Dividend Policy in Switzerland - UZH - Doctoral Program in ... · Dividend Policy in Switzerland...

37

Dividend Policy in Switzerland Bogdan Stacescu October 30, 2004 Abstract The paper examines dividend policy for a sample of Swiss companies. Several factors that determine cross-sectional variations in dividend policy - such as profitability, growth opportunities and riskiness - are identified. The partial adjustment model based on the idea of stable target payout ratios is found to perform reasonably well. While dividend changes seem to be more closely associated with past and current rather than future net income growth, they could signal a persistent shift in the level of earnings. There also seems to be a significant relationship between losses and dividend cuts. 1 Introduction The very reason for the existence of dividend payments is a matter for debate. While there are many important explanations for the firms’ and investors’ behaviour in this area, none of them is generally accepted. The ”dividend irrelevance” proposition still looms large and empirical findings do not provide overwhelming support to one particular explanation. It seems that more research is needed to check the validity of theoretical models and to find additional regularities concerning dividends. The paper examines some of the characteristics of dividend policy using Swiss data. The aim is to single out several regularities concerning dividend payments, to compare results with those from previous research, and to test some of the predictions of theoretical litera- ture. The next section of the paper summarizes some of the alternative theories concerning div- idends. Section 3 presents several empirical results from previous studies. Section 4 briefly presents the data, and section 5 identifies some of the sources of cross-sectional variation in dividend policy. Companies that do not pay dividends are usually either younger, smaller, riskier, high-growth companies or older, more established companies facing persistent diffi- culties. Lower dividend payments are associated with higher market-to-book ratios, higher share price volatility and higher leverage. There is also some evidence that institutional investors prefer dividend-paying companies. Section 6 examines the relationship between dividends and earnings over time. In his classic study, Lintner (1956) suggests that managers set target payout ratios and gradually adjust dividends in order to reach the target. When applied to a sample of Swiss companies, the partial adjustment model performs reasonably well in most cases. A large body of literature suggests that dividends are used to signal future profitabil- ity. Empirical evidence on this issue is however rather mixed. Section 6.2. presents some evidence based on the Swiss sample. As in previous studies using US data, it seems that dividend changes are associated with past and current changes in earnings growth rather 1

Transcript of Dividend Policy in Switzerland - UZH - Doctoral Program in ... · Dividend Policy in Switzerland...

Dividend Policy in Switzerland

Bogdan Stacescu

October 30, 2004

Abstract

The paper examines dividend policy for a sample of Swiss companies. Several factors

that determine cross-sectional variations in dividend policy - such as profitability, growth

opportunities and riskiness - are identified. The partial adjustment model based on the idea

of stable target payout ratios is found to perform reasonably well. While dividend changes

seem to be more closely associated with past and current rather than future net income

growth, they could signal a persistent shift in the level of earnings. There also seems to be

a significant relationship between losses and dividend cuts.

1 Introduction

The very reason for the existence of dividend payments is a matter for debate. While

there are many important explanations for the firms’ and investors’ behaviour in this area,

none of them is generally accepted. The ”dividend irrelevance” proposition still looms large

and empirical findings do not provide overwhelming support to one particular explanation.

It seems that more research is needed to check the validity of theoretical models and to find

additional regularities concerning dividends.

The paper examines some of the characteristics of dividend policy using Swiss data. The

aim is to single out several regularities concerning dividend payments, to compare results

with those from previous research, and to test some of the predictions of theoretical litera-

ture.

The next section of the paper summarizes some of the alternative theories concerning div-

idends. Section 3 presents several empirical results from previous studies. Section 4 briefly

presents the data, and section 5 identifies some of the sources of cross-sectional variation in

dividend policy. Companies that do not pay dividends are usually either younger, smaller,

riskier, high-growth companies or older, more established companies facing persistent diffi-

culties. Lower dividend payments are associated with higher market-to-book ratios, higher

share price volatility and higher leverage. There is also some evidence that institutional

investors prefer dividend-paying companies.

Section 6 examines the relationship between dividends and earnings over time. In his

classic study, Lintner (1956) suggests that managers set target payout ratios and gradually

adjust dividends in order to reach the target. When applied to a sample of Swiss companies,

the partial adjustment model performs reasonably well in most cases.

A large body of literature suggests that dividends are used to signal future profitabil-

ity. Empirical evidence on this issue is however rather mixed. Section 6.2. presents some

evidence based on the Swiss sample. As in previous studies using US data, it seems that

dividend changes are associated with past and current changes in earnings growth rather

1

than with future ones. However, a more in-depth look at the data suggests that changes

in dividends signal a persistent change in the average level of earnings (as shown in Table

16). Thus the good news associated with dividend increases may be that - at least over the

medium term - earnings have shifted to a higher level.

Section 6.3. presents evidence that losses are to a significant extent a necessary condition

for dividend cuts. Section 7 concludes.

2 Motivation and Related Literature

Dividend policy has long been a subject of research and debate. There are many theoret-

ical and empirical results describing the decisions companies make in this area. At the same

time, however, there is no generally accepted model describing payout policy. Moreover,

empirical findings are often contradictory or difficult to interpret in light of the theory.

In their seminal paper, Miller and Modigliani (1961) showed that under certain assump-

tions dividends are irrelevant; all that matters is the firm’s investment opportunities. Miller

and Modigliani considered the case of perfect capital markets (no transaction costs or tax

differentials, no pricing power for any of the participants, no information asymmetries or

costs), rational behaviour (more wealth being preferred to less, indifference between cash

payments and share value increases) and perfect certainty (future investments and profits

are given).

In the environment described above, Miller and Modigliani show that dividend policy

does not affect the value of the firm. This is true whether one considers the value of the

firm to be given by the discounted cash flow method, by the stream of future dividends

or earnings or as a sum of current earnings and future investment opportunities. Given

perfect capital markets, the firm will always be able to compensate the cash outflow by at-

tracting new money (via new shares or debt) if this is required by its investment programme.

In ”real life”, however, people seem to care about dividends. Lintner’s (1956) classical

study on dividend policy suggests that ”dividends represent the primary and active deci-

sion variable in most situations”. The interviews and research conducted on 28 companies

suggested that firms set their current dividends based on their previous history. The main

decision concerned the possible change in the payment rate and this decision was based

on (expected future) earnings. Dividend policy seemed characterized by ”inertia and con-

servatism”; managers seemed to think that investors reward stability and avoided making

unsustainable changes in payout ratios. Lintner suggests a model of partial adjustment to

a given payout rate.

In a recent study, Brav, Graham, Harvey and Michaely (2004) find that ”maintaining

the dividend level is a priority on par with investment decisions” and that less than half of

the executives they interviewed agree that ”the availability of good investment opportuni-

ties is an important or very important factor affecting dividend decisions”. Although to a

somehow lesser degree, Lintner’s findings seem valid almost half a century later.

Researchers have tried to explain the importance of dividends by looking for ”imperfec-

tions” that can undermine the irrelevance proposition. Modigliani and Miller themselves

suggested that taxes can be a factor: dividends are taxed in a different way from capital

gains. Information asymmetries between the management of a company and its (prospec-

tive) shareholders can lead to dividends being used as costly signals. Agency problems

2

between shareholders and management or shareholders and debtholders in a world of imper-

fect contracting - mean that dividends can be used as a way to control the behaviour of the

other party. Incomplete markets could reduce the investors’ ability to substitute between

cash and capital gains depending on their liquidity needs.

Static models based on taxes suggest that there could be ’tax clienteles’ attempting to

reduce their tax outlays. Individuals in high tax brackets should choose low-dividend paying

companies, while corporations should choose high-dividend paying shares. In equilibrium, as

Miller and Modigliani (1961) there will be no effect on share prices. There is however little

evidence that the tax clientele effect is very important (Allen and Michaely 2002). Crockett

and Friend (1988) note that there were no significant effects on dividends generated by

the gradual decrease in income tax rates over the 1940-1985 period. They also point out

that retained earnings are not significantly correlated with capital gains; over the 1970s ”a

substantial volume of retained earnings was associated with substantial capital losses”.

Dynamic tax models imply that high marginal tax rate investors could also reduce their

tax liabilities by selling their shares before the shares go ex-dividend and buying them again

afterwards. Investors with a low dividend tax rate will be willing to do the opposite. Thus

the tax effect will be seen in volume rather than price; however, given transaction costs,

taxes will also influence prices. Empirical evidence seems to give more support to dynamic

than to static strategies (Allen and Michaely 2002). A survey of financial executives by Brav,

Graham, Harvey and Michaely (2004) finds that from the management’s point of view tax

concerns are of secondary importance when deciding dividend policy.

Modigliani and Miller (1961) assume that information is the same and free for all partic-

ipants. In practice, however, this assumption is not likely to hold and information asymme-

tries can have important consequences. An important class of models is based on the idea

that dividends can be used as signals of firm quality.

Bhattacharya (1979) builds a two-period model with two types of firms. Investments

are made during the first period; their expected profitability is known to management, but

not to outside investors. In order to signal the quality of their investment, the managers

of ’good’ firms (managers are assumed to act in the interest of initial shareholders) will

commit to paying high dividends in the second period. Since attracting outside financing

(during the second period) is expensive due to transaction costs, the ’low quality’ firms will

be unable to imitate the ’high quality’ ones.

Miller and Rock (1985) also build a signalling model - the cost of the signal in their

version being forced reductions in investment. The model of John and Williams (1985) uses

taxes as the main cost of dividends; thus, unlike the previous two models, it can be used

to distinguish between dividends and share repurchases, which enjoy a more favourable

tax treatment. High dividends are a signal of undervalued shares (high firm quality) -

shareholders will have to pay taxes on them, but they retain a proportionately higher share

in the firm, which is valuable to them. The opposite is true if the firm is overvalued.

John and Williams also show that their model implies that dividends are smoothed with

respect to share prices rather than net cash inflows as in previous models. They suggest

that ”firms with more risky returns on assets pay lower dividends, other things equal”.

Kumar (1988) builds a model that explains dividend smoothing - one of the most salient

features of dividend policy. Dividends once again signal a firm’s quality (productivity), but,

since they are overinvested in the firm, managers will try to underinvest by underreporting

a firm’s productivity. While there is no fully revealing equilibrium, Kumar shows that firms

will tend to cluster around optimal dividend levels.

The signalling models provide an explanation for the positive stock price reaction to

3

the announcement of dividend increases or initiations. At least some empirical evidence,

however, seems to suggest that the increase in dividend payments is not followed by an in-

crease in firms’ earnings (Benartzi, Michaely, Thaler 1997). Indeed, it has been shown that

earnings growth is higher in after dividend cuts. Thus the increase in earnings precedes the

dividend increase rather than follow it. While they agree that dividends are used to convey

information to the market, managers seem not to think within the ’costly signalling’ frame-

work used in academic models (Brav et al. 2004). Grullon, Michaely and Swaminathan

(2002) suggest that rather than an increase in profitability dividend increases could reflect

a decrease in risk - the ’maturity hypothesis’.

Agency theory suggests that dividends can be used as a means to control a firm’s man-

agement. Distributing dividends reduces the free cash flow problem and increases the man-

agement’s equity stake. The question remains why the shareholders would not use debt

or share repurchases instead. LaPorta, Lopez-de-Silanes and Shleifer (2000) find that in

countries with better shareholder rights firms pay proportionally more dividends. Therefore

”there is no evidence that in countries with low investor protection, management will vol-

untarily commit itself to pay out higher dividends and to be monitored more frequently by

the market” (Allen and Michaely 2002).

Fudenberg and Tirole (1995) build a model that shows that, when managers are risk-

averse and more recent information has a higher weight in assessing their performance, there

will be both dividend and earnings smoothing.

Another agency problem is that between shareholders and debtholders. The risk that

shareholders will expropriate debtholders by paying themselves excessive dividends has led

to the often encountered covenants restricting dividend policy in bond contracts. Empirical

studies also suggest that firms hold more cash than the minimum stipulated in bond con-

tracts in order to consolidate their reputation as good quality borrowers. (Kalay 1982). The

reputation effect is also supported by the fact that firms in financial distress are reluctant

to cut dividends (DeAngelo and DeAngelo 1990).

To sum up, there are several credible explanations for the existence of dividends, although

none of them is generally accepted or above criticism. The Miller and Modigliani proposition

of dividend irrelevance is still widely mentioned, as is the idea of a ”dividend puzzle”.

3 Previous Empirical Findings

There are many empirical studies that try to assess the validity of the various theories

concerning dividend policy. Their findings, whether they are focused on signalling, taxes or

agency explanations, are often contradictory.

Denis, Denis, and Sarin (1994) examine the predictions of the signalling, overinvestment

(free cash flow) and dividend clientele hypotheses. Using large (more that 10%) changes in

dividends per share for US firms over the 1962-1988 period, they find stronger support for the

signalling and dividend clientele hypotheses than for the overinvestment theory. The proxies

used for the first two are significant in a regression explaining the excess returns of dividend

announcements, while the proxies based on Tobin’s q are insignificant. Denis et al. also find

that firms increase capital expenditures following dividend increases and decrease them after

dividend decreases; this also contradicts the overinvestment/free cash flow explanation. The

results in Yoon and Starks (1995) also support the signalling hypothesis.

4

Johnson (1995) examines the use of debt and dividends as predicted by the signalling or

free cash flow theories. He finds that share price reactions to straight debt issues announce-

ments is significantly different from zero (at a 10% level) for low-dividend-paying companies,

but insignificantly different from zero for companies that pay high dividends. For the sub-

group of low growth - low dividends firms, the reaction is significant at a 1% level. The

evidence thus suggests that dividends and debt are substitutes, whether for signalling or

management control purposes.

Michaely, Thaler and Womack (1995) examine market reactions to dividend initiations

and omissions. As in earlier papers, they find that the magnitude of short-term reactions to

omissions is much higher than the reaction to dividend initiations. This could be because

the change in the dividend yield is much higher for omissions than for initiations. More

importantly, they find that prices tend to drift in the same direction over the following

year. For a smaller sample, they compare this drift with the drift generated by earnings

surprises and find that the former is distinct from and stronger than the latter. They also

examine turnover around the dividend announcement day and find weak evidence in favour

of clientele effects.

DeAngelo, DeAngelo and Skinner (1992) examine the connection between losses and

dividend cuts and omissions. They find that ”an annual loss is essentially a necessary

condition for dividend reductions in firms with established earnings and dividend records”.

Benartzi, Michaely and Thaler (1997) examine earnings growth around dividend changes

and find that the earnings growth rates do not increase for companies that have increased

dividends, while they do increase for companies that have decreased them. They argue

that dividend changes are more related to past and current earnings growth than to future

earnings growth. Based on their empirical results, Grullon, Michaely and Swaminathan

(2002) argue that dividend increases signal a decrease in risk rather than an increase in

profitability.

Bernheim and Wantz (1995) explore the influence of taxes on the effect of dividend

change announcements. They define the ”bang-for-the-buck” as ”the share price response

per dollar of dividends”. Dividend signalling models imply that the ”bang-for-the-buck”

should increase when the relative taxation of dividends increase, while free cash flow models

generally suggest that there should be a decrease in the announcement effect. The authors

find that US data over the 1962-1988 period supports the signalling hypothesis.

Hubbard and Michaely (1997) analyse the ’Citizens Utilities Case’. Until 1990, Citizens

Utilities Company had two classes of stock: one of them paid stock dividends and the other

an equivalent amount of cash dividends. Despite the unfavourable tax treatment of cash

dividends, the second type of shares traditionally sold at a premium, and this premium

seems even larger in the 1980s than in the 1960s. The tax reform in 1986 led to a movement

in the ’right’ direction, but this effect was only temporary. The authors look for evidence of

clientele effects and differences in liquidity, but find that they cannot account for the strange

behaviour of relative prices.

In conclusion, empirical results do not always agree and there is still no overwhelming

support for just one of the competing explanations for dividends. It is possible that theories

based on signalling, tax differentials or agency problems all have a real basis - they are not,

after all, mutually exclusive. It may also be that there are additional valid explanations.

5

4 Data

The paper uses data on listed Swiss companies over the 1974-2004 period. There are

175 non-financial, non-utility companies in the overall sample. The sources for the data

are Datastream and annual reports (for information on the main shareholders). Because of

limited data availability, smaller samples are used in some of the following sections.

Unlike American companies, that pay dividends on a quarterly basis, Swiss companies

usually pay dividends only once a year. (Ex-dividend days are usually in May or June).

Thus the analysis in this paper uses yearly observations. This has the obvious disadvantage

of reducing the number of data points. On the other hand, studies such as Lintner (1956)

and DeAngelo, DeAngelo and Skinner (1992) argue that the main horizon for dividend policy

is the whole year even in the American case.

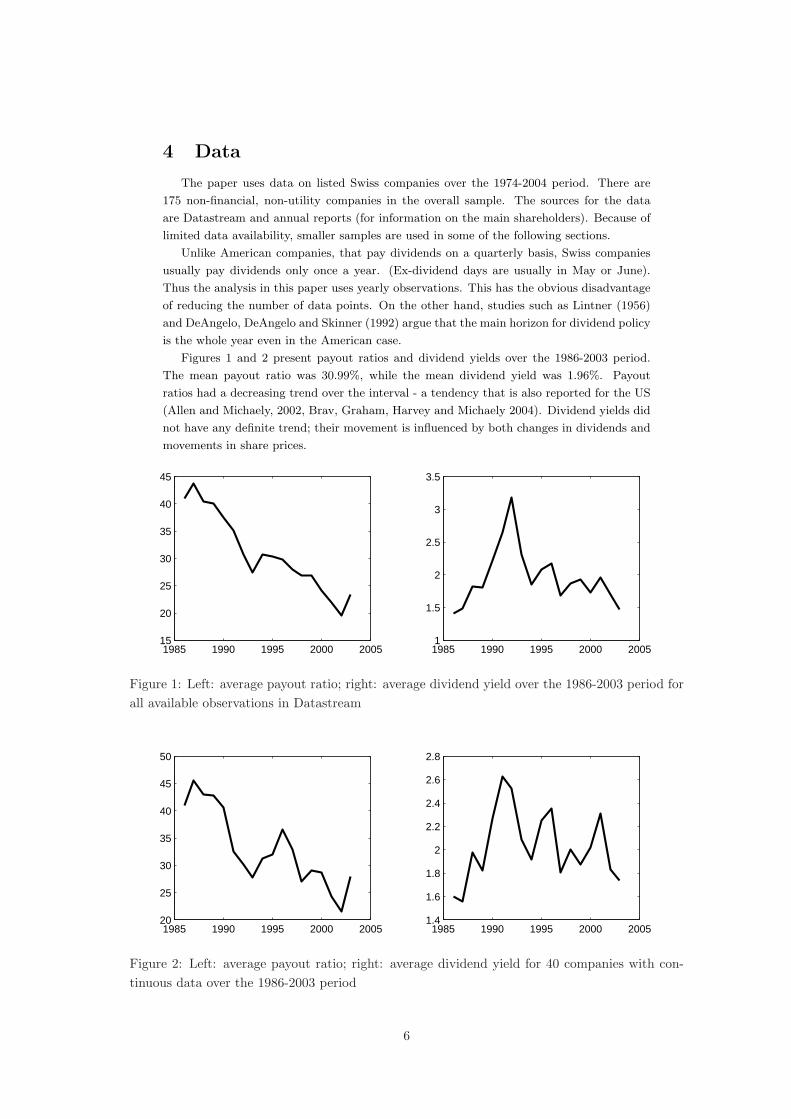

Figures 1 and 2 present payout ratios and dividend yields over the 1986-2003 period.

The mean payout ratio was 30.99%, while the mean dividend yield was 1.96%. Payout

ratios had a decreasing trend over the interval - a tendency that is also reported for the US

(Allen and Michaely, 2002, Brav, Graham, Harvey and Michaely 2004). Dividend yields did

not have any definite trend; their movement is influenced by both changes in dividends and

movements in share prices.

1985 1990 1995 2000 200515

20

25

30

35

40

45

1985 1990 1995 2000 20051

1.5

2

2.5

3

3.5

Figure 1: Left: average payout ratio; right: average dividend yield over the 1986-2003 period forall available observations in Datastream

1985 1990 1995 2000 200520

25

30

35

40

45

50

1985 1990 1995 2000 20051.4

1.6

1.8

2

2.2

2.4

2.6

2.8

Figure 2: Left: average payout ratio; right: average dividend yield for 40 companies with con-tinuous data over the 1986-2003 period

6

Table 1: Comparison between dividend-paying and non-paying companies, 2000-2003

Variable Mean Mean p-valuespaying group non-paying group

Mean market-to-book ratio, 2000-2003 2.226 3.401 0.052Mean return on assets, 2000-2003 5.093 -4.566 0.000Mean return on equity, 2000-2003 10.893 -21.359 0.000Mean capital gearing, 2000-2003 37.770 37.120 0.881Mean price volatility, 2000-2003 24.740 38.250 0.000Beta coefficient 0.86 1.33 0.009Mean total assets, 2000-2003 (CHF, thousands) 4,643,377 1,484,523 0.108Mean sales, 2000-2003 (CHF, thousands) 3,017,036 467,396 0.184Mean foreign-owned share of capital, 2001-2003 8.08 15.42 0.081Share of capital owned by large shareholders, 2003 46.03 41.78 0.412Share of voting rights for large shareholders, 2003 42.19 40.34 0.780

5 Cross-Sectional Comparisons of Dividend Pay-

ments

5.1. Who pays dividends?

There are several features that distinguish firms that pay dividends from firms that do

not.

The analysis in this subsection focuses on the 2000-2003 period and distinguishes between

companies that had at least one dividend payment over the four years and companies that

had none. Table 1 summarizes some of the main features of the two groups.

Not surprisingly, companies that paid dividends over the 2000-2003 period had signif-

icantly higher profitability than companies that did not. It is interesting to note that

non-paying companies made losses on average, while companies that paid dividends had

positive mean returns on assets and equity.

Non-paying firms had a higher market-to-book ratio. Indeed, agency theory suggests

that companies with better growth opportunities (proxied by the market-to-book ratio) are

less likely to have free cash flow problems. Therefore dividends as an instrument to discipline

management are less useful to these companies. Denis, Denis and Sarin (1994) note that

dividend yield and Tobin’s q are negatively related; this relationship seems to hold for the

Swiss sample. The fact that leverage is virtually identical for the two groups of companies

may mean that dividends and debt are used in different ways to control management, as

suggested by Johnson (1995).

Companies that did not pay dividends over the four years also had higher price volatility

(where price volatility is computed as the band within which the share price moved around

the mean price during the year) and higher betas. They also tended to have lower total assets

and lower sales (although the difference is not significant for the latter). Together with the

higher market-to-book ratio, these differences give support to the ”maturity hypothesis” of

Grullon, Michaely and Swaminathan (2002): companies that are younger and riskier tend

7

to pay lower dividends.

Ownership concentration does not seem to affect the option to pay dividends. This

conclusion holds whether one considers the share of voting rights or the share of the equity

owned by large shareholders (shareholders that have more than 5% of a company’s voting

rights and that are obliged to make their ownership public under Swiss regulations). Two

other aspects concerning ownership seem to be more closely related with the decision to

pay dividends. Institutional investors (investment companies and pension funds) only held

significant participations in dividend-paying companies. This finding is similar to results

from previous papers, such as Grinstein and Michaely (2003). Dividend-paying companies

also had a lower foreign-owned share of capital.

There were no significant differences between various industries regarding the decision

to pay dividends.

To sum up, companies that do not pay dividends seem to be either old, established com-

panies going through protracted difficulties, or - more often - younger, smaller and riskier

companies.

5.2. Sources of Cross-Section Variation

This section focusses on the relationship between payout ratios and dividend yields and

the variables described above over the 2000-2003 period. It also presents results for the

subsample of companies that had at least one dividend payment in one of the four years.

As it will be shown below, the relationship between dividend payments and the variables

described above is not always monotonic.

Table 2 shows that, taking the whole set of firms, more profitable companies have higher

dividend yields and payout ratios. Taking just the group of companies with positive dividend

payments over the 2000-2003 period, however, the relationship is only significant for the

payout ratio and returns on assets. The other correlations are insignificant and even have

”wrong” signs.

The fact that companies with higher price volatility and higher market-to-book ratios

have lower dividend yields and payout ratios supports the ”maturity hypothesis” of Grullon,

Michaely and Swaminathan (1994). ”Younger” (smaller, riskier, growing) companies pay

less dividends than ”older” ones. One could note, however, that there the correlations with

firm size are not significant in this sample. Thus, while starting to pay dividends could be

a sign of firm ”maturity”, increasing dividend payments could be a sign that the company

is moving from a ”riskier” to a quieter period in its life. As Grullon et al. point out, the

positive reaction on dividend increase announcements could be generated by the fact that

investors take them as a sign of risk reduction rather than profitability increase. This result

is related to Lintner’s (1956) finding that managers are reluctant to increase dividends if

they are not sure that future earnings will be stable enough to prevent dividend decreases.

Capital gearing is negatively correlated with the payout ratio and the dividend yield, with

the former relationship being usually positive. This may be because of debt covenants or

because leveraged firms try to increase their retained earnings and reduce their dependence

on external financing. It could also be that debt and dividends are alternative means to

reduce agency problems. The relationship is not very strong, however, and using the ratio

between total debt and the market value instead of capital gearing leads to an insignificant

correlation.

Dividend policy shows no very strong influence from ownership structure. There is a

positive correlation between ownership concentration (indicated by the total voting rights

8

Table 2: Dividend yield and firm characteristics

Variables Correlation Correlation Correlation - ”paying” Correlation - ”paying”(averages (2003) subsample (averages subsample

2000-2003) 2000-2003) (2003)Market-to-book ratio -0.309*** -0.053 -0.308* -0.128Returns on assets 0.214*** 0.264*** -0.048 0.199Returns on equity 0.129 0.216*** -0.121 -0.051Sales -0.048 -0.054 -0.114 -0.040Total assets -0.064 -0.062 -0.153 -0.044Capital gearing -0.059* -0.010 -0.038 -0.060Price volatility -0.532*** -0.481*** -0.464*** -0.414***Voting rights oflarge shareholders 0.179* 0.192** 0.187** 0.073Capital share oflarge shareholders 0.122 0.153* 0.153 0.024Share of capital owned byfamilies and employees -0.015 -0.024 -0.096 -0.093Foreign-owned shareof capital -0.04 0.068 0.084 -0.038Share of capital owned byinstitutions 0.162* 0.029 0.187** 0.056Payout ratio 0.633*** 0.537*** 0.418*** 0.367***

* Significant at a 10% confidence level.

**Significant at a 5% confidence level.

***Significant at a 1% confidence level.

9

Table 3: Payout ratio and firm characteristics

Variables Correlation Correlation Correlation - ”paying” Correlation - ”paying”(averages (2003) subsample (averages subsample (2003)

2000-2003) 2000-2003)Market-to-book ratio -0.188** -0.001 -0.114 -0.028Returns on assets 0.337*** 0.419*** 0.266** 0.205**Returns on equity 0.199** 0.332*** 0.006 -0.063Sales 0.063 0.050 0.028 0.068Total assets 0.067 0.066 0.033 0.076Capital gearing -0.132 -0.176** -0.196*** -0.238***Price volatility -0.497*** -0.375*** -0.407*** -0.287***Voting rights oflarge shareholders -0.004 -0.0297 0.030 -0.016Capital share oflarge shareholders -0.032 -0.011 -0.015 -0.068Share of capital ownedby families and employees -0.096 -0.074 -0.121 -0.164Foreign-owned shareof capital 0.046 0.014 0.194** 0.107Share of capital ownedby institutions -0.036 -0.094 -0.032 0.019

* Significant at a 10% confidence level.

**Significant at a 5% confidence level.

***Significant at a 1% confidence level.

10

Table 4: Dividend payments across industries, 2000-2003

Industry Mean payout ratio, Mean dividend yield,2000-2003 2000-2003

Transport (7 companies) 36.45% 2.34%Retailers (8 companies) 33.45% 2.27%Chemicals and pharmaceuticals 21.27% 1.39%(20 companies)Electrical engineering and electronics 12.86% 1.28%(21 companies)Machinery (23 companies) 16.85% 1.52%Food and luxury goods (11 companies) 30.81% 1.67%Building contractors and materials 22.81% 1.30%(6 companies)Miscellaneous industrials (28 companies) 17.39% 1.52%Miscellaneous services (51 companies) 24.15% 2.06%

of major shareholders) and dividend yield. The relationship does not hold for payout ratios,

however. While the foreign participation in companies that made no dividend payments

over the period was higher than in the dividend-paying companies, within the latter group

foreign investors seem to prefer companies with higher payout ratios.

We have seen above that significant institutional ownership (ownership by investment

companies and pension funds) is only associated with dividend-paying companies. There is

some evidence that institutions prefer companies with higher dividend yields, but the rela-

tionship between institutional holdings and payout ratios is not significant. Grinstein and

Michaely (2003) also report that the relationship between institutional ownership and divi-

dend yield is not monotonic. They find that institutions choose dividend-paying companies,

but they show no preference for higher dividends.

There is a positive and significant relationship between dividend yields and payout ra-

tios. While the relationship is hardly surprising, it shows that one of the reasons for higher

dividend yields is that companies pay a higher share of their earnings as dividends.

There are no very large differences between various industries concerning payout ratios

and dividend yields (as shown in table 4). The groups are based on the classification of the

Swiss stock exchange. Broadly speaking, industrial companies pay less dividends than those

in the service sector.

The simple analysis of correlations allows us to determine several factors affecting divi-

dend yields and payout ratios. These findings can be checked using regression analysis. The

regression results show that the variables outlined above explain part of the variability in

dividend policy across firms. Robust (White) residuals were used in both cases to avoid

heteroscedasticity problems.

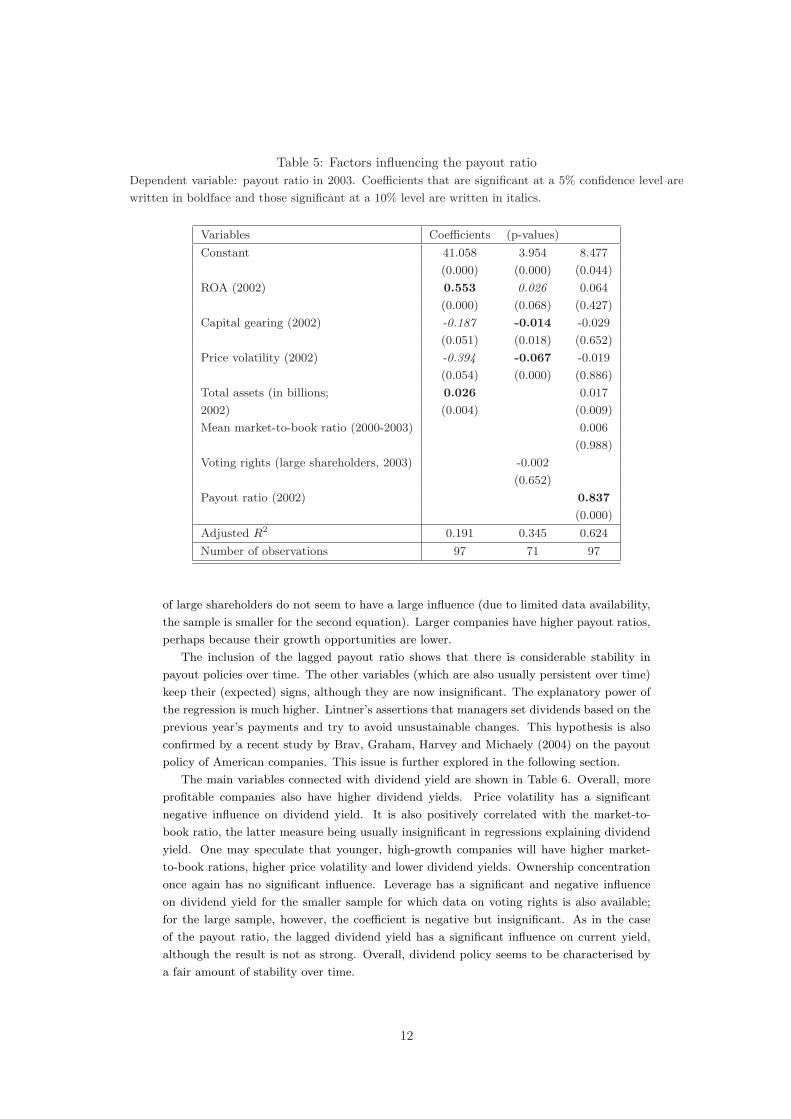

Table 5 presents the main factors influencing payout ratios. As noted above, higher

profitability is associated with higher payout ratios. Leverage has a negative influence on

payout ratios - this can be the result of debt covenants or, as Johnson (1995) suggests, of the

fact that debt and dividends are substitutes in controlling management. The voting rights

11

Table 5: Factors influencing the payout ratioDependent variable: payout ratio in 2003. Coefficients that are significant at a 5% confidence level are

written in boldface and those significant at a 10% level are written in italics.

Variables Coefficients (p-values)

Constant 41.058 3.954 8.477

(0.000) (0.000) (0.044)

ROA (2002) 0.553 0.026 0.064

(0.000) (0.068) (0.427)

Capital gearing (2002) -0.187 -0.014 -0.029

(0.051) (0.018) (0.652)

Price volatility (2002) -0.394 -0.067 -0.019

(0.054) (0.000) (0.886)

Total assets (in billions; 0.026 0.017

2002) (0.004) (0.009)

Mean market-to-book ratio (2000-2003) 0.006

(0.988)

Voting rights (large shareholders, 2003) -0.002

(0.652)

Payout ratio (2002) 0.837

(0.000)

Adjusted R2 0.191 0.345 0.624

Number of observations 97 71 97

of large shareholders do not seem to have a large influence (due to limited data availability,

the sample is smaller for the second equation). Larger companies have higher payout ratios,

perhaps because their growth opportunities are lower.

The inclusion of the lagged payout ratio shows that there is considerable stability in

payout policies over time. The other variables (which are also usually persistent over time)

keep their (expected) signs, although they are now insignificant. The explanatory power of

the regression is much higher. Lintner’s assertions that managers set dividends based on the

previous year’s payments and try to avoid unsustainable changes. This hypothesis is also

confirmed by a recent study by Brav, Graham, Harvey and Michaely (2004) on the payout

policy of American companies. This issue is further explored in the following section.

The main variables connected with dividend yield are shown in Table 6. Overall, more

profitable companies also have higher dividend yields. Price volatility has a significant

negative influence on dividend yield. It is also positively correlated with the market-to-

book ratio, the latter measure being usually insignificant in regressions explaining dividend

yield. One may speculate that younger, high-growth companies will have higher market-

to-book rations, higher price volatility and lower dividend yields. Ownership concentration

once again has no significant influence. Leverage has a significant and negative influence

on dividend yield for the smaller sample for which data on voting rights is also available;

for the large sample, however, the coefficient is negative but insignificant. As in the case

of the payout ratio, the lagged dividend yield has a significant influence on current yield,

although the result is not as strong. Overall, dividend policy seems to be characterised by

a fair amount of stability over time.

12

Table 6: Factors influencing dividend yieldDependent variable: Dividend yield in 2003. Coefficients that are significant at a 5% confidence level

are written in boldface and those significant at a 10% level are written in italics.

Variables Coefficients (p-values)

Constant 3.954 3.925 0.604 3.567

(0.000) (0.031) (0.000) (0.000)

ROA (2002) 0.026 0.030 0.027 0.031

(0.081) (0.046) (0.099) (0.048)

Capital gearing (2002) -0.014 -0.016 -0.016

(0.004) (0.019) (0.022)

Price volatility (2002) -0.067 -0.059 -0.052

(0.000) (0.000) (0.003)

Voting rights (large shareholders, 2003) -0.0023 -0.003 -0.002

(0.696) (0.423) (0.736)

Dividend yield (2002) 0.602 0.107

(0.002) (0.301)

Mean market-to-book ratio (2000-2003) -0.037 -0.069

(0.353) (0.199)

Adjusted R2 0.345 0.347 0.332 0.354

Number of observations 71 71 107 71

6 The Dynamic Aspect: Dividends and Earnings

6.1. The Lintner Model and Payout Targets

As we have seen in the previous section, dividend policy seems to be stable over time.

Lintner (1956) suggests that managers set targets concerning payout ratios and they adjust

dividend payments in order to gradually reach that target. Under this hypothsis, the target

ratio is given by

D∗t = γEt,

and the adjustment equation is

Dt −Dt−1 = α + δ(D∗t −Dt−1) + εt,

where Dt are dividends paid in year t, Et are earnings for the same year, and D∗t is the

desired level of dividends in year t.

Combining the two equations the model proposed by Lintner can be written as:

∆Dt = α + β1Dt−1 + β2Et + ut

The change in dividends is thus modelled as a function of lagged dividends and current

earnings. The equation is a partial adjustment model, which can be consistently estimated

by ordinary least squares. The target payout ratio is estimated as −β̂2/β̂1, while the speed

of adjustment is given by −β̂1.

Estimating the Lintner model requires data over a longer period of time, and as a result

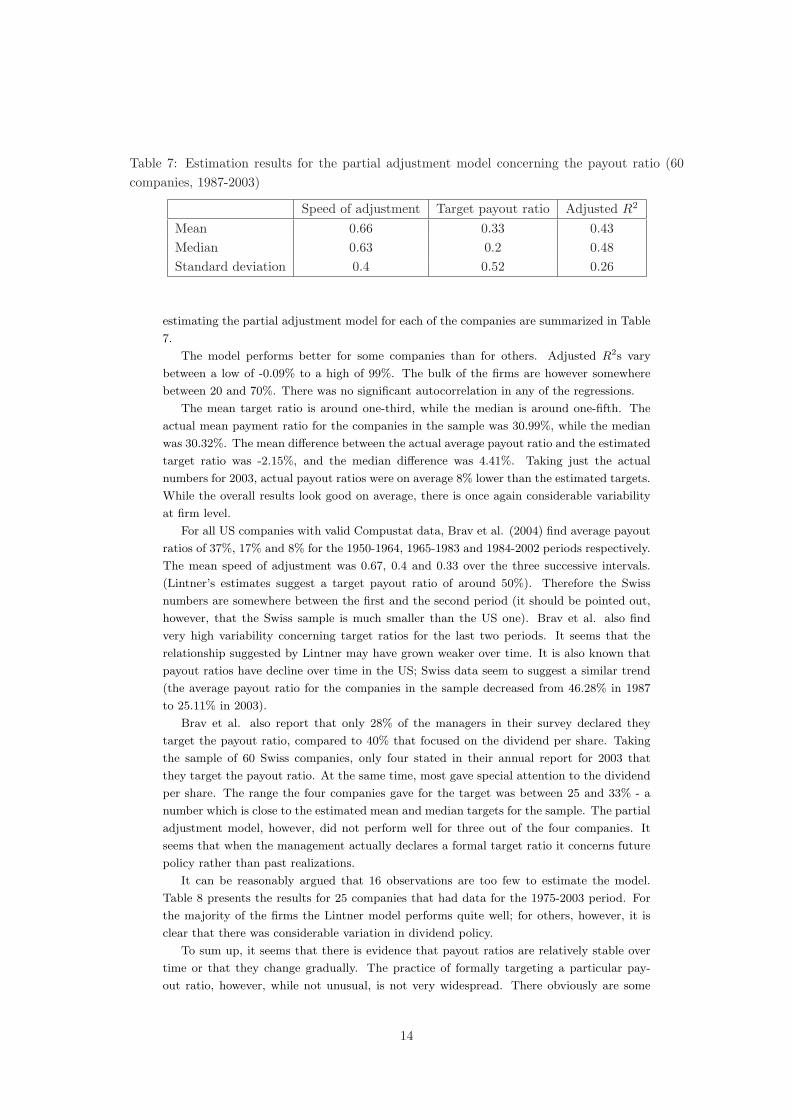

the sample is reduced to 60 companies for the 1987-2003 period (16 years). The results of

13

Table 7: Estimation results for the partial adjustment model concerning the payout ratio (60companies, 1987-2003)

Speed of adjustment Target payout ratio Adjusted R2

Mean 0.66 0.33 0.43Median 0.63 0.2 0.48Standard deviation 0.4 0.52 0.26

estimating the partial adjustment model for each of the companies are summarized in Table

7.

The model performs better for some companies than for others. Adjusted R2s vary

between a low of -0.09% to a high of 99%. The bulk of the firms are however somewhere

between 20 and 70%. There was no significant autocorrelation in any of the regressions.

The mean target ratio is around one-third, while the median is around one-fifth. The

actual mean payment ratio for the companies in the sample was 30.99%, while the median

was 30.32%. The mean difference between the actual average payout ratio and the estimated

target ratio was -2.15%, and the median difference was 4.41%. Taking just the actual

numbers for 2003, actual payout ratios were on average 8% lower than the estimated targets.

While the overall results look good on average, there is once again considerable variability

at firm level.

For all US companies with valid Compustat data, Brav et al. (2004) find average payout

ratios of 37%, 17% and 8% for the 1950-1964, 1965-1983 and 1984-2002 periods respectively.

The mean speed of adjustment was 0.67, 0.4 and 0.33 over the three successive intervals.

(Lintner’s estimates suggest a target payout ratio of around 50%). Therefore the Swiss

numbers are somewhere between the first and the second period (it should be pointed out,

however, that the Swiss sample is much smaller than the US one). Brav et al. also find

very high variability concerning target ratios for the last two periods. It seems that the

relationship suggested by Lintner may have grown weaker over time. It is also known that

payout ratios have decline over time in the US; Swiss data seem to suggest a similar trend

(the average payout ratio for the companies in the sample decreased from 46.28% in 1987

to 25.11% in 2003).

Brav et al. also report that only 28% of the managers in their survey declared they

target the payout ratio, compared to 40% that focused on the dividend per share. Taking

the sample of 60 Swiss companies, only four stated in their annual report for 2003 that

they target the payout ratio. At the same time, most gave special attention to the dividend

per share. The range the four companies gave for the target was between 25 and 33% - a

number which is close to the estimated mean and median targets for the sample. The partial

adjustment model, however, did not perform well for three out of the four companies. It

seems that when the management actually declares a formal target ratio it concerns future

policy rather than past realizations.

It can be reasonably argued that 16 observations are too few to estimate the model.

Table 8 presents the results for 25 companies that had data for the 1975-2003 period. For

the majority of the firms the Lintner model performs quite well; for others, however, it is

clear that there was considerable variation in dividend policy.

To sum up, it seems that there is evidence that payout ratios are relatively stable over

time or that they change gradually. The practice of formally targeting a particular pay-

out ratio, however, while not unusual, is not very widespread. There obviously are some

14

Table 8: Estimation results for the partial adjustment model concerning the payout ratio (25companies, 1975-2003)

Speed of adjustment Target payout ratio Adjusted R2

Mean 0.49 0.29 0.47Median 0.54 0.27 0.45Standard deviation 0.35 0.29 0.21

caveats to consider when one applies the Lintner model to company data. Using annual

data, one needs a long period to estimate the target - and it is quite likely that even if the

payout ratio is indeed targeted, the benchmark itself will have bee adjusted over time (as

a result of business cycles or institutional trends or major unexpected events in the life of

the company). Still, as previous empirical studies have noted, the partial adjustment model

performs reasonably well for a large number of companies.

6.2. Dividends and Past, Current and Future Earnings

Many models suggest that dividends are costly signals of future profitability. This can

explain both why dividends are paid in spite of the tax advantage for capital gains and

why announcements of dividend increases are usually accompanied by positive share price

reactions.

Empirical evidence on the validity of the signalling hypothesis is not completely conclu-

sive. The positive (negative) share price reaction to the announcement of dividend increases

(decreases) is widely documented; however, the precise reasons for this reaction are still a

matter for debate. Yoon and Starks (1995) find that dividend change announcements are

associated with revisions in analysts’ forecasts of current income. Bernheim and Wantz

(1995) find that increases in dividend taxation lead to increases in the share price response

for an increase in dividends (which they call the ”bang-for-the buck”) - therefore an in-

crease in the cost of the signal increases its effectiveness. Kao and Wu (1994) examine the

relationship between unexpected dividend and earnings changes and argue that ”dividends

reflect past, current and future earnings information”. Penman (1983) finds that ”both

dividend announcements and managements’ earnings forecasts possess information about

managements’ expectations”. However, he also notes that firms usually do not fully adjust

their dividends to reflect future expected earnings increases; changes in dividends have less

explanatory power than earnings forecasts. Amihud and Murgia (1997) find that share price

reactions to dividend change announcements are similar in Germany and the US, although

in the former dividends were not tax disadvantaged at the time. Benartzi, Michaely and

Thaler (1997) and Grullon, Michaely and Benartzi (2003) strongly dispute the idea that

dividend changes forecast future changes in earnings.

In order to examine the relationship between dividends and earnings I use data on 73

companies over the 1982-2004 period. The resulting sample has 741 firm-years for which

data on (split-adjusted) dividends per share is available for five previous and at least three

future years. In 48 of these years companies reduced dividends by more than 10% and in 8

of them by less than 10%. In 202 cases there was no change in dividends per share, while in

96 of them dividends were increased by less than 10% and in 242 by more than 10%. In 35

15

of the firm-years there was an initial dividend omission, while in 78 firms continued not to

pay dividends after an initial omission. In 32 years companies resumed dividend payments

(all companies enter the sample beginning with a dividend payment).

The central year in each group is denoted year 0. The previous five years are years -4

to -1, and the following three years are 1 to 3. Dividends are assigned to year t if they are

declared in that particular year (and paid from the net income of year t− 1). The earnings

figures are those reported for the year. Market values for year t are those at the end of the

year.

This section examines the connection between changes in (split-adjusted) dividends per

share and changes in (split-adjusted) earnings per share. The change in dividends in com-

puted as

∆D0/1 =D0 −D−1

D−1,

where D0 are dividends announced in year 0 and D−1 are dividends announced in year -1.

The ”past” growth in earnings is expressed as

Ratio−2/−1 =E−1

E−2,

where E−2 are earnings per share for year -2 and E−1 are earnings per share for year -1.

Therefore it is the change in earnings between the year to which dividend announced in year

0 ”belong” and the previous year. A higher value of the ratio means that earnings were

lower in the year -2 compared to the year -1 - or that dividends are paid from earnings that

were higher than in the previous year. ”Current” earnings growth is computed as

Ratio−1/0 =E−1

E0,

therefore a value below 1 means that earnings in the year dividends were announced were

higher than in the previous year.

”Future” earnings changes are given by

Ratio1/0 =E1

E0.

Years 0 when the number of shares for a company changed by more than 20% have been

excluded from the sample. While some of these years represent mere share splits, others

can reflect mergers, capital reductions and other major events in the life of the company.

Changing the sample to include these observations does not significantly alter results.

This approach has the advantage that dividend omissions and resumed payments can be

treated to some extent in the same framework as as dividend cuts and increases. The main

disadvantage is that years with losses cannot be included in the sample. The connection

between losses and dividend changes is examined in the following subsection.

Observations are grouped according to the sign and size of the change in dividends be-

tween year -1 and year 0. Years with initial dividend omissions, with no dividend payments

following a previous year when there were also no dividends, with resumed dividend pay-

ments and with dividend decreases each form a group. Dividend increases - a more numerous

category - are analysed both by each quintile according to the size of the increase and as a

group. Earnings ratios for each subsample are then compared to a benchmark group that

had no dividend changes in year 0. Both mean and median tests are used in order to get a

clearer picture and minimise the effect of outliers. Earnings ratios are also compared to one

- the null hypothesis being in this case that earnings were flat between the two years.

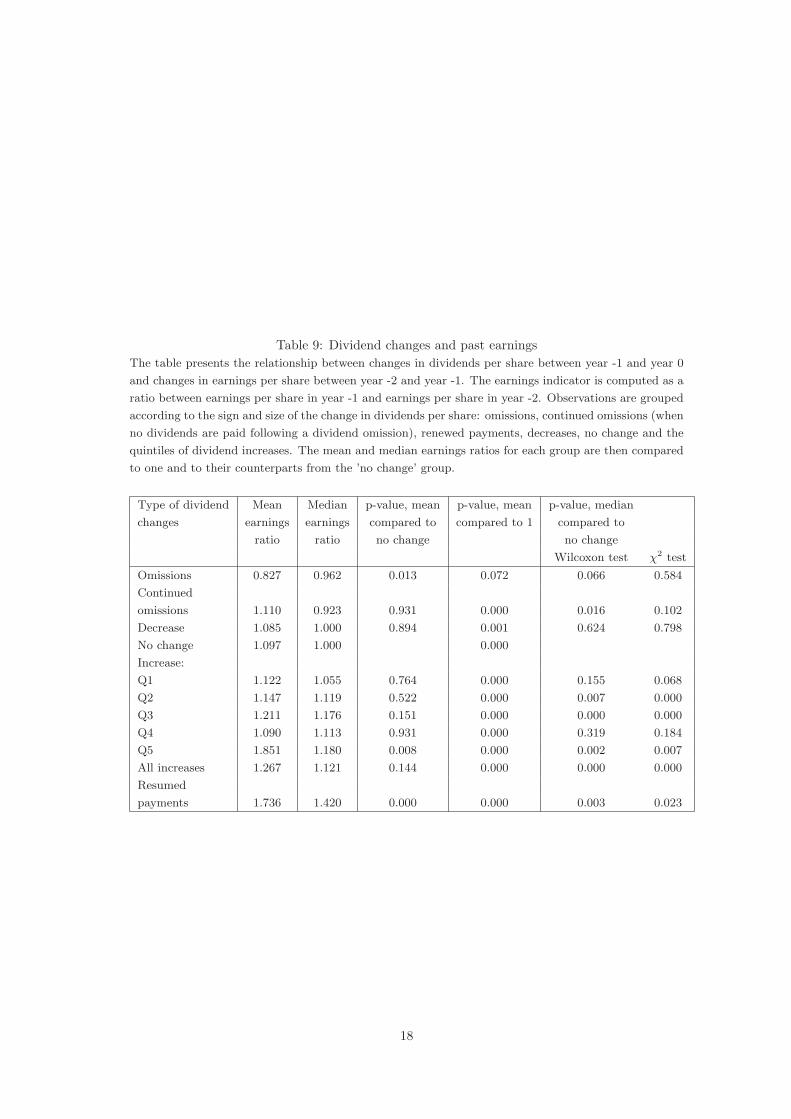

Table 9 presents results for earnings growth between years -2 and -1. Companies that

omitted dividends in year 0 were the only ones that experienced significant past earnings

16

decreases. Companies that increased dividends had a higher earnings increase than those

that made no changes - median tests suggest that the difference is significant, but mean

tests are not as decisive, perhaps as a result of outliers. Companies that started paying

dividends again in year 0 had the highest earnings increase over the previous period. (The

mean and median earnings ratio were higher for companies that started paying dividends

again compared to companies that merely increased them, and the difference is significant

for the medians). The means and medians for the different quintiles of dividend increases

suggest a higher increase in dividends is related to a higher increase in earnings, although

the relationship is far from strong. For dividend decreases, the situation is not very clear,

with the median tests suggesting earnings stayed flat and the mean test suggesting a slight,

but significant increase. Overall one can say that companies that increased dividends or

resumed payments in year 0 had experienced large past earnings increases, while companies

that omitted them experienced significant decreases. In these respects there seems to be a

strong link between past earnings growth and dividends.

Table 10 examines the relationship between dividend changes declared in year 0 and

earnings changes between year -1 and year 0 (the connection between dividend changes

and current earnings). Except for mean of the first quintile of dividend increases and re-

sumed payments, results are significant or close to significance. Companies that decide to

omit dividends in year 0 experience much lower earnings for that year (a higher number

means a larger decrease in earnings from year -1 to year 0). Earnings are also decreasing,

although not by the same proportion, for companies that cut dividends. Significance tests

suggest that this time there is a large difference between the ”decrease” and the ”no change”

group. Companies that increase dividends have significantly higher earnings in year 0. For

companies that resume dividend payments, one might expect significant earnings increases,

but this is not the case. It seems that when companies decide to restart paying dividends

earnings have already increased over the previous years. Companies that continue not to

pay dividends actually experience the highest earnings increase. Indeed, several empirical

studies (including Benartzi, Michaely and Thaler (1997) and Grullon, Michaely and Thaler

(2003)) suggest that there are high earnings growth rates after a dividend omission as the

company recovers following the crisis.

The picture becomes less clear-cut as soon as we move on to changes in earnings for the

following year. Table 11 presents the results for future earnings changes. While companies

that resumed payments continue to experience earnings increases, this growth is not signif-

icantly different from that of companies that did not change their dividends. For dividend

increasers as a group there is some weak evidence for faster growth, while earnings for div-

idend decreasers remain largely flat. The results for dividend omissions do not allow any

definite conclusion.

Benartzi, Michaely and Thaler (1997) also examine the relationship between past, current

and future earnings growth and dividend changes and conclude that, while the connection

with contemporaneous earnings is strong, dividend changes have little to say about future

earnings changes. Indeed, they emphasize that the only strong connection appears to be

that between dividend cuts and higher earnings growth. As an additional result, they find

that earnings are less likely to fall during the first year after a dividend increase (results are

less significant for the second year).

For comparison, results based on the measures in Benartzi et al. are presented in the

appendix (tables 19 to 22). The indicator is the ratio between net earnings before extraordi-

nary items and preference dividends and the market value of the company at the end of year

-1. Given that US firms pay dividends on a quarterly basis, Benartzi et al. compute annual

dividends as four times the last quarterly dividend in each year. The Swiss sample uses the

17

Table 9: Dividend changes and past earningsThe table presents the relationship between changes in dividends per share between year -1 and year 0

and changes in earnings per share between year -2 and year -1. The earnings indicator is computed as a

ratio between earnings per share in year -1 and earnings per share in year -2. Observations are grouped

according to the sign and size of the change in dividends per share: omissions, continued omissions (when

no dividends are paid following a dividend omission), renewed payments, decreases, no change and the

quintiles of dividend increases. The mean and median earnings ratios for each group are then compared

to one and to their counterparts from the ’no change’ group.

Type of dividend Mean Median p-value, mean p-value, mean p-value, median

changes earnings earnings compared to compared to 1 compared to

ratio ratio no change no change

Wilcoxon test χ2 test

Omissions 0.827 0.962 0.013 0.072 0.066 0.584

Continued

omissions 1.110 0.923 0.931 0.000 0.016 0.102

Decrease 1.085 1.000 0.894 0.001 0.624 0.798

No change 1.097 1.000 0.000

Increase:

Q1 1.122 1.055 0.764 0.000 0.155 0.068

Q2 1.147 1.119 0.522 0.000 0.007 0.000

Q3 1.211 1.176 0.151 0.000 0.000 0.000

Q4 1.090 1.113 0.931 0.000 0.319 0.184

Q5 1.851 1.180 0.008 0.000 0.002 0.007

All increases 1.267 1.121 0.144 0.000 0.000 0.000

Resumed

payments 1.736 1.420 0.000 0.000 0.003 0.023

18

Table 10: Dividend changes and current earningsThe table presents the relationship between changes in dividends per share between year -1 and year

0 and changes in earnings per share over the same period. The earnings indicator is computed as a

ratio between earnings per share in year -1 and earnings per share in year 0. Observations are grouped

according to the sign and size of the change in dividends per share: omissions, continued omissions (when

no dividends are paid following a dividend omission), renewed payments, decreases, no change and the

quintiles of dividend increases. The mean and median earnings ratios for each group are then compared

to one and to their counterparts from the ’no change’ group.

Type of dividend Mean Median p-value, mean p-value, mean p-value, median

changes earnings earnings compared to compared to 1 compared to

ratio ratio no change no change

Wilcoxon test χ2 test

Omissions 2.786 1.369 0.000 0.000 0.066 0.015

Continued

omissions 0.765 0.689 0.003 0.099 0.000 0.020

Decrease 1.699 1.202 0.000 0.001 0.005 0.000

No change 0.987 1.000 0.248

Increase:

Q1 1.000 0.970 0.760 0.000 0.939 0.262

Q2 0.903 0.901 0.029 0.000 0.005 0.000

Q3 0.920 0.901 0.137 0.000 0.000 0.000

Q4 0.851 0.850 0.001 0.000 0.000 0.000

Q5 0.920 0.807 0.195 0.000 0.000 0.000

All increases 0.920 0.867 0.024 0.000 0.000 0.000

Resumed

payments 1.453 0.886 0.025 0.000 0.313 0.827

19

Table 11: Dividend changes and future earningsThe table presents the relationship between changes in dividends per share between year -1 and year 0

and changes in earnings per share over the following period. The earnings indicator is computed as a

ratio between earnings per share in year 1 and earnings per share in year 0. Observations are grouped

according to the sign and size of the change in dividends per share: omissions, continued omissions (when

no dividends are paid following a dividend omission), renewed payments, decreases, no change and the

quintiles of dividend increases. The mean and median earnings ratios for each group are then compared

to one and to their counterparts from the ’no change’ group.

Type of dividend Mean Median p-value, mean p-value, mean p-value, median

changes earnings earnings compared to compared to 1 compared to

ratio ratio no change no change

Wilcoxon test χ2 test

Omissions 1.255 0.940 0.615 0.072 0.084 0.047

Continued

omissions 1.350 1.936 0.065 0.000 0.322 0.881

Decrease 1.059 1.000 0.440 0.103 0.092 0.106

No change 1.2547 1.021 0.000

Increase:

Q1 1.141 1.1219 0.642 0.000 0.068 0.067

Q2 1.0589 1.100 0.422 0.000 0.553 0.020

Q3 1.093 1.055 0.513 0.000 0.713 0.651

Q4 1.057 1.106 0.433 0.000 0.698 0.337

Q5 1.080 1.0814 0.480 0.000 0.588 0.211

All increases 1.074 1.087 0.085 0.000 0.499 0.061

Resumed

payments 1.114 1.168 0.693 0.000 0.453 0.537

20

simple annual dividend. As a result, the relationship between earnings and ”past” dividends

for the Swiss sample is close to that shown for year 0 in the Benartzi et al. paper. In the

Swiss case, the change in dividends is that between dividends announced at the beginning

of year -1 and those announced at the beginning of year 0, while the change in earnings

is between years -2 and -1. For the US case, the change in dividends is between dividends

announced at the end of year -1 and dividends announced at the end of year 0, while the

change in earnings is between year -1 and year 0.

The relationship between ”past” earnings growth and dividend changes is similar to that

in the paper based on US data, albeit slightly weaker. The relationship between dividend

changes and earnings growth rates over the following two years are insignificant in both

cases.

Mean earnings over a longer period an also be used to get a broader picture. Table

12 in the appendix presents the situation for mean past earnings over the previous five

years compared to earnings in year 0, while table 13 presents the corresponding situation

for earnings over the following three years. Companies that increase dividends have had

significant earnings growth compared to past values, while companies that omitted them

experienced significant decreases. Earnings are flat for dividend decreasers. As for future

earnings, the mean tests suggest that earnings increase for all groups, but none of them have

changes that are significantly different from the ”no change” group. It is just the median

tests that suggest that earnings growth was lower for the companies that omitted dividends.

One can also examine the connection between dividends and earnings growth using

regression analysis. Table 14 presents results using the variables in Benartzi et al. (1997).

Earnings changes for current and future periods are regressed on the size of the dividend

change. Just like in the study using US data, there is a weakly significant connection only

for the first year.

Table 15 presents the results using the ratios of earnings per share. For current changes

coefficients are significant, but the explanatory power is very low. For future changes coef-

ficients are insignificant and the signs are wrong. For past changes, the signs are right, but

the coefficients are insignificant and the explanatory power of the equation is very low.

Therefore, if categorical analysis shows weak results for the connection between dividend

changes and current and future earnings growth, the situation is even worse for regression

analysis. One of the reason may be that, as Lintner suggested, managers do not fully adjust

dividends to changes in earnings. Since the variability of earnings is obviously higher than

that of dividends, this will result in a low explanatory power for dividend changes. One

could also note that the significant relationships are the ”past” one using income before

extraordinary income and the ”current” one using the final net income. The reason for this

difference might be the earnings smoothing across periods, as suggested for instance by the

model of Fudenberg and Tirole (1995).

So far it seems that dividend changes ”signal” past or current rather than future earnings

growth rates. Thus the role of dividends as signals for future profitability seems open to

doubt. An alternative hypothesis is that dividend changes signal permanent (or persistent)

shifts in earnings. Lintner (1956) suggests that managers are reluctant to increase dividends

if the earnings increase is temporary. The model of Fudenberg and Tirole (1995) suggests

that managers smooth earnings and dividends in order to avoid negative reports that can

jeopardise their position. Therefore managers will only cut dividends if the company’s

position is really bad. Benartzi et al. (1997) actually find that dividend-increasing companies

are less likely to experience dividend decreases over the next two years than companies that

made no changes in their payout.

21

Table 12: Dividend changes and mean past earningsThe table presents the relationship between changes in dividends per share between year 0 and year 1

and changes in earnings per share over the previous years. The earnings indicator is computed as a ratio

between the mean earnings per share over years -4 to -1 and earnings per share in year 0. Observations

are grouped according to the sign and size of the change in dividends per share: omissions, continued

omissions (when no dividends are paid following a dividend omission), renewed payments, decreases, no

change and the quintiles of dividend increases. The mean and median earnings ratios for each group are

then compared to one and to their counterparts from the ’no change’ group.

Type of dividend Mean Median p-value, mean p-value, mean p-value, median

changes earnings earnings compared to compared to 1 compared to

ratio ratio no change no change

Wilcoxon test χ2 test

Omissions 3.101 1.102 0.000 0.000 0.138 0.493

Continued

omissions 2.365 0.826 0.000 0.000 0.951 0.478

Decrease 1.157 1.003 0.451 0.000 0.573 0.444

No change 0.964 0.916 0.101

Increase

Q1 0.854 0.855 0.124 0.000 0.165 0.134

Q2 0.742 0.754 0.002 0.000 0.000 0.000

Q3 0.747 0.698 0.004 0.000 0.000 0.000

Q4 0.736 0.712 0.002 0.000 0.000 0.000

Q5 0.736 0.657 0.004 0.000 0.000 0.000

All increases 0.771 0.743 0.000 0.000 0.000 0.000

Resumed

payments 1.172 0.565 0.306 0.080 0.130 0.008

22

Table 13: Dividend changes and mean future earningsThe table presents the relationship between changes in dividends per share between year 0 and year 1

and changes in earnings per share over the following years. The earnings indicator is computed as a ratio

between the mean earnings per share over years 1 to 3 and earnings per share in year 0. Observations

are grouped according to the sign and size of the change in dividends per share: omissions, continued

omissions (when no dividends are paid following a dividend omission), renewed payments, decreases, no

change and the quintiles of dividend increases. The mean and median earnings ratios for each group are

then compared to one and to their counterparts from the ’no change’ group.

Type of dividend Mean Median p-value, mean p-value, mean p-value, median

changes earnings earnings compared to compared to 1 compared to

ratio ratio no change no change

Wilcoxon test χ2 test

Omissions 1.370 0.891 0.824 0.000 0.084 0.047

Continued

omissions 2.948 1.195 0.001 0.000 0.144 0.297

Decrease 1.157 1.003 0.451 0.000 0.573 0.444

No change 1.300 1.101 0.000 0.000

Increase

Q1 1.202 1.145 0.589 0.000 0.505 0.526

Q2 1.082 1.103 0.228 0.000 0.853 0.880

Q3 1.187 1.095 0.554 0.000 0.773 0.651

Q4 1.226 1.109 0.707 0.000 0.916 0.732

Q5 1.167 1.091 0.485 0.000 0.523 0.788

All increases 1.149 1.095 0.097 0.000 0.665 0.626

Resumed

payments 1.294 1.317 0.982 0.000 0.130 0.150

23

Table 14: Dividend changes and earnings growthThe dependent variable is the change in earnings normalised by the market value of the company

at the end of year -1. The difference is between years -1 and -2 for past growth, years 0 and -1

for current growth and years 1 and 0 for future growth. The change in dividends is computed as

(DPS0−DPS−1)/DPS−1, where DPSt are (split-adjusted) dividends per share. I is a dummy variable

that takes the value 1 for dividend decreases. The numbers in brackets are the p-values. As in Benartzi

et al. (1997), observations with studentized residuals above 2 have been eliminated from the sample.

Variables Past growth Current growth Future growth

Intercept -0.026 0.029 0.018

(0.000) (0.005) (0.094)

Dividend change 0.006 0.008 -0.005

(0.015) (0.148) (0.229)

I∗ div. change 33.856 0.048 -0.006

(0.271) (0.140) (0.856)

D2 0.030 -0.023 -0.016

(0.000) (0.051) (0.265)

D3 0.037 -0.022 -0.025

(0.000) (0.053) (0.078)

D4 0.046 -0.032 -0.012

(0.000) (0.006) (0.409)

D5 0.083 -0.035 -0.021

(0.000) (0.018) (0.149)

Adjusted R2 0.197 0.026 -0.001

Table 15: Dividend changes and changes in earnings per share

Variables Past change Current change Future changeIntercept 1.085 1.083 1.031 0.989 1.137 1.144

(0.000) (0.000) (0.000) (0.000) (0.000) (0.000)Dividend change 0.010 0.011 -0.068 -0.033 -0.026 -0.032

(0.443) (0.393) (0.019) (0.061) (0.278) (0.217)I∗ Div. change -0.035 -1.048 0.178

(0.724) (0.015) (0.509)Adjusted R2 -0.001 -0.002 0.007 0.049 -0.001 -0.003

24

Table 16: Dividend changes and mean past and future earningsThe table presents the relationship between changes in dividends per share between year 0 and year 1

and changes in earnings per share over the surrounding years. The earnings indicator is computed as a

ratio between the mean earnings per share over years 1 to 3 and earnings per share in years -5 to -1.

Observations are grouped according to the sign and size of the change in dividends per share: omissions,

continued omissions (when no dividends are paid following a dividend omission), renewed payments,

decreases, no change and the quintiles of dividend increases. The mean and median earnings ratios for

each group are then compared to one and to their counterparts from the ’no change’ group.

Type of dividend Mean Median p-value, mean p-value, mean p-value, median

changes earnings earnings compared to compared to 1 compared to

ratio ratio no change no change

Wilcoxon test χ2 test

Omissions 1.040 0.678 0.107 0.338 0.016 0.280

Continued

omissions 3.552 1.386 0.001 0.000 0.206 0.094

Decrease 1.013 0.992 0.009 0.631 0.006 0.172

No change 0.964 1.180 0.000

Increase:

Q1 1.483 1.291 0.682 0.000 0.165 0.072

Q2 1.587 0.754 0.288 0.000 0.000 0.000

Q3 1.609 1.516 0.206 0.000 0.001 0.000

Q4 1.743 1.506 0.058 0.000 0.008 0.005

Q5 1.897 1.613 0.006 0.000 0.002 0.008

All increases 1.636 1.435 0.020 0.000 0.000 0.000

Resumed

payments 2.727 2.192 0.000 0.080 0.007 0.061

p-value, mean p-value, median

Wilcoxon test χ2 test

Increases vs. decreases 0.000 0.000 0.000

Resumed payments vs. increases 0.000 0.097 0.157

Table 16 presents the results for the comparison between average earnings for the previous

five years (years -4 to -1) and the following three years (years 1 to 3). The picture seems

quite clear and it lends support Lintner’s claims. Dividend increases are associated with

higher average earnings over the following years. The mean values actually increase from one

quintile to the next, suggesting a correspondence between the size of the dividend increase

and the size of the increase in future earnings. Companies that resume dividend payments

are likely to experience even higher future earnings when compared to the previous years.

The median tests also suggest that dividend decreases and omissions are associated with a

shift to lower earnings levels.

To sum up, it seems that there is some evidence suggesting that the good news dividends

signal is connected with the shift to a higher level of earnings rather than with an increase

in the earnings’ growth rate. The higher growth seems to have taken place in years -1 and 0,

and perhaps the good news brought by the The correlations between dividend changes and

the ratio in mean earnings levels (which exclude dividend omissions and renewed payments)

are significant at 5% (the Pearson correlation) and 1% (the Spearman rank correlation)

25

Table 17: Dividend payments over successive years

First year Next year PercentageDividend omissions: 35 No payment:25 71%

Resumed payments: 10 29%No payments No payment: 57 73%following omissions:78 Resumed payments: 21 27%Resumed payments: 32 No change: 11 34.4%

Dividend increases: 18 56.3%Dividend omissions: 3 9.3%

Dividend decreases: 56 Dividend decreases: 9 16.1%No change: 17 30.4%Dividend increases: 24 42.9%Dividend omissions: 6 10.6%

No change: 202 Dividend cuts:13 6.4%No change: 88 43.6%Dividend increases: 83 41.1%Omissions: 18 8.9%

Dividend increases: 383 Dividend cuts: 37 10.9%No change: 76 22.5%Dividend increases: 208 61.6%Dividend omissions: 17 5%

significance levels.

The appendix presents some robustness tests for the result. Taking just three previous

years instead of five does not significantly alter results (Table 23). Using the difference be-

tween mean net earnings before extraordinary items over the same two periods (normalized

by the market value at the end of year -1) also supports the idea of a sustainable shift in

earnings (Table 24).

A casual look at the data shows that there is some evidence that dividend move slowly

over time, as a result of smoothing or gradual adjustment to ”sustainable” levels. Table

17 presents the observations for year 1 and the dividend changes over the following year.

Dividend increases are most likely to be followed by other increases, and the same is true

for years when dividend payments are resumed. It can be seen from the table that dividend

omissions are likely to extend over several years - this happens in spite of significant im-

provements in earnings, as shown in Table 16.

This subsection has confirmed that there is little connection between dividend changes

and future earnings growth rates. Past earnings growth seems to determine dividend changes

and not the other way round. It seems more likely that dividend changes signal that earn-

ings will move to a new level at least over the medium term. While the higher growth

seems to have taken place before or around the dividend increase, dividends could signal

that earnings will stay at a higher level over the next period. This finding is in agreement

with the intuition in Lintner (1956) and Grullon, Michaely and Swaminathan (2002). To

some extent, it also supports the basic idea of signalling models.

26

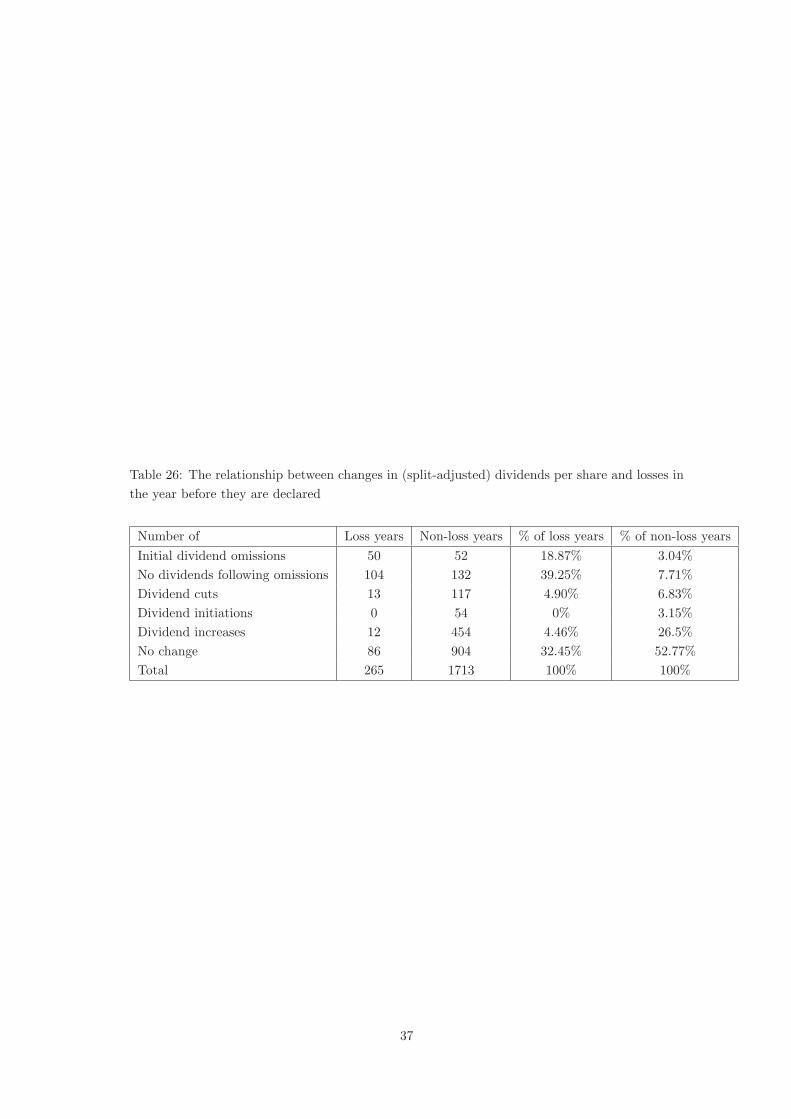

6.3. Dividends and losses

The previous section dealt with the relationship between earnings and dividends in years

with positive earnings. This section looks at dividend payments around loss years. Earnings

are measured by ”net income available to common shares” from Datastream.

DeAngelo, DeAngelo and Skinner (1992) find that ”an annual loss is essentially a nec-

essary condition for dividend reductions” for firms with an established history as dividend

payers. They find that dividend cuts and omissions are extremely rare for companies with

positive earnings, while half of loss-making companies cut dividends and 15% of them omit

payments. This can be considered a proof that companies are reluctant to cut dividends,

as suggested for instance by the model of Fudenberg and Tirole. DeAngelo and DeAngelo

(1990) find that companies in financial distress seem reluctant to cut dividends, the most

likely explanation being agency problems between shareholders and debtholders.

Tables 25 and 26 in the appendix present the link between losses and dividend changes

in the case of Swiss companies. The tables include information for all the firm-years with

valid data on dividends and earnings over the 1974-2003 period.

Empirical studies have shown that dividend cuts and omissions are much fewer than

dividend increases. This can be taken as a sign of the managers’ reluctance to cut dividends:

dividends are only increased gradually in order to avoid unfavourable revisions, while cuts

are usually abrupt. This asymmetry is confirmed by the large sample presented here as well

as the smaller one in the previous section.

As suggested by previous research, loss years are much more likely to be associated with

dividend cuts and omissions. Some empirical studies have also suggested that dividends pre-

fer dividend cuts to dividend omissions, since the latter have a more negative interpretation.

DeAngelo et al. (1992) have 108 dividend cuts and 26 omissions out of 2531 firm-years. For

the Swiss sample, the proportion between cuts and omissions is more balanced. As seen in

the previous section, companies tend not to pay dividends for several years after a dividend

omission. The data also show that this happens even if the following years have positive

earnings (the result is also confirmed by the analysis in the previous section).

DeAngelo et al. also show that losses help explain dividend reductions over and above

current profitability or the change in earnings from the previous period. Table 18 presents

the results for the Swiss sample. Observations included in the sample follow at least three

years of positive dividend payments. Earnings are normalized by book value (as in DeAngelo

et al.) and by total assets. The results are quite similar to those in the paper based on

US data. The loss dummy brings additional information even when current and previous

earnings are taken into consideration. One may think that in loss years the additional

negative effect of bad news concerning dividends is smaller.

27

Table 18: Logit regressions for dividend reductionsThe table presents several factors affecting the decision to reduce dividends. The dependent variable is

a binary variable equal to 1 for years with losses and 0 otherwise. NI is net income, BV is the book

value, and TA is total assets.

Variables Coefficients (p-values)

Intercept -1.937 -1.665 -1.433 -1.109

(0.000) (0.000) (0.000) (0.000)

Loss dummy 1.570 1.098

(0.000) (0.045)

NI/BV -0.069 -0.101

(0.173) (0.099)

∆NI/BV 0.0472 0.064

(0.218) (0.197)

NI/TA -13.095 -17.619

(0.003) (0.000)

∆NI/TA 10.014 9.825

(0.006) (0.007)

Pseudo-R2 0.07 0.02 0.10 0.08

P-value, likelihood

ratio test 0.0001 0.043 2.7 ∗ 10−6 3.9 ∗ 10−6

7 Conclusions