DRIVING COMPETIVE EDGE WITH INTELLIGENT OPERATIONS · DRIVING COMPETIVE EDGE WITH INTELLIGENT...

33

Structured FINANCE, Stuttgart, 25 November 2015 Presentation by Pascal Visée DRIVING COMPETIVE EDGE WITH INTELLIGENT OPERATIONS

Transcript of DRIVING COMPETIVE EDGE WITH INTELLIGENT OPERATIONS · DRIVING COMPETIVE EDGE WITH INTELLIGENT...

Structured FINANCE, Stuttgart, 25 November 2015 Presentation by Pascal Visée

DRIVING COMPETIVE EDGE WITH INTELLIGENT OPERATIONS

2 P Visée GEE ! 2015 ©

CONTENT

Brief personal intro

Case Study Unilever GBS journey

Intelligent Operations

Plenary discussion

3 P Visée GEE ! 2015 ©

MY CV IN 17 IMAGES

Fin Dir

Finland

SVP Finance

North East Asia

Fin Dir

Germany

SVP Finance

Europe

Group

Treasurer

Chief ES

(GBS) Officer

Supervisory

board

Supervisory

board

Supervisory

board

Supervisory

board

Supervisory

board

Independent Advisor on

Business Ops & Technology

Born NL1961 MSc, LLM,

CA Military

service

4 P Visée GEE ! 2015 ©

CONTENT

Brief personal intro

Case Study Unilever GBS journey #

Intelligent Operations

Plenary discussion

# Using charts of Unilever Investor Seminars 2012 & 2014

5 P Visée GEE ! 2015 ©

OUR GLOBAL BUSINESS SERVICES JOURNEY

From

Traditional ‘Back-office’

Organised by Function

To

Streamlined operational processes

that serve customers and consumers better

2010

Think Big

2011

Start Smart

2012/14

Scale-up Fast

Source : Unilever Investor Seminar Paris November 2012

6 P Visée GEE ! 2015 ©

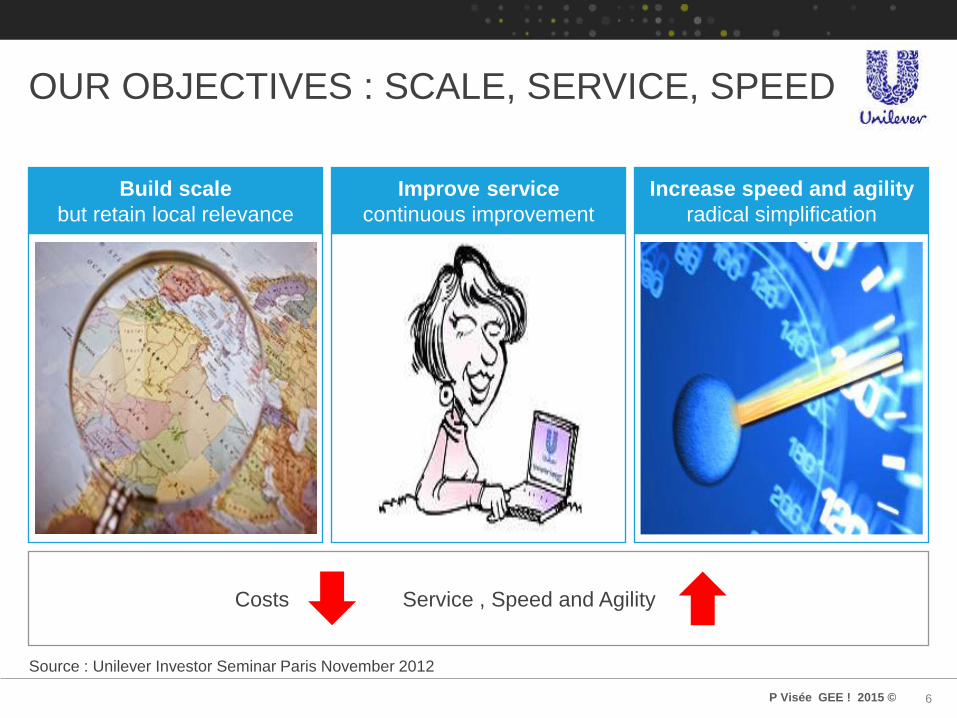

OUR OBJECTIVES : SCALE, SERVICE, SPEED

Build scale

but retain local relevance

Improve service

continuous improvement

Increase speed and agility

radical simplification

Service , Speed and Agility Costs

Source : Unilever Investor Seminar Paris November 2012

7 P Visée GEE ! 2015 ©

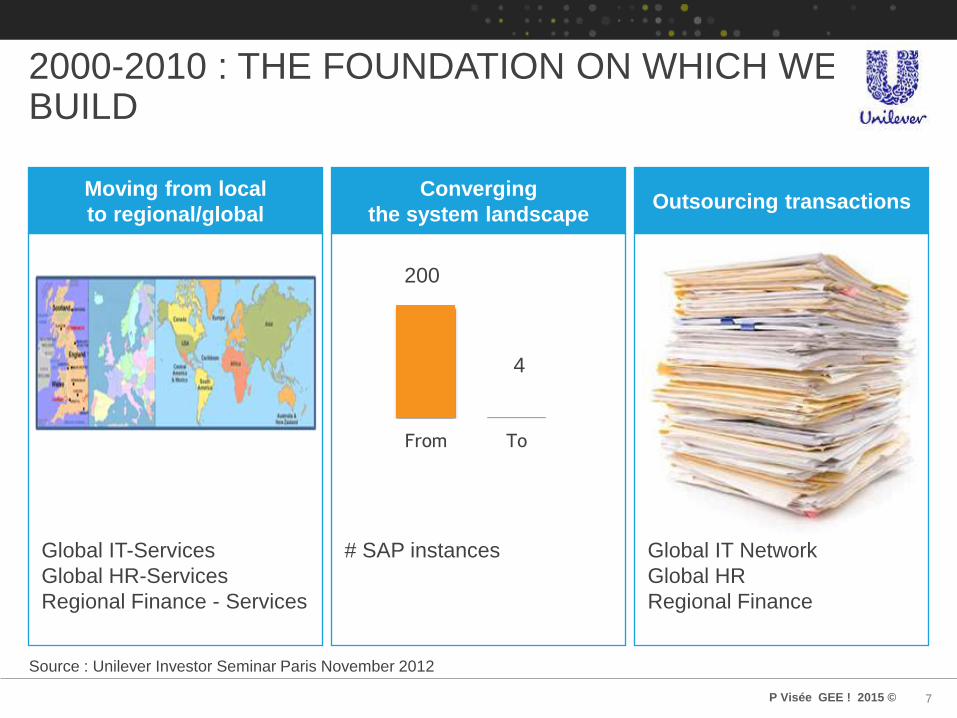

2000-2010 : THE FOUNDATION ON WHICH WE BUILD

Moving from local

to regional/global

Converging

the system landscape Outsourcing transactions

Source : Unilever Investor Seminar Paris November 2012

From To

200

4

Global IT-Services

Global HR-Services

Regional Finance - Services

# SAP instances Global IT Network

Global HR

Regional Finance

8 P Visée GEE ! 2015 ©

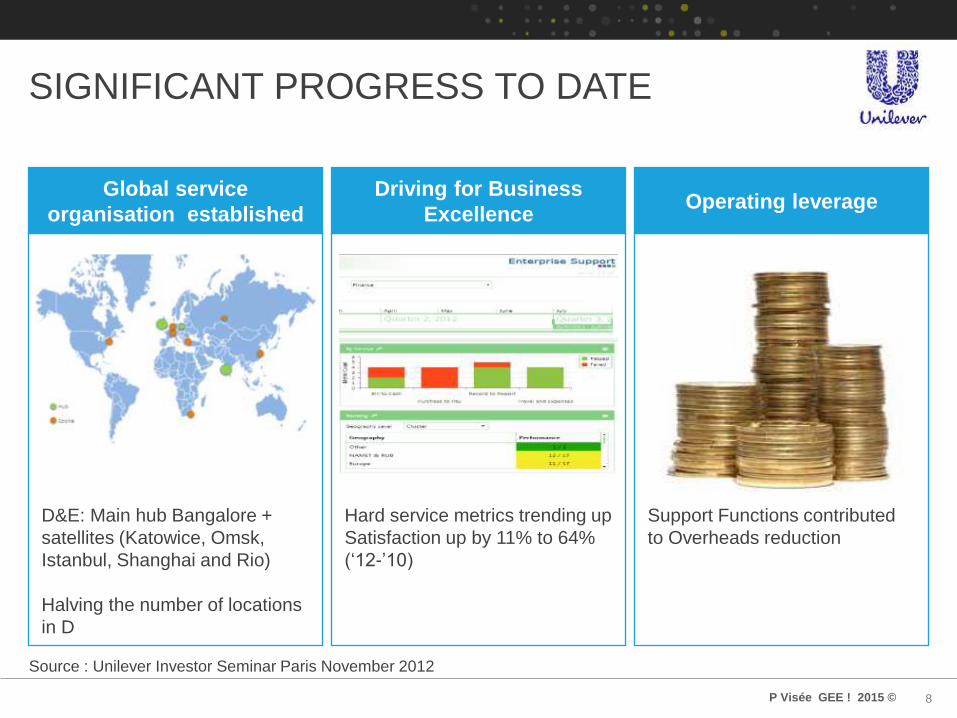

SIGNIFICANT PROGRESS TO DATE

Global service

organisation established

Driving for Business

Excellence Operating leverage

Source : Unilever Investor Seminar Paris November 2012

D&E: Main hub Bangalore +

satellites (Katowice, Omsk,

Istanbul, Shanghai and Rio)

Halving the number of locations

in D

Hard service metrics trending up

Satisfaction up by 11% to 64%

(‘12-’10)

Support Functions contributed

to Overheads reduction

9 P Visée GEE ! 2015 ©

D & E MINDSET IN EVERYTHING WE DO

D&E relevant

innovation and services

Cost advantages

arbitrage, efficiencies,

synergies

Speed and agility

through co-location

Leverage

talent and employer

brand

Bangalore Operation Centre : 1400 FTE’s on site – 550 own and 850 co-located vendor partners

Source : Unilever Investor Seminar Paris November 2012

10 P Visée GEE ! 2015 ©

WE HAVE A BROAD SCOPE OF RESPONSIBILITY

HR

Solutions

Finance

solutions

Travel &

facilities

IT

Solutions

Information

& Analytics

Real

Estate

Technology Information

security

Source : Unilever Investor Seminar London December 2014

11 P Visée GEE ! 2015 ©

EVERYTHING WE DO MUST MEET TWO CRITERIA

Creating a better, simpler, more

agile place to work

Delivering profitable growth &

cost efficiency

Source : Unilever Investor Seminar London December 2014

12 P Visée GEE ! 2015 ©

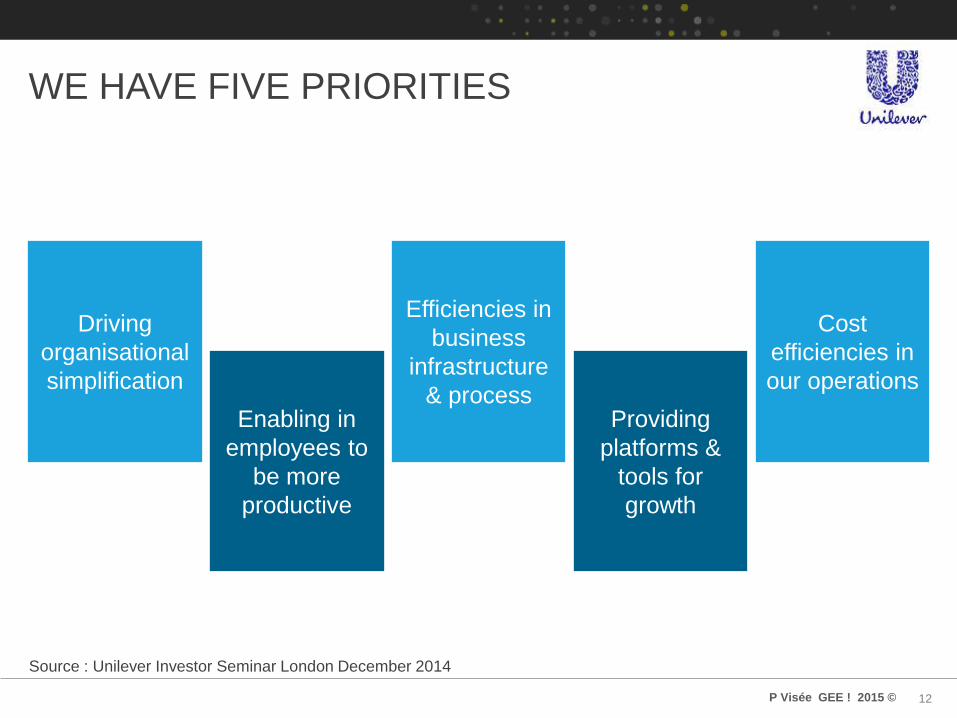

WE HAVE FIVE PRIORITIES

Enabling in

employees to

be more

productive

Providing

platforms &

tools for

growth

Driving

organisational

simplification

Efficiencies in

business

infrastructure

& process

Cost

efficiencies in

our operations

Source : Unilever Investor Seminar London December 2014

13 P Visée GEE ! 2015 ©

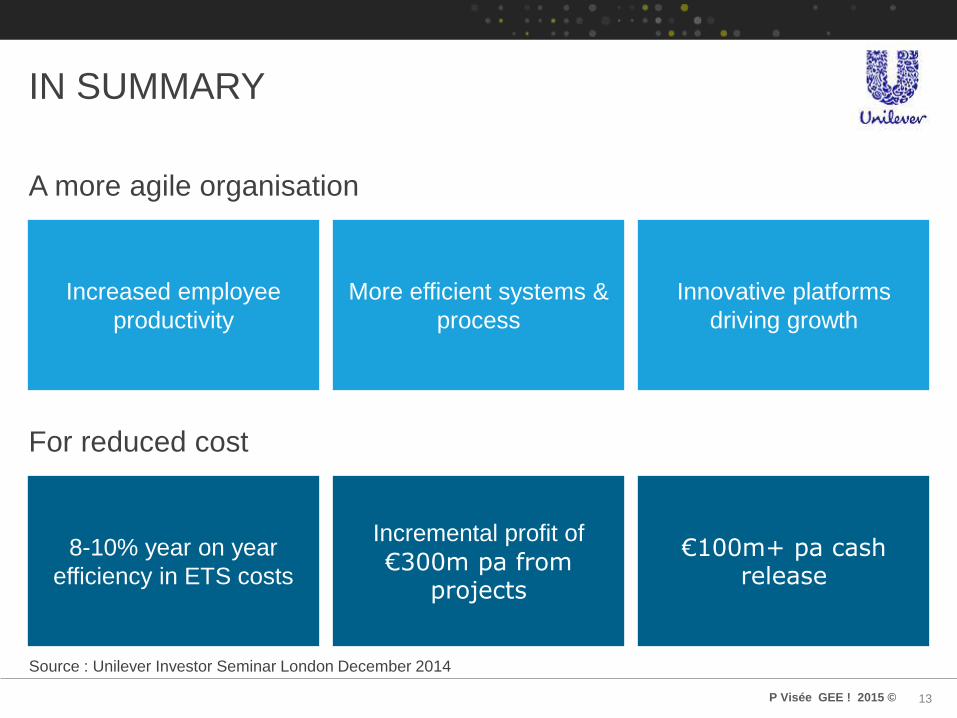

IN SUMMARY

More efficient systems &

process

Increased employee

productivity

Innovative platforms

driving growth

A more agile organisation

Incremental profit of

€300m pa from projects

8-10% year on year

efficiency in ETS costs

€100m+ pa cash release

For reduced cost

Source : Unilever Investor Seminar London December 2014

14 P Visée GEE ! 2015 ©

CONTENT

Brief personal intro

Case Study Unilever GBS journey

Intelligent Operations

Plenary discussion

15 P Visée GEE ! 2015 ©

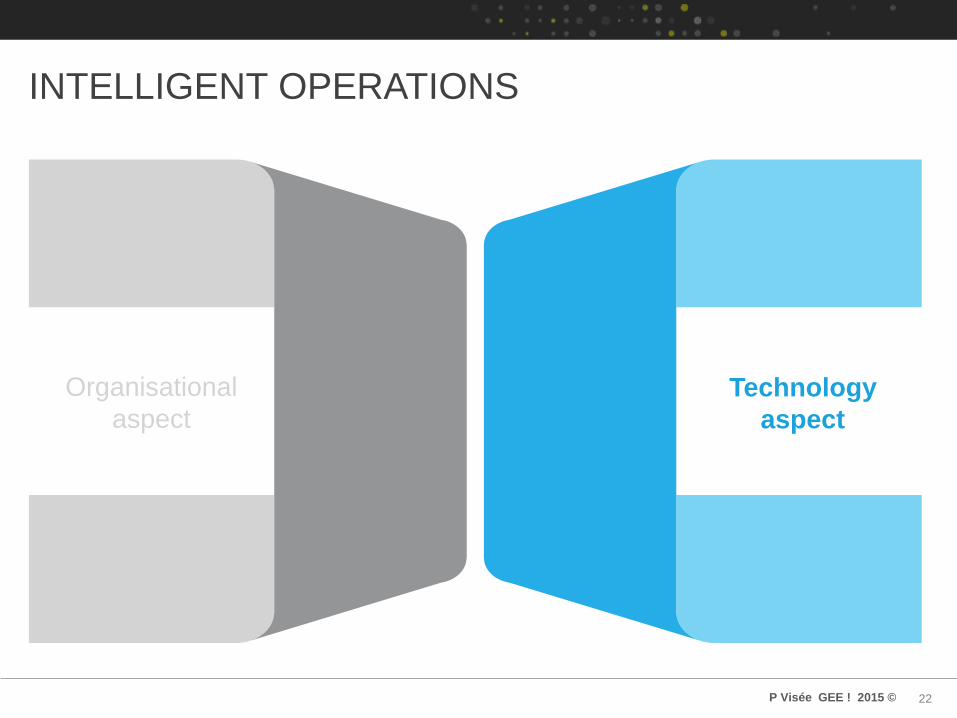

INTELLIGENT OPERATIONS

Organisational

aspect Technology aspect

16 P Visée GEE ! 2015 ©

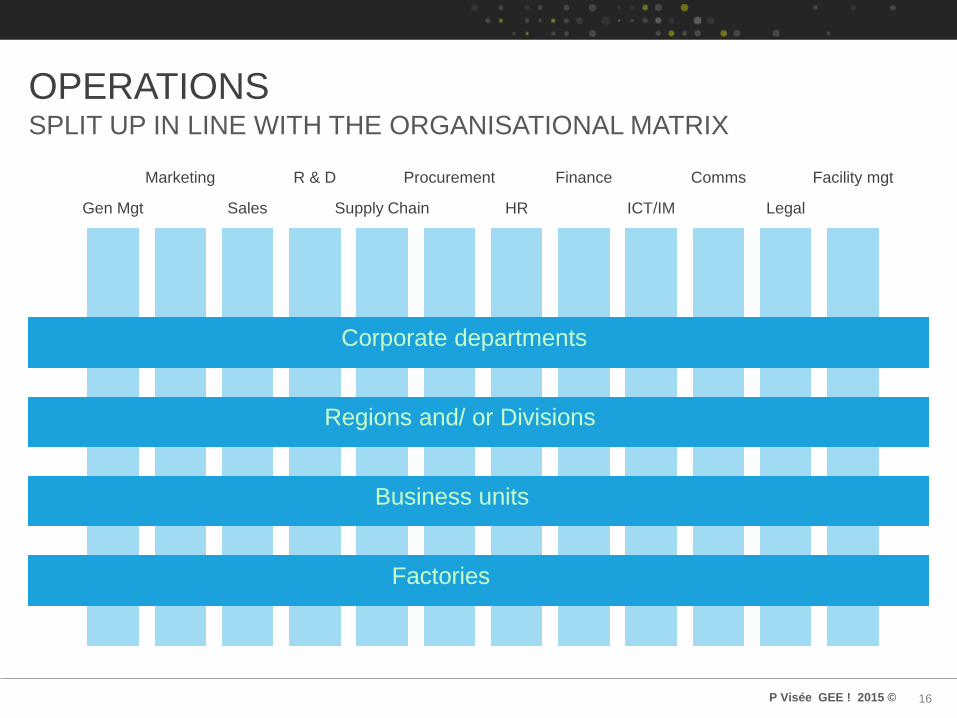

OPERATIONS

Corporate departments

Regions and/ or Divisions

Business units

Factories

Gen Mgt

Marketing

Sales

R & D

Supply Chain

Procurement

HR

Finance

ICT/IM

Comms

Legal

Facility mgt

SPLIT UP IN LINE WITH THE ORGANISATIONAL MATRIX

17 P Visée GEE ! 2015 ©

WITHIN THE MATRIX EVERY FUNCTION HAS ITS ‘OPERATION’

Gen Mgt

Marketing

Sales

R & D

Supply Chain

Procurement

HR

Finance

ICT/IM

Comms

Legal

Facility mgt

Functional Strategy, Leadership, Change Mgt & ‘Technical’ Expertise

Functional Operations, i.e. Finance Operations, Sales Operations etc

18 P Visée GEE ! 2015 ©

‘END-TO-END’ PROCESS MANAGEMENT : CUSTOMER FIRST!

All processes geared towards

business outcomes in particular

customer satisfaction

E.g. Supply Chain E.g. Order-to-Cash

Buying

Logistics

Production

Warehousing

Distribution

Physical Process : Administrative Process :

Order – Sales Function

Fullfillment – SC Function

Bill – Finance Function

Collect – Finance Function

19 P Visée GEE ! 2015 ©

‘OPERATIONS’ BEST MANAGED BY PROCESS

Gen Mgt

Marketing

Sales

R & D

Supply Chain

Procurement

HR

Finance

ICT/IM

Comms

Legal

Facility mgt

Functional Operations, i.e. Finance Operations, Sales Operations etc mostly managed by Function

Operations best managed by process, i.e. geared towards business outcomes e.g. customer satisfaction

20 P Visée GEE ! 2015 ©

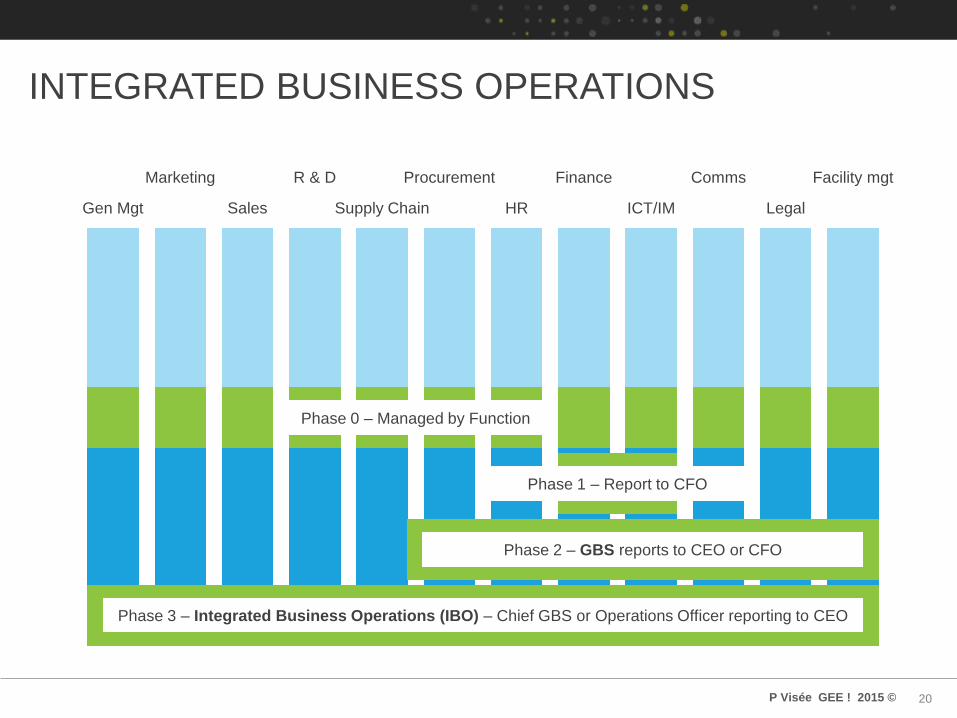

INTEGRATED BUSINESS OPERATIONS

Gen Mgt

Marketing

Sales

R & D

Supply Chain

Procurement

HR

Finance

ICT/IM

Comms

Legal

Facility mgt

Phase 0 – Managed by Function

Phase 1 – Report to CFO

Phase 2 – GBS reports to CEO or CFO

Phase 3 – Integrated Business Operations (IBO) – Chief GBS or Operations Officer reporting to CEO

21 P Visée GEE ! 2015 ©

SIMPLIFICATION OF BACK-END TO ENABLE FRONT-END

‘07 ‘09 ‘13 ‘15

Country Shared

Services

creations

Build a hybrid

model across IT

finance & sales

True business

services including

procurement

Integrated, true

hybrid & business

partner

‘02 ‘09 ‘11 ‘14

Regional

Business

Services

Hybrid model

across all regions

True business

services –

Finance & HR

Analytics & digital

workplace

‘00 ‘05 ‘10 ‘12

Global IT, HR

Regional Finance

SSC

Developing & emerging

mindset across all

Business Services

Scale, service,

speed

Digital

‘99 ‘03 ‘06 ‘10

Shared Services

Creation

Building a progressive

Business Model

Agile & flexible

Operating Model

Simpler, faster,

flatter

22 P Visée GEE ! 2015 ©

INTELLIGENT OPERATIONS

Organisational

aspect

Technology

aspect

23 P Visée GEE ! 2015 ©

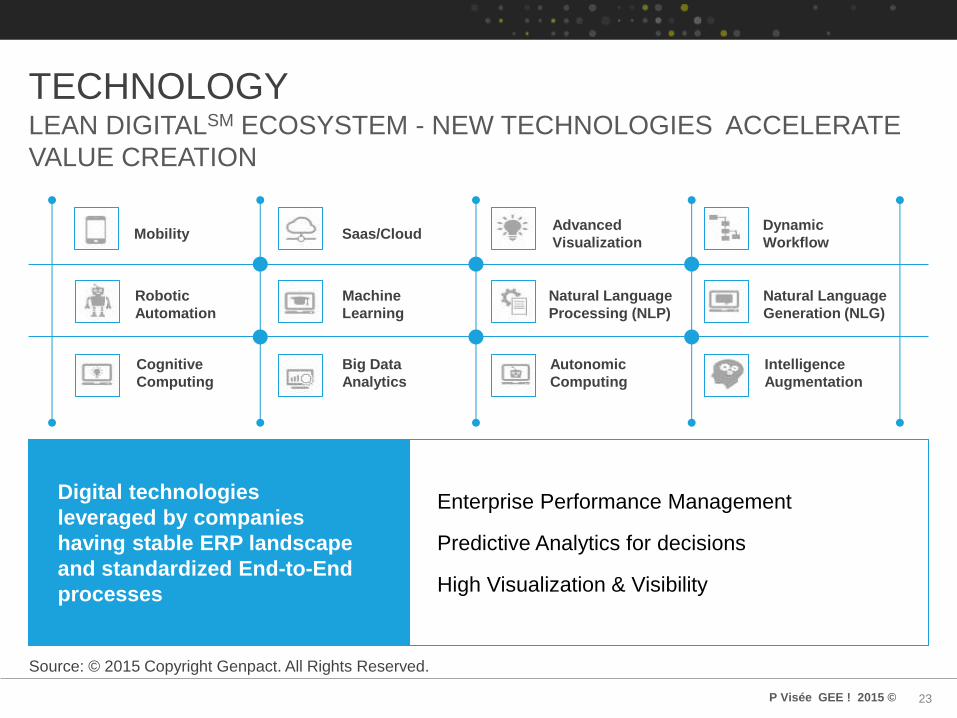

TECHNOLOGY

LEAN DIGITALSM ECOSYSTEM - NEW TECHNOLOGIES ACCELERATE

VALUE CREATION

Mobility

Robotic

Automation

Cognitive

Computing

Saas/Cloud

Machine

Learning

Big Data

Analytics

Advanced

Visualization

Natural Language

Processing (NLP)

Autonomic

Computing

Dynamic

Workflow

Natural Language

Generation (NLG)

Intelligence

Augmentation

Digital technologies

leveraged by companies

having stable ERP landscape

and standardized End-to-End

processes

Enterprise Performance Management

Predictive Analytics for decisions

High Visualization & Visibility

Source: © 2015 Copyright Genpact. All Rights Reserved.

24 P Visée GEE ! 2015 ©

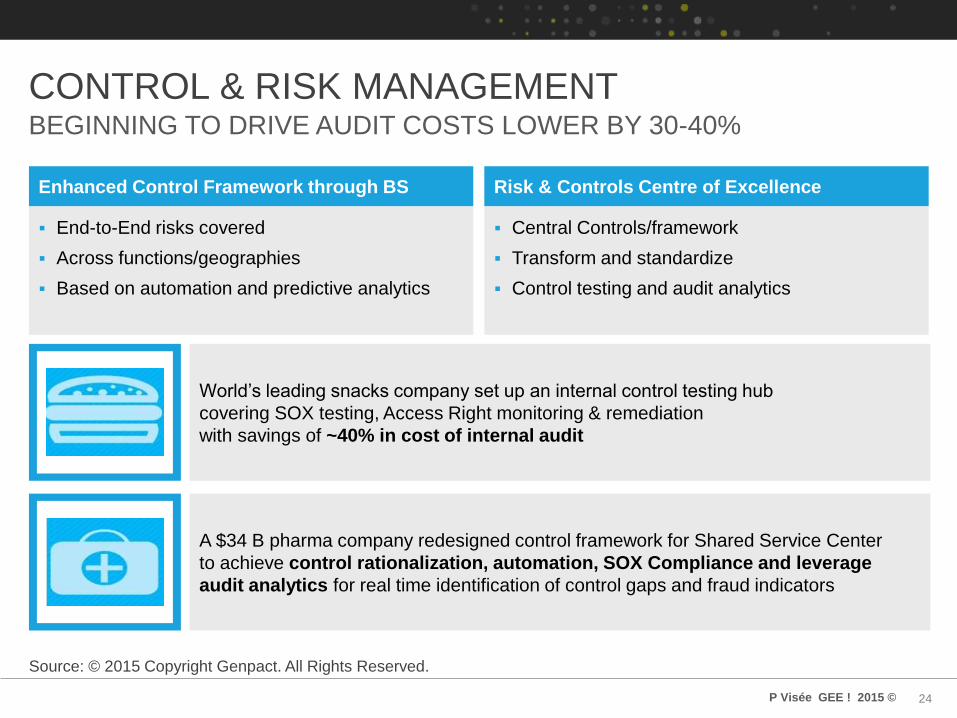

CONTROL & RISK MANAGEMENT BEGINNING TO DRIVE AUDIT COSTS LOWER BY 30-40%

End-to-End risks covered

Across functions/geographies

Based on automation and predictive analytics

Enhanced Control Framework through BS

Central Controls/framework

Transform and standardize

Control testing and audit analytics

Risk & Controls Centre of Excellence

World’s leading snacks company set up an internal control testing hub

covering SOX testing, Access Right monitoring & remediation

with savings of ~40% in cost of internal audit

A $34 B pharma company redesigned control framework for Shared Service Center

to achieve control rationalization, automation, SOX Compliance and leverage

audit analytics for real time identification of control gaps and fraud indicators

Source: © 2015 Copyright Genpact. All Rights Reserved.

25 P Visée GEE ! 2015 ©

FINANCIAL PLANNING & ANALYSIS (FP&A)

Decision

Making

Business

Partnering

High End

Analysis

Recurring Variance

Analysis & Support

Standard

Reporting

Strategic Decisions

Market Strategy, Scenarios

creation, Profitability analysis

Budget, Forecast, BI

Analytics, Ad-hoc analysis

Variance Analysis, P&L

Analysis, Budget Support

Standard Monthly

Reports, Dashboards

Reta

ined

F

P&

A -

BS

Management

Reporting COE

Analytics

Support

HUB

Business

Facing

Strategic

Moves into a foundation of stable

transactional Business Services

High Success Rate

CPG at forefront

Transactional Contextual/Judgmental

VS

Hard to move FP&A to BS:

High end

Strategic to business

Core process

Myths

FP&A is:

Easier to move to shared services

3 times better performance

Faster stabilisation

Reality

COMPANIES ARE MOVING FP&A TO BUSINESS SERVICES

Source: © 2015 Copyright Genpact. All Rights Reserved.

26 P Visée GEE ! 2015 ©

CONTENT

Brief personal intro

Case Study Unilever GBS journey

Intelligent Operations

Plenary discussion

27 P Visée GEE ! 2015 ©

STATEMENT 1

Generally speaking, I view the quality of the middle and backoffice

operations of large companies as relatively poor and often in sharp

contrast with the sophistication of the core business.

Fully agree

= 1

Mostly agree

= 2

Partially

agree = 3

Mostly

disagree = 4

Totally

disagree = 5

28 P Visée GEE ! 2015 ©

STATEMENT 2

For large MNC’s I see a growing trend to organise

middle and backoffice operations through a GBS organisation.

Fully agree

= 1

Mostly agree

= 2

Partially

agree = 3

Mostly

disagree = 4

Totally

disagree = 5

29 P Visée GEE ! 2015 ©

STATEMENT 3

Digitisation is a hype.

Fully agree

= 1

Mostly agree

= 2

Partially

agree = 3

Mostly

disagree = 4

Totally

disagree = 5

30 P Visée GEE ! 2015 ©

STATEMENT 4

Digitisation is one of the key trends that will shape MNC’s for the

future. Not acting on it could bring lasting competitive disadvantage.

Fully agree

= 1

Mostly agree

= 2

Partially

agree = 3

Mostly

disagree = 4

Totally

disagree = 5

31 P Visée GEE ! 2015 ©

STATEMENT 5

Establishing a GBS organisation can be a critical enabler for the

digitisation journey, as it establishes both discipline & agility.

Fully agree

= 1

Mostly agree

= 2

Partially

agree = 3

Mostly

disagree = 4

Totally

disagree = 5

32 P Visée GEE ! 2015 ©

STATEMENT 6

The level of ‘intelligence’ in my own companies

(middle & backoffice) operations I view as

Very high

= 1 High = 2 Medium = 3 Low = 4 Very low = 5

Genpact

Platz der Einheit 1,

Kastor Tower, 20. Etage

60327 Frankfurt am Main

Germany

+49 (0) 69 975030

www.genpact.com/leandigital

Thank You