Ditech (I-32) Jumbo AA Fixed Rate - American Financial...

25

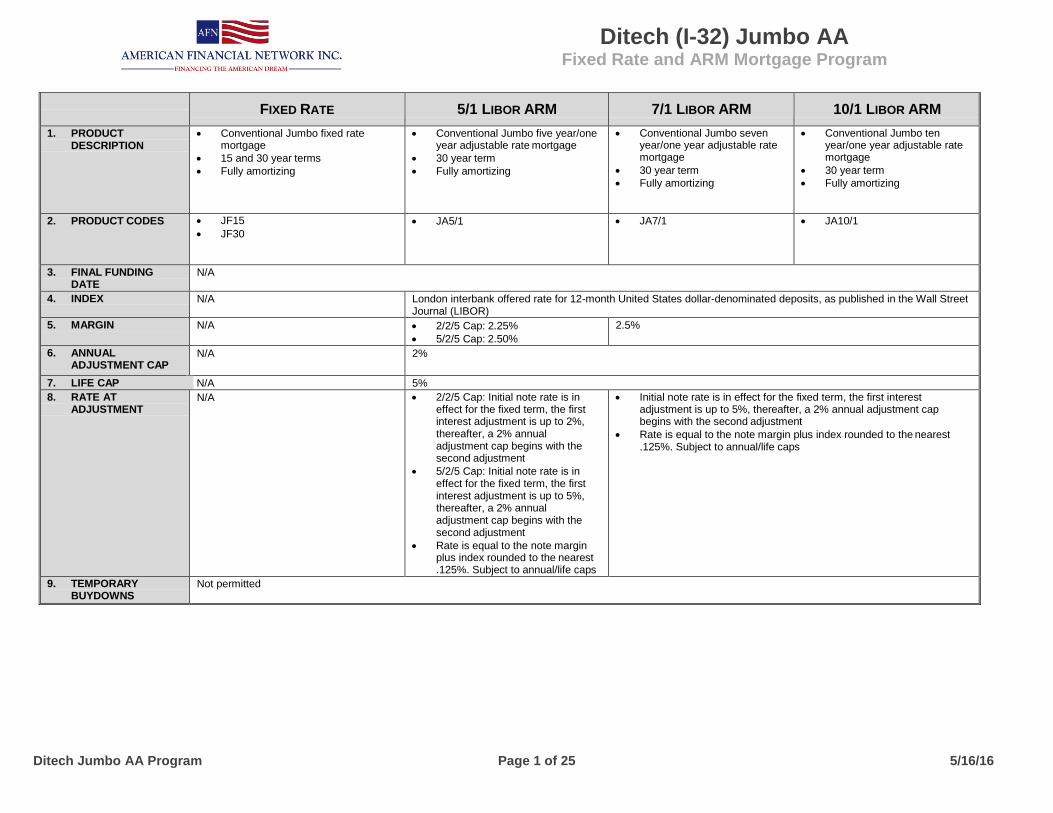

Ditech (I-32) Jumbo AA Fixed Rate and ARM Mortgage Program Ditech Jumbo AA Program Page 1 of 25 5/16/16 FIXED RATE 5/1 LIBOR ARM 7/1 LIBOR ARM 10/1 LIBOR ARM 1. PRODUCT DESCRIPTION Conventional Jumbo fixed rate mortgage 15 and 30 year terms Fully amortizing Conventional Jumbo five year/one year adjustable rate mortgage 30 year term Fully amortizing Conventional Jumbo seven year/one year adjustable rate mortgage 30 year term Fully amortizing Conventional Jumbo ten year/one year adjustable rate mortgage 30 year term Fully amortizing 2. PRODUCT CODES JF15 JF30 JA5/1 JA7/1 JA10/1 3. FINAL FUNDING DATE N/A 4. INDEX N/A London interbank offered rate for 12-month United States dollar-denominated deposits, as published in the Wall Street Journal (LIBOR) 5. MARGIN N/A 2/2/5 Cap: 2.25% 5/2/5 Cap: 2.50% 2.5% 6. ANNUAL ADJUSTMENT CAP N/A 2% 7. LIFE CAP N/A 5% 8. RATE AT ADJUSTMENT N/A 2/2/5 Cap: Initial note rate is in effect for the fixed term, the first interest adjustment is up to 2%, thereafter, a 2% annual adjustment cap begins with the second adjustment 5/2/5 Cap: Initial note rate is in effect for the fixed term, the first interest adjustment is up to 5%, thereafter, a 2% annual adjustment cap begins with the second adjustment Rate is equal to the note margin plus index rounded to the nearest .125%. Subject to annual/life caps Initial note rate is in effect for the fixed term, the first interest adjustment is up to 5%, thereafter, a 2% annual adjustment cap begins with the second adjustment Rate is equal to the note margin plus index rounded to the nearest .125%. Subject to annual/life caps 9. TEMPORARY BUYDOWNS Not permitted

Transcript of Ditech (I-32) Jumbo AA Fixed Rate - American Financial...

Ditech (I-32) Jumbo AA Fixed Rate and ARM Mortgage Program

Ditech Jumbo AA Program Page 1 of 25 5/16/16

FIXED RATE 5/1 LIBOR ARM 7/1 LIBOR ARM 10/1 LIBOR ARM

1. PRODUCT DESCRIPTION

Conventional Jumbo fixed rate mortgage

15 and 30 year terms

Fully amortizing

Conventional Jumbo five year/one year adjustable rate mortgage

30 year term

Fully amortizing

Conventional Jumbo seven year/one year adjustable rate mortgage

30 year term

Fully amortizing

Conventional Jumbo ten year/one year adjustable rate mortgage

30 year term

Fully amortizing

2. PRODUCT CODES JF15

JF30

JA5/1 JA7/1 JA10/1

3. FINAL FUNDING DATE

N/A

4. INDEX N/A London interbank offered rate for 12-month United States dollar-denominated deposits, as published in the Wall Street Journal (LIBOR)

5. MARGIN N/A 2/2/5 Cap: 2.25%

5/2/5 Cap: 2.50%

2.5%

6. ANNUAL ADJUSTMENT CAP

N/A 2%

7. LIFE CAP N/A 5%

8. RATE AT ADJUSTMENT

N/A 2/2/5 Cap: Initial note rate is in effect for the fixed term, the first interest adjustment is up to 2%, thereafter, a 2% annual adjustment cap begins with the second adjustment

5/2/5 Cap: Initial note rate is in effect for the fixed term, the first interest adjustment is up to 5%, thereafter, a 2% annual adjustment cap begins with the second adjustment

Rate is equal to the note margin plus index rounded to the nearest .125%. Subject to annual/life caps

Initial note rate is in effect for the fixed term, the first interest adjustment is up to 5%, thereafter, a 2% annual adjustment cap begins with the second adjustment

Rate is equal to the note margin plus index rounded to the nearest .125%. Subject to annual/life caps

9. TEMPORARY BUYDOWNS

Not permitted

Ditech (I-32) Jumbo AA Fixed Rate and ARM Mortgage Program

Ditech Jumbo AA Program Page 2 of 25 5/16/16

FIXED RATE 5/1 LIBOR ARM 7/1 LIBOR ARM 10/1 LIBOR ARM

10. QUALIFYING RATE AND RATIOS

Qualifying Rate

Qualify using note rate

Ratios

See LTV/CLTV Limitations section

Qualifying Rate

2/2/5 Cap: Qualify using greater of note rate plus 2% or fully indexed rate

5/2/5 Cap: Qualify using greater of note rate plus 5% or fully indexed rate

Ratios

See LTV/CLTV Limitations section

Qualifying Rate

Qualify using greater of note rate or fully indexed rate

Ratios

See LTV/CLTV Limitations section

11. TYPES OF FINANCING

Purchase Mortgage

Non-arm’s length transactions are permitted with family members. See the Jumbo chapter of the Client Guide for specific requirements

Rate & Term Refinance

Refinancing a first lien that was previously a cash out refinance requires the loan to be seasoned for 12 months as of the application date

If existing mortgage was a purchase transaction, the note date of the existing loan must be at least 120 days from to the note date of the new loan

If the existing mortgage was a rate/term refinance transaction, no seasoning requirements

Buy-out of co-owner –see the Jumbo chapter Client Guide for complete requirements

Continuity of Obligation - see the Jumbo chapter of the Client Guide

Loan amount may include

Paying off the outstanding principal balance of

Existing first loan, plus any required per diem interest

Pay off of the outstanding principal balance of any existing subordinate liens that were used in whole to acquire the subject property or existing subordinate lien with at least 12 month seasoning (from date of application). Draws on HELOC within the last 12 months (from date of application) may not exceed $2,000. HELOC must be paid off and closed.

Closing costs and prepaids

Prepayment penalty associated with the existing mortgage

Cash-out limited to the lesser of $2,000 or 2% of the principal amount of the new loan

Principal curtailments are not permitted

Delinquent real estate taxes and/or HOA dues may not be included in the loan amount. See the Jumbo chapter of the Client Guide for complete requirements.

Properties currently listed for sale are not eligible

Properties previously listed for sale must have been off the market and the listing agreement canceled at least one day prior to date of application

Intent to occupy letter required for primary residences

Owner occupied properties located in Texas subject to Texas Section 50(a)(6) are not permitted

No cash out is permitted

A copy of the current mortgage or note is required to determine the previous terms are not subject to Texas Section 50(a)(6) (also known as Home Equity Deed of Trust, Home Equity Installment Contract or Residential Home Loan Deed of Trust)

If the first or second Texas Section 50(a)(6) loan is being paid off, regardless of whether the borrower is getting any cash back, the loan is not eligible

If the first mortgage is not a Texas Section 50(a)(6) loan and the second mortgage is a Texas Section 50(a)(6) loan, the second lien may be subordinated and is considered a rate & term refinance. The second lien must be subordinate to the ditech first mortgage. Borrower cannot receive any cash back from the first mortgage transaction.

Ditech (I-32) Jumbo AA Fixed Rate and ARM Mortgage Program

Ditech Jumbo AA Program Page 3 of 25 5/16/16

FIXED RATE 5/1 LIBOR ARM 7/1 LIBOR ARM 10/1 LIBOR ARM

Cash-Out Refinance

At least one borrower must have held title to subject property for at least 6 months, measured from date vested on title to note date, with the following exceptions

Delayed Financing

See Jumbo chapter of the Client Guide for details

If owned less than 12 months, LTV must be based on lower of appraised value or original sales price plus the cost of any documented improvements.

If owned more than 12 months, LTV is based on the current appraised value. HUD-1 or deed must be provided to verify ownership

Payoff of junior liens opened less than 12 months prior to loan application must be included in cash out limitations

Payoff of junior liens opened 12 or months prior to loan application may be excluded from cash out limitations

If draws on HELOC within the last 12 months (from date of application) exceeds $2,000, seasoning is based on the date of last draw

Continuity of Obligation - see the Jumbo chapter of the Client Guide

Delayed Financing – must be treated as a cash out refinance transaction

Properties currently listed for sale are not eligible

Properties previously listed for sale must have been off the market and the listing agreement canceled at least one day prior to date of application

Max 70% LTV for properties listed for sale in the 6 months prior to application date

Owner occupied properties located in Texas subject to Texas Section 50(a)(6) are not permitted

A copy of the current mortgage or note is required to determine the previous terms are not subject to Texas Section 50(a)(6) (also known as Home Equity Deed of Trust, Home Equity Installment Contract or Residential Home Loan Deed of Trust)

If the first or second Texas Section 50(a)(6) loan is being paid off, regardless of whether the borrower is getting any cash back, the loan is not eligible

12. MINIMUM LOAN AMOUNT

Minimum loan amount is $1 higher than Fannie Mae/Freddie Mac high balance county loan limits

Refer to the Loan Limit Look up Table for eligibility in specific MSAs for county loan limits. High-Balance Loan Amounts

Ditech (I-32) Jumbo AA Fixed Rate and ARM Mortgage Program

Ditech Jumbo AA Program Page 4 of 25 5/16/16

FIXED RATE 5/1 LIBOR ARM 7/1 LIBOR ARM 10/1 LIBOR ARM

13. LTV/CLTV LIMITATIONS

PRIMARY RESIDENCE

Units Loan Amount LTV/CLTV Credit Score DTI Ratio

Purchase and Rate & Term Refinance

1

$1,500,0002 80% 700 43%

$1,500,0002 65% 680 40%

$2,000,000 70% 720 43%

$2,500,000 70% 720 40%

2 $1,500,000

2 80% 700 43%

$1,500,0002 65% 680 40%

3 - 4 $1,000,000

2 80% 700 43%

$1,000,0002 65% 680 40%

Cash Out Refinance1

1

$1,000,0002 75% 700

40%

$1,500,0002 70% 700

$2,000,000 50% 720

2 $1,000,000

2 75% 700

$1,500,0002 70% 700

3 - 4 $1,000,0002 75% 700

Delayed Financing

1-4 $1,000,0002 50% 700 40%

1Maximum cash out $325,000 (includes debts paid off with loan proceeds)

2Reduce LTV/CLTV by 5% in AZ, FL and NV

Ditech (I-32) Jumbo AA Fixed Rate and ARM Mortgage Program

Ditech Jumbo AA Program Page 5 of 25 5/16/16

FIXED RATE 5/1 LIBOR ARM 7/1 LIBOR ARM 10/1 LIBOR ARM

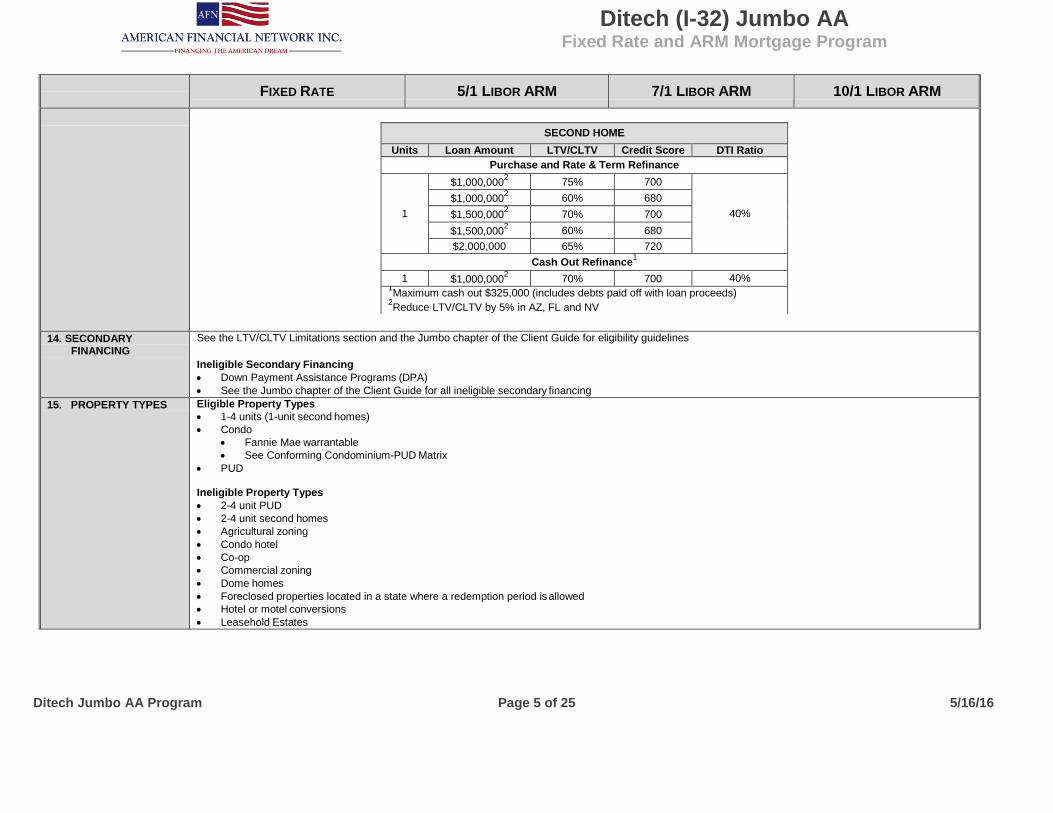

SECOND HOME

Units Loan Amount LTV/CLTV Credit Score DTI Ratio

Purchase and Rate & Term Refinance

1

$1,000,0002 75% 700

40%

$1,000,0002 60% 680

$1,500,0002 70% 700

$1,500,0002 60% 680

$2,000,000 65% 720

Cash Out Refinance1

1 $1,000,0002 70% 700 40%

1Maximum cash out $325,000 (includes debts paid off with loan proceeds)

2Reduce LTV/CLTV by 5% in AZ, FL and NV

14. SECONDARY FINANCING

See the LTV/CLTV Limitations section and the Jumbo chapter of the Client Guide for eligibility guidelines

Ineligible Secondary Financing

Down Payment Assistance Programs (DPA)

See the Jumbo chapter of the Client Guide for all ineligible secondary financing

15. PROPERTY TYPES Eligible Property Types

1-4 units (1-unit second homes)

Condo

Fannie Mae warrantable

See Conforming Condominium-PUD Matrix

PUD

Ineligible Property Types

2-4 unit PUD

2-4 unit second homes

Agricultural zoning

Condo hotel

Co-op

Commercial zoning

Dome homes

Foreclosed properties located in a state where a redemption period is allowed

Hotel or motel conversions

Leasehold Estates

Ditech (I-32) Jumbo AA Fixed Rate and ARM Mortgage Program

Ditech Jumbo AA Program Page 6 of 25 5/16/16

FIXED RATE 5/1 LIBOR ARM 7/1 LIBOR ARM 10/1 LIBOR ARM

Manufactured/mobile homes

Mixed-use property

Modular/Pre-Cut/Panelized homes

Non-warrantable condo projects

Property with deed/resale restrictions (except age restricted communities)

Property with more than 20 acres

Properties sold at auction (including previously approved condo or PUD units)

Unique Properties (such as earth homes, log homes, etc.)

Working farms, ranch, orchard, regardless of amount of income or loss received from property

See the Jumbo chapter of the Client Guide for complete eligibility guidelines and ineligible property types

16. OCCUPANCY Primary Residence

Second Homes

17. GEOGRAPHIC LOCATIONS/ RESTRICTIONS

Ineligible States

New York

Permitted only for Delegated Clients who underwrite and close loans in their own name. See Approval Authority section for limited eligibility

West Virginia

18. STATE SPECIFIC REQUIREMENTS

The State Requirements are located in the Compliance Section, Chapter 2 of the Client Guide.

19. ASSUMPTIONS Not permitted Permitted only after the initial note rate ends and in accordance with the Due on Sale and Assumption qualifications. Creditworthy borrowers only.

20. ESCROW WAIVERS See the Client Guide for escrow waiver eligibility

21. PREPAYMENT PENALTY

None

Ditech (I-32) Jumbo AA Fixed Rate and ARM Mortgage Program

Ditech Jumbo AA Program Page 7 of 25 5/16/16

FIXED RATE 5/1 LIBOR ARM 7/1 LIBOR ARM 10/1 LIBOR ARM

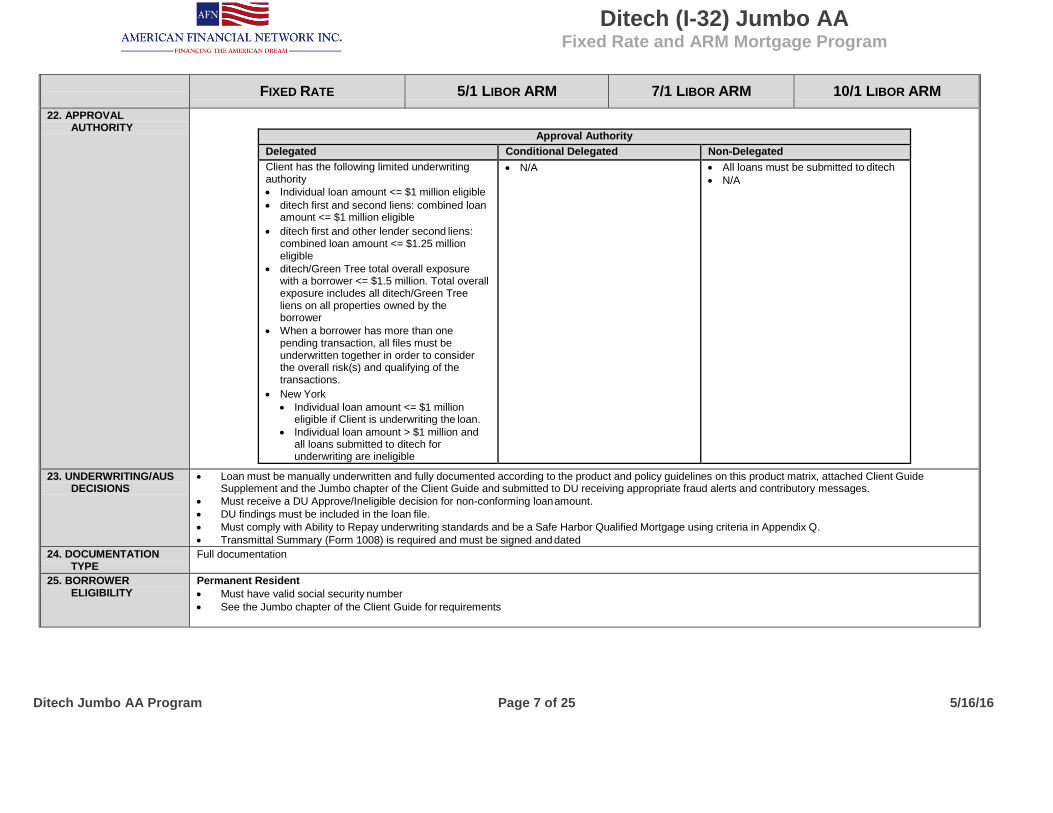

22. APPROVAL AUTHORITY

Approval Authority

Delegated Conditional Delegated Non-Delegated

Client has the following limited underwriting authority

Individual loan amount <= $1 million eligible

ditech first and second liens: combined loan amount <= $1 million eligible

ditech first and other lender second liens: combined loan amount <= $1.25 million eligible

ditech/Green Tree total overall exposure with a borrower <= $1.5 million. Total overall exposure includes all ditech/Green Tree liens on all properties owned by the borrower

When a borrower has more than one pending transaction, all files must be underwritten together in order to consider the overall risk(s) and qualifying of the transactions.

New York

Individual loan amount <= $1 million eligible if Client is underwriting the loan.

Individual loan amount > $1 million and all loans submitted to ditech for underwriting are ineligible

N/A All loans must be submitted to ditech

N/A

23. UNDERWRITING/AUS DECISIONS

Loan must be manually underwritten and fully documented according to the product and policy guidelines on this product matrix, attached Client Guide Supplement and the Jumbo chapter of the Client Guide and submitted to DU receiving appropriate fraud alerts and contributory messages.

Must receive a DU Approve/Ineligible decision for non-conforming loan amount.

DU findings must be included in the loan file.

Must comply with Ability to Repay underwriting standards and be a Safe Harbor Qualified Mortgage using criteria in Appendix Q.

Transmittal Summary (Form 1008) is required and must be signed and dated

24. DOCUMENTATION TYPE

Full documentation

25. BORROWER ELIGIBILITY

Permanent Resident

Must have valid social security number

See the Jumbo chapter of the Client Guide for requirements

Ditech (I-32) Jumbo AA Fixed Rate and ARM Mortgage Program

Ditech Jumbo AA Program Page 8 of 25 5/16/16

FIXED RATE 5/1 LIBOR ARM 7/1 LIBOR ARM 10/1 LIBOR ARM

Non-Permanent Resident

Not permitted

First Time Homebuyer

Permitted

Foreign Nationals

Not permitted

Trusts Agreements

See the Jumbo chapter of the Client Guide for eligibility

26. CO-BORROWERS Loans with more than 4 borrowers are ineligible

Co-applicants, co-mortgagors, guarantors and cosigners may not be interested party to the transaction, such as property seller, builder or real estate broker

Non-occupant co-borrower must be a family member or have an established relationship and motivation, not including equity participation for profit, must be provided

Non-occupant co-borrowers permitted for primary residence only

Occupant borrower

Max 35% HTI ratio

Max 43% DTI ratio (within program parameters)

Max combined DTI cannot exceed 43% (within program parameters)

Must contribute a minimum of 5% own funds

27. CREDIT Credit Score Requirements

See the LTV/CLTV Limitations section for minimum credit score requirements

All borrowers must meet credit score requirements, regardless of whether income is used to qualify

24 month credit history required

Trade Line Requirements

Authorized user accounts may not be used to satisfy the trade line requirements.

Disputed accounts may not be used to satisfy the tradeline requirements

A minimum of 3 tradelines with a 12 month history is required regardless of whether the account is open or closed

A minimum of 3 open trade lines for borrowers who do not have a previous mortgage history

If unable to meet the minimum 3 open trade line requirements, credit may be acceptable if all of the following are met

The borrower has a prior mortgage history reviewed for at least 12 months

The borrower exhibits significant credit depth and favorable performance

All borrowers must meet the trade line requirements

Ditech (I-32) Jumbo AA Fixed Rate and ARM Mortgage Program

Ditech Jumbo AA Program Page 9 of 25 5/16/16

FIXED RATE 5/1 LIBOR ARM 7/1 LIBOR ARM 10/1 LIBOR ARM

Housing (Mortgage/Rental) Payment History (PITIA)

Inclusive of all liens regardless of position

Applies to all mortgages on all financed properties

All borrowers must demonstrate a 24 month housing payment history

0x30 in the last 12 months

1x30 in the last 13 – 24 months

0x60 in last 24 months

Subject mortgage must be current on delivery

If primary residence is owned free and clear, a public records search must be provided

Borrowers living rent free acceptable – loan file must provide reason for lack of current housing payment (document on 1003, 1008 and borrower letter of explanation)

Revolving Debt

2x30 in last 12 months

Installment Debt

1x30 in last 12 months

Significant Derogatory Credit

See the Jumbo chapter of the Client Guide for the following:

Bankruptcy

Foreclosure

Modification of Distressed Loan

Preforeclosure

Short sale, deed-in-lieu

28. ASSET/RESERVES Borrower Investment

A minimum 5% down payment must be paid from the borrower’s own funds. The balance may be paid from any of the acceptable asset sources (borrower’s funds or gift funds)

All assets disclosed on the application must be verified, regardless of whether the assets are needed to close or for reserves.

Earnest money deposit must be sourced and verified on all loans

Gift Funds

Primary residence only

Seller Contributions

6% (lesser of appraised value or purchase price)

Ditech (I-32) Jumbo AA Fixed Rate and ARM Mortgage Program

Ditech Jumbo AA Program Page 10 of 25 5/16/16

FIXED RATE 5/1 LIBOR ARM 7/1 LIBOR ARM 10/1 LIBOR ARM

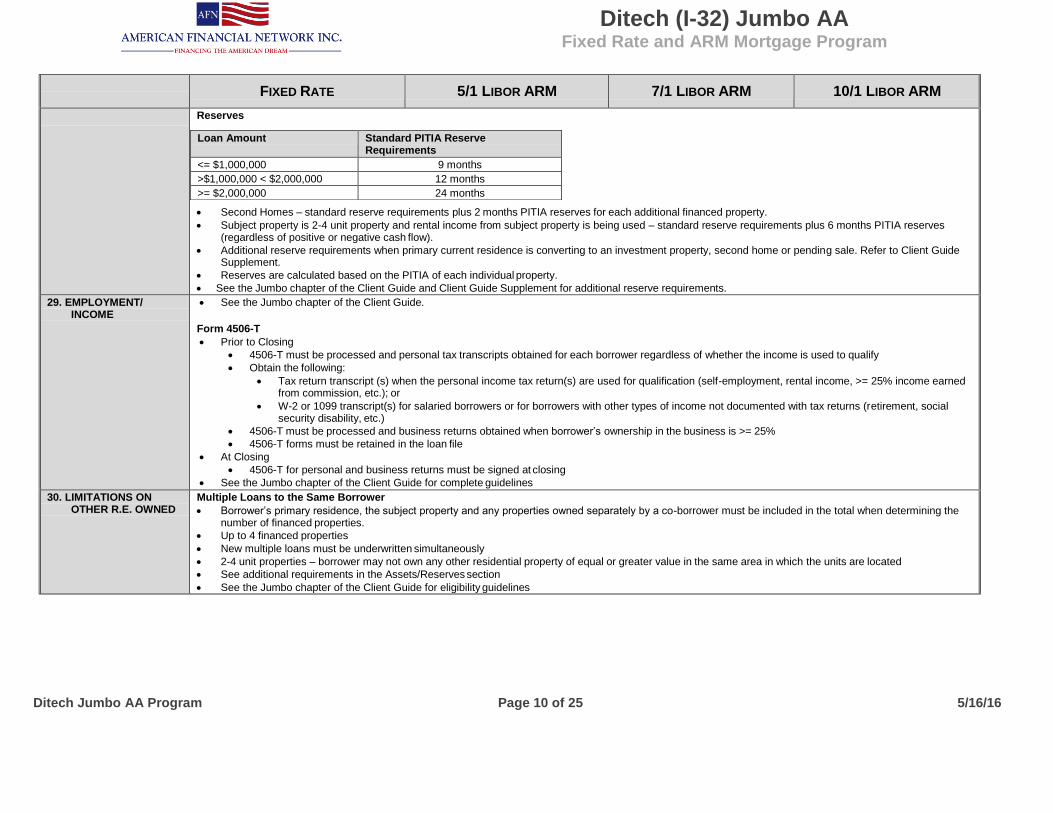

Reserves

Second Homes – standard reserve requirements plus 2 months PITIA reserves for each additional financed property.

Subject property is 2-4 unit property and rental income from subject property is being used – standard reserve requirements plus 6 months PITIA reserves (regardless of positive or negative cash flow).

Additional reserve requirements when primary current residence is converting to an investment property, second home or pending sale. Refer to Client Guide Supplement.

Reserves are calculated based on the PITIA of each individual property.

See the Jumbo chapter of the Client Guide and Client Guide Supplement for additional reserve requirements.

Loan Amount Standard PITIA Reserve Requirements

<= $1,000,000 9 months

>$1,000,000 < $2,000,000 12 months

>= $2,000,000 24 months

29. EMPLOYMENT/ INCOME

See the Jumbo chapter of the Client Guide.

Form 4506-T

Prior to Closing

4506-T must be processed and personal tax transcripts obtained for each borrower regardless of whether the income is used to qualify

Obtain the following:

Tax return transcript (s) when the personal income tax return(s) are used for qualification (self-employment, rental income, >= 25% income earned from commission, etc.); or

W-2 or 1099 transcript(s) for salaried borrowers or for borrowers with other types of income not documented with tax returns (retirement, social security disability, etc.)

4506-T must be processed and business returns obtained when borrower’s ownership in the business is >= 25%

4506-T forms must be retained in the loan file

At Closing

4506-T for personal and business returns must be signed at closing

See the Jumbo chapter of the Client Guide for complete guidelines

30. LIMITATIONS ON OTHER R.E. OWNED

Multiple Loans to the Same Borrower

Borrower’s primary residence, the subject property and any properties owned separately by a co-borrower must be included in the total when determining the number of financed properties.

Up to 4 financed properties

New multiple loans must be underwritten simultaneously

2-4 unit properties – borrower may not own any other residential property of equal or greater value in the same area in which the units are located

See additional requirements in the Assets/Reserves section

See the Jumbo chapter of the Client Guide for eligibility guidelines

Ditech (I-32) Jumbo AA Fixed Rate and ARM Mortgage Program

Ditech Jumbo AA Program Page 11 of 25 5/16/16

FIXED RATE 5/1 LIBOR ARM 7/1 LIBOR ARM 10/1 LIBOR ARM

31. APPRAISAL REQUIREMENTS

Appraisal Report

Appraisal(s) must be ordered through Clients standard ordering process/AMC.

An Interior and Exterior Appraisal Report and Collateral Desktop Analysis (CDA) are required for all loans.

CDA (Collateral Desktop Analysis) and field review must be ordered through Clear Capital

The CDA is a desktop review appraisal completed by a licensed appraiser with local market expertise.

Final LTV/CLTV cannot be based on a review value. All LTVs must use an appraised value that is supported by a review document

Transferred appraisals are not permitted

Condition ratings C1 through C4 are permitted

Quality ratings Q1 through Q5 are permitted

Loan amount >$1,000,000 requires two Interior and Exterior Appraisal Reports with interior photos

Appraisals must be completed by two independent companies (may be same AMC)

The LTV will be determined by the lower of the two appraised values

CDA requirements apply based on the lower of the two appraisals

Units Initial Review

Type CDA Recommends

Field Review

Variance

<= 65.00%

65.01 - 75.00%

75.01 - 80.00%

1 CDA No >= 0% and <5% Accept Accept Accept

>=5% and < 0% Accept Accept Subsequent Field Review Required

>=10% Subsequent Field Review Required

Subsequent Field Review Required

Subsequent Field Review Required

Yes Any Subsequent Field Review Required

Subsequent Field Review Required

Subsequent Field Review Required

2-4 Field Review N/A N/A Default to Field Review

Default to Field Review

Default to Field Review

Field Review Variance Threshold 10% 10% 5%

34. MORTGAGE INSURANCE

N/A

35. SPECIAL REQUIREMENTS/ RESTRICTIONS

Rebuttal Presumption Mortgages are not permitted

Escrow Holdbacks are not permitted

Ditech (I-32) Jumbo AA Fixed Rate and ARM Mortgage Program

Ditech Jumbo AA Program Page 12 of 25 5/16/16

JUMBO AA FIXED RATE CLIENT GUIDE SUPPLEMENT

This supplemental guide works in conjunction with the Product Matrix and Client Guide. The Client Guide contains complete eligibility and underwriting guidelines.

ELIGIBILITY

Age of Documents Credit and appraisal documents may not be more than 90 days from the note date for existing construction

Credit and appraisal documents may not be more than 120 days from the note date for new construction

Land Trusts Not permitted

Multiple Financed Properties

The following identifies properties are subject to limitations Types of Property Ownership Yes/No Joint ownership of residential real estate (considered to be the same as total ownership of an individual property), even if borrower is not

obligated on the Note Yes

Ownership in commercial real estate No

Ownership of a multi-family property consisting of more than 4 dwelling units. No

Joint or total ownership of a property that is held in the name of a corporation or S-corporation, even if borrower is the owner of the corporation and the financing is in the name of the corporation or S-corporation.

No

Joint or total ownership of a property that is held in the name of a corporation or S-corporation, even if borrower is the owner of the

corporation; however the financing is in the name of the borrower. Yes

A property held in a family trust that is owned by the trust and not owned by the beneficiary Yes

Ownership in a timeshare if categorized as an installment debt. No

Obligation on a mortgage debt for a residential property (regardless of whether or not the borrower is an owner of the property). Yes

Ownership of a vacant (residential) lot. No Ownership of a property that is held in the name of an LLC or partnership (limited or general partnership) where the borrower(s) have an

individual or combined ownership in the LLC or partnership Yes

Ownership of a manufactured home and the land on which it is situated and titled as real property. Yes

Ownership of a manufactured home on a leasehold estate not titled as real property (chattel lien on the home). No

TRANSACTIONS

Ineligible Transaction

Single Close Construction to Permanent

Delayed Financing Considered a cash-out refinance

LTV is based on the lesser of the purchase price or appraised value,

The original purchase transaction was an arm's length transaction. If the seller of the property was an LLC, the principals of the LLC must be documented,

The original purchase transaction is documented by the settlement statement, which confirms that no mortgage financing was used to obtain the subject property. A recorded trustee's deed (or similar alternative) confirming the amount paid by the grantee to trustee may be substituted for a settlement statement if a settlement statement was not provided to the purchaser at time of sale. The preliminary title search or report must confirm that there are no existing liens on the subject property,

The source of funds used for the purchase transaction must be documented. If the source of funds used to acquire the property was an unsecured loan or HELOC secured by another property, the new settlement statement must show these sources being paid off with the proceeds.

The new loan amount must not be more than the actual documented amount of the borrower's initial investment in purchasing the property plus the financing of closing costs, prepaid items, and points.

All other cash-out refinance eligibility requirements are met.

Ditech (I-32) Jumbo AA Fixed Rate and ARM Mortgage Program

Ditech Jumbo AA Program Page 13 of 25 5/16/16

JUMBO AA FIXED RATE CLIENT GUIDE SUPPLEMENT

This supplemental guide works in conjunction with the Product Matrix and Client Guide. The Client Guide contains complete eligibility and underwriting guidelines.

Pending Sale of Current Primary Residence

Qualify with the PITIA of both the current property and new primary residence, or

Qualify based on new primary residence if all of the following is met

>= 30% in current property

Executed sales contract for the current residence, and

Lender’ commitment to buyer of current property if contract indicates financing contingency and

Reserves required below

Document equity with a full appraisal dated no more than 60 days prior to the note date

Departing property with less than 30% documented equity or undocumented

Standard reserve requirements plus 6 months PITIA reserves for the departing property Departing property with more than 30% documented equity

Standard reserve requirements plus 2 months PITIA reserves for the departing property

Conversion of Primary to Second Home

Qualify with the PITIA of both the retained property and new primary residence

Document equity with a full appraisal dated no more than 60 days prior to the note date

Departing property with less than 30% documented equity or undocumented

Standard reserve requirements plus 6 months PITIA reserves for the departing property Departing property with more than 30% documented equity

Standard reserve requirements plus 2 months PITIA reserves for the departing property

Conversion of Primary to Investment Property

Document equity with a full appraisal dated no more than 60 days prior to the note date

1 unit property:

Departing property with less than 30% documented equity or undocumented

Rental income cannot be used to offset the mortgage payment

Standard reserve requirements plus 6 months PITIA reserves for the departing property

Departing property with more than 30% documented equity

75% of gross rental income may be used to offset the mortgage payment

Standard reserve requirements plus 2 months PITIA reserves for the departing property

2-4 unit property:

Departing property with less than 30% documented equity or undocumented

Rental income for unit occupied by borrower not permitted

Follow Rental Income requirements for rental income from other units

Standard reserve requirements plus 6 months PITIA reserves for the departing property

Departing property with more than 30% documented equity

75% of gross rental income for unit occupied by borrower may be used to offset the mortgage payment

Follow Rental Income requirements for rental income from other units

Standard reserve requirements plus 2 months PITIA reserves for the departing property

Documentation Requirements:

Fully executed lease

Evidence of receipt of security deposit

Ditech (I-32) Jumbo AA Fixed Rate and ARM Mortgage Program

Ditech Jumbo AA Program Page 14 of 25 5/16/16

JUMBO AA FIXED RATE CLIENT GUIDE SUPPLEMENT

This supplemental guide works in conjunction with the Product Matrix and Client Guide. The Client Guide contains complete eligibility and underwriting guidelines.

Verification of deposit into borrower’s account

Proposed rent must be deemed reasonable for size and location of property

Permanent Financing for New Construction

Transaction is treated as a rate and term refinance

1 unit only

2-4 units, condos and attached PUDs are ineligible

Full appraisal with interior and exterior inspection completed with an as is value

Appraisal update/Completion certificate required if appraisal completed subject to completion

All construction work must be completed and paid for prior to the closing of permanent financing

Escrow holdbacks are not permitted

FINANCING

Subordinate Financing

Not less than 5 years remaining from the Note date of new proposed lien unless the subordinate financing fully amortizes under a level monthly payment plan prior to that time

Fixed Rate

When monthly payments are required, they must cover, at a minimum, the interest due to ensure negative amortization does not occur.

If financing provided by the property seller is more than 2% below current market par rate for combo loans for the subordinate lien as of the date of application, it must be considered a sales concession and the subordinate financing amount must be deducted from the sales price.

Variable Rate

Total amount of secondary or subordinate financing fully amortizes during its term AND

Combined annual payment adjustments of the loan and the secondary or subordinate financing does not exceed:

Lesser of a 2% interest rate increase OR

8.50% payment increase

The repayment terms must provide for regular monthly payments that cover at least the interest due so that negative amortization will not occur.

CREDIT

Disputed Accounts Confirm the accuracy of disputed trade lines reported on the borrower's credit report. If it is determined that the disputed trade line information is accurate, ensure the disputed trade lines are considered in the credit risk assessment.

The borrower must provide a signed and dated satisfactory explanation. Third party documentation must be provided to support borrower explanation.

Landlord Reference

A landlord reference is required using: Credit report verification for the most recent 24 months; Cancelled checks for the most recent 24-month period and a copy of the lease verifying the due date; or A verification of rent (VOR) from a management company with a 24-month payment history and 12 months cancelled checks when the landlord is an interested party to

the transaction (e.g., seller, broker, etc.). In addition, a copy of the lease verifying the due date in lieu of a landlord reference must be provided. Non-Borrowing Spouse

Include 100% of any joint debts in the DTI ratio

Separate credit report for non-borrowing spouse is not required

Self employment losses from non-borrowing spouse:

Can be excluded from the borrower’s qualifying income subject to verification the borrower has no interest in the business.

Should the borrower have an ownership interest in the business, then the full amount of the loss would be deducted from the borrower’s qualifying income.

Ditech (I-32) Jumbo AA Fixed Rate and ARM Mortgage Program

Ditech Jumbo AA Program Page 15 of 25 5/16/16

JUMBO AA FIXED RATE CLIENT GUIDE SUPPLEMENT

This supplemental guide works in conjunction with the Product Matrix and Client Guide. The Client Guide contains complete eligibility and underwriting guidelines.

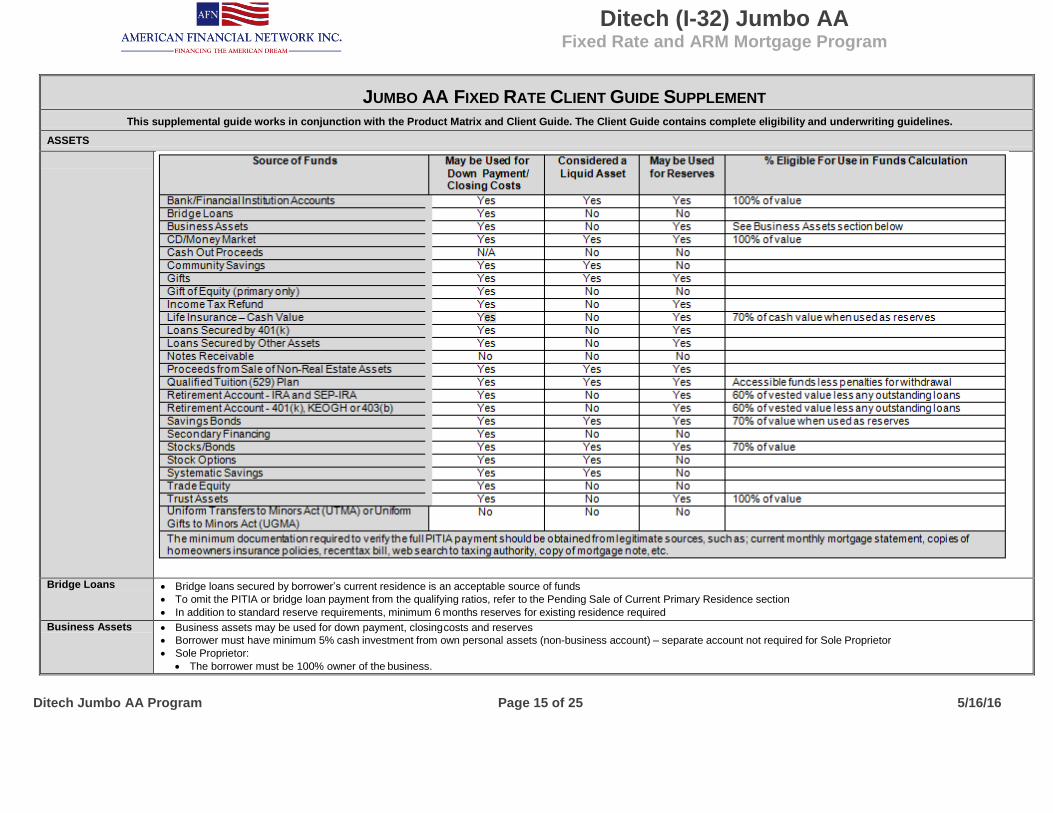

ASSETS

Bridge Loans Bridge loans secured by borrower’s current residence is an acceptable source of funds

To omit the PITIA or bridge loan payment from the qualifying ratios, refer to the Pending Sale of Current Primary Residence section

In addition to standard reserve requirements, minimum 6 months reserves for existing residence required

Business Assets Business assets may be used for down payment, closing costs and reserves

Borrower must have minimum 5% cash investment from own personal assets (non-business account) – separate account not required for Sole Proprietor

Sole Proprietor:

The borrower must be 100% owner of the business.

Ditech (I-32) Jumbo AA Fixed Rate and ARM Mortgage Program

Ditech Jumbo AA Program Page 16 of 25 5/16/16

JUMBO AA FIXED RATE CLIENT GUIDE SUPPLEMENT

This supplemental guide works in conjunction with the Product Matrix and Client Guide. The Client Guide contains complete eligibility and underwriting guidelines.

Provide verification from accountant, CPA or borrower if tax returns are self-prepared

Partnership

The borrower must be a general partner

Verify ability to withdraw funds to the extent of ownership percentage and there is no required repayment

Provide verification from accountant, CPA or all other general partners

Verify percentage of ownership using Form 1065 and Schedule K-1

Corporation

Verify ability to withdraw funds to the extent of ownership percentage and there is no required repayment

Provide verification from account, CPA or corporate resolution indicating stock holder approval

Verify percentage of ownership with Compensation of Officers section of corporate tax return

The impact of the withdrawal must be considered by the underwriter in a cash flow analysis to determine no negative impact to the business based on the withdrawal of the funds. Provide all of the following:

Six months business bank statements

YTD P&L Statement

Current balance sheet for most recent quarter

Letter from applicant confirming impact to the business

Business assets are not considered liquid assets.

The business accountant (must not be related to the borrower or be an interested third party) must provide a letter indicating the

Borrower has access to the funds, and

There is no required repayment and

Funds are not an advancement against future earnings or future cash distributions

Large Deposits The borrower must provide a written explanation and documentation of the source of funds for any large deposits that are inconsistent with the borrower's monthly income. If the source of the large deposit is readily identifiable on the account statement, such as a direct deposit from an employer, the Social Security Administration, etc., additional documentation is not required. However, if there is any question that the funds may have been borrowed or there are consistent deposits that are not income, additional documentation must be obtained

New Accounts

Document source of funds used to open a new account within the last qualified 90 days of the application date, regardless of the amount

Obtain a letter of explanation signed by the applicant(s) for significant large deposits.

Additional documentation to support the explanation is required.

Deposits > 25% - Not required for Funds

If during any monthly period the aggregate total of deposits on an account statement(s) (other than deposits from an identifiable source) is > 25% of the applicant’s gross monthly qualifying income:

Deduct the large deposit(s) from the ending account balance and allow the remaining verified balance in the account to be used as funds to qualify.

If the ending account balance is less than the large deposit(s), no funds from the account may be used and it is not necessary to deduct the difference in funds from another account.

In the event that an asset balance is reduced by the amount of large deposit(s), adhere to the following guidance:

The reason for the change in the asset amount must be documented on the underwriting loan transmittal and the AUS decision must be rerun

Ending balance more than the large deposit:

Additional documentation or explanation is not required.

Ending balance less than the large deposit:

Document the underwriting loan transmittal with the rationale for not using the account. Deposits > 25% - Required for Funds

Ditech (I-32) Jumbo AA Fixed Rate and ARM Mortgage Program

Ditech Jumbo AA Program Page 17 of 25 5/16/16

JUMBO AA FIXED RATE CLIENT GUIDE SUPPLEMENT

This supplemental guide works in conjunction with the Product Matrix and Client Guide. The Client Guide contains complete eligibility and underwriting guidelines.

If during any monthly period the aggregate total of deposits on an account statement(s) (other than deposits from an identifiable source) is > 25% of the applicant’s gross monthly qualifying income, further analysis is required.

Prior to requesting a letter of explanation from the applicant(s), determine which deposit(s) are insignificant (i.e., $50, $75), as the source(s) of these small deposits are not required to be documented or explained.

Obtain a letter of explanation signed by the applicant(s) for significant large deposits.

Additional documentation to support the explanation is required.

Gifts Gift of Equity

Primary residence only

Must be provided by family member, domestic partner or fiancé

Borrower must contribute 5% of own funds

Gift or grant from employer, municipality or non-profit organization

Primary residence only

Cannot be used as reserves

Borrower must contribute 5% of own funds

The following are not permitted

Gift from family members in non-arms length transactions when subject is a second home

Gift of equity for second homes

Life Insurance – Cash Value

Net proceeds from the cash surrender value or from a loan against a life insurance policy are an acceptable source of funds for down payment closing costs and reserves. The most recent statement from the insurance company reflecting the following:

life insurance company name;

borrower as the policy owner;

period covered and ending cash value;

no statements identifying restrictions for withdrawals; and

any outstanding loans. If used for closing, verification of liquidation and receipt of funds must be documented with either a copy of the check from the insurer or payout statement issued by the insurer. If used for reserves, only 70% of the net cash value less any new or outstanding loans may be used. The cash value must be documented but does not need to be liquidated.

Section 1031 Tax Exchange

Not permitted

Stock Options Must be vested and immediately available to the borrower

Use current stock price to determine gain

May not be used to meet reserve requirements

Obtain any of the following

Most recent 2 months statements (must list number of options and price)

Most recent quarterly statement (must list number of options and price) or

Value verified by current statement from stockbroker

Proof of liquidation and receipt of funds required.

Sweat Equity Not permitted

Trade Equity Property seller may agree to take a borrower’s currently owned property in trade as part of the Downpayment

Borrower must contribute minimum 5% cash down payment from own funds

Provide all of the following:

Sales contract

Full interior/exterior appraisal of property being traded

Ditech (I-32) Jumbo AA Fixed Rate and ARM Mortgage Program

Ditech Jumbo AA Program Page 18 of 25 5/16/16

JUMBO AA FIXED RATE CLIENT GUIDE SUPPLEMENT

This supplemental guide works in conjunction with the Product Matrix and Client Guide. The Client Guide contains complete eligibility and underwriting guidelines.

Fully executed HUD-1

Full executed and recorded deed transferring title

LIABILITIES/DEBTS

Bridge Loans Bridge loans must be included in the borrower’s debt-to-income ratio.

Payment may be excluded if all of the following is provided:

executed sales contract for current residence and

commitment to the buyer of the current residence (if the contract contains a financing contingency) and

standard reserve requirements plus 6 months PITIA reserves pm the current residence

Business Debts of Self-Employed Borrowers

The debt must be considered as part of the borrower’s individual recurring monthly debt obligations if any one of these conditions cannot be met.

The account has no late payments in the last 12 months and no more than 1 x 30 in the last 24-month period.

Evidence, such as canceled company checks that the debt has been paid out of company funds.

The cash flow analysis of the company took the payment of the debt into consideration.

Business Expenses

When a self-employed borrower indicates that certain liabilities are paid by his or her business or business debt appears on the borrower's individual credit report, the liability must be included in the DTI unless:

There are no late payments in the last 12 months;

There is no more than 1x30 in the last 24 months;

A minimum of twelve months evidence documenting that the debt is paid by the business account; and

A cash flow analysis for the business took the payment obligation into consideration.

The payment must be included in the borrower’s individual recurring monthly debt obligations if any of the following situations exist:

The business does not provide sufficient evidence that the obligation was paid out of company funds;

The business provides acceptable evidence of its payment of the obligation, but the cash flow analysis of the business does not reflect any business expense related to the obligation (such as an interest expense - and taxes and insurance, if applicable - equal to or greater than the amount of interest that one would reasonably expect to see given the amount of financing shown on the credit report and the age of the loan). It is reasonable to assume that the obligation has not been accounted for in the cash flow analysis; or

If the account in question has lates in the past 12 months or more than 1x30 in the past 24 months.

Court Ordered Assignment of Debt

When the borrower has outstanding debt that was assigned to another party by court order (e.g., divorce decree or separation agreement), and the creditor does not release the borrower from liability, it may be excluded from the debt-to-income ratio if all of the following is met

No delinquent payments in the previous consecutive 12 month period

Evidence that primary obligor has been making the payments for the past 12 consecutive months documented with one of the following:

Cancelled checks

Copies of money orders

Other acceptable documentation

If the account had any late payments in the past 12months, the payment must be included in the DTI ratio

Installment Debt All installment accounts that extend beyond 10 payments remaining will be included in long-term obligations for qualifying purposes.

Installment payments with 10 or less months remaining do not need to be included in long-term obligations unless:

The excluded installment payment is significant enough to affect the applicant's ability to make the mortgage payments. In this instance, the payment must be included in the total DTI ratio.

Deferred loan payments

Must be included in DTI ratio

If payment not indicated on the credit report, provide payment letter or forbearance agreement to determine payment Student loans

Ditech (I-32) Jumbo AA Fixed Rate and ARM Mortgage Program

Ditech Jumbo AA Program Page 19 of 25 5/16/16

JUMBO AA FIXED RATE CLIENT GUIDE SUPPLEMENT

This supplemental guide works in conjunction with the Product Matrix and Client Guide. The Client Guide contains complete eligibility and underwriting guidelines.

Must be included in DTI ratio

If payment letter or forbearance agreement does not verify the payment, calculate the payment using the appropriate interest rate for Stafford student loan (based on 10 year amortization)

July 2006 to present: 6.80%

July 1998 to June 2006: 7.14%

July 1995 to June 1998: 7.94%

Prior to 1995 or open date is not provided: 8.25% Student loan in default

Must be paid in full at or prior to closing

If renegotiated payment plan has been established, copies of the past 12 months’ payments and repayment agreement are required

If less than 12 months payments, loan must be paid in full

Loans Secured by Borrower’s Assets

When the borrower uses his or her financial assets as security for a loan, the monthly payment must be included in the DTI

Provide a copy of the applicable loan instrument that shows the financial asset as collateral for the loan

If the borrower intends to use the same asset to satisfy reserve requirements, reduce the value of the asset by the proceeds from the secured loan and any related fees to determine whether the borrower has sufficient liquidity remaining.

Contingent Liability Co-signed/court order mortgage liability

A borrower can have a contingent liability from either cosigning for another party to obtain credit or have debt that was assigned to another party through a court order (such as under a divorce decree or separate agreement), and the borrower has not been released from the liability.

The monthly payment for the contingent liability must be included in the borrower’s total qualifying debts if the borrower’s credit history or the cosigned debt itself exhibits a derogatory payment history.

The borrower must meet all of the following requirements in order to exclude the cosigned debt from the borrower’s Debt-to-Income (DTI) ratio:

Evidence that the primary obligor has been making the payments for the past consecutive 12 months, documented by any of the following:

Cancelled checks

Copies of money orders

Other acceptable documentation Mortgage Assumption

The contingent liability is not required to be counted as part of the borrower’s recurring monthly debt obligations, if it can be verified that the property purchaser has at least a 12- month history of making regular, timely payments for the mortgage.

All of the following documentation is required:

Evidence of the transfer of ownership

Copy of the formal, executed assumption agreement

Credit report indicating that consistent and timely payments were made for the assumed mortgage

If timely payments during the most recent 12-month period cannot be documented, the applicable mortgage payment must be counted as part of the recurring monthly debt obligations.

Pay Off Revolving Debt

Source of funds must be documented.

Minimum $10 monthly payment for each debt paid must be included in DTI

If a revolving debt or HELOC is to be paid off and closed, the loan file must contain the following documentation in order to exclude the payment from the DTI:

Copy of the HUD-1 Settlement Statement specifically naming the debt as being paid off. and

Supplemental credit report or direct verification with the creditor supporting the debt is closed or

Closing instructions requiring closure of debt (HELOC payoff, subject property only)

Pay Down Revolving Debt

Source of funds must be documented

If a revolving or HELOC account is to be paid off or paid down, but not closed, the existing monthly payment on the current outstanding balance should be counted in the DTI ratio.

Ditech (I-32) Jumbo AA Fixed Rate and ARM Mortgage Program

Ditech Jumbo AA Program Page 20 of 25 5/16/16

JUMBO AA FIXED RATE CLIENT GUIDE SUPPLEMENT

This supplemental guide works in conjunction with the Product Matrix and Client Guide. The Client Guide contains complete eligibility and underwriting guidelines.

Ensure any funds to pay off a revolving account are clearly indicated that funds are to close the account rather than simply to pay down the account to a $0 balance and remain open.

If a HELOC account is being paid down, rather than closed, the full line amount of the HELOC must be calculated in the CLTV.

Pay Off Installment Debt

Source of funds must be documented.

Verify debt has been paid with one of the following:

Copy of the HUD-1

Supplemental credit report or

Verification from the creditor

Pay Down Installment Debt

If an installment debt is paid down to less than 10 months, the debt does not need to be calculated in the DTI ratio unless the excluded installment payment is significant enough to

affect the borrower's ability to make the mortgage payments and the borrower has limited reserves.

Revolving Accounts

In the absence of a verified or stated payment amount according to the credit report, a payment should be calculated at 5% of the outstanding

All revolving accounts, regardless of months remaining, must be included in the total DTI ratio, unless the debt has been paid off and closed.

30 day accounts

Open 30-day charge accounts, where a minimum monthly payment is disclosed, may be treated as a revolving account, only if a minimum monthly payment is supported by the credit report or a monthly statement.

The loan file must contain comments clearly indicating the manner in which the open 30-day charge account was addressed

An open 30-day charge account, where the reported monthly payment equals the total outstanding balance or indicates a zero payment, requires the balance to be paid in full every month.

The loan file must contain evidence of sufficient assets to cover the unpaid balance, in addition to the down payment, closing costs and reserves.

If sufficient assets are verified, the payment can be excluded from the DTI calculation.

If assets are insufficient, a payment of 5% of the outstanding balance must be included in the DTI calculation

This applies to personal and business charge accounts reflected on the credit report.

See the Jumbo chapter of the Client Guide for additional information on debt paid by the business

HELOC Existing HELOC that will be subordinate to the proposed mortgage:

Whether the HELOC is frozen or not, use the monthly payment reflected on the credit report as a liability.

If the credit report does not indicate a payment, use the payment from the most recent billing statement.

If the payment is not reflected on the credit report and a billing statement is not obtained, use 0.75% of the full line amount.

If there is no payment reflected on the credit report but there is a zero balance, no monthly payment is required to be counted in the recurring monthly debt.

If HELOC is new, qualify the borrower at 0.75% of the full line amount

Note: HELOCs that have been frozen by the lender, with or without a balance, must still be calculated into the CLTV.

If the subordinate financing is a deferred Community Second loan:

If repayment of the loan is deferred for five years or more, then the monthly payment should not be included in the monthly housing expense calculation.

If repayment is deferred less than five years, then the payment required at the end of the deferral period must be included in the monthly housing expense calculation.

If paid off or paid down but not closed:

Include existing monthly payment on current outstanding balance in the DTI ratio

Include the full line amount in the CLTV ratio

If paid off and closed, provide all of the following to exclude the payment from the DTI ratio:

Ditech (I-32) Jumbo AA Fixed Rate and ARM Mortgage Program

Ditech Jumbo AA Program Page 21 of 25 5/16/16

JUMBO AA FIXED RATE CLIENT GUIDE SUPPLEMENT

This supplemental guide works in conjunction with the Product Matrix and Client Guide. The Client Guide contains complete eligibility and underwriting guidelines.

Copy of HUD1 specifically naming the debt a being paid off and

Supplemental credit report or direct verification with the creditor supporting the debt is closed or

Closing instructions requiring closure of debt.

INCOME/EMPLOYMENT

Prior Employment Verification

Verbal verification of employment required for previous employment

Extended Absence Must be employed in current job for 6 months or longer

Document two year work history prior to the absence

Salaried Borrower Most recent paystub(s) covering most recent 30 days of earnings and YTD income,

Most recent two year's W-2s and/or 1099s,

Verbal Verification of Employment, and

Variable income (bonus, commissions, overtime, second job) may be removed when not needed to qualify – provide justification for not using the income in the file

Removal of income not needed to qualify is not permitted when borrower is employed by a family owned business

Bonus and Overtime Income

The following documentation must be obtained:

Most recent paystub(s) covering at least 30 days earnings and YTD income,

Most recent two year's W-2s,

Verbal verification of employment, and

Written verification of employment, employer letter or equivalent indicating likelihood of continuance. If written confirmation of continuance cannot be obtained, provide documentation indicating employer statement could not be obtained and rationale for inclusion of the income

Commission Income

The following income documentation must be obtained:

most recent paystub(s) covering at least 30 days earnings and YTD income,

most recent two year’s W-2s or 1099s

most recent two year's personal income tax returns with all schedules,

verbal verification of employment and

written verification of employment, employee letter or equivalent itemizing commission income

Self-Employed Evidence that the borrower has at least two consecutive years of self-employment operating the same business in the same location is required to demonstrate income stability.

All tax returns must be signed and dated

All of the following documentation is required:

>= 25% ownership

Most recent two year’s personal tax returns with all schedules

Most recent two year’s K-1s (partnership and s-corporation)

Most recent two year’s business tax returns (excluding sole proprietor)

YTD P&L signed and dated by the preparer and borrower prior to the note date, if more than 120 days have passed since end of business fiscal year

Current Balance Sheet signed and dated by the preparer and borrower prior to the note date, if more than 120 days have passed since end of business fiscal year (excluding sole proprietor)

Verbal verification of employment within 30 calendar days prior to note date

< 25% ownership

Most recent two year’s personal tax returns with all schedules

Most recent two year’s K-1s (partnership and s corporation)

Verbal verification of employment within 30 calendar days prior to note date

Ditech (I-32) Jumbo AA Fixed Rate and ARM Mortgage Program

Ditech Jumbo AA Program Page 22 of 25 5/16/16

JUMBO AA FIXED RATE CLIENT GUIDE SUPPLEMENT

This supplemental guide works in conjunction with the Product Matrix and Client Guide. The Client Guide contains complete eligibility and underwriting guidelines.

The loan file must contain the following:

The Self-employed Income Analysis Fannie Mae Form 1084 or Freddie Mac Form 91 used to analyze individual returns

Fannie Mae Form 1088 used to analyze business returns

Income not needed to qualify

Business must be analyzed to ensure that it will not negatively affect borrower’s personal income or assets

Provide 2 years tax returns to determine if there is a loss that may impact stable monthly qualifying income

Provide additional information to fully evaluate the impact of a business loss

Business losses from a non-borrowing spouse can be excluded subject to verification that the borrower has not interest in the business. If borrower has an interest, the full amount of the loss must be deducted from qualifying income

Rental Income Subject Property (2-4 unit primary residence)

Rental Income derived from the subject property primary residence may be used as qualifying income provided the amount does not exceed 30% of the total of all other qualifying income (excluding rental income from the subject property).

Rent loss insurance covering six months if using rental income to qualify.

Property Owned at Least One Year

Provide all of the following:

Most recent two year's personal income tax returns; and

Current 12-month lease agreement(s).

Property Owned Less than One Year and Is Not Reported on Tax Return

Provide all of the following:

Operating Income Statement (Form 216); and

Current 12-month lease agreement(s).

If the borrower owned rental property during the previous tax year, the most recent two year's personal income tax returns are required.

Lease agreements may not be used as standalone documentation to show monthly rental income stability. They may be used to support the rental income used to qualify.

Lease agreements are required to evidence rental income disclosed on personal income tax returns.

Operating Income Statement required if:

Rental income is used to qualify;

The borrower has owned the property less than one year; and

The rental income is not reported on Schedule E.

Rental income for the property must be based on current rents, except in the following circumstances when market rents must be used:

Current rent exceeds market rents;

Property is new or proposed construction; or

The property is vacant.

If one of the units will be occupied by the borrower, no income may be used for that unit.

The income approach on the appraisal must support the rental income used for qualifying.

No History of Receiving Rental Income

Appraiser's opinion of market rent; and

Current 12-month lease agreement(s), if applicable.

History of Receiving Rental Income

Most recent two year's personal tax returns, including Schedule E.

Existing Lease

Ditech (I-32) Jumbo AA Fixed Rate and ARM Mortgage Program

Ditech Jumbo AA Program Page 23 of 25 5/16/16

JUMBO AA FIXED RATE CLIENT GUIDE SUPPLEMENT

This supplemental guide works in conjunction with the Product Matrix and Client Guide. The Client Guide contains complete eligibility and underwriting guidelines.

Current lease agreement(s);

Evidence of rental income for 12 months, or period of the lease if less than 12 months.

New Lease

Current lease agreement(s); and

Evidence of receipt of the initial deposit.

Treatment of Income or Loss

No more than 30% of the total of all other qualifying income (excluding net rental income from the subject property) may be from the subject property.

Total all income (except net rental income from the subject property) to be used for qualifying and multiply by 30%. If the net rental income from the subject property does not exceed 30% of the total of all other qualifying income, the full amount may be added tot he total qualifying income.

if the net rental income from the subject property exceeds 30% of the total of all other qualifying income, no more than the calculated amount may be added to the total qualifying income.

Other Real Estate Owned

Property Owned at Least One Year

Provide all of the following:

Most recent two year's personal income tax returns; and

Current 12-month lease agreement(s).

Property Owned Less than One Year and Is Not Reported on Tax Return

Provide all of the following:

Current 12-month lease agreement(s); and

Verification of rents received. If the borrower owned rental property during the previous tax year, the most recent two year's personal income tax returns are required. Lease agreements may not be used as standalone documentation to show monthly rental income stability. They may be used to support the rental income used to qualify. Lease agreements are required to evidence rental income disclosed on personal income tax returns. Operating Income Statement not required.

History of Rental Income must be confirmed by:

Most recent two year's personal income tax returns, including Schedule E;

Current lease agreements may only be used if a property is not listed on Schedule E because it was acquired subsequent to filing the tax return. Existing Lease

Current lease agreement(s);

Evidence of rental income for 12 months, or period of the lease if less than 12 months.

New Lease

Current lease agreement(s); and

Evidence of receipt of the initial deposit.

Treatment of Income or Loss

If the monthly rental income less the full PITIA is positive, it must be added to the total monthly income.

If the monthly rental income less the full PITIA is negative, the monthly net rental loss must be added to the borrower's total monthly obligations. The full PITIA for the rental property is factored into the amount of the net rental income (or loss), therefore it should not be counted as a monthly obligation. It must be reported on the loan application.

Ditech (I-32) Jumbo AA Fixed Rate and ARM Mortgage Program

Ditech Jumbo AA Program Page 24 of 25 5/16/16

JUMBO AA FIXED RATE CLIENT GUIDE SUPPLEMENT

This supplemental guide works in conjunction with the Product Matrix and Client Guide. The Client Guide contains complete eligibility and underwriting guidelines.

The full monthly payment for the borrower's primary residence must be counted as a monthly obligation. Alimony/Child Support

Must be court ordered to be used as qualifying income

Corporate Relocation

A borrower may use funds provided by his or her employer to pay part of the down payment, closing costs, and prepaids after the borrower has met the minimum required investment.

Relocation assistance in the form of reimbursement from the employer that is to be received after closing is not considered available funds to close, but may be considered reserves.

Provide all of the following:

Copy of the relocation policy and evidence of eligibility for benefits;

Copy of the request for funds anticipated for closing; and

Evidence of receipt of funds from employer. See the Jumbo chapter of the Client Guide for additional requirements.

Depletion of Assets Not permitted

Employment by Relative

A borrower employed by a family member or employed by a family-held business, property seller or real estate broker is eligible with :

Most recent paystub(s) covering most recent 30 days of earnings and YTD income,

Most recent two year's W-2s and/or 1099s,

Verbal Verification of Employment, and

Evidence that borrower does not have 25% or more ownership in the business

If business is a corporation provide one of the following:

A signed copy of the most recent corporate tax return OR

If corporate returns cannot be obtained because the borrower claims no ownership, confirm and document the loan file that the borrower is not listed as a principal of the corporation via public sources such as State Licensing Agencies.

Employment by Interested Party

Most recent paystub

Most recent 2 year’s W-2s or 1099s and

Most recent 2 years signed personal tax returns

Foster Care Income Foster care income must be likely to continue for the next three years from the date of the application. Any of the following types of documentation is required:

letter from organization providing the income,

most recent 2 years signed personal tax returns or

copies of deposit slips or bank statements confirming regular payments

Note Receivables The Note income must be expected to continue for a minimum of three years from the date of the application.

A copy of the note is required to document amount, frequency and duration of payments

One of the following must be provided to document receipt of the income for the most recent 12 months:

most recent personal income tax returns with all schedules, or

bank statements showing regular deposits of funds

Projected Income The borrower must have a legally binding contract with terms and conditions of employment. Offer letters are not acceptable; The borrower must be employed in the new job prior to closing; Must have liquid PITIA reserves equal to the number of months between the note date and the start date of the new employment in addition to reserves required by the

program; and Written VOE verifying that borrower has begun employment.

Retirement, Pension, Annuity Income

Verification of receipt of income for at least 60 days is required

Provide the following documentation:

Ditech (I-32) Jumbo AA Fixed Rate and ARM Mortgage Program

Ditech Jumbo AA Program Page 25 of 25 5/16/16

JUMBO AA FIXED RATE CLIENT GUIDE SUPPLEMENT

This supplemental guide works in conjunction with the Product Matrix and Client Guide. The Client Guide contains complete eligibility and underwriting guidelines.

Distributions Most recent 2 months bank statements and

Any of the following:

Written verification from entity supplying the income

Most recent award letter

Most recent year’s 1099

Must recent year’s signed personal tax returns

Social Security Retirement, Disability or Supplemental Security Income received by borrower from their own account or work record: provide SSA Award letter

Retirement, Disability or Survivor Benefits drawn from another person's account or work record: provide SSA Award Letter and three year continuance

Trust Income 3 month consecutive history of receipt required

Provide:

Trust Agreement or

Trustee’s statement confirming amount, frequency and duration and

Most recent 3 months bank statements

PROPERTY

Mineral, Oil and Gas Rights

Properties with gas, oil and/or subsurface mineral rights are permitted if:

The exercise of such rights will not result in damage to the subject property or impairment of the use or marketability of the subject property for residential purposes and there is no right of surface or subsurface entry within 200 feet of the residential structure, or

There are comprehensive endorsements to the title insurance policy that affirmatively insures against damage or loss due to the exercise of such rights, such as but not limited to:

Environmental Protection Lien Endorsement; and

Restrictions, Encroachments, Minerals Endorsement without any deletions; and

Minerals and Surface Damage Endorsement