Dodd Frank Act 2015 Rule Implementation: Will The World End?

22

Dodd Frank Act 2015 Rule Implementation Will The World End?

-

Upload

jillayne-schlicke -

Category

Real Estate

-

view

271 -

download

0

Transcript of Dodd Frank Act 2015 Rule Implementation: Will The World End?

Dodd Frank Act2015 Rule ImplementationWill The World End?

Intro

• NY Times Article

• YouTube Video

• CFPB website

• Yes, we have new disclosures coming

• No, the world will not end

• David Stevens, President of MBA

• “CFPB has only one mission”

Why We Have Dodd Frank

• Dodd-Frank Wall Street Reform Act

• Signed by President Obama in 2010

• A reaction to subprime RMBS meltdown in the summer of 2008 and predatory lending.

• Laws v. Rules

• Rules have been going into effect one at a time.

• The Act created the CFPB

• Dodd-Frank is massive. Only three sections target our industry: IX, X, and XIV.

Questions:

• As an industry, today, are we ready for this change?

• Every industry hates regulation.

• Every industry wishes regulators would regulate their competitors more often than their own firms.

• We will always complain that we are not ready.

• We will always find a way to make the transition.

Dodd Frank

IX

Creates Qualified Mortgages (2014)

Risk Retention Rule on Non-QMs (2014)

Ability to Repay (2014)

2

X

Creates the CFPB (2010)

XIV

Raises the bar on bank LOs (2014)

Attacks predatory lending “steering” (2011)

Section 1419Consumer Disclosures (2015)

Questions:

• Are we explaining the benefits of Dodd Frank Act to our Agents and Lenders?

• Dodd Frank is polarizing. People either love it or hate it. And people who hate it are more vocal. Our job is to just help them through the transition. You’re like a counselor and your patient won’t leave the bum.

• Avoid websites that spread hyperbole and fear

Questions:

• We are still finding Agents/Lenders that are not aware of CFPB

• Realtors are almost 100% clueless.

• Lenders who are not aware are lenders who…

• Aren’t in a position of power

• Are new to the industry and not originating.

• Aren’t focused on compliance

• Are not loan originators

Questions:

•How will CFPB affect transactions that do not involve a Lender:• cash

• RESPA only applies to transactions that contain a federally-related loan. Follow all other laws you currently follow RE cash transactions.

• seller carry-backs

• YES There are some new rules re: seller financing.

• lease with option to purchase

• THIS IS THE MOST PROBABLY AREA FOR LEGAL ACTION

Seller Financing• Seller financers that engage in a minimum number of

transactions are considered creditors under the Truth in Lending Act (TILA). Specifically, seller financers would be considered creditors if they extend credit secured by a dwelling six or more times in the preceding calendar year, or extend more than one high-cost mortgage in any 12-month period.

• Accordingly, such seller financers are excluded from the definition of loan originators for purposes of the compensation provisions unless they use table funding. In addition, the rule contains two additional special exclusions from the compensation, steering, qualification, and identification provisions for certain seller financers. These exceptions are:

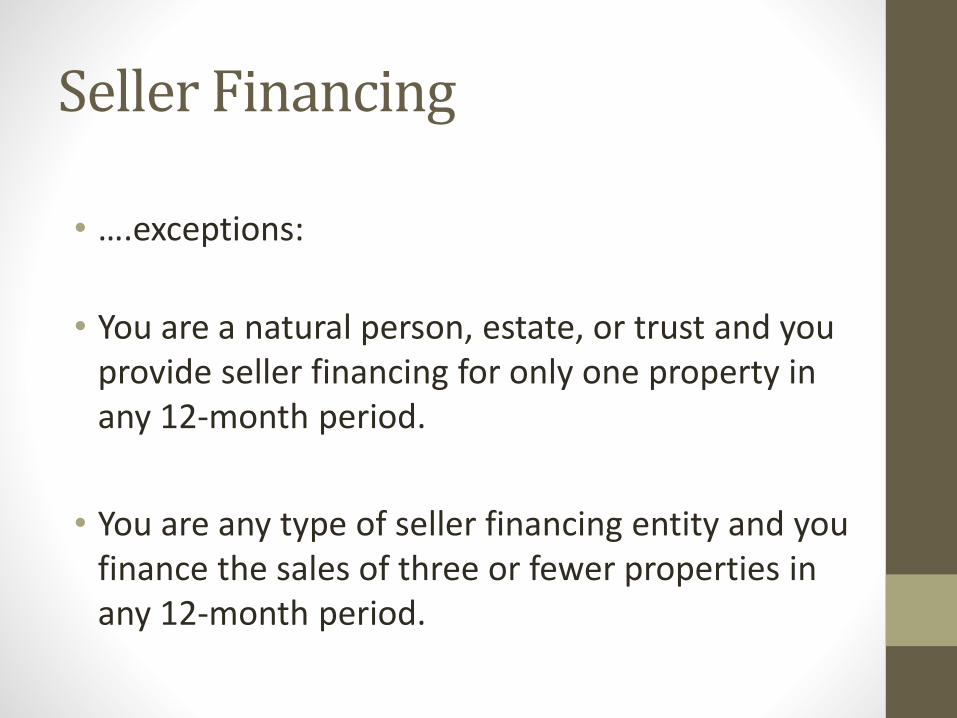

Seller Financing

• ….exceptions:

• You are a natural person, estate, or trust and you provide seller financing for only one property in any 12-month period.

• You are any type of seller financing entity and you finance the sales of three or fewer properties in any 12-month period.

Considerations• Focus on the positive: This will help consumers

understand loan programs and fees.

• You can be a resource for Realtors and consumers.

• Getting the docs in the hands of borrowers in advance of consummation (signing documents) is great idea.

• This gives consumers a chance to ask questions in advance.

• If the lender screws up? Then the transaction is delayed. Lenders will not want to screw up. This will motivate them to provide accurate and honest information on their final disclosures

• We may see most lenders preparing the HUD I (Closing Disclosure) because they are responsible for the content.

Who Provides the Closing Disclosure: • Under the final rule, the creditor is responsible

for delivering the Closing Disclosure form to the consumer.

• A creditor may use settlement agents to provide the disclosure, provided the settlement agent complies with the requirements of the rule, and the creditor must ensure that the Closing Disclosure is provided in accordance with the rule.

Total Interest Percentage:

P and I x by loan term

TOTAL PAYMENTS

Subtract from the total^ the principal amount of loan

= all the interest.

Principal loan amount divided by interest = %

MUST add in the interim interest

Closing Disclosure Timing

• The creditor must provide the Closing Disclosure to the consumer at least three business days before the consumer closes on the loan.

• If there are changes to the Closing Disclosure between the time it is issued and closing, depending on the nature of the change, the creditor must provide an updated Closing Disclosure with another three-business-day waiting period, or simply provide an updated Closing Disclosure by closing.

Changes Requiring an Updated Closing Disclosure & Additional 3 Day Wait:

(1) changes to the APR greater than 1/8 of a percent (or 1/4 of a percent for loans with irregular payments or periods),

(2) changes to the loan product, or

(3) the addition of a prepayment penalty.

Less-significant changes can be disclosed on an updated Closing Disclosure without the need for an additional three-business-day waiting period.

Definition of “Business Day”

• Consistent with the existing requirement to provide final Truth in Lending Disclosures to a consumer at least three business days before closing, the final rule uses the special definition of "business day," which is any day other than Sundays and certain legal public holidays.

Rescission is extended….

• If the required rescission notice or material TILA disclosures are not delivered or if they are inaccurate, the consumer’s right to rescind may be extended from three days after becoming obligated on a loan to up to three years.

Rescission rights after the three-business-day rescission period (closed-end credit only):

• The disclosed finance charge is considered accurate if it does not vary from the actual finance charge by more than one-half of 1 percent of the credit extended or $100, whichever is greater.

• The disclosed finance charge is considered accurate if it does not vary from the actual finance charge by more than 1 percent of the credit extended for the initial and subsequent refinancings of residential mortgage transactions when the new loan is made at a different financial institution. (This excludes high-cost mortgage loans subject to section 1026.32, transactions in which there are new advances, and new consolidations.)

Guide to rescission

• http://files.consumerfinance.gov/f/201308_cfpb_tila-narrative-exam-procedures.pdf

• Page 32

Rescission rights in foreclosure:

• The disclosed finance charge is considered accurate if it does not vary from the actual finance charge by more than $35.

• Overstatements are not considered violations.

• The consumer can rescind if a mortgage broker fee that should have been included in the finance charge was not included.

• Jillayne SchlickeCE Forward, Inc. dba [email protected]