DMP Power Shifts

15

1 © 2014 Deloitte Development LLC. All rights reserved. Member of Deloitte Touche Tohmatsu Limited Power Shifts How Low Gas Prices, Renewables and Environmental Regulations are changing the Electric Power Industry

Transcript of DMP Power Shifts

1 © 2014 Deloitte Development LLC. All rights reserved. Member of Deloitte Touche Tohmatsu Limited

Power Shifts How Low Gas Prices, Renewables and Environmental Regulations are changing the Electric Power Industry

2 © 2014 Deloitte Development LLC. All rights reserved. Member of Deloitte Touche Tohmatsu Limited

Abstract

The investor owned utility business model and its companion the regulatory compact have served the

electric power industry well for nearly a century. It worked by balancing the interests of shareholders

eager for a fair return on their invested capital in exchange for an independent ratemaking authority

that suggested that just and reasonable rates were set fairly allocating the costs and revenue

requirements across customer classes. In exchange for this balancing of interests the utility accepted an

obligation to serve all customers and to provide reliable service. When contentious issues arose the

parties deferred to a quasi-judicial regulatory hearings process.

But this is not about the history of the electric power industry or its

regulation but rather it’s the emerging shape of the electric power

sector’s future. So what should we expect?

The future environment for the industry is the nexus of ruthless economic pressures of low natural gas

prices, comprehensive renewable energy portfolio standards, low load growth, and new environmental

regulations. The last time this type of power shift took place it gave rise to the FERC-regulated

wholesale merchant generation segment that dominates power plant construction and operation today.

3 © 2014 Deloitte Development LLC. All rights reserved. Member of Deloitte Touche Tohmatsu Limited

This is the second in a series of research whitepapers prepared by Deloitte MarketPoint based upon the

results of its North American Integrated Energy Markets Reference Case analysis of how these factors

are causing power shifts in market fundamentals, transformational changes in technology, regulation

and their implications for the electric power industry.

The first paper in the series “How Achievable are Renewable Portfolio Standards?” explored the

implications of growing wind and solar resources on the fuel mix, embedded cost, reliability and reserve

margins and whether the market infrastructure could actually support the projects. Some of those

themes are revisited here as they play out in interfuel competition and the search for equilibrium as big

shifts continue to transform electricity markets at both wholesale and retail, generation and energy

delivery, state rate-regulated and FERC-regulated levels.

Ten Power Shift drivers are changing North American Integrated Markets: 1. Many US markets have excess capacity even with 30 GW of Coal Plant Retirements since 2010

2. Loss of baseload coal and nuclear capacity in several Canadian power markets

3. Aggressive US Renewable Portfolio Standards are not likely to be met as scheduled in several states

4. The next generation of power plants have already been built ---in the previous boom cycle of the

market

5. Gas demand for power generation is expected to be flat to slow growing through 2025

6. Low gas prices undermine the economics of building new renewable as well as thermal capacity

7. Reliability is could be challenged from loss of baseload generation and increase in intermittent

renewables and just in time fuel

8. Growing dependence upon gas fired generation increases probability of price volatility

9. Utility business model is challenged by distributed energy and net metering

10. Real-time pricing threatens to disrupt customers by moving away from average cost pricing

For more insight about regional power market fundamentals and the inter-fuel competition at work in

today’s energy markets, see the North American Integrated Energy Markets Reference Case advisory

service and other papers in this series or contact Deloitte MarketPoint.

www.deloittemarketpoint.com

4 © 2014 Deloitte Development LLC. All rights reserved. Member of Deloitte Touche Tohmatsu Limited

Introduction The first Power Shift began with environmental concerns over acid rain, smog and later carbon

emissions along with concerns about energy efficiency and conservation that evolved into renewable

portfolio standards to expand the market share of wind and solar energy and more recently to

greenhouse gas emissions reduction policy goals and proposed US EPA regulations.1

The second Power Shift at work affected the utility business model and began in the late 1970’s when

rising inflation eroded the economics of new power plant construction – especially nuclear power after

the Three Mile Island accident.2 Until then, each new power plant built reduced the average cost of

service and thus rates. That virtuous circle turned vicious when inflation and regulatory delays caused

power plant construction costs to skyrocket.

Public reactions to rate spikes and regulator reactions to power plant construction cost increases and

delays in construction schedule resulted in the third phase of the Power Shift as regulators ordered

changes in industry structure breaking up the vertical energy company monopoly by introducing

competition (1978 PURPA), regulated energy delivery in the wires and pipes business segment (1992

EPAct), and arm’s length transmission operation and the independent system operator (ISO) formation

process to improve access and cost allocation and energy competition in many markets (FERC 888, 889,

and 2000).3

So what are the factors driving the next phase in the Power Shift in the electric power industry?

1. Is Abundant, Low Priced Natural Gas Crowding Out Fuel Competition?

2. How Achievable are Renewable Portfolio Standards?

3. Will Weak Demand Leave Utilities and Merchant Power Generators Starving for Growth?

This paper frames the progression of factors driving in this fourth phase of the Power Shift for the

electric power industry including the growth of renewable energy to meet RPS targets combined with

low natural gas prices, regulatory changes designed to reduce greenhouse gas emissions and all within a

low growth environment. These shifts reflect the implications for market equilibrium of what must be

built (renewable energy), what can no longer pragmatically be built (new coal fired generation) and

what’s left. What’s left is essentially demand response and efficiency to optimize the performance of a

portfolio or a regional market and, when new capacity is required for grid reliability, more likely than not

will be gas fired generation if the economics for new power plant construction make such units

profitable.

1 US EPA Climate Change Initiatives and Regulatory Proposals.

2 Cohen, Bernard L., University of Pittsburgh, Plenum Press, 1990, Chapter 9, The Nuclear Option What Went Wrong?

http://www.phyast.pitt.edu/~blc/book/chapter9.html 3 Report to Congress on Competition in Wholesale and Retail Energy Markets.

5 © 2014 Deloitte Development LLC. All rights reserved. Member of Deloitte Touche Tohmatsu Limited

What’s left is also the source of a new type of power customer, especially commercial and industrial

customers who seek to take control of their energy costs and manage their energy use strategy in ways

that are predictable, affordable, sustainable and flexible.

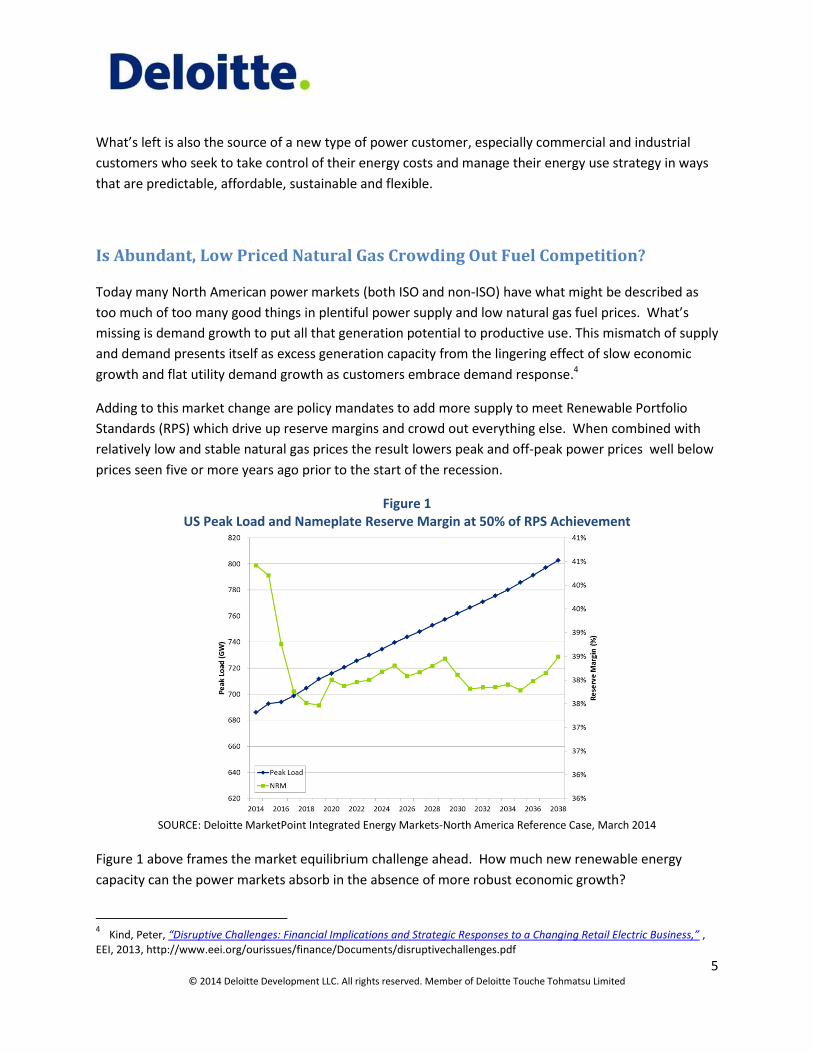

Is Abundant, Low Priced Natural Gas Crowding Out Fuel Competition? Today many North American power markets (both ISO and non-ISO) have what might be described as

too much of too many good things in plentiful power supply and low natural gas fuel prices. What’s

missing is demand growth to put all that generation potential to productive use. This mismatch of supply

and demand presents itself as excess generation capacity from the lingering effect of slow economic

growth and flat utility demand growth as customers embrace demand response.4

Adding to this market change are policy mandates to add more supply to meet Renewable Portfolio

Standards (RPS) which drive up reserve margins and crowd out everything else. When combined with

relatively low and stable natural gas prices the result lowers peak and off-peak power prices well below

prices seen five or more years ago prior to the start of the recession.

Figure 1 US Peak Load and Nameplate Reserve Margin at 50% of RPS Achievement

SOURCE: Deloitte MarketPoint Integrated Energy Markets-North America Reference Case, March 2014

Figure 1 above frames the market equilibrium challenge ahead. How much new renewable energy

capacity can the power markets absorb in the absence of more robust economic growth?

4 Kind, Peter, “Disruptive Challenges: Financial Implications and Strategic Responses to a Changing Retail Electric Business,” ,

EEI, 2013, http://www.eei.org/ourissues/finance/Documents/disruptivechallenges.pdf

6 © 2014 Deloitte Development LLC. All rights reserved. Member of Deloitte Touche Tohmatsu Limited

From 2014 to about 2019 the answer appears to be that retiring coal generation capacity will largely be

replaced by wind and solar projects under RPS. By 2020 reserve margins based on nameplate capacity

grow substantially and remain high hovering around 38% over the forecast period. Since the

contribution to capacity from intermittent sources such as wind during peak demand can be much less

than nameplate, the dependable reserve margin is numerically lower – much lower. By applying

renewable de-rating factors for wind, hydro, and solar, the "dependable" reserve margin eventually falls

for a steady level of around 17%.

However, the substantial increase in wind capacity and energy has implications beyond just raising the

apparent reserve margin. The generation at very low marginal cost reduces overall power prices,

particularly during periods of high wind generation such as during off-peak hours and in shoulder

months.

Figure 2 shows capacity additions with new renewable generation projected to meet only 50% state RPS

requirements. The Deloitte MarketPoint analysis suggests that some of the renewable energy capacity

mandated by the states cannot economically be built due to a variety of factors including limitations on

turbine manufacturing, installation labor, related equipment, suitable sites, and permitting make

achieving even these levels difficult, leaving the potential for further RPS reductions or deadline

extensions.

Figure 2

US Capacity Changes

SOURCE: Deloitte MarketPoint Integrated Energy Markets-North America Reference Case, March 2014

Reserve margin growth and more mandated renewable capacity are expected to depress wholesale

profit margins enough that new gas-fired generation might be uneconomic in many regions. Merchant

generators worry that persistently low power prices will force the retirement of more existing power

7 © 2014 Deloitte Development LLC. All rights reserved. Member of Deloitte Touche Tohmatsu Limited

generation units beyond coal. Particularly vulnerable are older gas fired generation and possibly some

nuclear plants.

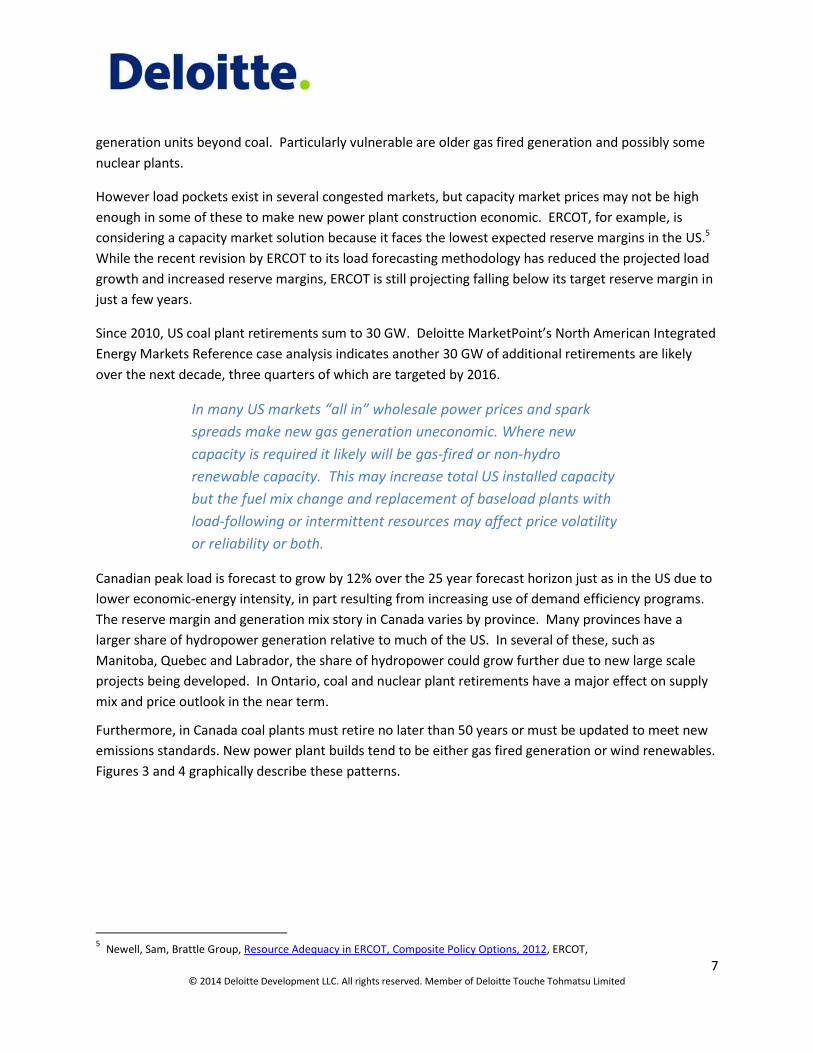

However load pockets exist in several congested markets, but capacity market prices may not be high

enough in some of these to make new power plant construction economic. ERCOT, for example, is

considering a capacity market solution because it faces the lowest expected reserve margins in the US.5

While the recent revision by ERCOT to its load forecasting methodology has reduced the projected load

growth and increased reserve margins, ERCOT is still projecting falling below its target reserve margin in

just a few years.

Since 2010, US coal plant retirements sum to 30 GW. Deloitte MarketPoint’s North American Integrated

Energy Markets Reference case analysis indicates another 30 GW of additional retirements are likely

over the next decade, three quarters of which are targeted by 2016.

In many US markets “all in” wholesale power prices and spark

spreads make new gas generation uneconomic. Where new

capacity is required it likely will be gas-fired or non-hydro

renewable capacity. This may increase total US installed capacity

but the fuel mix change and replacement of baseload plants with

load-following or intermittent resources may affect price volatility

or reliability or both.

Canadian peak load is forecast to grow by 12% over the 25 year forecast horizon just as in the US due to

lower economic-energy intensity, in part resulting from increasing use of demand efficiency programs.

The reserve margin and generation mix story in Canada varies by province. Many provinces have a

larger share of hydropower generation relative to much of the US. In several of these, such as

Manitoba, Quebec and Labrador, the share of hydropower could grow further due to new large scale

projects being developed. In Ontario, coal and nuclear plant retirements have a major effect on supply

mix and price outlook in the near term.

Furthermore, in Canada coal plants must retire no later than 50 years or must be updated to meet new

emissions standards. New power plant builds tend to be either gas fired generation or wind renewables.

Figures 3 and 4 graphically describe these patterns.

5 Newell, Sam, Brattle Group, Resource Adequacy in ERCOT, Composite Policy Options, 2012, ERCOT,

8 © 2014 Deloitte Development LLC. All rights reserved. Member of Deloitte Touche Tohmatsu Limited

Figure 3

Canadian Reserve Margin

SOURCE: Deloitte MarketPoint Integrated Energy Markets-North America Reference Case, March 2014

Figure 4

Canadian Capacity Changes

SOURCE: Deloitte MarketPoint Integrated Energy Markets-North America Reference Case, March 2014

9 © 2014 Deloitte Development LLC. All rights reserved. Member of Deloitte Touche Tohmatsu Limited

How Achievable are Renewable Portfolio Standards? Twenty-nine states adopted renewable portfolio standards (RPS) programs. Eight other states set goals for renewable generation. In states with RPS, targets typically reach 20% renewable generation as a percent of load by 2020. California has a more aggressive target to reach 33% by 2020. While there is broad public support for clean energy goals, Deloitte MarketPoint’s analysis of RPS targets and goals suggests that many state program goals are not likely to be met, at least in the time frames set, due to unfavorable economic conditions, poor regional wind or solar regimes, and lack of suitable land on which to site and build projects. But existing RPS programs have resulted in significant growth of new renewable capacity. To test how achievable reaching the full RPS targets might be, Deloitte MarketPoint’s March 2014 North American Integrated Energy Markets Reference Case simulated two target RPS scenarios at 100% and 50% of the RPS target. Separate analysis found that 50% was a reasonable level of RPS target achievement across the states although other scenarios are possible. Of course, there are substantial regional variations. As is typical with model simulations, assumptions are used to guide analysis. For example, Deloitte MarketPoint assumes current laws and regulations will continue and where there are uncertainties, scenarios are used as a standard analytics practice method so clients can assess the implications of differences themselves. Based upon the Deloitte MarketPoint Reference Case analysis, total RPS investment cost between 2014 and 2020 is estimated to range from $50 billion in the Reference Case (at the assumed 50% RPS achievement level) to as much as $128 billion under the 100% RPS Target Scenario.

With abundant and low cost natural gas prices, the “all in” wholesale electricity price projection remains modest for much of the reference case horizon. Since low expected power prices will not make new renewable generation projects economic, additional subsidies in the form of Renewable Energy Credits, Feed-In Tariffs or Production Tax Credits, will need to be high enough for investors to cover their cost and earn a return on their investment. It isn’t just the amount of new wind and solar capacity that needs to be added for state RPS targets, but it’s also the accelerated rate that these programs require that make achieving RPS programs problematic.

10 © 2014 Deloitte Development LLC. All rights reserved. Member of Deloitte Touche Tohmatsu Limited

Figure 5 Growth of Renewable Generation

SOURCE: Deloitte MarketPoint Integrated Energy Markets-North America Reference Case, March 2014

Figure 5 shows the growth in wind and solar generation under the Reference Case (50% RPS Target) and 100% RPS Target cases. The remainder of the renewables targets, roughly equal to 20% of load is from hydro generation (where it qualifies). To meet RPS targets, most of the build out needs to occur by 2020 with at least a doubling of the current amount of generation.

The Deloitte MarketPoint Reference Case skepticism about achieving RPS targets is not just the size and pace at which RPS programs must be implemented, but it is also one of cost. Putting aside operational and integration cost to ISOs, RTOs, and utilities, renewable generation is relatively costly, compared with other technologies when availability and utilization are taken into account.

Deloitte MarketPoint Reference Case overnight wind capital cost assumptions range from $1100/kw to $1900/kw in more expensive regions. These values are on a nameplate basis for on-shore wind capacity and have also been in decline over the past two decades, in part due the increase in turbine size and scale of the projects. However, our expectation is that continuous declining capital cost for wind projects will likely moderate as efficiencies, and the sheer size of the projects will likely be capped. Furthermore our analysis does not consider the impact of aggressive build out patterns inflating labor and materials costs which would likely occur to some degree.

Although these costs are roughly in alignment with the cost of a new Combined Cycle Gas Turbine (CCGT), the availability and utilization for renewables such as wind is only on average 25% - 35% compared with as much as 90% availability for a CCGT plant. This affects plant economics greatly.

11 © 2014 Deloitte Development LLC. All rights reserved. Member of Deloitte Touche Tohmatsu Limited

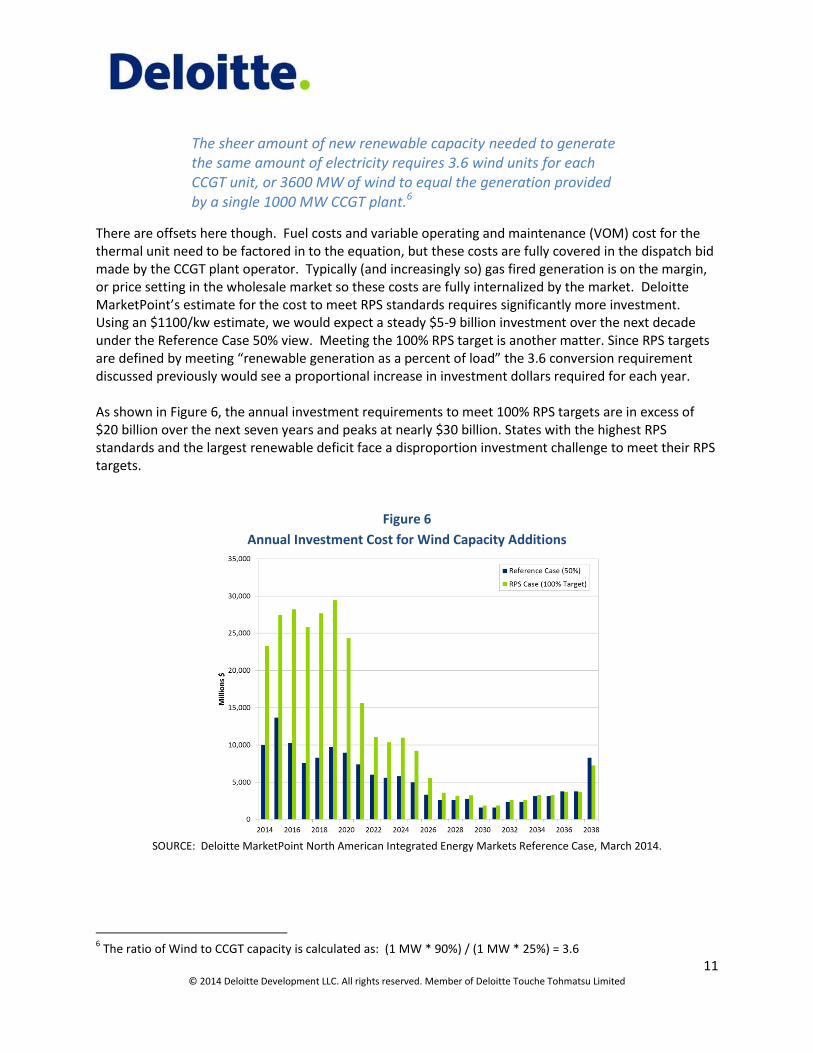

The sheer amount of new renewable capacity needed to generate the same amount of electricity requires 3.6 wind units for each CCGT unit, or 3600 MW of wind to equal the generation provided by a single 1000 MW CCGT plant.6

There are offsets here though. Fuel costs and variable operating and maintenance (VOM) cost for the thermal unit need to be factored in to the equation, but these costs are fully covered in the dispatch bid made by the CCGT plant operator. Typically (and increasingly so) gas fired generation is on the margin, or price setting in the wholesale market so these costs are fully internalized by the market. Deloitte MarketPoint’s estimate for the cost to meet RPS standards requires significantly more investment. Using an $1100/kw estimate, we would expect a steady $5-9 billion investment over the next decade under the Reference Case 50% view. Meeting the 100% RPS target is another matter. Since RPS targets are defined by meeting “renewable generation as a percent of load” the 3.6 conversion requirement discussed previously would see a proportional increase in investment dollars required for each year. As shown in Figure 6, the annual investment requirements to meet 100% RPS targets are in excess of $20 billion over the next seven years and peaks at nearly $30 billion. States with the highest RPS standards and the largest renewable deficit face a disproportion investment challenge to meet their RPS targets.

Figure 6

Annual Investment Cost for Wind Capacity Additions

SOURCE: Deloitte MarketPoint North American Integrated Energy Markets Reference Case, March 2014.

6 The ratio of Wind to CCGT capacity is calculated as: (1 MW * 90%) / (1 MW * 25%) = 3.6

12 © 2014 Deloitte Development LLC. All rights reserved. Member of Deloitte Touche Tohmatsu Limited

Will Weak Demand Leave Utilities and Merchant Generators Starving for Growth? Low natural gas prices in the US are expected to maintain their current trend for the next 3 years. US gas demand growth is primarily driven by growth in power generation. In Canada, gas demand growth is projected to be primarily driven by natural gas use in oil sands production and for electric generation. In Mexico, gas demand is expected to increase from growth in power generation and industrial manufacturing growth taking advantage of Mexico’s favorable labor wage rates. But the larger US economy has yet to see the strong economic growth in manufacturing that low gas prices are expected to encourage

Significant fuel switching takes place in the power generation sector and rapid retirement of older coal generating plants due to environmental regulations like MACT and the eventual replacement for CSAPR causes gas demand to grow, at about 1% per year.

The result is that investor owned utilities and merchant power generators are starving for growth in markets where RPS mandates are required to be met thus crowding out both marginal existing power plants of all fuel types just as they undermine the economics of new power plant construction making them unprofitable to build. There is significant structural fuel switching in the US power generation sector. Rapid retirement of older coal generating plants due to environmental regulations like MACT and the eventual replacement for CSAPR causes gas demand to grow, at about 1% per year, but the combined impact of RPS mandates, higher reserve margins from all that renewable energy and low natural gas prices is crowding out new power plants except for renewables.

At the same time, commercial and industrial customers are using this opportunity to control their future energy costs with combined heat and power projects, more energy efficiency and a focus on sustainability strategies that seek to proactively manage energy spend. The preferred route for growth on the residential side sees vendors of solar rooftop systems use zero-down financing, solar leases, avoided cost sell-back regulations and tax credits to build the market share of solar neighborhood by neighborhood, and community by community. Microgrids are also emerging as a competitive threat to utility demand growth and customer empowerment. Microgrids focus on a combination of supply side and demand response programs to enable a group of customers or a commercial or industrial complex to be as self-sufficient or ‘off-grid’ as possible. Smart meter and smarter grid technologies enable microgrids to function smoothly without adversely affecting either customer or grid reliability. Taken together these customer-driven strategies are a clear part of the big power shift underway in the electric power industry.

13 © 2014 Deloitte Development LLC. All rights reserved. Member of Deloitte Touche Tohmatsu Limited

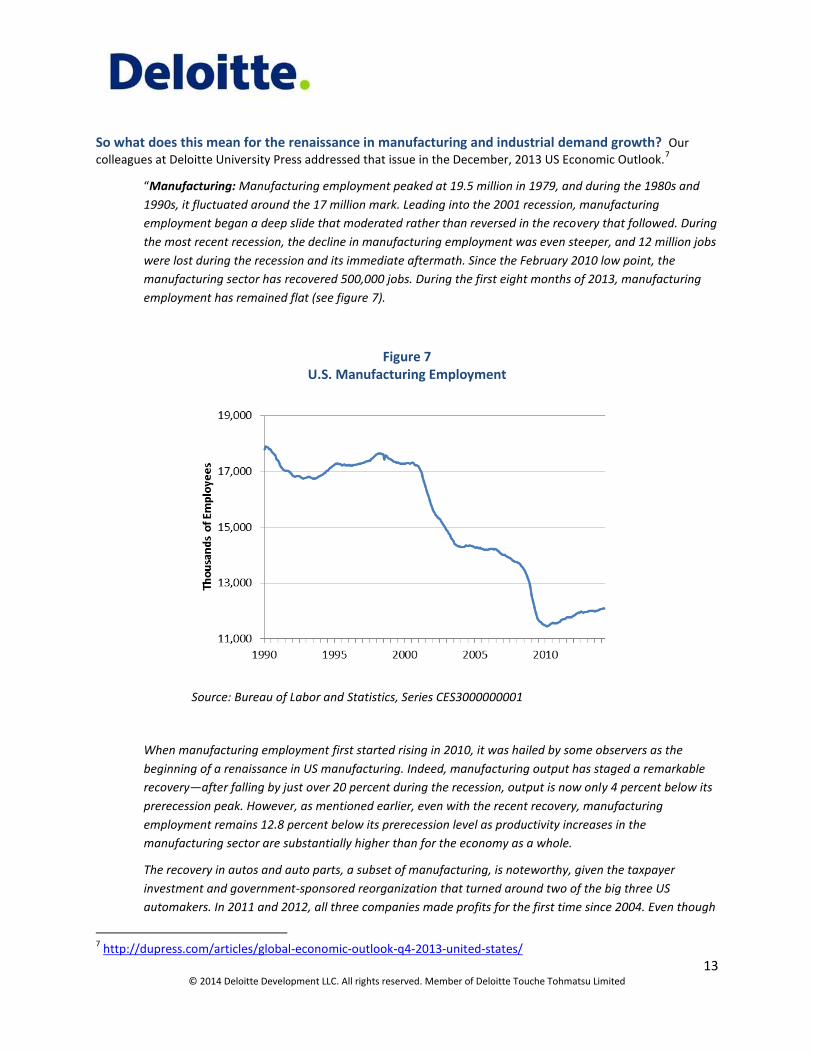

So what does this mean for the renaissance in manufacturing and industrial demand growth? Our

colleagues at Deloitte University Press addressed that issue in the December, 2013 US Economic Outlook.7

“Manufacturing: Manufacturing employment peaked at 19.5 million in 1979, and during the 1980s and

1990s, it fluctuated around the 17 million mark. Leading into the 2001 recession, manufacturing

employment began a deep slide that moderated rather than reversed in the recovery that followed. During

the most recent recession, the decline in manufacturing employment was even steeper, and 12 million jobs

were lost during the recession and its immediate aftermath. Since the February 2010 low point, the

manufacturing sector has recovered 500,000 jobs. During the first eight months of 2013, manufacturing

employment has remained flat (see figure 7).

Figure 7 U.S. Manufacturing Employment

Source: Bureau of Labor and Statistics, Series CES3000000001

When manufacturing employment first started rising in 2010, it was hailed by some observers as the

beginning of a renaissance in US manufacturing. Indeed, manufacturing output has staged a remarkable

recovery—after falling by just over 20 percent during the recession, output is now only 4 percent below its

prerecession peak. However, as mentioned earlier, even with the recent recovery, manufacturing

employment remains 12.8 percent below its prerecession level as productivity increases in the

manufacturing sector are substantially higher than for the economy as a whole.

The recovery in autos and auto parts, a subset of manufacturing, is noteworthy, given the taxpayer

investment and government-sponsored reorganization that turned around two of the big three US

automakers. In 2011 and 2012, all three companies made profits for the first time since 2004. Even though

7 http://dupress.com/articles/global-economic-outlook-q4-2013-united-states/

14 © 2014 Deloitte Development LLC. All rights reserved. Member of Deloitte Touche Tohmatsu Limited

employment in auto and auto parts accounts for less than 7 percent of manufacturing employment, this

subsector accounted for 31 percent of the 503,000 manufacturing jobs created since manufacturing

employment’s low point in February 2010.

As the manufacturing sector continues to recover and expand, it should be able to continue generating

jobs; falling energy prices and a large consumer market make the US an attractive place to manufacture.

However, high productivity will limit the size of employment growth in this sector.

15 © 2014 Deloitte Development LLC. All rights reserved. Member of Deloitte Touche Tohmatsu Limited

About Deloitte MarketPoint Reference Cases.

North American Integrated Energy Markets and other Deloitte MarketPoint Reference Cases provides independent and consistent views of oil, gas and power markets, built up from the regional level to provide a global perspective. Each Reference Case includes deliverables you need -- summary of the analysis, insights, data files, presentation decks -- plus the unique ability to play what-if scenarios with your data to create your own forecasts. Unlike traditional forecast services, our Reference Cases are delivered live on the interactive MarketBuilder platform to put our highly transparent, granular and easily configurable models at your fingertips.

About Deloitte MarketPoint

Deloitte MarketPoint is a leading provider of energy resource economics, market fundamental analysis and strategic insight for the global oil, gas and power markets. MarketPoint helps clients frame the uncertainty in their economic future. Using cutting-edge technologies, we offer actionable decision support solutions that capture the way world markets actually work. www.deloittemarketpoint.com

This publication is solely for informational purposes. Where the results of analysis are discussed in this publication, the results are based on the application of economic logic and specific assumptions. These results are not intended to be predictions of events or future outcomes. Deloitte MarketPoint is not, by means of this publication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services to any person. This publication is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor. Deloitte MarketPoint shall not be responsible for any loss sustained by any person who uses or relies on this publication.