Distant but close: The Impact of Immigrant Remittances on Latin America Manuel Orozco,...

156

The Impact of Immigrant The Impact of Immigrant Remittances on Latin Remittances on Latin America America Manuel Orozco, Manuel Orozco, Inter-American Dialogue Inter-American Dialogue May 30 May 30 th th 2005 2005

-

date post

21-Dec-2015 -

Category

Documents

-

view

217 -

download

3

Transcript of Distant but close: The Impact of Immigrant Remittances on Latin America Manuel Orozco,...

Distant but close:Distant but close:The Impact of Immigrant The Impact of Immigrant Remittances on Latin Remittances on Latin AmericaAmerica

Manuel Orozco, Manuel Orozco,

Inter-American DialogueInter-American Dialogue

May 30May 30thth 2005 2005

The Geography of migration and The Geography of migration and remittances: distant proximities remittances: distant proximities

through transnationalismthrough transnationalism

AsiaJapanHong Kong

PhilippinesChinaIndiaSingaporeVietnamThailandMalaysia

AfricaSouth AfricaCongoGhana

MoroccoMalawiEthiopiaMozambiqueLesothoSwaziland

AmericaUnited StatesCanadaBrazil

MexicoEl SalvadorDom. Rep.EcuadorJamaicaCubaColombiaParaguayVenezuelaHaiti

EuropeFranceU.K.GermanyItalyBelgium

SpainTurkeyAlbaniaArmeniaGreecePortugal

OceaniaAustraliaNew Zealand

Middle EastUnited Arab Em.Saudi ArabiaKuwait

JordanEgypt

GDP: (X-M) + I + G + C

-DOMESTIC SAVINGS - INVESTMENT-FOREIGN SAVINGS - INVESTMENT

-FDI: Transnational capital, migrant capital investment-TECHNOLOGY TRANSFER-UNILATERAL TRANSFERS

-ODA- BILATERAL & MULTILATERAL-PRIVATE DONATIONS

FOUNDATIONS, PPOs, HTAs-WORKER REMITTANCES

-Maquila, Tourism, Non-traditional exports-Transportation, Telecommunication, Nostalgic Trade

The national income equation in Latin America: a The national income equation in Latin America: a rent seeking and courtesan state?rent seeking and courtesan state?

Immigrant economic practices (annual expenses)

ConsumptionDonationsFamily remittancesCapital investment

Household economy (US$270)

Community(US$10,000 year)

Trade and services retail(US$3,000) Property

and other I(US$5,000)

Main remittance recipient countries worldwideMain remittance recipient countries worldwide

$0.00 $2,000,000,000.00 $4,000,000,000.00 $6,000,000,000.00 $8,000,000,000.00 $10,000,000,000.00 $12,000,000,000.00

India

Mexico

Philippines

Brazil

Morocco

Egypt, Arab Rep.

Turkey

El Salvador

Bangladesh

J ordan

Dominican Republic

Colombia

Yugoslavia, Fed. Rep.

Yemen, Rep.

Ecuador

Cuba

Sri Lanka

Pakistan

Indonesia

J amaica

Haiti

Albania

Croatia

Nicaragua

Guyana

Cape Verde

Tonga

Belize

Remittances per capita (2001)Remittances per capita (2001)

522363

360299

213

194176

169159

157134

130112110

106100

90

8581

60

4641

41

14

11

8

75

$0 $100 $200 $300 $400 $500 $600

Tonga

J amaica

J ordan

El Salvador

Dominican Republic

Albania

Cape Verde

Belize

Yugoslavia, Fed. Rep.

Guyana

Nicaragua

Croatia

Morocco

Ecuador

Cuba

Haiti

Mexico

Yemen, Rep.

Philippines

Sri Lanka

Egypt, Arab Rep.

Colombia

Turkey

Bangladesh

India

Pakistan

Brazil

Indonesia

The Latin American The Latin American contextcontext

The level of engagementThe level of engagement

The 5TsThe 5Ts

Remittances to Latin America and the Remittances to Latin America and the Caribbean by Region (%)Caribbean by Region (%)

Caribbean, $6,248, 14%

Central America, $7,791, 17%

Mexico, $16,613, 37%

South America, $14,629, 32%

US$ 45.2 billion

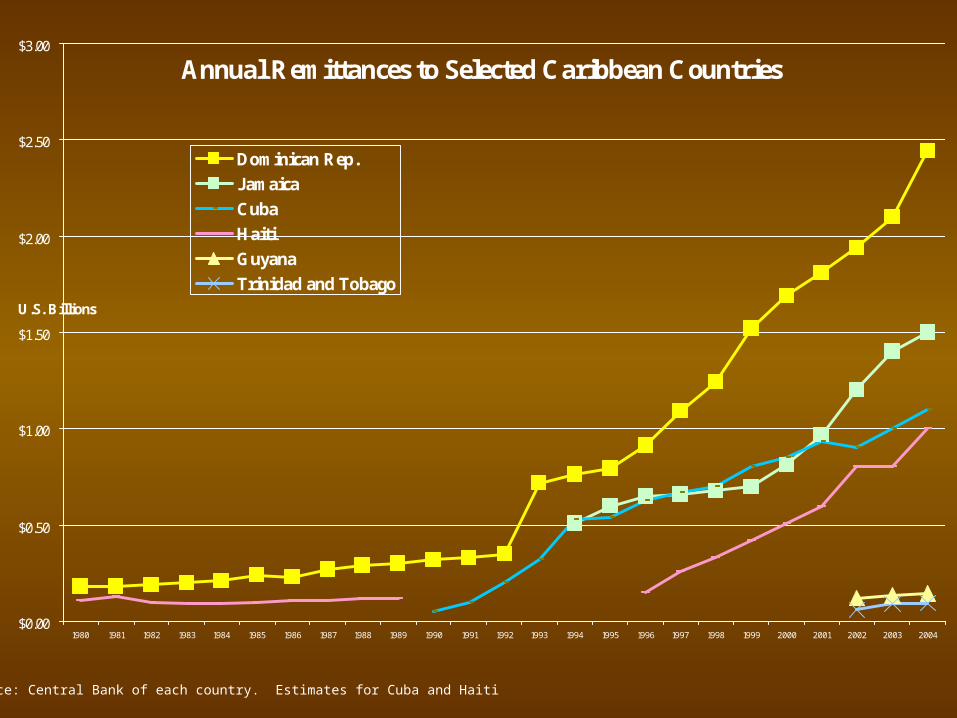

Annual Remittances to Selected Caribbean Countries

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

U.S. Billions

Dominican Rep.

Jamaica

Cuba

Haiti

Guyana

Trinidad and Tobago

Source: Central Bank of each country. Estimates for Cuba and Haiti

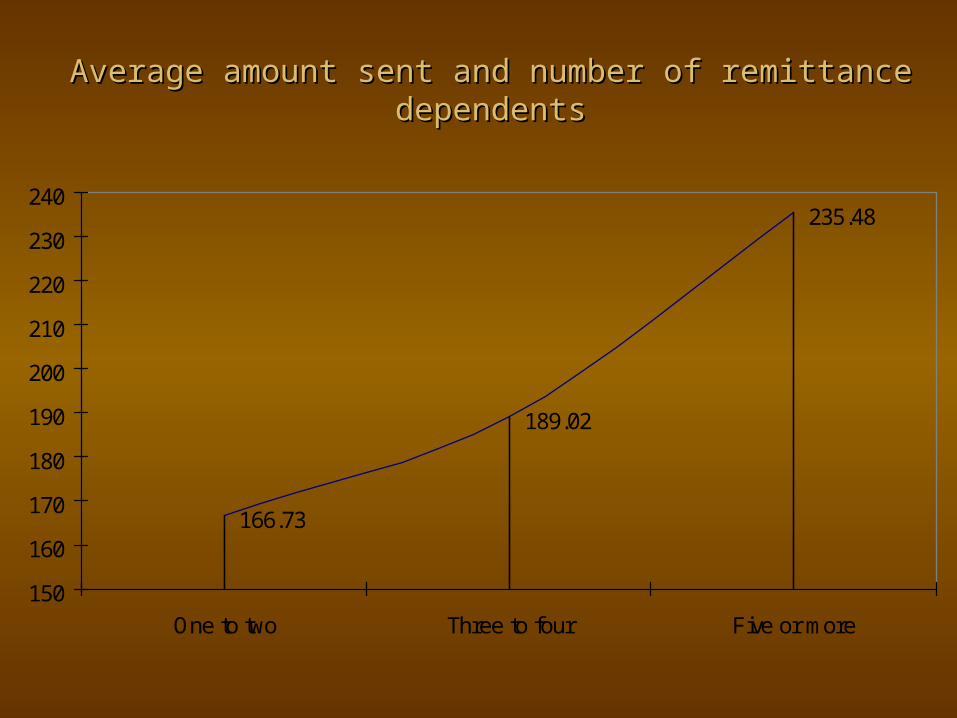

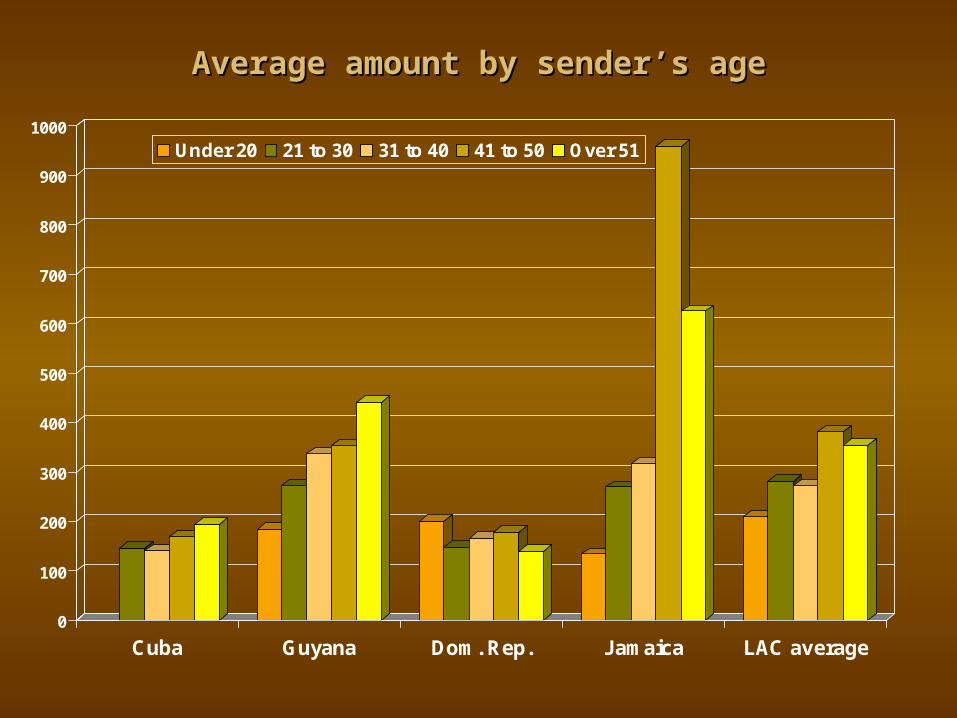

Commitment to families . . .Commitment to families . . .Average amount sent and number of remittance dependents

166.73

189.02

235.48

150

160

170

180

190

200

210

220

230

240

One to two Three to four Five or more

Length of Commitment . . .Length of Commitment . . .Average amount sent and length of time living in U.S.Average amount sent and length of time living in U.S.

140

240

340

440

540

640

740

840

940

Less than one year One to three Four to six Seven to nine Over ten

Jamaica Guyana Other Latin Americans

130

150

170

190

210

230

250

270

290

Less than one year One to three Four to six Seven to nine Over ten

Dominican Cuba Other Latin Americans

Percent of remittance senders who . . .Percent of remittance senders who . . .

55

5

9

3

62

22

38

61

5

55

20

20

12

58

38

36

73

1

63

33

43

40

16

66

54

67

75

21

52

46

37

19

26

77

39

41

48

16

52

16

21

6

3

47

21

59

60

12

63

Is a U.S. Citizen

Earns over US$35,000

Have completed theUniversity

Belong to an HTA

Have a bank account

Have debit or credit cards

are 35 or younger

Household have 3 or lesspeople

Send more than 500

Are males

Other Latin America

Guyana

Jamaica

Cuba

Dominican Republi

Jamaicans: younger with formal education, Bank accounts, higher income and live in smaller households

Caribbean immigrant home country engagement Caribbean immigrant home country engagement seems greater than other Latin immigrants . . .seems greater than other Latin immigrants . . .

Percent of immigrant remitters who . . . D.R. Cuba Jamaica GuyanaOther

L.A.

Travel at least once a year 69 13 69 45 24

Spends more than one thousand dollars per stay 64 50 52 54 62

Call at least once a week 77 48 73 42 62

Buys home country goods 65 29 64 84 78

Helps family meet other financial needs 14 9 33 47 19

Helps family pay for mortgage loans 13 1 16 21 12

Has a mortgage loan in home country 6 2 15 18 10

Has a bank account in home country 29 2 58 48 22

Has a small family business in home country 3 2 2 8 3

Effects and trends in Effects and trends in home countryhome country

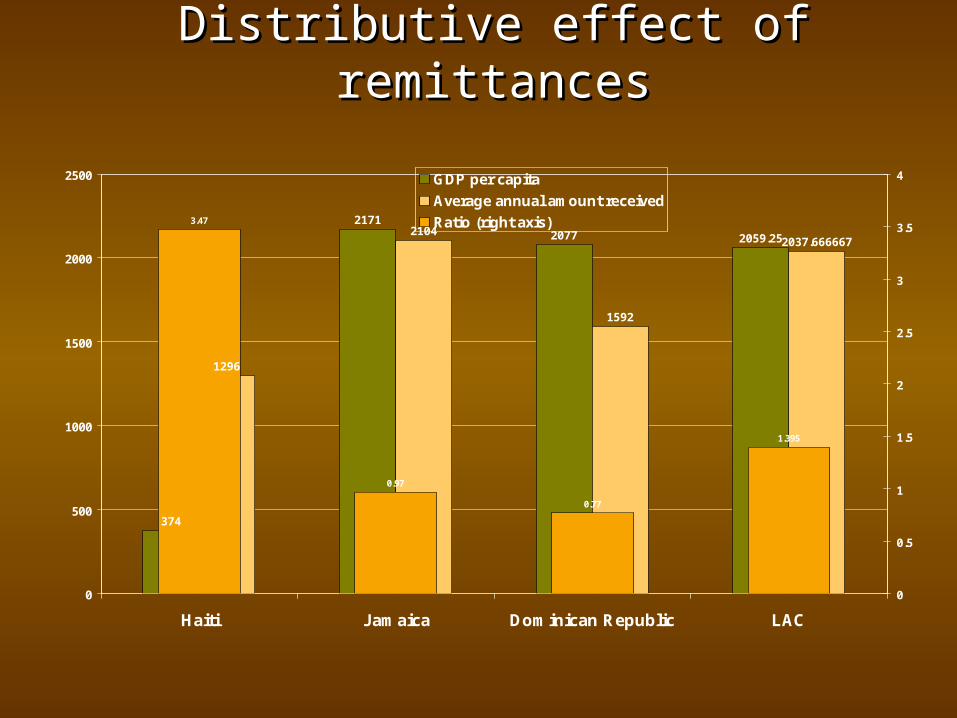

Distributive effect of remittancesDistributive effect of remittances

374

21712077 2059.25

1296

2104

1592

2037.666667

3.47

0.97

0.77

1.395

0

500

1000

1500

2000

2500

Haiti Jamaica Dominican Republic LAC

0

0.5

1

1.5

2

2.5

3

3.5

4GDP per capita

Average annual amount received

Ratio (right axis)

Remittance recipient householdsRemittance recipient households

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

México El Salvador Nicaragua R.D. Guyana Ecuador

UrbanaRural

Source: El Salvador, Honduras and Guatemala: Bendixen and Associates survey; Dominican Republic: Emmanuel Sylvestre & Associates survey (commissioned out by the author); Guyana: Laparkan Trading survey (commissioned out by the author); Ecuador: Mauricio Orbe (PulsoEcuador); Mexico: El Colegio de la Frontera Norte. “Problemas y Perspectivas de las Remesas de los Mexicanos y Centroamericanos en Estados Unidos,” El Colegio de la Frontera Norte: Departamento de Estudios Económicos. Mexico: 2002, p. 30.

Female remittance recipients (%)Female remittance recipients (%)

64

65

66

67

68

69

70

71

72

73

Female

REPUBLICA DOMINICANA GUYANA JAMAICA CUBA LAC average

Remittance recipient (relationship)Remittance recipient (relationship)

0

5

10

15

20

25

30

Spouse Children Parents Sibblings Other

REPUBLICA DOMINICANA CUBA GUYANA Total

Phone calls to selected Latin American countriesPhone calls to selected Latin American countries

0.7

0.3

0.5

0.6

0.7

0

200,000,000

400,000,000

600,000,000

800,000,000

1,000,000,000

1,200,000,000

El Salvador Guatemala Honduras Dominican Rep. Jamaica

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

Total minutes (2003 est.)

Household-to-household minutes (2003)

Ratio

Source: Encuesta de inmigrantes en New York; US Census Bureau; 2000 and 2001 International Telecommunications Data, Linda Blake and Jim Lande. Washington, FCC, December 2001, and January 2003. * calculo basedo en un promedio de 4 llamadas al mes por 5, 8, 15, 25 y 30 minutos por llamada Formula utilizada es ∑ de llamadas = minutos anuales * Porciento que llama * Porcentaje inmigrantes que remiten (Censo 2000 de pobl.)

$0

$20,000,000

$40,000,000

$60,000,000

$80,000,000

$100,000,000

$120,000,000

$140,000,000

El Salvador Guatemala Honduras Dominican Rep. Jamaica

U.S. revenue Payment to country

Goods bought by Guyanese diasporaGoods bought by Guyanese diaspora

62%

58%

51%

49%

47%

46%

42%

38%

36%

32%

32%

29%

27%

25%

22%

21%

0% 10% 20% 30% 40% 50% 60% 70%

Spices (curry, )

Fresh Fish

Peppers

Salted Fish

Noodles

Fresh Fruits and vegetables

Rum

Peas

Processed fruit

Sugar

Other

Cook utensils

Pickles

Craft Items

Cigarettes

Confectioneries

Products bought by Jamaicans in the U.S.Products bought by Jamaicans in the U.S.

0 20 40 60 80 100

OTHER

PEAS

SUGAR

NOODLES

CRAFT ITEMS

SALTED FISH

PICKLES

COOKING UTENSILS

FRESH FISH AND SHRIMP

CIGARETTES

PEPPERS

CONFECTIONERIES

FRESH FRUITS AND VEGETABLES

RUM

PROCESSED FRUIT

SPICES

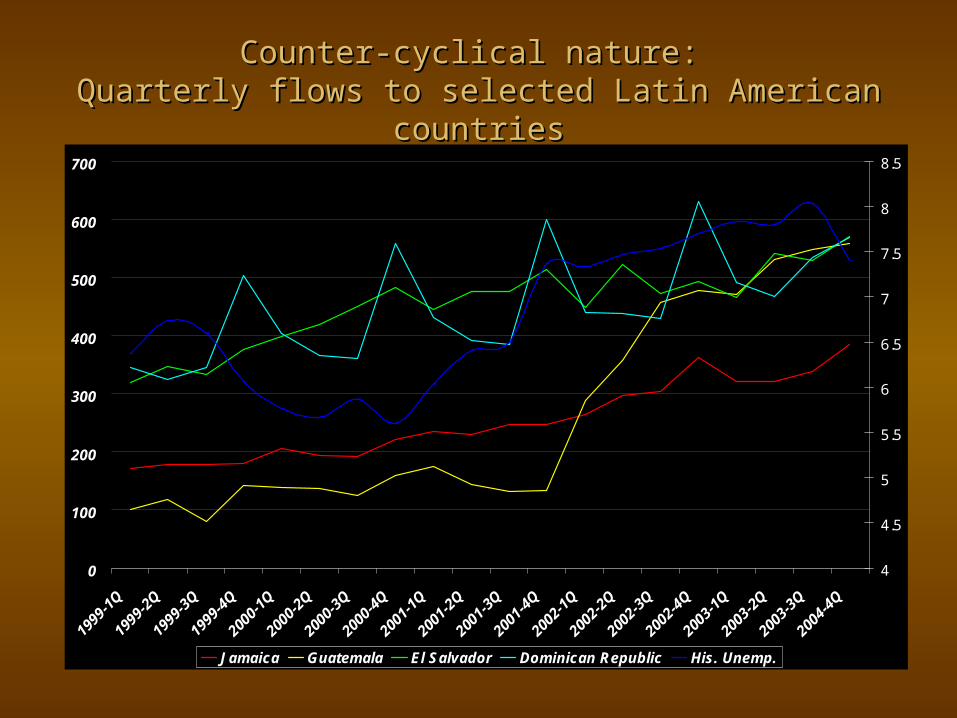

Counter-cyclical nature: Counter-cyclical nature: Quarterly flows to selected Latin American countriesQuarterly flows to selected Latin American countries

0

100

200

300

400

500

600

700

1999

-1Q

1999

-2Q

1999

-3Q

1999

-4Q

2000

-1Q

2000

-2Q

2000

-3Q

2000

-4Q

2001

-1Q

2001

-2Q

2001

-3Q

2001

-4Q

2002

-1Q

2002

-2Q

2002

-3Q

2002

-4Q

2003

-1Q

2003

-2Q

2003

-3Q

2004

-4Q

4

4.5

5

5.5

6

6.5

7

7.5

8

8.5

Jamaica Guatemala El Salvador Dominican Republic His. Unemp.

90

110

130

150

170

190

210

230

250

1/1/1999 5/1/1999 9/1/1999 1/1/2000 5/1/2000 9/1/2000 1/1/2001 5/1/2001 9/1/2001 1/1/2002 5/1/2002 Sept. 2002 1/1/2003 5/1/2003 9/1/2003 Jan.04 May. 04

15

20

25

30

35

Remittances (left axis)

Consumer Prices (left axis)

FX (right axis)

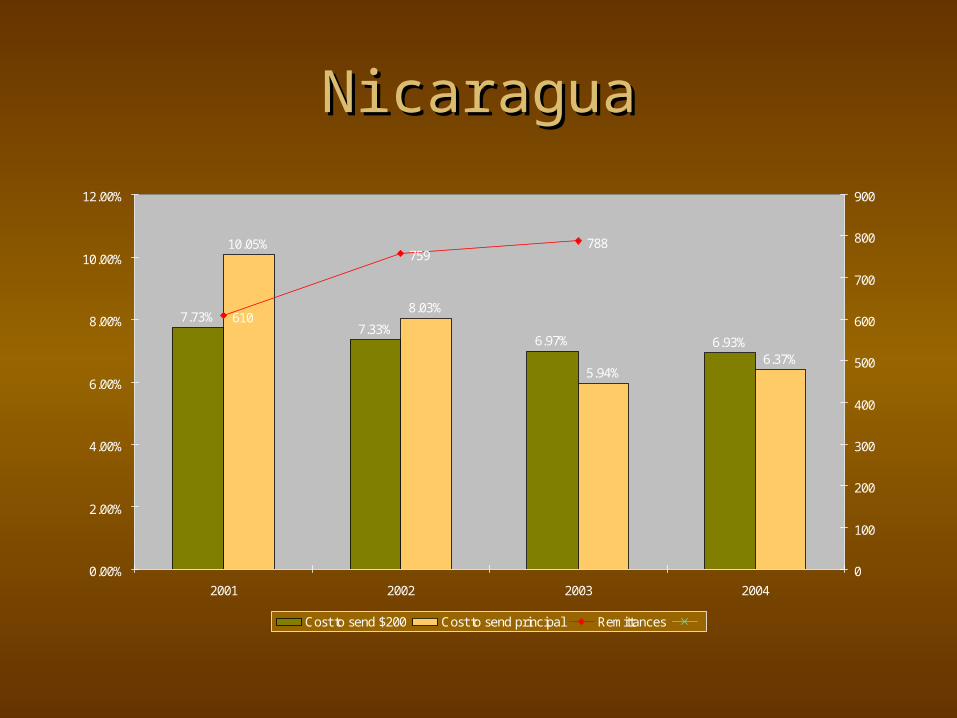

Dominican Republic: Remittances, prices, interest and exchange rates

Foreign Foreign ExchangeExchange

Current Current Price IndexPrice Index

Interest Interest LendingLending RateRate

Hispanic Hispanic UnemploymentUnemployment

-0.507-0.507 0.46 ***0.46 *** -0.105-0.105 0.1790.179

.09 ***.09 ***R2 = 0.54 adjusted R2 = 0.29, statistical significance p< .10 * , p < 0.05 **, p < 0.01 ***

•Home country variations in exchange rates and unemployment in the U.S. among Latinos do not have an effect on transfers. •Market of transfers occur independently from exchange rate variations: under the economic crisis affecting devaluation, remittance transfers, and the control of its volume by companies, were not related to exchange rates.•Remittances responded specifically to changes in prices

Jamaica: Macroeconomic determinantsJamaica: Macroeconomic determinants

0

50

100

150

200

250

1/1/

1999

3/1/

1999

5/1/

1999

7/1/

1999

9/1/

1999

11/1

/199

9

1/1/

2000

3/1/

2000

5/1/

2000

7/1/

2000

9/1/

2000

11/1

/200

0

1/1/

2001

3/1/

2001

5/1/

2001

7/1/

2001

9/1/

2001

11/1

/200

1

1/1/

2002

3/1/

2002

5/1/

2002

Jul.

2002

Sept.

2002

Dec. 2

002

2/1/

2003

4/1/

2003

6/1/

2003

8/1/

2003

Oct

. 200

3

Dec. 2

003

0

10

20

30

40

50

60

70

Remit cpi FX lending

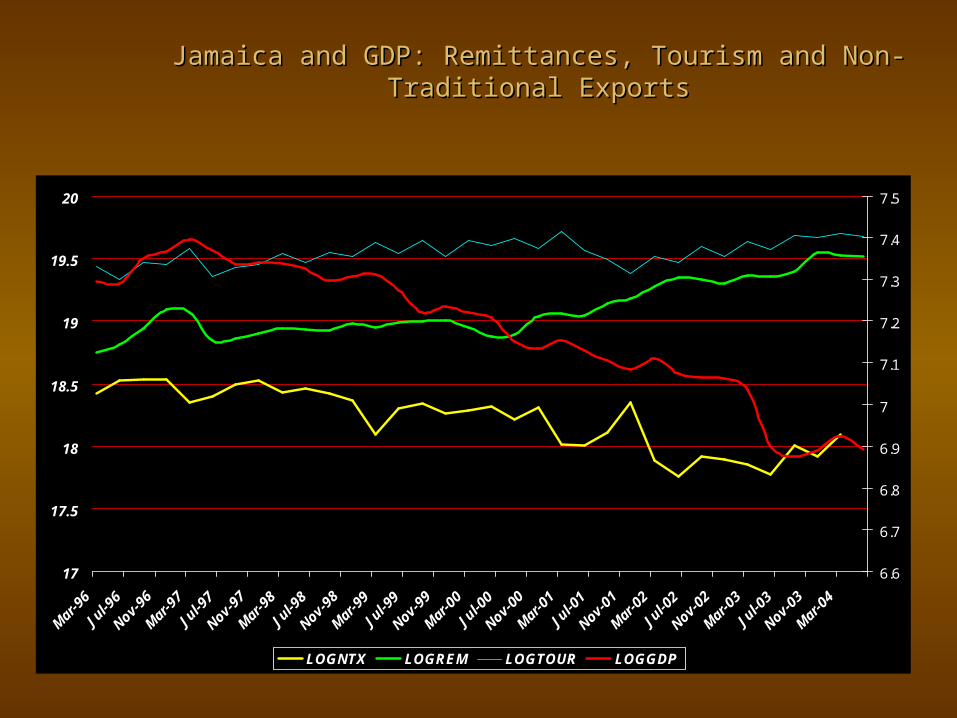

Jamaica and GDP: Remittances, Tourism and Non-Traditional ExportsJamaica and GDP: Remittances, Tourism and Non-Traditional Exports

17

17.5

18

18.5

19

19.5

20

Mar

-96

Jul-9

6

Nov-96

Mar

-97

Jul-9

7

Nov-97

Mar

-98

Jul-9

8

Nov-98

Mar

-99

Jul-9

9

Nov-99

Mar

-00

Jul-0

0

Nov-00

Mar

-01

Jul-0

1

Nov-01

Mar

-02

Jul-0

2

Nov-02

Mar

-03

Jul-0

3

Nov-03

Mar

-04

6.6

6.7

6.8

6.9

7

7.1

7.2

7.3

7.4

7.5

LOGNTX LOGREM LOGTOUR LOGGDP

Levels and determinants Levels and determinants of Engagementof Engagement

Comparisons among Latin Comparisons among Latin American and Caribbean American and Caribbean immigrants in the U.S.immigrants in the U.S.

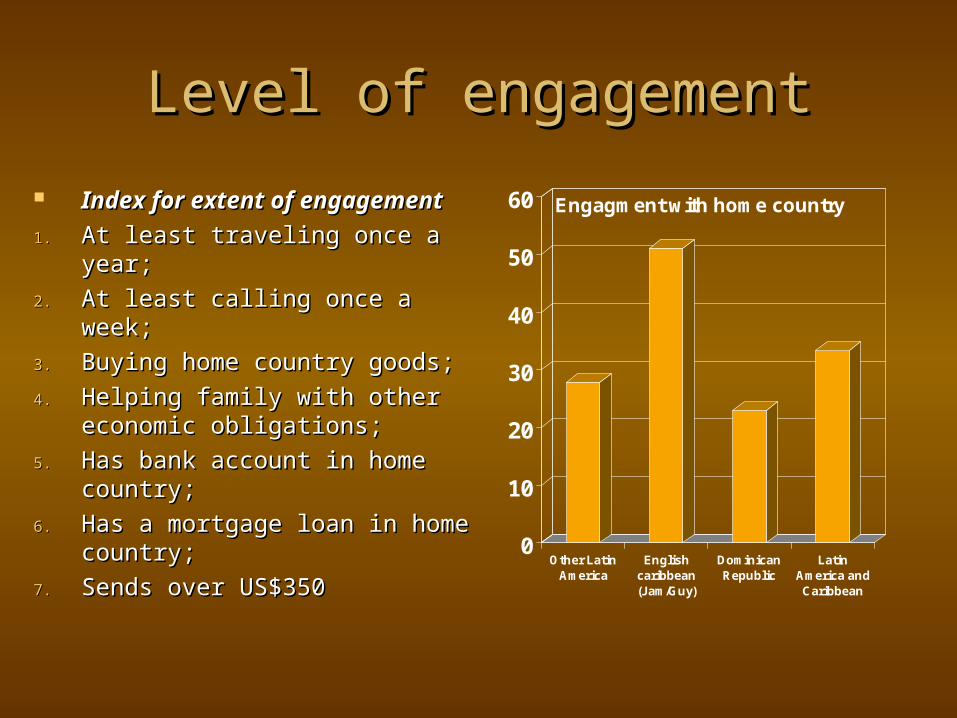

Level of engagementLevel of engagement

Index for extent of Index for extent of engagementengagement

1.1. At least traveling once a year;At least traveling once a year;

2.2. At least calling once a week;At least calling once a week;

3.3. Buying home country goods;Buying home country goods;

4.4. Helping family with other Helping family with other economic obligations;economic obligations;

5.5. Has bank account in home Has bank account in home country;country;

6.6. Has a mortgage loan in home Has a mortgage loan in home country;country;

7.7. Sends over US$350Sends over US$3500

10

20

30

40

50

60

Other LatinAmerica

Englishcaribbean(Jam/Guy)

DominicanRepublic

LatinAmerica andCaribbean

Engagment with home country

Determinants of engagementDeterminants of engagementEnglish

CaribbeanDominican

RepublicOther Latin

America

Independent variables:Independent variables: Significance Sign Significance Sign Significance Sign

Relative's relationship (spouse, parents or children) * (+) *** (+)

Length of time in the U.S. ** (+) *** (-)

Number of relatives living in U.S. household * (-)

Age *** (+)

Gender (male: 1; woman:0) *** (+)

Education ** (-)

Personal income *** (+)

Holding U.S. citizenship *** (-)

Has bank account in U.S.

OLS statistical procedure using level of engagement as dependent variable. Other Latin America: immigrants from Bolivia, Cuba, Colombia, Ecuador, El Salvador, Guatemala, Honduras, Mexico, and Nicaragua.

0

10

20

30

40

50

60

70

80

1970 1980 1990 2000

Costa Rica

El Salvador

Honduras

Nicaragua

Panama

Guyana

Jamaica

Haiti

Dominican Republic

Percent of Latin American and Caribbean people with a tertiary education and living in the US

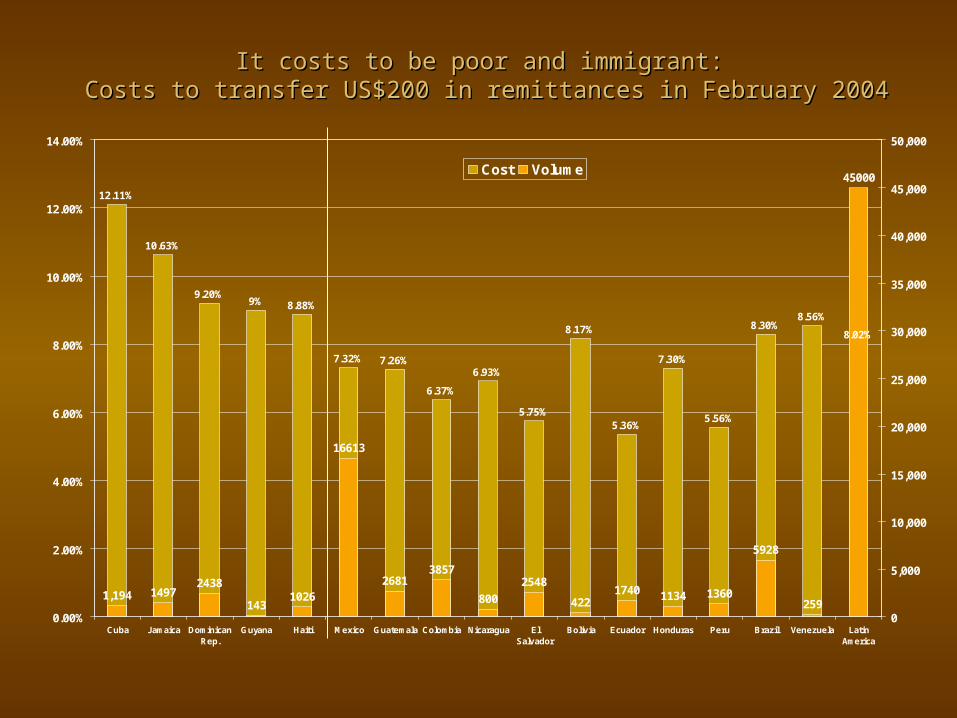

It costs to be poor and immigrant: It costs to be poor and immigrant: Costs to transfer US$200 in remittances in February 2004Costs to transfer US$200 in remittances in February 2004

12.11%

10.63%

9.20%9% 8.88%

7.32% 7.26%

6.37%

6.93%

5.75%

8.17%

5.36%

7.30%

5.56%

8.30%8.56%

8.02%

1,194 14972438

1431026

16613

26813857

800

2548

4221740 1134 1360

5928

259

45000

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

Cuba Jamaica DominicanRep.

Guyana Haiti Mexico Guatemala Colombia Nicaragua ElSalvador

Bolivia Ecuador Honduras Peru Brazil Venezuela LatinAmerica

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

Cost Volume

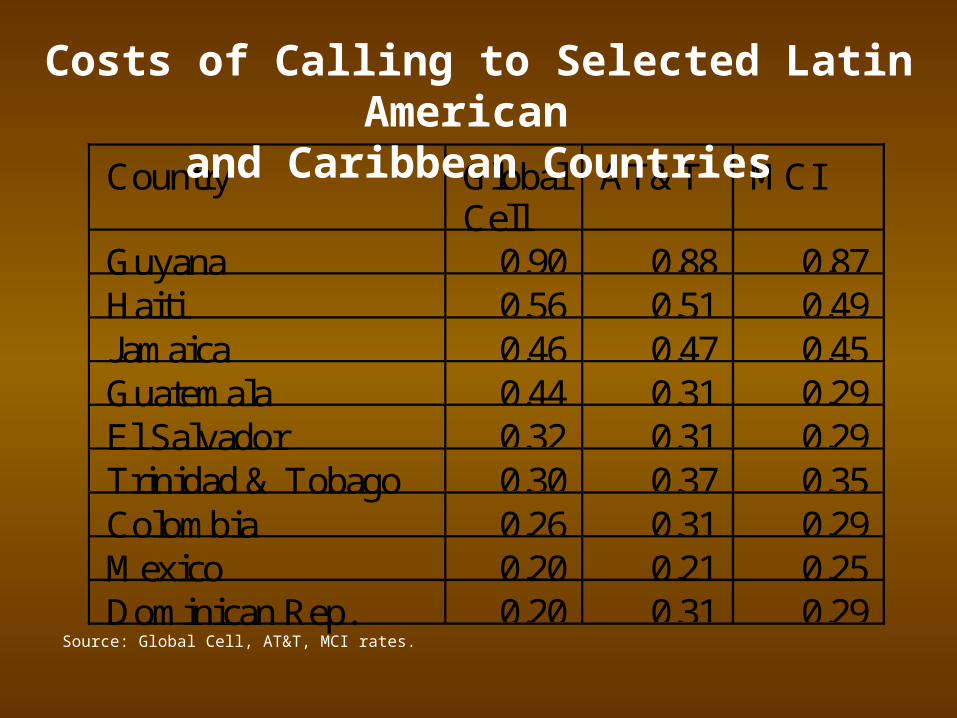

Country GlobalCell

AT&T MCI

Guyana 0.90 0.88 0.87Haiti 0.56 0.51 0.49Jamaica 0.46 0.47 0.45Guatemala 0.44 0.31 0.29El Salvador 0.32 0.31 0.29Trinidad & Tobago 0.30 0.37 0.35Colombia 0.26 0.31 0.29Mexico 0.20 0.21 0.25Dominican Rep. 0.20 0.31 0.29Source: Global Cell, AT&T, MCI rates.

Costs of Calling to Selected Latin American and Caribbean Countries

Diaspora organizingDiaspora organizing

Hometown associations in Hometown associations in Latin AmericaLatin America

Philanthropy for the Philanthropy for the homelandhomeland

• HTAs are small voluntary philanthropic organizations;• Their organizational structure is commensurate to the

groups’ proposed goals;• The activities focus on basic health, education and public

infrastructure;• The resources raised are relatively small in volume

(US$10,000);• Donations are significant however in rural recipient

localities; • Partnership with governments enhance development goals.

Source: Orozco, Manuel (2003), Hometown Associations and their Present and Future Partnerships: New Development Opportunities? Inter-American Dialogue, Report commissioned by the U.S. Agency for International Development. Washington, DC. September.

40 41

7496

3920

112127

177

270

0

50

100

150

200

250

300

Guanajuato Jalisco San Luis P. Zacatecas Other

19982002

Mexican Clubs by State of Mexican Clubs by State of OriginOrigin

Source: Orozco, Manuel (2003), Hometown Associations and their Present and Future Partnerships: New Development Opportunities? Inter-American Dialogue, Report commissioned by the U.S. Agency for International Development. Washington, DC. September.

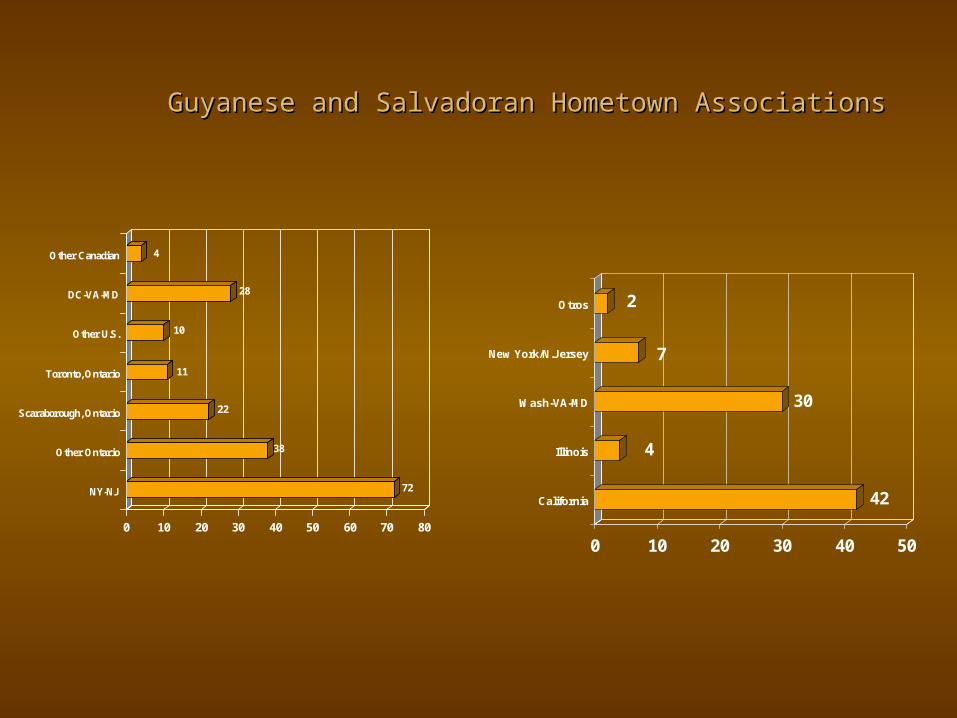

72

38

22

11

10

28

4

0 10 20 30 40 50 60 70 80

NY-NJ

Other Ontario

Scaraborough, Ontario

Toronto, Ontario

Other U.S.

DC-VA-MD

Other Canadian

Guyanese and Salvadoran Hometown Associations Guyanese and Salvadoran Hometown Associations

42

4

30

7

2

0 10 20 30 40 50

California

Illinois

Wash-VA-MD

New York/N.Jersey

Otros

Issue identification: Range of Activities in Mexico Issue identification: Range of Activities in Mexico ( of HTAs working on given project)( of HTAs working on given project)

0 10 20 30 40 50 60

Health and Education

Other Donations

Infrastructure

Church

Recreation

Town Beautification

Economic Investment

Cemetery

Resource allocationResource allocation

40%

29%

17%

8% 6%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Less than5,000

5,000 to 10,000 10,000 to20,000

20,000 to40,000

Over 40,000

HTAs Donations (US$)

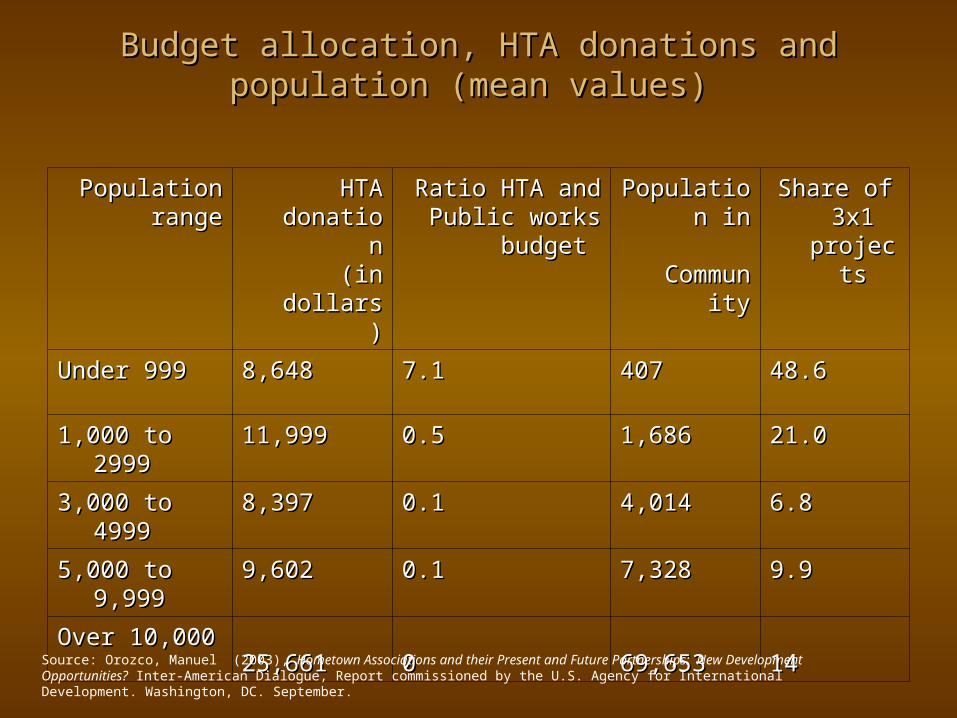

Budget allocation, HTA donations and population (mean Budget allocation, HTA donations and population (mean values) values)

Population rangePopulation range HTA donationHTA donation(in dollars)(in dollars)

Ratio HTA and Ratio HTA and Public works budget Public works budget

Population inPopulation in CommunityCommunity

Share of 3x1 Share of 3x1 projectsprojects

Under 999Under 999 8,6488,648 7.17.1 407407 48.648.6

1,000 1,000 to 2999to 2999 11,99911,999 0.50.5 1,6861,686 21.021.0

3,000 3,000 to 4999to 4999 8,3978,397 0.10.1 4,0144,014 6.86.8

5,000 5,000 to 9,999to 9,999 9,6029,602 0.10.1 7,3287,328 9.99.9

Over 10,000Over 10,00025,66125,661 00 69,65369,653 1414

Source: Orozco, Manuel (2003), Hometown Associations and their Present and Future Partnerships: New Development Opportunities? Inter-American Dialogue, Report commissioned by the U.S. Agency for International Development. Washington, DC. September.

The reality of The reality of transnational familiestransnational families

Is poverty out of the picture Is poverty out of the picture with transnational migration?with transnational migration?

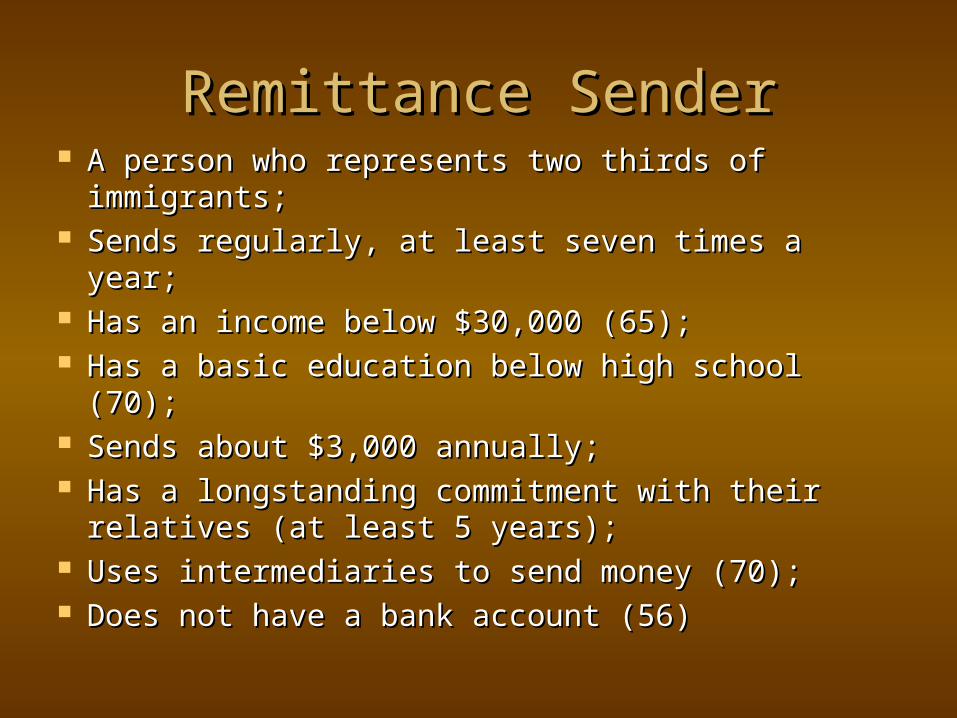

Remittance SenderRemittance Sender A person who represents two thirds of A person who represents two thirds of

immigrants;immigrants; Sends regularly, at least seven times a year;Sends regularly, at least seven times a year; Has an income below $30,000 (65);Has an income below $30,000 (65); Has a basic education below high school (70);Has a basic education below high school (70); Sends about $3,000 annually;Sends about $3,000 annually; Has a longstanding commitment with their Has a longstanding commitment with their

relatives (at least 5 years);relatives (at least 5 years); Uses intermediaries to send money (70);Uses intermediaries to send money (70); Does not have a bank account (56)Does not have a bank account (56)

Remittances from Latin American immigrants in the United StatesRemittances from Latin American immigrants in the United States

Sixty percent of Latin American immigrants send remittances; The average transactions that immigrants send is $240 and do it regularly over twelve times a year. The regularity of the amount is four times more than in 2001.The aggregate volume of such amounts adds to a little over 30 billion dollars a year from the continental United States;In six states immigrants are sending at least one billion dollars;Latinos in California alone send nearly ten billion;The total volume from these six states adds to twenty-one billion dollars

$0

$1,000,000,000

$2,000,000,000

$3,000,000,000

$4,000,000,000

$5,000,000,000

$6,000,000,000

$7,000,000,000

$8,000,000,000

$9,000,000,000

$10,000,000,000California

New York

Texas

Florida

Illinois

New Jersey

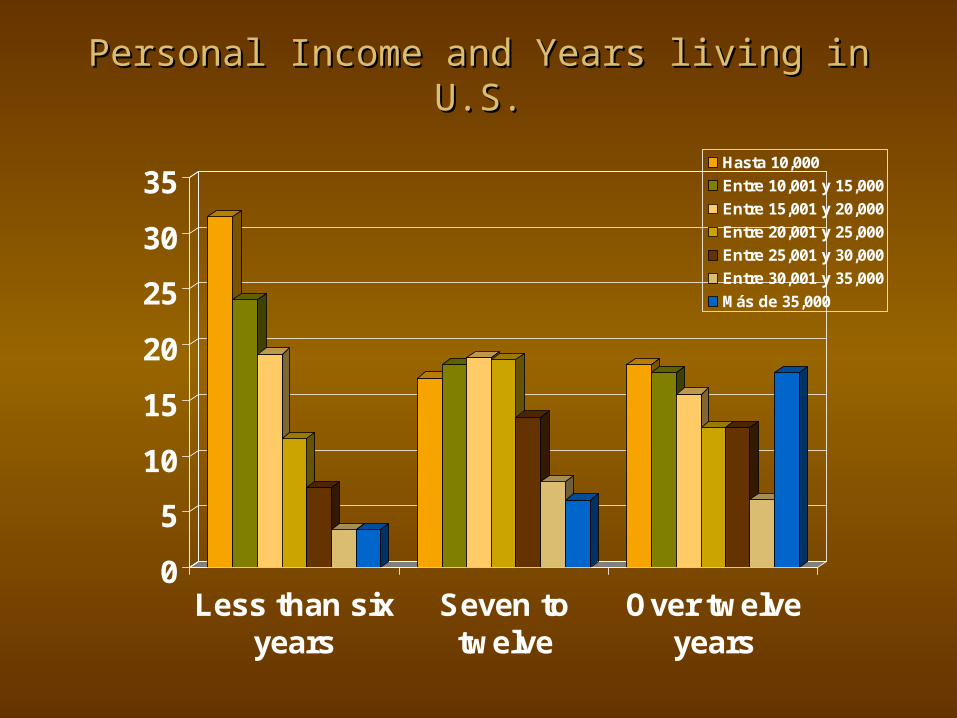

Personal Income and Years living Personal Income and Years living in U.S.in U.S.

0

5

10

15

20

25

30

35

Less than sixyears

Seven totwelve

Over twelveyears

Hasta 10,000

Entre 10,001 y 15,000

Entre 15,001 y 20,000

Entre 20,001 y 25,000

Entre 25,001 y 30,000

Entre 30,001 y 35,000

Más de 35,000

Remittance senders without bank accountsRemittance senders without bank accounts

0

5

10

15

20

25

30

35

40

45

No bank account

Cuba Dom. Rep. Jamaica Guyana LAC averege

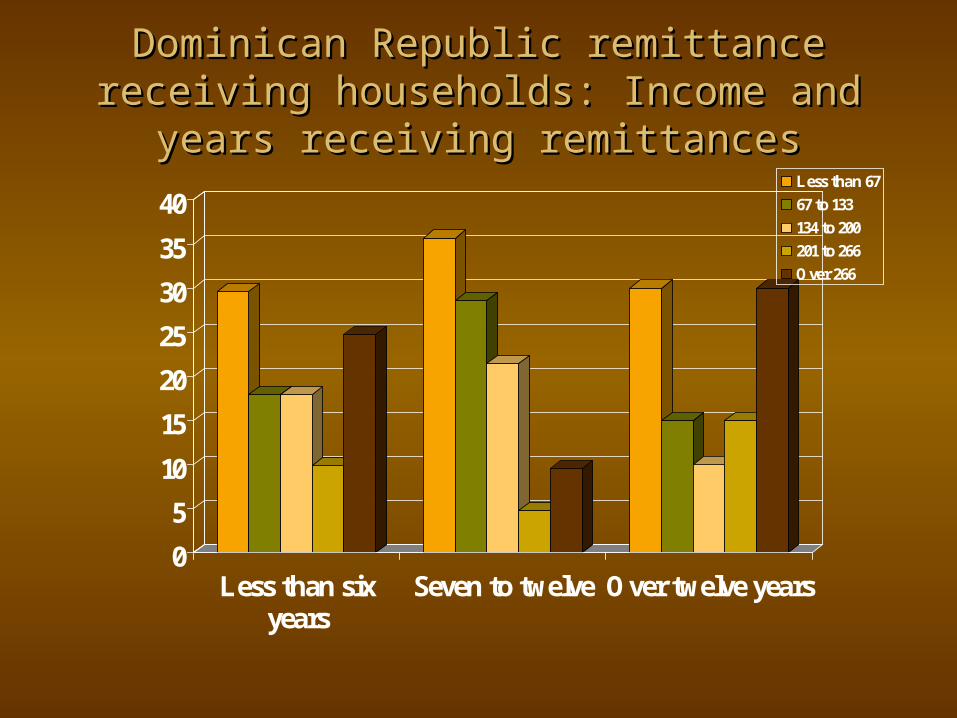

Dominican Republic remittance receiving Dominican Republic remittance receiving households: Income and years receiving households: Income and years receiving

remittancesremittances

0

5

10

15

20

25

30

35

40

Less than sixyears

Seven to twelve Over twelve years

Less than 6767 to 133134 to 200201 to 266Over 266

Remittance receiving households: Remittance receiving households: some financial characteristics some financial characteristics

0

10

20

30

40

50

60

70

Mexico El Salvador Nicaragua R.D. Guatemala Honduras Guyana

SavingsInvestmentBank account

Source: IDB. Receptores de Remesas en Centroamérica, Ciudad de Guatemala, Guatemala, 3 de Septiembre 2003. BID; IDSource: IDB. Receptores de Remesas en Centroamérica, Ciudad de Guatemala, Guatemala, 3 de Septiembre 2003. BID; IDB. Receptores de Remesas en B. Receptores de Remesas en Mexico, Ciudad de Mexico, Mexico, Octubre 2003. BID. Guyana: Laparkan Trading survey Mexico, Ciudad de Mexico, Mexico, Octubre 2003. BID. Guyana: Laparkan Trading survey (carried out by the author)(carried out by the author); ; . . Nicaragua: Nicaragua: ENCUESTA NACIONAL SOBRE GOBERNABILIDAD Y ELECCIONES: MODULO SOBRE MIGRACIÓN, USO DE ENCUESTA NACIONAL SOBRE GOBERNABILIDAD Y ELECCIONES: MODULO SOBRE MIGRACIÓN, USO DE REMESAS FAMILIARES Y AHORRO, Managua 05 de julio de 2001REMESAS FAMILIARES Y AHORRO, Managua 05 de julio de 2001, INSTITUTO DE ESTUDIOS NICARAGUENSES; DR: , INSTITUTO DE ESTUDIOS NICARAGUENSES; DR: Emmanuel Silvestre’s survey (commissioned out by the author)Emmanuel Silvestre’s survey (commissioned out by the author)

Remittances as Remittances as Institutions of Institutions of Development Development

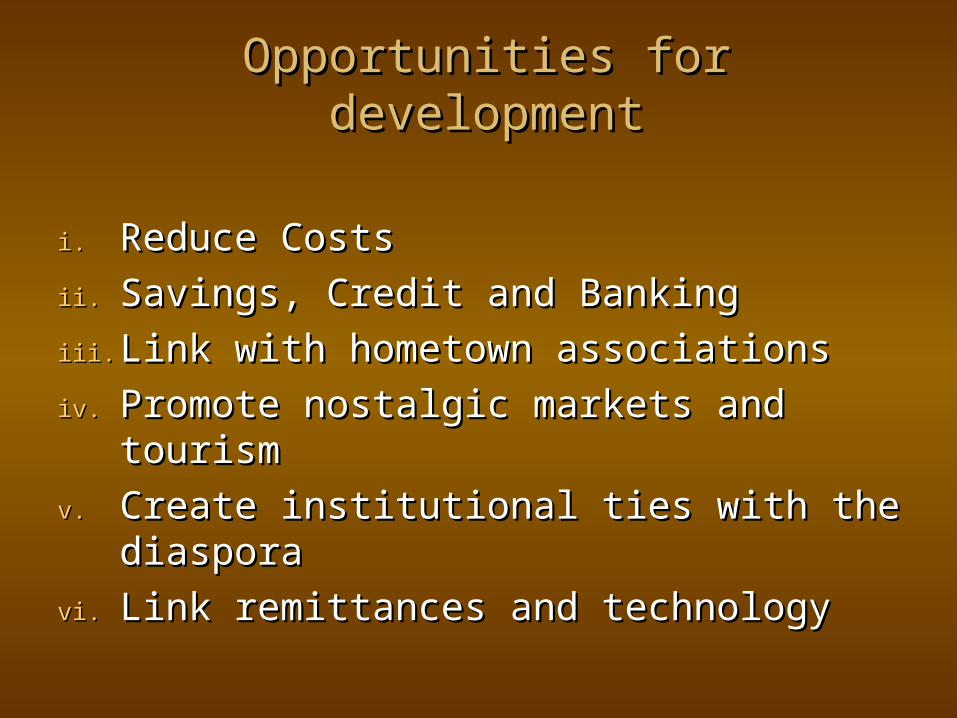

Opportunities for developmentOpportunities for development

i.i. Reduce CostsReduce Costs

ii.ii. Savings, Credit and BankingSavings, Credit and Banking

iii.iii. Link with hometown associationsLink with hometown associations

iv.iv. Promote nostalgic markets and Promote nostalgic markets and tourism tourism

v.v. Create institutional ties with the Create institutional ties with the diaspora diaspora

vi.vi. Link remittances and technologyLink remittances and technology

Strategy 1: Reduction in transfer costs Strategy 1: Reduction in transfer costs

Promotion strategic alliances between remittance agencies and Promotion strategic alliances between remittance agencies and banks, such as VISA with Quiqeyana, Banco Cuscatlan, Banco banks, such as VISA with Quiqeyana, Banco Cuscatlan, Banco Uno y Gigante Express in Central America and the Dominican Uno y Gigante Express in Central America and the Dominican Republic Republic

Strategic agreements between banks in the country of Strategic agreements between banks in the country of residence and the country of origin residence and the country of origin Bank of America, Citibank (C2iT), etc.Bank of America, Citibank (C2iT), etc. Software Platforms for banks: Mastrex InternationalSoftware Platforms for banks: Mastrex International ATMs and MAC: Mitchell’s Bank ATMs and MAC: Mitchell’s Bank Alliances among US and Latin American credit unions, such as Alliances among US and Latin American credit unions, such as

IRNet IRNet

Total cost of remittance transfer by industry sectorTotal cost of remittance transfer by industry sector

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

2001 2002 2003 2004.01 2004.06 2004.11

NMTA

Western Union

Moneygram

Vigo

US Banks and all Credit Unions

other

A score card on Remittance Transfers: What works best to the customer’s benefit.

CriteriaCriteria IndicatorsIndicators RankingRanking

1. 1. Transfer feeTransfer fee Lowered fees for customers may indicate lowered costs for Lowered fees for customers may indicate lowered costs for remittance companies.remittance companies.

2. 2. Exchange rate usedExchange rate used If there is no exchange rate, no currency purchase costs are If there is no exchange rate, no currency purchase costs are incurred by sender and recipients. Fees may be higher, incurred by sender and recipients. Fees may be higher, however.however.

3. 3. Transfer mechanism (hand delivery, Transfer mechanism (hand delivery, money order, electronic transfer: debit money order, electronic transfer: debit card, bank to bank, internet, courier card, bank to bank, internet, courier agency transfer, etc.)agency transfer, etc.)

More capital intensive the transactions mean lower costs for More capital intensive the transactions mean lower costs for the company, but not necessarily lower fees for the the company, but not necessarily lower fees for the consumer.consumer.

4. 4. Marketplace competition (supply Marketplace competition (supply side)side)

The higher number the number of companies in any The higher number the number of companies in any market, the lower the transfer costs. The exception is when market, the lower the transfer costs. The exception is when companies are formed in monopolies, oligopolies or companies are formed in monopolies, oligopolies or remittance ‘cartels’.remittance ‘cartels’.

5. 5. Business location and geographic Business location and geographic coveragecoverage

Companies located within areas with a better economic Companies located within areas with a better economic infrastructure exhibit lower transaction costsinfrastructure exhibit lower transaction costs

6. 6. Development supportDevelopment support Support to the local community adds value to the product Support to the local community adds value to the product and loyalty to the companyand loyalty to the company

7. 7. Relationship with Financial Services Relationship with Financial Services IntermediationIntermediation

Offering services such as banking or bill payment increases Offering services such as banking or bill payment increases interest in the companyinterest in the company

8. 8. TransparencyTransparency A company that advertises its exchange rates cultivates or A company that advertises its exchange rates cultivates or promotes more trust from the customer. promotes more trust from the customer.

9. 9. Compliance to regulationsCompliance to regulations A company that meets all the requirements operate as a A company that meets all the requirements operate as a remitter.remitter.

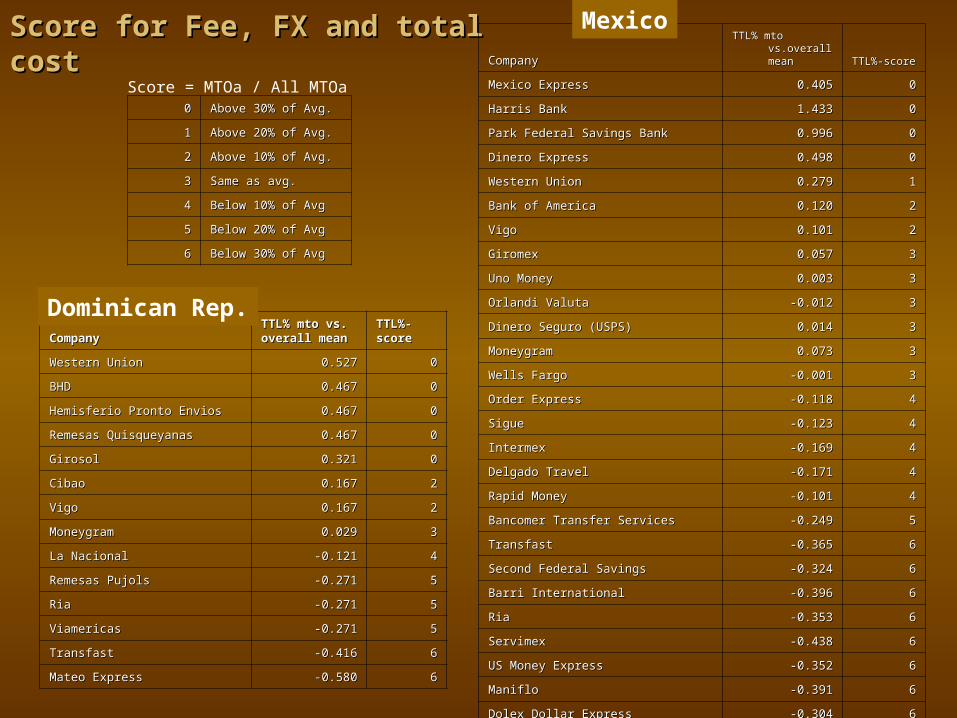

Score for Fee, FX and total costScore for Fee, FX and total cost

00 Above 30% of Avg.Above 30% of Avg.

11 Above 20% of Avg.Above 20% of Avg.

22 Above 10% of Avg.Above 10% of Avg.

33 Same as avg.Same as avg.

44 Below 10% of AvgBelow 10% of Avg

55 Below 20% of AvgBelow 20% of Avg

66 Below 30% of AvgBelow 30% of Avg

CompanyCompany

TTL% mto TTL% mto vs.overall vs.overall meanmean TTL%-scoreTTL%-score

Mexico ExpressMexico Express 0.4050.405 00

Harris BankHarris Bank 1.4331.433 00

Park Federal Savings BankPark Federal Savings Bank 0.9960.996 00

Dinero ExpressDinero Express 0.4980.498 00

Western UnionWestern Union 0.2790.279 11

Bank of AmericaBank of America 0.1200.120 22

VigoVigo 0.1010.101 22

GiromexGiromex 0.0570.057 33

Uno MoneyUno Money 0.0030.003 33

Orlandi ValutaOrlandi Valuta -0.012-0.012 33

Dinero Seguro (USPS)Dinero Seguro (USPS) 0.0140.014 33

MoneygramMoneygram 0.0730.073 33

Wells FargoWells Fargo -0.001-0.001 33

Order ExpressOrder Express -0.118-0.118 44

SigueSigue -0.123-0.123 44

IntermexIntermex -0.169-0.169 44

Delgado TravelDelgado Travel -0.171-0.171 44

Rapid MoneyRapid Money -0.101-0.101 44

Bancomer Transfer ServicesBancomer Transfer Services -0.249-0.249 55

TransfastTransfast -0.365-0.365 66

Second Federal SavingsSecond Federal Savings -0.324-0.324 66

Barri InternationalBarri International -0.396-0.396 66

RiaRia -0.353-0.353 66

ServimexServimex -0.438-0.438 66

US Money ExpressUS Money Express -0.352-0.352 66

ManifloManiflo -0.391-0.391 66

Dolex Dollar ExpressDolex Dollar Express -0.304-0.304 66

Mexico

Score = MTOa / All MTOa

CompanyCompanyTTL% mto vs. TTL% mto vs. overall meanoverall mean

TTL%-TTL%-scorescore

Western UnionWestern Union 0.5270.527 00

BHDBHD 0.4670.467 00

Hemisferio Pronto EnviosHemisferio Pronto Envios 0.4670.467 00

Remesas QuisqueyanasRemesas Quisqueyanas 0.4670.467 00

GirosolGirosol 0.3210.321 00

CibaoCibao 0.1670.167 22

VigoVigo 0.1670.167 22

MoneygramMoneygram 0.0290.029 33

La NacionalLa Nacional -0.121-0.121 44

Remesas PujolsRemesas Pujols -0.271-0.271 55

RiaRia -0.271-0.271 55

ViamericasViamericas -0.271-0.271 55

TransfastTransfast -0.416-0.416 66

Mateo ExpressMateo Express -0.580-0.580 66

Dominican Rep.

Remittance Market Composition in Latin AmericaRemittance Market Composition in Latin America

MatureMature ConsolidatingConsolidating IncipientIncipient

Composition of market share, Composition of market share, Efficiency of transactions (use of Efficiency of transactions (use of modern technology, extended modern technology, extended networks nation wide, safe networks nation wide, safe transfers), transfers), Compliance to regulatory Compliance to regulatory environment, environment, Tradition of transferring money, Tradition of transferring money, Multiple new and old Multiple new and old players(MTOs, banks, MFIs), players(MTOs, banks, MFIs), Costs to customers are lower than Costs to customers are lower than average, Information and average, Information and transparency, transparency, Investment accessibleInvestment accessible

NoneNone Mexico, Mexico, El Salvador, El Salvador,

Dominican Dominican Republic, Republic, Ecuador, Ecuador,

JamaicaJamaica

ColombiaColombia Honduras Honduras

PeruPeruGuyanaGuyana

HaitiHaitiCubaCuba

NicaraguaNicaraguaArgentina Argentina VenezuelaVenezuela

Strategy II: Savings, Credit and Strategy II: Savings, Credit and RemittancesRemittances

a.a. Monitoring transfers, especially the exchange Monitoring transfers, especially the exchange raterate

b.b. Motivate savings and credit institutions to Motivate savings and credit institutions to attract remittance senders and recipients attract remittance senders and recipients

c.c. Bring low cost banking centers where there is Bring low cost banking centers where there is a high concentration of families who receive a high concentration of families who receive remittancesremittances

d.d. Offer incentives to households that receive Offer incentives to households that receive remittances;remittances;

e.e. Allow micro-finance and credit unions to Allow micro-finance and credit unions to become agents of remittances and savings become agents of remittances and savings institutionsinstitutions

““The demand for financial services by remittance receiving households The demand for financial services by remittance receiving households rests on the intersection between the role of microfinance institutions, rests on the intersection between the role of microfinance institutions,

such as credit unions, and rural sector development.” such as credit unions, and rural sector development.”

$1.2$4.1

$9.6$13.5

$17.1

$24.0

$41.2

$0.0

$10.0

$20.0

$30.0

$40.0

$50.0

Q4 01 Q1 02 Q2 02 Q3 02 Q4 02 Q1 03 Q2 03

Volume of Remittances Distributed by 62 Central American CUs in US$ Millions

Mexico: Remittances to rural households Mexico: Remittances to rural households

$106,862 $442,704$1,053,786

$1,923,668

$3,256,231

$15,027,550

$0

$2,000,000

$4,000,000

$6,000,000

$8,000,000

$10,000,000

$12,000,000

$14,000,000

$16,000,000

Menos de 999 1,000 a 2999 3,000 a 4999 5,000 a 9,999 10,000 a 14,999 Mas de 15,000

15 recibe US$250 al mes, siete veces al año.

People with bank accounts People with bank accounts (remittance recipients and non-recipients) (remittance recipients and non-recipients)

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Guatemala Honduras El Salvador Mexico Ecuador

RecipientsNon-Recipients

Source: Multilateral Investment Fund-Inter-American Development Bank, Receptores de Remesas en Mexico, Octubre 2003; Receptores de remesas en Guatemala, El Salvador y Honduras, Septiembre 2003; Receptores de Remesas en Ecuador, Mayo 2003. Washington, DC: MIF-IADB/FOMIN-BID.

MFI Relevance: Zacatecas MFI Relevance: Zacatecas Municipalities Municipalities

(pop.)(pop.)BanksBanks Credit UnionsCredit Unions MTOsMTOs FINRURALFINRURAL

Jerez (55,000)Jerez (55,000) Bancomer, Bancomer, Banamex, Banamex, Bital, Bital, BanorteBanorte

Caja Popular Caja Popular MexicanaMexicana

Thirteen Thirteen money money transfer transfer ‘centros ‘centros de de cambio’cambio’

Tepetongo Tepetongo (5,000)(5,000)

Tlatenango Tlatenango (24,000)(24,000)

Bancomer, Bancomer, Bital, Bital, BanorteBanorte

Caja Popular Caja Popular MexicanaMexicana

FiveFive

Tepechitlan Tepechitlan (5,000)(5,000)

BanorteBanorte OneOne

MomaxMomax OneOne

Jalpa (20,000)Jalpa (20,000) Bancomer, Bancomer, Bital, Bital, BanorteBanorte

Caja Popular Caja Popular MexicanaMexicana

ThreeThree

JuchipilaJuchipila Bancomer, Bancomer, Bital, Bital, BanorteBanorte

ThreeThree

Jerez, Zacatecas: Jerez, Zacatecas: 15% of RRH have bank accounts15% of RRH have bank accounts

Lugar Frecuencia PorcentajeCasa de Cambio 75 34.4Bancomer 38 17.4Elektra 25 11.5HSBC 22 10.1Banamex 15 6.9Correo/telégrafos 11 5.0BANORTE 6 2.8Banco (No Especificado) 7 3.2Viajes Jerez 5 2.3Otros 6 2.8No sabe/no recuerda 8 3.7Total 218 100.0

Remittances and microfinanceRemittances and microfinance1. 1. Competitive position: The institution . . .Competitive position: The institution . . .

a. has offered remittances since ____a. has offered remittances since ____

b. offers money transfers on its own, through partnership or in a networkb. offers money transfers on its own, through partnership or in a network

c. has experienced growth in the transfers (number of transactions; market share)c. has experienced growth in the transfers (number of transactions; market share)

d. offers a competitive fee and enjoys profit marginsd. offers a competitive fee and enjoys profit margins

e. has a competitive foreign exchangee. has a competitive foreign exchange

f. has a remittance marketing toolf. has a remittance marketing tool

2.2. Financial intermediation: The institution Financial intermediation: The institution

a. offers remittance distribution to membersa. offers remittance distribution to members

b. opens bank accounts to remittance recipient households in the institution’s vicinity;b. opens bank accounts to remittance recipient households in the institution’s vicinity;

c. Has a crosselling marketing toolc. Has a crosselling marketing tool

d. Provides range of financial servicesd. Provides range of financial services

e. Provides credit for productive investment [mobilizes savings from remittance transfers]e. Provides credit for productive investment [mobilizes savings from remittance transfers]

f. Remittance senders has a financial relationship with institutionf. Remittance senders has a financial relationship with institution

3. 3. Regulatory environment: The institution . . .Regulatory environment: The institution . . .

a. Has awareness of regulatory issues in money transfersa. Has awareness of regulatory issues in money transfers

b. Report its activities to partner money transfer companyb. Report its activities to partner money transfer company

c. Report its activities to government agenciesc. Report its activities to government agencies

4. 4. Technological applicationsTechnological applications

a. The money transfer occurs through mainstream but modern platformsa. The money transfer occurs through mainstream but modern platforms

b. Innovative technologies are implemented (cards, wifi, online transfers, bundled softwares).b. Innovative technologies are implemented (cards, wifi, online transfers, bundled softwares).

5. 5. Data Management: The institution . . .Data Management: The institution . . .

a. Systematizes flowsa. Systematizes flows

b. Performs market research and client analysisb. Performs market research and client analysis

6.6. External assistance: The institution . . . External assistance: The institution . . .

a. Donors or investors provide technical assistance for remittance transfer incorporation or innovation (equipment, regulatory compliance, training, market research, etc.)a. Donors or investors provide technical assistance for remittance transfer incorporation or innovation (equipment, regulatory compliance, training, market research, etc.)

b. Donors or investors provide working capital for remittance operationb. Donors or investors provide working capital for remittance operation

7.7. Institutional efforts: The institution . . . Institutional efforts: The institution . . .

a. Has invested resources to compete in the marketa. Has invested resources to compete in the market

b. Business is generating non-negligible revenueb. Business is generating non-negligible revenue

c. Relationship to local economyc. Relationship to local economy

d. Relationship to local communityd. Relationship to local community

Minimum indicators leveraging the relationship Minimum indicators leveraging the relationship between financial intermediation and remittancesbetween financial intermediation and remittances

Remittance market service coverageRemittance market service coverage: The institution provides : The institution provides remittance transfer operations to its clients or members, as well as to remittance transfer operations to its clients or members, as well as to the communities where its branches operate.the communities where its branches operate.Indicator: Indicator: Coverage where there is competition (MFI branches / Competitor branches)Coverage where there is competition (MFI branches / Competitor branches)

Effective market presenceEffective market presence: As a minimum, market presence is : As a minimum, market presence is achieved through a combination of partnership with money transfer achieved through a combination of partnership with money transfer companies, offer of a low cost remittance transaction and a distribution companies, offer of a low cost remittance transaction and a distribution capacity.capacity.Indicators: Indicators: Transfer volume (transfers / month, rate of transactions per institution’s branch), Transfer volume (transfers / month, rate of transactions per institution’s branch), transaction cost (institution’s transfer cost / market average),transaction cost (institution’s transfer cost / market average), number of branches, .number of branches, .

Accessible financial servicesAccessible financial services: The institution markets, designs and : The institution markets, designs and provides recipients with an array of various product options, including provides recipients with an array of various product options, including savings, credit, insurance, pension funds.savings, credit, insurance, pension funds.Indicator: Indicator: financial services (number of remittance recipients that are clients)financial services (number of remittance recipients that are clients) ..

Information management and adaptationInformation management and adaptation: Institutional awareness : Institutional awareness and management of the market composition of recipients, adoption of and management of the market composition of recipients, adoption of adequate technologies linking MFI systems with remittance transfers.adequate technologies linking MFI systems with remittance transfers.Indicator: Indicator:

Banks, Credit Unions and Microfinance Banks, Credit Unions and Microfinance institutions offering remittancesinstitutions offering remittances

InstitutionInstitution CountryCountry TypeType

Banco Industrial (BI)Banco Industrial (BI) GuatemalaGuatemala Commercial Commercial bankbank

Cooperativa de Ahorro y Crédito SalcajáCooperativa de Ahorro y Crédito Salcajá GuatemalaGuatemala Credit UnionCredit Union

Banco Salvadoreño (BSal)Banco Salvadoreño (BSal) El SalvadorEl Salvador Commercial Commercial bankbank

Federation of Salvadoran Savings and Credit Federation of Salvadoran Savings and Credit Cooperative (FEDECACES)Cooperative (FEDECACES) El SalvadorEl Salvador Credit Union Credit Union

Banco Solidario (BSol)Banco Solidario (BSol) EcuadorEcuador Transformed Transformed MFIMFI

National Savings and Financial Services Bank (BANSEFI)National Savings and Financial Services Bank (BANSEFI) MexicoMexico State bankState bank

Oaxaca BankOaxaca Bank MexicoMexico MicrobankMicrobank

Wells FargoWells Fargo MexicoMexico Commercial Commercial bankbank

Financiera El ComercioFinanciera El Comercio ParaguayParaguay MFIMFI

CoverageCoverageEffective coverageby branch locationMFIs and operations

in rural areas

% % RuralRural (%)(%)

4040 1111

5050 1717

6060 1111

7070 2222

Over 75Over 75 39.239.2

TotalTotal 100.00100.00n=19

MFI Ratio MFI Ratio to WU to WU AgentsAgents

El SalvadorEl Salvador

AMC de RLAMC de RL 44%44%

Apoyo IntegralApoyo Integral 29%29%

Banco ProCreditBanco ProCredit 36%36%

FEDECACESFEDECACES 51%51%

Fundacion CampoFundacion Campo 14%14%

Fundacion Jose Napoleon Fundacion Jose Napoleon DuarteDuarte 22%22%

GuatemalaGuatemala

FENACOACFENACOAC 41%41%

Genesis EmpresarialGenesis Empresarial 36%36%

SalcajaSalcaja 47%47%

Rate of transactions per institution’s branch

(%)(%)

Less than 50 transactionsLess than 50 transactions 47.447.4

51 51 to 200 transactions to 200 transactions 10.510.5

201 201 to 400 transactionsto 400 transactions 21.121.1

Over 400 transactionsOver 400 transactions 21.121.1

TotalTotal 100.0100.0

n=19

PercentPercent

Above transfer costAbove transfer cost 3232

Same to average transfer Same to average transfer costcost

1111

Below transfer costBelow transfer cost 4747

Data not availableData not available 1111

Total Total 100.0100.0

Above or below transfer cost

n=19

Transfer volume, number of account holder Transfer volume, number of account holder and branches by institution (2004). and branches by institution (2004).

Transfer volume, number of account holder and branches by institution (2004).

Transfer Transfer cost cost (company / (company / market market average)average)

Volume Volume of of transfertransfers per s per monthmonth

Number Number of of remittancremittance e recipientrecipients that are s that are clientsclients

Total Total number number of clientsof clients

Number Number of of branchesbranches

FEDECACESFEDECACES 3.9% / 4.2% 3.9% / 4.2% 17,50017,500 4,375 4,375 90,00090,000 2626

Banco Salvadoreño Banco Salvadoreño (BSal)(BSal)

3.9% / 4.2%3.9% / 4.2% 58,00058,000 17,00017,000 n/an/a 110110

SalcajaSalcaja 6.1% / 5.8%6.1% / 5.8% 10001000 7,6507,650 15,00015,000 33

El ComercioEl Comercio 9.8% / 8.7%9.8% / 8.7% 200200 1,3301,330 7,0007,000 1111

Banco Industrial (BI)Banco Industrial (BI) 6.5% / 5.8%6.5% / 5.8% 200,000200,000 100,000100,000 500,000500,000 Over 250Over 250

Banco Solidario Banco Solidario (BSol)(BSol)

0% /4% 0% /4% 12,00012,000 4,0004,000 91,60091,600 3232

BANSEFIBANSEFI 5.4% / 5.4%5.4% / 5.4% 25,00025,000 2,5002,500 500,000500,000 550550

Wells FargoWells Fargo 5.4 % / 5.4% 5.4 % / 5.4% 70,00070,000 250,000250,000 Over 1 Over 1 millionmillion

Over 3000Over 3000

Source: Orozco, Manuel, Survey commissioned to Borge & Asociados, 2004; Institutional interviews, January 2004 & 2005.

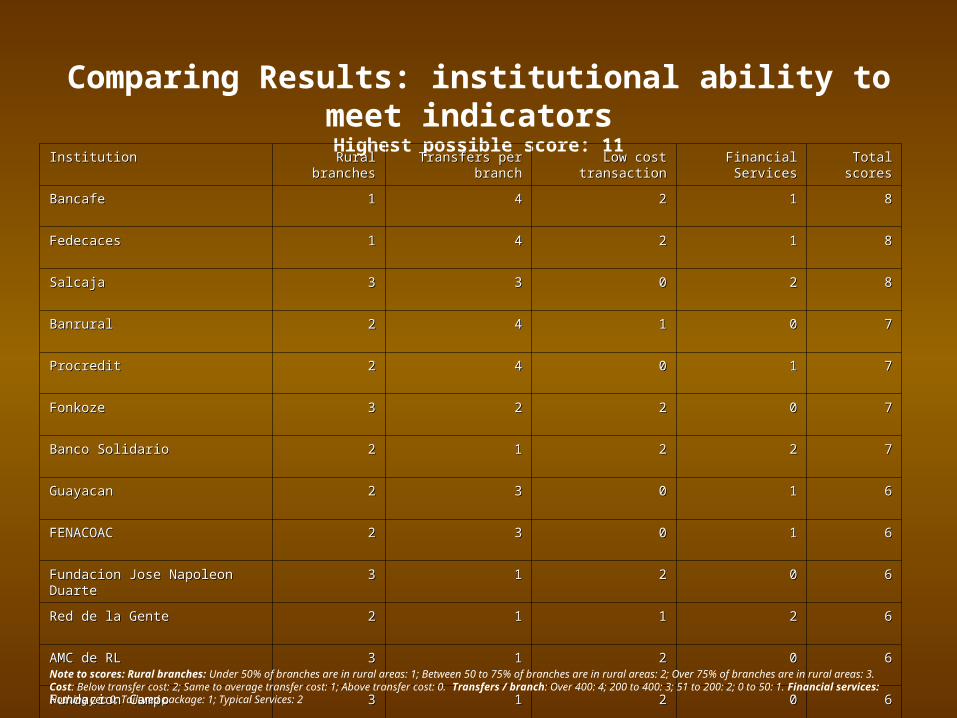

Comparing Results: institutional ability to meet indicators Highest possible score: 11

InstitutionInstitution Rural Rural branchesbranches

Transfers per Transfers per branchbranch

Low cost Low cost transactiontransaction

Financial Financial ServicesServices

Total Total scoresscores

Bancafe Bancafe 11 44 22 11 88

Fedecaces Fedecaces 11 44 22 11 88

Salcaja Salcaja 33 33 00 22 88

Banrural Banrural 22 44 11 00 77

Procredit Procredit 22 44 00 11 77

Fonkoze Fonkoze 33 22 22 00 77

Banco Solidario Banco Solidario 22 11 22 22 77

Guayacan Guayacan 22 33 00 11 66

FENACOAC FENACOAC 22 33 00 11 66

Fundacion Jose Napoleon Fundacion Jose Napoleon DuarteDuarte

33 11 22 00 66

Red de la Gente Red de la Gente

22 11 11 22 66

AMC de RL AMC de RL 33 11 22 00 66

Fundacion Campo Fundacion Campo

33 11 22 00 66

Coosadeco Coosadeco 22 22 00 11 55

El Comercio El Comercio 22 11 00 22 55

Integral Integral 22 11 22 00 55

Nu Nvu, Oaxaca Nu Nvu, Oaxaca

33 11 .. 11 55

Fedecredito Fedecredito 11 11 22 11 55

Genesis Genesis 33 .. .. 33

Note to scores: Rural branches: Under 50% of branches are in rural areas: 1; Between 50 to 75% of branches are in rural areas: 2; Over 75% of branches are in rural areas: 3. Cost: Below transfer cost: 2; Same to average transfer cost: 1; Above transfer cost: 0. Transfers / branch: Over 400: 4; 200 to 400: 3; 51 to 200: 2; 0 to 50: 1. Financial services: Nothing yet: 0; Tailored package: 1; Typical Services: 2

Money transfers by banksMoney transfers by banks20032003 20042004

Method employedMethod employed Charge Charge Percent ofPercent ofamount sent*amount sent*

Charge Charge Percent ofPercent ofamount amount

sent*sent*

Debit Card withdrawal at ATM Debit Card withdrawal at ATM (Community banks)(Community banks)

7.47.4 1.511.51 1.51.5

US Bank as MT, pick up at US Bank as MT, pick up at Mexican Bank/AgencyMexican Bank/Agency

16.216.2 3.363.36 17.7417.74 4.54.5

Credit UnionsCredit Unions 21.421.4 5.35.3 16.6516.65 3.93.9

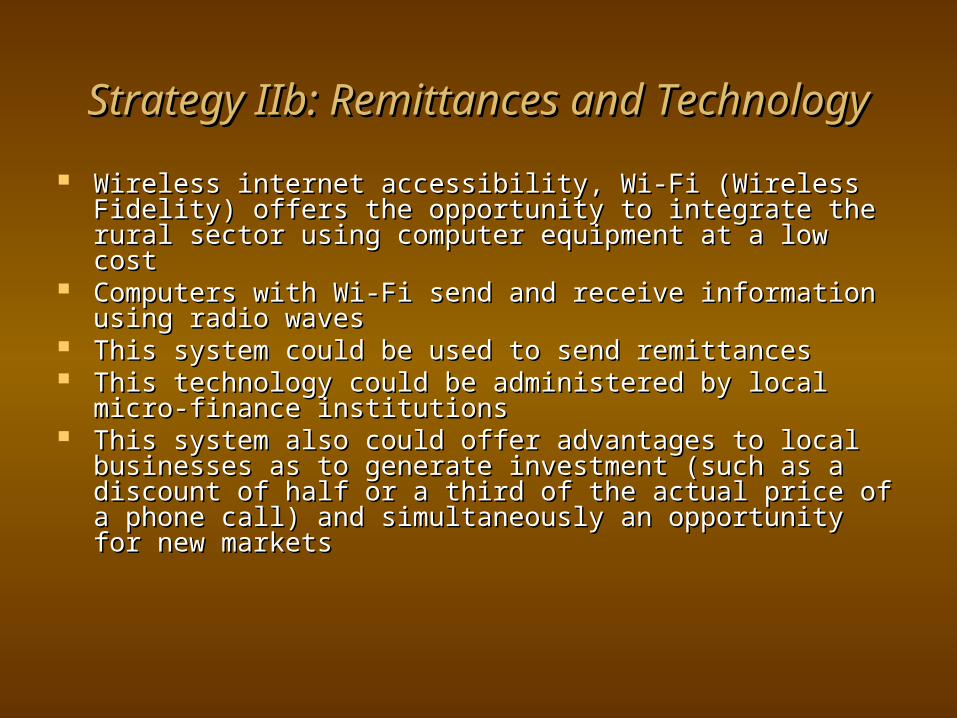

Strategy IIb: Remittances and TechnologyStrategy IIb: Remittances and Technology

Wireless internet accessibility, Wi-Fi (Wireless Fidelity) Wireless internet accessibility, Wi-Fi (Wireless Fidelity) offers the opportunity to integrate the rural sector using offers the opportunity to integrate the rural sector using computer equipment at a low costcomputer equipment at a low cost

Computers with Wi-Fi send and receive information using Computers with Wi-Fi send and receive information using radio wavesradio waves

This system could be used to send remittances This system could be used to send remittances This technology could be administered by local micro-This technology could be administered by local micro-

finance institutions finance institutions This system also could offer advantages to local businesses This system also could offer advantages to local businesses

as to generate investment (such as a discount of half or a as to generate investment (such as a discount of half or a third of the actual price of a phone call) and simultaneously third of the actual price of a phone call) and simultaneously an opportunity for new marketsan opportunity for new markets

Strategy III: Alliances with Home Town Strategy III: Alliances with Home Town Associations Associations

Seek communication and dialogue with HTAs;Seek communication and dialogue with HTAs; Social developmentSocial development

Donor technical assistance for project identification;Donor technical assistance for project identification; Support of a transnational community radio; Support of a transnational community radio; Donor support on governance and democratic Donor support on governance and democratic

participation; participation; Donor partnerships in social (health and education) and Donor partnerships in social (health and education) and

infrastructural projects infrastructural projects Economic development Economic development

Government incentives to attract private sector Government incentives to attract private sector involvement;involvement;

Government support in investment feasibility analysis;Government support in investment feasibility analysis; Financial infrastructureFinancial infrastructure

Support education on financial services;Support education on financial services; Support to link technology to education, communication Support to link technology to education, communication

and remittances in the rural areas.and remittances in the rural areas.

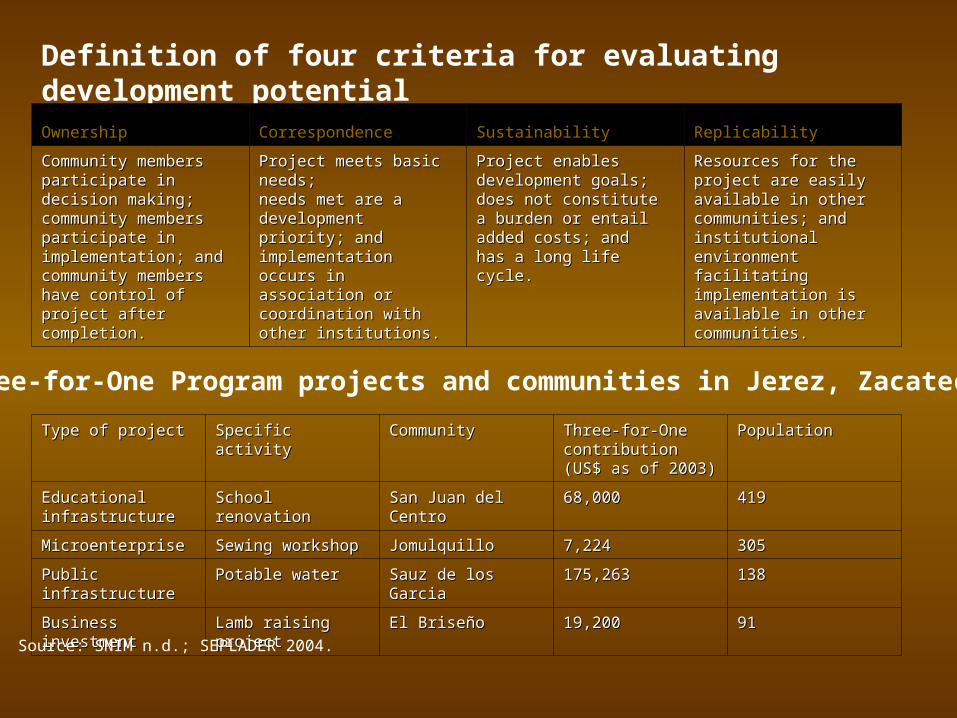

Definition of four criteria for evaluating development potential

OwnershipOwnership CorrespondenceCorrespondence SustainabilitySustainability ReplicabilityReplicability

Community members Community members participate in decision participate in decision making;making;community members community members participate in participate in implementation; andimplementation; andcommunity members community members have control of project have control of project after completion.after completion.

Project meets basic Project meets basic needs;needs;needs met are a needs met are a development priority; development priority; andandimplementation occurs implementation occurs in association or in association or coordination with other coordination with other institutions.institutions.

Project enables Project enables development goals;development goals;does not constitute a does not constitute a burden or entail added burden or entail added costs; andcosts; andhas a long life cycle.has a long life cycle.

Resources for the Resources for the project are easily project are easily available in other available in other communities; and communities; and institutional institutional environment facilitating environment facilitating implementation is implementation is available in other available in other communities.communities.

Type of projectType of project Specific activitySpecific activity CommunityCommunity Three-for-One Three-for-One contributioncontribution(US$ as of 2003)(US$ as of 2003)

PopulationPopulation

Educational Educational infrastructureinfrastructure

School renovationSchool renovation San Juan del San Juan del CentroCentro

68,00068,000 419419

MicroenterpriseMicroenterprise Sewing workshopSewing workshop JomulquilloJomulquillo 7,2247,224 305305

Public Public infrastructureinfrastructure

Potable waterPotable water Sauz de los GarciaSauz de los Garcia 175,263175,263 138138

Business Business investmentinvestment

Lamb raising Lamb raising projectproject

El BriseñoEl Briseño 19,20019,200 91 91

Three-for-One Program projects and communities in Jerez, Zacatecas

Source: SNIM n.d.; SEPLADER 2004.

Scorecard for evaluating a project’s potential for enhancing equity

CriteriaCriteria SchoolSchool

Micro-Micro-enterprisenterprisee

Potable Potable waterwater

LambLambraisinraisingg

OwnershipOwnership

Participation in decision making;Participation in decision making; 44 44 33 33

Participation in implementation;Participation in implementation; 55 55 33 44

Control of projectControl of project 33 55 44 44

CorrespondenceCorrespondence

Project meets basic needs;Project meets basic needs; 44 44 55 33

Needs met are a development priority;Needs met are a development priority; 33 33 55 33

Implementation in association or coordination with other Implementation in association or coordination with other institutionsinstitutions 44 55 33 55

SustainabilitySustainability

Enables development goals;Enables development goals; 44 44 55 44

Does not constitute burden or entail added costs;Does not constitute burden or entail added costs; 44 33 55 44

Long life cycle Long life cycle 33 22 55 44

ReplicabilityReplicability

Resources are easily available in other communities;Resources are easily available in other communities; 44 44 44 33

Institutional environment is available in other communities Institutional environment is available in other communities 44 44 44 44

TotalTotal 4242 4343 4646 4141Source: Scorecard developed by the authors.

Strategy IV: Expansion of Financial Investment Strategy IV: Expansion of Financial Investment

0

10

20

30

40

50

60

70

80

90

Mexico El Salvador Dominican Rep. Ecuador

Adquisición de productos nostálgicos

Rum

Cigars

Tamales

Bread

Tea

Cheese

Strategy IVa: Promotion of the nostalgic Strategy IVa: Promotion of the nostalgic market market

a.a. Risk and investment analysisRisk and investment analysisb.b. Build partnerships between the private Build partnerships between the private

sector and the immigrant community;sector and the immigrant community;c.c. Financing small investment projects Financing small investment projects

within rural sectorswithin rural sectorsd.d. Involve home town associations and Involve home town associations and

NGOs with strategies to invest NGOs with strategies to invest

Strategy IVb: Tourism and Migration Strategy IVb: Tourism and Migration

Establish travel packages to traditional Establish travel packages to traditional places places

Establish new and innovative products Establish new and innovative products for tourists for tourists

Create new investment strategies to Create new investment strategies to promote tourismpromote tourism

Strategy V: Connecting the external community with assistance Strategy V: Connecting the external community with assistance

a.a. Adopt linking with the diaspora as part of the Adopt linking with the diaspora as part of the country’s foreign policy. Use the consulates as country’s foreign policy. Use the consulates as points of contact.points of contact.

b.b. Forge mutual confidence: Forge mutual confidence: a.a. Support their activities carried out as an organized groupSupport their activities carried out as an organized groupb.b. Establish ties through meetings and conferences;Establish ties through meetings and conferences;c.c. Help in the creation of a diaspora agenda;Help in the creation of a diaspora agenda;d.d. Carry out services demanded by the community;Carry out services demanded by the community;e.e. Implement summer camps programsImplement summer camps programs

c.c. Create an office of attention to nationals linving Create an office of attention to nationals linving abroadabroad

a.a. Unit of community contactUnit of community contactb.b. Unit linking the state and the communityUnit linking the state and the communityc.c. Unit of study and analysisUnit of study and analysis

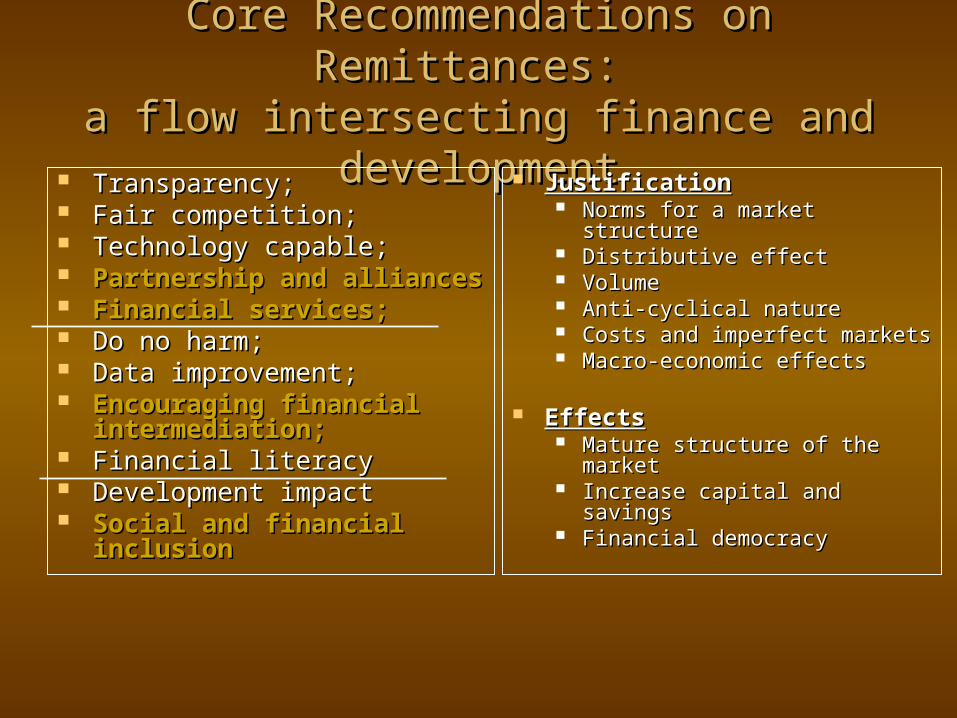

Core Recommendations on Remittances: Core Recommendations on Remittances: a flow intersecting finance and developmenta flow intersecting finance and development

Transparency;Transparency; Fair competition;Fair competition; Technology capable;Technology capable; Partnership and alliancesPartnership and alliances Financial services;Financial services; Do no harm;Do no harm; Data improvement;Data improvement; Encouraging financial Encouraging financial

intermediation;intermediation; Financial literacyFinancial literacy Development impactDevelopment impact Social and financial Social and financial

inclusion inclusion

JustificationJustification Norms for a market structureNorms for a market structure Distributive effectDistributive effect VolumeVolume Anti-cyclical natureAnti-cyclical nature Costs and imperfect marketsCosts and imperfect markets Macro-economic effectsMacro-economic effects

EffectsEffects Mature structure of the Mature structure of the

marketmarket Increase capital and savingsIncrease capital and savings Financial democracyFinancial democracy

Promoting financial literacy and consumer rightsPromoting financial literacy and consumer rights

Best Practices of Remittance Transfers: What works to the customer’s benefit.

CriteriaCriteria IndicatorsIndicators

1. 1. Transfer feeTransfer fee Lowered fees for customers may indicate Lowered fees for customers may indicate lowered costs for remittance companies.lowered costs for remittance companies.

2. 2. Exchange rate usedExchange rate used If there is no exchange rate, no currency If there is no exchange rate, no currency purchase costs are incurred by sender and purchase costs are incurred by sender and recipients. Fees may be higher, however.recipients. Fees may be higher, however.

3. 3. Transfer mechanism (hand delivery, money Transfer mechanism (hand delivery, money order, electronic transfer: debit card, bank to order, electronic transfer: debit card, bank to bank, internet, courier agency transfer, etc.)bank, internet, courier agency transfer, etc.)

More capital intensive the transactions More capital intensive the transactions mean lower costs for the company, but not mean lower costs for the company, but not necessarily lower fees for the consumer.necessarily lower fees for the consumer.

4. 4. Marketplace competition (supply side)Marketplace competition (supply side) The higher number the number of The higher number the number of companies in any market, the lower the companies in any market, the lower the transfer costs. The exception is when transfer costs. The exception is when companies are formed in monopolies, companies are formed in monopolies, oligopolies or remittance ‘cartels’.oligopolies or remittance ‘cartels’.

5. 5. Business location and geographic coverageBusiness location and geographic coverage Companies located within areas with a Companies located within areas with a better economic infrastructure exhibit better economic infrastructure exhibit lower transaction costslower transaction costs

6. 6. Development supportDevelopment support Support to the local community adds value Support to the local community adds value to the product and loyalty to the companyto the product and loyalty to the company

7. 7. Financial ServicesFinancial Services Offering services such as banking or bill Offering services such as banking or bill payment increases interest in the companypayment increases interest in the company

8. 8. TransparencyTransparency A company that advertises its exchange A company that advertises its exchange rates cultivates or promotes more trust rates cultivates or promotes more trust from the customer. from the customer.

9. 9. Compliance to regulationsCompliance to regulations A company that meets all the requirements A company that meets all the requirements operate as a remitter.operate as a remitter.

Financial Financial InstitutionInstitution

Assets Assets AccountsAccounts Approx # of accts. Opened via RemittancesApprox # of accts. Opened via Remittances Type of RemittanceType of Remittance

CitibankCitibank <50,000<50,000 Introduction of a checkless account to send moneyIntroduction of a checkless account to send money Access account / Affinity cardAccess account / Affinity card

Bank of Bank of AmericaAmerica

$736 $736 billion billion <70,000<70,000 20 20 of new accounts within the last year comeof new accounts within the last year come from the Hispanic segmentfrom the Hispanic segment

SafeSend - ATM cardSafeSend - ATM card

Bank of Bank of BeltonBelton

N/AN/A N/AN/A ACH - $20ACH - $20

Central Bank Central Bank of Kansas Cityof Kansas City

$7,333,646 $7,333,646 <5,000<5,000 Over the last six months until 1/04, about 25 of new accounts Over the last six months until 1/04, about 25 of new accounts opened had Spanish-sounding surnames. opened had Spanish-sounding surnames.

Stored-value cardStored-value card

Commercial Commercial Federal BankFederal Bank

$12.2 $12.2 billionbillion N/AN/A Standard WT and cash cards Standard WT and cash cards

First National First National Bank of Bank of OmahaOmaha

$626.7 $626.7 millionmillion <10,000<10,000 At least 40 of bank clients use remittances.At least 40 of bank clients use remittances. Standard WT and secondary Standard WT and secondary ATMATM

Harris Harris Bank/Bank of Bank/Bank of MontrealMontreal

$197 $197 billionbillion <50,000<50,000 Growth in remittances has been double digit since Growth in remittances has been double digit since the service began in 1999. the service began in 1999.

Standard WT Standard WT

Mitchell BankMitchell Bank $74.9 $74.9 millionmillion <500<500 125 125 remittance accounts remittance accounts International Transfer Acct. with International Transfer Acct. with dual ATM carddual ATM card

Northshore Northshore BankBank

$1.59 $1.59 billionbillion <500<500 400 400 remittance accountsremittance accounts Standard WT Dual ATM and Standard WT Dual ATM and debit card for Mexico debit card for Mexico

Security Security Savings BankSavings Bank

$761,058,304 $761,058,304 N/AN/A Standard WTStandard WT

United United Americas Americas BankBank

$89.4 $89.4 millionmillion <1000<1000 <1000<1000

US Bank US Bank $189 $189 billionbillion 12 12 overall increase in market share of Hispanics since the 2001 overall increase in market share of Hispanics since the 2001 launch of its Hispanic initiative. Since its launch, launch of its Hispanic initiative. Since its launch, 56 of all non-account holders have converted into regular customers 56 of all non-account holders have converted into regular customers

Secure Money Transfer (SMT) at Secure Money Transfer (SMT) at the ATM and Secure Money the ATM and Secure Money Transfer with the People’s Transfer with the People’s Network Network

Wells FargoWells Fargo $388 $388 billion billion <250,000<250,000 Above average cross-sales levels for border transaction customers. Above average cross-sales levels for border transaction customers. WF’s cross-sell ratio exceeds the banks’ average. WF’s cross-sell ratio exceeds the banks’ average.

Intercuenta Express, an account-Intercuenta Express, an account-to-account wire transfer service. to-account wire transfer service. Dinero al Instante, similar WTDinero al Instante, similar WT

Rem

ittan

ces,

ban

ks a

nd n

ew a

ccou

nts

Credit unions, remittance and membershipCredit unions, remittance and membership

Financial Financial InstitutionInstitution

Assets Assets AccouAccountsnts

Approx # of accts. Opened via RemittancesApprox # of accts. Opened via Remittances Type of RemittanceType of Remittance

Chicanos por Chicanos por la Causa la Causa Federal CUFederal CU

$4.47 $4.47 millionmillion

<500<500 In 2003, the CU made 355 transmissions worth $150,000.In 2003, the CU made 355 transmissions worth $150,000. IRnetIRnet

Greater El Greater El Paso's CUPaso's CU

$940,348,56$940,348,560 0

<500<500 Averages close to 70 transactions per month at about $Averages close to 70 transactions per month at about $300-$500 300-$500 each.each.

IRnetIRnet

Midwest Midwest Industrial Industrial Credit UnionCredit Union

$5.5 $5.5 millionmillion <500<500 25-35 25-35 remittance transactions per month. Over the past two remittance transactions per month. Over the past two years, years, the newest influence on the CU has been 75 Hispanic.the newest influence on the CU has been 75 Hispanic.

IRnetIRnet

Coasthills Coasthills Community Community CUCU

$402 $402 millionmillion <500<500 In 2002, the CU made 268 Vigo transactions and 394 in 2003. In 2002, the CU made 268 Vigo transactions and 394 in 2003. 75 of individuals who open accounts at the Santa Maria branches 75 of individuals who open accounts at the Santa Maria branches are Spanish-speaking. are Spanish-speaking.

IRnetIRnet

Latino Latino Community Community Credit UnionCredit Union

$14 $14 millionmillion <1000<1000 In 2003, the CU wired $1.5 million. In 2003, the CU wired $1.5 million. IRnet and Visa ATM check IRnet and Visa ATM check card.card.

Santa Cruz Santa Cruz Community Community CUCU

$58,215,520 $58,215,520 From 2002-2003, volume has doubled both in terms of number From 2002-2003, volume has doubled both in terms of number of transactions of transactions and dollar amounts. and dollar amounts.

VigoVigo

Laredo Laredo Federal Federal Credit UnionCredit Union

$81 $81 million million <500<500 30 30 transactions per monthtransactions per month VigoVigo

““The demand for financial services by remittance receiving households The demand for financial services by remittance receiving households rests on the intersection between the role of microfinance institutions, rests on the intersection between the role of microfinance institutions,

such as credit unions, and rural sector development.” such as credit unions, and rural sector development.”

$1.2$4.1

$9.6$13.5

$17.1

$24.0

$41.2

$0.0

$10.0

$20.0

$30.0

$40.0

$50.0

Q4 01 Q1 02 Q2 02 Q3 02 Q4 02 Q1 03 Q2 03

Volume of Remittances Distributed by 62 Central American CUs in US$ Millions

Mexico: Remittances to rural households Mexico: Remittances to rural households

$106,862 $442,704$1,053,786

$1,923,668

$3,256,231

$15,027,550

$0

$2,000,000

$4,000,000

$6,000,000

$8,000,000

$10,000,000

$12,000,000

$14,000,000

$16,000,000

Menos de 999 1,000 a 2999 3,000 a 4999 5,000 a 9,999 10,000 a 14,999 Mas de 15,000

15 recibe US$250 al mes, siete veces al año.

Strategy IIb: Remittances and TechnologyStrategy IIb: Remittances and Technology

Wireless internet accessibility, Wi-Fi (Wireless Fidelity) Wireless internet accessibility, Wi-Fi (Wireless Fidelity) offers the opportunity to integrate the rural sector using offers the opportunity to integrate the rural sector using computer equipment at a low costcomputer equipment at a low cost

Computers with Wi-Fi send and receive information using Computers with Wi-Fi send and receive information using radio wavesradio waves

This system could be used to send remittances This system could be used to send remittances This technology could be administered by local micro-This technology could be administered by local micro-

finance institutions finance institutions This system also could offer advantages to local businesses This system also could offer advantages to local businesses

as to generate investment (such as a discount of half or a as to generate investment (such as a discount of half or a third of the actual price of a phone call) and simultaneously third of the actual price of a phone call) and simultaneously an opportunity for new markets an opportunity for new markets

Volume and Price in Volume and Price in Latin AmericaLatin America

Manuel OrozcoManuel Orozco

Remittances to Latin America, 2001-2003

9,273

2,600

1,600

1,807

1,920

584

1,400

967

930

905

810

460

610

103

42

10,502

4,600

2,431

2,206

2,111

1,689

1,575

1,288

1,265

1,138

931

770

759

235

119

104

59

38

13,266

5200

3,067

2217

2316

2106

1656.9

1425.9

1194

1295

977

862

787.5

247

306

136.5

340

88

225

73.5

0 2,000 4,000 6,000 8,000 10,000 12,000 14,000

Mexico

Brazil a

Colombia

Dominicana

El Salvador

Guatemala

Ecuador

Jamaica

Cuba a

Peru

Haiti a

Honduras

Nicaragua a

Venezuela

Costa Rica

Guyana a

Bolivia

Trinidad y Tobago

Argentina

Belize

2003 (38 billion)2002 (32 billion)2001 (24 billion)

Quarterly flows to selected Latin American Quarterly flows to selected Latin American countriescountries

20

70

120

170

220

Jan-

99

Mar

-99

May

-99

Jul-9

9

Sep-9

9

Nov-99

Jan-

00

Mar

-00

May

-00

Jul-0

0

Sep-0

0

Nov-00

1-Ja

n

1-Mar

1-May

1-Ju

l

1-Sep

1-Nov

2-Ja

n

2-Mar

2-May

Jul.

2002

Sept.

2002

Nov. 200

2

3-Ja

n

3-Mar

3-May

3-Ju

l

3-Sep

5

5.5

6

6.5

7

7.5

8

8.5

9

Jamaica

Guatemala

El Salvador

Dominican Republic

Latino Unemployment

Remittances to Latin America: average amount sent by an immigrantRemittances to Latin America: average amount sent by an immigrant

393

365

340

300

299

286

281

273

266

263

244

236

223

208

199

183

173

156

154

153

146

0 50 100 150 200 250 300 350 400 450

El Salvador

Mexico

Costa Rica

Ecuador

Brazil

Chile

Paraguay

Guatemala

Jamaica

Colombia

Honduras

Bolivia

Argentina

Panama

Uruguay

Dom. Rep.

Peru

Venezuela

Guyana

Haiti

Nicaragua

2003 2002

Latin Remittance SenderLatin Remittance Sender

A person who represents two thirds of A person who represents two thirds of immigrants;immigrants;

Sends regularly, at least ten times a year;Sends regularly, at least ten times a year; Has an income below $25,000 (60);Has an income below $25,000 (60); Has a basic education below high school (50);Has a basic education below high school (50); Sends about $3,000 annually;Sends about $3,000 annually; Has a longstanding commitment with their Has a longstanding commitment with their

parents (at least 5 years);parents (at least 5 years); Uses intermediaries to send money (70);Uses intermediaries to send money (70); Does not have a bank account (40);Does not have a bank account (40); Is an adult over 36 years old;Is an adult over 36 years old;

Average amount sent and length of time living in the Average amount sent and length of time living in the U.S.U.S.

0

5

10

15

20

25

30

35

Menos de un año Entre uno y tresaños

Entre cuatro yseis años

Entre siete ynueve años

Mas de diez

Cuba Guyana Dominican Republic LAC average

Immigrants and bank accountsImmigrants and bank accounts

0

10

20

30

40

50

60

70

80

Bank Account (%) No Bank Account (%)

Cuba Guyana Dominican Republic Total

Why doesn’t have a bank account?Why doesn’t have a bank account?

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

Do not trust banks Doesn't have papers Doesn't need bank acc.

Cuba Guyana Dominican Republic LAC average

Do you have debit, credit card, or bothDo you have debit, credit card, or both

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

I have both Credit Debit I have none

Cuba Guyana Dominican Republic LAC average

Do you have financial obligations (loans)?Do you have financial obligations (loans)?

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

Cuba Guyana Dominican Republic LAC average

Personal Income and Years living in U.S.Personal Income and Years living in U.S.

0

5

10

15

20

25

30

35

Less than sixyears

Seven totwelve

Over twelveyears

Hasta 10,000

Entre 10,001 y 15,000

Entre 15,001 y 20,000

Entre 20,001 y 25,000

Entre 25,001 y 30,000

Entre 30,001 y 35,000

Más de 35,000

Remittances and the Remittances and the MarketMarket

Some features and trendsSome features and trends

Money TransferCompany

MTC’s bank

MTC’s rec. country Agent Distributor

AD’s bank

Data Transfer Report(customer’s sendingInformation)

Wire Transfer (cash transferAmount)

MTC’s AgentPOS

MTC’s AgentPOS

Remittance sender

Remittance

recip

ient

Regulatory EnvironmentComplianceMonitoring

International money transfer operation

MTC: Money transfer companyPOS: Point of saleAD: Agent distributor (on receiving side)

TWO DATASTREAMS

The Transfer of Remittances: A Diffuse The Transfer of Remittances: A Diffuse MarketMarket

• Change•Proliferation of companies in process of consolidation, • Slow but gradual decline in the transfer costs;•New practices and services provided•Growing interest of the banking community and governments

•Continuity•Charges remain expensive, as well as exchange rate•Charges vary among countries•Competition has yet to affect oligopolies•Little incentives on senders or recipients

Competition among major remittance Competition among major remittance recipientsrecipients

0

2

4

6

8

10

12

14

16

Company 90s Company 02 Prices 90s Prices 02

MexicoEl SalvadorDominican RepublicGuatemalaJamaica

Number of money transfer companies holding 50 or more of market share

Cost of sending money to selected countries (as percent of principal sent)