Download - M2 Telecommunications

38

Acquisition of Primus Telecom Holdings Pty Ltd NOT FOR DISTRIBUTION OR RELEASE IN THE UNITED STATES and Entitlement Offer M2 Investor Presentation, 16 April 2012, Slide 1 16 April 2012

Transcript of Download - M2 Telecommunications

Acquisition of Primus Telecom Holdings Pty Ltd NOT FOR DISTRIBUTION OR RELEASE IN THE UNITED STATES

and Entitlement Offer

M2 Investor Presentation, 16 April 2012, Slide 1

16 April 2012

Important Notice and DisclaimerThis disclaimer and important notice applies to this presentation and any information provided in relation to or in connection with the information contained in it or the Offer This disclaimer and important notice applies to this presentation and any information provided in relation to or in connection with the information contained in it or the Offer. The information in this presentation is not a prospectus. This presentation provides information in summary form as at the date of this presentation. Some of that information is based on publicly available sources, has not been independently verified and may not be complete. For further information relating to M2 Telecommunications Group Ltd (M2) see the periodic and continuous disclosure announcements lodged with ASX by M2 which are available on the ASX website.This presentation contains certain forward looking statements. Forward looking statements should or can generally be identified by the use of forward looking words such as “anticipate”, “believe”, “expect”, “forecast”, “estimate”, “will”, “could”, “may”, “target”, “plan” and other similar expressions within the meaning of securities laws of applicable jurisdictions, and include earnings guidance and statements of intention about future matters and the outcome and effects of the equity raising. Indications of, and guidance or outlook on, future earnings, distributions or financial position or performance are also forward looking statements. The forward looking statements contained in this presentation involve known and unknown risks and uncertainties and other factors, many of which are beyond the g g p , y ycontrol of M2, and may involve significant elements of subjective judgement and assumptions as to future events which may or may not be correct. M2 assumes no obligation to update or revise such information to reflect any change in expectations, beliefs, hopes, intentions or strategies. No representations, warranty or assurance (express or implied) is given that the occurrence of the events expressed or implied in any forward looking statements in this presentation will actually occur. Past performance information given in this presentation is given for illustrative purposes only and should not be relied upon and is not an indication of future performance. See the “Key risks” section of this presentation for a discussion of certain risks that may impact the outcome of matters discussed in forward looking statements. There can be no assurance that actual outcomes will not differ materially from these forward looking statements.To the maximum extent permitted by law, no person, including M2 and its affiliates, related bodies corporate, officers, employees and representatives (including agents, the underwriter and advisors), accepts any liability or responsibility for any expenses, losses, damages or costs incurred by an investor as a result of their participation in the Offer and the information in this presentation being y y y y g y ginaccurate or incomplete in any way for any reason, whether by negligence or otherwise. The underwriter and advisors have not authorised or caused the issue, lodgement, submission, dispatch or provision of this presentation and do not make or purport to make any statement in this presentation and there is no statement in this presentation which is based on any statement by the underwriter and advisors. The underwriter and advisors take no responsibility for any information in this presentation or any action taken by investors on the basis of such information. To the maximum extent permitted by law, the underwriter, the advisors and any of their respective affiliates, related bodies corporate, officers, employees and representatives (including agents) do not accept any liability or responsibility for any expenses, losses, damages or costs incurred by an investor as a result of their participation in the Offer and the information in this presentation being inaccurate or incomplete in any way for any reason, whether by negligence or otherwise, make no representation or warranty, express or implied, as to the currency, accuracy, completeness, reliability, fairness or correctness of the information contained in this presentation and take no responsibility for any part of this presentation. The underwriter and advisors make no recommendations as to whether investors or their related parties should participate in the Offer nor do they make any representations or warranties to investors concerning this Offer, or any such information and investors represent, warrant and agree that they have not relied on any statements made by any of the underwriter and advisors or any of their affiliates in relation to the issue of new shares or the Offer generally.The information contained in this presentation is not investment or financial product advice (nor tax, accounting or legal advice). This presentation has been prepared without taking into account the investment objectives, financial situation or particular needs of any person. Investors should obtain their own professional, legal, tax, business and/or financial advice before making any investment decision.This presentation does not constitute an offer to issue or sell, or to arrange to sell, securities or other financial products. In particular, this presentation and the information contained in it does not

tit t ff t ll th li it ti f ff t b iti i th U it d St t Thi t ti t b di t ib t d l d i th U it d St t Th titl t d th constitute an offer to sell, or the solicitation of an offer to buy, any securities in the United States. This presentation may not be distributed or released in the United States. The entitlements and the new shares offered in the Offer have not been and will not be registered under the U.S. Securities Act of 1933, as amended (the Securities Act) or the securities laws of any state or other jurisdiction of the United States and may not be offered or sold, directly or indirectly, in the United States absent registration or in a transaction exempt from, or not subject to, the registration requirements of the Securities Act and any other applicable securities laws.The release, publication or distribution of this presentation in jurisdictions outside Australia may be restricted by law. Any failure to comply with such restrictions may constitute a violation of applicable securities laws. This presentation may not be copied by you, or distributed to any other person.All amounts are presented in Australian dollars unless otherwise stated. The information in this presentation remains subject to change without notice. M2 in conjunction with the underwriter reserves the right to withdraw or vary the timetable for the proposed Offer without notice

M2 Investor Presentation, 16 April 2012, Slide 2

right to withdraw or vary the timetable for the proposed Offer without notice.Goldman Sachs Australia Pty Ltd and its affiliates are acting as exclusive financial adviser to M2 in relation to the Acquisition, sole underwriter of the A$83.1 million Entitlement Offer and sole mandated lead arranger, underwriter and bookrunner of the A$250.0 million acquisition bridge loan facility. In the course of its ordinary business, affiliate(s) of Goldman Sachs Australia Pty Ltd may execute currency or other hedging transactions with counterparties including in connection with the acquisition.

Presentation Content

Transaction Overview

Overview of Primus

The New M2 Group

Acquisition Terms and FundingAcquisition Terms and Funding

Appendix 1 – Key Riskspp y

Appendix 2 – Jurisdictions & Selling Restrictions

M2 Investor Presentation, 16 April 2012, Slide 3

Transaction Overview

M2 Telecommunications Group Ltd (“M2”) acquires Primus Telecom Holdings Pty Ltd (“Primus”) for $192.4m(1)

on a debt free basis and including $10.6m of restricted cash(2)

Primus is a leading full service telecommunications provider in Australia, with: Revenues of $280.2m in CY2011 EBITDA of $39.9m in CY2011$

Consolidates M2’s position as the leading challenger in the Small and Medium Business (“SMB”) market Incorporates the known and trusted brands of iPrimus and Primus into the M2 Group Contributes a proven managed / hosted services capability Approximately 500 highly skilled and passionate team members, including the experienced Management team Significant opportunity for cross-sale of complementary service offerings Expected to complete on 1 June 2012

Acquisition

Expected to complete on 1 June 2012

Combined Group pro forma CY2011 revenue of $677.4m Combined Group pro forma CY2011 EBITDA of $97.2m(3)

8.6% EPS accretive on an underlying basis in pro forma CY2011(3)(4) including $5m p.a. of expected synergiesMaterial Financial

Benefit 22.8% accretive to free cash flow per share(3)(4)(5)Benefit

Acquisition and refinance of existing debt funded through a combination of an underwritten traditional renounceable Entitlement Offer to raise $83.1m and a renegotiated senior debt facility of $182.5m(6)

Renounceable Entitlement Offer chosen to raise capital as it affords all shareholders an equal opportunity to participate while also offering rights trading in place of take up

Fundingparticipate, while also offering rights trading in place of take-up

The M2 Board aims to maintain its dividend policy of 70% of NPAT

(1) Excludes the transaction costs associated with the acquisition, new debt facility and the Entitlement Offer and is subject to a post completion adjustment based on Primus’ working capital balance at completion.(2) Cash on deposit to secure bank guarantees for property lease and supplier security requirements.(3) Includes pre-tax synergies of $5.1m anticipated to be derived on an annual basis over the FY13 year (refer to “Cost Synergies” slide for initiatives). The synergies do not include the cost of achieving these

synergies, estimated to be $0.5m in one-off expenses.(4) Free cash flow per share & EPS have been derived including the number of shares and rights issued

M2 Investor Presentation, 16 April 2012, Slide 4

(4) Free cash flow per share & EPS have been derived including the number of shares and rights issued. (5) Free cash flow defined as operating cash flow minus capex.(6) M2 has received in principle approval for the senior bank facility and expects to enter into the facility prior to completion of the acquisition. As an interim measure M2 has also entered into a $250.0m, 364-day,

senior secured acquisition bridge financing facility that is expected to remain undrawn pending completion of the Entitlement Offer and senior bank facility.

Strategic Rationale

Approximately 165,000 customers across retail, business and wholesale segmentsApproximately 500 team members in Melbourne head office and mainland capital cities Long-standing recognised and trusted brands Long-standing, recognised and trusted brandsSignificant synergy opportunitiesPotential savings as a result of enhanced buying leverage with suppliersStrengthens M2’s position in lead up to NBN through enhanced reach and scale

Scale

Portfolio of advanced, next generation products and servicesPlatform to develop cloud services and benefit from industry wide trends towards

hosted and managed service models

Capability

hosted and managed service models IP / Hosted Voice solution:

SIP Trunks Accela Hosted telephony offering

27,000 square feet of advanced data centre facilities in Melbourne and Sydney Ability to expand to over 46 000 square feet Ability to expand to over 46,000 square feet Product offerings include co-location, virtual / dedicated hosting and cloud-

based managed servicesMetro Fibre rings with ~100 route kilometres and ~10,800 fibre kilometres in five

major Australian cities High bandwidth solutions via a direct optical network

M2 Investor Presentation, 16 April 2012, Slide 5

High bandwidth solutions via a direct optical network

Complementary Strengths

M2 is the pre-eminent challenger in the SMB market

P i h t d ti l i d t tPrimus has strong credentials in consumer and corporate segments

Primus has a targeted market approach and a focus on service, consistent with M2 strategywith M2 strategy

The Primus next generation product capability provides the opportunity to utilise M2’s existing Inside Sales teams to sell hosted and managed service utilise M2 s existing Inside Sales teams to sell hosted and managed service offerings to the large M2 SMB customer base

Primus was the first provider to be certified for Business to Business (“B2B”) p ( )interoperability with NBN Co

M2 is prepared for the NBN world with market reach, scale and capability

M2 Investor Presentation, 16 April 2012, Slide 6

Presentation Content

Transaction Overview

Overview of Primus

The New M2 Group

Acquisition Terms and FundingAcquisition Terms and Funding

Appendix 1 – Key Riskspp y

Appendix 2 – Jurisdictions & Selling Restrictions

M2 Investor Presentation, 16 April 2012, Slide 7

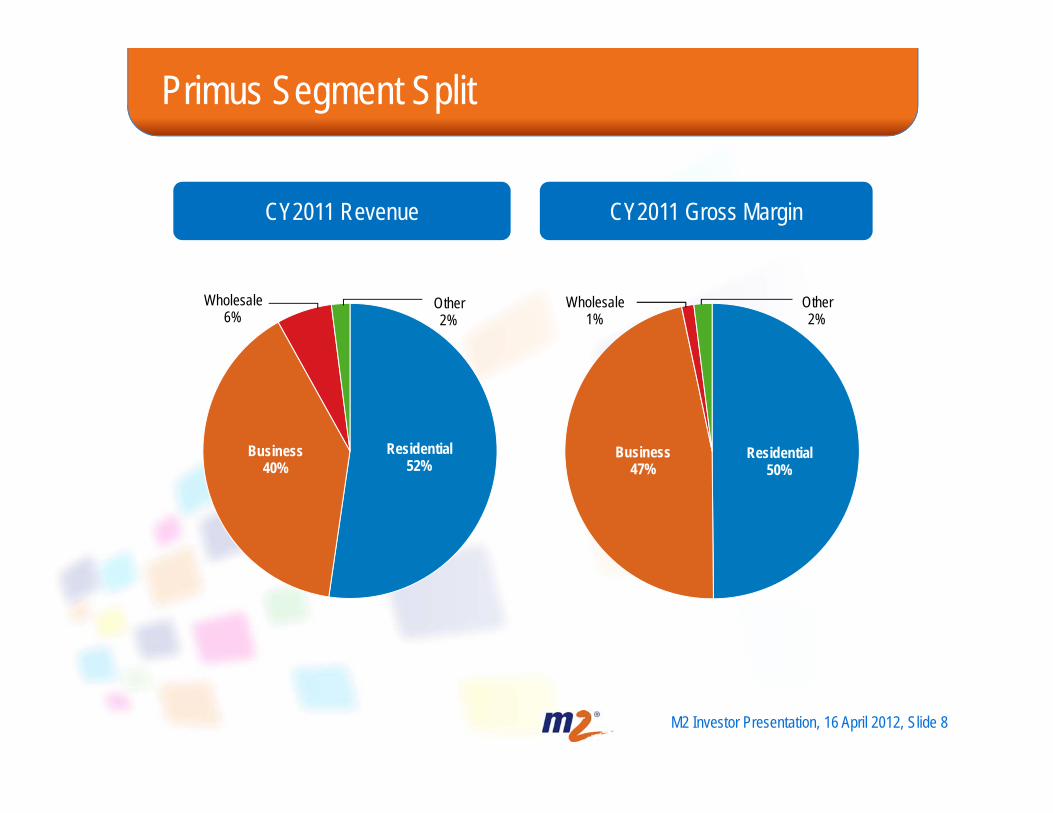

Primus Segment Split

CY2011 Revenue CY2011 Gross Margin

Wholesale6%

Other2%

Wholesale1%

Other2%

Business Residential Business Residential40% 52% 47%

es de t a50%

M2 Investor Presentation, 16 April 2012, Slide 8

Primus Network Overview

Metro Fibre rings in Perth, Brisbane, Adelaide, Melbourne and Sydney

Network Highlights Primus Australia National Footprint

27,000 square feet of data centre facilities across three sites

On-net services in all states and territories in Australia

National and international MPLS network serving all markets in Australia

Fault-tolerant Broadsoft-based VoIP switch

DSLAMS i 290+ h DSLAMS in 290+ exchanges

290+ exchanges offer ADSL2+ capabilities up to 20 Mbps

5 TDM switches

24 x 7 Network Management Centre

M2 Investor Presentation, 16 April 2012, Slide 9

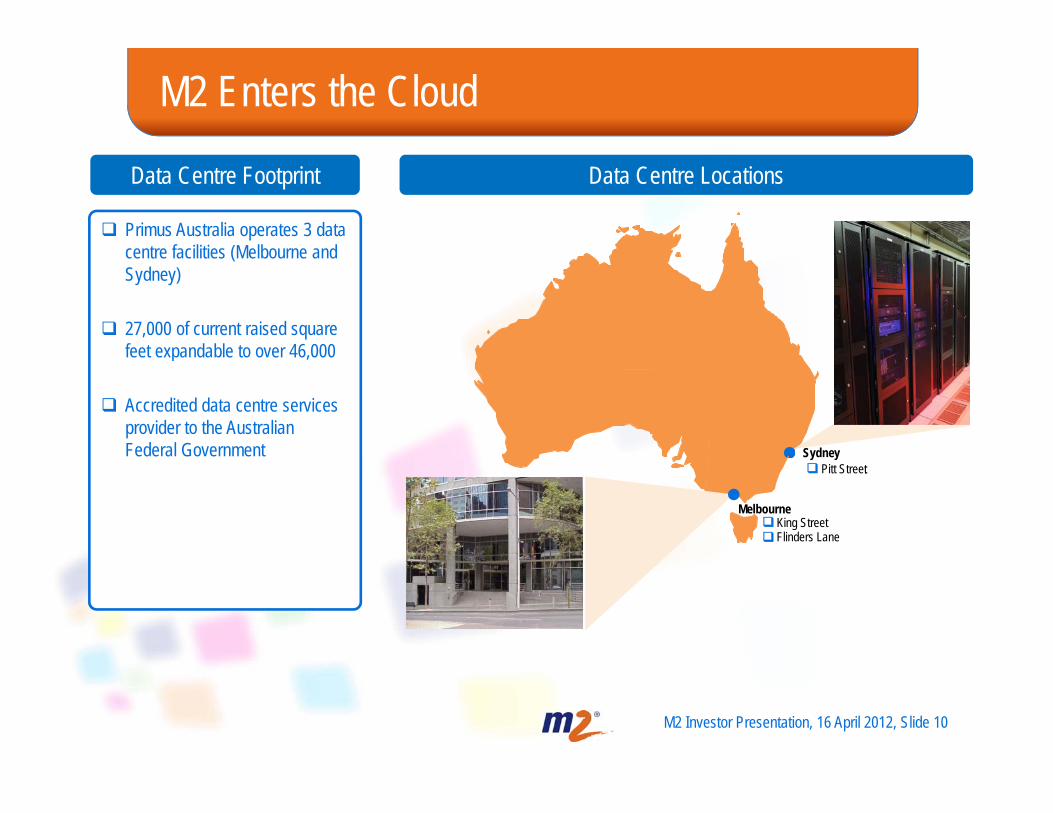

M2 Enters the Cloud

Primus Australia operates 3 data centre facilities (Melbourne and

Data Centre Footprint Data Centre Locations

centre facilities (Melbourne and Sydney)

27,000 of current raised square feet expandable to over 46,000feet expandable to over 46,000

Accredited data centre services provider to the Australian Federal Government Sydney

Melbourne

y y Pitt Street:

King Street Flinders Lane

M2 Investor Presentation, 16 April 2012, Slide 10

Fibre Rings in Five Major Australian Cities

Perth, WA~9.1 Route km

~1,200 Fibre km

Brisbane, QLD~10.6 Route km~1,530 Fibre km

Sydney, NSW35 1 R t k~35.1 Route km

~4,500 Fibre km

Adelaide, SA~17.8 Route km~1 280 Fibre km

Melbourne, VIC~23.1 Route km~2,300 Fibre km

1,280 Fibre km

Network includes ~100 route kilometres and ~10,800 fibre kilometres

A platform from which to meet the growing demand for high speed low latency connectivity

M2 Investor Presentation, 16 April 2012, Slide 11

A platform from which to meet the growing demand for high speed low latency connectivity

Presentation Content

Transaction Overview

Overview of Primus

The New M2 Group

Acquisition Terms and FundingAcquisition Terms and Funding

Appendix 1 – Key Riskspp y

Appendix 2 – Jurisdictions & Selling Restrictions

M2 Investor Presentation, 16 April 2012, Slide 12

The New M2

Residential SMB WholesaleCorporate

Comprehensive range of telecommunications services for businesses

Wholesale supply to telecommunications and internet service providers

Range of fixed line, data and mobile services

Full suite of managed services offerings delivered via next generation network

National Dealer Network, large Inside Sales Team and superior customer service

p

Portfolio of mobile, voice and data products in addition to a full range of advisory

Targeted marketing approach to leverage strength in on-net areas

gencompassing metro fibre rings and data centres

service a full range of advisory services

M2 Investor Presentation, 16 April 2012, Slide 13

Business Combination

M2 PrimusMarkets Access to SMB market through engaged

national dealer channelFull suite of offerings for the Corporate market

national dealer channelCustomers Large SMB customer base 165,000 customers across residential,

business and wholesale baseBrands Known and trusted brands in respective

tKnown and trusted brands in respective

tsegments segmentsCapability Approximately 70 people in Inside Sales Team,

increasing product penetration and customer retention

Suite of next generation service offerings to address needs of current and prospective customers

SMB customer knowledge and strength Medium to Corporate customer knowledge and strength

Team Approximately 450 team members across Australia headquartered in Melbourne

Approximately 500 team members across Australia headquartered in MelbourneAustralia, headquartered in Melbourne Australia, headquartered in Melbourne

Service Australian-based customer support ensuring high levels of customer satisfaction

Australian-based customer support ensuring high levels of customer satisfaction

M2 Investor Presentation, 16 April 2012, Slide 14

Future State Platform

User-Centric Portal Drive single-supplier & per month / per user pricing

Software Services CRM HR Accounting Payroll

Hosted Services eMail Storage Security

Software Essentials

Word Processing Spreadsheet Presentations

Backup

InfrastrCloud

Mobi

le, P

C et

c

Services g y

Managed Hosted Voice Internet VideoInstant & Unified

Messaging

p ructureP

Devic

es –

M

IP Essentials

VoiceFixed / Mob

Internet

Network Access & Delivery

Premises

M2 Investor Presentation, 16 April 2012, Slide 15

Network Access & Delivery

Cost Synergies

M2 has identified over $5.0m per annumin potential cost synergies to be achieved,

likely to be realised from the following:likely to be realised from the following:

Reduction in overall corporate costs

Potential consolidation of premises

Efficiencies derived from consolidation of IT infrastructure and applications

Consolidation of network backhaul links

Greater efficiency in bandwidth management

Potential savings through enhanced buying leverage

Other operational efficiencies

M2 Investor Presentation, 16 April 2012, Slide 16

Other operational efficiencies

Combined Group Segment Split

CY2011 Pro Forma Revenue CY2011 Pro Forma Gross Margin

Other2 %

Wholesale

Other2 %

Wholesale9%

Residential32%

Wholesale15%

Residential29%

9%

Business52%

Business60%

N t b h t dd d t di

M2 Investor Presentation, 16 April 2012, Slide 17

Note: numbers shown may not add due to rounding.

Combined Group Pro Forma Financials

$m M2 CY2011(1)(2)

Primus CY2011(3)(4) Adjustments(5)(6) Pro Forma

CY2011% Change

for M2

Revenue 397.2 280.2 677.4 70.6%

EBITDA 52.2 39.9 5.1 97.2 86.1%

EBIT 44.7 16.7 5.1 66.5 48.7%

NPAT 29 2 10 4 (1 3) 38 3 31 1%NPAT 29.2 10.4 (1.3) 38.3 31.1%

NPAT (underlying)(7) 33.6 11.1 (1.3) 43.4 29.3%

EPS (cents)(8) 22.2 n/a 24.5 10.2%

EPS (cents, underlying)(7)(8) 25.5 n/a 27.7 8.6%(1) The M2 CY11 results are derived from the audited results for the year ended 30 June 2011 and the half year reviewed results for the 6 months ended 31 December 2011 adjusted for the

gain on the Clear Telecoms deferred consideration of $3.6m.(2) M2 CY11 results include the acquisitions of the assets of Clear Telecoms and Edirect from the respective date of acquisition. (3) The Primus CY11 results have been extracted from the audited accounts for the year ended 31 December 2011 adjusted to exclude non-recurring one-off and related party items including

ro alties and management fees Additionall it incl des a notional ta charge ass ming a 30% ta rateroyalties and management fees. Additionally, it includes a notional tax charge assuming a 30% tax rate.(4) Australian Accounting Standards allow for 12 months from completion to finalise accounting and purchase price allocation. Fair value adjustments will be subject to purchase price allocation

after completion. No amortisation charge has been included for any customer contracts deemed under Australian Accounting Standards, to have been acquired through the acquisition of Primus.

(5) Includes pre-tax synergies of $5.1m anticipated to be derived on an annual basis over the FY13 year (refer to “Cost Synergies” slide for initiatives). The synergies do not include the cost of achieving these synergies, estimated to be $0.5m in one-off expenses.

(6) Restatement of the interest & tax expense to reflect the new $182.5m debt facility, initially drawn to $139.6m.(7) U d l i NPAT d EPS h i l d dd b k f h t f $5 1 ti ti t (t t l f bi d ) i t d ith i ti t t t ( i t th

M2 Investor Presentation, 16 April 2012, Slide 18

(7) Underlying NPAT and EPS each include an add back of a non-cash cost of $5.1m amortisation costs (total for combined group) associated with existing customer contracts (prior to the purchase price allocation).

(8) In accordance with AASB 133, EPS calculations have been derived including the number of shares and rights issued.

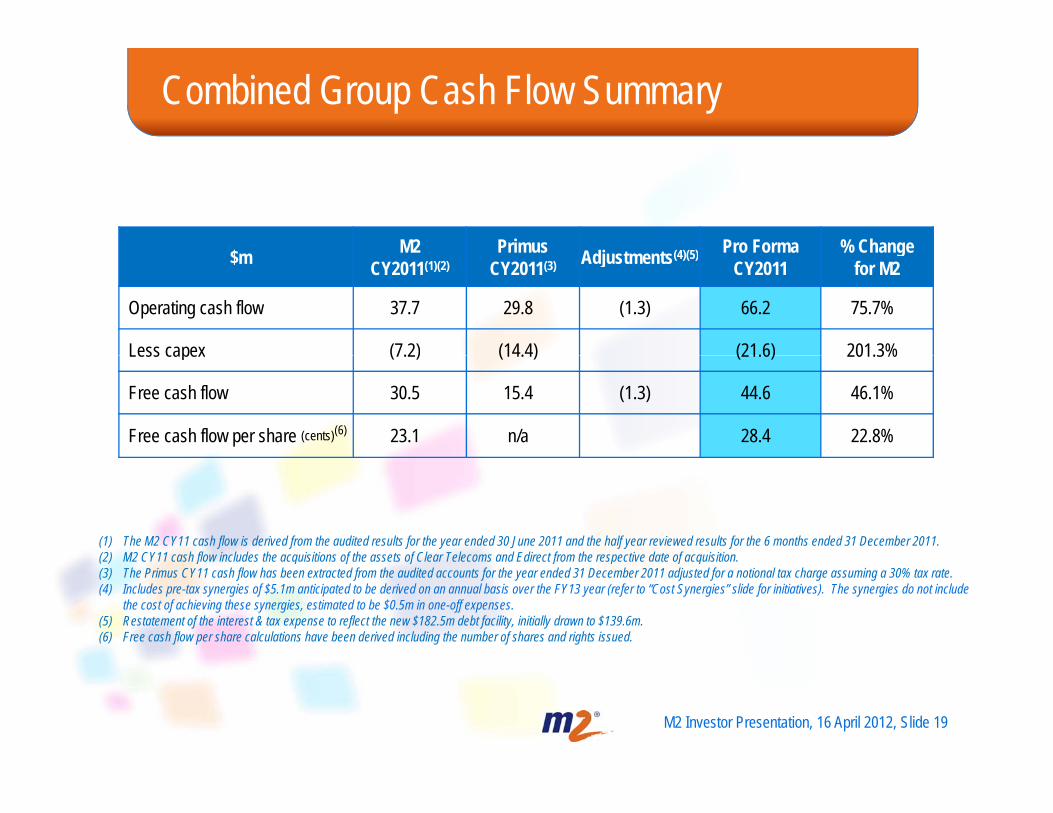

Combined Group Cash Flow Summary

$ M2 Primus Adj t t (4)(5) Pro Forma % Change$m CY2011(1)(2) CY2011(3) Adjustments(4)(5)CY2011

% gfor M2

Operating cash flow 37.7 29.8 (1.3) 66.2 75.7%

Less capex (7.2) (14.4) (21.6) 201.3%Less capex (7.2) (14.4) (21.6) 201.3%

Free cash flow 30.5 15.4 (1.3) 44.6 46.1%

Free cash flow per share (cents)(6) 23.1 n/a 28.4 22.8%

(1) The M2 CY11 cash flow is derived from the audited results for the year ended 30 June 2011 and the half year reviewed results for the 6 months ended 31 December 2011.(2) M2 CY11 cash flow includes the acquisitions of the assets of Clear Telecoms and Edirect from the respective date of acquisition.(2) M2 CY11 cash flow includes the acquisitions of the assets of Clear Telecoms and Edirect from the respective date of acquisition.(3) The Primus CY11 cash flow has been extracted from the audited accounts for the year ended 31 December 2011 adjusted for a notional tax charge assuming a 30% tax rate. (4) Includes pre-tax synergies of $5.1m anticipated to be derived on an annual basis over the FY13 year (refer to “Cost Synergies” slide for initiatives). The synergies do not include

the cost of achieving these synergies, estimated to be $0.5m in one-off expenses.(5) Restatement of the interest & tax expense to reflect the new $182.5m debt facility, initially drawn to $139.6m.(6) Free cash flow per share calculations have been derived including the number of shares and rights issued.

M2 Investor Presentation, 16 April 2012, Slide 19

Combined Group Pro Forma Balance Sheet

$m M2 at31-Dec-11(1)

PrimusPro Forma at31-Dec-11(2)

Acquisition Adjustments(4)(5)

Debt and Equity Adjustments(6)

Pro Forma31-Dec-11

Cash at bank(3) 16.7 10.6 (197.4) 189.4 19.3Other current assets 54 6 36 5 91 1Other current assets 54.6 36.5 91.1Non-current assets 127.1 119.2 79.8 326.2Total assets 198.4 166.4 (117.5) 189.4 436.6Current liabilities 80.4 37.2 20.0 137.6Non-current liabilities 16.7 16.6 88.7 122.0Total liabilities 97.1 53.8 108.7 259.6Net assets 101.4 112.6 (117.5) 80.6 177.0Equity 101.4 112.6 (117.5) 80.6 177.0Net tangible assets (14.3) 106.7 (197.4) 80.6 (24.3)Net debt(7) 9.7 11.2 197.4 (80.6) 137.7

Pro Forma 31-Dec-11 Net Debt / EBITDA = 1.42x(7)

Pro Forma 31-Dec-11 EBITDA to interest coverage = 9.1x(7)

(1) The M2 balance sheet as at 31 December 2011 has been extracted from the reviewed M2 financial statements for the 6 months ended 31 December 2011.(2) The Primus balance sheet as at 31 December 2011 has been extracted from the audited financial statements for the year ended 31 December 2011, adjusted to reflect those items not forming part of the acquisition

transaction including intercompany loans and free cash. (3) Includes $10.6m of restricted cash held by Primus. (4) Australian Accounting Standards allow for 12 months from completion to finalise accounting and purchase price allocation. Fair value adjustments will be subject to purchase price allocation after completion. (5) Represents the purchase price of $192.4m, plus expensed costs associated with the acquisition of Primus of $5.0m and is subject to a post completion adjustment based on Primus’ working capital balance at completion. Purchase price includes the acquisition of $10.6m of restricted cash held by Primus.

Pro Forma 31 Dec 11 EBITDA to interest coverage 9.1x Consistent with existing M2 Board policy, use of cash surplus will be considered for accelerated debt reduction

M2 Investor Presentation, 16 April 2012, Slide 20

j p p j g p p p q y(6) Represents total net funds raised of $218.6m (comprising $138.0m of debt and $80.6m of equity), supplemented by $8.0m of M2 excess cash, of which $29.3m will be used to refinance existing debt, $192.4m to fund the

acquisition and $5.0m to fund cash transaction costs. (7) Calculated inclusive of finance leases, exclusive of restricted cash. Debt is based on a commitment letter and term sheet provided by Bankwest and Westpac, subject to a number of conditions, with a proposed facility limit of $182.5m, including cash advance facilities of $172.5m and an overdraft facility of $10.0m. Proposed debt facilities have a term of 3 years, with year one amortisation on cash advance facilities totalling $20.0m.

Trading Update (Excluding Transaction)

M2 has maintained focus on delivering underlying business objectives:

Continued focus on organic growth:g g

2H12 channel focus: drive breadth and depth of Commander channel

Move from trial to full deployment of appointment setting function, with a dedicated p y pp g ,centre operational from April 2012

Finalise recruitment of additional Inside Sales resources

Take extended wholesale data product offering to new markets

Continue to actively assess complementary, “bolt-on” and transformational acquisition opportunitiesopportunities

Launch Phase 1 Ninja

Targeted re-launch of Commander brand to reinforce challenger identity and improve

M2 Investor Presentation, 16 April 2012, Slide 21

g g y pawareness

FY12 Guidance Reaffirmed

$m FY11(a) FY12 Guidance(1) % Change (from midpoint)

Total Revenue 426.8(2) 380 – 420 Down 6%Customer Revenues 375.0 380 - 420 Up 7%

EBITDA 48.3 58 – 62 Up 24%EBITDA Margin (EBITDA / Total Revenue) 11.3 % 15.0% Up 33%NPAT 27.6 30 – 34 Up 16%NPAT (underlying)(3) 31.3 34 – 38 Up 15%NPAT (underlying, excluding transaction costs)(3)(4) 31.3 38 – 42 Up 28%EPS (cents)(5) 21.5 24 – 28 Up 21%

One month of Primus contribution following completion on 1 June 2012 The M2 Board aims to maintain its dividend policy of 70% of NPAT post acquisition

EPS (cents, underlying)(3)(5) 24.1 27 – 31 Up 20%EPS (cents, underlying excluding transaction costs)(3)(4)(5) 24.1 31 – 35 Up 37%

The M2 Board aims to maintain its dividend policy of 70% of NPAT post acquisition(1) Australian Accounting Standards allow for 12 months from completion to finalise accounting and purchase price allocation. Fair value adjustments will be subject to purchase price allocation after completion.(2) Total Revenue in FY11 included approximately $55.0m in very low margin revenues, relating to the Edirect business prior to its acquisition by M2 in March 2011. Following M2’s acquisition of Edirect,

these revenues ceased and therefore are not in the FY12 guidance. The resulting effect of this revenue elimination is a marked increase in FY12 profit margins compared to FY11.(3) Underlying NPAT and EPS guidance each include an add back of a non-cash cost of $3.7m amortisation costs associated with customer contracts acquired in the relevant period (in accordance with

Australian Accounting Standards). No amortisation charge has been included for any customer contracts deemed under Australian Accounting Standards to have been acquired through the acquisition of Primus.

M2 Investor Presentation, 16 April 2012, Slide 22

(4) NPAT excluding transaction costs includes an add-back of $5.0m for expensed costs associated with the acquisition of Primus (excludes capitalised costs associated with the establishment of the new debt facility and the Entitlement Offer).

(5) In accordance with AASB 133, EPS calculations have been derived including the number of shares and rights issued. Whilst the guidance range has not changed, the “% Change” has increased due to the restatement of FY11(a) EPS for the entitlement offer fraction.

Presentation Content

Transaction Overview

Overview of Primus

The New M2 Group

Acquisition Terms and FundingAcquisition Terms and Funding

Appendix 1 – Key Riskspp y

Appendix 2 – Jurisdictions & Selling Restrictions

M2 Investor Presentation, 16 April 2012, Slide 23

Acquisition Terms and Funding

Purchase price of $192.4m(1) on a debt free basis including $10.6m of restricted cash(2)

The acquisition is expected to complete on 1 June 2012 following satisfaction of conditions precedent Funded through a combination of new equity and senior debt Funded through a combination of new equity and senior debt

One for four renounceable Entitlement Offer with rights trading to raise approximately $83.1m, fully underwritten by Goldman Sachs

New $182.5m senior facility to be provided by Westpac and Bankwest As an interim measure M2 has also entered into a $250 0m 364-day senior secured acquisition bridge financing facility that As an interim measure M2 has also entered into a $250.0m, 364-day, senior secured acquisition bridge financing facility that

is expected to remain undrawn pending completion of the Entitlement Offer and senior bank facility

Sources and uses of funds – projected at time of acquisitionSources $m Uses $mExcess cash used to fund acquisition 8.0 Acquisition of Primus 192.4

Entitlement offer 83.1 Costs associated with the acquisition(3) 9.0

Debt 139.6 Refinance of existing debt 29.3

Total 230.7 Total 230.7

(1) Excludes the transaction costs associated with the acquisition, new debt facility and the Entitlement Offer and is subject to a post completion adjustment based on Primus’ working capital balance at completion

M2 Investor Presentation, 16 April 2012, Slide 24

working capital balance at completion.(2) Cash on deposit to secure bank guarantees for property lease and supplier security requirements.(3) Includes the transaction costs associated with the acquisition, new debt facility and the Entitlement Offer.

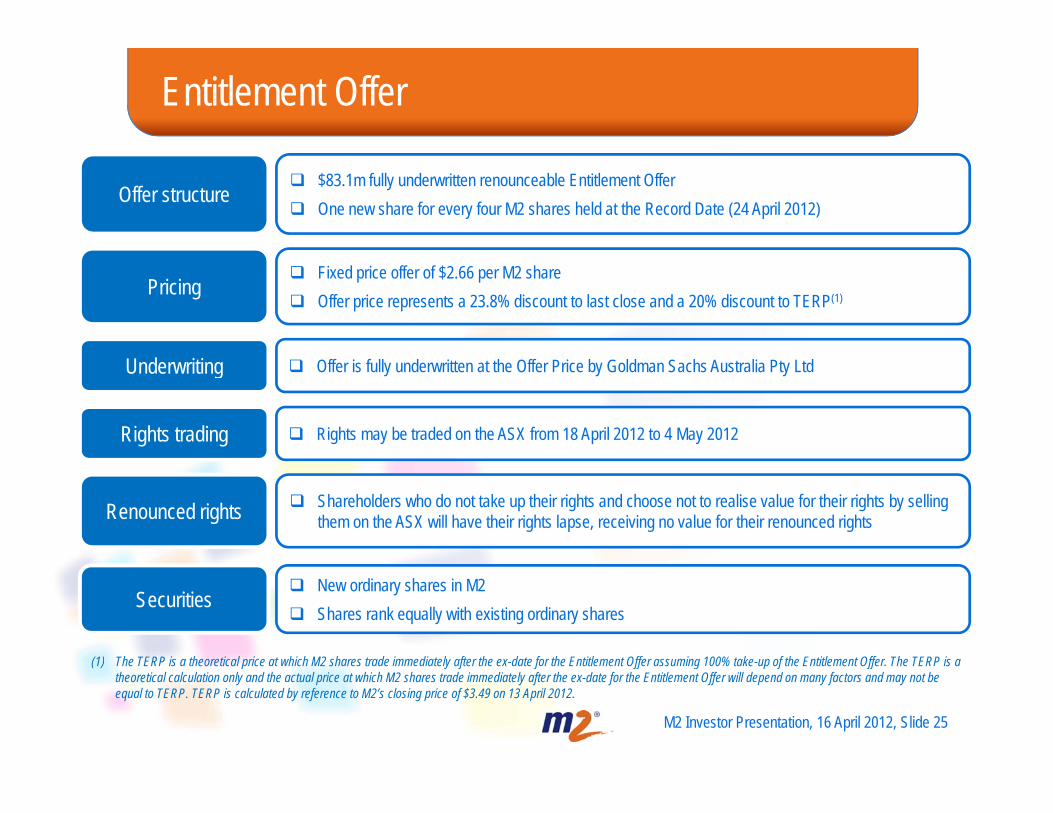

Entitlement Offer

$83.1m fully underwritten renounceable Entitlement Offer One new share for every four M2 shares held at the Record Date (24 April 2012)

Offer structure

Fixed price offer of $2.66 per M2 share Offer price represents a 23.8% discount to last close and a 20% discount to TERP(1)Pricing

Offer is fully underwritten at the Offer Price by Goldman Sachs Australia Pty LtdUnderwriting

Rights may be traded on the ASX from 18 April 2012 to 4 May 2012Rights trading

Shareholders who do not take up their rights and choose not to realise value for their rights by selling them on the ASX will have their rights lapse, receiving no value for their renounced rightsRenounced rights

(1) The TERP is a theoretical price at which M2 shares trade immediately after the ex-date for the Entitlement Offer assuming 100% take-up of the Entitlement Offer The TERP is a

New ordinary shares in M2 Shares rank equally with existing ordinary shares

Securities

M2 Investor Presentation, 16 April 2012, Slide 25

(1) The TERP is a theoretical price at which M2 shares trade immediately after the ex-date for the Entitlement Offer assuming 100% take-up of the Entitlement Offer. The TERP is a theoretical calculation only and the actual price at which M2 shares trade immediately after the ex-date for the Entitlement Offer will depend on many factors and may not be equal to TERP. TERP is calculated by reference to M2’s closing price of $3.49 on 13 April 2012.

Entitlement Offer Timetable

Key Event Date

Launch Entitlement Offer 16 April 2012

Rights trading commences 18 April 2012

Record date (for entitlements under the offer) 7pm, 24 April 2012

Dispatch of Offer Booklet 27 April 2012

Rights trading ends 4pm, 4 May 2012

Offer closes 5pm, 11 May 2012

Settlement of new shares issued under the Entitlement Offer 21 May 2012

New shares commence trading on ASX 22 May 2012

Note: The above timetable is indicative only and subject to change. M2 in conjunction with the underwriter reserves the right to amend any or all of these events, dates and times subject to the Corporations Act 2001 (Cth), the Australian Securities Exchange (ASX) Listing Rules and other applicable laws. In particular, M2 in conjunction with the underwriter reserves the right to extend the closing date of the Entitlement Offer to accept late applications either generally or in particular cases

M2 Investor Presentation, 16 April 2012, Slide 26

conjunction with the underwriter reserves the right to extend the closing date of the Entitlement Offer, to accept late applications either generally or in particular cases or to withdraw the Entitlement Offer without prior notice. The commencement of quotations of new shares is subject to confirmation from ASX. All references in this investor presentation are to Melbourne Time.

Presentation Content

Transaction Overview

Overview of Primus

The New M2 Group

Acquisition Terms and FundingAcquisition Terms and Funding

Appendix 1 – Key Riskspp y

Appendix 2 – Jurisdictions & Selling Restrictions

M2 Investor Presentation, 16 April 2012, Slide 27

Key Risks

This section discusses the key risks attaching to an investment in shares in M2, which may affect the future operating and financial performance of M2 and the value of M2 shares (before and after the proposed acquisition of Primus). Before investing or increasing your investment in M2 shares you should consider whether this investment is suitable for you having regard to publicly available information (including this shares, you should consider whether this investment is suitable for you having regard to publicly available information (including this Presentation), your personal circumstances and following consultation with financial or other professional advisers. The risks in this section are not, and are not to be considered or relied on as, an exhaustive list of the risks relevant to an investment in shares in M2. Additional risks and uncertainties that M2 is unaware of, or that it currently considers to be immaterial, may also become important factors that adversely affect M2's operating and financial performance.

K i kKey risks

CompetitionM2 operates in a competitive telecommunications market. In particular, M2 will compete against larger telecommunications companies which have considerable scale and market power. The size and financial strength of some of M2’s competitors can make it difficult for M2 to compete effectively in the telecommunications market M2's financial performance or operating margins could be adversely affected if the actions of effectively in the telecommunications market. M2 s financial performance or operating margins could be adversely affected if the actions of competitors or potential competitors become more effective, or if new competitors enter the market and M2 is unable to counter these actions.

NBNThe Australian Federal Government is rolling out a National Broadband Network (“NBN”) which is planned to cover approximately 93% of premises across Australia over the next decade. All telecommunication retail service providers will have equivalent access to acquiring wholesale services on the NBN which is intended to create a more level competitive playing field in the industry This new competitive environment with the services on the NBN, which is intended to create a more level competitive playing field in the industry. This new competitive environment with the NBN may enable the entrance of new competitors in the market which could have an adverse impact on the future financial performance of M2 if it is unable to effectively compete against the new competitors. Further, some of the assets that M2 will acquire through the acquisition of Primus are only relevant for providing telecommunication services over Telstra’s existing copper access network and so the value of those assets may be adversely affected by the rollout of the NBN and the resulting industry wide migration from the copper access network to the NBN.

M2 Investor Presentation, 16 April 2012, Slide 28

Key Risks (continued)

Integration riskM2’s acquisition of Primus will be the largest business acquired by M2 in its history by a significant margin. As a result, there is a risk that the integration of Primus may be more complex than currently anticipated, encounter unexpected challenges or issues and take longer than expected, divert management attention or not deliver the expected benefits and this may affect M2’s operating and financial performance. Additionally the acquisition of Primus will bring ownership of a range of network infrastructure assets which may potentially increase ongoing Additionally, the acquisition of Primus will bring ownership of a range of network infrastructure assets, which may potentially increase ongoing capital expenditure requirements and may require M2 to operate new types of businesses that it has not previously had experience operating. Further, the integration of the Primus accounting processes and systems may lead to revisions, which may impact on the Combined Group’s reported financial results. Other general integration risks include loss of knowledge through M2 being unable to retain key management personnel who may be targeted for recruitment by competitors following completion of the transaction; possible loss of customer contracts due to normal competitive market pressure; lack of a well formed disaster recovery plan in the Primus business and the need to relocate the Primus network operations centre in Sydneyoperations centre in Sydney.

Relationship with suppliersM2’s ability to provide its telecommunication services and products is highly dependent on securing wholesale services from its carrier suppliers, which are principally Telstra and Singtel Optus. The business of M2 could be materially impacted if any of the wholesale providers were unable to provide services as contracted or made a decision to supply services on unfavourable terms (except for services that are deemed “declared ser ices” b the ACCC and hich ha e reg lated pricing) If M2’s carrier s ppliers failed to s ppl the ser ices or changed terms to be less services” by the ACCC and which have regulated pricing). If M2’s carrier suppliers failed to supply the services, or changed terms to be less favourable than those currently offered to M2 or Primus, this change might materially impact upon the financial performance of the Combined Group.

Ability to service debtM2's ability to service its existing and new debt, and refinance expiring debt on acceptable terms, will depend on its future performance and cash fl hi h i ill b ff d b i f f hi h id f M2' l ( h h i i d l flows, which in turn will be affected by various factors, some of which are outside of M2's control (such as changes in interest and general economic and credit market conditions). Any inability to secure sufficient debt funding (including to refinance on acceptable terms) from time to time or to service its existing and new debt may have a material adverse effect on M2's financial performance and prospects. In particular, if M2 is unable to enter into binding facility documentation with its senior lenders for the proposed $182.5 million facility and drawdown under that facility on or prior to completion of its acquisition of Primus, it will be required to refinance the proposed bridge loan within 12 months of the date of this presentation. Further, the level of interest and fees payable on the proposed bridge loan will progressively and materially step up if M2 is

M2 Investor Presentation, 16 April 2012, Slide 29

unable to refinance the proposed bridge loan within 3 months, 6 months and 9 months, respectively, which would have an adverse impact on the profitability of M2.

Key Risks (continued)

Operational Risks

Sustainability of growthThe continued strong growth in sales and profitability of M2 is dependent upon a number of factors, including M2's ability to win new customers on a profitable basis and to retain and grow revenues from existing customers. This organic growth is conditional upon the continued improvements in performance of M2’s various sales channels, the ongoing achievement of sales objectives by M2’s existing sales teams and the provision of a consistent high quality customer service experience. If any of these growth factors were negatively impacted and growth was impaired then the financial performance and reputation of the business would be negatively impacted.

Operating costsM2's ability to operate profitably is dependent on a combination of the scalability of its operations and the costs of its operating structure. M2's y p p y p y p p gability to maintain a relatively low cost operating structure is not guaranteed and there is no assurance that these low operating costs can be maintained. Whilst M2 has consistently delivered improvements in operating margins through a combination of improved buying from carriers and reducing operating expenses by implementing business efficiency initiatives, there is no guarantee that these improvements can be maintained. Notwithstanding that the Combined Group expects to be able to realise synergy benefits from the purchase of Primus, a failure to effectively manage operating costs would have a negative impact on the financial performance of the Combined Group.

Technology changesThe telecommunications industry is constantly evolving with new technologies and products which could act as substitutes for the products or services offered by M2. There is no guarantee that M2 can effectively keep up with changes in technological developments and failure to keep pace with changes in technology could result in the Combined Group’s business finding it increasingly difficult to compete in its chosen target segments.

Information technologyThe telecommunications industry is heavily dependent upon technology for the delivery of the various services made available to customers and M2 has invested significantly in the development of management information and other information technology systems designed to maximise the efficiency of M2's operations. Should these systems not be adequately maintained, secured or updated, or M2's disaster recovery processes not be adequate, system failures may negatively impact on M2's performance. Whilst the risk is considered a low probability, the consequences co ld be e treme ith a s stained fail re of M2’s billing processes for e ample possibl res lting in a fail re of the b siness

M2 Investor Presentation, 16 April 2012, Slide 30

could be extreme, with a sustained failure of M2’s billing processes, for example, possibly resulting in a failure of the business.

Key Risks (continued)

InfrastructureM2 has traditionally adopted an “infrastructure light” model in operating its business, relying on its carrier suppliers to provide the vast majority of the infrastructure that is required to provide services to its end user customers. The acquisition of Primus includes a number of infrastructure elements that M2 has not traditionally managed including voice switching infrastructure DSLAM’s Data Centres and Fibre Rings The risks elements that M2 has not traditionally managed including voice switching infrastructure, DSLAM’s, Data Centres and Fibre Rings. The risks associated with these assets include:That the capital expenditure requirements have been underestimated and that future capital expenditure may affect free cash flow;That the infrastructure is seen as directly competitive to M2’s key carrier supply partners and impacts on our ability to access new products from those suppliers, or to continue to negotiate favourable commercial arrangements with them; andThat the infrastructure becomes redundant as the NBN is deployed and that M2 fails to achieve an economic return on that infrastructure i t tinvestment.All these risks could have detrimental impact on the financial performance of the Combined Group.

Security or privacy of dataThe protection of customer, employee, third party and company data is critical to M2's operations. M2 has access to a significant amount of customer, employee and third party information, including through its database of customers. The legal and regulatory environment surrounding information security and privacy is increasingly complex and demanding. Customers, employees and third parties such as suppliers also have high expectations that M2 will adequately protect their personal information. A breach of customer, employee, third party or company data could attract significant media attention, damage M2's customer or supplier relationships and reputation and ultimately result in lost sales, penalties or litigation. This could have a material adverse effect on M2's future financial performance and financial position.

Regulatory riskg yThe M2 business operates in an increasingly regulated industry with strong penalties existing for non compliance with regulations including fines and undertakings that may include customer redress and restrictions on future marketing of services. M2’s future growth prospects are heavily reliant on its ability to market its services through its various sales channels, so any regulatory change, event or enforcement action which would restrict those activities would have a material adverse impact on M2’s growth and in turn, its future financial performance.

M2 Investor Presentation, 16 April 2012, Slide 31

Key Risks (continued)

Acquisition risks

Completion riskThere are a number of conditions in the equity purchase agreement to acquire Primus which must be satisfied prior to the completion of the transaction. These conditions include a requirement that there is no order by a government authority or action restraining, enjoining or otherwise prohibiting the completion of the acquisition. Should any of the conditions precedent fail to be satisfied within the time limits prescribed in the equity purchase agreement, M2 may not be able to complete its acquisition of Primus but M2 may nevertheless have already completed the Entitlement Offer. As such, there is a risk that M2 will be overcapitalised in those circumstances.

Reliance on information providedM2 undertook a due diligence process in respect of Primus, which relied in part on the review of financial and other information provided by the g p p , p p yvendor of Primus. Despite making reasonable efforts, including seeking external legal and accounting advice where appropriate, M2 has not been able to verify the accuracy, reliability or completeness of all the information which was provided to it against independent data. Similarly, M2 has prepared (and made assumptions in the preparation of) the financial information relating to Primus on a stand‐alone basis and also the Combined Group’s pro forma financial information included in this Presentation in reliance on limited financial information and other information provided by the vendor of Primus. M2 is unable to verify the accuracy or completeness of all of that information. If any of the data or information provided to and relied upon by M2 in its due diligence process and its preparation of this Presentation proves to be incomplete incorrect inaccurate or and relied upon by M2 in its due diligence process and its preparation of this Presentation proves to be incomplete, incorrect, inaccurate or misleading, there is a risk that the actual financial position and performance of Primus and the Combined Group may be materially different to the financial position and performance expected by M2 and reflected in this Presentation. Notwithstanding that M2 has sought comprehensive and wide ranging warranties and indemnities from the vendor of Primus, investors should note that there is no assurance that the due diligence conducted will have identified all material issues and risks in respect of the acquisition and that warranties and indemnities will adequately compensate for any losses arising from those material issues. Therefore, there is a risk that unforeseen issues and risks may arise, which may also have a material impact on M2 also have a material impact on M2.

Historical liabilityIf the acquisition of Primus completes, M2 may become directly or indirectly liable for any liabilities that Primus has incurred in the past, which were not identified during its due diligence or which are greater than expected, and for which the market standard protection (in the form of insurance, representations and warranties and indemnities) negotiated by M2 prior to its agreement to acquire Primus turns out to be inadequate in the circ mstances S ch liabilit ma ad ersel affect the financial performance or position of M2 post acq isition

M2 Investor Presentation, 16 April 2012, Slide 32

in the circumstances. Such liability may adversely affect the financial performance or position of M2 post‐acquisition.

Key Risks (continued)

Acquisition accountingIn accounting for the acquisition in the pro forma combined balance sheet contained in this Presentation, M2 has presented the historical carrying values of the acquired assets and liabilities of Primus as at 31 December 2011 and reflected the excess of the purchase price over the net assets as goodwill In accordance with Australian Accounting Standards M2 will undertake a formal fair value assessment of all of the assets liabilities as goodwill. In accordance with Australian Accounting Standards, M2 will undertake a formal fair value assessment of all of the assets, liabilities and contingent liabilities of Primus post‐acquisition, which may give rise to a different fair value allocation to that used for purposes of the pro forma financial information set out in this Presentation. Such a scenario will result in a reallocation of the fair value of assets and liabilities acquired to or from goodwill and also an increase or decrease in depreciation and amortisation charges in the Combined Group’s income statement (and a respective increase or decrease in net profit after tax).

Th t l lt f th C bi d G ill b diff t t th di l d d tl t d f ti h ld b The actual results of the Combined Group will be different to those disclosed and consequently a greater degree of caution should be exercised when assessing this informationThe pro forma Combined Group financial information set out in this Presentation illustrates the indicative financial performance of the Combined Group for the year ended 31 December 2011 and financial position of the Combined Group as at 31 December 2011, assuming the acquisition of Primus had occurred on 1 January 2011 and inclusive of the Entitlement Offer and anticipated debt financing. A number of assumptions have been made to prepare the pro forma Combined Group information, a number of which have been derived based on information provided to M2 by Primus, for which M2 is unable to verify the accuracy or completeness of, and there is no assurance that all material issues and risks in relation to the acquisition of Primus have been identified. To the extent that this information (or any of the other assumptions upon which the pro forma financial information is based) is incomplete, incorrect, inaccurate or misleading, there is a risk that the profitability and future results of the operations of the Combined Group may differ (including in a materially adverse way) from M2’s expectation as reflected in this Presentation and additional liabilities may emerge.The FY12 guidance (including EPS guidance) shown in this Presentation does not take into account items that will be required to be accounted g ( g g ) qfor as part of M2’s acquisition accounting in FY12 including: (i) fair value accounting adjustments that may arise from the acquisition of Primus and any associated impact on depreciation and amortisation charges; (ii) any potential acquisition benefits, synergies and associated implementation costs; or (iii) alignment of accounting policies. Hence, this information is provided for illustrative purposes only and is not represented as being indicative of M2’s view on future financial performance.

M2 Investor Presentation, 16 April 2012, Slide 33

Key Risks (continued)General risksGeneral risks

Credit riskM2 has customers which pay in arrears which means that M2 bears the risk of those customers defaulting on their payment obligations. This results in a loss of revenue for M2 to the extent that if those debts are irrecoverable and also creates additional expenses for M2 in seeking to enforce these obligations.

Reliance on key personnelM2's growth and profitability may be limited by the loss of key senior management personnel, the inability to attract new suitably qualified personnel or by increased compensation costs associated with attracting and retaining key personnel.

Risks associated with renouncing entitlements under the Entitlement OffergPrices obtainable for entitlements under the Entitlement Offer may rise and fall over the entitlement trading period. If you sell your entitlements at one stage in the entitlement trading period, you may receive a higher or lower price than a shareholder who sells their entitlements at a different stage in the entitlement trading period. There is no guarantee that there will be a viable market on ASX for your entitlements during, or on any particular day in, the entitlements trading period. You should also note that if you sell, or do not take up, all or part of your entitlement, then your percentage shareholding in M2 will be diluted by not participating to the fullest extent possible in the Entitlement Offer and you will not be exposed to future increases or decreases in y p p g p y pM2's share price in respect of the New Shares which would have been issued to you had you taken up all of your entitlement.

Taxation implications of the offerThe tax consequences from selling entitlements or from doing nothing may be different. Before selling entitlements or choosing to do nothing in respect of entitlements, you should seek independent tax advice and may wish to refer to the tax disclosures contained in section 3.7 of the offer booklet which will provide further information on potential taxation implications for certain Australian resident shareholdersbooklet which will provide further information on potential taxation implications for certain Australian resident shareholders.

DividendsThe payment of dividends on M2's shares is dependent on a range of factors including the profitability of its group, the availability of cash, capital requirements of the business and obligations under debt instruments. Any future dividend levels will be determined by the M2 Board having regard to its operating results and financial position at the relevant time. That said, there is no guarantee that any dividend will be paid by M2 or, if paid that they will be paid at previous levels

M2 Investor Presentation, 16 April 2012, Slide 34

paid, that they will be paid at previous levels.

Glossary

Defined Term DefinitionBusiness to Business (“B2B”) interoperability

Business to Business (B2B) interoperability – A machine interface between two organisations for the purpose of performing functions such as direct systems integration, supporting automated order management, assurance and billing operation

Combined Group M2 Telecommunications Group Ltd and its subsidiaries together with Primus Telecom Holdings Pty Ltd and its subsidiariesCombined Group M2 Telecommunications Group Ltd and its subsidiaries together with Primus Telecom Holdings Pty Ltd and its subsidiaries

DSLAMs Digital Subscriber Line Access Multiplexer used for provision of ADSL (Asymmetric Digital Subscriber Line) services

Data Centre Purpose built facility for housing computing and network infrastructure

Fibre Rings Optical Fibre laid in the streets often forming a ring type topology for the purpose of connecting customers and equipment to a network

Inside Sales A team within M2 dedicated to selling new products to existing customers

IP Internet ProtocolIP Internet Protocol

NBN National Broadband Network

Ninja Internal project name for M2’s next generation billing and customer care platform

Restricted Cash Cash that is set aside for a specific purpose and not available for general and immediate use by an organisation

SIP Trunks Session Initiation Protocol - IP equivalent services to that of ISDN (Integrated Services Digital Network)

M2 Investor Presentation, 16 April 2012, Slide 35

Transaction Overview

Overview of PrimusOverview of Primus

The New M2 Group

Acquisition Terms and Funding

The New M2 Group

Acquisition Terms and FundingAcquisition Terms and Funding

Appendix 1 – Key Risks

Acquisition Terms and Funding

Appendix 1 – Key Risks

Appendix 2 – Jurisdictions & Selling Restrictions

pp y

M2 Investor Presentation, 16 April 2012, Slide 36

Jurisdictions and Selling RestrictionsThis document does not constitute an offer of new ordinary shares ("New Shares") of M2 in any jurisdiction in which it would be unlawful. New Shares may not be offered or sold in any country outside Australia except to the extent permitted below.

Hong KongWARNING: The contents of this document have not been reviewed by any Hong Kong regulatory authority. You are advised to exercise caution in relation to the offer. If you are in doubt about any contents of this document, you should obtain independent professional advice.

New ZealandThe New Shares are not being offered or sold to the public within New Zealand other than to existing shareholders of M2 with registered addresses in New Zealand to whom the offer of New Shares is being made in reliance on the Securities Act (Overseas Companies) Exemption Notice 2002 (New Zealand). The offer of New Shares is renounceable in favour of members of the public.This document has not been registered, filed with or approved by any New Zealand regulatory authority under the Securities Act 1978 (New Zealand). This document is not an investment statement or prospectus under New Zealand law and is not required to, and may not, contain all the information that an investment statement or prospectus under New Zealand law is required to contain.

SingaporeThis document and any other materials relating to the New Shares have not been, and will not be, lodged or registered as a prospectus in Singapore with the Monetary Authority of Singapore. Accordingly, this document and any other document or materials in connection with the offer or sale, or invitation for subscription or purchase, of New Shares, may not be issued, circulated or distributed, nor may the New Shares be offered or sold, or be made the subject of an invitation for subscription or purchase, whether directly or indirectly, to persons in Singapore except pursuant to and in accordance with exemptions in Subdivision (4) Division 1 Part XIII of the Securities and Futures Act Chapter 289 of Singapore (the "SFA") or as Singapore except pursuant to and in accordance with exemptions in Subdivision (4) Division 1, Part XIII of the Securities and Futures Act, Chapter 289 of Singapore (the SFA ), or as otherwise pursuant to, and in accordance with the conditions of any other applicable provisions of the SFA. This document has been given to you on the basis that you are (i) an existing holder of M2’s shares, (ii) an "institutional investor" (as defined in the SFA) or (iii) a "relevant person" (as defined under section 275(2) of the SFA). In the event that you are not an investor falling within any of the categories set out above, please return this document immediately. You may not forward or circulate this document to any other person in Singapore.Any offer is not made to you with a view to the New Shares being subsequently offered for sale to any other party. There are on-sale restrictions in Singapore that may be applicable to investors who acquire New Shares. As such, investors are advised to acquaint themselves with the SFA provisions relating to resale restrictions in Singapore and comply accordingly. q , q p g g p p y g y

United StatesThis document does not constitute an offer to sell, or the solicitation of an offer to buy, any securities in the United States. Neither this document nor any entitlement and acceptance form may be distributed in the United States.

The New Shares have not been, and will not be, registered under the US Securities Act of 1933 or the securities laws of any state or other jurisdiction of the United States. The entitlements t b t k b i th U it d St t b h ti f th t b fit f i th U it d St t Th N Sh t b ff d

M2 Investor Presentation, 16 April 2012, Slide 37

may not be taken up by persons in the United States or by persons who are, or are acting for the account or benefit of, a person in the United States. The New Shares may not be offered, sold or resold in the United States except in a transaction exempt from, or not subject to, the registration requirements of the US Securities Act and the applicable securities laws of any state or other jurisdiction in the United States.

Thank you

M2 Investor Presentation, 16 April 2012, Slide 38