DISPUTE RESOLUTION PANEL - nirc@icai DRP PPT - Yogesh ji.pdf · DRP? •Dispute Resolution Panel...

37

DISPUTE RESOLUTION PANEL SECTION 144C OF INCOME TAX ACT 1961

Transcript of DISPUTE RESOLUTION PANEL - nirc@icai DRP PPT - Yogesh ji.pdf · DRP? •Dispute Resolution Panel...

DISPUTE RESOLUTION PANEL

SECTION 144C OF INCOME TAX ACT 1961

Genesis

• The multinational corporations operating in India face taxation issues on three counts:

– income characterization (withholding tax on royalties and fees

for technical services)

– permanent establishment issues

– transfer pricing.

• The resulting litigation induces a high degree of uncertainty into business operations of the corporations in India

2 YKV/CIT 06/13/2015

Statute

• The intent to minimize tax disputes

• SECTION 144C OF THE INCOME-TAX ACT, 1961 - DISPUTE RESOLUTION PANEL (DRP) - REFERENCE TO - RECONSTITUTION OF DRPs AT DELHI, MUMBAI

& BENGALURU - SUPERSESSION OF EARLIER SPECIFIED ORDERS- ORDER NO.1/FT&TR/2015 [F.NO.500/25/2014-SO/FT&TR-2(1)], DATED 1-1-2015.

3 YKV/CIT 06/13/2015

DRP?

• Dispute Resolution Panel (DRP ) is a collegium of three commissioners rank officers to hear the dispute between assessee and the A.O in a transfer pricing taxation matter. Finance (No.2) Bill, 2009 inserted section 144C effective from 1st day of October, 2009 in the income tax act to create an alternative dispute resolution mechanism

4 YKV/CIT 06/13/2015

PURPOSE

• Minimize Litgation

• Well Considered Findings

• Speaking Directions

• Opportunity of hearing to both sides

• Three member panel

5 YKV/CIT 06/13/2015

Basis

• In the Notes on Clauses to the Finance Bill 2009, the purpose and context of this provision has been explained as – – “The subjects of transfer pricing audit and the taxation of

foreign company are at nascent stage in India. Often the Assessing Officers and Transfer Pricing Officers tend to take a conservative view. The correction of such view takes very long time with the existing appellate structure.

– With a view to provide speedy disposal, it is proposed to amend the Income-tax Act so as to create an alternative dispute resolution mechanism within the income-tax department and accordingly, section 144C has been proposed to be inserted so as to provide inter alia the Dispute Resolution Panel as an alternative dispute resolution mechanism.”

6 YKV/CIT 06/13/2015

Basis

• The Explanatory notes to Finance (No.2) Act 2009 issued by the Board also give following reason for this amendment -

• “The dispute resolution mechanism presently in place is time consuming and finality in high demand cases is attained after long drawn litigation till Supreme Court. In order to address the concern of the multi-national companies and to provide mechanism for speedy disposal of their cases so as to attain finality, a new section 144C is inserted in the Income-tax Act to facilitate expeditious resolution of disputes.”

7 YKV/CIT 06/13/2015

Basis

• Existing appellate structure is time consuming. The purpose of this mechanism is to provide speedy disposal of disputes.

• Assessing Officers tend to take a conservative view- that can be rationalized via this mechanism.

8 YKV/CIT 06/13/2015

DRP-ADR

• The Dispute Resolution Panel (DRP) under the Income Tax Act, 1961 is an Alternative Dispute Resolution (ADR) mechanism for resolving the disputes relating to Transfer Pricing in International Transactions.

• Section 144C [Reference to Dispute Resolution Panel] governs the provisions relating to DRP constituted by [Central Board of Direct Taxes] for this purpose.

9 YKV/CIT 06/13/2015

DRP-ADR

• Section 144C comes into picture when the order proposed by the Assessing Officer is prejudicial to the interest of the assessee. The AO forwards a draft of the proposed order to the assessee in order to invite his acceptance or objections to the same.

• Assessee under section 144C refers to a Foreign Company and any person in whose case AO proposes to make any variation in the income or loss stated in the return filed by such person, as a consequence of the order passed by the Transfer Pricing Officer under Sub Section (3) of Section 92CA of the ITA.

06/13/2015 YKV/CIT 10

Earlier system

• Prior to the formation of DRP the assessee had to approach the Commissioner of Income Tax Appeal CIT (A) against the Assessment Order to contest it.

• The assessee has an additional option to approach DRP on the basis Draft Order issued by AO. The Draft Order can be acceptable or unacceptable to the Assessee.

• In case, the assessee wants to file the Objections against the variations proposed by the AO, the same can now be done.

11 YKV/CIT 06/13/2015

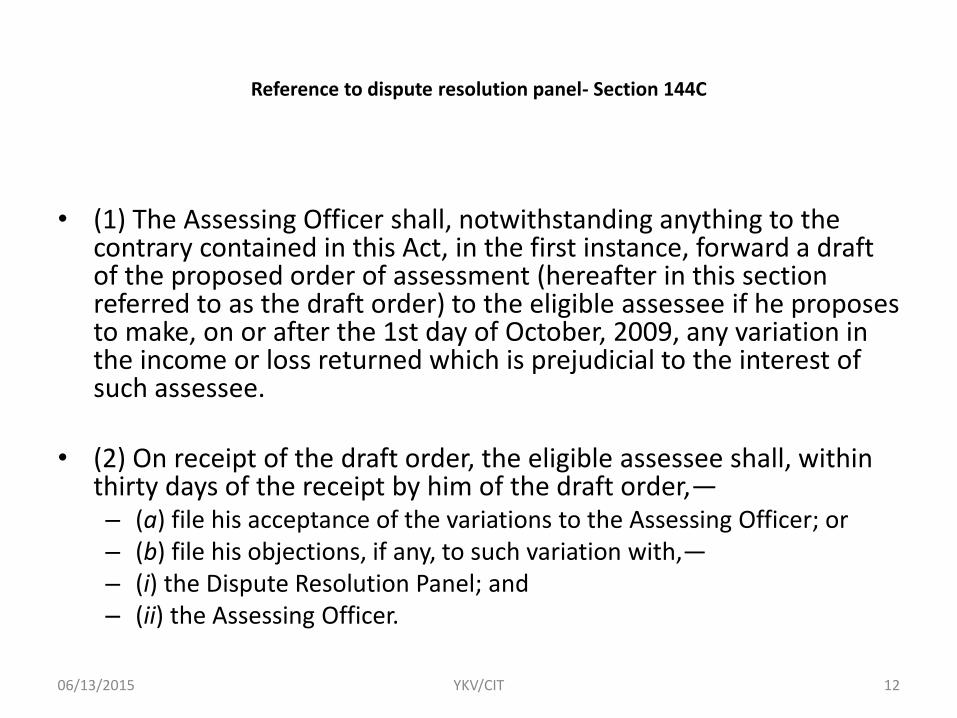

Reference to dispute resolution panel- Section 144C

• (1) The Assessing Officer shall, notwithstanding anything to the

contrary contained in this Act, in the first instance, forward a draft of the proposed order of assessment (hereafter in this section referred to as the draft order) to the eligible assessee if he proposes to make, on or after the 1st day of October, 2009, any variation in the income or loss returned which is prejudicial to the interest of such assessee.

• (2) On receipt of the draft order, the eligible assessee shall, within

thirty days of the receipt by him of the draft order,— – (a) file his acceptance of the variations to the Assessing Officer; or – (b) file his objections, if any, to such variation with,— – (i) the Dispute Resolution Panel; and – (ii) the Assessing Officer.

YKV/CIT 12 06/13/2015

Reference to dispute resolution panel- Section 144C

• (3) The Assessing Officer shall complete the assessment on the basis of the draft order, if— – (a) the assessee intimates to the Assessing Officer the acceptance of the

variation; or – (b) no objections are received within the period specified in sub-section (2).

• (4) The Assessing Officer shall, notwithstanding anything contained

in section 153 [or section 153B], pass the assessment order under sub-section (3) within one month from the end of the month in which,— – (a) the acceptance is received; or – (b) the period of filing of objections under sub-section (2) expires.

• (5) The Dispute Resolution Panel shall, in a case where any objection is

received under sub-section (2), issue such directions, as it thinks fit, for the guidance of the Assessing Officer to enable him to complete the assessment.

YKV/CIT 13 06/13/2015

Reference to dispute resolution panel- Section 144C

• (6) The Dispute Resolution Panel shall issue the directions referred to in sub-section (5), after considering the following, namely:— – (a) draft order; – (b) objections filed by the assessee; – (c) evidence furnished by the assessee; – (d) report, if any, of the Assessing Officer, Valuation Officer or Transfer Pricing Officer or any

other authority; – (e) records relating to the draft order; – (f) evidence collected by, or caused to be collected by, it; and – (g) result of any enquiry made by, or caused to be made by, it.

• (7) The Dispute Resolution Panel may, before issuing any directions referred to in sub-section (5),— – (a) make such further enquiry, as it thinks fit; or – (b) cause any further enquiry to be made by any income-tax authority and report the result of

the same to it.

YKV/CIT 14 06/13/2015

Reference to dispute resolution panel- Section 144C

• (8) The Dispute Resolution Panel may confirm, reduce or enhance the variations proposed in the draft order so, however, that it shall not set aside any proposed variation or issue any direction under sub-section (5) for further enquiry and passing of the assessment order.

[Explanation.—For the removal of doubts, it is hereby declared that the power of the Dispute Resolution Panel to enhance the variation shall include and shall be deemed always to have included the power to consider any matter arising out of the assessment proceedings relating to the draft order, notwithstanding that such matter was raised or not by the eligible assessee.]

06/13/2015 YKV/CIT 15

Reference to dispute resolution panel- Section 144C

• (9) If the members of the Dispute Resolution Panel differ in opinion on any point, the point shall be decided according to the opinion of the majority of the members.

• (10) Every direction issued by the Dispute Resolution Panel shall be

binding on the Assessing Officer. • (11) No direction under sub-section (5) shall be issued unless an

opportunity of being heard is given to the assessee and the Assessing Officer on such directions which are prejudicial to the interest of the assessee or the interest of the revenue, respectively.

• (12) No direction under sub-section (5) shall be issued after nine months

from the end of the month in which the draft order is forwarded to the eligible assessee.

YKV/CIT 16 06/13/2015

• (13) Upon receipt of the directions issued under sub-section (5), the Assessing Officer shall, in conformity with the directions, complete, notwithstanding anything to the contrary contained in section 153 [or section 153B], the assessment without providing any further opportunity of being heard to the assessee, within one month from the end of the month in which such direction is received.

• (14) The Board may make rules for the purposes of the efficient

functioning of the Dispute Resolution Panel and expeditious disposal of the objections filed under sub-section (2) by the eligible assessee.

06/13/2015 YKV/CIT 17

Reference to dispute resolution panel- Section 144C

• (14A) The following sub-section (14A) shall be inserted after sub-section (14) of section 144C by the Finance Act, 2013, w.e.f. 1-4-2016 :

• (14A) The provisions of this section shall not apply to any assessment or reassessment order passed by the Assessing Officer with the prior approval of the [Principal Commissioner or] Commissioner as provided in sub-section (12) of section 144BA.

YKV/CIT 18 06/13/2015

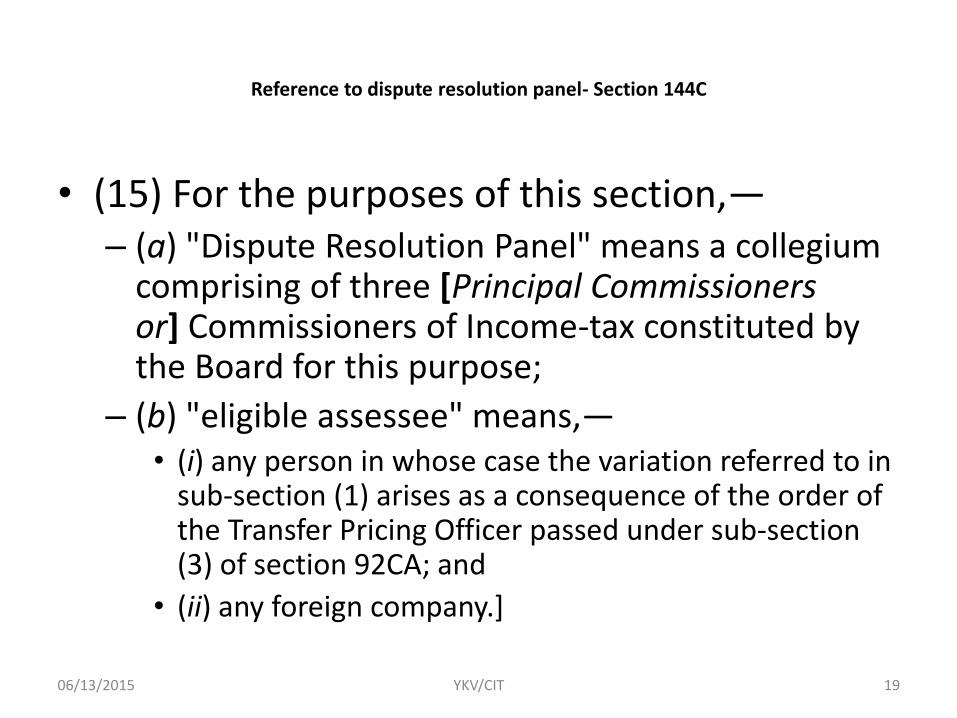

Reference to dispute resolution panel- Section 144C

• (15) For the purposes of this section,— – (a) "Dispute Resolution Panel" means a collegium

comprising of three [Principal Commissioners or] Commissioners of Income-tax constituted by the Board for this purpose;

– (b) "eligible assessee" means,— • (i) any person in whose case the variation referred to in

sub-section (1) arises as a consequence of the order of the Transfer Pricing Officer passed under sub-section (3) of section 92CA; and

• (ii) any foreign company.]

06/13/2015 YKV/CIT 19

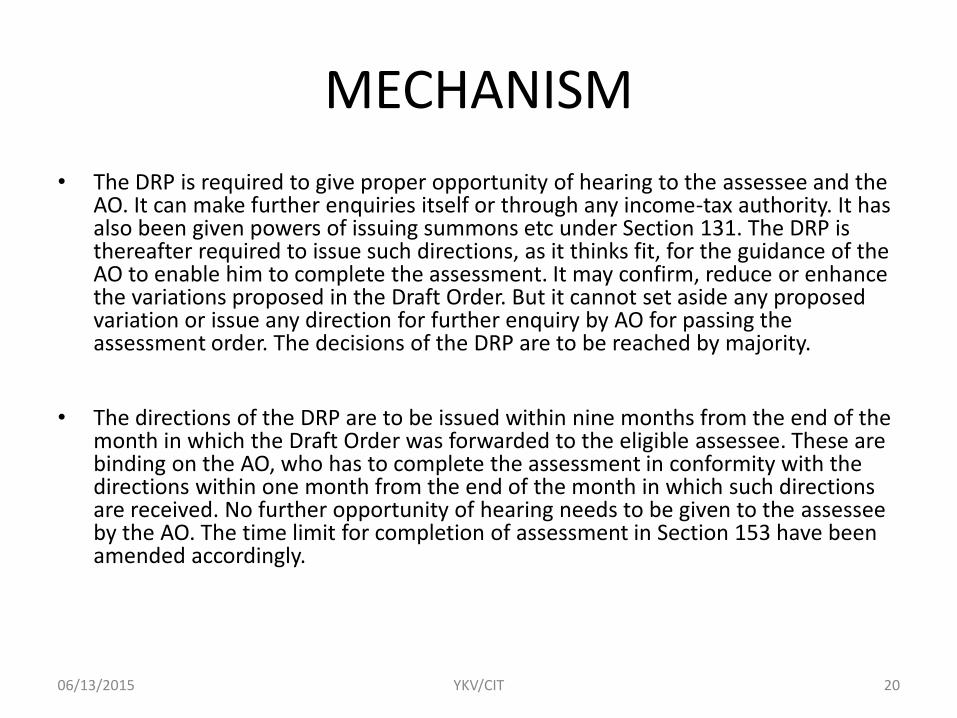

MECHANISM

• The DRP is required to give proper opportunity of hearing to the assessee and the AO. It can make further enquiries itself or through any income-tax authority. It has also been given powers of issuing summons etc under Section 131. The DRP is thereafter required to issue such directions, as it thinks fit, for the guidance of the AO to enable him to complete the assessment. It may confirm, reduce or enhance the variations proposed in the Draft Order. But it cannot set aside any proposed variation or issue any direction for further enquiry by AO for passing the assessment order. The decisions of the DRP are to be reached by majority.

• The directions of the DRP are to be issued within nine months from the end of the month in which the Draft Order was forwarded to the eligible assessee. These are binding on the AO, who has to complete the assessment in conformity with the directions within one month from the end of the month in which such directions are received. No further opportunity of hearing needs to be given to the assessee by the AO. The time limit for completion of assessment in Section 153 have been amended accordingly.

20 YKV/CIT 06/13/2015

The Procedure

• After receiving Objections the DRP goes through the Draft Order;

objections filed by the assessee; evidence furnished by the assessee; report, if any, of the Assessing Officer, Valuation Officer or Transfer Pricing Officer or any other authority; records relating to the draft order; evidence collected by, or caused to be collected by, it; and result of any enquiry made by, or caused to be made by, it and issue such directions, as it thinks fit, for the guidance of the AO to enable him to complete the assessment.

• The DRP may confirm, reduce or enhance the variations proposed in the draft order, however, it shall not set aside any proposed variation or issue any direction for the guidance of the AO for further enquiry and passing of the assessment order.

• If the members of the DRP differ in opinion on any point, the point shall be decided according to the opinion of the majority of the members.

21 YKV/CIT 06/13/2015

The Procedure

• The Directions for the guidance of AO will be given only after the assessee and the AO have been given an opportunity to present their case.

• After receiving the Directions in the nature of guidance from DRP the AO shall, in conformity with the directions, complete the assessment without providing any further opportunity of being heard to the assessee, within one month from the end of the month in which such direction is received.

• The Directions given by DRP are binding on the AO, the Directions can be challenged by the assessee before the Income Tax Appellate Tribunal (ITAT).

• The DRP has to complete the hearing and give its final Directions within a period of 9 months from the end of the month in which the draft order was forwarded to the assessee.

06/13/2015 YKV/CIT 22

Structure

• Recently, a Division Bench of Hon'ble Bombay High Court, while deciding the Writ Petition filed by Vodafone India Services Pvt. Ltd. vs Union of India and Others made the following observation with regards to DRP.

• "The proceeding before the DRP is not an appeal proceeding but a correcting mechanism in the nature of a second look at the proposed assessment order by high functionaries of the revenue keeping in mind the interest of the assesee. It is a continuation of the Assessment proceedings till such time a final order of assessment which is appealable is passed by the Assessing Officer. This also finds support from Section 144C(6) which enables the DRP to collect evidence or cause any enquiry to be made before giving directions to the Assessing Officer under Section 144C(5) . The DRP procedure can only be initiated by an assessee objecting to the draft assessment order. This would enable correction in the proposed order (draft assessment order) before a final assessment order is passed. Therefore, we are of the view that in the present facts this issue could be agitated before and rectified by the DRP."

23 YKV/CIT 06/13/2015

Nature

• The DRP is an Alternative Dispute Mechanism, set up with a view to minimize the tax disputes relating to Transfer Pricing in International Transactions.

• The process of inviting objections to the Draft Assessment Order gives an opportunity to the assessee to raise objections, if any, at an early date and helps in giving finality to the Assessment Order.

• The fixed time frame of 9 months to decide the Matter assures the assesse that the Matter will be decided in a fixed time.

• The binding nature of the Order of the DRP on the Aseesssing Officer provides a clear picture to the Assessee with regards to its Tax Liability.

24 YKV/CIT 06/13/2015

DRP Rules

• Vide its Notification 84/2009 of 20-11-2009, Board has notified a new set of Rules called Income-tax (Dispute Resolution Panel) Rules, 2009. Rule 3(2) of these provides that the Board shall assign three Commissioners of Income-tax by name to each DRP as members who, shall carry on the functions of the DRP in addition to their regular duties as Commissioners. Where a member of a DRP is transferred, the Board shall assign another Commissioner in his place.

• Each DRP will have a secretariat for receiving objections and documents etc, and for issuing notices and directions etc on its behalf.

• The objections of the eligible assessee to the Draft Order are to be filed with the Secretariat within the specified period in Form No. 35A in paper book form in quadruplicate together with copies of the Draft Order and evidence the assessee intends to rely upon including any documents submitted to the AO.

• The DRP has power to permit the assessee to produce new evidence or examine a witness or file an affidavit etc, but after recording reasons for doing so. Further, Rule 10(2) says that jurisdiction of the DRP shall not be confined only to the grounds raised in the objections but will cover all matters arising out of the proceedings.

25 YKV/CIT 06/13/2015

Important

• The Gujarat High Court in the case of Pankaj Extrusion Ltd. v. ACIT 2011] 198 TAXMAN 6 (Guj.) held that the plain reading of clause (b) of sub-section (15) of section 144C would show that an assessee can be stated to be an eligible assessee as referred to in sub-section (1) of section 144C in whose case variation referred to in the said sub-section arises as a consequence of order of TPO passed under sub-section (3) of section 92CA.

26 YKV/CIT 06/13/2015

DRP Features

• DRP route is optional

• Powers of DRP-the panel shall consider the following;

– the draft order,

– objections filed by the assessee,

– evidence furnished by the assessee,

– report, if any, of the AO, the Valuation Officer or the TPO or any other authority,

– records relating to the draft order,

– evidence collected by, or caused to be collected by it, and

– results of any enquiry made by it or caused to be made by it.

27 YKV/CIT 06/13/2015

DRP Features

• DRP has power of enhancement

• DRP has no power to remit back case to AO for further enquiry

• DRP can entertain additional evidences

• Time-limit for issue of directions

• DRP’s directions are binding on AO

• Both assessee and revenue( July 2012) can file appeal against DRP order before ITAT

28 YKV/CIT 06/13/2015

Implications of introduction of DRP in the assessment process

• - Section 144C has been inserted in Chapter-XIV of the Income Tax Act relating to procedure of assessment. DRP is a part of the assessment machinery and the proceedings before the DRP are part of assessment proceedings.

• The same are neither appellate nor settlement nor arbitration process.

• The directions of the DRP are binding on the AO , but can be contested by the AO and the assessee. An alternate dispute resolution mechanism that does not bind both parties to the dispute can have no finality. This only confirms that the DRP mechanism is part of the assessment process only.

29 YKV/CIT 06/13/2015

Implications of introduction of DRP in the assessment process

• The implications of the new procedure are - In the cases of the ‘eligible assessees' (foreign companies and Transfer

Pricing cases under Section 92CA(3) ) the AO pass a Draft Order seeking objections by assessee. The assessment proceedings will be over only after the procedure laid down in Section 144C is completed. it is open for these assessees to not file objections against the Draft Order before the DRP and instead challenge the assessment order before the Commissioner (Appeals).

In cases where objections are filed against the Draft Order, the DRP has to issue directions within nine months, from the end of the month in which that order was forwarded to the assessee. The AO will have another month to pass the assessment order. Therefore, the assessment process in these cases will be extended by almost a year. This will be over and above the time taken by the TPO for passing the order under Section 92CA(3).

06/13/2015 YKV/CIT 30

Implications of introduction of DRP in the assessment process

• The jurisdiction of the DRP will commence from the time assessee's objections against Draft Order are received and will continue till directions are issued by it.

• The principles of natural justice will apply in the proceedings before the DRP . The DRP will have to consider the objections, examine the records, the evidence produced, conduct any other enquiries that may be necessary, give opportunity of hearing to both parties, and pass a reasoned and speaking order on the objections raised by the assessee.

• The matters in these cases are complicated and involve large revenue, the responsibility of the DRPs is onerous.

06/13/2015 YKV/CIT 31

Implications of introduction of DRP in the assessment process

• DRPs have the power to enhance the income proposed in the Draft Order wherever necessary.

• DRPs, being part of the assessment process, is governed by normal rules of evidence and jurisprudence applicable to the assessing authorities – including Instructions of the Board. The normal practice in assessment proceedings is that in case of doubt the assessing authorities err on the side of Revenue, i.e. where two views are possible they take the view in favour of Revenue.

• Further, DRPs are not appellate bodies they may decide any ongoing disputes of law coming from earlier years in favour of Revenue till these legal questions are finally settled by High Court or Supreme Court.

32 YKV/CIT 06/13/2015

Implications of introduction of DRP in the assessment process

• First appeal against assessment orders completed as per the directions of DRP will lie before the Tribunal. Tribunal is the final fact finding body.

06/13/2015 YKV/CIT 33

Implications of introduction of DRP in the assessment process

• It is common experience that Tribunal decides disputes of facts on the basis of assertions / averments made and evidence led before the lower authorities, except in a few cases where it admits new evidence on special grounds. In matters coming to it in second appeal from orders of Commissioner (Appeals), deficiencies in rival evidence get addressed in first appeal and the issues in dispute get fully crystallized by the time they reach Tribunal. This would not be so in matters coming to it in first appeal from the orders passed on the basis of directions of the DRP.

06/13/2015 YKV/CIT 34

Implications of introduction of DRP in the assessment process

• The Tribunal has 65 benches located at about 30 stations whereas there are nearly 300 Commissioner (Appeals) stationed at over 100 stations. Section 254(2A) of the Income Tax Act expects that the Tribunal will decide appeals within four years from the end of the year in which these are filed, that too wherever possible. Therefore, it is unlikely that first appeals in these cases will get decided faster than those going to the Commissioner (Appeals).

06/13/2015 YKV/CIT 35

Implications of introduction of DRP in the assessment process

• The Tribunal has powers to stay tax demands up to an aggregate period of 365 days. However, where the Tribunal grants stay it has the obligation to decide the appeal within the stay period, provided the delay is not attributable to the assessee. The Tribunal also has the power of setting aside an assessment back to the AO. Both these powers are not available to the Commissioner (Appeals). Therefore, the assessees opting for the DRP route can move the Tribunal for grant of stay of disputed demand. Since this will be a first appeal it is more likely that the Tribunal would be inclined to stay the demand.

• Since both the Department as well as the taxpayer are entitled to go in further appeals against the orders of ITAT to the High Court and then to Supreme Court, neither the orders of DRP nor of the Tribunal will be final.

06/13/2015 YKV/CIT 36

Implications of introduction of DRP in the assessment process

• To sum up, DRPs are an extension of the assessment process to a the level of a collegium of three Commissioners. This can curb blatantly illegal variations to the returned incomes. A silver lining for the taxpayer is that it can straight away file appeal against the assessment order to Tribunal and seek stay of disputed tax demand.

37 YKV/CIT 06/13/2015