Do Firms Choose Their Stock Liquidity? A Study of ...sofie2012/slides/Xiao.pdf · Do Firms Choose...

32

Do Firms Choose Their Stock Liquidity? A Study of Innovative Firms and Their Stock Liquidity Nishant Dass Vikram Nanda Steven C. Xiao

Transcript of Do Firms Choose Their Stock Liquidity? A Study of ...sofie2012/slides/Xiao.pdf · Do Firms Choose...

Do Firms Choose Their Stock Liquidity?

A Study of Innovative Firms and Their

Stock Liquidity

Nishant Dass

Vikram Nanda

Steven C. Xiao

Motivation

Stock liquidity is a desirable feature for some firms

Higher liquidity is associated with lower expected return on

assets and thus lower cost of capital (Amihud and

Mendelson,1986)

Liquid stock, which incorporates more information in the

price, plays a stronger role in monitoring the managers

(Holmström and Tirole, 1993)

However, not every firm may want or need liquidity –

facilitates market for corporate control; leakage of

proprietary information..

Motivation

Firms can adopt liquidity-enhancing policies to

improve liquidity

- Amihud and Mendelson (2000) suggest a number

of means to increase stock liquidity including

increasing investor base and reducing information

asymmetry.

- Many papers have linked changes in liquidity to

firm actions such as equity issuance

Motivation

However, evidence documenting the efforts of

firms to improve the stock liquidity is lacking

We ask whether firms choose stock liquidity

by studying a group of firms that, we contend,

are more reliant on equity financing:

innovative firms

Motivation

Firms with focus on innovation produce unique

products

– Firms with unique products will have greater ripple

effects of bankruptcy on their customers, suppliers,

and workers. (Titman, 1984; Titman, Wessels, 1988)

Innovative firms tend to have more intangible assets

which have lower collateral value

Therefore, innovative firms will have lower leverage

ratios and more reliant on equity financing

Motivation

We classify firms as innovative either by their

investments in R&D or number of patents/citations

Intuitively, one would expect innovative firms to

have lower stock liquidity as their assets are

informationally more opaque to the market

However, we find that innovative firms are positively

associated with stock liquidity, suggesting that these

firms might be taking deliberate actions to improve

their stock liquidity.

Motivation: Summary of Findings

We identify that innovative firms indeed take actions that are

known to improve liquidity:

- Issue more frequent guidance (Coller and Yohn, 1997)

- More likely to do stock splits (Muscarella and Vetsuypens, 1996;

Lin, Singh and Yu, 2009)

- More likely to make SEOs (Eckbo et al., 2000; and Kothare,

1997)

- More likely to hire reputed underwriter (Amihud and

Mendelson, 1988; Ellis, Michaely and O’Hara, 2000)

- More likely to have option listed (Mayhew and Mihov, 2004)

More importantly, these actions do help innovative firms

improve their stock liquidity

Motivation: Summary of Findings (cont)

An exogenous increase in liquidity improves firm value

and such effect is stronger for innovative firms

- we find that this stronger effect is concentrated among

innovative firms with more equity-based compensation

Innovative firms are more likely to have access to

public debt, higher credit rating, and fewer

(quantitative) covenants in bank loans

The role of monitoring is taken by equity holders

- Innovative firms are associated with higher institutional

ownership, higher likelihood of a blockholder, and higher

equity-based compensation for managers

Hypotheses

H1: Innovative firms have greater stock liquidity but

less so when they have access to alternative sources

of capital or less financially constrained

H2: Innovative firms will take deliberate actions that

are known to improve stock liquidity

H3: The impact of a marginal increase in liquidity on

value (Tobin’s Q) would be greater for innovative

firms

Data: Dependent Variables

Four proxies for stock illiquidity

Amihud’s (2002) Illiquidity:

Negative Turnover:

Data: Dependent Variables

Bid-Ask Spread:

Probability of Informed Trading (PIN) by Easley, Kiefer,

O’Hara, and Paperman (1996)

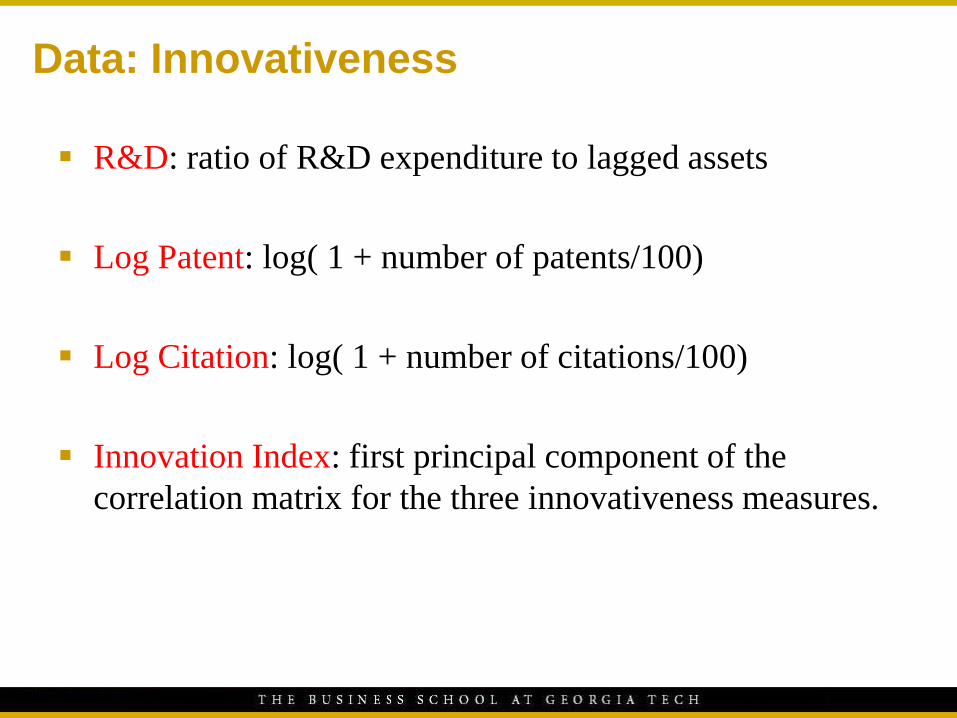

Data: Innovativeness

R&D: ratio of R&D expenditure to lagged assets

Log Patent: log( 1 + number of patents/100)

Log Citation: log( 1 + number of citations/100)

Innovation Index: first principal component of the

correlation matrix for the three innovativeness measures.

Empirical Analysis: H1

To confirm the negative association between

innovativeness and illiquidity, we estimate the

following model:

Firm characteristics includes: Log Assets, Leverage, Cash,

Tobin’s Q, NYSE Dummy, ROA, Tangibility, Firm’s Age,

Return Volatility

Empirical Analysis: H1

Empirical Analysis: H1

H1: Innovative firms have greater stock liquidity but

less so when they have access to alternative sources

of capital

Test whether relationship between innovativeness and

illiquidity is weaker when firms have access to public

debt, high market power, and pay dividend:

Empirical Analysis: H1

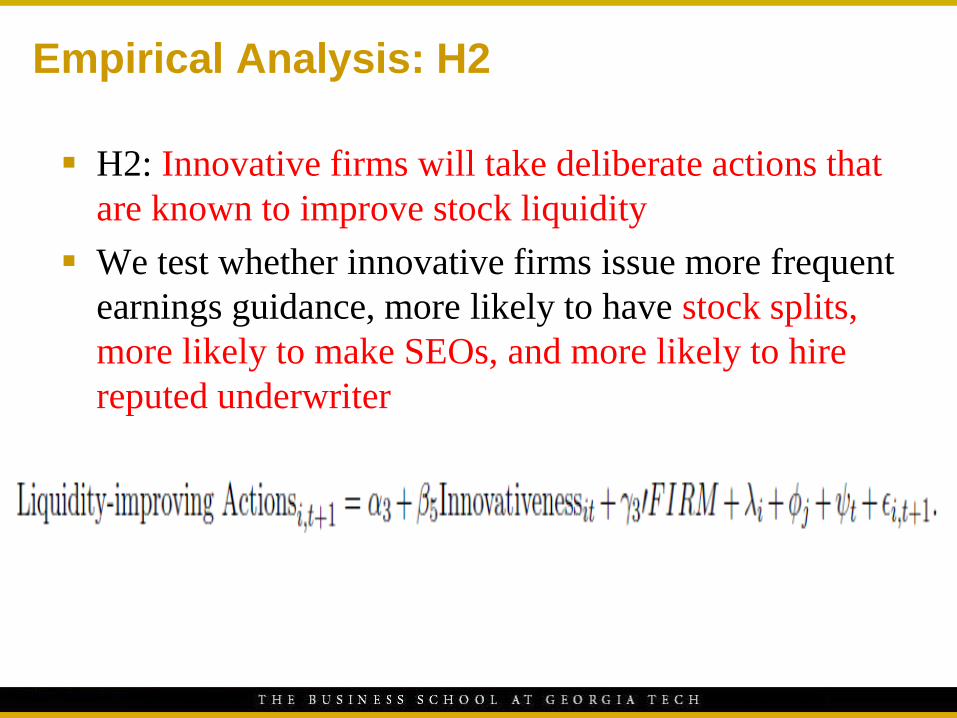

Empirical Analysis: H2

H2: Innovative firms will take deliberate actions that

are known to improve stock liquidity

We test whether innovative firms issue more frequent

earnings guidance, more likely to have stock splits,

more likely to make SEOs, and more likely to hire

reputed underwriter

Empirical Analysis: H2

Empirical Analysis: H2

H2: Innovative firms will take deliberate actions that

are known to improve stock liquidity

We test whether these actions indeed improve stock

liquidity

We instrument actions with industry median (or

mean) of these action variables to rule out

endogenous decisions

Empirical Analysis: H2

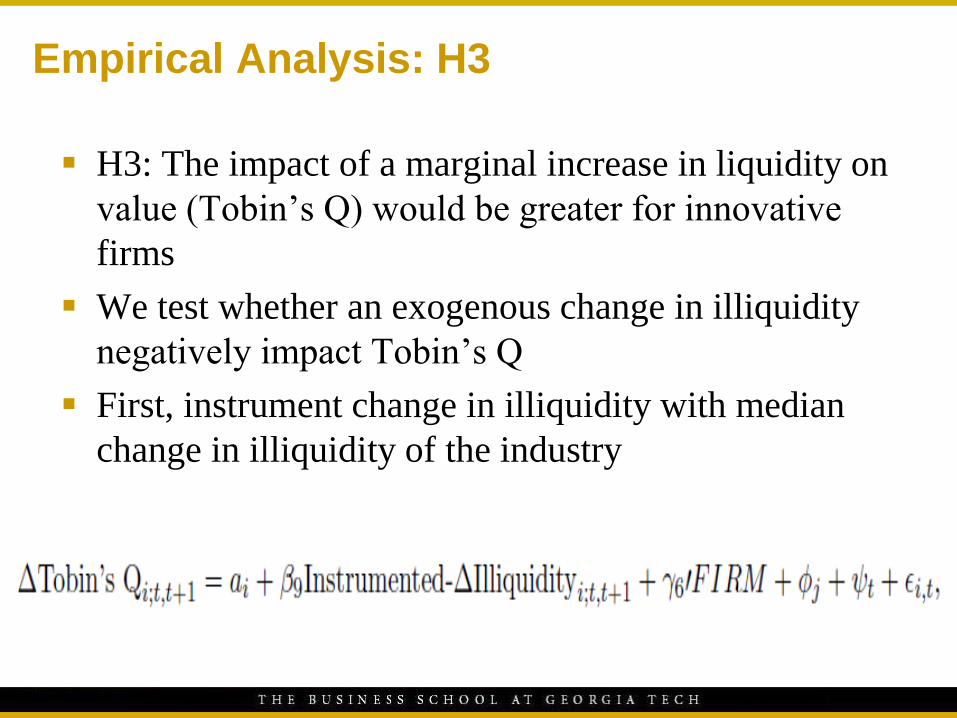

Empirical Analysis: H3

H3: The impact of a marginal increase in liquidity on

value (Tobin’s Q) would be greater for innovative

firms

We test whether an exogenous change in illiquidity

negatively impact Tobin’s Q

First, instrument change in illiquidity with median

change in illiquidity of the industry

Empirical Analysis: H3

Empirical Analysis: H3

Second, we look at an exogenous shocks to the firms’

stock illiquidity -- decimalization

Specifically, we test whether change in illiquidity

surrounding decimalization negatively impact firm

value

Empirical Analysis: H3

Empirical Analysis: Debt of Innovative Firms

What type of debt financing do innovative firms

prefer?

We argue that attempts of innovative firms at

mitigating the information asymmetry in stock

market benefit them in the debt markets

Firm also lower the information asymmetry by

generating information in the public debt markets

Due to lower leverage ratio, innovative firms should

receive favorably from creditors

Empirical Analysis: Debt of Innovative Firms

We find that innovative firms:

- Are more likely to have public debt

- Higher credit rating

- Fewer (quantitative) loan covenants

Empirical Analysis: Who Monitors Innovative Firms?

Innovative firms have lower leverage ratio and

fewer covenants in their bank loans

Due to reliance on equity financing, equity

holders assume the role of monitoring

We find that innovative firms have greater

institutional ownership, more likely to have

blockholders, and higher equity-based

compensation

Empirical Analysis: Who Monitors Innovative Firms?

Empirical Analysis: Does Incentive Contract Help?

Innovative firms, whose assets and managers’ decisions

are more opaque, benefit more from incentive contract

We examine whether value effect of liquidity is greater

for innovative firms with high equity-based

compensation

We test this again with the exogenous shock to liquidity

(decimalization)

Empirical Analysis: Does Incentive Contract Help?

Concluding Remarks

Innovative firms are positively associated with

stock liquidity

Innovative firms take actions to improve

liquidity and these actions do work

Innovative firms benefit more than others by

having higher stock liquidity in terms of firm

value

Concluding Remarks

Innovative firms return to public capital

markets, which helps reduce information

asymmetry; their private debt is less likely to

have covenant or fewer covenants if any

Equity-holders assume the role of monitoring

innovative firms

As innovative firms have greater incentive

contract, an exogenous decrease in illiquidity

increases firms’ value more than other firms,

consistent with the argument of Holström and

Tirole