Does a CCP reduce counterparty risk in a heterogeneous ... · Rod Garratt (FRBNY) and Peter...

30

The views expressed in this paper are those of the authors and do not necessarily reflect those of the Federal Reserve Bank of New York, the Federal Reserve System or the Bank of England. Does a CCP reduce counterparty risk in a heterogeneous network? Rod Garratt (FRBNY) and Peter Zimmerman (BoE) CEMLA, Seminar on Network Analysis and Financial Stability Issues, 2014

Transcript of Does a CCP reduce counterparty risk in a heterogeneous ... · Rod Garratt (FRBNY) and Peter...

The views expressed in this paper are those of the authors and do not necessarily reflect those of the

Federal Reserve Bank of New York, the Federal Reserve System or the Bank of England.

Does a CCP reduce counterparty risk in a

heterogeneous network?

Rod Garratt (FRBNY) and Peter Zimmerman (BoE) CEMLA, Seminar on Network Analysis and Financial Stability Issues, 2014

2

One of the benefits of central clearing is that it reduces the

aggregate level of exposures in the system by netting offsetting

claims.

This is true in a world where all asset classes are

simultaneously novated to a CCP.

Duffie and Zhu (2011) shows that when a single asset class (or

a subset of the asset classes) is switched to central clearing,

bilateral exposures may increase, as a result of reduced netting

opportunities across pairs of banks, resulting in an overall loss

in netting efficiency.

Netting Efficiency

3

(i) central clearing in a single asset is bad

(ii) central clearing in a single asset is good

Netting Efficiency

A B -1

1

1

-1

-1

1

B A

1 -1

CCP

-1

A

1

C B

-1 1 1 -1

A

1

-1 C B

-1

1 1

CCP -1

4

In both cases introducing a CCP in all assets would minimize

net exposures.

It is the fact that some assets are less conducive to central

clearing than others that makes this (ideal) solution impractical.

Netting Efficiency

5

Duffie and Zhu’s results are not based on actual exposure

networks.

Rather they express the total exposure of dealer i to dealer j of

all positions in asset class k by a random variable

They specify a distribution that is assumed to generate these

exposures and their results are based on expected exposures

with respect to this distribution.

Because they assume symmetry in the distributions across all

dealers, they can compute the expected total net exposure with

or without a CCP by looking at a single dealer.

Duffie and Zhu (2011)

6

Taking as given the distribution used to generate exposures,

they are able to express conditions for whether or not a CCP is

beneficial solely in terms of the number of assets classes (K)

and the number of dealers (N).

𝐾 <𝑁2

4(𝑁 − 1)

Advantage: it relates the question of whether or not the

introduction of a CCP in a single asset class is beneficial or not

to easily observable parameters.

Disadvantage: the implied networks are too homogeneous and

lack the scale-free property typically associated with financial

networks (Soramaki et al. 2007, and Ianaoka et al., BoJ

working paper, 2004).

Duffie and Zhu (2011)

7

Barabási and Albert (1999) argue that two features are

essential to capture real world networks: growth and

preferential treatment.

To incorporate the growing character of the network, they

propose that the network construction begin with a small

number (m0) of nodes.

At every time step a new node is added, which is linked to m

existing nodes.

To incorporate preferential attachment, they assume that the

probability that a new node will be connected to an existing

node i is given by 𝑘𝑖/ 𝑘𝑗𝑗 where ki is the connectivity of node i.

This network evolves into a scale-free network (the number of

links k originating from a given node exhibits a power law

distribution P(k)=k-α) with power α=3.

Barabási and Albert (1999)

8

Barabási and Albert obtain results that hold when the number of

nodes becomes very large

Assumption of a large network is not necessarily realistic for our

purposes

Duffie and Zhu consider a network of size 12, which is the number

of entities that, at the time of writing their paper, had partnered

with ICE Trust to create a CCP for clearing credit default swaps.

Table 1 in Galbiati and Soramaki (2012) covers a wider range of

CCP networks; none of them have more than 60 members.

We use a simpler version that has an exact solution for a

network of any size

DMS Network

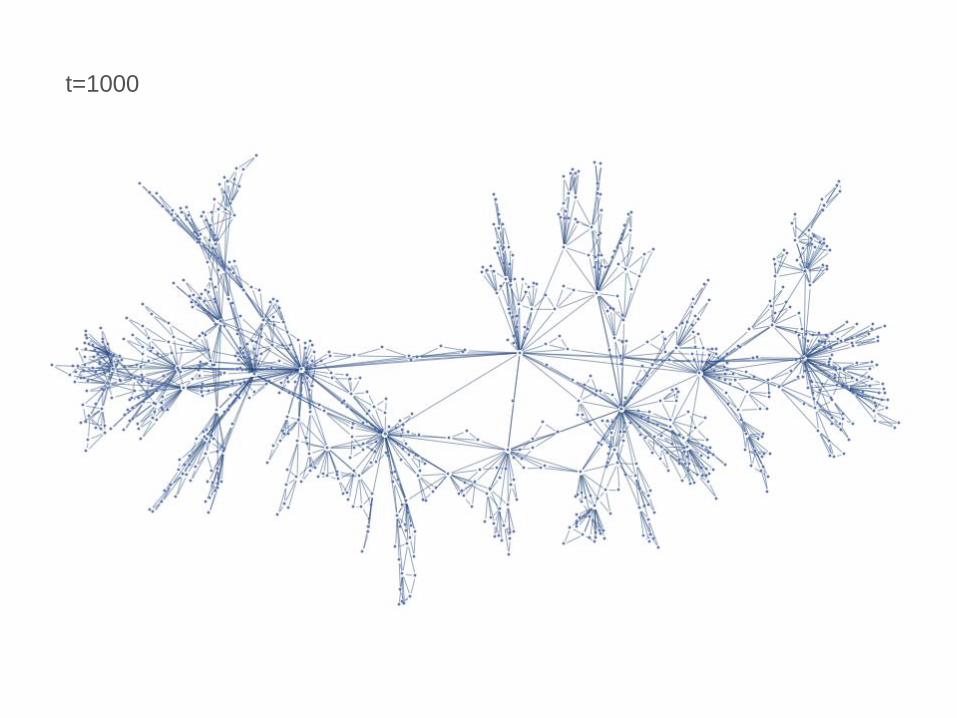

Dorogovtsev, Mendes and Samukin (2001)

9

1. Begin time t = 2 with 3 nodes. Each has two links connecting

to one another.

2. At each step a new node is added with two links. Choose an

existing link at random: each is chosen with equal probability.

Connect the new node to the two nodes which share that link.

DMS Network

This process generates an

undirected network of size N

=t+1, which tends towards a

scale-free network with

exponent a = 3 as t becomes

large.

t=100

t=100

t=500

t=1000

Degree Densities for t=100, 500 and 1000 (blue, pink, green). Power function parameter a=2,3.

15

for a given t

𝑃𝑡 𝑠

=𝑡

𝑡 + 1

𝑠 − 1

2𝑡 − 3𝑃𝑡−1 𝑠 − 1 + 1 −

𝑠

2𝑡 − 3𝑃𝑡−1 𝑠 +

1

𝑡 + 11[𝑠=2]

for 𝑡 ≥ 3 with the initial condition 𝑃2 𝑠 = 1[𝑠=2]

Exact solution for any t is messy, but obtainable (see DMS)

In the limit

lim𝑡→∞

𝑃𝑡 𝑠 =12

𝑠(𝑠 + 1)(𝑠 + 2)

Point 1: we can obtain finite and limit predictions for the

expected number of links each node has: 𝐸𝑡(𝑆) = 𝑗𝑃𝑡(𝑗) 𝑡−1𝑗=2

Distribution of S

16

We now need to determine the value (or weight) of each link.

As in Duffie and Zhu, we assume that if two dealers have a link

in one asset class, then they have a link in all K asset classes.

For each pair of connected nodes i and j, we generate the net

exposures 𝑋𝑖𝑗𝑘 , k=1,…,K, as K iid normal random variables with

mean 0 and standard deviation s.

𝑌𝑖𝑗𝐾 = max

𝑋𝑖𝑗

𝑘 , 0𝐾

𝑘=1

denotes node i’s netted exposure to node j 𝑓 𝐾 = 𝐸 𝑌𝑖𝑗

𝐾

denotes expected net exposure between any two nodes

Bilateral Exposures

17

𝑓 𝐾 = 𝐸 𝑌𝑖𝑗𝐾 = 𝐸 max

𝑋𝑖𝑗

𝑘 , 0𝐾

𝑘=1= max 𝑥, 0 𝑝𝐾 𝑥 𝑑𝑥

∞

−∞

= 𝑥𝑝𝐾 𝑥 𝑑𝑥∞

0

where 𝑝𝐾 𝑥 is the pdf of 𝑋𝑖𝑗𝑘𝐾

𝑘=1 .

Since 𝑋𝑖𝑗𝑘~𝑁 0, 𝜎2 , we know that 𝑋𝑖𝑗

𝑘~𝐾𝑘=1 𝑁 0,𝐾𝜎2 .

Thus

𝑓 𝐾 = x1

2𝜋𝐾𝜎𝑒𝑥𝑝 −

𝑥2

2𝐾𝜎2 dx =𝐾

2𝜋𝜎

∞

0

Point 2: we can obtain an expression for the expected net

exposure associated with each link

f(K)

18

𝜑𝑁,𝐾 = 𝐸 𝑌𝑖𝑗𝐾

𝑗∈𝐽𝑖

= 𝐸 𝐸 𝑌𝑖𝑗𝐾

𝑗∈𝐽𝑖

|𝑆 = 𝐸 𝑆𝑓(𝐾)

= 𝐸 𝑆 𝑓(𝐾)

With a CCP net exposure of a given node i becomes

𝜑𝑁,𝐾 = 𝐸 𝐸 𝑌𝑖𝑗𝐾−1 +

𝑗∈𝐽𝑖

𝑌𝑖,𝐶𝐶𝑃𝑆 |𝑆 = 𝐸 𝑆𝑓 𝐾 − 1 + 𝑓(𝑆)

= 𝐸 𝑆 𝑓 𝐾 − 1 + 𝐸 𝑓(𝑆)

Change in expected net exposure

𝜑𝑁,𝐾 −𝜑𝑁,𝐾 = 𝐸 𝑆 𝑓 𝐾 − 1 + 𝐸 𝑓(𝑆) − 𝐸 𝑆 𝑓(𝐾)

I. Expected netting efficiency

19

Change in expected net exposure

𝜑 𝑁,𝐾 − 𝜑𝑁,𝐾 = 𝐸 𝑆 𝑓 𝐾 − 1 + 𝐸 𝑓(𝑆) − 𝐸 𝑆 𝑓 𝐾 < 0

iff

𝐾 + 𝐾 − 1 <𝐸 𝑆

𝐸 𝑆

DMS network: 𝐸𝑡 𝑆 =4𝑡−2

𝑡+1→ 4 and hence for large t,

𝐸 𝑆

𝐸 𝑆~

4

12

𝑠(𝑠 + 1)(𝑠 + 2)∞𝑠=2

= 1.73 < 2 + 1

I. Expected netting efficiency

Result 1. CCP reduces netting efficiency for all K>2.

(Strengthens D&Z)

20

Can show that

𝑣𝑁,𝐾 −𝑣𝑁,𝐾 < 0

iff

2 𝐾 − 1 <𝑉𝑎𝑟 𝑆 − 𝑉𝑎𝑟 𝑆

𝐸 𝑆3/2 − 𝐸[𝑆]𝐸 𝑆

DMS network: R.H.S increases without bound as t gets large

Why? Asymptotically, 𝐸 𝑆2 is infinite, but 𝐸 𝑆𝑚 will be finite for

any 𝑚 < 2.

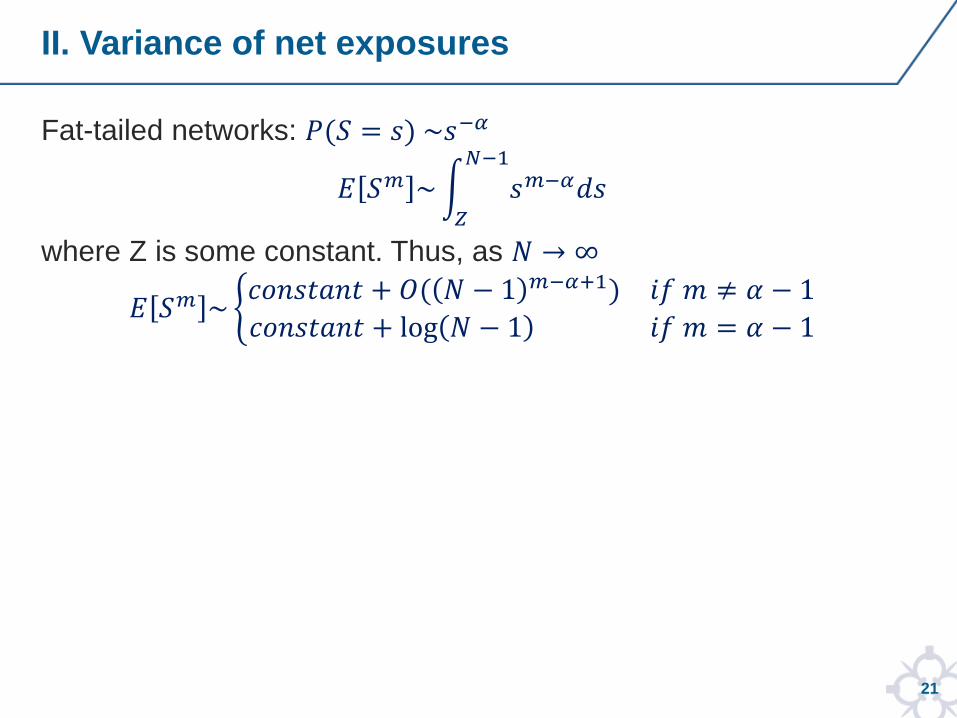

II. Variance of net exposures

21

Fat-tailed networks: 𝑃(𝑆 = 𝑠) ~𝑠−𝛼

𝐸 𝑆𝑚 ~ 𝑠𝑚−𝛼𝑑𝑠𝑁−1

𝑍

where Z is some constant. Thus, as 𝑁 → ∞

𝐸 𝑆𝑚 ~ 𝑐𝑜𝑛𝑠𝑡𝑎𝑛𝑡 + 𝑂( 𝑁 − 1 𝑚−𝛼+1) 𝑖𝑓 𝑚 ≠ 𝛼 − 1

𝑐𝑜𝑛𝑠𝑡𝑎𝑛𝑡 + log 𝑁 − 1 𝑖𝑓 𝑚 = 𝛼 − 1

II. Variance of net exposures

22

Can show that

𝑣𝑁,𝐾 −𝑣𝑁,𝐾 < 0

iff

2 𝐾 − 1 <𝑉𝑎𝑟 𝑆 − 𝑉𝑎𝑟 𝑆

𝐸 𝑆3/2 − 𝐸[𝑆]𝐸 𝑆

DMS network: R.H.S increases without bound as t gets large

Means when you write the variance in terms of expectations

operators, everything is finite except for an 𝐸 𝑆2 term in the

numerator. Therefore RHS increases without bound as the

network becomes larger.

II. Variance of net exposures

Result 2. If agent’s preferences put any weight on volatility,

then for large enough network a CCP would be viewed as

beneficial.

23

Finite Case: Tradeoff between mean and variance

24

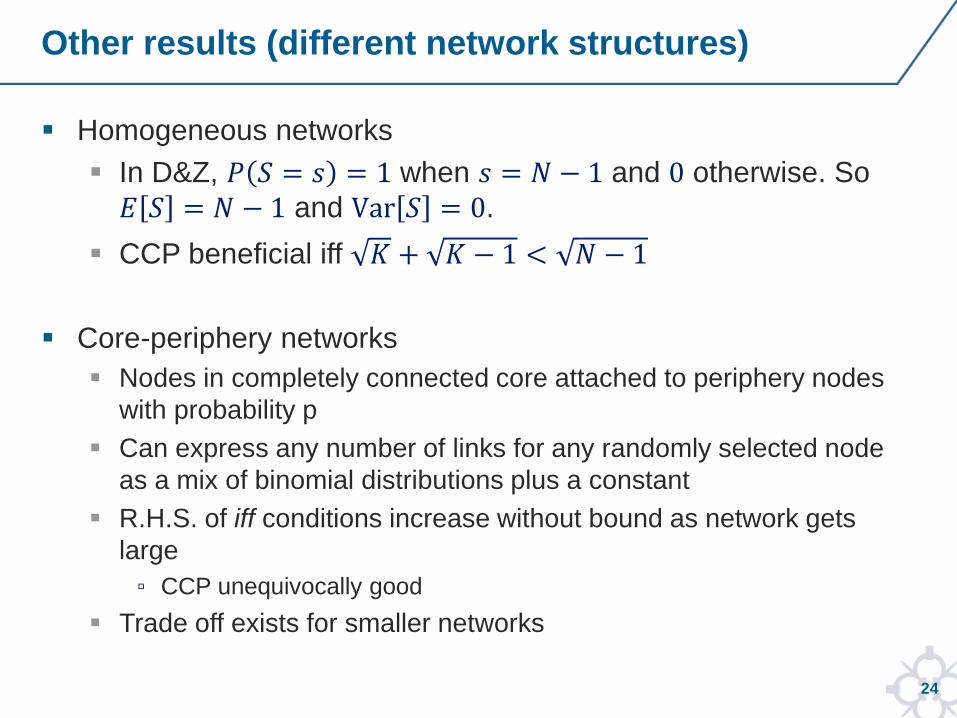

Homogeneous networks

In D&Z, 𝑃 𝑆 = 𝑠 = 1 when 𝑠 = 𝑁 − 1 and 0 otherwise. So

𝐸 𝑆 = 𝑁 − 1 and Var 𝑆 = 0.

CCP beneficial iff 𝐾 + 𝐾 − 1 < 𝑁 − 1

Core-periphery networks

Nodes in completely connected core attached to periphery nodes

with probability p

Can express any number of links for any randomly selected node

as a mix of binomial distributions plus a constant

R.H.S. of iff conditions increase without bound as network gets

large

▫ CCP unequivocally good

Trade off exists for smaller networks

Other results (different network structures)

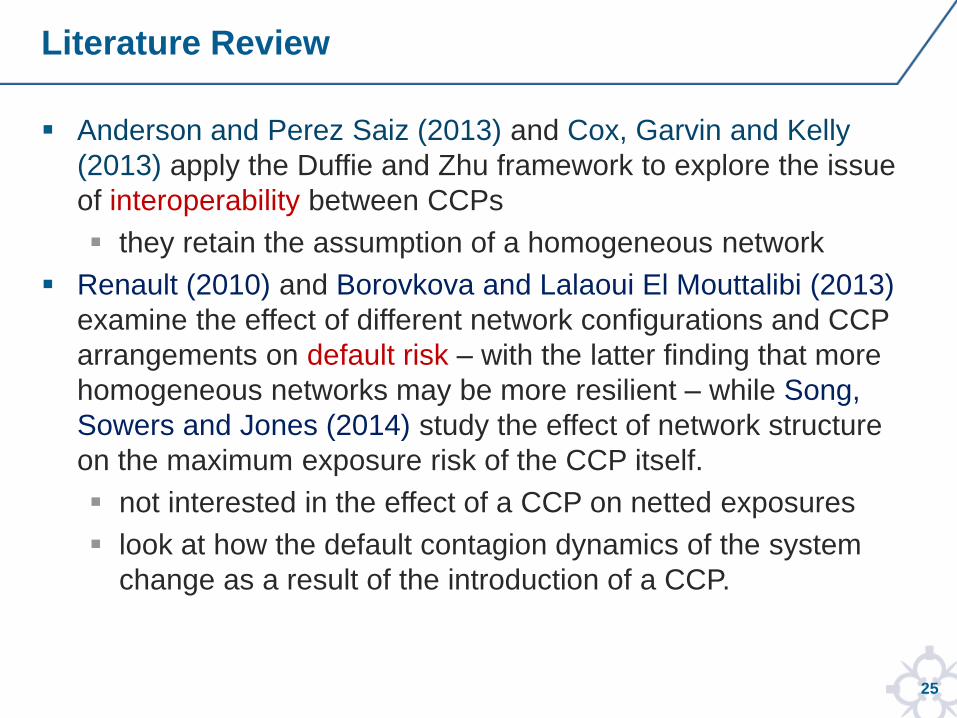

25

Anderson and Perez Saiz (2013) and Cox, Garvin and Kelly

(2013) apply the Duffie and Zhu framework to explore the issue

of interoperability between CCPs

they retain the assumption of a homogeneous network

Renault (2010) and Borovkova and Lalaoui El Mouttalibi (2013)

examine the effect of different network configurations and CCP

arrangements on default risk – with the latter finding that more

homogeneous networks may be more resilient – while Song,

Sowers and Jones (2014) study the effect of network structure

on the maximum exposure risk of the CCP itself.

not interested in the effect of a CCP on netted exposures

look at how the default contagion dynamics of the system

change as a result of the introduction of a CCP.

Literature Review

26

Cont and Kokholm (2014) extends D&Z in a different way to

ours: they relax the assumption of normality of link weights, but

they do not vary the pattern of network links.

In particular, they allow for different distributions and

heterogeneity of risk across asset classes.

They look not only at expected exposures but also tails

(99% quantile of total exposure and 99% quantile of

conditional expectation).

They don’t look at variance.

use a simulation approach with two asset classes; don’t

adopt an analytical approach.

Literature Review

27

Jackson and Manning (2007) and Galbiati and Soramaki (2012)

use different approaches to examine the desirability of tiering—

restricting direct access to the CCP to a limited set of

counterparties.

adequacy of margin requirements

Literature Review

28

In general, the data is being collected from now, but it is not

back-dated, and in particular we don’t have data over the 2008

crisis period

Our approach is applicable to growing networks or in cases of

financial innovation.

Suppose a regulator hosts a market which is expected to

grow (in terms of numbers of participants) over the next few

years.

Our paper provides insight as to whether a CCP is beneficial

or not.

▫ If the network is expected to grow to a very large size, the CCP

is likely to be beneficial.

▫ But if the number of potential participants is bounded at a fairly

low number, then the CCP may provide less efficient netting

than bilateral trading does.

Justification for theoretical approach/ Concluding remarks

29

Having more data is only a panacea if you know how it all fits

together.

Suppose that a regulator can collect the network data for

each individual asset class.

It would then need to fit these together to form the overall

exposure network across all K asset classes.

In reality it will be difficult to identify the nodes in each

network with the same corporate entity.

▫ eg, the part of MegaBank Corp. which trades CDS might be a

different corporate entity to that which trades T-bills.

Our approach allows the regulator not to be concerned

about the identity of each node, but to use the pattern of the

network as a whole.

Justification for theoretical approach/ Concluding remarks

30

Thank you!