Doing Business in South Africa Moving from Strategy to .../media/IE Singapore/Files/Events... ·...

6

-0- Doing Business in South Africa Moving from Strategy to Implementation iAdvisory Seminar Series Singapore, 22 February 2012 Kobus van der Wath Founder and Group Managing Director, The Beijing Axis & Chairman, The Beijing Axis Africa Pty Ltd. www.thebeijingaxis.com -1- This document is issued by The Beijing Axis. While all reasonable care has been taken in the preparation of this document, no responsibility or liability is accepted for errors or omissions of fact or for any opinions expressed herein. Opinions, projections and estimates are subject to change without notice. This document is for information purposes only, and solely for private circulation. The information contained here has been compiled from sources believed to be reliable. While every effort has been made to ensure that the information is correct and that the views are accurate, The Beijing Axis cannot be held responsible for any loss, irrespective of how it may arise. In addition, this document does not constitute any offer, recommendation or solicitation to any person to enter into any transaction or to adopt any investment strategy, nor does it constitute any prediction of likely future movements or events in any form. Some investments discussed here may not be suitable for all investors. Past performance is not necessarily indicative of future performance; the value, price or income from investments may fall as well as rise. The Beijing Axis, and/or a connected company may have a position in any of the investments mentioned in this document. All concerned are advised to form their own independent judgement with respect to any matter contained in this document. -2- The Beijing Axis’ Knowledge & Network Synergies Beijing Axis Commodities • Commodity Marketing • Commodity Procurement Beijing Axis Capital • Transaction Origination • Corporate Finance Advisory Beijing Axis Procurement • Comprehensive Procurement Solutions Beijing Axis Strategy • Strategy Formulation • Strategy Implementation Founded in 2002; has successfully worked with many international and Chinese/Asian MNCs Operates in four synergistic cross-border China/Asia businesses Provides services across various sectors, with a core focus on the MINING, RESOURCES, INDUSTRIAL and ENGINEERING sectors Provides solutions to international firms as they act in unfamiliar territory in China/Asia Provides solutions to Chinese/Asian firms as they venture out and ‘go global’ -3- Africa Axis’ Knowledge & Network Synergies Africa Axis Commodities • Commodity Marketing • Commodity Procurement Africa Axis Capital • Transaction Origination • Corporate Finance Advisory Africa Axis Procurement • Comprehensive Procurement Solutions Africa Axis Strategy • Strategy Formulation • Strategy Implementation Founded in 2010; has successfully worked with many international and African MNCs Operates in four synergistic cross-border African businesses Provides services across various sectors, with a core focus on the MINING, RESOURCES, INDUSTRIAL, ENGINEERING and OTHER SERVICES sectors Provides solutions to international/African firms as they go global Provides solutions to Asian/International firms as they venture into Africa -4- Getting Started Strategic Imperatives Strategy Implementation Case Studies Final Word -5- South America Africa Other Asia Regional GDP Comparison (USD bn, 2015F)* Bubble Size: Nominal GDP (USD bn, 2015F) Developed economies are expected to continue to lose share in world GDP in the coming years 2011E to 2015F 2011E to 2015F GDP Average Growth Rate (%, 2011E-2015F) Forecast world average GDP growth until 2015F: 3.95% % of World GDP (2015F) Shaded bubbles represent 2011E figures Rising real incomes and high commodity prices will drive growth BRICS 2015F GDP (USD bn) 2011* Growth Rate (%) 2010 GDP Per Capita (USD) China 10,903.6 9.2% 4,382.1 India 2,359.2 7.4% 1,370.8 Russia 1,926.1 4.1% 10,355.7 Brazil 2,546.7 2.9% 10,816.5 South Africa 425.6 3.1% 7,274.4 *Note: Data based on IMF World Economic Outlook *Note: Other Asia includes Bangladesh, Sri Lanka, Nepal, Pakistan, Bhutan, Burma, North Korea, Kazakhstan, Tajikistan, Turkmenistan and Uzbekistan. Source: IMF 2012; The Beijing Axis Analysis

Transcript of Doing Business in South Africa Moving from Strategy to .../media/IE Singapore/Files/Events... ·...

-0-

Doing Business in South Africa Moving from Strategy to Implementation iAdvisory Seminar Series Singapore, 22 February 2012 Kobus van der Wath Founder and Group Managing Director, The Beijing Axis & Chairman, The Beijing Axis Africa Pty Ltd.

www.thebeijingaxis.com

-1-

This document is issued by The Beijing Axis. While all reasonable care has been taken in the preparation of this document, no responsibility or liability is accepted for errors or omissions of fact or for any opinions expressed herein. Opinions, projections and estimates are subject to change without notice. This document is for information purposes only, and solely for private circulation. The information contained here has been compiled from sources believed to be reliable. While every effort has been made to ensure that the information is correct and that the views are accurate, The Beijing Axis cannot be held responsible for any loss, irrespective of how it may arise. In addition, this document does not constitute any offer, recommendation or solicitation to any person to enter into any transaction or to adopt any investment strategy, nor does it constitute any prediction of likely future movements or events in any form. Some investments discussed here may not be suitable for all investors. Past performance is not necessarily indicative of future performance; the value, price or income from investments may fall as well as rise. The Beijing Axis, and/or a connected company may have a position in any of the investments mentioned in this document. All concerned are advised to form their own independent judgement with respect to any matter contained in this document.

-2-

The Beijing Axis’ Knowledge & Network Synergies

Beijing Axis Commodities

• Commodity Marketing • Commodity Procurement

Beijing Axis Capital

• Transaction Origination • Corporate Finance Advisory

Beijing Axis Procurement

• Comprehensive Procurement Solutions

Beijing Axis Strategy

• Strategy Formulation • Strategy Implementation

� Founded in 2002; has successfully worked with many international and Chinese/Asian MNCs � Operates in four synergistic cross-border China/Asia businesses � Provides services across various sectors, with a core focus on the MINING, RESOURCES,

INDUSTRIAL and ENGINEERING sectors

� Provides solutions to international firms as they act in unfamiliar territory in China/Asia

� Provides solutions to Chinese/Asian firms as they venture out and ‘go global’

-3-

Africa Axis’ Knowledge & Network Synergies

Africa Axis Commodities

• Commodity Marketing • Commodity Procurement

Africa Axis Capital

• Transaction Origination • Corporate Finance Advisory

Africa Axis Procurement

• Comprehensive Procurement Solutions

Africa Axis Strategy

• Strategy Formulation • Strategy Implementation

� Founded in 2010; has successfully worked with many international and African MNCs � Operates in four synergistic cross-border African businesses � Provides services across various sectors, with a core focus on the MINING, RESOURCES,

INDUSTRIAL, ENGINEERING and OTHER SERVICES sectors

� Provides solutions to international/African firms as they go global

� Provides solutions to Asian/International firms as they venture into Africa

-4-

Getting Started Strategic Imperatives Strategy Implementation Case Studies Final Word

-5-

South America Africa

Other Asia

Regional GDP Comparison (USD bn, 2015F)* Bubble Size: Nominal GDP (USD bn, 2015F)

Developed economies are expected to continue to lose share in world GDP in the coming years

2011E to 2015F

2011E to 2015F

GDP Average Growth Rate (%, 2011E-2015F)

Forecast world average GDP growth until 2015F: 3.95%

% of World GDP (2015F)

Shaded bubbles represent 2011E figures

Rising real incomes and high commodity prices will drive growth

BRICS 2015F GDP (USD bn)

2011* Growth Rate (%)

2010 GDP Per Capita (USD)

China 10,903.6 9.2% 4,382.1 India 2,359.2 7.4% 1,370.8 Russia 1,926.1 4.1% 10,355.7 Brazil 2,546.7 2.9% 10,816.5 South Africa 425.6 3.1% 7,274.4

*Note: Data based on IMF World Economic Outlook *Note: Other Asia includes Bangladesh, Sri Lanka, Nepal, Pakistan, Bhutan, Burma, North Korea, Kazakhstan, Tajikistan, Turkmenistan and Uzbekistan. Source: IMF 2012; The Beijing Axis Analysis

-6- Source: IMF; UNCTAD; The Beijing Axis Analysis

Tertiary Industry

Africa

Secondary Industry

Primary Industry

USD 63 tn

USD 63 tn

USD 22.2 tn

USD 1.7 tn

USD 1.7 tn

USD 1.7 tn

USD 1.7 tn

USD 1.7 tn

Government Consumption/ Expenditure

Net Exports

Gross Capital Formation

Private Consumption/ Expenditure

Developing Countries

(excl. Africa)

Africa

North America

Asia

Europe

Developed Countries

Other Developing Countries

Africa

South Africa

Others

Egypt

Southern Africa

Northern Africa

Central Africa

Eastern Africa

Western Africa

Africa

Kenya

Algeria

Nigeria

Angola

Middle East

Tanzania Ghana

-7-

Top 15 African Economies (GDP USD bn, Average Growth 2005-2010)

African Nominal GDP Rank (2010)

S. Africa (364, 3.5%)

Egypt (219, 5.9%)

Nigeria (194, 6.7%)

Algeria (159, 3%)

Morocco (91, 4.6%)

Angola (84, 13.9%)

Libya (62, 4.8%)

Sudan (62, 7.1%)

Tunisia (44, 4.4%)

Kenya (4.8%)

Ghana Ethiopia

Tanzania

Cote d'Ivoire 7%)

Cameroon

Source: World Bank; IMF; The Beijing Axis Analysis

Bubble size represents GDP (2010)

Number in the brackets is the average GDP growth (2005-2010)

Rank Country GDP (USD bn) Rank Country GDP

(USD bn) Rank Country GDP (USD bn)

1 South Africa 363.6 18 Botswana 14.8 35 Malawi 5.1

2 Egypt 218.9 19 Equatorial Guinea 14.0 36 Guinea 4.5

3 Nigeria 193.6 20 DRC 13.1 37 Swaziland 3.6 4 Algeria 159.4 21 Gabon 13.0 38 Mauritania 3.6 5 Morocco 91.2 22 Senegal 12.9 39 Togo 3.1 6 Angola 84.3 23 Namibia 12.1 40 Lesotho 2.1 7 Libya 62.3 24 Congo 11.9 41 Eritrea 2.1

8 Sudan 62.0 25 Mauritius 9.7 42 Central African Rep. 2.0

9 Tunisia 44.2 26 Mozambique 9.5 43 Sierra Leone 1.9 10 Kenya 31.4 27 Mali 9.2 44 Cape Verde 1.6

11 Ghana 31.3 28 Burkina Faso 8.8 45 Burundi 1.6

12 Ethiopia 29.7 29 Madagascar 8.7 46 Liberia 0.9 13 Tanzania 23.0 30 Chad 7.5 47 Seychelles 0.9

14 Cote d'Ivoire 22.7 31 Zimbabwe 7.4 48 Guinea-

Bissau 0.8

15 Cameroon 22.3 32 Benin 6.6 49 Gambia 0.8 16 Uganda 17.0 33 Rwanda 5.6 50 Comoros 0.5

17 Zambia 16.1 34 Niger 5.5 51 Sao Tome and Principe 0.2

-8-

African Countries GDP Comparison (USD bn, 2010)*

South Africa

Libya

Nigeria

Algeria Morocco

Angola

Sudan

Tunisia

Ghana

Kenya

Ethiopia

Cote d’lvoire

Tanzania

Cameroon

Egypt Uganda

ZambiaBotswana

Gabon

GDP Per Capita (2010) Other Small

African Countries

Mineral-rich South Africa is the region’s largest economy and only BRICS member

Regional Breakdown

2010 GDP (USD bn)

CAGR (2000-2010)

Northern Africa 597.9 8.2% Southern Africa 406.4 11.3% Western Africa 348.5 14.6% Eastern Africa 178.8 10.6% Middle Africa 198.6 17.8%

Average GDP Growth Rate (%, 2005-2010) Size of the bubble: Nominal GDP (USD bn, 2010)*

*Note: Other Small African Countries include: Mali, Burkina Faso, Madagascar, Chad, Zimbabwe, Benin, Rwanda, Niger, Malawi, Guinea, Mauritania, Togo, Lesotho, Eritrea, Central African Republic, Sierra Leone, Cape Verde, Burundi, Djibouti, Gambia , Liberia, Seychelles, Guinea-Bissau, Comoros, Sao Tome and Principe Regional breakdown is based on UN Classification

Source: IMF; The Beijing Axis Analysis

Why is Angola here

North Africa remains largely dependent on oil exports

-9- Source: Statistics South Africa; IMF; CEIC; The Beijing Axis Analysis

GDP and Population Composition by Province (%, 2010)

Total GDP: USD 363.6 bn

Northern Cape

North West

Eastern Cape

Free State

Limpopo

Western Cape

Gauteng

Northern Capepe

NoN

on by Provin

Limpopo

stern CapeEastern Castern Castern C

Free Stateeeee

Western Cape

KwaZulu-Natal

ulation Compositio

Gauteng

positio

g7% 11%

7%

17% 21%

6% 7%

6% 6%

2% 2%

14% 8%

14% 10%

Mpumalanga

GDP as % of SA Total Population as % of SA Total

GDP Value Added by Sector (%, 1980-2010)

a

GDP Value Added by Sector (%, 1980 2010)

Composition of GDP - Expenditure Approach (%, 1980-2010)

In 2005 South Africa became a net importer

Total Population: 50 mn

-10-

Ease of Doing Business Ranking (2012)

Country Risk Score (Jan 2012)

Top 30 Economies’ Business Environment Comparison Bubble Size: FDI Inflows (USD bn, 2010)

US Japan

Iran

Argentina

India

Mexico

Thailand

Spain

Saudi Arabia

Poland

Belgium

France

U K

Austria

Canada Norway Australia

Sweden Germany

Challenging

Favourable

High-risk Low-risk

Source: UNCTAD; World Bank; IFC; IMS; Euromoney; The Beijing Axis Analysis

High risk and difficulty in doing business Low risk and favourable

business environment

China bubble size (FDI inflows): USD 105 bn

-11- Source: AT Kearney; Centre on Budget and Policy Priorities; The Beijing Axis Analysis

Rank 2007

1

2

6

3

10

11

7

4

21

16

18

9

20

12

8

-

13

-

24

14

Rank 2012

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

World FDI Confidence Index (2012)

Increasing Confidence

(2012) World Open Budget Index (2010)

Increasing Clarity

High scores indicate clarity, scope and availability of documents on public spending FD

I Con

fiden

ce In

dex

Ran

king

-12-

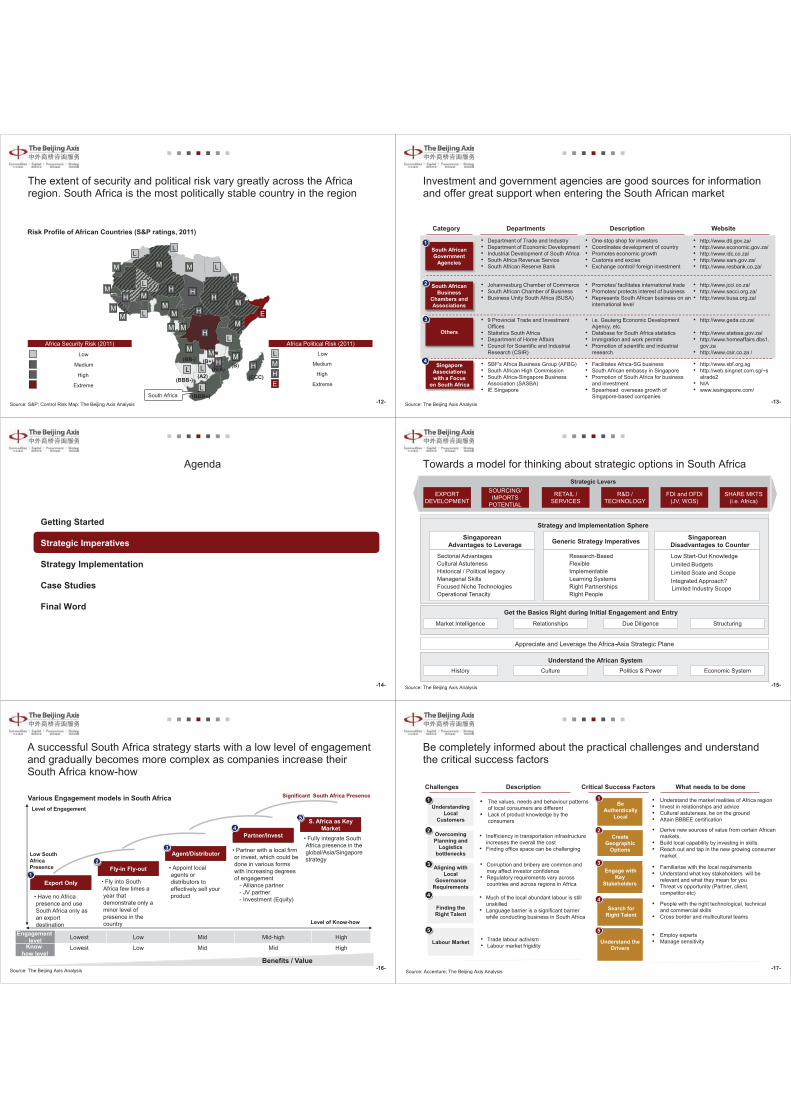

Africa Security Risk (2011)

Low

Medium

High

Extreme

Africa Political Risk (2011)

Low

Medium

High

Extreme

Risk Profile of African Countries (S&P ratings, 2011)

H

E

L

L

L

L L

L

L

L

M M

M

M M M M

M M M

H

H

H

M

M M

M H

H H H

H

L

M M

(BBB+)

(BB-)

(BBB-)

(B+) (B)

(A2) (N/A)

(CCC)

South Africa

L M H E

Source: S&P; Control Risk Map; The Beijing Axis Analysis -13- Source: The Beijing Axis Analysis

South African Government

Agencies

1

Category

• Department of Trade and Industry • Department of Economic Development • Industrial Development of South Africa• South Africa Revenue Service • South African Reserve Bank

Singapore Associations with a Focus

on South Africa

• SBF's Africa Business Group (AFBG) • South African High Commission • South Africa-Singapore Business

Association (SASBA) • IE Singapore

Others

• 9 Provincial Trade and Investment Offices

• Statistics South Africa • Department of Home Affairs • Council for Scientific and Industrial

Research (CSIR)

Departments Website

• http://www.dti.gov.za/ • http://www.economic.gov.za/ • http://www.idc.co.za/ • http://www.sars.gov.za/ • http://www.resbank.co.za/

• http://www.sbf.org.sg • http://web.singnet.com.sg/~s

atrade2 • N/A • www.iesingapore.com/

Description

• One-stop shop for investors • Coordinates development of country • Promotes economic growth• Customs and excise • Exchange control/ foreign investment

• http://www.geda.co.za/

• http://www.statssa.gov.za/ • http://www.homeaffairs.dbs1.

gov.za • http://www.csir.co.za /

• i.e. Gauteng Economic Development Agency, etc.

• Database for South Africa statistics • Immigration and work permits • Promotion of scientific and industrial

research

• Facilitates Africa-SG business • South African embassy in Singapore • Promotion of South Africa for business

and investment • Spearhead overseas growth of

Singapore-based companies

South African Business

Chambers and Associations

• Johannesburg Chamber of Commerce • South African Chamber of Business • Business Unity South Africa (BUSA)

• Promotes/ facilitates international trade • Promotes/ protects interest of business • Represents South African business on an

international level

• http://www.jcci.co.za/ • http://www.sacci.org.za/ • http://www.busa.org.za/

3

2

4

-14-

Getting Started Strategic Imperatives Strategy Implementation Case Studies Final Word

-15-

Strategic Levers

EXPORT DEVELOPMENT

SHARE MKTS (i.e. Africa)

FDI and OFDI (JV, WOS)

SOURCING/ IMPORTS

POTENTIAL

R&D / TECHNOLOGY

RETAIL / SERVICES

Strategy and Implementation Sphere

Understand the Chinese System History Culture Politics & Power Economic System

Appreciate and Leverage the China - Africa Strategic Plane

Get the Basics Right during Initial Engagement and Entry Market Intelligence Relationships Due Diligence Structuring

South African Advantages to Leverage

Sectorial Advantages Cultural Astuteness Historical / Political legacy Managerial Skills Focused Niche Technologies Operational Tenacity

Generic Strategy Imperatives

Research - Based Flexible

Implementable Learning Systems Right Partnerships

Right People

South African Disadvantages to Counter

Low Start - Out Knowledge Limited Budgets Limited Scale and Scope No Patience / Commitment to China No Integrated Approach

Strategy and Implementation Sphere

Understand the African System History Culture Politics & Power Economic System

Appreciate and Leverage the Africa-Asia Strategic Plane -

Get the Basics Right during Initial Engagement and Entry Market Intelligence Relationships Due Diligence Structuring

Singaporean Advantages to Leverage

Sectorial Advantages Cultural Astuteness Historical / Political legacy Managerial Skills Focused Niche Technologies Operational Tenacity

Generic Strategy Imperatives

Research-Based Flexible Implementable Learning Systems Right Partnerships Right People

Singaporean Disadvantages to Counter Low Start-Out Knowledge Limited Budgets Limited Scale and Scope Integrated Approach?

Source: The Beijing Axis Analysis

Limited Industry Scope

-16-

Low South Africa Presence

Source: The Beijing Axis Analysis

Export Only

Fly-in Fly-out

Agent/Distributor

S. Africa as Key Market

1

2

3

• Have no Africa presence and use South Africa only as an export destination

Significant South Africa Presence

• Fly into South Africa few times a year that demonstrate only a minor level of presence in the country

• Appoint local agents or distributors to effectively sell your product

• Fully integrate South Africa presence in the global/Asia/Singapore strategy

Partner/Invest

• Partner with a local firm or invest, which could be done in various forms with increasing degrees of engagement

- Alliance partner - JV partner - Investment (Equity)

4

5

Benefits / Value

Lowest Low Mid Mid-high High

Lowest Low Mid Mid High

Engagement level

Know how level

Level of Engagement

Level of Know-how

Various Engagement models in South Africa

-17-

▪ Familiarise with the local requirements ▪ Understand what key stakeholders will be

relevant and what they mean for you ▪ Threat vs opportunity (Partner, client,

competitor etc)

Description

▪ The values, needs and behaviour patterns of local consumers are different

▪ Lack of product knowledge by the consumers

What needs to be done Critical Success Factors Challenges

Be Authentically

Local

▪ Understand the market realities of Africa region ▪ Invest in relationships and advice ▪ Cultural astuteness, be on the ground ▪ Attain BBBEE certification

1

Overcoming Planning and

Logistics bottlenecks

• Inefficiency in transportation infrastructure increases the overall the cost

• Finding office space can be challenging

2 Create

Geographic Options

▪ Derive new sources of value from certain African markets.

▪ Build local capability by investing in skills ▪ Reach out and tap in the new growing consumer

market

2

Aligning with Local

Governance Requirements

• Corruption and bribery are common and may affect investor confidence

• Regulatory requirements vary across countries and across regions in Africa

Engage with Key

Stakeholders

▪ Employ experts ▪ Manage sensitivity • Trade labour activism

• Labour market frigidity

Search for Right Talent

4

3

Labour Market

• Much of the local abundant labour is still unskilled

• Language barrier is a significant barrier while conducting business in South Africa

Understand the Drivers

▪ People with the right technological, technical and commercial skills

▪ Cross border and multicultural teams

3

5

Understanding Local

Customers

1

5

Finding the Right Talent

4

Source: Accenture; The Beijing Axis Analysis

-18-

Getting Started Strategic Imperatives Strategy Implementation Case Studies Final Word

-19- Source: Various; The Beijing Axis Analysis

Black Economic Empowerment

Basic Knowledge of Political/Economic

Situation

Service Providers

Ethnic and Cultural Issues

A deep understanding of affirmative action policies is required. Policies that deal with this issue need to be implemented for success in South Africa. If the plan is to sell to the government or to government-funded organisations, BEE accreditation is compulsory.

When doing business in the country, South Africans expect at least some background knowledge of its history and current political system. A thorough research on the history of South Africa is highly recommended.

Various world-class service providers have operations in South Africa. This includes top law and accounting firms, consultancies, government agencies, as well as due diligence and real estate companies.

South Africa is very diverse. Willingness to cooperate with people of different ethnic backgrounds is essential for doing business in South Africa.

Issues Description

Conservative Market Environment

South Africa has a relatively conservative market environment, meaning that players usually only use well-known suppliers. As a result, an effective and a sustained market development strategy is vital for success in the country.

1

3

2

4

5

-20-

Smaller issues

Larger issues

Long term Requires Awareness

• Complications deriving from new potential nationalistic policies may impact long-term sustainability of your business in South Africa

• Awareness of the stability and fluctuations of the South African currency (Rand)

Bubble size: Probability of Occurrence • Short-term action is required in order to address the issues of operating in a foreign/ unfamiliar environment

Source: The Beijing Axis Analysis

• Economic growth story, both in Asia and South Africa, can influence your overall business strategy

External Issues

Internal Issues

Currency Issues

Operating Issues

Market Issues

Political Issues

Cultural Issues

• Awareness of your respective market conditions and potential future obstacles

• Good awareness of major labour issues. Choosing a stance and tactic vis-a-vis the unions should be a critical component of your South Africa strategy

Macro- Economic

Issues

Short term Requires Action

Labour Issues

• Work towards diminishing the impact of cultural differences in regards to ways of doing business

-21- Source: Accenture; The Beijing Axis Analysis

Market Research

Value Proposition

Market Entry Strategy

Sourcing Manufacturing Distribution

Strategy Strategy Implementation

What is the target market?

What is the right product/ service?

What is the best market entry strategy?

Marketing and

Promotion

What is the most feasible way to source?

Where/ How should production take place?

What are the channels to market?

What is the most effective marketing strategy?

Do a deep dive analysis of the local market. Understand competitors and consumers by tapping into local knowledge

Ensure the product/services are appealing to the local consumers

Highly depends on risk appetite, however a comprehensive entry strategy is essential for success

Partner or build solid relationships with local suppliers in order to learn about local consumers’ preferences

Leverage the existing innovative mechanism in the market

Direct personal selling and visibility in the informal sector is key for success; traditional routes tend not to be as successful

Key

Que

stio

nsAc

tion

-22- Source: The Beijing Axis Analysis

• Accurate Information

• Right People in the Team

• Integrate (become an insider)

• Due Diligence

• Right Partners

• Right Service Providers

• Comprehensive Strategy Formulation

• Appropriate Operational Business

Model

-23-

Getting Started Strategic Imperatives Strategy Implementation Case Studies Final Word

-24-

Project Overview

Southern African market entry strategy and assistance with operational establishment Implementation •Comprehensive market study to gauge the Southern African market and identify opportunities for the client’s planned market entry

•Analysis of all the relevant client industries to anticipate demand and growth in the forthcoming years

•Methodically constructed a database of all the major industry players, competitors and projects in the pipeline

•Constructed a matrix of all factors influencing the supply side in a number of southern African countries

•On-the-ground investigations on establishing an operational base for the client in southern Africa to provide the client with the best practical options to start operations immediately

Case Study 1

Source: The Beijing Axis Analysis

Project Outcome

•The project is on-going •Brand has been established; physical infrastructure is now being rolled out •Africa sales have surpassed USD 200 mn

-25-

Case Study 2

Project Overview

Market entry strategy for South Africa and Africa market

Implementation •Conducted a feasibility study that included: -Overview of South Africa’s construction & engineering industry and equipment industry -Analysis of the challenges faced by Asian companies in South Africa -Assessment of the current outlook for the client’s products

•A strategic assessment to gauge the viability of various modes of market entry •Integrated all the findings to produce an actionable business plan, composing of various elements such as: -Requirements and process flow for setting up a venture -Optimal business model -Production and operating requirements assessment -Start-up schedules and financial analysis and projections -Partner and acquisition plan

Source: The Beijing Axis Analysis

Project Outcome

The project is on-going

•Brand is now being established

•Sales is gradually ramping up

•Currently designing maintenance and support infrastructure

-26-

Case Study 3

Project Overview

Market entry strategy for a South African player

Implementation • Engaged in market research and analysis, establishing the

market size, players and overall environment for the travel industry

• Looked at a spectrum of modes and models of engagement covering organic growth, partnerships and acquisitions

• Integrated all the findings from the steps described above to produce an actionable business plan. This plan included the following: - Requirements and process flow for setting up a new

venture - Optimal business model - Marketing and sales strategy - License and association membership requirements and

assessment - Management and personnel considerations - Start-up location and financial analysis and projections - Preliminary partner/acquisition plan

Source: The Beijing Axis Analysis

Project Outcome

•The project is in the implementation phase. •Current establishing physical infrastructure •Have identified initial break even client list

-27- Source: The Beijing Axis Analysis

Southern African market entry

� Culture matters

� Information is key

� Stakeholder relations is crucial

� Governance is pivotal

� Sales planning and roll out are key

� Get close to the market - be on the ground

� Culture matters

� Information is key

� Stakeholder relations is crucial

� Governance is pivotal � Maintenance and support are

crucial

� Brand positioning is important

� Culture matters

� Information is key

� Stakeholder relations is crucial

� Governance is pivotal

� Corporate landscape very different – understand them well

� Duel diligence is important

Analysis Strategy Design

Engagement Implementation

South Africa and Africa market entry

Singapore market entry

-28-

Getting Started Strategic Imperatives Strategy Implementation Case Studies Final Word

-29- Source: The Beijing Axis Analysis

� Africa far more important in the global economy – the world has changed and is changing still, with many far-reaching implications: Africa an opportunity

� Doing business in South Africa is relatively easy but needs a systematic approach – understand the variability, volatility and exceptions

� Be strategy (horizon) led, not operations (today) led - good strategy implementation is key (Processes, systems and people (partners in SA))

� Appreciate value of strategic intelligence and only listen to true experts – avoid myth, hype and orthodoxies

� Use information well, but it has to be the right information – This is the main aid in risk mitigation

� All about people – right people, right attitudes, right skills, right leadership, right focus

� Analysis, strategy design, engagement and implementation

-30-

THANK YOU! Kobus van der Wath Founder and Group Managing Director, The Beijing Axis & Chairman, The Beijing Axis Africa Pty Ltd E-mail: [email protected]

Beijing, China Cheryl Tang, GM, China [email protected] +86 10 6440 2106

Shanghai, China Julia Wang Procurement Specialist [email protected] +86 21 5158 3584 ext. 6249

Hong Kong TBA Secretary Corporate Office 3806 Central Plaza, 18 Harbour Rd, Wanchai, HK

Singapore Kobus van der Wath, Founder Penthouse & LV 42, Suntec Tower 3, 8 Temasek Blvd, Singapore 038988 +65 6829 2189

Perth, Australia Kobus van der Wath, Founder [email protected]

Johannesburg, South Africa Dirk Kotze Director; GM, Africa [email protected] +27 (0)11 201 2453

London, UK/Europe Matt Pieterse MD, Beijing Axis Capital [email protected]

Russia Desk Lilian Luca (Beijing) MD, Beijing Axis Procurement [email protected]

Latin America Desk Javier Cuñat (Beijing) GM, Beijing Axis Strategy [email protected]

www.thebeijingaxis.com