DOCUMENT RESUME ED 241 774 AUTHOR Guidelines for Management Consulting Programs for

219

DOCUMENT RESUME ED 241 774 CE 038 578 AUTHOR Vaughan, Gary L. TITLE Guidelines for Management Consulting Programs for Small-Scale Enterprise. Appropriate Technologies for Development.. Manual M-14. INSTITUTION' Peace Corps, Washington, DC. Information Collection and Exchange Div. PUB DATE Dec 81 CONTRACT 81/487-3740 NOTE 229p. PUB TYPE Guides - Classroom Use - Guides (For Teachers) (052) EDRS PRICE DESCRIPTORS MF01/PC10 Plus Postage. Annotated Bibliographies; *Business Administratioi; Case Studies; Check Lists; *Developing Nations; Entrepreneurship; Guidelines; Instructional Materials; Postsecondary Education; Program Descriptions; Program Development; Program Guides; Program Implementation; Questionnaires; Records (Forms); Rural Areas; *Rural Development; Rural Education; *Small Businesses; Technical Assistance; Volunteers; Volunteer Training ABSTRACT This manual is designed to assist management consultants in working with small-scale entrepreneurs in developing countries. Addressed in an overview ,of the small-scale enterprise (SSE) are: the role of the SSE.in third world development, problems of SSEs, and target firms. The second chapter deals with various forms of management assistance to SSEs, including general considerations in management consulting and program approaches to SSE management assistance. Examined in a discussion of management assistance to target firms are the implementation experience of the Tulua Management.Consulting Program in Colombia, guidelines for seminars for SSE managers and employees, suggestions for providing consulting assistance to target firms, and work related to management consulting. Appendixes to the manual include sample seminar and teaching aids, aids for conducting a management consultancy, and resources for management consulting to SSEs. (MN)' *********************************************************************** * Reproductions supplied by EDRS are the best that can be made * * from the original document. * ***********************************************************************

Transcript of DOCUMENT RESUME ED 241 774 AUTHOR Guidelines for Management Consulting Programs for

DOCUMENT RESUME

ED 241 774 CE 038 578

AUTHOR Vaughan, Gary L.TITLE Guidelines for Management Consulting Programs for

Small-Scale Enterprise. Appropriate Technologies forDevelopment.. Manual M-14.

INSTITUTION' Peace Corps, Washington, DC. Information Collectionand Exchange Div.

PUB DATE Dec 81CONTRACT 81/487-3740NOTE 229p.PUB TYPE Guides - Classroom Use - Guides (For Teachers) (052)

EDRS PRICEDESCRIPTORS

MF01/PC10 Plus Postage.Annotated Bibliographies; *Business Administratioi;Case Studies; Check Lists; *Developing Nations;Entrepreneurship; Guidelines; InstructionalMaterials; Postsecondary Education; ProgramDescriptions; Program Development; Program Guides;Program Implementation; Questionnaires; Records(Forms); Rural Areas; *Rural Development; RuralEducation; *Small Businesses; Technical Assistance;Volunteers; Volunteer Training

ABSTRACTThis manual is designed to assist management

consultants in working with small-scale entrepreneurs in developingcountries. Addressed in an overview ,of the small-scale enterprise(SSE) are: the role of the SSE.in third world development, problemsof SSEs, and target firms. The second chapter deals with variousforms of management assistance to SSEs, including generalconsiderations in management consulting and program approaches to SSEmanagement assistance. Examined in a discussion of managementassistance to target firms are the implementation experience of theTulua Management.Consulting Program in Colombia, guidelines forseminars for SSE managers and employees, suggestions for providingconsulting assistance to target firms, and work related to managementconsulting. Appendixes to the manual include sample seminar andteaching aids, aids for conducting a management consultancy, andresources for management consulting to SSEs. (MN)'

************************************************************************ Reproductions supplied by EDRS are the best that can be made *

* from the original document. *

***********************************************************************

INFOFMTICN CDLIECTICti fi maw=

Peace Corps' Information Collection s Exchange (takkgssiestablished so that the strategies and technologies devel-oped by Peace Corps Iblunteers, theft co- workers, and theircounterparts could be made available to the wide range ofdemplormeit organizations and individual workers who mightfind them useful. Training guides, curricula, lesson plans,project reports, annuals and other Peace Corpe-generatedmaterials developed in the field are collected and reviewed.Sore are reprinted "as is"; others provide a source of fieldbased information for the production of manuals or for re-search in particular program areas. Materials that you sub-mit to the Information Collection &Exchange thus becomepart of the Peace Corps' larger contribution to develcsirent.

Information about ICE publications and services is availablethrough:

Peace CorpsInformation Collection ExchangeOffice of Training and Program Support806 Connecticut Avenue, N.W.Washington, D.C. 20526

Add your experience to the ICE Resource Center. Send ra-terials that you've prepared so that we can share themwith others working in the development field. Your tech-nical insights 'serve as the basis for the generation ofICE manuals, reprints and resource packets, and alsoensure that ICE is providing the most updated, innovativeproblernsolving techniques and information available toyou and your fellow development workers.

Peace Corps3

GUIDELINES FOR MANAGEMENT

CONSULTING PROGRAMS FOR

SMALL-SCALE ENTERPRISE

Written by

Gary L. Vaughan

Peace Corps

Information Collection and Exchange

Manual M-14

December, 1981September 1983

4

c'

ArAir

ti

GUIDELINES FOR MANAGEMENT CONSULTING PROGRAMSFOR SMALL-SCALE ENTERPRISEDecember, 1981

0Prepared for the Peace Corpsby Gary V4ughan underContract No. 81/487-3740

Available through:Peace Corps, ICE806 Connecticut Avenue, N.W.Washington, D.C. 20526

/ 5

PREFACE

This manual is designed to,assist management consul-tants working with small-scale entrepreneurs in developingcountries. It also contains material of interest to PeaceCorps or developing country programmers who plan devdlopmentprojects for the small-scale enterprise (SSE) sector. Thebulk of the manual deals with management assistance to onetype of SSE in,developing countriesz owner-operated small in-dustrial firms,. Much of this emphasis flows from my pastfield experience as a Peace Corps Volunteer in Colombia.Nonetheless, many of the tools and techniques explained inthis handbook may have applicability to other types of SSEsor even to other forms of business organization throughoutthe Third World.

In writing this, I have synthesized a growing body ofreference material in small-scale enterprise development- -some of which is presently available to Peace Corps Volunteersand staff through Peace Corps' office of Information Collec-tion and Exchange (ICE) in Washington. This manual providesthe reader with insights into answering the following ques-tions:

(1) Why are SSEs important. in Third World development?.

(2) What problems are commonly faced by the small-scale entrepreneur?

(3) What role can management consultants play in help-ing small-scale entrepreneurs -solve such problems,thereby boosting SSEs' productivity and profitabil-ity?

(4) what kinds of development programs or deliverysystems are effective in planning for, training,and supporting SSE management consultants?How can such programs' effectiveness be evaluated?

(5) Finally, how-does a management consultant go aboutassisting a small business in the Third World, andwhat techniques (in human relations and in variousareas of business administration) will help the -

consultant improve both the quality and accept-ability of his advide to the small entrepreneur?

This manual offers answers to all of these questionsin a practical, handbook format. Chapter One deals withquestions (1) through (3), and provides ttlp reader withbadcground information on how SSEs, with the aid of manage-ment consultants, may play an important role in developingThird World economies. In addressing question (4), ChapterTwo briefly examines a variety of programs which have at-tempted to boost SSE productivity and profitability throughmanagement consulting assistance. It also sets forth my ownrgcommendation for SSE assistance in the form of a hostcountry Economic Development Intern Program. This programwould train local high school or university graduates to as-sist "target firms" (i.e. those firmg carefully selected forproduction potential) using the tools and techniques out-lined in this book.

From the background information On SSEs provided inthe first two chapters, we move on to a discussion of ap-plied techniques in Chapter Three, and additional sourcesof practical guidance in the Appendices and Selected Bibli-ography. In addressing question (5) above, these sectionsprovide the management consultant with a variety of toolsto help him or her in consulting work--regardless of theprogram methodology chosen. For example, Chapter Three dis-cusses how to organize and teach a seminar'to SSE managersand employees. It examines the use of human relationsskills in building an effective consultant-client relation-ship. This chapter also offers appropriate advice for con-sulting on specific problems in finance and accounting,marketing, personnel management, planning, and other areas.Appendicvk, tc the manual provide additional practical guid-ance to the consultant, such as seminar audiovisual mate-rials, classroom handouts, and case studies, as well asforms useful in planning and executing a consultancy. TheDirectories of Selected Small-Scale Enterprise DevelopmentOrganizations and Information Sources in Appendix III,Exhibit 132: indicate further sources of information for theSSE consultant. Finally, the Selected Bibliography directithe oontultant to a wide array of reference materials onthe subject of SSE promotion.

There are a number of well-written books on smallbusiness administration in industrialized countries and agrowing body of work concerning the promotion of SSEs in theThird World. In writing this manual, I hope'to make furthercontributions to the field by:

41.

translating a number of appropriate concepts andprinciples from modern small business administra-tion in the United States into a methodology forassisting SSEs in developing countries;

reviewing a variety of.recent foreign assistanceprograms which have attempted to promote SSEsthrough the use of management consulting services;

proposing that the "target firm" approach, whencompared to other SSE programs, is a lean and cost-effective means of helping the urban and ruralpoor; and,

providing guidance to the prospective user of this' manual without hampering creativity or initiative.

As the manual's title implies, this handbook offersprogrammatic and technical guidelines so that the reader maydevelop his or her own program, specifically tailored to theneeds and realities of a given developing country. Conse-quently, this reference work is not a self- contained pre-.scriptionfor consulting success. Success will, largely de-pend on the initiative and ingenuity of the user, as wellas on his or her willingness to consult other appropriate,information sources.

A number of people assisted me with the general con-cept 'and content of this manual. Gary Petersen, now a region-al director for the United S ,:ates Small Business Administra-tiol, and Michael J. McGuire, a former Peace Corps colleaguein Colombia, gave me valuable a4,%;ica in designing the "tar-get firm" program outlined in this book. Jose Manuel Arenas,Financial Manager'of the Colombina Candy Company, JeanFrancois Christin, consultant,for the United Nations Indus-trial Development Organization (UNIDO), and Howard Lewis,Peace Corps Volunteer.in Ecuador were also helpful in advis-ing me during the early stages of preparing this manual.I wish to thank the Fundaci6n para el Desarrollo Industrialand my supervisors in Peacb Corps/Colombia, Peter Fraserand William Phelps, for encouraging my work with,SSEs, as.well as the small entrepreneurs of Tulue, Colombia, whoprovided me with the experience necessary to research thisbook. I also gratefully acknowledge the editorial assist-ance of Pirie Gall and Susan Hewes of Peace Corps' Officeof Programming and Training Coordination (OPTC), WilliamPhelps, formerly of Peace Corps' Latin America Regional Office,

iii

8

SZ

and ichael Hirsh, Program and Training Officer for PeaceCorP/Ecuador. This manual would never have been producedwithout their time and patience in editing various draftsof the manuscript. In addition, I would like to acknowledgeall the hard work of the several secretaries who contributedto typing this manual. Finally, I owe a great debt oe'zrati-tude to the late Alonso Lozano Guerrero, former ExecutiveSecretary of the Chamber of Commerct of TuluA, who providedme with the inspiration necessary to write this handbook.

h

This doct.ment does not bear the approval (nor imply such) of theUnited States Agency for Ilternational Development, or any of itsOfficers.

iv

9

TABLE OF CONTENTS

CHAPTER ONE : THE SMALL-SCALE ENTERPRISE'

A. SomeDefinitions

1. What is a "Business"? 12. What is a."gmall-Scale Enterprise"? 13. How Management of Small-Scale Enterprise

Differs from that of Large'arge Enterprise "I' 2

B. The Role of Small-Scale Enterprises inThird World Development

1. Why are Small-Scale Enterprises Important? 52. Promoting the Development of SSEs 6

r.

C. Problems of Small-Scale Enterprises 7

1. Capital 9

2. Marketing 103. Human Resources . 124. Technical Constraints t 145. The General Business Environment 156.`Business Practices 17

D. The Target Firm

CHAPTER TWO : MANAGEMENT ASSISTANCE TO SSE,s

A. Managemert Consulting: GeneralConsiderations

1.9

1. Checklist of Guidelines for Designers. of SSE Consulting Programs 232. Focus and Purpoie of Managem6nt Con-

sultancy 25,3. Interdependence Be..:ween Consulting AY

and Cred±t 274. The Role of Management Consulting

Assistance in a Small-Scale EnterpriseDevelopment Program 28

5: Cross-Cultural Considerations 29

B. Program Approaches to SSE ManageMentAssistance

1. A Brief Overview 332. The Economic Development Intern Program

a. Purpose and General Approach 35

v

10

\' b. Intern win the iitld 36

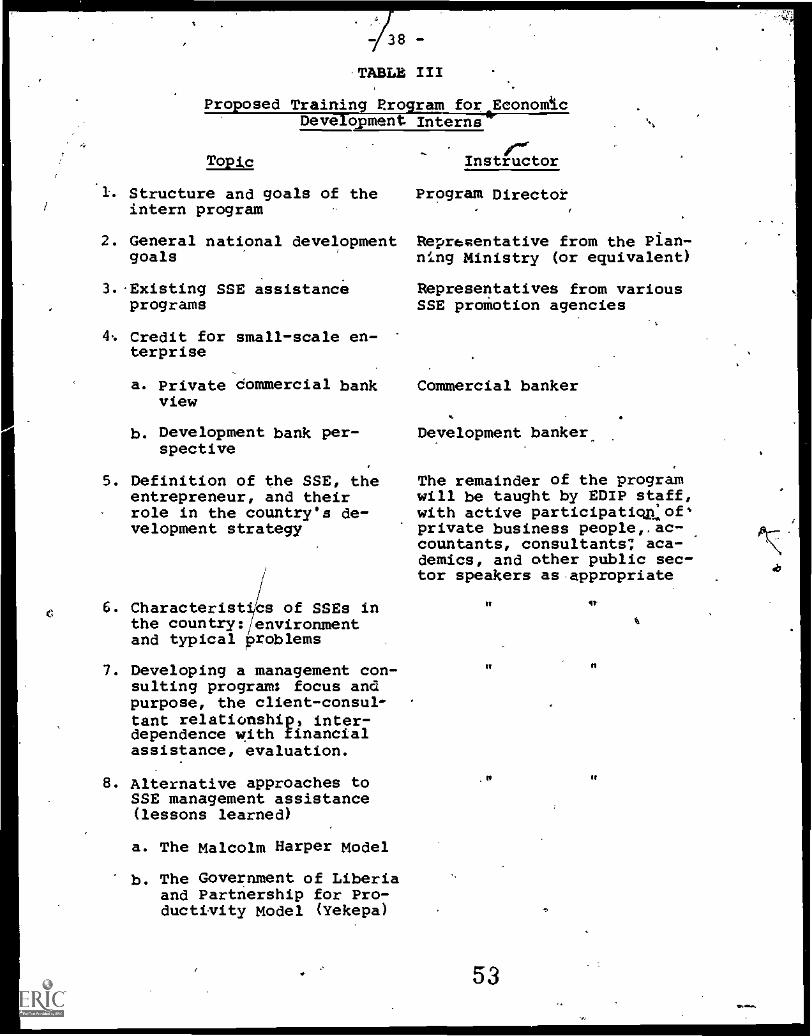

c. Training and Supporting the Interns 37d. Vrogram Organization and Funding 41e. Conclusion . 45

(

.

CHAPTER THREE ; 40:GEMENT ASSISTANCE TO 'TARGETFIRMS

--IN..,

/A. The Tulu& Experience: A Case Study-.

1. Colombia and its Small Business Assistance-Programs

2. Tulu& and its Business Environment ?3. The Tulu& Management Consulting Program

B. Seminars for SSE Managers and Employees

1. Sponsoring and Cooperating Institutions2. Role of the Seminar in a Management

Consulting Program3. Recruitment for the Seminar4. Preparation for the Seminar: Location.

and Teaching' Materials5. Teaching Techniques6. Evaluation of the Seminar and Selection

of Clients-for the Consultancy

474951

57

6264

6668

73

C. Consulting Assistance to Target Firms

1.. Building the Consulting Relationship 772. Planning; the Consultancy 793. Conduct of the Consultancy 834. Final.Recommendations, Followup and

Evaluation 905. Guidelines to Consulting on Specific

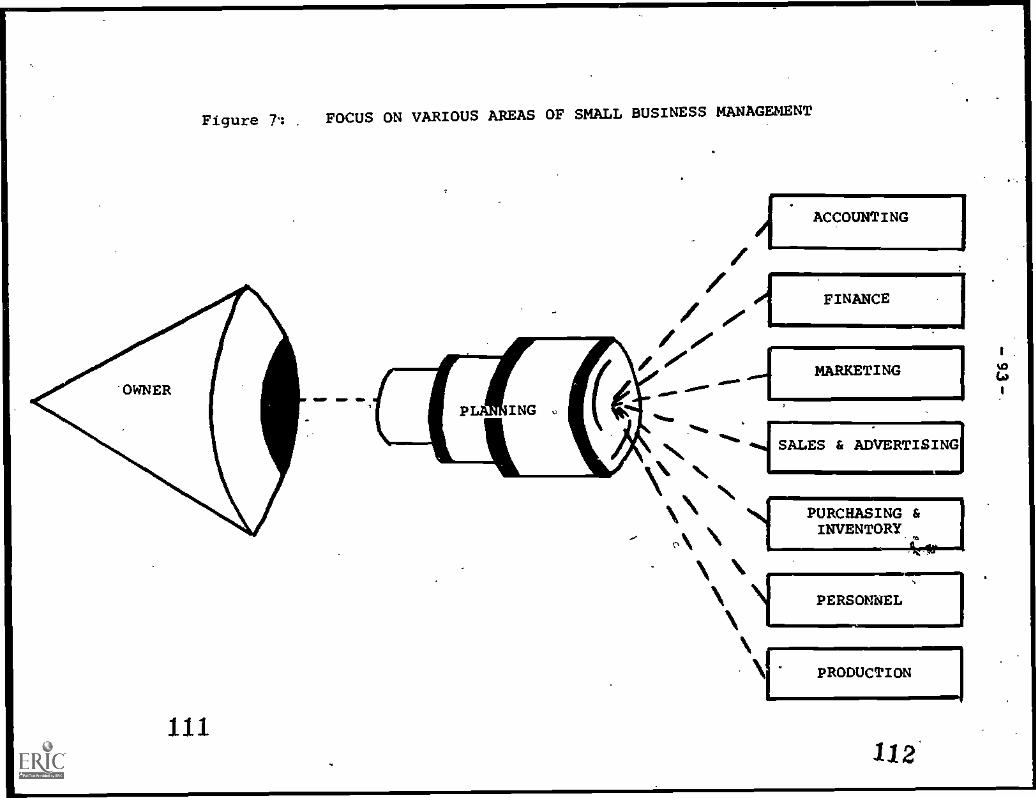

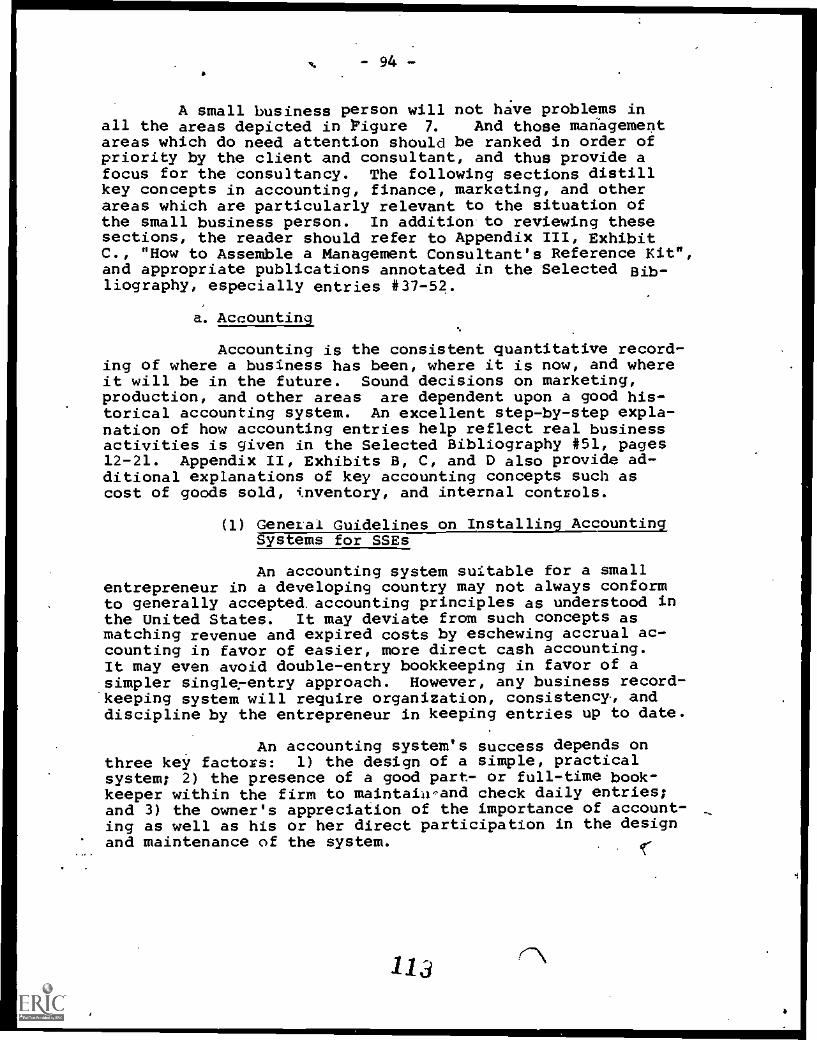

Problems 92a. Accounting 94b: Finance 101c. Marketing and Sales 110d. Purchasing and Inventory 113e. Personnel 119f. Production 124g. Planning 127

D. Work Related to Management Consulting

1. Small Business Cooperatives 1302. Trade Fairs 1323. External Investment Promotion 133

CHAPTER FOUR : CONCLUSION 135

vi

4

APPENDICES

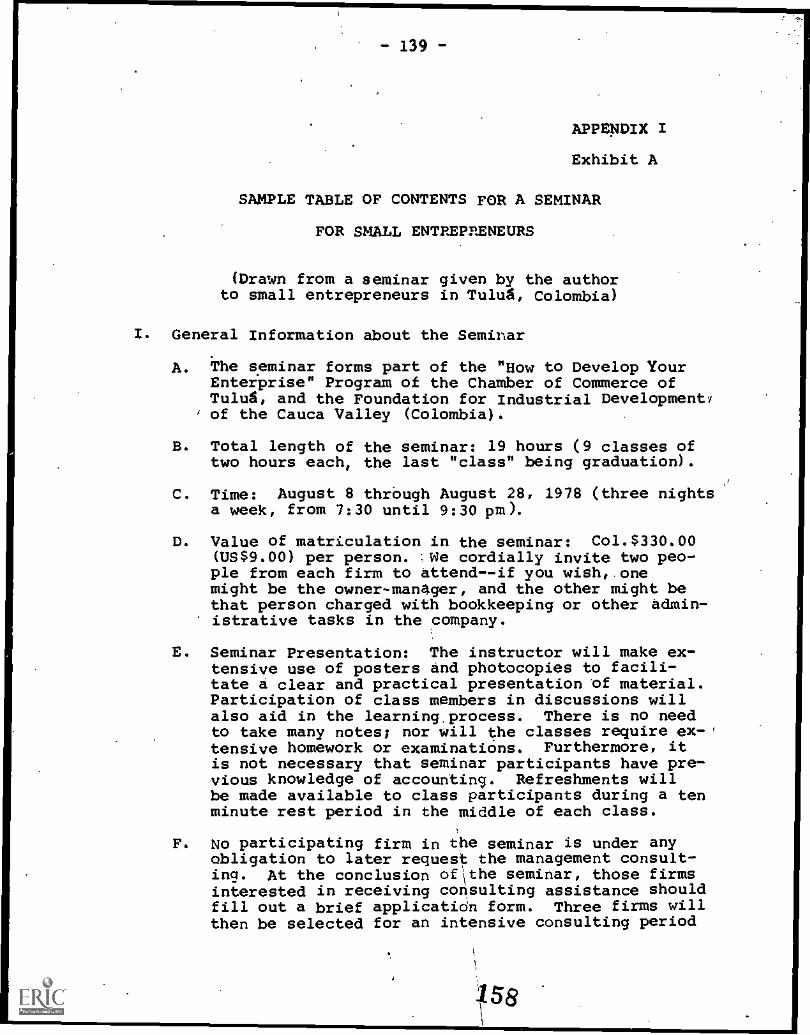

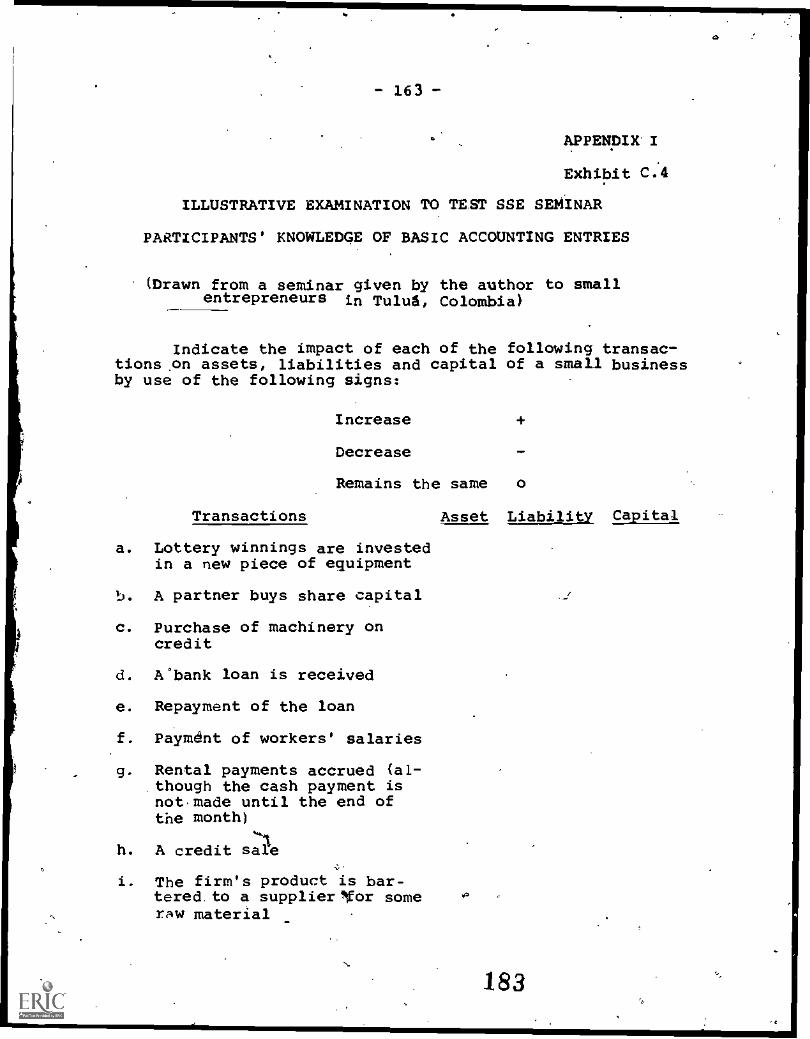

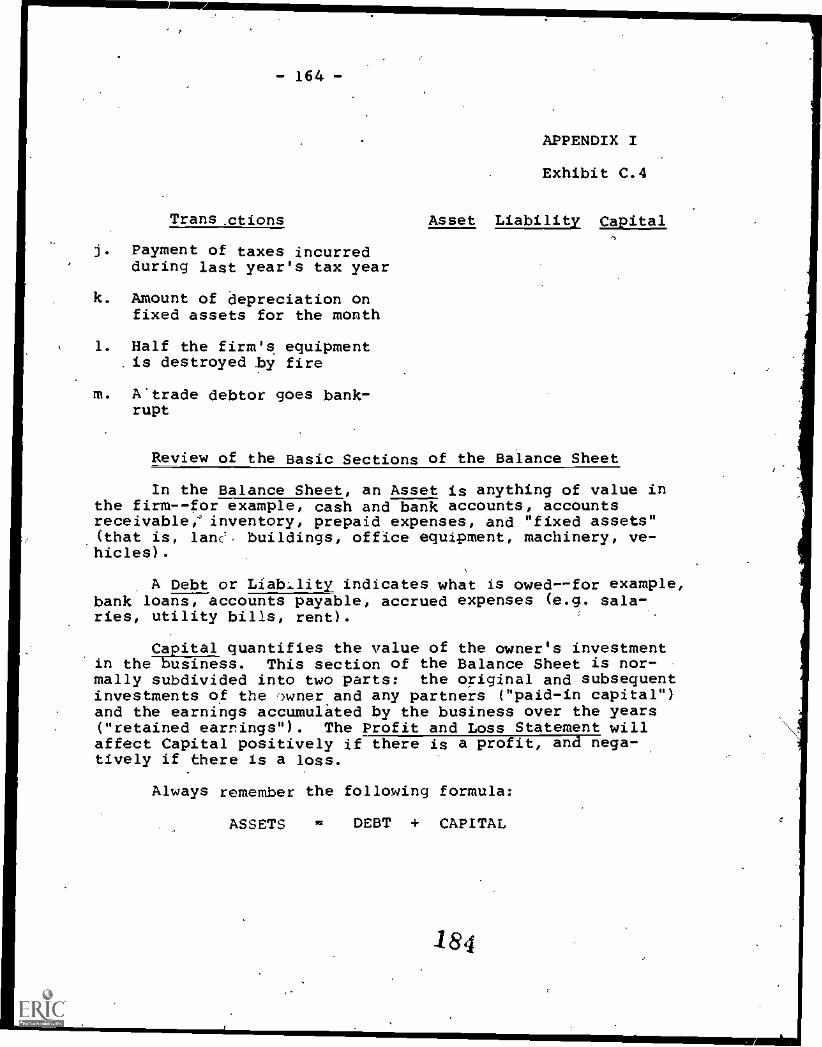

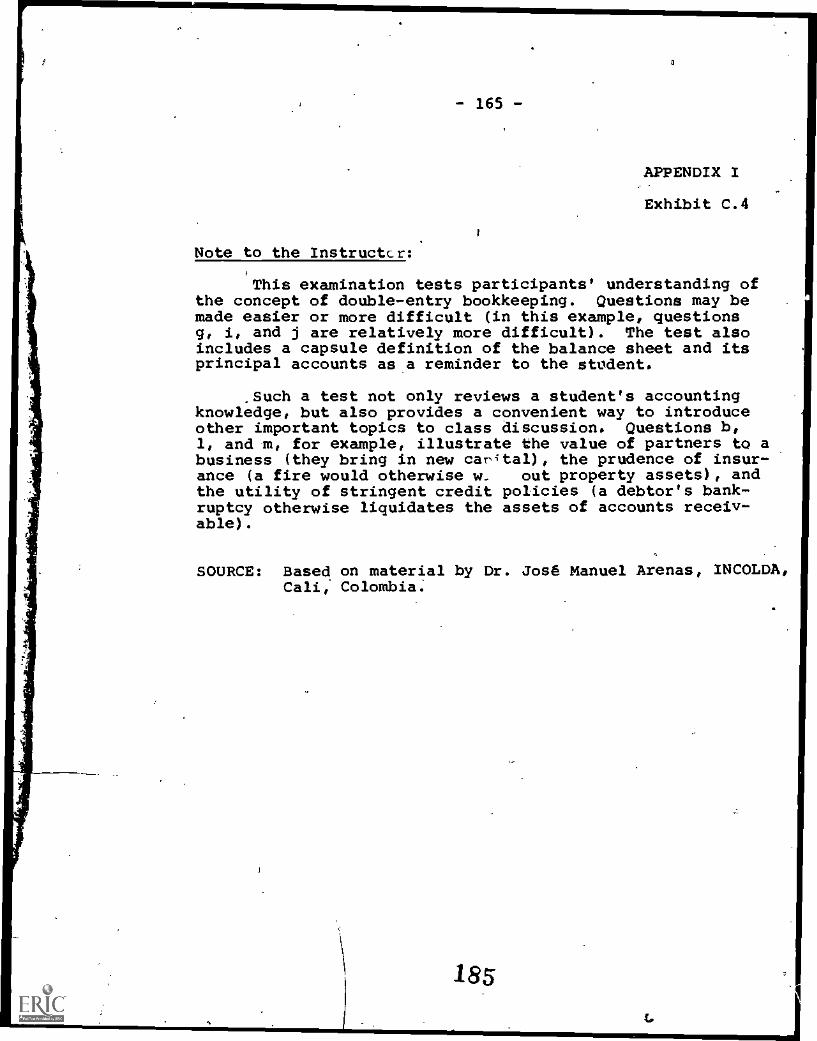

APPENDIX I. SAMPLE SEMINAR AND TEACHING AIDS

A. Sample Table of Contents for aSeminar for Small Entrepreneurs 139

B: Poster or Blackboard Illustrations

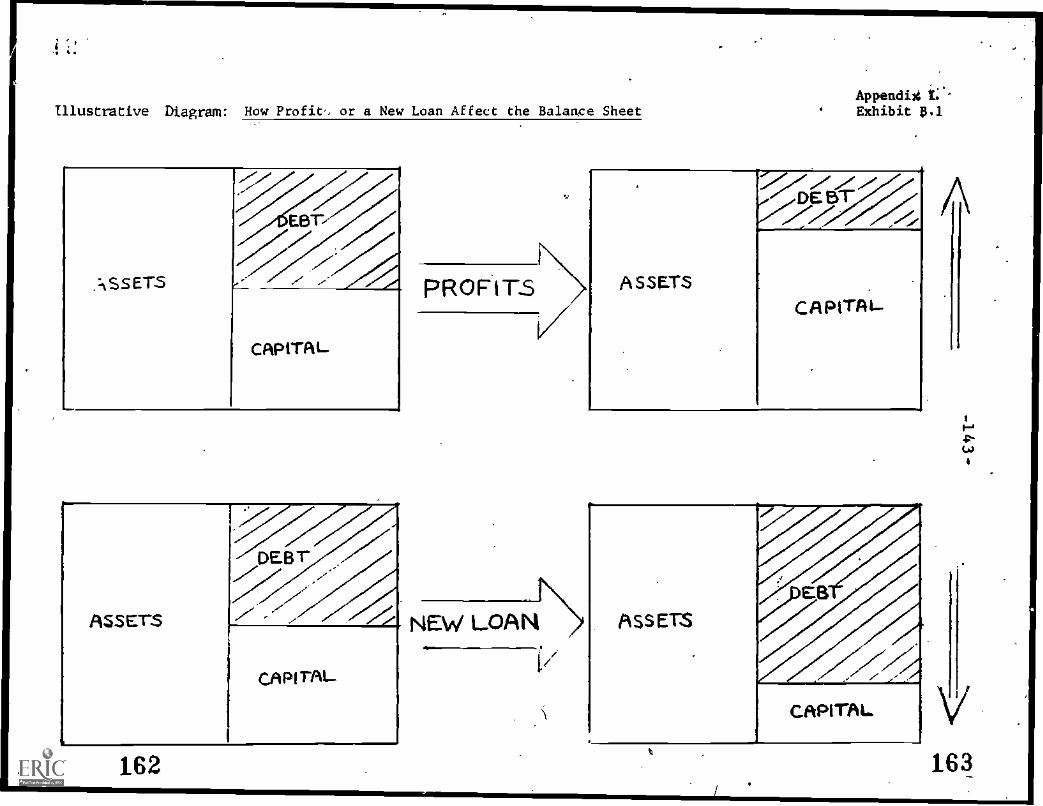

1. Illustrative Diagram: HowProfits or a New Loan canAffect the Balance Sheet

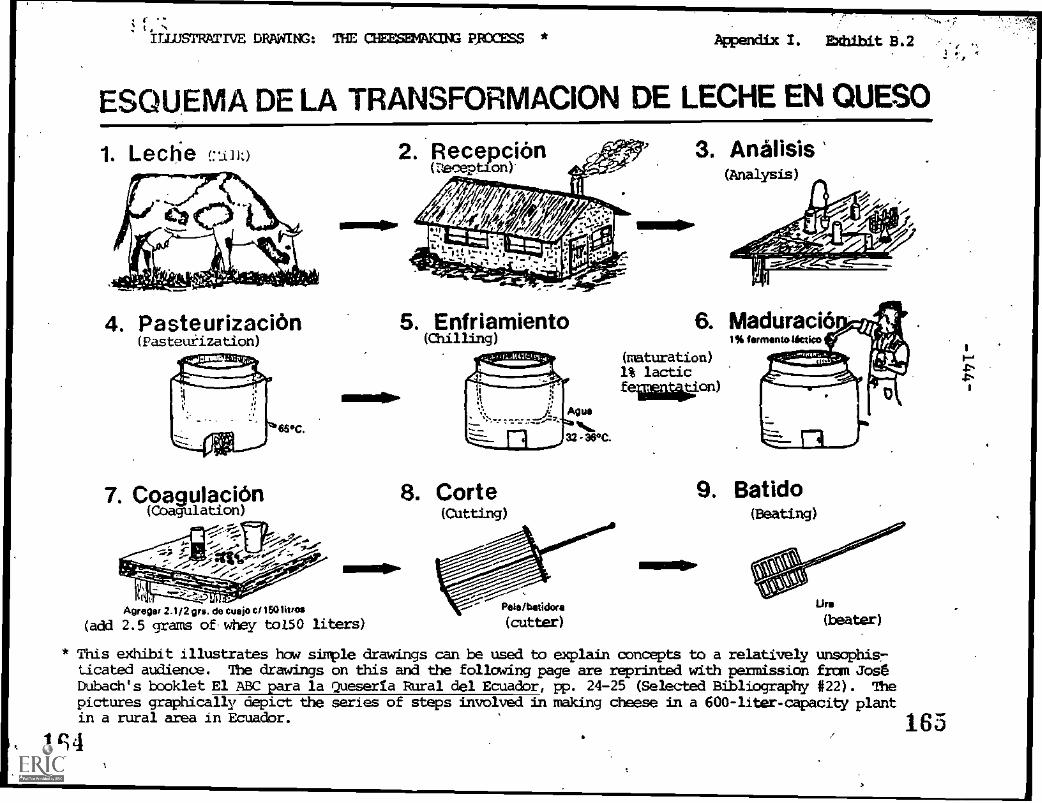

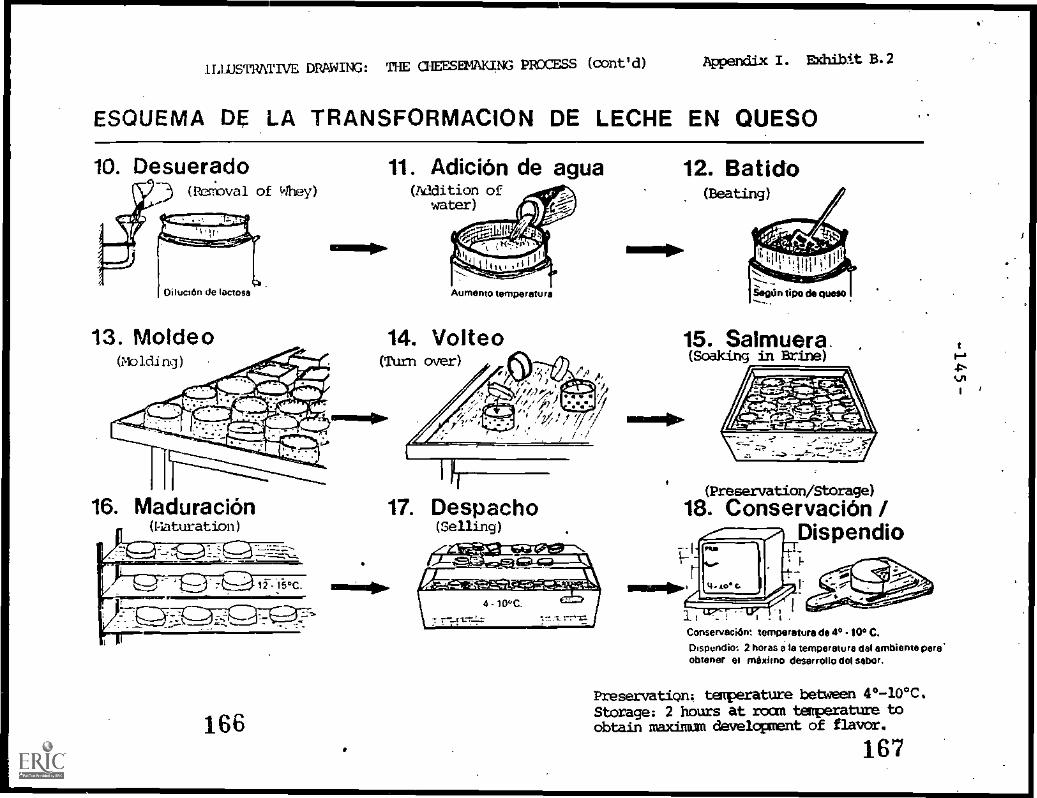

2. Illustrative Drawing: TheCheesemaking Process

Sample Classroom Handouts

1.. Illustrative Case Materialswhich"the Consultant can Usein Seminar Presentations, forSmall Entrepreneurs

.11

143

144

a. Case No. 1: "The CachacoTailor Shop" 147

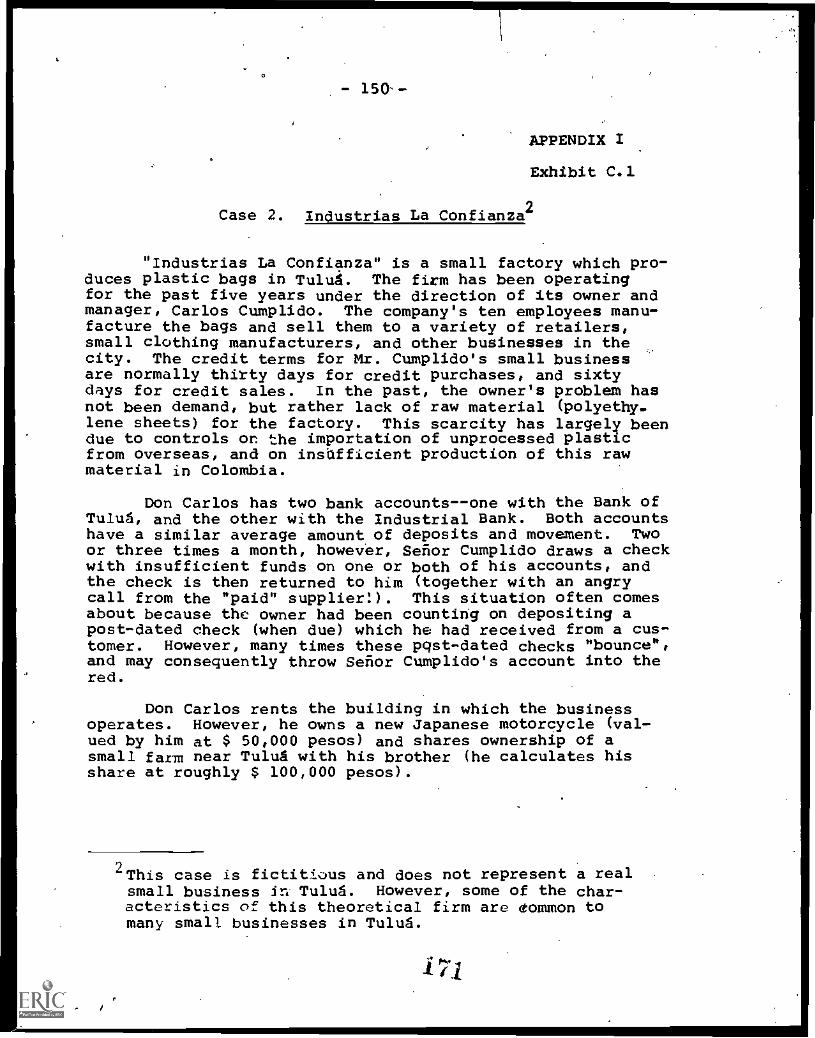

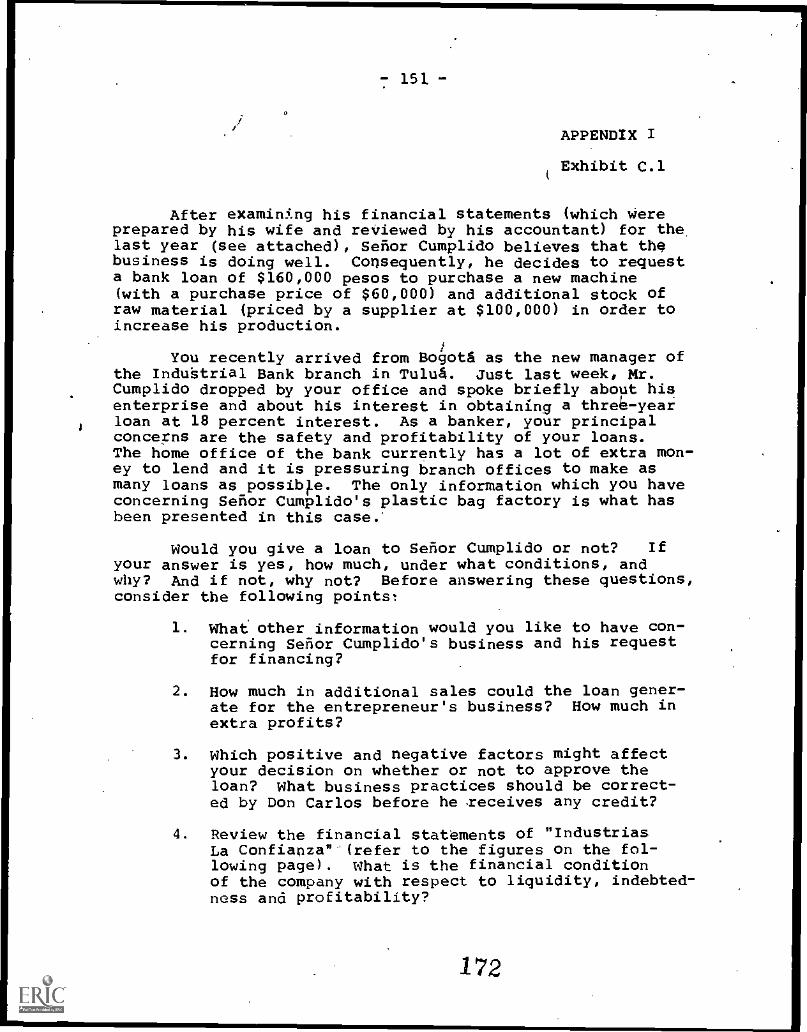

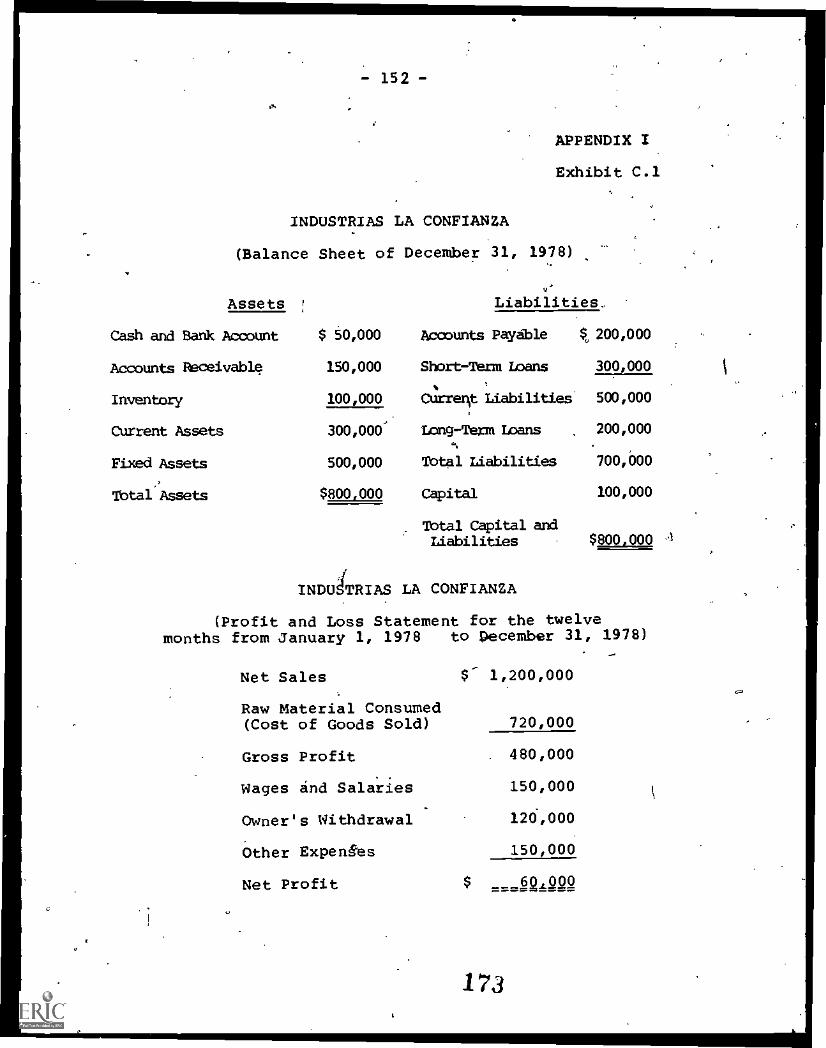

b. Case No. 2 "Industrias'La Confianza" 150

2. Sample Handout. which can beUsed'during a Senina; forSmall Entrepreneurs: TheCalculation and Significanceof Cost of Goods Sold andInventory 155

3. Sample Homework Problem which1d,; /can Test SSE Seminar. Parti-

cipants' Knowledge of Account-ing Controls 159

4. Illustrative-Examinati o n toTest SSE Seminar Participants'Knowledge of Basic AccountingEntries 163

vii 12

APPENDIX II. AIDS IN CONDUCTING A MAAGEMENTCONSULTANCY

A. Pre-Screening Instrument forSelecting Target Firms 167

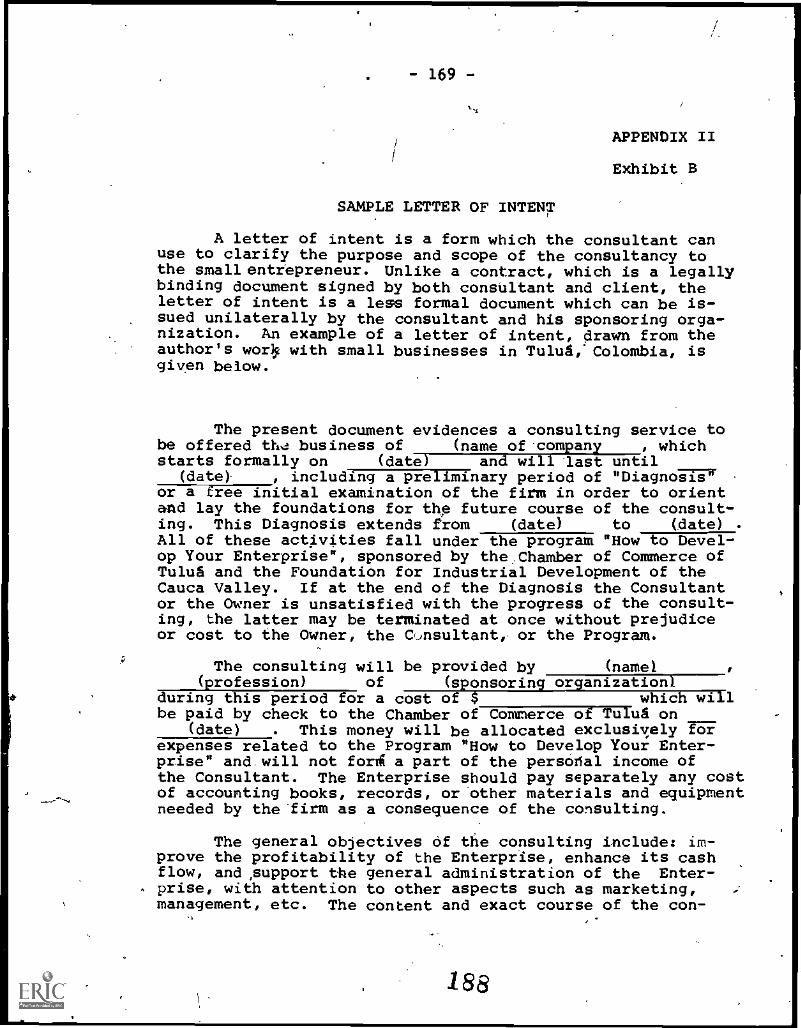

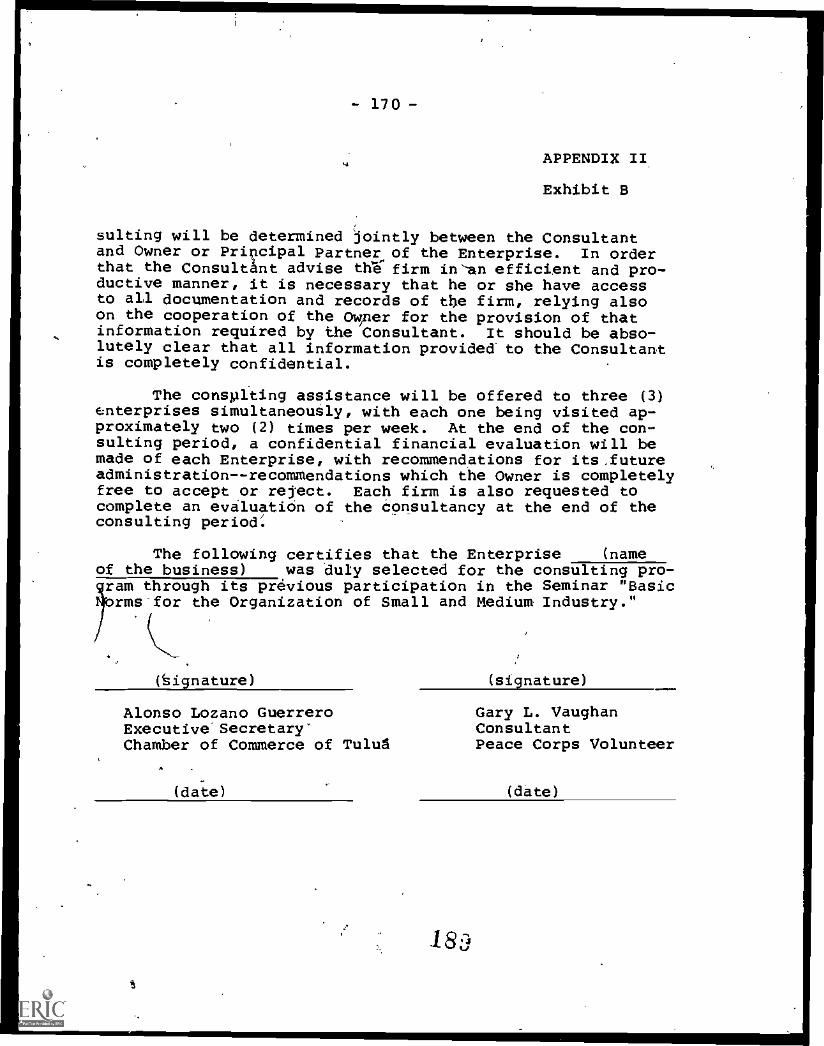

B. Sample Letter of Intent 169

C. Accounting Interview Questionnaire 171

D. How to Build an Effective Consult-ing Relationship by Becoming aBetter Listener 175

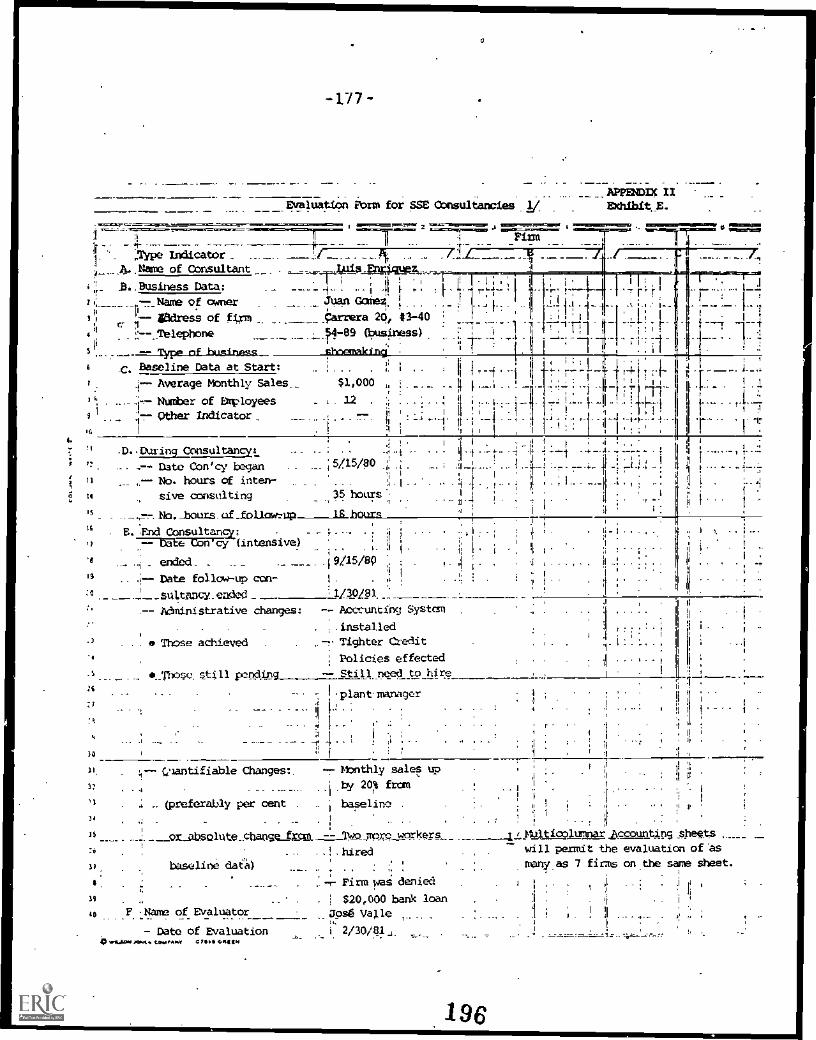

E. Evaluation Form for SSE Consul-, . tancies 177

APPENDIX III. RESOURCES FOR MANAGEMENT CONSULTINGTO SSEs

A. A Review of Selected SSE Manage-ment Assistance Programs 179

B. Directories of Selected SSE Develop-ment Organizations and InformationSources 187

.C. How to Assemble a Management Con-sultant's Reference Kit 195

D. Selected Bibliography 199

13viii

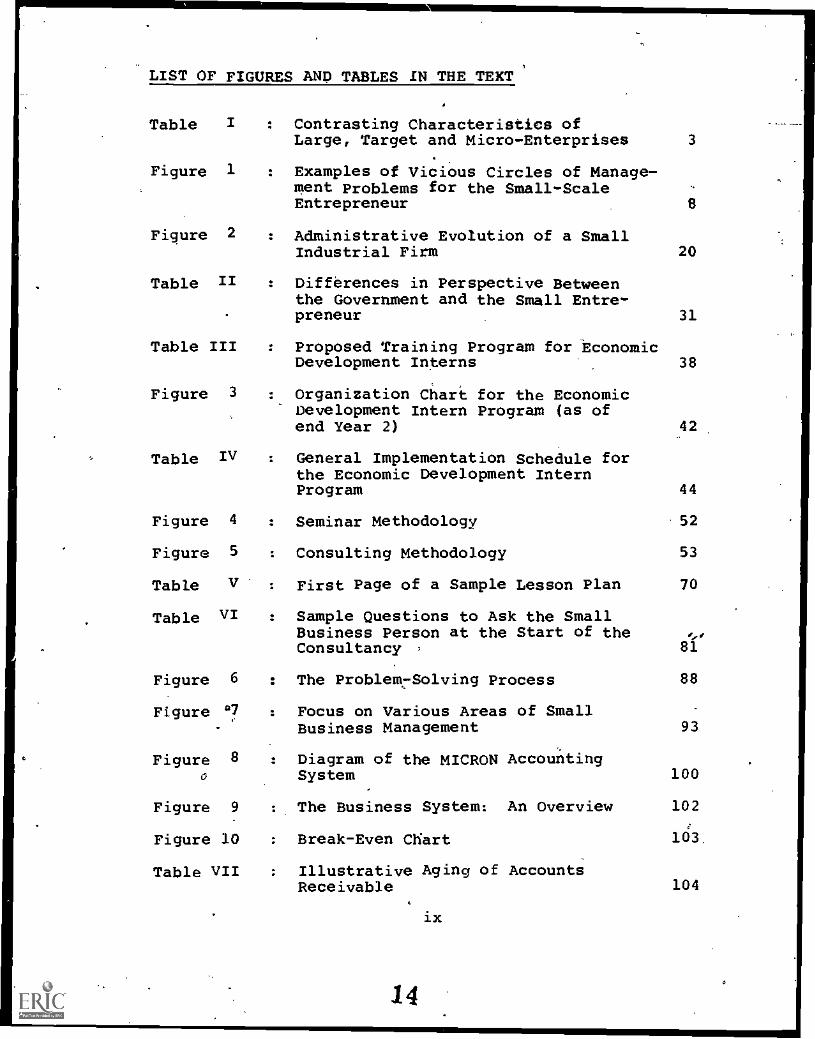

LIST OF FIGURES AND TABLES IN THE TEXT

Table I

Figure 1

Figure 2

Table II

Table III

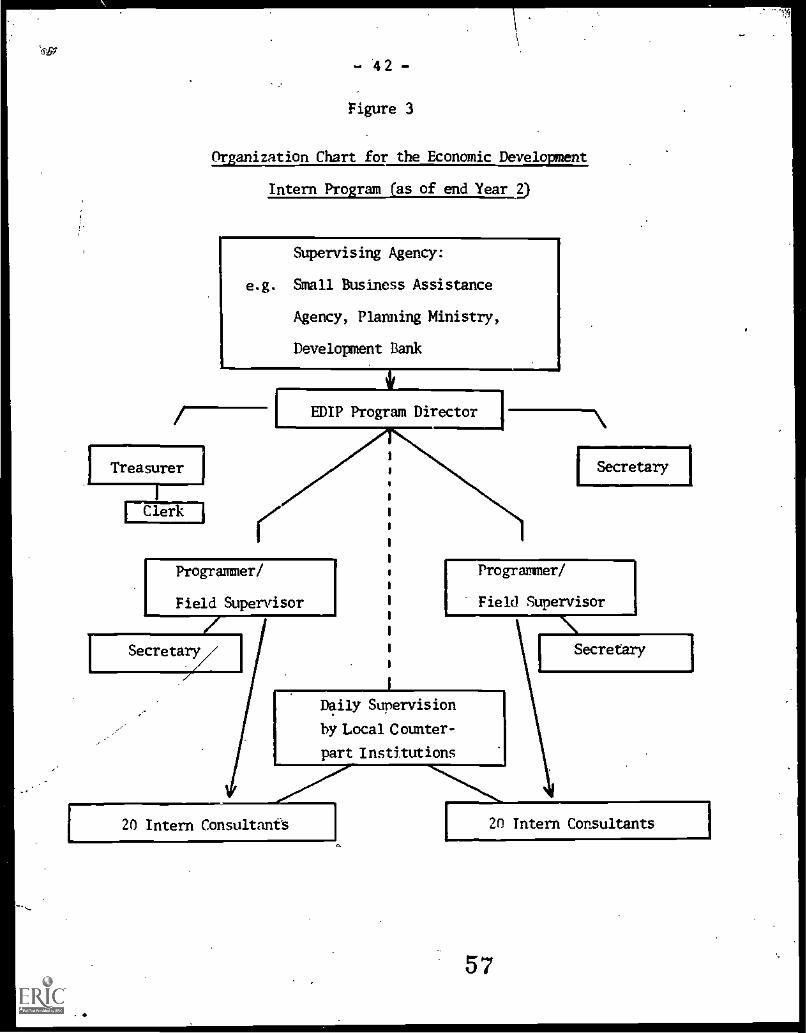

Figure 3

Table IV

Figure

Figure 5

Table V

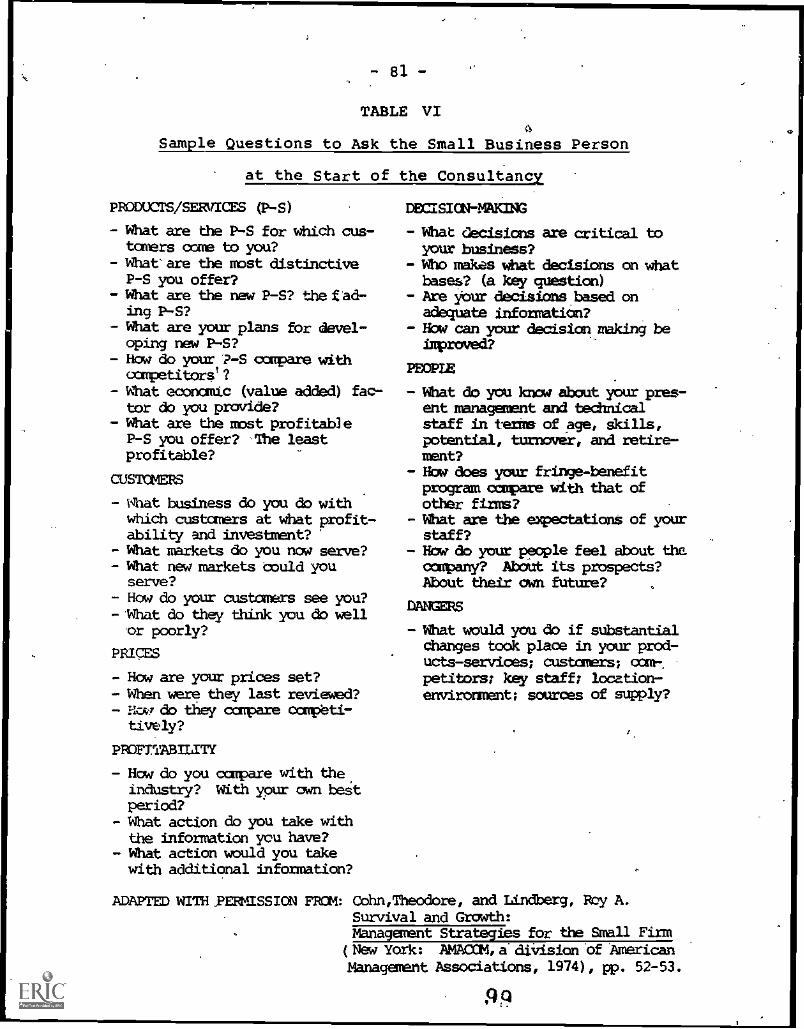

Table VI

Figure 6

Figure p7

Figure0

Contrasting Characteristics ofLarge, Target and Micro-Enterprises 3

Examples of Vicious Circles of Manage-ment Problems for the Small-ScaleEntrepreneur 8

Administrative Evolution of a SmallIndustrial Firm 20

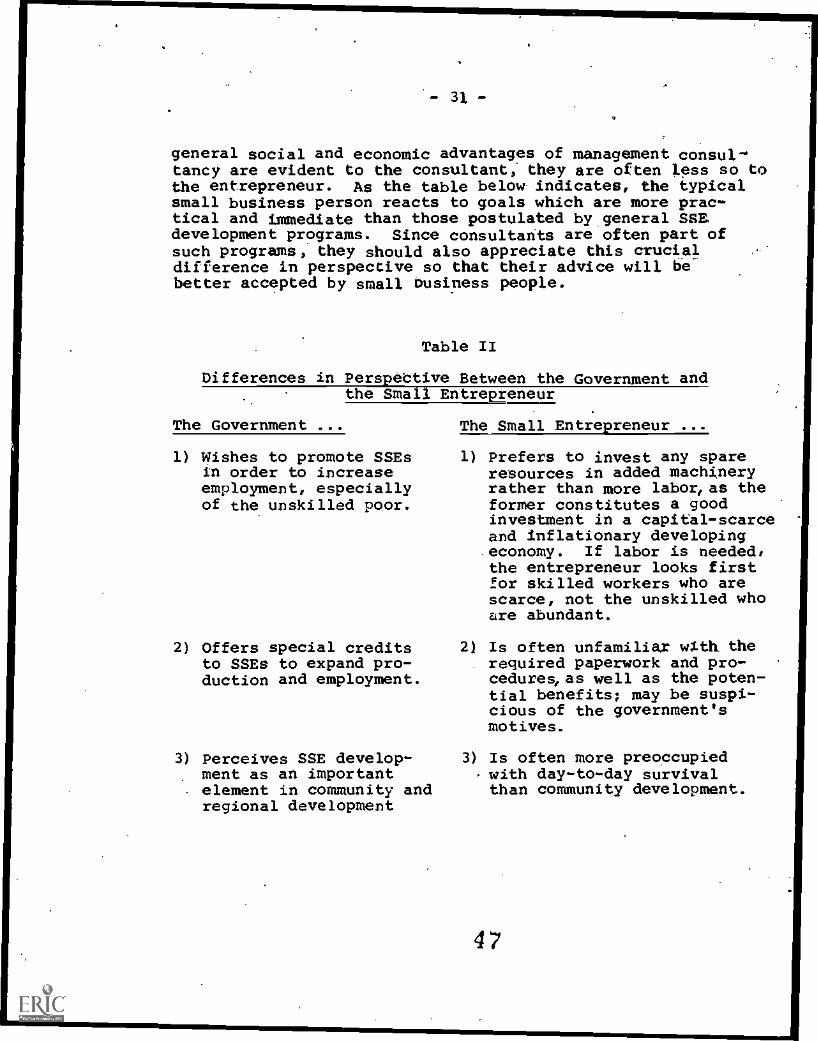

Differences in Perspective Betweenthe Government and the Small Entre-preneur 31

Proposed Training Program for EconomicDevelopment Interns 38

Organization Chart for the EconomicDevelopment Intern Program (as ofend Year 2) 42

General Implementation Schedule forthe Economic Development InternProgram 44

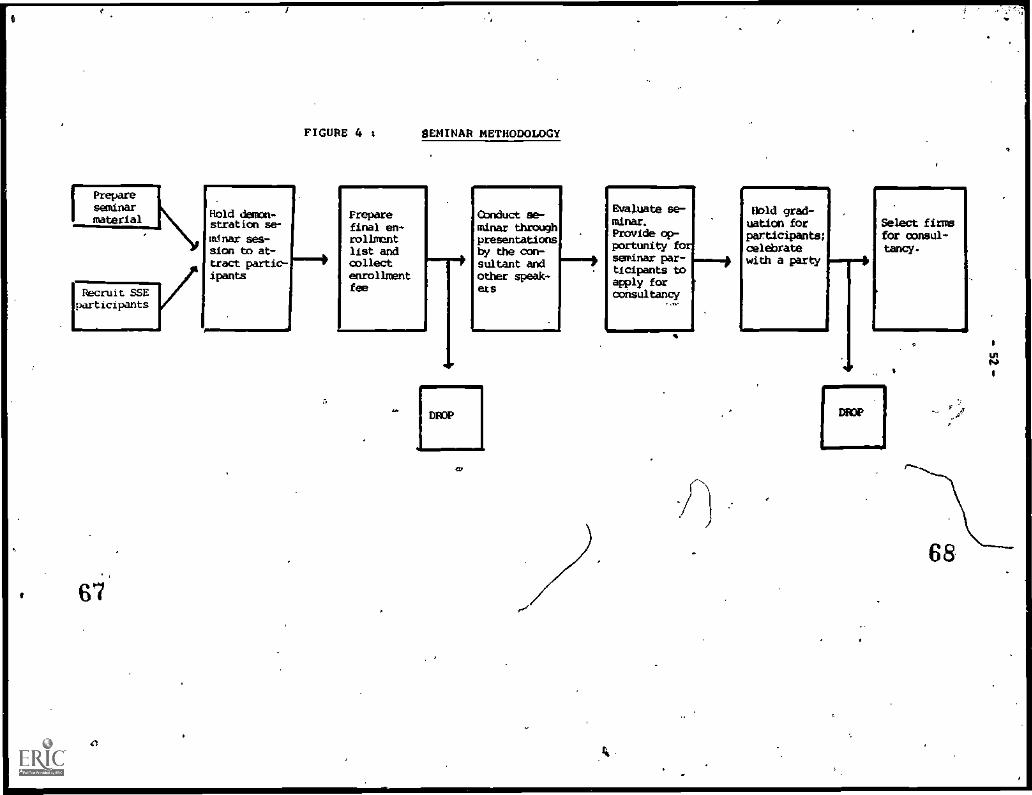

: Seminar Methodology 52

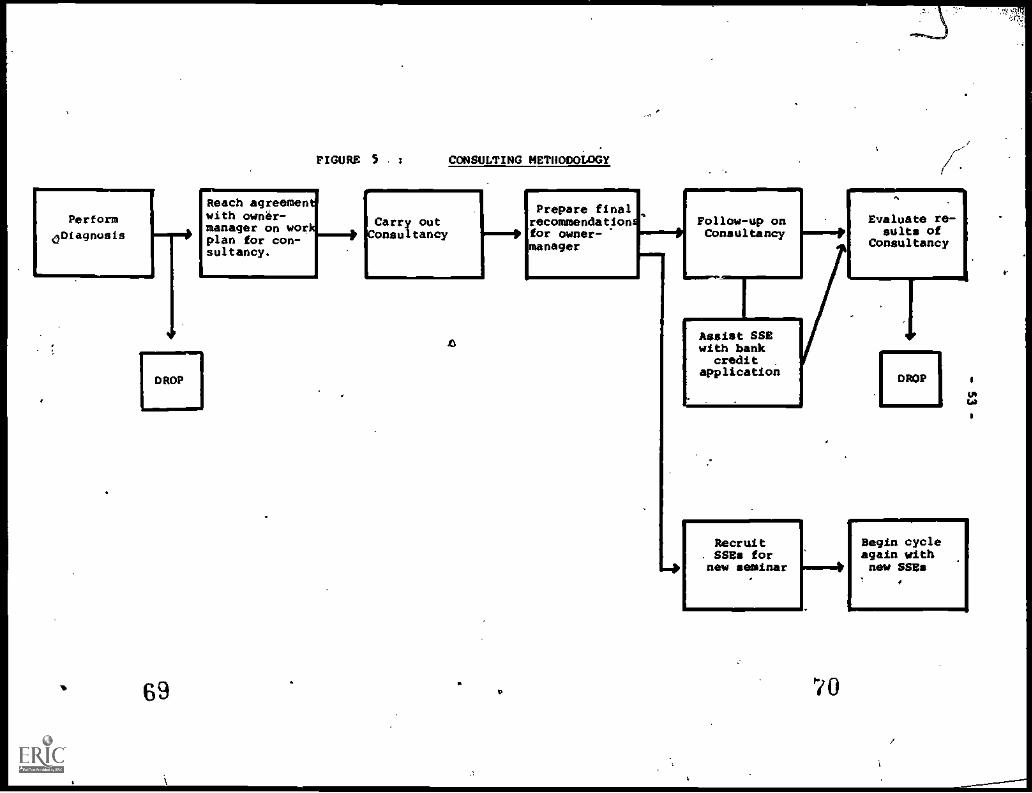

Consulting Methodology 53

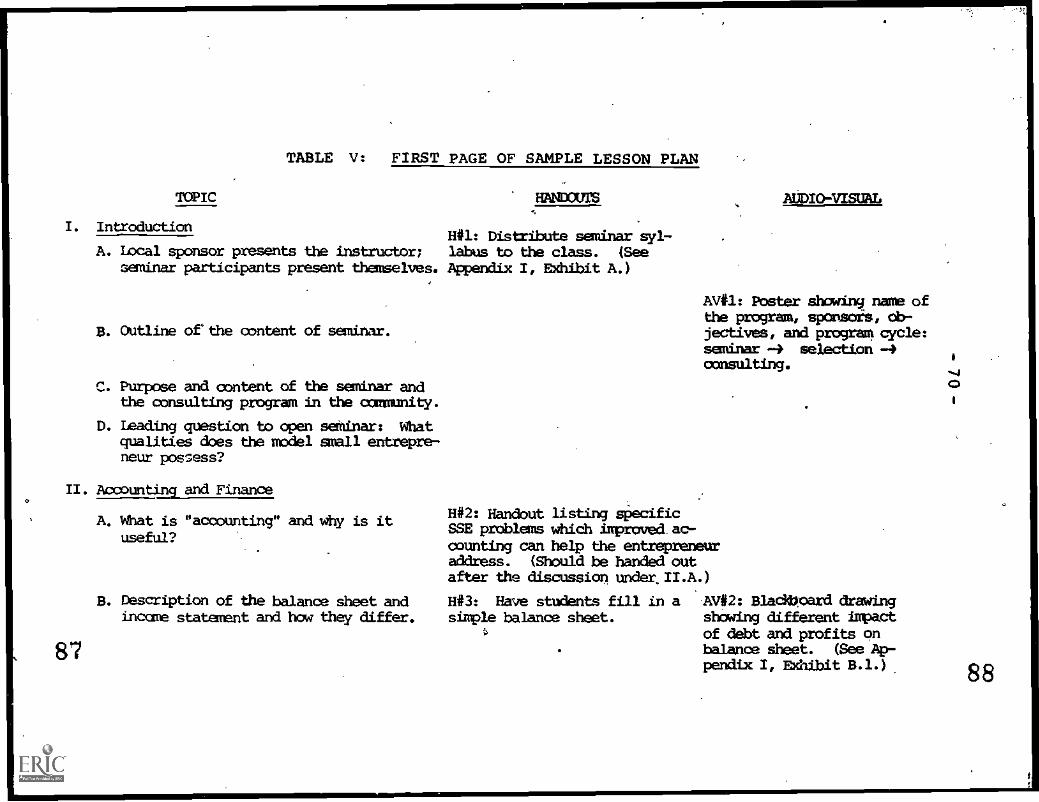

: First Page of a Sample Lesson Plan 70

Sample Questions to Ask the SmallBusiness Person at the Start of theConsultancy

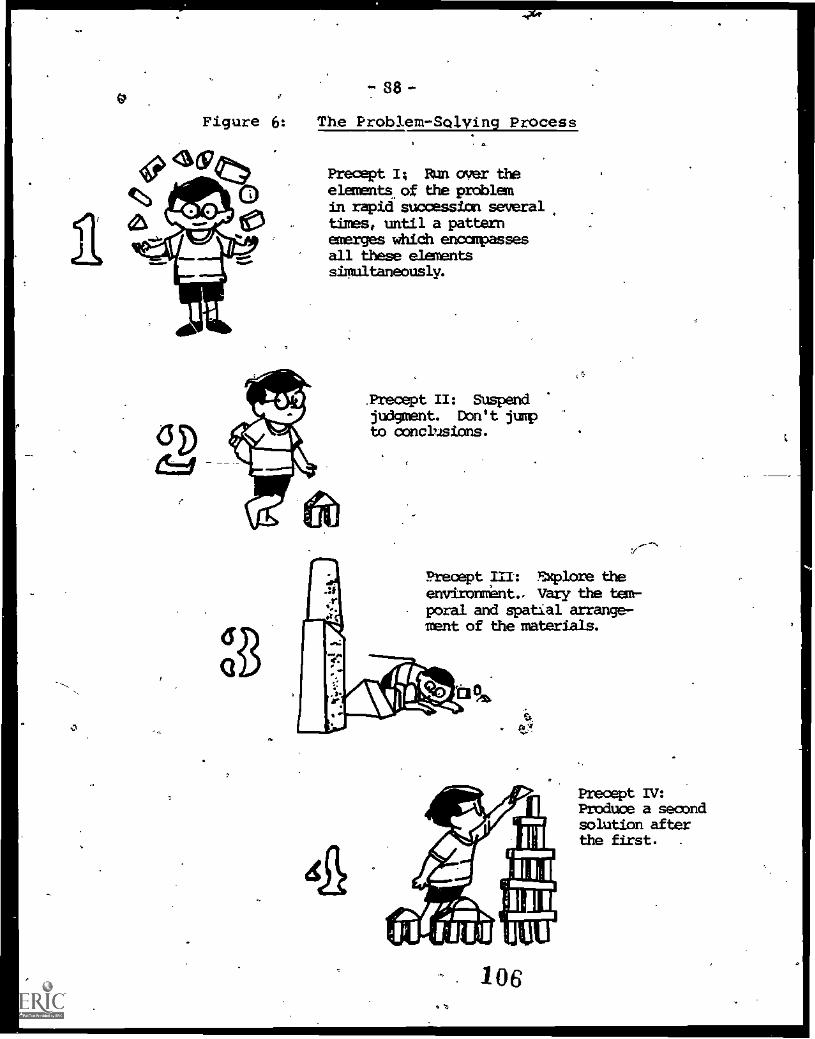

The Problem - Solving Process

Focus on Various Areas of SmallBusiness Management

8 Diagram of the MICRON AccountingSystem

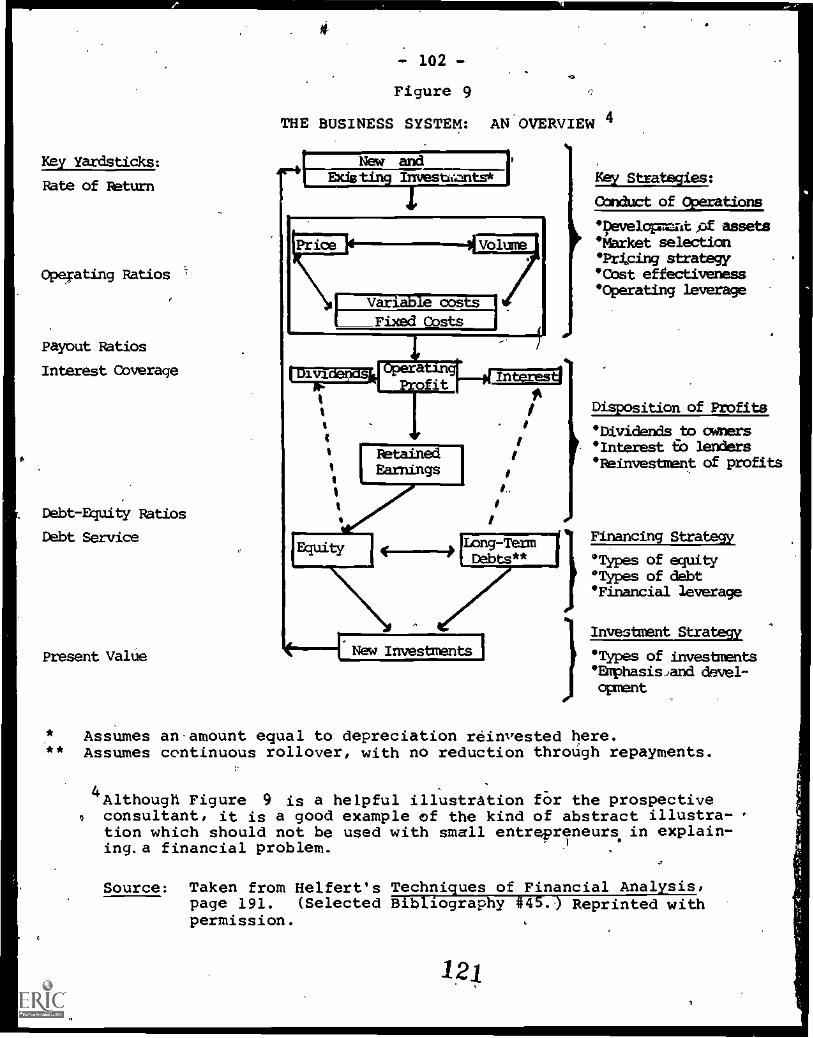

Figure 9

Figure 10

Table VII

The Business System: An Overview

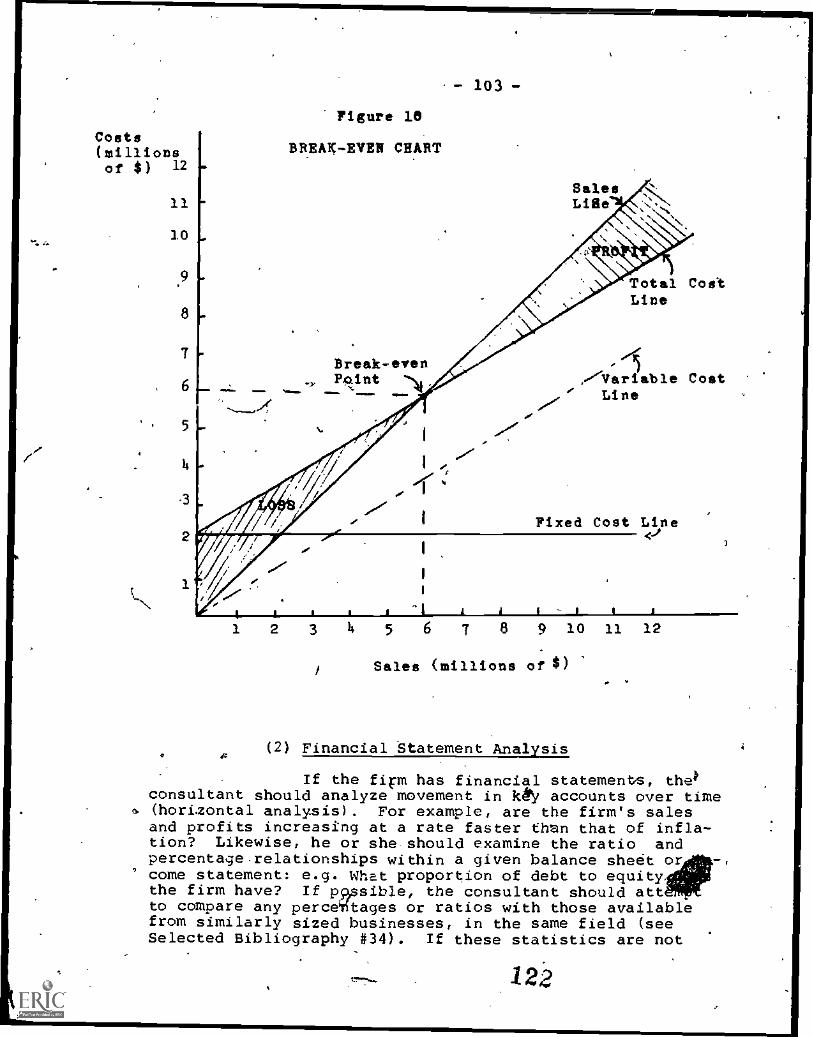

Break-Even Chart

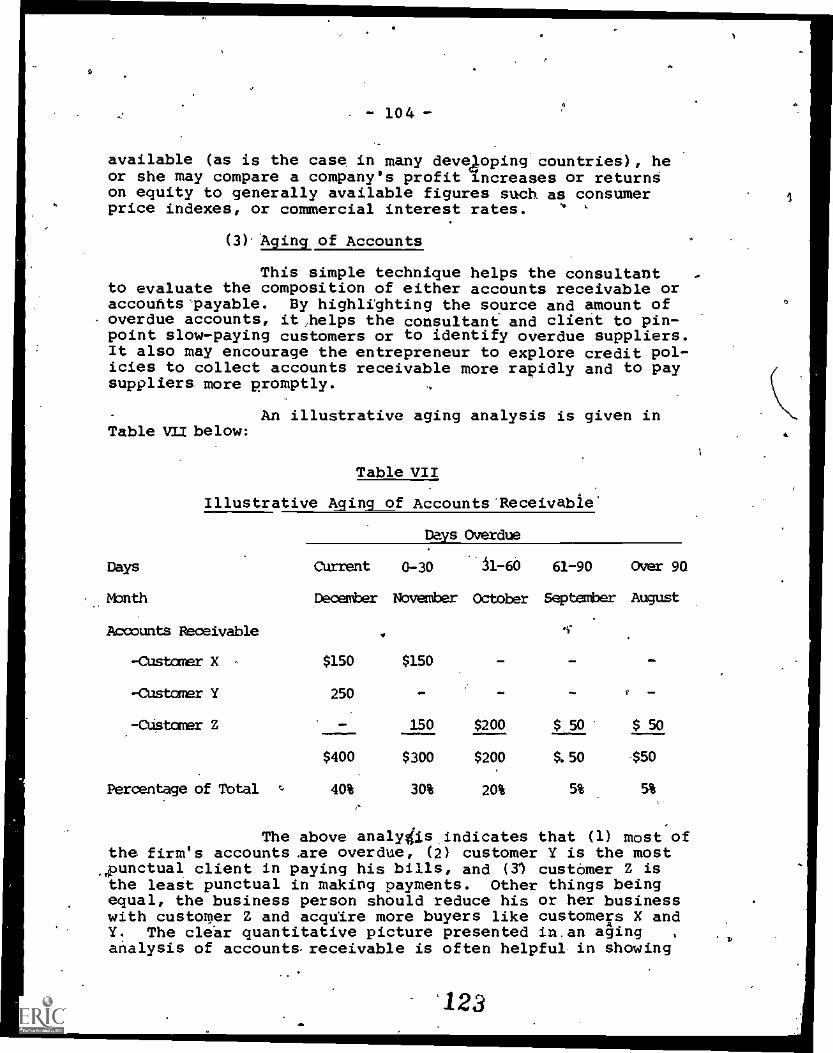

Illustrative Aging of AccountsReceivable

14

ix

e#181

88

93

100

102

103.

104

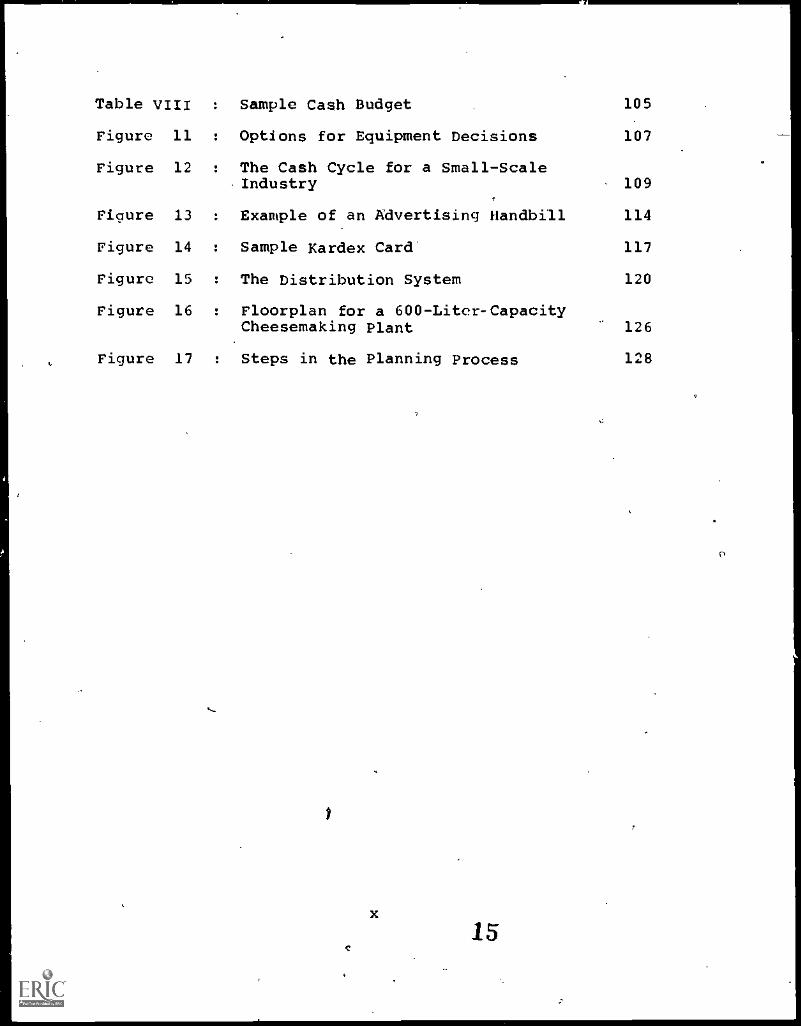

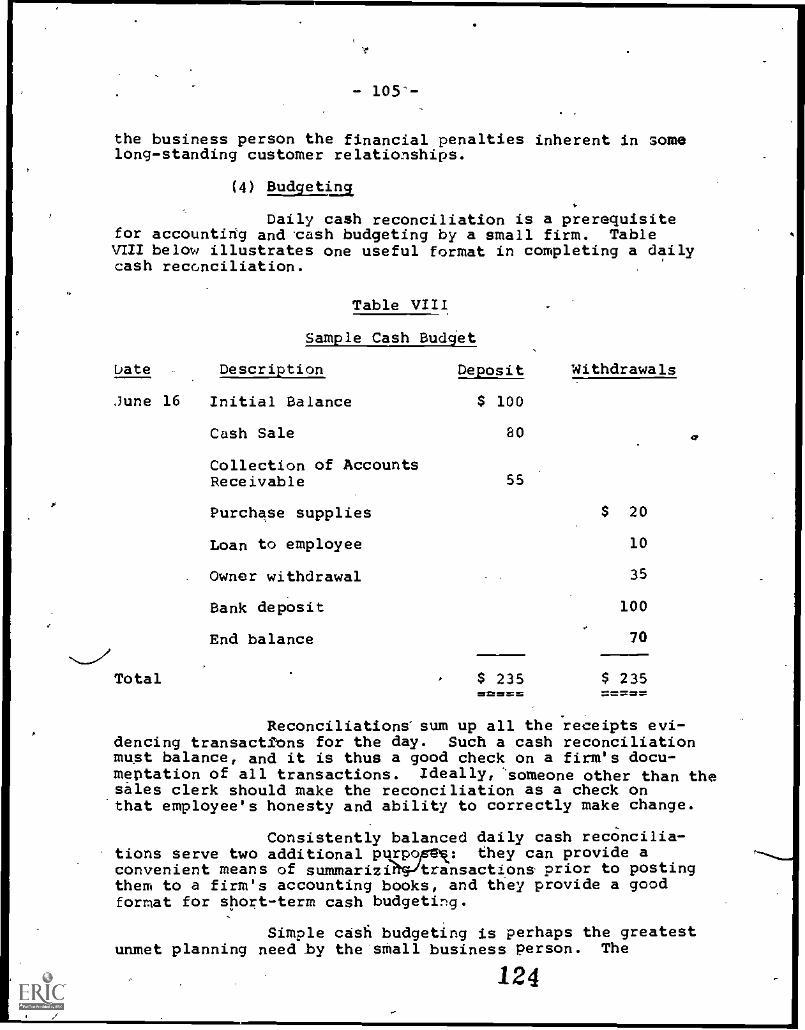

Table VIII : Sample Cash Budget 105

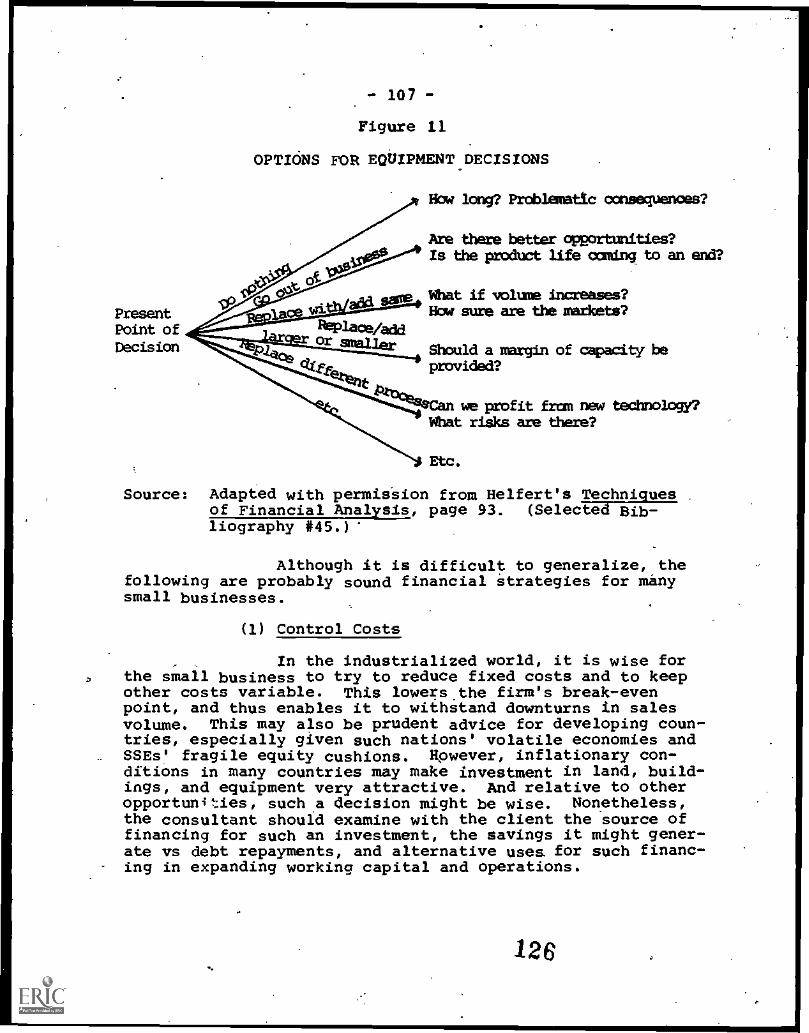

Figure 11 : Options for Equipment Decisions 107

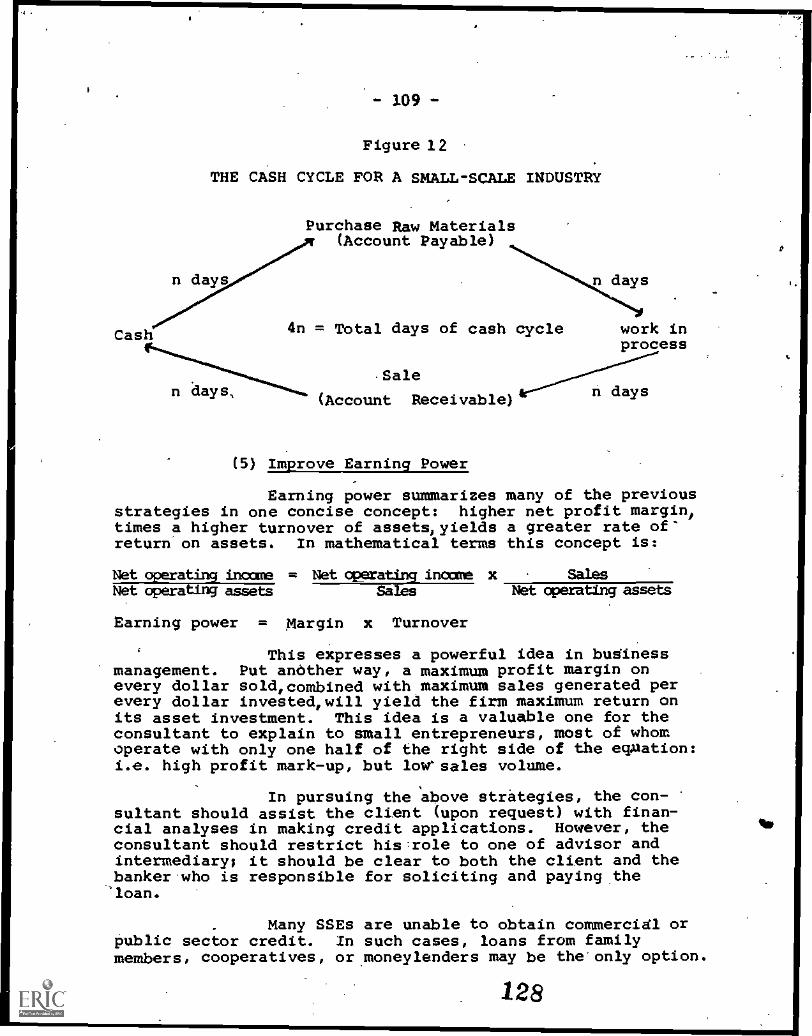

Figure 12 : The Cash Cycle for a Small-Scale'Industry 109

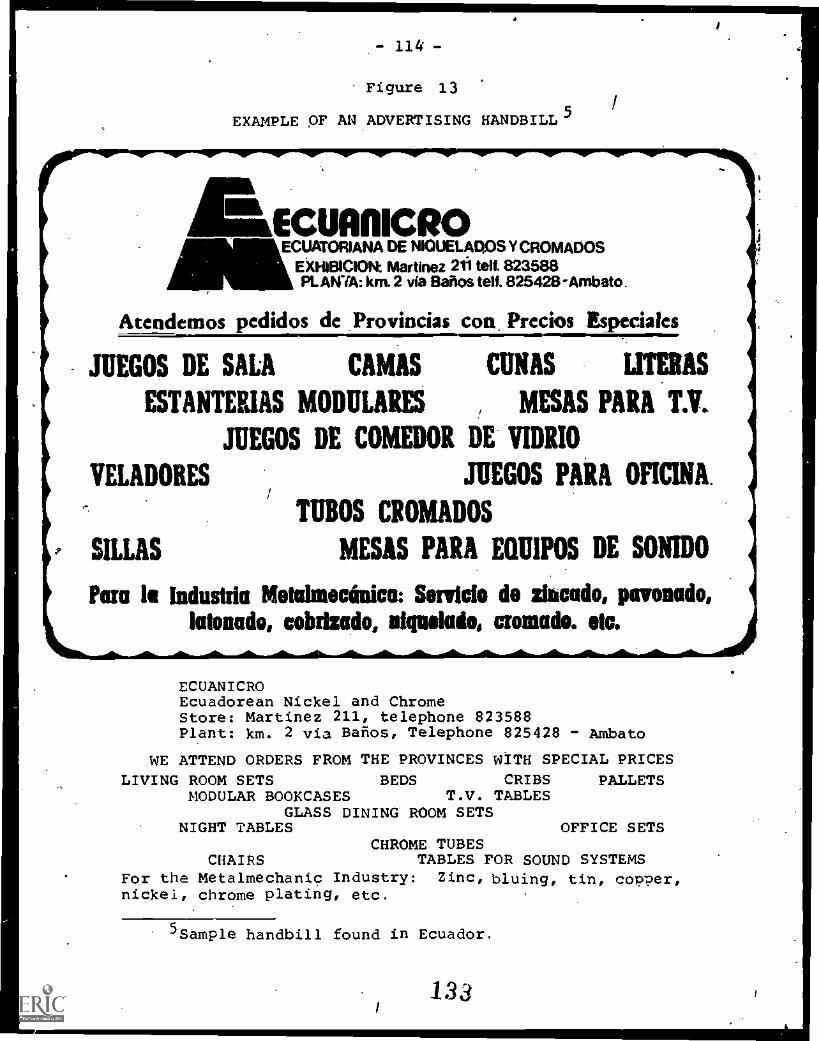

Figure 13 : Example of an Advertising Handbill 114

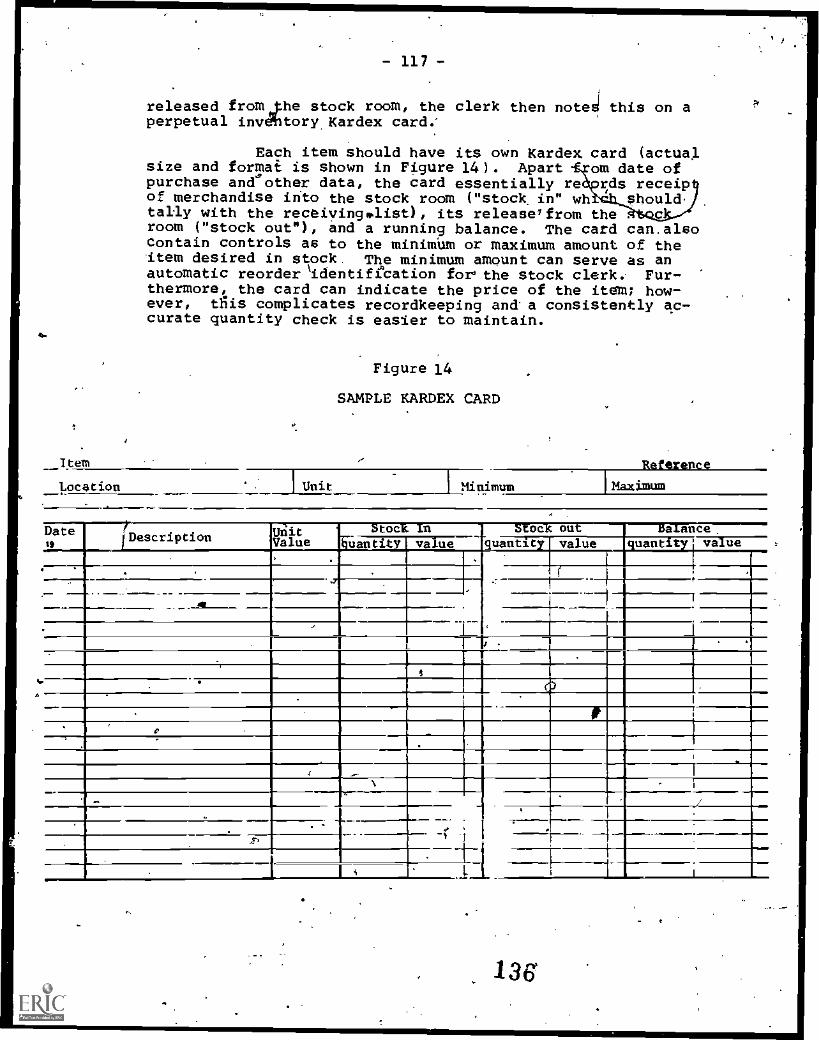

Figure 14 : Sample Kardex Card' 117

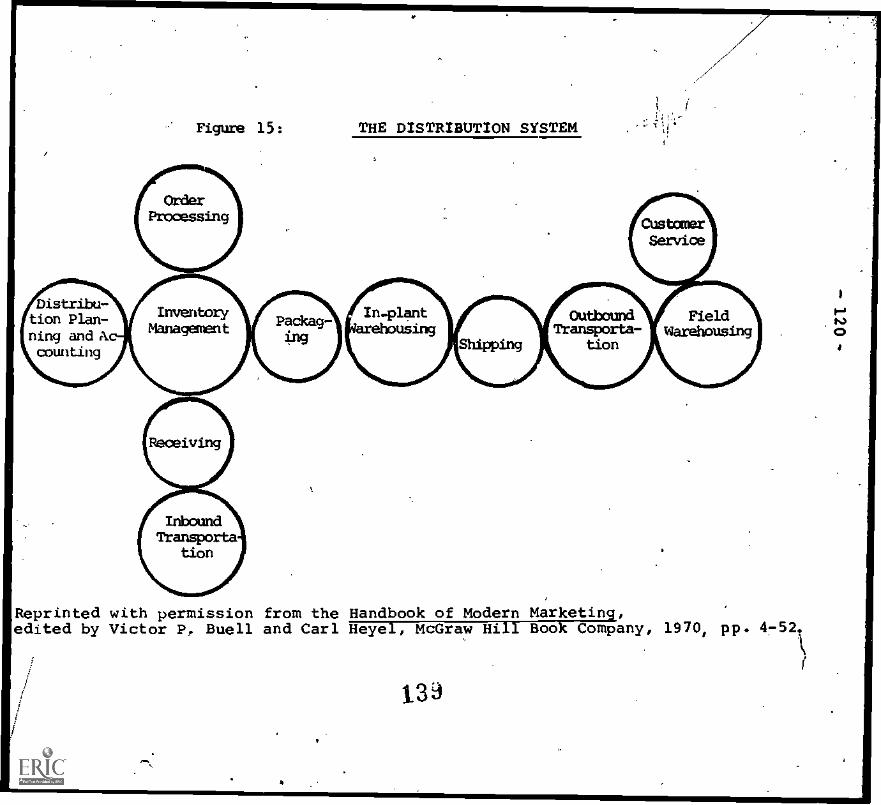

Figure 15 : The Distribution System 120

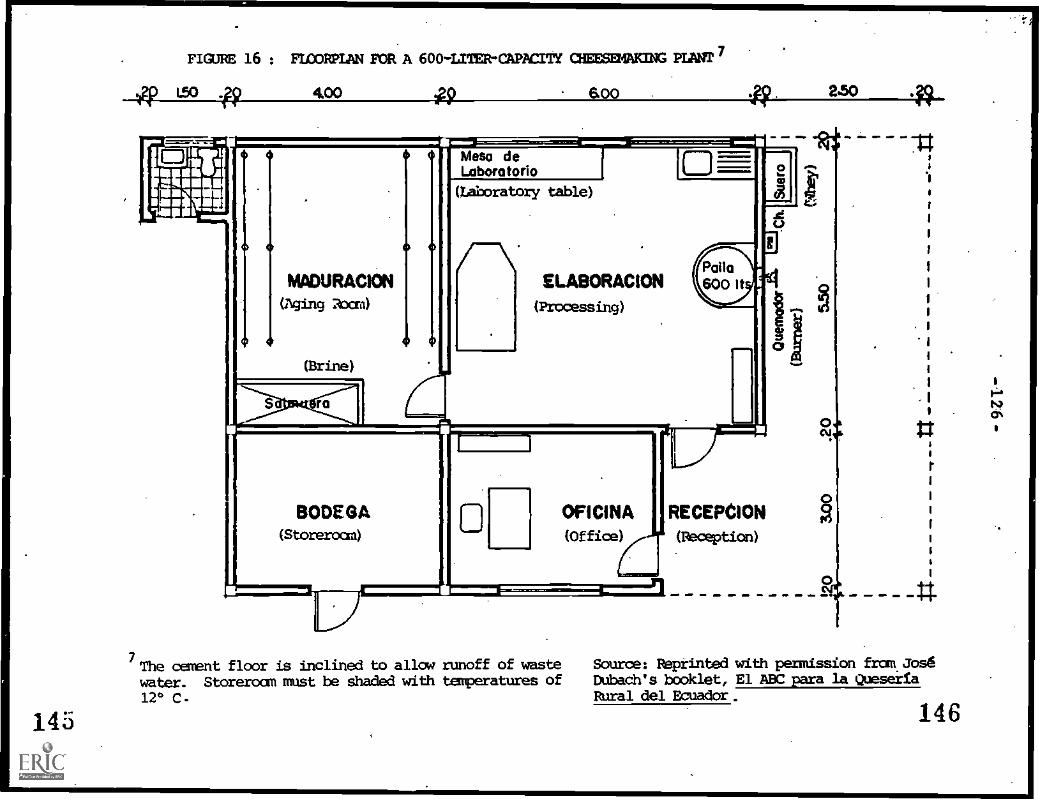

Figure 16 : Floorplan for a 600-Liter-CapacityCheesemaking Plant 126

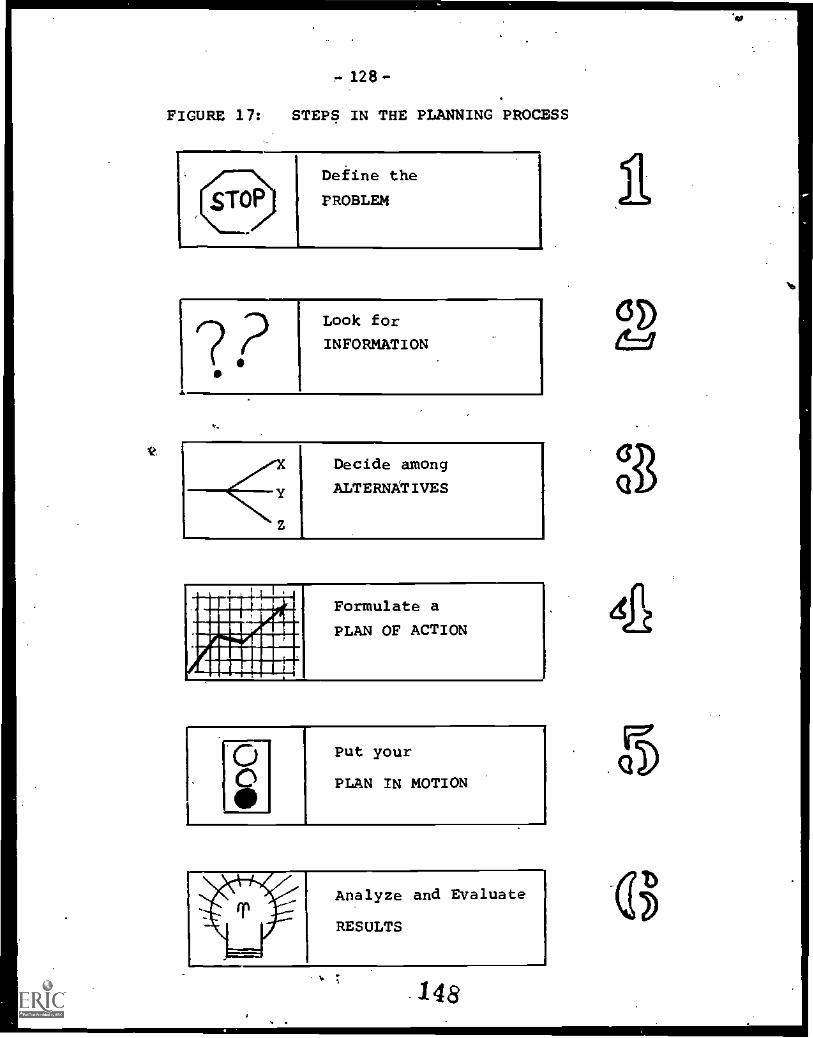

Figure 17 : Steps in the Planning Process 128

x

15

CHAPTER 1

THE SMALL-SCALE ENTERPRISE

A. Some Definitions

1. What is a "Business"?

Businesses assume a variety of organizational formsthroughout the world: from cooperatives to corporatiots,from capitalistic to state-run enterprises, from small scaleto huge. However, all types of businesses share the goal. ofmaximizing output per unit of input, regardless of whetherthat return is measured by higher dividends, more valuablemember shares, or by a surpassed production quota set by thestate economic plan. Moreover, in achieving greater outputper unit of input, all enterprises must bring together threekey ingredients: resources (land, labor, and capital), tech-nology, and their organization or management.

This manual focuses on one particular form of busi-ness organization: the owner-operated, small-scale enterprise,especially the small manufacturing firm. It discusses theimportance of efficiently running a business; that is, soundmanagement of the small entrepreneur's time, technology, andresources. Specifically, the guidelines in this manual helpexplain both the art and the science of efficient businessadministration to the prospective management consultant.The tools and concepts set forth herein should be of generalusefulness regardless of the country or kinds of small busi-nesses which the consultant encounters. '

2. What is a "Small-Scale Enterprise "?

A television repair shop in New York is one exampleof a small-scale enterprise. A metal-working firm in Libe-ria is another example. And an artisan leather-worker inEcuador is a third. All these firms have traits in commonwhich--di-st-i-ngtri-sh-them-from--1arge-enterpr-i-ses---Ye-f-businesses in developing countries often have special char-acteristics which set them apart from their counterparts inthe industrialized world.

Each country appears to have a different officialdefinition of small-scale enterprise or small business.The United States Small Business Administration, for exam-ple, defines as "small" those manufacturers with up to1,500 employees and all retail firms with sales up toUS$7.5 million per year. The World Bank, on the other hand,

4

I6

characterizes small-scale = nterprises (or SSEs) ts_firms pos-sessing less than US$250 0 (1976 prices) in fixed assets,excluding land. And a co tracted study for the United StatesAgency for International evelopment (A.I.D.) by PracticalConcepts Incorporated (P I) recommends yet another definition:SSEs are those firms wi a maximum of 20 workers, no morethan US$50,000 in total assets, and maximum capital costs perworkplace provided of S$5,000. The PCI definition providesa rough quantitative i ea of the size of "target firm" SSEs,a concept discussed 1 ter in this manual.

Yet even thi numerical measure is a very relativeone. For example, i some impoverished countries, a firmwith US$50,000 in a sets and 20 workers may well be manageri-ally advanced and r latively large compared with most otherbusinesses in the ountry. By contrast, in a more highly de-veloped country a company with double or treble that quanti-ty of assets and rkers may be relatively small, given thegreater wealth of the economy, sophistication of the market,and number of lax/ge national and multinational enterprisesoperating in the/country. Consequently,.a qualitative descrip-tion is. needed to focus on what is meant by the concept of .

small-scale enterprise. The table on the following page provi,%-.-ssuch a qualitative indication by comparing large businesses and twotypes of small-scale enterprises: the micro or very smallenterprise, and the transitional or "target" SSE, which is amain concern of this book.

3. How Management of Small-Scale Enterprise Differs fromthat of Large Enterprise.

Thousands of books have been written on business ad-ministration and organization. Many of the concepts in thosevolumes (such as accounting, planning and personnel admini-stration)appear to be generally applicable to any size busi-ness organization. Why then the special concern with manage-ment assistance toward SSEs? What makes SSEs unique, requ-,r-ing separately designed management systems?

Illustrating the difference between a Piper Cub and aBoeLng 747 jet aircraft is one useful way to depict the contrastsbetween large and small-scale business management.) Thebasic processes governing the flight of both planes are the

iThis example is drawn from Cohn and Lindberg's Survi-val and Growth: Management Strategies for the RrrFirm. pp.-1T781 .(See entry #42 in the Selected Bib-1::ography).

17

Table I. Contrasting Characteristic

Micro-Enterprise

1. Local, neighborhood market

2. Marginal resources

3. Owner is often illiterate

4. Owner-manager usually con-trols all equity

5. Hand_ tools and some mactutnery (if a manufacturer)

6. One to three employees

7. Examples: a neighborhoodgrocery store, a tailor,a cobbler.

18

of Large., Target and Micro-Enterprises

Target Firm SSE

1. Often a regional market

2. Adequate equity base andperhaps limited access tobank and trade credit

3. Owner is often.. literateand has access to techni-cally trained or expe-rienced workforce; manage-ment is simple and cen-tralized'

4. Owner-manager may shareequity with partners orfamily members

Large Enter rise

1. National or itvisrna-tional market

2. Well financed by avariety of creditsources

3. Sophisticated mana-gerial and technicalpersonnel; complex'organization

1

1.4

4. Strong differentia-tion between managersand owners of capitalor stock

5. Power tools and light ma- 5. If a manufacturingchinery, some home-made firm, has light and(if an industrial firm) heavy machinery (some

imported)

6. Ten to 15 employees 6. Many employees

7. Examples: a metal-working 7. Examples: a manufac-shop making bicycle frames, Curer of biCycles, aa small manufacturer of 'textile plant, a dis-children's clothing, a lo- count departmentcal agricultural supply store.store.

19

same. Both aircraft take off, cruise, and land; both arecontrolled and directed by pilots; and both are subject tothe same laws of aerodynamics. There, however, the similar-ities end. The Piper Cub is steered by a manual stick andrudder pedals, plus a few simple gauges. The 747, on theother hand, requires a complex set of machines and instru-ments to guide its flight., Moreover, the pilot of the PiperCub, flying at ninety miles per hour with a good tail wind,must constantly view the scene at hand to watch for possibledangers. By contrast, the jet crew flying at hundreds ofmiles per hour must focus their attention, through instru-ments, on the far horizon where they will arrive in a mat-ter of minutes; their immediate environment is of much lessimportance to them.

The same comparison applies to large and small firms.The sophisticated planning and organization of large enter-prises (and the standard business textbooks which adopt thisperspective) are often not applicable to small companies.Complex accounting systems suitable for large corporationsare usually not appropriate for SSEs--especially for smallfirms in the Third World. Costly market research methods,mass advertising, and hierarchical approaches to personnelmanagement and organization are also usually inappropriate.However, simplified accounting systems, marketing techniques,personnel administration, and other management skills areurgently needed by small firms and'are some of the topicscovered in this manual.

5

20

1

- 5 -

B. The Role of Small-Scale Enterprises in Third WorldDevelopment

1. Why are Small-Scale Enterprises Important?

Small-scale enterprises often form an important partof a nation's economy and may account for up to one-half ofa country's labor force and productive output. In addition,successful small businesses may spur greater economic growthin their communities through what economists call "backwardand forward linkages". An example of such linkages,isfound in the sweater knitting enterprises of Mira; Ecuador,where Peace Corps Volunteer's in the 1960s helped developthe occupation into a booming regional industry. Today, thiseconomic sector extends from shepherds, spinners of wool, andbutton-makers (backward linkages) through the sweater knittersto traders with national and international market connections .

(forward linkages).2

SSEs play a key role in many economies because theymeet a special need not often filled by larger business or-ganizations. Such needs include:

- - Providing products or services to specialized,often localized markets: for example, printshops, makers of women's and children's clothing.

Processing dispersed, bulky, and often perish-able raw materials, where small plants near suchinputs are at an advantage: for example, saw-milling, cheese-making, pottery manufacture.

- - Providing ease of access to dispersed consumers:for example, neighborhood general stores, ta-verns, street vendors.

-- Making handicrafts where precise, hand crafts-manship is required; for example, basket-weavers, leatherworkers, jewelers.

- - Providing necessary flexibility in meeting cus-tomers' needs: for example, job metalworkingshops, electrical appliance repair, tailoring.

In addition to their economic importance, SSEs, ifencouraged to grow, may also offer other socio-economic

2 For further details see entry #14 in the Selected Bi-bliography.'

21

benefits. They may prove an excellent source of trained mana-gerial talent. Moreover, given their relatively lower costper workplace as compared to larger firms, they may generateemployment opportunities more efficiently. Other socio -eco-nomic attributes of SSEs include decentralizing a country'seconomic establishment (perhaps reducing the flow of rural-urban migration), enhancing national savings rates based onmany small owner-managers'high propensity to-save for invest-ment, and preserving skills in traditional handicrafts. Indeed,it is such broad social and economic effects which help justi-fy public assistance to private, profit-making small entrepre-neurs. Countries have long offered tariff preferences, taxwrite-offs, and worker training to attract'large-scale enter-prise for some of these same reasons. .It would seem equallyjustifiable to work through small business people for similareconomic and even more attractive social ends.

2. Promoting the Development of SSEs

Once a country decides to encourage small-scale enter-prise, it mayimplement a variety of programs to promote theirdevelopment: One approach is to strengthen SSE infrastructurethrough the provision of plantsand equipment (for example, sub-sidized buildings and public services in an industrial park forSSEs). Another strategy is to bolster SSEs' capital positionthrough tax reductions, bank credit, or government procurementsfrom small-scale businesses. Marketing is another importantarea where SSEs need support. Here government can help bysponsoring trade fairs, by assisting with the export of SSEs'products and services, and by compiling national trade directo-ries for use by local and foreign consumers.

Public programs can also stimulate small firm innova-tion by financing prototypes and by assuring patent protectionfor small entrepreneurs. They can boost product demand byconducting market surveys and by organizing national qualitycontrol standards. Finally, technical assistance and trainingmay help entrepreneurs in important areas such as vocationalinstruction for workers and management training for smallbusiness owner-managers.

Although all of these SSE promotion strategies areuseful, different countries will,find different program mixesto be appropriate depending on their own social and economicconditions.3

3 Entries #1-B in the Selected Bibliography providemore extensive discussion of the range of SSEdevelopment program options available to developingcountries.

22

4

C. Problems of Small-Scale Enterprises

SSEs play different roles in different economies. In theUnited States, for example, franchise operations are,common-place and many small businesses are important subcontractorsin supplying inputs (or marketing outputs) to large corpora-tions. In Colombia, a growing economy and dynamic entrepreneur-ial spirit have made SSEs an important factor in manufac-turing, retailing, and services. And in many other countries,small national economies and fragile sources of local entre-prenelirship may mean that all entrepreneurs, regardless ofsize, constitute a limited' and precious development resource.

Despite these differing contexts, small businessesthroughout 'the world face challenges in six major problemareas: capital, marketing, human resources, technical ortechnological constraints, general business environment, andbusiness practices. With the help of a management consul-tant, the small entrepreneurcan take effective steps to ad-dress the first four problems. And if a number of his or.her peers receive such assistance, some inhibiting generalbusiness practices may also change for the better. SectionC.5 of Chapter /hree of this manual offers guidelines tothe consultant in advising the entrepreneur on these speci-fic problems. However, the general business environment

.'prevalent in any given, country is usually a situation which.,both consultant-and entrepreneur must learn to live with..Yet a recognition of such environmental limits is often help-ful to both the consultant and the client in structuring thegoals and expected outcomes of any consultancy.

As Figure 1 illustrates, some of these areas--delegationof management authority, lack of working capital, and aft en-trepreneur's reactive management style--may pose complicatedand interrelated problems for which there are no easy solu-tions. Fortunately; however, an SSE is not assaulted by eachof these woes with equal intensity. A particular problem or'set of problems may prpdominate among small businesses in-one country or region and not be found in another. Moreover,in the same region or country, different SSEs will oftenface different sets of difficulties. Consequently, althoughthe following list of problems will not be faced by each andevery client, it will likely sum up the entirety of problemsfound in the consultant's portfolio. In becoming more famil-iar with such typical problem areas, the consultant andclient'should be better able to devise prospective solutions.

23

a

8-

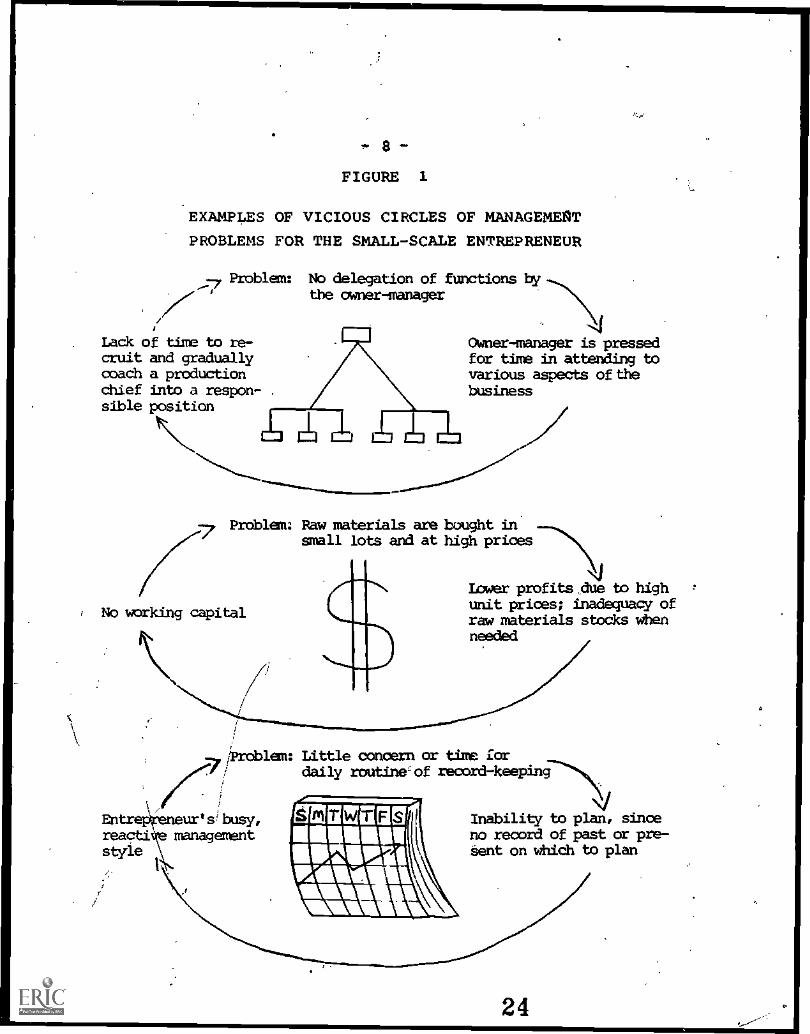

FIGURE 1

EXAMPLES OF VICIOUS CIRCLES OF MANAGEMEgT

PROBLEMS FOR THE SMALL-SCALE ENTREPRENEUR

.7 Problem:

Lack of time to re-cruit and graduallycoach a productionchief into a respon-sible position

No delegation of functions by -...the ovmer-manager

NJOwner- manager is pressedfor tine in attending tovarious aspects of thebusiness

Problem: Raw materials are bought in ...,

small lots and at high prices

No working capital

IDwer profits .due to highunit prices; inadequacy ofraw materials stocks whenneeded

-7 /Problem: Little concern or time fordaily routine` of record-keepinF"%\

Entrepreneur' sf busy,reactive managementstyle

<-

OM% IMa%INA IL

Inability to plan, sinceno record of past or pre-tent on which to plan

24

- 9

1. Capital

Small entrepreneurs often cite lack of capital astheir number one problem. Yet while they commonly mean lackof addition41 cash, poor management of existing'current°sets may be an equal or greater concern. Small firms do of-ten need outside capital, and the greatest indication of thisneed is typically a negative working capital position, (wherecurrent liabilities exceed current assets). Thiq situationis brought about by a number of factors. First,)the smallbusiness person's weak marketing poditionMen forces himor her to sell a service or product on liberal credit terms.Meanwhile, the entrepreneur often may have to pay suppliersunder more stringent credit terms, or even cash. Second,inflation in many countries escalates the cost of raw mate-rials. In developing countries, such materials make up be-tween 50 and 80 percent of the cost of goods sold, and anyinflation consequently has "a greater negative impact on work-ing capital. Third, small entrepreneurs are often reluctantto bring in equity capital by acquiring a partner andthus, are undercapitalized. And fourth, a small businessperson's poor record-keeping, adverse credit history, andweak 'collateral position often leave him isolated from for-mal credit sources. As a result, the entrepreneur mayresort to moneylenders, whose rates may exceed prevailingcommercial rates several times over. Even if commerciallenders are available, they may not offer the entrepreneurcredit under repayment and other terms suitable to his or herbusiness.

The small business person also may suffer from poormanagement of existing assets. Many small firms, for exam-ple, possess no accounting or formal record-keeping systems;in New York, one small business person's only cash controlsystem consisted of two shopping bags--one for receipts andone for payments, due. In-the Third World, records are ofteneven more inadequate because of less education and trainingthan in industrialized countries.

Poor accounting records limit controls on cash flow,inhibit a correct estimation of cost -price relationships,and may well lead to bad checks, unpaid bills, andlgener'almismanagement of cash resources. Furthermore, weak histor-ical record-keeping also makes any .cash budgeting or fore-casting difficult. Conversely, use of such planning tech-niques may often he2p to avoid temporary cash shortfalls.

:25

01

-.10 -

Lack of cash and poor management of existing resourcesmay affect the small enterprise in a number of ways. Suchconstraints compel the owner-manager to spend an inordinate'amount of energy avoiding or replenishing periodic cash de-ficits. They can lead the owner to abuse trade credit, whichin turn may prove a negative reference in a later applicationfor commercial or public sector loans. And they may restrictthe entrepreneur's ability to take quick adliantage. of profitopportunities. For example, without a cash reserve, the C

small business person is unable to exploit seasonal discountsfrom his supplier or put money down on an attractively pricedpiece of equipment. By .encouraging improyed financialmanagement, the consultant can help the entrepreneur betteraddress his or her capital constraints. Chapter Three, SectionC.5., of this manual provides the coAdultant with' specifictools in accounting and finance which he or she may use inassisting the small business person'in this area.

4 2. Marketing

A market for his or her-product or services is justas important to the small entrepreneur as capital. The mar-keting problem can be viewed from two persgectives: lack oftimely and adequate demand, aid poor marketing practices bythe small business person in exploiting available demand.

Small enterprises often encounter difficulties-in' se-curing a steady market for their output. This situation ispartly due to SSEs' competition with large businesses and part-

-ly due to the even fiercer competition among themselves. A de-

.

pendable market is also threatened by periodic swings in thebusiness cycle in capitalistic economies.. Given their weak eauitybase and typical concentration within a narrow range of Prod-ucts or services, small businesses often fare worse thanlarger enterprises. SSEs' markets maybe further disruptedby sudden changes in government jo1icies affecting interna-tional trade, internal price controls, or the money supply.

Geographic isolation of SSEs--especially those insmall towns and rural areas--often presents another impedimentto timely marketing. Poor roads, sporadic transport, and un-reliable communications can impede the marketing of productsaneElow of market information to the small entrepreneur.

Many of these problems are beyond the control of thesmall business person. He or she can, however, try to betteraddress demand constraints through improved marketing prac-tices. Yet often the small-scale entrepreneur has no

4/ 26

9

preplanned marketing strategy. His or her products may be ofuneven quality relative to,dustomer desires or of a designundistinguishable from competing products. The entrepreneurmay also display his output poorly and may make limited useof salespeople. MoreoVer, in meeting demand, the entrepre-neur's purchasing practices- are often uneconomical (frequentsmall purchases as opposed to planned buying in larger lots),and inventory information and control may be nonexistent.

In short, the small business person often lacks anoverall marketing strategy.. He or she may be well aware ofthe benefit of buying cheap and selling dear and may also bean expert salesperson. Yet the entrepreneur typically lacksa planned approach to the purchasing-inventory-sales cycleof the business. One cause of this may be due to the absenceof any record-keeping, cash budgeting, and other accountingcontrols. Thus the owner-managercannot promote the most .

profitable or best'-selling product becausehe or she is oftennot sure just which item. is most profitable or best selling.The owner could reach a better decision if he or she couldimprove market research; sales promotion and advertising,take advantage of volume marketing, and learn to weigh thevalue of customer relationships in comparison with marginalreturns on various productn. Moreover, although `small firmsare theoretically more flexible than large firms, SSEs (es-pecially small manufacturers) must pay particular attentionto meeting customers' needs for timely delivery of qualityproducts. They must develop ways of offering follow-up ser.vice or guarantees for defects in workmanship of the itemssold.

This situation may affect the way in which smallbusinesses address their markets. First, small entrepreneursoften fail to consciously decide on a discreet line of busi-ness. A retailer of men's clothing, for example, may stocka variety of other merchandise such as bicycles or appli-ances.He or she may have added the different merchandiseeither because he got a "good buy",or because he felt thata quicker profit opportunity was more readily available inthat line than his own. Likewise, a small-scale industrial-ist may choose to divide operations between production anda small retailing outlet. Despite the higher retail mark-up,-low sales volume may indicate that the entrepreneur's timeand resources would be better spent in improving production.

These examples are not to say that diversification isinappropriate to small business. On the contrary; a retailoutlet well integrated with a small manufacturer may be a

27

12

sound marketing approach. In general, however, sideline ac-tivities do not reflect a conscious marketing strategy, butrather a "scatter-shot" and unfocused approach to marketing.

Small entrepreneurs may also tend to exploit highmarginal returns in a narrow upper-class market rather thanlower marginal returns and higher volume sales in a massmarket. This may be due to 'limited territory and populationor to the low purchasing power of the clientele; In somecases, this marketing approach may reflect a sound strategyin addressis,, a narrow market. In many other instances, how-ever, this attitude may be unduly limiting and may reflecta small entrepreneur's reluctance to expand business opera-tions (and profits) into wider markets.

Nonetheless, this situation is changing, especiallyin rapidly-growing, middle-income countries. Colombia, forexample, offers two contrasting types of markets within thefurniture-making industry. On the one hand, many small °

businesses hand-carve colonial wooden furniture, selling Alow volume of high-priced items to an upper-class market.On the other hand, many other small entrepreneurs mass pro-duce inexpensive, plastic-upholstered, metal-frame furnituiefor a larger market. Thus, changing market, conditions cangradually bring about more dynamic marketing strategies bysmall business people. The guidelines on marketing and sales,and purchasing and inventory (see Chapter Three, Section C.5.)will also better enable the consultant to assist the smallentrepreneur in meeting marketing constratntS.

3. Human Resources

Given the'relative labor intensiveness of smallbusinesses, human resources are crucially important, and theowner-manager usually sets the tone for the workplace. Infact, a small-scale enterprise is largely an extension ofthe entrepreneur's own personality and ego. However, thispersonalization and informality of small businesses also, poseobstacles to the management consultant, 'since he or sheusually recommends increaded organization of the small firmas a requirement to further growth.

The small entrepreneur typically maintains close con-trol over the activities of the business. A typical smallentrepreneur often has no formal education beyond primaryschool. Formerly a worker, the owner may have started thebusiness with a loan from relatives or with severance payfrom his or her last employment. Though hardly a simple

28

-13

individual, the owner is often a pragmatist whose personaland business horizons are limited to the needs of the day.Also, as an ex-craftsman, he may find it difficult to re-linquish his daily concern with the production process anddevote himself tc the abstractions of management. In orderto survive, he or she normally has great self-reliance,, ag-gressiveness, and a sense of initiative in dealing withclients, suppliers, and workers, as well as a healthy skep-ticism when dealing with outsiders.

The central role of the owner-manager within the SSEis not necessarily bad, but it does present problems oncethe firm begins to expand. A centralized, informal manage-rial style often includes poor record-keeping, little dele-gation of authority to subordinates, and lack of formal jobdescriptions. The result is usually an owner who is simul-taneously technician, record-keeper, salesman, purchaser,and manager. In assuming all these tasks, he or she is prob-ably neglecting the best possible use of the employees, whomight assume some of these responsibilities. Moreover, along-term implication of such centralized management is thatif the owner dies or becomes ill, there is no trained succes-sor or replacement to run the business. Intsmall firmsowned and managed by families, relatives brought into thebusiness may help resolve the succession problem. However,a family-run business may also promote chaotic decision-making as various family members compete for authority in,the firm.

The dominance of a family or of a single owner-manager in directing the business may also influence theoverall goals of the enterprise. Although increased profitsare commonly sought by most small entrepreneurs, there maybe other competing objectives. For example, a prestigiousfamily business may consider tradition and social positionto be more important than added earnings; or, having reacheda level of self-support, a business owner-operator may de-cide that the extra workload, responsibilities"and unfamil-iar roles associated with expansion and greater profits aresimply not worth it.

While labor is plentiful in most developing countries,skilled workers are usually at a premium. And SSE employeesare often more poorly trained and educated than their coun-terparts in large firms. In addition, employees in SSEsnormally do not receive benefits under social security, min-imum wage, and health insurance laws. Such situations oftenlead to high'employee turnover among SSEs as workers move to

29

- 14-

larger companies which offer such benefits, or start theirown small business.

Small enterprises are often unable to hire qualifiedmanagers given their competition with larger firms for em-ployees and given the demanding work environment of SSEs.Also, the small-scale entrepreneur is typically loath totrust one of his or her own workers, let alone an outsider,with the technical and financial secrets of his business.After all, the employee might quit and start a competing en-terprise in the same line (as might have been the case withthe owner).

Fortunately, the entrepreneur can remedy many humanresource problems by modifying personnel practices. By fol-lowing the guidelines in Chapter Three, Section C.5., partic-ularly those on Personnel, the consultant can assist theentrepreneur in making the best possible use of his or hermanpower.

4. Technical Constraints

One's first acquaintance with-an SSE in the ThirdWorld can be an eye-opening experience. A small tailor shop,for example, may be located. in a cramped section of theowner's home, with five or six workers bent over sewing ma-chines. A small metal-working enterprise may straggle overa half-vacant lot covered by a tin roof. It may have toolsand machinery strewn about, and what passes for a stock roommay be filled to overflowing with jumbled parts and equip-ment. If the firm is a retail enterprise, it may have mer-chandise scattered in no apparent order, with music blaringto attract potential customers off the street.

The problem of physical plant and business layoutmay warKant considerable technical assistance. For example,a cabinet-maker may request help in making the most efficientuse of raw materials and labor in producing wooden furniture,perhaps through the use of time-motion studies of his or her em-ployees' work routines.

While addressing technical weaknesses is importantto the small entrepreneur, most small businesses (especiallysmall manufacturing firms) are in greater need of managementrather than technical assistance for two reasons. First,many small business people were once workers or craftsMenthemselves. While having mastered a manual skill and abilityto work with machinery, they are often more puzzled by the

30

- 15 -

abstractions associated with business administration.Second, small entrepreneurs must have some basic technicalgrasp of their business (or a foreman who does) or theywould not survive. Frequently, however, they postpone deal-ing with records, planning,. and improved persondel practices--especially while their firm is still small. Nonetheless,*there are general technical areas in which the managementconsultant can help the client improve his or her performance.(Refer to the section on Production on pages 124- 127-fortips on the kindsof technical advice which a managementconsultant might convey to a client.)

5. The General Business Environment

Small businesses have to exist in social. and econo7/mic environments which usually deal with themloOre harshlythan with larger firms. With less capital, greWter ptoductspecialization, and fewer personnel than large,ccompinies,SSEs may be ill-equipped to handle sudden change* 'in consumerpreferences or downturns in the economy. SMall_firms mayalso find it difficult to deal with local legal.requirementssuch as income taxes, social security for employes, andlegal registration of the business with a local chamber ofcommerce or government agency. Often the time and paper-work associated with these regulations are more onerous thanthe fees or taxes paid. Finally, due to their smallness,SSE-s may find themselves squeezed out by larger firms in ob-taining commercial credit, in attracting "skilled workers andmanagers, and even in acquiring adequate shares of existingpublic services. on the other hand, SSEs can sometimes avoidthose legally mandated costs paid by larger businesses (e.g.social security taxes for workers, income taxes, duties onimported goods, minimum wages); and as a consequence, may evenbe able to offer certain goods and services at a more eco-nomical price than larger firms.

Business support services are often weaker for SSEsthan for larger enterprises, and in many developing countriessuch services may be inadequate or nonexistent for any sizebusiness. Although the consultant cannot really change ,thegeneral availability of such serices, he or she should befamiliar with the adequacy of the local business infrastruc-ture. Such knowleage will het i: the consultant in structuringthe scope of a consultanc. and in planning for follow-upservices to the client u= :..n c=71asion of the consultancy.

31

-16 -

The sophistication of business infrastructures willvary by country. Howeveroin many developing countries theconsultant should be prepared to cope with deficiencies insupport services such as the following:

(a) Diversified capital markets: Credit may belimited to a government hank or the local money-lenders local equity markets or commercialcredit services to margirll borrowers usually donot exist. In addition, existing credit sourcesmay offer a limited range of credit packages,often unsuited to the needs of small businesses.

(b) Certified public accountants (CPAs): CPAs pro-vide a valuable internal control by auditingthe accounts of the entrepreneur's firm. By au-diting other companies, CPAs may also help as-sure honest practices by other enterprises withwhich the small business person deals. In manycountries, however, tax accountants (often with.only bookkeeping training) are far more commonthan CPAs.

(c) Factoring services: In industrialized countries,factoring firms purchase accounts receivable at adiscount and then collect from as many debtors aspossible in ord'.r to make a profit. The scarcityof such services in the Third World (especiallyto SSEs) deprives small businesses of anothercredit source, as well as a check against slow-paying customers.

(d) Civic associations: Developing countries oftenlack strong trade associations or the equivalentof better business bureaus.

(e') Information concerning markets and credit histo-ries of other bnsinesses: In the United States,a small business person can consult a creditreporting service on potential clients and canread a variety of marketing studies concerning-his or her particular product. Such informationis deficient for large companies in developingcountries and is almost nonexistent for SSEs.

32

sp.

4

-17 -

6. Business Practices

A difficult business environment for small enterprisesoften affects how the businesses are run and their relation-ships with the outside-world. The greater risk associatedwith small entrepreneurship often makes for greater informal-ity, greater skepticism, and less planning than in large com-panies. Given the harsher terms of the environment, thesmall entrepreneur may often carry these qualities to extremesin the eyes of an outsider. Yet when one considers the un-certainties of the environment, particularly the lack ofbusiness checks and balances found in more industrializedeconomies, these business practices are more understandable.For SgEs in many developing countries,typical business prac-tices may include the following:

(a) Mistrust: Absence of auditors, factoring agen-cies, and credit reporting services often leadto poor compliance with the terms of sales indeveloping countries. Poor quality control pro-cedures--particularly in small businesses--makethe warning "buyer beware" especially necessary.Consequently, post-dated checks and high dis-counts given for cash purchases are more prevalentthan in industrialized countries.

(b) Legal informality: SSEs in developing nationsoften enjoy a kind of'outlaw status". They maynot pay taxes, and many do not pay workers theminimum wage. These small firms also often donot officially register their businesses, andthey customarily ignore public health and zoningstandards. As a result, their relationship withlocal authorities is at best one of benign ne-glect. An unfortunate consequence of such'"ille-gality is that small entrepreneurs may expendmore effort in escaping the notice of the taxcollectdk than in improving the administrationof their businesses. Thus, if an owner has anaccounting system, he or she often will not keepaccurate records, but rather an official set ofbooks which will look good to the government andproduce a nominal income for his income taxreturn. A micro-entrepreneur may survive verywell without accurate financial statements andother such legal niceties. A growing smallbusiness person, however, in postponing a legaland administrative formalization of the firm,

33

- 18 -

may run the risk of official fines and denialof bank credit. He or she may also eventual-ly lose real financial and administrativecontrol" of the enterprise.

(c) Reactive management: Most small entrepreneursare jacks-of-all-trades and consequently oftenappear overworked and disorganized. A varietyof factors--including a lack of skilled help,lower educational levels of the entrepreneur,and little access to technological labor-savingdevices such-as computers- -may make the smallbusiness in the Third World even greater preyto a "busy" management style. Within twentyminutes on a typical day, the small owner-manager may ring up a sale, chat with a sup-plier, help a worker adjust a lathe, and stepout for a beer with the local moneylender.As a result, the owner may often flounderabout in trying to address the dangers (or op-portunities) confronting his or her enterpris,e. -

The'level of small business mistrust and legal in-formality will vary by country and by culture. Where suchconditions prevail, the consultant must try to understandand adapt himself to them. Reactive management styles, onthe other hand, can often be remedied throUgh individualconsultancies. Although some of this informality is unavoid-able (and even enjoyable) to the small business person, muchcan be brought under control through improved managementpractices, especially planning. Small entrepreneurs oftenfail to plan properly due to a variety of reasons: ignoranceabout planning techniques, lack of an appropriate time andplace in which to plan, or a general 'fear and reluctance toconfront the future. Some small entrepreneurs in the ThirdWorld may also resist planning given the highly uncertainbusiness environment in many of the countries. Such a cir-cumstance, however, is all the more reason for trying toanticipate and decide on contingencies for the future. Oftensmall entrepreneurs will intuitively accept the usefulnessof planning, but it is usually difficult for them to changehabits and acquire the necessary discipline in order to plan.(See guidelines to consulting on Planning on page 127.)Nonetheless, small business people (especially those of"target firms" desdribed in the next section) can and willimprove their planning techniques given enough patience andpersistence on the part of the management consultant.

34.

- 19 -

D. The Target Firm

Thousands, perhaps millions, of SSEs may exist in a givendeveloping country. An extension program cannot possiblyprovide individualized consulting services to all these enter-prises. Consequently, one approach is to target assistanceto those firms with real growth potential. Providingmanagement consulting to such "target firms" is animportant focus of this manual.

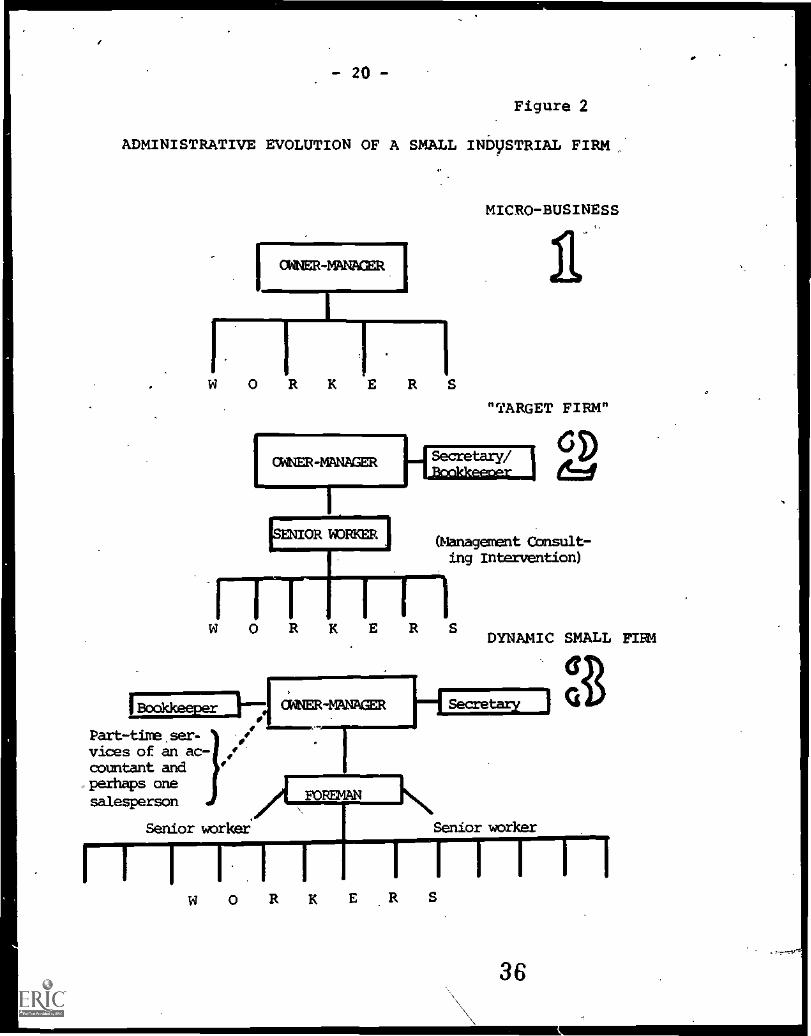

What exactly is a "target firm"? In essence, such a firmhas reached a threshold size where 'the need for accounting,marketing, and other management controls is self-evident tothe owner-entrepreneur. He or she must improve the. admini-stration of business resources.in'order.to grow or the enter-prise may stagnate or die. The target firm has reached acrossroad where improved organization (as opposed to technol-ogy, credit, or other resources) is the main barrier tofuture growth. The size and characteristics of target firmswill vary with differing cultures and economies, just as thedefinition of small business differs from country to country.Figure 2 on the following page provides one illustration ofthe evolution of a target firm. Other features of this kindof small-scale enterprise include:

(a) Size: The target firm.maintains between five to 15employees, with total assets ranging from US$25,000-50,000 (1979 dollars).

(b) Property: The entrepreneur owns some property: forexample, plant equipment, a motor scooter, and per-haps his or her own home or place of business (al-though such items may not be acceptable as collateralby a local commercial bank for one reason or another).The entrepreneur has probably surpassed his "basichuman needs" although often his workers have not.

(c) Education: The owner can read, write, and figure,or else he or she has a trusted manager or familymember in the business who can.

(d) Finance: The target firm entrepreneur likely has aEiiiiricount though he might not reconcile it withhis monthly statement. He or she has little or nocommercial bank credit and makes use of moneylendersand other informal credit channels.

35

- 20 -

Figure 2

ADMINISTRATIVE EVOLUTION OF A SMALL INbySTRIAL FIRM

OWNER-MNAGER

W O R K E R S

CMNER-WINAGER

MICRO-BUSINESS

"TARGET FIRM"

Secretary/Ds

e=i

(Management Consult-ing Intervention)

DYNAMIC SMALL Flat

Part-time,ser-vices of an ac- ff

countant andperhaps one

salesperson

Senior worker.

EOREMA14_1\

Senior worker

W O R K E R S

36

- 21

Clearly, the target fUm approach is only one of a va-riety 'of ways to convey management assistance to SSEs. Butthen why focus on the relatively prosperous target firm?Why not concentrate on micro-entrepreneurs who may be in_greater need? The guidelines below may help to answer thesequestions:

(a) Maximize rate of return

Resources--particularly skilled human resources--areat a premium in developing countries. Consequently,management consultants would do well to focus theirassistance, at least initially, for maximum impact'on the local economy.

A consultant's workload does not correlate directlywith firm size, but rather with the number of fireshe or she deals with. Thus, the same consultant maybe able to assist four target firms (with perhaps atotal of 40 employees and US$400,000 in net sales),as opposed to only five micro-enterprises, with per-haps only 15 employees and not more than US$100,000in net sales. In fact, the consultant might even beable to handle more target firms, since their prob-lems are usually more focused and easily addressedthan those of smaller SSEs.

In order to maximize economic impact, a consultingprogram should target those firms which will makebest use of its advice through hiring more employees,producing or trading more output, or expanding phys-ical plant. However, a great many SSEs in develop-ing countries do not fit the target firm description.Most are micro-enterprises which were formed morebecause of a lack of better employment opportunitiesthan because an entrepreneur decided to try to applyhis or her skills in meeting a real economic need.A seller of lottery tickets, for example, is an ex-treme example of the former. The vendor is not ex-ploiting a productive market niche but merely provid-ing a redundant service in the absence of other em-ployment possibilities. On the other hand, thereare large numbers of target firm entrepreneursthroughout the Third World who could dramatically ex-pand production and employment, given management.as-sistance. The expansion of such firms may even pro-vide more productive work for underemployed micro-entrepreneurs.

37

22 -

(b) Seek entrepreneurs who will listen and act

The target firm entrepreneur has already met mostof his or her needs for food, education, andhousing. This relative security may make him moreopen to the consultant's recommendations and adviceand more capable of translating them into practice.

The micro-entrepreneur, however, often has otherpressing needs on his or her mind besides new ad-ministrative practices. Moreover, many of thesetechniques are inappropriatd to a tiny firm since agood memory may well be more reliable than unfamil-iar written records in a tiny enterprise. Further-more, the micro-business person probably lacks thefinancial resources needed to put the consultant'srecommendations into action.

By analyzing and assisting target firms, the consul-tant will likely help small entrepreneurs tap theformal credit system. Micro-entrepreneurs, on theother hand, may well have to rely exclusively oncostly, uniquely designed credit systems to meettheir special needs.

(c) Make target firms models for other SSEs

SSEs generally have high employee turnover with manyworkers leaving to start their own businesses. Targetfirms may, therefore, prove to be informal traininggrounds and models for future entrepreneurs. Further-more, once management consultants gain experience inassisting target firms, they may prove to be excel-lent supervisors of less skilled and more numerousconsultants serving smaller business people. (Such asystem is described in Malcolm liarper's book, Con-sultancy for Small Businesses: The Concept - Train-ing the Consultants, which is discussed in ChapterTwo and in Appendix III, Exhibit A.) Thusta develop-ing country might best begin, ny SSE developmentprogram with a focus on target firms. The earlymeasurable benefits would help assure the survival ofthe program which might then go on to assist smallerbusinesses.

/- 23 -

'CHAPTER 2

MANAGEMENT ASSISTANCE TO SSEs

A. Management Consulting: General Considerations

1. Checklist of Guidelines for Designers of SSE Consult-ing Programs

Before organizing a management consulting program,designers should assess the rationale for such a program andhow it might best be structured to meet the needi of theirparticular country. Prospective consultants should also_ques-tigh how, consultancies could be organized at the Communitylevel. ihe checklist below provides a useful framework forconsidering such issues:

(a) Before contemplating ah SSE program, are smallenterprises important enough to the economy toWarrant special attention?

(b) If the answer is yes, define the needs of SSEs inyour country. Does lack of management assistanceconstitute a key constraint to small businessdevelopment?

(c) what local institutions (public or private) nowexist which may serve SSEs better than starting aspecific SSE assistance program?. What publicmeasures, such as.tax deductions or su4idizinginterest rates, might encourage these inptitutionso increase their - support services for SEs?Wh t other policy measures might directly\ assistSSE xpansion?

(d) noes a overnment SSE extension program alreadyexist in your country? Can it be improved? Is ---------an additi nal program really necessary?

(e) If the government decides to expand an existingSSE extension program or to launch a new one,what are its objectives? For example, on whatkind of SSE whl it foods its efforts (largeOrsmall; industri 1, commercial, or services; or aSpecific econom sub-sector in f given regionof the country).- Should the program work withnew or establi hed businesses, or both?

39

- 24 -

(f) Where will funding come from for'the.prograin (fromcentrayor,local government budgets, ,:rom theprivate sector, or from foreign sources)? Shouldspeci#1 taxes,be earmarked for the program's sup-port? Bette cathe program bemade self-sufficient r al st so (perhaps by charging SSEsand larg .firms f r iteservices), thus reducing,any d ndence on external financing?

(g) where will the extensionists for the program comefrom? Will they need only a primary school edu-cation? Will they be high school or universitygraduates? Should they have had prior experiencein managing small businesses themselves? If theyrequire further training, what kind will it be(classroom, field trips; on-the-job training)?

r(h) Should the consulting program start all at once,

with widespread coverage, or should some selectedadvisors and their consulting techniques be testedfor a year or so in.a pilot area?

(i) Is the management consultant to be a Peace CorpsVolunteer or an Economic Development Intern (inthe model discussed later on), or will someoneelse carry out a similar role? The followingquestions provide some guidelines for designerswho decide on this type of approach:

(1) What is the interest of the local sponsoringinstitution in receiving the consultant? Willthe entity provide him or her with officespace and other slUpport? In the case of anEDIP intern, will it eventually be able to payfully for services rendered?

(2) In addition to supervision, does the localinstitution provide the consultant with a coUterpart who will ideally replace the consul-tant after_hki or her departure? If not, woulda local university or trade school be interest--ed in recommending recent graduates for fur-ther training as extensionists by the consul-tant?

(3) Is the tiwing of the consultant's arrival inthe community propitious? Should situationslike a local political crisis or economicdepression postpone the person's arrival, orotherwise modify the program approach?

40

0

- 25 -

(4) Apart from the sponsoring institution, whichlocal organizations could the consultant helpmobilize to assist SSEs in looking out fortheir own interests? Are trade associations,chambers of commerce, or other business or-ganizations good possibilities?

0) Which government entities are already repre-sented in the community and working directlyor indirectly with SSEs? How, might the con-sultant constructively cooperate, rather thancompete, with such organizations in assistingSSEs?

(6) Is the consultant able to take a balanced ap-proach to his or her task? The consultantmay be tempted to one of two extremes: totake all program tasks upon him or herself,leaving little room for community participa-tion, or to do nothing unless he or she re-ceives explicit guidance from the local in-stitution. Ideally, the consultant should.stimulate local individuals and organizationsto more actively pursue their own interests,supplying expert advice when appropriate.Consequently, the personal role and ego in-volvement of the consultant in any programshould be downplayed, and the role of thelocal institution should be highlighted.

(7) How will the consultant's program be evalu-ated? It is best to establish objective quan7titative criteria which will set a goal forsuccess and a lower limit for failure. Con-sultancies do fail, often either because theynever should have been attempted with a givenclient or because the'consultant was inexpert.Therefore, evaluations are necessary to de-tect such failures (or successes) and thushelp prevent for assure) future replication.

rY

2. Focus and Purpose of Management Consultancy

A management consultant ultimately seeks to boost thereturn on investment to the small-scale enterprise by workingclosely with the owner-manager. This return is,normally ex-pressed in profits although it may also take the form ofsales growth or increased liquidity. In achieving this goal,the management consultant must rely on knowledge of account-ing, finance, marketing, personnel administration, planning,and tax and legal questions, plus a willingness to learn

41

- 26 -

about the basics of the technical aspects of theblient'sbusiness.'

Management consulting, with its reliance on skills inbusiness administration and human relations, is different fromtechnical assistance to a small firm. Technical advice relieson a consultant's knowledge of a technical skill or trade suchas engineering, construction, or metalworking; in small-scaleindustries such assistance would focus primarily on the pro-duction side of the business. Because of the unique and com-plementary skills each brings to the job, a management con-sultant and a technical advisor would make an ideal team inproviding comprehensive assistance to a small entrepreneur.

In assisting the small firm, the consultant shouldfollow a logical, predictable pattern which both eases thework and makes methods and recommendations understandable tothe client. A typical consulting work plan should probablyinclude the following steps:

(a) Diagnosis of the firm.

(b) Development of the objectives and requirementsof the consultancy.

(c) Review of present business operations.

(d) Development:of new methods to meet requirements.

(e) Evaluation of alternatives to establish the bestone for the client.

(f) Final written recommendations.

Ogl' Implementation of the recommendations.

(h) Evaluation and follow-up.

The last two stepi are normally beyond the consul-tant's complete control. This fact points to a basic frus-tration of contulting-ork--namely, the client is free toaccept or reject the consultant's advice. Or, the client mayaccept the consultant's recommendations but then lack thenecessary resources to. put them into practice. Nonetheless,if the consultant accurately diagnoses the client's interestsand resources before the start of the consultancy, at leastthe latter pitfall can often be avoided.

In developing a program, the consultant should decidewhether to concentrate assistance on new or established busi-nesses, or both. Generally, it is easier to work with ongoing

42

cs

- 27 -

businesses than with new ones. New firms lack a history uponwhich future plans can be based, and the owner and his or.herproduct have yet to be tested in the marketplace. Moreover,construction delays, financing shortfalls, and other logis-tical problems can complicate a new firm's start -up. There-fore, it is usually preferable to begin consulting with anestablished business which has a verifiable track record.The consultant may further decide to specialize in a givensmall business sector, such as retail trade or some subsectorof manufacturing, where his or her talents may be most ap-plicable.

Although it may be most effective to limit consult-ing efforts to target firms, this programming goal, like anyother, may be modified to meet field realities. Once in thefield, the sponsoring institution will probably expect theconsultant to assist a variety of local businesses, many of-which may not conform to programming criteria Yet consult-ing with a mix of large, very small, and target firm enter-prises is not necessarily something to )1p Avoided. All sizefirms play a role in local or regional development. Main- -

taining he health of selected larger firms (so that theycontin to purchase outputs from and provide inputs to SSEs)is of n as important to the deVelopment of SSEs as directasst tance to them. Larger firms can often serve as rolemo is for SSEs and the consultant will likely learn of ac-c nting and management systems which SSE target clients mayuse in a modified form as they grow. And successful workwith a few large companies can often serve to increase aconsultant's credibility among small-scale entrepreneurs.Selected micro-entrepreneurs, on the other hand, through asincere interest in learning how to make the best possibleuse of their more limited resources, may also make excellent -

use of consulting assistance and balance out the consultant's"portfolio".

3. Interdependence Between Consulting and Credit

The objectivity and confidentiality which a consul-tant develops with a client may be fruitless if resources arelacking to carry out the recommendations. Sinbe target firmsdo have some equity cushion, there are generally resourcesavailable for realizing the consultancy's goals. Yet if theconsultant recommends changes requiring a major influx ofcapital--such as the purchase of a new machine, or a.dou-.bling of sales necessitatkhg a major increase in cash tied upin ipventory or accounts receivable -- substantial outsidefiglincing may be required. External financial assistancemay therefore prove indispensable in helping the SSE imple-;ment the advisor's suggestions. Preferably, the management

43

- 28 -

consulting should precede the owner's request for credit.In fact, the consultant will typically perform cash projec-tions to assist the owner in his or her request for financing.

Since access to capital is usually a critical ingre-dient to realizing a consultant's recommendations, creditand management consulting assistance could be provided bythe same entity. For example, a development bank with asmall business loan department might provide both types ofassistance to small entrepreneurs. From a practical andprogramming standpoint, however, it is often preferable forthe two services to be supplied by different institutionswith a close referral relationship.

4. The Role of Management Consulting Assistance in aSmall-Seale Enterprise Development Program

The focus of this manual is on how to carry out amanagement consulting program to train small-scale entre-preneurs in developing countries through individualized man-agement consulting and a complementary group instruction ap-proach. The techniques outlined in this book possess fourmajor advantages over providing other inputs, and are adapt-able enough to be used in coordination with other approacheswhen necessary:

(a) Although developing countries do require addition-al resources, weak management of existing re-sources,is often a more serious problem. Thus,any program designed to improve general manage-ment skills would help to effectively addressthis constraint to development.

(b) Despite small entrepreneurs' naming inadequatecredit as their principal problem, poor manage-ment is probably the number one cause of businessfailure. Sound management advice provided in atimely fashion will likely not only diminish thehigh bankruptcy rate among struggling small busi-nesses, but will also help healthy SSEs expandmore rapidly, thus providing more of the generalsocial and economic benefits discussed in ChapterOne.

4),

(c) Management consulting offers at least a dual im-pact in assisting SSEs. While the consultanttrains the small business pclson (who can inturn share this newly acquired knowledge with his orher peers), the consultant, at the same time,is gaining valuable experience wh: :ch can be

44

f!- 29 -

applied in future consultancies. Furthermore, theconsultant's advice may also serve to .train otherprofessionals-..lawyers, accountants, and clerks- -who render valuable support services to SSEs.Such individuals often.gain valuable experiencein assisting SSEs by working together with theconsultant during the consultancy, and by provid-ing SSEs with more sophisticated services oncethe consultancy has ended.

(d) Individual management consulting services can beprovided on a cost-effective basis. Not only'foes this manual's Economic Development InternProgram (focusing on the target firm) fulfillthis criterion, but so do a number of other pro-.grams described briefly in this chapter, and inmore depth in Appendix iii, Exhibit A.

Cr.

5. Cross-Cultural .Considerations

Just as the consultant must be wise in business andinterpersonal skills, so he or she must be aware of culturalsurroundings_ and how these affect the management consultingtask. The SSE advisor must appreciate his or her culturalenvironment at two levels: first, the 'general'customs ofthe region or country, and seconds the'mix of politics, taboosand traditions peculiar to his or her own community.