DISTELL ’04 - ShareData - ShareData Online - South ... · Inside DISTELL ’04 FEATURES SOCIAL...

94

Embedding a performance culture Solid returns despite difficult trading conditions DISTELL ’04 ANNUAL REPORT Looking ahead | Reviewing operations | Financial highlights DISTELL How we’ve measured up Analysis of performance 4 Duty-bound Focal point for governance 28

Transcript of DISTELL ’04 - ShareData - ShareData Online - South ... · Inside DISTELL ’04 FEATURES SOCIAL...

Embedding aperformance culture

Solid returns despitedifficult trading conditions

DISTELL ’04ANNUAL REPORT Looking ahead | Reviewing operations | Financial highlights

DISTELL

How we’vemeasured upAnalysis ofperformance

4

Duty-boundFocal point forgovernance

28

DISTELL ANNUAL REPORT 2004

PH

OT

OG

RA

PH

ER

:A

DR

IAA

N O

OS

TH

UIZ

EN

I

NS

PIR

ER

:S

AR

É K

OT

ZE

AN

D F

RIE

ND

MA

RLE

NE

S

HO

T O

N L

OC

AT

ION

AT

PL

AIS

IR D

E M

ER

LE

IN

SI

DE

D

IS

TE

LL

’

04

CO

NT

EN

TS

Inside DDIISSTTEELLLL ’’0044

F E A T U R E S S O C I A L

R E V I E W S

F I N A N C I A L S

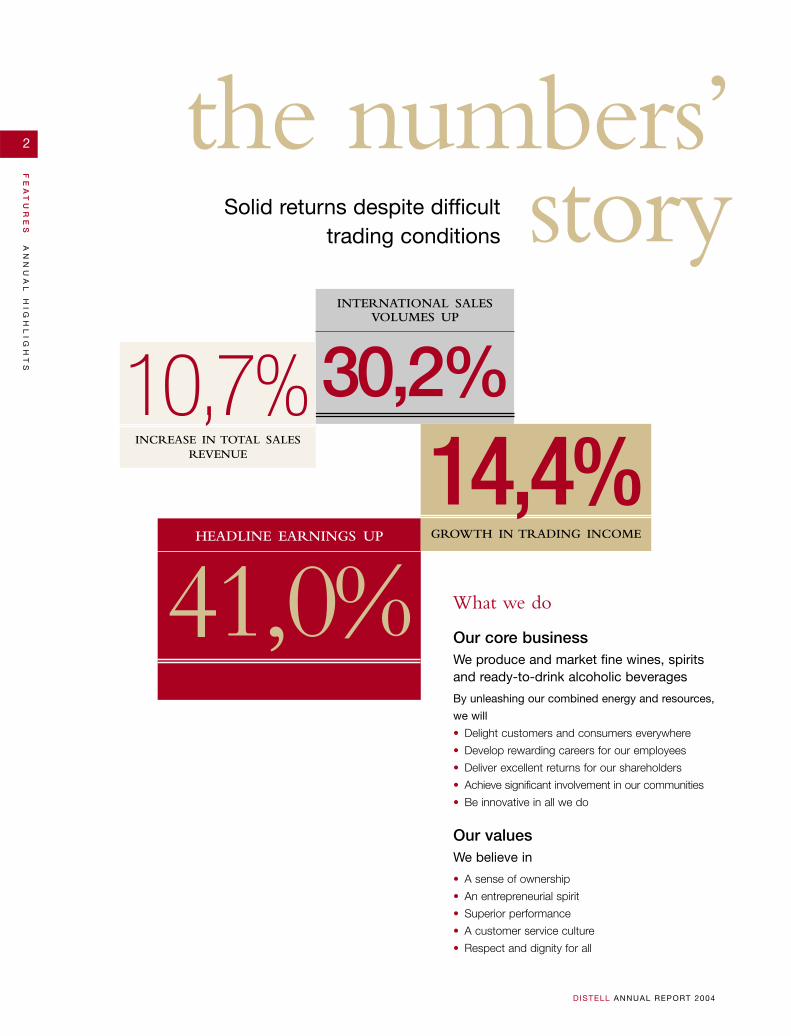

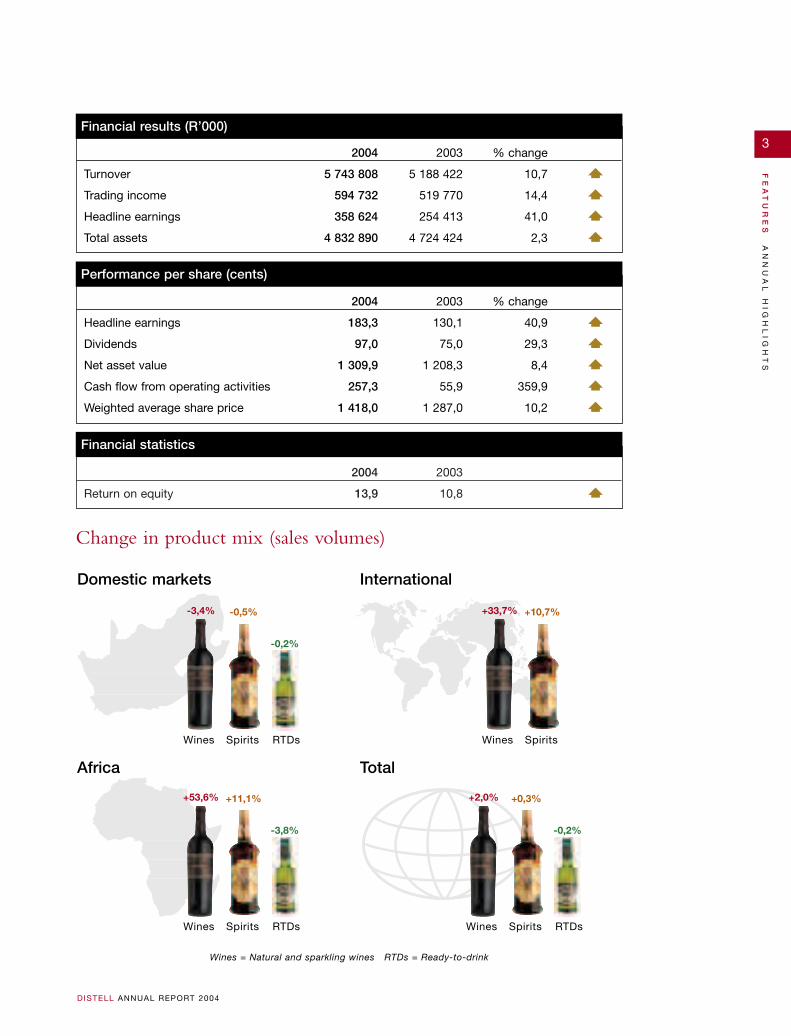

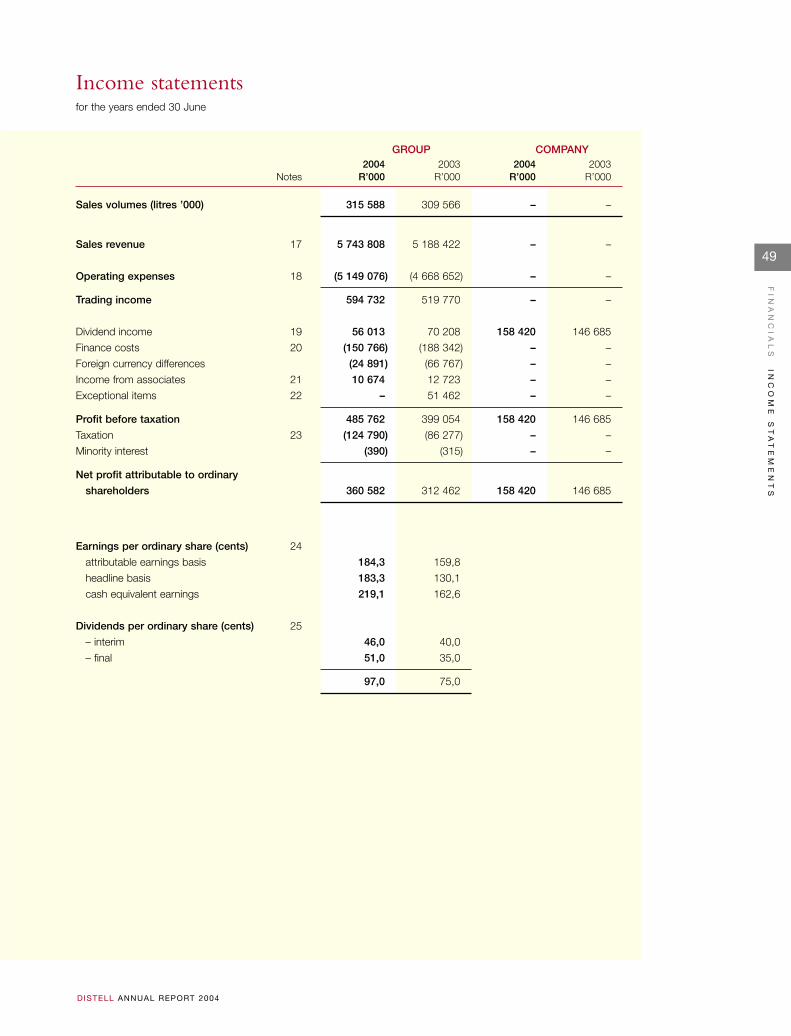

2 The numbers’ storyFinancial highlights

4 How we’ve measured upObjectives and performance

6 Our groupStructure of the group

7 Our global presenceDistell around the world

8 Board mattersComposition of the board andexecutive management

10 Our brands at a glance

12 Seven-year financial reviewfor the years ended 30 June

15 Analysis of shareholders

16 A challenging yearChairman’s statement

20 Performance & growthManaging director’s report

28 Duty-boundCorporate governance report

35 Taking responsibilityCorporate responsibility report

42 Our peopleEmbedding a performance culture

44 The Distell way

45 Annual financial statements

86 Notice to shareholders,voting forms and dates ofimportance to shareholders

42 2 28 4

we introduce ourDDIISSTTEELLLL IINNSSPPIIRREERRSSOUR MODELS FOR 2004

Employees across the company were asked to

nominate those of their colleagues whose example

sets the benchmark for others to emulate.

Achievement is after all a team effort. The eight

people featured in this report were selected as true

Distell inspirers.

FRONT COVERPHOTOGRAPH: ADRIAAN OOSTHUIZEN INSPIRER: BRENDA DLAMINI SHOT ON LOCATION AT BOHEMIA, STELLENBOSCH

1

FE

AT

UR

ES

DISTELL ANNUAL REPORT 2004

inspiring eachotherFirmly focused on the future while

building on the past, Distell people striveto do what others only dream.

INTERNATIONAL SALESVOLUMES UP

30,2%

the numbers’story

What we do

2

FE

AT

UR

ES

AN

NU

AL

H

IG

HL

IG

HT

S

D ISTELL ANNUAL REPORT 2004

Solid returns despite difficulttrading conditions

Our core businessWe produce and market fine wines, spiritsand ready-to-drink alcoholic beverages

By unleashing our combined energy and resources,

we will

• Delight customers and consumers everywhere

• Develop rewarding careers for our employees

• Deliver excellent returns for our shareholders

• Achieve significant involvement in our communities

• Be innovative in all we do

Our valuesWe believe in

• A sense of ownership

• An entrepreneurial spirit

• Superior performance

• A customer service culture

• Respect and dignity for all

INCREASE IN TOTAL SALESREVENUE

10,7%

HEADLINE EARNINGS UP

41,0%GROWTH IN TRADING INCOME

14,4%

2004 2003

Return on equity 13,9 10,8

2004 2003 % change

Headline earnings 183,3 130,1 40,9

Dividends 97,0 75,0 29,3

Net asset value 1 309,9 1 208,3 8,4

Cash flow from operating activities 257,3 55,9 359,9

Weighted average share price 1 418,0 1 287,0 10,2

2004 2003 % change

Turnover 5 743 808 5 188 422 10,7

Trading income 594 732 519 770 14,4

Headline earnings 358 624 254 413 41,0

Total assets 4 832 890 4 724 424 2,3

Change in product mix (sales volumes)

3

FE

AT

UR

ES

AN

NU

AL

H

IG

HL

IG

HT

S

D ISTELL ANNUAL REPORT 2004

Financial results (R’000)

Performance per share (cents)

Financial statistics

Africa Total

Wines = Natural and sparkling wines RTDs = Ready-to-drink

Wines Spirits RTDs

-3,4% -0,5%

-0,2%

Wines Spirits

+33,7% +10,7%

Wines Spirits RTDs

+53,6% +11,1%

-3,8%

Wines Spirits RTDs

+2,0% +0,3%

-0,2%

Domestic markets International

4

FE

AT

UR

ES

OB

JE

CT

IV

ES

D ISTELL ANNUAL REPORT 2004

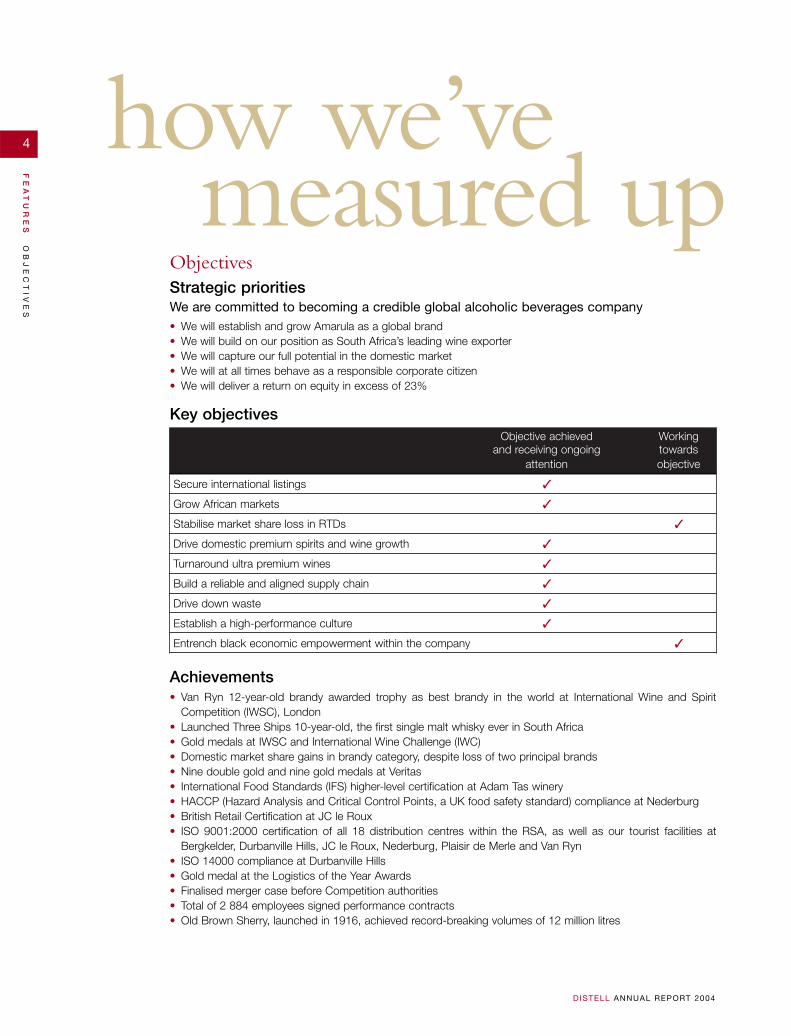

how we’vemeasured up

Strategic prioritiesWe are committed to becoming a credible global alcoholic beverages company• We will establish and grow Amarula as a global brand• We will build on our position as South Africa’s leading wine exporter• We will capture our full potential in the domestic market• We will at all times behave as a responsible corporate citizen• We will deliver a return on equity in excess of 23%

Key objectivesObjective achieved Working

and receiving ongoing towardsattention objective

Secure international listings ✓

Grow African markets ✓

Stabilise market share loss in RTDs ✓

Drive domestic premium spirits and wine growth ✓

Turnaround ultra premium wines ✓

Build a reliable and aligned supply chain ✓

Drive down waste ✓

Establish a high-performance culture ✓

Entrench black economic empowerment within the company ✓

Achievements• Van Ryn 12-year-old brandy awarded trophy as best brandy in the world at International Wine and Spirit

Competition (IWSC), London• Launched Three Ships 10-year-old, the first single malt whisky ever in South Africa• Gold medals at IWSC and International Wine Challenge (IWC)• Domestic market share gains in brandy category, despite loss of two principal brands• Nine double gold and nine gold medals at Veritas• International Food Standards (IFS) higher-level certification at Adam Tas winery• HACCP (Hazard Analysis and Critical Control Points, a UK food safety standard) compliance at Nederburg• British Retail Certification at JC le Roux • ISO 9001:2000 certification of all 18 distribution centres within the RSA, as well as our tourist facilities at

Bergkelder, Durbanville Hills, JC le Roux, Nederburg, Plaisir de Merle and Van Ryn • ISO 14000 compliance at Durbanville Hills• Gold medal at the Logistics of the Year Awards• Finalised merger case before Competition authorities• Total of 2 884 employees signed performance contracts• Old Brown Sherry, launched in 1916, achieved record-breaking volumes of 12 million litres

Objectives

5

FE

AT

UR

ES

PE

RF

OR

MA

NC

E

D ISTELL ANNUAL REPORT 2004

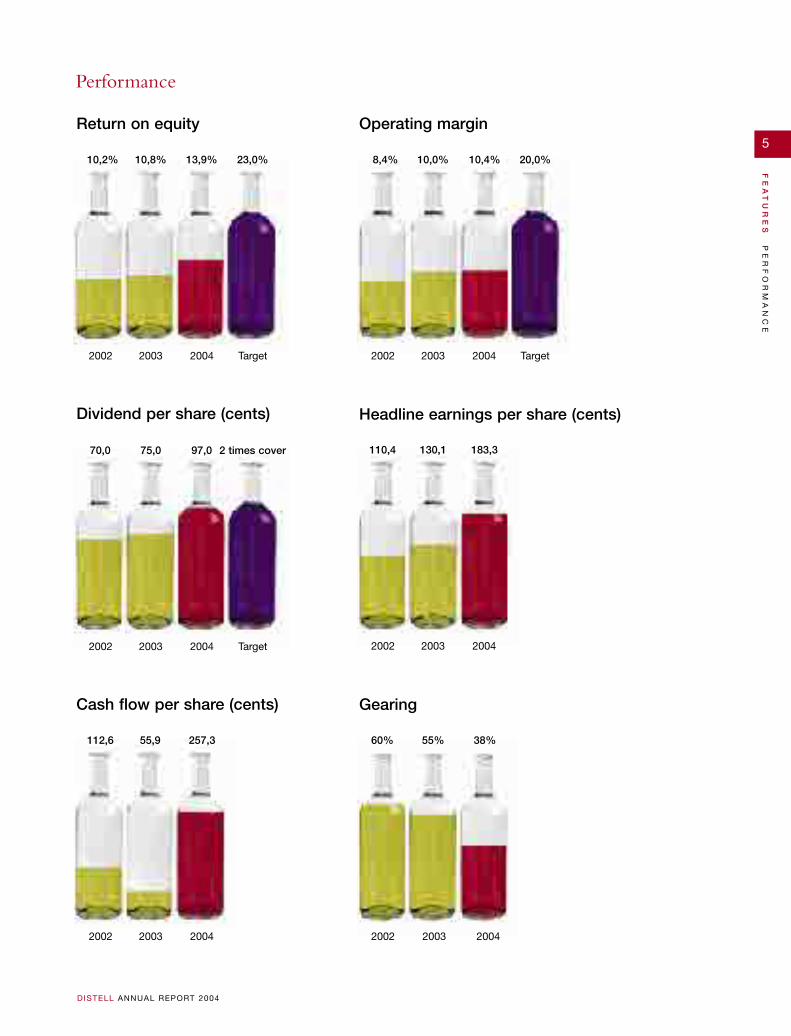

Performance

Return on equity Operating margin

Dividend per share (cents) Headline earnings per share (cents)

Cash flow per share (cents) Gearing

2002 2003 2004 Target

10,2% 10,8% 13,9% 23,0%

2002 2003 2004 Target

70,0 75,0 97,0 2 times cover

2002 2003 2004

112,6 55,9 257,3

2002 2003 2004

60% 55% 38%

2002 2003 2004

110,4 130,1 183,3

2002 2003 2004 Target

8,4% 10,0% 10,4% 20,0%

6

FE

AT

UR

ES

GR

OU

P

ST

RU

CT

UR

E

D ISTELL ANNUAL REPORT 2004

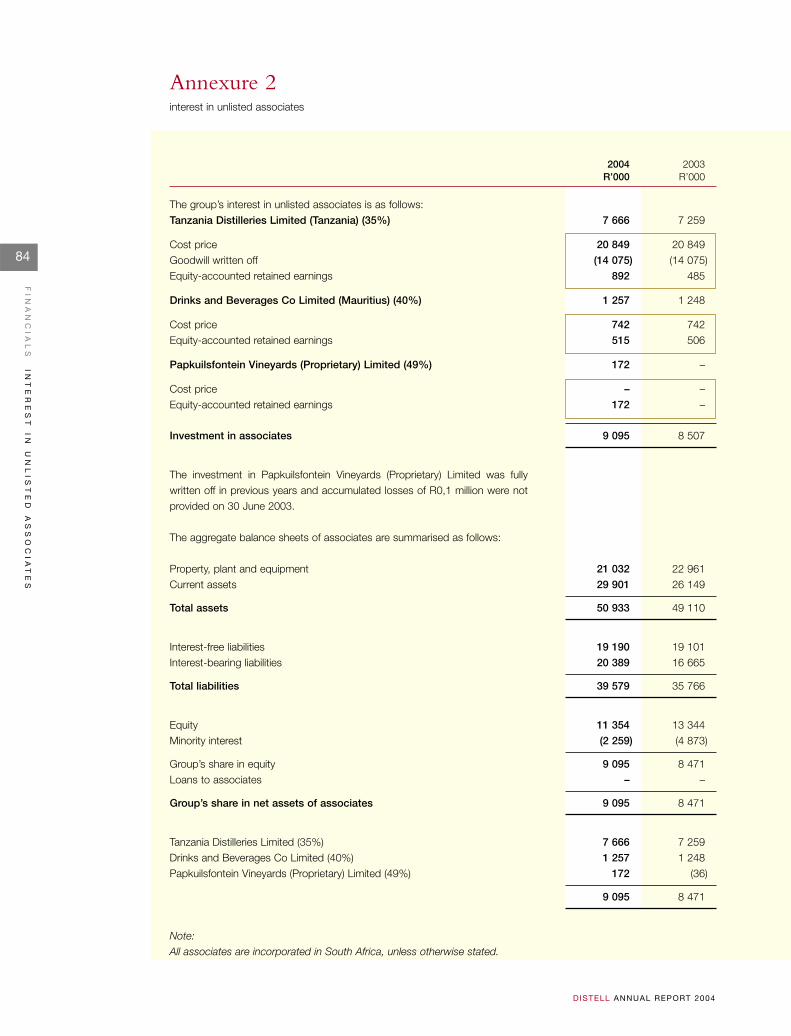

Subsidiaries

Manufacturers and distributors of brandedalcoholic beverages

• Distell Limited (100%)

• Stellenbosch Farmers’ Winery Limited (100%)

Manufacturers of wine

• Nederburg Wines (Proprietary) Limited (100%)

• Durbanville Hills Wines (Proprietary) Limited (66%)

Farming

• Nederburg Wine Farms Limited (100%)

Wholesale distributors of branded alcoholicand other beverages

• Distell Namibia Limited (100%)

• Expo Liquor Limited (100%)

• Swaziland Liquor Distributors Limited (100%)

Sorter and washer of second-hand bottles

• Ecowash (Proprietary) Limited (100%)

Manufacturer and distributor ofmaturation vats

• Tonnellerie Radoux (SA) (Proprietary) Limited(50%)

Manufacturer and distributor of brandedalcoholic and other beverages (associate)

• Tanzania Distilleries Limited (35%)

Manufacturers of wine

• Lusan Holdings (Proprietary) Limited (50%)

• Papkuilsfontein (Proprietary) Limited (49%)

Distell Group LimitedListed on the JSE SecuritiesExchange South Africa

DISTELL

Joint ventures and associates

South African Distilleries and Wines (SA) Limited (100%)

Other investors10%

Other Beverage Interests(Proprietary) Limited(“SABMiller”) 30%

Remgro-KWVInvestments Limited

60%

Our group

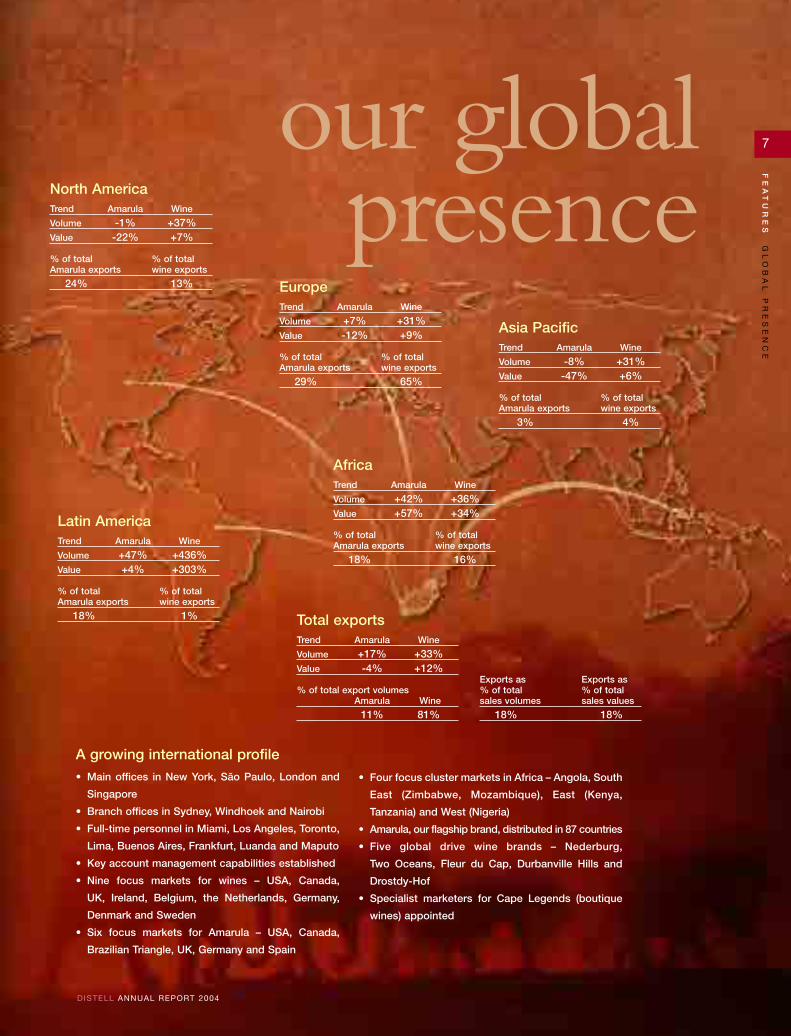

A growing international profile• Main offices in New York, São Paulo, London and

Singapore

• Branch offices in Sydney, Windhoek and Nairobi

• Full-time personnel in Miami, Los Angeles, Toronto,

Lima, Buenos Aires, Frankfurt, Luanda and Maputo

• Key account management capabilities established

• Nine focus markets for wines – USA, Canada,

UK, Ireland, Belgium, the Netherlands, Germany,

Denmark and Sweden

• Six focus markets for Amarula – USA, Canada,

Brazilian Triangle, UK, Germany and Spain

• Four focus cluster markets in Africa – Angola, South

East (Zimbabwe, Mozambique), East (Kenya,

Tanzania) and West (Nigeria)

• Amarula, our flagship brand, distributed in 87 countries

• Five global drive wine brands – Nederburg,

Two Oceans, Fleur du Cap, Durbanville Hills and

Drostdy-Hof

• Specialist marketers for Cape Legends (boutique

wines) appointed

our globalpresence

EuropeTrend Amarula Wine

Volume +7% +31%Value -12% +9%

% of total % of totalAmarula exports wine exports

29% 65%

AfricaTrend Amarula Wine

Volume +42% +36%Value +57% +34%

% of total % of totalAmarula exports wine exports

18% 16%

Latin AmericaTrend Amarula Wine

Volume +47% +436%Value +4% +303%

% of total % of totalAmarula exports wine exports

18% 1% Total exportsTrend Amarula Wine

Volume +17% +33%Value -4% +12%

% of total export volumesAmarula Wine

11% 81%

Exports as Exports as% of total % of totalsales volumes sales values

18% 18%

Asia PacificTrend Amarula Wine

Volume -8% +31%Value -47% +6%

% of total % of totalAmarula exports wine exports

3% 4%

North AmericaTrend Amarula Wine

Volume -1% +37%Value -22% +7%

% of total % of totalAmarula exports wine exports

24% 13%

7

FE

AT

UR

ES

GL

OB

AL

P

RE

SE

NC

E

D ISTELL ANNUAL REPORT 2004

Joe Madungandaba*Chief executive officer of Community InvestmentHoldings. Chairman of Marine Data Systems and deputychairperson of Transtel Audit Committee, executivedirector of Jasco Electronic Holdings Ltd and non-executive director of Air Liquide Healthcare.Attended 5 out of 6 meetings.

David Nurek*Regional chairman of Investec Western Cape, deputychairman of Foschini, and also a director of New ClicksHoldings, Pick ’n Pay,Aspen Pharmaceuticals and Trencor.Attended 4 out of 6 board meetings; 4 out of 4 auditcommittee meetings; and 5 out of 5 remunerationcommittee meetings.

Daan Prins*Business consultant, previously financial director ofRothmans International.Attended 6 out of 6 board meetings; and 4 out of 4 auditcommittee meetings.

Jan Scannell#

Managing directorAttended 6 out of 6 board meetings.

Peter Swartz*Proprietor of Swartz Properties (Pty) Ltd and also adirector of Absa, Ellerine, New Clicks, Sanlam and SunwestInternational.Attended 6 out of 6 board meetings; and 5 out of 5remuneration committee meetings.

Thys VisserDeputy chairman and chief executive officer of Remgroand also a director of Rainbow Chicken and Nampak.Attended 5 out of 6 board meetings; 4 out of 4 auditcommittee meetings; and 5 out of 5 remunerationcommittee meetings.

* Independent# Executive

8

FE

AT

UR

ES

BO

AR

D

D ISTELL ANNUAL REPORT 2004

The board is the focal point for the group’s execution of corporate governance.This body is ultimately accountable and responsible for the performance, affairsand behaviour of Distell, formalised in a charter for the board and its committees.

board mattersBoard of directors

Duimpie Bayly* Director of Duimpie Bayly & Associates, consultant andadviser to the wine industry.Attended 6 out of 6 board meetings.

Peter Bester*Retired as executive chairman of Cadbury Schweppes (SA)Ltd in 2001. He is currently director of ABI, AnglovaalIndustries, Suidwes Beleggings and National Brands.Appointed 28 April 2004.Attended 2 out of 2 board meetings.

Piet BeyersDirector of Remgro, Richemont, VenFin and Unilever-BestfoodsRobertsons.Attended 5 out of 6 board meetings.

Merwe Botha#

Financial directorAppointed 8 December 2003.Attended 4 out of 4 board meetings.

Johan Carinus*Wine farmer, also a director of Stellenbosch Vineyards andHet Jan Marais Fund.Attended 6 out of 6 board meetings.

Smartie Genade#

Operations directorAttended 6 out of 6 board meetings.

Jakes Gerwel*Served as director-general in the Office of former PresidentNelson Mandela. Presently director of Naspers, OldMutual, Goldfields, and chairman of Brimstone, AfriconEngineering and Educor. Also the chancellor of RhodesUniversity and chairman of the board of trustees of theNelson Mandela Foundation.Appointed 28 April 2004.Attended 1 out of 2 board meetings.

Dr Edwin de la H HertzogChairman of Medi-Clinic Corporation and also a directorof Remgro,Total (SA) and Trans Hex Group.Attended 5 out of 6 board meetings.

9

FE

AT

UR

ES

BO

AR

D

D ISTELL ANNUAL REPORT 2004

Executive management

Jan Scannell (53)Managing directorBCom, LLB

Jan joined the Distillers Corporation in 1979. He wasappointed as director in 1988, and as managing director in1994. In December 2000, he was appointed as managingdirector of Distell. Jan must ensure that the companydelivers on its objectives, and is responsible for building ahigh-performance culture.

Merwe Botha (51)Financial directorBCom Hons (Taxation), BCompt Hons, CA(SA)

Merwe joined the Distillers Corporation in 1980. He wasappointed financial director in 1997 and to his presentposition at Distell in December 2000. Merwe is responsiblefor financial planning and control, information technology,statutory reporting and internal audit.

Stoffel Cronjé (50)Company secretary and human resource director MA

Stoffel joined the Distillers Corporation in 1980. He wasappointed group secretary and human resource director in1990 and to his present position at Distell in December2000. Stoffel performs all statutory company secretarialfunctions. He also oversees the human resources division.

Smartie Genade (53)Operations director BCom (Hons), MBA

Smartie joined Stellenbosch Farmers’ Winery (SFW) in1972. He was appointed director in 1988,managing directorin 2000 and to his present position at Distell in December2000. Smartie oversees the operations of the group,including packaging, distribution, technical services,procurement and supply chain management.

Hennie Heÿl (58)Primary production directorMSc Agric

Hennie joined the Distillers Corporation in 1974. He wasappointed technical director in 1988, production directorin 1997 and to his present position at Distell in December2000. Hennie is responsible for our farms; grape, wine,brandy and other raw material procurement; distillation,winemaking and blending.

Etienne Heyns (49)International operations directorBCom (Hons), MBA

Etienne joined Distell as international operations directorin May 2002. He has over 20 years of experience ininternational marketing. Etienne is responsible for growingour international revenue by providing superior service toexisting customers and obtaining new listings.

Gert Loubser (56)Quality management and research directorMSc, PhD

Gert joined SFW in 1974. He was appointed research anddevelopment director in 1994 and to his present position atDistell in December 2000.Gert must ensure that total qualitymanagement is implemented throughout the group and thatongoing research leads to new products and processes.

Malcolm Searle (44)Marketing directorBCom (Hons)

Malcolm joined Distell as marketing director in January2004. He has almost 20 years experience in the FMCGbusiness, and has worked as marketing executive in severalcountries across the globe. Malcolm is responsible forbuilding strong brand portfolios on market strategies thatleverage consumer insights and drive innovation.

André Steyn (54)Corporate affairs directorBCom (Hons), LLB

André joined SFW in 1978. He was appointed humanresources, industry and corporate affairs director in 1990and to his present position at Distell in December 2000.André is responsible for managing the corporate reputation,internal communication and new business opportunities.

Tim Tarr (46)Sales director

Tim joined the Distillers Corporation in 1979. He wasappointed national sales director in 1995 and to his presentposition at Distell in December 2000.Tim must ensure thatwe retain and improve our market leadership in SouthAfrica, Botswana, Lesotho, Namibia and Swaziland. Heoversees all our sales forces.

Valerio Toros (41)Business process improvement directorBEng (Mech), MBA

Valerio joined the Distillers Corporation in 1991 as projectengineer. After overseeing the SFW/Distillers mergerimplementation from 2000 to 2001, he became the groupmanager of business process improvement (BPI). He wasappointed as BPI director at the end of 2003. Valerio isresponsible for the Distell Management Operating System(DMOS), and for major projects and initiatives to improvecompany performance.

Domestic(From left)

• Chateau Libertas• Cellar Cask• Graça• Grünberger• JC le Roux• Paarl Perlé• Sedgwick’s

Old Brown Sherry• Zonnebloem

Global(From left)

• Nederburg• Two Oceans• Durbanville Hills• Drostdy-Hof• Fleur du Cap• Obikwa• Oracle

Cape legends(From left)

• Alto• Hill & Dale• Le Bonheur• Neethlingshof• Plaisir de Merle• Stellenzicht• Tukulu• Uitkyk

10

FE

AT

UR

ES

OU

R

BR

AN

DS

A

T

A

GL

AN

CE

D ISTELL ANNUAL REPORT 2004

Our brands at a glance

Wines

(From left)

• Savanna• Hunters• Esprit• Klipdrift & Cola

(Clockwise from left)

• Amarula• Klipdrift • Klipdrift Premium• Klipdrift Gold• Flight of the Fish Eagle• Mellow-wood• Nederburg Brandy• Van Ryn range• V.R• Viceroy• Richelieu• Oude Meester• Old Buck• Mainstay• Three Ships

Ready-to-drink (RTDs)

11

FE

AT

UR

ES

OU

R

BR

AN

DS

A

T

A

GL

AN

CE

D ISTELL ANNUAL REPORT 2004

Spirits

12

FE

AT

UR

ES

SE

VE

N-

YE

AR

F

IN

AN

CI

AL

R

EV

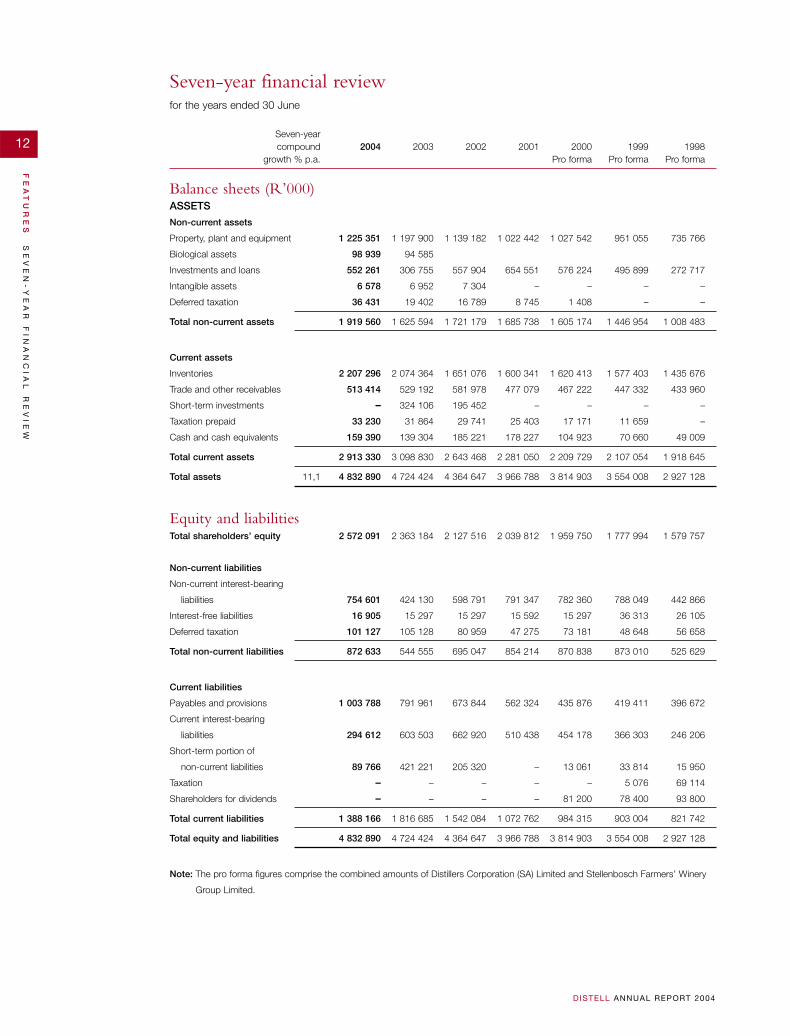

IE

W

D ISTELL ANNUAL REPORT 2004

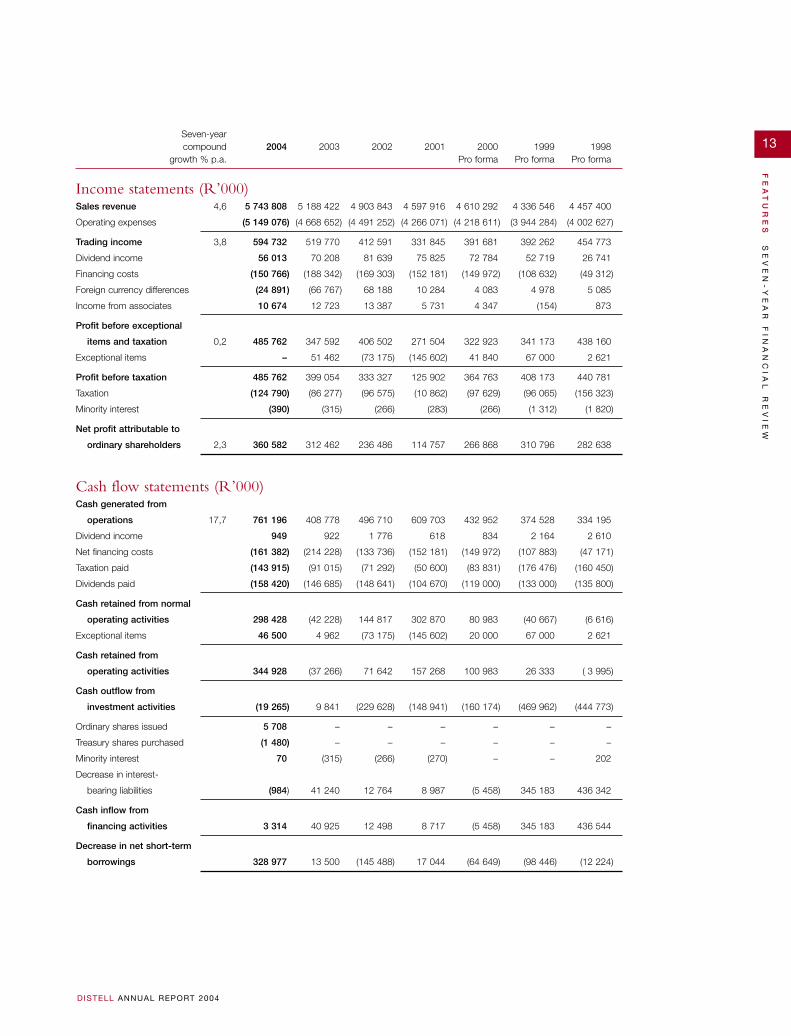

Seven-yearcompound 2004 2003 2002 2001 2000 1999 1998

growth % p.a. Pro forma Pro forma Pro forma

Balance sheets (R’000)ASSETS

Non-current assets

Property, plant and equipment 1 225 351 1 197 900 1 139 182 1 022 442 1 027 542 951 055 735 766

Biological assets 98 939 94 585

Investments and loans 552 261 306 755 557 904 654 551 576 224 495 899 272 717

Intangible assets 6 578 6 952 7 304 – – – –

Deferred taxation 36 431 19 402 16 789 8 745 1 408 – –

Total non-current assets 1 919 560 1 625 594 1 721 179 1 685 738 1 605 174 1 446 954 1 008 483

Current assets

Inventories 2 207 296 2 074 364 1 651 076 1 600 341 1 620 413 1 577 403 1 435 676

Trade and other receivables 513 414 529 192 581 978 477 079 467 222 447 332 433 960

Short-term investments – 324 106 195 452 – – – –

Taxation prepaid 33 230 31 864 29 741 25 403 17 171 11 659 –

Cash and cash equivalents 159 390 139 304 185 221 178 227 104 923 70 660 49 009

Total current assets 2 913 330 3 098 830 2 643 468 2 281 050 2 209 729 2 107 054 1 918 645

Total assets 11,1 4 832 890 4 724 424 4 364 647 3 966 788 3 814 903 3 554 008 2 927 128

Equity and liabilitiesTotal shareholders’ equity 2 572 091 2 363 184 2 127 516 2 039 812 1 959 750 1 777 994 1 579 757

Non-current liabilities

Non-current interest-bearing

liabilities 754 601 424 130 598 791 791 347 782 360 788 049 442 866

Interest-free liabilities 16 905 15 297 15 297 15 592 15 297 36 313 26 105

Deferred taxation 101 127 105 128 80 959 47 275 73 181 48 648 56 658

Total non-current liabilities 872 633 544 555 695 047 854 214 870 838 873 010 525 629

Current liabilities

Payables and provisions 1 003 788 791 961 673 844 562 324 435 876 419 411 396 672

Current interest-bearing

liabilities 294 612 603 503 662 920 510 438 454 178 366 303 246 206

Short-term portion of

non-current liabilities 89 766 421 221 205 320 – 13 061 33 814 15 950

Taxation – – – – – 5 076 69 114

Shareholders for dividends – – – – 81 200 78 400 93 800

Total current liabilities 1 388 166 1 816 685 1 542 084 1 072 762 984 315 903 004 821 742

Total equity and liabilities 4 832 890 4 724 424 4 364 647 3 966 788 3 814 903 3 554 008 2 927 128

Note: The pro forma figures comprise the combined amounts of Distillers Corporation (SA) Limited and Stellenbosch Farmers’ Winery

Group Limited.

Seven-year financial reviewfor the years ended 30 June

13

FE

AT

UR

ES

SE

VE

N-

YE

AR

F

IN

AN

CI

AL

R

EV

IE

W

D ISTELL ANNUAL REPORT 2004

Seven-yearcompound 2004 2003 2002 2001 2000 1999 1998

growth % p.a. Pro forma Pro forma Pro forma

Income statements (R’000)Sales revenue 4,6 5 743 808 5 188 422 4 903 843 4 597 916 4 610 292 4 336 546 4 457 400

Operating expenses (5 149 076) (4 668 652) (4 491 252) (4 266 071) (4 218 611) (3 944 284) (4 002 627)

Trading income 3,8 594 732 519 770 412 591 331 845 391 681 392 262 454 773

Dividend income 56 013 70 208 81 639 75 825 72 784 52 719 26 741

Financing costs (150 766) (188 342) (169 303) (152 181) (149 972) (108 632) (49 312)

Foreign currency differences (24 891) (66 767) 68 188 10 284 4 083 4 978 5 085

Income from associates 10 674 12 723 13 387 5 731 4 347 (154) 873

Profit before exceptional

items and taxation 0,2 485 762 347 592 406 502 271 504 322 923 341 173 438 160

Exceptional items – 51 462 (73 175) (145 602) 41 840 67 000 2 621

Profit before taxation 485 762 399 054 333 327 125 902 364 763 408 173 440 781

Taxation (124 790) (86 277) (96 575) (10 862) (97 629) (96 065) (156 323)

Minority interest (390) (315) (266) (283) (266) (1 312) (1 820)

Net profit attributable to

ordinary shareholders 2,3 360 582 312 462 236 486 114 757 266 868 310 796 282 638

Cash flow statements (R’000)Cash generated from

operations 17,7 761 196 408 778 496 710 609 703 432 952 374 528 334 195

Dividend income 949 922 1 776 618 834 2 164 2 610

Net financing costs (161 382) (214 228) (133 736) (152 181) (149 972) (107 883) (47 171)

Taxation paid (143 915) (91 015) (71 292) (50 600) (83 831) (176 476) (160 450)

Dividends paid (158 420) (146 685) (148 641) (104 670) (119 000) (133 000) (135 800)

Cash retained from normal

operating activities 298 428 (42 228) 144 817 302 870 80 983 (40 667) (6 616)

Exceptional items 46 500 4 962 (73 175) (145 602) 20 000 67 000 2 621

Cash retained from

operating activities 344 928 (37 266) 71 642 157 268 100 983 26 333 ( 3 995)

Cash outflow from

investment activities (19 265) 9 841 (229 628) (148 941) (160 174) (469 962) (444 773)

Ordinary shares issued 5 708 – – – – – –

Treasury shares purchased (1 480) – – – – – –

Minority interest 70 (315) (266) (270) – – 202

Decrease in interest-

bearing liabilities (984) 41 240 12 764 8 987 (5 458) 345 183 436 342

Cash inflow from

financing activities 3 314 40 925 12 498 8 717 (5 458) 345 183 436 544

Decrease in net short-term

borrowings 328 977 13 500 (145 488) 17 044 (64 649) (98 446) (12 224)

14

FE

AT

UR

ES

SE

VE

N-

YE

AR

F

IN

AN

CI

AL

R

EV

IE

W

D ISTELL ANNUAL REPORT 2004

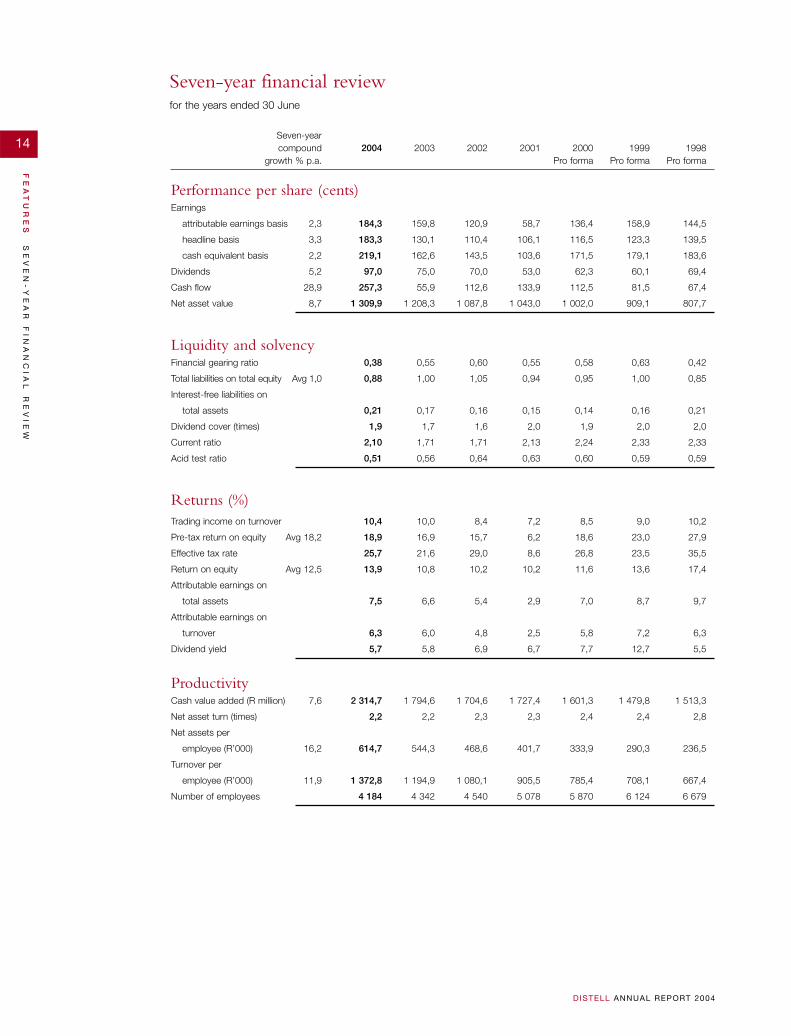

Seven-yearcompound 2004 2003 2002 2001 2000 1999 1998

growth % p.a. Pro forma Pro forma Pro forma

Performance per share (cents)Earnings

attributable earnings basis 2,3 184,3 159,8 120,9 58,7 136,4 158,9 144,5

headline basis 3,3 183,3 130,1 110,4 106,1 116,5 123,3 139,5

cash equivalent basis 2,2 219,1 162,6 143,5 103,6 171,5 179,1 183,6

Dividends 5,2 97,0 75,0 70,0 53,0 62,3 60,1 69,4

Cash flow 28,9 257,3 55,9 112,6 133,9 112,5 81,5 67,4

Net asset value 8,7 1 309,9 1 208,3 1 087,8 1 043,0 1 002,0 909,1 807,7

Liquidity and solvencyFinancial gearing ratio 0,38 0,55 0,60 0,55 0,58 0,63 0,42

Total liabilities on total equity Avg 1,0 0,88 1,00 1,05 0,94 0,95 1,00 0,85

Interest-free liabilities on

total assets 0,21 0,17 0,16 0,15 0,14 0,16 0,21

Dividend cover (times) 1,9 1,7 1,6 2,0 1,9 2,0 2,0

Current ratio 2,10 1,71 1,71 2,13 2,24 2,33 2,33

Acid test ratio 0,51 0,56 0,64 0,63 0,60 0,59 0,59

Returns (%)Trading income on turnover 10,4 10,0 8,4 7,2 8,5 9,0 10,2

Pre-tax return on equity Avg 18,2 18,9 16,9 15,7 6,2 18,6 23,0 27,9

Effective tax rate 25,7 21,6 29,0 8,6 26,8 23,5 35,5

Return on equity Avg 12,5 13,9 10,8 10,2 10,2 11,6 13,6 17,4

Attributable earnings on

total assets 7,5 6,6 5,4 2,9 7,0 8,7 9,7

Attributable earnings on

turnover 6,3 6,0 4,8 2,5 5,8 7,2 6,3

Dividend yield 5,7 5,8 6,9 6,7 7,7 12,7 5,5

ProductivityCash value added (R million) 7,6 2 314,7 1 794,6 1 704,6 1 727,4 1 601,3 1 479,8 1 513,3

Net asset turn (times) 2,2 2,2 2,3 2,3 2,4 2,4 2,8

Net assets per

employee (R’000) 16,2 614,7 544,3 468,6 401,7 333,9 290,3 236,5

Turnover per

employee (R’000) 11,9 1 372,8 1 194,9 1 080,1 905,5 785,4 708,1 667,4

Number of employees 4 184 4 342 4 540 5 078 5 870 6 124 6 679

Seven-year financial reviewfor the years ended 30 June

15

FE

AT

UR

ES

AN

AL

YS

IS

O

F

SH

AR

EH

OL

DE

RS

D ISTELL ANNUAL REPORT 2004

Number of % of Number of % of issuedOrdinary shares holders holders shares shares

Distribution of shareholdersPublic shareholders 3 250 99,00 19 244 164 9,80

Non-public shareholders

Major beneficial shareholders 2 0,06 176 022 000 89,64

Directors, including those of subsidiaries, and

their associates 30 0,91 889 150 0,46

The Distell Group Share Trust 1 0,03 201 322 0,10

3 283 100,00 196 356 636 100,00

Number of shares in issue2004 2003

Total number of shares in issue 196 356 636 195 580 000

Shares purchased by The Distell Group Share Trust

and accounted for as treasury shares (201 322) –

196 155 314 195 580 000

Weighted number of shares 195 625 710 195 580 000

Major beneficial shareholdersThe following shareholders have a holding of greater than 5% of the issued shares of the company:

Number of % ofshares total

Remgro-KWV Investments Limited 117 348 000 59,76

Other Beverage Interests (Proprietary) Limited (“SABMiller”) 58 674 000 29,88

JSE Securities Exchange South Africa2004 2003 2002 2001 2000 1999 1998

Price per share (cents)

highest during the year 1 725 1 500 1 500 1 000 1 050 810 1 800

lowest during the year 1 100 1 105 735 675 690 400 700

closing at year-end 1 500 1 201 1 350 730 870 810 700

weighted average 1 418 1 287 1 008 788 869 527 1 227

Price earnings ratio 8,1 7,5 11,2 12,4 6,0 6,0 5,6

JSE Actuaries’ price index at

year-end (1997: 100 cents)

Distell Group Limited 96 77 87 47 56 52 45

Closing price/net asset value per share 1,1 1,0 1,2 0,7 1,2 1,3 1,2

Weighted average number of shares

in issue (’000) 195 626 195 580 195 580 195 580 140 000 140 000 140 000

Number of shares traded (’000) 3 533 2 784 6 263 3 647 2 224 4 646 2 765

Shares traded/shares in issue (%) 1,8 1,4 3,2 1,9 1,6 3,3 2,0

Value of shares traded (R’000) 50 114 35 833 63 124 28 722 19 323 24 497 33 928

Number of transactions 1 069 981 1 386 1 220 749 1 197 850

Number of shareholders 3 283 3 389 1 738 2 268 2 042 2 131 2 108

Market capitalisation (R million) 2 934 2 349 2 640 1 428 1 218 1 134 980

Net asset value/market capitalisation 0,88 1,01 0,81 1,43 0,86 0,79 0,82

Information for the period 1998 to 2000 refers to the listed shares of Distillers Corporation (SA) Limited.

Analysis of shareholdersat 30 June 2004

16

RE

VI

EW

SC

HA

IR

MA

N’

S

ST

AT

EM

EN

T

D ISTELL ANNUAL REPORT 2004DISTELL ANNUAL REPORT 2004

The past year has been characterised by a much

strengthened rand, reduced inflation, lower interest rates

and accelerated discretionary spending among South

Africa’s middle and higher income groups on the one

hand, but slower spending by lower income consumers,

who comprise the majority of South Africans, on the

other. Job shedding prompted by a more robust currency

that has made the country’s exports less price-competitive

on international markets, the growing impact of HIV/Aids

and adverse weather conditions in many agricultural areas

continue to erode their already limited spending power.

Understandably, the domestic market for alcoholic

beverages experienced muted growth, showing a volume

increase for the past year of just 1,9%, with beer the main

contributor.

A stronger rand has had a significant impact on much of

the local liquor industry, particularly the wine sector,

where there has been increasing consolidation in an effort

to maintain a presence on international markets. Over the

past few years, some local wine producers have used a weak

rand as their single biggest competitive advantage. Now

that this has been lost to them, their profit margins have

suffered, particularly in the face of a global oversupply of

wine, compounded by a record 2004 vintage, which has

delivered exceptional tonnage and quality. Californian

producers, now aided by a weaker dollar, Australian and

New Zealand producers are seeking new ways to market

their wines and deplete their build-up of stocks from

earlier vintages. At the same time, the beleaguered French

industry has responded to changed market conditions with

a revitalised and more competitive operating system. It

should be noted that while these countries are supported

by government subsidies in their efforts, no such benefit is

available to the South African wine industry.

Domestic competition has intensified, with producers

unable or unwilling to sell their wines abroad, courting

local consumers more assiduously then ever, buoyed by

greater variety and aggressive pricing strategies.

Simultaneously, a strong rand has made South Africa a

favourable market for foreign producers.

Distell was forced to stringently review its operating costs

at the start of the decade and to rationalise its product

ranges while servicing a variety of price points in both

retail and on-consumption segments, inculcating a culture

of fiscal discipline.This, coupled with an ongoing policy of

brand building that eschews discounting as a tactic of

growing market share in favour of investing in trademarks

for the long term, has accorded us a measure of resilience

against these conditions.

We have also been cushioned to some extent by our strong

domestic support base across a wide spectrum of products

and pricing segments in wine, spirits and ready-to-drink

alcoholic beverages (RTDs). Given our focus on both retail

and on-consumption channels in export markets, our

vulnerability to the advancing power of the multiple

grocers in many key export markets has also been

contained.

The company also continues to find ways of making the

supply chain more cost-efficient through research and

partnerships with supplier growers, planning wines in the

vineyard and matching growing costs to the eventual selling

prices, production site energy audits, judicious use of water

and recycling. Our suppliers are responding in similar vein

and are passing on the benefits of a stronger rand.

Notwithstanding a stronger currency and a decline in

global tourism, South Africa remains an attractive tourist

destination, particularly for Europeans and North

Americans, and the country has continued to outperform

its key competitors. The Cape and the winelands have

grown in popularity, along with leading game parks and

lodges.This development has been good for Amarula, the

country’s most widely distributed alcoholic beverage, and

for our portfolio of wines.CONTINUED OVERLEAF

A statement from Distell’schairman, David Nurek

a challengingyear

PH

OT

OG

RA

PH

ER

:A

DR

IAA

N O

OS

TH

UIZ

EN

I

NS

PIR

ER

:S

ELW

YN

G

RA

HA

M

SH

OT

ON

LO

CA

TIO

N A

T S

HO

OT

ER

S,

ST

RA

ND

17

RE

VI

EW

SC

HA

IR

MA

N’

S

ST

AT

EM

EN

T

D ISTELL ANNUAL REPORT 2004

Inclusive teamwork,commitment and

innovation are SelwynGraham’s cornerstoneof delivering superior

service levels andworld-class quality.

18

RE

VI

EW

SC

HA

IR

MA

N’

S

ST

AT

EM

EN

T

D ISTELL ANNUAL REPORT 2004

The company is also actively engaged in promoting the

biodiversity of the Cape, in the interests of nature conser-

vation and ecotourism, and has played a vital role in the

establishment of the Biodiversity and Wine Initiative. Its

guidelines, set out in the Biodiversity Bill and scheduled to

become law during 2004,have in many instances already been

implemented in our own vineyards and those of our suppliers.

They have also been incorporated into South Africa’s very

progressive Integrated Production of Wine system that

promotes sustainable winegrowing and production.

Encouragingly, both Government and the private sector

have heightened their focus on broad-based black

economic empowerment (BEE). Distell is actively involved

in the shaping of the Liquor Industry Charter that has been

reviewing the entire manufacturing and distribution chain,

from ownership and management to employee equity and

skills development, procurement practices, enterprise

development and social investment. The company serves

on the Charter’s steering committee and is represented on

all its working groups.At the same time, the Wine Industry

Charter, facilitated by the SA Wine and Brandy Company,

is making headway in setting targets in all these areas

pertaining to wine.

Internally, BEE is a drive project of Distell. We are co-

ordinating and strengthening our focus in areas such

as preferential procurement, enterprise and skills

development, employment equity and corporate social

investment.

The inclusion of a broad-based black shareholder in Distell

is currently being attended to by a subcommittee of the

board of directors.

As a founding member of the Wine Industry Ethical Trade

Association (WIETA) we have been contributing to the

development of its code of socially responsible and ethical

labour practices. All 18 of our sites are being evaluated by

the NGO’s independent audit committee, a process due

for completion later in 2004. The audit process covers a

comprehensive range of issues such as health and safety;

freedom of association; the right of workers to participate

in decisions affecting them; worker benefits and

conditions; child labour; fair disciplinary procedures; and

the sourcing of and contractual obligations to seasonal

workers.

The finalisation of the Liquor Act and its implementation

are to be welcomed as the culmination of constructive

negotiation between Government, producers, wholesalers,

distributors and retailers and as a boost for BEE. Not only

does the bill encourage diversity of ownership across all

three tiers of the industry, but it also provides a more stable

basis from which to promote the responsible consumption

of alcohol.

However, we are concerned at the tardiness to effect

legislation at provincial level.To date, just two of the nine

provinces have promulgated liquor licensing legislation –

Gauteng and Eastern Cape, and both of these are

fundamentally flawed in that they create more confusion

and bureaucracy. There is an urgent need to formalise

retail trade in a way that is acceptable to producers, sellers

and consumers and that makes it possible to effectively

advance responsible drinking.

Another issue that requires urgent consideration is the

discriminatory level of excise duties applied to wine, which

CONTINUED FROM PAGE 16

Distell is actively involved in the shaping of the Liquor Industry

Charter that has been reviewing the entire manufacturing and

distribution chain, from ownership and management to employee

equity and skills development, procurement practices, enterprise

development and social investment.

19

RE

VI

EW

SC

HA

IR

MA

N’

S

ST

AT

EM

EN

T

D ISTELL ANNUAL REPORT 2004

last February were increased 30,7%, and spirits, which rose

13,8%, while beer went up just 9%.

We are of the view that excess consumption of all alcoholic

beverages and under-age drinking is best addressed

through holistic measures that identify and target

vulnerable groups with appropriate interventions such as

education and life-skills programmes for consumers;

training licensees in how to develop and entrench a culture

of moderation among their patrons; counselling and

rehabilitating abusers; and by adopting responsible

advertising, packaging, promotion and sales. This is the

route we have taken through our industry body, the

Industry Association for the Responsible Use of Alcohol

(ARA) of which we are a leading corporate member.

We are gratified by the considerable progress made by

Government in combating illicit liquor trading. However,

cross-border activities such as round-tripping and

smuggling continue, partially exacerbated by such high

excise duties, thus providing another compelling reason for

a revision in State policy towards taxation of wines and

spirits.

We welcome three new directors to our board. They are

Peter Bester, former executive chairman of Cadbury

Schweppes (SA) Limited and a director of several other

boards, who brings a wealth of business and marketing

expertise, Merwe Botha, Distell’s financial director, whose

financial acumen is well established, and Jakes Gerwel,

former director-general in the Office of the State

President, chairman of the board of trustees of the Nelson

Mandela Foundation, chancellor of Rhodes University and

a director of several major corporates. Professor Gerwel’s

academic and socio-economic insights and his contri-

bution to business are greatly valued.

On behalf of the board, I express our appreciation to every

member of Distell for their hard work, expertise and

commitment and their role in delivering a solid

performance in undoubtedly difficult circumstances.

DM Nurek

Chairman

16 August 2004

20

RE

VI

EW

SM

AN

AG

IN

G

DI

RE

CT

OR

’S

R

EP

OR

T

D ISTELL ANNUAL REPORT 2004

OverviewWe continued to improve performance across various

dimensions of our business during the year under review,

making considerable progress towards achieving the

important objectives we set ourselves four years ago.These

are:

• To grow our international business

• To capture the true potential of our brands in the

domestic market

• To reduce our cost base through continuous process

improvement in order to fund international expansion,

while simultaneously meeting short-term shareholder

expectations

Although much still needs to be done to fulfil our

aspirations, we can reflect on four years of continuous

improvement.

This year, headline earnings grew 41,0%. Profit before

taxation and exceptional items rose 39,8%, achieving

cumulative annual growth of 21,3% over a three-year

period.

The extremely volatile exchange rates since 2001 have

obviously impacted on our performance, given that we are

a substantial exporter of wines and spirits. Over the past

year alone, the rand strengthened by 16,4% on average

against the currencies of the countries in which we trade

and our performance should be evaluated in this context.

International growthOverseas markets

Our focus is to build a core portfolio of brands in key

markets. Amarula Cream, the company’s biggest spirits

brand and also South Africa’s most widely distributed

alcoholic beverage brand internationally, is a top priority.

In addition, five wine drive brands – Nederburg, Fleur du

Cap,Two Oceans, Durbanville Hills and Drostdy-Hof – are

targeted for growth in nine export markets.

Our international business showed exceptional growth over

the past financial year, reflecting a 30,2% increase in sales

volumes, well in excess of the robust targets we set

ourselves.

Wine volumes grew 33,7%, significantly outperforming the

20% average for the South African wine export industry

over the same period. Moreover, Amarula recorded an

impressive growth of 12,7% in what proved to be a very

competitive cream liqueur category.

Wine volume growth was led primarily by key global drive

brands such as Drostdy-Hof (27%), Two Oceans (32%),

Nederburg (23%) and Fleur du Cap (16%).

Volume gains for these brands were supported by broad

distribution in both European and North American

markets, which responded enthusiastically to these

products.

CONTINUED OVERLEAF

A review of operationsby the managing director

performance &growth

PH

OT

OG

RA

PH

ER

:A

DR

IAA

N O

OS

TH

UIZ

EN

I

NS

PIR

ER

:S

CH

ALK

BU

RG

ER

S

HO

T O

N L

OC

AT

ION

AT

NE

DE

RB

UR

G

21

RE

VI

EW

SM

AN

AG

IN

G

DI

RE

CT

OR

’S

R

EP

OR

T

D ISTELL ANNUAL REPORT 2004

By drawing out the best inpeople through understandingtheir needs, Schalk Burgerinspires exceptionalperformance, finding thebalance between sensitivitiesand the task at hand.

By drawing out the best inpeople through understandingtheir needs, Schalk Burgerinspires exceptionalperformance, finding thebalance between sensitivitiesand the task at hand.

22

RE

VI

EW

SM

AN

AG

IN

G

DI

RE

CT

OR

’S

R

EP

OR

T

D ISTELL ANNUAL REPORT 2004

We also strengthened our presence through listings with

multiple retailers globally, giving us greater product

exposure, although numerous opportunities remain to

be exploited. Our performance and participation in

the multiple grocer distribution environment of the

Netherlands and the United Kingdom, did not meet

expectations. Consequently, new strategies are being

pursued. These include the restructuring of our direct

selling arm in Europe as well as of our agent network

worldwide to capitalise on profitable opportunities.

Amarula Cream’s growth has come from key markets such

as the US, Canada, Germany, Scandinavia, Brazil and the

UK. The brand continued to outperform the category,

notwithstanding increased competition, which saw a

number of new cream liqueur launches and substantial

investments by the major liquor companies.

International sales revenue increased by just 4,3% mainly

due to the strengthening of the rand. Our challenge

remains to protect margins through a continued focus on

achieving greater efficiency throughout the value chain.

Africa

Our Grow Africa Study Project, completed last year,

articulates a clear strategy for the continent. Once again we

are concentrating on four key markets, focusing our

attention on a core portfolio of brands.

Management has started to implement the recommend-

ations flowing from this project, restructuring and

expanding our organisational structures in the regions and

investing in the development of marketing capacity,

establishing marketing teams in a number of African

countries.We also hold a 29,2% stake in African Distilleries

of Zimbabwe, a 40% share in Drinks and Beverages Co in

Mauritius and a 35% share in Tanzania Distilleries Limited.

The Tanzanian company, which produces and distributes a

selection of our brands in its domestic market, continues to

deliver excellent returns to its shareholders. In Kenya we

have entered into agreements with local partners to

manufacture and distribute selections of our brands.

The domestic marketThe domestic market has been characterised by further

trade consolidation, new entrants into the market, surpluses

in the supply of unfortified wines with resultant pressure on

prices and margins, and a substantial increase in excise

duties on wines, spirits and flavoured alcoholic beverages

announced in February 2004.

The domestic market for alcoholic beverages grew by 1,9%

during the past year, beer being the main contributor to this

growth. However, recent statistics indicate that market share

growth in beer has slowed down.

Our task is to capture the true potential of our brands in

the local market, and we accept the challenges we face.We

continue to focus on growing drive brand contributions

in targeted consumer segments. Since favourable trade

relationships are crucial to the success of our strategies, we

have made it a core element of our approach to offer

distinctive value propositions across trade channels that

deliver mutually advantageous benefits. During the year we

continued to focus on:

• Building winning value “key account management” and

“category management strategies”, which are crucial to

favourable customer relationships

• Improving consumer promotion effectiveness across all

consumer segments

• Developing world-class sales, promotion and

merchandising capabilities

Surveys on service levels and customer satisfaction are

regularly undertaken. The most recent of these, in-

dependently undertaken, showed that the vast majority

of our customers rated our service as very good to

excellent.

Our Grow Africa Study Project, completed last year, articulates

a clear strategy for the continent. Once again, we are

concentrating on four key markets, focusing our attention on

a core portfolio of brands.

CONTINUED FROM PAGE 20

23

RE

VI

EW

SM

AN

AG

IN

G

DI

RE

CT

OR

’S

R

EP

OR

T

D ISTELL ANNUAL REPORT 2004

Distell’s overall volumes in the domestic market remained

constant.This was due in part to the loss of the distribution

rights to the Martell and KWV 10 and 20-year-old brandies

in terms of a ruling by the Competitions Tribunal in

June 2003. However, the loss of these brandy trademarks, as

well as a decline in sales volumes of unfortified wines, was

offset by growth elsewhere in the portfolio.

Marketing activity

Distell is the owner of a well-balanced portfolio of

trademarks. Consumer branding is at the heart of

everything we do and starts with marketing strategy as a

driver of business strategy.

Our long-term success depends on our ability to continue

to build and develop a well-balanced portfolio of brands to

satisfy consumer needs. Our approach is to improve market

segmentation, consumer understanding, brand positioning

and investment decision-making, effective market

execution and measuring trade implementation.

Constant innovation is essential in all facets of marketing

and is at the heart of a newly embarked on marketing

renewal programme that seeks to deliver a new excitement

and agility to our brands and our marketing people.

We have introduced improved measures to sharpen our

consumer insights and to manage consumer knowledge,

while a new focus on market activation will also provide

consumers the opportunity to encounter our brands with

greater frequency and impact.

Operational efficienciesOperational management continued to improve

efficiencies, customer service levels, product quality and

cost-effectiveness, with most key performance indicators

showing significant improvement on previous years.

Since effective procurement practices provide the most

important opportunity to reduce our overall cost base, they

remain a top priority. By closely collaborating with key

suppliers we have succeeded in protecting margins

previously eroded by the volatility in the exchange rate.

Some operational highlights were:

• ISO 9001:2000 listings achieved by all our distribution

centres located in South Africa

• A gold medal earned by our distribution arm at the 2004

Logistics Achiever of the Year Awards

• The International Food Standards (IFS) higher-level

certification accorded the Adam Tas cellars, responsible

for a high percentage of export wines. As far as we are

aware, this makes Distell the first South African wine

producer and marketer to attain this IFS level.

• Both Adam Tas and sparkling wine production centre,

JC le Roux received British Retail Certification.

• Global Conformity Services audited JC le Roux and

Nederburg for HACCP and has recommended

certification.

Financial and operational performance

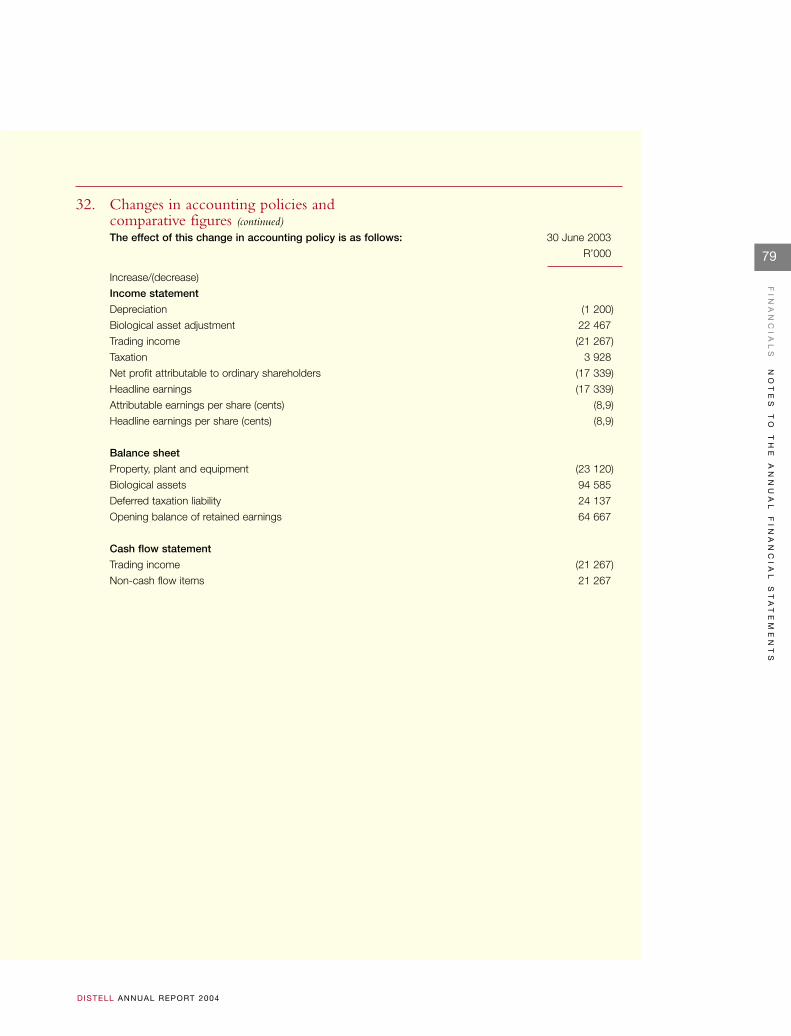

Effect of the change in accounting policyDistell’s accounting policy has been changed to comply

with the new South African Statement of Generally

Accepted Accounting Practice (GAAP) dealing with

Agriculture (AC137). In accordance with this new

statement, vineyards owned by the group must be valued at

fair value. Fair value was calculated by discounting net cash

flows of the vineyards over the balance of their lifespan at

an appropriate discount rate.

The effect of this change in the period under review is

not material. Comparative figures for the year ended

30 June 2003 have been restated, reducing trading income

With empathy, support,clear and unambiguous

communication, and the abilityto ensure that tasks are

completed effectively,Brenda Dlamini (right) creates

a healthy and productiveworking environment.

Colleague Thabile Skwele (left)nominated Brenda as a

true inspirer.

CONTINUED OVERLEAF

24

RE

VI

EW

SM

AN

AG

IN

G

DI

RE

CT

OR

’S

R

EP

OR

T

D ISTELL ANNUAL REPORT 2004

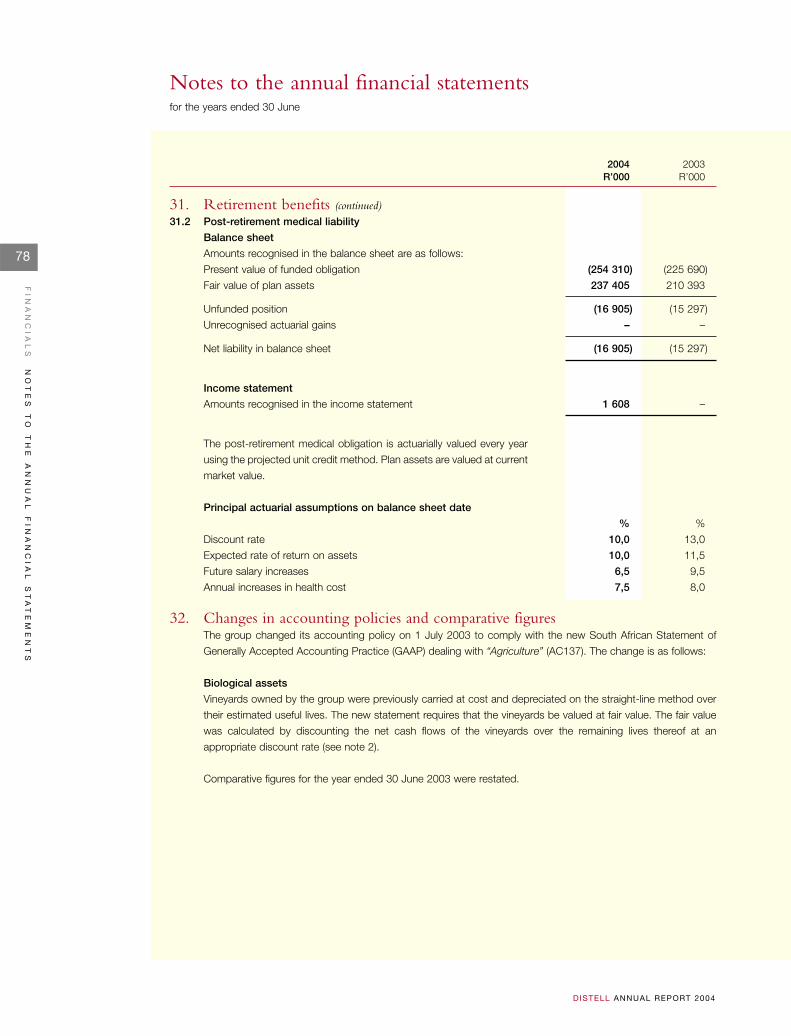

by R21,3 million and headline earnings by R17,4 million.

(See notes 2 and 32 to the financial statements on

pages 59 and 78.)

Sales revenueSales revenue grew 10,7% to R5,7 billion on a sales volume

increase of 1,9%.

Total sales volumes for the second six months of the

financial year showed a strong growth of 5,2% on the

corresponding period of the previous year.

International sales volume growth outpaced sales growth in

the domestic market further improving overall sales mix,

given the increased geographic spread of our activities. Sales

volumes outside South Africa accounted for 18,3%

(2003: 17,1%) of total sales volumes.

Locally, sales volumes showed marginal growth of 0,4% but

reflected a more profitable product mix. Our trademarks in

the important spirits category performed better than our

other categories. Although Distell relinquished its

distribution rights to the Martell brandies at the beginning

of the financial year, and the KWV brandies during the

third quarter, spirit volumes were still able to grow 2,0%. If

Martell sales are excluded, spirit volumes actually showed a

growth of 7,4%, with brandy reflecting an increase of 7,9%.

However, sales volumes of unfortified wine came under

pressure, declining 2,7% because of increased product and

price competition that stemmed from a stronger focus on

the local market by domestic and international players.

Although the market for ready-to-drink alcoholic

beverages (RTDs) remains extremely competitive, Distell

succeeded in achieving marginal volume growth in this

category.

International sales volumes, excluding Africa, increased

30,2%. Volume growth for both Amarula Cream and

unfortified wines accelerated this year. Amarula Cream

achieved volume growth of 12,7% (2003: 8,1%) and

unfortified wines 33,7% (2003: 19,3%). However,

international sales revenue, mainly as a result of the

substantial improvement in the value of the rand, grew

by just 4,3%.

Sales revenue derived from African countries (including

BLNS countries) increased 12,3%.

Trading incomeThe increase in trading income was driven largely by

increased sales revenue, a continued improvement in sales

mix and margins, disciplined cost management and the

containment of overhead costs through ongoing initiatives

to enhance efficiencies across various dimensions of

the business.

Net operating margin, a key performance indicator,

improved from 10,0% to 10,4% notwithstanding the

unfavourable impact of the stronger rand on export

margins.

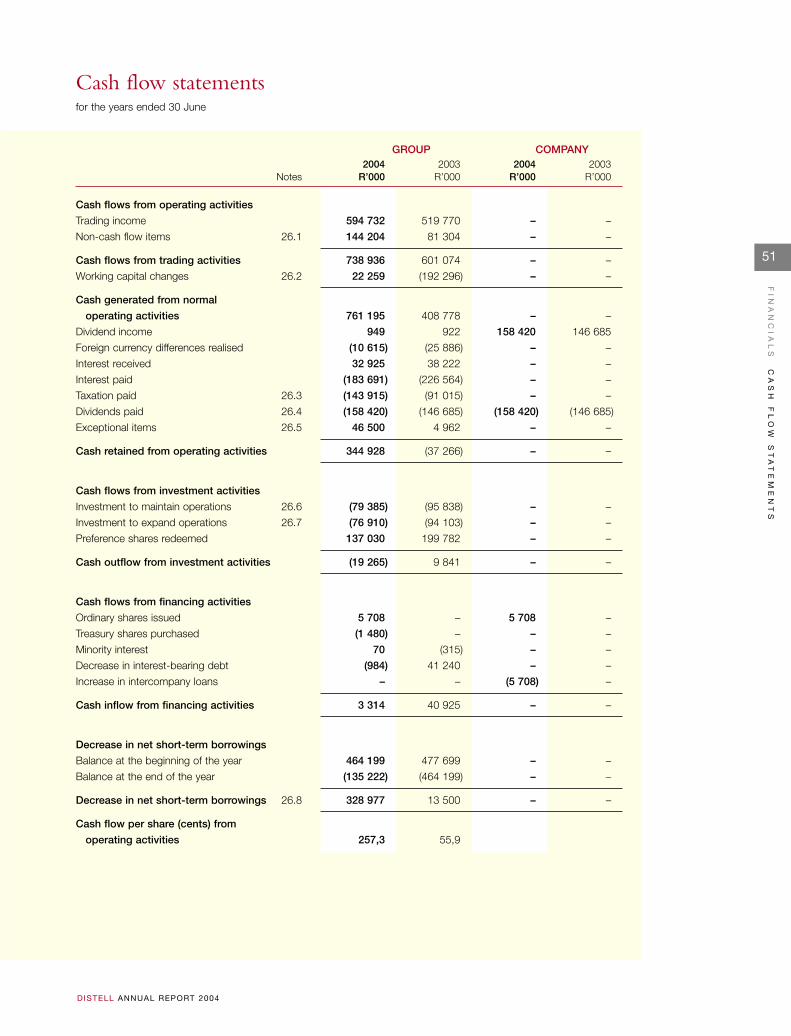

Financing costs and cash flowCash flow from trading activities (before working capital

movements) rose to R738,9 million from last year’s

R601,1 million.

Cash flow from operating activities improved by

R382,2 million, mainly as a result of an increase in trading

income, improved working capital management and an

amount of R46,5 million received as compensation for

relinquishing the distribution rights to Martell brandies

last year.

PH

OT

OG

RA

PH

ER

:A

DR

IAA

N O

OS

TH

UIZ

EN

I

NS

PIR

ER

:B

RU

CE

MO

OD

IE

SH

OT

ON

LO

CA

TIO

N A

T G

OR

DO

N’S

BA

Y

CONTINUED FROM PAGE 23

CONTINUED OVERLEAF

25

RE

VI

EW

SM

AN

AG

IN

G

DI

RE

CT

OR

’S

R

EP

OR

T

D ISTELL ANNUAL REPORT 2004

Bruce Moodie believes that performing under pressuredemands teamwork and that highly effective teams arebuilt through exercising mutual respect, leadership anddeveloping a sense of humour.

26

RE

VI

EW

SM

AN

AG

IN

G

DI

RE

CT

OR

’S

R

EP

OR

T

D ISTELL ANNUAL REPORT 2004

We continue to invest in global markets to build our

brands as part of a profitable growth strategy and look

forward to increased sales in an improved global

economic climate.The group substantially reduced fixed investment spend,

with investment to maintain and expand operations

amounting to R161,2 million (2003: R195,8 million).

The group generated net cash flow of R188,6 million, and

net financing costs, as a result, decreased by R23,4 million

to R94,8 million.

Interest cover, which is net interest paid in relation to profit

before interest and taxation, improved from 3,9 to

6,1 times.

Foreign currency movementsAny change in the rate of exchange between transaction

date and settlement or period-end date is disclosed

separately in the income statement in terms of GAAP.

During the period under review a loss of R24,9 million

(2003: R66,8 million) was reflected in this regard.

TaxationThe effective tax rate increased from 21,6% to 25,7%,

mainly as a result of non-taxable income included under

exceptional items the previous year.

Headline earningsHeadline earnings increased by 41,0% to R358,6 million.

This growth is largely attributable to growth in trading

income of 14,4%, and a reduction in financing costs and

foreign currency conversion losses. However, if the effect of

the change in accounting policy is excluded, headline

earnings grew 32,0%.

DividendsThe directors have resolved to declare dividend number

32 of 51 cents (2003: 35 cents) per share, making a total

dividend of 97 cents per share for the year ended

30 June 2004 (2003: 75 cents). This dividend represents a

dividend cover of 1,9 times (2003: 1,7 times) by headline

earnings.

Details regarding dividend payment dates and related

matters are disclosed in note 25 to the financial statements.

Investment and fundingTotal assets increased R108,5 million to R4,8 billion, an

increase of 2,3% on the previous year.

Capital expenditure amounted to R161,2 million. Of this,

R37 million was spent on the second and final phase in the

expansion and upgrade of the Nederburg cellar in Paarl to

support the continued growth of the brand domestically

and internationally.

Management’s focus on the systematic reduction in working

capital is reflected in an overall reduction of R22,3 million.

The increase in inventory, mainly as a result of an increase in

bulk wines and spirits, is necessitated by the group’s long-term

view of consumer demand for its products.The investment in

bulk inventories under maturation is planned accordingly.

Net interest-bearing liabilities were reduced from

R733,9 million to R485,9 million at 30 June 2004. Net

interest-bearing liabilities relative to net cash inflow from

normal operating activities improved to 0,64 from a level of

1,80 at the prior year-end.The group’s gearing, as measured

by net interest-bearing debt relative to net assets, decreased

at year-end to 18,9% from last year’s 31,1%.The group has

substantial unutilised borrowing facilities.

Legal and legislative issuesAs announced on 12 December 2003, the appeal by the

Competition Commission against certain findings of the

Competition Tribunal in the merger between Distillers

Corporation (SA) Limited and Stellenbosch Farmers’

Winery Group Limited was dismissed in a judgment

handed down by the Competition Appeal Court on

11 December 2003.

In September 2003, the National Assembly approved the

new Liquor Bill, which accommodates the industry’s

CONTINUED FROM PAGE 24

27

RE

VI

EW

SM

AN

AG

IN

G

DI

RE

CT

OR

’S

R

EP

OR

T

D ISTELL ANNUAL REPORT 2004

concerns, and in particular allows companies to hold

licences in both manufacturing and distribution. There is

to be an automatic conversion of existing licences and

licence holders must demonstrate within 12 months

thereafter that they meet certain criteria set by the Minister

of Trade and Industry.We believe these criteria are sound.

During the legislative process the Government committed

itself to ensuring the Bill would not adversely affect the

industry’s efficiency.

ProspectsManagement continues to focus resources on the

important strategic initiatives required to achieve our goals

of growing international business, capturing the full

potential of our brands domestically and reducing our cost

base to be competitive wherever we trade.To this end, we

have introduced a formal process to regularly monitor and

report on progress achieved and to provide for special

interventions so that major initiatives do deliver on target.

The domestic market is likely to remain extremely

competitive in the near term but a favourable medium to

longer-term outlook for the South African economy leads

us to believe consumer demand for alcoholic beverages will

strengthen, driven in part by lower inflation and interest

rates.

We continue to invest in global markets to build our brands

as part of a profitable growth strategy and look forward to

increased sales in an improved global economic climate.

We are confident Distell is well positioned to capture

opportunities in domestic and foreign markets and the

group expects to continue to reflect real growth in

earnings and has budgeted accordingly.

JJ Scannell

Managing director

16 August 2004

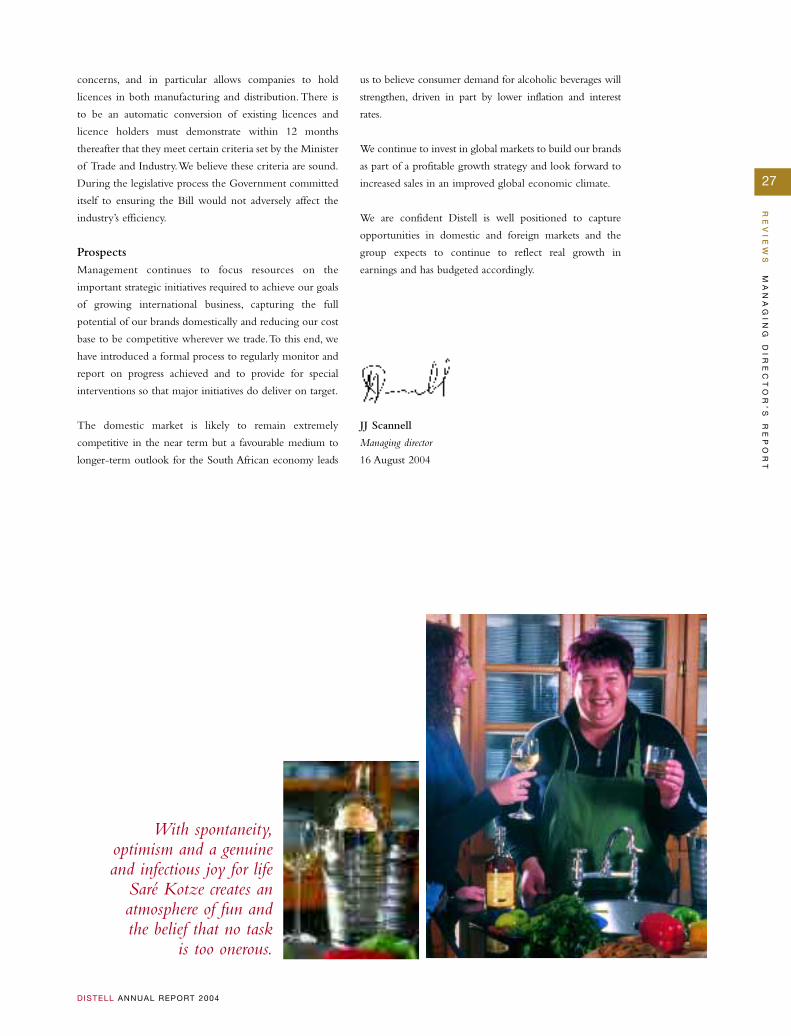

With spontaneity,optimism and a genuineand infectious joy for life

Saré Kotze creates anatmosphere of fun andthe belief that no task

is too onerous.

28

SO

CI

AL

CO

RP

OR

AT

E

GO

VE

RN

AN

CE

D ISTELL ANNUAL REPORT 2004

Corporate governance reportCorporate governance, critically important to Distell’s

success as a business and in protecting the interests of its

shareholders, is managed and monitored by the company’s

board of directors and several of its subcommittees.

The directors are unreservedly committed to the principles

of good governance and to this end accept full

accountability in applying the necessary disciplines in

maintaining the highest standards of professionalism,

integrity, independence, fairness and social responsibility,

and they acknowledge their accountability to all

stakeholders. Transparency in the management process

gives shareholders and other interest groups the assurance

that the group is managed according to ethical norms and

international best practice within the boundaries of

prudently determined risk parameters.

The board is of the opinion that the group substantially

complies with all the significant principles incorporated in

the Code of Corporate Practices and Conduct, as set out

in the second King Report (King II) and the JSE Securities

Exchange Listings Requirements.

Board of directorsThe board evaluates and reviews the strategic direction of

the group, agrees on key performance indicators and

identifies key risk areas and responses. Executive

management is then charged with the detailed planning

and implementation of these strategies in accordance with

appropriate risk parameters.

The board holds management accountable for its activities,

which are monitored and controlled through regular

reports and discussions. In this way the board is able to:

• Retain full and effective control over the group, and

monitor management’s implementation of planning

strategies

• Review the performance of executive management

against business plans, budgets and industry standards

• Consider significant financial matters, including

investment decisions

• Identify, consider, monitor and, if appropriate, approve

financial and non-financial matters relevant to the

business of the group

• Ensure a comprehensive system of policies, procedures

and controls is operative and adhered to

• Ensure sound governance, including compliance with

relevant laws and regulations, audit and accounting

principles and the group’s internal governing documents

and codes of conduct

• Define levels of materiality, hold certain powers and

delegate other matters with the necessary written

authority and terms of reference to management or

board committees

• Be aware of and commit to the underlying principles of

good corporate governance, monitor and maintain

compliance

The board is chaired by independent, non-executive

director DM Nurek and comprises 11 non-executive

directors (of whom eight are independent) and threeP

HO

TO

GR

AP

HE

R:

AD

RIA

AN

OO

ST

HU

IZE

N

IN

SP

IRE

R:

DU

RA

ND

T V

AN

AS

WE

GE

N

SH

OT

ON

LO

CA

TIO

N A

T L

E B

ON

HE

UR

CONTINUED OVERLEAF

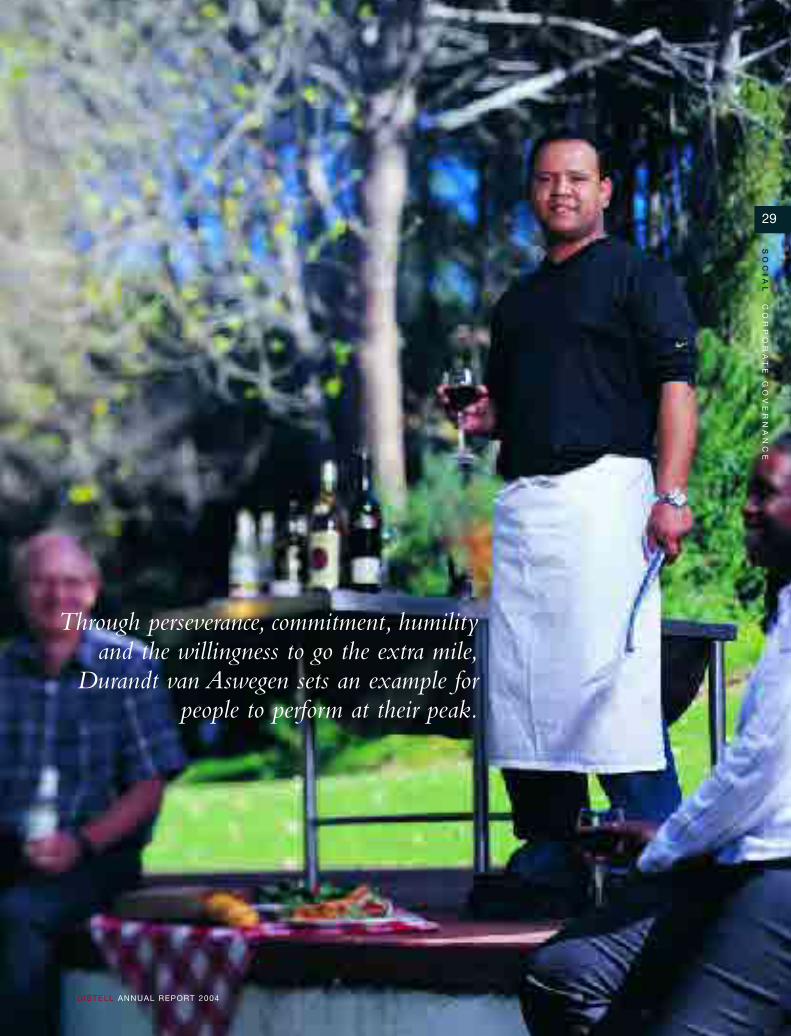

duty-bound Adhering to the principles of sound

corporate governance

Through perseverance, commitment, humilityand the willingness to go the extra mile,

Durandt van Aswegen sets an example forpeople to perform at their peak.

29

SO

CI

AL

CO

RP

OR

AT

E

GO

VE

RN

AN

CE

D ISTELL ANNUAL REPORT 2004

30

SO

CI

AL

CO

RP

OR

AT

E

GO

VE

RN

AN

CE

D ISTELL ANNUAL REPORT 2004

executive directors, including the managing director. The

roles of the chairman and managing director are separated

with responsibilities divided between them.The chairman

has no executive functions.

Non-executive directors, appointed for their knowledge

and experience of a wide range of businesses and business

sectors, augment the skills and experience of the executive

directors and management and contribute independent

viewpoints to matters under consideration. All directors

have the appropriate knowledge and experience necessary

to fulfil their duties and enjoy significant influence at

meetings.This ensures a balance of authority and precludes

any one director from exercising unfettered powers of

decision-making.

Generally, directors have no fixed term of appointment but

retire by rotation. At each annual general meeting of the

company, a third of the directors (those longest in office

since their last election) retire and, if available, are

considered for reappointment.

Procedures for appointments to the board are formal and

transparent and a matter for the board as a whole. The

board is always mindful of the need to maintain an infusion

of fresh thinking and a relevant mix of skills and

experience.

The effectiveness of the board composition and the

performance of all its directors, including the chairman, are

assessed annually.

Non-executive directors receive no share options, nor

material benefits from Distell, other than their directors’

fees.

All board members are required to disclose the extent of

their shareholdings in Distell, other directorships and any

potential conflict of interest. It is incumbent on directors to

act in the best interests of the company at all times.Where

a potential conflict of interest does exist, they are expected

to recuse themselves from relevant discussions and

decisions.

Directors and other nominated employees are required to

advise and obtain clearance from the chairman before

dealing in Distell shares. The chairman will withhold

clearance during a closed period or any period when there

exists unpublished, price-sensitive information in relation

to the company shares.

The board convenes at least every two months to review a

formal schedule of matters for which its members are fully

briefed in advance. Effective chairmanship and a formal

agenda ensure that all issues requiring attention are raised

and addressed. This enables directors to discharge their

responsibilities in determining if prescribed functions have

been carried out according to set standards within the

boundaries of prudent, predetermined risk levels and in

line with international best practice.

Adequate “Directors and Officers” insurance cover has

been purchased by the company to meet any material

claims against directors and officers.

In addition, all directors have unlimited access to the

advice of the company secretary, who acts as an adviser to

the board and its subcommittees on issues, including

compliance with group rules and procedures, statutory

regulations and with the King II. Independent professional

advice is available to directors in appropriate circumstances

at the company’s expense.

The names and credentials of the directors and their

attendance at board meetings are detailed on page 8.

Board subcommitteesSpecific responsibilities have been delegated to board

committees, with defined terms of reference from

approved charters.All chairs of committees report orally on

the proceedings of their committees at the subsequent

board meeting and minutes of committee meetings are

provided to the board.The principal board committees are

as follows:

The audit and risk committeeThe audit and risk committee regularly evaluates the

group’s exposure and responses to significant business,

strategic, statutory and financial risks and reviews:

• the effectiveness of risk management processes; and

• the appropriateness and adequacy of the systems of

internal financial and operational controls.

The committee also reviews and evaluates accounting

policies and financial information issued to the public, to

ensure appropriate standards of governance and reporting

are maintained.

The audit and risk committee is responsible for

recommending the appointment of the external auditors,

determines their fees and assesses the performance of

internal as well as external auditors. The committee also

ensures effective communication between directors,

management and internal and external auditors. The risk

CONTINUED FROM PAGE 28

31

SO

CI

AL

CO

RP

OR

AT

E

GO

VE

RN

AN

CE

D ISTELL ANNUAL REPORT 2004

management workgroup assists the audit and risk

committee with its risk management function.

The audit and risk committee comprises three non-

executive directors, whose details are provided on page 8.

The committee is chaired by Mr D Prins, an independent

non-executive director. The chairman of the board does

not act as chairman of the audit and risk committee.

The committee meets at least four times a year. The

external auditors, the managing director, the financial

director and the company secretary are in attendance at

each meeting and other members of the management

team, including internal audit representatives, attend as

required. However, when issues are raised with the external

auditors in which executive attendees have a vested

interest, the latter recuse themselves.

Audit and risk committee members, as well as the internal

and external auditors, have unlimited access to whatever

information they require in discharging their

responsibilities. Moreover, the internal and external

auditors have unlimited access to the chairman.

The internal audit department reports directly to the audit

and risk committee and is also responsible to the financial

director on day-to-day matters. The managing director is

copied on all significant reports which are then discussed

with him.

The remuneration committeeThe remuneration committee is responsible for the

assessment and approval of a broad remuneration strategy

for the group, including short and long-term incentive pay

structures for executive management.These remuneration

strategies are aimed at rewarding employees at market-

related levels and in accordance with their contribution to

the group’s operating and financial performance in terms

of basic pay as well as short and long-term incentives. To

promote identification with shareholders’ interests, share

incentives are considered a critical element of executive

incentive pay.

The committee determines the remuneration of executive

and non-executive directors and senior management.

The remuneration committee is responsible for the

identification, assessment and nomination of potential new

directors. During the year it nominated Prof GJ Gerwel

and Messrs PM Bester and MJ Botha. New directors are

provided with suitable induction material designed to

familiarise them with all aspects of the business.

The remuneration committee consists of three non-

executive directors, whose details are provided on page 8,

and is chaired by Mr DM Nurek.

In compliance with its charter the committee met five

times during the year.

Accountability and auditInternal auditThe mandate of the group’s internal audit function

operates in terms of the audit and risk committee’s

approved charter to provide management with an

independent, objective consulting and assurance service

that reviews matters relating to control, risk management,

corporate governance and operational efficiency.

The primary mandate of the group’s internal auditors is to

examine and evaluate the effectiveness of operational

activities, the attendant business risks and the effectiveness

of the system of internal operational and financial control

to manage such risks and to bring material deficiencies,

instances of non-compliance and development needs to

the attention of management, the external auditors and the

audit and risk committee for resolution. In particular, the

internal audit function assesses the relevance, reliability and

The group’s exposure and responses to significant

business, strategic, statutory and financial risks and reviews

are regularly evaluated.

CONTINUED OVERLEAF

32

SO

CI

AL

CO

RP

OR

AT

E

GO

VE

RN

AN

CE

D ISTELL ANNUAL REPORT 2004

integrity of management and financial information, the

efficient and economic use of resources, the safeguarding of

assets, compliance with relevant policies, procedures, laws

and regulations and the prevention of waste, extravagance

and fraud.

The function of the group’s internal audit is also to provide

a risk management facilitation role, ensuring the process of

risk management is always accorded the highest priority,