Doing Business in China: 7 Mistakes to Avoid · Our six core services help our clients make their...

43

Fiducia Limited and its affiliates exclude all liability for any damages and losses arising out of or in connection with this presentation. The information is for general guidance and does not replace specialised advice. Copyright © 2017, Fiducia Limited. All rights reserved. 7 Mistakes to Avoid When Doing Business in China Thaddaeus Mueller, Director June 20 th , 2017 In cooperation with

Transcript of Doing Business in China: 7 Mistakes to Avoid · Our six core services help our clients make their...

Fiducia Limited and its affiliates exclude all liability for any damages and losses arising out of or in connection with this presentation. The information is for general guidance and does not replace specialised advice.

Copyright © 2017, Fiducia Limited. All rights reserved.

7 Mistakes to Avoid When Doing

Business in China

Thaddaeus Mueller, Director

June 20th, 2017

In cooperation with

2

Background

35 years offering set-up and expansion support

4 strategically located offices:

120+ foreign and Chinese specialists

Our clients benefit from our integrated services and long-term approach.

Beijing | Hong Kong | Shanghai | Shenzhen

3

Our six core services help our clients make their growth plans operational and profitable.

Fiducia – Service Overview

4

Our Industries

We have accumulated industry-specific experience by advising clients over many years in related industries.

Fiducia’s US Clients

5

Mistake No. 1

Missing out on unfolding

opportunities

6

US-China Trade Opportunities

The Chinese consumer market will grow by almost the same amount as the US market by 2020. Trade policy under Trump is likely to bolster exports to China as a way of bringing the trade deficit down.

Fast-Growing Consumption in China 2015-2020

2.6

2.3

1.6 0.4

0.4

US$

trillion Consumption Growth 2015-

2020

Private consumption

2015

US Trade of Goods with China

Exports

Imports

US$

billion

2016

2015

2014

2013

2012

7

Opportunities by Sector

China’s demographic and economic trends lays a strong foundation for these sectors.

Medical

Technology

E-Commerce

Green Tech

Entertainment

Machinery

Transportation

8

Opportunities by Sector | Aviation Industry

China's first large jetliner, the COMAC C919, made its maiden flight on May 5th, 2017.

The radar cover, wings and tail are the only Chinese parts in it.

Source: Aerotime

9

Mistake No. 2

Underestimating the pace of

regulatory change

10

High-Tech Status

Companies engaged in R&D or high-tech goods and services can apply for a range of tax incentives, such as the High and New Technology Enterprise (HNTE) Status.

Who is eligible?

Registered resident enterprise for >1 year

Innovative products/services within key industries

Proprietary intellectual property

3-5% of total annual revenue invested in R&D

>60% of revenue spent on high-tech related operations

>10% of staff dedicated to R&D

25%

Standard Corporate

Income Tax (CIT):

11

Two-Invoices System

The regulation limits the number of invoices between healthcare supplies manufacturers and hospitals to a maximum of two.

Impact on Distribution Structures

Policy Goals

12

Mistake No. 3

Leaving space for compliance

risks

13

Compliance in China

Non-compliance in China can come in different shapes and sizes.

14

Internal Compliance

Loopholes in inventory control

systems

Weak company policy on

accounts receivable

The earlier these red flags are identified, the quicker management can act

and take preventative measures.

Rank Country Index

1 Denmark 90

2 New Zealand 90

9 Canada 82

15 Hong Kong 77

18 USA 74

79 China 40

123 Mexico 30

Corruption Perceptions Index 2016

Very Clean

Highly Corrupt

Weak internal control of chop

usage

Unclear purchasing procedures

15

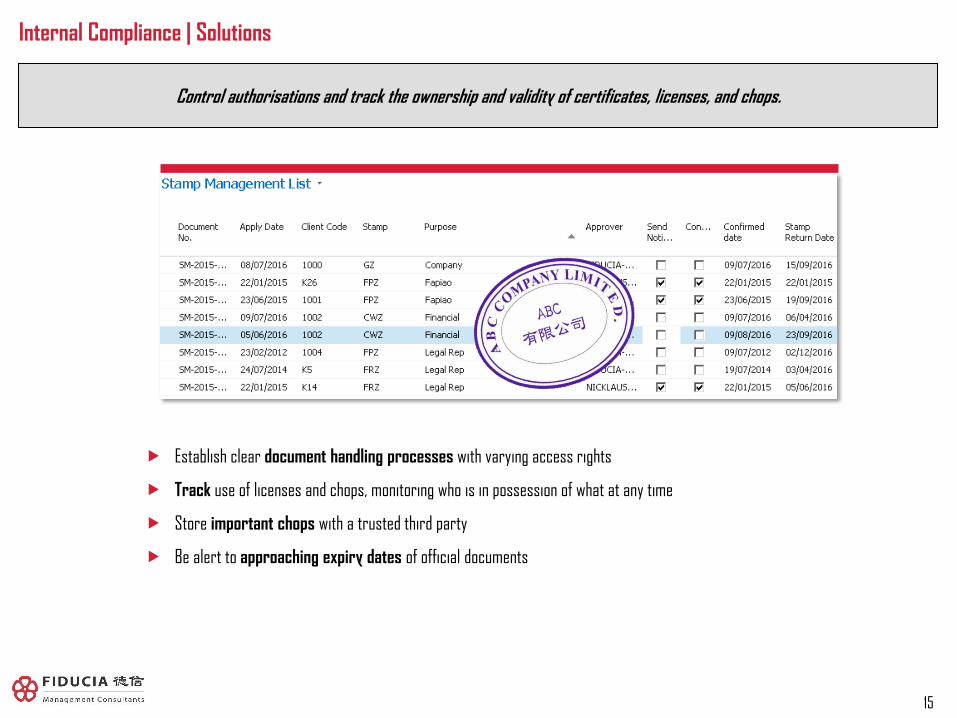

Internal Compliance | Solutions

Control authorisations and track the ownership and validity of certificates, licenses, and chops.

Establish clear document handling processes with varying access rights

Track use of licenses and chops, monitoring who is in possession of what at any time

Store important chops with a trusted third party

Be alert to approaching expiry dates of official documents

16

Mistake No. 4

Being unfamiliar with local HR

trends

17

Top HR Trends in China, 2017

Rising living costs, cultural change, and fresh regulations in China will give rise to new challenges.

18

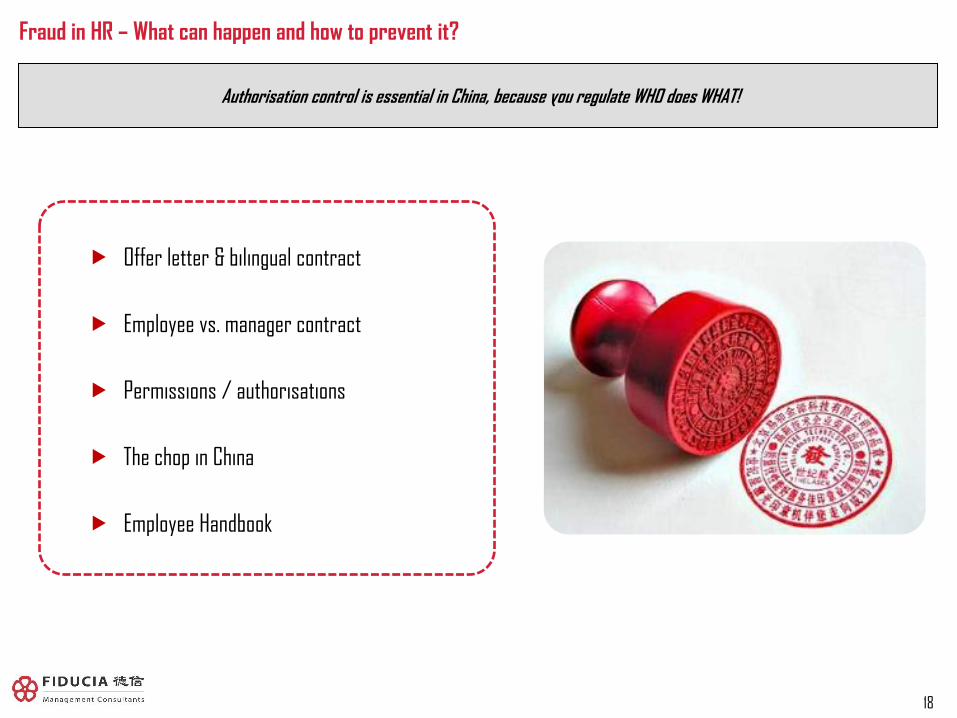

Fraud in HR – What can happen and how to prevent it?

Authorisation control is essential in China, because you regulate WHO does WHAT!

Offer letter & bilingual contract

Employee vs. manager contract

Permissions / authorisations

The chop in China

Employee Handbook

19

Mistake No. 5

Miscalculating your cash flow

planning

20

Registered Capital Requirements and Cash Flow Planning

Cash flow planning is challenging in China because (a) RMB is a non-convertible currency, and

(b) required approvals for capital increase take a long time.

Cash flow needs until operation

becomes self-financing Timeline for capital injection Borrowing gap

Shareholder loan Bank financing Capital increase

2. Financing options

1. Plan your business and cash flow

21

Mistake No. 6

Being mislead when selling into

China

22

Building the Right Distributor Relations

Most foreign companies start selling into China via distributors. These evaluation criteria and key questions should be considered when setting up your China distribution.

Choosing the Right Distributor Drafting the Right Agreement

Product know-how

Distribution capability

Business development

Professionalism

Exclusivity is NOT required

The trademark should NOT belong to the

distributor

Register original AND Chinese language

brand name

Don’t let the distributor define your

strategy

23

Mistake No. 7

Overlooking Hong Kong as a

stepping stone

24

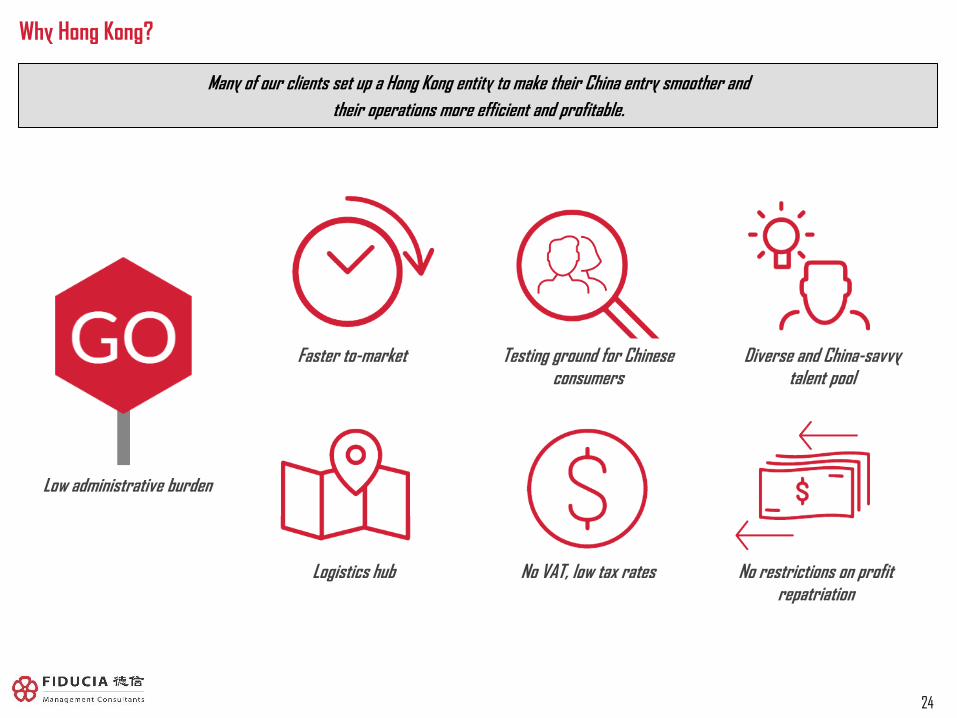

Why Hong Kong?

Many of our clients set up a Hong Kong entity to make their China entry smoother and

their operations more efficient and profitable.

Low administrative burden

Testing ground for Chinese consumers

Logistics hub No VAT, low tax rates

Faster to-market Diverse and China-savvy talent pool

No restrictions on profit repatriation

25

Comparing HK and PRC

Hong Kong China

Company incorporation (days) Approx. 5 Approx. 180

Capital requirements HKD 1 (EUR 0.12) Recommended Capital equal to at least expenses for one year

of operation

Social Security Tax 5% Approx. 50%

Value-Added Tax 0% 17%

Profit Tax 16.5% 25%

Withholding Tax on dividends 0% 5%

Individual Income Tax 15% From 3% to 45% (common tax rates from 20% to 30%)

Hong Kong is an attractive location for foreign companies seeking increased involvement in Asian markets.

3

26

The Fiducia Managers Team – Talk to Us!

How Fiducia Can Help You: Obtain research and advice

Set up / buy / restructure a company

Outsource accounting and treasury

Source products

Sell products and services

Recruit talent

27

What Is Your Next Move?

www.fiducia-china.com | [email protected]

Shanghai

T (+86) 21 6389 8288

F (+86) 21 6389 8388

Hong Kong

T (+852) 2523 2171

F (+852) 2810 4494

Shenzhen

T (+86) 755 8329 2303

F (+86) 755 8329 0821

Fiducia Management Consultants – Providing China Insight Since 1982

Beijing

T (+86) 10 85236308

F (+86) 10 8523 5789

Certain Tax Aspects of Doing

Business in China

Presented by:

R. Daniel Fales, CPA, JD

June 20, 2017

U.S. Tax Perspectives

• Disregarded Entity

• Foreign Subsidiary

• Foreign Partnership

Disregarded Entities

• Check the Box Regulations – Treas.Reg. §

301.7701-2 and § 301.7701-3

They changed the game for entity classification

These regulations added the term “Disregarded

Entity”

• Per Se Corporations under Treas.Reg. §

301.7701-2(b)(8)

Gufen Youxian Gongsi

PRC Entities for Foreign Investment

• Wholly Foreign Owned Enterprises – WFOE

A PRC limited liability company

• Equity Joint Ventures

A PRC limited liability company between a Chinese

and foreign partner

• Representative Office – RO

Treated as a branch of a U.S. company

The Election Process

• An election is only needed if an entity is to be classified

as something other than its default classification.

Treas.Reg. § 301.7701-3(a)

• For foreign entities it is:

A partnership if it has two or more members and at least

one member does not have limited liability

A corporation if all members have limited liability

A disregarded entity if it has a single owner that has

limited liability from its owner

• Treas.Reg. § 301.7701-3(b)(2)

• These are different rules for eligible foreign entities than

domestic entities!

The Election Process

• If you want a classification other than the default

classification then you must file an entity classification

election

• This is filed on Form 8832

• There are strict timelines for when the election must be

filed

Ramifications of Being Disregarded

• The income, gain, loss, deductions and credits of the disregarded entity are

not separately reported by the parent corporation

• Instead the disregarded entity is treated as a division of the parent

corporation

• There is no deferral of the disregarded entities’ taxable income

• You will be able to utilize the losses of the disregarded entity

• There is an immediate need to plan for proper utilization of U.S. foreign tax

credits to the U.S. parent corporation – even if the U.S. parent corporation is

a flow through entity

• U.S. foreign tax credit planning can be among the most highly technical

aspects of U.S. taxation – it also can produce results that are not at all

intuitive

Foreign Corporation Status

• A foreign corporation is respected by the IRC as a

separately taxed entity

• The income and loss of the foreign corporation will not

be subject to U.S. taxation until the repatriation of the

profits

This has been the subject of considerable

Congressional and IRS scrutiny over the last few

years

See the CAT and Apple Congressional hearings

Subpart F

• If you are a Controlled Foreign Corporation (CFC) as defined by IRC

§ 957 then you need to be aware of the income inclusion rules of

Subpart F of the IRC

• If more than 50% of the total combined voting power of all classes of

stock and the total value of the stock of the corporation is owned by

any U.S. person at anytime during the year then you are deemed to

be a CFC

• If a CFC meets the definition for 30 days or more during the taxable

year then every U.S. person who is an owner of the CFC and owns

stock on the last day of the year is required to include their share of

the CFC’s Subpart F income for the year

Company Rules - PFICs

• Even if a foreign subsidiary does not meet the definition

of being a CFC, the PFIC rules may require a current

income inclusion

• A PFIC is defined in IRC § 1297 as a foreign corporation

if 75% or more of the gross income is passive or the

average percentage of its assets that produce passive

income is at least 50%

• Once classified as a PFIC, then there are certainly

technical rules that kick in to prevent utilizing a corporate

solution to avoid current U.S. income taxation

Transfer Pricing

• Transfer pricing is the allocation of income between controlled

entities

• Transfer pricing impacts both the U.S. entity and the Chinese

entity, with each country seeking to insure that the appropriate

amount of taxable income is reported

• When looking at transfer pricing you need to look at the global

impact and not just a “one way approach”

• Both the U.S. and China have significant enforcement

initiatives with regard to insuring transfer pricing is not being

used to unreasonably shift profits

Transfer Pricing

• The U.S. and China can impose significant penalties if

upon a transfer pricing examination they determine that the

transfer pricing being utilized is unjustifiable.

• The U.S. can impose penalties of either 20% or 40% for

transfer pricing violations if the audit adjustment meets

certain thresholds.

• Penalty Protection – A contemporaneous transfer pricing

study/documentation

• If you can provide contemporaneous transfer pricing

documentation as provided for in Treasury Regulations

then you can avoid penalties.

Foreign Reporting

• The focus of U.S. international tax has been to increase

the amount of information that is being reported

• Under this new regime of increased information reporting

has been the increased use of penalties for

noncompliance with required international tax reporting

• There have been several very high profile cases of

confiscatory penalties be applied and upheld for non-

reporting

• The IRS and Treasury have run and may continue to run

Voluntary Disclosure Initiatives

Selected Foreign Reports

• Foreign Bank Accounts – FinCen Form 114 (Due

by June 30th)

• Foreign Financial Assets – Form 8938

• CFCs – Form 5471

• Foreign Partnerships – Form 8865

• U.S. Withholdings – Forms 1042 and 1042-S

Tax Treaties

• Bi-lateral tax treaties are entered into between two sovereign tax

jurisdictions to prevent double taxation for entities conducting business

or having taxable contacts within the two contracting states

• The U.S. and the PRC entered into a bi-lateral income tax treaty in

1984

• Permanent Establishment is the necessary contact a business

enterprise must have with either the U.S. or PRC to become subject to

tax. Article 5

• Note Article 5, Section 5 – “[W]here a person, other than an agent of

independent status…, is acting on behalf of an enterprise and habitually

exercises in a Contracting State an authority to conclude contracts in

the name of the enterprise, that enterprise shall be deemed to have a

permanent establishment in that Contracting State…”

Thank you for your time!

QUESTIONS?

R. Daniel Fales, CPA, JD

Shareholder

513.241.3111