Download presentation source

33

Are Refiners Entering a Are Refiners Entering a Golden Age or a Short Golden Age or a Short Cycle? Cycle? Global Refining Strategies 2007 Barcelona, Spain April 2007 Joanne Shore John Hackworth Energy Information Administration www.eia.doe.gov

description

Transcript of Download presentation source

Are Refiners Entering a Are Refiners Entering a Golden Age or a Short Cycle?Golden Age or a Short Cycle?

Global Refining Strategies 2007Barcelona, SpainApril 2007

Joanne ShoreJohn HackworthEnergy Information Administration

www.eia.doe.gov

Short-Term Cycle or Golden Age? Short-Term Cycle or Golden Age?

• What has driven prices, margins, and light heavy price differentials to current high levels?– How are these three variables

related?

– What are the main drivers?

• How long might prices, margins, & differentials stay elevated? 0

10

20

30

40

50

60

70

80

90

100

Jan-95 Jan-00 Jan-05

$/B

arre

l

No. 2 Heating Oil Gulf Coast

WTI Crude Price

Crude Oil & Distillate Fuel Prices

Source: Bloomberg spot prices

OutlineOutline

• High Prices: Crude Oil

• Drivers and Uncertainties Behind Margins and Differentials

• Other Supply/Demand Factors Affecting Future Petroleum Markets– Energy Efficiency– Biofuels– Surge in Capacity

Expansion Plans

The Main Factor Behind High Product The Main Factor Behind High Product Prices: Crude Oil PricesPrices: Crude Oil Prices

• Strong Demand Growth

• Less Supply Growth

• Different Prospects for Future than seen in 1980

0

1

2

3

4

5

6

1991-1997

Average

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Mil

lio

n B

arr

els

Pe

r D

ay

World Surplus Crude Oil Production Capacity Forecast

Today: Little World Crude Oil Surplus Today: Little World Crude Oil Surplus Production CapacityProduction Capacity

Source: EIA Short Term Energy Outlook March 2007

0

10

20

30

40

50

60

70

80

0 1 2 3 4 5 6 7 8

Surplus OPEC Capacity MMB/D

WT

I P

rice

- 2

005

$/B

arre

l

WTI Crude Price vs. OPEC Surplus Crude Production Capacity (Apr 1999 - Sept 2006)

Source: Bloomberg WTI; EIA Calculations

Today: See Typical Economic Relationship Today: See Typical Economic Relationship Between Little Surplus Capacity and PriceBetween Little Surplus Capacity and Price

Prospects for Demand Correction Different Prospects for Demand Correction Different than Early 1980’s Correctionthan Early 1980’s Correction

World Demand (MMB/D)

0102030405060708090

1965 1974 1983 1992 2001

Gasoline & Naphtha

Middle Distillates

Fuel Oil

Other

• Fuel oil decline will not ease market pressure today as in early 1980s

• Easy fuel efficiency gains made in early 1980s

• Large Asian economies account for more growth today

Notes: World Excluding FSU, Gasoline includes aviation gasoline & light distillate feedstocks

Source: BP World Statistical Review 2006

Today’s OPEC & Non-OPEC Production Today’s OPEC & Non-OPEC Production Requirements Different Than 1979-80Requirements Different Than 1979-80

0

5

10

15

20

25

30

35

40

4519

65

1969

1973

1977

1981

1985

1989

1993

1997

2001

2005

Mil

lio

n B

arre

sl P

er D

ay

OPEC

Non-OPEC

OPEC & Non-OPEC Crude Oil Production

Source: EIA Annual & Monthly Energy Reviews.

Limited Prospects for Non-OPEC Crude Limited Prospects for Non-OPEC Crude Supply Increases in Short RunSupply Increases in Short Run

• Fewer non-OPEC exploration prospects, field size declining

• Most efficient companies have limited access to known reserves

• Tar sands growth costly and slow

1%14%

85%

FullInternationalCompanyAccess

LimitedInternationalAccess

SovietReserves

National OilCompanyReserves

Source: Data from Business Week Online Slide Show: Why the Oil Giants Look Weaker http://www.businessweek.com/magazine/content/06_20/b3984001.htm May 15, 2006

16%

19%

65%

2004

1960s Known Reserve Access

Prices Expected to Remain Relatively High Prices Expected to Remain Relatively High in Short Termin Short Term

• Future uncertain but could stay relatively high

• OPEC position has strengthened

• Demand growth has moderated only slightly

• No large surge in non-OPEC crude or other supply -- and costly

• Only OPEC can build excess capacity

$0

$10

$20

$30

$40

$50

$60

$70

$80

Jan

-98

Jan

-99

Jan

-00

Jan

-01

Jan

-02

Jan

-03

Jan

-04

Jan

-05

Jan

-06

Jan

-07

Jan

-08

WTI Crude Oil Price $/Barrel

Source: EIA Short Term Energy Outlook March 2007

Drivers & Uncertainties Behind Refinery Drivers & Uncertainties Behind Refinery Margins and DifferentialsMargins and Differentials

• Margins– Growing, but volatile

– Shift in gasoline and distillate contributions

– Refining utilization – over-emphasized factor?

• Light-Heavy Differentials and the Importance of Crude oil Price

• Future Considerations

3-2-1 Spread (Margin Indicator) Grew with 3-2-1 Spread (Margin Indicator) Grew with Crude Price – But Not SmoothlyCrude Price – But Not Smoothly

$0

$5

$10

$15

$20

$25

$30

$35

$40Ja

n-9

0

Jan

-92

Jan

-94

Jan

-96

Jan

-98

Jan

-00

Jan

-02

Jan

-04

Jan

-06

Sp

read

--

$/B

arre

l

$0

$10

$20

$30

$40

$50

$60

$70

$80

Cru

de

Pri

ce -

- $/

Bar

rel

Crude Price and Spread ($/Barrel)

WTI Spot

3-2-1 Spread

Source: Bloomberg Spot Data: Gulf Coast Gasoline, No. 2 and WTI.

Distillate Cracks Increased More than Distillate Cracks Increased More than GasolineGasoline

$0

$2

$4

$6

$8

$10

$12

$141

99

0

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

$/B

arre

l

GC Conv - WTI GC No2 - WTI

Annual Average Gulf Coast Spot Cracks

Source: Bloomberg spot prices – Gulf Coast Conventional & No. 2 minus WTI

World Utilization Up, But Atlantic Basin World Utilization Up, But Atlantic Basin Utilization Not Changed Much RecentlyUtilization Not Changed Much Recently

50%55%60%65%70%75%80%85%90%95%

100%

1980 1985 1990 1995 2000 2005

World

U.S.

EU-25

U.S & European Refinery Utilizations

Source: BP World Statistics 2006 (crude runs/capacity) and EIA Annual Energy Review (gross inputs/capacity).

Light-Heavy Differentials Rose Since 2000, Light-Heavy Differentials Rose Since 2000, But Will They Remain High?But Will They Remain High?

38%

35%

24%

3%

60%

25%

14%1% LPG & Gases

Gasoline

Distillate

Heavy Gas Oil &Bottoms

Light Crude

Heavy Crude

Crude Oil Fractions

• Product markets drive light-heavy product prices

• Impact of total product barrel value on crude value

• Differential: Incentives for heavy-crude high-conversion refining

Light-Heavy Product Price Difference Light-Heavy Product Price Difference Increases with Crude Oil PriceIncreases with Crude Oil Price

0102030405060708090

100J

an

-95

Ja

n-9

6

Ja

n-9

7

Ja

n-9

8

Ja

n-9

9

Ja

n-0

0

Ja

n-0

1

Ja

n-0

2

Ja

n-0

3

Ja

n-0

4

Ja

n-0

5

Ja

n-0

6

Ja

n-0

7

$/B

arr

el

No. 2 Heating Oil Gulf Coast

WTI Crude Price

3% Resid Gulf Coast

Crude Oil, Distillate, Residual Fuel Prices

Source: Bloomberg spot price

Light-Heavy Crude Price Differential Light-Heavy Crude Price Differential & Crude Oil Price Move Together& Crude Oil Price Move Together

$0

$4

$8

$12

$16

$20Ja

n-9

5

Jan

-96

Jan

-97

Jan

-98

Jan

-99

Jan

-00

Jan

-01

Jan

-02

Jan

-03

Jan

-04

Jan

-05

Jan

-06

Jan

-07

Lig

ht-

Hea

vy D

iffe

ren

tial

$0

$16

$32

$48

$64

$80

Cru

de

Pri

ce

WTI-Maya

WTI Crude Price

Crude Price & Price Differential ($/Barrel)

Source: Bloomberg spot prices

If WTI Drops from $70 to $40, Will Differential Drop If WTI Drops from $70 to $40, Will Differential Drop by 40% ($17-$10)?by 40% ($17-$10)?

R2 = 0.807

$0

$5

$10

$15

$20

$25

$0 $20 $40 $60 $80

WTI

WT

I-M

aya

Sp

read

WTI Price Versus WTI-Maya Spread 1/91-3/07

Source Bloomberg WTI Cushing and Maya.

If WTI Drops from $70 to $40, Margin Relationship If WTI Drops from $70 to $40, Margin Relationship Less CertainLess Certain

R2 = 0.467

$0

$5

$10

$15

$20

$25

$0 $20 $40 $60 $80

WTI

3-2

-1 P

ric

e S

pre

ad

WTI Price Versus 3-2-1 Spread (1/91-3/07*)

Note: Three hurricane months excluded (Aug-Oct 2006) Source Bloomberg Gulf Coast product spot prices and WTI Cushing.

Bottom Line: Crude Price Important Bottom Line: Crude Price Important Indicator of Future ReturnsIndicator of Future Returns

• Rising price: Increasing margins, increasing differentials

• Declining price: Decreasing margins, decreasing differentials

• Price settles within a high price band– Margins lose their boost from rising market dynamics,

but may stay higher than seen in the 1990’s– Differentials remain high -- even with more conversion

capacity

Other Supply/Demand Factors Affecting Other Supply/Demand Factors Affecting Future Petroleum MarketsFuture Petroleum Markets

Demand • Distillate/Gasoline Shift • Energy Efficiency

Supply• Biofuels Reducing Need for

Some Capacity• Capacity Expansions –

Oversupply?40%

45%

50%

55%

60%

65%

70%

1985

1988

1991

1994

1997

2000

2003

Middle Distillates Share of Gasoline and Middle Distillates Consumption

EU-25

World Excl FSU and EU-25

Source: BP World Statistics 2006.

Demand Factors Impacting Future Atlantic Demand Factors Impacting Future Atlantic Basin NeedsBasin Needs

• Europe’s growing imbalance between distillate & gasoline

• U.S. continued growth in gasoline & distillate – with distillate growing more strongly

• Potential increase in efficiency requirements (greenhouse gas, energy security, etc.)

– Europe’s potential mandates– U.S potential policy change– Slow impacts 0

200

400

600

800

1,000

1,200

19

95

19

97

19

99

20

01

20

03

20

05

Th

ou

sa

nd

Ba

rre

ls P

er

Da

y

Europe's Gasoline Exports & U.S. Net Imports

OECD Europe Exports

U.S. Imports

Note: U.S. imports includes blending components. 2006 is based on January-October data. Source: IEA, EIA Petroleum Supply Monthly & Annual

Biofuels Changing Capacity NeedsBiofuels Changing Capacity Needs

• Europe’s biofuel interest increasing– Biodiesel compatible with diesel

capacity shortfall– Ethanol in gasoline exacerbates

over-supply situation

• U.S. seeing diminishing need for new gasoline capacity– Increase in ethanol– Increase in import availability

from Europe

Refinery Capacity Poised for Major Refinery Capacity Poised for Major ExpansionsExpansions

• Incentives resulted in capacity investment plans

• Plans cover all areas– Increased throughputs– Increased use of low-quality

heavy feedstocks– Increased light product yields– Upgrade to top quartile

U.S. Capacity Expansions 2007 through 2011 (KB/D)U.S. Capacity Expansions 2007 through 2011 (KB/D)

5-Year Expansions

Dist. FCC HC Coking

Conoco Phillips 120 0 20 90

Flint Hills 50 0 0 0

Marathon 180 0 70 44

Motiva 325 0 75 80

Total 0 0 0 50

Sinclair 0 0 0 30

Valero 75 0 0 0

Other 57 33 30 4

Creep-Closings 250 158 0 0

TOTAL 1057 191 195 298

Note: Dist: Crude distillation unit; FCC: Fluid catalytic cracking; HC: Hydrocracking. Sources: Oil & Gas Journal, company presentations, Hydrocarbon Processing Boxscore

Capacity and Complexity Increases Through Capacity and Complexity Increases Through Next 5 YearsNext 5 Years

0

500

1000

1500

2000

2500

3000

3500

4000

Asia-Pacific Middle East Europe U.S.

Th

ou

sa

nd

Ba

rre

ls P

er

Da

y

Dist FCC HC Coker

Refinery Capacity Expansions 2007 through 2011

Note: Dist: Crude distillation; FCC: Fluid catalytic cracking; HC: Hydrocracking. Source: EIA, FACTS, company presentations, Oil and Gas Journal, Hydrocarbon Processing Boxscore.

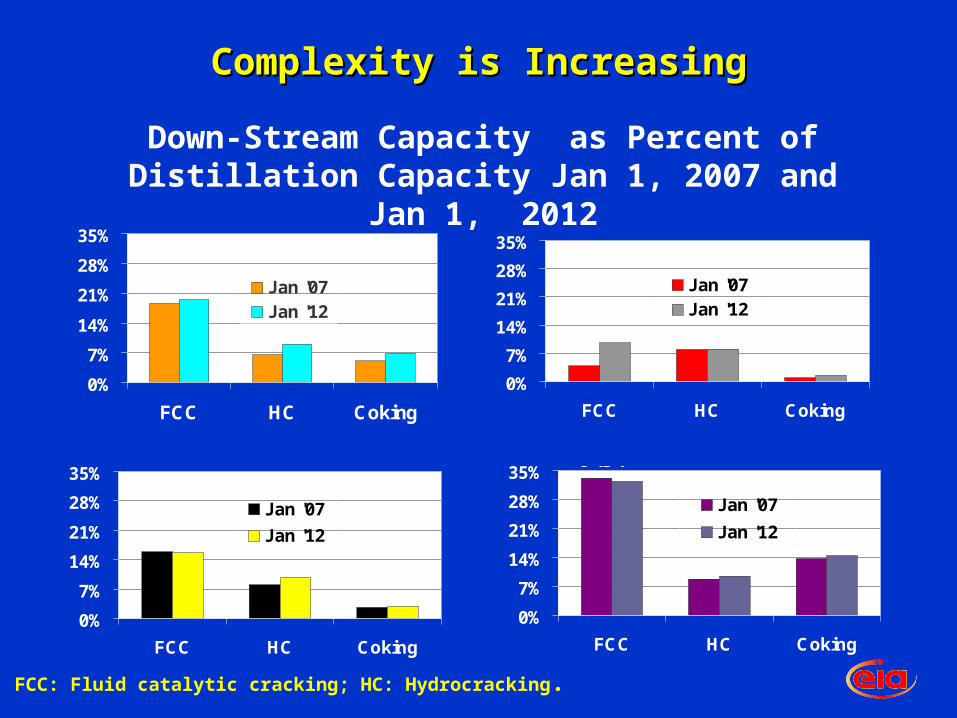

Complexity is IncreasingComplexity is Increasing

0%

7%

14%

21%

28%

35%

FCC HC Coking

Jan '07Jan '12

Asia Pacific

0%

7%

14%

21%

28%

35%

FCC HC Coking

Jan '07Jan '12

Middle East

0%

7%

14%

21%

28%

35%

FCC HC Coking

Jan '07

Jan '12

Europe

0%

7%

14%

21%

28%

35%

FCC HC Coking

Jan '07

Jan '12

U.S.

Down-Stream Capacity as Percent of Distillation Capacity Jan 1, 2007 and Jan 1, 2012

Note: FCC: Fluid catalytic cracking; HC: Hydrocracking.

Capacity and Consumption 5-Year ChangesCapacity and Consumption 5-Year Changes2007 through 20112007 through 2011

0

500

1000

1500

2000

2500

3000

3500

4000

U.S. Europe Middle East Asia Pacific

Distillation Capacity Demand

Th

ou

san

d B

arre

ls P

er D

ay

Sources: Capacity see previous slides; Demand: EIA, BP World Statistical World Review 2006, FACTS, IEA

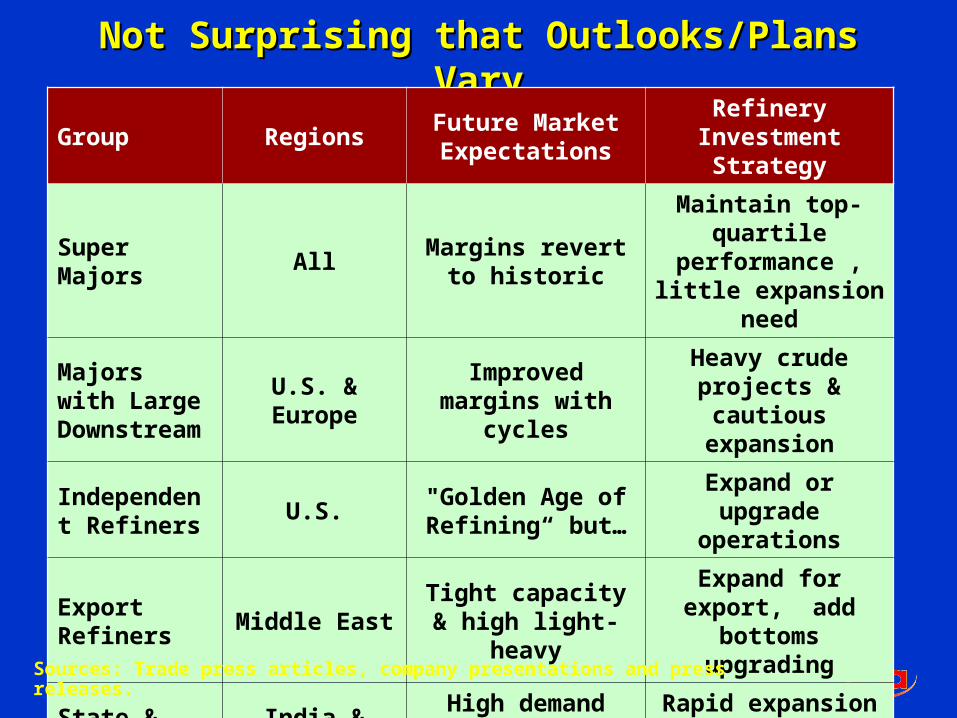

Not Surprising that Outlooks/Plans VaryNot Surprising that Outlooks/Plans Vary

Group RegionsFuture Market Expectations

Refinery Investment Strategy

Super Majors AllMargins revert to

historic

Maintain top-quartile

performance , little expansion need

Majors with Large Downstream

U.S. & EuropeImproved margins

with cycles

Heavy crude projects & cautious

expansion

Independent Refiners

U.S."Golden Age of Refining“ but…

Expand or upgrade operations

Export Refiners

Middle East Tight capacity & high light-heavy

Expand for export, add bottoms upgrading

State & Private

India & ChinaHigh demand growth, better

margins

Rapid expansion existing & grassroots

Sources: Trade press articles, company presentations and press releases.

Potential for Over or Under Expansion – And Potential for Over or Under Expansion – And Does it Matter?Does it Matter?

• Barring calamities: – In the next 2-3 years, capacity will likely remain tight – In next 5-10 years, not likely to see utilizations drop to levels

seen in early 1980’s from expansion

• Expansion that reduces utilization several percentage points not likely to have much impact on margins

• Regionally, the highest risk for oversupply that might impact Atlantic Basin margins is in Middle East; Atlantic Basin is not likely to over-expand

• Decrease in residual fuel supply from bottoms upgrading not likely to be enough to push residual fuel prices much closer to crude oil price and significantly reduce differentials. (Demand for residual fuel is declining.)

• Rising facility construction costs and biofuels use may reduce rate of facility expansion

Looking Ahead: Crude Price FactorLooking Ahead: Crude Price Factor

• Forecast: Fluctuate in band much higher than during the 1990’s (perhaps in the $60-$70 range?)

• Margin impact:– Lose the boost from being in a “rising” market– But still may support higher margins than in the 1990’s

• Light-Heavy differential impact:– Remain elevated– Demand for residual fuel is shrinking (e.g., bunker fuel

market)– Even with more conversion capacity destroying residual

fuel supply, residual price not likely to rise more towards crude oil

• Uncertainty: If crude oil prices fall, margins and differentials fall

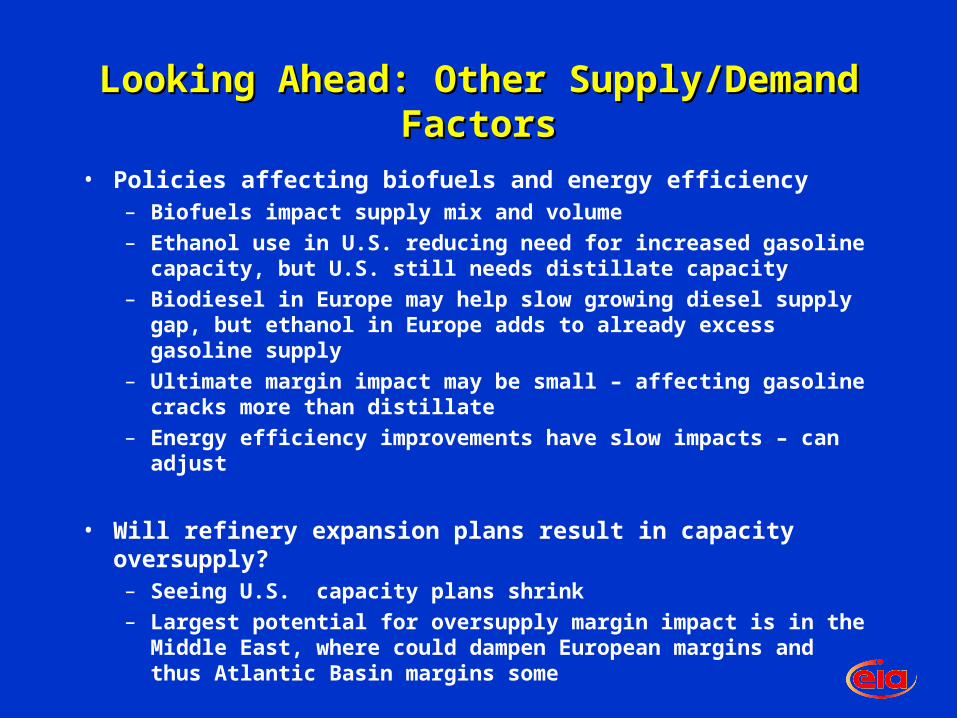

Looking Ahead: Other Supply/Demand Looking Ahead: Other Supply/Demand FactorsFactors

• Policies affecting biofuels and energy efficiency– Biofuels impact supply mix and volume

– Ethanol use in U.S. reducing need for increased gasoline capacity, but U.S. still needs distillate capacity

– Biodiesel in Europe may help slow growing diesel supply gap, but ethanol in Europe adds to already excess gasoline supply

– Ultimate margin impact may be small – affecting gasoline cracks more than distillate

– Energy efficiency improvements have slow impacts – can adjust

• Will refinery expansion plans result in capacity oversupply?– Seeing U.S. capacity plans shrink

– Largest potential for oversupply margin impact is in the Middle East, where could dampen European margins and thus Atlantic Basin margins some

Short Cycle or Golden Age?Short Cycle or Golden Age?