District Court Stringency and Firm Restatement Policy · District Court Stringency and Firm...

66

District Court Stringency and Firm Restatement Policy † C.S. Agnes Cheng School of Accounting & Finance The Hong Kong Polytechnic University Kowloon, Hong Kong Tel: (852) 2766-7772, E-mail: [email protected] Henry He Huang SySyms School of Business Yeshiva University New York, NY 10033 Tel: (832) 276-3834, E-mail: [email protected] Zhen Lei School of Accounting & Finance The Hong Kong Polytechnic University Kowloon, Hong Kong Tel: (852) 3400-3641, E-mail: [email protected] Haitian Lu * School of Accounting & Finance The Hong Kong Polytechnic University Kowloon, Hong Kong Tel: (852) 2766-7065, E-mail: [email protected] This version: May, 2017 † Agnes Cheng thanks Hong Kong Government Research Grant Council - General Research Fund (#590213), and Haitian Lu thanks the National Natural Science Foundation of China (#71503225) for the support of this project. * Corresponding author. Tel.: +852 2766 7065; Fax: +852 2356 9845. E-mail address: [email protected] (Haitian Lu).

Transcript of District Court Stringency and Firm Restatement Policy · District Court Stringency and Firm...

District Court Stringency and Firm Restatement Policy †

C.S. Agnes Cheng

School of Accounting & Finance

The Hong Kong Polytechnic University

Kowloon, Hong Kong

Tel: (852) 2766-7772, E-mail: [email protected]

Henry He Huang

SySyms School of Business

Yeshiva University

New York, NY 10033

Tel: (832) 276-3834, E-mail: [email protected]

Zhen Lei

School of Accounting & Finance

The Hong Kong Polytechnic University

Kowloon, Hong Kong

Tel: (852) 3400-3641, E-mail: [email protected]

Haitian Lu*

School of Accounting & Finance

The Hong Kong Polytechnic University

Kowloon, Hong Kong

Tel: (852) 2766-7065, E-mail: [email protected]

This version: May, 2017

† Agnes Cheng thanks Hong Kong Government Research Grant Council - General Research Fund (#590213), and

Haitian Lu thanks the National Natural Science Foundation of China (#71503225) for the support of this project. * Corresponding author. Tel.: +852 2766 7065; Fax: +852 2356 9845. E-mail address: [email protected]

(Haitian Lu).

District Court Stringency and Firm Restatement Policy

Abstract

Firms’ litigation risk heightens when prior misstatement came to knowledge of the management.

This study examines how district court stringency in dismissing 10b-5 securities lawsuits affects

misreporting firms’ restatement policy. We find misreporting firms headquartered in more

stringent courts are more likely to make accounting irregularity restatement, before they are sued.

Using supreme court’s Tellabs decision as a shock to pleading standard in some, but not all, courts,

we find evidence consistent with preemptive disclosure hypothesis. Event study shows that upfront

restatements mitigate value losses upon lawsuit when firms’ home court is stringent. This paper

uncovers significant role of court stringency in the litigation-disclosure nexus.

Key words: Court stringency, Accounting misreporting, Securities lawsuit, Restatement

JEL Classification Code: M41; K22; G39

1. Introduction

Quality of financial reporting is vital to securities market. Numerous evidence has shown

the high frequency and severe adverse consequence of accounting misreporting. When managers

discover the accounting mistake, the federal securities law and accounting rules require firms to

issue a restatement correcting prior misreporting.1 In the real world, however, some firms are up

front with restatements, others opportunistically choose not to restate. The systematic under-

correction of misstatements can lower investors’ confidence in the market. Enforcing restatements

by the misreporting firms is thus important to protect investors, especially when external

monitoring is weak.

As public enforcement by the SEC is resource constrained, the private securities lawsuit

pursuant to the SEC 10b-5 anti-fraud provision plays unique roles in compensating victims, and

deterring frauds (See Habib et al. 2014 for a review). However, whether this mechanism is

effective in enforcing restatements by misreporting firms is unexplored. We answer this question

using novel, court-level data.

Firms’ litigation risk heightens when managers became aware of accounting mistakes. Since

securities litigation poses large costs to firms, economic theories predict that firms’ restatement

policy can be pre-emptive or defensive, depending on the net benefits of disclosure. The

preemptive disclosure hypothesis (Skinner, 1994, 1997) posits that the deterrence effect of

litigation motivates managers to make timelier restatements, for it helps to weaken the claim that

1 The SEC has ruled that “there is a duty to correct statements made in any filing…if the statements either have become

inaccurate by virtue of subsequent events or are later discovered to have been false or misleading from the outset,

and the issuer knows or should know that persons are continuing to rely on all or any material portion of the statements”

(Sec. Act. Rel. 6084, 17 SEC Dock. 1048, 1054 (1979)). The FASB (2005) ASC Topic 250, Accounting Changes and

Error Corrections, states, ‘‘Any error in the financial statements of a prior period discovered after the financial

statements are issued shall be reported as an error correction, by restating the prior-period financial statements.’’

See also Accounting Principles Board Opinion 20; Statement of Financial Accounting Standards (SFAS) No. 16; and

SFAS No. 154 (issued in May, 2005), among others.

managers withheld private information to keep price distorted, and reduce potential damages by

shortening the class period. Alternatively, the defensive disclosure hypothesis (Kothari, Shu, and

Wysocki, 2009; Rogers and Buskirk, 2009) predicts that due to catastrophic consequences of

restatement including lawsuits 2 , managers tend to avoid difficult decisions, gambling that

subsequent corporate events would allow them to bury the accounting mistakes. Using different

measures of litigation risk, prior empirical work generates mixed results. 3 Whether higher

litigation risk prompts misreporting firms to “admit their mistakes” is an empirical question.

To shed light on this debate, this paper exploits plausibly exogenous variation of the federal

district court stringency where firms are headquartered. In the United States, the private

enforcement on financial frauds pursuant to the Securities and Exchange Act of 1934 and the

Private Securities Litigation Reform Act (PSLRA) of 1995 is achieved primarily through the

country’s 94 federal district courts4 under supervision by circuit (appellate) courts and the supreme

court. Though technically securities lawsuits can be filed in any of the district courts where the

defendant firm has a place of business5, multiple filings need to be consolidated in one case

typically heard by the district court where the defendant firm is headquartered6. This assumption

2 These consequences include, for example, negative market responses (Palmrose, Richardson, and Scholz, 2004),

increased cost of capital (Hribar and Jenkins, 2004), management turnover (Collins et al. 2009) and the resultant

securities lawsuits (Francis, Philbrick and Schipper, 1994). 3 For example, Baginski, Hassell and Kimbrough (2002) argue that American and Canadian firms are under “similar

business environment but different litigation environments”. They find Canadian firms make more frequent and

precise management forecasts than U.S. firms. Srinivasan, Wahid and Yu (2015) find U.S. listed firms headquartered

in weak rule-of-law countries are less likely to restate than are firms from strong rule-of-law countries, supporting the

preemptive disclosure hypothesis. 4 The five federal district courts located outside the 50 states are excluded from this study. They include those existed

in Puerto Rico, the Virgin Island, the District of Columbia, Guam, and the Northern Mariana Islands. 5 Securities and Exchange Act of 1934, ch.404, sec.27, 48 Stat. 881, 902-03 (codified as amended at 15 U.S.C § 78aa

(2006)). 6 The legal and empirical basis for this assumption is discussed in detail in Section 3.2.

is validated by data. Over our sample period (2001-2014) over two-thirds of the 10b-5 lawsuits

were heard by the district courts where defendant firms are headquartered.

Unlike prior work which estimates litigation risk at either country (Baginski, Hassell and

Kimbrough, 2002; Srinivasan, Wahid, and Yu, 2015), industry (Francis, Philbrick, and Schipper,

1994), or firm-level (Kim and Skinner, 2012), this paper measures litigation risk at court-level,

and investigates whether misreporting firms headquartered in more stringent district court

jurisdictions are more likely to restate. Specifically, we estimate the dismissal rate of a district

court on securities lawsuits within five years prior to a headquartering firm’s fiscal year end.

Higher dismissal rate means a district court is less shareholder-friendly, thus inversely related to

litigation risk for firms under its jurisdiction.7

To appreciate this independent variable, we note the following: First, court dismissal rate

reflects the average outcomes of past securities lawsuits heard by almost randomly assigned district

judges, and therefore exogenous to individual firm characters or individual case merits. Second, it

is unlikely that firms choose or move their headquartering place based on stringency of a district

court. Third, this variable captures the within-country, securities law enforcement by the courts,

with variations both across districts and over the time, enabling more powerful tests.

Note the district court stringency can affect both headquartering firms’ incentive to misreport

and their propensity to restate upon discovery. This paper focuses on the latter, which includes

only misreporting firms. Among the misreporting firms, we distinguish those making preemptive

restatements with those keeping strategic silence. We then ask whether more stringent courts

7 To illustrate with example, suppose the district court of North Carolina have dismissed 90% of filed securities

lawsuits in a given period, whilst the district court of South Carolina dismissed only 10% in the same period. It sends

signal to headquartering firms in North Carolina district court that even if sued, the probability of receiving legal

penalties is low.

prompt misreporting firms to be upfront with restatements. It follows, crucial to our identification

strategy is to pick firms known to make accounting mistakes.

We use three methods to identify misreporting firms. Our first sample comprises all 10b-5

defendant firms with alleged GAAP violations from 2000 to 2014 (hereafter “Sample 1”). In the

post-PSLRA period with heightened pleading standards, securities lawsuits in the 2000s typically

point to hard evidence of fraud such as GAAP related accounting misrepresentations (Choi, Nelson,

and Pritchard, 2009). Among these defendant firms, some made corresponding restatement before

the lawsuit whilst others did not. We then ask whether more stringent court prompts defendant

firms to make preceding restatement.

Allegations of GAAP violation in 10b-5 lawsuits can be meritorious or frivolous, to refine

our sample of misreporting firms we include defendant firms that made corresponding restatement

before and after the lawsuits (hereafter “Sample 2”). This sample has the best counterfactual group

since firms’ own and eventual restatements are prima facie evidence of their accounting mistakes.

In constructing our Sample 2, firms’ restatement period must match the class period in the 10b-5

lawsuit with alleged GAAP violation. We then ask whether more stringent court prompts these

misreporting firms to make restatement before the lawsuit.

We note that not all misreporting firms were detected by securities lawsuits. To mitigate our

reliance on lawsuits to identify misreporting firms, we construct a larger sample that exploits firms’

earnings management levels (hereafter “Sample 3”). Specifically, for each industry and year, we

first estimate the discretionary accruals of each restating firms. The counterfactual group of non-

restating misreporting firms is then identified as those in the same industry and year, whose

discretionary accrual is either higher than the 90th percentile or lower than the 10th percentile that

of the restating firms. Built on this sample, we ask whether firms in more stringent courts are more

likely to make restatements.

In all three samples, we find firms headquartered in the jurisdiction of low-dismissal rate

(more stringent) district courts are more likely to make accounting irregularity-based (as opposed

to error-based) restatements.8 Remarkably, court dismissal rate is the only variable that exhibits

both statistical significance and large economic magnitude: Ceteris paribus, one standard

deviation increase in court dismissal rate leads to 4.89%, 6.87% and 1.53% reduction in

restatement propensity compared to an average restating rate of 28.2%, 55.6% and 30.4% in our

1st, 2nd, and 3rd sample. To appreciate, an one standard deviation increase in dismissal rate amounts

to increase that from the level of Illinois (Northern) to that of California (Northern) district court.

To provide causal evidence that misreporting firms are more upfront with restatements when

their home court becomes more stringent, we exploit the supreme court’s rulings in Tellabs v.

Makor (hereafter “Tellabs”) in 2007 that alter the pleading standard in some, but not all underling

courts. Tellabs is the landmark case and one of the supreme court’s first efforts to clarify the strong

inference standard of Scienter, a key legal element to plead 10b-5 claims. We find following

Tellabs, which raised the pleading standard to bring cases against a defendant in courts that had

previously exercised low standards, there is increase in restatement propensity for firms

headquartered in such districts.

8 We separately considered the effect of court dismissal rate on error-based restatements and do not find significant

results. To the extent that 10b-5 lawsuits is only relevant when the misstatement was due to fraud (accounting

irregularities) rather than errors, the non-result on error-based restatements lends additional support to our claim that

managers actively consider their home court stringency when deciding whether to restate. However, this non-result

on error-based accounting restatement must be interpreted with caution due to sample size and the way we construct

counterfactual groups. See Section 5.2 in the robustness test for details.

Why misreporting firms make pre-emptive restatement in the presence of litigation risk? To

shed light on this query we study the shareholder wealth effect of pre-emptive restatements across

district court jurisdictions. By focusing on the market reactions around two event dates, the “class

end” date and “case filing” date, we find that overall, the market anticipate higher legal cost for

firms headquartered in more stringent district courts. However, the CAR differences between

restating and non-restating misreporting firms is only significant when we allow the effect of

restatement on CAR to depend on defendant firm’s home court dismissal rate. Interestingly, for

misreporting firms in more stringent courts, making preemptive restatement saves shareholder

value. However, for misreporting firms in less stringent courts, preemptive restatement harms

shareholder value. We rationalize this result following the Akerlof (1970) adverse selection model,

which predicts the value of being honest (through preemptive restatement) increases when

investors perceive the court enforcement available to them is high.

In robustness tests, we first use simple model to show that the external validity of our results

should not be affected by unobservable misreporting firms. We next present evidence of a placebo

test which shows court dismissal rate only affects irregularity-based restatement but not error-

based accounting restatements. Finally, we show our results are robust to alternative court

stringency estimations.

This paper first contributes to the study on the role of courts in making laws credible. Prior

accounting and finance research tends to assume that laws are enforced with full strength and

therefore the cross-country (state) difference is whether having particular laws “on paper”. For

example, many work use staggered adoption of anti-takeover (Business Combination) laws by U.S.

states as shocks to corporate governance (Garvey and Hanka, 1999; Bertrand and Mullainathan,

2003; Wald and Long, 2007; Atanassov, 2013). Unlike these studies, we emphasize on the role of

courts as law enforcers, and the resultant variation in litigation risk across firms. In law and

economics literature, court and judge tendencies are used to predict, for example, the effect of

incarceration on individual’s earnings prospect (Kling, 2006), patent rights protection on corporate

innovation (Galasso and Schankerman, 2015), and bankruptcy laws on personal lending behaviors

(Dobbie, Goldsmith-Pinkham, and Yang, 2016), etc. We extend this approach to examine the

effect of court stringency on firms’ restatement policy.

We also contribute to the debate on litigation-disclosure nexus, using novel, court-based

evidence. The important question “why firms voluntarily disclose bad news?” was asked in earlier

important work including Skinner (1994, 1997), Kothari, Shu, and Wysocki (2009), Rogers and

Buskirk (2009), Donelson et al. (2012), etc. The consensus is that securities litigation risk is a key

determinant of such disclosure. However, due to the endogenous relationship between litigation

and disclosure, the empirical evidence is mixed. For example, Field, Lowry and Shu (2005)

employ a simultaneous equation methodology and find no evidence that earnings warnings trigger

litigation. Baginski, Hassell and Kimbrough (2002) compare U.S. and Canadian firms which they

argue are under “similar business environment but different litigation environments”. Their finding

that Canadian firms make more management forecasts than U.S. firms appear to support the

defensive disclosure hypotheses. On the contrary, Srinivasan, Wahid, and Yu (2015) find U.S.

listed firms headquartered in weak rule-of-law countries are less likely to restate than firms from

strong rule-of-law countries despite higher earnings management levels, and their interpretation is

that home country enforcement affects firms’ likelihood of admitting accounting mistakes. Our

result supports the preemptive disclosure hypothesis (Skinner 1994, 1997) and findings of

Srinivasan, Wahid, and Yu (2015), however our design based on variations of the within-country

court enforcement of 10b-5 lawsuits across districts and over the time is novel, and enables more

powerful tests.

Finally, we contribute to the restatement literature by providing much needed evidence on

misreporting firms’ restatement policy. Prior works in accounting use restatements to infer the

magnitude of financial misreporting, because they are readily observable. However, we show there

are many misreporting firms opportunistically choose not to restate. The systematic under-

correction of misreporting lowers investors’ confidence in the market. One novelty of this paper

is our employment of different methods (using ex post evidence) to identify the counterfactual

firms. More importantly, we show evidence that in more stringent courts misreporting firms tend

to make more restatements, and firms increases their restatement propensity following exogenous

increase in court stringency. The policy implication of this finding is that courts can ex ante enforce

misreporting firms to admit their mistakes by tightening their stringency in securities lawsuits.

The rest of this paper proceeds as follows: Section 2 describes the institutional setup relevant

to our analysis. Section 3 presents sample selection, data and descriptive statistics. Section 4

presents empirical results. Section 5 presents robustness tests. Section 6 concludes.

2. Securities Lawsuits and U.S. Federal Courts

2.1. The Evolution of Securities Class Action Lawsuits

In the U.S. securities law, the SEC Rule 10b-5 is one of the most important rules targeting

securities fraud. The rule prohibits any fraud or deceit in connection with the purchase or sale of

any security. The plaintiff under this rule are typically shareholders, and the defendants include

the firm and any person involved in the fraudulent activity. The shareholder class action concept,

which emerged in 1960s, was made applicable to securities cases by the “fraud-on-the-market”

presumption of reliance.9 The lighter requirement causes both meritorious and frivolous securities

litigations brought on behalf of thousands of investors. To regulate private enforcements the U.S.

Congress enacted the Private Securities Litigation Reform Act (PSLRA) in 1995.

Prior to the PSLRA, plaintiffs could proceed with minimal evidence of fraud and then use

pretrial discovery to seek further proof. Defending against these suits could prove extremely costly,

and defendant firms often found it cheaper to settle than fight to win the case, inducing more

frivolous lawsuits. The PSLRA heightened the pleading standards in three important ways: First,

it requires plaintiff to identify with specificity each misleading statement and why it is

misleading.10 Second, it requires a plaintiff to prove that the defendant acted with the “required

state of mind” (“Scienter”), which typically include fraudulent intent, actual knowledge or

recklessness.11 This evidence is hard to obtain, especially because the Exchange Act 21D(b)(3)(B)

prevents plaintiffs to obtain ‘discovery’ from the defendant unless and until the defendant’s motion

to dismiss is denied by the court. Finally, the PSLRA provides a “safe harbor rule” that frees

companies’ forward-looking disclosures from lawsuits so long as the disclosure is accompanied

by cautionary language or made without actual knowledge of falsity.

Because of these heightened pleading standard, securities class actions in the late 1990s and

2000s shift to hard evidence of fraud such as GAAP related accounting misstatements (Choi,

9 In the U.S. Supreme Court decision in Basic v. Levinson (1988), it was held: “It has been noted that ‘it is hard to

imagine that there ever is a buyer or seller who does not rely on market integrity. Who would knowingly roll the dice

in a crooked crap game?’…An investor who buys or sells stock at the price set by the market does so in reliance on

the integrity of that price. […] Because most publicly available information is reflected in market price, an investor’s

reliance on any public material misrepresentations, therefore, may be presumed for purposes of a rule 10b-5 action”.

See Basic, Inc. v. Levinson 485 U.S. 224 (1988). 10 In alleging misleading statement under the PSLRA, the plaintiff must state “each statement alleged to have been

misleading, reasons why the statement is misleading, and if an allegation regarding the statement or omission is made

on information and belief, the complaint shall state with particularity all facts on which that belief is formed” See, 15

U.S.C. § 78u-4(b)(1). 11 In alleging scienter under the PSLRA, the plaintiff must, “with respect to each act or omission alleged to violate

this chapter, state with particularity facts giving rise to a strong inference that the defendant acted with the required

state of mind.” (15 U.S.C. § 78u-4(b)(2)). See also the decision in Ernst & Ernst v. Hochfelder (1976) and Tellabs Inc.

v. Makor Issues & Rights Ltd. (2007).

Nelson and Pritchard, 2009). In this paper we use 10b-5 lawsuits from 2000 to 2014 which covers

the post-PSLRA period.

2.2. The Securities Class Action Procedures

A typical securities class action involves four stages. In the first stage, a plaintiff files a lawsuit

and asks to be the lead plaintiff. A 60-day clock for any individual or entity to file paperwork with

the court asking to be the lead plaintiff is triggered when the first securities lawsuit is announced.

After the deadline, the court reviews all pleadings and appoint the lead plaintiff and lead counsel.

In the second stage, plaintiffs’ counsel files their amended consolidated complaint, and the

defendants then have a deadline to file their motion to dismiss. A motion to dismiss is essentially

an argument by the defendants that, even if all facts alleged in the complaint were true, they are

insufficient to give rise to liability under SEC Rule 10b-5. The court then decides, based on both

plaintiff’s complaints and defendant’s motions, whether to uphold plaintiff’s Rule 10b-5 claim. If

yes, the court enters an order denying defendant’s motion to dismiss, which then gives class

plaintiffs the right to obtain “discovery” from the defendant. This is the pivotal stage in securities

lawsuits, for the costs of litigation increases substantially if the plaintiffs claim is not dismissed by

court. Because almost all cases end up either dismissed or settled, prior work uses “passing the

motion to dismiss” as proxy for “plaintiff win” (Choi, 2007; Choi, Nelson, and Pritchard, 2009;

Dyck, Morse, and Zingales, 2010).

If plaintiff survives the motion to dismiss then it enters the third stage of discovery. Discovery

typically involves requests for document production, admissions, and depositions of officers,

employees, experts and third parties. Once completed, plaintiff must seek class certification under

Rule 23 of the Federal Rules of Civil Procedure. If granted by court, the case officially becomes a

securities class action. At this point, defendants can face great liability if the case goes to trial and

the often likely outcome is a settlement.

In the final stage, the plaintiff and defendant’s attorney often negotiate a settlement. The

settlement must seek court’s preliminary and final approval. Once approved, the claims

administrator takes over to receive the settlement fund, sends out court approved notices to the

investor class, receive and process the claims and distributes the settlement funds. The whole

process takes a typical 3-4 years to complete.

2.3. Federal Courts and Splits in Pleading Standards

In the U.S., federal courts are given exclusive jurisdiction to hear 10b-5 related securities

lawsuits.12 There are 94 district courts (5 outside the main territory), 13 circuit (appellate) courts,

and one supreme court throughout the country. Each district court has geographical jurisdiction

over a number of counties.13 All federal judges are appointed by the President and approved by

the Senate to have lifetime tenure. Each district court has at least one judge, with some busy

districts such as Southern District of New York and Central District of California each has 28

judges.

The assignment of cases to federal judges is made on a rotational or, more often, random basis

(Bird, 1975; Galasso and Schankerman, 2015).14 Appeals against district court rulings are brought

to its upper circuit court. There are twelve circuit courts dividing the country into different

12 See Section 27 of the 1934 Securities Exchange Act. 13 For geographical jurisdiction of federal district courts, see PACER: https://www.pacer.gov/psco/cgi-bin/county.pl. 14 Though there might be a need to assign more specialized and complex cases to more experienced judge, “to

implement a program that would attempt to assign cases according to the relative abilities of the judges in a district is

understandably unpopular” (Bird, 1975, pp. 483). Moreover, many courts see a danger in fostering judge specialization,

because if certain judges in a district become experts to whom cases in particular areas of the law always would be

assigned, it deprives other judges of the opportunity, provided by random selection, to gain expertise in that legal area.

See Bird (1975).

regions15. The California-based 9th circuit court, for example, has 29 appellate judges, overseeing

13 district courts, and covers 20% of American population. Circuit courts in the U.S. are influential

law-makers for their ability to set legal precedent in their jurisdiction with minimal supervision by

the supreme court. This is particularly the case for securities lawsuits: On average, securities cases

make up less than 1% of Supreme Court’s docket, or about 1.5 cases per year, making circuit courts

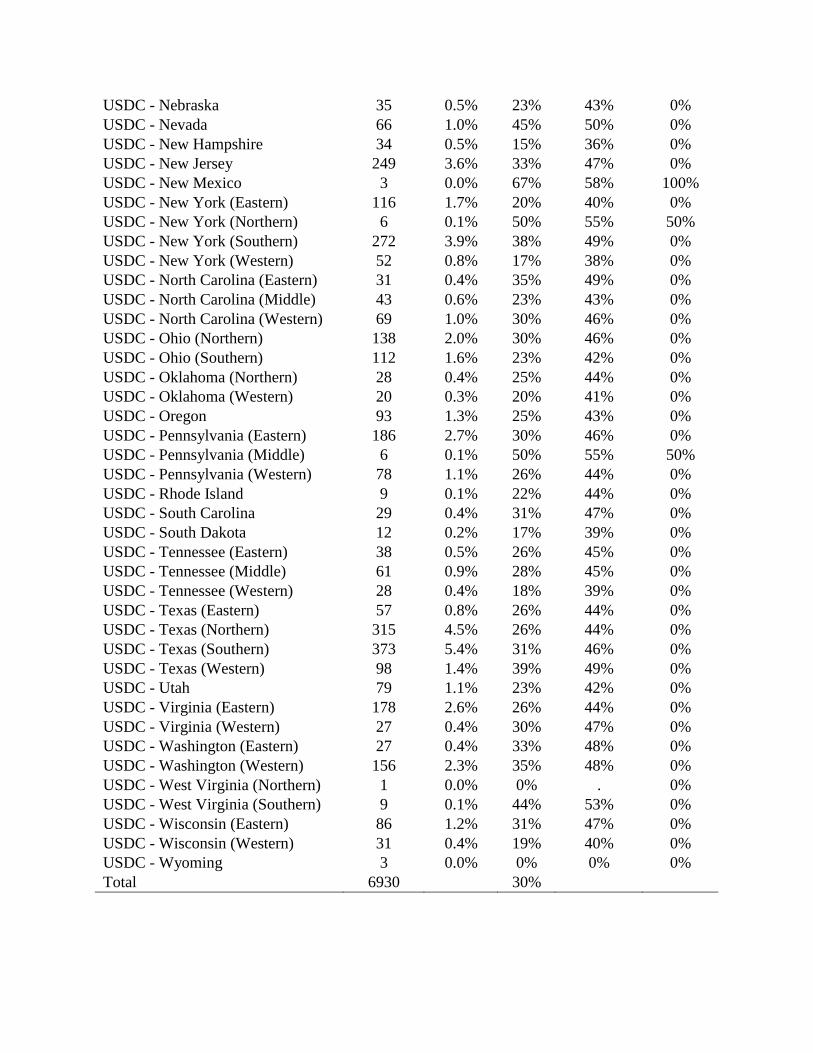

the de facto final arbiter (Pritchard, 2011). Appendix B visualizes the geographical jurisdiction of

federal district courts and their corresponding circuit courts. Colors and numbers show their

average dismissal rate and standard deviation over our sample period.

Attorneys, commentators and scholars have long recognized the split in stringency among

circuit courts in securities lawsuits. The split centers on the pleading standard of Scienter, a core

legal element to plead a 10b-5 claim.16 The element of Scienter requires plaintiffs to “state with

particularity facts giving rise to a strong inference that the defendant acted with the required state

of mind.” 17 It is well known that hard evidence of Scienter is difficult to obtain prior to discovery,

and in practice whether plaintiff’s evidence can satisfy Scienter depends largely on the “strong

inference” standard of the relevant court.

On the split in strong inference standard, Choi and Pritchard (2012) divide circuit courts into

three groups (explained next when we discuss Tellabs case): The 1st, 4th, 6th, and 9th circuits

adopted a “preponderance” standard which is pro-defendant firms (of which the 9th Circuit is

probably an extreme); the 2nd, 8th, 10th and 11th circuits adopted an “equal inference” standard

positioned in the middle; the 3rd and 7th circuits adopted a “reasonable person’s” standard which is

15 The thirteenth court of appeals is the United States Court of Appeals for the Federal Circuit, which has nationwide

jurisdiction over certain appeals based on their subject matter. 16 Legal elements to plead a 10b-5 action include evidences supporting plaintiffs’ claims for: (1) materiality; (2)

misrepresentation or omission; (3) scienter; (4) reliance; (5) causation; and (6) damages. See relevant statutory sections,

case law and analysis in Choi and Pritchard (2015). 17 See Exchange Act § 21D(b)(2), 15 U.S.C. 78u-4(b)(2).

pro-plaintiffs.18 To the extent that district court judges make decisions under the prospect of

appellate court scrutiny, the pleading standards adopted by each circuit court exhibit substantial

influence over its underling district courts.

3. Sample and Data

3.1. Data and Sample Distribution

We purchased the Securities Class Action Services (SCAS) database from RiskMetrics’

Institutional Shareholder Services (ISS) to identify all securities lawsuits filed in federal courts.

The SCAS offers detailed portfolio views of securities lawsuits including plaintiffs, defendants,

court, allegations, class periods, claim deadline dates, claims administrator details and pertinent

related data since 1982. This database is known for precision19 and used by Cheng et al. (2010)

and Donelson et al. (2012). Owing to the need to construct court dismissal rate in the post-PSLRA

period, we include lawsuits filed against public companies in NYSE, ASE, or NASDAQ with

alleged Rule 10b-5 violation from 2001 to 2014. The restatement data come from Audit Analytics

(AA). For restatement identification, we exclude firms labelled in AA as “Res Clerical Errors”

since we are interested in restatements that involve (intentional) accounting irregularities. All

financial statement variables are from Compustat, and the stock trading data come from CRSP.

Our objective is to identify a group of firms that made accounting mistakes, some are upfront

with restatements and others keep strategic silence. In practice, whether or not a firm has

18 See Choi and Pritchard (2012, pp. 853-854), citing representative Circuit Court decisions. These standards are

illustrated further in section 4.3 the discussion of Tellabs case. 19 One other (free) database popular for securities class action lawsuit study is the Stanford Law School Securities

Class Action Clearinghouse (SCAC) database. However, as Karpoff et al. (2017) observe, the filing date on the SCAC

database postdates the time at which investors first learn of the purported misconduct that triggers the litigation by an

average of 150 calendar days. For accuracy we purchase the commercial database whose primary purpose is to assist

institutional investors that have a claim in securities lawsuits.

misreported earnings can only be identified through evidences ex post such as firms’ own

restatements, the SEC sanctions, or court trial outcomes. As the SEC is resource constrained, and

most securities litigations end up with settlements rather than trial, this paper employs the

following methods to identify misreporting firms.

Sample 1: 10b-5 defendant firms with alleged GAAP violations

The first sample of misreporting firms (hereafter “sample 1”) is identified using ex post

evidence from securities lawsuits. These firms are caught by shareholders in securities lawsuits,

sued for fraud under SEC rule 10b-5, and in particular, they are alleged of GAAP violations in

plaintiff’s claims. Some of these defendant firms made restatement before the lawsuit, others did

not. Table 1 summarizes our screening process, and below is a step-by-step illustration.

We start with 3,375 securities class action lawsuits with federal filing date between December

31, 2000 to December 31, 2013 in the SCAS database. Merging the lawsuit cases with Compustat

data by ticker or company name, we obtain 1,953 consolidated lawsuits.

In practice, plaintiffs’ counsel can raise multiple allegations under 10b-5 antifraud liability

such as GAAP violations, misrepresentations regarding the business, failure to warn, and

misleading forward-looking statements. Given our focus on GAAP-based financial misstatements,

we exclude cases with only non-accounting allegations, leaving the sample to 1,298.

We next eliminate observations without valid control variables in our tests, and obtain a final

sample comprising 649 lawsuits from 2000 to 2013, among which in 183 cases the defendant firms

made pre-lawsuit restatements, and in 466 cases the defendant firms did not make restatement

before lawsuits. Table 4, Panel A divides our sample 1 lawsuits by their headquartering district

courts, and Panel D reports their yearly distribution.

Sample 2: 10b-5 defendant firms with restatements

The second sample of misreporting firms (hereafter “sample 2”) relies on firms’ own

restatement before and after the lawsuit. Unlike sample 1, in sample 2, counterfactual firms are the

10b-5 defendant firms that made corresponding restatement within the five years after case filing

date. Firms’ own and eventual restatements offers direct evidence that they should have, but did

not make restatement before the lawsuits.

We start with sample 1 and take out the 466 counterfactual firms. Then, we restrict the

counterfactual firms to be the ones that make a restatement within five years after case filing date.

We carefully check to make sure each eventual restatement matches the class period in the 10b-5

lawsuit with alleged GAAP violation. This exercise eliminates the counterfactual firms to 99

observations. Finally, to best match the counterfactual firms with restating firms in the same class-

end year and industry, we select restating firms from sample 1 with the 99 counterfactual firms by

year and industry, which eliminates 59 restating firms. Our final sample 2 consists of 124 restating

firms and 99 counterfactual firms. Table 2 summarizes the screening process for sample 2. Table

4, Panel B displays the distribution of sample 2 by district courts, and Panel D reports their yearly

distribution.

Sample 3: High Earnings Management Firms

Solely relying on securities lawsuits to identify misreporting firms can be problematic, for

not all misreporting were detected by shareholders. Therefore, our third sample of misreporting

firms (hereafter “sample 3”) is identified using the discretionary accrual level of restating and non-

restating firms.

First, we restrict our sample to 101,029 Compustat firm-years with valid discretionary

accruals calculated from Modified Jones Model (Dechow, Sloan, and Sweeney, 1995) with fiscal

year end from January 1, 2001 to December 31, 2014. Among these observations, 7,842 are firms

that restated their financials in the following year. We then obtain the 90th percentile and 10th

percentile discretionary accruals of the restating firms categorized by year and SIC 2-digit industry

code, and match the restating firms with non-restating firms that have discretionary accrual either

higher than the 90th percentile, or lower than the 10th percentile discretionary accruals of the

restating firms in the same industry and year. This selects 25,871 non-restating misreporting firm-

years. Finally, we match the restating and non-restating misreporting firms with SCAS, CRSP and

Compustat variables in later tests, and obtain a sample of 6,930 observations from January 1, 2001

to December 31, 2014, with 2,106 restating firm-years and 4,824 non-restating firm-years. Table

3 summarizes the sampling process for sample 3. Table 4, Panel C reports the distribution of

sample 3 by district courts, and Panel D reports yearly distribution.

Several notes on the rationale behind each sample are in order: Among the three samples,

sample 2 based on defendant firm’s own restatements has the most accurate counterfactual group.

However, the size of sample 2 is small so that we may sacrifice external validity for internal

validity. Sample 1 based 10b-5 defendant firms with alleged GAAP violation has the “second best”

counterfactual group, and it has larger sample size. Sample 1 thus draws a reasonable balance

between internal and external validity. Sample 3 based on firms’ earnings management level has

the largest sample size yet the least accurate counterfactual group, for high earnings management

level can be correlated with, but not hard evidence of misreporting. In this paper, we report results

using each constructed sample of misreporting firms, with an objective to provide validation of

evidence that achieve both internal and external validity.

3.2. Explanatory Variables and Descriptive Statistics

Our key explanatory variable is court dismissal rate, defined by the number of securities cases

dismissed within five years prior to a firm’s fiscal year end in the federal district court where the

firm is headquartered, divided by total such cases filed in the same period in the same court:

𝑑𝑖𝑠𝑚𝑖𝑠𝑠𝑎𝑙𝑖,𝑡 =𝑛𝑜_𝑑𝑖𝑠𝑚𝑖𝑠𝑠𝑎𝑙𝑖,𝑡

𝑛𝑜_𝑓𝑖𝑙𝑖𝑛𝑔𝑠𝑖,𝑡

(1)

where, 𝑛𝑜_𝑑𝑖𝑠𝑚𝑖𝑠𝑠𝑎𝑙𝑖,𝑡 is the number of cases dismissed within the five years prior to the end of

fiscal year 𝑡 of firm 𝑖 handled by the district court where firm 𝑖 is headquartered; and

𝑛𝑜_𝑓𝑖𝑙𝑖𝑛𝑔𝑠𝑖,𝑡 is the number of cases filed within the five years prior to the end of fiscal year 𝑡 of

firm 𝑖 handled by the district court where firm 𝑖 is headquartering.

Note that it may take several years for a case to have any sort of resolution, while other cases

may be dismissed much faster. Therefore, cases dismissed within five years may not exactly

correspond to cases filed during the same period. However, to account for the fact that different

district courts have very different number of firms and lawsuit filings, we believe this scaling

method is reasonable. In the robustness tests, we provide results using alternative estimation of

court dismissal rate which takes into account the lag between case filing and dismissal dates.

One key assumption, that the 10b-5 securities lawsuits are typically heard by the district court

that the defendant firm is headquartered, requires elaboration and validation. In the U.S., though

technically a securities lawsuit can be filed in the court of any federal district where the defendant

firm has place of business, multiple filings need to be consolidated in one case typically heard by

the district court where the defendant firm is headquartered. Two statutory provisions: 28 U.S.C.

§ 1404(a) and 1406(a) provided legal basis for this claim. Section 1404(a) protects parties and

witnesses from an undue expenditure of time and money. Because of the nature of claims in private

securities lawsuits, substantially all of the witnesses and sources of proof are likely to be located

at the firm’s headquarters. Section 1406(a) allows for transfer of a case that has been brought in

an improper forum. Plaintiffs who file suit outside of the federal district of the firm’s headquarter

are highly vulnerable to either dismissal based on the well-established doctrine of forum non

conveniences or transfer to the district court of the defendant firm’s headquarter. Cox, Thomas,

and Bai (2009) report their interview with well-known plaintiffs’ counsels who consistently

reflected that it is impractical for them to engage in forum shopping due to the strong likelihood

that their choice of a venue other than the defendant firm’s principal place of business will be

immediately followed by a successful defendant’s motion to relocate the suit. Hence, rather than

engaging in in futile act, they file suit initially in the defendant company’s home district court.

We verify this assumption using lawsuit and court data between December 31, 2000 to

December 31, 2013. Within the 1,836 cases that have valid federal court filing from SCAS and

headquarter address from Compustat, 67.3%, or over two thirds, are consolidated at and heard by

the defendant firms’ headquartering district court, providing validity to our assumptions.

Our controls of firm characteristics follow the litigation risk and restatement literature. We

first include the natural logarithm of total assets, leverage ratio, and book-to-market ratio.

Following work on restatements (Files, Swanson, and Tse, 2009; Srinivasan, Wahid, and Yu, 2015)

we take ROA, sales growth and last year stock return as control variables for firm performance.

We further control the stock trading activities by including previous-year stock return volatility,

market risk factor loading (beta), stock turnover, and stock return skewness (Kim and Skinner,

2012). Finally, to control for the strength of governance and monitoring system we include whether

a firm’s auditor is a Big 4 auditor (Srinivasan, Wahid, and Yu, 2015). All variables are defined in

Appendix A, and winsorized at 1% level except for restating dummy and court dismissal rate.

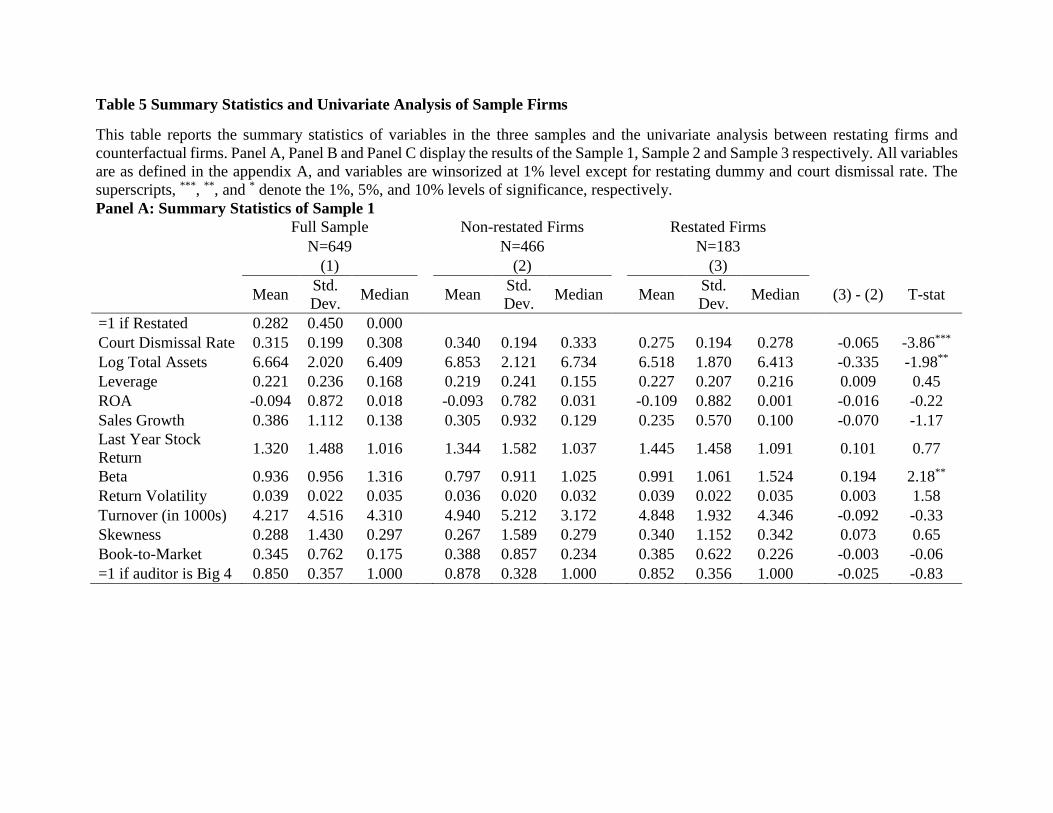

Table 5, Panel A, B and C summarizes the descriptive statistics of variables in our sample 1,

2 and 3, respectively, and compares characters of restated and non-restated firms in each sample.

For sample 1, the average court dismissal rate is 31.5%. Mean log total assets (firm size) is

6.66, leverage 22.1% of total assets, and book-to-market ratio at 0.345. The average ROA is -9.4%

of total assets, and sales growth rate at 38.6%. Average daily return volatility is 3.9%, skewness

0.288, and annual turnover at 4.22 million. 85.0% of the firms are audited by the Big 4 auditor

firms. Comparing the restated firms with non-restated firms in sample 1, we find that restated firms

have significantly lower court dismissal rate, smaller firm size and marginally lower sales growth,

and other characteristics are almost similar. This lends us confidence that our non-restated firms

are a good match for restated firms.

For sample 2, the average dismissal rate is 33.5%. Mean log total assets (firm size) is 6.74,

leverage 23.5% of total assets, and book-to-market ratio at 0.55. The average ROA is -8.8% of

total assets, and sales growth rate at 22.7%. Average daily return volatility is 3.7%, skewness 0.351,

and annual turnover at 4.18 million. 87.0% of the firms are audited by the Big 4 auditor firms.

Compared with firms in sample 1, firms in sample 2 have higher accounting returns but lower

growth. Comparing the restated firms and non-restated firms in sample 2, we find that restated

firms have lower court dismissal rate, smaller firm size, lower leverage, higher beta and marginally

lower sales growth.

For sample 3, the average dismissal rate is 38.8%. Mean log total assets (firm size) is 5.98,

leverage 23.0% of total assets, and book-to-market ratio at 0.73. The average ROA is -5.8% of

total assets, and sales growth rate at 13.4%. Average daily return volatility is 3.7%, skewness 0.456,

and annual turnover at 2.10 million. 80.5% of the firms are audited by the Big 4 auditor firms.

Compared with firms in sample 1 and sample 2, firms in sample 3 have even higher accounting

returns but lower growth, smaller size and lower stock turnover. Comparing the restated firms and

non-restated firms in sample 3, we find that restated firms have larger firm size, higher leverage,

lower ROA, lower sales growth, higher last-year stock return, higher beta, lower return volatility

and higher likelihood to be audited by Big 4. As expected, the difference between restated firms

and non-restated firms in sample 3 is distinct from sample 1 and sample 2, due to the difference in

sampling method and a weaker internal validity.

From the univariate analysis of sample 1, 2 and 3, we could find that beta is the most

significant characteristic that distinguish between the restated firms and counterfactual firms, and

court dismissal rate and size may also distinguish these two types of firms.

4. Empirical Results

4.1. Baseline Model

To test the predictive power of prior court dismissal rate on misreporting firms’ propensity to

make restatement in the following year, we propose the following probit model:

𝑅𝑒𝑠𝑡𝑎𝑡𝑖𝑛𝑔𝑖,𝑡+1

= 𝛽0 + 𝛽1𝑑𝑖𝑠𝑚𝑖𝑠𝑠𝑎𝑙𝑖,𝑡 + 𝛽2𝑙𝑒𝑣𝑖,𝑡 + 𝛽3𝑙𝑛𝑎𝑡𝑖,𝑡 + 𝛽4𝑟𝑒𝑡𝑢𝑟𝑛𝑖,𝑡

+ 𝛽5𝑅𝑂𝐴𝑖,𝑡 + 𝛽6𝑠𝑎𝑙𝑒𝑠𝑔𝑟𝑡ℎ𝑖,𝑡 + 𝛽7𝑠𝑡𝑑𝑖,𝑡 + 𝛽8𝑡𝑢𝑟𝑛𝑜𝑣𝑒𝑟𝑖,𝑡

+ 𝛽9𝑠𝑘𝑒𝑤𝑛𝑒𝑠𝑠𝑖,𝑡 + 𝛽10𝐵𝑖𝑔4𝑖,𝑡 + 𝛽11𝑏𝑡𝑚𝑖,𝑡 + 𝛽12𝑏𝑒𝑡𝑎𝑖,𝑡 + 𝜀𝑖,𝑡

(2)

where, 𝑅𝑒𝑠𝑡𝑎𝑡𝑖𝑛𝑔𝑡+1 is an indicator variable that takes 1 if the firm restates in fiscal year t+120;

𝑑𝑖𝑠𝑚𝑖𝑠𝑠𝑎𝑙𝑡 is the court dismissal rate for the headquartering firm; 𝑙𝑒𝑣𝑡 is the book leverage at the

end of fiscal year t; 𝑙𝑛𝑎𝑡𝑡 is the natural logarithm of total assets at the end of fiscal year t; 𝑟𝑒𝑡𝑢𝑟𝑛𝑡

is the annual total return over fiscal year t; 𝑅𝑂𝐴𝑡 is the return on total assets in the fiscal year t;

𝑠𝑎𝑙𝑒𝑠𝑔𝑟𝑡ℎ𝑡 is sales growth from fiscal year t-1 to t; 𝑠𝑡𝑑𝑡 is the daily return volatility over fiscal

year t; 𝑡𝑢𝑟𝑛𝑜𝑣𝑒𝑟𝑡 is the turnover over fiscal year t; 𝑠𝑘𝑒𝑤𝑛𝑒𝑠𝑠𝑡 is the return skewness over fiscal

year t; 𝐵𝑖𝑔4𝑡 is an indicator variable that takes 1 if the firm has a Big 4 auditor firm as its auditor;

𝑏𝑡𝑚𝑡 is the book-to-market ratio at the end of fiscal year t; and 𝑏𝑒𝑡𝑎𝑡 is the market risk factor

loading from CAPM model, estimated from the monthly stock returns of the 5-year period before

the most recent fiscal year end. We control for the state fixed effects because some states have

more than one district court and we need to disentangle the effect of court stringency from the

unobservable state level economic, social and political effects. We also control for industry fixed

effects and year fixed effects.

Table 6 reports the impact of court dismissal rate on the likelihood of firm issuing restatement

conditioning on that they committed accounting mistakes using sample 1 (Column 1), sample 2

(Column 2) and sample 3 (Column 3). Industry fixed effects, year fixed effects and state fixed

effects are included in all of the three regressions. The industry and year fixed effects filter out

time-varying and industry-level shocks that may affect the restatement decision, and the state fixed

effect controlled for state-wide differences in business and regulatory environment.

20 Note that for the counterfactual firms in sample 1 and sample 2, we take their class-end date as the hypothetical

restating date and the latest fiscal year up to the class-end date as fiscal year t in equation 2, since the restating firms

and counterfactual firms are matched by lawsuit and class-end year in these two samples. However, as the restating

firms and counterfactual firms in sample 3 are matched by discretionary accrual level, industry and fiscal year, we

directly take their fiscal year as fiscal year t in equation 2.

We find court dismissal rate exhibits a large negative impact on the likelihood of misreporting

firm issuing restatement (p=0.0256, 0.0207 and 0.0648 for the regressions with sample 1, 2 and 3,

respectively). Remarkably, court dismissal rate is the only variable that has both statistical

significance and large consistent economic magnitude among the regressions with three samples:

Column 1, Column 2 and Column 3 shows one standard deviation increase in court dismissal rate

(lowered district litigation risk) leads to 4.89%, 6.87% and 1.53% reduction in restatement

propensity, holding constant all controls and fixed effects, compared to an average restating rate

of 28.2%, 55.6% and 30.4% for the three samples, respectively. The one standard deviation

increase in dismissal rate amounts to increase that from the level of Illinois (Northern) to that of

California (Northern) district court.

Stock returns, ROA, Sales growth, Beta, Turnover, and Book-to-Market all exhibit either

insignificant effect on restatement before lawsuits or significant but contradict effects among

samples. Surprisingly, having a big 4 auditor has little impact on restatement propensity, probably

because auditors are concerned about their own legal and reputational penalties when their audited

firm made accounting mistakes (Seetharaman, Gul, and Lynn, 2002; Hope and Langli, 2010). In

sum, our baseline model analysis supports the preemptive disclosure hypothesis.

4.2. Instrumental Variable Analysis Using the Tellabs Case

To validate our proposition that firms’ restatement propensity is driven by court stringency, we

exploit the landmark case of Tellabs, Inc v. Makor Issues & Rights, Ltd. The case was originally

dismissed by the district court of Northern Illinois, reversed by the 7th circuit court upon appeal21,

further appealed to the supreme court which granted certiorati22, and finally judge Posner of the

21 See 437 F.3d 588, 602 (7th Cir. 2006) 22 See Tellabs, Inc. v. Makor Issues & Rights, Ltd. 551 U.S. 308 (2007).

7th circuit court rendered final ruling following supreme court’s clarified pleading standard.23 We

choose Tellabs because it is one of the supreme court’s first efforts to clarify the key legal element

in 10b-5 lawsuits: the strong inference standard for pleading Scienter.

Prior to Tellabs, different court of appeals followed their own approach in interpreting the

strong inference standards, and monitor by the supreme court is close to nonexistent (Westerland

et al., 2010). To illustrate, the “preponderance” standard adopted by the 1st, 4th, 6th, and 9th

circuit is most favorable to defendant. It requires the inference that the defendants had the requisite

Scienter (fraudulent intent or recklessness) to be the most plausible when compared with

competing inference of “No Scienter”. In the middle, the “equal inference” standard adopted by

the 2nd, 8th, 10th and 11th circuit required at least a “tie” of competing inference of Scienter and

No Scienter. Lastly, the “reasonable person” standard adopted by the 3rd and 7th circuits is most

favorable to plaintiffs. It only requires the court to look at the plausibility of the plaintiff’s

allegations, without requiring any assessment of competing inferences (Choi and Pritchard, 2012).

Importantly, the supreme court’s ruling on Tellabs in 2007 clarifies what is required for the

plaintiff to plead Scienter. In the supreme court’s certiorari, it addressed if there is a tie of

competing evidence showing the inference of fraudulent intent is at least as likely as an innocent

one, the ties go to the plaintiff. 24 This stance of the supreme court mimics the middle, “equal

inference” standard adopted by the 2nd, 8th, 10th and 11th circuit, which is more stringent than

the “preponderance” standard adopted by the 1st, 4th, 6th, and 9th circuit, and less stringent than

the “reasonable person” standard adopted by the 3rd and 7th circuit. To the extent that lower courts

make decisions anticipating upper court’s tendency and risk of reversal (Gulati, Choi and Posner,

23 See Makor Issues & Rights, Ltd. v. Tellabs, Inc., F.3d, No. 04-1687, 2008 WL 151180 (7th Cir. Jan. 17, 2008). 24 Specifically, Justice Ginsburg, writing for the Tellabs majority, held: “A complaint will survive, we hold, only if a

reasonable person would deem the inference of scienter cogent and at least as compelling as any opposing inference

on could draw from the facts alleged.” see Tellabs, Inc. v. Makor Issues & Rights, Ltd. 551 U.S. 308 (2007), at 324.

2012; Choi, Gulati, and Posner, 2016), the effect of Tellabs is that it homogenizes what is required

for plaintiffs to establish scienter across all circuits. Specifically, we hypothesize that the Tellabs

decision exogenously increase the pleading standard of federal courts that previously adopted a

“pro-defendant” standard of scienter, and perhaps decrease that of the federal courts that

previously adopted a “pro-plaintiff” standard of scienter.

We exploit this homogenizing effect into a two-stage, instrumental variable test. Our

instrumental variable is the relative stringency of district courts in the pre-Tellabs period. In the

first stage, following Choi and Pritchard (2011), we categorize district courts under the 1st, 4th,

6th, and 9th circuit as “pre-event low” stringency courts, and those under the 3rd and 7th circuit

as “pre-event high” stringency courts. If the homogenizing effect exists, then we expect to see a

decrease (increase) of dismissal rate in “pre-event low (high)” stringency courts in the post-

Tellabs period. In the second stage, we explore the impact of the (instrumented) change in court

dismissal on the change in restatement propensity for misreporting firms headquartered in the

relevant district courts.

Several notes on this instrumental variable design are in order: First, we believe this instrument

satisfies the conditions of both relevance and exclusion restriction. District court’s pre-event

stringency should be correlated with the homogenizing shock of Tellabs decision. It is also unlikely

that this dummy variable should have direct effect on the change of firms’ restatement policy upon

the ruling by supreme court, other than through the channel of changes in district court stringency.

Second, on the methodology, to balance internal validity and sample size, we choose our sample

1 misreporting firms as the testing sample in our two stage test. We choose two relative long event

window, the 6-year window (3-year pre- and post-Tellabs) and the 10-year window (5-year pre-

and post-Tellabs), taking into account the fact that it takes time for managers of the misreporting

firms to know about their accounting mistakes and to deliberate on their restatement decision in

response to altered pleading standard.25 Third, as the Tellabs decision spans 2006 through 2007,

these two years are excluded from our event window. Therefore, our pre-event period for the 6-

year window is from January 2003 to December 2005; the post-event period for the 6-year window

is from January 2008 to December 2010; the pre-event period for the 10-year window is from

January 2001 to December 2005; and the post-event period for the 10-year window is from January

2008 to December 2012.

Table 7 reports the results. In the first stage test (Column 1 and 3), the pre-event low stringency

dummy is negatively associated with changes in dismissal rate following Tellabs for both event

windows (p=0.0984 and 0.0338, respectively), confirming our assumption that the supreme court’s

Tellabs decision prompts low-stringency courts to increase stringency (decrease dismissal rate) in

post-Tellabs period. On the other hand, we do not find a symmetric increase in dismissal rate in

pre-event high stringency courts (the coefficient is insignificantly negative). This result is not

surprising26, and finds perfect match with Choi and Pritchard (2011), who find Tellabs correlates

with a significantly lower dismissal rate on Scienter grounds in circuits previously applying a

higher “preponderance” standard, yet no significant shift in the courts previous applying the lower

“reasonableness” standard.

In the second stage, our instrumented change in court dismissal rate presents significantly

negative correlation with the change in restating rates for both event windows (p=0.0296 and

0.0013, respectively), suggesting that court dismissal rate has a negative impact on misreporting

25 For example, in our sample of misreporting firms, the mean and medium days for the time gap between misreporting

fiscal year and restatement date (or class end date) are 151 and 132 days respectively. 26 One can reasonably expect that the effect of intensified monitoring by the supreme court to have stronger effect on

the previously lax, rather than previously stringent underline courts.

firms’ propensity to make restatement. Taken together, evidence from Tellabs decision validates

and provides causal evidence supporting a preemptive disclosure hypothesis.

4.3. Court Stringency and Market Responses to Pre-emptive Restatements

So far we have shown that misreporting firms make timelier restatements when they face a

more stringent court. A natural question is whether such a restatement policy is “rational” in the

sense that there are gains in making pre-emptive restatements. To shed light on this query this

section studies the shareholder wealth effect of pre-emptive restatements in the presence of varying

district court stringency.

Our empirical strategy is to compare the market reaction around two key dates for our samples

of misreporting defendant firms. The first is the “class end date” which is the date when the truth

that “corrected” the stock price was first revealed to the market (Kellogg, 1984; Griffin, Grundfest,

and Perino, 2004; Gande and Lewis, 2009). For firms making pre-lawsuit restatement their class

end date is typically the same with their restatement date. For firms that did not make pre-lawsuit

restatement the class end date is their “deemed” restatement date, which we extract from the SCAS.

The second event date is the “case filing date”, which is the date when the first plaintiff filed the

lawsuit in a district court. We examine both event dates because the class end date was the first

time that market knows about the misreporting, and studies that only focus on filing date returns

tend to underestimate the true economic costs associated with securities lawsuits (Gande and Lewis,

2009).

Note this event study can only be conducted using our sample 1 and 2 of sued firms, where both

event dates are available. Merging the daily stock trading data from CRSP and the filing dates and

class-end dates from SCAS reduces our sample 1 misreporting firms to 520 observations and

sample 2 misreporting firms to 286 observations.

Table 8 employing standard event study methodology presents very interesting results. Column

(1) and (2) show the 5-day (-2, +2) cumulative abnormal return (CAR) around class-end date and

case-filing date on sample 1, and Column (3) and (4) on sample 2. We first find the correlation of

court dismissal rate and CAR is significantly positive on the class-end date but insignificantly

negative on the filing date. On the economic magnitude, one standard deviation increase in court

dismissal rate leads to a net gain of 0.7% and 1.2% in market value around the class-end date, but

a net loss of 0.2% and 0.1% around the case-filing date, for sample 1 and 2 respectively.

Cumulatively the effect of court dismissal rate on CAR is positive. This evidence is consistent

with investors anticipate more legal cost for firms headquartered in high litigation risk districts.

To the extent that the market anticipates and capitalizes expected loss (including legal cost) of

securities lawsuits, we then ask whether preemptive restatements help to save shareholder value.

Interestingly, we find firms’ honesty in making pre-emptive restatements appear not rewarded by

the market. Data show that in sample 1, restated firms suffer 3.1% more loss around the class-end

date and 3.4% more loss around the case-filing date than non-restated firms. In sample 2, restated

firms suffer 0.8% more loss around the class-end date and 4.1% more loss around the case-filing

date than non-restating firms. However, the cumulative CAR differences between restating and

non-restating firms are not statistically significant.

At first look, our result seems to suggest that managers are not making rational decisions by

timely admitting their accounting mistakes. However, by allowing the effect of restatement on

CAR to depend on defendant firm’s home court dismissal rate changes the picture. We find the

CAR difference between restated and non-restated firms becomes significantly negative with the

increase of court dismissal rate. One standard deviation increase in court dismissal rate leads to

6.3% and 8.8% more shareholder value loss for restated firms than non-restated firms around the

two dates in sample 1 (p=0.0514 and 0.0028 respectively), and 7.1% and 5.5% more shareholder

value loss for restated firms than non-restated firms around the two dates in sample 2 (p=0.0014

and 0.0041 respectively). A “mechanical” explanation of the result is that investors are more

surprised (thus react more negatively) to learn that firms under more stringent courts did not restate.

The other way to interpret this result is that, for misreporting firms in more stringent courts, making

preemptive restatement saves shareholder value. However, for misreporting firms in less stringent

courts, preemptive restatement harms shareholder value.

This interesting result can be rationalized under Akerlof’s (1970) adverse selection model. In

the absence of stringent courts, the expected legal penalty for misreporting is low, thus most

misreporting firms have incentive to hide their accounting mistakes. In a lemon’s market where

investors cannot differentiate honest and opportunistic firms, honest (restating) firms are penalized

more. However, in the presence of stringent courts, the expected legal penalty for misreporting is

high and credible, causing honest firms to be rewarded by the market.

Taken together, our evidence suggests the value of being honest (through pre-emptive

restatements) increases as court stringency increases. Upfront restatements pay off (in saving

shareholders value) when investors perceive the court enforcement available to them is high.

5. Robustness Check

5.1. The Effect of Unobservable Misreporting Firms

Most of our results come from sample 1 and 2, which rely on lawsuits to identify misreporting

firms. However, many misreporting firms are not eventually sued. In this subsection, we use

simple model to show that omitting those non-sued firms does not threat the external validity of

our results. In an ideal experimental environment, we would have

𝑅𝑒𝑠𝑡𝑎𝑡𝑖𝑛𝑔 𝑅𝑎𝑡𝑒 =#𝑠𝑟𝑠𝑡 + #𝑛𝑠𝑟𝑠𝑡

#𝑠𝑟𝑠𝑡 + #𝑛𝑠𝑟𝑠𝑡 + #𝑠𝑛𝑟𝑠𝑡 + #𝑛𝑠𝑛𝑟𝑠𝑡 (3)

where, #𝑠𝑟𝑠𝑡 is the number of sued and restating firms; #𝑛𝑠𝑟𝑠𝑡 is the number of non-sued but

restating firms; #𝑠𝑛𝑟𝑠𝑡 is the number of sued but non-restating misreporting firms; and #𝑛𝑠𝑛𝑟𝑠𝑡

is the number of non-sued and non-restating misreporting firms.

Now, in sample 1 and sample 2, we do not have the number of non-sued but restating firms and

the number of non-sued and non-restating misreporting firms. This leads to a biased measure of

restating rate:

𝑅𝑒𝑠𝑡𝑎𝑡𝑖𝑛𝑔 𝑅𝑎𝑡𝑒̂ =#𝑠𝑟𝑠𝑡

#𝑠𝑟𝑠𝑡 + #𝑠𝑛𝑟𝑠𝑡. (4)

The key determinants of how 𝑅𝑒𝑠𝑡𝑎𝑡𝑖𝑛𝑔 𝑅𝑎𝑡𝑒̂ biases are the correlation between the number

of non-sued but restating firms and court dismissal rate and the correlation between the number of

non-sued and non-restating misreporting firms and court dismissal rate. Ceteris paribus, if the

number of non-sued but restating firms and court dismissal rate are not correlated or negatively

correlated, we still have that restating rate in high-dismissal rate court is lower than restating rate

in low-dismissal rate court because putting the number of non-sued but restating firms on both the

numerator and denominator of the right-hand side of equation 4 increases the restating rate and the

original higher restating rate increases even higher mathematically:

#𝑠𝑟𝑠𝑡𝑙 + #𝑛𝑠𝑟𝑠𝑡𝑙

#𝑠𝑟𝑠𝑡𝑙 + #𝑠𝑛𝑟𝑠𝑡𝑙 + #𝑛𝑠𝑟𝑠𝑡𝑙>

#𝑠𝑟𝑠𝑡ℎ + #𝑛𝑠𝑟𝑠𝑡ℎ

#𝑠𝑟𝑠𝑡ℎ + #𝑠𝑛𝑟𝑠𝑡ℎ + #𝑛𝑠𝑟𝑠𝑡ℎ

𝑖𝑓 #𝑠𝑟𝑠𝑡𝑙

#𝑠𝑟𝑠𝑡𝑙 + #𝑠𝑛𝑟𝑠𝑡𝑙>

#𝑠𝑟𝑠𝑡ℎ

#𝑠𝑟𝑠𝑡ℎ + #𝑠𝑛𝑟𝑠𝑡ℎ 𝑎𝑛𝑑 #𝑛𝑠𝑟𝑠𝑡𝑙 ≥ #𝑛𝑠𝑟𝑠𝑡ℎ ,

where, the subscript 𝑙 denotes the low-dismissal rate court; and the subscript ℎ denotes the high-

dismissal rate court. This is supported by the disclosure literature (Field, Lowry and Shu, 2005)

that the preemptive disclosure is made to reduce the litigation risk and it is easier for companies to

avoid lawsuits in low-dismissal rate court than in high-dismissal rate court, which leads to the

negative correlation between the number of non-sued but restating firms and court dismissal rate.

Also, ceteris paribus, if the number of non-sued and non-restating misreporting firms and court

dismissal rate are not correlated or negatively correlated, we still have that restating rate in high-

dismissal rate court is lower than restating rate in low-dismissal rate court because putting the

number of non-sued and non-restating firms on both the numerator and denominator of the right-

hand side of equation 4 decreases the restating rate and the original higher restating rate is still

higher mathematically:

#𝑠𝑟𝑠𝑡𝑙

#𝑠𝑟𝑠𝑡𝑙 + #𝑠𝑛𝑟𝑠𝑡𝑙 + #𝑛𝑠𝑛𝑟𝑠𝑡𝑙>

#𝑠𝑟𝑠𝑡ℎ

#𝑠𝑟𝑠𝑡ℎ + #𝑠𝑛𝑟𝑠𝑡ℎ + #𝑛𝑠𝑛𝑟𝑠𝑡ℎ

𝑖𝑓 #𝑠𝑟𝑠𝑡𝑙

#𝑠𝑟𝑠𝑡𝑙 + #𝑠𝑛𝑟𝑠𝑡𝑙>

#𝑠𝑟𝑠𝑡ℎ

#𝑠𝑟𝑠𝑡ℎ + #𝑠𝑛𝑟𝑠𝑡ℎ 𝑎𝑛𝑑 #𝑛𝑠𝑛𝑟𝑠𝑡𝑙 ≥ #𝑛𝑠𝑛𝑟𝑠𝑡ℎ .

It is reasonable to assert that non-restating misreporting firms in low-dismissal rate court are

more likely to avoid lawsuits, and thus become non-sued non-restating misstating firms, which

leads to the negative correlation between the number of non-sued non-restating misstating firms

and court dismissal rate.

To verify the analysis above, we construct sample 3 contains both sued misreporting firms and

non-sued misreporting firms and conduct the regression of equation 2. The results confirm our

argument that firms are more likely to restate their accounting misstatement when they are

headquartered in the jurisdiction of low-dismissal rate courts.

5.2. Impact of Court Stringency on the Propensity of Restating Accounting Errors

This paper highlights the impact of court stringency on the propensity of restating irregularities.

In this subsection, we check the impact of court stringency on the likelihood of restating accounting

errors. Unlike accounting irregularities which is more related to fraud, accounting errors are mainly

due to accidental omissions which are unlikely to support a 10b-5 lawsuits. This key difference

allows us to use restatement propensity on accounting errors as a placebo in a falsification test.

Intuitively, if firms’ restatement policy is indeed affected by their home court stringency in 10b-5

lawsuits, which, by definition, is only relevant to fraud, then we should not expect to find court

stringency to have significant effect on restatement propensity for accounting errors.

This test is clearly tougher because in our sample, the number of firms that restate accounting

errors and are sued in securities class action lawsuits is only 5. One alternative approach is to

construct a new sample (hereafter “accounting error sample”). In the accounting error sample, we

match all firms that restate accounting errors between January 1, 2001 and December 31, 2015

with the non-restating misreporting firms from sample 3.27 Then, we re-run the regression of

equation 2 on the accounting error sample. Table 9 reports the results. We find court dismissal

rate exhibits an insignificantly positive impact on the likelihood of misstated firm restating

accounting errors (p=0.5825). This evidence, albeit coarse, lends some support to our argument

that court stringency is only relevant to the restatement of accounting irregularities, which are

related to fraud, and not relevant to the restatement of accounting errors, which reflects

(unintentional) omissions.

27 This way of construction, we admit, is not accurate, for the counterfactual firms are selected from firms that are

considered to have accounting irregularity rather than error. However, the fact is that we cannot hope to identify firms

that made accounting errors and haven’t restated their errors.

5.3 Alternative Measure of Court Dismissal Rate

One shortcoming in the construction of our key explanatory variable, court dismissal rate, is

that cases dismissed within five years may not exactly correspond to cases filed during the same

period. However, to account for the fact that different district courts have very different number

of headquartering firms and lawsuit filings, we believe this scaling method is reasonable. To

address this issue empirically, this subsection tests our baseline hypothesis using alternative court

dismissal rate that takes into account the gap between case filing date and case dismissal date.

Our alternative court dismissal rate is defined by the number of securities cases dismissed

within five years prior to a firm’s fiscal year end in the federal district court where the firm is

headquartered, divided by total such cases filed in the same court in the five years lagged 587 days

to the period used to calculate the number of cases dismissed. 587 days is the average gap between

the filing date and dismissal date for our 1,634 dismissed cases from 1996 to 2013 in the SCAS

database:

𝑑𝑖𝑠𝑚𝑖𝑠𝑠𝑎𝑙𝑖,𝑡,587 =𝑛𝑜_𝑑𝑖𝑠𝑚𝑖𝑠𝑠𝑎𝑙𝑖,𝑡

𝑛𝑜_𝑓𝑖𝑙𝑖𝑛𝑔𝑠𝑖,𝑡,587

(5)

where, 𝑛𝑜_𝑑𝑖𝑠𝑚𝑖𝑠𝑠𝑎𝑙𝑖,𝑡 is the number of cases dismissed within the five years prior to the end of

fiscal year 𝑡 of firm 𝑖 handled by the district court where firm 𝑖 is headquartered; and

𝑛𝑜_𝑓𝑖𝑙𝑖𝑛𝑔𝑠𝑖,𝑡,587 is the number of cases filed within the five years ended 587 days prior to the end

of fiscal year 𝑡 of firm 𝑖 handled by the district court where firm 𝑖 is headquartered.

We re-run the baseline regression analysis in Equation 2 with this alternative court dismissal

rate. The sample period starts from August 10th, 2002 instead of December 31st, 2000 as it requires

587-day gap between case filing date and case dismissal date to calculate the alternative court

dismissal rate. Table 10 reports the results using sample 1 (Column 1), sample 2 (Column 2) and

sample 3 (Column 3). We find court dismissal rate exhibits a large negative impact on the

propensity of misreporting firms issuing restatement (p=0.0721, 0.0239 and 0.0647 for the

regressions with sample 1, 2 and 3, respectively). This evidence supports that the gap between case

filing date and case dismissal date does not contaminate our results.

6. Conclusion

This paper provides the first evidence that district court stringency affects misreporting firms’

propensity to admit their accounting mistakes through restatements. Novelty to this study is our

exploitation of the variation of federal district court dismissal rate in securities lawsuits as proxy

for court stringency. We find strong evidence supporting a preemptive disclosure hypothesis:

Misreporting firms headquartered in more stringent courts are more likely to make irregularity-

based, not error-based, accounting restatement. This result is robust to our three constructed

samples of misreporting firms to balance both internal and external validity, and to alternative

measures of court stringency. Instrumental variable analysis using supreme court’s Tellabs

decision provides causal evidence to our baseline result. Event study on the value implication of

pre-emptive restatements shows that investors not only anticipate higher legal cost for firms in

more stringent courts, but also the value of being honest increases as firms’ home court stringency

increases. In sum, this paper uncovers the significant, but often neglected role of court stringency

in enforcing misreporting firms to timely admit their accounting mistakes.

Reference

Ajinkya, B., Bhojraj, S., Sengupta, P., 2005. The association between outside directors,

institutional investors and the properties of management earnings forecasts. Journal of Accounting

Research 43, 343-376.

Akerlof, G.A., 1970. The market for “lemons”: Quality uncertainty and the market

mechanism. The Quarterly Journal of Economics 84, 488-500.

Amoah, N.Y., Tang, A.P., 2013. Resolution of restatement-induced lawsuits after the Private

Securities Litigation Reform Act. Research in Accounting Regulation 25, 41-46.

Atanassov, J., 2013. Do hostile takeovers stifle innovation? Evidence from antitakeover legislation

and corporate patenting. Journal of Finance 68(3): 1097‒1131.

Badertscher, B., J. Phillips, M. Pincus, and S. Rego. 2009. Earnings management strategies and

the trade-off between tax benefits and detection risk: To conform or not to conform? The

Accounting Review 84 (1):63-97.

Baginski, S.P., Hassell, J.M., Kimbrough, M.D., 2002. The effect of legal environment on

voluntary disclosure: Evidence from management earnings forecasts issued in US and Canadian

markets. The Accounting Review 77, 25-50.

Ball, R., 2001. Infrastructure requirements for an economically efficient system of public financial

reporting and disclosure. Brookings-Wharton papers on financial services 2001, 127-169.

Beatty, A., Weber, J., Yu, J.J., 2008. Conservatism and debt. Journal of Accounting &

Economics 45, 154-174.

Bertrand, M., and Mullainathan, S., 2003. Enjoying the quiet life? Corporate governance and

managerial preferences. Quarterly Journal of Economics 111(5), 1043-75.

Bhide, A. V., and H. H. Stevenson., 1990. Why be honest is honesty does not pay? Harvard

Business Review 68(5), 121–129.

Bhojraj, S., Libby, R., Yang, H., 2010. Analyzing guidance at the firm level: The association

between guidance frequency, guidance properties, and market reactions. Unpublished Paper,

Available a t/http://papers. ssrn. com/sol3/papers. cfm.

Billings, Brooke, M., Cedergren, M.C., 2015. Strategic silence, insider selling and litigation

risk. Journal of Accounting & Economics 59, 119-142.

Bird, S. W. 1975. The assignment of cases to federal district court judges. Stanford Law Review

27(2), 475-487.

Brown, S.V., Tucker, J.W., 2011. Large‐sample evidence on firms’ year‐over‐year MD&A

modifications. Journal of Accounting Research 49, 309-346.

Brown, S., Hillegeist, S.A., Lo, K., 2005. Management forecasts and litigation risk. Sauder School

of Business Working Paper.

Burks, J.J., 2007. Sarbanes-Oxley and the effect of restatements on CEO and CFO compensation

and turnover. THE University of Iowa.

Burns, N., Kedia, S., 2006. The impact of performance-based compensation on

misreporting. Journal of Financial Economics 79, 35-67.