Draft Regulatory Impact Statement - ntc.gov.auF71E0D6C-96B1-7379-D72F-4F... · National Transport...

170

2014 Heavy Vehicle Charges Determination Draft Regulatory Impact Statement November 2013

Transcript of Draft Regulatory Impact Statement - ntc.gov.auF71E0D6C-96B1-7379-D72F-4F... · National Transport...

2014 Heavy Vehicle Charges Determination Draft Regulatory Impact Statement

November 2013

National Transport Commission

2014 Heavy Vehicle Charges Determination – Draft regulatory Impact statement

Report prepared by: National Transport Commission

ISBN:

Heavy vehicle charges determination – RIS February 2014 i

Report outline Title: Heavy Vehicle Charges Determination

Type of report: Regulatory Impact Statement

Purpose: For SCOTI noting

Abstract: This document presents the results of a comprehensive review of heavy vehicle charges the National Transport Commission (NTC) conducted in 2012 and 2013 in collaboration with a broad range of stakeholders, including industry representatives and the Australian, state and territory government. The NTC has identified several areas within the current charging framework that required further analysis. Where appropriate, the NTC recommends changes to address as many of the issues identified in the Heavy Vehicles Charges Review and improve the current charging framework. This Heavy Vehicle Charges Determination is the second step of a two-stage process, which was endorsed by ministers in November 2012. The determination aims at implementing new charges from 1 July 2014.

Key milestones: Public consultation: 25 November 2013 to 17 January 2014 SCOTI voting: February 2014

Key words: Heavy vehicles charges, PAYGO, determination, consultation, NTC, HVCI, NHVR, cost recovery, cost base, A-trailer, road expenditure, arterial roads, local roads, cost allocation matrix, pricing principles, usage data, annual adjustment, expenditure template, expenditure accountability, structure of charges, standard axle charge, axle grouping charge, pavement wear, equivalent standard axle, ESA, indexation, averaging, attributable costs, non-attributable costs, common costs, modularity, rebates, concessions, SMVU, road user charge, registration, weigh-in-motion, equity, economic efficiency.

Contact: National Transport Commission L15/628 Bourke Street MELBOURNE VIC 3000 (03) 9235 5000 or [email protected] www.ntc.gov.au

Heavy vehicle charges determination – RIS February 2014 ii

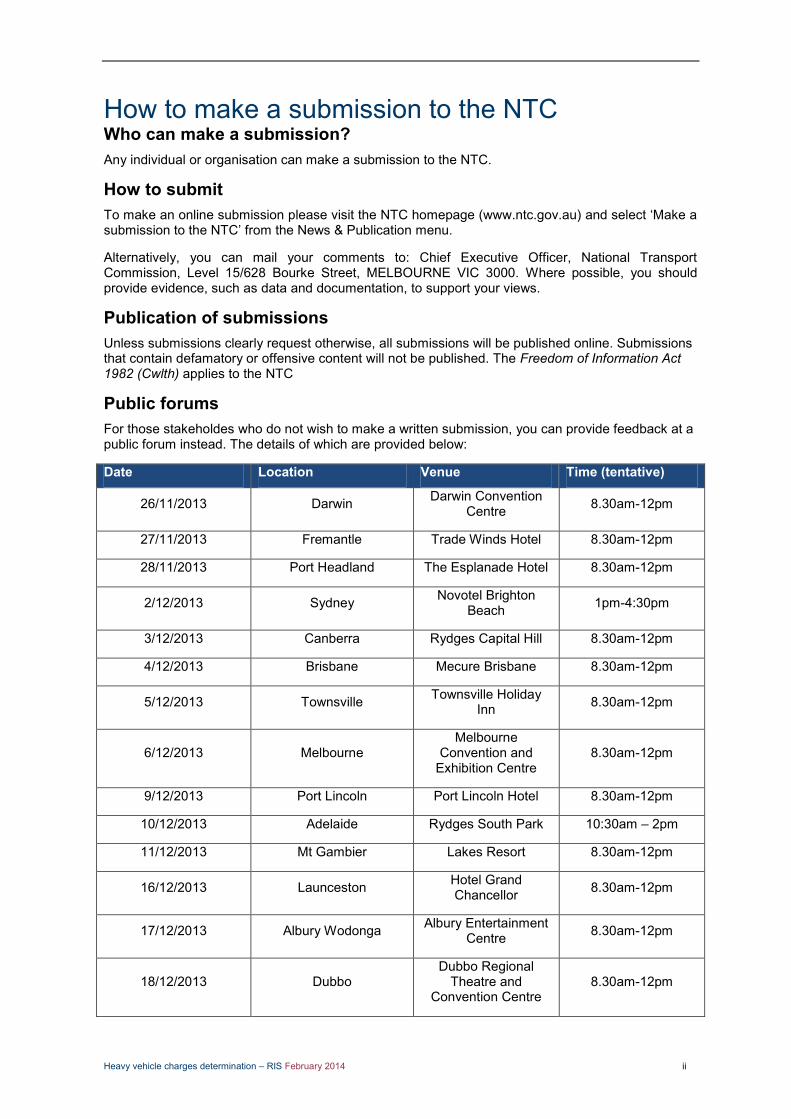

How to make a submission to the NTC Who can make a submission? Any individual or organisation can make a submission to the NTC.

How to submit To make an online submission please visit the NTC homepage (www.ntc.gov.au) and select ‘Make a submission to the NTC’ from the News & Publication menu.

Alternatively, you can mail your comments to: Chief Executive Officer, National Transport Commission, Level 15/628 Bourke Street, MELBOURNE VIC 3000. Where possible, you should provide evidence, such as data and documentation, to support your views.

Publication of submissions Unless submissions clearly request otherwise, all submissions will be published online. Submissions that contain defamatory or offensive content will not be published. The Freedom of Information Act 1982 (Cwlth) applies to the NTC

Public forums For those stakeholdes who do not wish to make a written submission, you can provide feedback at a public forum instead. The details of which are provided below:

Date Location Venue Time (tentative)

26/11/2013 Darwin Darwin Convention Centre 8.30am-12pm

27/11/2013 Fremantle Trade Winds Hotel 8.30am-12pm

28/11/2013 Port Headland The Esplanade Hotel 8.30am-12pm

2/12/2013 Sydney Novotel Brighton Beach 1pm-4:30pm

3/12/2013 Canberra Rydges Capital Hill 8.30am-12pm

4/12/2013 Brisbane Mecure Brisbane 8.30am-12pm

5/12/2013 Townsville Townsville Holiday Inn 8.30am-12pm

6/12/2013 Melbourne Melbourne

Convention and Exhibition Centre

8.30am-12pm

9/12/2013 Port Lincoln Port Lincoln Hotel 8.30am-12pm

10/12/2013 Adelaide Rydges South Park 10:30am – 2pm

11/12/2013 Mt Gambier Lakes Resort 8.30am-12pm

16/12/2013 Launceston Hotel Grand Chancellor 8.30am-12pm

17/12/2013 Albury Wodonga Albury Entertainment Centre 8.30am-12pm

18/12/2013 Dubbo Dubbo Regional

Theatre and Convention Centre

8.30am-12pm

Heavy vehicle charges determination – RIS February 2014 iii

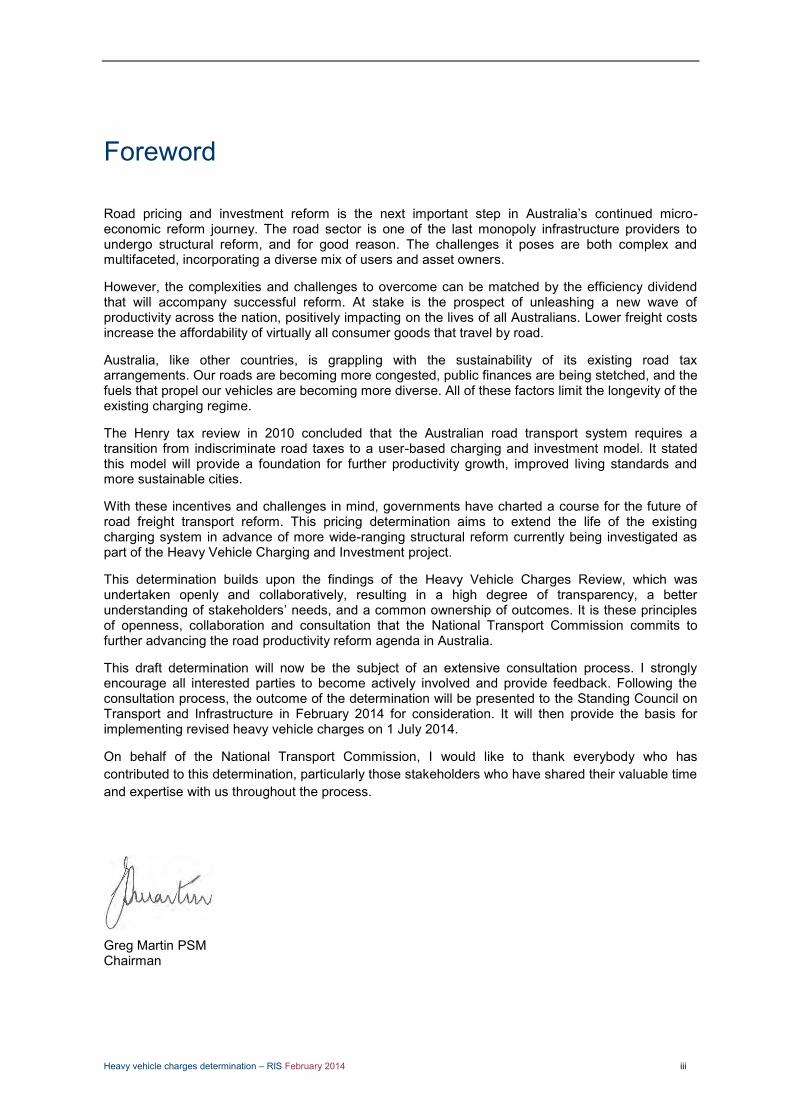

Foreword

Road pricing and investment reform is the next important step in Australia’s continued micro-economic reform journey. The road sector is one of the last monopoly infrastructure providers to undergo structural reform, and for good reason. The challenges it poses are both complex and multifaceted, incorporating a diverse mix of users and asset owners.

However, the complexities and challenges to overcome can be matched by the efficiency dividend that will accompany successful reform. At stake is the prospect of unleashing a new wave of productivity across the nation, positively impacting on the lives of all Australians. Lower freight costs increase the affordability of virtually all consumer goods that travel by road.

Australia, like other countries, is grappling with the sustainability of its existing road tax arrangements. Our roads are becoming more congested, public finances are being stetched, and the fuels that propel our vehicles are becoming more diverse. All of these factors limit the longevity of the existing charging regime.

The Henry tax review in 2010 concluded that the Australian road transport system requires a transition from indiscriminate road taxes to a user-based charging and investment model. It stated this model will provide a foundation for further productivity growth, improved living standards and more sustainable cities.

With these incentives and challenges in mind, governments have charted a course for the future of road freight transport reform. This pricing determination aims to extend the life of the existing charging system in advance of more wide-ranging structural reform currently being investigated as part of the Heavy Vehicle Charging and Investment project.

This determination builds upon the findings of the Heavy Vehicle Charges Review, which was undertaken openly and collaboratively, resulting in a high degree of transparency, a better understanding of stakeholders’ needs, and a common ownership of outcomes. It is these principles of openness, collaboration and consultation that the National Transport Commission commits to further advancing the road productivity reform agenda in Australia.

This draft determination will now be the subject of an extensive consultation process. I strongly encourage all interested parties to become actively involved and provide feedback. Following the consultation process, the outcome of the determination will be presented to the Standing Council on Transport and Infrastructure in February 2014 for consideration. It will then provide the basis for implementing revised heavy vehicle charges on 1 July 2014.

On behalf of the National Transport Commission, I would like to thank everybody who has contributed to this determination, particularly those stakeholders who have shared their valuable time and expertise with us throughout the process.

Greg Martin PSM Chairman

Heavy vehicle charges determination – RIS February 2014 iv

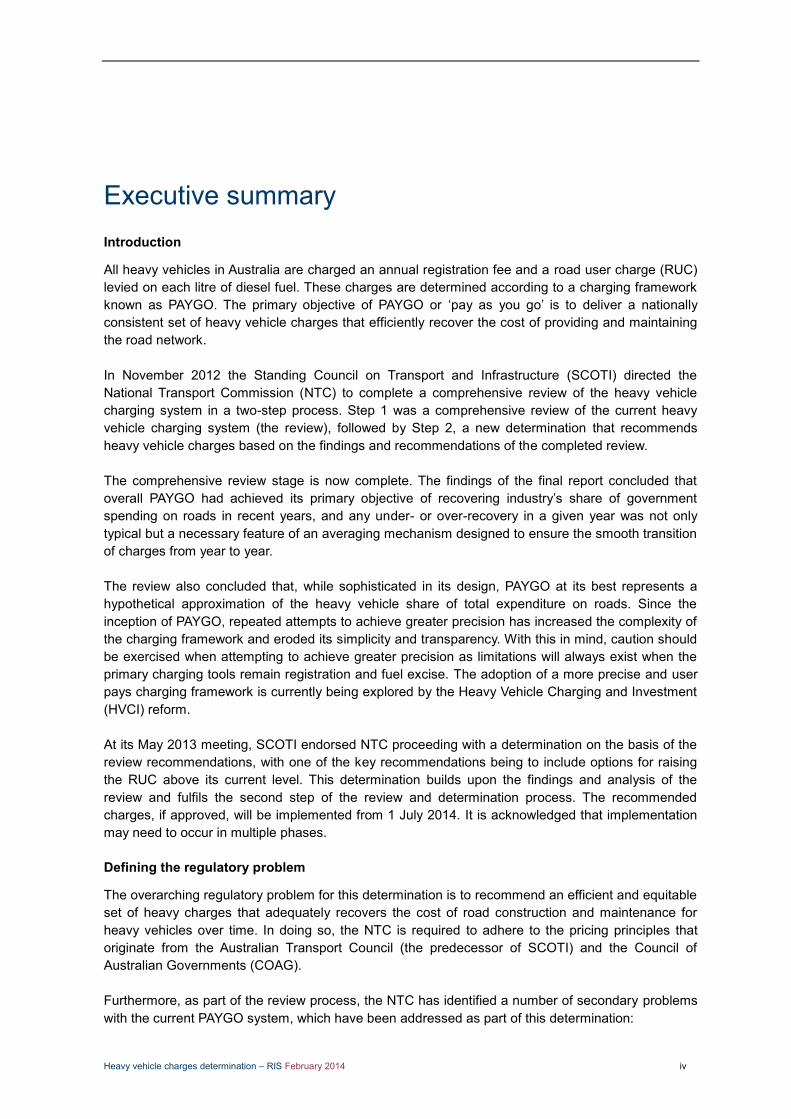

Executive summary Introduction

All heavy vehicles in Australia are charged an annual registration fee and a road user charge (RUC) levied on each litre of diesel fuel. These charges are determined according to a charging framework known as PAYGO. The primary objective of PAYGO or ‘pay as you go’ is to deliver a nationally consistent set of heavy vehicle charges that efficiently recover the cost of providing and maintaining the road network. In November 2012 the Standing Council on Transport and Infrastructure (SCOTI) directed the National Transport Commission (NTC) to complete a comprehensive review of the heavy vehicle charging system in a two-step process. Step 1 was a comprehensive review of the current heavy vehicle charging system (the review), followed by Step 2, a new determination that recommends heavy vehicle charges based on the findings and recommendations of the completed review. The comprehensive review stage is now complete. The findings of the final report concluded that overall PAYGO had achieved its primary objective of recovering industry’s share of government spending on roads in recent years, and any under- or over-recovery in a given year was not only typical but a necessary feature of an averaging mechanism designed to ensure the smooth transition of charges from year to year. The review also concluded that, while sophisticated in its design, PAYGO at its best represents a hypothetical approximation of the heavy vehicle share of total expenditure on roads. Since the inception of PAYGO, repeated attempts to achieve greater precision has increased the complexity of the charging framework and eroded its simplicity and transparency. With this in mind, caution should be exercised when attempting to achieve greater precision as limitations will always exist when the primary charging tools remain registration and fuel excise. The adoption of a more precise and user pays charging framework is currently being explored by the Heavy Vehicle Charging and Investment (HVCI) reform. At its May 2013 meeting, SCOTI endorsed NTC proceeding with a determination on the basis of the review recommendations, with one of the key recommendations being to include options for raising the RUC above its current level. This determination builds upon the findings and analysis of the review and fulfils the second step of the review and determination process. The recommended charges, if approved, will be implemented from 1 July 2014. It is acknowledged that implementation may need to occur in multiple phases. Defining the regulatory problem

The overarching regulatory problem for this determination is to recommend an efficient and equitable set of heavy charges that adequately recovers the cost of road construction and maintenance for heavy vehicles over time. In doing so, the NTC is required to adhere to the pricing principles that originate from the Australian Transport Council (the predecessor of SCOTI) and the Council of Australian Governments (COAG). Furthermore, as part of the review process, the NTC has identified a number of secondary problems with the current PAYGO system, which have been addressed as part of this determination:

Heavy vehicle charges determination – RIS February 2014 v

how best to calculate the cost base ensuring ongoing cost recovery how to produce a consistent set of usage data how to ensure accurate and consistent reporting of expenditure data, and increase the

accountability of jurisdictional cost submissions what the most efficient and equitable structure of heavy vehicle charges is in terms of axle

grouping charging and split between RUC and registration how to improve the methodology for calculating pavement wear impacts of different vehicle

classes how to appropriately adjust heavy vehicle charges from one year to the next what the most appropriate approach to concessions and rebates is what the most appropriate mechanism for recovering NHVR costs in accordance with the

NHVR intergovernmental agreement is.

The options and implementation

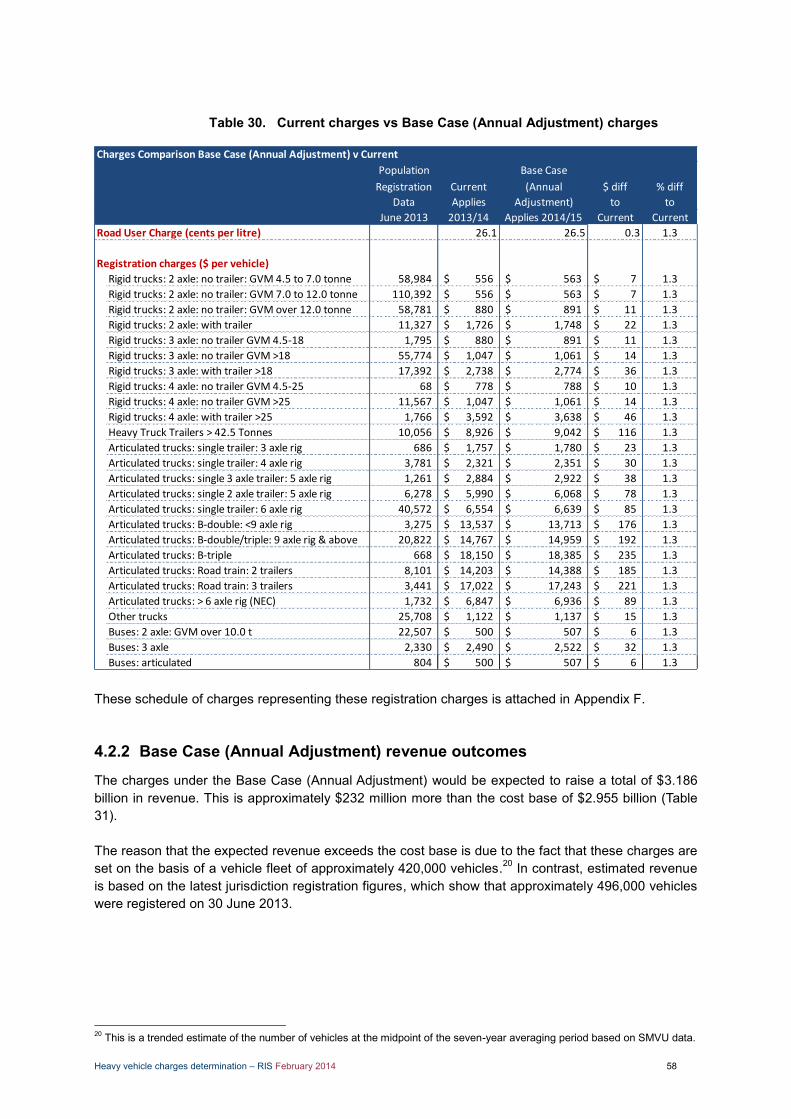

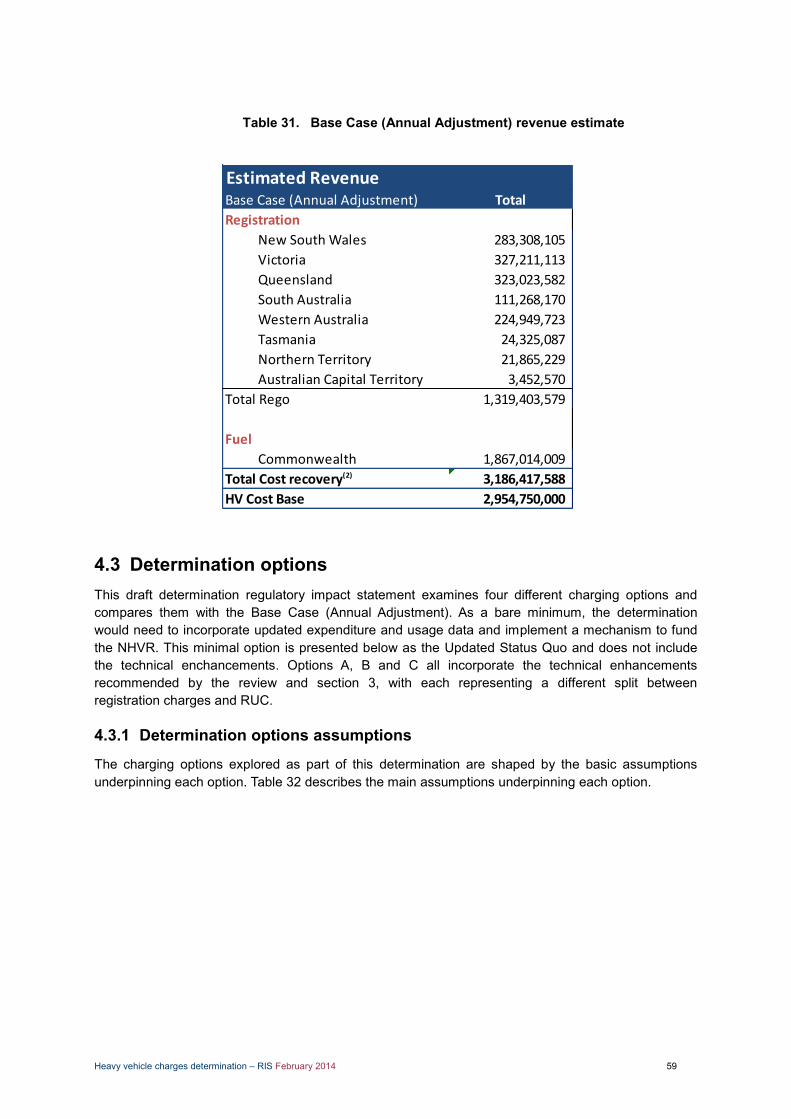

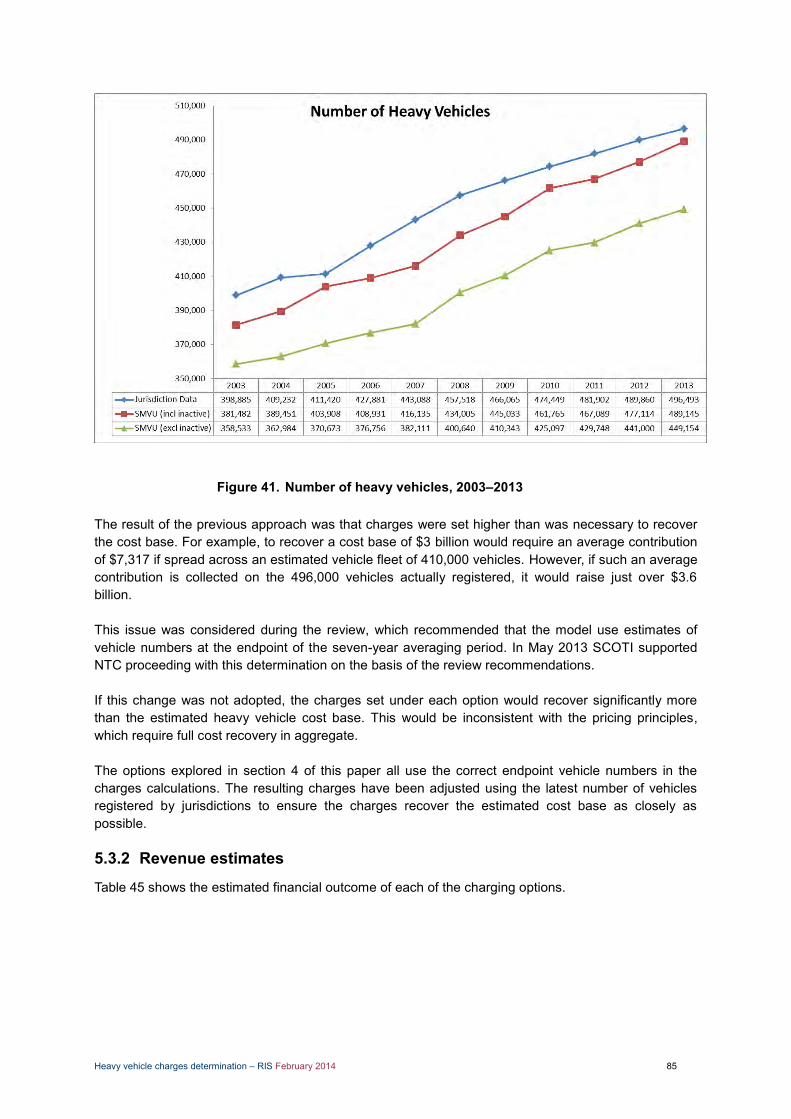

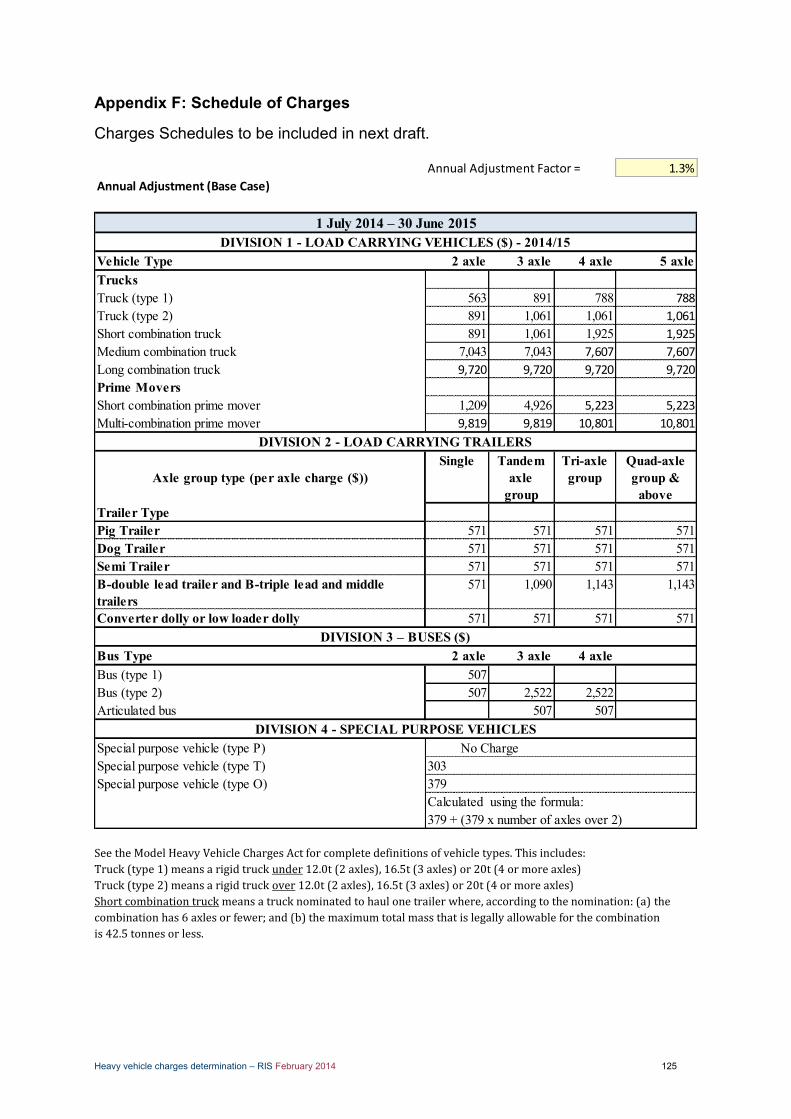

This determination presents a range of charges options which can then be compared to the counterfactual. The Base Case (Annual Adjustment) represents the charges that would be in place if there were no determination, and an annual adjustment were made to the current charges as required by legislation. The annual adjustment increases current charges to ensure that overall cost recovery keeps pace with changes in road expenditure and vehicle usage. Under the Base Case, registration charges are set on the basis of an estimate of vehicle numbers at 420,246 using data from the Survey of Motor Vehicle Use.

The four alternative charging options considered in the RIS are described below, all of which incorporate the recovery of NHVR costs.

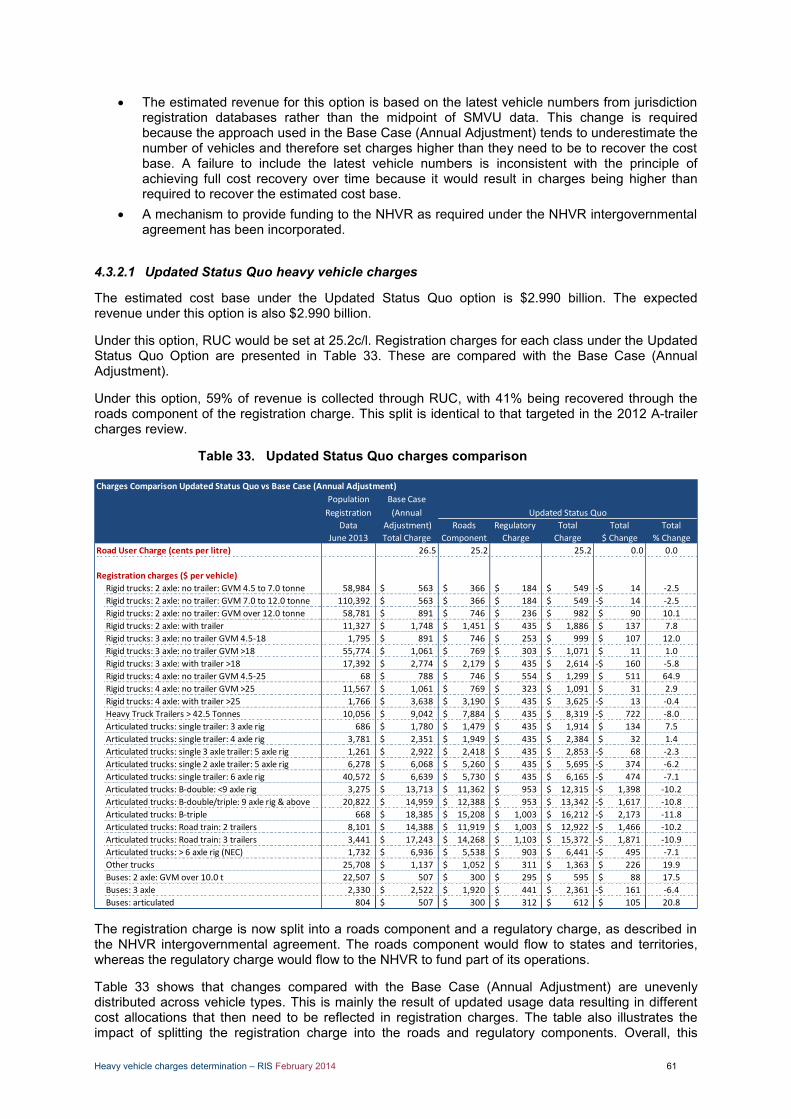

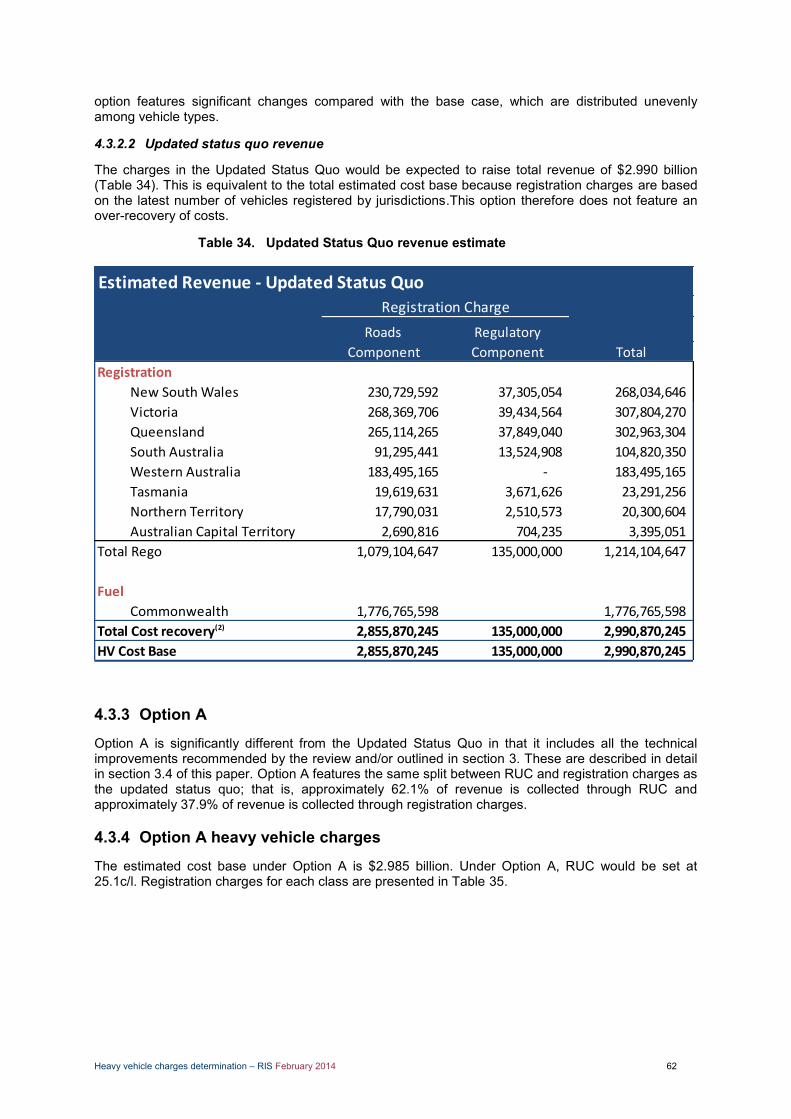

The option described as Updated Status Quo represents the minimal change that would need to be undertaken in any determination. This involves using the charges methodology underpinning the current charges with updated road expenditure and vehicle usage data. In addition, this option uses the most recent vehicle numbers from jurisdiction registration databases to estimate registration revenue.

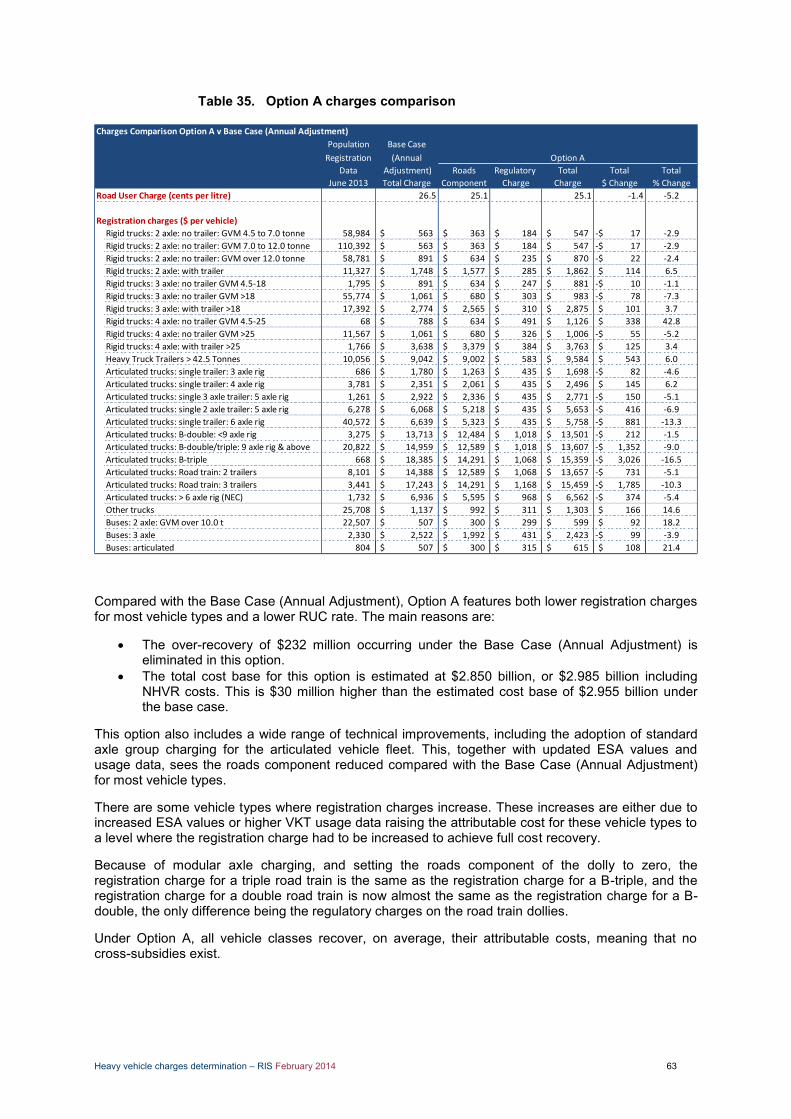

Option A incorporates a range of technical improvements resulting from the Review and further work undertaken since then while maintaining the current split in revenue raised through RUC and registration charges.

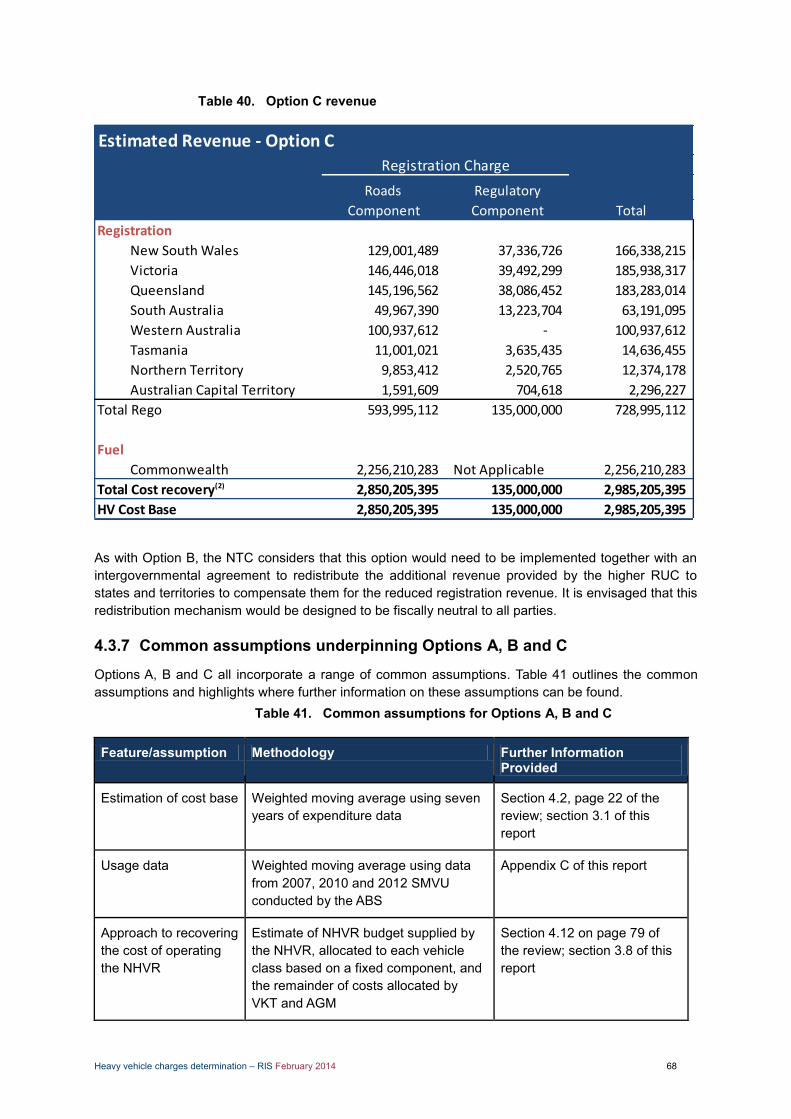

Options B and C include the same technical improvements as Option A, but recover a higher proportion of revenue through RUC than is currently the case. Option B represents a moderate shift whereas Option C represents the most significant shift that could reasonably be accommodated while leaving room for future annual adjustments.

The technical improvements included in Option A, Option B and Option C include all technical improvements recommended by the Review, such as ESA refinement, modular axle charging, and change of cost measurement.

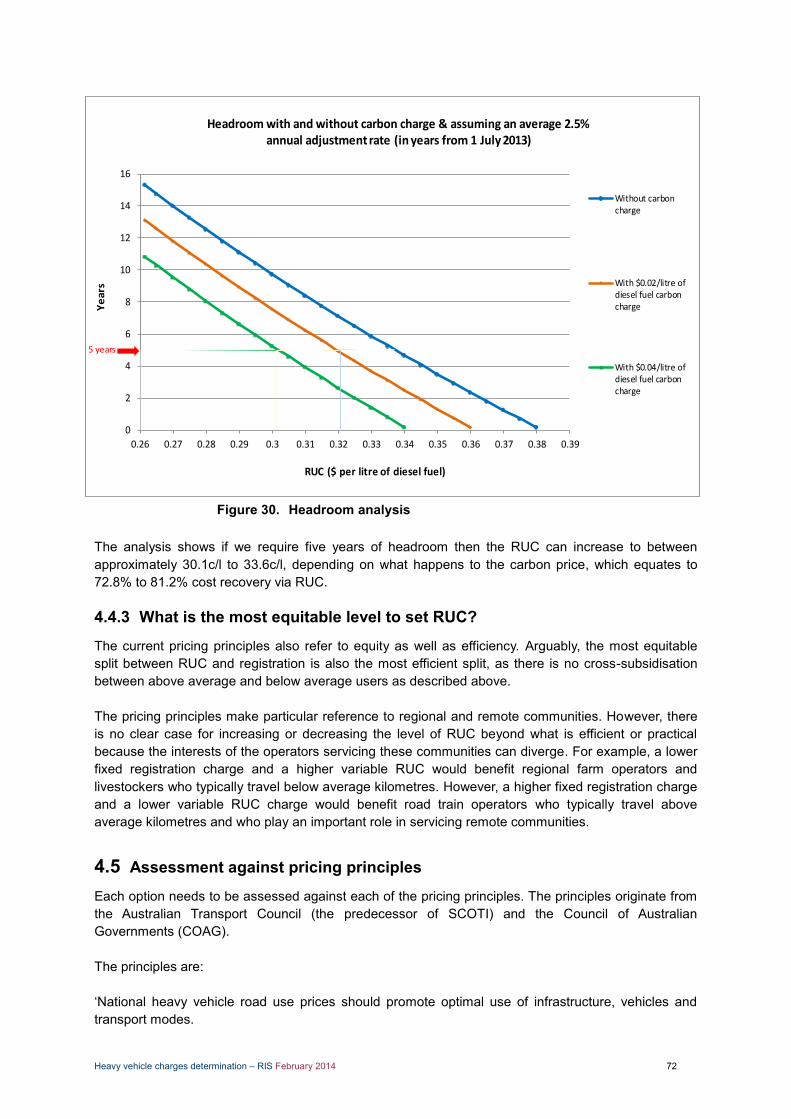

The NTC found there was a strong efficiency argument for increasing the RUC to approximately 72%, which closely aligns with Option B. The option advocates approximately 72% recovery via RUC. When examining the practicalities of a higher variable charge and in particular avoiding the 38.1c/l excise cap, there did appear to be sufficient headroom to go beyond 72%; that is, there was adequate room to accommodate future annual adjustment increases without breaching the cap.

After considering the equity issues involved with setting the RUC, there appears to be no compelling case to either increase or decrease the level of RUC beyond what is determined to be efficient or practical.

Based on the analysis presented in this determination, there is a strong efficiency argument for Option B. However, Option A creates the least change in terms of revenue impacts to the jurisdicitons and Commonwealth and could be implemented more quicly than either option B or C. Option C goes the furthest in terms of changes to the split in revenue through RUC and registration

Heavy vehicle charges determination – RIS February 2014 vi

charges, and like option B, it would require an inter-governmental agreement to re-distribute the additional revenue raised through RUC to states and territories.

In terms of implementation pathways, the time that would be required to negotiate and implement a revenue-redistribution agreement suggests that a phased implementation path may be appropriate if Option B or C were to be adopted. For example, If Option B was selected as the preferred option, the following two-phase approach could be adopted for implementation:

Phase 1 – Option A (effective 1 July 2014) (see table 1); and Phase 2 – Option B (future date to be determined) (see table 2).

Heavy vehicle charges determination – RIS February 2014 vii

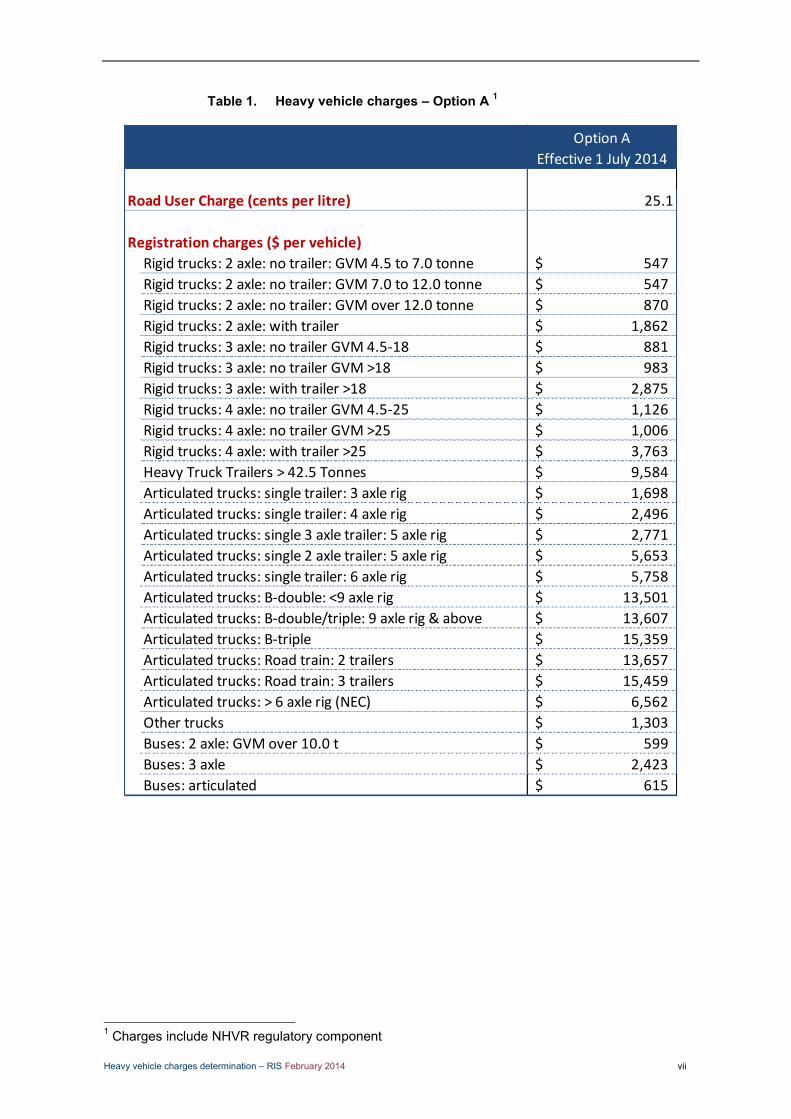

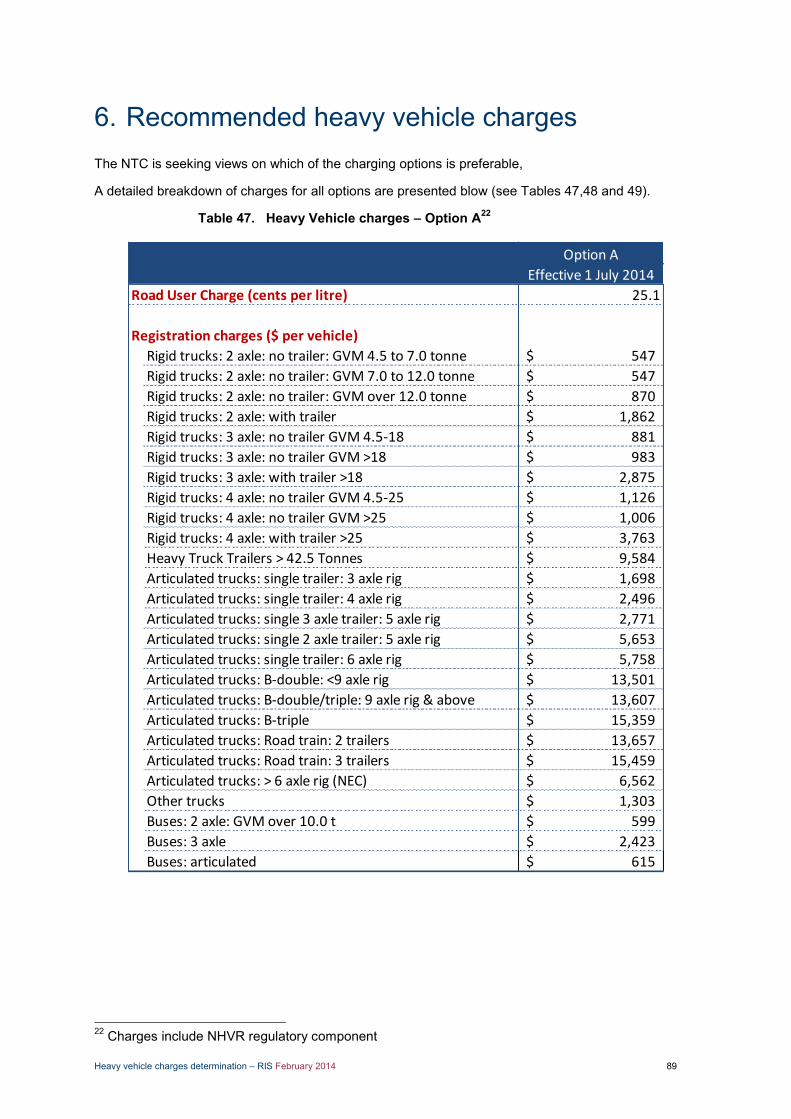

Heavy vehicle charges – Option A 1 Table 1.

1 Charges include NHVR regulatory component

Option A

Effective 1 July 2014

Road User Charge (cents per litre) 25.1

Registration charges ($ per vehicle)

Rigid trucks: 2 axle: no trailer: GVM 4.5 to 7.0 tonne 547$

Rigid trucks: 2 axle: no trailer: GVM 7.0 to 12.0 tonne 547$

Rigid trucks: 2 axle: no trailer: GVM over 12.0 tonne 870$

Rigid trucks: 2 axle: with trailer 1,862$

Rigid trucks: 3 axle: no trailer GVM 4.5-18 881$

Rigid trucks: 3 axle: no trailer GVM >18 983$

Rigid trucks: 3 axle: with trailer >18 2,875$

Rigid trucks: 4 axle: no trailer GVM 4.5-25 1,126$

Rigid trucks: 4 axle: no trailer GVM >25 1,006$

Rigid trucks: 4 axle: with trailer >25 3,763$

Heavy Truck Trailers > 42.5 Tonnes 9,584$

Articulated trucks: single trailer: 3 axle rig 1,698$

Articulated trucks: single trailer: 4 axle rig 2,496$

Articulated trucks: single 3 axle trailer: 5 axle rig 2,771$

Articulated trucks: single 2 axle trailer: 5 axle rig 5,653$

Articulated trucks: single trailer: 6 axle rig 5,758$

Articulated trucks: B-double: <9 axle rig 13,501$

Articulated trucks: B-double/triple: 9 axle rig & above 13,607$

Articulated trucks: B-triple 15,359$

Articulated trucks: Road train: 2 trailers 13,657$

Articulated trucks: Road train: 3 trailers 15,459$

Articulated trucks: > 6 axle rig (NEC) 6,562$

Other trucks 1,303$

Buses: 2 axle: GVM over 10.0 t 599$

Buses: 3 axle 2,423$

Buses: articulated 615$

Heavy vehicle charges determination – RIS February 2014 viii

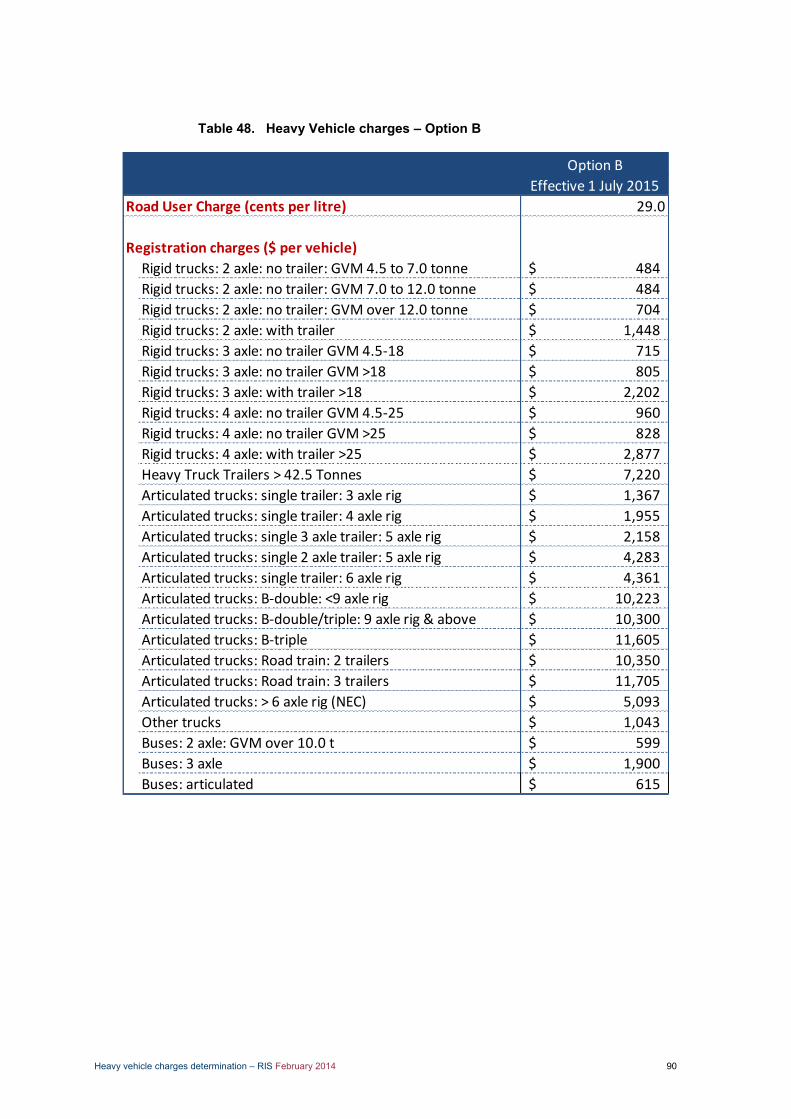

Heavy vehicle charges – Option B 2 Table 2.

2 Charges include NHVR regulatory component

Option B

Effective 1 July 2015

Road User Charge (cents per litre) 29.0

Registration charges ($ per vehicle)

Rigid trucks: 2 axle: no trailer: GVM 4.5 to 7.0 tonne 484$

Rigid trucks: 2 axle: no trailer: GVM 7.0 to 12.0 tonne 484$

Rigid trucks: 2 axle: no trailer: GVM over 12.0 tonne 704$

Rigid trucks: 2 axle: with trailer 1,448$

Rigid trucks: 3 axle: no trailer GVM 4.5-18 715$

Rigid trucks: 3 axle: no trailer GVM >18 805$

Rigid trucks: 3 axle: with trailer >18 2,202$

Rigid trucks: 4 axle: no trailer GVM 4.5-25 960$

Rigid trucks: 4 axle: no trailer GVM >25 828$

Rigid trucks: 4 axle: with trailer >25 2,877$

Heavy Truck Trailers > 42.5 Tonnes 7,220$

Articulated trucks: single trailer: 3 axle rig 1,367$

Articulated trucks: single trailer: 4 axle rig 1,955$

Articulated trucks: single 3 axle trailer: 5 axle rig 2,158$

Articulated trucks: single 2 axle trailer: 5 axle rig 4,283$

Articulated trucks: single trailer: 6 axle rig 4,361$

Articulated trucks: B-double: <9 axle rig 10,223$

Articulated trucks: B-double/triple: 9 axle rig & above 10,300$

Articulated trucks: B-triple 11,605$

Articulated trucks: Road train: 2 trailers 10,350$

Articulated trucks: Road train: 3 trailers 11,705$

Articulated trucks: > 6 axle rig (NEC) 5,093$

Other trucks 1,043$

Buses: 2 axle: GVM over 10.0 t 599$

Buses: 3 axle 1,900$

Buses: articulated 615$

Heavy vehicle charges determination – RIS February 2014 ix

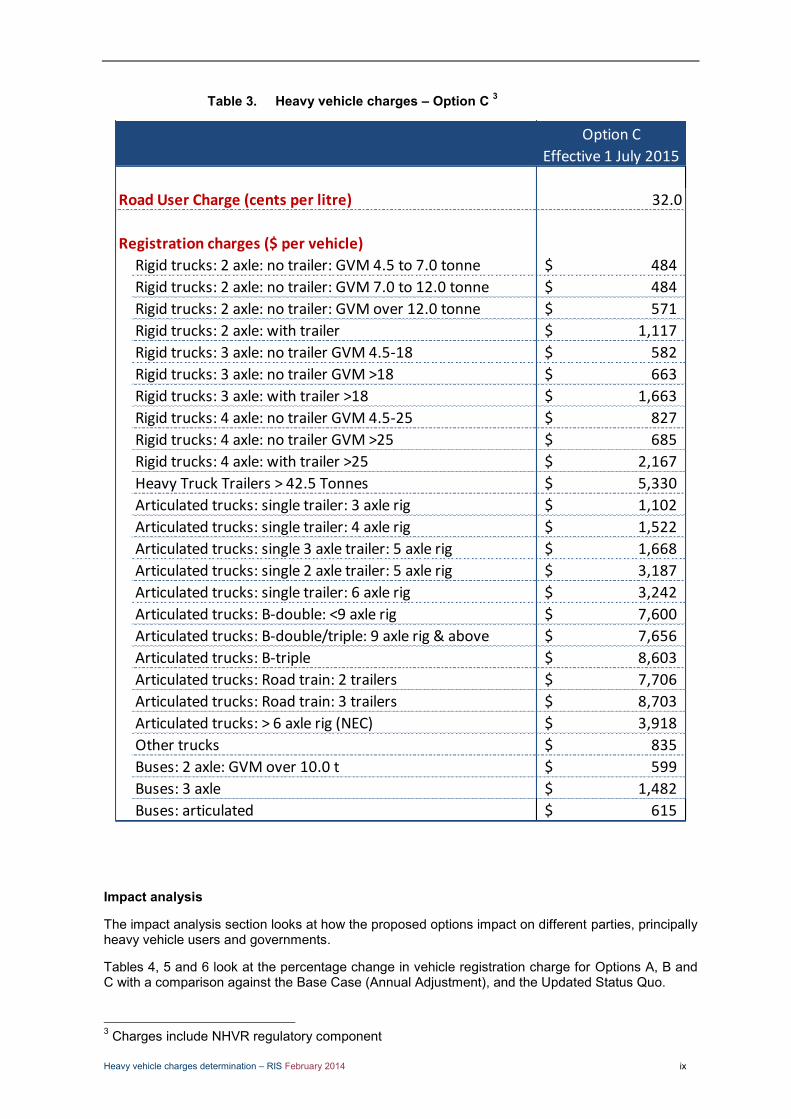

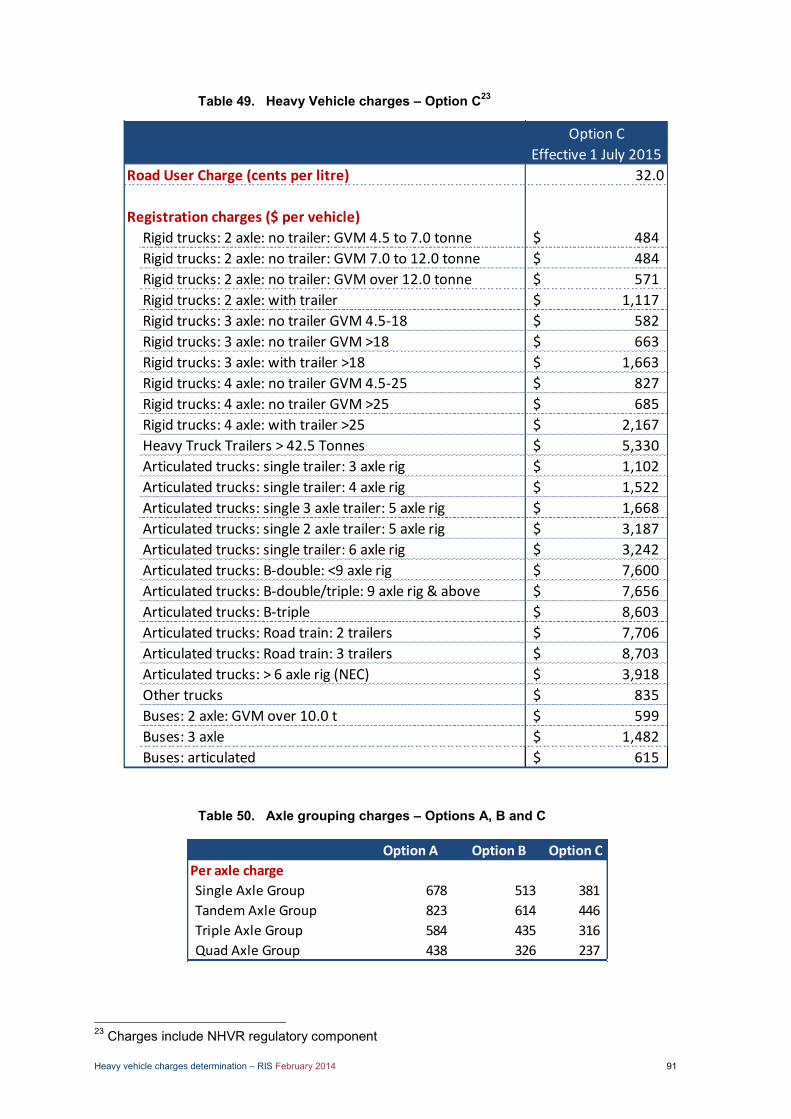

Heavy vehicle charges – Option C 3 Table 3.

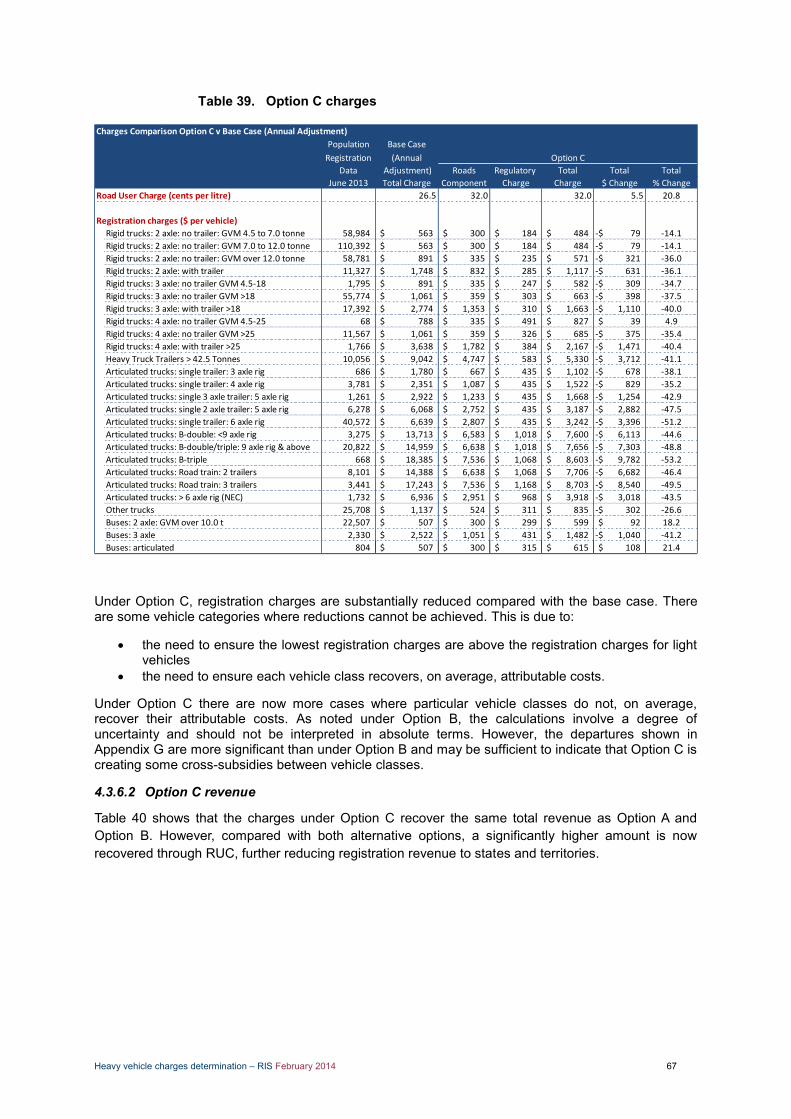

Impact analysis

The impact analysis section looks at how the proposed options impact on different parties, principally heavy vehicle users and governments.

Tables 4, 5 and 6 look at the percentage change in vehicle registration charge for Options A, B and C with a comparison against the Base Case (Annual Adjustment), and the Updated Status Quo.

3 Charges include NHVR regulatory component

Option C

Effective 1 July 2015

Road User Charge (cents per litre) 32.0

Registration charges ($ per vehicle)

Rigid trucks: 2 axle: no trailer: GVM 4.5 to 7.0 tonne 484$

Rigid trucks: 2 axle: no trailer: GVM 7.0 to 12.0 tonne 484$

Rigid trucks: 2 axle: no trailer: GVM over 12.0 tonne 571$

Rigid trucks: 2 axle: with trailer 1,117$

Rigid trucks: 3 axle: no trailer GVM 4.5-18 582$

Rigid trucks: 3 axle: no trailer GVM >18 663$

Rigid trucks: 3 axle: with trailer >18 1,663$

Rigid trucks: 4 axle: no trailer GVM 4.5-25 827$

Rigid trucks: 4 axle: no trailer GVM >25 685$

Rigid trucks: 4 axle: with trailer >25 2,167$

Heavy Truck Trailers > 42.5 Tonnes 5,330$

Articulated trucks: single trailer: 3 axle rig 1,102$

Articulated trucks: single trailer: 4 axle rig 1,522$

Articulated trucks: single 3 axle trailer: 5 axle rig 1,668$

Articulated trucks: single 2 axle trailer: 5 axle rig 3,187$

Articulated trucks: single trailer: 6 axle rig 3,242$

Articulated trucks: B-double: <9 axle rig 7,600$

Articulated trucks: B-double/triple: 9 axle rig & above 7,656$

Articulated trucks: B-triple 8,603$

Articulated trucks: Road train: 2 trailers 7,706$

Articulated trucks: Road train: 3 trailers 8,703$

Articulated trucks: > 6 axle rig (NEC) 3,918$

Other trucks 835$

Buses: 2 axle: GVM over 10.0 t 599$

Buses: 3 axle 1,482$

Buses: articulated 615$

Heavy vehicle charges determination – RIS February 2014 x

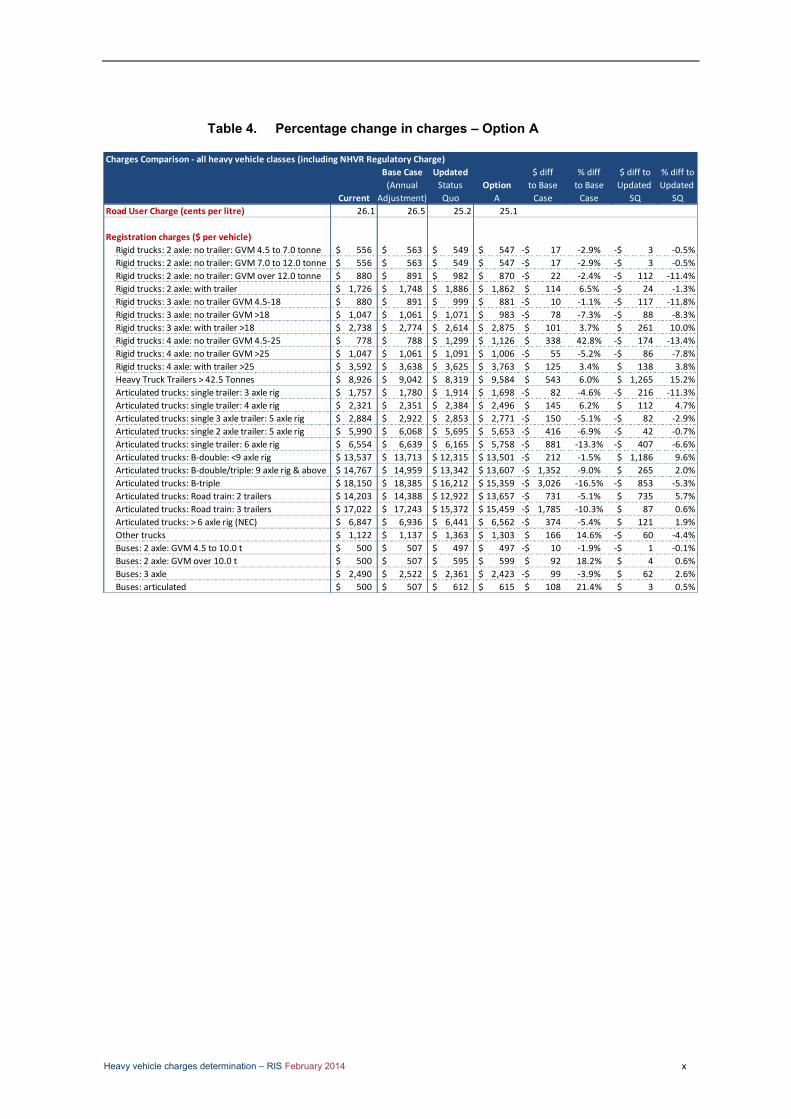

Percentage change in charges – Option A Table 4.

Charges Comparison - all heavy vehicle classes (including NHVR Regulatory Charge)

Base Case Updated $ diff % diff $ diff to % diff to

(Annual Status Option to Base to Base Updated Updated

Current Adjustment) Quo A Case Case SQ SQ

Road User Charge (cents per litre) 26.1 26.5 25.2 25.1

Registration charges ($ per vehicle)

1 Rigid trucks: 2 axle: no trailer: GVM 4.5 to 7.0 tonne 556$ 563$ 549$ 547$ 17-$ -2.9% 3-$ -0.5%

2 Rigid trucks: 2 axle: no trailer: GVM 7.0 to 12.0 tonne 556$ 563$ 549$ 547$ 17-$ -2.9% 3-$ -0.5%

3 Rigid trucks: 2 axle: no trailer: GVM over 12.0 tonne 880$ 891$ 982$ 870$ 22-$ -2.4% 112-$ -11.4%

4 Rigid trucks: 2 axle: with trailer 1,726$ 1,748$ 1,886$ 1,862$ 114$ 6.5% 24-$ -1.3%

5 Rigid trucks: 3 axle: no trailer GVM 4.5-18 880$ 891$ 999$ 881$ 10-$ -1.1% 117-$ -11.8%

6 Rigid trucks: 3 axle: no trailer GVM >18 1,047$ 1,061$ 1,071$ 983$ 78-$ -7.3% 88-$ -8.3%

7 Rigid trucks: 3 axle: with trailer >18 2,738$ 2,774$ 2,614$ 2,875$ 101$ 3.7% 261$ 10.0%

8 Rigid trucks: 4 axle: no trailer GVM 4.5-25 778$ 788$ 1,299$ 1,126$ 338$ 42.8% 174-$ -13.4%

9 Rigid trucks: 4 axle: no trailer GVM >25 1,047$ 1,061$ 1,091$ 1,006$ 55-$ -5.2% 86-$ -7.8%

# Rigid trucks: 4 axle: with trailer >25 3,592$ 3,638$ 3,625$ 3,763$ 125$ 3.4% 138$ 3.8%

# Heavy Truck Trailers > 42.5 Tonnes 8,926$ 9,042$ 8,319$ 9,584$ 543$ 6.0% 1,265$ 15.2%

# Articulated trucks: single trailer: 3 axle rig 1,757$ 1,780$ 1,914$ 1,698$ 82-$ -4.6% 216-$ -11.3%

# Articulated trucks: single trailer: 4 axle rig 2,321$ 2,351$ 2,384$ 2,496$ 145$ 6.2% 112$ 4.7%

# Articulated trucks: single 3 axle trailer: 5 axle rig 2,884$ 2,922$ 2,853$ 2,771$ 150-$ -5.1% 82-$ -2.9%

# Articulated trucks: single 2 axle trailer: 5 axle rig 5,990$ 6,068$ 5,695$ 5,653$ 416-$ -6.9% 42-$ -0.7%

# Articulated trucks: single trailer: 6 axle rig 6,554$ 6,639$ 6,165$ 5,758$ 881-$ -13.3% 407-$ -6.6%

# Articulated trucks: B-double: <9 axle rig 13,537$ 13,713$ 12,315$ 13,501$ 212-$ -1.5% 1,186$ 9.6%

# Articulated trucks: B-double/triple: 9 axle rig & above 14,767$ 14,959$ 13,342$ 13,607$ 1,352-$ -9.0% 265$ 2.0%

# Articulated trucks: B-triple 18,150$ 18,385$ 16,212$ 15,359$ 3,026-$ -16.5% 853-$ -5.3%

# Articulated trucks: Road train: 2 trailers 14,203$ 14,388$ 12,922$ 13,657$ 731-$ -5.1% 735$ 5.7%

# Articulated trucks: Road train: 3 trailers 17,022$ 17,243$ 15,372$ 15,459$ 1,785-$ -10.3% 87$ 0.6%

# Articulated trucks: > 6 axle rig (NEC) 6,847$ 6,936$ 6,441$ 6,562$ 374-$ -5.4% 121$ 1.9%

# Other trucks 1,122$ 1,137$ 1,363$ 1,303$ 166$ 14.6% 60-$ -4.4%

# Buses: 2 axle: GVM 4.5 to 10.0 t 500$ 507$ 497$ 497$ 10-$ -1.9% 1-$ -0.1%

# Buses: 2 axle: GVM over 10.0 t 500$ 507$ 595$ 599$ 92$ 18.2% 4$ 0.6%

# Buses: 3 axle 2,490$ 2,522$ 2,361$ 2,423$ 99-$ -3.9% 62$ 2.6%

# Buses: articulated 500$ 507$ 612$ 615$ 108$ 21.4% 3$ 0.5%

Heavy vehicle charges determination – RIS February 2014 xi

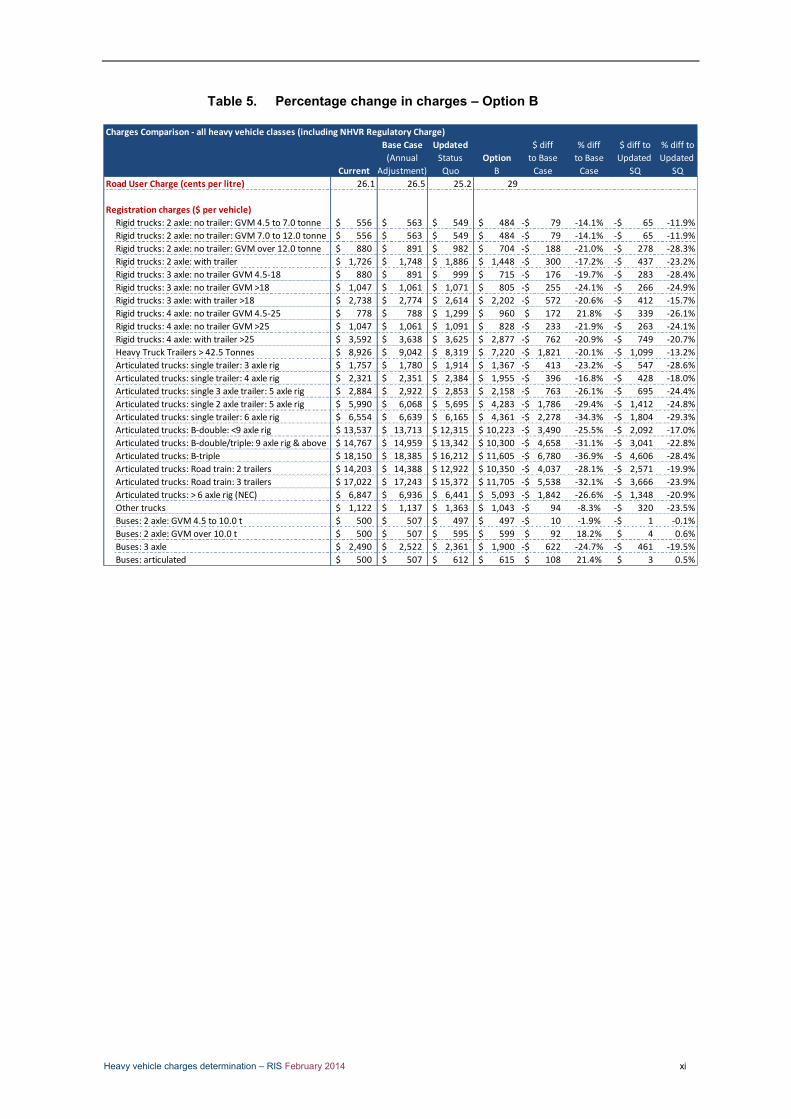

Percentage change in charges – Option B Table 5.

Charges Comparison - all heavy vehicle classes (including NHVR Regulatory Charge)

Base Case Updated $ diff % diff $ diff to % diff to

(Annual Status Option to Base to Base Updated Updated

Current Adjustment) Quo B Case Case SQ SQ

Road User Charge (cents per litre) 26.1 26.5 25.2 29

Registration charges ($ per vehicle)

Rigid trucks: 2 axle: no trailer: GVM 4.5 to 7.0 tonne 556$ 563$ 549$ 484$ 79-$ -14.1% 65-$ -11.9%

Rigid trucks: 2 axle: no trailer: GVM 7.0 to 12.0 tonne 556$ 563$ 549$ 484$ 79-$ -14.1% 65-$ -11.9%

Rigid trucks: 2 axle: no trailer: GVM over 12.0 tonne 880$ 891$ 982$ 704$ 188-$ -21.0% 278-$ -28.3%

Rigid trucks: 2 axle: with trailer 1,726$ 1,748$ 1,886$ 1,448$ 300-$ -17.2% 437-$ -23.2%

Rigid trucks: 3 axle: no trailer GVM 4.5-18 880$ 891$ 999$ 715$ 176-$ -19.7% 283-$ -28.4%

Rigid trucks: 3 axle: no trailer GVM >18 1,047$ 1,061$ 1,071$ 805$ 255-$ -24.1% 266-$ -24.9%

Rigid trucks: 3 axle: with trailer >18 2,738$ 2,774$ 2,614$ 2,202$ 572-$ -20.6% 412-$ -15.7%

Rigid trucks: 4 axle: no trailer GVM 4.5-25 778$ 788$ 1,299$ 960$ 172$ 21.8% 339-$ -26.1%

Rigid trucks: 4 axle: no trailer GVM >25 1,047$ 1,061$ 1,091$ 828$ 233-$ -21.9% 263-$ -24.1%

Rigid trucks: 4 axle: with trailer >25 3,592$ 3,638$ 3,625$ 2,877$ 762-$ -20.9% 749-$ -20.7%

Heavy Truck Trailers > 42.5 Tonnes 8,926$ 9,042$ 8,319$ 7,220$ 1,821-$ -20.1% 1,099-$ -13.2%

Articulated trucks: single trailer: 3 axle rig 1,757$ 1,780$ 1,914$ 1,367$ 413-$ -23.2% 547-$ -28.6%

Articulated trucks: single trailer: 4 axle rig 2,321$ 2,351$ 2,384$ 1,955$ 396-$ -16.8% 428-$ -18.0%

Articulated trucks: single 3 axle trailer: 5 axle rig 2,884$ 2,922$ 2,853$ 2,158$ 763-$ -26.1% 695-$ -24.4%

Articulated trucks: single 2 axle trailer: 5 axle rig 5,990$ 6,068$ 5,695$ 4,283$ 1,786-$ -29.4% 1,412-$ -24.8%

Articulated trucks: single trailer: 6 axle rig 6,554$ 6,639$ 6,165$ 4,361$ 2,278-$ -34.3% 1,804-$ -29.3%

Articulated trucks: B-double: <9 axle rig 13,537$ 13,713$ 12,315$ 10,223$ 3,490-$ -25.5% 2,092-$ -17.0%

Articulated trucks: B-double/triple: 9 axle rig & above 14,767$ 14,959$ 13,342$ 10,300$ 4,658-$ -31.1% 3,041-$ -22.8%

Articulated trucks: B-triple 18,150$ 18,385$ 16,212$ 11,605$ 6,780-$ -36.9% 4,606-$ -28.4%

Articulated trucks: Road train: 2 trailers 14,203$ 14,388$ 12,922$ 10,350$ 4,037-$ -28.1% 2,571-$ -19.9%

Articulated trucks: Road train: 3 trailers 17,022$ 17,243$ 15,372$ 11,705$ 5,538-$ -32.1% 3,666-$ -23.9%

Articulated trucks: > 6 axle rig (NEC) 6,847$ 6,936$ 6,441$ 5,093$ 1,842-$ -26.6% 1,348-$ -20.9%

Other trucks 1,122$ 1,137$ 1,363$ 1,043$ 94-$ -8.3% 320-$ -23.5%

Buses: 2 axle: GVM 4.5 to 10.0 t 500$ 507$ 497$ 497$ 10-$ -1.9% 1-$ -0.1%

Buses: 2 axle: GVM over 10.0 t 500$ 507$ 595$ 599$ 92$ 18.2% 4$ 0.6%

Buses: 3 axle 2,490$ 2,522$ 2,361$ 1,900$ 622-$ -24.7% 461-$ -19.5%

Buses: articulated 500$ 507$ 612$ 615$ 108$ 21.4% 3$ 0.5%

Heavy vehicle charges determination – RIS February 2014 xii

Percentage change in charges – Option C Table 6.

Charges Comparison - all heavy vehicle classes (including NHVR Regulatory Charge)

Base Case Updated $ diff % diff $ diff to % diff to

(Annual Status Option to Base to Base Updated Updated

Current Adjustment) Quo C Case Case SQ SQ

Road User Charge (cents per litre) 26.1 26.5 25.2 32

Registration charges ($ per vehicle)

Rigid trucks: 2 axle: no trailer: GVM 4.5 to 7.0 tonne 556$ 563$ 549$ 484$ 79-$ -14.1% 65-$ -11.9%

Rigid trucks: 2 axle: no trailer: GVM 7.0 to 12.0 tonne 556$ 563$ 549$ 484$ 79-$ -14.1% 65-$ -11.9%

Rigid trucks: 2 axle: no trailer: GVM over 12.0 tonne 880$ 891$ 982$ 571$ 321-$ -36.0% 411-$ -41.9%

Rigid trucks: 2 axle: with trailer 1,726$ 1,748$ 1,886$ 1,117$ 631-$ -36.1% 768-$ -40.7%

Rigid trucks: 3 axle: no trailer GVM 4.5-18 880$ 891$ 999$ 582$ 309-$ -34.7% 417-$ -41.7%

Rigid trucks: 3 axle: no trailer GVM >18 1,047$ 1,061$ 1,071$ 663$ 398-$ -37.5% 409-$ -38.2%

Rigid trucks: 3 axle: with trailer >18 2,738$ 2,774$ 2,614$ 1,663$ 1,110-$ -40.0% 950-$ -36.4%

Rigid trucks: 4 axle: no trailer GVM 4.5-25 778$ 788$ 1,299$ 827$ 39$ 4.9% 473-$ -36.4%

Rigid trucks: 4 axle: no trailer GVM >25 1,047$ 1,061$ 1,091$ 685$ 375-$ -35.4% 406-$ -37.2%

Rigid trucks: 4 axle: with trailer >25 3,592$ 3,638$ 3,625$ 2,167$ 1,471-$ -40.4% 1,458-$ -40.2%

Heavy Truck Trailers > 42.5 Tonnes 8,926$ 9,042$ 8,319$ 5,330$ 3,712-$ -41.1% 2,990-$ -35.9%

Articulated trucks: single trailer: 3 axle rig 1,757$ 1,780$ 1,914$ 1,102$ 678-$ -38.1% 812-$ -42.4%

Articulated trucks: single trailer: 4 axle rig 2,321$ 2,351$ 2,384$ 1,522$ 829-$ -35.2% 861-$ -36.1%

Articulated trucks: single 3 axle trailer: 5 axle rig 2,884$ 2,922$ 2,853$ 1,668$ 1,254-$ -42.9% 1,186-$ -41.6%

Articulated trucks: single 2 axle trailer: 5 axle rig 5,990$ 6,068$ 5,695$ 3,187$ 2,882-$ -47.5% 2,508-$ -44.0%

Articulated trucks: single trailer: 6 axle rig 6,554$ 6,639$ 6,165$ 3,242$ 3,396-$ -51.2% 2,922-$ -47.4%

Articulated trucks: B-double: <9 axle rig 13,537$ 13,713$ 12,315$ 7,600$ 6,113-$ -44.6% 4,715-$ -38.3%

Articulated trucks: B-double/triple: 9 axle rig & above 14,767$ 14,959$ 13,342$ 7,656$ 7,303-$ -48.8% 5,686-$ -42.6%

Articulated trucks: B-triple 18,150$ 18,385$ 16,212$ 8,603$ 9,782-$ -53.2% 7,608-$ -46.9%

Articulated trucks: Road train: 2 trailers 14,203$ 14,388$ 12,922$ 7,706$ 6,682-$ -46.4% 5,216-$ -40.4%

Articulated trucks: Road train: 3 trailers 17,022$ 17,243$ 15,372$ 8,703$ 8,540-$ -49.5% 6,669-$ -43.4%

Articulated trucks: > 6 axle rig (NEC) 6,847$ 6,936$ 6,441$ 3,918$ 3,018-$ -43.5% 2,523-$ -39.2%

Other trucks 1,122$ 1,137$ 1,363$ 835$ 302-$ -26.6% 528-$ -38.8%

Buses: 2 axle: GVM 4.5 to 10.0 t 500$ 507$ 497$ 497$ 10-$ -1.9% 1-$ -0.1%

Buses: 2 axle: GVM over 10.0 t 500$ 507$ 595$ 599$ 92$ 18.2% 4$ 0.6%

Buses: 3 axle 2,490$ 2,522$ 2,361$ 1,482$ 1,040-$ -41.2% 879-$ -37.2%

Buses: articulated 500$ 507$ 612$ 615$ 108$ 21.4% 3$ 0.5%

Heavy vehicle charges determination – RIS February 2014 xiii

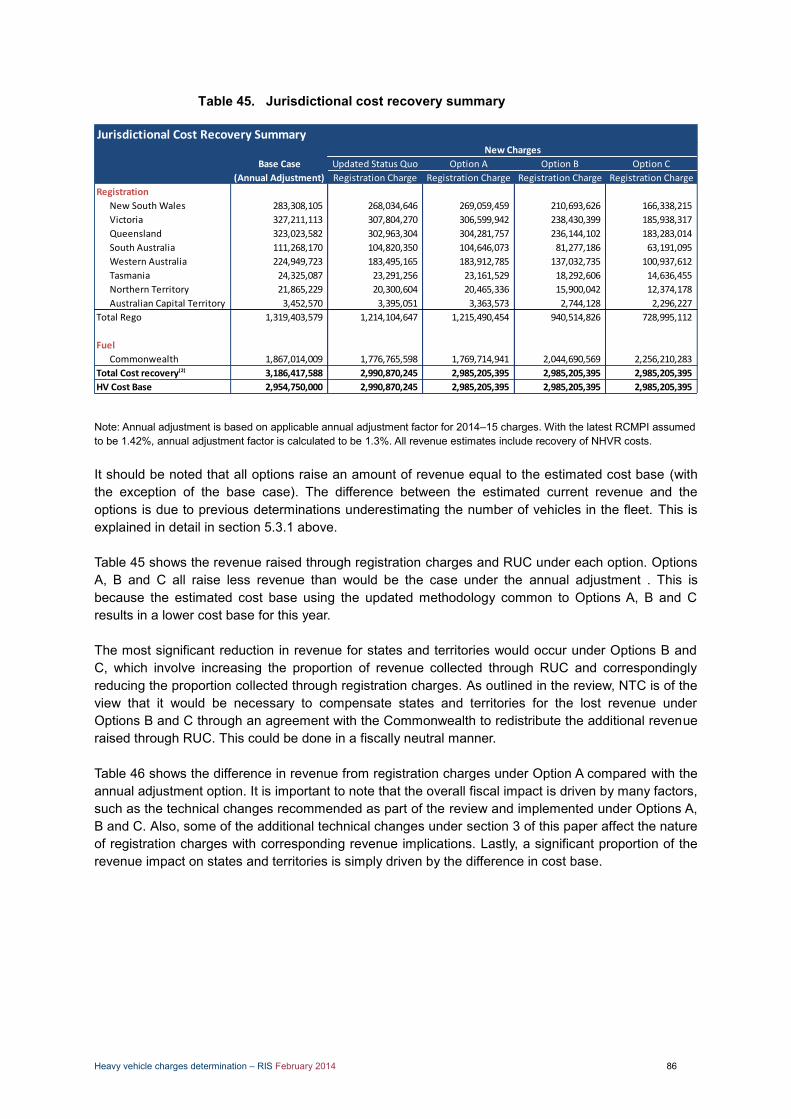

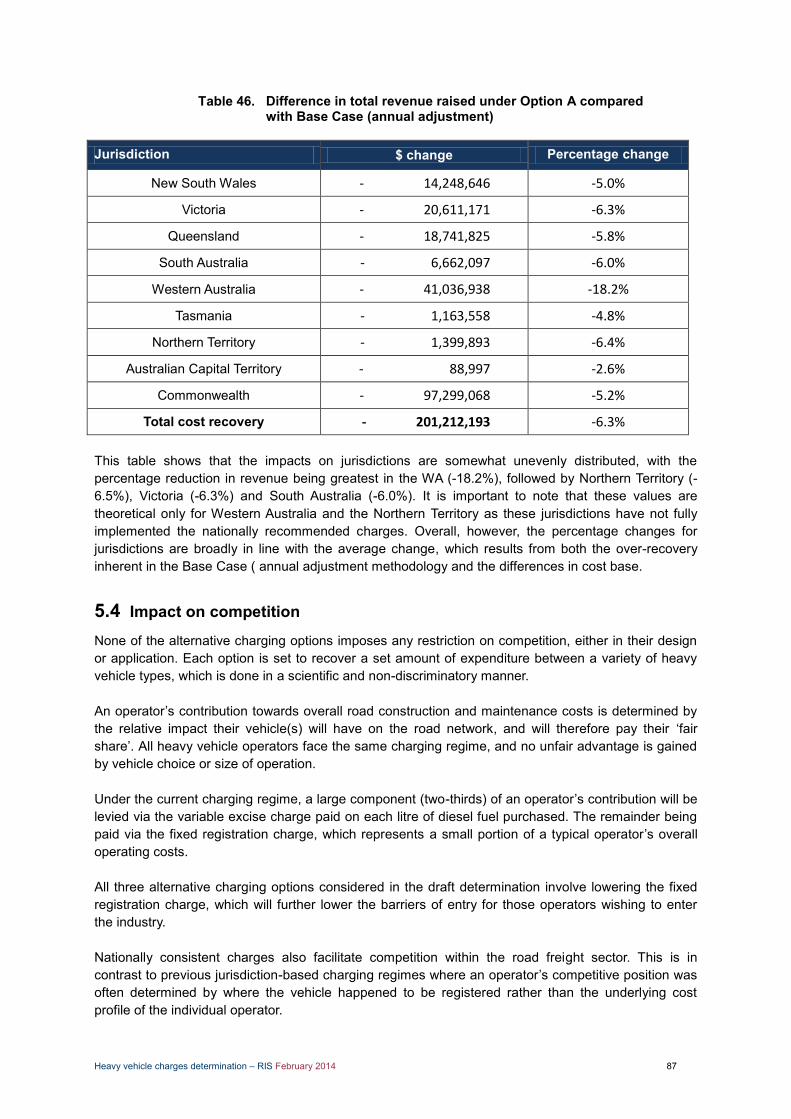

Table 7 shows an estimation in the change of revenues under each option for the Commonwealth, state and territory governments.

Commonwealth and jurisdictional revenue implications Table 7.

Note: The total cost recovery for the base case is higher than the calculated cost base as charges are derived using a mid-point usage figure but revenue is estimated on an up to date registration number.

The following section provides an overview of the PAYGO charging framework, the key policy issues considered, and summary of the key recommendations to improve PAYGO.

Policy development process

In completing this draft determination, the NTC adopted a ‘co-design’ approach in formulating key recommendations and arriving at a final schedule of heavy vehicle charges. The determination builds upon the findings of the Heavy Vehicle Charges Review, which was undertaken openly and collaboratively, resulting in a high degree of transparency, a better understanding of stakeholders’ needs, and a common ownership of outcomes.

This approach included a series of stakeholder workshops, tele-presences, public forums, public consultations, and bilateral meetings. Like the charges review, the determination regulatory impact statement will be subject to the same level of public consultation and stakeholder engagement.

Background to PAYGO

PAYGO was implemented in 1995, when heavy vehicle registration charges varied widely between states and territories, resulting in significant market distortions. An operator’s competitive advantage was often dictated by the location the business was registered in, as opposed to the underlying efficiencies of the operator.

PAYGO introduced a system where industry was required to pay their fair share of government spending on roads through consistent national charges. These charges were also designed to meet a number of key efficiency and equity objectives enshrined in the first set of pricing principles.

Inherent limitations of the PAYGO charging framework

The determination aims to rectify a number of limitations of the current charging system. However, there are some inherent limitations that cannot be resolved without wholesale reform of heavy vehicle charging. These limitations include:

Averaging – Multiple levels of averaging will remain a feature of the current charging framework as more disaggregated data is not available. This includes averaging of costs across the network and usage across vehicle types.

Input data limitations – The current usage data is survey based as opposed to observable actual usage data and this will continue in the absence of any clear cost-effective alternative.

Jurisdictional Cost Recovery Summary

Base Case Updated Status Quo Option A Option B Option C

(Annual Adjustment) Registration Charge Registration Charge Registration Charge Registration Charge

Registration

New South Wales 283,308,105 268,034,646 269,059,459 210,693,626 166,338,215

Victoria 327,211,113 307,804,270 306,599,942 238,430,399 185,938,317

Queensland 323,023,582 302,963,304 304,281,757 236,144,102 183,283,014

South Australia 111,268,170 104,820,350 104,646,073 81,277,186 63,191,095

Western Australia 224,949,723 183,495,165 183,912,785 137,032,735 100,937,612

Tasmania 24,325,087 23,291,256 23,161,529 18,292,606 14,636,455

Northern Territory 21,865,229 20,300,604 20,465,336 15,900,042 12,374,178

Australian Capital Territory 3,452,570 3,395,051 3,363,573 2,744,128 2,296,227

Total Rego 1,319,403,579 1,214,104,647 1,215,490,454 940,514,826 728,995,112

Fuel

Commonwealth 1,867,014,009 1,776,765,598 1,769,714,941 2,044,690,569 2,256,210,283

Total Cost recovery(2) 3,186,417,588 2,990,870,245 2,985,205,395 2,985,205,395 2,985,205,395

HV Cost Base 2,954,750,000 2,990,870,245 2,985,205,395 2,985,205,395 2,985,205,395

New Charges

Heavy vehicle charges determination – RIS February 2014 xiv

Non-deterministic charge setting framework – The NTC’s heavy vehicle charge setting recommendations are non-binding, which means states and territories can choose not to adopt the charges. This allows for concession lobbying in each state and territory, which can undermine the full implementation of national charging across Australia.

Lag between cost base measurement and implementation of charges – The current PAYGO methodology involves a delay between the measurement of the cost base and the implementation of charges that are set based upon that cost base.

Improving PAYGO

The scope of this determination does not allow for structural or wholesale change to the current charging system but instead focuses on improving the PAYGO system by both updating it with new input data and also revising the current methodology where evidence suggests it could be improved.

The key changes to the PAYGO system are described below. For a more complete understanding of the issues involved, this determination should be read in conjunction with the heavy vehicle charges review document.

Calculating the cost base

The current method for calculating the cost base involves averaging seven years of road construction and maintenance expenditure reported by the states and territories. Before the averaging occurs, past (nominal) road expenditure data is converted to current year (real) terms using the Bureau of Infrastructure, Transport and Regional Economics (BITRE) Road Construction and Maintenance Price Index (RCMPI) to avoid downward bias caused by using historical data. The RCMPI is used because it tracks the cost of key inputs that go into road construction expenditure, namely asphalt, sand, labour, diesel, concrete, plant hire and other inputs.

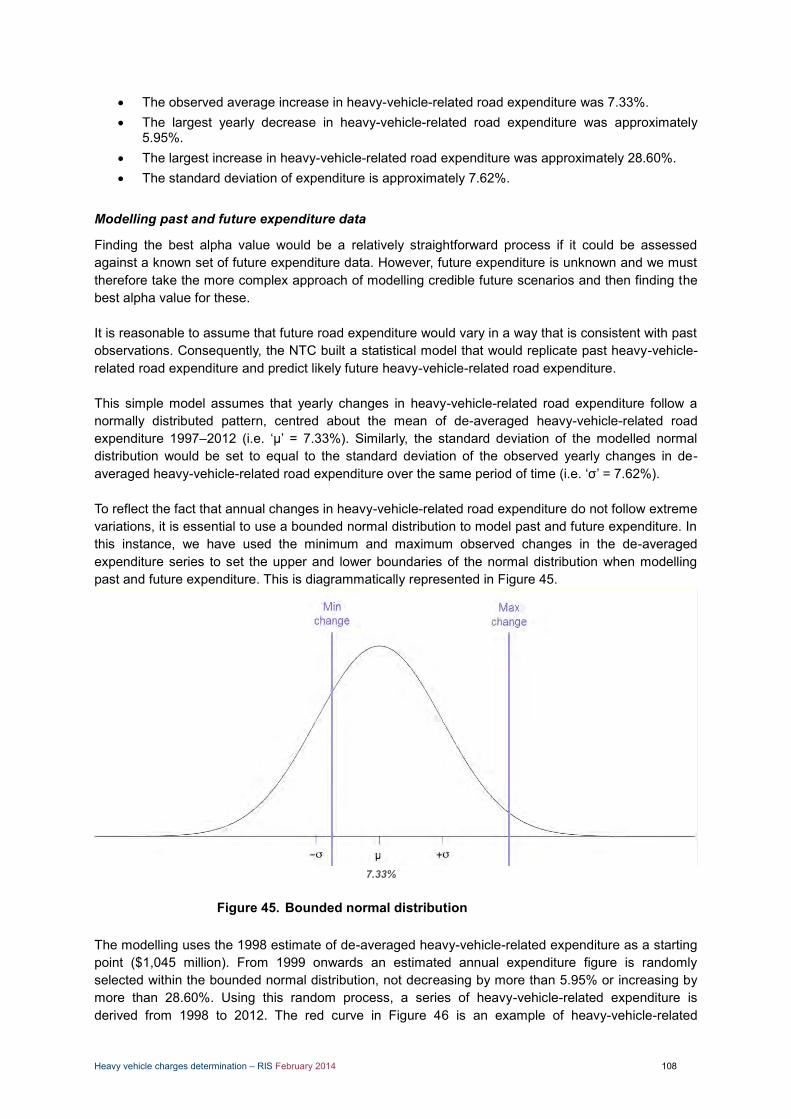

Use of the RCMPI has been criticised because of the volatility of the annual changes in the index. This volatility can be explained by the expansion in infrastructure construction that has occurred over the last decade due to the mining boom. However, the adoption of a highly volatile index in the averaging mechanism violates one of the original objectives of the averaging mechanism, namely to smooth the graduation of charges over time. It is for this reason that the NTC, in consultation with stakeholders, recommends the adoption of an alternative averaging mechanism.

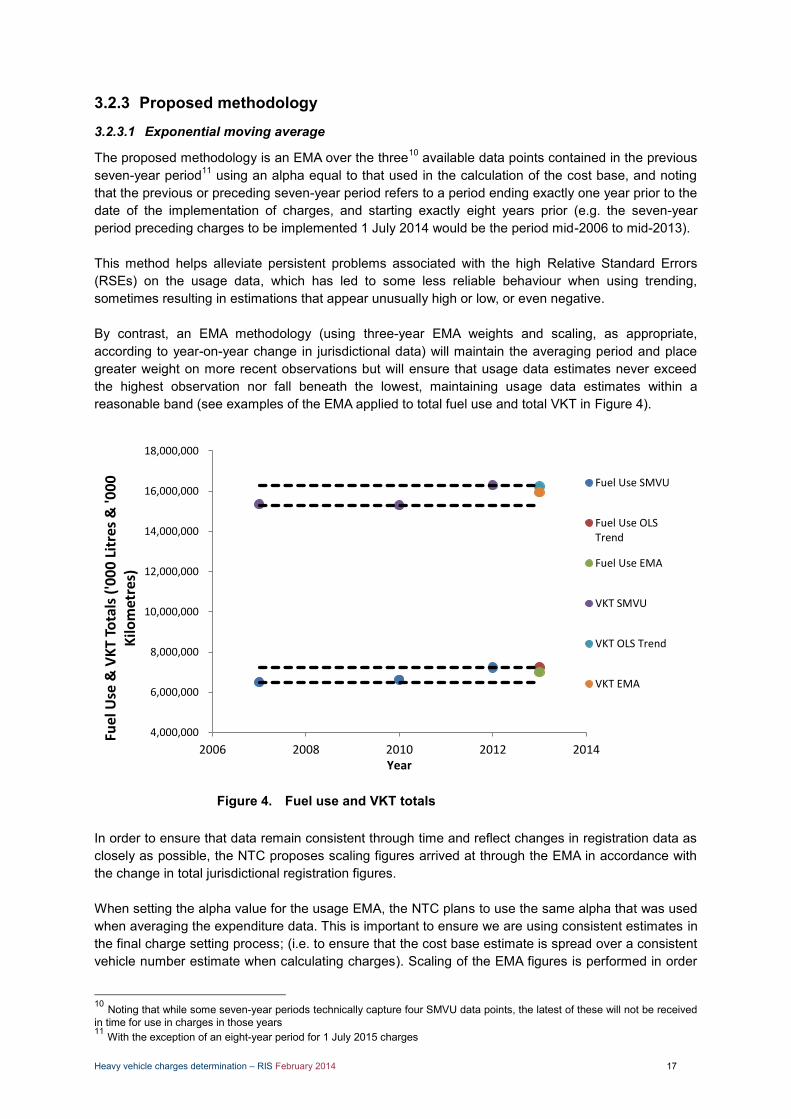

The NTC recommended and ministers approved the adoption of an exponential moving average of nominal expenditure over seven years (EMA7). The EMA or ‘exponentially weighted moving average’ is a particular type of weighted moving average where the weighting for each subsequent datum point will decrease exponentially. Giving a greater weight to more recent expenditure results in a similar outcome to the status quo but without the volatility of the RCMPI. The exact weight attributed to each of the seven years is determined by an alpha value between 0 and 1.

In determining the most appropriate value of alpha, the NTC conducted a series of statistical tests over a randomly generated series of expenditure profiles informed by past expenditure patterns. These tests looked at how well each value of alpha performed against a set of performance criteria, namely:

full cost recovery over time limiting over- and under-recoveries smoothness.

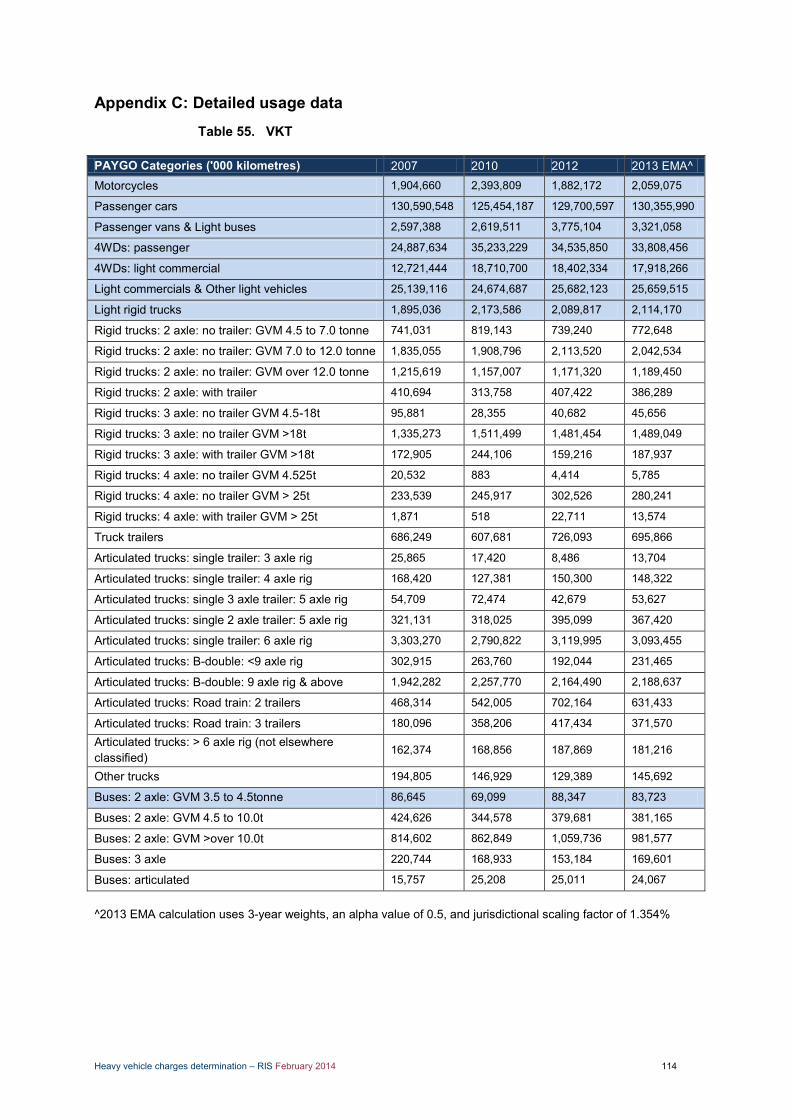

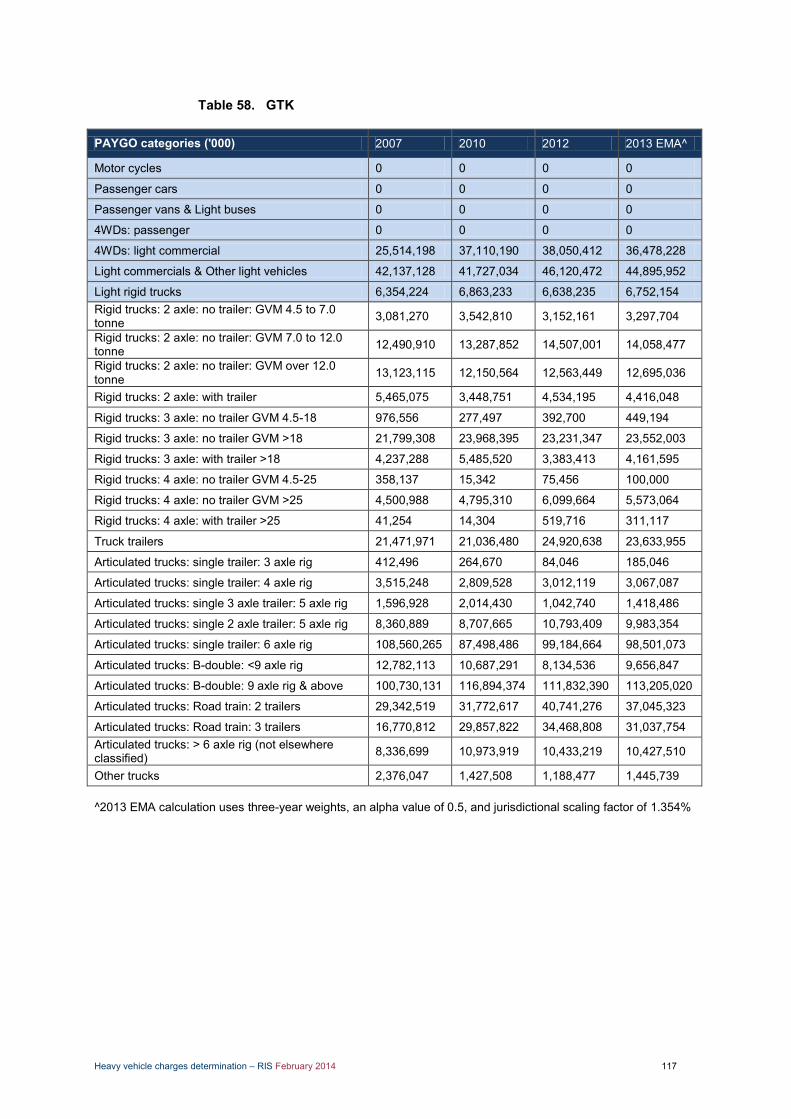

Usage dataset

The current PAYGO model uses information on vehicle population, vehicle kilometres travelled, gross tonne kilometres and fuel consumption, sourced from the Survey of Motor Vehicle Use (SMVU) and published by the Australian Bureau of Statistics to calculate heavy vehicle charges.

These parameters play a crucial role in how costs are allocated through the cost allocation matrix, deriving the cost base, calculating charges, and in estimating the total revenue raised by the Commonwealth, state and territory governments.

As part of the review the NTC acknowledged a number of issues stemming from the survey-based nature of the data; however, in the absence any superior alternative, the retention of the SMVU was required to calculate the charges.

Heavy vehicle charges determination – RIS February 2014 xv

The review concluded that an up-to-date estimate of vehicle numbers should be used instead of a midpoint, and the estimate should be consistent with actual registration data supplied by the states and territories. In particular, the estimate should include ‘inactive’ vehicles.4 These changes were necessary to ensure consistency in the final heavy vehicle charges calculation; that is, an up-to-date estimate of costs should be spread over an up-to-date estimate of vehicle numbers, not a deflated midpoint. In addition, Options A, B and C use registration data supplied by the states and territories to ensure estimates of revenue from registration charges are accurate.

A key outcome of using updated vehicle numbers, based on actual registration figures has been a reduction in per vehicle registration charges.

In the determination the NTC also found that attempting to use a trended estimate for usage parameters created a number of nonsensical outcomes – that is, negative usage values. To resolve this issue the NTC employed a weighted averaging methodology similar to that used for the cost base calculation. Because of the two year survey frequency, there are only three data points within the seven-year window, so the the result is adjusted for recent changes in total vehicle numbers.

Expenditure template and accountability

Presently the NTC is required to accept expenditure data reported by each jurisdiction without mandate or additional powers to audit or independently assess the prudency or efficiency of those costs. There is also no role for the NTC to conduct any assessment on whether the jurisdictional expenditure data has been reported correctly.

In other network infrastructure businesses, expenditure accountability is a key feature of the regulatory regime, where capital and operational costs are reviewed ex-ante, ex-post or both. Designing an appropriate framework for the scrutiny of costs can deliver significant efficiency benefits for road users.

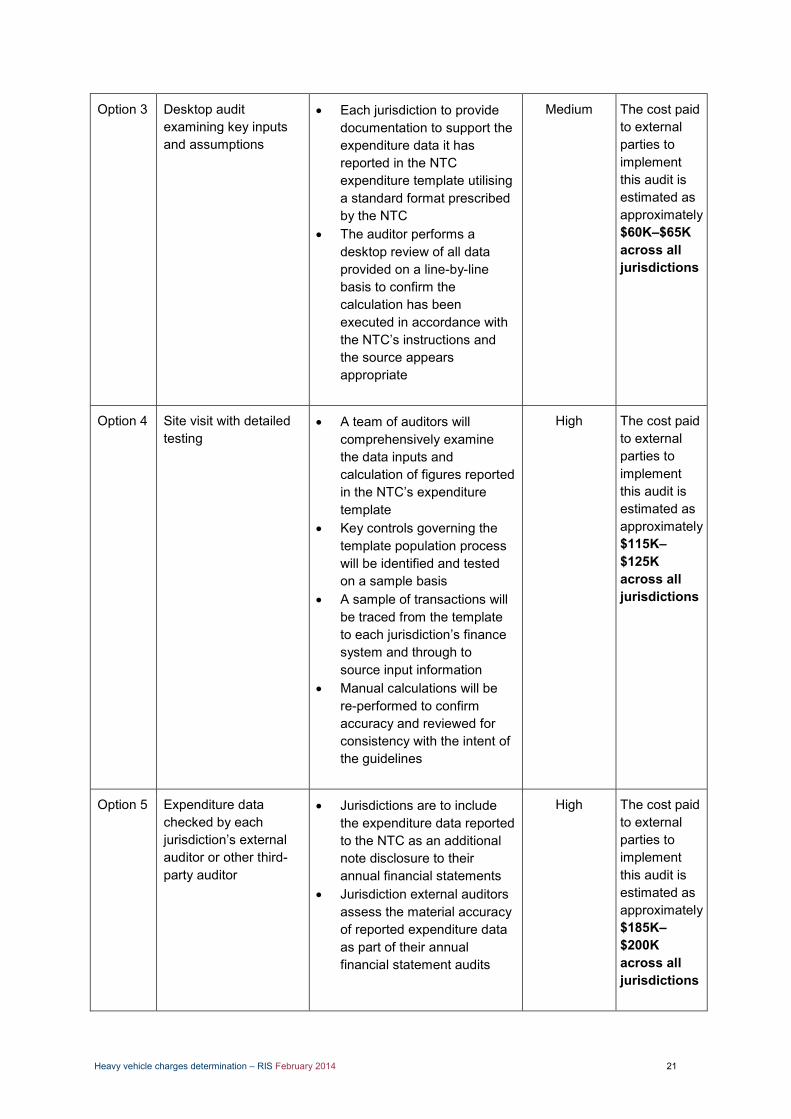

As part of the determination process, the NTC investigated the possibility of introducing procedural-style audits that would assess the accuracy and consistency of jurisdictional cost reporting through the NTC expenditure template. In assessing which of the options to recommend, the NTC carefully considered both industry expectations and jurisdictional resource constraints.

As part of broader accountability measures, the NTC has also committed to further investigating the introduction of benchmark reporting of jurisdictional costs. Benchmarking is an important accountability tool used in other network infrastructure businesses and helps explain cost differential to users of the network.

Charges for articulated trailers

The current charges system allocates costs, and sets charges based on vehicle configuration. While this approach works for the rigid fleet, it creates unintended distortions for articulated vehicles and trailers given their modular nature; that is, trailers and prime movers can be configured in a number of ways to form different combinations. In particular, ‘A-trailer’ charges have traditionally been set higher than other axle types in an attempt to ensure B-doubles ‘pay their way’. Sections of industry argued that operators who used A-trailers outside of the B-double configuration were being unfairly penalised; in addition, the relatively high A-trailer charge was dis-incentivising the use of safer and more productive vehicles. The review concluded that future charges for articulated vehicles and trailers should acknowledge their modularity, and proposed alternative methods for achieving that goal. As part of the draft determination, the NTC concluded that the axle grouping charge approach was superior because it: delivers a more accurate representation of the load carrying capacity that results in the road pavement impact; provides a logical progression of charges, meets the heavy vehicle charges requirements set by COAG; and provides a simple and easy-to-understand charging structure. Estimation of relative levels of pavement wear

All heavy vehicles are responsible for different levels of pavement wear, and measuring each vehicle’s relative impact is important in determining what charges they pay. In the PAYGO model, 4 Vehicles that pay registration but do not travel on public roads during the relevant survey period.

Heavy vehicle charges determination – RIS February 2014 xvi

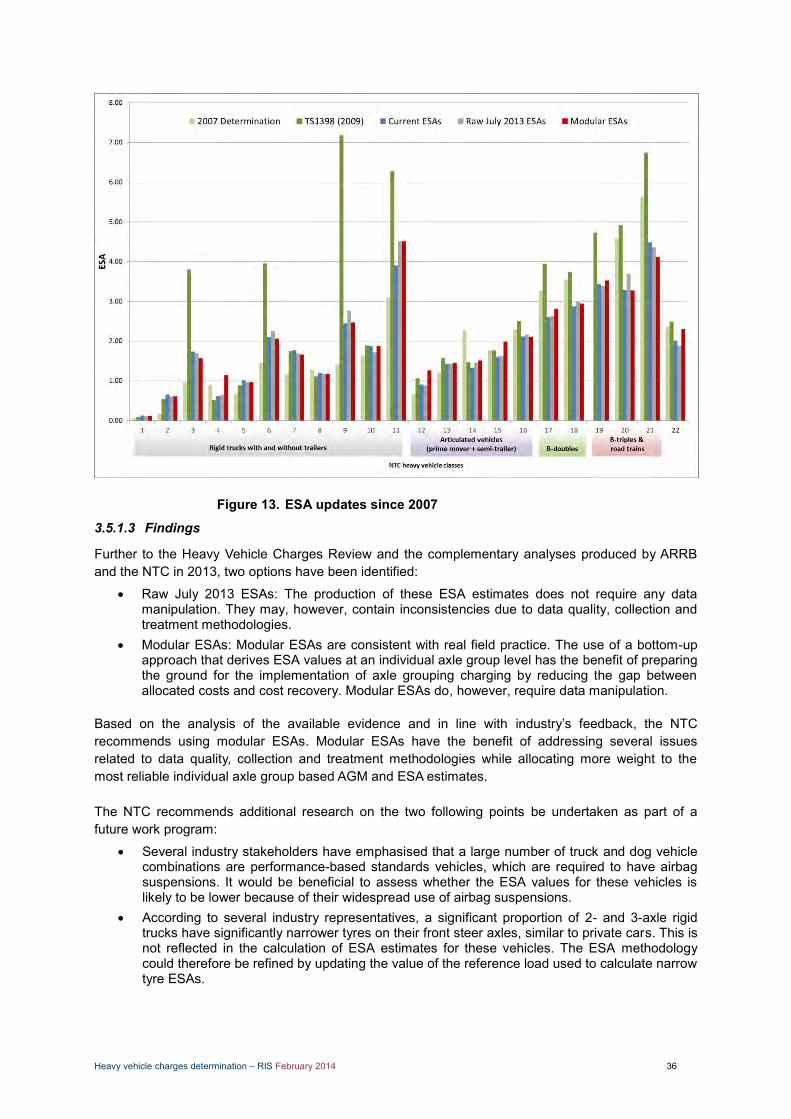

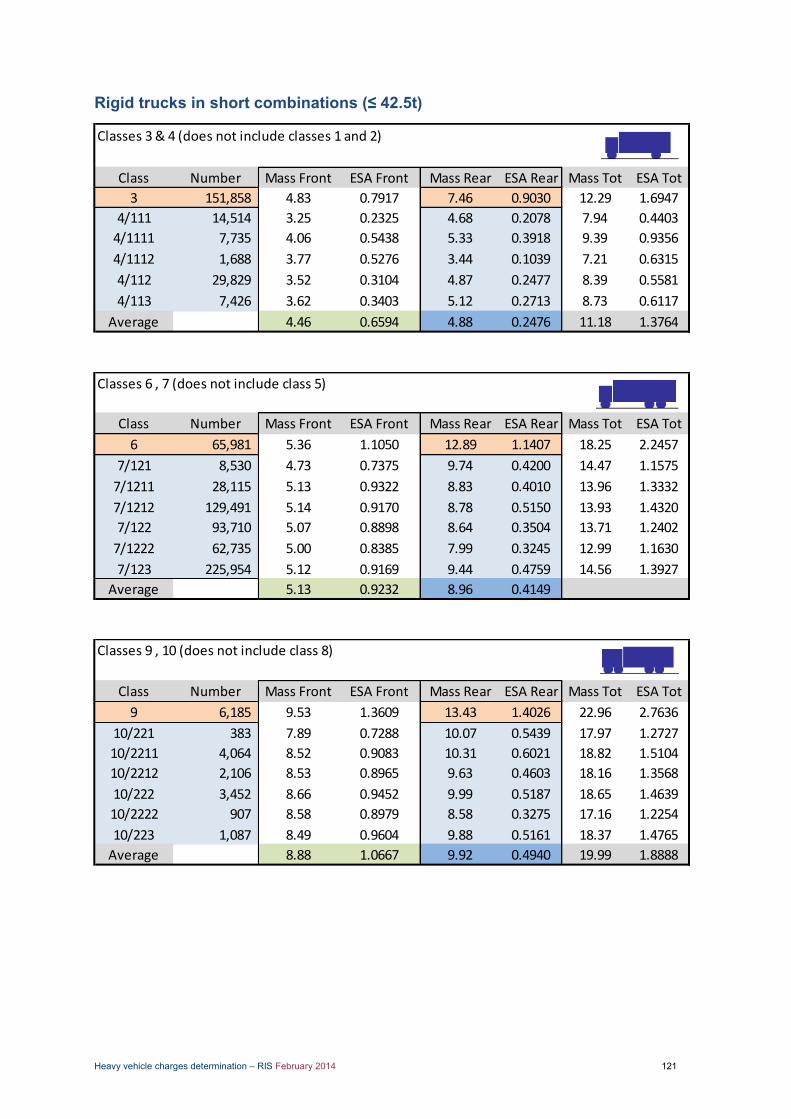

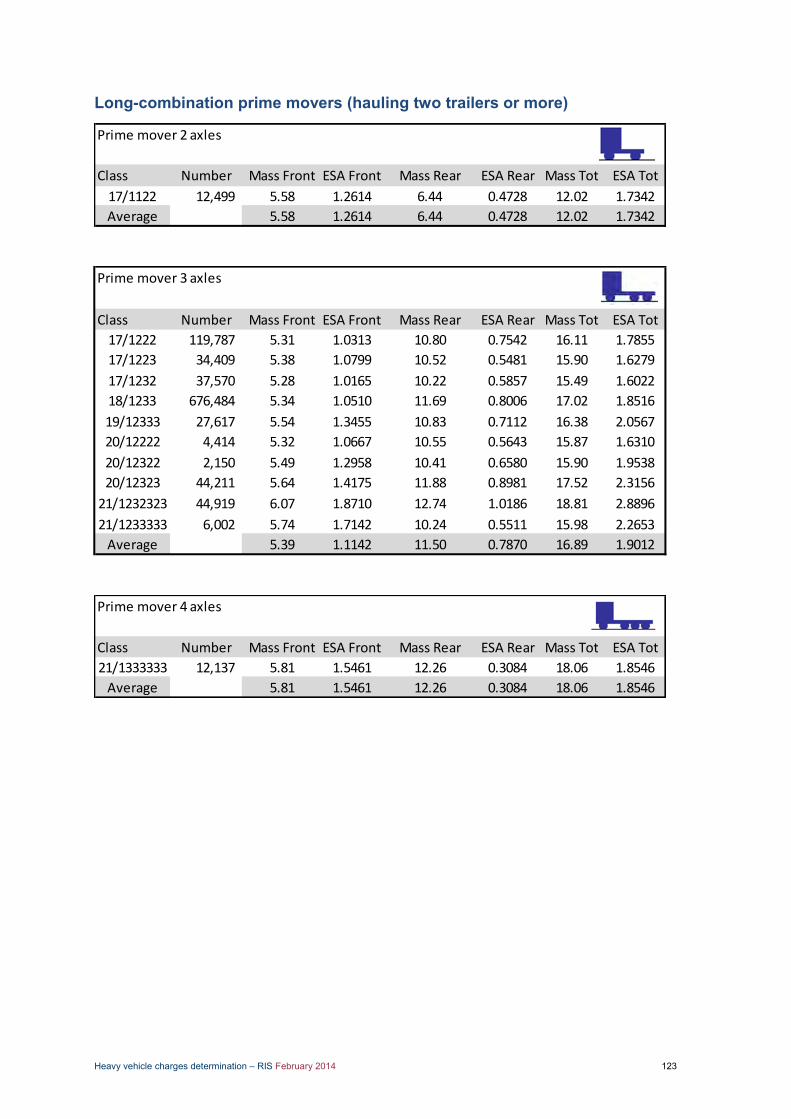

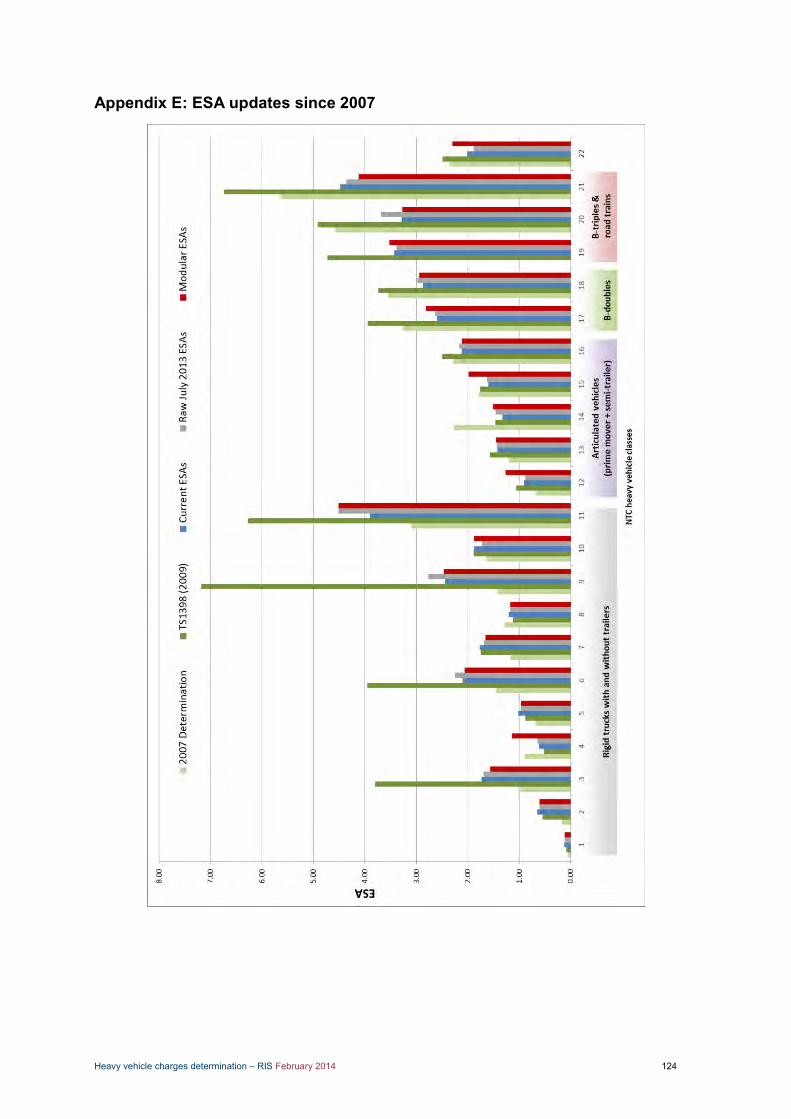

pavement wear is measured using the equivalent standard axle (ESA) methodology. As part of the review, a number of issues arose requiring a re-examination of certain aspects of the methodology.

The review recommended the re-assessment of bus and coach ESAs due to misclassification of weigh-in-motion (WIM) records used to derive the ESA estimate. When categorising WIM records between vehicle classes, an overlap in wheelbase ranges made it impossible to distinguish certain rigid trucks from certain buses/coaches using WIM data alone. Research conducted as part of the determination has resolved this problem using verification techniques like number plate recognition technology to derive more accurate ESA estimates for buses and coaches.

As part of the draft determination, the NTC recommends the adoption of modular ESAs for allocating costs to articulated vehicles. This is similar to the articulated charging issue. Modular ESAs are superior in that they acknowledge that articulated vehicles are modular in their use, and therefore the measurement of their relative impact on pavement wear should also be modular.

An assumption of the PAYGO model is that light vehicles (vehicles weighing less than 4.5t) cause no pavement wear. This assumption is made on the basis that a well-built road designed for trucks will not be damaged by cars. Industry raised doubts about this assumption; however, after reviewing the latest research into the issue, the NTC concluded that the assumption does hold and ESA values for light vehicles should remain at zero for as part of this determination. The NTC may re-examine this assumption in a future determination if new research becomes available.

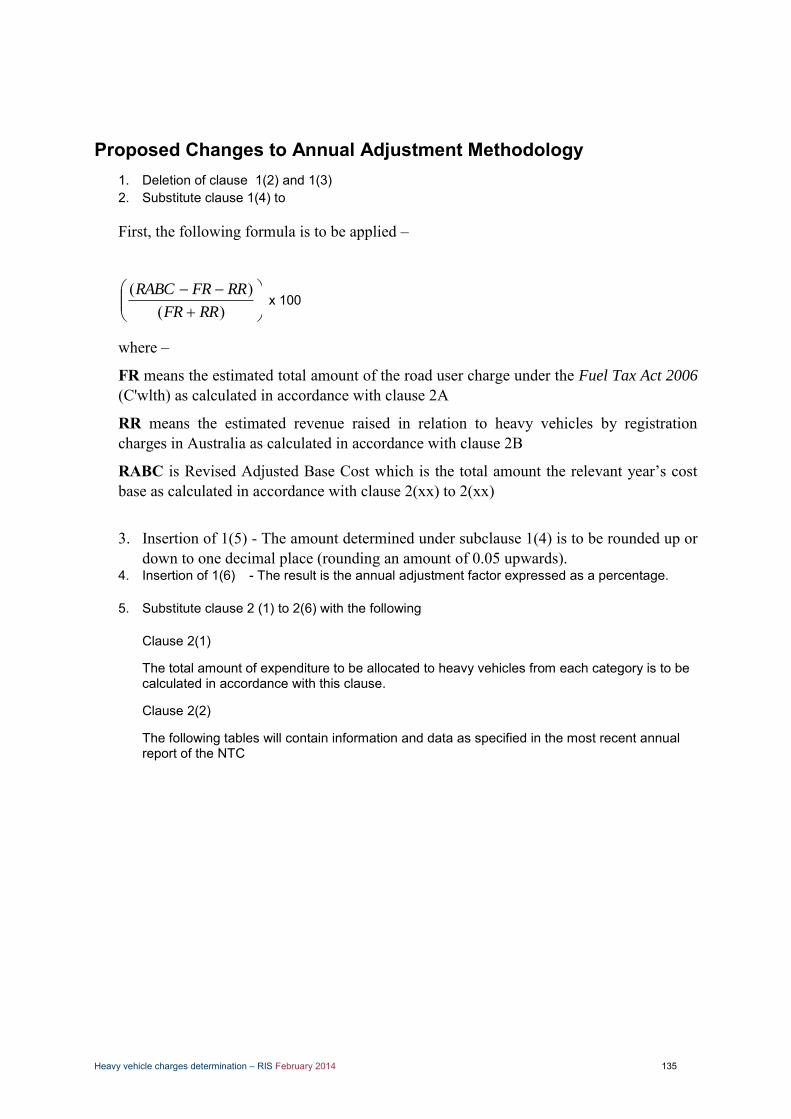

Annual adjustment

The annual adjustment process amends charges between determinations to take account of changes in heavy vehicle expenditure while also reflecting changes in the overall fleet size and mix between light and heavy vehicles. It was designed as a relatively simple, cost-effective and mechanistic method by which charges could be adjusted each year to ensure ongoing cost recovery.

The review found a number of issues relating to the current annual adjustment formula, and concluded it did not accurately reflect the changes in expenditure and usage from year to year. The review also recommended the adoption of an alternative formula.

As part of the draft determination, the NTC has explored a number of options and recommended the adoption of a ‘dynamic annual adjustment formula’. The key difference with this approach is that it better reflects actual changes in usage and expenditure from year to year between determinations.

Rebates / concessions / national charges

The purpose of this determination is to recommend a set of national heavy vehicle charges. However, states and territories have the ability to modify the national charges through rebates and concessions. As part of the determination, the NTC has recommended that jurisdictions consider the following principles when granting rebates or concessions:

Define clear objectives – define the problem and set clear objectives for the concession.

Minimise distortions – structure the concession to achieve the objective in the least distorted way (e.g. it should not impact on vehicle choice).

Ensure transparency – make the concession transparent in terms of the objective and the size of the subsidy.

Monitor and review – monitor and review the concession over time to see how much is being recovered and whether the original objectives are being met.

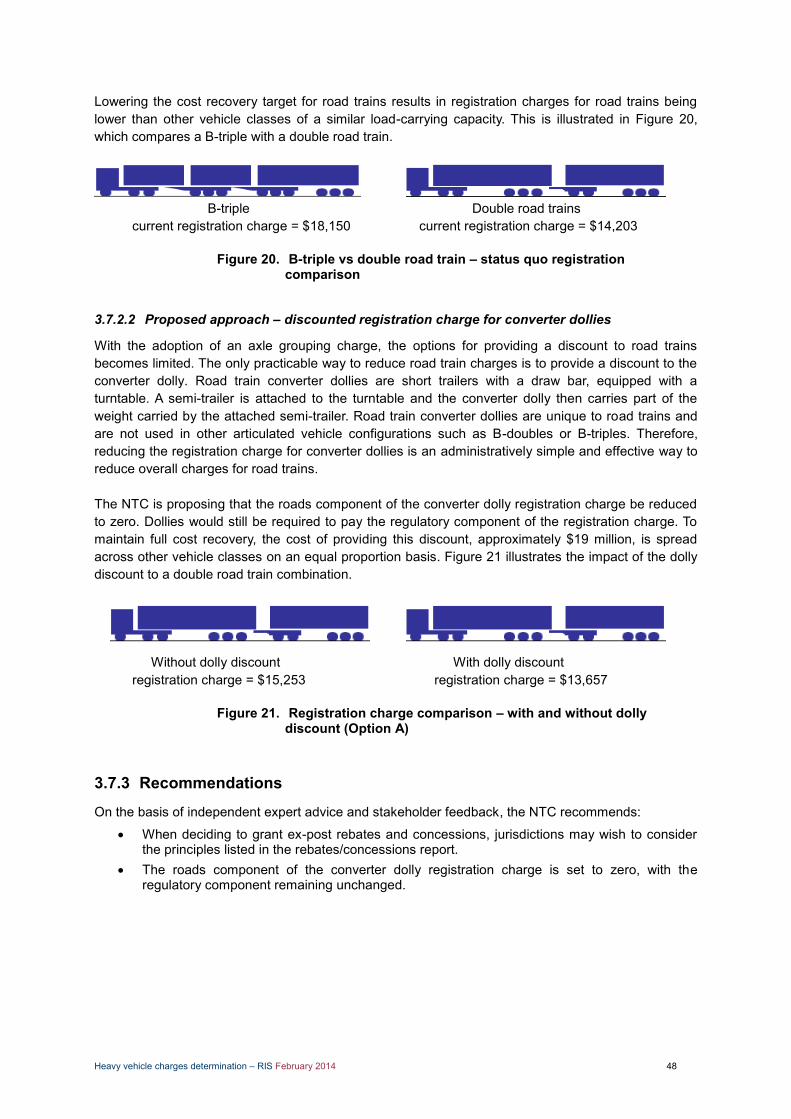

With respect to the road train discount and remote community service obligation (CSO), the NTC recommends setting the roads component of the converter dolly registration charge to zero, with the regulatory component remaining unchanged.

NHVR funding

The National Heavy Vehicle Regulator (NHVR) commenced operations on 21 January 2013, and is expected to commence administering the National Heavy Vehicle Law in the near future. As part of the determination, the NTC has been tasked with designing the mechanism for the recovery of ongoing NHVR costs as per the NHVR intergovernmental agreement.

Heavy vehicle charges determination – RIS February 2014 xvii

In evaluating various cost recovery options, the NTC concluded that when spreading the costs among vehicle classes primary consideration should be given to preserving the natural progression of charges as payload capacity increases, and to that end, the NTC recommends a ‘multifactor allocation mechanism’ for the recovery of NHVR costs.

Summary of recommendations

Presented in Table 8 is a summary of the recommendations to improve the current PAYGO system. These recommendations build upon previous recommendations made as part of the Heavy Vehicle Charges Review.

Summary of recommendations Table 8.

Issue Draft recommendations

1. Calculating the cost base The use of an exponential moving average (EMA) calculated over a 7 year period with an alpha value of 0.50.

2. Usage dataset The use of an EMA with three-year weights and alpha value consistent with that used in the cost base calculation (0.5).

3. Expenditure template and accountability

Implementation of a one-off audit/review of expenditure data modelled on ‘Option 4 – Site visit with detailed testing’ from next financial year.

The audit timing should take into account jurisdictional resource constraints (anticipated post October 2014 completion date).

The audit is paid for by respective jurisdictions. The cost of the audit is reported in the NTC expenditure

template and recoverable from heavy vehicles only. The NTC will coordinate the procurement and execution of

the audit. The NTC will investigate further the introduction of

benchmark reporting in consultation with each jurisdiction and industry.

4. Charges for articulated trailers

The adoption of an axle grouping charge for all trailer axles.

5. Estimation of relative levels of pavement wear

The use of modular ESAs for the purposes of calculating heavy vehicle charges.

Further research is conducted into refining the ESA measurement.

The adoption of the revised ESA estimates for buses and coaches for use in the PAYGO model.

The retention of the current ESA values for light vehicle classes.

6. Annual adjustment The adoption of the dynamic annual adjustment formula for future annual adjustments of heavy vehicle charges.

7. Rebates / concessions / national charges

When deciding to grant ex-post rebates and concessions, jurisdictions may wish to consider the principles listed in the

Heavy vehicle charges determination – RIS February 2014 xviii

Issue Draft recommendations

rebates/concessions report. The registration charge for road train converter dollies5 are

reduced to the value of the regulatory component as a means to reduce overall charges for road trains.

8. NHVR funding The use of a multi-factor allocation mechanism for the recovery of NHVR costs.

Next steps

This draft determination RIS will be subjected to a comprehensive public consultation process. The NTC will then consider the feedback received from stakeholders and prepare a final determination RIS.

The final determination RIS will then be presented to SCOTI, with the recommendation that it approve the final recommended heavy vehicle charges.

Following a SCOTI decision, NTC would then work with states, territories and the Commonwealth to implement the approved charges in accordance with SCOTI’s decisions.Acknowledgments

The NTC acknowledges Andradi Adhiputro, Matthew Bereni, Steve Condylios, Chris Egger, Peter Halligan and Ramon Staheli in preparing this report. The NTC also acknowledges significant input from the Australian Trucking Association and its state associations, NatRoad, Cement Concrete & Aggregates Australia, the National Road Freighters Association, Australian Livestock and Rural Transporters Association, the Heavy Vehicle Charging and Investment Reform Project, the National Heavy Vehicle Regulator, the Australian Taxation Office, the Office of Best Practice Regulation, the Commonwealth Department of Infrastructure and Transport, the Department of Infrastructure, The Treasury, the Department of Infrastructure, Energy & Resources Tasmania, Transport for NSW, the Department of Transport and Main Roads Queensland, the Department of Planning, Transport and Infrastructure South Australia, Main Roads Western Australia, VicRoads and each state and territory road authority.

5 Road train converter dollies are short trailers with a draw bar, equipped with a turntable. A semi-trailer is attached to the turntable and the converter dolly then carries part of the weight carried by the attached semi-trailer. Road train converter dollies are unique to road trains and are not used in other articulated vehicle configurations such as B-doubles or B-triples.

Heavy vehicle charges determination – RIS February 2014 1

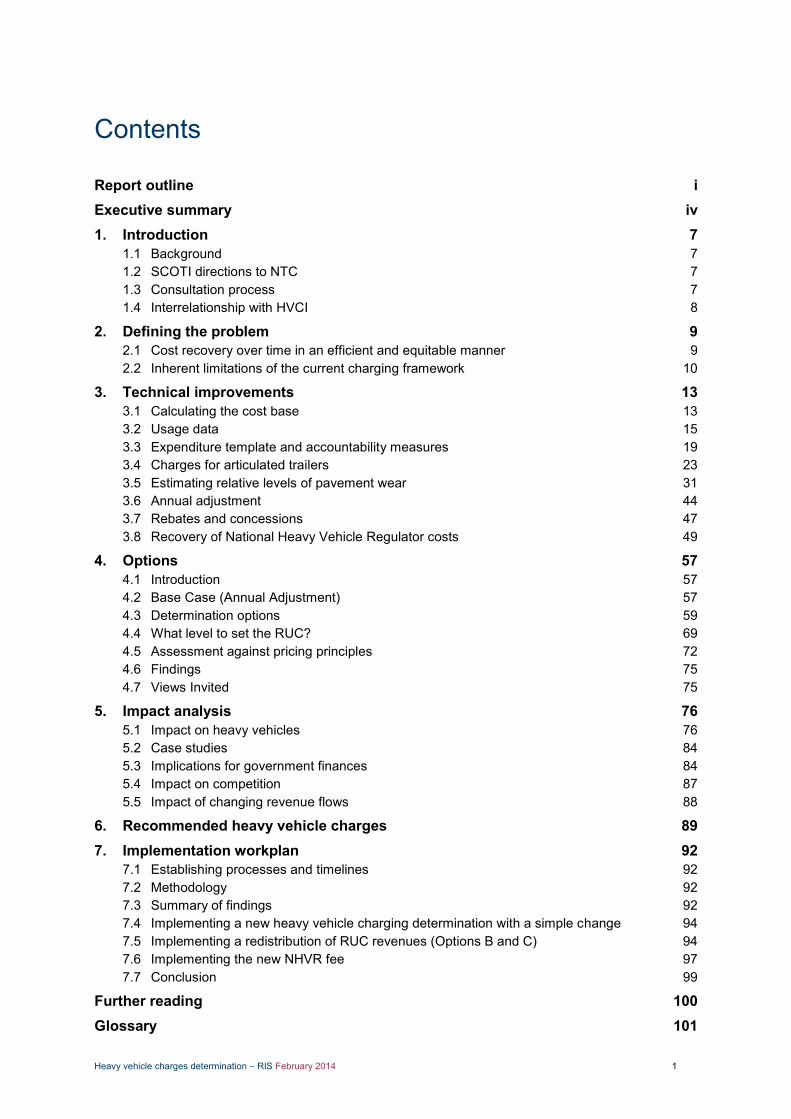

Contents

Report outline i Executive summary iv

1. Introduction 7

1.1 Background 7 1.2 SCOTI directions to NTC 7 1.3 Consultation process 7 1.4 Interrelationship with HVCI 8

2. Defining the problem 9 2.1 Cost recovery over time in an efficient and equitable manner 9 2.2 Inherent limitations of the current charging framework 10

3. Technical improvements 13

3.1 Calculating the cost base 13 3.2 Usage data 15 3.3 Expenditure template and accountability measures 19 3.4 Charges for articulated trailers 23 3.5 Estimating relative levels of pavement wear 31 3.6 Annual adjustment 44 3.7 Rebates and concessions 47 3.8 Recovery of National Heavy Vehicle Regulator costs 49

4. Options 57

4.1 Introduction 57 4.2 Base Case (Annual Adjustment) 57 4.3 Determination options 59 4.4 What level to set the RUC? 69 4.5 Assessment against pricing principles 72 4.6 Findings 75 4.7 Views Invited 75

5. Impact analysis 76

5.1 Impact on heavy vehicles 76 5.2 Case studies 84 5.3 Implications for government finances 84 5.4 Impact on competition 87 5.5 Impact of changing revenue flows 88

6. Recommended heavy vehicle charges 89

7. Implementation workplan 92 7.1 Establishing processes and timelines 92 7.2 Methodology 92 7.3 Summary of findings 92 7.4 Implementing a new heavy vehicle charging determination with a simple change 94 7.5 Implementing a redistribution of RUC revenues (Options B and C) 94 7.6 Implementing the new NHVR fee 97 7.7 Conclusion 99

Further reading 100

Glossary 101

Heavy vehicle charges determination – RIS February 2014 2

Abbreviations 102

APPENDICES 103 Appendix A: Summary of Review Recommendations 104 Appendix B: The methodology for calculating the cost base and setting the alpha value 107 Appendix C: Detailed usage data 114 Appendix D: Modular ESA calculations 118 Appendix E: ESA updates since 2007 124 Appendix F: Schedule of Charges 125 Appendix G: Attributable Cost Calculations 131 Appendix H: Annual Adjustment Formula 133

Amendment to Model Heavy Vehicle Charges Act 134

Background 134 Determination Recommendation 134 Current Annual Adjustment Methodology 134 Proposed Changes to Annual Adjustment Methodology 135 H-1. Model Heavy Vehicle Charges Act 2008 – Schedule 1 140 H-2. Changes Amendment Act 2010 144 Appendix 3 – Tables currently published in NTC Annual report 148 Appendix I: Case Studies 150

Heavy vehicle charges determination – RIS February 2014 3

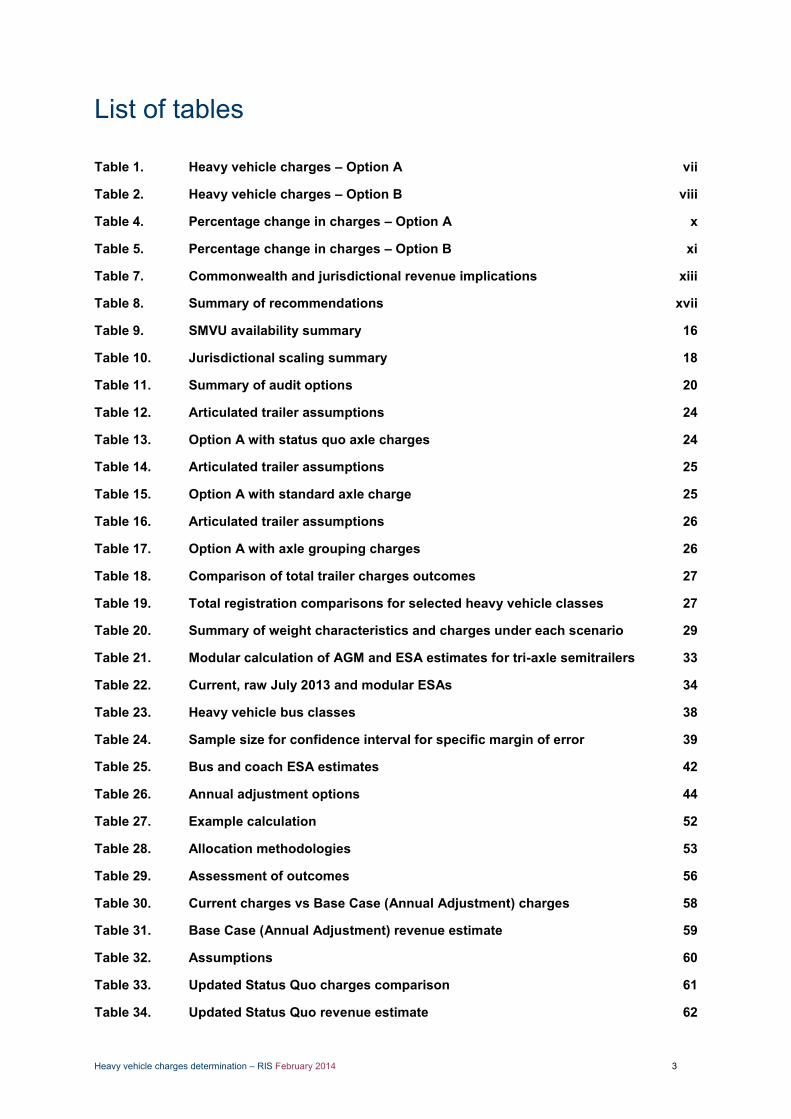

List of tables

Heavy vehicle charges – Option A vii Table 1.

Heavy vehicle charges – Option B viii Table 2.

Percentage change in charges – Option A x Table 4.

Percentage change in charges – Option B xi Table 5.

Commonwealth and jurisdictional revenue implications xiii Table 7.

Summary of recommendations xvii Table 8.

SMVU availability summary 16 Table 9.

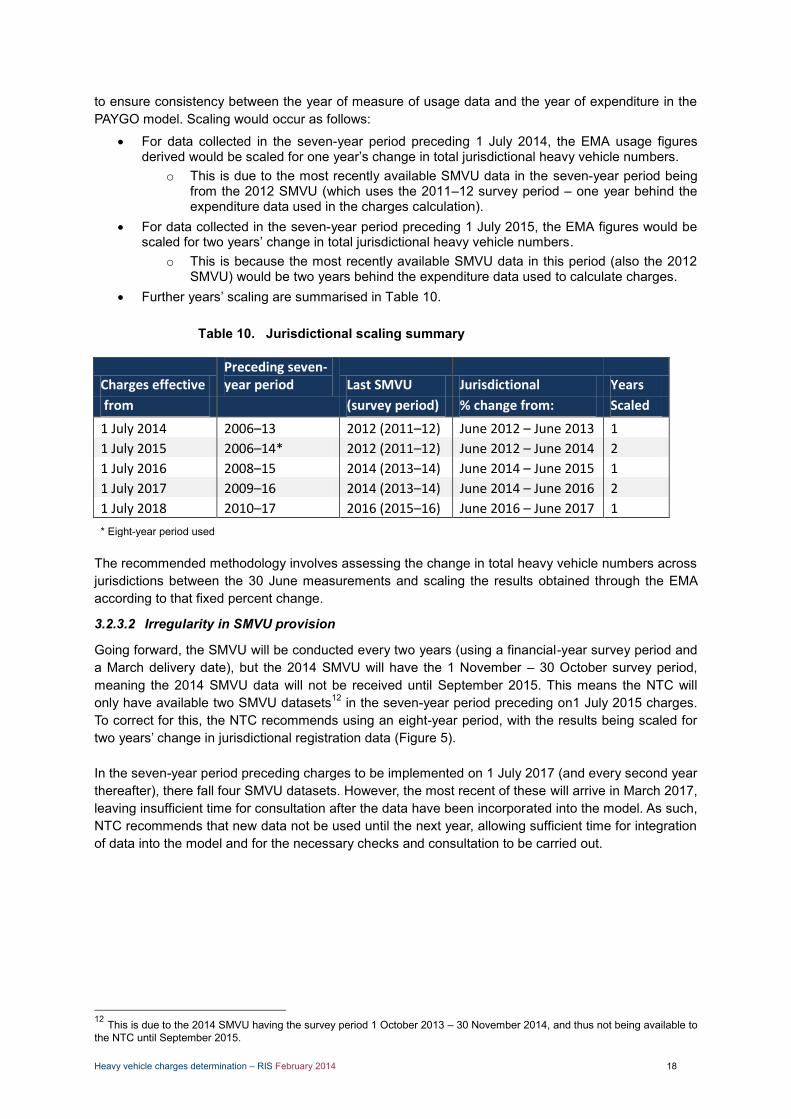

Jurisdictional scaling summary 18 Table 10.

Summary of audit options 20 Table 11.

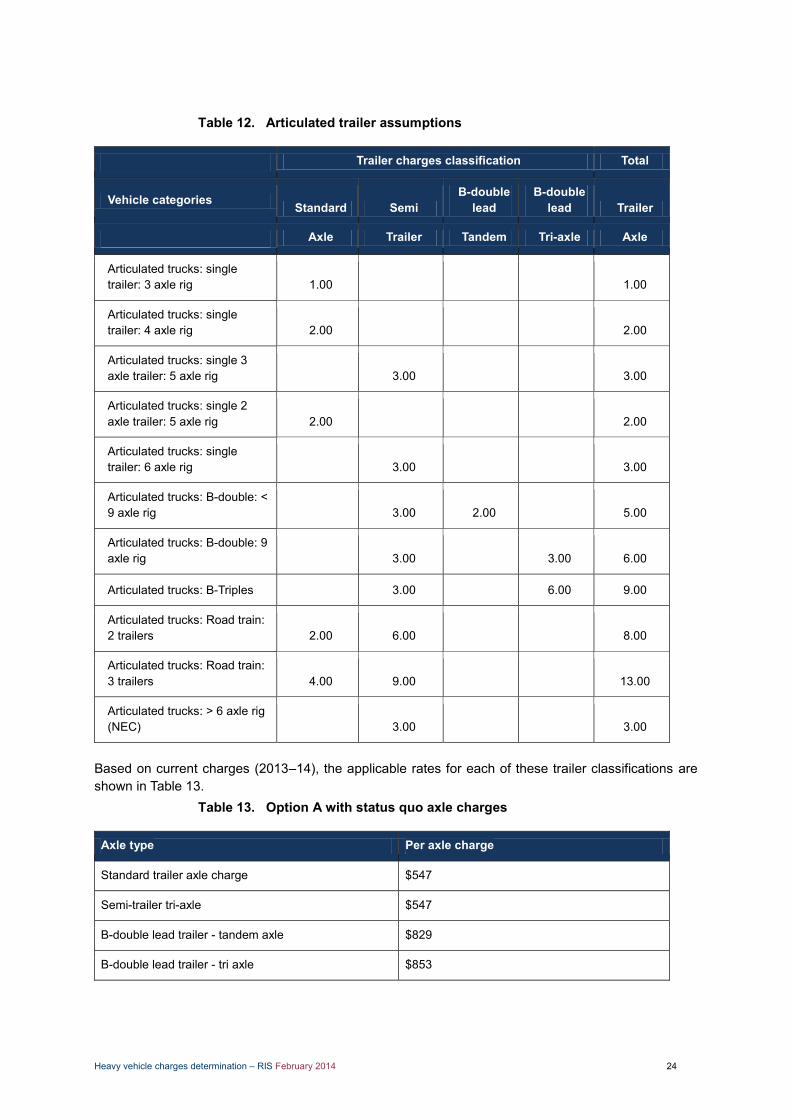

Articulated trailer assumptions 24 Table 12.

Option A with status quo axle charges 24 Table 13.

Articulated trailer assumptions 25 Table 14.

Option A with standard axle charge 25 Table 15.

Articulated trailer assumptions 26 Table 16.

Option A with axle grouping charges 26 Table 17.

Comparison of total trailer charges outcomes 27 Table 18.

Total registration comparisons for selected heavy vehicle classes 27 Table 19.

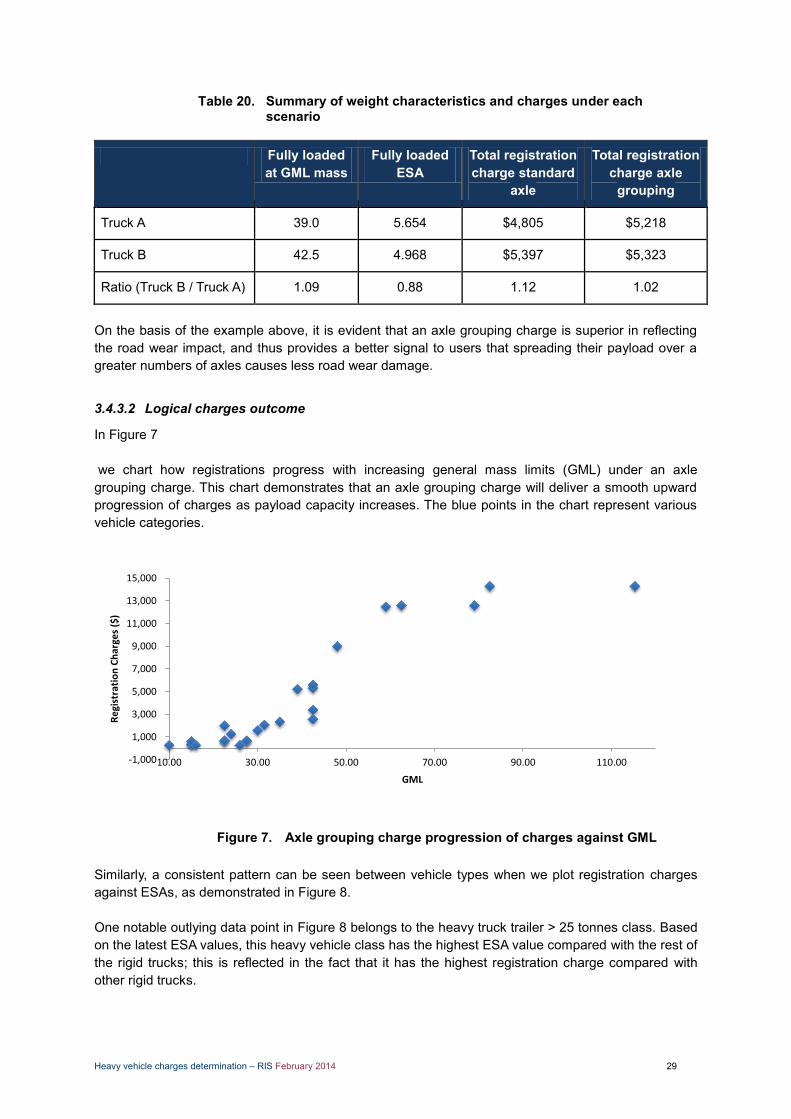

Summary of weight characteristics and charges under each scenario 29 Table 20.

Modular calculation of AGM and ESA estimates for tri-axle semitrailers 33 Table 21.

Current, raw July 2013 and modular ESAs 34 Table 22.

Heavy vehicle bus classes 38 Table 23.

Sample size for confidence interval for specific margin of error 39 Table 24.

Bus and coach ESA estimates 42 Table 25.

Annual adjustment options 44 Table 26.

Example calculation 52 Table 27.

Allocation methodologies 53 Table 28.

Assessment of outcomes 56 Table 29.

Current charges vs Base Case (Annual Adjustment) charges 58 Table 30.

Base Case (Annual Adjustment) revenue estimate 59 Table 31.

Assumptions 60 Table 32.

Updated Status Quo charges comparison 61 Table 33.

Updated Status Quo revenue estimate 62 Table 34.

Heavy vehicle charges determination – RIS February 2014 4

Option A charges comparison 63 Table 35.

Option A revenue estimate 64 Table 36.

Option B charges comparison 65 Table 37.

Option B revenue estimate 66 Table 38.

Option C charges 67 Table 39.

Option C revenue 68 Table 40.

Common assumptions for Options A, B and C 68 Table 41.

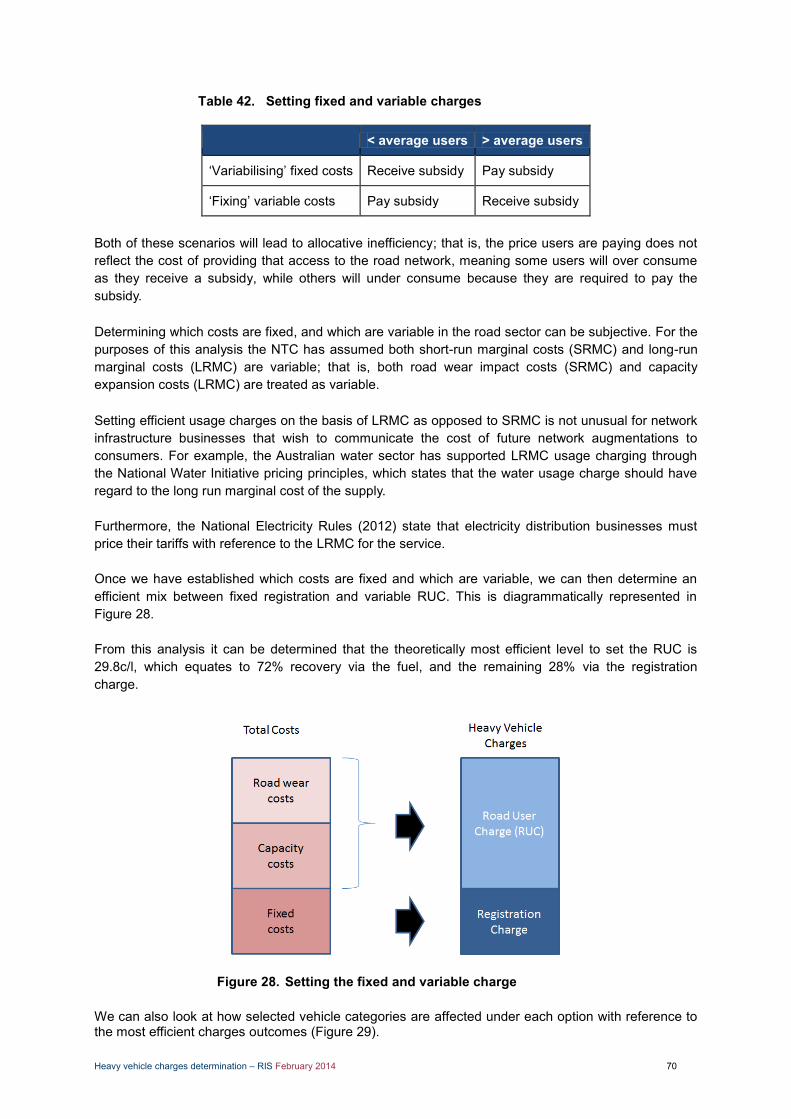

Setting fixed and variable charges 70 Table 42.

Assessment of options against pricing principles 73 Table 43.

Comparison of percentage change in charges paid 80 Table 44.

Jurisdictional cost recovery summary 86 Table 45.

Difference in total revenue raised under Option A compared with Base Case Table 46.(annual adjustment) 87

Heavy Vehicle charges – Option A 89 Table 47.

Heavy Vehicle charges – Option B 90 Table 48.

Axle grouping charges – Options A, B and C 91 Table 50.

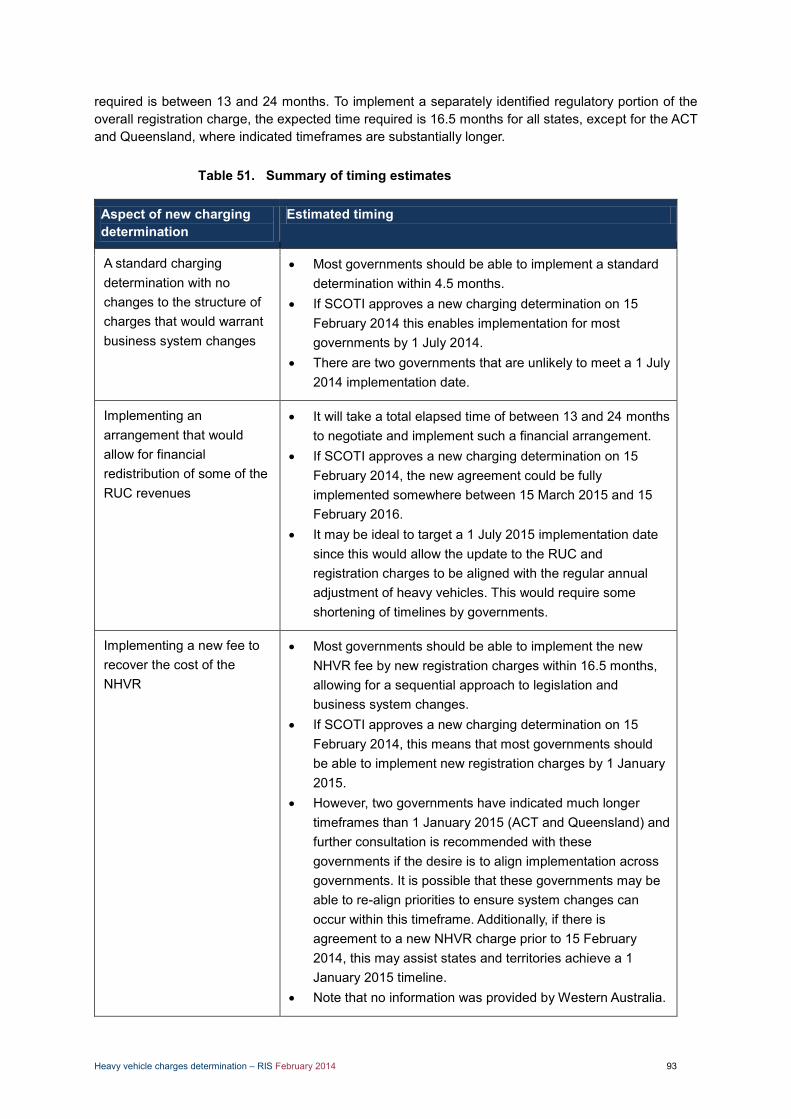

Summary of timing estimates 93 Table 51.

Process steps and estimated time taken to negotiate and implement a Table 52.redistribution of RUC revenues 96

Estimate of de-averaged heavy-vehicle-related road expenditure (1997 to 2012)107 Table 53.

Historic comparison of averaging methodologies 112 Table 54.

VKT 114 Table 55.

Vehicle numbers 115 Table 56.

Fuel use 116 Table 57.

GTK 117 Table 58.

Heavy vehicle charges determination – RIS February 2014 5

List of figures

Figure 1. Interrelationship with HVCI project 8

Figure 2. Timing difference illustration 11

Figure 3. Fuel use example – seven-year trend displaying negative results 16

Figure 4. Fuel use and VKT totals 17

Figure 5. SMVU use in usage data calculation 19

Figure 6. Two articulated configurations with similar payload capacity 28

Figure 7. Axle grouping charge progression of charges against GML 29

Figure 8. Axle grouping charge – progression of charges against ESA 30

Figure 9. Unlikely heavy vehicle configurations 32

Figure 10. Example of data mining used to identify unlikely heavy vehicle configurations 32

Figure 11. Example of problem vehicle configurations 33

Figure 12. Current, raw July 2013 and modular ESAs 35

Figure 13. ESA updates since 2007 36

Figure 14. Vehicle identification process used by heavy vehicle checking stations in NSW39

Figure 15. Example of TruckScan data results (NSW data only, two-axle buses ≥ 10t) 40

Figure 16. Sample axle load calculation 40

Figure 17. Sample bus usage profile 41

Figure 18. Sample urban bus loading profiles 41

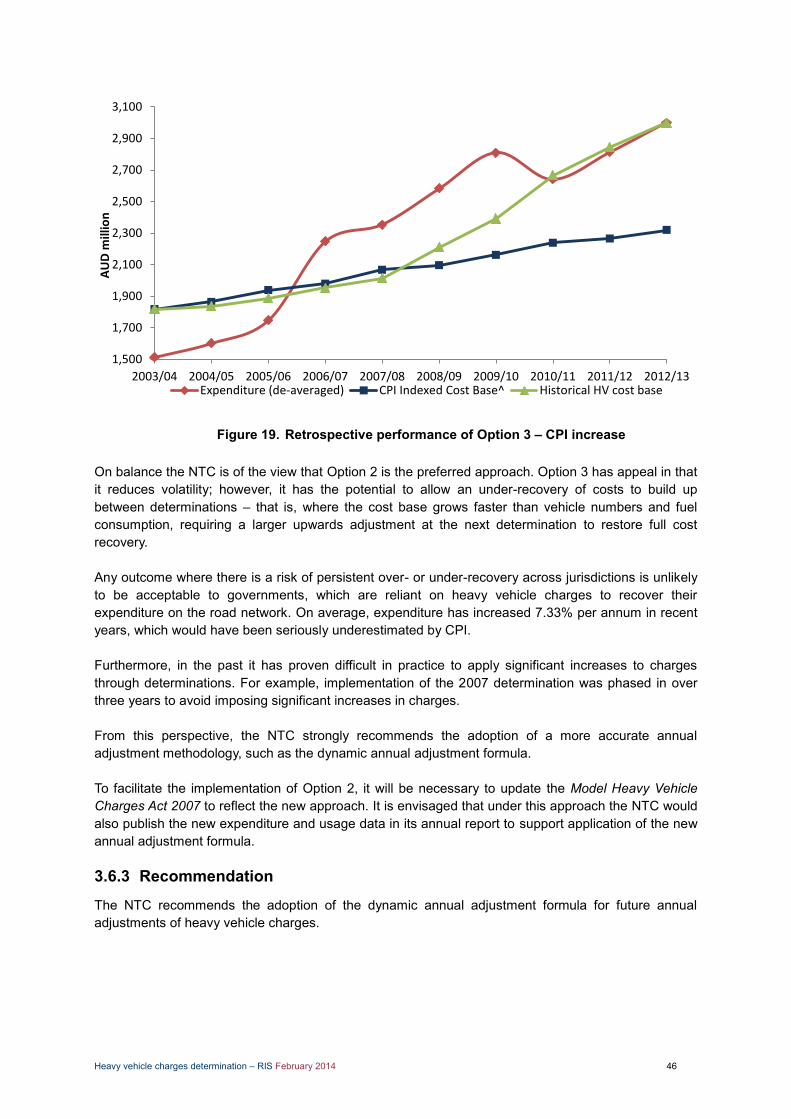

Figure 19. Retrospective performance of Option 3 – CPI increase 46

Figure 20. B-triple vs double road train – status quo registration comparison 48

Figure 21. Registration charge comparison – with and without dolly discount (Option A) 48

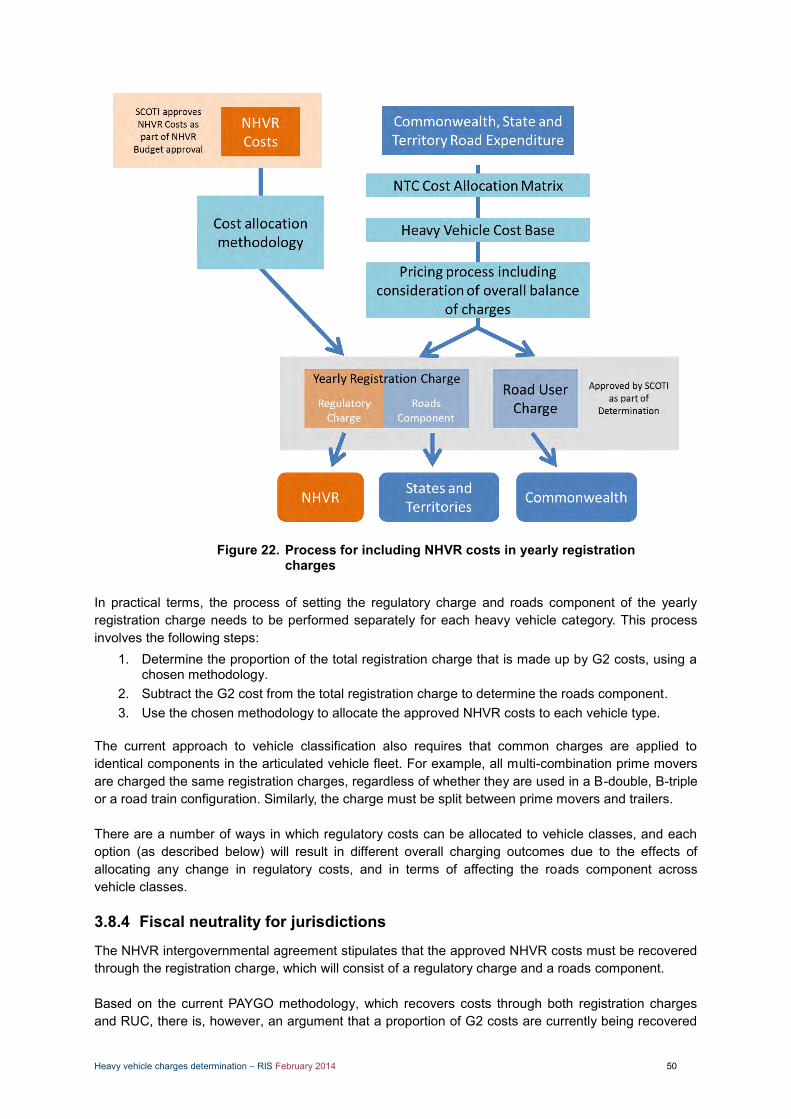

Figure 22. Process for including NHVR costs in yearly registration charges 50

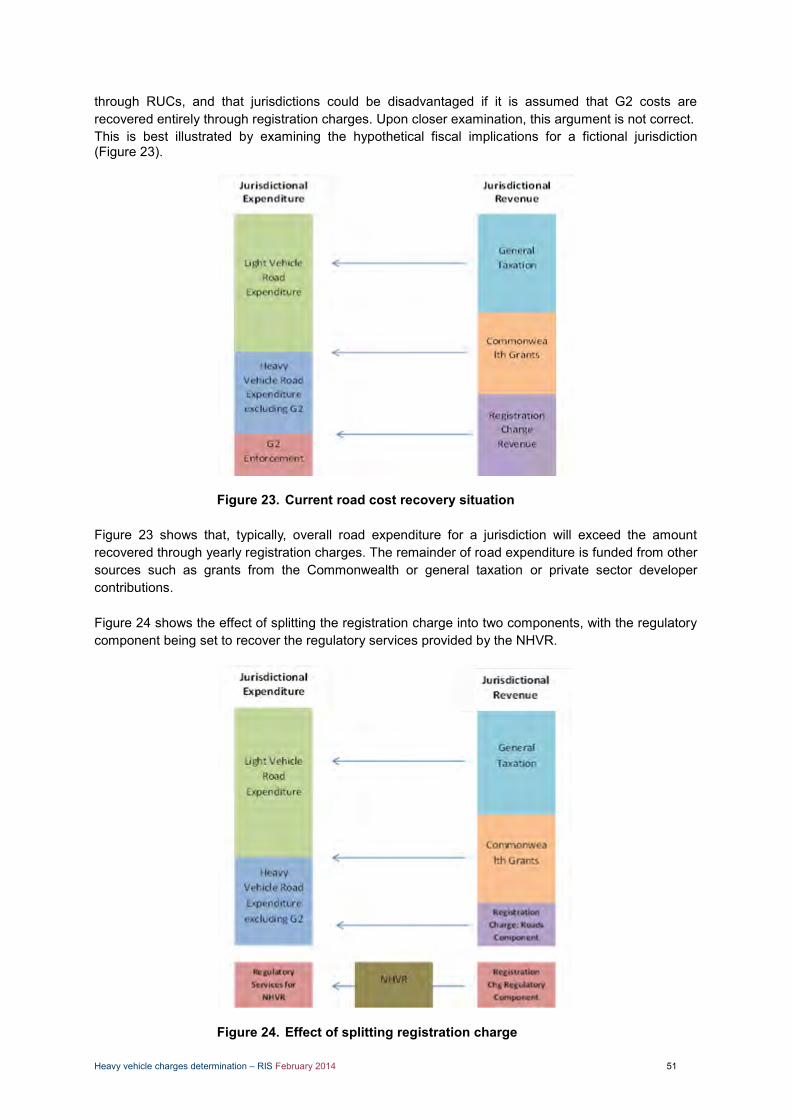

Figure 23. Current road cost recovery situation 51

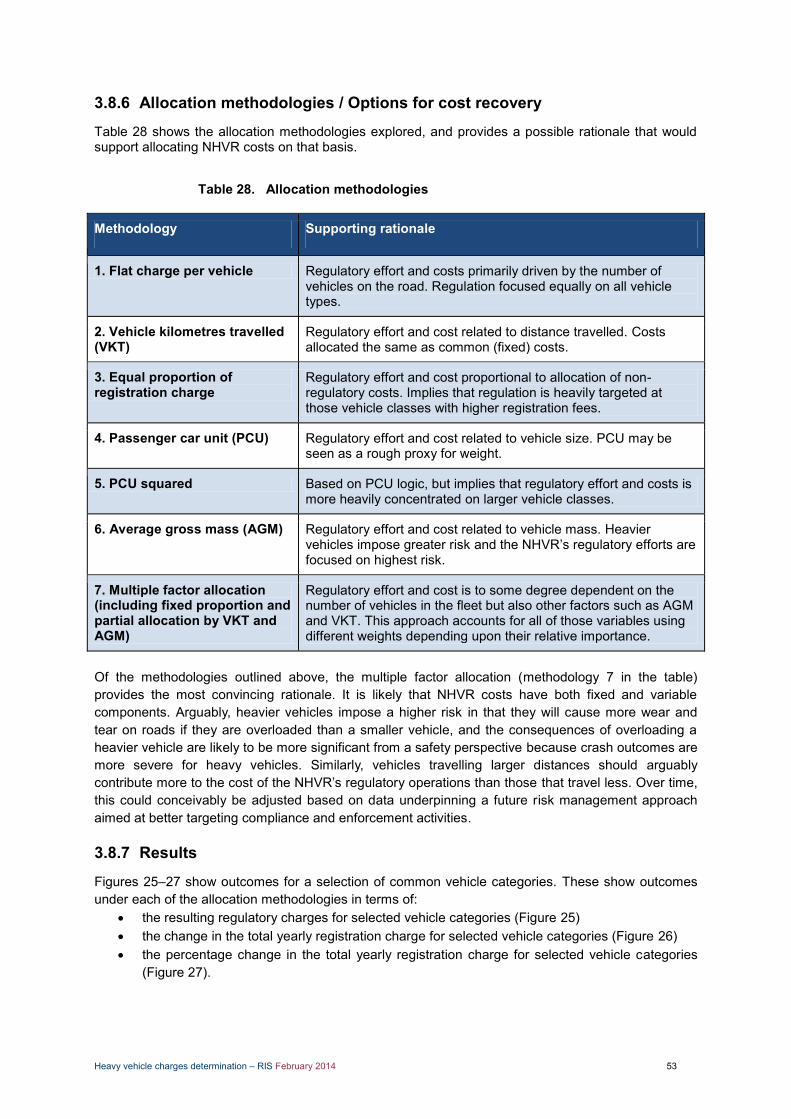

Figure 24. Effect of splitting registration charge 51

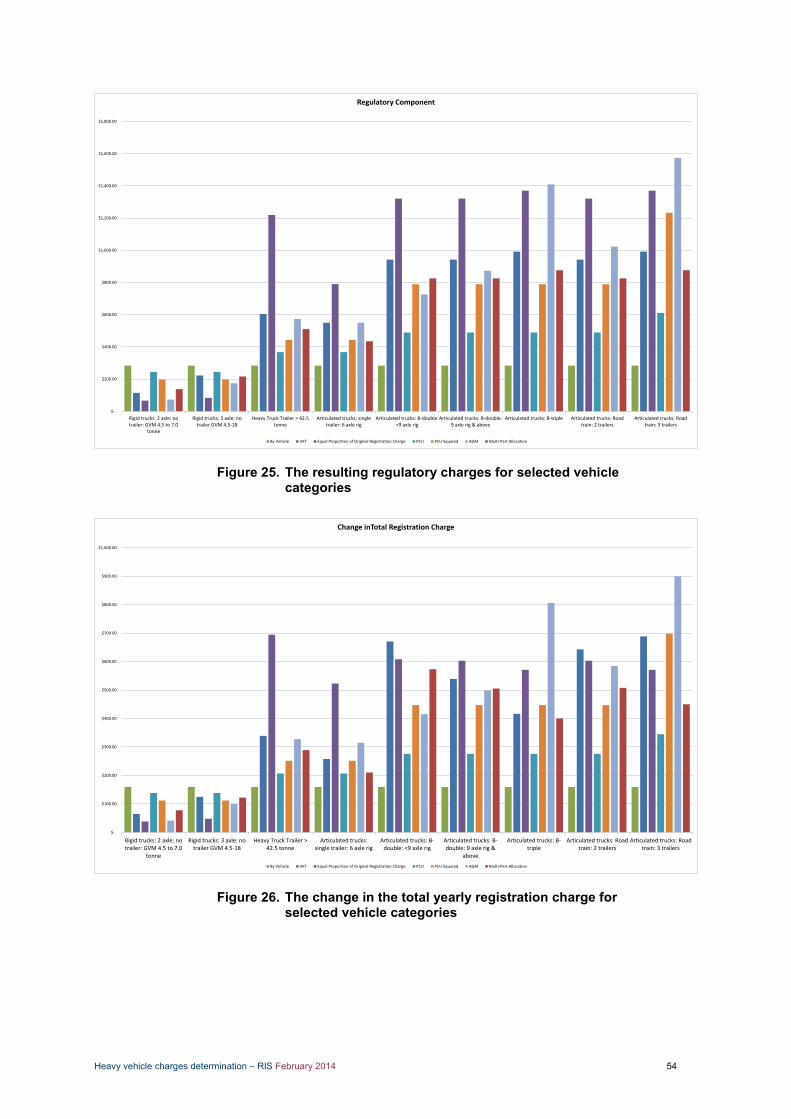

Figure 25. The resulting regulatory charges for selected vehicle categories 54

Figure 26. The change in the total yearly registration charge for selected vehicle categories54

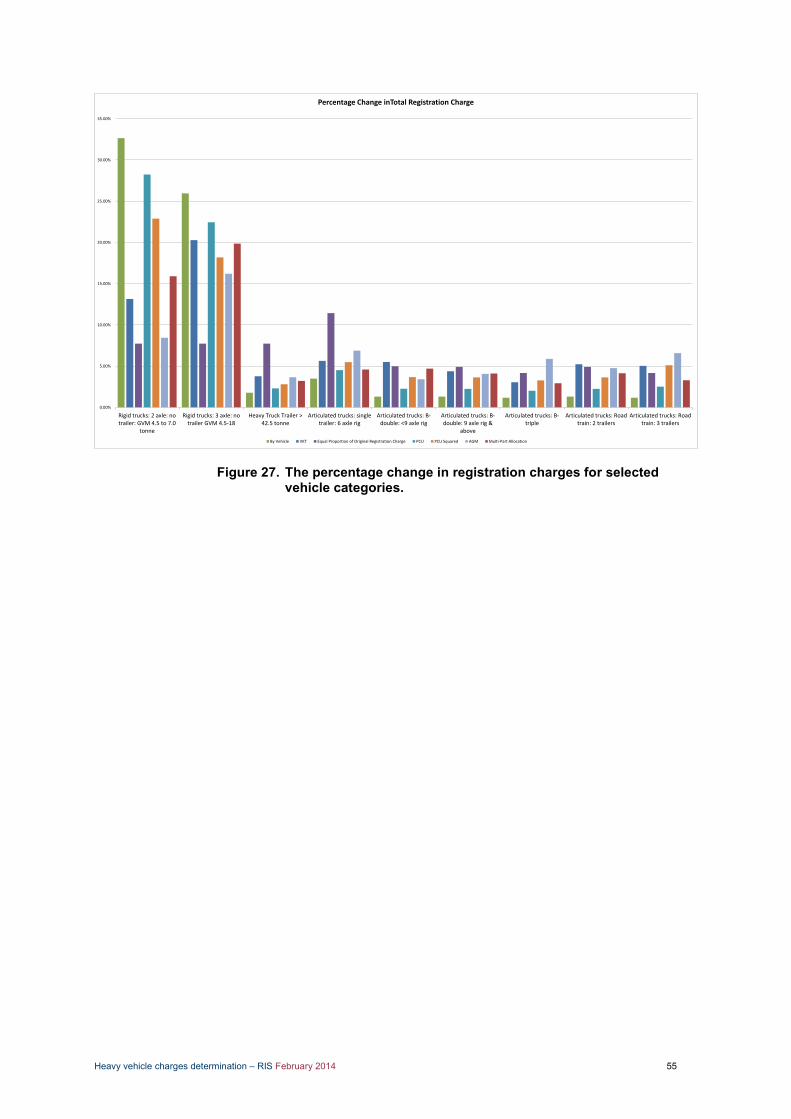

Figure 27. The percentage change in registration charges for selected vehicle categories.55

Figure 28. Setting the fixed and variable charge 70

Figure 29. Distributional efficiency impact on different vehicle type 71

Figure 30. Headroom analysis 72

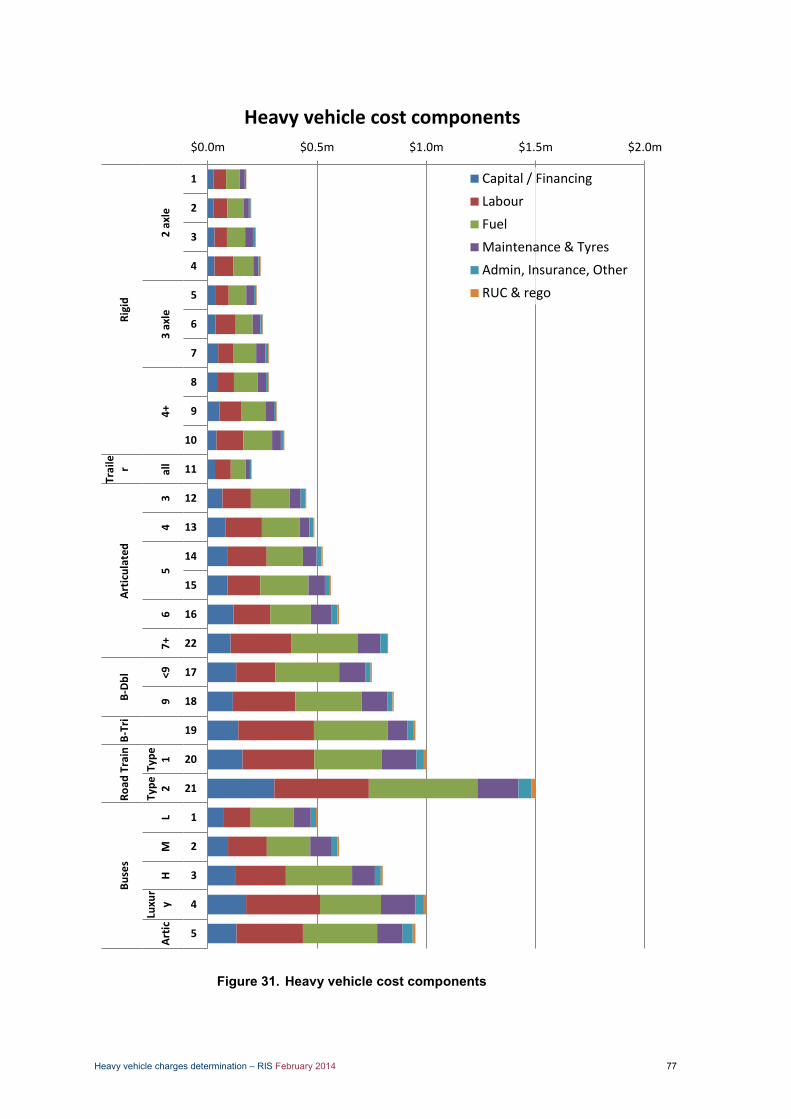

Figure 31. Heavy vehicle cost components 77

Figure 32. Cost of transporting freight per vehicle type 78

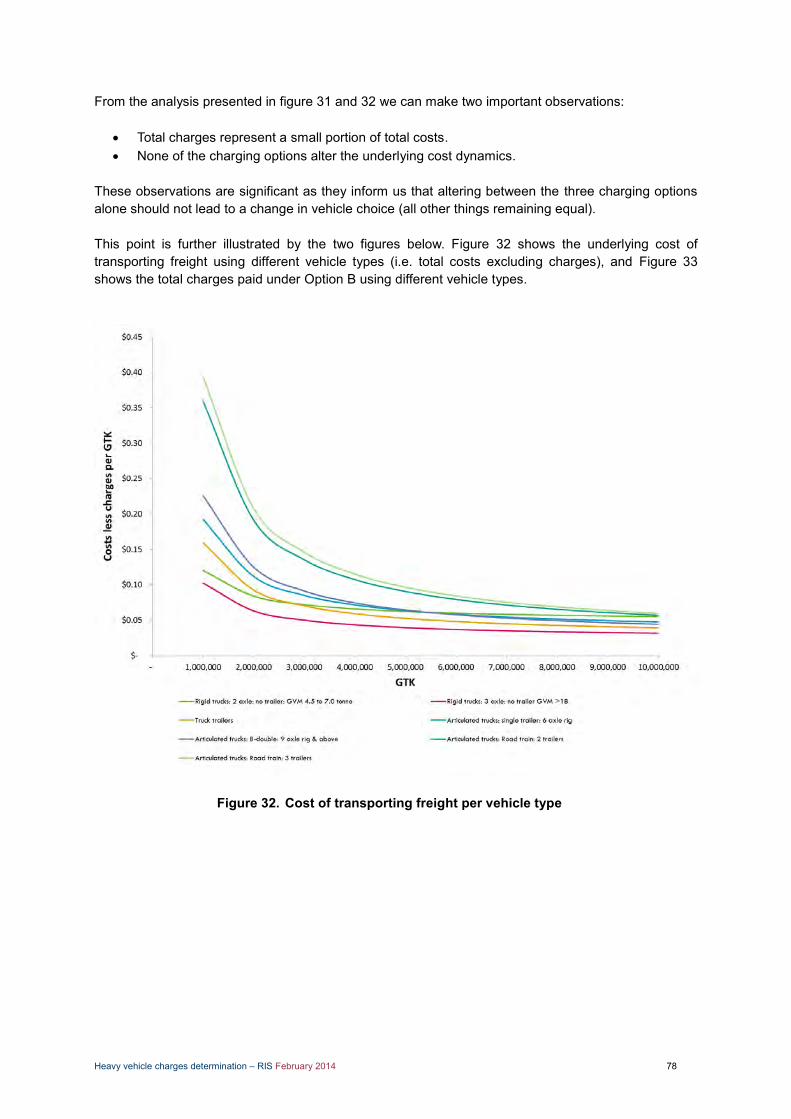

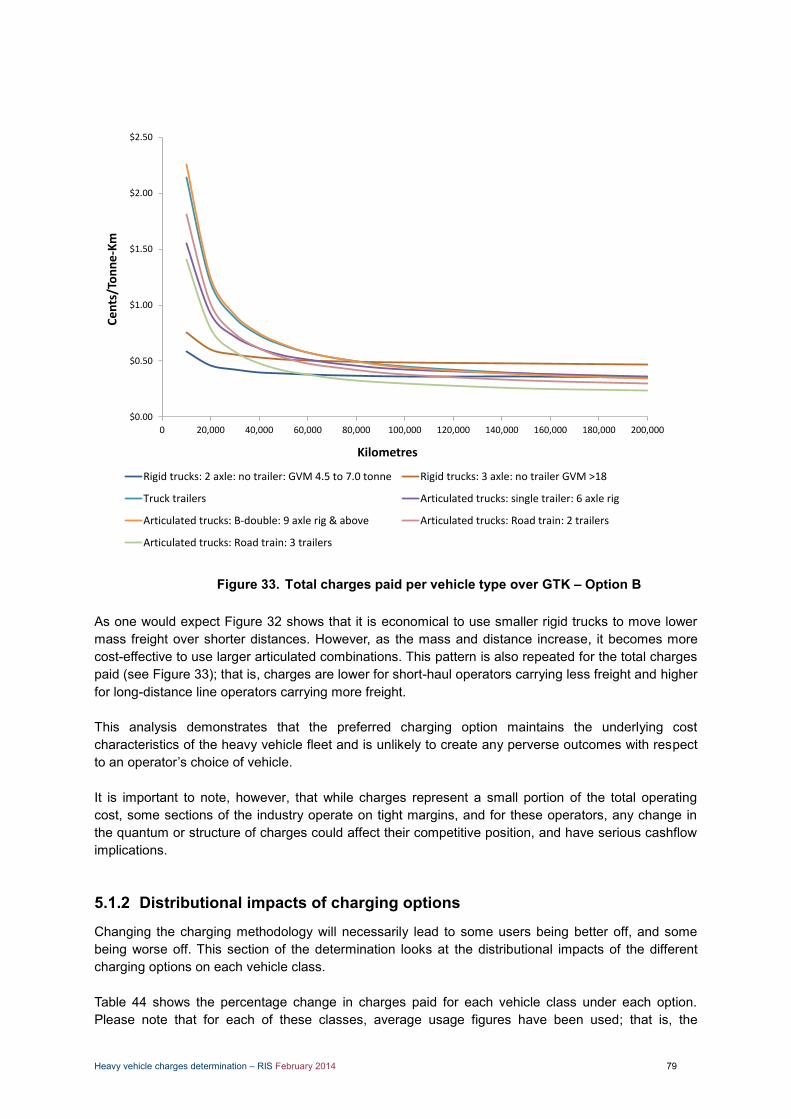

Figure 33. Total charges paid per vehicle type over GTK – Option B 79

Heavy vehicle charges determination – RIS February 2014 6

Figure 34. Rigid truck: 2 axle: no trailer: GVM 4.5 to 7.0 tonne 81

Figure 35. Rigid truck: 3 axle: no trailer: GVM > 18 tonne 81

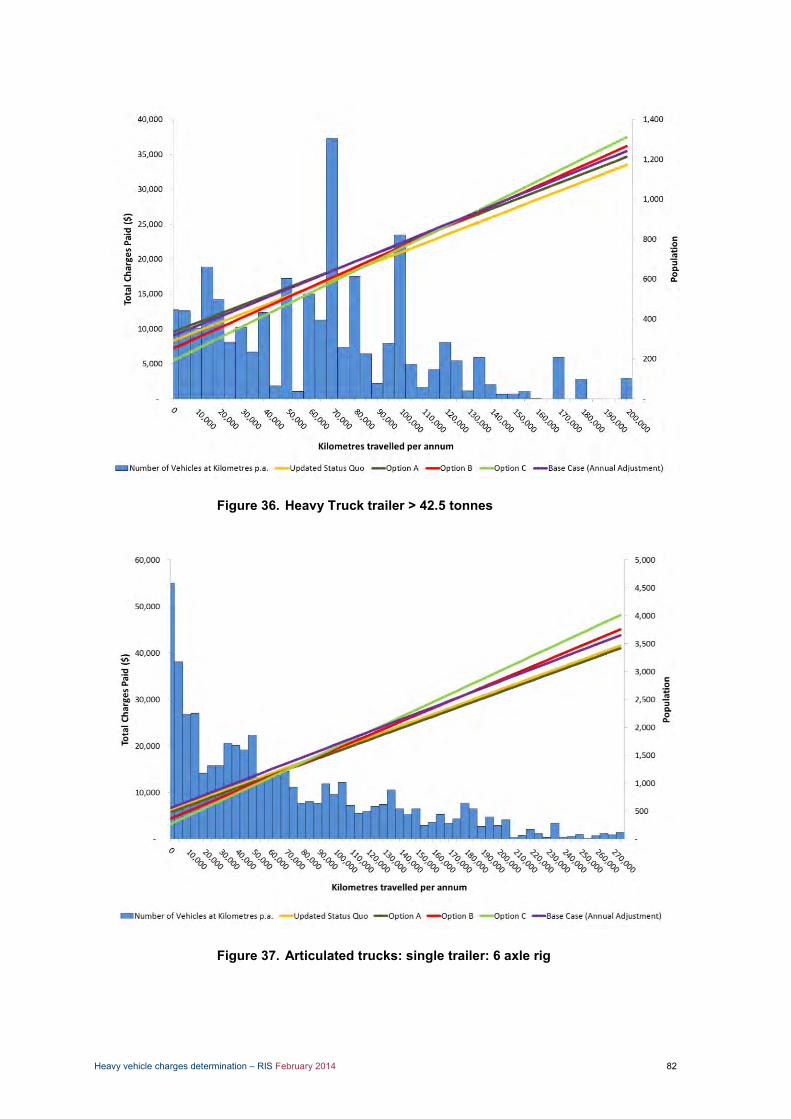

Figure 36. Heavy Truck trailer > 42.5 tonnes 82

Figure 37. Articulated trucks: single trailer: 6 axle rig 82

Figure 38. Articulated trucks: B-double: 9 axle rig & above 83

Figure 39. Articulated trucks: Road Train: 2 trailers 83

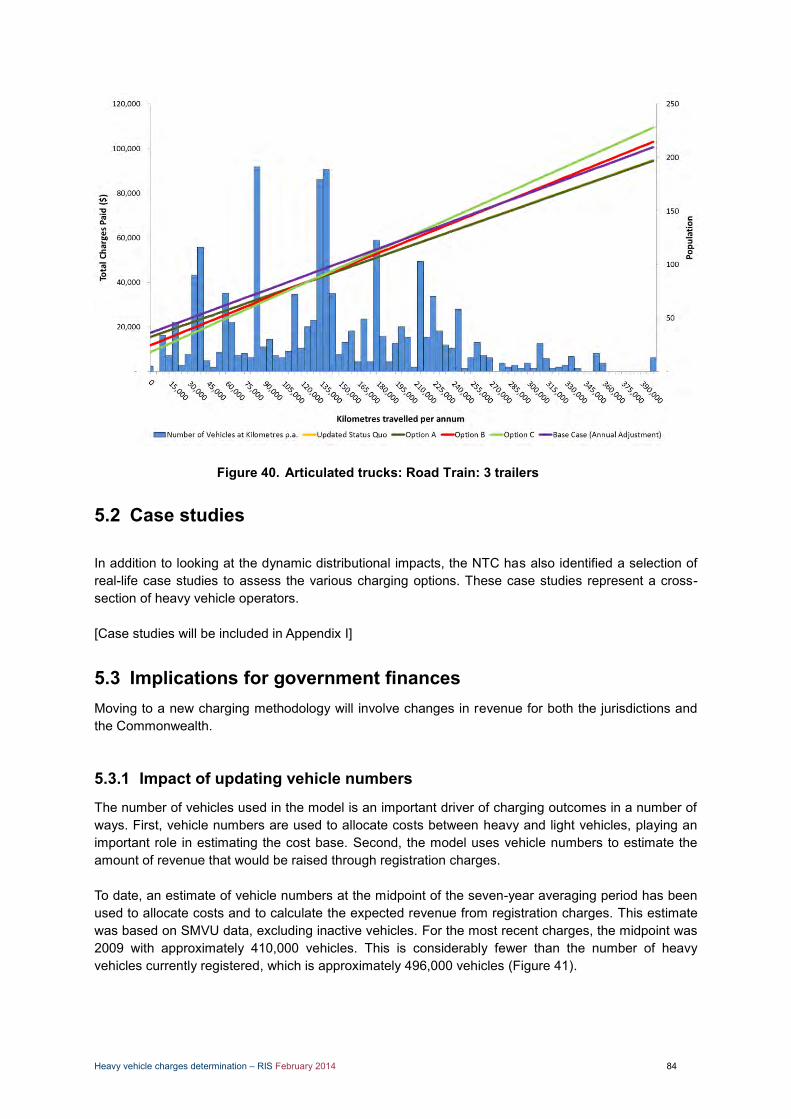

Figure 40. Articulated trucks: Road Train: 3 trailers 84

Figure 41. Number of heavy vehicles, 2003–2013 85

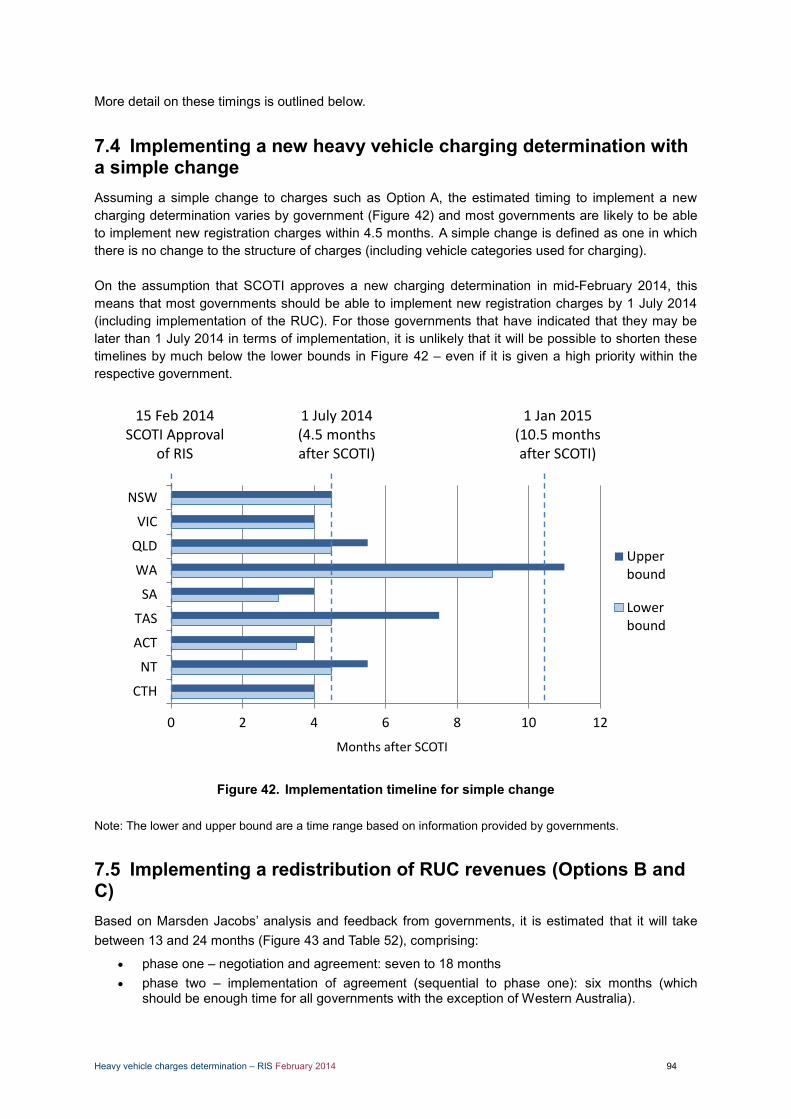

Figure 42. Implementation timeline for simple change 94

Figure 43. Estimated time to negotiate and implement a redistribution of RUC 95

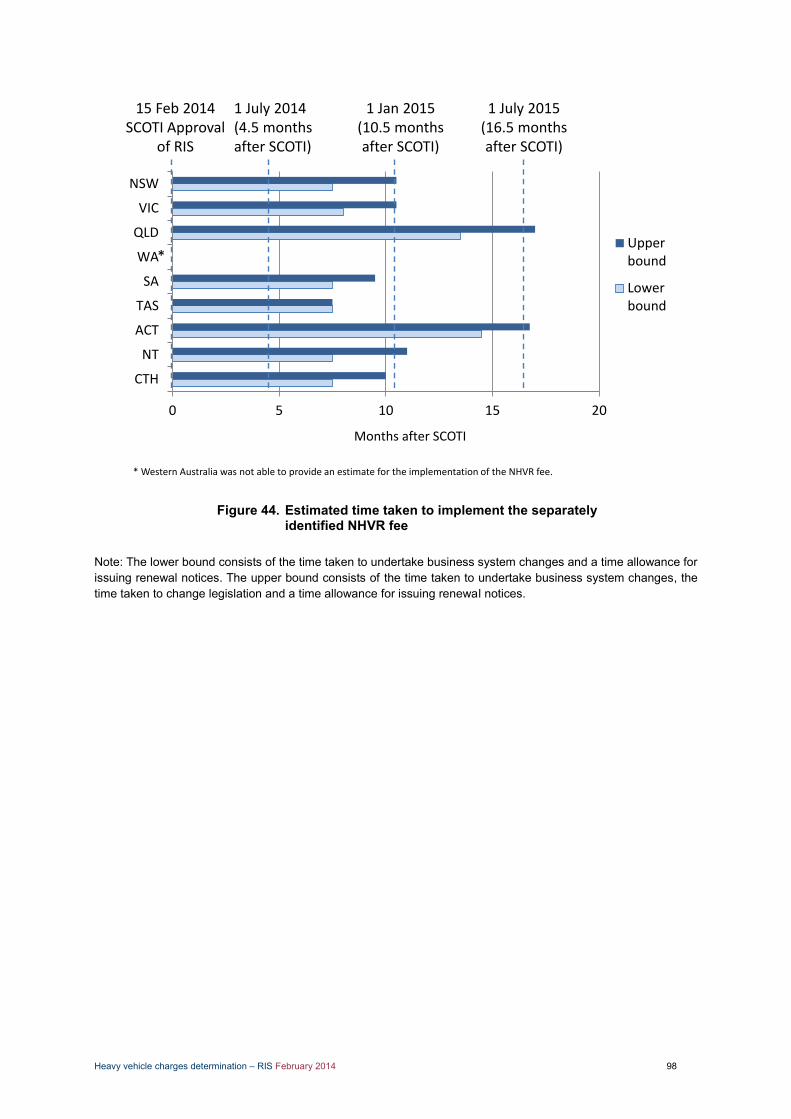

Figure 44. Estimated time taken to implement the separately identified NHVR fee 98

Figure 45. Bounded normal distribution 108

Figure 46. Cost base scenario testing using past expenditure 109

Figure 47. Frequency distribution of optimal alpha (equal weights) 110

Figure 48. Trade-off between FCR, OU and SM: a stylised example 110

Figure 49. Frequency distribution of optimal alpha (differentiated weights) 111

Figure 50. Weights for EMA7 with alpha value equal to 0.50 112

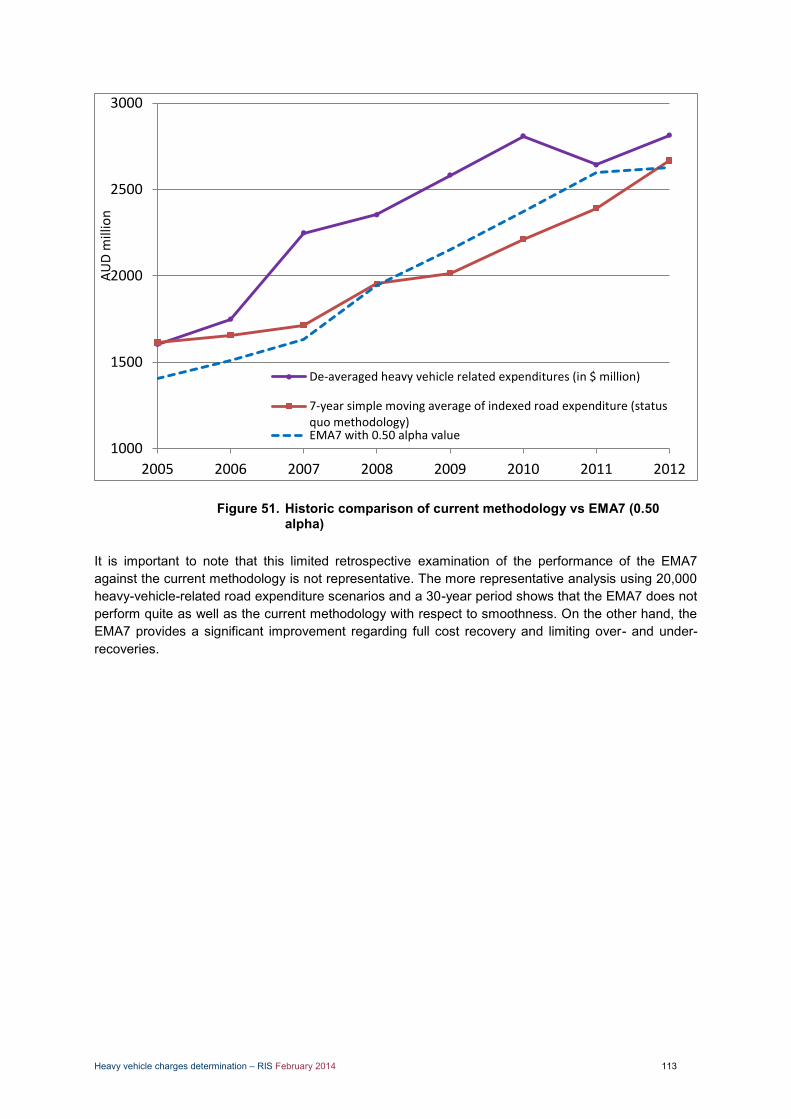

Figure 51. Historic comparison of current methodology vs EMA7 (0.50 alpha) 113

Heavy vehicle charges determination – RIS February 2014 7

1. Introduction

1.1 Background Heavy vehicles in Australia are defined as any vehicle weighing 4.5 tonnes or heavier. These vehicles are charged an annual registration charge and a road user charge (RUC), which is levied on each litre of diesel fuel. These charges are determined according to a charging framework known as PAYGO. The primary objective of PAYGO or ‘pay as you go’ is to deliver nationally consistent heavy vehicle charges that recover both capital and operating costs related to heavy vehicle use in the year they are incurred. These charges are designed to promote the optimal use of the existing network. The National Transport Commission (NTC) has been administering the PAYGO system for almost two decades. During that time the NTC has completed several heavy vehicle charges determinations aimed at refining the PAYGO system. This determination was initiated after the ‘A-trailer’ review of February 2012, when it became apparent that the structure of charges was potentially inhibiting the use of safer and more productive vehicles. The ‘A trailer’ review also highlighted a number of limitations in both source data and methodology when calculating a final schedule of charges.

1.2 SCOTI directions to NTC In November 2012 the Standing Council on Transport and Infrastructure (SCOTI) directed the NTC to complete a comprehensive review of the heavy vehicle charging system in a two-step process. Step 1 was a comprehensive review of the current heavy vehicle charging system (the review), followed by Step 2, a new determination that recommends heavy vehicle charges based on the findings and recommendations of the completed review. The comprehensive review stage was completed in 2012 and early 2013, with the final policy paper published in May 2013. At its May 2013 meeting SCOTI endorsed NTC to proceed with a determination on the basis of the review recommendations, with one of the key recommendations being to include options for raising the RUC above its current level6. This determination builds upon the findings and analysis of the review and fulfils the second step of the review and determination process. The recommended charges, if approved, will be implemented from 1 July 2014. It is acknowledged that implementation may need to occur in multiple steps.

1.3 Consultation process The NTC has carried out the review and determination processes in cooperation with a wide range of stakeholders. The adoption of a ‘co-design’ approach has been a key feature of this process, which has resulted in a shared understanding of issues among stakeholders and co-ownership of outcomes. In completing the heavy vehicle charges review, the NTC conducted wide-ranging consultation activities including:

an initial scoping workshop policy development workshops a modelling workshop Australia-wide consultation forums bilateral consultation sessions.

6 A full summary of the review recommendations can be found in Appendix A.

Heavy vehicle charges determination – RIS February 2014 8

In progressing to the determination, the NTC committed to undertaking a similar level of consultation.

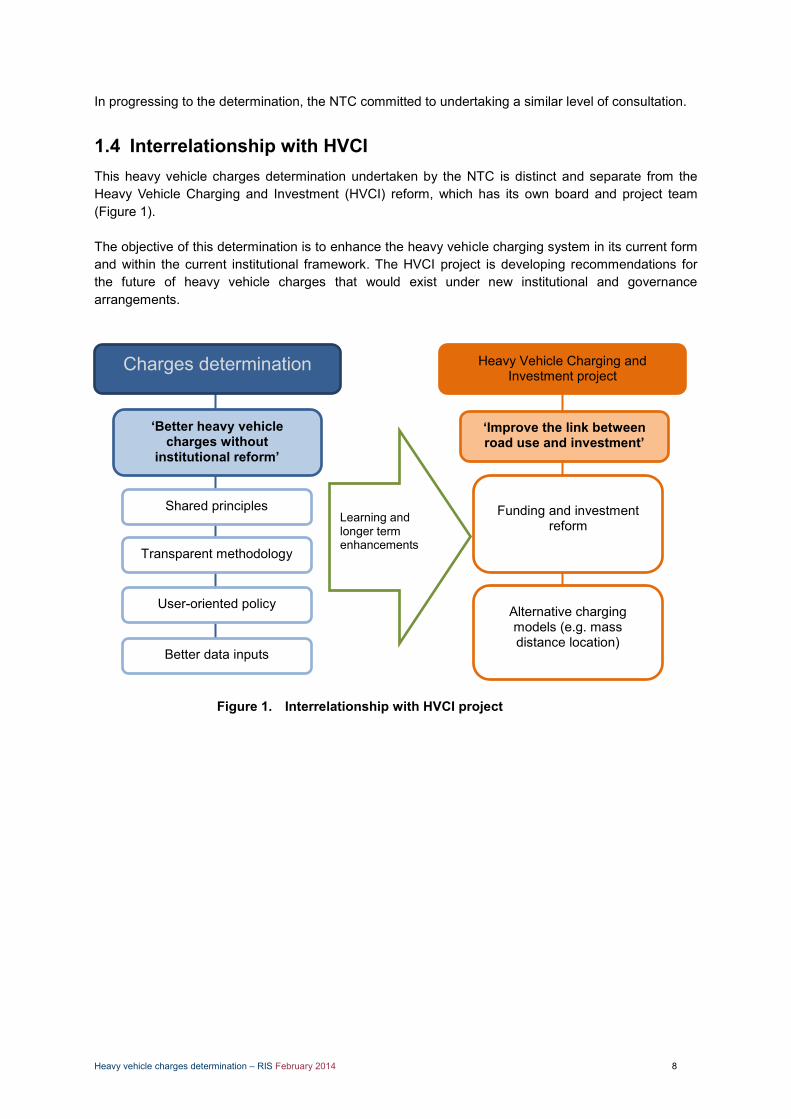

1.4 Interrelationship with HVCI This heavy vehicle charges determination undertaken by the NTC is distinct and separate from the Heavy Vehicle Charging and Investment (HVCI) reform, which has its own board and project team (Figure 1). The objective of this determination is to enhance the heavy vehicle charging system in its current form and within the current institutional framework. The HVCI project is developing recommendations for the future of heavy vehicle charges that would exist under new institutional and governance arrangements.

Figure 1. Interrelationship with HVCI project

Charges determination Heavy Vehicle Charging and Investment project

‘Better heavy vehicle charges without

institutional reform’

Shared principles

‘Improve the link between road use and investment’

Transparent methodology

User-oriented policy

Better data inputs

Alternative charging models (e.g. mass distance location)

Learning and longer term enhancements

Funding and investment reform

Heavy vehicle charges determination – RIS February 2014 9

2. Defining the problem

2.1 Cost recovery over time in an efficient and equitable manner The overarching regulatory problem for this determination is to recommend an efficient and equitable set of heavy charges that adequately recovers the cost of road construction and maintenance for heavy vehicles in Australia. In doing so, the NTC is required to adhere to the pricing principles that originate from the Australian Transport Council (ATC) (the predecessor of SCOTI) and the Council of Australian Governments (COAG). The principles are: ‘National heavy vehicle road use prices should promote optimal use of infrastructure, vehicles and transport modes. This is subject to the following:

full recovery of allocated infrastructure costs while minimising both the over and under recovery from any class of vehicle

cost effectiveness of pricing instruments transparency the need to balance administrative simplicity, efficiency and equity (e.g. impact on regional

and remote communities/access) the need to have regard to other pricing applications such as light vehicle charges, tolling and

congestion.’

Following the Productivity Commission's inquiry into road and rail infrastructure pricing, the ATC provided further direction to the NTC: ‘ATC direct the NTC, in developing its determination, to apply principles and methods that ensure the delivery of full cost recovery in aggregate, further develop indexation adjustment arrangements to ensure the ongoing delivery of full expenditure recovery in aggregate and remove cross-subsidisation across different heavy vehicle classes, recognising that transition to any new arrangement may require a phased approach’ (COAG 2007). As part of the review process, the NTC has identified several secondary problems, which are addressed in this report:

What is the best way to calculate the cost base? How to produce a consistent set of usage data? How to ensure accurate and consistent reporting of expenditure data? How will the accountability of jurisdictional cost submissions be increased? What is the most efficient and equitable structure for heavy vehicle charges in terms of axle

charging and split between RUC and registration? How can the methodology for calculating pavement wear impacts of different vehicle classes

be improved? How should heavy vehicle charges be appropriately adjusted from one year to the next? What is the most appropriate approach to concessions, rebates and road train adjustments? What is the most appropriate mechanism for recovering National Heavy Vehicle Regulator

(NHVR) costs in accordance with the NHVR intergovernmental agreement?

Heavy vehicle charges determination – RIS February 2014 10

2.2 Inherent limitations of the current charging framework While this determination seeks to address as many of the outstanding issues associated with the current heavy vehicle charging system as possible, there are inherent limitations that cannot be resolved without more extensive reform, as being considered through the HVCI project. These limitations are outlined below.

2.2.1 Averaging

It is common for an infrastructure charging regime to apply averaging to some degree, as deriving a user’s precise cost on the network is ether impossible or too costly to ascertain. The PAYGO charging framework in particular uses multiple levels of averaging to calculate heavy vehicle charges. This includes averaging multiple usage parameters and expenditure of jurisdictions.

2.2.1.1 Averaging usage data

The charging model uses Survey of Motor Vehicle Use (SMVU) data from the Australian Bureau of Statistics (ABS) for vehicle kilometres travelled (VKT), fuel consumption and gross tonne kilometres (GTK) for each vehicle category. These inputs are in the form of an average for each vehicle class. The result of this approach is that users within a vehicle class who travel less, or weigh less than the average, will pay a higher cost per tonne/kilometre than another user who travels above the average. This ‘inequity’ within vehicle class typically affects certain types of operators (e.g. primary producers who only use their vehicle seasonally to move livestock from the paddock to the point of sale). Similarly, volume-constrained operators will fare differently to mass-constrained operators. Effectively, the fact that charges for different vehicle classes are set based on average usage characteristics creates ‘winners and losers’. Which operators end up ‘winning‘ or ‘losing‘ depends on the structure of charges and the balance between registration and the RUC.

2.2.1.2 Averaging state expenditure

The heavy vehicle cost base is derived by averaging heavy-vehicle-related road expenditure across all jurisdictions. Heavy vehicle charges are then set to recover the annualised amount. However, this methodology does not ensure that the revenue returned to state or territory equals their historic or future expenditure, thus creating a disjoint between investment and revenue. This disjoint creates perverse incentives for jurisdictions when undertaking both maintenance and capital works, as the jurisdiction undertaking new works will not recoup the full value of the expenditure, while those jurisdictions who did not undertake the work will benefit, thus introducing geographic cross-subsidisation.

2.2.2 Input data limitations

The PAYGO model uses SMVU datasets from the ABS to calculate heavy vehicle charges. The ABS published these datasets annually until 2007. No data was collected in 2008 or 2009. In 2010 the survey recommenced, with the collection frequency reduced to once every two years (biennually). Reducing the frequency of the SMVU to once every two years has reduced its reliability and accuracy. Furthermore, the SMVU dataset originates from a survey rather than a full census of heavy vehicle usage, making it an estimate rather than a precise measure. This is reflected in the standard errors associated with certain vehicle classes. A further limitation of the survey method used to produce the SMVU dataset is the self-report method of data collection. Poor recollection of the required information or misunderstanding of the question can contribute to inaccuracies in the data.

Heavy vehicle charges determination – RIS February 2014 11

2.2.3 Non-deterministic charge setting framework

The NTC makes what is effectively a recommendation on national charges, which is not technically binding on state and territory governments. Non-implementation and a wide range of concessions being offered across state and territory governments have the potential to undermine the national nature of the charges. The charging framework also lacks an appropriate governance framework to provide guidance on the triggering conditions for new heavy vehicle charges determinations. This lack of clarity leads to price reviews being initiated on an ad hoc basis.

2.2.4 Lag between cost base measurement and implementation of charges

The current PAYGO methodology involves a lag between the measurement of the cost base and the implementation of charges that are set to recover the cost base. For example, the charges outlined in this draft regulatory impact statement are based on expenditure data for the seven years up to, and including, the 2012–13 financial year. However, any charges approved by SCOTI would not become effective until 1 July 2014 at the earliest. This has always been a feature of PAYGO and any associated annual adjustment mechanism. Figure 2 illustrates the delay.

Figure 2. Timing difference illustration Under PAYGO, the expenditure data and vehicle numbers estimated after the end of Year 1 (based on the seven years of expenditure and fuel consumption data leading up to and including Year 1) are used to determine the cost base and set charges that then apply throughout Year 3. These charges are collected in year 3 from the number of vehicles registered in Year 3, and on the amount of fuel used in Year 3. Changes in the estimated cost base over time will be different from changes in vehicle numbers and fuel use. This is illustrated above where the cost base expands more rapidly (measured as a

Heavy vehicle charges determination – RIS February 2014 12

percentage change) than either the number of registered vehicles or fuel consumption. Where this is the case, the following outcomes are likely to occur:

Actual revenue in Year 3 will usually be higher than the expected revenue calculated at the time the charges are set. This is because expected revenue is calculated on the basis of vehicle numbers and fuel consumption in Year 1 because this is the latest available information when charges are set.

Where the cost base expands rapidly it is possible that actual revenue in Year 3 is lower than the cost base would be for that year.

Over time, revenue will ‘catch up’ to the cost base during periods where the cost base grows more slowly than the combined revenue base of fuel consumption and vehicle numbers.

Even under a worst-case scenario where growth in the cost base permanently outpaces the combined growth in fuel consumption and vehicle numbers, the outcome is that the growth in revenue will lag the growth in the cost base. However, in the long run, total revenue will exceed total expenditure due to the revenue uplift provided by the growth in fuel consumption and vehicle numbers.

The only effective way to eliminate circumstances where there is a delay in collecting the appropriate level of revenue (to match the actual cost base) would be to set charges based on a forward looking cost base derived from forecast expenditure. While adopting a forward-looking cost base would be desirable for a number of reasons, this is a formidable task and cannot be achieved within the timeframe of this determination. This issue is currently being explored by the HVCI project.

Heavy vehicle charges determination – RIS February 2014 13

3. Technical improvements SCOTI asked the NTC to proceed with this determination on the basis of the review recommendations. A number of the review recommendations were final and these have been directly incorporated in the options presented in this determination. The review also contained a number of recommendations that required further work to be undertaken as part of the determination. These recommendations are explored in the remainder of this section, which builds on the recommendations that were made to transport ministers in the final review.

3.1 Calculating the cost base

3.1.1 Background

The heavy vehicle cost base is derived from total road expenditure reported by states and territories each year. It includes arterial road expenditure data provided by states and territories, as well as local road expenditure data from the ABS. Until the 2007 determination the NTC’s charges methodology used an average of three years of heavy vehicle allocated expenditure to calculate the cost base to be recovered through heavy vehicle charges. Following the 2007 determination this period was extended to seven years to increase the smoothing effect due to the rapid rise in road expenditure that occurred from 2003–04 onwards. The 2013 Heavy Vehicle Charges Review focused on the examination of the following three major features of the cost base calculation.

3.1.1.1 Indexing

The current methodology employs indexation as a way to estimate the cost base and to avoid downward bias caused by the application of historical data. When deriving the cost base, past (nominal) road expenditure data is converted to current year (real) terms using BITRE Road Construction and Maintenance Price Index (RCMPI). Use of the RCMPI has been criticised by numerous stakeholders because of the volatility of the annual changes in the index. During consultation with stakeholders the use of alternative indexing mechanisms was suggested. After reviewing various indexing mechanisms, the NTC recommended dropping the use of any indexing mechanisms in favour of a more mechanistic approach, which would achieve a similar outcome but would avoid confusion and outside influences. Ministers supported the NTC proceeding towards developing the determination on this basis.

3.1.1.2 Averaging period

The averaging methodology currently used to calculate the cost base relies on a seven-year simple moving average. During consultation with stakeholders, the use of alternative averaging periods was suggested. The analysis undertaken as part of the 2013 Heavy Vehicle Charges Review demonstrated that a longer averaging period (e.g. seven years) was preferable to a shorter averaging period (e.g. three years) in most cases. Consequently, the NTC recommends retaining the averaging period of seven years.

3.1.1.3 Averaging mechanism

As outlined in the 2013 Heavy Vehicle Charges Review, the use of de-averaged latest year’s expenditure data to calculate the cost base would lead to unacceptably volatile charges. It is therefore essential to use an averaging mechanism to estimate current expenditures. Several averaging mechanisms were investigated during this review. The NTC created a dedicated assessment framework to compare the respective performance of these averaging mechanisms. The assessment framework is based on the following four objectives, noting that the second and third objectives conflict.

Heavy vehicle charges determination – RIS February 2014 14

1. Full cost recovery over time 2. Limiting over and under-recoveries 3. Smoothness 4. Simple and transparent