Driving Shopper Behavior in Grocery - Market Track · Marke rac Perspective TM Driving Shopper...

8

www.markettrack.com Market Track Perspective TM Driving Shopper Behavior in Grocery Survey results show high propensity to change stores and brands based on deals ompetition in the grocery space has never been more intense. As trade class lines blur and a larger focus is placed on grocery items in mass, dollar, club and drug stores, grocery retailers have had to expand their competitive set considerably. Add to that an uncertain economy, increased fuel costs and extreme weather in many parts of the country, and you now have shoppers who have become much more price conscious and promotionally driven. As we discovered in our recent Grocery Shopper Insight Survey, shoppers are more actively looking for where to find the best price on household items and groceries, and have a very high propensity to switch stores and brands. It has become increasingly difficult to understand how to incent an everyday shopper on their weekly grocery shopping trip to pick one grocer over another, or one brand over another. How do those in the grocery space ensure they are capturing the attention of an increasingly discriminating shopper? Shoppers are selective—over 40% are going to more than one store to complete their grocery shopping, with three-quarters citing “better prices on certain products and categories” as the reason for shopping at multiple stores, according to our recent Grocery Shopper Insight Survey. The majority of grocery shoppers (72%) are also seeking promotions for every type of grocery trip, whether they are buying only a handful of items, or filling their cart. They hold little allegiance to a select store or brand if presented the right promotional value—53% of grocery shoppers are either likely or very likely to change where they stock- up on groceries if they knew prices were lower somewhere else, while only 22% are either unlikely or very unlikely to switch. Similarly, 85% of grocery shoppers said they try new brands when they are on sale. Fundamentally, shopper behavior has changed, and strategies and tactics to drive behavior continue to evolve. Developing a promotional strategy that differentiates a retailer enough to cause a grocery shopper to change where they typically shop, or differentiates a brand enough to cause shoppers to change what they typically buy, is a task that requires a detailed understanding of who their target shoppers are, the buying behaviors and tendencies Market Track’s Shopper Insight Series Throughout this Perspective we will be unpacking the responses from our most recent Grocery Shopper Insight Survey. In a study of 1,000 individuals that are either primarily responsible or share responsibility for purchasing groceries for their households, we identify the differences in buying behaviors and trip drivers between shopper demographics. The survey results allow us to contrast the profiles of grocery cart-fillers versus basket- fillers, frequent versus infrequent grocery shoppers, young urban grocery shoppers versus older, rural grocery shoppers, and how promotions impact the behaviors of each. We then discuss an application of these findings to promotional planning in order to understand how different category allocations, product allocations, and promotion types and overlays better attract one demographic versus another. Please note that this Perspective reports Market Track’s initial findings from our Grocery Shopper Insight Survey conducted in February 2014. We will provide additional shopper insights in publications throughout the course of 2014. Please reach out to your Market Track account team for an advanced look into the results of our Grocery Shopper Insight Survey. C

-

Upload

vuongkhuong -

Category

Documents

-

view

221 -

download

1

Transcript of Driving Shopper Behavior in Grocery - Market Track · Marke rac Perspective TM Driving Shopper...

www.markettrack.com

Market Track PerspectiveTM

Driving Shopper Behavior in GrocerySurvey results show high propensity to change stores and brands based on deals

ompetition in the grocery space has never been more intense. As trade class lines blur and a larger focus is placed on grocery items in mass, dollar, club and drug stores, grocery retailers have had to expand their competitive set considerably. Add to that an uncertain economy, increased fuel costs and extreme weather in many parts of the country, and you now have shoppers who have become much more

price conscious and promotionally driven. As we discovered in our recent Grocery Shopper Insight Survey, shoppers are more actively looking for where to find the best price on household items and groceries, and have a very high propensity to switch stores and brands.

It has become increasingly difficult to understand how to incent an everyday shopper on their weekly grocery shopping trip to pick one grocer over another, or one brand over another. How do those in the grocery space ensure they are capturing the attention of an increasingly discriminating shopper?

Shoppers are selective—over 40% are going to more than one store to complete their grocery shopping, with three-quarters citing “better prices on certain products and categories” as the reason for shopping at multiple stores, according to our recent Grocery Shopper Insight Survey. The majority of grocery shoppers (72%) are also seeking promotions for every type of grocery trip, whether they are buying only a handful of items, or filling their cart. They hold little allegiance to a select store or brand if presented the right promotional value—53% of grocery shoppers are either likely or very likely to change where they stock-up on groceries if they knew prices were lower somewhere else, while only 22% are either unlikely or very unlikely to switch. Similarly, 85% of grocery shoppers said they try new brands when they are on sale.

Fundamentally, shopper behavior has changed, and strategies and tactics to drive behavior continue to evolve. Developing a promotional strategy that differentiates a retailer enough to cause a grocery shopper to change where they typically shop, or differentiates a brand enough to cause shoppers to change what they typically buy, is a task that requires a detailed understanding of who their target shoppers are, the buying behaviors and tendencies

Market Track’s Shopper Insight SeriesThroughout this Perspective we will be unpacking the responses from our most recent Grocery Shopper Insight Survey. In a study of 1,000 individuals that are either primarily responsible or share responsibility for purchasing groceries for their households, we identify the differences in buying behaviors and trip drivers between shopper demographics. The survey results allow us to contrast the profiles of grocery cart-fillers versus basket-fillers, frequent versus infrequent grocery shoppers, young urban grocery shoppers versus older, rural grocery shoppers, and how promotions impact the behaviors of each.

We then discuss an application of these findings to promotional planning in order to understand how different category allocations, product allocations, and promotion types and overlays better attract one demographic versus another. Please note that this Perspective reports Market Track’s initial findings from our Grocery Shopper Insight Survey conducted in February 2014. We will provide additional shopper insights in publications throughout the course of 2014. Please reach out to your Market Track account team for an advanced look into the results of our Grocery Shopper Insight Survey.

C

2 Market Track PerspectiveTM

of their target shoppers, and how competitive promotional patterns and strategies may be inhibiting their ability to attract their target shopper. Once that understanding is achieved, consistent monitoring, measurement, and adaptability are critical to sustaining their promotional strategy.

What promotions actually drive results? How can retailers and manufacturers in the grocery space optimize their promotional efforts to increase sales? In this issue of Market Track’s Shopper Insight Series, we will provide a process that will help retailers and manufacturers understand how successful they are at engaging their target shoppers using promotions, and how to identify and execute the right changes and adaptations to promotional strategy in order to attract new shoppers to shop their stores or buy their brands.

Promotions and pricing are central to shopper behaviorEssential to any effective promotional strategy for grocery retailers and manufacturers is a knowledge of the week to week buying behaviors of grocery shoppers—particularly, the segment of shoppers the retailer or manufacturer wants to attract. As we discussed in our Reach & Impact Shopper Insight Survey in 2013, if retailers or manufacturers fail to reach their target shoppers with the right promotional message at the right time, they risk losing that shopper not just for that purchase, but for future purchases as well. With that in mind, in our Grocery Shopper Insight Survey, we first set out to understand the buying behaviors of

grocery shoppers to create a foundation from which a winning promotional strategy can be formed.

Among the most important initial findings from our survey results was the resounding response that promotions are essential to shoppers’ grocery trips. We probed our survey respondents

on everything from whether or not they use promotions, to what types of promotions they use, to which of their behaviors are governed by promotions. The results showed that today’s shoppers are heavily reliant on the promotional engagements of retailers and manufacturers to pick stores, brands, purchase quantities, basket and cart additions, unplanned purchases, and more.

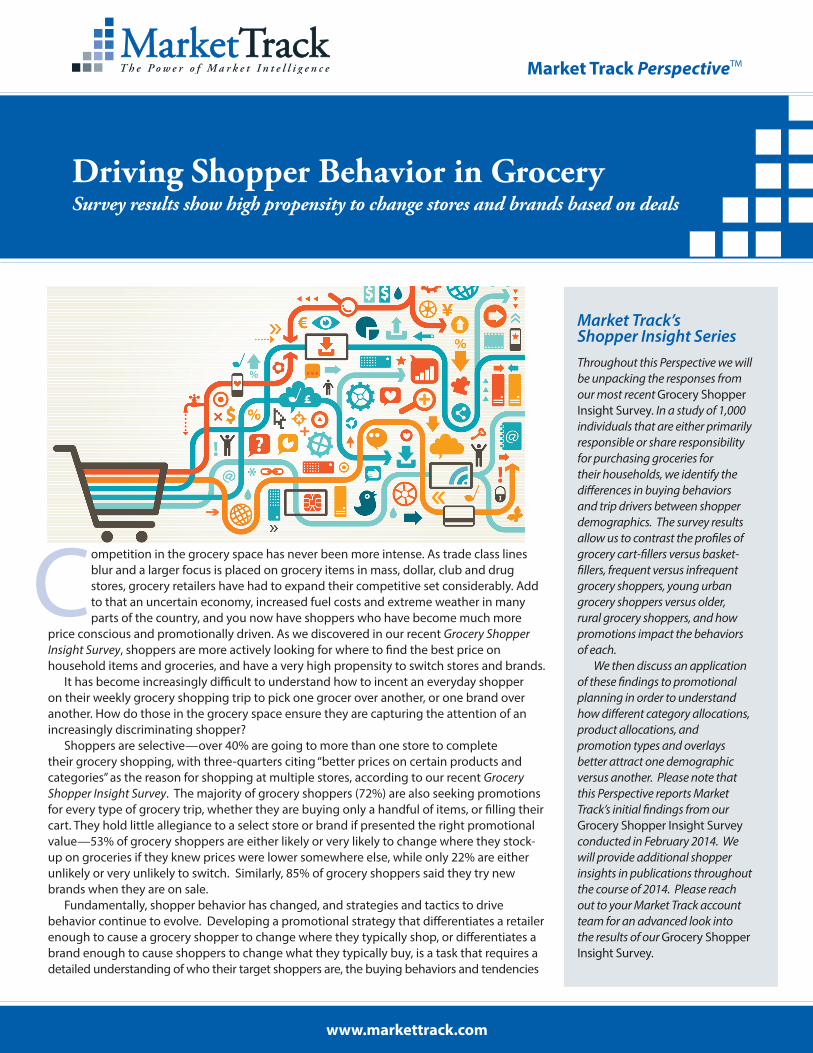

Figure 1 shares the likelihood with which shoppers will use different promotional media types to find promotions for their grocery trips.

The top media type by a wide margin was print, with just under 90% of grocery shoppers claiming they either “Definitely” or “Probably” will use print ads to find promotions prior to a store trip. Printed coupons was a close second among grocery shoppers at about 80%, followed by Online promotions and Digital Coupons, both of which received roughly 55%. At the low-usage end of

Figure 1: Grocery shopper media type usage

Among all demographics, print is the most prevalent way shoppers are looking for promotions prior to their grocery trips

Source: Market Track Grocery Shopper Insight Survey

3The Power of Market Intelligence

the spectrum was Smartphones or Tablets, for which over 50% of survey respondents said they either “Definitely” or “Probably” will not use either to find promotions prior to grocery shopping trips.

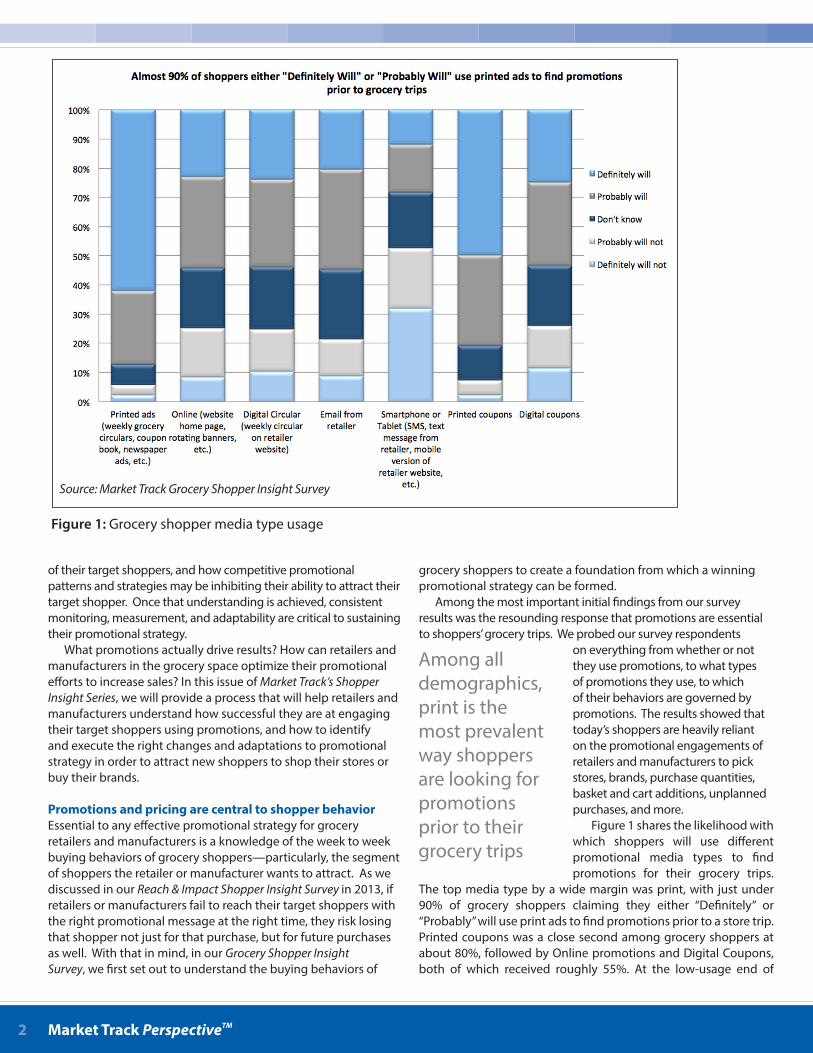

Beyond simply understanding which media types are being used to find promotions, we found that of the deciding factors that determine where a shopper brings their business, promotions and pricing is the top influencer—even more influential than how close shoppers live to their nearest grocery retailer. Out of seven factors survey respondents were asked to rank in terms of what influences their store choice, over 55% ranked promotions and pricing as the top influencer, and just under 90% ranked promotions and pricing in their top three factors (see figure 2). Grocery shoppers are not only using promotions, but the vast majority are also relying heavily on promotions to make decisions on where to shop and what to buy.

Trip Frequency: More urban “Daily” grocery shoppers than rural or suburbanGrocery shopping is a common calendar item to find on anybody’s weekly schedule. Whether the grocery shopper is making a trip to replenish their entire kitchen, or stopping by the grocery store to pick up an ingredient or two for dinner that evening, we found that 84% of shoppers buy groceries in-store at least once per week.

With the vast majority of shoppers making trips to buy groceries each week, it is even more important for retailers and manufacturers to understand the trip frequency behaviors of their target audience in order to develop a promotional plan that is differentiated for that segment of shoppers. Our survey found that grocery trip frequency can vary based on a wide range of factors. For example, among rural,

suburban, and urban shoppers, we found there was quite a bit of overlap in how frequently each group shops for groceries, yet there was one key differentiator for urban shoppers that should impact how retailers promote to that segment.

More than 30% of rural, suburban, and urban shoppers claimed to shop for groceries once per week, while over 70% of each group claimed to shop for groceries either once per week, or 2-3 times per week. However, nearly 10% of urban shoppers claimed to shop daily

for groceries, as opposed to less than 5% each for rural and suburban shoppers, which opens up both opportunity and competition to win shopping trips every day, particularly for store locations in urban areas. With one out of every ten urban shoppers making grocery store visits every day, retailers competing for this segment of shoppers require a consistent line of omni-channel promotional engagement, rather than promoting via a single weekly circular. There are opportunities to engage more readily through digital promotions, such as email, online, mobile and social media.

Figure 2: Top influences in deciding where to shop

Not surprisingly, pricing and promotions are the most influential factors in helping shoppers decide where they will shop for groceries

Source: Market Track Grocery Shopper Insight Survey

4 Market Track PerspectiveTM

Trip Frequency: Higher income shoppers make more frequent grocery tripsThere were also correlations to be found between annual household income and how frequently grocery shoppers make trips to the store. Of the different annual household incomes we polled, those who make more than $100,000 per year claimed to shop more frequently than shoppers of lower income levels. The group of shoppers that make more than $100,000 had the highest percentage of respondents (over 90%) of any income demographic group claim to shop either once per week or more. Conversely, the group of shoppers that claimed an annual household income of less than $25,000 had the highest percentage of respondents (over 25%) claim to shop for groceries 2-3 times per month or less.

Depending on which income levels retailers or manufacturers are trying to attract to their stores, there is opportunity to modify their promotional frequency to best suit their target demographic. If a retailer wants to attract shoppers with an annual income of $25,000 or less, for example, and they currently are publishing multiple circulars per week, there may be an opportunity to save on printing costs by pairing back their promotional calendar without the risk of losing their target shoppers to competitors. Similarly, if a retailer or manufacturer wants to target a shopper with an annual income of over $100,000, additional promotional investment may be required to keep the more regular shopper engaged.

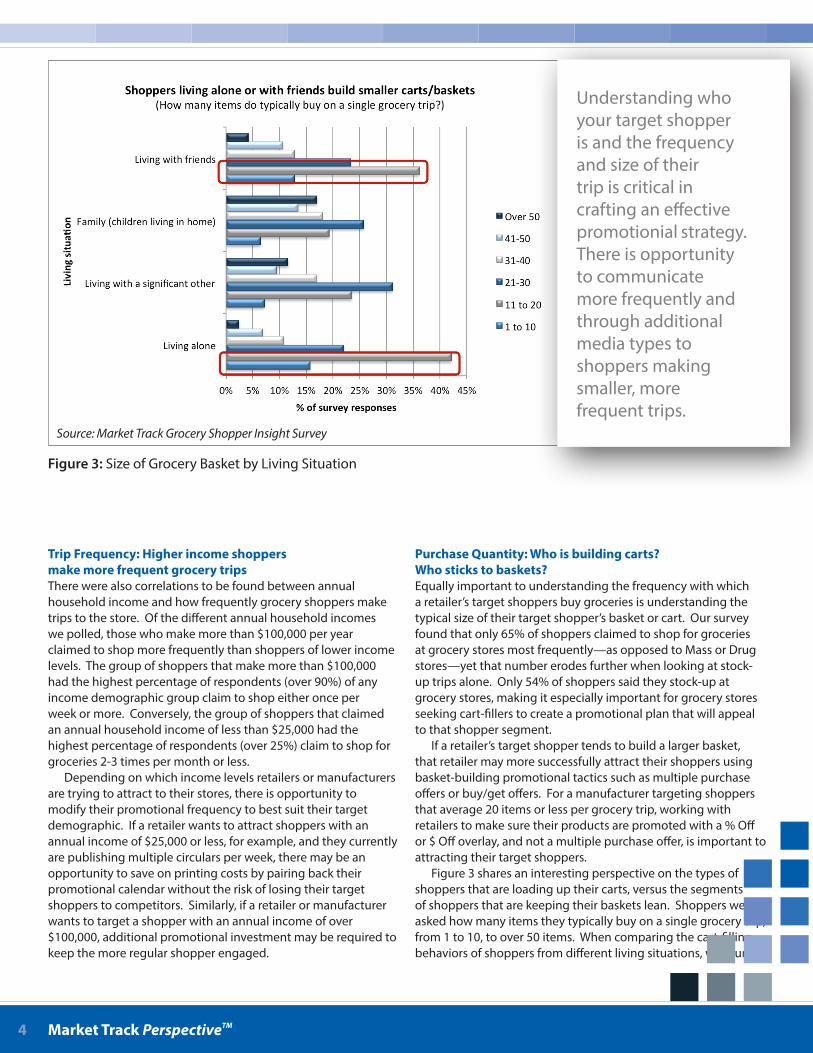

Purchase Quantity: Who is building carts? Who sticks to baskets?Equally important to understanding the frequency with which a retailer’s target shoppers buy groceries is understanding the typical size of their target shopper’s basket or cart. Our survey found that only 65% of shoppers claimed to shop for groceries at grocery stores most frequently—as opposed to Mass or Drug stores—yet that number erodes further when looking at stock-up trips alone. Only 54% of shoppers said they stock-up at grocery stores, making it especially important for grocery stores seeking cart-fillers to create a promotional plan that will appeal to that shopper segment.

If a retailer’s target shopper tends to build a larger basket, that retailer may more successfully attract their shoppers using basket-building promotional tactics such as multiple purchase offers or buy/get offers. For a manufacturer targeting shoppers that average 20 items or less per grocery trip, working with retailers to make sure their products are promoted with a % Off or $ Off overlay, and not a multiple purchase offer, is important to attracting their target shoppers.

Figure 3 shares an interesting perspective on the types of shoppers that are loading up their carts, versus the segments of shoppers that are keeping their baskets lean. Shoppers were asked how many items they typically buy on a single grocery trip, from 1 to 10, to over 50 items. When comparing the cart-filling behaviors of shoppers from different living situations, we found

Figure 3: Size of Grocery Basket by Living Situation

Source: Market Track Grocery Shopper Insight Survey

Understanding who your target shopper is and the frequency and size of their trip is critical in crafting an effective promotionial strategy. There is opportunity to communicate more frequently and through additional media types to shoppers making smaller, more frequent trips.

5The Power of Market Intelligence

that shoppers that either live alone OR live with friends have a tendency to build smaller baskets.

Nearly 60% of shoppers living alone, and about 50% of those living with friends claimed to build baskets of 20 items or less in a single grocery trip. Though the results for shoppers living alone were fairly expected, it is an important finding that a minority of those living with friends purchase groceries for their whole household. Particularly in areas with many young, single shoppers who have roommates, retailer and manufacturer promotions may be more effectively constructed to attract the smaller basket builders who buy groceries for themselves, rather than the stock-up shoppers buying for an entire household.

Shoppers living with a family proved to be the largest cart-fillers of the four groups, by contrast. About 50% of shopper respondents living with family claimed to purchase over 31 items per grocery trip; 17% claimed to buy over 50 items per trip, by far the largest percentage of respondents among the different living situation segments.

Needless to say, shoppers filling a cart with 50+ items per grocery will be attracted by a different promotional value proposition than shoppers who live alone or live with friends. The separation between the behaviors of these two groups

illustrates the importance of understanding how different shoppers behave, and the implications of varying shopper behaviors to a retailer or manufacturer’s promotional plan.

Category Mix: Secondary Trip Driving Categories are Critical for DifferentiationThere are a variety of factors that influence a grocery shopper’s decision to shop at a given store that fall outside of a retailer’s control—for instance, the proximity of the store to the shopper’s home. Other than opening a new store location closer to that shopper’s home, there is nothing a retailer can do to change an influencer like proximity. Within the spectrum of factors retailers have more control over are the promotions and discounts for their products, store cleanliness and layout, level of customer service, loyalty programs and perks, among others.

One critical factor that can be easily overlooked, but which retailers can control, is the product subcategory assortment within a retailer’s omni-channel promotions, irrespective of pricing. Grocers will typically promote an array of different products from each department within their four walls each week, but choosing which products to promote at the subcategory level should be supported by methodical decision-making.

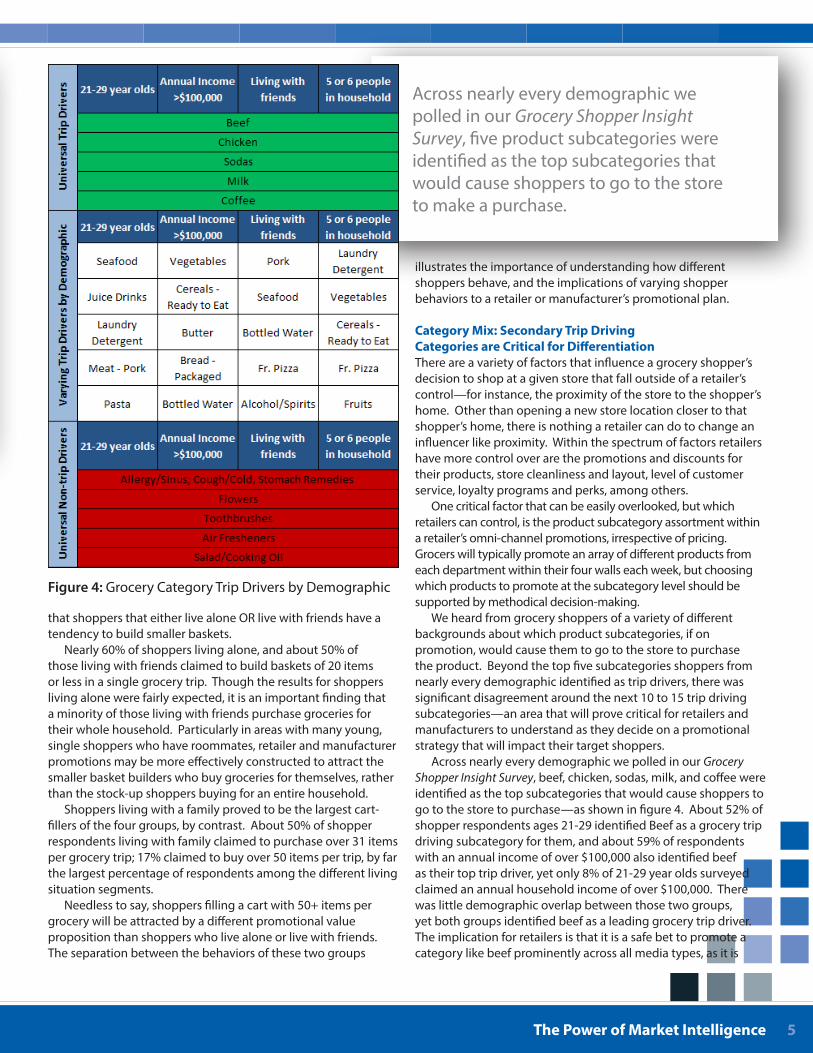

We heard from grocery shoppers of a variety of different backgrounds about which product subcategories, if on promotion, would cause them to go to the store to purchase the product. Beyond the top five subcategories shoppers from nearly every demographic identified as trip drivers, there was significant disagreement around the next 10 to 15 trip driving subcategories—an area that will prove critical for retailers and manufacturers to understand as they decide on a promotional strategy that will impact their target shoppers.

Across nearly every demographic we polled in our Grocery Shopper Insight Survey, beef, chicken, sodas, milk, and coffee were identified as the top subcategories that would cause shoppers to go to the store to purchase—as shown in figure 4. About 52% of shopper respondents ages 21-29 identified Beef as a grocery trip driving subcategory for them, and about 59% of respondents with an annual income of over $100,000 also identified beef as their top trip driver, yet only 8% of 21-29 year olds surveyed claimed an annual household income of over $100,000. There was little demographic overlap between those two groups, yet both groups identified beef as a leading grocery trip driver. The implication for retailers is that it is a safe bet to promote a category like beef prominently across all media types, as it is

Figure 4: Grocery Category Trip Drivers by Demographic

Across nearly every demographic we polled in our Grocery Shopper Insight Survey, five product subcategories were identified as the top subcategories that would cause shoppers to go to the store to make a purchase.

6 Market Track PerspectiveTM

a subcategory that attracts nearly all demographics.

That said, beef is a heavily promoted subcategory among most grocery retailers. For example, in the 12 month period ending in January 2014, beef was promoted on the front page of Kroger and Safeway banner circulars every week, and on the front page of Ahold banner circulars in all but five weeks. This is not a surprising discovery, given shoppers want promotions on the beef subcategory, yet retailers are still left to question

how they can differentiate their subcategory allocation to edge out their competition. To get a better idea on how to approach this question, retailers need to look past the top five to ten product subcategories that shoppers identified to leverage the variations in trip drivers among different demographics.

We reviewed the 11th through 15th most selected trip driving subcategories—identified as the “Varying Trip Drivers by Demographic” in figure 4—among the same respondent demographics. Comparing the top five trip driving

subcategories to those ranked 11 through 15, there are clear disparities in category preference between demographics. One example is pasta, which 26% of 21-29 year old respondents identified as a trip driver when promoted—the only demographic in this example to identify pasta in the top 11-15. Likewise, butter was uniquely identified by 28 % of shopper respondents with an annual income of greater than $100,000, alcohol/spirits was uniquely identified by 30% of respondents living with friends, and fruit was uniquely identified by 29% of those living in a household with five to six people.

It is in this set of subcategories where grocers can measure how well they are promoting to their target shoppers. If, for instance, HEB in Dallas instituted a new strategy to attract a larger segment of shoppers ages 21-29 to their stores in 2014, based on the preferences of our survey respondents, they may have more success reaching that demographic with a pasta promotion instead of a vegetables or butter promotion. To form a more complete promotional strategy, HEB could then review the competitive activity of Tom Thumb—an in-market competitor—to identify when they promoted vegetables or butter in 2013, and add pasta to their promotional calendar on those weeks, knowing 21-29 year olds may not find the subcategory mix at Tom Thumb attractive.

The subcategory allocation within any promotional media type has a direct impact on a retailer’s ability to drive grocery shopping trips week to week. Using a combination of competitive

Retailers need to look past the top five to ten product subcategories that shoppers identified to leverage the variations in trip drivers among different demographics.

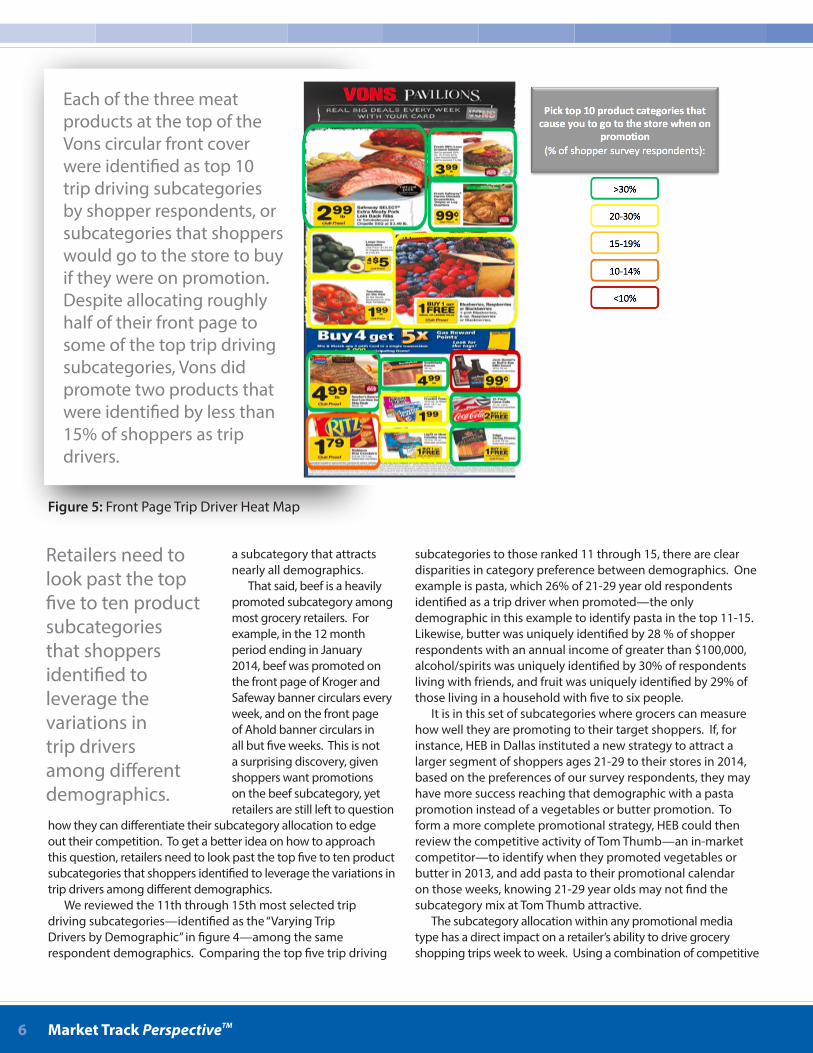

Each of the three meat products at the top of the Vons circular front cover were identified as top 10 trip driving subcategories by shopper respondents, or subcategories that shoppers would go to the store to buy if they were on promotion. Despite allocating roughly half of their front page to some of the top trip driving subcategories, Vons did promote two products that were identified by less than 15% of shoppers as trip drivers.

Figure 5: Front Page Trip Driver Heat Map

7The Power of Market Intelligence

promotional data, along with an understanding of the tendencies of their target grocery shoppers, will add a method by which a promotional plan can be constructed to drive specific shopper behavior, in accordance with a retailer’s overall strategy.

Translating Behaviors to Promotional StrategyUnderstanding shopper behaviors and grocery trip drivers is only useful if the data and information can translate into effective strategy changes, a process in which Market Track specializes in our day to day engagement with both retailer and manufacturer clients. To this point we have shared some of the initial grocery shopper behavioral and trip driving findings across a variety of demographics. In this next section, we will provide some examples of how to take action on these findings using real circulars.

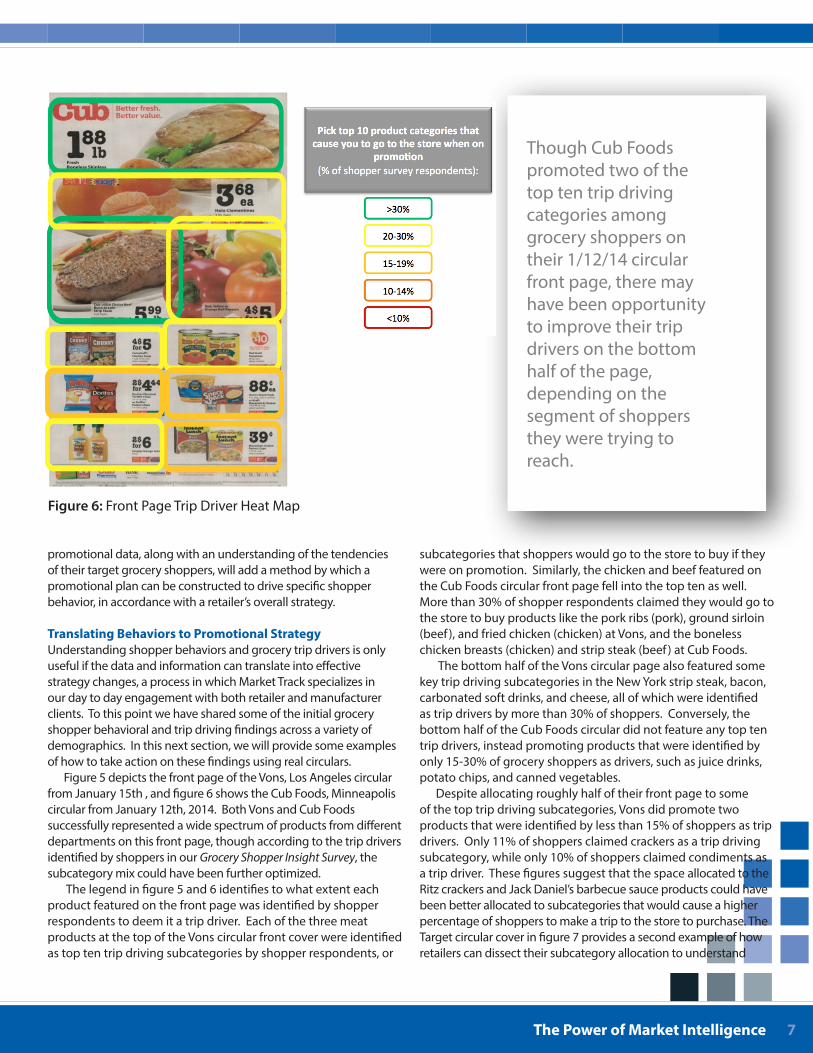

Figure 5 depicts the front page of the Vons, Los Angeles circular from January 15th , and figure 6 shows the Cub Foods, Minneapolis circular from January 12th, 2014. Both Vons and Cub Foods successfully represented a wide spectrum of products from different departments on this front page, though according to the trip drivers identified by shoppers in our Grocery Shopper Insight Survey, the subcategory mix could have been further optimized.

The legend in figure 5 and 6 identifies to what extent each product featured on the front page was identified by shopper respondents to deem it a trip driver. Each of the three meat products at the top of the Vons circular front cover were identified as top ten trip driving subcategories by shopper respondents, or

subcategories that shoppers would go to the store to buy if they were on promotion. Similarly, the chicken and beef featured on the Cub Foods circular front page fell into the top ten as well. More than 30% of shopper respondents claimed they would go to the store to buy products like the pork ribs (pork), ground sirloin (beef ), and fried chicken (chicken) at Vons, and the boneless chicken breasts (chicken) and strip steak (beef ) at Cub Foods.

The bottom half of the Vons circular page also featured some key trip driving subcategories in the New York strip steak, bacon, carbonated soft drinks, and cheese, all of which were identified as trip drivers by more than 30% of shoppers. Conversely, the bottom half of the Cub Foods circular did not feature any top ten trip drivers, instead promoting products that were identified by only 15-30% of grocery shoppers as drivers, such as juice drinks, potato chips, and canned vegetables.

Despite allocating roughly half of their front page to some of the top trip driving subcategories, Vons did promote two products that were identified by less than 15% of shoppers as trip drivers. Only 11% of shoppers claimed crackers as a trip driving subcategory, while only 10% of shoppers claimed condiments as a trip driver. These figures suggest that the space allocated to the Ritz crackers and Jack Daniel’s barbecue sauce products could have been better allocated to subcategories that would cause a higher percentage of shoppers to make a trip to the store to purchase. The Target circular cover in figure 7 provides a second example of how retailers can dissect their subcategory allocation to understand

Though Cub Foods promoted two of the top ten trip driving categories among grocery shoppers on their 1/12/14 circular front page, there may have been opportunity to improve their trip drivers on the bottom half of the page, depending on the segment of shoppers they were trying to reach.

Figure 6: Front Page Trip Driver Heat Map

© 2014 Market Track. All rights reserved.

Learn More

For more insight into the entire promotional landscape or an analysis of your digital and print strategies, call Market Track at 1.800.235.3781 or e-mail [email protected].

About Market TrackMarket Track is a market intelligence firm dedicated to increasing our customers’ returns on their promotional investments and providing real-time visibility into e-commerce pricing. We support our 850+ clients through monitoring and analyzing over 200 U.S. and Canadian markets for every channel of trade and 1 billion buy pages from 3,000 global merchants, enabling dynamic decision making by turning data into actionable insights.

Key Takeaways• Out of seven factors grocery shoppers

were asked to rank in terms of what influences their store choice, over 55% ranked promotions and pricing as the top influencer, and just under 90% ranked promotions and pricing in their top three factors.

• Just under 90% of grocery shoppers claiming they either “Definitely” or “Probably” will use print ads to find promotions prior to a store trip. Printed coupons was a close second among grocery shoppers at about 80%.

• Nearly 60% of shoppers living alone, and about 50% of those living with friends claimed to build baskets of 20 items or less in a single grocery trip. By comparison, only about 25% of respondents living with family (children living in home) claimed to build baskets of 20 items or less on their grocery trips.

• Beyond the top five subcategories shoppers from nearly every demographic identified as trip drivers (Beef, Chicken, Carbonated Soft Drinks, Milk, Coffee), there was significant disagreement between grocery shopper segments around the next 10 to 15 trip driving subcategories. These secondary trip driver categories will prove critical for retailers and manufacturers to understand as they decide on a promotional strategy that will impact their target shoppers.

www.markettrack.com

how successfully they appealed to shoppers. In this case study, however, shoppers were asked about trip driving subcategories specifically for the Memorial Day, July 4th, and Labor Day holidays. We found that trip drivers changed radically from a standard grocery trip to a grocery trip for an event or holiday, and figure 7 illustrates how Target successfully created a front page subcategory allocation to match the preferences of July 4th grocery shoppers.

All six of the products Target promoted on their 6/30/13 circular front page fell within the top 15 subcategories shoppers selected as items they would add to their cart if they were discounted prior to any of the three summer holidays. Sodas, hot dogs, and beef, in particular, made up three of the top four likely cart-additions prior to July 4th, with 30% or more of respondents selecting each. Target constructed a circular front page that was specifically suited to build the baskets of July 4th grocery shoppers.

In summaryPerhaps the most critical lesson shoppers taught us in our Grocery Shopper Insight Survey was the importance of making data-supported decisions during promotional planning. The disparity in the behaviors and preferences of different grocery shopper segments requires that retailers and manufacturers learn about their target shopper, and what their competitors are doing to attract their target shoppers. Additionally, with the availability of a variety of promotional and product information sources for grocery shoppers’, there is an unprecedented willingness to change their preferences or behaviors to find the best value. If retailers and manufacturers fail to engage their target shoppers with regular promotional messaging, they risk losing their shoppers to competing stores or brands for both current and future purchases.

In this first iteration of our Grocery Shopper Insight Series, we introduced the framework for a process for combining competitive promotional data with shopper insights to achieve a data-supported, targeted promotional plan. Over the course of the next several months, we will narrow our focus on the different stages of the ad planning process, and recommend some best practices for incorporating both competitive promotional data and shopper insights into each stage. Our goal is to share the process through which many of our clients have improved their ability to target their strategic shopper segments with relevant, timely promotions.

Figure 7: Front Page Trip Driver Heat Map, Target Circular, 6/30/2013