Divorce Cases: Uncovering Critical Information in Tax ...

106

Divorce Cases: Uncovering Critical Information in Tax Returns and Financial Statements Discovery Strategies, Analyzing Tax Returns and Financial Documents, Using Financial Experts Today’s faculty features: 1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 1. THURSDAY, APRIL 29, 2021 Presenting a live 90-minute webinar with interactive Q&A William P. Allen, Partner, Brisbane Consulting Group, Buffalo, NY Mark S. Gottlieb, CPA/ABV/CFF, ASA, CVA, CBA, MST, Mark S. Gottlieb, CPA, PC, New York, NY Valentina Shaknes, Partner, Krauss Shaknes Tallentire & Messeri LLP, Greenwich, CT

Transcript of Divorce Cases: Uncovering Critical Information in Tax ...

Divorce Cases: Uncovering Critical Information in Tax Returns and Financial StatementsDiscovery Strategies, Analyzing Tax Returns and Financial Documents, Using Financial Experts

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 1.

THURSDAY, APRIL 29, 2021

Presenting a live 90-minute webinar with interactive Q&A

William P. Allen, Partner, Brisbane Consulting Group, Buffalo, NY

Mark S. Gottlieb, CPA/ABV/CFF, ASA, CVA, CBA, MST, Mark S. Gottlieb, CPA, PC, New York, NY

Valentina Shaknes, Partner, Krauss Shaknes Tallentire & Messeri LLP, Greenwich, CT

Tips for Optimal Quality

Sound QualityIf you are listening via your computer speakers, please note that the quality of your sound will vary depending on the speed and quality of your internet connection.

If the sound quality is not satisfactory, you may listen via the phone: dial 1-877-447-0294 and enter your Conference ID and PIN when prompted.Otherwise, please send us a chat or e-mail [email protected] immediatelyso we can address the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing QualityTo maximize your screen, press the ‘Full Screen’ symbol located on the bottom right of the slides. To exit full screen, press the Esc button.

FOR LIVE EVENT ONLY

Continuing Education Credits

In order for us to process your continuing education credit, you must confirm your participation in this webinar by completing and submitting the Attendance Affirmation/Evaluation after the webinar.

A link to the Attendance Affirmation/Evaluation will be in the thank you email that you will receive immediately following the program.

For additional information about continuing education, call us at 1-800-926-7926 ext. 2.

FOR LIVE EVENT ONLY

Program Materials

If you have not printed the conference materials for this program, please complete the following steps:

• Click on the link to the PDF of the slides for today’s program, which is located to the right of the slides, just above the Q&A box.

• The PDF will open a separate tab/window. Print the slides by clicking on the printer icon.

FOR LIVE EVENT ONLY

PERSONAL INCOME TAX RETURNS:IRS FORM 1040

Informational Disclosures no longer have line numbers

(A) Filing Status Moved to Top of Page

(B) Cryptocurrency question moved from Schedule 1

(A) Detail for Schedule C, Schedule E, and Schedule E, Page 2 on Schedule 1

(B) Qualified Business Income (QBI) Deduction – Line 13

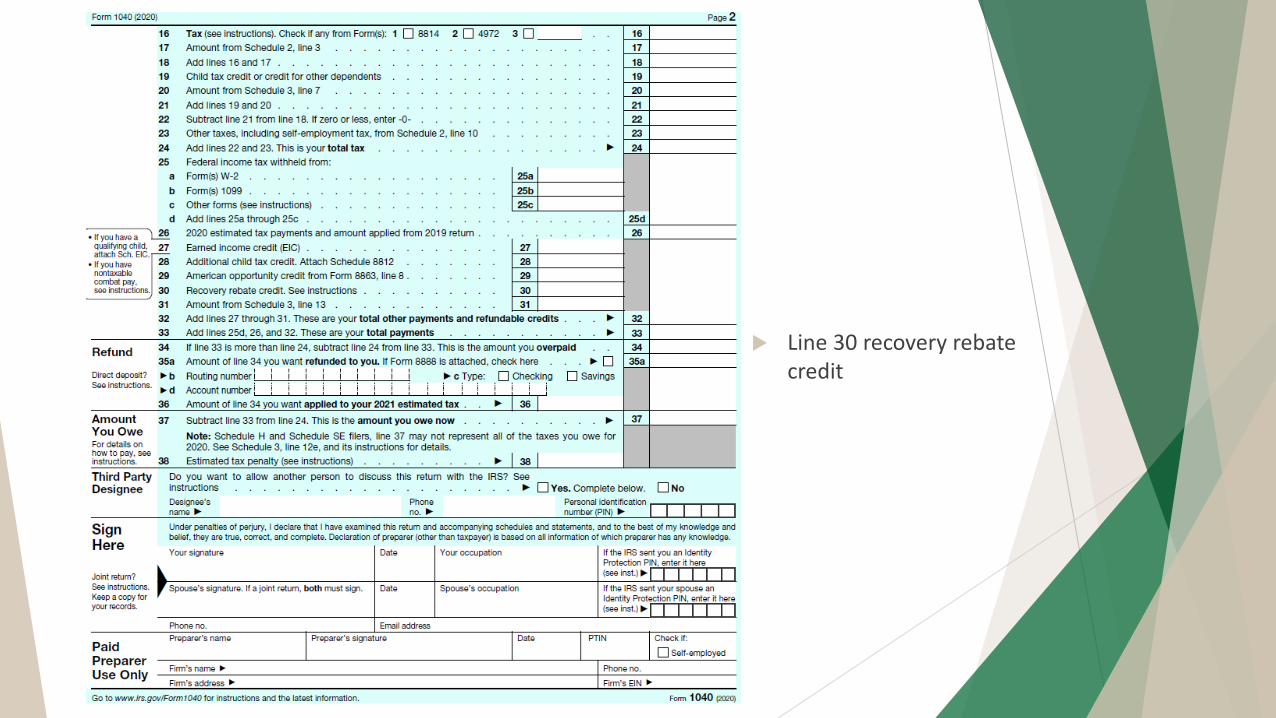

Line 30 recovery rebatecredit

1. What assets have they paid property taxes on?2. Anything sold or purchased?3. State and local taxes paid to other states could indicate income generated in those states4. Line 20: Casualty & Theft Losses:

a. If reported, inquire as to disposition of insurance proceeds?5. Interest:

a. Ask for all loan applications; great source

FORM 1040 U.S. INDIVIDUAL INCOME TAX RETURN SCHEDULE A: ITEMIZED DEDUCTIONS

2020 Tax Update: Changes to Individual and Business Income Taxes and IRS Forms

1. Is there interest income from an individual?2. Match interest to broker statements3. Beware of tax-exempt interest; see Line 2A of Form 10404. Part III-Foreign Accounts and Trusts

a. Used to report income from foreign sourcesb. Foreign tax credit intended to make sure you are only taxed once on foreign income (e.g.

not taxed by US and foreign country) but at the higher of the US or foreign tax ratec. If you meet certain tests, you may qualify to exclude some of the foreign income on the tax

returnd. Requirement to report foreign income referred to as the foreign bank and financial

accounts report (FBAR) – required to report on foreign assets in excess of $10,000.e. An entry on this line may be the only clue as to the existence of what is called a

foreign asset protection trust.

FORM 1040 U.S. INDIVIDUAL INCOME TAX RETURN SCHEDULE B INTEREST AND ORDINARY DIVIDENDS

2020 Tax Update: Changes to Individual and Business Income Taxes and IRS Forms

FORM 1040 U.S. INDIVIDUAL INCOME TAX RETURN SCHEDULE D: CAPITAL GAINS & LOSSES

2020 Tax Update: Changes to Individual and Business Income Taxes and IRS Forms

1. Sale of investments such as stocks and bonds2. Capital loss carryover

a. Losses from the sale of capital losses are allowed to offset gains from the sale of capitalassets or, if there is a net loss from such sales, deductible against ordinary income to amaximum of $3,000. Any capital losses not deductible due to the $3,000 maximum may bededucted in subsequent years until fully utilized.

b. If separate returns are filed after a net capital loss was reported on a joint return, thecarryover is allocated to each taxpayer based on his or her net losses for the precedingtaxable year. If the losses were incurred jointly, the losses are divided equally. Thus, eachparty may carry his or her half of the loss to the following year.

FORM 1040 U.S. INDIVIDUAL INCOME TAX RETURN SCHEDULE D: CAPITAL GAINS & LOSSES

2020 Tax Update: Changes to Individual and Business Income Taxes and IRS Forms

2. Capital loss carryoverc. Be careful if brokerage accounts are not held jointly. See Finkelstein v. Finkelstein, 268

A.D.2d 273, 701 N.Y.S.2d 52 (2000), NYS Appellate Court held that a capital loss carryforward accumulated by the parties constituted a marital asset subject to distribution. Thewife was allowed an amount, which represented the reduction in taxes she would have hadfor the years 1996 and 1997 (which was the only definitive value placed on the asset byher accountant).

d. Tax losses and gains that are incurred during the marriage but deferred to the future affectvalue today – see Wechsler re: built in gains, unrealized gains in stocks, and real estate. Becareful when asset swapping.

1. Part II: Pass through entitiesa. S-Corporationsb. Partnerships

2. Get tax returns/financial statements for all entities3. Remember losses does not always mean zero cash flow4. Important to identify business entities early on in the case5. Part III Trusts

a. Need all trust documentsb. ID beneficiaries and all trusteesc. Separate property issues

FORM 1040 – U.S. INDIVIDUAL INCOME TAX RETURN SCHEDULE E, PAGE 2 INCOME OR LOSS FROM PARTNERSHIPS AND S. CORPORATIONS

2020 Tax Update: Changes to Individual and Business Income Taxes and IRS Forms

PARTNERSHIP INCOME TAX RETURNS:IRS FORM 1065

S CORPORATION INCOME TAX RETURNS:IRS FORM 1120-S

Lines G & H - New to 2020 Form A.Tax Exempt Interest

B. Other taxes

C. Non-Deductible

D. Distributions

E. Loans

CONTACT USLouis Cercone, Jr.CPA, CFE, CFF, ABV, ASA, CVAManaging [email protected]

Douglas SosnowskiCPA/ABV, ASA, [email protected]

William AllenCPA/ABV, [email protected]

Benjamin SchuverCPA/ABVSenior [email protected]

Johnathon Miles CPA/[email protected]

Paul HerlanDirector of Business [email protected]

Kelly Mandell-KlumppCPASenior [email protected]

Jenna DahleidenDirector of Client [email protected]

Divorce Cases:

Uncovering Critical Information in Tax

Returns and Financial Statements

Mark S. Gottlieb CPA/ABV/CFF, ASA, CVA, CBA

www.msgcpa.com – NY: 646-661-3800 / CT: 203-357-1500 / NJ: 973-226-4500

www.msgcpa.com – NY: 646-661-3800 / CT: 203-357-1500 / NJ: 973-226-4500

OBJECTIVES1. How to read & understand financial statements.

2. How are financial statements used as an investigative tool.

3. What does a financial statement not provide that you need to know.

4. How financial statements differ from tax returns.

www.msgcpa.com – NY: 646-661-3800 / CT: 203-357-1500 / NJ: 973-226-4500

MAIN COMPONENTS OF FINANCIAL STATEMENTS

Balance Sheet

Income Statement

Footnotes

www.msgcpa.com – NY: 646-661-3800 / CT: 203-357-1500 / NJ: 973-226-4500

BALANCE SHEET

Primary Components:• Assets• Liabilities• Equity

THINK PHOTOGRAPHAccounting Equation

Assets - Liabilities = Equitywww.msgcpa.com – NY: 646-661-3800 / CT: 203-357-1500 / NJ: 973-226-4500

BALANCE SHEETAssets • Current Assets

• Fixed Assets

• Other Assets

www.msgcpa.com – NY: 646-661-3800 / CT: 203-357-1500 / NJ: 973-226-4500

TYPES OF CURRENT ASSETS• Cash• Marketable Securities• Accounts Receivable• Inventory• Prepaid Expenses• Loans To Shareholders

Converted to cash within the next 12 months

www.msgcpa.com – NY: 646-661-3800 / CT: 203-357-1500 / NJ: 973-226-4500

TYPES OF FIXED ASSETS• Land• Building• Leasehold Improvements• Machinery, Equipment, Furniture, Fixtures• Transportation / Vehicles• Less: Accumulated Depreciation

Used in the trade or businesswww.msgcpa.com – NY: 646-661-3800 / CT: 203-357-1500 / NJ: 973-226-4500

TYPES OF OTHER ASSETS

• Intangible Assets• Security Deposits• Due From Affiliated or Related Parties

Not intended to be converted into cash within the next 12 monthswww.msgcpa.com – NY: 646-661-3800 / CT: 203-357-1500 / NJ: 973-226-4500

TYPES OF LIABILITIES

• Current Liabilities

• Long Term (Non-Current) Liabilities

www.msgcpa.com – NY: 646-661-3800 / CT: 203-357-1500 / NJ: 973-226-4500

TYPES OF CURRENT LIABILITIES

• Accounts Payable/Accrued Expenses• Notes/Loans Payable – Current Portion• Taxes (Income, Payroll, etc.) Payable• Loans From Shareholders

Items to be paid within the next 12 months

www.msgcpa.com – NY: 646-661-3800 / CT: 203-357-1500 / NJ: 973-226-4500

TYPES OF LONG TERM LIABILITIES

• Notes/Loans Payable – Non currentportion

• Deferred Income Taxes

Items not expected to be paid within the next 12 months

www.msgcpa.com – NY: 646-661-3800 / CT: 203-357-1500 / NJ: 973-226-4500

ASSETS• Cash- Cash in bank, petty cash, etc.

• Marketable Securities – Excess/idle cash that is invested & liquid.Recorded at lower of historical cost or market value.

• Accounts Receivable – Amounts due from customers or clients forwork/services/goods performed/sold that have not yet beencollected.

• Inventory – Raw materials, finished product ready to be used orsold.

• Prepaid Expenses – Prepayment of an expense that will beexpended over the next 12 months (i.e. insurance).

www.msgcpa.com – NY: 646-661-3800 / CT: 203-357-1500 / NJ: 973-226-4500

ASSETS• Fixed Assets (PPE) – Assets purchased not intended for sale but

used in the trade or business. i.e. furniture, machines, equipment, auto, etc. These items are often reported net of accumulated depreciation.

• Intangible Assets – Assets with no physical existence, yet have substantial value. i.e. goodwill, customers lists, etc. (Generally recorded when purchased)

• Security Deposits – A deposit or measure of security. i.e. rent, etc.

www.msgcpa.com – NY: 646-661-3800 / CT: 203-357-1500 / NJ: 973-226-4500

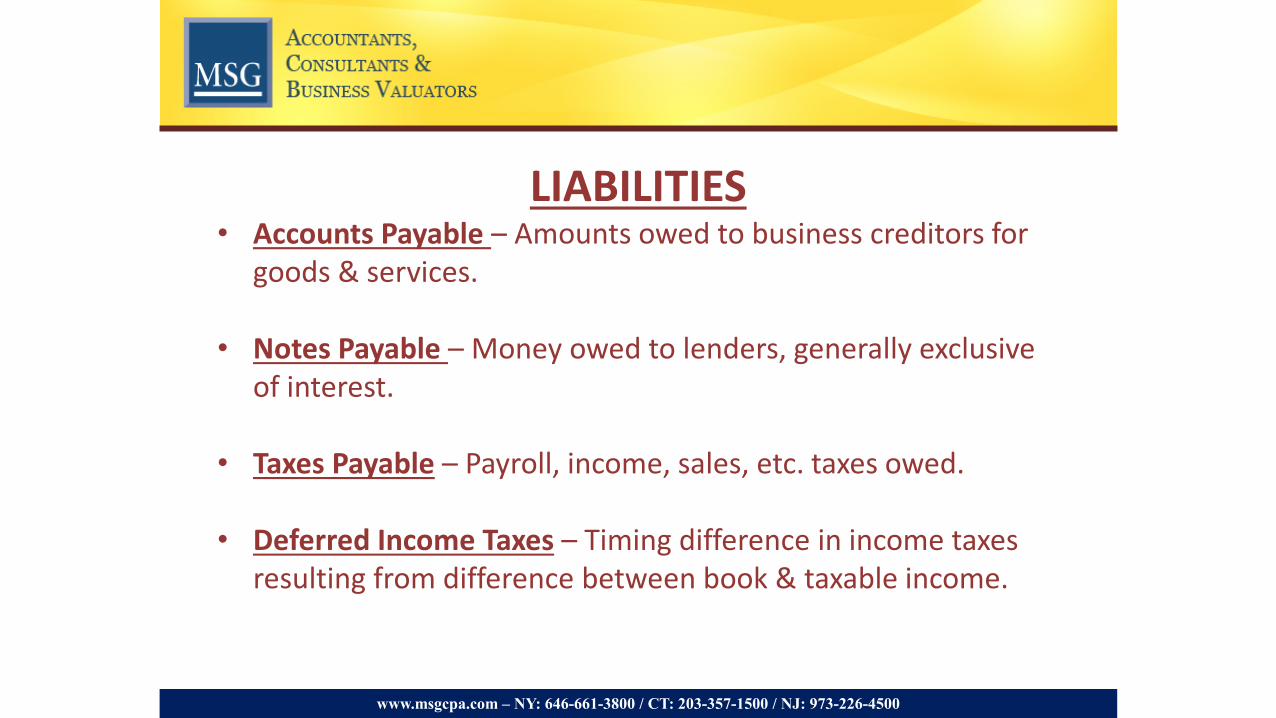

LIABILITIES• Accounts Payable – Amounts owed to business creditors for

goods & services.

• Notes Payable – Money owed to lenders, generally exclusive of interest.

• Taxes Payable – Payroll, income, sales, etc. taxes owed.

• Deferred Income Taxes – Timing difference in income taxes resulting from difference between book & taxable income.

www.msgcpa.com – NY: 646-661-3800 / CT: 203-357-1500 / NJ: 973-226-4500

EQUITYComponents of equity depend upon how the business is organized and capitalized.

General Types of Entities

• Sole Proprietorship

• Corporation

• Partnership

www.msgcpa.com – NY: 646-661-3800 / CT: 203-357-1500 / NJ: 973-226-4500

EQUITY – CORPORATE ENITITY

• Common Stock – Par/Stated Value of Stock at time of organization.

• Additional Paid In Capital – Amounts contributed as capital in excess of par value.

• Retained Earnings – Accumulated sum of profit or loss of business (net of dividend distributions).

www.msgcpa.com – NY: 646-661-3800 / CT: 203-357-1500 / NJ: 973-226-4500

ASSETS LIABILITIES & EQUITYCurrent Assets Current LiabilitiesCash 250,000$ Accounts Payable 115,000$ Marketable Securities 50,000 Current Portion of Long-term Debt 24,000 Accounts Receivable 125,000 Taxes Payable 3,600 Inventory 85,000 Pension Contribution Payable 6,400 Officer Loans 35,000 Total Current Liabilities 149,000 Prepaid Expenses 15,000

Total Current Assets 560,000

Fixed AssetsLand 100,000 Long Term LiabilitiesBuilding 250,000 Mortgages, Notes and Bonds Payable 150,000 Equipment 75,000 Loans from Shareholders 50,000 Furniture & Fixtures 50,000 Total Long Term Liabilities 200,000

Subtotal 475,000

Less: Accumulated Depreciation 110,000 Total Liabilities 349,000 Subtotal 110,000

Net Fixed Assets 365,000

Intangible AssetsIntangible Assets-Goodwill 150,000 Less: Accumulated Amortization 50,000

Net Intangible Assets 100,000 Stockholders' Equity

Other Assets Common Stock 1,000 Due to Related Party 200,000 Additional Paid In Capital 119,000 Security Deposits 25,000 Retained Earnings 781,000

Total Other Assets 225,000 Total Equity 901,000

Total Assets 1,250,000$ Total Liabilities & Equity 1,250,000$

INCOME STATEMENTSPrimary Components:• Gross Income/Sales• Direct Costs/Cost of Goods Sold• Gross Profit• Operating Expenses (Selling, General, & Admin)• Income Taxes

THINK MOVIE CAMERAAccounting Equation

Income – Expenses = Net Incomewww.msgcpa.com – NY: 646-661-3800 / CT: 203-357-1500 / NJ: 973-226-4500

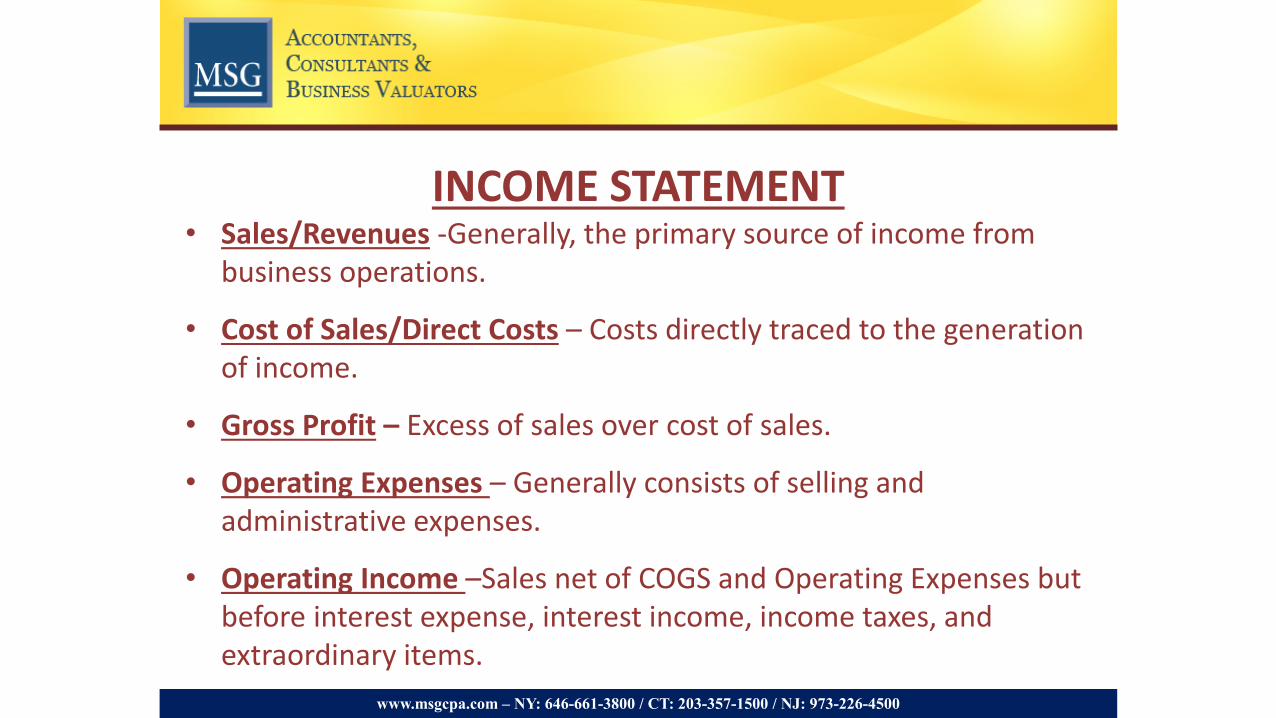

INCOME STATEMENT• Sales/Revenues -Generally, the primary source of income from

business operations.

• Cost of Sales/Direct Costs – Costs directly traced to the generation of income.

• Gross Profit – Excess of sales over cost of sales.

• Operating Expenses – Generally consists of selling and administrative expenses.

• Operating Income –Sales net of COGS and Operating Expenses but before interest expense, interest income, income taxes, and extraordinary items.

www.msgcpa.com – NY: 646-661-3800 / CT: 203-357-1500 / NJ: 973-226-4500

Revenues Income before other expenses 1,280,050 Gross Sales 3,500,000$ Less: Returns and Allowances 125,000 Officer's Compensation 175,000 Net Sales 3,375,000

Depreciation and Amortization 10,000 Cost of SalesBeginning Inventory 100,000 Operating Income 1,095,050 Purchases 1,600,000 Ending Inventory (200,000) Other expenses (income)

Total Cost of Sales 1,500,000 Interest Income (1,000) Interest Expense 4,400

Gross Profit 1,875,000 Total other expenses (income) 3,400

Operating Expenses Income before income taxes 1,091,650 Advertising 12,000 Auto & Truck 6,000 Corporate Income TaxesBank Charges 300 Federal, State & Local Taxes 300,650 Dues and Fees 2,150 Total Taxes 300,650 Employee Benefit Program 22,000 Equipment Rental 15,000 NET INCOME (LOSS) 791,000$ Insurance 6,000 Legal & Professional 11,500 Maintenance 5,500 Meals & Travel 21,200 Miscellaneous 3,900 Office 57,500 Postage 8,800 Rent & Utilities 76,400 Repairs 3,300 Salaries and Related Taxes 340,000 Telephone 3,400

Total Operating Expenses 594,950

A FEW TERMS YOU SHOULD KNOW!!Cash Basis – INCOME is recorded when received and EXPENSESare recorded when paid.

Accrual Basis – INCOME is recorded when earned and EXPENSESare recorded when incurred.

Calendar Year – An accounting year encompassing 12 months that ends on December 31st.

Fiscal Year – An accounting year encompassing 12 months that ends on any date other than December 31st.

www.msgcpa.com – NY: 646-661-3800 / CT: 203-357-1500 / NJ: 973-226-4500

TYPES OF ACCOUNTING RECORDS THAT ARE MAINTAINED BEFORE FINANCIAL STATEMENTS ARE PREPARED

• Sales Journals• Purchase Journals• Cash Receipts Journals• Cash Disbursement Journals• Payroll Journals• General Journals

The type and sophistication of accounting journals/records is greatly dependent upon the method of

accounting & the size & nature of the business.www.msgcpa.com – NY: 646-661-3800 / CT: 203-357-1500 / NJ: 973-226-4500

SIMPLIFIED ACCOUNTING FLOW CHARTTransactions Recorded In Various Journals

Journals Are Posted To General Ledger

Adjustments Are Made To Accounting Records

Adjusted Totals Are Summarized In A Trial Balance

Final Trial Balance Totals Are Used To Prepare Financial Statements

www.msgcpa.com – NY: 646-661-3800 / CT: 203-357-1500 / NJ: 973-226-4500

FINANCIAL STATEMENT FOOTNOTESOften one of the most valuable parts of financial statements and often the most overlooked. Footnotes provide additional detail not explicit within the financial statements.

Examples of information provided within the financial statement footnotes:• Accounting Methodologies• Acquisition Information• Debt & Borrowing Details• Commitments & Contingencies• Pension Benefits• Info Related to Different Segments of Business• Other

www.msgcpa.com – NY: 646-661-3800 / CT: 203-357-1500 / NJ: 973-226-4500

TYPES OF FINANCIAL STATEMENTS REPORTS

• Audit

• Review

• Compilation

www.msgcpa.com – NY: 646-661-3800 / CT: 203-357-1500 / NJ: 973-226-4500

AUDITED FINANCIAL STATEMENTS

Financial statements present fairly, in all material respects, an entity’s financial position, results of operations, & cash flows in accordance with Generally Accepted Accounting Principles (GAAP). All due diligence performed by the accountant to arrive at this conclusion must be made in accordance with Generally Accepted Auditing Standards.

Think highest degree of assurance provided by independent, outside accountant.

www.msgcpa.com – NY: 646-661-3800 / CT: 203-357-1500 / NJ: 973-226-4500

REVIEW FINANCIAL STATEMENTS

Due diligence is performed in the form of analytical procedures which compares financial data to prior periods to ascertain whether information appears reasonable.

The purpose and scope of this is greatly different from an audit, it does not provided the same level of assurance and only seeks to test for reasonableness.

www.msgcpa.com – NY: 646-661-3800 / CT: 203-357-1500 / NJ: 973-226-4500

COMPILATION/COMPILED FINANCIAL STATEMENTS

The accountant places information that remains the representation of management into the form of financial statements without expressing any assurance that it presents fairly the financial condition of the business.

No verification of any kind or due diligence has been performed.

www.msgcpa.com – NY: 646-661-3800 / CT: 203-357-1500 / NJ: 973-226-4500

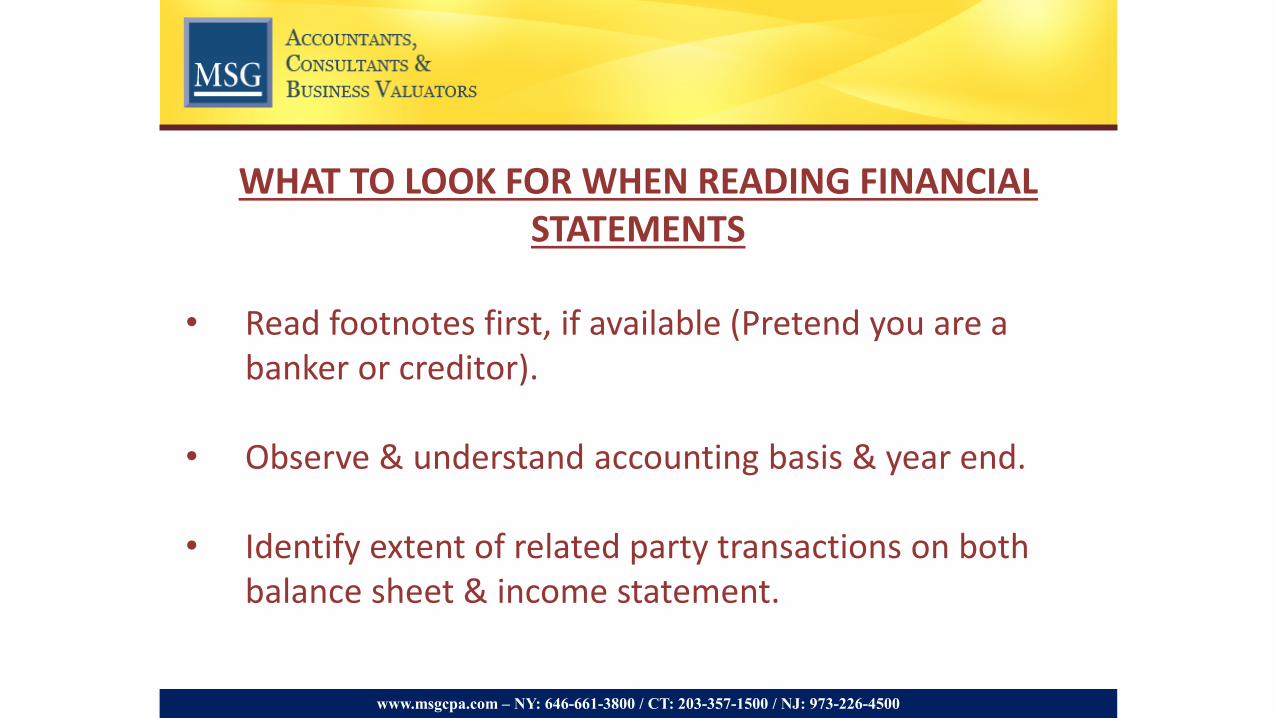

WHAT TO LOOK FOR WHEN READING FINANCIAL STATEMENTS

• Read footnotes first, if available (Pretend you are a banker or creditor).

• Observe & understand accounting basis & year end.

• Identify extent of related party transactions on both balance sheet & income statement.

www.msgcpa.com – NY: 646-661-3800 / CT: 203-357-1500 / NJ: 973-226-4500

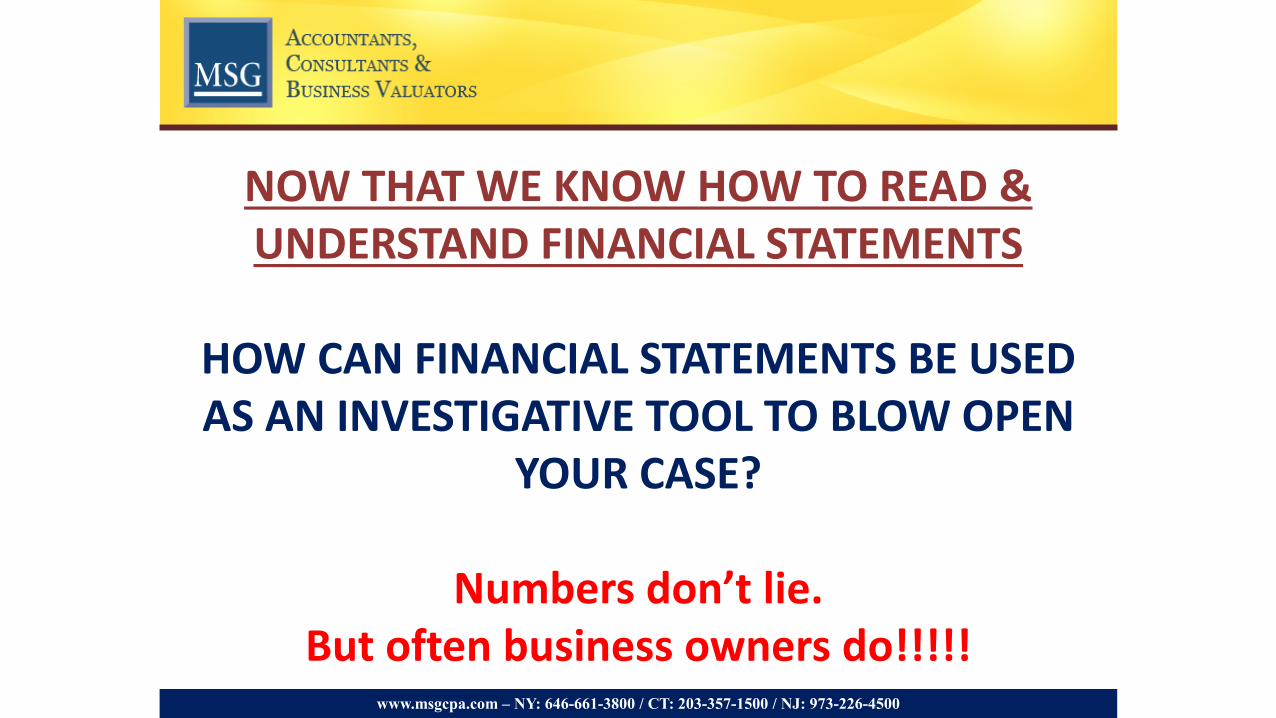

NOW THAT WE KNOW HOW TO READ & UNDERSTAND FINANCIAL STATEMENTS

HOW CAN FINANCIAL STATEMENTS BE USED AS AN INVESTIGATIVE TOOL TO BLOW OPEN

YOUR CASE?

Numbers don’t lie.But often business owners do!!!!!

www.msgcpa.com – NY: 646-661-3800 / CT: 203-357-1500 / NJ: 973-226-4500

THE MOST EFFECTIVE WAYS TO USE FINANCIAL STATEMENTS AS AN INVESTIGATIVE TOOL

• Trend Analysis • Ratio Analysis• Other Financial Models

Review historical accounting records to identify questionable accounting practices. This is as close

as we can get to having a crystal ball.www.msgcpa.com – NY: 646-661-3800 / CT: 203-357-1500 / NJ: 973-226-4500

TREND ANALYSIS

Look for changes/fluctuations from year to year to identify discretionary, personal spending or any other unusual items.

• Nominal ($) Analysis• Common Size (%) Analysis• Growth Analysis

www.msgcpa.com – NY: 646-661-3800 / CT: 203-357-1500 / NJ: 973-226-4500

RATIO ANALYSIS

Compare subject to peers by using outside databases.

• RMA• Integra• IRS• Industry Studies, etc.

www.msgcpa.com – NY: 646-661-3800 / CT: 203-357-1500 / NJ: 973-226-4500

OTHER FINANCIAL MODELS

Among the many items to be identified, financial models are often used to quantify risks of a business.

• DuPont Analysis

• Altman Z-Score

Financial models are often a great illustrative tool to express issues to the Court.

www.msgcpa.com – NY: 646-661-3800 / CT: 203-357-1500 / NJ: 973-226-4500

DuPONT ANALYSIS

Measures Return on Equity• Operating efficiency• Asset efficiency• Financial leverage

Companies that demonstrate a higher return on equity with minimal debt can expand without large capital

outlays by allowing owners to access cash generated by the business for consumption or reinvestment.

www.msgcpa.com – NY: 646-661-3800 / CT: 203-357-1500 / NJ: 973-226-4500

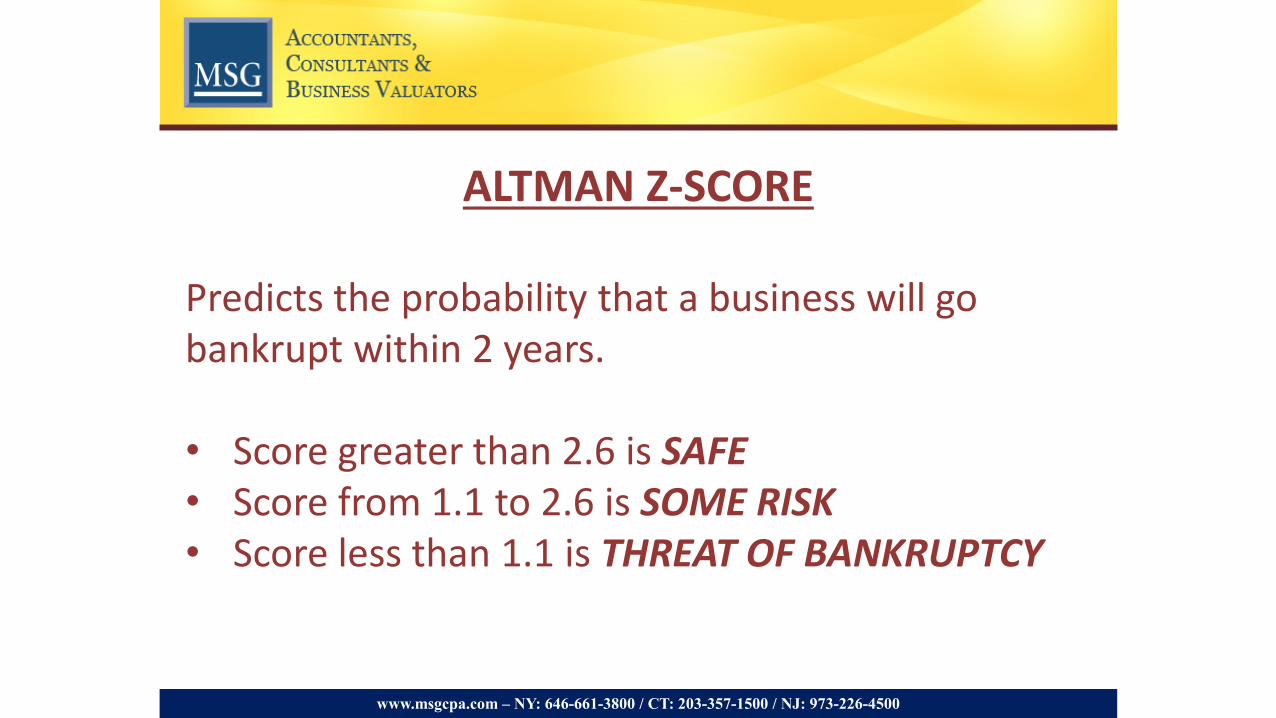

ALTMAN Z-SCORE

Predicts the probability that a business will go bankrupt within 2 years.

• Score greater than 2.6 is SAFE• Score from 1.1 to 2.6 is SOME RISK• Score less than 1.1 is THREAT OF BANKRUPTCY

www.msgcpa.com – NY: 646-661-3800 / CT: 203-357-1500 / NJ: 973-226-4500

EXHIBIT 1

ABC COMPANY

HISTORICAL BALANCE SHEETS AS OF DECEMBER 31,

2010 2009 2008 MIN MAX MEAN MEDIANASSETSCurrent AssetsCash 202,436$ 168,886$ 144,525$ 144,525$ 202,436$ 171,949$ 168,886$ Marketable Securities - - - - - - - Accounts Receivable 198,248 59,086 57,440 57,440 198,248 104,925 59,086 Employee Loans Receivable - 9,850 - - 9,850 3,283 - Loan Receivable - Affiliated Company 54,911 - 4,000 - 54,911 19,637 4,000 Inventory - - - - - - - Escrow - - - - - - - Prepaid Taxes - - - - - - -

Total Current Assets 455,595 237,822 205,965 205,965 455,595 299,794 237,822

Fixed AssetsBuilidng, Machinery & Equipment 595,733 555,161 537,423 537,423 595,733 562,772 555,161

Subtotal 595,733 555,161 537,423 537,423 595,733 562,772 555,161

Less: Accumulated Depreciation 434,754 387,231 368,665 368,665 434,754 396,883 387,231 Subtotal 434,754 387,231 368,665 368,665 434,754 396,883 387,231

Net Fixed Assets 160,979 167,930 168,758 160,979 168,758 165,889 167,930

Intangible AssetsIntangible Assets 275,000 275,000 275,000 275,000 275,000 275,000 275,000 Less: Accumulated Amortization 131,109 112,776 94,443 94,443 131,109 112,776 112,776

Net Intangible Assets 143,891 162,224 180,557 143,891 180,557 162,224 162,224

Other AssetsPayroll Exchange - - 14,618 - 14,618 4,873 - Security Deposits - - - - - - -

Total Other Assets - - 14,618 - 14,618 4,873 -

Total Assets 760,465$ 567,976$ 569,898$ 567,976$ 760,465$ 632,780$ 569,898$

LIABILITIES & EQUITYCurrent LiabilitiesAccounts Payable 138,744$ 119,349$ 86,576$ 86,576$ 138,744$ 114,890$ 119,349$ Current Portion of Long-term Debt - - - - - - - 401K Payable 8,330 14,923 9,546 8,330 14,923 10,933 9,546 Pension Match Payable - - - - - - - Escrow Payable 725 - - - 725 242 -

Total Current Liabilities 147,799 134,272 96,122 96,122 147,799 126,064 134,272

Long Term LiabilitiesMortgages, Notes and Bonds Payable 27,295 - - - 27,295 9,098 - Loans from Shareholders - - - - - - - Long-term deferred tax liability - - - - - - -

Total Long Term Liabilities 27,295 - - - 27,295 9,098 -

Total Liabilities 175,094 134,272 96,122 96,122 175,094 135,163 134,272

Stockholders' EquityPartner's Capital 585,371 433,704 473,776 433,704 585,371 497,617 473,776

Total Equity 585,371 433,704 473,776 433,704 585,371 497,617 473,776

Total Liabilities & Equity 760,465$ 567,976$ 569,898$ 567,976$ 760,465$ 632,780$ 569,898$

ANALYTICSDOLLARS

EXHIBIT 2

ABC COMPANY

HISTORICAL BALANCE SHEETS - COMMON SIZEAS OF DECEMBER 31,

2010 2009 2008 MIN MAX MEAN MEDIANASSETSCurrent AssetsCash 26.6% 29.7% 25.4% 25.4% 29.7% 27.2% 26.6%Marketable Securities 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%Accounts Receivable 26.1% 10.4% 10.1% 10.1% 26.1% 15.5% 10.4%Employee Loans Receivable 0.0% 1.7% 0.0% 0.0% 1.7% 0.6% 0.0%Loan Receivable - Affiliated Company 7.2% 0.0% 0.7% 0.0% 7.2% 2.6% 0.7%Inventory 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%Escrow 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%Prepaid Taxes 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Total Current Assets 59.9% 41.9% 36.1% 36.1% 59.9% 46.0% 41.9%

Fixed AssetsBuilidng, Machinery & Equipment 78.3% 97.7% 94.3% 78.3% 97.7% 90.1% 94.3%

Subtotal 78.3% 97.7% 94.3% 78.3% 97.7% 90.1% 94.3%

Less: Accumulated Depreciation 57.2% 68.2% 64.7% 57.2% 68.2% 63.3% 64.7%Subtotal 57.2% 68.2% 64.7% 57.2% 68.2% 63.3% 64.7%

Net Fixed Assets 21.2% 29.6% 29.6% 21.2% 29.6% 26.8% 29.6%

Intangible AssetsIntangible Assets 36.2% 48.4% 48.3% 36.2% 48.4% 44.3% 48.3%Less: Accumulated Amortization 17.2% 19.9% 16.6% 16.6% 19.9% 17.9% 17.2%

Net Intangible Assets 18.9% 28.6% 31.7% 18.9% 31.7% 26.4% 28.6%

Other AssetsCertificates of Deposit 0.0% 0.0% 2.6% 0.0% 2.6% 0.9% 0.0%Security Deposits 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Total Other Assets 0.0% 0.0% 2.6% 0.0% 2.6% 0.9% 0.0%

Total Assets 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0%

LIABILITIES & EQUITYCurrent LiabilitiesAccounts Payable 18.2% 21.0% 15.2% 15.2% 21.0% 18.1% 18.2%Current Portion of Long-term Debt 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%401K Payable 1.1% 2.6% 1.7% 1.1% 2.6% 1.8% 1.7%Pension Match Payable 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%Escrow Payable 0.1% 0.0% 0.0% 0.0% 0.1% 0.0% 0.0%

Total Current Liabilities 19.4% 23.6% 16.9% 16.9% 23.6% 20.0% 19.4%

Long Term LiabilitiesMortgages, Notes and Bonds Payable 3.6% 0.0% 0.0% 0.0% 3.6% 1.2% 0.0%Loans from Shareholders 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%Long-term deferred tax liability 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Total Long Term Liabilities 3.6% 0.0% 0.0% 0.0% 3.6% 1.2% 0.0%

Total Liabilities 23.0% 23.6% 16.9% 16.9% 23.6% 21.2% 23.0%

Stockholders' EquityPartner's Capital 77.0% 76.4% 83.1% 76.4% 83.1% 78.8% 77.0%

Total Equity 77.0% 76.4% 83.1% 76.4% 83.1% 78.8% 77.0%

Total Liabilities & Equity 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0%

COMMON SIZE ANALYTICS

EXHIBIT 3

ABC COMPANY

HISTORICAL BALANCE SHEETS - GROWTH ANALYSISAS OF DECEMBER 31,

2010 2009 2008 2010 2009 2008ASSETSCurrent AssetsCash 145.4% 251.0% 954.5% 19.9% 16.9% 954.5%Marketable Securities n/a n/a n/a n/a n/a n/aAccounts Receivable 25.9% -22.9% -42.2% 235.5% 2.9% -42.2%Employee Loans Receivable n/a -21.7% n/a -100.0% n/a -100.0%Loan Receivable - Affiliated Company n/a n/a n/a n/a -100.0% n/aInventory n/a n/a n/a n/a n/a n/aEscrow n/a n/a n/a n/a n/a -100.0%Prepaid Taxes n/a n/a n/a n/a n/a n/a

Total Current Assets 51.8% 35.1% 58.0% 91.6% 15.5% 58.0%

Fixed AssetsBuilidng, Machinery & Equipment 4.7% 3.5% 3.6% 7.3% 3.3% 3.6%

Subtotal 4.7% 3.5% 3.6% 7.3% 3.3% 3.6%

Less: Accumulated Depreciation 8.0% 5.9% 6.8% 12.3% 5.0% 6.8%Subtotal 8.0% 5.9% 6.8% 12.3% 5.0% 6.8%

Net Fixed Assets -2.5% -1.6% -2.8% -4.1% -0.5% -2.8%

Intangible AssetsIntangible Assets 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%Less: Accumulated Amortization 19.9% 21.7% 24.1% 16.3% 19.4% 24.1%

Net Intangible Assets -10.2% -9.7% -9.2% -11.3% -10.2% -9.2%

Other AssetsCertificates of Deposit n/a n/a n/a n/a -100.0% n/aSecurity Deposits n/a n/a n/a n/a n/a n/a

Total Other Assets n/a n/a n/a n/a -100.0% n/a

Total Assets 14.8% 6.3% 13.3% 33.9% -0.3% 13.3%

LIABILITIES & EQUITYCurrent LiabilitiesAccounts Payable 3.4% -2.5% -31.0% 16.3% 37.9% -31.0%Current Portion of Long-term Debt n/a n/a n/a n/a n/a n/a401K Payable -11.9% 10.6% -21.7% -44.2% 56.3% -21.7%Pension Match Payable n/a n/a n/a n/a n/a -100.0%Escrow Payable n/a n/a n/a n/a n/a n/a

Total Current Liabilities 1.9% -2.0% -31.2% 10.1% 39.7% -31.2%

Long Term LiabilitiesMortgages, Notes and Bonds Payable n/a n/a n/a n/a n/a n/aLoans from Shareholders n/a n/a n/a n/a n/a n/aLong-term deferred tax liability n/a n/a n/a n/a n/a n/a

Total Long Term Liabilities n/a n/a n/a n/a n/a n/a

Total Liabilities 7.8% -2.0% -31.2% 30.4% 39.7% -31.2%

Stockholders' EquityPartner's Capital 17.3% 9.3% 30.5% 35.0% -8.5% 30.5%

Total Equity 17.3% 9.3% 30.5% 35.0% -8.5% 30.5%

Total Liabilities & Equity 14.8% 6.3% 13.3% 33.9% -0.3% 13.3%

ANNUAL GROWTH COMPOUND ANNUAL GROWTH

EXHIBIT 4

ABC COMPANY

HISTORICAL INCOME STATEMENTS FOR THE YEARS ENDING DECEMBER 31,

2010 2009 2008 MIN MAX MEAN MEDIANRevenuesGross Sales 3,086,765$ 2,493,330$ 2,843,699$ 2,493,330$ 3,086,765$ 2,807,931$ 2,843,699$ Less: Returns and Allowances - - - - - - - Net Sales 3,086,765 2,493,330 2,843,699 2,493,330 3,086,765 2,807,931 2,843,699

Cost of SalesBeginning Inventory - - - - - - - Purchases - - - - - - - Ending Inventory - - - - - - -

Total Cost of Sales - - - - - - -

Gross Profit 3,086,765 2,493,330 2,843,699 2,493,330 3,086,765 2,807,931 2,843,699

Operating ExpensesAdvertising 59,029 84,197 132,321 59,029 132,321 91,849 84,197 Auto & Truck 47,073 37,103 33,764 33,764 47,073 39,313 37,103 Closing Costs 203,682 271,254 254,648 203,682 271,254 243,195 254,648 Computer Expenses 44,472 20,871 19,578 19,578 44,472 28,307 20,871 Contributions 2,764 2,175 - - 2,764 1,646 2,175 Dues and Fees 25,146 7,828 7,800 7,800 25,146 13,591 7,828 Education & Training 7,631 - 2,866 - 7,631 3,499 2,866 Employee Benefit Program 151,655 98,101 143,869 98,101 151,655 131,208 143,869 Equipment Rental 12,249 10,961 8,775 8,775 12,249 10,662 10,961 Insurance 18,723 14,107 14,612 14,107 18,723 15,814 14,612 Legal & Professional 56,856 49,080 26,950 26,950 56,856 44,295 49,080 Licenses - 400 - - 400 133 - Maintenance 18,579 19,336 12,724 12,724 19,336 16,880 18,579 Meals & Entertainment 17,321 13,239 10,155 10,155 17,321 13,572 13,239 Miscellaneous 11,909 - - - 11,909 3,970 - Office 79,465 45,933 52,243 45,933 79,465 59,214 52,243 Online Services 597 2,984 4,928 597 4,928 2,836 2,984 Open House & Promotions 33,019 49,255 43,602 33,019 49,255 41,959 43,602 Outside Services 64,425 500 - - 64,425 21,642 500 Pension and Profit Sharing 73,016 63,933 87,647 63,933 87,647 74,865 73,016 Postage 19,387 14,534 19,216 14,534 19,387 17,712 19,216 Rent 62,750 108,736 144,015 62,750 144,015 105,167 108,736 Salaries and Wages 1,707,833 1,199,096 1,266,876 1,199,096 1,707,833 1,391,268 1,266,876 Service Charges - - 588 - 588 196 - Subscriptions - - 58 - 58 19 - Taxes - Other 2,029 1,635 - - 2,029 1,221 1,635 Taxes - Payroll 114,202 82,243 111,512 82,243 114,202 102,652 111,512 Telephone 20,739 17,490 21,826 17,490 21,826 20,018 20,739 Travel 4,326 - 533 - 4,326 1,620 533 Utilities - - - - - - -

Total Operating Expenses 2,858,877 2,214,991 2,421,106 2,214,991 2,858,877 2,498,325 2,421,106

Income before other expenses 227,888 278,339 422,593 227,888 422,593 309,607 278,339

Officer's Compensation - - - - - - -

Depreciation and Amortization 65,854 36,900 41,916 36,900 65,854 48,223 41,916

Operating Income 162,034 241,439 380,677 162,034 380,677 261,383 241,439

Other expenses (income)Interest Income (759) (971) - (971) - (577) (759) Miscellaneous (income) expense - (7,879) - (7,879) - (2,626) - Interest Expense 960 - - - 960 320 -

Total other expenses (income) 201 (8,850) - (8,850) 201 (2,883) -

Income before income taxes 161,833 250,289 380,677 161,833 380,677 264,266 250,289

Corporate Income TaxesState and local taxes - - - - - - -

Total Taxes - - - - - - -

NET INCOME (LOSS) 161,833$ 250,289$ 380,677$ 161,833$ 380,677$ 264,266$ 250,289$

DOLLARS ANALYTICS

EXHIBIT 5

ABC COMPANY

HISTORICAL INCOME STATEMENTS - COMMON SIZEFOR THE YEARS ENDING DECEMBER 31,

2010 2009 2008 MIN MAX MEAN MEDIANRevenuesGross Sales 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0%Less: Returns and Allowances 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%Net Sales 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0%

Cost of SalesBeginning Inventory 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%Purchases 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%Ending Inventory 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Total Cost of Sales 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Gross Profit 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0%

Operating ExpensesAdvertising 1.9% 3.4% 4.7% 1.9% 4.7% 3.3% 3.4%Auto & Truck 1.5% 1.5% 1.2% 1.2% 1.5% 1.4% 1.5%Closing Costs 6.6% 10.9% 9.0% 6.6% 10.9% 8.8% 9.0%Computer Expenses 1.4% 0.8% 0.7% 0.7% 1.4% 1.0% 0.8%Contributions 0.1% 0.1% 0.0% 0.0% 0.1% 0.1% 0.1%Dues and Fees 0.8% 0.3% 0.3% 0.3% 0.8% 0.5% 0.3%Education & Training 0.2% 0.0% 0.1% 0.0% 0.2% 0.1% 0.1%Employee Benefit Program 4.9% 3.9% 5.1% 3.9% 5.1% 4.6% 4.9%Equipment Rental 0.4% 0.4% 0.3% 0.3% 0.4% 0.4% 0.4%Insurance 0.6% 0.6% 0.5% 0.5% 0.6% 0.6% 0.6%Legal & Professional 1.8% 2.0% 1.0% 1.0% 2.0% 1.6% 1.8%Licenses 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%Maintenance 0.6% 0.8% 0.5% 0.5% 0.8% 0.6% 0.6%Meals & Entertainment 0.6% 0.5% 0.4% 0.4% 0.6% 0.5% 0.5%Miscellaneous 0.4% 0.0% 0.0% 0.0% 0.4% 0.1% 0.0%Office 2.6% 1.8% 1.8% 1.8% 2.6% 2.1% 1.8%Online Services 0.0% 0.1% 0.2% 0.0% 0.2% 0.1% 0.1%Open House & Promotions 1.1% 2.0% 1.5% 1.1% 2.0% 1.5% 1.5%Outside Services 2.1% 0.0% 0.0% 0.0% 2.1% 0.7% 0.0%Pension and Profit Sharing 2.4% 2.6% 3.1% 2.4% 3.1% 2.7% 2.6%Postage 0.6% 0.6% 0.7% 0.6% 0.7% 0.6% 0.6%Rent 2.0% 4.4% 5.1% 2.0% 5.1% 3.8% 4.4%Salaries and Wages 55.3% 48.1% 44.6% 44.6% 55.3% 49.3% 48.1%Service Charges 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%Subscriptions 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%Taxes - Other 0.1% 0.1% 0.0% 0.0% 0.1% 0.1% 0.1%Taxes - Payroll 3.7% 3.3% 3.9% 3.3% 3.9% 3.6% 3.7%Telephone 0.7% 0.7% 0.8% 0.7% 0.8% 0.7% 0.7%Travel 0.1% 0.0% 0.0% 0.0% 0.1% 0.1% 0.0%Utilities 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Total Operating Expenses 92.6% 89.0% 85.1% 85.1% 92.6% 88.9% 89.0%

Income before other expenses 7.4% 11.0% 14.9% 7.4% 14.9% 11.1% 11.0%

Officer's Compensation 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Depreciation and Amortization 2.1% 1.5% 1.5% 1.5% 2.1% 1.7% 1.5%

Operating Income 5.2% 9.6% 13.4% 5.2% 13.4% 9.4% 9.6%

Other expenses (income)Interest Income 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%Miscellaneous (income) expense 0.0% -0.3% 0.0% -0.3% 0.0% -0.1% 0.0%Interest Expense 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Total other expenses (income) 0.0% -0.4% 0.0% -0.4% 0.0% -0.1% 0.0%

Income before income taxes 5.2% 9.9% 13.4% 5.2% 13.4% 9.5% 9.9%

Corporate Income TaxesState and local taxes 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Total Taxes 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

NET INCOME (LOSS) 5.2% 9.9% 13.4% 5.2% 13.4% 9.5% 9.9%

COMMON SIZE ANALYTICS

EXHIBIT 6

ABC COMPANY

HISTORICAL INCOME STATEMENTS - GROWTH ANALYSISFOR THE YEARS ENDING DECEMBER 31,

2010 2009 2008 2010 2009 2008RevenuesGross Sales -1.2% -11.7% -11.0% 23.8% -12.3% -11.0%Less: Returns and Allowances n/a n/a n/a n/a n/a n/aNet Sales -1.2% -11.7% -11.0% 23.8% -12.3% -11.0%

Cost of SalesBeginning Inventory n/a n/a n/a n/a n/a n/aPurchases n/a n/a n/a n/a n/a n/aEnding Inventory n/a n/a n/a n/a n/a n/a

Total Cost of Sales n/a n/a n/a n/a n/a n/a

Gross Profit -1.2% -11.7% -11.0% 23.8% -12.3% -11.0%

Operating ExpensesAdvertising -25.0% -22.4% -5.3% -29.9% -36.4% -5.3%Auto & Truck 1.8% -8.7% -24.2% 26.9% 9.9% -24.2%Closing Costs -9.6% -0.7% -7.5% -24.9% 6.5% -7.5%Computer Expenses 47.5% 22.7% 41.3% 113.1% 6.6% 41.3%Contributions n/a n/a n/a 27.1% n/a n/aDues and Fees 53.8% 6.4% 12.9% 221.2% 0.4% 12.9%Education & Training n/a n/a n/a n/a -100.0% n/aEmployee Benefit Program 10.6% -6.4% 28.5% 54.6% -31.8% 28.5%Equipment Rental -15.7% -26.8% -57.0% 11.8% 24.9% -57.0%Insurance -2.1% -15.9% -26.7% 32.7% -3.5% -26.7%Legal & Professional 33.3% 42.9% 12.1% 15.8% 82.1% 12.1%Licenses n/a n/a n/a -100.0% n/a n/aMaintenance -0.8% 0.9% -33.1% -3.9% 52.0% -33.1%Meals & Entertainment 23.9% 20.6% 11.6% 30.8% 30.4% 11.6%Miscellaneous n/a n/a n/a n/a n/a n/aOffice 15.6% -5.5% 1.5% 73.0% -12.1% 1.5%Online Services -42.2% -1.8% 59.2% -80.0% -39.4% 59.2%Open House & Promotions -22.5% -16.7% -38.6% -33.0% 13.0% -38.6%Outside Services n/a n/a n/a 12785.0% n/a n/aPension and Profit Sharing -19.2% -32.0% -36.6% 14.2% -27.1% -36.6%Postage 16.4% 8.7% 56.3% 33.4% -24.4% 56.3%Rent -28.2% -19.9% -15.0% -42.3% -24.5% -15.0%Salaries and Wages 6.7% -7.6% -9.8% 42.4% -5.4% -9.8%Service Charges n/a n/a n/a n/a -100.0% n/aSubscriptions n/a n/a -87.6% n/a -100.0% -87.6%Taxes - Other n/a n/a n/a 24.1% n/a n/aTaxes - Payroll 3.5% -10.7% 8.2% 38.9% -26.2% 8.2%Telephone -0.7% -9.1% 3.0% 18.6% -19.9% 3.0%Travel 26.4% n/a -75.1% n/a -100.0% -75.1%Utilities n/a n/a n/a n/a n/a -100.0%

Total Operating Expenses 2.4% -8.8% -9.1% 29.1% -8.5% -9.1%

Income before other expenses -24.7% -27.8% -20.8% -18.1% -34.1% -20.8%

Officer's Compensation n/a n/a n/a n/a n/a n/a

Depreciation and Amortization 9.1% -14.7% -17.3% 78.5% -12.0% -17.3%

Operating Income -30.5% -29.3% -21.1% -32.9% -36.6% -21.1%

Other expenses (income)Interest Income n/a n/a n/a n/a n/a n/aMiscellaneous (income) expense n/a n/a n/a n/a n/a n/aInterest Expense n/a n/a n/a n/a n/a n/a

Total other expenses (income) n/a n/a n/a n/a n/a n/a

Income before income taxes -30.5% -28.0% -21.1% -35.3% -34.3% -21.1%

Corporate Income TaxesState and local taxes n/a n/a n/a n/a n/a n/a

Total Taxes n/a n/a n/a n/a n/a n/a

NET INCOME (LOSS) -30.5% -28.0% -21.1% -35.3% -34.3% -21.1%

COMPOUND ANNUAL GROWTH ANNUAL GROWTH

WHAT DOES A FINANCIAL STATEMENT NOT PROVIDE

• Cash basis financial statements do not provide accounts receivable & accounts payable.

• Balance sheet does not report business’s goodwill, value of workforce, or other intangible assets (unless purchased).

• Most assets on balance sheet are reported at historical cost or lower of cost or market. It does not show fair market value of assets and liabilities.

• Personal expenses of owners are sometimes hidden with operating expenses of business.

• Does not indicate value of business.

www.msgcpa.com – NY: 646-661-3800 / CT: 203-357-1500 / NJ: 973-226-4500

HOW DO FINANCIAL STATEMENTS DIFFER FROM TAX RETURNS

• Basis of accounting may be different. • Cash vs. Accrual• Tax vs. Book

• Fiscal vs. Calendar year reporting.• Financial statements may provide footnotes that

tell a story.

www.msgcpa.com – NY: 646-661-3800 / CT: 203-357-1500 / NJ: 973-226-4500

www.msgcpa.com – NY: 646-661-3800 / CT: 203-357-1500 / NJ: 973-226-4500

Questions & Comments

METHODS TO OBTAIN DISCOVERY IN MATRIMONIAL CASES

By Valentina Shaknes, Esq. Krauss Shaknes Tallentire & Messeri LLP

BROAD FINANCIAL DISCOVERY IN MATRIMONIAL CASES

• C.P.L.R. Section 3101(a) mandates “full disclosure of all matter material and necessary in the prosecution or defense of an action, regardless of the burden of proof.”

• Consistently with this general mandate, New York Domestic Relations Law (“DRL”) provides for broad financial discovery in matrimonial proceedings.

• DRL Section 236 B(4) provides for compulsory disclosure by both parties. Financial discovery is mandatory.

Types of Discovery

• In matrimonial cases, discovery can be sought from

• Party; and

• Non-parties.

• Generally, discovery should be sought from the party first before going to third-parties.

Party Discovery:STATEMENT OF NET WORTH

• In matrimonial cases, discovery begins with a STATEMENT OF NET WORTH.

• Statements of net worth are of utmost importance in matrimonial proceedings.

• These documents are sworn statements that have four essential parts: • Expenses • Income • Assets; and • Liabilities.

Party Discovery:STATEMENT OF NET WORTH (con’t)

• A demand for a statement of net worth can be served at any time after the commencement of an action.

• Under the New York Court Rules, a SNW must be filed with the Court 10 days prior to the Preliminary Conference. NYCRR 202.16(f)(i).

• Statement of Net Worth must be accompanied by:• The most recent paystub; most recently filed tax returns; most

recent income reporting form(s) (Form W2 / K1 / 1099); and attorney’s retainer agreement.

Discovery Devices:NOTICE FOR DISCOVERY AND INSPECTION

• The most commonly used discovery device;• Governed by CPLR § 3120;• Served upon party to the action;• Can be served at any time after the commencement of the

action;• Must specify time, place and manner of the “inspection”; and• Must give responder at least 20 days to produce the

documents.

Discovery Devices:NOTICE FOR DISCOVERY AND INSPECTION

(con’t)• Each request should be stated with “reasonable particularity”;

• Practice tip: be specific and use statement of net worth when preparing the request;

• Follow up with additional demands• Document production MUST be supplemented or amended upon

learning that the response was incorrect or incomplete when made or has become incorrect or incomplete following production (CPLR § 3101(h))

FRCP vs. CPLR

• Notice:• FRCP Rule 34: The request shall include a “reasonable time, place

and manner for the inspection” of the documents; however, the receiving party must respond in writing within 30 days of being served.

• CPLR § 3120: 20 days notice is required.

Discovery Devices:SUBPOENAS

• Governed by CPLR § 3120 and § 2301 (scope);

• Must give at least 20 days to respond;

• Must specify time, place and manner of production;

• May be served upon party and non-parties;

• Two types of subpoenas: subpoenas to produce documents and subpoenas to give testimony.

Discovery Devices:SUBPOENAS (con’t)

• Subpoenas may be issued by attorneys; no court order required (except for certain circumstances, such as medical providers);

• Non-party subpoenas must be served on party, along with responses.

• Disclosure from non-parties: • No distinction between disclosure from party and non-party, except that

CPLR § 3101(a)(4) requires that “circumstances or reasons” for seeking disclosure be stated.

Discovery Devices:SUBPOENAS (con’t)

• Disclosure from non-parties:

• No distinction between disclosure from party and non-party, except that CPLR § 3101(a)(4) requires that “circumstances or reasons” for seeking disclosure be stated;

• No requirement that party demonstrate the discovery sought is not available from a party or another source;

• Court of Appeals held that the same “material and necessary” standard applies to discovery from non-parties.

• See Kapon v. Koch, 23 N.Y.3d 32 (2014).

FRCP vs. CPLR

• Notice:• FRCP Rule 45: No notice time specified for subpoena seeking

production of documents. • CPLR § 3120: Must give 20 days notice to comply with document

demand.• Where Subpoena can be Served:

• FRCP Rule 45: anywhere in the United States. • CPLR § 3119: Must submit an out-of-state subpoena to the

county clerk and the county clerk shall issue the out-of-state subpoena.

Discovery Devices:INTERROGATORIES

• Non-party subpoenas must be served on party, along with responses;

• CPLR § 3130 and 3132 governs the use and service of Interrogatories;

• CPRL 3131 governs the scope;• Served on a party as of right;• May be served on non-parties with a Court Order;• Limited to financial information.

Discovery Devices:INTERROGATORIES (con’t)

• Scope of interrogatories:

Any matters embraced in the disclosure requirement of CPLR § 3101: anything material and necessary to the prosecution or defense of an action.

• Answers to interrogatories are a sworn statement; and

• May require production of documents relevant to questions.

FRCP vs. CPLR

• Limit on Number of Interrogatories: • FRCP Rule 33: Unless otherwise stipulated or court ordered, may

only serve 25 interrogatories on any party. • CPLR: No limit.

• Who Can be Served:• FCRP Rule 33: Only a party to the litigation can be served with

interrogatories.• CPLR § 3130: Third parties may be served interrogatories with a

court order and is limited to financial information.

Discovery Devices:DEPOSITIONS

• Available for parties and non-parties;• More than just fact-finding;• Essential part of trial preparation;• New York rules do not allow deposition of experts (unlike

the federal rules); • Generally, defendant is considered to have “priority” to

take deposition Plaintiff may not serve a deposition notice on defendant (without Court Order) until defendant’s time to serve a responsive pleading has expired (CPLR § 3106).

FRCP vs. CPLR

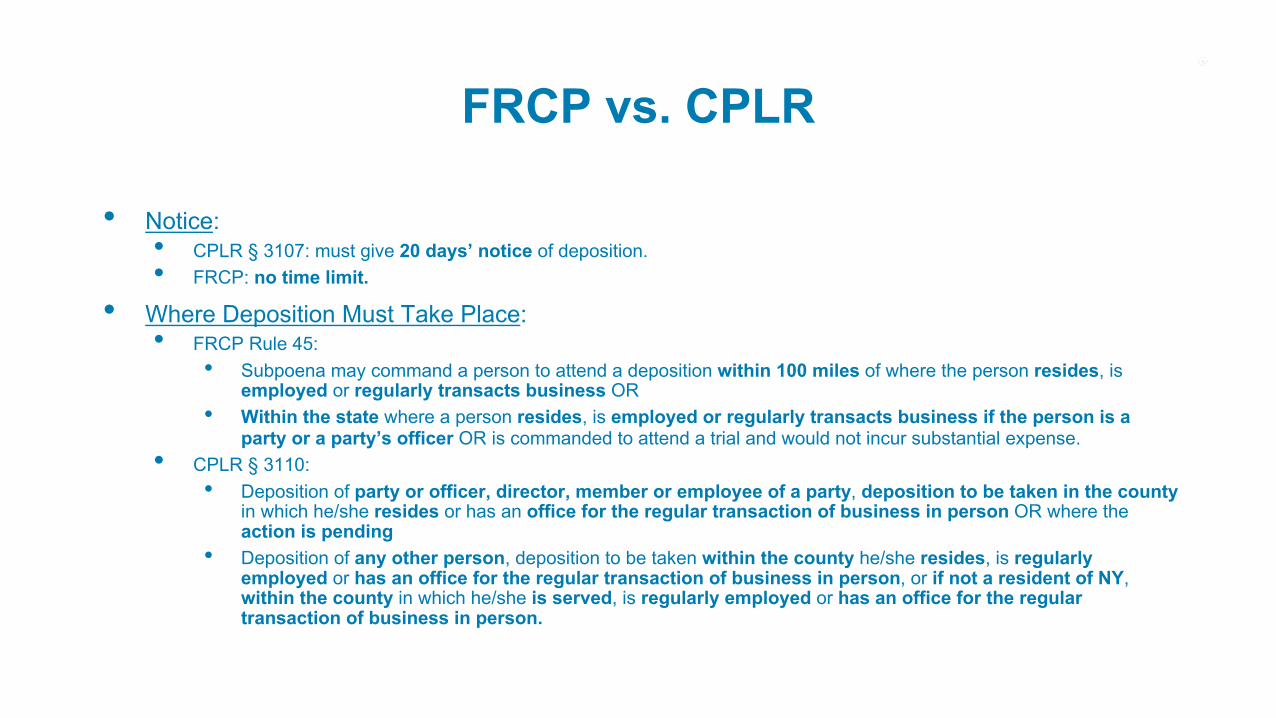

• Notice:• CPLR § 3107: must give 20 days’ notice of deposition.• FRCP: no time limit.

• Where Deposition Must Take Place: • FRCP Rule 45:

• Subpoena may command a person to attend a deposition within 100 miles of where the person resides, is employed or regularly transacts business OR

• Within the state where a person resides, is employed or regularly transacts business if the person is a party or a party’s officer OR is commanded to attend a trial and would not incur substantial expense.

• CPLR § 3110: • Deposition of party or officer, director, member or employee of a party, deposition to be taken in the county

in which he/she resides or has an office for the regular transaction of business in person OR where the action is pending

• Deposition of any other person, deposition to be taken within the county he/she resides, is regularly employed or has an office for the regular transaction of business in person, or if not a resident of NY, within the county in which he/she is served, is regularly employed or has an office for the regular transaction of business in person.

ELECTRONIC DISCOVERY

• Documents are increased stored electronically;

• Electronically stored documents are subject to discovery demands;

• Computers and electronic storage (including “clouds”) are akin to a file cabinet.

• Spoilation is a major issue:

• Electronically stored information must be preserved:• Must be addressed at the preliminary conference;• Preservation letters / notices should be sent to parties and non-parties when relevant.

ELECTRONIC DISCOVERY (con’t)

Spoilation is a major issue:

• Electronically stored information must be preserved:

• Must be addressed at the preliminary conference;

• Preservation letters / notices should be sent to parties and non-parties when relevant.

ELECTRONIC DISCOVERY (con’t)

• Form of production:• CPLR § 3122 directs to produce documents as they are

kept in the ordinary course of business or be organized and labeled to correspond to the categories in the request.

• Cost of production:• Absent a court order or compelling reasons to the contrary,

party seeking discovery should bear the costs incurred in the production.

ROLE OF ACCOUNTANTS AND FINANCIAL EXPERTS

IN MATRIMONIAL CASES

Financial experts may be

• Neutral (appointed by court or by agreement of parties); or

• Retained by one party.

ROLE OF ACCOUNTANTS AND FINANCIAL EXPERTS (con’t)

Two main areas:

• Division of property; and

• Determination of appropriate child and spousal support

ROLE OF ACCOUNTANTS AND FINANCIAL EXPERTS (con’t)

DIVISION OF PROPERTY

Financial experts assist with:

• Identification of assets, including asset tracing;• Classification of assets: marital v. separate;• Valuation of assets;• Division of assets between the parties; and• Tax issues.

ROLE OF ACCOUNTANTS AND FINANCIAL EXPERTS (con’t)

Determination of appropriate child and spousal support:

• Determination of income:

• Business owners;• Imputation of income; • Lifestyle analysis; and• Tax consequences from changes in the law regarding

deductibility of spousal support.