Draft Final v2

95

Thinking People. Report on Pilot Implementation of Property Valuation Methodology in Phuentsholing Municipality SC 103840 BHU: Support to BHU Strengthening Economic Management (Contract No. 114191, 114193, 114195) Empowering Governance of Tomorrow Thinking Cities

-

Upload

tenzin-namgay -

Category

Documents

-

view

29 -

download

3

description

Proverty Valuation in Bhutanese Towns

Transcript of Draft Final v2

Thinking People. Report on Pilot Implementation of Property Valuation Methodology in Phuentsholing Municipality

SC 103840 BHU: Support to BHU Strengthening Economic Management (Contract No. 114191, 114193, 114195)

Empowering Governance

of Tomorrow

Thinking Cities

At Deloitte, our shared commitment is to

improve public outcomes, through a focus

on people and the people dedicated to their

service. We take the time to think, exploring

the complex issues facing the public sector

and developing relevant, timely, and

sustainable solutions for our clients to use

today for a better tomorrow. It’s this

commitment to our clients, the communities

in which we operate, and smarter business

practices that ensures we too play our part in

building a better society.

At Deloitte, we’re focused on our clients and

on our clients’ clients.

At Deloitte, we are Thinking people.

Contents

1 EXECUTIVE SUMMARY ............................................................................................................ 5 1.1 Background ........................................................................................................................... 5 1.2 Property Valuation & Taxation in Bhutan............................................................................. 5 1.3 Proposed Property Valuation Methodology ......................................................................... 6 1.4 PVM Toolkit ........................................................................................................................... 6 1.5 Activities Undertaken ............................................................................................................ 6 1.6 Next Steps ............................................................................................................................. 6

2 INTRODUCTION ........................................................................................................................ 8 2.1 Background ........................................................................................................................... 8 2.2 Our Scope of Work ................................................................................................................ 8 2.3 Rationale for the Assignment ............................................................................................... 9

3 UNDERSTANDING PROPERTY TAX ...................................................................................... 10 3.1 Introduction ......................................................................................................................... 10 3.2 Property Tax ........................................................................................................................ 10 3.3 Advantages and Disadvantages of Property Tax .............................................................. 10 3.4 Pre-requisites for Effective Property Tax System ............................................................. 11

4 VALUATION FOR PROPERTY TAX ........................................................................................ 12 4.1 Rationale for Valuation Approach ...................................................................................... 12 4.2 Components of an Efficient Property Tax Framework ...................................................... 13 4.3 Objective Valuation Methodology in Property Tax Framework ......................................... 13

5 CURRENT PROPERTY TAX SYSTEM IN PHUENTSHOLING THROMDE .............................. 15 5.1 Issues in Property Valuation & Taxation ............................................................................ 15

6 PROPOSED PROPERTY VALUATION METHODOLOGY FOR PHUENTSHOLING ................ 17 6.1 Land Valuation .................................................................................................................... 17 6.2 Building valuation ............................................................................................................... 18 6.3 Other Building Details ......................................................................................................... 18

7 PVM TOOLKIT ......................................................................................................................... 20 7.1 Customizable masters ........................................................................................................ 20 7.2 Data History ......................................................................................................................... 21 7.3 Scenario Creation ............................................................................................................... 22 7.4 Base Scenario Generator .................................................................................................... 22 7.5 Reports ................................................................................................................................ 23

8 ACTIVITIES UNDERTAKEN FOR PILOTING PVM IN PHUENTSHOLING THROMDE ............ 24

9 NEXT STEPS ........................................................................................................................... 26

10 ANNEXURE ............................................................................................................................. 28 10.1 Matrix for Giving Weightages to Different Land Uses of PUDP 2007-17........................... 28

10.2 Official of the Following Agencies are to be Trained ........................................................ 29 10.3 Training Material ................................................................................................................. 30 10.4 Valuation Report of the 50 properties as generated by the Toolkit .................................. 43

Acronyms

ADB Asian Development Bank

BDFC Bhutan Development and Finance Corporation

BNB Bhutan National Bank

BOB Bank of Bhutan

BR Base rate

BSR Bhutan Schedule of Rates

DCD Development Control Division

DES Department of Engineering Services

DNP Department of National Properties

GIS Global Information System

LCR Land Compensation Rates

LDC Least Developed Countries

MoWHS Ministry of Works and Human Settlement

MRAS Municipal Revenue Administration System

MTEF Medium Term Expenditure Framework

NLCS National Land Commission Secretariat

NPPF National Pension and Provident Fund

OVM Objective Valuation Methodology

PAVA Property Assessment and Valuation Agency

PT Phuentsholing Thromde

PUDP Phuentsholing Urban Development Plan

PVM Property Valuation Methodology

QCG Quick Cost Guide

RCC Reinforced Concrete Cement

RGoB Royal Government of Bhutan

RICB Royal Insurance Corporation of Bhutan

SQCD Standard Quality Control Division

ULB Urban Local Body

Pilot Implementation of Property Valuation Methodology in Phuentsholing Thromde

SC 103840 BHU: Support to BHU Strengthening Economic Management (Contract No. 114191, 114193, 114195)

Deloitte Touche Tohmatsu India Private Limited Page 5

1 Executive Summary

Background 1.1

During the initiation phases of ADB-funded Strengthening Public Management Program, it was

recommended that the Thromdes need to adopt a value-based property tax system instead of the

existing unit-based system. Hence, as a first step Ministry of Works and Human Settlement, has

devised methodology for property valuation to be adopted by the Thromdes. Following up on the

objective of Strengthening Economic Management for local government and recommendations of

Strengthening Public Management this assignment aims to pilot the proposed methodology in

Phuentsholing. This will be followed up with requisite municipal council approvals to shift to a value-

based property tax system. As per the terms of reference, the following is the scope of work for pilot

implementation of Property Valuation Methodology in Phuentsholing Thromde:

1. Valuation of a sample of 50 building/structures based on Bhutan Schedule of Rates (BSR)

guidelines & rates and recent PVM methodology and rules and regulations, prepared by

MoWHS, in Phuentsholing Thromde.

2. Preparation of PVM based property tax model and excel based PVM toolkit

3. Capacity building and training of the selected employees of Phuentsholing Thromde on the

implementation of PVM methodology, tax model and toolkit

4. Preparation of a status report on the implementation of the PVM piloting.

Property Valuation & Taxation in Bhutan 1.2

1.2.1 Property Valuation

There are two major components of property valuation:

Land Valuation – Property Assessment and Valuation Agency was made responsible for undertaking

all assessment and valuation work pertaining to properties. The methodology adopted for land value

calculation is provided below.

Base rate for land is calculated as a weighted average of the following rates

1. Average rate (per unit area) from the primary data source, which is the true reflection of the

prevailing market rates obtained based on telephonic enquiry made, interview with buyers

and sellers, advertised prices etc.

2. Lhenzhung 2006 rates (per unit area)

3. Average of rates (per unit area) given by the Financial Institutions (Bhutan National Bank

(BNB), Bank of Bhutan (BOB), Royal Insurance Corporation of Bhutan (RICB), National

Pension and Provident Fund (NPPF) and Bhutan Development Finance Corporation (BDFC))

4. Official transacted rates as per the records of the Thromde/NLCS

Building Valuation - The Department of Engineering Services publishes the Quick Cost Guide to

building valuation based on the prevailing Bhutan Schedule of Rates used for estimation purposes.

The value of the building is calculated based on the construction cost of the building. The cost is

typically based on type of building (RCC, Load Bearing, and Temporary Structures), number of floors,

floor to ceiling height, Plinth Area, Average room size factor, types of material used for construction

etc.

1.2.2 Property tax

The current Land tax applicable in Phuentsholing is calculated based on Unit Area of the property.

The land tax rate is applied on the area of the property to arrive at the land tax. The current tax rate

which has been effective from 2011 has been notified based on minor changes to the tax rates

notified in 1992.

Pilot Implementation of Property Valuation Methodology in Phuentsholing Thromde

SC 103840 BHU: Support to BHU Strengthening Economic Management (Contract No. 114191, 114193, 114195)

Deloitte Touche Tohmatsu India Private Limited Page 6

The Urban house Tax is calculated on per unit basis. This is collected along with the Land Tax. The

urban house tax is calculated based on the type of structure (Buildings / Houses) and its classification

done based on the range of plinth area. The Tax is computed based on the number of units in the

buildings/ houses/ units for residential category and commercial category.

Proposed Property Valuation Methodology 1.3

Valuation of land shall be based on the Land Compensation Rates as defined by PAVA. The base

rate is defined as per land-use and zoning defined in Phuentsholing Urban Development Plan.

Additionally, weightages shall be allocated for specific factors as identified in the structural plan. The

cumulative weightages for these factors shall be multiplied with the PAVA base rate to arrive at the

current valuation rate of the land. This will be multiplied with the area of the land to arrive at the value

of the land. Valuation of building shall be done based on the construction cost of the building. The

cost would be calculated based on type of building, number of floors, floor to ceiling height, average

room factor, etc. The valuation shall also take into consideration, other building attributes like cellar,

parking, fencing, etc. Based on these parameters and rates taken from Quick Cost Guide of the

Bhutan Schedule of Rates, the cost of construction shall be determined. Other buildings such as

boundary wall, parking area, lamp posts, water tanks etc. are valued on the basis of rates prescribed

in BSR.

PVM Toolkit 1.4

An Excel based Toolkit has been developed to assist in piloting and institutionalization of the PVM in

Phuentsholing Thromde. The toolkit enables the officials update PAVA and BSR rates as and when

they are updated. The toolkit also has provision to update details of the property as and when they

change. The Thromde can also customise the toolkit to maintain additional property details as and

when they are added to the valuation methodology. Additionally the toolkit enables tracking of

changing value of each property over the years as the PAVA rates, BSR rates and property details

change. The toolkit has the provision to calculate slab rates to keep overall tax burden same as the

existing burden which enabling the Thromde to adjust the extent of cross-subsidisation. Based on the

proposed methodology, the differentiation between residential and non-residential property is being at

the time of valuation. Hence, this differentiation is not being provided in the property tax model in the

toolkit. Provision has been made in the toolkit to have scenarios for property tax based on only the

value of the property.

Activities Undertaken 1.5

The following activities have been undertaken for piloting of PVM in Phuentsholing:-

1. Selection of Properties for piloting

2. Preparation of Data Collection

Template

3. Preparation of value based property

tax model

4. Development of Toolkit

5. Data Migration

6. Training

Next Steps 1.6

With the Property Valuation Methodology in place, the following are the pertinent next steps for the

Government to strengthen the methodology and adopt a value-based property tax system.

Structure of Property Valuation and Tax- Presently there is a practice of levying differential land-tax

rates on residential and non-residential properties. This difference has been maintained at 1:2 level

for residential and commercial. However, post assessing the proposed valuation methodology we

have observed that this difference is increasing to 1:3. In that scenario, it will be not possible to

maintain similar tax structure for various types of land. Additionally, further discrimination in tax rates

might not be acceptable especially after differential treatment during valuation. To maintain the tax

burden on the taxpayers at the same level as in the previous methodology it is suggested that the

Pilot Implementation of Property Valuation Methodology in Phuentsholing Thromde

SC 103840 BHU: Support to BHU Strengthening Economic Management (Contract No. 114191, 114193, 114195)

Deloitte Touche Tohmatsu India Private Limited Page 7

levels of difference during valuation be reduced. To do this the toolkit will come in handy as it has

provisions for scenarios to be tested before actual implementation.

Finalization of Tax Slabs - In discussion with stakeholders, the tax slabs and rates need to be

finalised.

Requisite Amendments – Amendments to Municipal Finance Rules, Municipal Finance Policy and

Local Government Act would be required to bring in value based property tax system.

Property Survey – With an updated properties database, the Thromde shall be in a better position to

levy the tax at the fair value of the property.

MRAS - Provisions need to be made in the Municipal Revenue Administration System to enable

valuation of properties and levy of tax based on value of the property.

Pilot Implementation of Property Valuation Methodology in Phuentsholing Thromde

SC 103840 BHU: Support to BHU Strengthening Economic Management (Contract No. 114191, 114193, 114195)

Deloitte Touche Tohmatsu India Private Limited Page 8

2 Introduction

Background 2.1

Bhutan has achieved a robust economic growth in the last decade. Despite its numerous political and

economic difficulties, the country has shown a growth rate of nearly 9.7% in 2012. It is also interesting

to note that Bhutan is the only country in the world that measures happiness - a holistic concept

combining material well-being with an individual’s spiritual, emotional, and cultural wellbeing. Despite

all this, Bhutan is still a poverty ridden country and on the UN's list of Least Developed Countries

(LDC).

The Royal Government of Bhutan (RGoB), since its transition to parliamentary democracy in 2008,

has taken up additional measures to institutionalize the decentralized public management. As it

embarks on an agenda of development through decentralization and democratization, the RGoB

recognizes enormous challenges. The key challenges among these are:

1. Inadequate institutional and human resource capacity at local government level

2. Inadequate resource base of local governments

3. Cumbersome and complex multilevel administrative systems, and procedures that have

affected the efficiency and effectiveness of local administration

To meet these challenges, the Government is pursuing various strategies under its 11th five year plan

(2013-2018). While the strategies are well-defined, major gaps exist in terms of financing, technology,

accountability, regulation, and capacity. The Government has outlined decentralized governance as a

crosscutting development strategy, as part of this process RGoB is implementing local government

capacity development strategy and municipal finance policy. ADB is providing assistance to RGoB to

achieve this vision under the umbrella of various programs like Strengthening Public Management,

Strengthening Economic Management and Capital Market Development. Under Strengthening

Economic Management, ADB is extending support to strengthen the revenue administration at

national and local level by augmentation of own revenue through reforming the taxation methodology.

During the initiation phases of Strengthening Public Management, it was recommended that the

Thromdes need to adopt a value-based property tax system instead of the existing unit-based system.

Hence, as a first step Ministry of Works and Human Settlement, has devised methodology for

property valuation to be adopted by the Thromdes. Following up on the objective of Strengthening

Economic Management for local government and recommendations of Strengthening Public

Management this assignment aims to pilot the proposed methodology in Phuentsholing. This will be

followed up with requisite municipal council approvals to shift to a value-based property tax system.

Our Scope of Work 2.2

As per the terms of reference, the following is the scope of work for pilot implementation of Property

Valuation Methodology in Phuentsholing Thromde:

1. Valuation of a sample of 50 building/structures based on Bhutan Schedule of Rates (BSR)

guidelines & rates and recent PVM methodology and rules and regulations, prepared by

MoWHS, in Phuentsholing Thromde.

2. Preparation of PVM based property tax model and excel based PVM toolkit

3. Capacity building and training of the selected employees of Phuentsholing Thromde on the

implementation of PVM methodology, tax model and toolkit

4. Preparation of a status report on the implementation of the PVM piloting.

Pilot Implementation of Property Valuation Methodology in Phuentsholing Thromde

SC 103840 BHU: Support to BHU Strengthening Economic Management (Contract No. 114191, 114193, 114195)

Deloitte Touche Tohmatsu India Private Limited Page 9

Rationale for the Assignment 2.3

Tax on property is the primary source of revenue for most of the local governments. Local

governments across the world devise

ways to unlock the true potential of

this revenue source. As depicted in

Exhibit 1, tax on property contributed

to about 16 per cent of total own

income of Phuentsholing Thromde.

With about 2275 identified properties

within Phuentsholing, there is a

potential for an augmentation of

income from properties. However,

with the current system of unit based

property tax system, the Thromde is

not in a position to tap this potential.

Phuentsholing being the commercial

capital of Bhutan has a vibrant

property market which is seeing an

upswing with a number of new

properties coming up. However, with the tax rates being unchanged since 1992 there is not much

increase in property tax receipts even though the property value has increased manifold.

Hence, it is pertinent for Phuentsholing to move to a value based property tax system to unlock this

revenue potential. In the absence of data on value of properties and in-house empirical methodology

to compute the same, the Thromde along with MoWHS agreed to adopt property valuation

methodology based on PAVA Compensation Rates and Bhutan Schedule of Rates.

This assignment aims to institutionalise the adoption of property valuation methodology through

implementation of an Excel based toolkit and pilot the same for 50 properties to pave the way for a

value based property tax system.

Property transfer tax

20%

Land Lease Rent

18%

Land Tax 16%

Solid Waste 15%

Water & sanitation

17%

Vehicle parking fee collection

7%

Auction Fees 2%

Others 5%

Exhibit 1: Components of total own revenue of Phuentsholing

Thromde (2011-12)

Pilot Implementation of Property Valuation Methodology in Phuentsholing Thromde

SC 103840 BHU: Support to BHU Strengthening Economic Management (Contract No. 114191, 114193, 114195)

Deloitte Touche Tohmatsu India Private Limited Page 10

3 Understanding Property Tax

Introduction 3.1

A Property Tax is levied by designated authority on the owner’s property. There are three types of

property: parcel of land, buildings and moveable personal objects. Under a property tax system, the

designated authority performs an assessment of the taxable value of each property, and tax is levied

in proportion to that value.

Property Tax 3.2

Property is defined as the parcel of land and any permanent structures erected on it. Property tax is

restricted to annual taxes and excludes one-off taxes on transfers, on realised capital gains or

betterment, or on annual wealth taxes.

Property tax is generally levied as a percentage of the assessment value of any property. The base

for this value assessment and the methodology differs from jurisdiction to jurisdiction. To calculate the

property tax, the authority will multiply the assessed value of the property by the applicable tax rate.

Property tax, in most cases, is levied by the local governments and is a primary source of revenue at

the local administration level as there is no other tax which can be geographically levied. As a primary

source of revenue, property tax plays an important role in decentralisation and the autonomy of local

governments. The duties of local governments are almost invariably such that it is impossible to

discharge them without central government grants which detract to a greater or lesser extent from

their independence. Increasing independent powers of raising revenues through property taxes thus

becomes important.

Advantages and Disadvantages of Property Tax 3.3

In addition to role in decentralisation of government, property tax has other advantages. Owing to the

high elasticity of property tax it is possible to be introduced and maintained in almost any

circumstances. Administration of property tax is cost effective compared to other taxes. It is possible

to have a cost to yield ratio of less than two per cent. It can be designed to be transparent and is

difficult to avoid. Compliance rates of 95 per cent are achievable through effective administration. In

general there is a direct relationship of assessed value to the taxpayer’s ability to pay. If designed

correctly the tax can also be marginally progressive. The revenue is predictable and elastic and is

very well suited as a source of locally generated revenue for local governments.

Some of the advantages also are the disadvantages. The transparent nature of property tax magnifies

any inconsistencies in public perception. Geographical nature of the tax exposes it to public scrutiny.

These inconsistencies can be both those of assessment and those of ability to pay. In a similar way

the difficulty of avoiding or evading property tax makes it unpopular.

Building buoyancy into property tax is also a difficult task. Buoyancy is a function of two mechanisms.

The first of these is the revaluation of properties at regular intervals. The second is the increase in the

rate of tax to produce the needed revenue. Either of the mechanisms could provide buoyancy. It is

technically possible to increase tax rates on an out-of-date valuation. Nonetheless there is always

resistance to revaluations. Both of these are highly political, hence extremely difficult to implement.

Pilot Implementation of Property Valuation Methodology in Phuentsholing Thromde

SC 103840 BHU: Support to BHU Strengthening Economic Management (Contract No. 114191, 114193, 114195)

Deloitte Touche Tohmatsu India Private Limited Page 11

Pre-requisites for Effective Property Tax System 3.4

There are a number of pre-requisites for a Government to introduce or reform property tax system

and have an effective administration in place. Few of these are outlined hereunder:

Political will: Levy of any tax requires political determination and public acceptance. The transparent

nature of property tax makes furtive introduction impossible. Hence, political determination is the most

important factor.

Administrative feasibility: Along with political will and public acceptance, there is administrative

inertia in introduction of property tax. Requirement of latest property data and frequent updates pose

an administrative roadblock. Once it has been surmounted, property tax is one of the easiest taxes to

administer.

Scope for increased yields: In most countries there is still immense potential in property tax to yield

more revenue. Owing to lack of political will, property taxes have not been revised for many years.

With an effective administration, there is potential for increased revenue flow from property tax.

Significance: While property tax is not significant as a source of revenue it is important in political

terms. As the foundation of local government autonomy, and as a means of financing some single

function authorities, there is sound justification for the introduction of the tax.

Pilot Implementation of Property Valuation Methodology in Phuentsholing Thromde

SC 103840 BHU: Support to BHU Strengthening Economic Management (Contract No. 114191, 114193, 114195)

Deloitte Touche Tohmatsu India Private Limited Page 12

4 Valuation for Property Tax Although the administration of property tax is a complex process in its entirety, there is no single

element that cannot be explained in simple terms. Policy makers and taxpayers are entitled to

understand property tax issues. In property tax the most contentious problems of valuation arise when

there is no sales evidence of that class of property. Valuations for property tax are defined by

legislation of the country which identifies what must be taken into account in such valuations.

Valuation standards define the matters to be taken into account in valuation practice primarily when

dealing with valuations for private sector activities such as mortgages, investment and accounting.

Such standards are increasingly international in character reflecting the growing awareness of the

strong links between valuation standards and financial markets, and globalization.

Value is a subjective term and the value of a property may differ from person to person. Value of a

property is derived from its various utilities. Hence it is appropriate to arrive at the fair value of any

property based on pre-determined influencing factors. The market value of any property is best

determined by the parties involved in such a transaction. For the purpose of tax computation, it is best

to put in place a framework to objectify the value of any property.

Rationale for Valuation Approach 4.1

There is a debate on the right approach of valuation for the purpose of property tax. With the

subjectivity of both the Lease Value and Capital Value approaches, there would always be a debate

on the fair value of the property computed by either of the approaches. It is political and administrative

feasibility, more than economic arguments that tend to be the deciding factor for choosing one

approach over the other. In places where rented properties are a common feature, it is easy to

procure information on rental values and easily accessible to taxing authority. In such a scenario,

using Annual Lease Value approach to assess properties for taxation is justified and the logical

approach.

In places where owner occupancy is more prevalent and where there is an active real estate market,

using the Capital Value approach is justified. This is subject to the condition that transaction

information is easily accessible to the taxing authority. In countries where house ownership is still low

and most families stay in rented accommodations, the Annual Lease Value is the most justified and

prevalent approach for assessment of properties for tax purposes. Same is true for most of the

commercial establishments in a country.

An Objective Valuation Methodology (OVM) ensures that the framework used for taxation of property

is fair in terms of incidence of tax and transparent in terms of assessment and application of the

same. It also ensures ease of implementation. An OVM would also enable self-assessment of taxes.

Property Tax Practice - India

Property tax or 'house tax' is a local tax on buildings, along with demarcated land, and imposed on

owners. The tax power is vested in the states and it is delegated by law to the local bodies,

specifying the valuation method, rate band, and collection procedures. The tax base is the annual

rateable value (ARV). Owner-occupied and other properties not producing rent are assessed on

cost and then converted into ARV by applying a percentage of cost. Vacant land is generally

exempted. Central government properties are exempted. Properties of foreign missions also enjoy

tax exemption without an insistence for reciprocity. The tax is usually accompanied by a number

of service taxes, e.g., water tax, drainage tax, conservancy (sanitation) tax, lighting tax, all using

the same tax base. The rate structure is flat on rural properties, but in the urban areas it is mildly

progressive with about 80% of assessments falling in the first two slabs.

Pilot Implementation of Property Valuation Methodology in Phuentsholing Thromde

SC 103840 BHU: Support to BHU Strengthening Economic Management (Contract No. 114191, 114193, 114195)

Deloitte Touche Tohmatsu India Private Limited Page 13

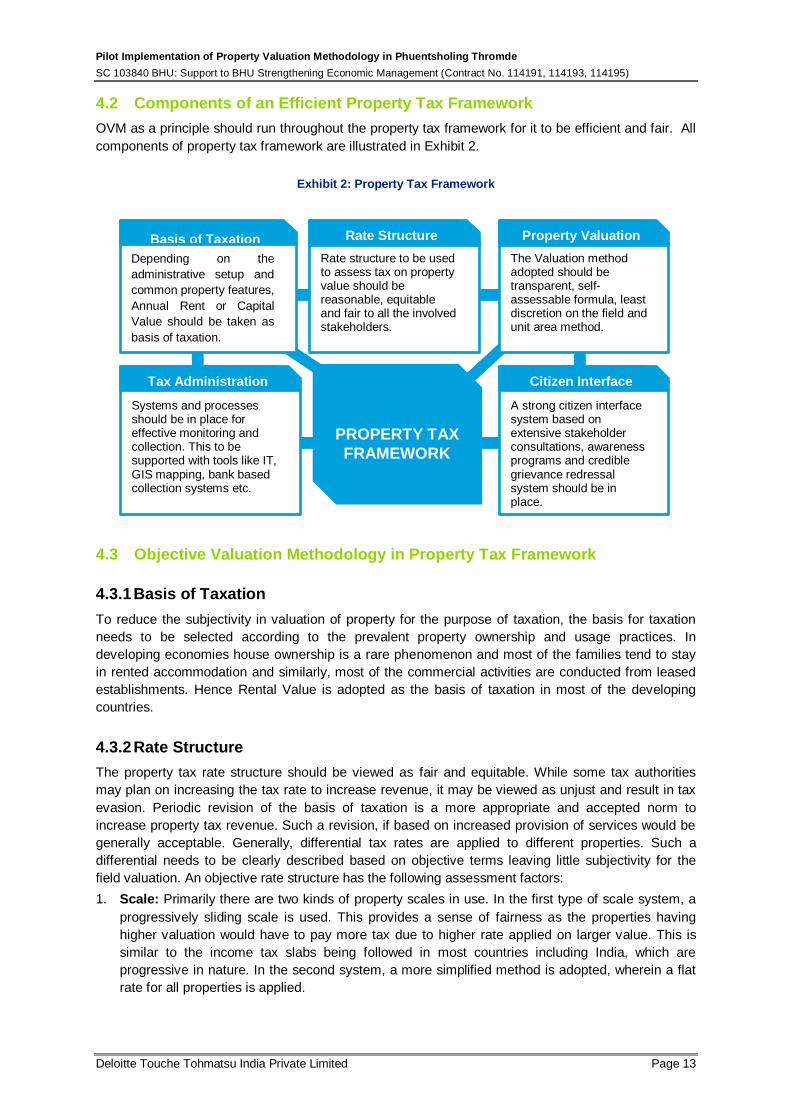

Components of an Efficient Property Tax Framework 4.2

OVM as a principle should run throughout the property tax framework for it to be efficient and fair. All

components of property tax framework are illustrated in Exhibit 2.

Exhibit 2: Property Tax Framework

Objective Valuation Methodology in Property Tax Framework 4.3

4.3.1 Basis of Taxation

To reduce the subjectivity in valuation of property for the purpose of taxation, the basis for taxation

needs to be selected according to the prevalent property ownership and usage practices. In

developing economies house ownership is a rare phenomenon and most of the families tend to stay

in rented accommodation and similarly, most of the commercial activities are conducted from leased

establishments. Hence Rental Value is adopted as the basis of taxation in most of the developing

countries.

4.3.2 Rate Structure

The property tax rate structure should be viewed as fair and equitable. While some tax authorities

may plan on increasing the tax rate to increase revenue, it may be viewed as unjust and result in tax

evasion. Periodic revision of the basis of taxation is a more appropriate and accepted norm to

increase property tax revenue. Such a revision, if based on increased provision of services would be

generally acceptable. Generally, differential tax rates are applied to different properties. Such a

differential needs to be clearly described based on objective terms leaving little subjectivity for the

field valuation. An objective rate structure has the following assessment factors:

1. Scale: Primarily there are two kinds of property scales in use. In the first type of scale system, a

progressively sliding scale is used. This provides a sense of fairness as the properties having

higher valuation would have to pay more tax due to higher rate applied on larger value. This is

similar to the income tax slabs being followed in most countries including India, which are

progressive in nature. In the second system, a more simplified method is adopted, wherein a flat

rate for all properties is applied.

Depending on the

administrative setup and

common property features,

Annual Rent or Capital

Value should be taken as

basis of taxation.

Basis of Taxation Rate structure to be used to assess tax on property value should be reasonable, equitable and fair to all the involved stakeholders.

Rate Structure The Valuation method adopted should be transparent, self-assessable formula, least discretion on the field and unit area method.

Property Valuation

Systems and processes should be in place for effective monitoring and collection. This to be supported with tools like IT, GIS mapping, bank based collection systems etc.

Tax Administration A strong citizen interface system based on extensive stakeholder consultations, awareness programs and credible grievance redressal system should be in place.

Citizen Interface

PROPERTY TAX

FRAMEWORK

Pilot Implementation of Property Valuation Methodology in Phuentsholing Thromde

SC 103840 BHU: Support to BHU Strengthening Economic Management (Contract No. 114191, 114193, 114195)

Deloitte Touche Tohmatsu India Private Limited Page 14

2. Usage: There is a standard differential of property based on its actual usage. Difference is made

in terms of residential, commercial, institutional, industrial, religious etc. A further differentiation

may be done based on owner occupied and rented properties.

3. Exemptions: A number of countries provide exemption from property tax to Government

buildings, places of worship, charitable institutions etc. based on tax laws applicable for that state

or country. Since such exemptions may be used for tax evasion purposes, an objective

description for such properties needs to be provided to leave little ambiguity in the field. This

needs to be supported with a robust monitoring system.

4.3.3 Property Valuation

Valuation system to be adopted for property tax should be based on clearly enunciated objective

parameters, be formula based to enable self-assessment and be easily implementable both by the

citizens and authority alike. Usage of an objective system for valuation leaves little scope for

subjectivity and discretion at field level hence is viewed as being fair and equitable. It would also bring

in transparency and acceptance of the taxes by the citizens. Normally per unit area rate for various

types of structures is provided by the ULBs. The unit area rate may be for Capital value or the Annual

Rental value depending on the methodology adopted by the ULB. This rate is applied to plinth/ carpet

area of the building, with deductions for maintenance expenditure or depreciation. Additional weights

are provided for use of building, access to main roads, etc. A case study is provided in the box below

detailing the parameters used for valuation adopted in Hyderabad, India.

4.3.4 Tax administration

Adoption of OVM for property tax would also enable the tax authority to improve the tax administration

system and plug loopholes. An OVM based property tax framework would leave little scope for tax

evasion. Adoption of OVM has to be preceded by collection of real data from the assessment region

to enable a fair and equitable tax framework. These include complete mapping of properties, unique

identification of each property, frequent update of data pertaining to utilization, type of construction,

construction deviation, rent etc. Various tools are at the disposal of the tax authority for added

efficiency in the system which includes GIS mapping of properties, computerization, system of

penalties and incentives, online/ bank based system for payment of taxes, online grievance redressal

system, periodic grievance tribunals, etc.

4.3.5 Citizen Interface

A robust property tax framework is based on citizen trust and transparency. Hence it is pertinent that

any reform to the framework is preceded with extensive stakeholder consultations and awareness

programs. A consensus building exercise needs to be taken up before implementing any reform in the

tax framework. This would ensure quick adoption and implementation of the new framework. It is

necessary to educate the stakeholders of all the parameters, objectivity and simplicity of the OVM

based tax framework. This when supported with a robust citizen interface mechanism including real

time tax dues data and grievance redressal system would tie all the loose ends and pave way for low

tax evasion and increase incidences of timely payment of property tax.

Property Tax Practice - Australia

Australia has property taxes known as property or land rates. Land rates and frequency of

payment are determined by local councils. Each council has land valuers who value the land's

worth. The land's worth is the value of the land only; it does not include existing dwellings on the

property. The assessed value of the land determines the total charges of rates. Rates can range

from $100 per quarter to $1,000 per quarter depending on the location and value of the land.

Quarterly payments are common, but frequency varies by locality.

Pilot Implementation of Property Valuation Methodology in Phuentsholing Thromde

SC 103840 BHU: Support to BHU Strengthening Economic Management (Contract No. 114191, 114193, 114195)

Deloitte Touche Tohmatsu India Private Limited Page 15

5 Current Property Tax System in

Phuentsholing Thromde This section describes the methodology followed by the Phuentsholing Thromde for property tax

calculation.

Land Tax Calculation:

The current Land tax applicable in Phuentsholing is calculated based on Unit Area of the property.

The land tax rate is applied on the area of the property to arrive at the land tax. The current tax rate

which has been effective from 2011 has been notified based on minor changes to the tax rates

notified in 1992. The complete land in Phuentsholing has been divided into five precincts as follows:

URBAN VILLAGE

URBAN CORE AND NEIGHBOURHOOD NODE

INSTITUTIONAL

HERITAGE

SPECIAL ECONOMIC ZONE

Each of these precincts is further classified into sub-precincts and as commercial and residential area.

Urban House Tax calculation:

The Urban house Tax is calculated on per unit basis. This is collected along with the Land Tax. The

urban house tax is calculated based on the type of structure (Buildings / Houses) and its classification

done based on the range of plinth area. The Tax is computed based on the number of units in the

buildings/ houses/ units for residential category and commercial category. For commercial buildings,

a unit is defined as either a shop or dwelling unit where one shop or office or warehouse occupies

larger spaces, unit calculated on a carpet area of 771 sq.ft. per unit and is applicable only for

commercial unit like shops, warehouses or offices. The tax rates for the Urban House tax have been

prevalent since 1993. While there was a revision of tax rates in 2011, tax rates for highest slab has

not been changed. The tax rate is not calculated based on the actual plinth area of the building rather

on the per unit basis which is classified based on a range of plinth area. For example, a class II

apartment includes all buildings with plinth area between 875 sqft to 1259 sq.ft. and is considered one

unit. Hence all apartments in this range are charged the same tax irrespective of the plinth area. Also

rates have been fixed in 1992 and have not been revised since.

Issues in Property Valuation & Taxation 5.1

The following section details out the issues in property taxation currently being followed by the

Phuentsholing Thromde

1. Basis of property valuation: The current methodology followed by the Phuentsholing

Thromde is not based on the actual value of the property. The revenue section does not use

the PAVA rates for calculation of land taxes. It is based on the area of the property classified

under five land precincts. The basis for the tax rates for the current land types is not well

defined. But it can be said that the property valuation does not follow land rates set by the

PAVA. It also does not take into consideration the Phuentsholing Urban Plan based zoning

which classifies the land into 23 zones based on land use which is more exhaustive. Similarly,

the building value being used to determine the urban house tax is not based on the actual

value of the building. The valuation used by DES and also Development Control Division

(DCD) of the Phuentsholing Thromde is not followed while taxation.

Pilot Implementation of Property Valuation Methodology in Phuentsholing Thromde

SC 103840 BHU: Support to BHU Strengthening Economic Management (Contract No. 114191, 114193, 114195)

Deloitte Touche Tohmatsu India Private Limited Page 16

2. Rate Structure: The rate structure currently being used has been in use since 1992. The

land tax has been revised in 2011, but the highest slab rate still remains unchanged. The

Urban house tax is still based on the 1992 rates, basis for which is currently not available.

3. Factors considered for PAVA land Valuation: The present structure of PAVA land

valuation in Bhutan is somewhat objective but is away from being perceived as fair and

equitable. There is a considerable amount of difference in the level of urban services being

provided within the same city. This difference is accentuated by the terrain of Bhutan. Hence,

it is pertinent to ensure that the valuation framework takes into account all the differentiating

factors to derive the true value of the land. Present valuation framework differential based on

utility of the building, distance from urban core and size of the land parcel. Hence, there

arises a need for a more inclusive and comprehensive objective framework.

4. Factors considered for Building Valuation: The Thromdes currently do not use any

valuation of buildings for calculation of property tax. The DES building valuation methodology

may be adopted for taxation purpose to start with.

Pilot Implementation of Property Valuation Methodology in Phuentsholing Thromde

SC 103840 BHU: Support to BHU Strengthening Economic Management (Contract No. 114191, 114193, 114195)

Deloitte Touche Tohmatsu India Private Limited Page 17

6 Proposed Property Valuation

Methodology for Phuentsholing As a first step for moving towards a tax system based on property value, Phuentsholing is undertaking

an exercise to value the properties within the administrative area of the Thromde. The property

valuation methodology has been designed by MoWHS which suggests valuation of land based on

PAVA methodology and valuation of building based on Bhutan Schedule of Rates. Each of these

methodologies are outlined here under.

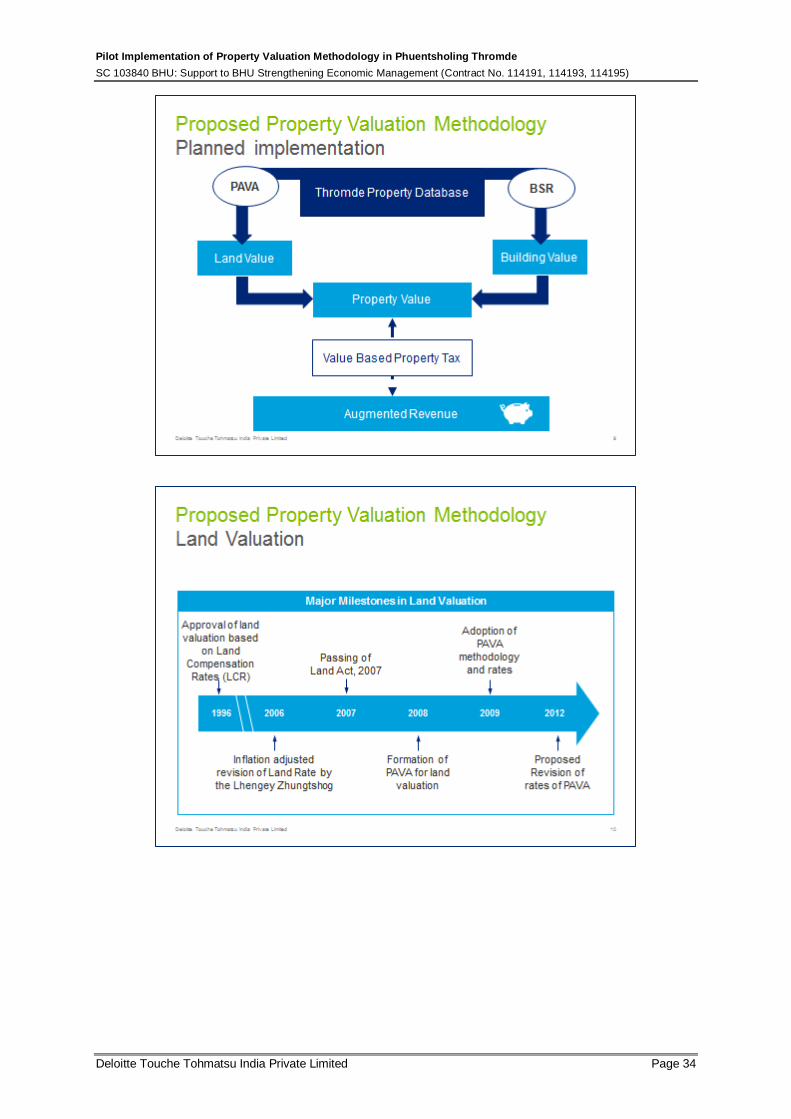

Land Valuation 6.1

Valuation of land shall be based on the Land Compensation Rates as defined by PAVA. The base

rate is defined as per land-use and zoning defined in Phuentsholing Urban Development Plan.

Additionally, weightages shall be allocated for specific factors as identified in the structural plan.

These weightages for Phuentsholing are provided in Annexure 10.1. The cumulative weightages for

these factors shall be multiplied with the PAVA base rate to arrive at the current valuation rate of the

land. This will be multiplied with the area of the land to arrive at the value of the land. This is

illustrated hereunder:

The factors currently used from structural plan for arriving at the average weightage are:

Land use as per local structure plan

Maximum building height allowed in the area

Maximum ground cover allowed for the building in the area

Accessibility in terms of access to roads including primary, secondary and tertiary roads.

How PAVA arrives at the base rates is not within the purview of the Thromde; however it is pertinent

to have an understanding of the methodology to enable the Thromde to move to its own valuation

methodology in the future. PAVA currently utilizes information from banks, insurance companies,

other financial institutions, realtors, primary surveys and transaction information from the Thromde.

PAVA is mandated to revise the base rates every three years. The methodology is illustrated

hereunder.

Pilot Implementation of Property Valuation Methodology in Phuentsholing Thromde

SC 103840 BHU: Support to BHU Strengthening Economic Management (Contract No. 114191, 114193, 114195)

Deloitte Touche Tohmatsu India Private Limited Page 18

( ) ( ) ( ) ( )

Where:

= Previous Base Rate

F = Value as per banks, financial institutions and insurance companies

R = Value as per official records with Thromde/NLCS

P = Transaction value as per primary survey of buyers/sellers

Building valuation 6.2

Valuation of building shall be done based on the construction cost of the building. The cost would be

calculated based on type of building, number of floors, floor to ceiling height, plinth area, average

room factor, material of construction etc. The valuation shall also take into consideration, other

building attributes like cellar, parking, fencing, etc. Based on these parameters and rates taken from

Quick Cost Guide of the Bhutan Schedule of Rates, the cost of construction shall be determined. The

Quick Cost Guide (QCG) has been prepared in 2005 which is being updated by the Standard Quality

Control Division (SQCD) under the Ministry of Works and Human Settlement.

The QCG defines average rate of construction per unit volume for different types of construction. The

QCG also defines Room Size Factor for range of average room sizes. Based on the average size of

rooms in the building the Room Size Factor is determined which is multiplied with the base rate as per

type of construction. This is then multiplied with the total volume of the building to arrive at the value

of the building. This is illustrated hereunder.

Other Building Details 6.3

Valuation of other building details such as parking, boundary wall, water tanks, area lighting, shed etc.

shall be the estimated construction value based on Bhutan Schedule of Rates (2012). Based on

actual survey of properties the other building details shall be captured. This would include the

specifications and volume/quantity of the construction. The construction price would then be

estimated to arrive at the value of these.

Pilot Implementation of Property Valuation Methodology in Phuentsholing Thromde

SC 103840 BHU: Support to BHU Strengthening Economic Management (Contract No. 114191, 114193, 114195)

Deloitte Touche Tohmatsu India Private Limited Page 19

Illustration of the Property Valuation based on the new PVM

Location – Sub Precinct “UV-1” under the

Precinct “Urban Village”

Land Area = 2400 sqft;

Land Use – Commercial

Type of Building – RCC frame building Age of Building – 2 Years, Life of Building – 75

Years

Number of floors – 4, Total plinth Area – 10000 sqft

Number of rooms – 10 Floor to Ceiling height – 2.40 m

Road Connection – Yes Soil Stability – Yes Water Availability - Yes

Land Valuation:

The base rate for land is calculated as follows:

BR = PAVA rate for 2009 = 21.89 Nu/sq.ft

The weights for the Land in Sub Precinct “UV-1” under the Precinct “Urban Village” are as follows:

No Type Factor for the

locality

Weights Total

Weight

Average

Weightage

1 Predominant uses allowed Commercial 2.0

4.8 1.6 2 Maximum Building Height 2 to 6 floors 2.0

3 Maximum Ground Cover

allowed

10% to 50% 0.8

The deduction weightages applicable for this plot for factors like Road Connection, Soil Stability and

Water Availability are as follows:-

No Type Maximum Deduction

Allowed

Deductions

Applicable

Total

Deductions

Applicable

1 Road Connection 5% 0.0

0.0 2 Soil Stability 10% 0.0

3 Water Availability 5% 0.0

Final Land Value for the location = Base Rate x Average Weightage x (1 – total deductions

applicable) = 21.89 x 1.6 x (1-0)= Nu 35.024 per sqft

Land value for the plot = Area x Land value for the location = 2400 x 35.024 = Nu 84, 057.60

Building valuation:

1. Total Area of building = 10000 sqft = 929.03 sqm

2. Average room size = (Total area / No. of rooms) x Floor to ceiling height

= (929.03 / 10) x 2.4 = 223.032

3. Cube root of average room size (2) = 6.06

4. Average room size factor as per DES quick cost guide = 0.903

5. Cost Index per sqm for office block 4-storey office block in Phuentsholing = 1696 per cum

6. Appreciation factor (from 2005 to 2014) = 1.84795 (i.e 84.795%)

7. Depreciation Factor = 1 – (Age of building/life of building) = 1 - 2/75 = 0.97

8. Cost of building = Total Area of building x (floor to ceiling height) x Average room size factor x

applicable BSR 2005 rate x Appreciation factor x depreciation factor

= 929.03 x 2.4 x 0.903 x 1696 x 1.84795 x 0.97 = Nu 6,120,917.54

Property value:

Land value + Building value = Nu 84,057.60 + Nu 6,120,917.54 = Nu. 6,204,975.14

Pilot Implementation of Property Valuation Methodology in Phuentsholing Thromde

SC 103840 BHU: Support to BHU Strengthening Economic Management (Contract No. 114191, 114193, 114195)

Deloitte Touche Tohmatsu India Private Limited Page 20

7 PVM Toolkit An Excel based Toolkit has been developed to assist Phuentsholing Thromde in piloting the property

valuation methodology. The toolkit has been designed with flexibility of data structure with a master

management module.

This would enable the

Thromde to customise

the toolkit as per their

requirements. The

primary objective of the

toolkit is to enable the

Thromde to

institutionalize the

property valuation

methodology and

conduct scenario

analysis to arrive at the

optimal value-based

taxation system. The

toolkit does not have

the capacity to run as

an administration

system. The key features of the toolkit are outlined hereunder.

Customizable masters 7.1

The core of the system is the PVM methodology based on PAVA Land Compensation Rates and

Quick Cost Guide of the Bhutan Schedule of Rates. While these modules have been designed as per

the current scenario, these are customizable to reflect additional and new classifications as and when

these are updated by the respective agencies.

The structure of data for maintaining land and building information has been created as per the

current requirements of PVM. However, this also is customizable to add new details for properties as

and when the need arises. A four level data tree structure has been designed to enable this

customization. These levels are as follows:

1. Data Description – Classification of information that is being maintained.

2. Data Header – Description of group of data

3. Data Detail – The actual information

4. Data type – The data can have various types which have been provided for in the toolkit.

This is illustrated with the example in Exhibit 4.

Exhibit 3: Welcome Screen of the Toolkit

Pilot Implementation of Property Valuation Methodology in Phuentsholing Thromde

SC 103840 BHU: Support to BHU Strengthening Economic Management (Contract No. 114191, 114193, 114195)

Deloitte Touche Tohmatsu India Private Limited Page 21

Exhibit 4: Data Structure of Toolkit

Data History 7.2

Provision has been made in the toolkit to keep the historic values of all the attributes, be it tax rates,

slabs or details of the properties. This would enable the Thromde to see temporal effects of various

scenarios. Thromde could also assess the tax collections from specific property through various tax

structures or through its development phases. This is a powerful feature for providing the right

information for optimal decision by the Thromde. A sample of historic data maintenance of a property

is provided hereunder.

Exhibit 5: History Data Maintenance

Pilot Implementation of Property Valuation Methodology in Phuentsholing Thromde

SC 103840 BHU: Support to BHU Strengthening Economic Management (Contract No. 114191, 114193, 114195)

Deloitte Touche Tohmatsu India Private Limited Page 22

Scenario Creation 7.3

Provision has been made in the system to make multiple scenarios for PAVA rates, QCG rates, tax

slabs, Tax rates, property classifications etc. The tax burden on taxpayers, revenue buoyancy,

expected revenue streams etc. can be compared across scenarios. This scenario module provides

the right information to the management of the Thromde. This would assist the Thromde both in

structuring the property tax system and stakeholder consultations. The scenario creation is

showcased in Exhibit 6.

Exhibit 6: Sample of Scenario Generation

Base Scenario Generator 7.4

As recommended under TA – 7724 ADB funded Strengthening Public Management; it is pertinent to

adopt a progressive slab based tax regime to ensure that tax burden is adjusted according to the

value of the property. Since, the value of the property already takes into consideration land-use,

location, size of property, accessibility, etc. the slabs can be based on property value alone. The

recommendations are provided in Annexure 10.2. Hence to provide for these recommendations, a tax

system generator has been provisioned in the toolkit. This calculates the existing the tax burden of the

taxpayer under the unit-based property tax system and designs a slab and rate structure for the

value-based property tax where there is minimum additional tax burden on the taxpayer. This is

stored as the base scenario for the toolkit against which all other scenarios can be benchmarked.

In order to maintain the tax burden at the same level as it is in the unit-based property tax system, the

tax rate should be between 0.06% to 0.08% of value of the property. However, Phuentsholing

Thromde does not have the power to enact a change of tax rates. Any change in tax rates would have

to be approved by the Parliament. Since, it will be difficult to get a rate change frequently; it is

recommended that the slabs be designed to balance this burden. In due course of time as PAVA and

DES revise their rates, the value of properties will increase and hence to tax receipts. As the values of

properties increase, they would move to higher slabs and mandate revision of rates which can then

be adjusted as per the requirements of the Thromde. The optimal rates can be arrived only when

valuation of all properties in the Thromde is complete. This would ensure that the tax rates are neither

a burden to the taxpayer nor on the fiscal health of the Thromde. Sample of the scenario generator is

given in Exhibit 7.

Pilot Implementation of Property Valuation Methodology in Phuentsholing Thromde

SC 103840 BHU: Support to BHU Strengthening Economic Management (Contract No. 114191, 114193, 114195)

Deloitte Touche Tohmatsu India Private Limited Page 23

Exhibit 7: Scenario Generator

Reports 7.5

Provision has been made in the toolkit to generate report that summarizes each scenario across the

change parameters and monitor expected revenue inflow from the properties already in the database.

Profile reports of each property can be generated which shows key property attributes, valuation of

land and building and expected property tax as per the base and final scenario. The Valuation Report

for the 50 properties is provided in Annexure 10.4.

Pilot Implementation of Property Valuation Methodology in Phuentsholing Thromde

SC 103840 BHU: Support to BHU Strengthening Economic Management (Contract No. 114191, 114193, 114195)

Deloitte Touche Tohmatsu India Private Limited Page 24

8 Activities undertaken for Piloting

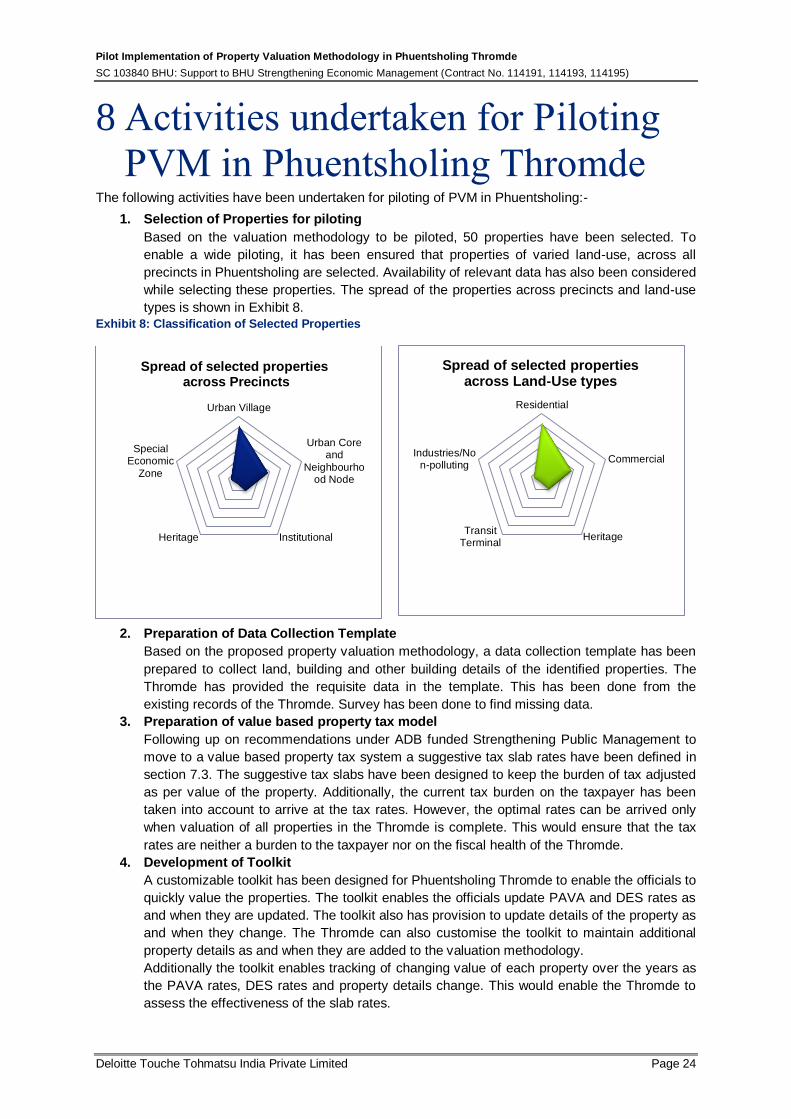

PVM in Phuentsholing Thromde The following activities have been undertaken for piloting of PVM in Phuentsholing:-

1. Selection of Properties for piloting

Based on the valuation methodology to be piloted, 50 properties have been selected. To

enable a wide piloting, it has been ensured that properties of varied land-use, across all

precincts in Phuentsholing are selected. Availability of relevant data has also been considered

while selecting these properties. The spread of the properties across precincts and land-use

types is shown in Exhibit 8.

Exhibit 8: Classification of Selected Properties

2. Preparation of Data Collection Template

Based on the proposed property valuation methodology, a data collection template has been

prepared to collect land, building and other building details of the identified properties. The

Thromde has provided the requisite data in the template. This has been done from the

existing records of the Thromde. Survey has been done to find missing data.

3. Preparation of value based property tax model

Following up on recommendations under ADB funded Strengthening Public Management to

move to a value based property tax system a suggestive tax slab rates have been defined in

section 7.3. The suggestive tax slabs have been designed to keep the burden of tax adjusted

as per value of the property. Additionally, the current tax burden on the taxpayer has been

taken into account to arrive at the tax rates. However, the optimal rates can be arrived only

when valuation of all properties in the Thromde is complete. This would ensure that the tax

rates are neither a burden to the taxpayer nor on the fiscal health of the Thromde.

4. Development of Toolkit

A customizable toolkit has been designed for Phuentsholing Thromde to enable the officials to

quickly value the properties. The toolkit enables the officials update PAVA and DES rates as

and when they are updated. The toolkit also has provision to update details of the property as

and when they change. The Thromde can also customise the toolkit to maintain additional

property details as and when they are added to the valuation methodology.

Additionally the toolkit enables tracking of changing value of each property over the years as

the PAVA rates, DES rates and property details change. This would enable the Thromde to

assess the effectiveness of the slab rates.

Urban Village

Urban Coreand

Neighbourhood Node

InstitutionalHeritage

SpecialEconomic

Zone

Spread of selected properties across Precincts

Residential

Commercial

HeritageTransit

Terminal

Industries/Non-polluting

Spread of selected properties across Land-Use types

Pilot Implementation of Property Valuation Methodology in Phuentsholing Thromde

SC 103840 BHU: Support to BHU Strengthening Economic Management (Contract No. 114191, 114193, 114195)

Deloitte Touche Tohmatsu India Private Limited Page 25

The toolkit has the provision to calculate slab rates to keep overall tax burden same as the

existing burden which enabling the Thromde to adjust the extent of cross-subsidisation.

Sample screenshots of the Toolkit is given in Exhibit 9.

Exhibit 9: Toolkit Screenshot

5. Data Migration

Data for the 50 selected properties has been migrated into the Toolkit and valuation done.

The valuation of all the properties has been done and saved into the Toolkit. The toolkit

recalculates the value of properties when the details of the property are updated or the rates

as defined by PAVA and DES are updated.

Valuation of Selected Properties

All the selected properties have been valued based on the migrated data. Detailed valuation

report on calculated value of each of the properties is given in Annexure 10.2.

6. Training

Official from Phuentsholing Thromde and MoWHS are being identified to undertake training to

use the toolkit to put the Property Valuation Methodology into practice. Training material for

the same is being finalized. A tentative list of agencies whose officials are to be trained is

given in Annexure 10.2. The draft of the training presentation is given in Annexure 10.3.

Pilot Implementation of Property Valuation Methodology in Phuentsholing Thromde

SC 103840 BHU: Support to BHU Strengthening Economic Management (Contract No. 114191, 114193, 114195)

Deloitte Touche Tohmatsu India Private Limited Page 26

9 Next Steps This report concludes our scope of work. RGoB and the Thromde need to take further action to

strengthen and institutionalize the property valuation methodology and adopt a value-based property

tax system. The following are the pertinent next steps:

Structure of Property Valuation and Tax

Presently there is a practice of levying differential land-tax rates on residential and non-residential

properties. This difference has been maintained at 1:2 levels for residential and commercial.

However, post assessing the proposed valuation methodology it has been observed that this

difference is increasing to 1:3. In that scenario, it will be not possible to maintain similar tax

structure for various types of land. Additionally, further discrimination in tax rates might not be

acceptable especially after differential treatment during valuation. To maintain the tax burden on the

taxpayers at the same level as in the previous methodology it is suggested that the levels of

difference during valuation be reduced or have no differentiation at valuation level to have

differential tax rates. To do this the toolkit will come in handy as it has provisions for scenarios to be

tested before actual implementation.

Finalization of Tax Slabs

In discussion with stakeholders, the tax slabs and rates need to be finalised. This has to be duly

substantiated with service costing. The benefits of moving to the value based property tax need to

be highlighted to the stakeholders.

Stakeholder Consultations

This is an important step for the success of the reform. Consultation with the taxpayers and their

agreement is needed for implementing value based property tax. There is a need to educate the

taxpayers of the benefits, ease and transparency of value-based tax. The actual tax burden also

needs to be quantified for solicit this agreement. These consultations would also provide critical

feedback to property classification, slab design and tariff fixation.

Requisite Amendments

The current Municipal Financial Policy, 2012 does not delineate the methodology to compute land

and urban house tax. While the move to value-based property tax was mentioned in the Draft

Municipal Finance Policy, 2009 the same has been dropped in the final version. The Municipal

Finance Rules are being drafted my MoWHS to put the Municipal Finance Policy, 2012 into

practice. It is recommended that the property valuation methodology form a part of these rules.

Additionally, the rules would also require delineating the methodology to levy property tax on the

value of the property computed based on PVM. Approval of parliament would also have to be

sought for the property tax slabs and rates. This landmark amendment would also pave the way for

other Thromdes to move to value based property tax.

Property Survey

Phuentsholing Thromde has already initiated an exercise to update the details of all the properties

with its jurisdiction. Additional land details have been updated by NLCS under the National

Cadastral Resurvey Project. This information shall also be made available to the Thromde post

processing. The Thromde shall be in a better position to levy the tax at the fair value of the property.

MRAS

When the property details are being updated into the Municipal Revenue Administration System,

provisions need to be made in the system to enable valuation of properties and levy of tax based on

value of the property.

Once the piloting of the PVM is done and value-based property tax implemented, the following maybe

taken up in the medium to long term as the taxpayers of the Thromde become more accepting to the

valuation.

Pilot Implementation of Property Valuation Methodology in Phuentsholing Thromde

SC 103840 BHU: Support to BHU Strengthening Economic Management (Contract No. 114191, 114193, 114195)

Deloitte Touche Tohmatsu India Private Limited Page 27

Single Property Tax

All property related taxes i.e. Land Tax, Urban House Tax, Garbage Collection and Street Lighting

Fee etc. may be clubbed together into a single tax to make monitoring, demand generation and

payment easier. This would require amendment to the Local Government Act.

Self-Assessment

The Thromde may move to valuation methodology which is objective and transparent, which would

enable the taxpayers to value their own property. Thromde may additionally levy self-assessed tax

on property owners. This would not only reduce the workload of the Thromde but also make

taxation more transparent and reduce the number of appeals.

Pilot Implementation of Property Valuation Methodology in Phuentsholing Thromde

SC 103840 BHU: Support to BHU Strengthening Economic Management (Contract No. 114191, 114193, 114195)

Deloitte Touche Tohmatsu India Private Limited Page 28

10 Annexure

Matrix for Giving Weightages to Different Land Uses of PUDP 2007-17 10.1

Uses allowed

Permissible

Building Height

LAND USE ZONE

R =

Pre

dom

ina

ntly r

esid

ential use

M =

All

uses in R

+ s

mall

busin

esses

C =

All

uses in R

& M

+ M

ediu

m b

usin

esses

P =

All

uses in R

+ R

ecre

atio

n

I =

S

erv

ice

ind

ustr

ies,

ware

housin

g,

go

dow

n,

sto

rage e

tc

G =

Recre

ation

al uses o

nly

U

=

Bus

&

truck

term

inals

, dry

p

ort

, air

port

,

trea

tme

nt

pla

nt,

dis

posal sites e

tc

N =

riv

er

fro

nts

, w

ate

rshe

ds e

tc

G to G

+1 (

1+

1/3

)

G+

2 t

o G

+3 (

1+

1/3

+1/3

)

Above G

+3 u

pto

G+

9 (

1+

1/3

+1/3

+1

/3)

To

tal W

eig

hti

ng

s

Avera

ge W

eig

hti

ng

s

Residential ( R )

Zone I

1

2.00 3.00 1.50

Zone III 2.00 3.00 1.50

Zone IV 1.67 2.67 1.33

Zone V 1.83 2.83 1.42

Zone VI 1.83 2.83 1.42

Zone VII 1.67 2.67 1.33

Zone VIII 1.67 2.67 1.33

Zone IX 1.67 2.67 1.33

Mixed Use (M) Zone III, IV,

VIII & IX 1.5

1.67 3.17 1.58

Commercial ( C )

Zone II

2

1.67 3.67 1.83

Zone VI 1.83 3.83 1.92

Zone VII 1.67 3.67 1.83

Public & Semipublic

(P)

Zone III

1.5

1.67 3.17 1.58

Zone IV 1.83 3.33 1.67

Zone V 1.67 3.17 1.58

Zone VII 1.67 3.17 1.58

Warehousing & Light

Industries ( I )

Zone I 1.5

1.67 3.17 1.58

Zone VI 1.67 3.17 1.58

Recreational (G) Zone I, II,

III & VIII 1.5

1.33 2.83 1.42

Utilities & Special

Reservation (U) 1.5

1.33 2.83 1.42

No Development Zone

(N) 1

1 2.00 1.00

Pilot Implementation of Property Valuation Methodology in Phuentsholing Thromde

SC 103840 BHU: Support to BHU Strengthening Economic Management (Contract No. 114191, 114193, 114195)

Deloitte Touche Tohmatsu India Private Limited Page 29

Official of the Following Agencies are to be Trained 10.2

S.No. Agency

1 Department of Public Accounts

2 Property Assessment and Valuation Agency

3 Department of Engineering Services

4 Phuentsholing Thromde

5 Thimphu Thromde

6 Gelephu Thromde

7 Samdrup-Jongkhar Thromde

Pilot Implementation of Property Valuation Methodology in Phuentsholing Thromde

SC 103840 BHU: Support to BHU Strengthening Economic Management (Contract No. 114191, 114193, 114195)

Deloitte Touche Tohmatsu India Private Limited Page 30

Training Material 10.3

Pilot Implementation of Property Valuation Methodology in Phuentsholing Thromde

SC 103840 BHU: Support to BHU Strengthening Economic Management (Contract No. 114191, 114193, 114195)

Deloitte Touche Tohmatsu India Private Limited Page 31

Pilot Implementation of Property Valuation Methodology in Phuentsholing Thromde

SC 103840 BHU: Support to BHU Strengthening Economic Management (Contract No. 114191, 114193, 114195)

Deloitte Touche Tohmatsu India Private Limited Page 32

Pilot Implementation of Property Valuation Methodology in Phuentsholing Thromde

SC 103840 BHU: Support to BHU Strengthening Economic Management (Contract No. 114191, 114193, 114195)

Deloitte Touche Tohmatsu India Private Limited Page 33

Pilot Implementation of Property Valuation Methodology in Phuentsholing Thromde

SC 103840 BHU: Support to BHU Strengthening Economic Management (Contract No. 114191, 114193, 114195)

Deloitte Touche Tohmatsu India Private Limited Page 34

Pilot Implementation of Property Valuation Methodology in Phuentsholing Thromde

SC 103840 BHU: Support to BHU Strengthening Economic Management (Contract No. 114191, 114193, 114195)

Deloitte Touche Tohmatsu India Private Limited Page 35

Pilot Implementation of Property Valuation Methodology in Phuentsholing Thromde

SC 103840 BHU: Support to BHU Strengthening Economic Management (Contract No. 114191, 114193, 114195)

Deloitte Touche Tohmatsu India Private Limited Page 36

Pilot Implementation of Property Valuation Methodology in Phuentsholing Thromde

SC 103840 BHU: Support to BHU Strengthening Economic Management (Contract No. 114191, 114193, 114195)

Deloitte Touche Tohmatsu India Private Limited Page 37

Pilot Implementation of Property Valuation Methodology in Phuentsholing Thromde

SC 103840 BHU: Support to BHU Strengthening Economic Management (Contract No. 114191, 114193, 114195)

Deloitte Touche Tohmatsu India Private Limited Page 38

Pilot Implementation of Property Valuation Methodology in Phuentsholing Thromde

SC 103840 BHU: Support to BHU Strengthening Economic Management (Contract No. 114191, 114193, 114195)

Deloitte Touche Tohmatsu India Private Limited Page 39

Pilot Implementation of Property Valuation Methodology in Phuentsholing Thromde

SC 103840 BHU: Support to BHU Strengthening Economic Management (Contract No. 114191, 114193, 114195)

Deloitte Touche Tohmatsu India Private Limited Page 40

Pilot Implementation of Property Valuation Methodology in Phuentsholing Thromde

SC 103840 BHU: Support to BHU Strengthening Economic Management (Contract No. 114191, 114193, 114195)

Deloitte Touche Tohmatsu India Private Limited Page 41

Pilot Implementation of Property Valuation Methodology in Phuentsholing Thromde

SC 103840 BHU: Support to BHU Strengthening Economic Management (Contract No. 114191, 114193, 114195)

Deloitte Touche Tohmatsu India Private Limited Page 42

Pilot Implementation of Property Valuation Methodology in Phuentsholing Thromde

SC 103840 BHU: Support to BHU Strengthening Economic Management (Contract No. 114191, 114193, 114195)

Deloitte Touche Tohmatsu India Private Limited Page 43

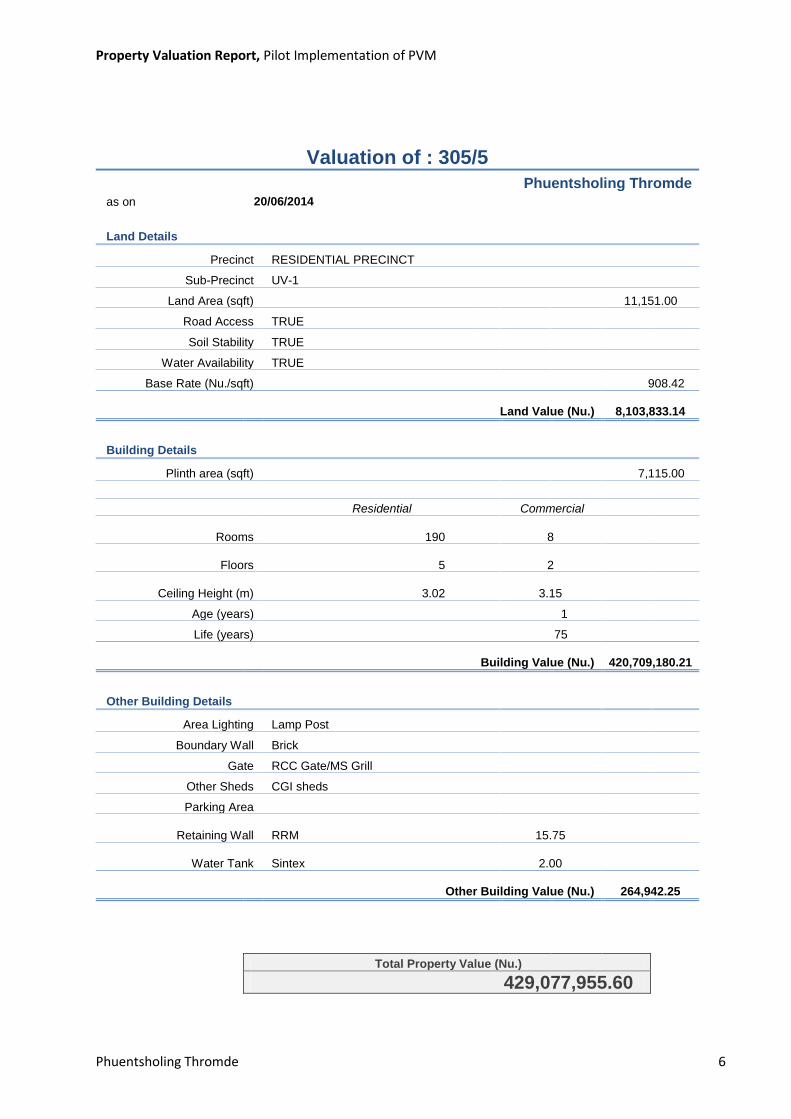

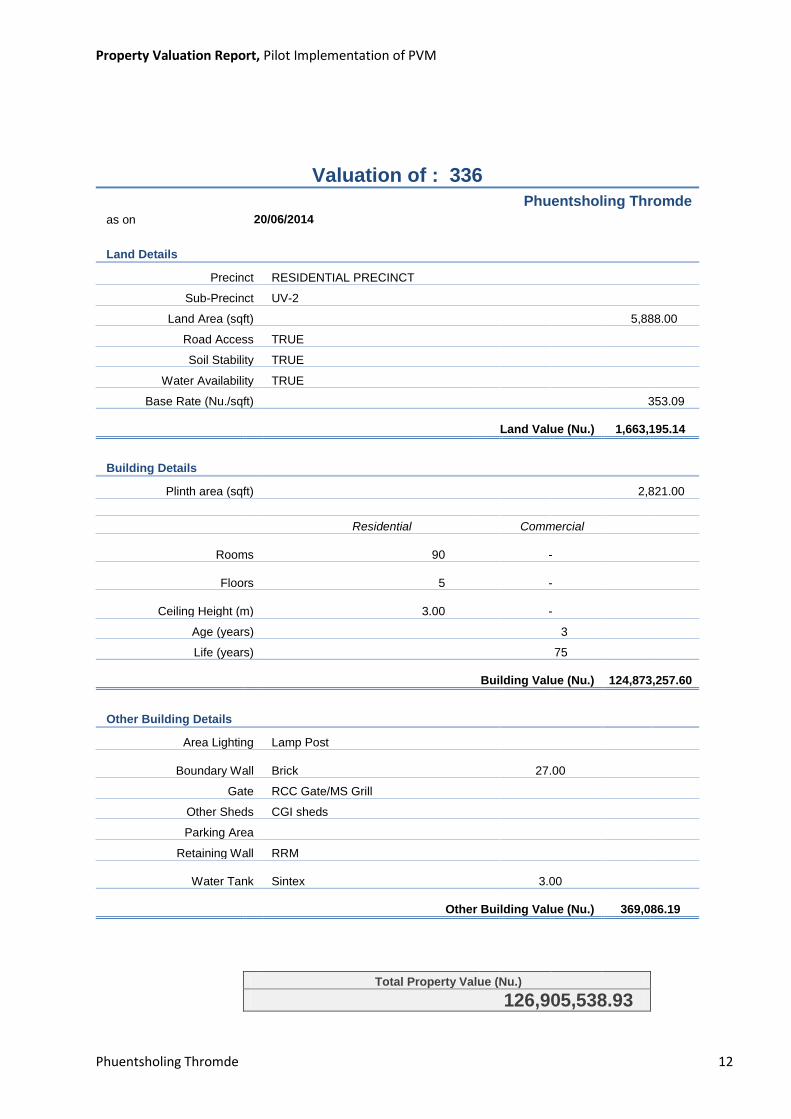

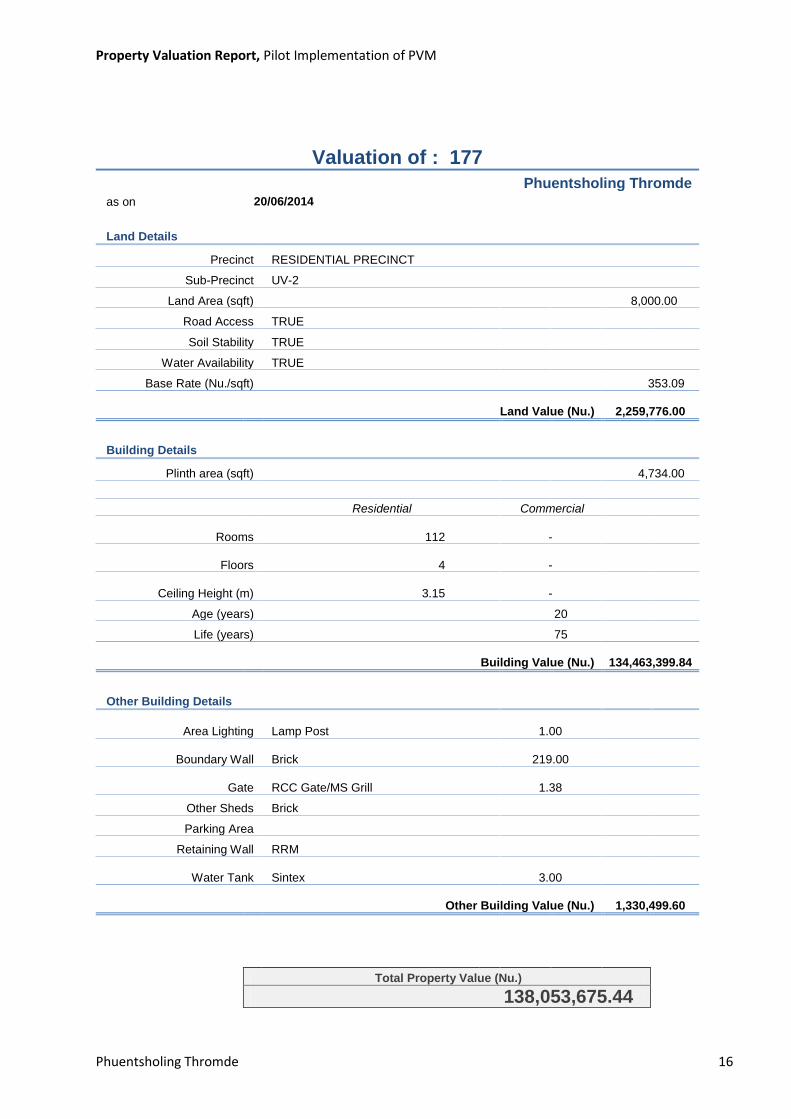

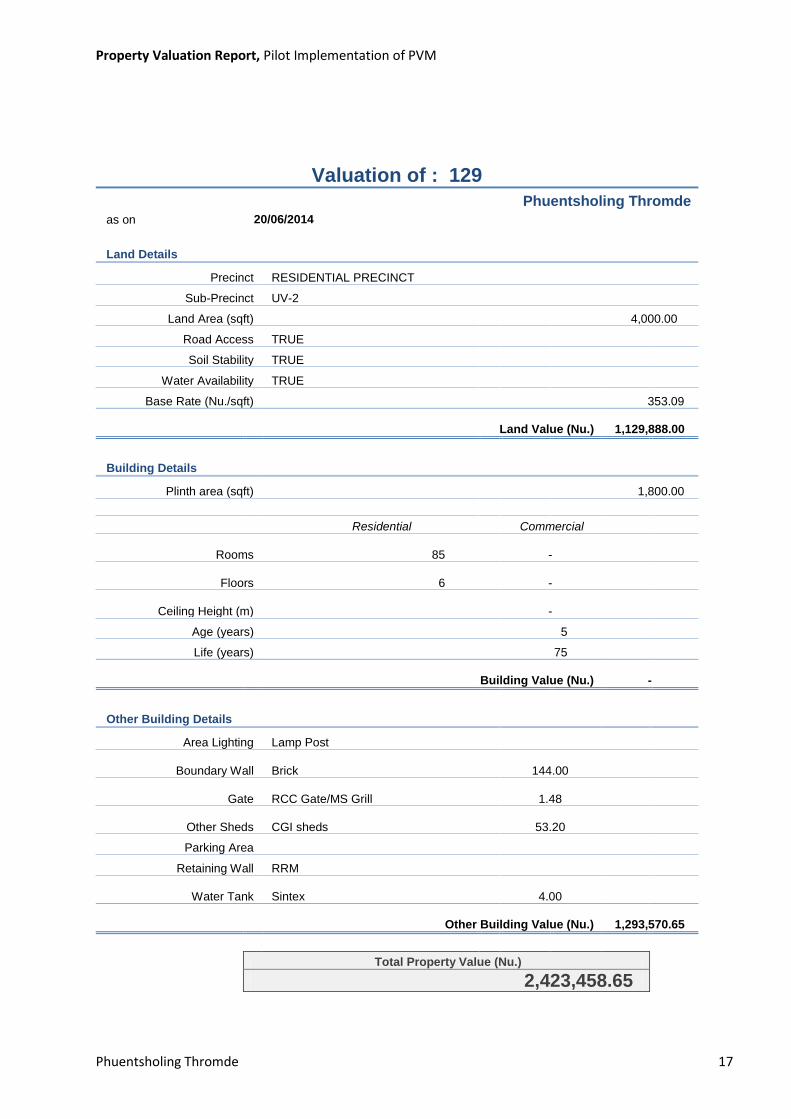

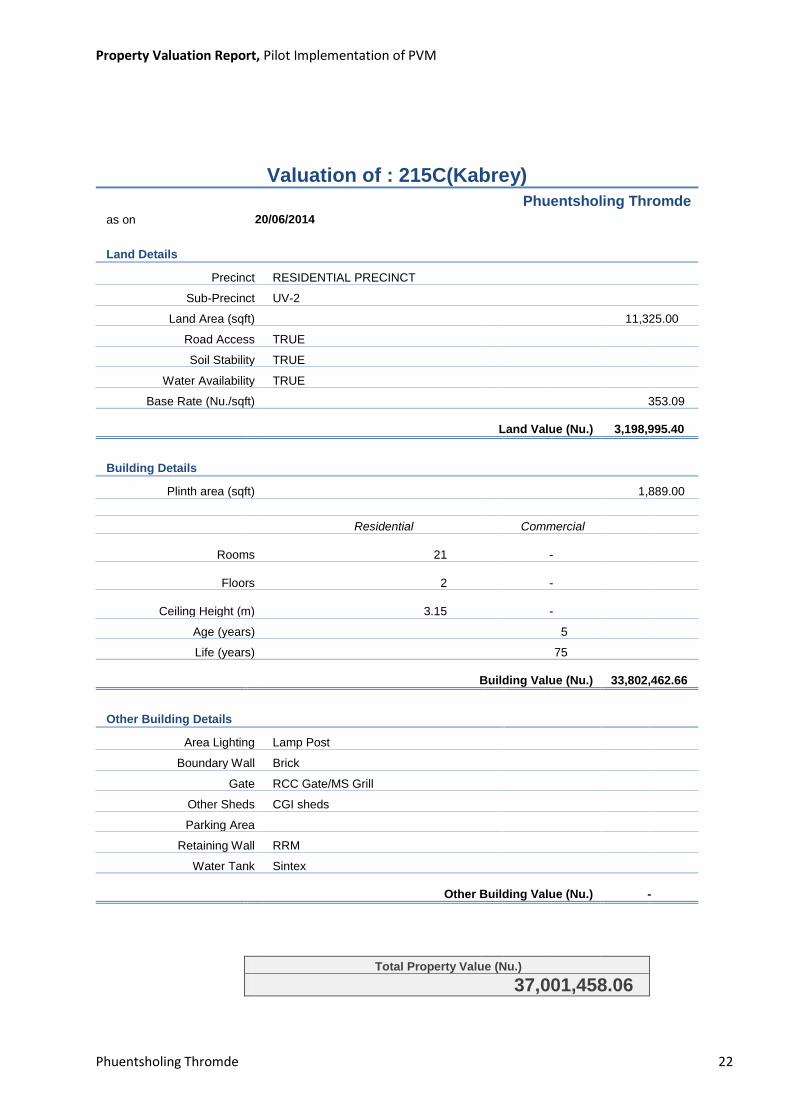

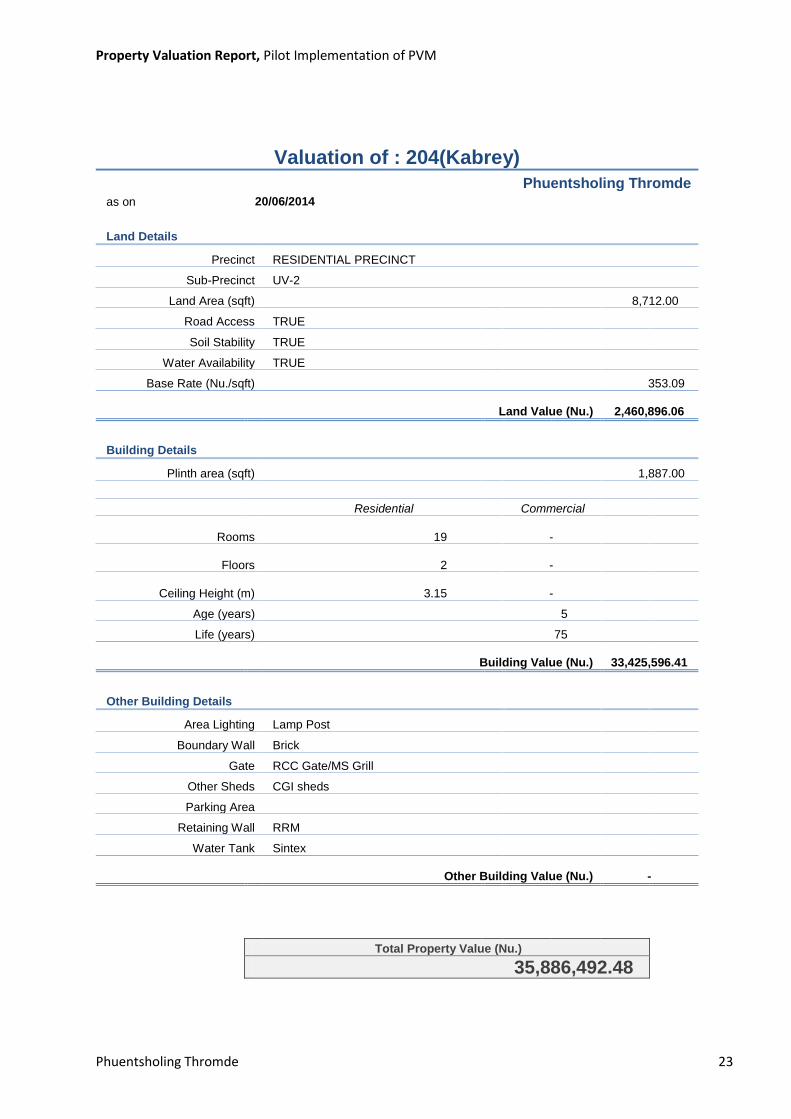

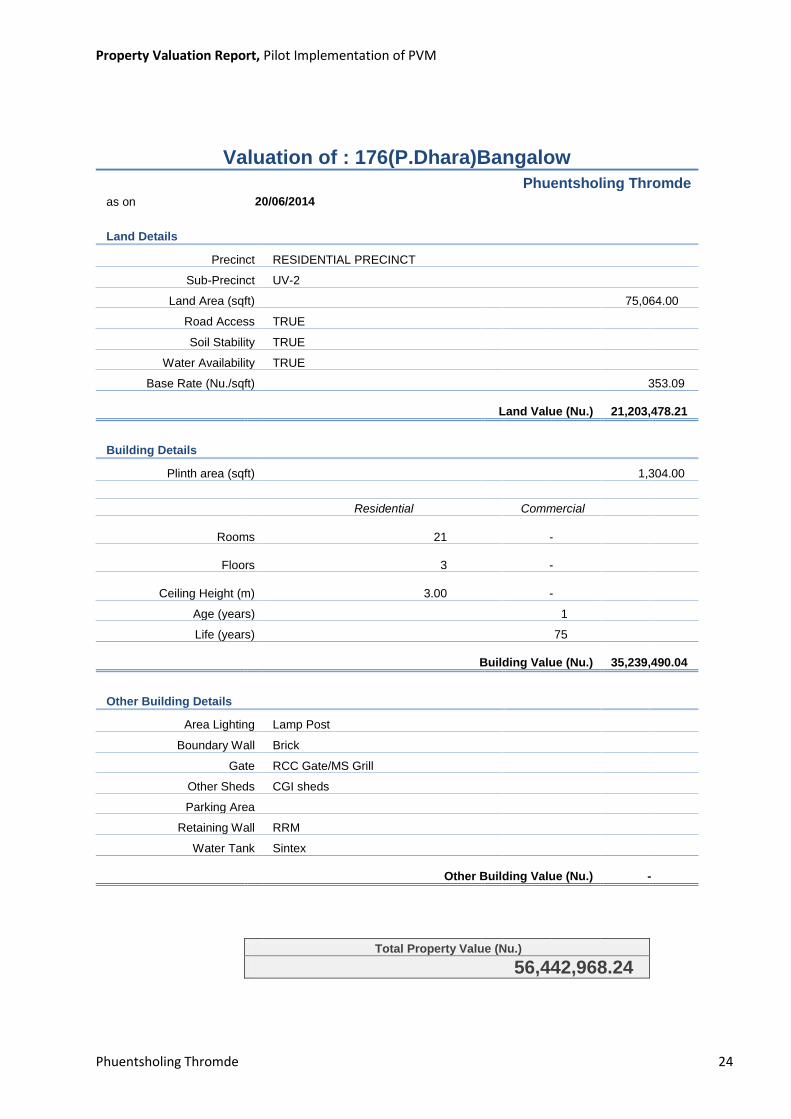

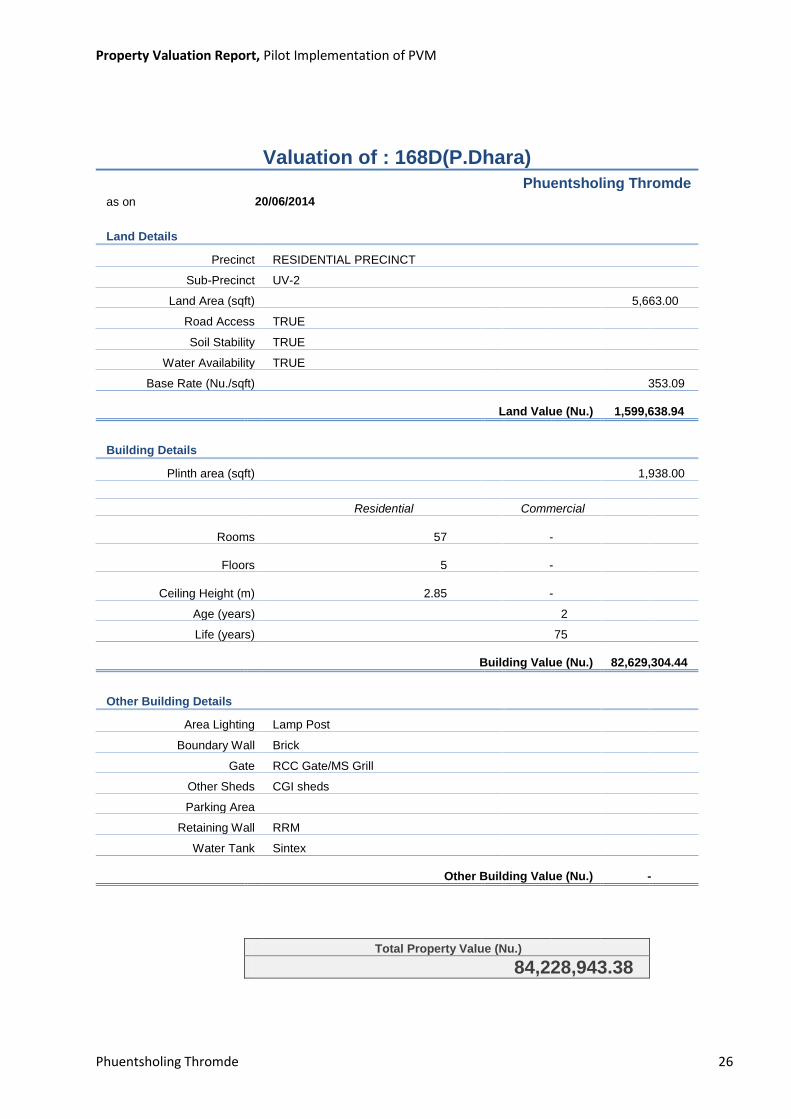

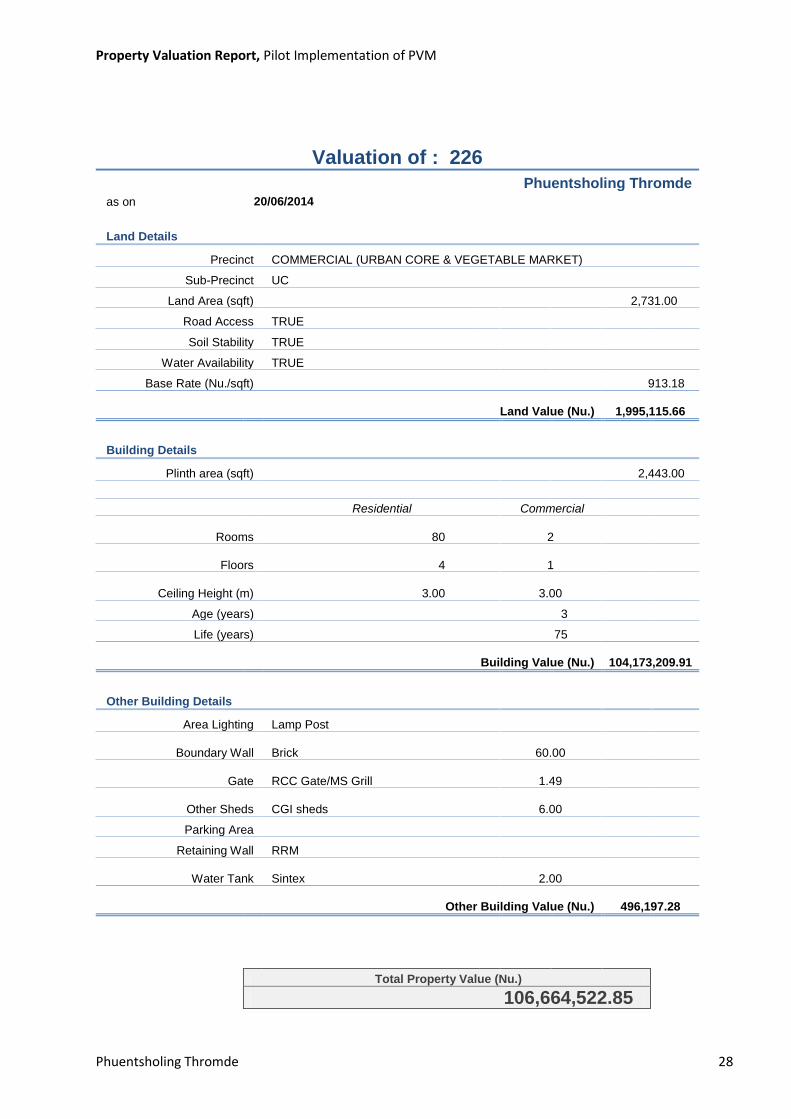

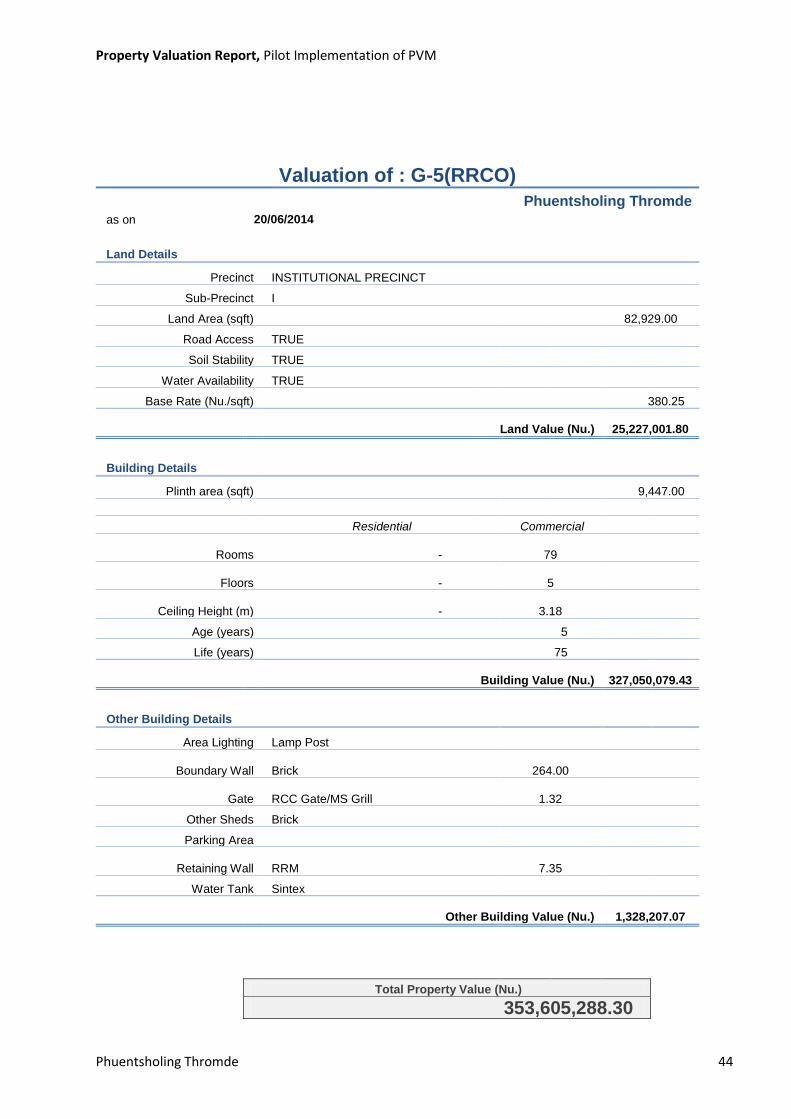

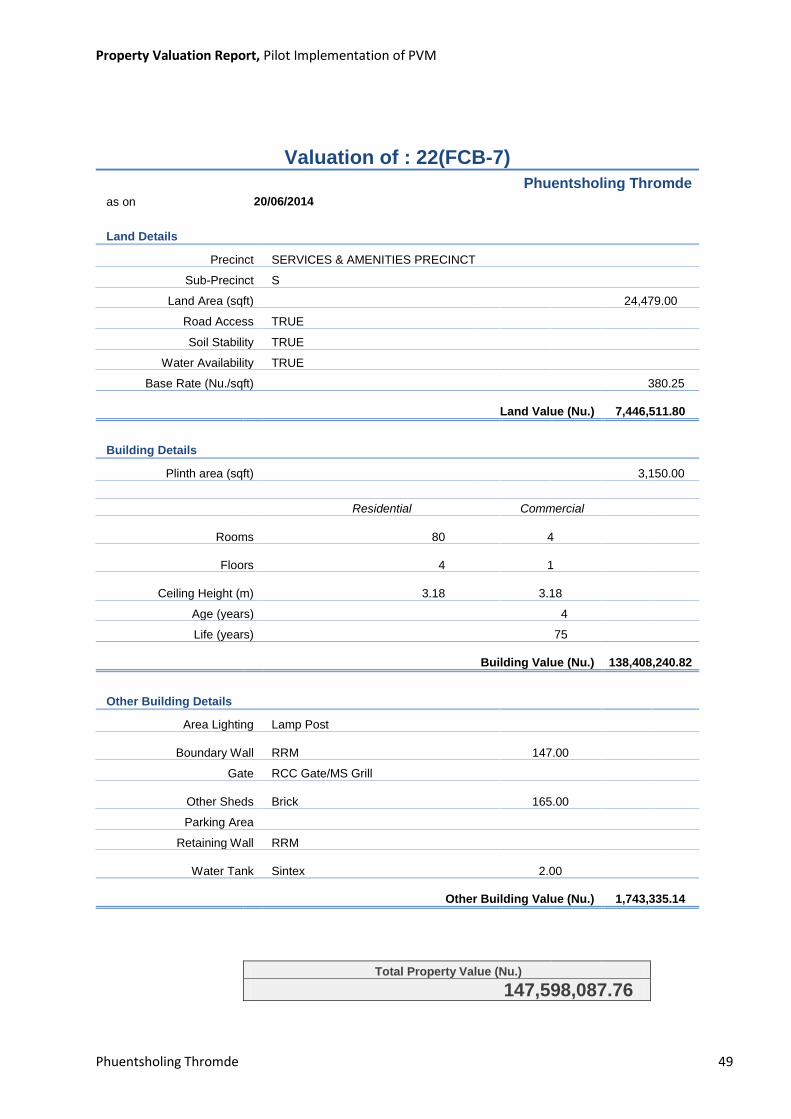

Valuation Report of the 50 properties as generated by the Toolkit 10.4

Property

Valuation

Report Pilot Implementation of PVM

Phuentsholing Thromde

Property Valuation Report, Pilot Implementation of PVM

Phuentsholing Thromde 1

Valuation of : 196A

Phuentsholing Thromde

as on 20/06/2014

Land Details

Precinct RESIDENTIAL PRECINCT

Sub-Precinct UV-1

Land Area (sqft) 11,283.00

Road Access TRUE

Soil Stability TRUE

Water Availability TRUE

Base Rate (Nu./sqft) 908.42

Land Value (Nu.)

8,199,762.29

Building Details

Plinth area (sqft) 3,518.00

Residential Commercial

Rooms 105 -

Floors 5 -

Ceiling Height (m) 3.00 -

Age (years) 7

Life (years) 75

Building Value (Nu.)

147,074,915.20

Other Building Details

Area Lighting Lamp Post

3.00

Boundary Wall RRM

106.50

Gate RCC Gate/MS Grill

1.47

Other Sheds CGI sheds

236.36

Parking Area

Retaining Wall RRM

Water Tank Sintex

3.00

Other Building Value (Nu.)

1,768,325.37

Total Property Value (Nu.)

157,043,002.86

Property Valuation Report, Pilot Implementation of PVM

Phuentsholing Thromde 2

Valuation of : 196B

Phuentsholing Thromde

as on 20/06/2014

Land Details

Precinct RESIDENTIAL PRECINCT

Sub-Precinct UV-1

Land Area (sqft) 4,812.00

Road Access TRUE

Soil Stability TRUE

Water Availability TRUE

Base Rate (Nu./sqft) 908.42

Land Value (Nu.)

3,497,053.63

Building Details

Plinth area (sqft) 2,211.00

Residential Commercial

Rooms 64

5

Floors 4

2

Ceiling Height (m) 2.85

2.85

Age (years) 5

Life (years) 75

Building Value (Nu.)

100,813,453.61

Other Building Details

Area Lighting Lamp Post

Boundary Wall RRM

50.70

Gate RCC Gate/MS Grill

Other Sheds CGI sheds

20.40

Parking Area

Retaining Wall RRM

Water Tank Sintex

1.00

Other Building Value (Nu.)

301,277.83

Total Property Value (Nu.)

104,611,785.08

Property Valuation Report, Pilot Implementation of PVM

Phuentsholing Thromde 3

Valuation of : 306

Phuentsholing Thromde

as on 20/06/2014

Land Details

Precinct RESIDENTIAL PRECINCT

Sub-Precinct UV-1

Land Area (sqft) 5,116.00

Road Access TRUE

Soil Stability TRUE

Water Availability TRUE

Base Rate (Nu./sqft) 908.42

Land Value (Nu.)

3,717,981.38

Building Details

Plinth area (sqft) 2,216.00

Residential Commercial

Rooms 56 -

Floors 4 -

Ceiling Height (m) 3.15 -

Age (years) 5

Life (years) 75

Building Value (Nu.)

80,108,931.84

Other Building Details