Divergent Monetary Policy –Implication for sub-Saharan ... · PDF fileImpact Divergent...

23

By Sarah O. Alade Deputy Governor, Economic Policy Central Bank of Nigeria Divergent Monetary Policy –Implication for sub-Saharan African Economies

Transcript of Divergent Monetary Policy –Implication for sub-Saharan ... · PDF fileImpact Divergent...

By Sarah O. Alade

Deputy Governor, Economic Policy Central Bank of Nigeria

Divergent Monetary Policy –Implication for sub-Saharan African Economies

Crisis background………

The recent financial crisis is one of the most significant macroeconomic crisis in recent times

Many countries suffered low investment rate, high unemployment rate and collapse of the financial market

Financial markets not only triggered the crisis, but played a role in transmission of shock to the real economy

Collapse on financial institutions, sharp decline on several assets, lack of credit, and loss of confidence in the financial system were all indicators of the grave situation

Crisis background………

The 2008 crisis caused huge recession and outpaced conventional monetary policy response

With the exceptional economic conditions, Central Banks took unconventional measures to promote investment and production in advanced economies

The massive expansionary monetary policy in industrialized countries had global effects and international spillovers that caused emerging markets economies to change their monetary and economic policy

Crisis background…..

The US and UK adopted some assets buying and bond purchasing measures to resuscitate their economies

This had implications for emerging market economies in the areas of capital inflows, bond yield, assets prices and exchange rate volatility.

The near zero interest rate in advanced economies gave rise to capital flows into emerging markets and SSA benefited from the inflows.

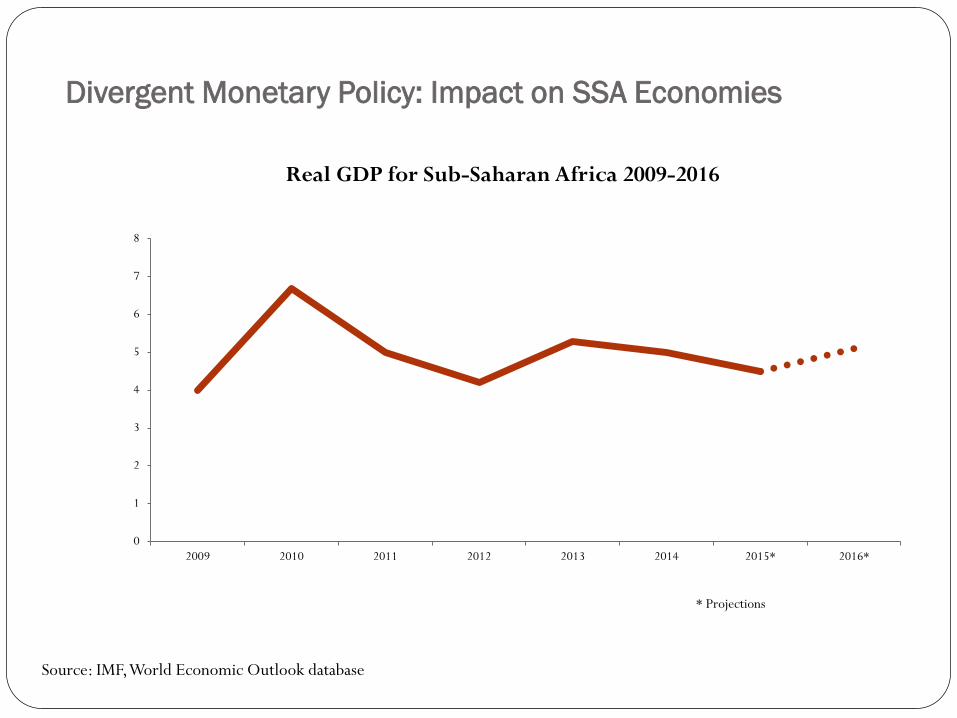

Divergent Monetary Policy: Impact on SSA Economies

While advanced economies experienced low growth, economies of emerging markets witnessed sustained growth as high interest rate attracted inflows from advanced economies

Quantitative Easing policies of the US FED and EU countries resulted in an unprecedented increase in monetary base, lower interest rates and flattened yield curve

With cheap and new capital flows into the SSA economies, many countries became highly exposed to external shocks.

Divergent Monetary Policy: Impact on SSA Economies

0

1

2

3

4

5

6

7

8

2009 2010 2011 2012 2013 2014 2015* 2016*

Real GDP for Sub-Saharan Africa 2009-2016

* Projections

Source: IMF, World Economic Outlook database

Sub-Saharan Africa: Real GDP Growth, 2004–15

0

2

4

6

8

Average 2004–08

2009 Average 2010–14

2015

Perce

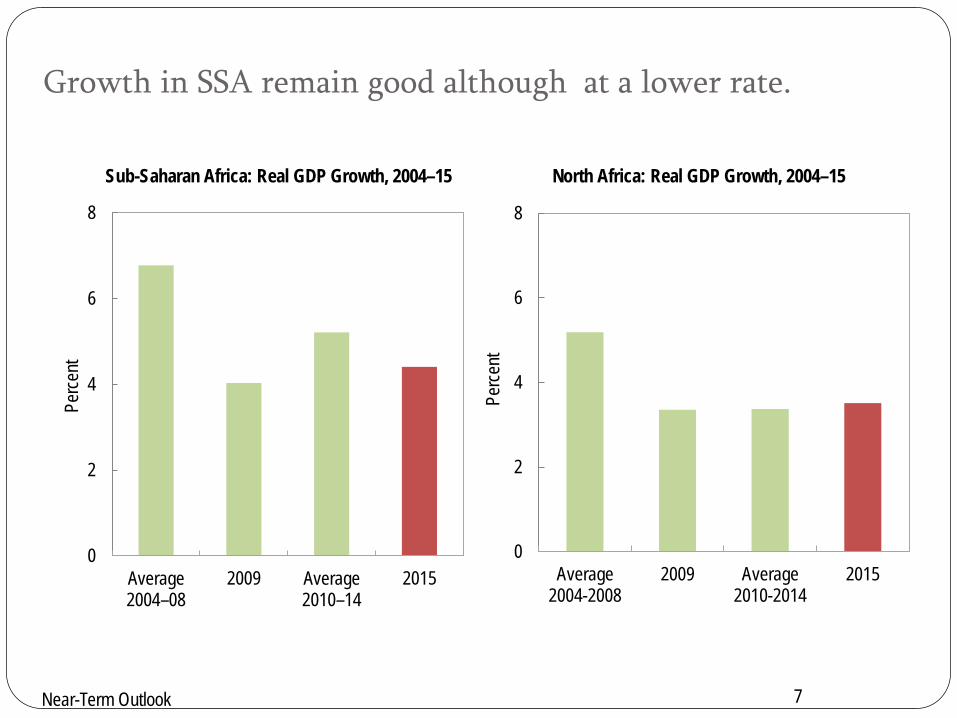

nt Growth in SSA remain good although at a lower rate.

Near-Term Outlook 7

North Africa: Real GDP Growth, 2004–15

0

2

4

6

8

Average2004-2008

2009 Average2010-2014

2015

Perce

nt

Near-Term Outlook 8

-5

0

5

10

15

20

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

Perce

nt

China

United States

Europe

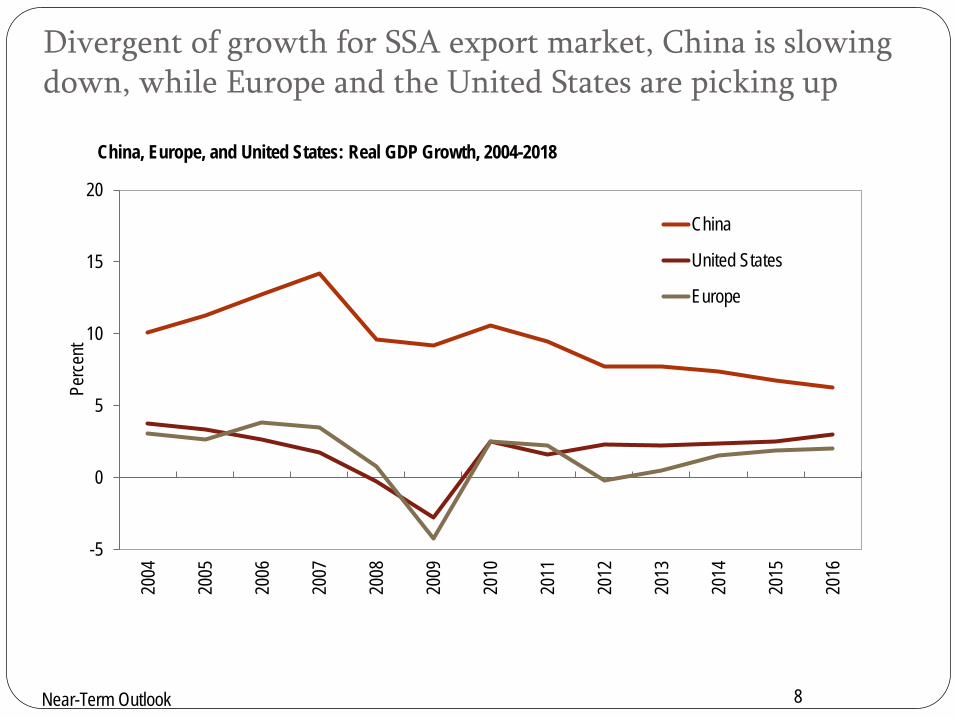

China, Europe, and United States: Real GDP Growth, 2004-2018

Divergent of growth for SSA export market, China is slowing down, while Europe and the United States are picking up

Divergent Monetary policy – Impact on SSA Economies

Quantitative Easing also promoted trading in the financial markets and some Sub-Saharan Africa countries raised huge amount of money from the international debt market taking advantage of the near zero interest rate.

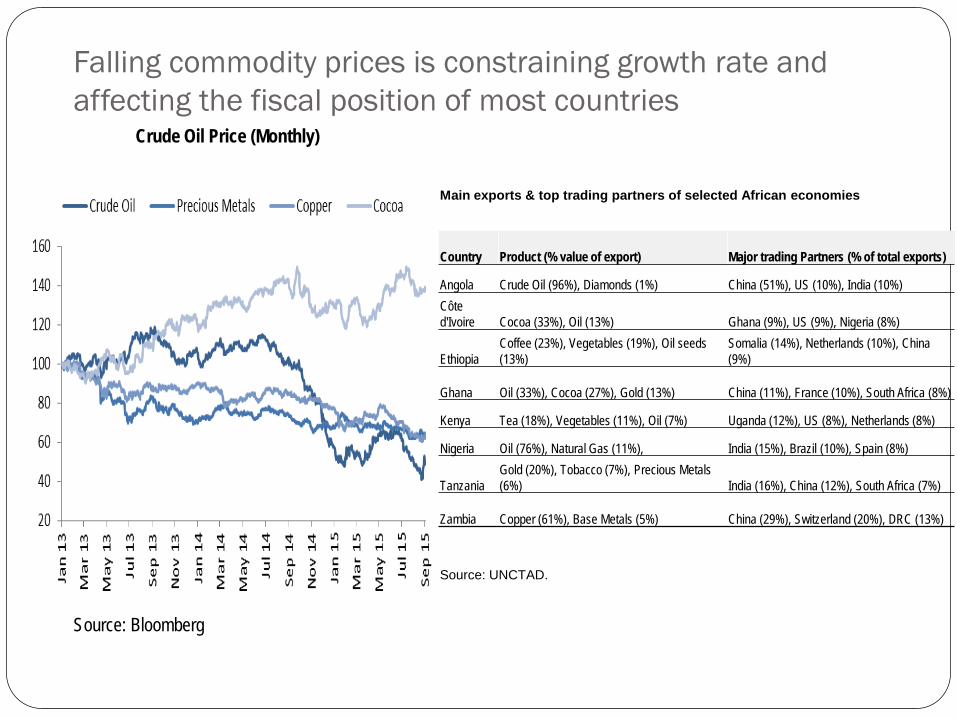

However, the drop in commodity prices is putting many SSA economies in a challenging position

Most SSA African countries are commodity exporters and low commodity prices will effect the external position and financing in these countries

Falling commodity prices is constraining growth rate and affecting the fiscal position of most countries

Source: Bloomberg

Crude Oil Price (Monthly)

Main exports & top trading partners of selected African economies

Country Product (% value of export) Major trading Partners (% of total exports)

Angola Crude Oil (96%), Diamonds (1%) China (51%), US (10%), India (10%) Côte d'Ivoire Cocoa (33%), Oil (13%) Ghana (9%), US (9%), Nigeria (8%)

Ethiopia Coffee (23%), Vegetables (19%), Oil seeds (13%)

Somalia (14%), Netherlands (10%), China (9%)

Ghana Oil (33%), Cocoa (27%), Gold (13%) China (11%), France (10%), South Africa (8%)

Kenya Tea (18%), Vegetables (11%), Oil (7%) Uganda (12%), US (8%), Netherlands (8%)

Nigeria Oil (76%), Natural Gas (11%), India (15%), Brazil (10%), Spain (8%)

Tanzania Gold (20%), Tobacco (7%), Precious Metals (6%) India (16%), China (12%), South Africa (7%)

Zambia Copper (61%), Base Metals (5%) China (29%), Switzerland (20%), DRC (13%)

Source: UNCTAD.

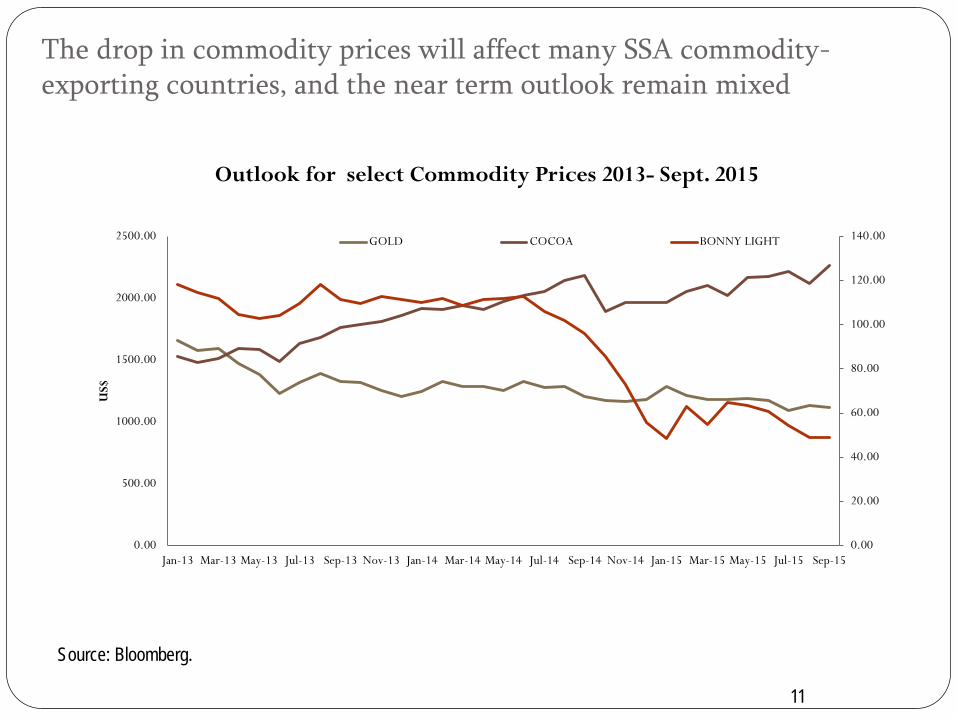

Source: Bloomberg.

The drop in commodity prices will affect many SSA commodity-exporting countries, and the near term outlook remain mixed

11

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

0.00

500.00

1000.00

1500.00

2000.00

2500.00

Jan-13 Mar-13 May-13 Jul-13 Sep-13 Nov-13 Jan-14 Mar-14 May-14 Jul-14 Sep-14 Nov-14 Jan-15 Mar-15 May-15 Jul-15 Sep-15

US$

Outlook for select Commodity Prices 2013- Sept. 2015

GOLD COCOA BONNY LIGHT

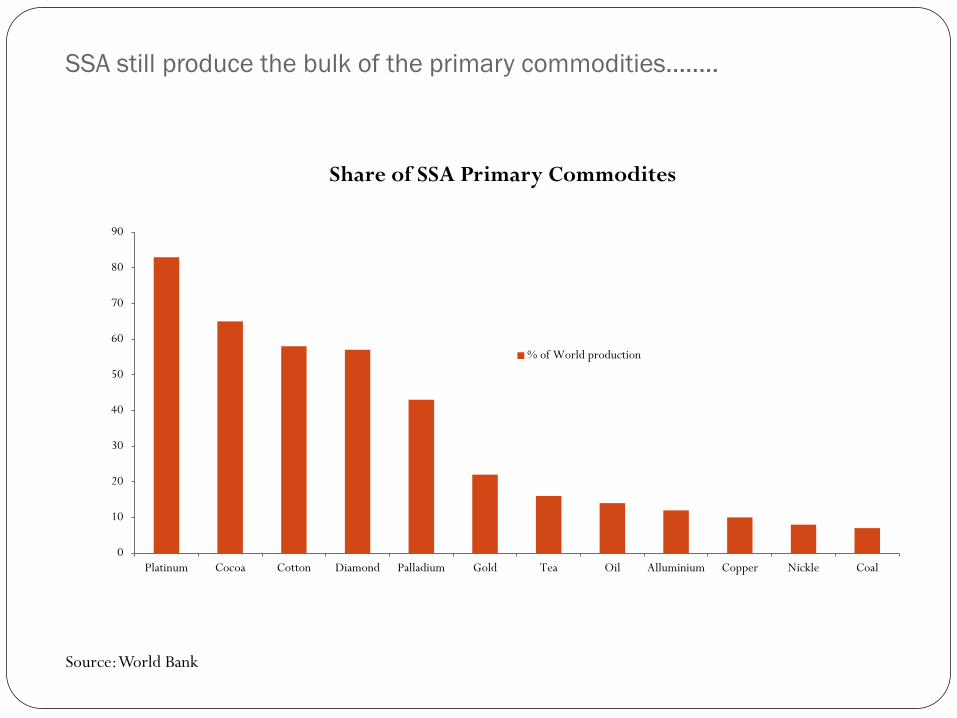

SSA still produce the bulk of the primary commodities……..

0

10

20

30

40

50

60

70

80

90

Platinum Cocoa Cotton Diamond Palladium Gold Tea Oil Alluminium Copper Nickle Coal

Share of SSA Primary Commodites

% of World production

Source: World Bank

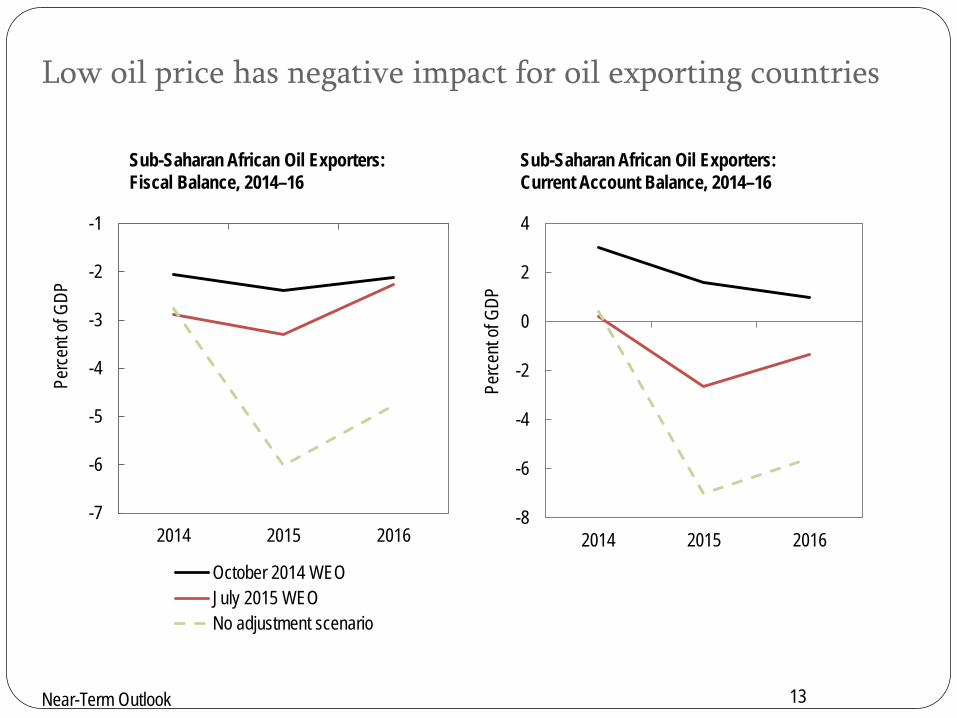

Sub-Saharan African Oil Exporters: Fiscal Balance, 2014–16

Sub-Saharan African Oil Exporters: Current Account Balance, 2014–16

Low oil price has negative impact for oil exporting countries

Near-Term Outlook

-7

-6

-5

-4

-3

-2

-1

2014 2015 2016

Perce

nt of

GDP

October 2014 WEOJuly 2015 WEONo adjustment scenario

-8

-6

-4

-2

0

2

4

2014 2015 2016

Perce

nt of

GDP

13

2008

2014 2015

2008

2014

2015

2008 2014

2015

2008 2014

2015

2008

2014 2015

-15

-10

-5

0

5

10

-6 -4 -2 0 2 4 6

Curre

nt ac

coun

t bala

nce (

perce

nt of

GDP)

Fiscal balance (percent of GDP)

Sub-Saharan AfricaOil exportersMiddle-income countriesLow-income countriesFragile states

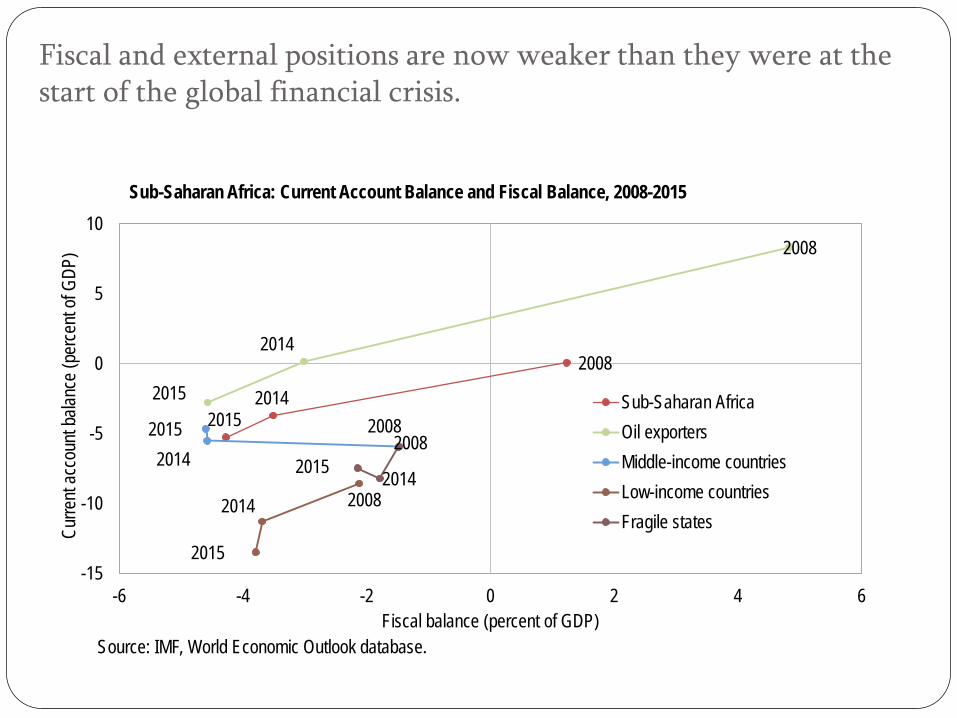

Source: IMF, World Economic Outlook database.

Sub-Saharan Africa: Current Account Balance and Fiscal Balance, 2008-2015

Fiscal and external positions are now weaker than they were at the start of the global financial crisis.

Near-Term Outlook

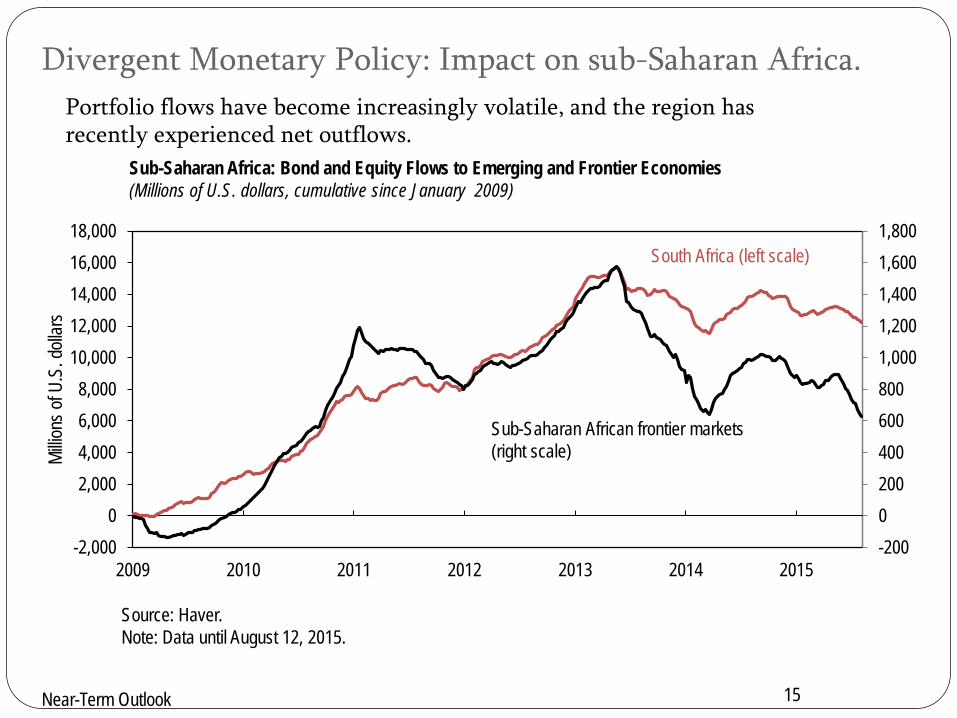

Divergent Monetary Policy: Impact on sub-Saharan Africa.

15

Sub-Saharan Africa: Bond and Equity Flows to Emerging and Frontier Economies (Millions of U.S. dollars, cumulative since January 2009)

-20002004006008001,0001,2001,4001,6001,800

2009 2010 2011 2012 2013 2014 2015-2,000

02,0004,0006,0008,000

10,00012,00014,00016,00018,000

Millio

ns of

U.S

. doll

ars

Sub-Saharan African frontier markets (right scale)

South Africa (left scale)

Source: Haver. Note: Data until August 12, 2015.

Portfolio flows have become increasingly volatile, and the region has recently experienced net outflows.

Near-Term Outlook

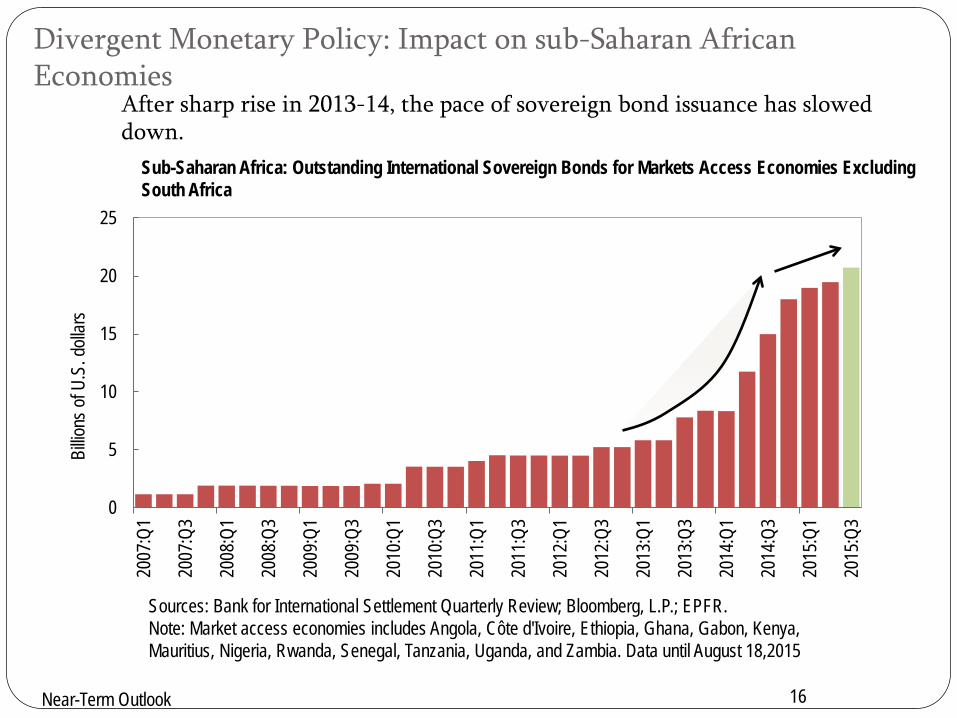

Divergent Monetary Policy: Impact on sub-Saharan African Economies

Sub-Saharan Africa: Outstanding International Sovereign Bonds for Markets Access Economies Excluding South Africa

Sources: Bank for International Settlement Quarterly Review; Bloomberg, L.P.; EPFR. Note: Market access economies includes Angola, Côte d'Ivoire, Ethiopia, Ghana, Gabon, Kenya, Mauritius, Nigeria, Rwanda, Senegal, Tanzania, Uganda, and Zambia. Data until August 18,2015

0

5

10

15

20

25

2007

:Q1

2007

:Q3

2008

:Q1

2008

:Q3

2009

:Q1

2009

:Q3

2010

:Q1

2010

:Q3

2011

:Q1

2011

:Q3

2012

:Q1

2012

:Q3

2013

:Q1

2013

:Q3

2014

:Q1

2014

:Q3

2015

:Q1

2015

:Q3

Billio

ns of

U.S

. doll

ars

16

After sharp rise in 2013-14, the pace of sovereign bond issuance has slowed down.

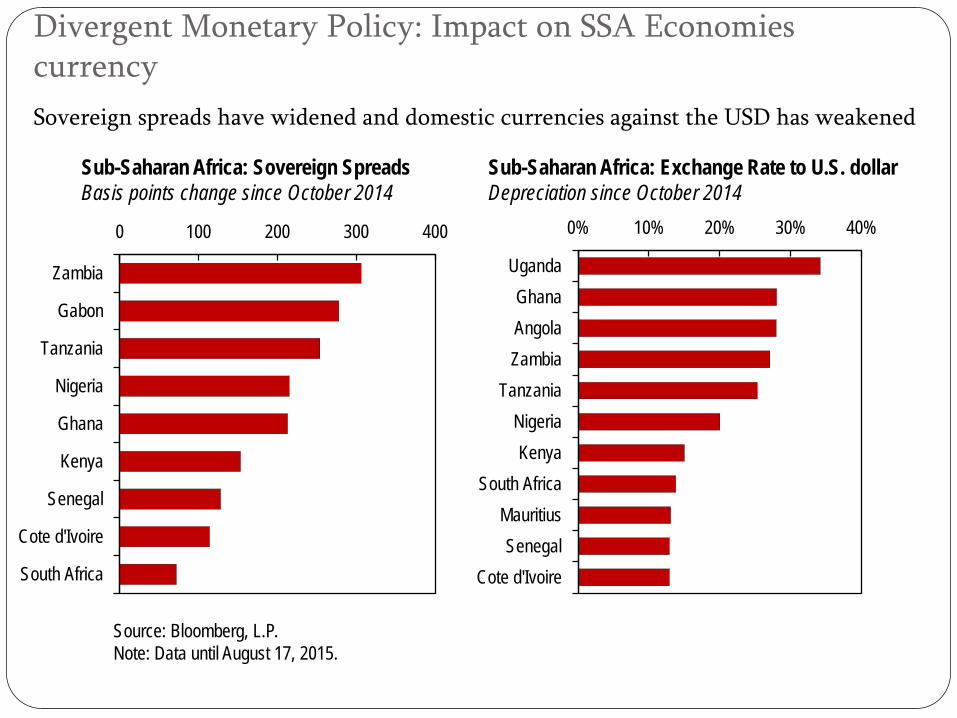

Sub-Saharan Africa: Sovereign Spreads Basis points change since October 2014

Sub-Saharan Africa: Exchange Rate to U.S. dollar Depreciation since October 2014

Divergent Monetary Policy: Impact on SSA Economies currency

Source: Bloomberg, L.P. Note: Data until August 17, 2015.

0 100 200 300 400

Zambia

Gabon

Tanzania

Nigeria

Ghana

Kenya

Senegal

Cote d'Ivoire

South Africa

0% 10% 20% 30% 40%

UgandaGhanaAngolaZambia

TanzaniaNigeriaKenya

South AfricaMauritiusSenegal

Cote d'Ivoire

Sovereign spreads have widened and domestic currencies against the USD has weakened

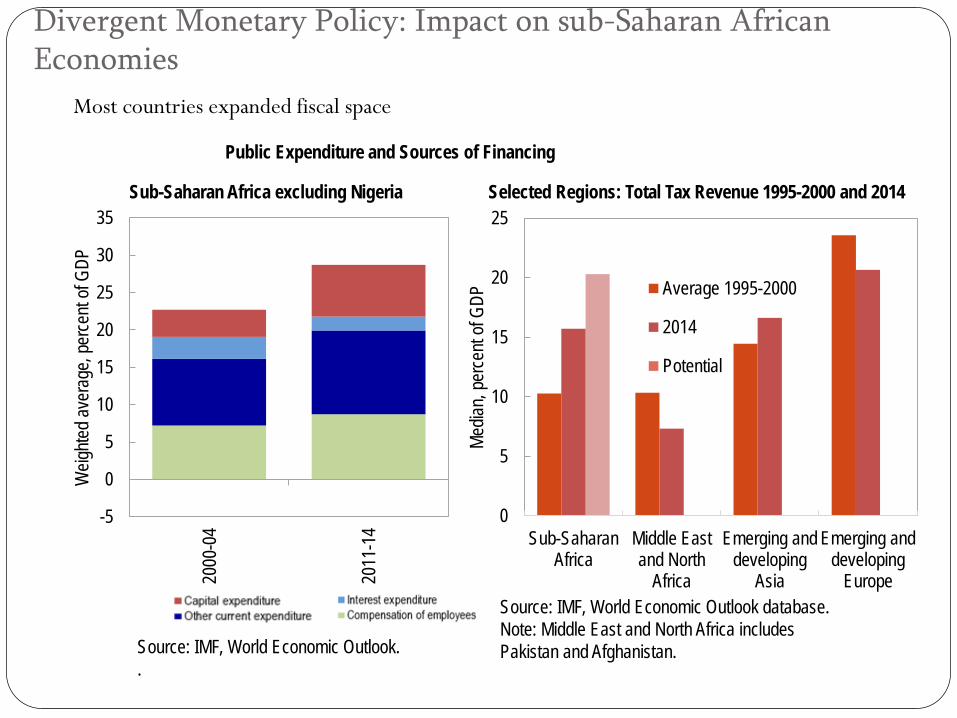

Sub-Saharan Africa excluding Nigeria

Source: IMF, World Economic Outlook. .

Public Expenditure and Sources of Financing

Divergent Monetary Policy: Impact on sub-Saharan African Economies

-5

0

5

10

15

20

25

30

3520

00-0

4

2011

-14

Weig

hted a

vera

ge, p

erce

nt of

GDP

Selected Regions: Total Tax Revenue 1995-2000 and 2014

0

5

10

15

20

25

Sub-SaharanAfrica

Middle Eastand North

Africa

Emerging anddeveloping

Asia

Emerging anddeveloping

Europe

Media

n, pe

rcent

of GD

P Average 1995-2000

2014

Potential

Source: IMF, World Economic Outlook database. Note: Middle East and North Africa includes Pakistan and Afghanistan.

Most countries expanded fiscal space

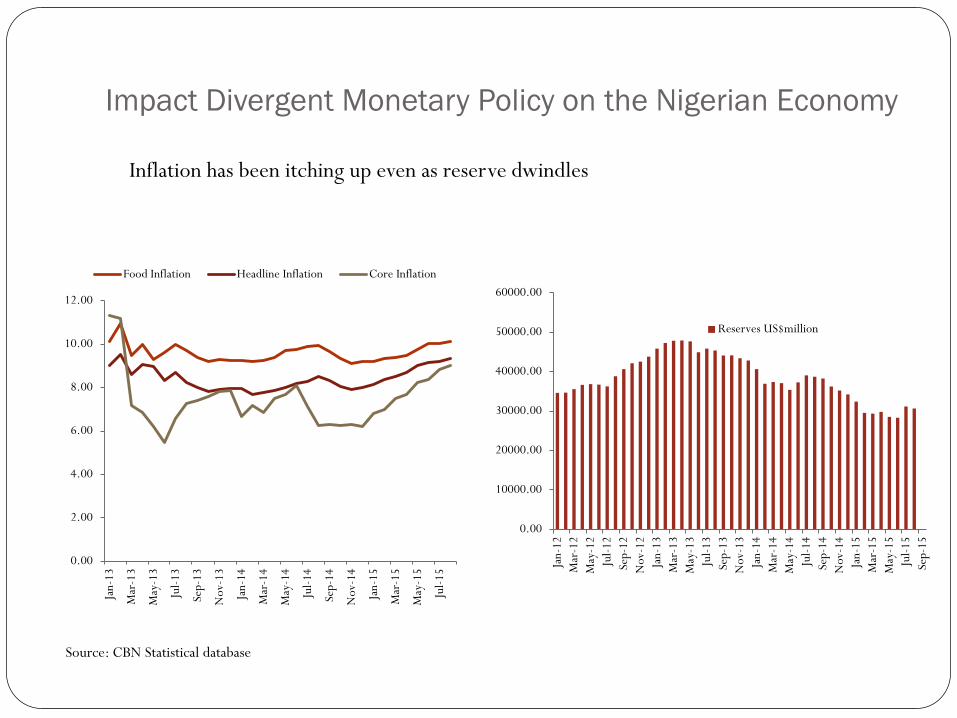

Impact Divergent Monetary Policy on the Nigerian Economy

Source: CBN Statistical database

Inflation has been itching up even as reserve dwindles

0.00

10000.00

20000.00

30000.00

40000.00

50000.00

60000.00

Jan-

12M

ar-1

2M

ay-1

2Ju

l-12

Sep-

12N

ov-1

2Ja

n-13

Mar

-13

May

-13

Jul-1

3Se

p-13

Nov

-13

Jan-

14M

ar-1

4M

ay-1

4Ju

l-14

Sep-

14N

ov-1

4Ja

n-15

Mar

-15

May

-15

Jul-1

5Se

p-15

Reserves US$million

0.00

2.00

4.00

6.00

8.00

10.00

12.00

Jan-

13

Mar

-13

May

-13

Jul-1

3

Sep-

13

Nov

-13

Jan-

14

Mar

-14

May

-14

Jul-1

4

Sep-

14

Nov

-14

Jan-

15

Mar

-15

May

-15

Jul-1

5

Food Inflation Headline Inflation Core Inflation

Divergent Monetary Policy: Near-term Outlook for sub-Saharan African Countries The recovery in advanced economies like US, UK and Euro zone areas

will be sustained

The European Central Bank has taken many steps to increase the degree of policy accommodation, including an expansion of its bond-buying program

The Bank of Japan has continued with very accommodative monetary policies, including a 0 % interest rate and purchases of Japanese government bonds and other assets.

The slow down in the Chinese economy despite liquidity injection will have a spillover effect on SSA economies especially in terms of commodity prices

Divergent Monetary Policy: Near Term Outlook for sub-Saharan Africa

The anticipated rate hike has been priced in, and would not have much of an economic impact on the region.

Risk to the regional outlook will be more effected by slow down in growth on China, increased production of shale oil in the USA, and geopolitical tension in the middle East (Iran deal, Libyan peace deal etc.)

Further decline in oil price could exacerbate upside risks to exchange rate on many countries and result in dislocations and inflationary pressures

Anticipated rate hike could foster another round of offshore positioning. Foreign investors may unwind fixed income and/or equity holding resulting in upward pressure on the domestic currency. This coupled with lower buffers from low commodity prices would put downward pressure on the domestic currency

Minimal impact of FED rate hike expected for the region in the short term

Divergent Monetary Policy: Near term Outlook for sub-Saharan Africa

Many SSA countries are better prepared now than at the start of the crisis due to hard lessons learned and some reforms implemented, although more needs to be done in some countries to strengthen institutional structures. Some of the reforms include

Fuel subsidy reform, Tax measures, including increasing tax rates, and Greater exchange rate flexibility, where feasible

Domestic fundamentals are more likely to be the most important determinants of how SSA economies financial conditions respond to FED normalization policy

Therefore, it is important that SSA economies continue to build strong system institution and strengthen financial system stability to be better prepared for the further FED actions.

Divergent Monetary Policy: Concluding Remarks

As global markets anticipate rate hike by the FED, it is important that its global implication is considered and forward guidance given.

Policy decisions should not be isolated, but most be consultative, gradual and predictable to avoid negative feedback effects for the US economy and the global economy.

Emerging market economies have sustained global growth during the crisis, and policies coordination is essential to avoid dislocation and strengthen financial system stability

Emerging markets should be prepared to manage capital flow volatility, build fiscal buffer and safeguard its financial system to weather the storm

Market during the taper tantrum of Spring 2013 underscores the importance of transparency and effective communication by the FED on the timing and magnitude of the normalization