hook for Sales Tax?Scott Peterson, VP of U.S. Tax Policy and Government

Affairs, Avalara

Making sales tax less taxing.2 © Avalara CONFIDENTIAL & PROPRIETARY

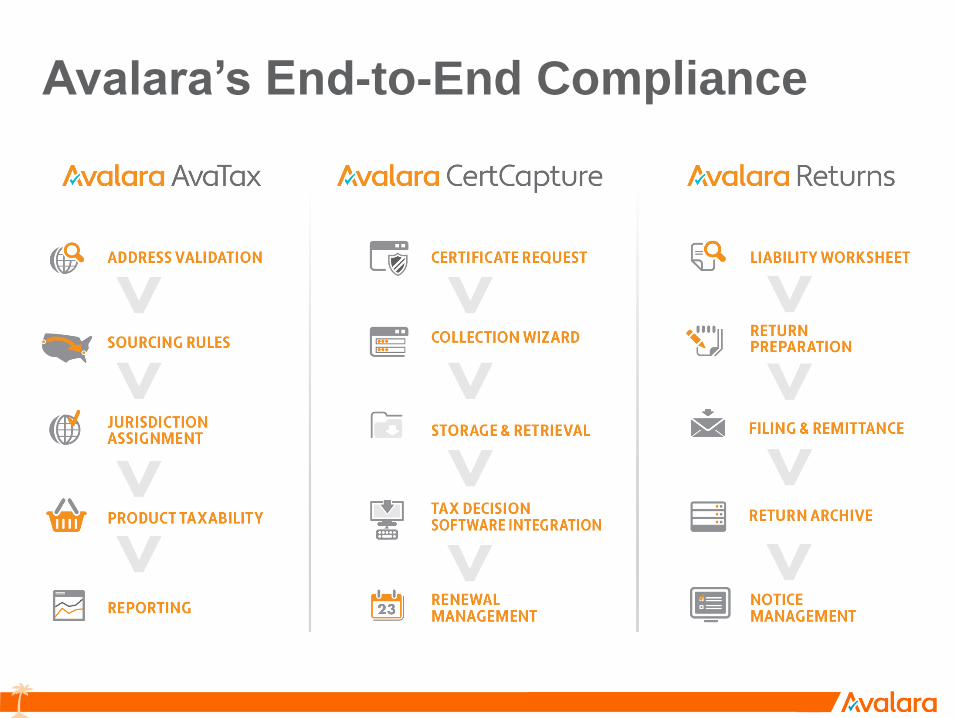

Avalara’s End-to-End Compliance

3 © Avalara CONFIDENTIAL & PROPRIETARY

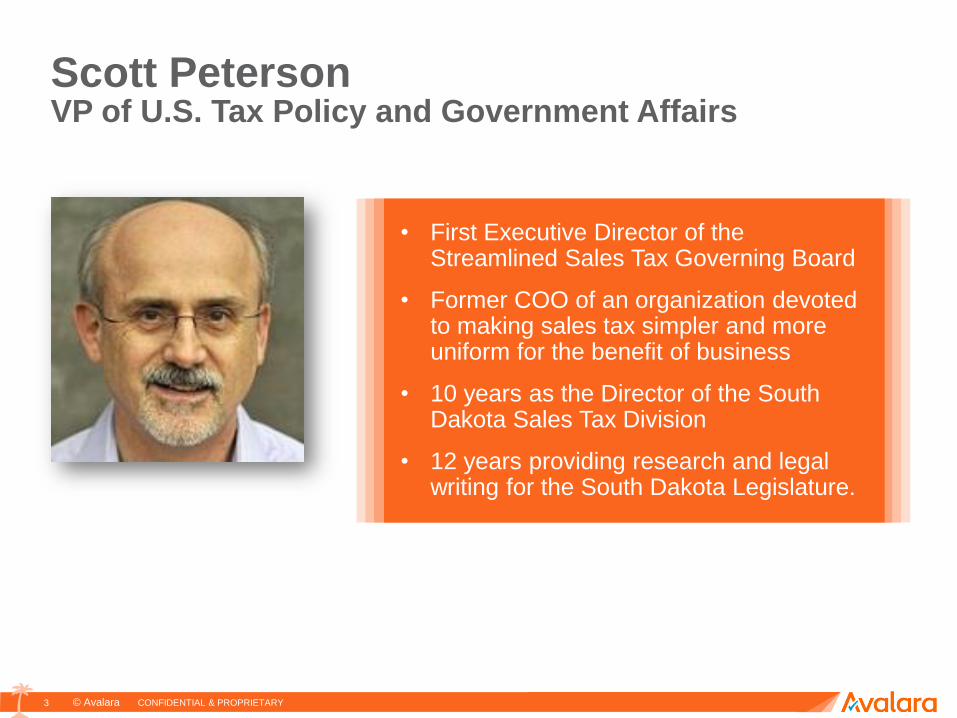

Scott PetersonVP of U.S. Tax Policy and Government Affairs

• First Executive Director of the Streamlined Sales Tax Governing Board

• Former COO of an organization devoted to making sales tax simpler and more uniform for the benefit of business

• 10 years as the Director of the South Dakota Sales Tax Division

• 12 years providing research and legal writing for the South Dakota Legislature.

Making sales tax less taxing.4 © Avalara CONFIDENTIAL & PROPRIETARY

Agenda

• Introduction

• What is Drop Shipping for Sales Tax Purposes

• Who collects: Vendors who Use Drop Shippers

or Drop Shippers

• Q&A

Making sales tax less taxing.5 © Avalara CONFIDENTIAL & PROPRIETARY

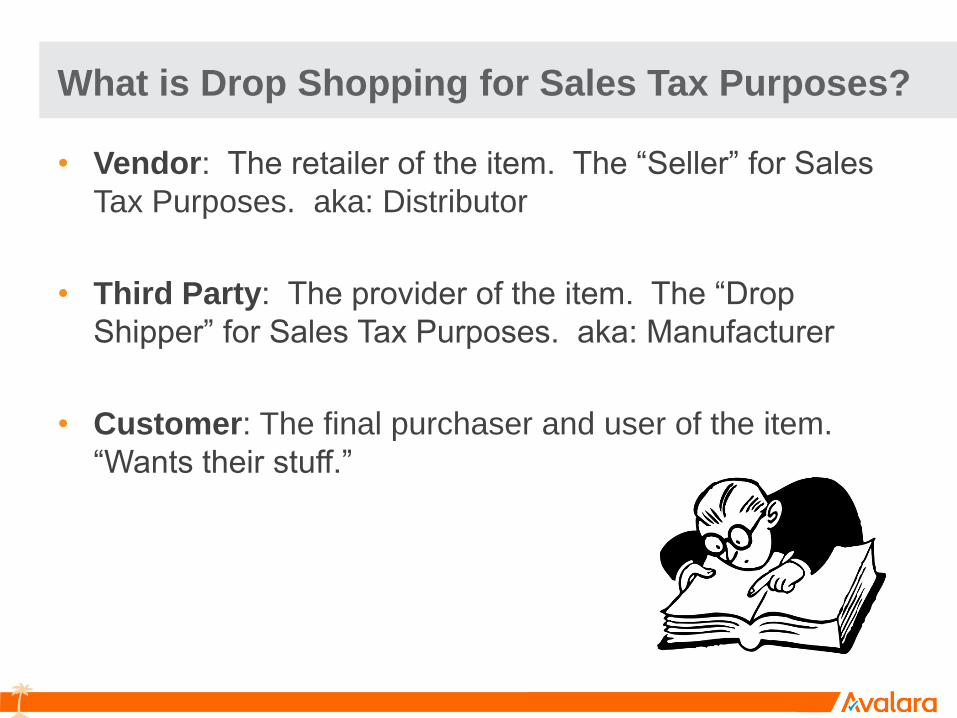

What is Drop Shopping for Sales Tax Purposes?

• Vendor: The retailer of the item. The “Seller” for Sales

Tax Purposes. aka: Distributor

• Third Party: The provider of the item. The “Drop

Shipper” for Sales Tax Purposes. aka: Manufacturer

• Customer: The final purchaser and user of the item.

“Wants their stuff.”

Making sales tax less taxing.6 © Avalara CONFIDENTIAL & PROPRIETARY

What is Drop Shopping for Sales Tax Purposes?

The Vendor

• accepts an order from a Customer,

• places the order with a Third Party,

• directs the Third Party to deliver the item directly to the

Customer, and

• bills the Customer for the item.

Making sales tax less taxing.7 © Avalara CONFIDENTIAL & PROPRIETARY

What is Drop Shipping for Sales Tax Purposes?

The Third Party

• accepts an order from a Vendor,

• delivers the order to the Customer,

• bills the Vendor for the items delivered.

Making sales tax less taxing.8 © Avalara CONFIDENTIAL & PROPRIETARY

What is Drop Shipping for Sales Tax Purposes?

The Customer

• places an order from a Vendor,

• pays the Vendor,

• receives the item directly from the Third Party.

Making sales tax less taxing.9 © Avalara CONFIDENTIAL & PROPRIETARY

What is Drop Shipping for Sales Tax Purposes?

• The Third Party may deliver the item to the Customer

in its own truck, arrange for delivery by common or

contract carrier, or have the customer pick up the item at

the third party's location.

• The Vendor does not make delivery, only sends the

customer an invoice.

Making sales tax less taxing.10 © Avalara CONFIDENTIAL & PROPRIETARY

What is Drop Shipping for Sales Tax Purposes?

• Vendor: The retailer of the item. The “Seller” for Sales

Tax Purposes.

• Third Party: The provider of the item. The “Drop

Shipper.”

• Customer: The final purchaser and user of the item.

“Wants his stuff.”

Making sales tax less taxing.11 © Avalara CONFIDENTIAL & PROPRIETARY

What is Drop Shipping for Sales Tax Purposes?

For Sales Tax Purposes, a Drop Shipment consists of

two sales:

1. The sale from the Vendor to the Customer.

2. The sale from the Third Party to the Vendor.

Making sales tax less taxing.12 © Avalara CONFIDENTIAL & PROPRIETARY

Who Collects?

• Nexus is the underlying legal issue.

• Nexus describes the contacts you have with a given

state and establishes whether that state can obligate

your company to collect sales taxes.

Making sales tax less taxing.13 © Avalara CONFIDENTIAL & PROPRIETARY

Who Collects?

A simple drop-ship relationship with a Third Party does not

typically trigger nexus for out of state Vendors. The actual

relationships between Third Parties and Vendors are subject to

scrutiny though.

States and the Courts evaluate items like these:

Does a Third Party…

• Store significant inventory on behalf of a Vendor?

• Solicit or advertise on behalf of the Vendor?

• Accept returns or orders on behalf of the Vendor?

• Makes referral to the Vendor?

• Have other customers besides the Vendor?

• Share Ownership with the Vendor?

• Process Orders, Returns or Process Payments to the Vendor?

Making sales tax less taxing.14 © Avalara CONFIDENTIAL & PROPRIETARY

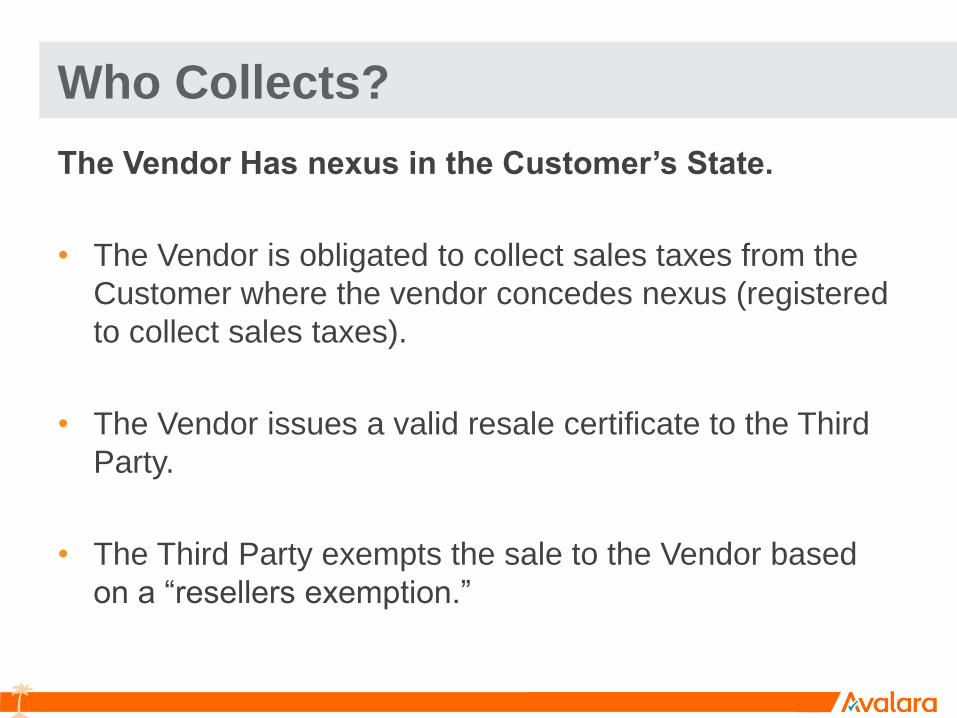

Who Collects?

The Vendor Has nexus in the Customer’s State.

• The Vendor is obligated to collect sales taxes from the

Customer where the vendor concedes nexus (registered

to collect sales taxes).

• The Vendor issues a valid resale certificate to the Third

Party.

• The Third Party exempts the sale to the Vendor based

on a “resellers exemption.”

Making sales tax less taxing.15 © Avalara CONFIDENTIAL & PROPRIETARY

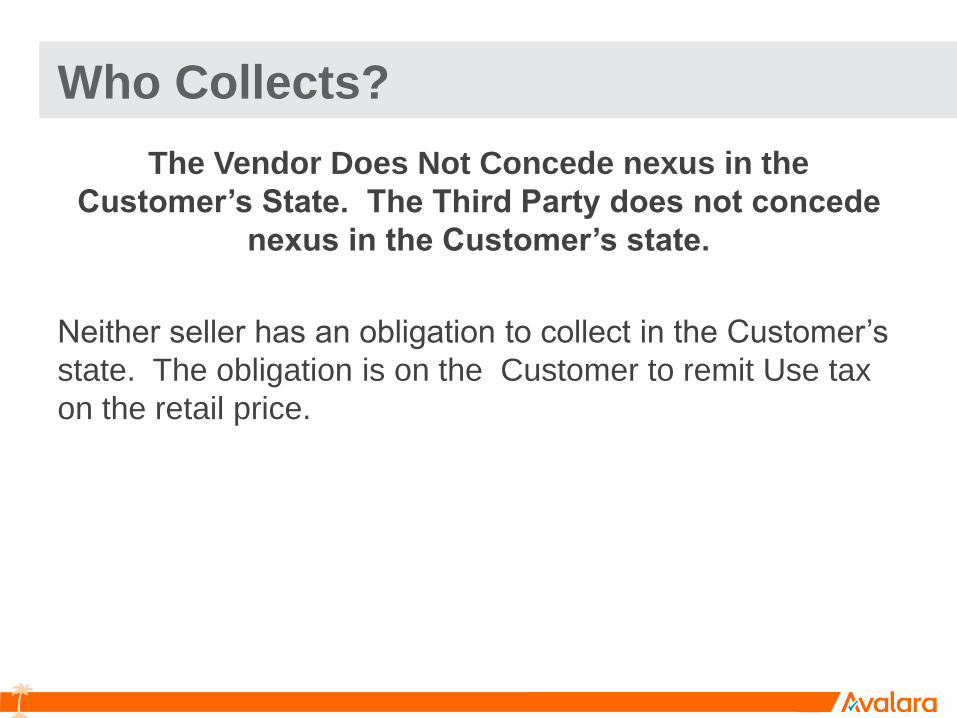

Who Collects?

The Vendor Does Not Concede nexus in the

Customer’s State. The Third Party does not concede

nexus in the Customer’s state.

Neither seller has an obligation to collect in the Customer’s

state. The obligation is on the Customer to remit Use tax

on the retail price.

Making sales tax less taxing.16 © Avalara CONFIDENTIAL & PROPRIETARY

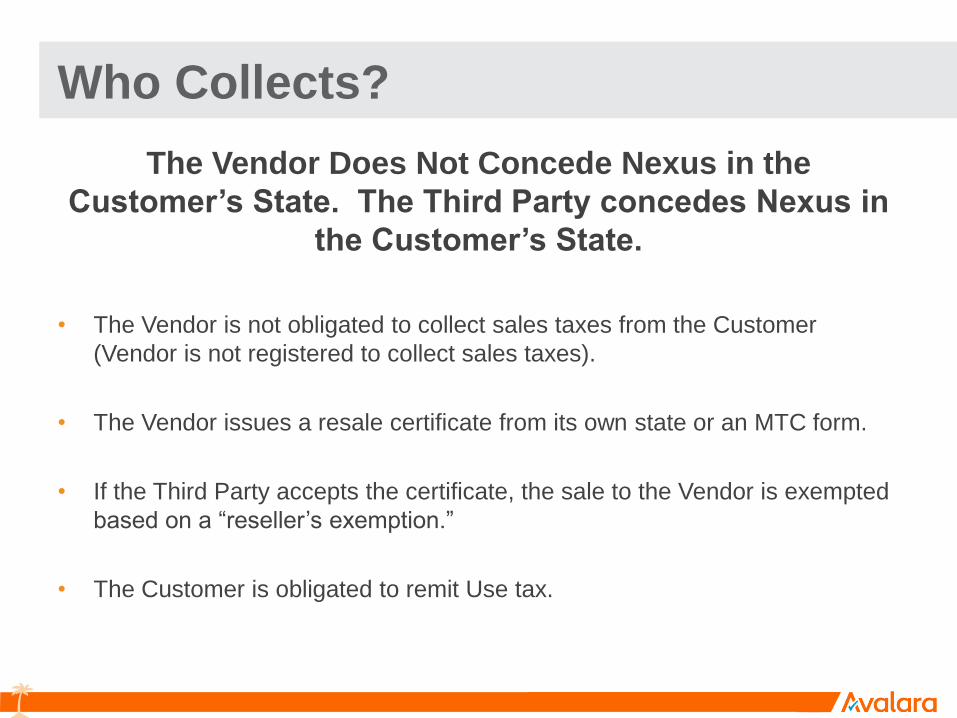

Who Collects?

The Vendor Does Not Concede Nexus in the

Customer’s State. The Third Party concedes Nexus in

the Customer’s State.

• The Vendor is not obligated to collect sales taxes from the Customer

(Vendor is not registered to collect sales taxes).

• The Vendor issues a resale certificate from its own state or an MTC form.

• If the Third Party accepts the certificate, the sale to the Vendor is exempted

based on a “reseller’s exemption.”

• The Customer is obligated to remit Use tax.

Making sales tax less taxing.17 © Avalara CONFIDENTIAL & PROPRIETARY

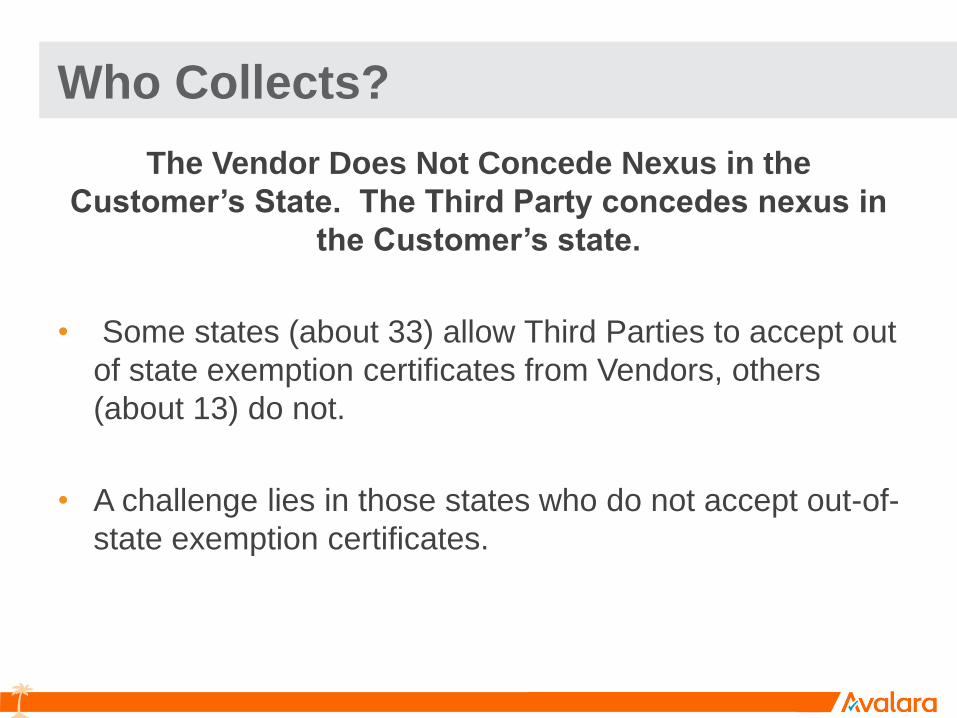

Who Collects?

The Vendor Does Not Concede Nexus in the

Customer’s State. The Third Party concedes nexus in

the Customer’s state.

• Some states (about 33) allow Third Parties to accept out

of state exemption certificates from Vendors, others

(about 13) do not.

• A challenge lies in those states who do not accept out-of-

state exemption certificates.

Making sales tax less taxing.18 © Avalara CONFIDENTIAL & PROPRIETARY

Who Collects?

The Vendor Does Not Concede Nexus in the

Customer’s State. The Third Party concedes nexus in

the Customer’s state.

• In States where foreign reseller exemption certificates

are accepted, the use tax obligation on the Customer.

Making sales tax less taxing.19 © Avalara CONFIDENTIAL & PROPRIETARY

Who Collects?

The Vendor Does Not Concede Nexus in the

Customer’s State. The Third Party concedes nexus in

the Customer’s state.

• In States where foreign reseller exemption certificates are not

accepted, rules exist to determine the appropriate tax base.

• For example, in CA, a Third Party is required to assess tax on the

sale to the Vendor at 110% of the price charged to the Vendor,

unless the Third Party knows the actual retail price paid by the

customer, then the Third Party must charge tax on the full retail

amount to the Vendor.

Making sales tax less taxing.20 © Avalara CONFIDENTIAL & PROPRIETARY

Who Collects?

The Vendor Does Not Concede Nexus in the

Customer’s State. The Third Party concedes nexus in

the Customer’s state.

In other states, the Third Party is obligated to collect sales taxes on the

actual price paid by the Vendor:

• DC

• Florida

• Louisiana

• Maryland

• Nebraska

• Nevada

• Tennessee

Making sales tax less taxing.21 © Avalara CONFIDENTIAL & PROPRIETARY

Who Collects?

The Vendor Does Not Concede Nexus in the Customer’s State. The Third

Party concedes nexus in the Customer’s state.

• Finally, some states obligate the Third Party to collect sales taxes on

the actual price paid by the Customer.

• California

• Connecticut

• Hawaii

• Massachusetts

• Rhode Island

• Wisconsin

Making sales tax less taxing.22 © Avalara CONFIDENTIAL & PROPRIETARY

Who Collects?

When a Customer has their own Exemption

Certificate, some states who do not allow the

Vendor’s foreign resale certificate will allow the

Third Party to accept a valid exemption certificate

from the final customer.

Making sales tax less taxing.23 © Avalara CONFIDENTIAL & PROPRIETARY

Takeaways:

1. There are Three Parties to a Drop Ship arrangement:

– Vendor

– Third Party

– Customer

2. There are Two Sales in a Drop Shipment:

– The sale from the Third Party to the Vendor

– The sale form the Vendor to the Customer.

Making sales tax less taxing.24 © Avalara CONFIDENTIAL & PROPRIETARY

Takeaways:

3. Use of a Third Party does not alter the obligation to

collect in a state where the Vendor already has nexus.

4. Even when a Vendor lacks nexus in the Customer’s

state, a Third Party with nexus in the customer’s state

may have an obligation to collect.

25 © Avalara CONFIDENTIAL & PROPRIETARY

Avalara streamlines the sales tax lifecycle

Real-time, accurate sales tax calculation

ERP,

Ecommerce,

POS / MPOS,

Payments,

etc.

Government

$ RemittancesTax rates

Customer invoice systems Automated storage,

management of tax certificates,

exemptions, etc.

Automated returnsprocessing and remittance

SaaS

26 © Avalara CONFIDENTIAL & PROPRIETARY

Guaranteed Accurate

For as long as you are a customer of Avalara AvaTax, if you ever suffer a negative audit finding and financial loss related to an inaccurate result returned by the Avalara service, we will pay your uncollected tax, penalty and interest, or refund your prior 12 months’ service fee, whichever is lower.

Learn more at Avalara.com

The right rate. Every time.

27 © Avalara CONFIDENTIAL & PROPRIETARY27

877-780-4848

Request a Demo

www.avalara.com/how-to-buy-avatax/

28 © AVALARA CONFIDENTIAL & PROPRIETARY

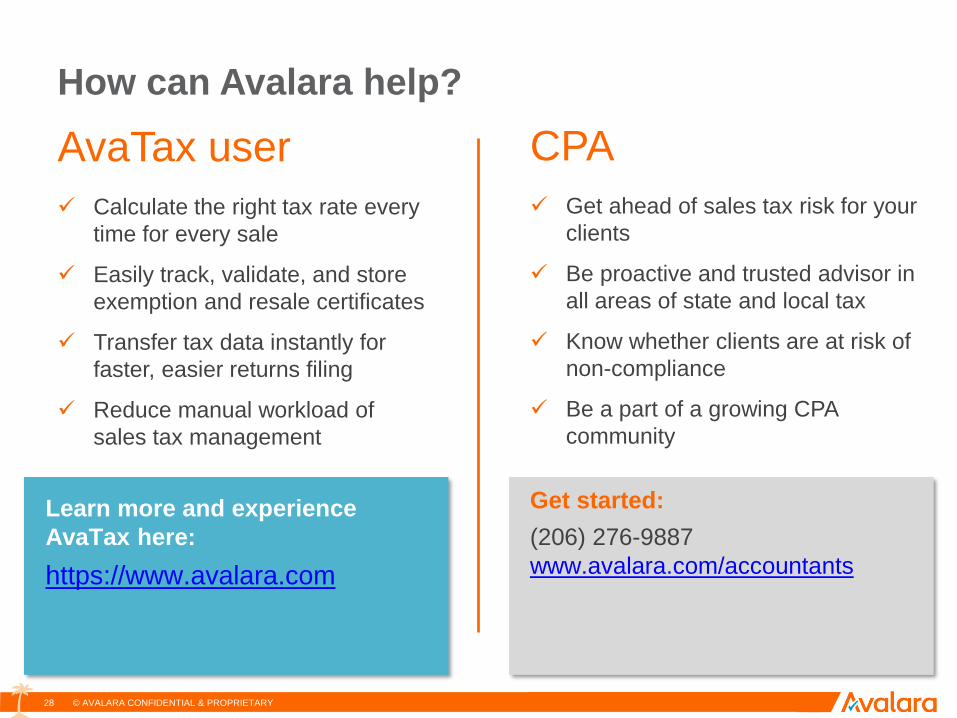

How can Avalara help?

AvaTax user

✓ Calculate the right tax rate every

time for every sale

✓ Easily track, validate, and store

exemption and resale certificates

✓ Transfer tax data instantly for

faster, easier returns filing

✓ Reduce manual workload of

sales tax management

CPA

✓ Get ahead of sales tax risk for your

clients

✓ Be proactive and trusted advisor in

all areas of state and local tax

✓ Know whether clients are at risk of

non-compliance

✓ Be a part of a growing CPA

community

Get started:

(206) 276-9887

www.avalara.com/accountants

Learn more and experience

AvaTax here:

https://www.avalara.com

![Order Fulfillment Process on Seller Center Drop-shippingVN].III.EN.Drop-shipping- Order... · 3 Drop-shipping Process •Verifying and fulfilling orders quickly can help prevent customers](https://static.fdocuments.us/doc/165x107/5b920b6609d3f210288d0be5/order-fulfillment-process-on-seller-center-drop-shipping-vniiiendrop-shipping-.jpg)