Drivers of Sustainable Supply Chain Management …...The 2009 Drivers of Sustainable Supply Chain...

24

Drivers of Sustainable Supply Chain Management Practice 2 0 0 9 18th Annual Trends and Issues in Logistics and Transportation

Transcript of Drivers of Sustainable Supply Chain Management …...The 2009 Drivers of Sustainable Supply Chain...

Drivers of Sustainable Supply Chain

Management Practice

2 0 0 9

18th Annual Trends and Issues in Logistics and Transportation

The 2009 Drivers of Sustainable Supply Chain Management Practice

18th Annual Trends and Issues in Logistics and Transportation

ii

The 2009Drivers of Sustainable Supply Chain Management Practice18th Annual Trends and Issues in Logistics and Transportation

Table of Contents

Executive Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1

The Economy Drives Decision Making . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .2

A Call to Create Supply Chain Practices that Sustain During Difficult Times . .4

Optimization . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .5

Synchronization . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .7

Profitability . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .9

Adaptability . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .11

Velocity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .13

Regional Differences in Supply Chain Management Practice: North America Versus The EEA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .15

Sustainable Supply Chain Management Practice . . . . . . . . . . . . . . . . . . . . . .16

More Research on Sustainable Supply Chain Management Practice . . . . . . .17

Who Participated in this Research? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .17

About the Authors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .18

The 2009 Drivers of Sustainable Supply Chain Management Practice

18th Annual Trends and Issues in Logistics and Transportation

iii

The 2009 Drivers of Sustainable Supply Chain Management Practice

18th Annual Trends and Issues in Logistics and Transportation

Executive Summary

Too often the response to these tough economic times has been to hibernate. While this strategy is certainly aimed atsurvival, not adapting to changing markets will leave companies unprepared when the economy rebounds. As theeconomist Joseph Schumpeter put it, companies that resist change are “standing on ground that is crumbling beneaththeir feet.”1

These changes are not for a season; some argue that continual economic and social change is the “new normal.”Instead of constantly reorienting to the changing conditions, perhaps a wiser approach derived from observing naturewould be to create sustainable supply chain practices that adapt to conditions. While the term “sustainable” has beenused lately in the context of environmental and green issues, it also succinctly conveys the need to build and developapproaches and techniques for managing and operating the supply chain that will make the firm more responsive to ahost of dynamic international conditions.

The purpose of this report – our 18th annual study on trends and issues in supply chain, logistics and transportationmanagement – is to examine the fundamental capabilities that firms must develop in order to establish sustainablesupply chain management practices. And, over the next few months we will be sharing more detailed results of thestudy highlighting these practices.

The findings from this year’s study suggest that there are strategic moves that the firm should make now to positionitself and its supply chain to outperform the competition both now and when recovery happens. They are:

� Building cross-enterprise approaches to managing supply chain activities

� Determining the optimal balance between customer service requirements and the total landed cost of providing thatservice on an order-by-order basis

� Investing in approaches, tools and technologies that enable optimized supply chain decision making

The challenge that firms must deal with is how to advance these strategies in a period of financial adversity. Theeconomy has leveled the playing field for business. In the past three years, the Masters of Logistics (firms with salesrevenues greater than $3 billion) had created a notable competitive gap in logistics and supply chain managementbetween themselves and other size firms. This gap has almost disappeared in 2009. The window of opportunity formedium- and small-sized firms to act is now. The study findings indicate that the Masters have implementedinitiatives that will enable them to emerge from the economic downturn in a position of greater strength than beforethe recession.

Finally, a research effort of this size and scope would not be possible without the continued support of the study’sparticipants. We would like to thank these professionals for taking time out of their busy schedules to share with all ofus their expertise and insights.

Sincerely,

Mary C. Holcomb, Ph.D. Karl B. Manrodt, Ph.D. Belinda Griffin Dawn Salvucci-Favier Associate Professor Associate Professor Senior Manager Senior DirectorUniversity of Tennessee Georgia Southern University Capgemini, Inc. JDA Software Group, Inc.

The 2009 Drivers of Sustainable Supply Chain Management Practice

18th Annual Trends and Issues in Logistics and Transportation

1 A.G Lafley and Ram Charan, The Game Changer (New York: Crown Business, 2008).

The EconomyDrives DecisionMaking

This past year presentedunprecedented challenges to firms aseconomies worldwide moved intorecession. The tough economic timessignificantly impacted howcompanies of all sizes managed andoperated their supply chains.Participants in our 18th annual studyon the trends and issues in supplychain, logistics and transportationmanagement told us that theeconomic hardship was compoundedby unpredictable demand, increasedcustomer demands and volatilecommodity and fuel prices. All ofthese combined to make 2009 one ofthe most difficult operating years everfor businesses.

The economic slide since 2008 hasplaced tremendous pressure on firmsto become much more efficient thanever before. In this relentless pursuit,customers have reminded companiesthat cost is not the only critical factorfor success – service is just asimportant. This was reinforced bythe study results, which showed thata commanding majority ofparticipants must “be all things to allpeople” when it comes to the overallstrategy of the firm. In 2008, 44.7percent of the study participantsreported that they were beingchallenged to deliver the bestpossible service at the lowest possiblecost to customers. This grew to 48.9percent in 2009. We have seengrowth in this strategic direction of“being all things to all people” since2006 when it passed customerservice as the top-ranked strategy.

This strategic direction requires thatfirms carefully differentiate servicelevels for customers. To be

successfully deployed, service andcost tradeoffs must be carefullyevaluated for each and everycustomer transaction. Analysis offirms by revenue size revealed thatlarge (greater than $3 billion) andmedium-sized ($500 million to $3billion) firms are much more focusedon reducing costs than small-sizedfirms (less than $500 million). Smallfirms are placing more emphasis onincreasing customer satisfaction.

Regardless of a firm’s size, theeconomic downturn was the mega-trend for 2009 that impacted thefirm’s overall business and logisticsstrategy. Beyond this factor, therewere several notable differences inhow other factors influenced the wayin which firms conducted business.For large firms (also known as theMasters of Logistics), dealing withchanges in the organizationalstructure was the second mostimpactful trend, followed closely bynew product introduction.

Medium-sized firms were mostaffected by increasing customerrequirements, the cost of logisticsservices and increased regulation andcompliance mandates. Besides theeconomy, the cost of logistics servicesand changes in the firm’sorganizational structure were the twofactors that most affected the logisticsstrategy of small-sized firms.

Over the past year, one of the topstrategic initiatives for large andmedium-sized companies was theexpansion into new markets. Largefirms also tackled three additionalstrategic initiatives that will positionthem to improve future performance.They developed or began using amore cross-enterprise approach tosupply chain management. This wascoupled with a move to standardizesupply chain processes. Last, but notleast, large firms also tackled theissue of excessive inventory in thesupply chain by initiating lean

2

The Masters of Logistics spent the past year engaged in strategicinitiatives that will position them to improve performance in thecoming year. These initiativesincluded:

� Developing and using a morecross-enterprise approach tosupply chain management

� Standardizing supply chainprocesses

� Implementing a lean approach toinventory management

Medium- and small-sized firmstook a different strategic direction– they concentrated their efforts onrenegotiating supplier contracts.

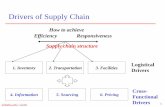

The purpose of this report is to put forward a set of elements that our studysuggests form the foundation of sustainable supply chain managementpractice. Five drivers have been identified: optimization, synchronization,profitability adaptability and velocity.

3

inventory efforts. Small-sized firms cited this initiative astheir number-one effort in 2009. Medium- and small-sized firms took a different strategic direction from largefirms in that they deployed a sizeable portion of theirefforts to renegotiation of supplier contracts.

The top two strategic initiatives undertaken by theMasters of Logistics is aimed at increasing the level ofintegration between supply chain partners. Supply chainintegration results in several benefits to the respectivemembers, including improved operational logisticsperformance related to cost, service, quality and/or time,as well as increased performance in areas such asprofitability, customer satisfaction and/or market share.

Aligning processes and approaches facilitates the flow ofinformation between supply chain partners. Surprisingly,the study results show that the customers of small firmsare much more willing to share information related to thedemand for their products than for medium or largefirms. Information sharing between small firms and theircustomers appears to be much more collaborative thanfor firms of other sizes where information sharing wouldbest be characterized as being coordinating in nature.The majority of respondents stated that the top criterionfor collaboration with customers is communication. Thiswas followed closely by top management commitmentand support, as well as visibility of demand. Whilesmall-sized firms seem to have the advantage incollaboration with customers at this time, the strategicinitiatives undertaken by the Masters of Logistics (the

large-sized firms) suggest that they now have in place thethree critical factors that are needed for extended supplychain collaboration. If leveraged properly, this certainlycreates an advantage for the Masters.

A Call to Create SupplyChain Practices that SustainDuring Difficult Times

Without exception, difficult economic times force firms ofall sizes to examine current business practices todetermine where they can be more efficient. After 9/11,economic conditions propelled companies into cost-cutting initiatives that impacted them – both positivelyand negatively – for several years afterwards. Very fewpeople predicted the depth and severity of the currenteconomic situation. Moreover, the global reach of therecession has left little doubt that business todayencompasses a broad geographic span.

What were the lessons learned after 9/11 that can beapplied to the current situation? Simply stated they are:

� Cost cutting must be done using a strategic filter

� Investments in improving supply chain capabilitiesshould not be delayed

The 2009 Drivers of Sustainable Supply Chain Management Practice

18th Annual Trends and Issues in Logistics and Transportation

17.0%

Customer service26.3%

Product/market

innovation7.8%

Cost leadership

Mix: Be all things to all

people48.9%

2009

Cost leadership

17.3%

Customer service29.5%

Product/market

innovation8.5%

Mix: Be all things to all

people44.7%

2008

4

The competitivesupply chain of the futuremust have:

Optimization

Synchronization

Profitability

Adaptability

Velocity

� Even in bad times, customerservice cannot be sacrificed

The reflection on the past led us tothe theme of this year’s study. Thechanges we are dealing with todayare not for a season; some argue thatcontinual economic and socialchange is the “new normal.” Insteadof constantly reorienting to thechanging conditions, perhaps a wiserapproach would be to createsustainable supply chain practice thatadapt to conditions. While the term“sustainable” has been used lately inthe context of environmental andgreen issues, it also succinctlyconveys the need to build anddevelop approaches and techniquesfor managing and operating thesupply chain that will make the firmmore responsive to a host ofinternational conditions.

Optimization

Current economic conditions presentan opportunity for shippers andcarriers to make real improvementsacross the supply chain as it relates tothe location of supply,manufacturing, points of distributionand flow of goods. Many companiesare rethinking their locationdecisions with consideration given toa hybrid geographic strategy thatincorporates “near shore” and “farshore” initiatives in the optimalsolution. This drive to "right size"the supply chain takes a total-landed-cost approach to all activitiesinvolved in supply chainmanagement from product idea tofinal product disposal. Almost allindustrial sectors from auto parts,farm machinery and consumer-packaged goods manufacturers toretailers are rationalizing theirnetworks in an attempt to design asupply chain that provides the

desired level of service at the lowestpossible cost. Transportationproviders are also an important partof “right sizing” the supply chain asthey manage and control thedownstream and upstream flows ofgoods. For example, CSXCorporation has continued toaggressively “right size” its railnetwork while maintaining therequired level of customer service.2

Right sizing the supply chain resultsin the alignment of resources foroptimal operations. When donecorrectly, the alignment will producedesirable results in tough economictimes and when the economyrecovers. In other words, the onlychanges that should be made to thenetwork structure are those thatdemonstrate the ability to create asustainable competitive advantage forthe supply chain as a whole.Furthermore, right sizing the supplychain is not a one-time effort. Thedynamic nature of the supply chainmeans that it will be an ongoing

quest to configure, calibrate andcontrol increasingly complexscenarios to derive optimal results.

This complexity in planning andexecution also challenges companiesto rethink their organizationalstructures, process flows and use oftechnology. In addition to strategicnetwork design decisions, companiescontinue to face the fundamentalproblem of how to optimize thedistribution of goods and services tothe marketplace. Strategic andtactical decisions that the firm makestoday will impact operations in thefuture. For example, a firm’sinvestment in supply chaintechnology will have implicationsbeyond the implementation stage. Ina global, dynamic and competitivemarket, companies must constantlyevaluate and effectively utilize thebest tools and technologies availableto optimize their operations.Software tools need to be capable ofproviding increasingly complexsupply chain solutions in addition to

5

ptimization is the alignment

of global supply chain

resources – both tangible and

intangible, own or outsourced –

to facilitate the success of supply

chain members.

O

2 Logistics Management, “Railroad shipping: CSX continues to ‘right size’," July 14, 2009.

assisting with firm-level decisionmaking. Spreadsheets and most“home-grown” tools alone will notprovide the decision-makingsolutions at the necessary speed in acomplex, competitive environment.

Three interrelated mega trends for both North American and the EEA are driving the “rightsizing” and alignment of resources in the firm and across the supply chain.

6

Both functions meet on a regular basis to discuss strategic decisions for both areas28.1%

Distribution decision making tends to drive distribution operations28.1%

Both functions report to the same person who makes these trade-off decisions26.3%

Either transportation drives the decision making process or the two are not integrated17.5%

“The transportation and

logistics management

technology solutions have

given us the ability to achieve

greater flexibility and agility in

our transportation network,”

said Hershey’s Cindy

Ambrose, project manager,

integrated transportation. “We

are now a truly consumer-

driven company, and we are

making better use of available

capacity and carrier assets to

deliver quality product at a

lower overall cost with superior

service.”

Current mega trends requirechanges to the supply chainnetwork and themanagement of logisticsactivities in order to optimizeoperations.

The management of North American distribution and outbound transportation activities indicates that very differentapproaches are used.

Synchronization

The benefits of synchronized supplychains have been written aboutextensively, but the concept remainsdifficult to operationalize.Manufacturers can reduce time tomarket, decrease costs and manageinventory turns through supply chainsynchronization. Synchronizationbetween members of a supply chainis a critical success factor in achanging environment. Supply chainmanagement must move from theintegration and management ofinternal functions to being able tocoordinate, organize and manage theactivities of the supply chain inwhich the company will beoperating.

Supply chain synchronization is oneof the essential drivers in a portfolioof sustainable supply chain

management practice; it is a crucialbuilding block towards trueintegration. While there has beencollaboration between supply chainpartners in improved communicationsuch as EDI and current Internet-based Web information exchanges,better information (point-of-sale dataand Collaborative Planning,Forecasting and Replenishmentinitiatives [CPFR]) and a generalwillingness to work more closelytogether, these improvements havebeen primarily gained by changinginternal business processes.Achieving supply chainsynchronization requires truecoordination between and among alltrading partners such that theyfunction as a single entity.

In this year’s study we focused ontwo aspects of synchronization: howwilling firms are to share data withtheir typical customer; and howimportant collaboration is with this

typical or average customer. Weselected a “typical or averagecustomer” for a reason. Instead oflooking at just “best customers” wewanted to see how widespread thelessons learned from this group weremaking their way down to otherproviders and/or customers. Areimprovements being experiencedacross the board?

What is interesting from the analysisis that the two continents havedifferent perspectives on sharing datawith their suppliers. North Americanrespondents are more willing toprovide information with a typicalcustomer as compared to those inEurope; these findings werestatistically significant.

Does it matter? That is, if firms aremore willing to share data will itimpact their financial performance?Based on our analysis firms that aremore willing to share data perform

7

ynchronization is the ability to

coordinate, organize and manage

end-to-end supply chain flows – products,

services, information, and financials - in

such a way that the supply chain

functions as a single entity.

S

2

8

“Implementing ‘best of breed’

supply chain solutions

provides Merck Serono with

one synchronized view of

demand. Having only one tool

as a demand data repository in

the entire company worldwide

allows us to easily follow an

aligned process across the

organization. Additionally,

having only one-application

instance forces us to define

clear rules in terms of forecast

data availability and process.

We now have timelines for

data availability and for

forecast submissions within

the whole organization.”

- Didier Dayen, head of supply

chain process, Merck Serono

NA EEA

Communication 1.43 1.73

Top management commitment andsupport

1.93 1.92

Visibility of demand 2.28 1.80

1=Very important; 7=Not very important

How important are the following to collaboration with your typical or averagecustomers?

better in terms of market share,competitive position, customerservice and product qualitycompared to those that don’t.

What is not different are the toolsutilized to foster collaboration withinthe supply chain. Communication,top management commitment andsupport, as well as visibility ofdemand are cited as the top threeareas. What is interesting is seeinghow highly top-managementcommitment and support is rankedfor initiatives involving a typical or

average customer. Is this perhapsdue to management’s ability to takethe lessons learned and apply themfurther down into the company’scustomer base, or is it a result of aneconomy where every customermatters?

13.4%

19.4%

14.9%

10.4%

29.9%

10.4%

1.5%

1.7%

5.3%

15.0%

23.6%

25.9%

19.3%

9.3%

0.0% 10.0% 20.0% 30.0%

As little as possible

Anything requested is shared

NA EEA

Sharing Data is Critical to Synchronization: How much data are you willing toshare with your typical customer?

Profitability

In the midst of a global recession anduncertainty around everything fromcommodity and fuel prices tosupplier viability, companies arefaced with making critical supplychain decisions that are intended toassist the firm in getting through thecurrent economic conditions. Thesedecisions, which are strategic andtactical in nature, will impact thefirm well beyond recovery of theglobal economy. The best strategicand tactical decisions will be thosethat position the firm and othersupply chain partners to be profitablein good and bad economic times.While factors such as sales revenues,market share and/or productinnovation are indicators of a firm’ssuccess in business, the bottom linecannot be ignored. Particularlyduring a time of concern about cashflow, as well as availability of credit

and financial soundness for bothsuppliers and customers, overallprofitability is a paramount concernfor the firm. In some cases, the firmis being asked to extend customercredit terms beyond the statedarrangements. On the other end ofthe supply chain, suppliers areasking for shorter payment cycles inorder to improve their liquidityposition. Suppliers that are unable tosecure credit may need even greaterfinancial assistance from theircustomers in order to make anddeliver the needed goods ormaterials.

Internal to the firm, there is aconcerted effort to ensure thatworking capital is increasinglyproductive. Over the past severalyears, large manufacturers haverealized revenue and profitabilitygrowth that allowed them to build upsizable cash reserves. There ispressure from investors to use thosecash holdings for productive

purposes. Yet many largemanufacturers appear to be temptedto buy back stock to boost shareprice in the short term. Smallermanufacturers, which are typicallysuppliers to the supply chain leaders,do not have cash reserves as deep asthose of large manufacturers. Theymay have to use some of theirliquidity to finance supply chainactivity if credit markets aren’taccessible, or as noted above theymay need the assistance of the largemanufacturers to help in weatheringthe recession. This use of cash bysmall, medium and large firms willput increased pressure on them tooptimize another working capitalcategory – inventory. While therehas been some progress in reducingthe amount of inventory held byindividual companies, the studyresults indicate that one of the majorchallenges during this past year hasbeen the excessive amount ofinventory in the supply chain. For

9

rofitability is the result of

creating value through supply chain

activities. Asset performance, working

capital, returns on investment for

infrastructure, technology, and people,

are some of the critical parts that create

value in a global environment.

P

3

10

Domino Foods, Inc.

Escalating business expectations areforcing C-level executives to take a hardlook at business processes. Butbusiness process change is no longerabout making individual processesfaster. It’s about creating opportunitiesfor growth and innovation that can leadto greater business value. Dominoturned its sights to procurementtransformation to find new ways to helpthe company build efficiencies andcreate savings across the enterprise.

Before embarking on an enterprise-wide procurement transformation,Domino Foods and Florida CrystalsCorporation (FCC), which had acquiredan interest in Domino, needed to rethinkthe systems and processes managingtheir master data. The Dominoacquisition increased business processcomplexity at both companies. Differentlevels of controls, inconsistentmanagement procedures, and multipledatabases thwarted their ability toexecute corporate spend analysis andmaterial planning.

Procurement transformation andstrategic sourcing programs—both ofwhich are ongoing at Domino Foods—have created significant business valueas buyers have shifted from location tocommodity-based buying. “We’ve notonly been able to drive operationalsavings across the enterprise, but havecreated a sustainable centralizedprocurement organization. And thebeauty of having it in place means thatthe integration of new acquisitions suchas C&H Sugar (2004) and Chr Hansen(2006) are that much easier,” notes DonWhittington, CIO, Domino Foods, Inc.

Reduce costs

Maximize profitability

Increase customer

satisfaction

Maximize asset

utilization

Although Cost Cutting is the Main Focus for Most Firms, Profitability is Also a KeyObjective for 2009

some firms inventory levels havebeen rising faster than revenue.

Even leading-edge supply chaincompanies are putting budgets undersevere review. New investments forcompanies of any size will be focusedon cost savings with an emphasis onshorter payback periods. Because ofthe impact on profitability anyexpenditure that the firm makes willbe assessed using a cost/value lens.The constraints on capital will putsupply chain and other informationtechnology (IT) budgets undercritical review. Many companies areusing zero-based budgetingtechniques, which entails going back

to a blank sheet of paper andbuilding spending back up ratherthan just assuming a growth rate thatkeeps IT within an acceptablepercentage of revenue. Capitalspending will favor projects with fastimplementation times and even fasterbenefit realization. For many firms,investment in supply chainmanagement technology enablesthem to quickly deliver results to thebottom line and often at a greaterreturn than estimated.

2.2 2.2 2.11.8 1.9

2.02.4

2.1 2.22.0

Market share Return on assets Overall product quality

Overall competitive

position

Overall customer service levels

Scale: 1 = Much better; 7 = Much worse

NA EEA

How Did Your Firm’s Performance Compare to Your Competitors?

Firms are expanding into newmarkets and embracing lean-inventory approaches in aneffort to improve profitability.

11

Adaptability

As noted earlier, the most pressingissue that study participants aredealing with is unpredictabledemand. Unpredictable demand isimpervious to economic conditions.It exists in good and bad times. Forthat reason, individual firms and thesupply chain as a whole must be ableto handle this challenge.

Furthermore, increasing pressure willcome from supply chain executiveswho recognize the importance ofbeing able to make adjustments inpractices, processes, and structures ofsystems and networks as conditionschange. This is the essence ofadaptability. Adaptability is the keyto building competitive advantage inan increasingly complex anddynamic operating environment. Itenables the firm to respond toexpected and unexpected events inan efficient and effective manner.

A critical question is whether asupply chain can be designed to beadaptable enough to handle a myriadof operating challenges. It is noteconomically feasible for a supplychain to plan for every businesspossibility. Rather, the focus must beon those parts that are critical to thesuccess of the company. The goal isto build flexibility while minimizingvulnerability in those areas toimprove adaptability – regardless ofwhat, where and when the nextchanges in operating conditionsoccur.

Visibility in the supply chain is vitallyimportant to adaptability. The abilityto adjust to changes in demand canbest be done as the situation isdeveloping – not after the fact.Visibility circles the globe to managethe flow of products, services, andinformation. Real-time access toorder information providesopportunities to drive down cost andimprove customer service.

Visibility is a lot like an onion withmultiple layers. The outer and mostvisible layer according to the studyrespondents is orders in transit.Peeling back the layers of the onionreveals that as the order movesfurther upstream in the firm (or morelayers are peeled back), visibilitydecreases. This finding is particularlydisconcerting for those products withlonger lead times as the probabilitythat conditions will change increasesover time.

Given the longer lead times that areinvolved with internationalcustomers, it isn’t surprising that thisis one of the primary areas that NorthAmerican (NA) firms are planning toexpend effort on in the next year.The emphasis on increasing visibilitywith international customers withinthe next year is also a focus for firmsin the European Economic Area(EEA). Increasing visibility at thispoint in the supply chain will enablefirms to be more responsive to

4

daptability is the degree to

which respective supply chain members

can change practices, processes and/or

structures of systems and networks in

response to unexpected events, their

effects or impacts.

A

12

changes in demand. As a result, itwill increase their adaptability.

Does visibility matter? For NArespondents, those with highvisibility scores reported higherperformance levels than low visibilityrespondents in four of five financialmeasures – market share, overallcompetitive position, customerservice levels and product quality.Just as important, a lack of visibilitycan lead to customer serviceinefficiencies, excess inventory andhigher-than-needed transportation

costs. Global supply chain visibilityallows firms to adjust plans andactivities as changing conditionswarrant. This is the fundamentalproperty of adaptability.

To achieve a responsivesupply chain, Lowe’s adopteda comprehensive, closed-loopplanning and forecastingprocess that was integratedthroughout its business andprovided forward visibility toLowe’s suppliers, distributionnetwork and transportationgroup. Armed with a singleversion of the truth from aforecasting perspective,Lowe’s now relies on its plansto drive efficient execution.This daily approach enablesLowe’s to align processes andmulti-echelon plans with itstop suppliers for consistentcollaboration, communicationand analysis methods. Lowe’salso leverages an all-inclusivetransportation managementplatform to support thecomplexity of its import anddomestic operations as itstrives to synchronize itsinternational and domestictransportation businessoperations.

Orders in transit 40.7%

Finished goods inventory

commitment 40.1%

Production schedule 39.9%

Commitment of raw

materials 18.5%

Customer Visibility of Orders

31.5%

38.1%

22.2%

8.1%

21.5%

44.9%

22.3%

11.3%

0.0% 10.0% 20.0% 30.0% 40.0% 50.0%

In my firm

With customers

With suppliers

With service providers

International Domestic

Where will effort be expended within the next year to increase visibility?

Adaptability will not bepossible until end-to-endvisibility of supply chain flows exists.

VelocityToday’s economy is based on speed-to-market where supply chainsoperate in minutes, not hours ordays. Delivering this type of servicerequires companies to continuallymonitor and adapt their strategy andtactics in this rapidly evolvingmarket. The analogy that is oftenused to describe supply chainvelocity is that of a pipeline: as apipeline grows longer to serve anexpanding market, the volume ofgoods flowing through itcorrespondingly expands. In orderfor supply chains to be moreresponsive to these changes theymust be able to increase the velocityof the end-to-end flows, includingproducts and services, informationand financials.

Unfortunately very few companieshave a true working knowledge ofthe velocity of their supply chains.While a small minority of companies

– such as Dell, Home Depot andWal-Mart – base their competitiveadvantage on knowing andmanaging the velocity of goods intheir networks, most are inwardlyfocused and have extremely limitedvisibility to what is occurring in their supply chains. In addition,this lack of visibility into supplychain velocity has become an evenbigger problem as companiesincrease the level of outsourcing,product lifecycles continue to getshorter and increasing customerservice levels demand even greatersupply chain flexibility.

As a result of today’s fast-pacedglobal business environment, the gapbetween supply lead time andcustomers’ order cycles is widening.As such, velocity is decreasing. Most companies address this gap byattempting to increase forecastaccuracy and carrying additionalinventory in the supply chain.Unfortunately, despite the use of

sophisticated forecasting techniques,forecast error continues to be anissue. Even worse, as each node inthe supply network builds bufferinventories to manage variability,inventories at each supply chainlevel begin to experience theinfamous "bullwhip" effect. Thus, asthe effect of lead times cascade downthe supply chain, the ability of anindividual company - and the supplychain as a whole - to serve anincreasingly demanding customerbecomes more and more difficult.Increasing supply chain velocitycannot be achieved by just focusingon forecasting and expanding supplychain inventories alone.

13

5

elocity is the speed at which

end-to-end flows occur in the supply

chain. It encompasses speed-to-market

for new product introduction and

execution when conditions are

rapidly changing.

V

14

Speeding time to market’ is a typicalmantra for the consumer productsindustry. Consumer goodsmanufacturers have a strong focuson streamlining efficiencies to driveimproved margins on theirproducts–especially in a constrainedeconomy–and are identifying waysto expedite bringing new productsto market.

A Fortune 50 Pharmaceutical &Consumer Products manufacturerpartnered with a global supply chainmanagement consulting firm toassess then design new processesto drive efficiencies from researchand development through ProductMarketing and Distribution. The newprocesses leveraged web-basedtechnologies to securely allow 25different organizations tosimultaneously collaborate, designand deploy new products ten timesfaster than their current process.They also leveraged this sameprocess globally to captureintellectual property for reuse, andto initiate global process excellenceacross the product developmentand supply chain.

This project highlighted a keyimperative for manufacturers today.They must develop tactics,processes and technologies thatcan substantially drive revenue liftand sustained market velocity.

Supply chain velocity – bothin North America and the EEA– is being hindered byactivities outside the controlof logistics/supply chainprofessionals.

New product introduction

Product promotions

Product promo�ons

Changes in product price

North Americ a E E A

Importance

Changes in product

price

New product

introduction

What Factors Impact the Firm’s Ability to be the Most Efficient on an Individual OrderBasis?

13.0

35.4 37.8

15.5

36.4

45.8

0

10

20

30

40

50

Number of FG inventory turns

Days sales in FG inventory

Avg days sales outstanding

North America EEA

Firm Velocity Performance

egional Differences in Supply Chain Management

Practice: North America Versus The EEA

The study results indicate that supply chain management practice

in the EEA, while alike in some respects, is clearly different

from North American (NA) practice in some key areas.

R

Strategic focus Some 40.4 percent of the EEA studyrespondents reported that customerservice was the overall strategy fortheir division or business unitcompared to 26.3 percent for NAparticipants. The main strategy forNA firms can best be characterized asa hybrid mix of “being all things toall people.”

Perhaps part of the emphasis oncustomer service by firms in the EEAcan be attributed to the fact that afterunpredictable demand, increasedcustomer demands with respect toprice and/or service levels was thesecond most difficult aspect ofmanaging and operating the supplychain. EEA firms also rated theirperformance on customer-servicelevels lower than their NAcounterparts.

Collaboration There are fundamental differences inthe importance of factors related tocollaboration for the EEA and NA.Firms in the EEA reported that top-management commitment andsupport is the most important aspectof successful collaboration with

customers, while NA firms ratedcommunication as the top factor.Study participants in both regions,however, agree that visibility of demand and aligned supplychain/logistics processes are also critical elements forcollaboration efforts.

15

Visibility of an order in EEA firms is best during order preparation. Overall order visibility isbetter in EEA companies than in NA firms.

RUSSIA

FINLAND

AUSTRIA

ITALY

SPAIN

SWEDEN

NORWAY

GERMANY

FRANCE

PORTUGAL

HUNGARYROMANIA

BULGARIA

TURKEY

DENMARK

POLAND BELARUS

UKRAINECZECH

SLOVAKIA

GREECE

CYPRUS

NETH.

BELGIUM

IRELAND

YUGOSLAVIA

ALBANIA

MOLDOVA

LITHUANIALATVIA

ESTONIA

LUX.LUX.

BOSNIAAnd

HERZ.

CROATIASLOVENIASWITZERLAND

MACEDONIA

ICELAND

U. S. A.

CANADA

MEXICOTHE BAHAMAS

CUBA

PANAMA

EL SALVADORGUATEMALAAA

BELIZEHONDURAS

NICARAGUAAA

COSTARICA

JAMAICAHAITI

DOM. REP.

ARGENTINA

BOLIVIA

COLOMBIA

PERU

BRAZIL

FRENCH GUIANA

SURINAME

GUYANA

CHILE

ECUADOR

PARAGUAY

URUGUAY

FALKLANDISLANDS

SOUTHGEORGIA

ISLAND

KENYA

ETHIOPIA

REATRTTER EAETRTTERI REAR

SUDAN

EGYPT

NIGER

MAURITANIA

MALI

NIGERIA

SOMALIA

NAMIBIA

LIBYA

CHAD

SOUTH AFRICA

TANZANIA

ANGOLA

ANGOLA

ALGERIA

MADAGASCAR

MOZAMBIQUEBOTSWANA

ZAMBIA

GABON

CENTRALAFRICAN

REPUBLIC

TUNISIAMOROCCO

UGANDA

SWAZILAND

LESOTHO

MALAWI

BURUNDI

RWANDA

TOGO

BENINGHANA

COTED'IVOIRELIBERIASIERRA LEONE

GUINEA

BURKINAFASO

GAMBIA

CAPEVERDE

CAMEROON

SAO TOME & PRINCIPE

ZIMBABWE

CONGO

DEM. REP.OF CONGO

EQUATORIAL GUINEA

WESTERNSAHARA

(occupied by Morocco)

DJIBOUTI

SENEGALLSENEGA

GUINEA BISSAU

Canary Islands

AZORES

JORDAN

ISRAELLEBANON

ARMENIA AZERBAIJAN

GEORGIA KYRGYZSTAN

TAJIKISTAN

KUWAIT

QATAR

BAHRAIN

U. A. E.

YEMEN

SYRIA

IRAQ

IRAN

OMAN

SAUDI ARABIA

RUSSIA

AFGHANISTAN

PAKISTAN

INDIA

CHINA

KAZAKHSTAN

TURKMENISTAN

UZBEKISTAN

MYANMAR

THAILAND

CAMBODIA

NEPALBHUTAN

VIETNAM

SRI LANKA

LAOS

BANGLADESH

MALAYSIA

MALAYSIA

PAPUANEW GUINEA

BRUNEI

SINGAPORES

PHILIPPINES

TAIWAN

I N D O N E S I A

JAPAN

MONGOLIA

SOUTH KOREA

NORTH KOREA

A U S T R A L I A

NEW ZEALAND

U. K.

MALTA

NEWCALEDONIA

FIJI

EAST TIMOR

VENEZUELA

Managing andOperating theSupply ChainBusiness conditions: EEAcompanies did not have the samelevel of difficulty in dealing with fueland commodity price volatility asdid NA firms. Instead, EEA studyparticipants stated that excessiveinventory in the supply chainpresented one of the majorchallenges to managing andoperating the supply chain in thecurrent economic downturn.

Procurement and inboundtransportation: In NA firms,procurement/purchasing decision-making tends to drive inboundtransportation execution. This isvery different for EEA firms whereboth functions meet on a regularbasis to discuss strategic decisions.This is reflected in data that showthat 31.3 percent of EEAparticipants had no change in thedays’ supply of inventory over thepast year, and 22.9 percent reportedan increase in days’ supply ofinventory of 1 to 5 percent. This iscompared to NA firms where thegeneral trend was a decline in thedays’ supply of inventory in therange of 6 to 10 percent.

SustainableSupply ChainPracticeDealing with the current economicconditions has put many firms in theposition of focusing most, if not all,of their attention on the short term.When the economy rebounds, these

same firms will find themselvesunprepared to take full advantage ofbetter business conditions. This isbecause they have not built supplychain management practices thatwill be sustainable through goodtimes as well as bad. This year’sstudy presented five drivers thatconstitute the core of sustainablepractice in supply chainmanagement. These drivers are theengine that will fuel the firm’sgrowth and success. They representcapabilities that will be difficult forthe competition to emulate, and theyare fundamental to creating aleading-edge supply chain.

While the economy has been a greatequalizer across companies of everysize, the study results indicate thatthe Masters are engaged in strategicinitiatives that will position them tocreate significant competitiveadvantage when the economyrebounds. They are:

� Standardizing supply chainprocesses in order to build cross-enterprise coordination

� Focusing on the “cost to serve” todetermine the optimal balancethat provides the greatestprofitability for ALL supply chainpartners

� Utilizing tools, technology andmethods that enable them to alignsupply chain resources for optimalperformance

Completed initiatives and effortscurrently underway suggest thatsmart firms are making strategic andtactical changes to their businessesand supply chains that will make itpossible for them to weather thiseconomic storm. More importantly,they are building for a moreprosperous future. These companieswill be ready to deploy and utilize

A majority of EEA firms usecommercially purchasedsoftware that is part of theirenterprise resource planningsystem to manage distributionactivities.

Sustainable Supply Chain Management Practice

20.3%

7.4%

5.4%

18.9%

12.8%

15.5%

17.6%

2.0%

54.3%

2.2%

0.0%

2.2%

10.9%

30.4%

0.0%

0.0%

0.0% 10.0% 20.0% 30.0% 40.0% 50.0% 60.0%

Commercially purchased - part of ERP

Commercially purchased "best of breed"

Commercially purchased "best of breed" ASP

Integrated silo sources through a software platform

Software package developed in-house

Manual / spreadsheet

Third party provider

Other

EEA NA

Managing Distribution Activities - EEA versus NA Firms

16

The 2009 Drivers of Sustainable Supply Chain Management Practice

18th Annual Trends and Issues in Logistics and Transportation

an array of capabilities thatincorporate the drivers of sustainablesupply chain management practice.

The question is: Will You be ReadyWhen the Economy Rebounds?

More Research onSustainableSupply ChainManagementPractice This year’s annual study examined avariety of issues and trends rangingfrom supply chain megatrends totransportation managementtechniques and approaches. We aretaking a different approach in thedissemination of the study resultsthis year. In addition to this reportthat provides an overview of the fivedrivers of sustainable supply chainmanagement practice, a short reportwill be issued for each driver –adaptability, synchronization,velocity, optimization, andprofitability – to further explore thedimensions and current state ofpractice.

Who Participatedin this Research?This year 830 individuals across theglobe participated in the study.Aggregated as a profile group, 63.4percent of the companies thatresponded to the survey have annualrevenues under $1 billion, whilethose with annual sales of $1 billionto $3 billion accounted for 12.1percent of the sample. Those firmswith sales greater than $3 billion

accounted for 24.6 percent. Thelatter group has been defined as theMasters of Logistics.

More than 14 industry sectors fromenergy/chemical/mining to retailingparticipated in this year’s study withthe core group of participants in themanufacturing sector (48.3 percent).Consumer products and generalmanufacturing represented thelargest sub-sectors of this group(18.3 and 16.6 percent,respectively). The next largest sectorthat participated in this year’s studyis retail, accounting for 12.1 percentof the total participants.

5.7%0.7%0.5%

1.4%3.2%

5.7%7.4%

14.9%2.7%

5.7%16.6%

18.3%5.0%

12.1%

OtherHealth managed care

UtilitiesCommunicationsAgriculture/food

Energy/chemical/miningLife sciences

Transportation service providerManufacturing - AerospaceManufacturing - AutomotiveManufacturing - Consumer …

Manufacturing - GeneralManufacturing - High tech

Retail

Study Participants by Industry Sector

< $250 million, 40.8%

$250 - $500 million, 10.3%

$500 million -$1 billion,

12.3%

$1 - $2 billion, 7.9%

$2 - $3 billion, 4.2%

$3 - $5 billion, 9.6%

$5 - $9 billion, 3.7%

> $9 billion, 11.3%

Annual Sales Revenue of Study Respondents

17

About theAuthors CapgeminiBelinda Griffin is a senior managerwith Capgemini Consulting. She hasover 15 years experience in logisticsand fulfillment and has developedsupply chain strategies for leadingcompanies worldwide.

Capgemini, one of the world’sforemost providers of consulting,technology and outsourcing services,enables its clients to transform andperform through technologies.Capgemini provides its clients withinsights and capabilities that boosttheir freedom to achieve superiorresults through a unique way ofworking, the Collaborative BusinessExperienceTM. The Group relies on itsglobal delivery model calledRightshore®, which aims to get theright balance of the best talent frommultiple locations, working as oneteam to create and deliver theoptimum solution for clients. Presentin more than 30 countries,Capgemini reported 2008 globalrevenues of EUR 8.7 billion andemploys 90,000 people worldwide.

More information is available atwww.capgemini.com.

JDA Software Group, Inc.Dawn Salvucci-Favier is seniordirector of product management,transportation for JDA Software. Inthis position, Salvucci-Favier isresponsible for overall productstrategy for JDA’s Transportation &Logistics Management solutions,working very closely with the sales,marketing and product developmentgroups at JDA. She has been in thisrole since JDA’s 2006 acquisition ofManugistics.

JDA® Software Group, Inc.(NASDAQ: JDAS) is the world’sleading supply chain solutionsprovider, helping companiesoptimize operations and improveprofitability. JDA drives businessefficiency for its global customer baseof more than 5,800 retailers,manufacturers, wholesaler-distributors and services industriescompanies through deep domainexpertise and innovative solutions.JDA’s combination of unmatchedservices, together with its integratedyet modular solutions formerchandising, supply chainplanning and execution and revenuemanagement, leverage the strongheritage and knowledge capital ofmarket leaders includingManugistics, E3, Intactix and Arthur.For further information, please visithttp://www.jda.com.

Georgia SouthernUniversityDr. Karl Manrodt is an associateprofessor in the Department ofManagement, Marketing & Logisticsat Georgia Southern University.Research interests revolve around therole of information in logisticssystems, performance measurement,the role of logistics in health care,and customer value determination ina logistics setting. His publicationshave appeared in such journals as theSupply Chain Management Review,Transportation Journal, theInternational Journal of PhysicalDistribution and MaterialsManagement, Interfaces, and theJournal of Business Logistics.

Georgia Southern University is agrowing nationally recognizedlogistics program located inStatesboro, Georgia. The Universityis a major teaching and researchinstitution and offers undergraduateand Ph.D. degrees in logistics andsupply chain management. Thefaculty publishes in a wide range of

topics and is invited to speak atevents across the globe. TheSouthern Center for IntermodalTransportation offers a wide range ofresearch services and resides in theCollege of Business.

For further information, please visithttp://www.GeorgiaSouthern.edu orhttp://www.manrodt.com

University of TennesseeDr. Mary Holcomb is associateprofessor of logistics andtransportation in the College ofBusiness at The University ofTennessee. Her professional careerincludes eighteen years at the OakRidge National Laboratory intransportation research for the U.S.Department of Energy, U.S.Department of Transportation, andthe U.S. Department of Defense. Dr.Holcomb’s background also consistsof varied industry experience withMilliken & Company, the formerBurlington Northern Railroad, andGeneral Motors. Her research hasappeared in the Journal of BusinessLogistics, Transportation Journal, theInternational Journal of LogisticsManagement, and Supply ChainManagement Review.

The internationally recognizedlogistics program at The University ofTennessee, Knoxville, is one of themost comprehensive andcontemporary programs in thenation. The faculty publishes widelyon topics of current industry concernand explores future trends throughresearch and studies.

For further information, please visithttp://mlt.bus.utk.edu

18

19

Karl B. Manrodt, Ph.D.Associate Professor of LogisticsDepartment of Management, Marketing & LogisticsP.O. Box 8154Georgia Southern UniversityStatesboro, GA 30460Direct: 912.681.0588Fax: [email protected]://www.manrodt.com

Mary Collins Holcomb, Ph.D.Associate Professor of LogisticsDepartment of Marketing & Logistics316 Stokely Management CenterUniversity of TennesseeKnoxville, TN 37996-0530Direct: 865.974.1658Fax: [email protected]://www.maryholcomb.com

Belinda GriffinSr ManagerCapgemini, U.S. LLC.45 Bartlett StreetMarlborough, MA 01752Direct: [email protected]

Ramon VeldhuijzenPrincipal Consultant Capgemini NetherlandsPapendorpseweg 100P.O. Box 2575 – 3500 GN– Utrecht,The NetherlandsDirect: +31 (0)30 689 00 [email protected]

Dawn Salvucci-FavierJDA Software9713 Key West Ave.Rockville, MD 20850Direct: [email protected]

The authors would like to especiallythank other team members whomade this work possible. At GeorgiaSouthern University, Mark Donatoand Davin Miller played a criticalrole in managing the Web site. AtCapgemini, Sumit Kumar providedinsight and case study analysis.Cathy Fitzgerald provided the designand layout of the report. In addition,the following individuals providedcountry specific research supportand analysis in their respectivecountries: Leanny PizzolanteAlbornoz (Spain), Karin Oerlemans(The Netherlands), Simon Mollart(UK), Lieven Loose (Belgium),Kristoffer Arvidsson (Sweden),Giorgio Vigano (Italy) StephenNestor (Australia) and ThiaguMathan (India). Additional thanks toCentro Español de Logística forpartnering with the team inconducting this year’s research. AtJDA, Jenni Ottum provided criticalsupport in copy editing and casestudy examples and Caroline Proctorfor directional support in launchingand marketing this study.

The 2009 Drivers of Sustainable Supply Chain Management Practice

18th Annual Trends and Issues in Logistics and Transportation