Dream It. FInance It. BuIlD It. - Ulster Savings Bank · 2015-03-04 · Dream It. FInance It. BuIlD...

14

DREAM IT. FINANCE IT. BUILD IT. Construction loans designed to your specifications Banking • Loans • Investments • Tax & Payroll • Insurance You’ve got US!

Transcript of Dream It. FInance It. BuIlD It. - Ulster Savings Bank · 2015-03-04 · Dream It. FInance It. BuIlD...

You’ve got US!

Dream It. FInance It. BuIlD It.

Construction loans designed to

your specifications

Banking • Loans • Investments • Tax & Payroll • Insurance

You’ve got US!

BR-M-721 9/09

Investment, Tax, Payroll and Insurance products and services available through Ulster Insurance Services, Inc. and Ulster Financial Group, Inc., subsidiaries of Ulster Savings

Bank, are NOT FDIC INSURED.

Member FDIC

Customer Service Center (866) 440-0391www.ulstersavings.com

CONSTRUCTION/PERMANENT MORTGAGE PROGRAM

PROPERTY TYPES• 1-2 Family, Owner Occupied Primary Residences• 1 Unit Second Homes• Rehabilitations, 1-2 Family Purchase & Refinance

CONSTRUCTION TYPES• Stick Built• Modular• Log*• Panelized*• Kit**Log, Panelized and Kit homes are on an exception basis only and may be subject to limiting

conditions.

TERMStandard term is 24 months.

RATEFixed Rate for the term of 24 months.

RATE LOCK PERIOD• Construction rate is locked for up to 120 days pursuant to Lock-In

Agreement.• Permanent rate can be locked for up to 60 days with standard rate

lock agreement and rate lock fee.• Extended rate locks are available for permanent financing.

MAXIMUM LTV (LOAN TO VALUE) Loan to value based on the lesser of the appraised value or the total acquisition.

Full Income VerificationCall lender for details. Loan to values over 80% are subject to mortgage insurance approval.

No Income VerificationCall lender for details. Rehabilitation – PurchaseMaximum LTV is 75% of the purchase price or “as is” value (whichever is less) plus the cost of improvements limited to 80% of the “as completed” value.

112

________________________________________________________________

________________________________________________________________

________________________________________________________________

________________________________________________________________

________________________________________________________________

________________________________________________________________

________________________________________________________________

________________________________________________________________

________________________________________________________________

________________________________________________________________

________________________________________________________________

________________________________________________________________

________________________________________________________________

________________________________________________________________

________________________________________________________________

________________________________________________________________

________________________________________________________________

________________________________________________________________

________________________________________________________________

________________________________________________________________

________________________________________________________________

________________________________________________________________

NOTES

112

MODULAR BUILT ITEMIZED COST BREAKDOWN

10% 2% 2% 65%

21%

Foundation completeCellar floor installedRough grading complete

Balance of manufacturer’s invoice due on delivery not to exceed 65% of the loan amount. If any of the 65% of the loan amount is available after paying the balance due on the invoice upon delivery, it will be disbursed after the unit has been set on the foundation

For the following items completed at the time of inspection:2% Roof, exterior siding and trim complete3% Water supply connected3% Sewer system complete2% Heating complete2% Plumbing complete2% Electric complete2% Interior trim complete1% Interior painting complete1% Floors complete1% Final grading complete2% Decks, steps and porches complete

100% COMPLETE, including a satisfactory completion certificate with the inspection.

CONSTRUCTION/PERMANENT MORTGAGE PROGRAM CONTINUED

Rehabilitation – RefinanceMaximum LTV will be 75% of the “as is” value plus the cost of improvements limited to 80% of the “as completed” value.

NOTE: “Sweat equity” is not permitted.

LAND REQUIREMENTS• Value attributed to land owned for less than one year is determined

by the lesser of the actual price paid or the current appraised value.• Value attributed to land owned for more than one year will be

determined by the appraisal.• Gifts of land are acceptable and the value will be determined by the

appraisal.• Any land liens must be satisfied at construction closing.

MORTGAGE INSURANCEMortgage insurance is required for LTVs greater than 80%.Insurance is obtained at construction. Premiums are collected at the time of the permanent closing.

THE APPROVAL PROCESS

GENERAL REQUIRED ITEMS• Copy of settlement statement from land purchase (if previously

acquired).• Copy of recorded deed.• Copies of bank statements or canceled checks showing source of

funds used to purchase land.• Copy of contract to purchase land.• Copies of all estimates, contracts, and paid receipts for all work

necessary to complete construction.• Copy of plans & specs for the home to be constructed.• Copies of most recent two years W-2’s.• Copies of most recent year to date pay stubs documenting one full

month earnings.• Copy of most recent two years signed personal tax returns including

all schedules (self-employed borrowers only).

10 3

THE APPROVAL PROCESS CONTINUED

• Copies of most recent two years signed business returns including all schedules (if applicable).

• Copies of two months most recent consecutive bank statements for all checking and savings accounts.

• Copies of most recent quarterly statements for any retirement and/or investment accounts.

• Satisfactory appraisal.

NOTE: The design and appeal of the subject property must conform to market standards. Ulster Savings Bank reserves the right to approve/decline all projects following review of plans and specifications.

RESERVE REQUIREMENTSFull Income VerificationReserves equal to 10% of the construction costs are required of which 5% must be liquid.

No Income VerificationReserves equal to 20% of the construction costs are required of which 10% must be liquid.

CLOSINGS

Ulster Savings Bank Construction program consists of two closings:

1. CONSTRUCTION LOAN CLOSINGAt the time of this closing you will incur the following closing costs:• Bank points (if applicable)• Application fee (paid prior to closing)• Flood certification fee• Credit report fee• Appraisal fee (paid prior to closing)• Underwriting fee• Settlement fee• Title review fee• Document preparation fee• Title insurance (determined by county and mortgage amount)• Recording fee• Tax service fee• Mortgage tax (New York properties only, varies by county and loan

amount)

CONSTRUCTION LOAN DEPARTMENT CONTINUED

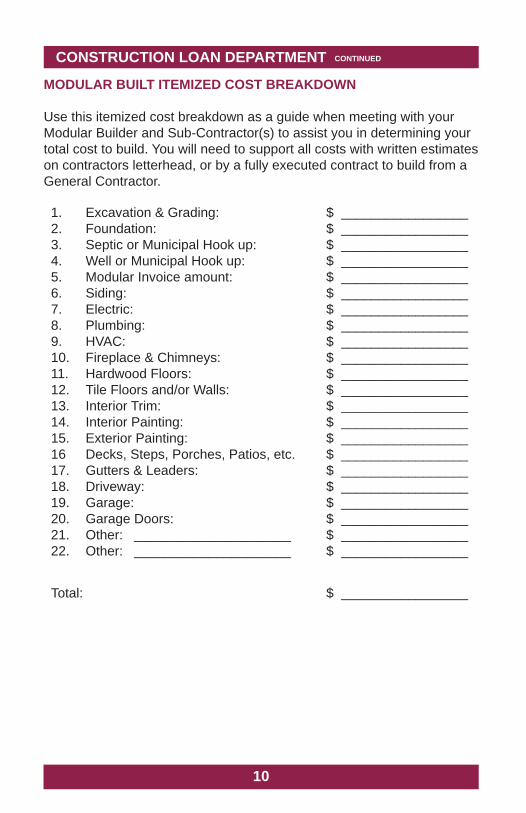

MODULAR BUILT ITEMIZED COST BREAKDOWN

Use this itemized cost breakdown as a guide when meeting with your Modular Builder and Sub-Contractor(s) to assist you in determining your total cost to build. You will need to support all costs with written estimates on contractors letterhead, or by a fully executed contract to build from a General Contractor.

1.2.3.4.5.6.7.8.9.10.11.12.13.14.15.1617.18.19.20.21.22.

Excavation & Grading:Foundation:Septic or Municipal Hook up:Well or Municipal Hook up:Modular Invoice amount:Siding:Electric:Plumbing:HVAC:Fireplace & Chimneys:Hardwood Floors:Tile Floors and/or Walls:Interior Trim:Interior Painting:Exterior Painting:Decks, Steps, Porches, Patios, etc.Gutters & Leaders:Driveway:Garage:Garage Doors:Other: _____________________Other: _____________________

$ _________________$ _________________$ _________________$ _________________$ _________________$ _________________$ _________________$ _________________$ _________________$ _________________$ _________________$ _________________$ _________________$ _________________$ _________________$ _________________$ _________________$ _________________$ _________________$ _________________$ _________________$ _________________

Total: $ _________________

94

CLOSINGS CONTINUED

SCHEDULING THE CONSTRUCTION CLOSINGBank attorneys must have the following prior to scheduling your closing:

• Title Report.• Survey (must be certified to Ulster Savings Bank, Its Successors

and/or Assigns, Borrowers and Title Company).• Builder Risk or Home Owners Policy (Policy must list Ulster Savings

Bank, Its Successors and/or Assigns, PO Box 3337, Kingston, NY 12402 as First Mortgage).

• Building Permit.

NOTE: At or following the construction closing you may begin to draw on construction funds provided all of the required documentation has been submitted to the bank. In order to receive an advance at closing for work that has already been completed, you must provide an under construction or as built foundation survey prior to closing. Under no circumstances can it be a proposed location or vacant land survey.

2. PERMANENT CLOSINGAt this closing the construction loan is converted into a permanent mortgage. Listed below are the closing costs that may be incurred at that time.

• Interest per diem (amount of interest due will vary depending on the day of the month you close)

• Settlement fee• Title review fee• Document preparation fee• Title insurance update fee• Recording fees• Appraisal fee (if necessary)• Credit report fee (if necessary)• Tax escrow deposit (if applicable)• Flood certification fee

SCHEDULING THE PERMANENT CLOSINGThe following will be required prior to scheduling:

• Permanent certificate of occupancy.• Certified survey showing house, driveway, well and septic, if applicable

(proposed subject under construction, or foundation survey not accecptable).• Conversion of builder’s risk policy to homeowner’s policy or renewal

of homeowner’s policy.• Update title insurance.• A final inspection showing 100% completion of all aspects of

the home in the appraisal report, based on the plans and specs submitted to the appraiser.

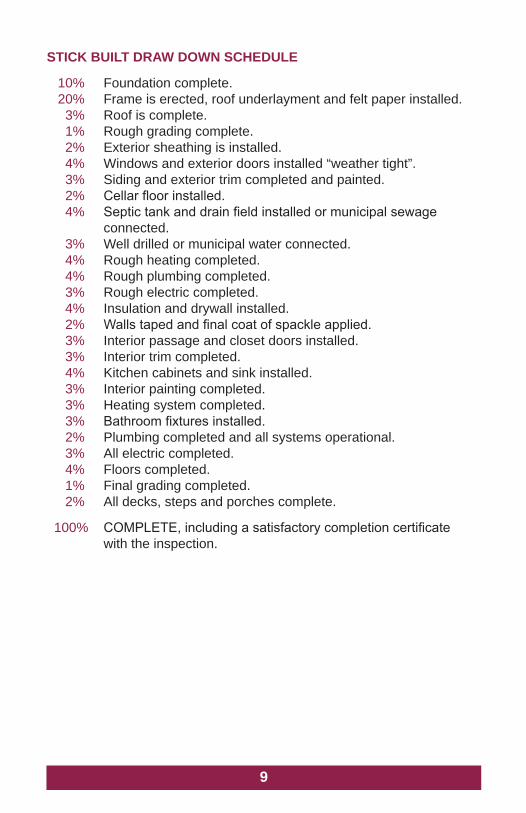

STICK BUILT DRAW DOWN SCHEDULE

10% 20% 3% 1% 2% 4% 3% 2% 4% 3% 4% 4% 3% 4% 2% 3% 3% 4% 3% 3% 3% 2% 3% 4% 1% 2%

Foundation complete.Frame is erected, roof underlayment and felt paper installed.Roof is complete.Rough grading complete.Exterior sheathing is installed.Windows and exterior doors installed “weather tight”.Siding and exterior trim completed and painted.Cellar floor installed.Septic tank and drain field installed or municipal sewage connected.Well drilled or municipal water connected.Rough heating completed.Rough plumbing completed.Rough electric completed.Insulation and drywall installed.Walls taped and final coat of spackle applied.Interior passage and closet doors installed.Interior trim completed.Kitchen cabinets and sink installed.Interior painting completed.Heating system completed.Bathroom fixtures installed.Plumbing completed and all systems operational.All electric completed.Floors completed.Final grading completed.All decks, steps and porches complete.

100% COMPLETE, including a satisfactory completion certificate with the inspection.

DRAWING ON CONSTRUCTION FUNDS

58

ORDERING INSPECTIONS All construction draws are based on the percentage of work completed.

Inspection fees are $100.00 and will be deducted from the draw.

NOTE: Prior to receiving any advances on your construction loan you must first provide an original under construction or as built foundation location survey. Survey must be certified to USB, its successors and/or assigns, borrowers and title company.

• Inspections are ordered by the customer through the Kingston office only. Please allow at least five days for inspection scheduling.

• Inspector will fax or call in a percentage complete based on the inspection schedule for your property.

• We will contact you to inform you of the inspection results and the amount of the disbursement.

• A title update is then ordered by the bank from your title company. This is to determine whether any additional liens have been placed on the premises. This update must be satisfactory.

• Monthly interest payments must be current.• Title updates for Connecticut properties are not applicable. Lien

waivers from all applicable contractors must be submitted prior to each disbursement on Connecticut properties.

NOTE: Title companies may begin to charge after a set number of updates. Please be sure to check with your title company. Any title charges will be deducted from the draw.

DISBURSEMENTS OF FUNDSThe funds can be disbursed in any of the following ways:

• Bank check mailed to your current address.• Electronic wire transfer (USB charges $20 for each transfer).• Branch pickup: at any of our convenient locations in Kingston,

New Paltz, Poughkeepsie, Saugerties, Stone Ridge, Phoenicia, Gardiner, Red Hook, Wappinger Falls, Windham and Woodstock.

• Direct deposit into an Ulster Savings Bank account.• All checks are issued to all parties on the note. Any deviation from

this policy, on any given disbursement, must be submitted in writing to the construction loan department. The entire process may take up to 10 business days.

CONSTRUCTION LOAN DEPARTMENT

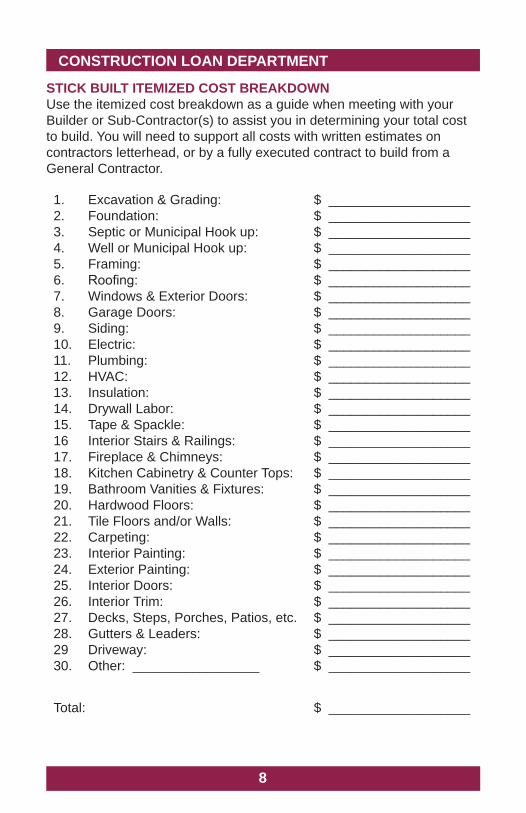

STICK BUILT ITEMIZED COST BREAKDOWNUse the itemized cost breakdown as a guide when meeting with your Builder or Sub-Contractor(s) to assist you in determining your total cost to build. You will need to support all costs with written estimates on contractors letterhead, or by a fully executed contract to build from a General Contractor.

1.2.3.4.5.6.7.8.9.10.11.12.13.14.15.1617.18.19.20.21.22.23.24.25.26.27.28.2930.

Excavation & Grading:Foundation:Septic or Municipal Hook up:Well or Municipal Hook up:Framing:Roofing:Windows & Exterior Doors:Garage Doors:Siding:Electric:Plumbing:HVAC:Insulation:Drywall Labor:Tape & Spackle:Interior Stairs & Railings:Fireplace & Chimneys:Kitchen Cabinetry & Counter Tops:Bathroom Vanities & Fixtures:Hardwood Floors:Tile Floors and/or Walls:Carpeting:Interior Painting:Exterior Painting:Interior Doors:Interior Trim:Decks, Steps, Porches, Patios, etc.Gutters & Leaders:Driveway:Other: _________________

$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________

Total: $ ___________________

76

CONSTRUCTION INTEREST BILLING• Interest bills are calculated and mailed out the first week of every

month.• Interest is billed in arrears (based on the previous month’s activity).• Interest is based on the total amount of money received, for the

number of days within the month.• Payments must be received by the 23rd of every month or a late

payment fee will apply.

QUESTIONS AND ANSWERS

Q Can I act as my own General Contractor?A Yes, you can. However, you must pay very close attention to disbursement guidelines. Funds are only disbursed based on completed work. You should consult with your attorney, municipal building department and insurance company regarding potential insurance issues.

Q Can I obtain financing to help purchase my land or pay off an existing lien on the land? A Yes. Ulster Savings Bank will finance up to 75% of the purchase price or the appraised value of the land (whichever is less). For example: If the purchase price of the land is $50,000 and the appraised value is $60,000, Ulster Savings Bank will give you 75% of the $50,000 toward the purchase of the land. The amount of money advanced on the land will then be deducted from the total loan amount. Disbursements will then be calculated on the reduced figure.

Q If I own my land free and clear, can I draw on the equity at the Construction Loan Closing? A Yes. You may draw up to 75% of the value of the land as determined by the appraisal.

Q Can I submit my own disbursement schedule or make changes to Ulster Savings Bank’s schedule?A Yes. Schedules can be revised to meet your particular needs. We advise you to review our schedule with your builder to determine whether or not he/she will be able to work from it. We only ask that the schedules be finalized and approved by the construction department prior to your construction loan closing.

Q Can I receive disbursements for the purchase of materials? A No. All disbursements are based upon completed work only.

Q What will happen if I use other forms of credit during construction? A Using other forms of credit may substantially change your financial picture to the extent that you may not qualify for the permanent financing.

Q What will happen if I do not finish the home at the end of the term? A The loan is considered to be in default and a default interest rate will be put in place. This will require you to payoff the loan or, at the banks sole discretion, you may modify the loan in order to extend the term.

Q What is the purpose of verifying reserves? A The objective of reserves is to assure the bank that you have ample funds to allow for cost overruns, upgrades, etc.

Q Can I convert to a permanent mortgage if I complete the house in less time than the construction loan term? A Yes. Provided you qualify, the house is 100% complete based on your inspection schedule, and we have received a certificate of occupancy. You may then close to a permanent mortgage at any time during the term of the construction loan.

Q When can I lock in my Permanent Loan Rate and for how long? A You can lock in your permanent loan rate for up to 60 days. Extended rate locks are available. Ask for details. Within those 60 days, the house must be 100% complete and all criteria for the permanent closing must be satisfied.

76

CONSTRUCTION INTEREST BILLING• Interest bills are calculated and mailed out the first week of every

month.• Interest is billed in arrears (based on the previous month’s activity).• Interest is based on the total amount of money received, for the

number of days within the month.• Payments must be received by the 23rd of every month or a late

payment fee will apply.

QUESTIONS AND ANSWERS

Q Can I act as my own General Contractor?A Yes, you can. However, you must pay very close attention to disbursement guidelines. Funds are only disbursed based on completed work. You should consult with your attorney, municipal building department and insurance company regarding potential insurance issues.

Q Can I obtain financing to help purchase my land or pay off an existing lien on the land? A Yes. Ulster Savings Bank will finance up to 75% of the purchase price or the appraised value of the land (whichever is less). For example: If the purchase price of the land is $50,000 and the appraised value is $60,000, Ulster Savings Bank will give you 75% of the $50,000 toward the purchase of the land. The amount of money advanced on the land will then be deducted from the total loan amount. Disbursements will then be calculated on the reduced figure.

Q If I own my land free and clear, can I draw on the equity at the Construction Loan Closing? A Yes. You may draw up to 75% of the value of the land as determined by the appraisal.

Q Can I submit my own disbursement schedule or make changes to Ulster Savings Bank’s schedule?A Yes. Schedules can be revised to meet your particular needs. We advise you to review our schedule with your builder to determine whether or not he/she will be able to work from it. We only ask that the schedules be finalized and approved by the construction department prior to your construction loan closing.

Q Can I receive disbursements for the purchase of materials? A No. All disbursements are based upon completed work only.

Q What will happen if I use other forms of credit during construction? A Using other forms of credit may substantially change your financial picture to the extent that you may not qualify for the permanent financing.

Q What will happen if I do not finish the home at the end of the term? A The loan is considered to be in default and a default interest rate will be put in place. This will require you to payoff the loan or, at the banks sole discretion, you may modify the loan in order to extend the term.

Q What is the purpose of verifying reserves? A The objective of reserves is to assure the bank that you have ample funds to allow for cost overruns, upgrades, etc.

Q Can I convert to a permanent mortgage if I complete the house in less time than the construction loan term? A Yes. Provided you qualify, the house is 100% complete based on your inspection schedule, and we have received a certificate of occupancy. You may then close to a permanent mortgage at any time during the term of the construction loan.

Q When can I lock in my Permanent Loan Rate and for how long? A You can lock in your permanent loan rate for up to 60 days. Extended rate locks are available. Ask for details. Within those 60 days, the house must be 100% complete and all criteria for the permanent closing must be satisfied.

DRAWING ON CONSTRUCTION FUNDS

58

ORDERING INSPECTIONS All construction draws are based on the percentage of work completed.

Inspection fees are $100.00 and will be deducted from the draw.

NOTE: Prior to receiving any advances on your construction loan you must first provide an original under construction or as built foundation location survey. Survey must be certified to USB, its successors and/or assigns, borrowers and title company.

• Inspections are ordered by the customer through the Kingston office only. Please allow at least five days for inspection scheduling.

• Inspector will fax or call in a percentage complete based on the inspection schedule for your property.

• We will contact you to inform you of the inspection results and the amount of the disbursement.

• A title update is then ordered by the bank from your title company. This is to determine whether any additional liens have been placed on the premises. This update must be satisfactory.

• Monthly interest payments must be current.• Title updates for Connecticut properties are not applicable. Lien

waivers from all applicable contractors must be submitted prior to each disbursement on Connecticut properties.

NOTE: Title companies may begin to charge after a set number of updates. Please be sure to check with your title company. Any title charges will be deducted from the draw.

DISBURSEMENTS OF FUNDSThe funds can be disbursed in any of the following ways:

• Bank check mailed to your current address.• Electronic wire transfer (USB charges $20 for each transfer).• Branch pickup: at any of our convenient locations in Kingston,

New Paltz, Poughkeepsie, Saugerties, Stone Ridge, Phoenicia, Gardiner, Red Hook, Wappinger Falls, Windham and Woodstock.

• Direct deposit into an Ulster Savings Bank account.• All checks are issued to all parties on the note. Any deviation from

this policy, on any given disbursement, must be submitted in writing to the construction loan department. The entire process may take up to 10 business days.

CONSTRUCTION LOAN DEPARTMENT

STICK BUILT ITEMIZED COST BREAKDOWNUse the itemized cost breakdown as a guide when meeting with your Builder or Sub-Contractor(s) to assist you in determining your total cost to build. You will need to support all costs with written estimates on contractors letterhead, or by a fully executed contract to build from a General Contractor.

1.2.3.4.5.6.7.8.9.10.11.12.13.14.15.1617.18.19.20.21.22.23.24.25.26.27.28.2930.

Excavation & Grading:Foundation:Septic or Municipal Hook up:Well or Municipal Hook up:Framing:Roofing:Windows & Exterior Doors:Garage Doors:Siding:Electric:Plumbing:HVAC:Insulation:Drywall Labor:Tape & Spackle:Interior Stairs & Railings:Fireplace & Chimneys:Kitchen Cabinetry & Counter Tops:Bathroom Vanities & Fixtures:Hardwood Floors:Tile Floors and/or Walls:Carpeting:Interior Painting:Exterior Painting:Interior Doors:Interior Trim:Decks, Steps, Porches, Patios, etc.Gutters & Leaders:Driveway:Other: _________________

$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________$ ___________________

Total: $ ___________________

94

CLOSINGS CONTINUED

SCHEDULING THE CONSTRUCTION CLOSINGBank attorneys must have the following prior to scheduling your closing:

• Title Report.• Survey (must be certified to Ulster Savings Bank, Its Successors

and/or Assigns, Borrowers and Title Company).• Builder Risk or Home Owners Policy (Policy must list Ulster Savings

Bank, Its Successors and/or Assigns, PO Box 3337, Kingston, NY 12402 as First Mortgage).

• Building Permit.

NOTE: At or following the construction closing you may begin to draw on construction funds provided all of the required documentation has been submitted to the bank. In order to receive an advance at closing for work that has already been completed, you must provide an under construction or as built foundation survey prior to closing. Under no circumstances can it be a proposed location or vacant land survey.

2. PERMANENT CLOSINGAt this closing the construction loan is converted into a permanent mortgage. Listed below are the closing costs that may be incurred at that time.

• Interest per diem (amount of interest due will vary depending on the day of the month you close)

• Settlement fee• Title review fee• Document preparation fee• Title insurance update fee• Recording fees• Appraisal fee (if necessary)• Credit report fee (if necessary)• Tax escrow deposit (if applicable)• Flood certification fee

SCHEDULING THE PERMANENT CLOSINGThe following will be required prior to scheduling:

• Permanent certificate of occupancy.• Certified survey showing house, driveway, well and septic, if applicable

(proposed subject under construction, or foundation survey not accecptable).• Conversion of builder’s risk policy to homeowner’s policy or renewal

of homeowner’s policy.• Update title insurance.• A final inspection showing 100% completion of all aspects of

the home in the appraisal report, based on the plans and specs submitted to the appraiser.

STICK BUILT DRAW DOWN SCHEDULE

10% 20% 3% 1% 2% 4% 3% 2% 4% 3% 4% 4% 3% 4% 2% 3% 3% 4% 3% 3% 3% 2% 3% 4% 1% 2%

Foundation complete.Frame is erected, roof underlayment and felt paper installed.Roof is complete.Rough grading complete.Exterior sheathing is installed.Windows and exterior doors installed “weather tight”.Siding and exterior trim completed and painted.Cellar floor installed.Septic tank and drain field installed or municipal sewage connected.Well drilled or municipal water connected.Rough heating completed.Rough plumbing completed.Rough electric completed.Insulation and drywall installed.Walls taped and final coat of spackle applied.Interior passage and closet doors installed.Interior trim completed.Kitchen cabinets and sink installed.Interior painting completed.Heating system completed.Bathroom fixtures installed.Plumbing completed and all systems operational.All electric completed.Floors completed.Final grading completed.All decks, steps and porches complete.

100% COMPLETE, including a satisfactory completion certificate with the inspection.

10 3

THE APPROVAL PROCESS CONTINUED

• Copies of most recent two years signed business returns including all schedules (if applicable).

• Copies of two months most recent consecutive bank statements for all checking and savings accounts.

• Copies of most recent quarterly statements for any retirement and/or investment accounts.

• Satisfactory appraisal.

NOTE: The design and appeal of the subject property must conform to market standards. Ulster Savings Bank reserves the right to approve/decline all projects following review of plans and specifications.

RESERVE REQUIREMENTSFull Income VerificationReserves equal to 10% of the construction costs are required of which 5% must be liquid.

No Income VerificationReserves equal to 20% of the construction costs are required of which 10% must be liquid.

CLOSINGS

Ulster Savings Bank Construction program consists of two closings:

1. CONSTRUCTION LOAN CLOSINGAt the time of this closing you will incur the following closing costs:• Bank points (if applicable)• Application fee (paid prior to closing)• Flood certification fee• Credit report fee• Appraisal fee (paid prior to closing)• Underwriting fee• Settlement fee• Title review fee• Document preparation fee• Title insurance (determined by county and mortgage amount)• Recording fee• Tax service fee• Mortgage tax (New York properties only, varies by county and loan

amount)

CONSTRUCTION LOAN DEPARTMENT CONTINUED

MODULAR BUILT ITEMIZED COST BREAKDOWN

Use this itemized cost breakdown as a guide when meeting with your Modular Builder and Sub-Contractor(s) to assist you in determining your total cost to build. You will need to support all costs with written estimates on contractors letterhead, or by a fully executed contract to build from a General Contractor.

1.2.3.4.5.6.7.8.9.10.11.12.13.14.15.1617.18.19.20.21.22.

Excavation & Grading:Foundation:Septic or Municipal Hook up:Well or Municipal Hook up:Modular Invoice amount:Siding:Electric:Plumbing:HVAC:Fireplace & Chimneys:Hardwood Floors:Tile Floors and/or Walls:Interior Trim:Interior Painting:Exterior Painting:Decks, Steps, Porches, Patios, etc.Gutters & Leaders:Driveway:Garage:Garage Doors:Other: _____________________Other: _____________________

$ _________________$ _________________$ _________________$ _________________$ _________________$ _________________$ _________________$ _________________$ _________________$ _________________$ _________________$ _________________$ _________________$ _________________$ _________________$ _________________$ _________________$ _________________$ _________________$ _________________$ _________________$ _________________

Total: $ _________________

112

MODULAR BUILT ITEMIZED COST BREAKDOWN

10% 2% 2% 65%

21%

Foundation completeCellar floor installedRough grading complete

Balance of manufacturer’s invoice due on delivery not to exceed 65% of the loan amount. If any of the 65% of the loan amount is available after paying the balance due on the invoice upon delivery, it will be disbursed after the unit has been set on the foundation

For the following items completed at the time of inspection:2% Roof, exterior siding and trim complete3% Water supply connected3% Sewer system complete2% Heating complete2% Plumbing complete2% Electric complete2% Interior trim complete1% Interior painting complete1% Floors complete1% Final grading complete2% Decks, steps and porches complete

100% COMPLETE, including a satisfactory completion certificate with the inspection.

CONSTRUCTION/PERMANENT MORTGAGE PROGRAM CONTINUED

Rehabilitation – RefinanceMaximum LTV will be 75% of the “as is” value plus the cost of improvements limited to 80% of the “as completed” value.

NOTE: “Sweat equity” is not permitted.

LAND REQUIREMENTS• Value attributed to land owned for less than one year is determined

by the lesser of the actual price paid or the current appraised value.• Value attributed to land owned for more than one year will be

determined by the appraisal.• Gifts of land are acceptable and the value will be determined by the

appraisal.• Any land liens must be satisfied at construction closing.

MORTGAGE INSURANCEMortgage insurance is required for LTVs greater than 80%.Insurance is obtained at construction. Premiums are collected at the time of the permanent closing.

THE APPROVAL PROCESS

GENERAL REQUIRED ITEMS• Copy of settlement statement from land purchase (if previously

acquired).• Copy of recorded deed.• Copies of bank statements or canceled checks showing source of

funds used to purchase land.• Copy of contract to purchase land.• Copies of all estimates, contracts, and paid receipts for all work

necessary to complete construction.• Copy of plans & specs for the home to be constructed.• Copies of most recent two years W-2’s.• Copies of most recent year to date pay stubs documenting one full

month earnings.• Copy of most recent two years signed personal tax returns including

all schedules (self-employed borrowers only).

________________________________________________________________

________________________________________________________________

________________________________________________________________

________________________________________________________________

________________________________________________________________

________________________________________________________________

________________________________________________________________

________________________________________________________________

________________________________________________________________

________________________________________________________________

________________________________________________________________

________________________________________________________________

________________________________________________________________

________________________________________________________________

________________________________________________________________

________________________________________________________________

________________________________________________________________

________________________________________________________________

________________________________________________________________

________________________________________________________________

________________________________________________________________

________________________________________________________________

NOTES

13

You’ve got US!

Dream It. FInance It. BuIlD It.

Construction loans designed to

your specifications

Banking • Loans • Investments • Tax & Payroll • Insurance

You’ve got US!

BR-M-721 9/09

Investment, Tax, Payroll and Insurance products and services available through Ulster Insurance Services, Inc. and Ulster Financial Group, Inc., subsidiaries of Ulster Savings

Bank, are NOT FDIC INSURED.

Member FDIC

Customer Service Center (866) 440-0391www.ulstersavings.com