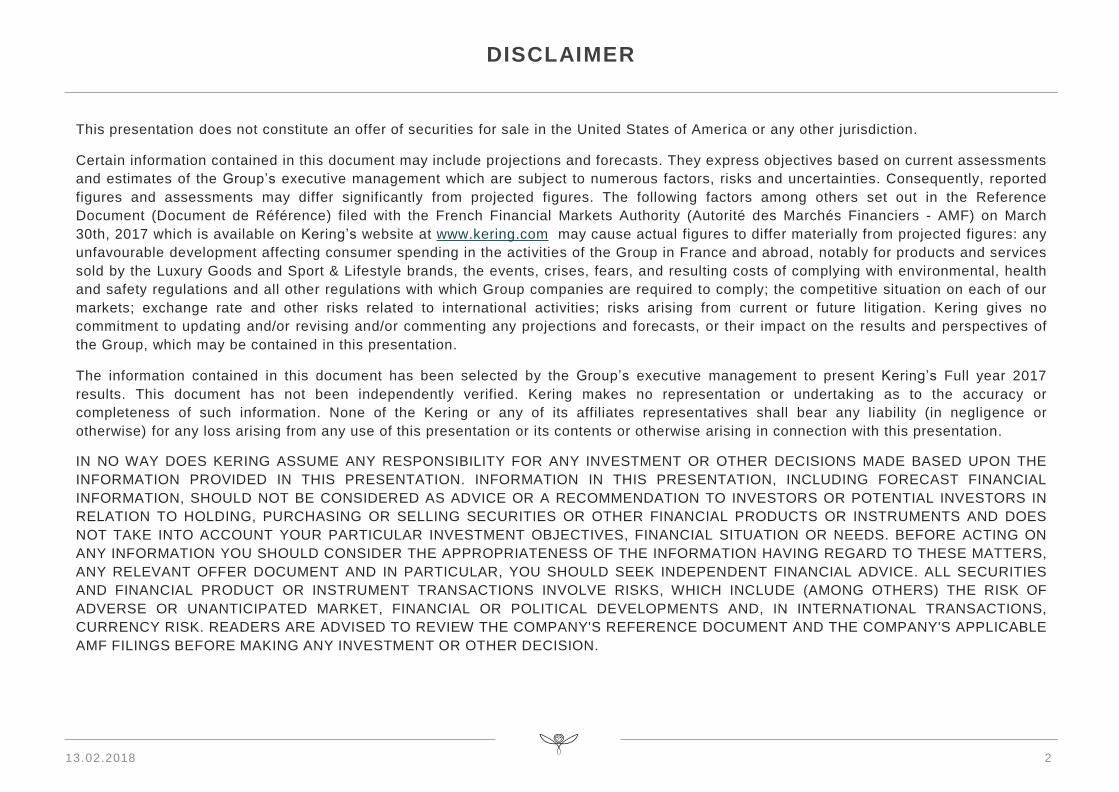

DISCLAIMER - kering.com · 2 DISCLAIMER This presentation does not constitute an offer of...

51

Transcript of DISCLAIMER - kering.com · 2 DISCLAIMER This presentation does not constitute an offer of...

2

DISCLAIMER

This presentation does not constitute an offer of securities for sale in the United States of America or any other jurisdiction.

Certain information contained in this document may include projections and forecasts. They express objectives based on current assessments

and estimates of the Group’s executive management which are subject to numerous factors, risks and uncertainties. Consequently, reported

figures and assessments may differ significantly from projected figures. The following factors among others set out in the Reference

Document (Document de Référence) filed with the French Financial Markets Authority (Autorité des Marchés Financiers - AMF) on March

30th, 2017 which is available on Kering’s website at www.kering.com may cause actual figures to differ materially from projected figures: any

unfavourable development affecting consumer spending in the activities of the Group in France and abroad, notably for products and services

sold by the Luxury Goods and Sport & Lifestyle brands, the events, crises, fears, and resulting costs of complying with environmental, health

and safety regulations and all other regulations with which Group companies are required to comply; the competitive situation on each of our

markets; exchange rate and other risks related to international activities; risks arising from current or future litigation. Kering gives no

commitment to updating and/or revising and/or commenting any projections and forecasts, or their impact on the results and perspectives of

the Group, which may be contained in this presentation.

The information contained in this document has been selected by the Group’s executive management to present Kering’s Full year 2017

results. This document has not been independently verified. Kering makes no representation or undertaking as to the accuracy or

completeness of such information. None of the Kering or any of its affiliates representatives shall bear any liability (in negligence or

otherwise) for any loss arising from any use of this presentation or its contents or otherwise arising in connection with this presentation.

IN NO WAY DOES KERING ASSUME ANY RESPONSIBILITY FOR ANY INVESTMENT OR OTHER DECISIONS MADE BASED UPON THE

INFORMATION PROVIDED IN THIS PRESENTATION. INFORMATION IN THIS PRESENTATION, INCLUDING FORECAST FINANCIAL

INFORMATION, SHOULD NOT BE CONSIDERED AS ADVICE OR A RECOMMENDATION TO INVESTORS OR POTENTIAL INVESTORS IN

RELATION TO HOLDING, PURCHASING OR SELLING SECURITIES OR OTHER FINANCIAL PRODUCTS OR INSTRUMENTS AND DOES

NOT TAKE INTO ACCOUNT YOUR PARTICULAR INVESTMENT OBJECTIVES, FINANCIAL SITUATION OR NEEDS. BEFORE ACTING ON

ANY INFORMATION YOU SHOULD CONSIDER THE APPROPRIATENESS OF THE INFORMATION HAVING REGARD TO THESE MATTERS,

ANY RELEVANT OFFER DOCUMENT AND IN PARTICULAR, YOU SHOULD SEEK INDEPENDENT FINANCIAL ADVICE. ALL SECURITIES

AND FINANCIAL PRODUCT OR INSTRUMENT TRANSACTIONS INVOLVE RISKS, WHICH INCLUDE (AMONG OTHERS) THE RISK OF

ADVERSE OR UNANTICIPATED MARKET, FINANCIAL OR POLITICAL DEVELOPMENTS AND, IN INTERNATIONAL TRANSACTIONS,

CURRENCY RISK. READERS ARE ADVISED TO REVIEW THE COMPANY'S REFERENCE DOCUMENT AND THE COMPANY'S APPLICABLE

AMF FILINGS BEFORE MAKING ANY INVESTMENT OR OTHER DECISION.

13.02.2018

INTRODUCTION

FRANÇOIS-HENRI PINAULT

CHAIRMAN AND CEO

ANALYSIS OF RESULTS

JEAN-MARC DUPLAIX

GROUP CHIEF FINANCIAL OFFICER

NET DEBTFCF FROM OPERATIONS

4,371

3,049

2016 2017

1,189

2,318

2016 2017

+4.6%

+8.1%

+27.2%

2015 2016 2017

1,6471,886

2,948

2015 2016 2017

In €m In €m

RECORD OPERATING PERFORMANCES IN 2017

% comparable growth*

GROUP RECURRING

OPERATING INCOME

€2,948m

+56% vs. 2016

FCF AND NET DEBT

FCF of €2,318m

Net debt down, debt-to-

EBITDA ratio at 0.9x

• Recurring operating income

at record level

• Operating margin up 3.8 pt

• Group CAPEX: €752m, 4.9%

of revenue

• Operating FCF

nearly doubled; Net debt down

by more than €1.3bn

€15,478m

+25.0% reported

+27.2% comparable

GROUP REVENUE

Western Europe

33% (+32%)

North America

21% (+23%)

Asia Pacific

27% (+33%)

RoW

11% (+23%)

Japan

8% (+11%)

As a % of revenue and (% comparable growth)

15.2%

19.0%

Group recurring operating income in €m and margin in %

€15,478m

€12,385m

x1.95

13.02.2018 5

- €1,322m

*: at constant scope and exchange rates

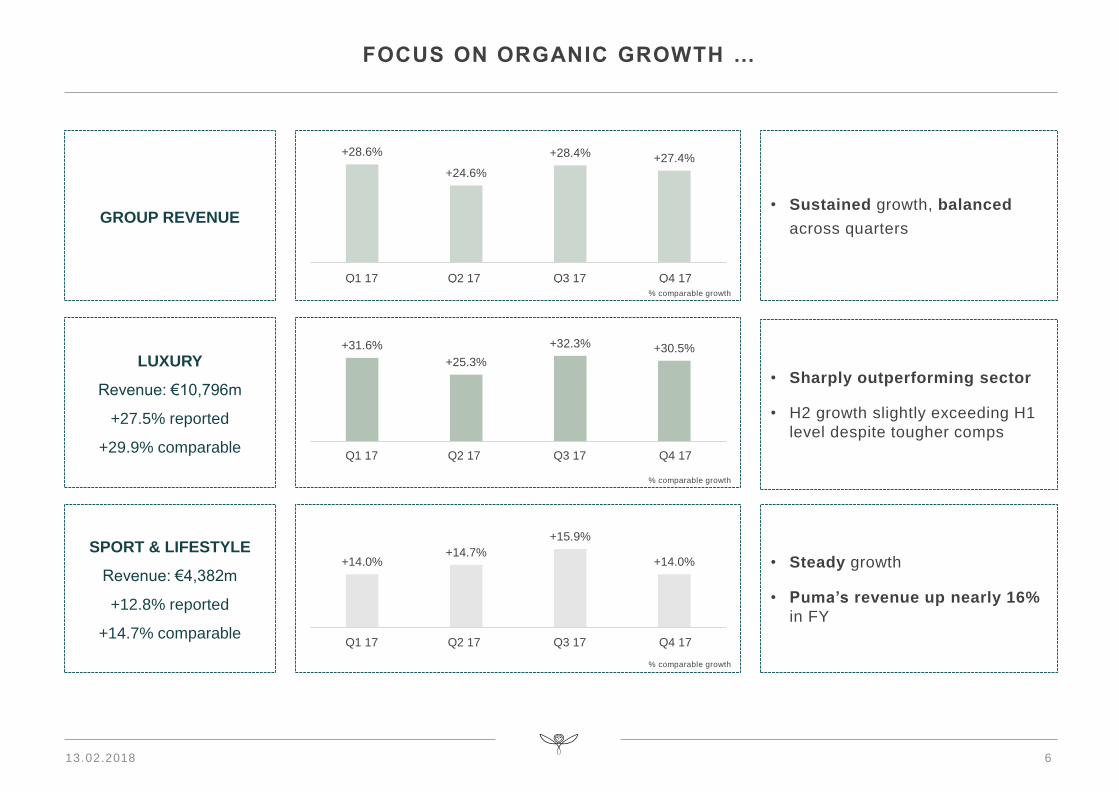

+28.6%

+24.6%

+28.4% +27.4%

T1 17 T2 17 T3 17 T4 17Q1 17 Q2 17 Q3 17 Q4 17

FOCUS ON ORGANIC GROWTH …

% comparable growth

% comparable growth

% comparable growth

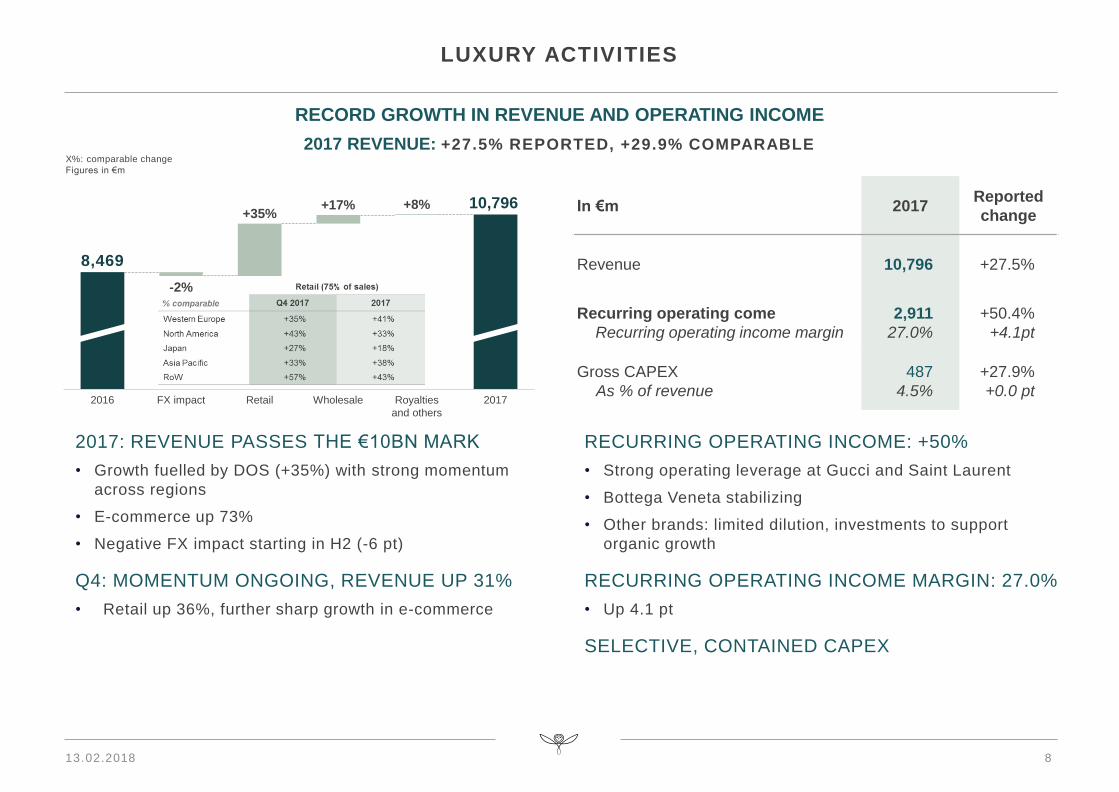

LUXURY

Revenue: €10,796m

+27.5% reported

+29.9% comparable

SPORT & LIFESTYLE

Revenue: €4,382m

+12.8% reported

+14.7% comparable

GROUP REVENUE

• Sharply outperforming sector

• H2 growth slightly exceeding H1

level despite tougher comps

• Steady growth

• Puma’s revenue up nearly 16%

in FY

• Sustained growth, balanced

across quarters

+31.6%

+25.3%

+32.3% +30.5%

T1 17 T2 17 T3 17 T4 17Q1 17 Q2 17 Q3 17 Q4 17

+14.0%+14.7%

+15.9%

+14.0%

T1 17 T2 17 T3 17 T4 17Q1 17 Q2 17 Q3 17 Q4 17

13.02.2018 6

Recurring operating

income

Reported change

(%)

Recurring operating

income margin

(%)

Luxury 2,911 +50.4% 27.0%

Sport & Lifestyle 244 +98.1% 5.6%

Corporate & Ohers (207) -19.7% -

Kering 2,948 +56.3% 19.0%

… AND ON HIGHER RECURRING OPERATING INCOME AND MARGIN

2,948

Luxury2016 Corporate & Others

+975

2017S&L

1,886

-34

+121

RECURRING OPERATING

INCOME BY ACTIVITY

CHANGE IN RECURRING

OPERATING INCOME BY

ACTIVITY

In €m

In €m

13.02.2018 7

Retail

+35%

Wholesale2016 FX impact Royalties

and others

10,796

2017

8,469

-2%

+17% +8%

RECORD GROWTH IN REVENUE AND OPERATING INCOME

8

LUXURY ACTIVITIES

2017: REVENUE PASSES THE €10BN MARK

• Growth fuelled by DOS (+35%) with strong momentum

across regions

• E-commerce up 73%

• Negative FX impact starting in H2 (-6 pt)

Q4: MOMENTUM ONGOING, REVENUE UP 31%

• Retail up 36%, further sharp growth in e-commerce

RECURRING OPERATING INCOME: +50%

• Strong operating leverage at Gucci and Saint Laurent

• Bottega Veneta stabilizing

• Other brands: limited dilution, investments to support

organic growth

RECURRING OPERATING INCOME MARGIN: 27.0%

• Up 4.1 pt

SELECTIVE, CONTAINED CAPEX

2017 REVENUE: +27.5% REPORTED, +29.9% COMPARABLE

In €m 2017Reported

change

Revenue 10,796 +27.5%

Recurring operating come

Recurring operating income margin

2,911

27.0%

+50.4%

+4.1pt

Gross CAPEX

As % of revenue

487

4.5%

+27.9%

+0.0 pt

13.02.2018

X%: comparable change

Figures in €m

9

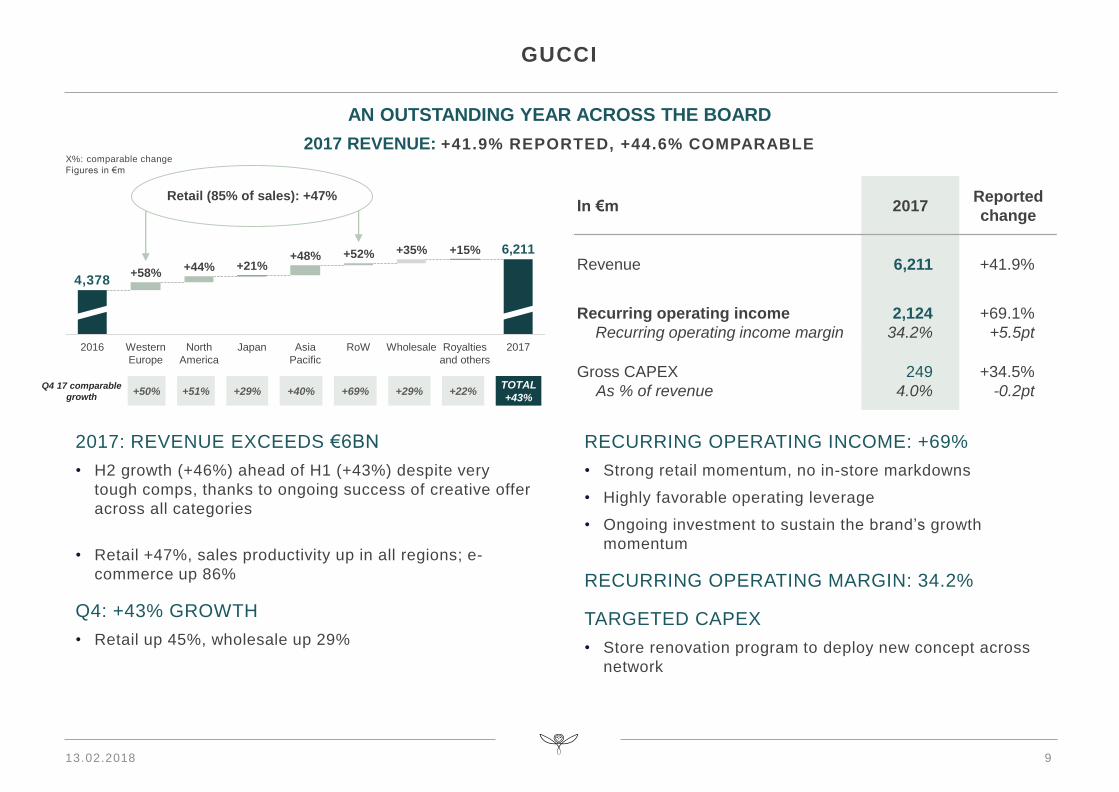

GUCCI

2016 Western

Europe

+58%4,378

North

America

Retail (85% of sales): +47%

2017

+35%

RoW

+52%

Asia

Pacific

6,211

Royalties

and others

+15%

Wholesale

+21%+48%

Japan

+44%

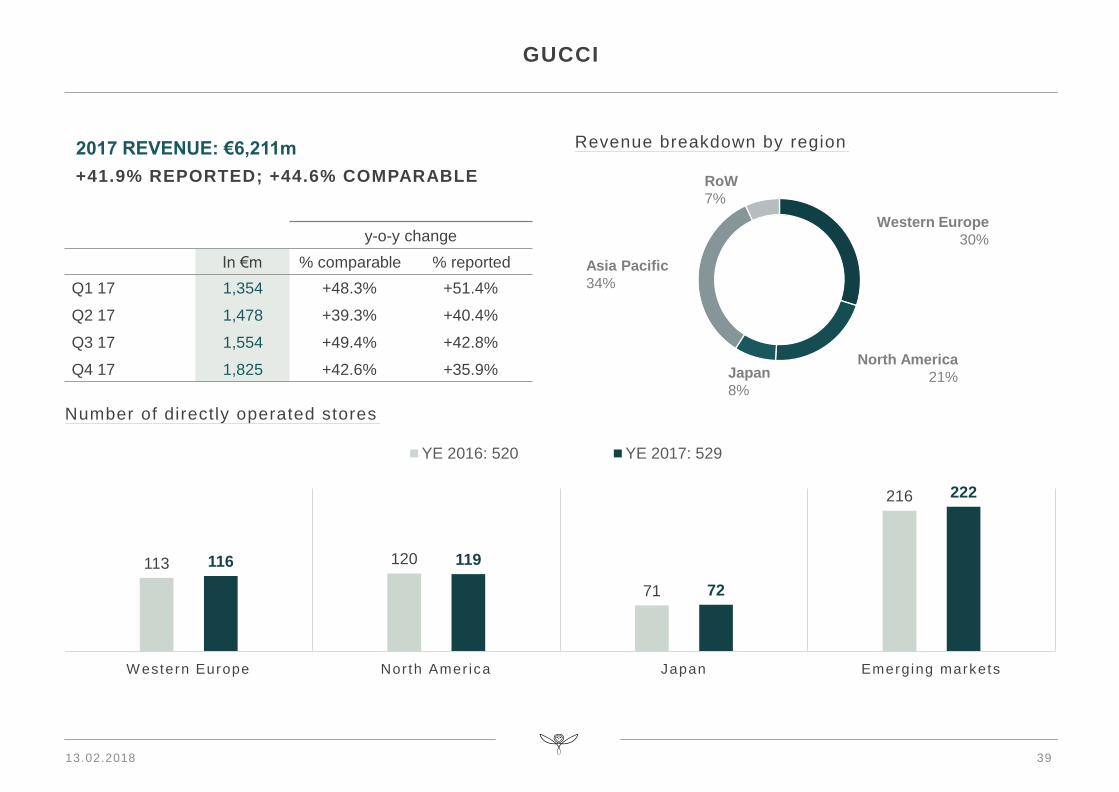

2017: REVENUE EXCEEDS €6BN

• H2 growth (+46%) ahead of H1 (+43%) despite very

tough comps, thanks to ongoing success of creative offer

across all categories

• Retail +47%, sales productivity up in all regions; e-

commerce up 86%

Q4: +43% GROWTH

• Retail up 45%, wholesale up 29%

AN OUTSTANDING YEAR ACROSS THE BOARD

2017 REVENUE: +41.9% REPORTED, +44.6% COMPARABLE

RECURRING OPERATING INCOME: +69%

• Strong retail momentum, no in-store markdowns

• Highly favorable operating leverage

• Ongoing investment to sustain the brand’s growth

momentum

RECURRING OPERATING MARGIN: 34.2%

TARGETED CAPEX

• Store renovation program to deploy new concept across

network

In €m 2017Reported

change

Revenue 6,211 +41.9%

Recurring operating income

Recurring operating income margin

2,124

34.2%

+69.1%

+5.5pt

Gross CAPEX

As % of revenue

249

4.0%

+34.5%

-0.2pt+50%Q4 17 comparable

growth+51% +29% +40% +29%

TOTAL

+43%+69% +22%

13.02.2018

X%: comparable change

Figures in €m

A YEAR OF STABILIZATION

10

BOTTEGA VENETA

Japan

Retail (83% of sales): +4%

North

America

2017

+4%

Wholesale

+19%

Asia

Pacific

Royalties

and others

1,176

-8%

RoW

-4%

+3%1,173

Western

Europe

+7%

2016

-2%

2017 REVENUE: +0.2% REPORTED, +2.4% COMPARABLE

2017: SALES UP SLIGHTLY

• Retail up 4%, solid performance from local customers in

Europe and APAC, marked improvement in the US in Q4

• Higher contribution from full-price sales in stores

• Sustained growth of Shoes and Ready-to-wear, Handbag

sales fueled by success of recent launches and seasonal

variations of iconic lines

Q4 UP 5%: SEQUENTIAL IMPROVEMENT

• Retail up 6%

• Wholesale rationalization nearly completed

RECURRING OPERATING INCOME NEARLY

STABLE

• Negative operating leverage limited thanks to strict cost

control

• Targeted increases in investments, notably communications

RECURRING OPERATING MARGIN MAINTAINED AT

25% LEVEL

CAPEX AIMED AT SUPPORTING FUTURE GROWTH

• Selective openings in prime locations to enhance visibility

(NYC) and renovation of DOS network to improve customer

experience

In €m 2017Reported

change

Revenue 1,176 +0.2%

Recurring operating income

Recurring operating income margin

294

25.0%

-1.1%

-0.3pt

Gross CAPEX

As % of revenue

51

4.3%

+19.2%

+0.7pt

X%: comparable change

Figures in €m

+1%Q4 17 comparable

growth+14% +10% +3% -1%

TOTAL

+5%+24% +2%

13.02.2018

11

SAINT LAURENT

REVENUE HITS €1.5BN MARK, MARGIN AT 25%

2017 REVENUE: +23.0% REPORTED, +25.3% COMPARABLE

2017: CONFIRMS GROWTH TRAJECTORY

• 7th consecutive year of 20%+ growth

• Retail up 27%, double-digit growth in all regions

• Continuing success in all categories boosted by strong

novelties introduced through the year

• Wholesale up 20%

Q4: +23% GROWTH

• Retail and e-commerce showing sustained momentum,

up 27%

• Wholesale posting solid double-digit growth

RECURRING OPERATING INCOME: +40%

• Operating leverage bolstered by critical mass

• Further investments in retail and communications with

omnichannel approach

RECURRING OPERATING INCOME MARGIN

EXCEEDING 25%

CAPEX ACCELERATION

• Consistent with store opening and renovation program

In €m 2017Reported

change

Revenue 1,502 +23.0%

Recurring operating income

Recurring operating income margin

377

25.1%

+40.4%

+3.1pt

Gross CAPEX

As % of revenue

73

4.9%

+26.3%

+0.2pt

Wholesale

+20%

Western

Europe

+27%

2016

1,220

Retail (69% of sales): +27%

2017

1,502

Royalties

and others

+27%

RoW

+16%

Japan Asia

Pacific

+39% +21%+19%

North

America

+18%Q4 17 comparable

growth+31% +30% +33% +14%

TOTAL

+23%+27% +13%

13.02.2018

X%: comparable change

Figures in €m

12

OTHER LUXURY BRANDS

2017: GROWTH GAINING PACE

• Growth speeding up in H2 (+18% vs. +10% in H1)

• Double-digit increase in Couture & Leather Goods (+18%)

driven by Balenciaga

• Solid performance in Jewelry, while Watches return to

growth

Q4: UP 19%

• Balenciaga achieves highest quarterly growth rate of all

Group brands

• Favorable trends intensified in North America, Japan and

APAC

SLIGHT INCREASE IN RECURRING OPERATING

INCOME

• Investments to step up development, notably in Jewelry

• Ongoing transformation at Brioni

• Margin dilution in H1, improvement in H2 thanks to rapid

progress and substantial operating leverage at

Balenciaga

GROWTH OF CAPEX

• Focus on DOS networks at Balenciaga, Alexander

McQueen and Jewelry Houses

A YEAR OF ACCELERATION AND INVESTMENT IN FUTURE

2017 REVENUE: +12.3% REPORTED, +14.1% COMPARABLE

2017

1,907

Royalties

and others

-11%

Wholesale

+7%

Retail

+26%

2016

1,698

In €m 2017Reported

change

Revenue 1,907 +12.3%

Recurring operating income

Recurring operating income margin

116

6.1%

+1.9%

-0.6pt

Gross CAPEX

As % of revenue

114

6.0%

+20.0%

+0.4pt

13.02.2018

X%: comparable change

Figures in €m

13

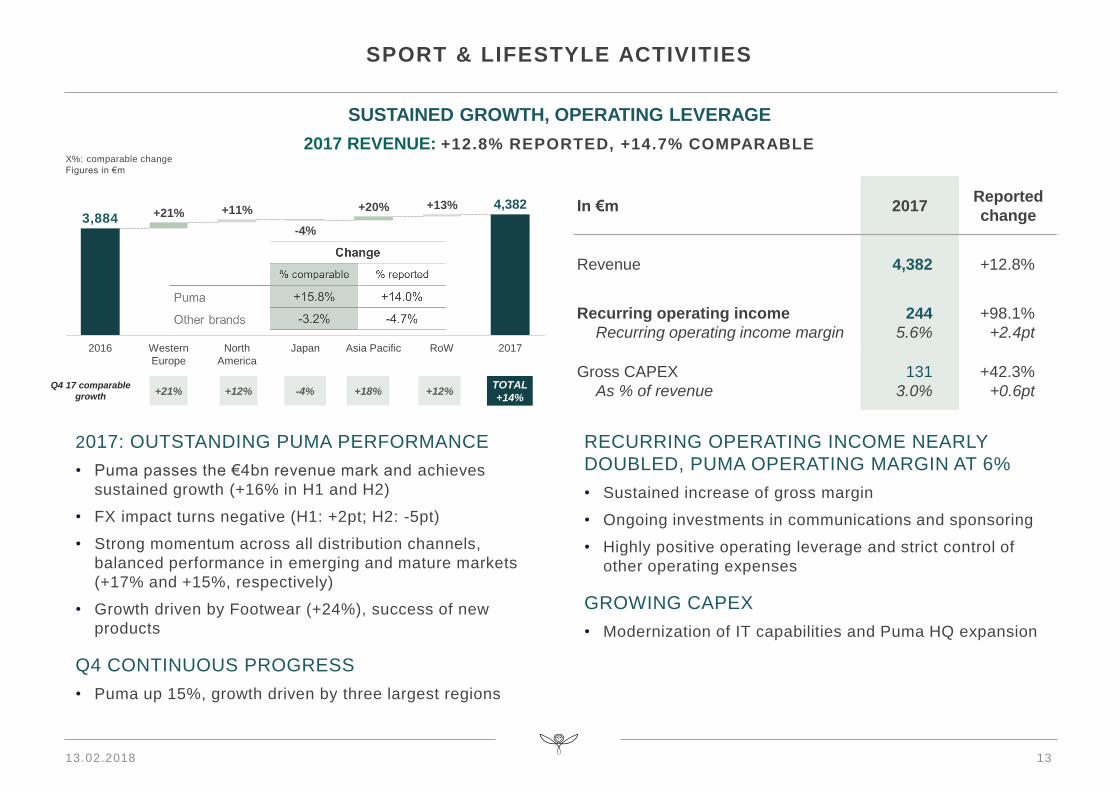

SPORT & LIFESTYLE ACTIVITIES

SUSTAINED GROWTH, OPERATING LEVERAGE

2017 REVENUE: +12.8% REPORTED, +14.7% COMPARABLE

2017: OUTSTANDING PUMA PERFORMANCE

• Puma passes the €4bn revenue mark and achieves

sustained growth (+16% in H1 and H2)

• FX impact turns negative (H1: +2pt; H2: -5pt)

• Strong momentum across all distribution channels,

balanced performance in emerging and mature markets

(+17% and +15%, respectively)

• Growth driven by Footwear (+24%), success of new

products

Q4 CONTINUOUS PROGRESS

• Puma up 15%, growth driven by three largest regions

RECURRING OPERATING INCOME NEARLY

DOUBLED, PUMA OPERATING MARGIN AT 6%

• Sustained increase of gross margin

• Ongoing investments in communications and sponsoring

• Highly positive operating leverage and strict control of

other operating expenses

GROWING CAPEX

• Modernization of IT capabilities and Puma HQ expansion

3,884 +21%

2016

+11%

Western

Europe

North

America

-4%

Japan

+20% +13%

Asia Pacific 2017

4,382

RoW

+21%Q4 17 comparable

growth+12% -4% +18% +12%

TOTAL

+14%

In €m 2017Reported

change

Revenue 4,382 +12.8%

Recurring operating income

Recurring operating income margin

244

5.6%

+98.1%

+2.4pt

Gross CAPEX

As % of revenue

131

3.0%

+42.3%

+0.6pt

13.02.2018

X%: comparable change

Figures in €m

14

FINANCIAL PERFORMANCE

In €m 2017 2016

Revenue 15,478 12,385

Gross margin 10,133 7,790

Recurring operating income 2,948 1,886

Other non-financial operating income and expenses

Net financial charges

Corporate income tax

Share in earnings of associates

Net result from discontinued operations

(242)

(243)

(591)

(2)

(5)

(506)

(202)

(296)

(2)

(12)

Consolidated net income

Of which net income, Group share

1,865

1,786

868

814

Net income, Group share, from continuing opeations excluding non-recurring

items2,002 1,282

Net income, Group share, per share (in euro)

Net income per share from continuing operations, excluding non-recurring items (in

euro)

14.17

15.89

6.46

10.17

13.02.2018

15

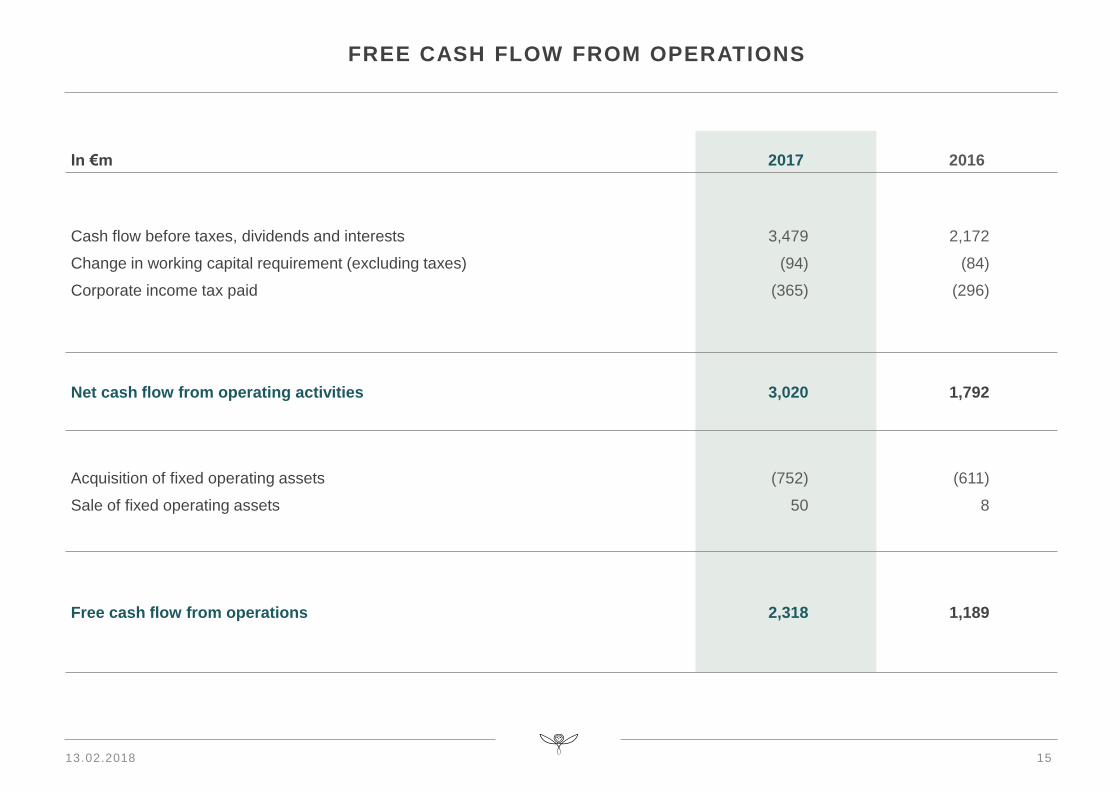

FREE CASH FLOW FROM OPERATIONS

In €m 2017 2016

Cash flow before taxes, dividends and interests

Change in working capital requirement (excluding taxes)

Corporate income tax paid

3,479

(94)

(365)

2,172

(84)

(296)

Net cash flow from operating activities 3,020 1,792

Acquisition of fixed operating assets

Sale of fixed operating assets

(752)

50

(611)

8

Free cash flow from operations 2,318 1,189

13.02.2018

16

NET FINANCIAL DEBT

184616

196

Purchase of Kering

shares, financial

investments and other

-2,318

3,049

Free cash flow

from operations

0.9x

Net debt at

December 31, 2017

4,371

Net debt at

December 31, 2016

Net interest paid and

dividends received

Dividends paid

1.9x

2016-2017 CHANGE

IN €M AND NET DEBT / EBITDA RATIO

13.02.2018

17

DIVIDEND PER SHARE (excluding distribution in kind of Puma shares)

(In €)

DIVIDEND UP 30%

3.75 3.754.00 4.00

4.60

6.00

2012 2013 2014 2015 2016 2017*

DIVIDEND PAYOUT

(In %)

37.3% 38.4% 42.9%49.6% 45.3%

37.8%

61.6% 64.0% 59.4%

102.2%

57.1%

35.6%

2012** 2013** 2014 2015 2016 2017*

en % du RNPdG poursuivi courant en % du cash flow disponiblein % of available cash flow

+30%

in % of recurring net income, Group share

13.02.2018 ** Reported not restated* Subject to April 26, 2018 AGM approval. Interim payment of

€2.00 paid on January 17, 2018

A LUXURY PURE PLAYER

JEAN-FRANÇOIS PALUS

GROUP MANAGING DIRECTOR

All information in this section is subject to approval of the dividend in kind by Kering shareholders

at the Annual General Meeting of April 26, 2018

GRADUALLY REFOCUSING ON LUXURY

13.02.2018

2008 2017

A European Group of retail companies A global Luxury Group with iconic brands

Luxury (71%)

By

ac

tiv

ity

By

re

gio

n

Redcats (18%)

Fnac (23%)

Cfao (14%)

Sport & Lifestyle (29%)

Other countries (11%)

Western Europe (33%)

Asia Pacific (35%)

North America (21%)

Re

ve

nu

e b

re

ak

do

wn

*

Conforama (16%)

Puma (12%)

Asia (9%)

Luxury (17%)

19*: Excluding corporate and others

Americas (14%)

France (39%)

Europe excluding

France (25%)

Oceania (1%)

Africa (12%)

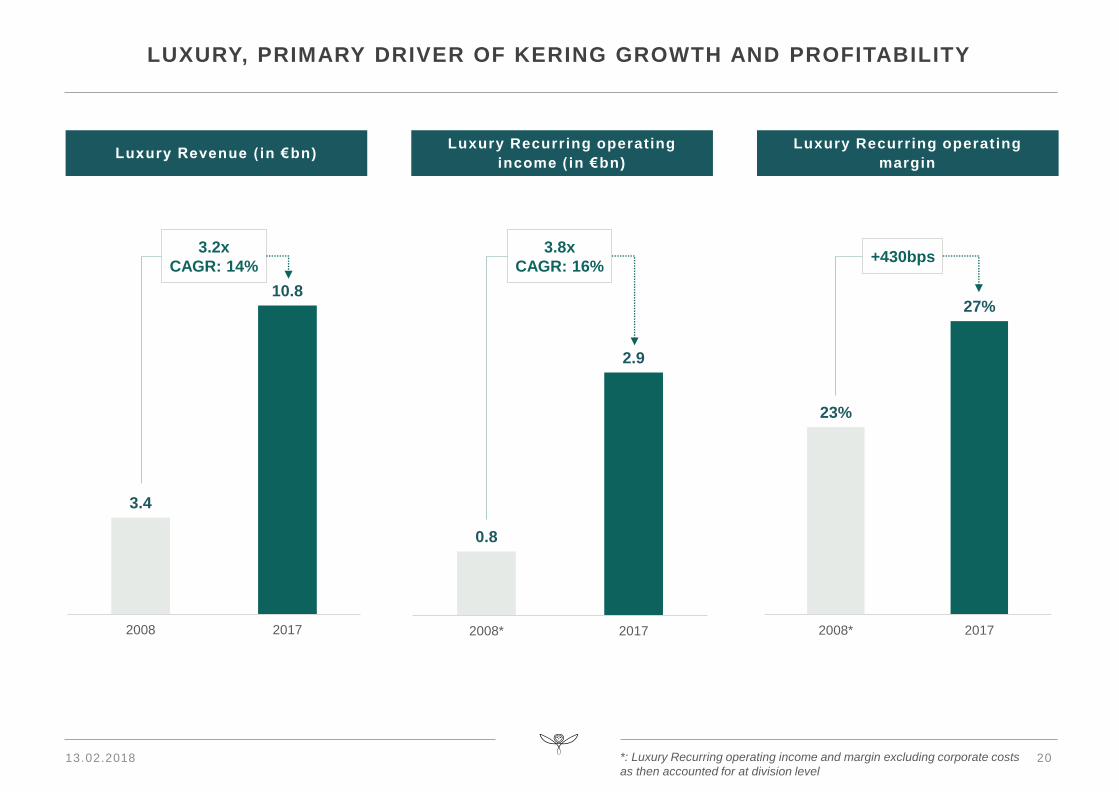

LUXURY, PRIMARY DRIVER OF KERING GROWTH AND PROFITABILITY

13.02.2018

Luxury Revenue ( in €bn)Luxury Recurring operating

income (in €bn)

Luxury Recurring operating

margin

3.4

10.8

2008 2017

0.8

2.9

2008* 2017

23%

27%

2008* 2017

3.2x

CAGR: 14%

3.8x

CAGR: 16%+430bps

20*: Luxury Recurring operating income and margin excluding corporate costs

as then accounted for at division level

A BALANCED ENSEMBLE OF COMPLEMENTARY BRANDS

Consistent posit ioning across al l Luxury segments An ensemble of brands at different stages of maturity

Product mix by brand (% of revenue)

13.02.2018 212017 data. Bubble size is representative of each brand’s revenue.

Retail including e-commerce

*: Other product categories & royalties

Leath

er

Go

od

s

Read

y-t

o-w

ear

Sh

oes

Watc

hes

Jew

elr

y

Oth

ers

*

Gucci

Bottega Veneta

Saint Laurent

Others - Soft

Luxury

Others - Hard

Luxury

Luxury 52% 16% 17% 3% 4% 8%

13.02.2018

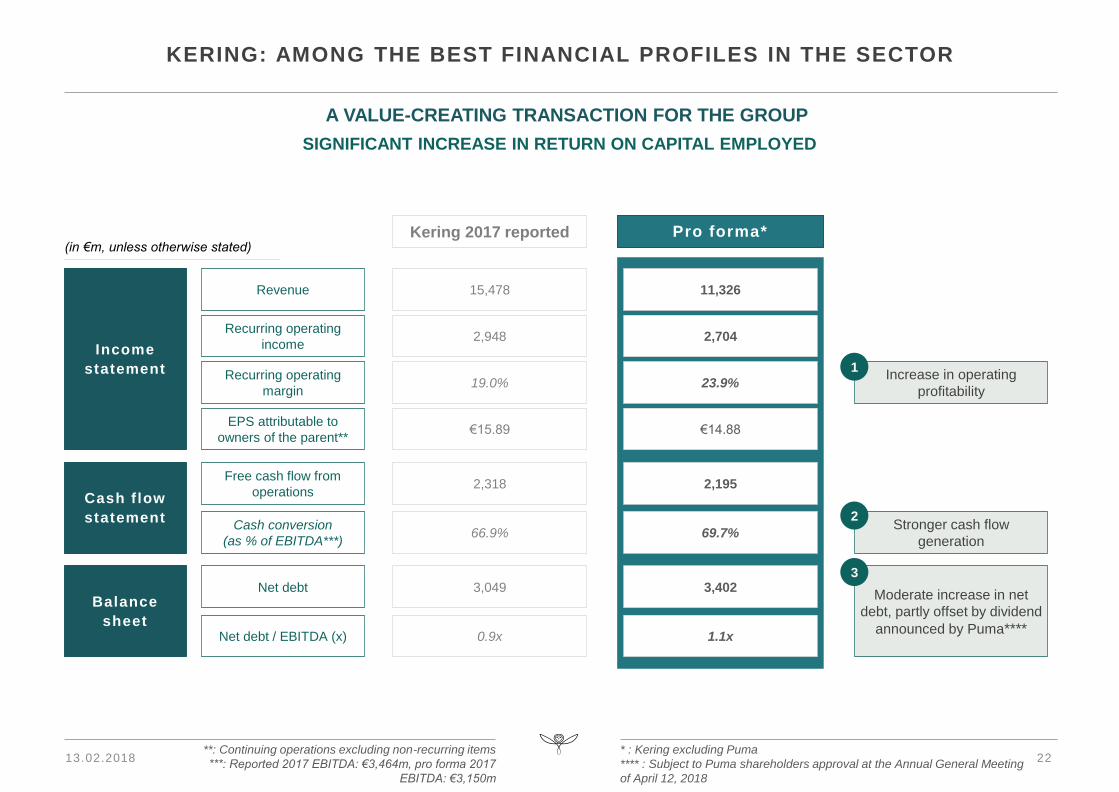

KERING: AMONG THE BEST FINANCIAL PROFILES IN THE SECTOR

Income

statement

Cash f low

statement

Revenue 15,478

Recurring operating

margin19.0%

Cash conversion

(as % of EBITDA***)

(in €m, unless otherwise stated)

66.9%

Balance

sheetNet debt / EBITDA (x) 0.9x

11,326

23.9%

69.7%

1.1x

Kering 2017 reported Pro forma*

Increase in operating

profitability

Stronger cash flow

generation

Recurring operating

income2,948 2,704

Free cash flow from

operations2,318 2,195

EPS attributable to

owners of the parent**€15.89 €14.88

Net debt 3,049 3,402Moderate increase in net

debt, partly offset by dividend

announced by Puma****

A VALUE-CREATING TRANSACTION FOR THE GROUP

1

2

22

3

* : Kering excluding Puma

**** : Subject to Puma shareholders approval at the Annual General Meeting

of April 12, 2018

**: Continuing operations excluding non-recurring items

***: Reported 2017 EBITDA: €3,464m, pro forma 2017

EBITDA: €3,150m

SIGNIFICANT INCREASE IN RETURN ON CAPITAL EMPLOYED

x3.9

63

245

2013 2017

23

INITIAL SUCCESS OF PUMA FOREVER FASTER PLAN AND RETURN TO PROFITABLE GROWTH

Operating income Market capitalization

• Gradual improvement in operating

margin

• More innovative, differentiating

products: improved gross margin

through better sell-through and

improved sourcing

• Activated operating leverage

13.02.2018

Revenue

• Gradual acceleration of revenue

growth

• Renewed, repositioned product offer

• Sustained, consistent growth

• Increased visibility, partnerships &

sponsorships

• Value creation

• +54.5% share performance since

12/31/2013 (from €235 to €363*)

As reported by Puma SE, in €m

%

margin

+39%

2.1% 5.9%in €bn

3.5

5.5

2013 2017

+€2.0bn

2,985

4,136

2013 2017

*: Share price as of 31/12/2017

24

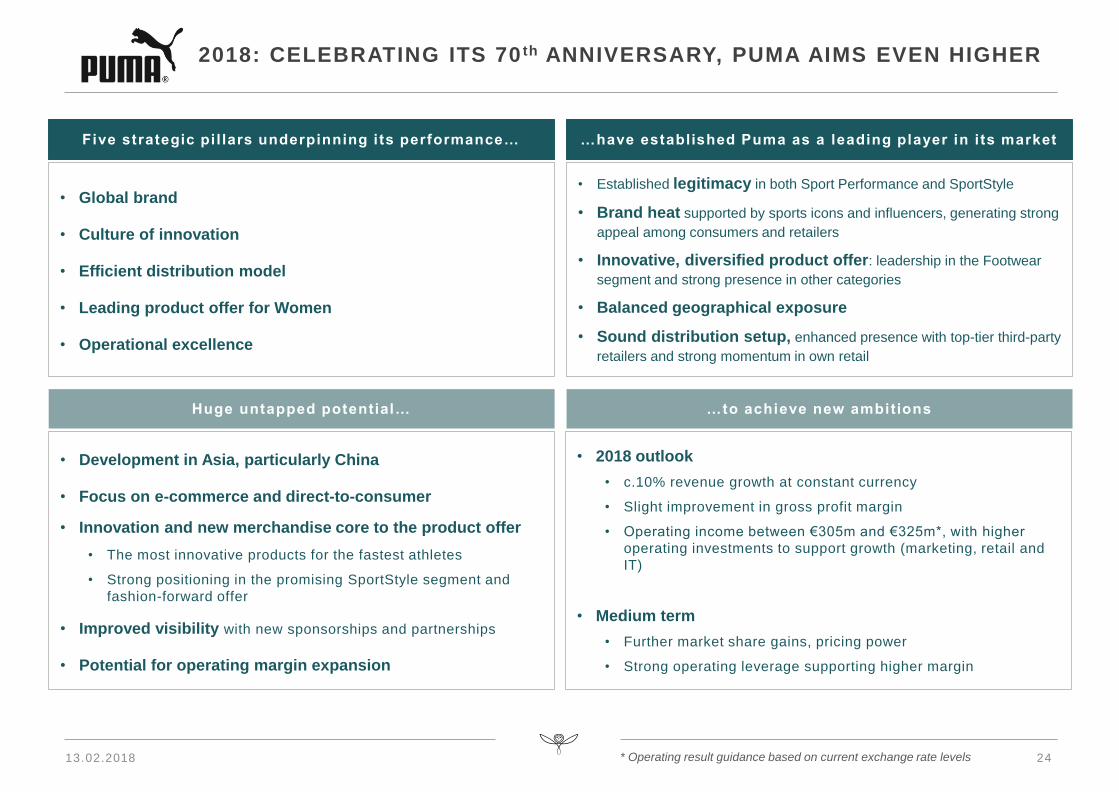

2018: CELEBRATING ITS 70 th ANNIVERSARY, PUMA AIMS EVEN HIGHER

13.02.2018

Five strategic pi l lars underpinning its performance…

• Global brand

• Culture of innovation

• Efficient distribution model

• Leading product offer for Women

• Operational excellence

…have established Puma as a leading player in i ts market

• Established legitimacy in both Sport Performance and SportStyle

• Brand heat supported by sports icons and influencers, generating strong

appeal among consumers and retailers

• Innovative, diversified product offer: leadership in the Footwear

segment and strong presence in other categories

• Balanced geographical exposure

• Sound distribution setup, enhanced presence with top-tier third-party

retailers and strong momentum in own retail

Huge untapped potential…

• Development in Asia, particularly China

• Focus on e-commerce and direct-to-consumer

• Innovation and new merchandise core to the product offer

• The most innovative products for the fastest athletes

• Strong positioning in the promising SportStyle segment and

fashion-forward offer

• Improved visibility with new sponsorships and partnerships

• Potential for operating margin expansion

…to achieve new ambitions

• 2018 outlook

• c.10% revenue growth at constant currency

• Slight improvement in gross profit margin

• Operating income between €305m and €325m*, with higher

operating investments to support growth (marketing, retail and

IT)

• Medium term

• Further market share gains, pricing power

• Strong operating leverage supporting higher margin

* Operating result guidance based on current exchange rate levels

13.02.2018

TECHNICAL ASPECTS OF THE DISTRIBUTION

Distribution

ratio

Kering shareholders will receive 1 Puma share for 12 Kering shares held

• Shareholders owning a number of Kering shares lower than 12 or which does not correspond to

a multiple of 12 will receive the number of Puma shares immediately below, together with a

cash payment for the balance

New corporate governance with Supervisory Board and Executive BoardPuma

governance

• Kering: 6-month period following the distribution

• Artemis: 12-month period following the distribution

Lock-up

commitments

Puma

shareholding

Float

14%

Kering

86%

Float

55%

Kering

16%

Artemis

29%

Post-DistributionPre-Distribution

25

13.02.2018

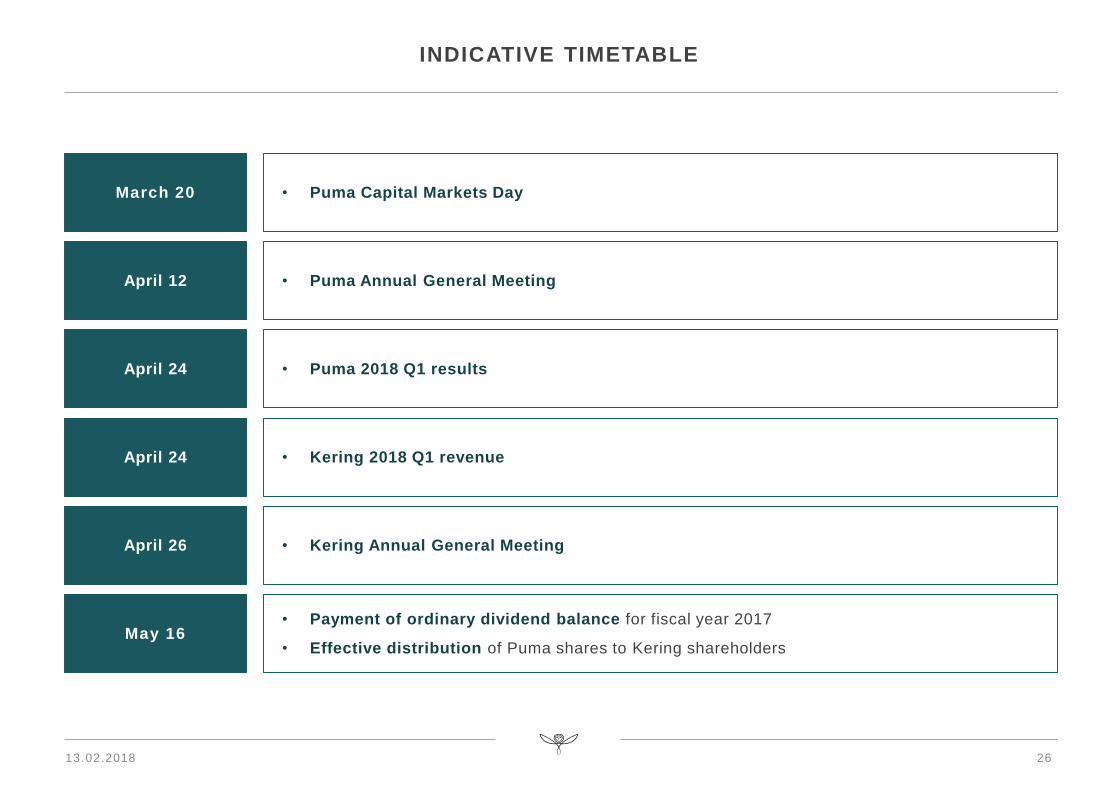

INDICATIVE TIMETABLE

26

May 16• Payment of ordinary dividend balance for fiscal year 2017

• Effective distribution of Puma shares to Kering shareholders

April 24 • Kering 2018 Q1 revenue

April 26 • Kering Annual General Meeting

April 24 • Puma 2018 Q1 results

March 20 • Puma Capital Markets Day

April 12 • Puma Annual General Meeting

13.02.2018

A VALUE-CREATING TRANSACTION

• Raising Kering’s status as a leading Luxury pure player

— Among the best financial profiles in the sector, with higher profitability, strong cash flow

generation and solid financial position

— Ambition to continue growing and developing its powerful ensemble of Luxury Houses

• Exposure to Puma value-creation potential, as a significant minority shareholder in Puma, with a

c.16% stake

• Strategy and execution carried out without disruption

• Increased autonomy for a talented, passionate management team

• Change in governance structure reflecting new shareholder base

• Opportunity to become shareholders in one of the world’s most iconic global Sports brands

• Direct benefit from Puma value-creation potential further enhanced by increased free float and

stock market visibility

• Option to keep or monetize Puma shares

27

For Puma

For Kering

For Kering

shareholders

For Puma

shareholders

• Significant improvement in stock market status thanks to the increase in free float (55% of

share capital post distribution)

• €12.50 dividend per share for the 2017 fiscal year *

*: Subject to Puma shareholders approval at Annual General Meeting

of April 12, 2018

NEW PROFILE: STRATEGY AND AMBITIONS

FRANÇOIS-HENRI PINAULT

CHAIRMAN AND CEO

29

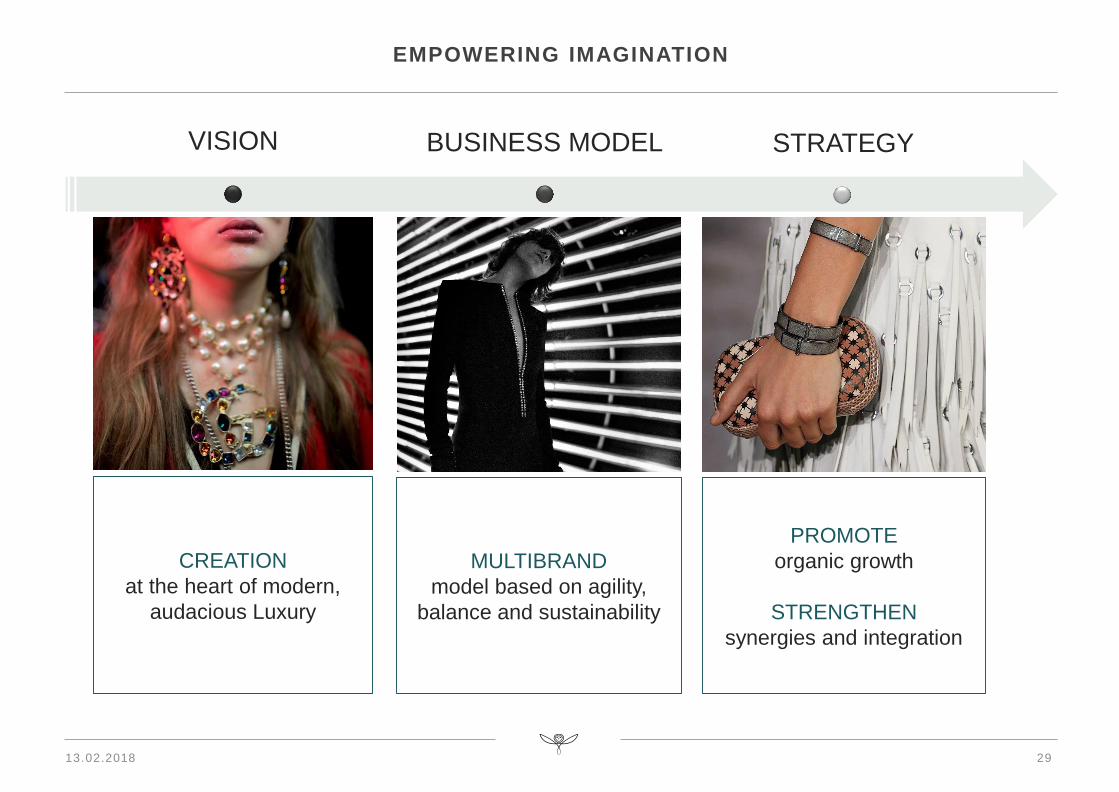

EMPOWERING IMAGINATION

VISION BUSINESS MODEL STRATEGY

CREATION

at the heart of modern,

audacious Luxury

PROMOTE

organic growth

STRENGTHEN

synergies and integration

MULTIBRAND

model based on agility,

balance and sustainability

13.02.2018

CREATIVITY

30

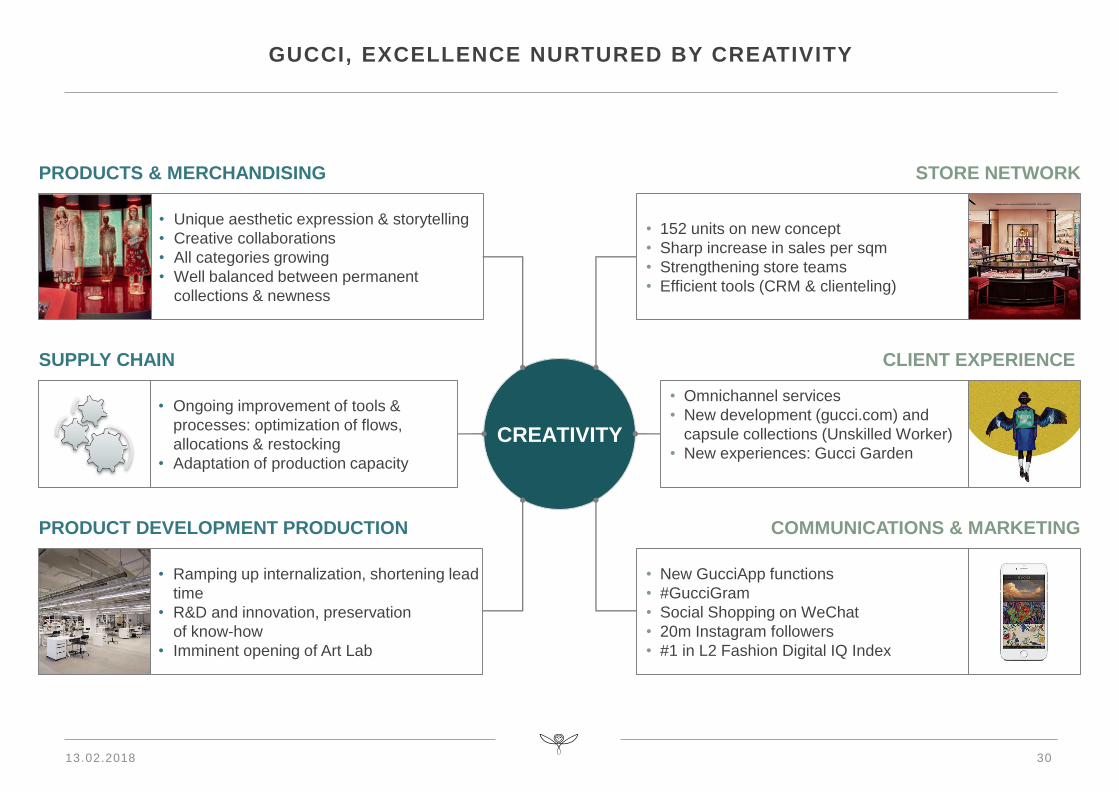

GUCCI, EXCELLENCE NURTURED BY CREATIVITY

STORE NETWORK

CLIENT EXPERIENCE

• 152 units on new concept

• Sharp increase in sales per sqm

• Strengthening store teams

• Efficient tools (CRM & clienteling)

• Omnichannel services

• New development (gucci.com) and

capsule collections (Unskilled Worker)

• New experiences: Gucci Garden

• New GucciApp functions

• #GucciGram

• Social Shopping on WeChat

• 20m Instagram followers

• #1 in L2 Fashion Digital IQ Index

COMMUNICATIONS & MARKETING

PRODUCTS & MERCHANDISING

SUPPLY CHAIN

PRODUCT DEVELOPMENT PRODUCTION

• Ongoing improvement of tools &

processes: optimization of flows,

allocations & restocking

• Adaptation of production capacity

• Ramping up internalization, shortening lead

time

• R&D and innovation, preservation

of know-how

• Imminent opening of Art Lab

• Unique aesthetic expression & storytelling

• Creative collaborations

• All categories growing

• Well balanced between permanent

collections & newness

13.02.2018

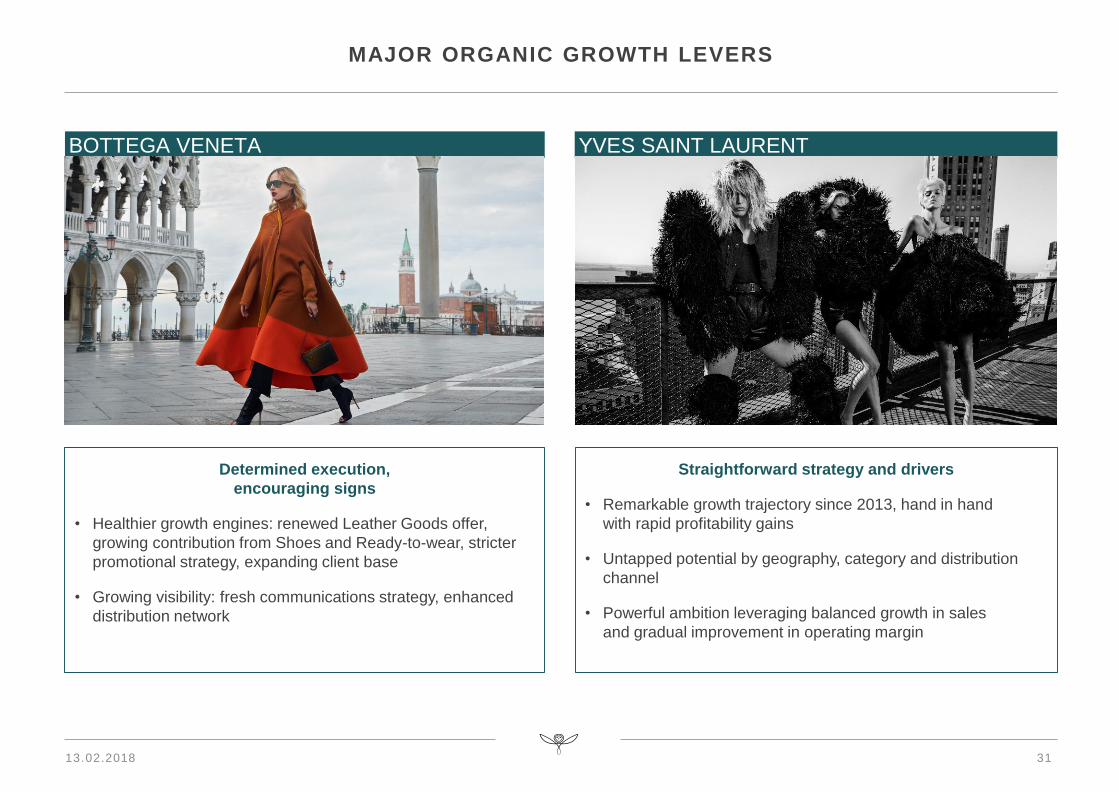

MAJOR ORGANIC GROWTH LEVERS

31

BOTTEGA VENETA YVES SAINT LAURENT

Determined execution,

encouraging signs

• Healthier growth engines: renewed Leather Goods offer,

growing contribution from Shoes and Ready-to-wear, stricter

promotional strategy, expanding client base

• Growing visibility: fresh communications strategy, enhanced

distribution network

Straightforward strategy and drivers

• Remarkable growth trajectory since 2013, hand in hand

with rapid profitability gains

• Untapped potential by geography, category and distribution

channel

• Powerful ambition leveraging balanced growth in sales

and gradual improvement in operating margin

13.02.2018

32

MAJOR ORGANIC GROWTH LEVERS

Successful creative renewal

• Fastest H2 growth of all Group brands, driven by Ready-to-wear and Shoes

• Considerable potential from Leather Goods

• Targeted openings: new flagships

• €1bn sales potential in medium term

Ambitious 3-year investment plan

• Increase visibility and scale of House

• Extension and renovation of store network, including historic Place Vendôme mansion

• Investments aimed at broadening offer and collections

• Major communications initiatives, notably around House’s 160th birthday

Multiple strengths, promising momentum

• Powerful creative content, artisanal skills, legitimacy in Men’s and Women’s, entering new product categories, considerable untapped potential

• Strengthening product offer: structuring sub-segments and introducing new items

• New organization, extension/relocation of DOS network, investments in brand notoriety

BALENCIAGA

ALEXANDER McQUEEN

BOUCHERON

13.02.2018

33

PERFORMANCE ACCELERATORS

AT THE HEART OF

BRAND STRATEGY

Audacity, creativity

Operational execution

Communications

Sharing of

resourcesSupply chain

Cross-brand expertise, innovation and digital

Talent excellence and best practices

INTEGRATED MODEL

SY

NE

RG

IES

SY

NE

RG

IES

INTEGRATED MODEL

13.02.2018

34

VALUE CREATION AND FINANCIAL AMBITIONS

REVENUE

RETURN

FINANCIAL

STRUCTURE

WCR

CAPEX • Enhanced Capex allocation

OPERATIONS

CAPITAL

EMPLOYED

USE

OF CASH

• Focus on same-store organic growth

LOWER NET

DEBT/EBITDA RATIO (vs. pro forma ratio)

• Higher store productivity

• Ongoing adaptation of organizations

• Net debt cost/maturity

• Dividend a priority

• Planning and inventory management

IMPROVED

RETURN ON

CAPITAL

EMPLOYED

SUSTAINED

GENERATION

OF FCF FROM

OPERATIONS

13.02.2018

Q&A

Appendix

37

2017 REVENUE

Reported change

In €m 2017 2016 €m %

Gucci

Bottega Veneta

Saint Laurent

Other brands

6,211.2

1,176.3

1,501.4

1,906.9

4,378.3

1,173.4

1,220.2

1,697.5

1,832.9

2.9

281.2

209.4

+41.9%

+0.2%

+23.0%

+12.3%

Luxury 10,795.8 8,469.4 2,326.4 +27.5%

Puma

Other brands

4,151.7

230.2

3,642.2

241.5

509.5

(11.3)

+14.0%

-4.7%

Sport & Lifestyle 4,381.9 3,883.7 498.2 +12.8%

Corporate & Others 300.0 31.8 268.2 -

Kering 15,477.7 12,384.9 3,092.8 +25.0%

13.02.2018

y-o-y change

In €m % comparable % reported

Q1 17

Q2 17

Q3 17

Q4 17

2,417

2,614

2,678

3,087

+31.6%

+25.3%

+32.3%

+30.5%

+34.0%

+26.0%

+26.6%

+24.6%

38

2017 REVENUE: €10,796m

+27.5% REPORTED; +29.9% COMPARABLE

LUXURY ACTIVITIES

Western Europe

34%

North America

19%Japan

9%

Asia Pacific

31%

RoW

7%

Number of directly operated stores

338

213248

506

367

219260

542

W estern Europe Nor th Amer ica Japan Emerging markets

YE 2016: 1,305 YE 2017: 1,388

Revenue breakdown by region

13.02.2018

y-o-y change

In €m % comparable % reported

Q1 17

Q2 17

Q3 17

Q4 17

1,354

1,478

1,554

1,825

+48.3%

+39.3%

+49.4%

+42.6%

+51.4%

+40.4%

+42.8%

+35.9%

39

2017 REVENUE: €6,211m

+41.9% REPORTED; +44.6% COMPARABLE

GUCCI

Western Europe

30%

North America

21%Japan

8%

Asia Pacific

34%

RoW

7%

Number of directly operated stores

113 120

71

216

116 119

72

222

W estern Europe Nor th Amer ica Japan Emerging markets

YE 2016: 520 YE 2017: 529

Revenue breakdown by region

13.02.2018

y-o-y change

In €m % comparable % reported

Q1 17

Q2 17

Q3 17

Q4 17

280

310

281

305

+2.3%

+1.7%

+0.9%

+4.7%

+4.7%

+2.2%

-4.5%

-1.0%

40

2017 REVENUE: €1,176m

+0.2% REPORTED; +2.4% COMPARABLE

BOTTEGA VENETA

Western Europe

28%

North America

11%

Japan

15%

Asia Pacific

40%

RoW

6%

Number of directly operated stores

56

30

58

111

61

30

59

120

W estern Europe Nor th Amer ica Japan Emerging markets

YE 2016: 255 YE 2017: 270

Revenue breakdown by region

13.02.2018

y-o-y change

In €m % comparable % reported

Q1 17

Q2 17

Q3 17

Q4 17

364

346

384

407

+33.4%

+23.7%

+22.2%

+22.9%

+35.4%

+24.3%

+17.7%

+17.5%

41

2017 REVENUE: €1,502m

+23.0% REPORTED; +25.3% COMPARABLE

SAINT LAURENT

Western Europe

37%

North America

22%

Japan

8%

Asia Pacific

26%

RoW

7%

Number of directly operated stores

37

25 27

70

47

29 30

78

W estern Europe Nor th Amer ica Japan Emerging markets

YE 2016: 159 YE 2017: 184

Revenue breakdown by region

13.02.2018

y-o-y change

In €m % comparable % reported

Q1 17

Q2 17

Q3 17

Q4 17

418

479

460

550

+11.1%

+9.1%

+17.0%

+18.8%

+12.3%

+9.2%

+13.0%

+14.7%

42

2017 REVENUE: €1,907m

+12.3% REPORTED; +14.1% COMPARABLE

OTHER LUXURY BRANDS

Western Europe

46%

North America

16%

Japan

10%

Asia Pacific

19%

RoW

9%

Number of directly operated stores

132

38

92109

143

41

99

122

W estern Europe Nor th Amer ica Japan Emerging markets

YE 2016: 371 YE 2017: 405

Revenue breakdown by region

13.02.2018

y-o-y change

In €m % comparable % reported

Q1 17

Q2 17

Q3 17

Q4 17

1,064

1,022

1,191

1,104

+14.0%

+14.7%

+15.9%

+14.0%

+16.5%

+15.7%

+11.9%

+8.0%

43

2017 REVENUE: €4,382m

+12.8% REPORTED; +14.7% COMPARABLE

SPORT & LIFESTYLE ACTIVITIES

Western Europe

30%

North America

27%

Japan

7%

Asia Pacific

17%

RoW

19%

Revenue breakdown by region

Number of directly operated stores

103142

35

454

120 131

41

497

W estern Europe Nor th Amer ica Japan Emerging markets

YE 2016: 734 YE 2017: 789

13.02.2018

44

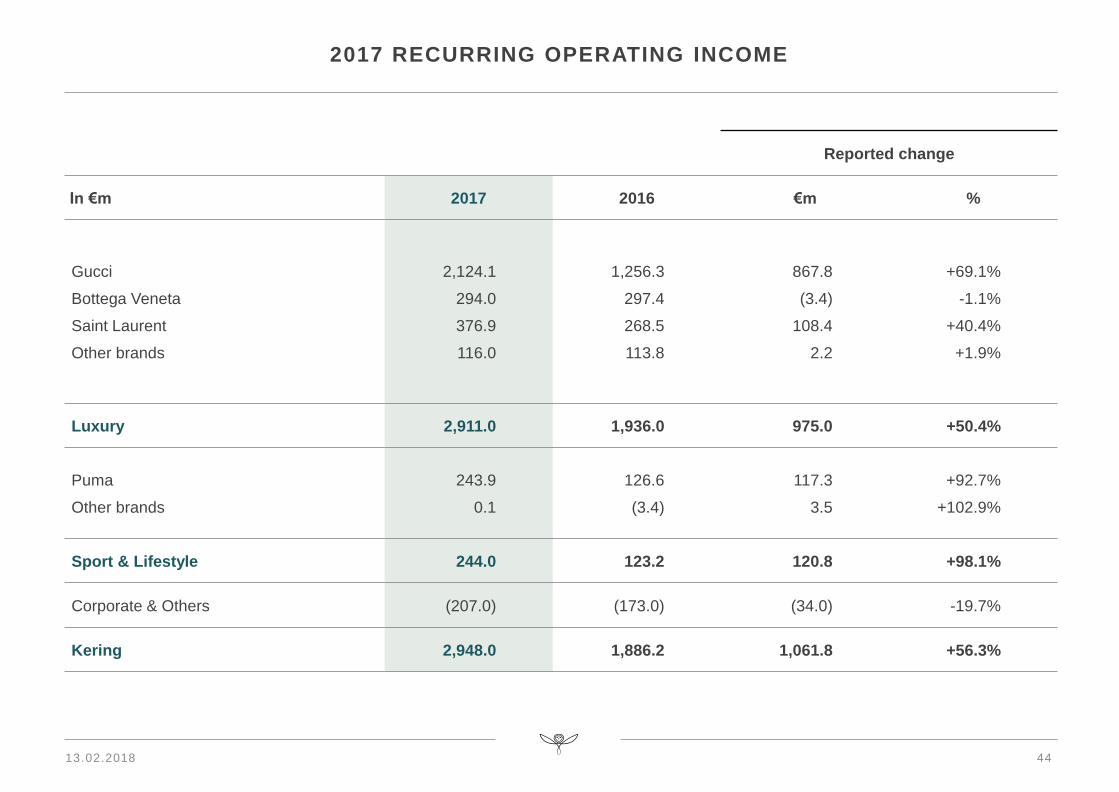

2017 RECURRING OPERATING INCOME

Reported change

In €m 2017 2016 €m %

Gucci

Bottega Veneta

Saint Laurent

Other brands

2,124.1

294.0

376.9

116.0

1,256.3

297.4

268.5

113.8

867.8

(3.4)

108.4

2.2

+69.1%

-1.1%

+40.4%

+1.9%

Luxury 2,911.0 1,936.0 975.0 +50.4%

Puma

Other brands

243.9

0.1

126.6

(3.4)

117.3

3.5

+92.7%

+102.9%

Sport & Lifestyle 244.0 123.2 120.8 +98.1%

Corporate & Others (207.0) (173.0) (34.0) -19.7%

Kering 2,948.0 1,886.2 1,061.8 +56.3%

13.02.2018

45

2017 EBITDA

Reported change

In €m 2017 2016 €m %

Gucci

Bottega Veneta

Saint Laurent

Other brands

2,331.0

337.3

422.1

184.9

1,424.5

341.7

312.2

177.0

906.5

(4.4)

109.9

7.9

+63.6%

-1.3%

+35.2%

+4.5%

Luxury 3,275.3 2,255.4 1,019.9 +45.2%

Puma

Other brands

314.4

6.0

187.2

2.8

127.2

3.2

+67.9%

+114.3%

Sport & Lifestyle 320.4 190.0 130.4 +68.6%

Corporate & Others (131.3) (127.2) (4.1) -3.2%

Kering 3,464.4 2,318.2 1,146.2 +49.4%

13.02.2018

46

2017 NET FINANCIAL COSTS AND INCOME TAX

In €m2017 2016

Cost of net debt

Other financial income and expenses

(128)

(115)

(128)

(74)

Financial costs (net) (243) (202)

In €m2017 2016

Tax on recurring income

Tax on non-recurring items

(622)

31

(345)

49

Total tax charge (591) (296)

Effective tax rate 24.0% 25.1%

Recurring tax rate 23.0% 20.5%

13.02.2018

5,185

2,137

4,823

5,180

2,943

18,260

12,626

Actif Passif

2017 BALANCE SHEETHEALTHY FINANCIAL STRUCTURE

-1,197

609

769 700

540

1,628

2018* 2019** 2020** 2021** 2022** beyond**

Total

€25,577m

• Equity: 49% of total balance sheet

• Debt-to-equity ratio: 24.1%

• Secured financing over the long term

• Optimization of debt cost/maturity

Current

assets

Non-

current

assets

Cash

Equity

Gross debt

CONDENSED BALANCE SHEET (In €m) LIQUIDITY OVERVIEW

NET FINANCIAL DEBT (In €m)

Non-current

liabilities

Current

liabilities

Assets L iab i l i t ies

13.02.2018 47* Gross debt minus cash & cash equivalents

** Gross debt

48

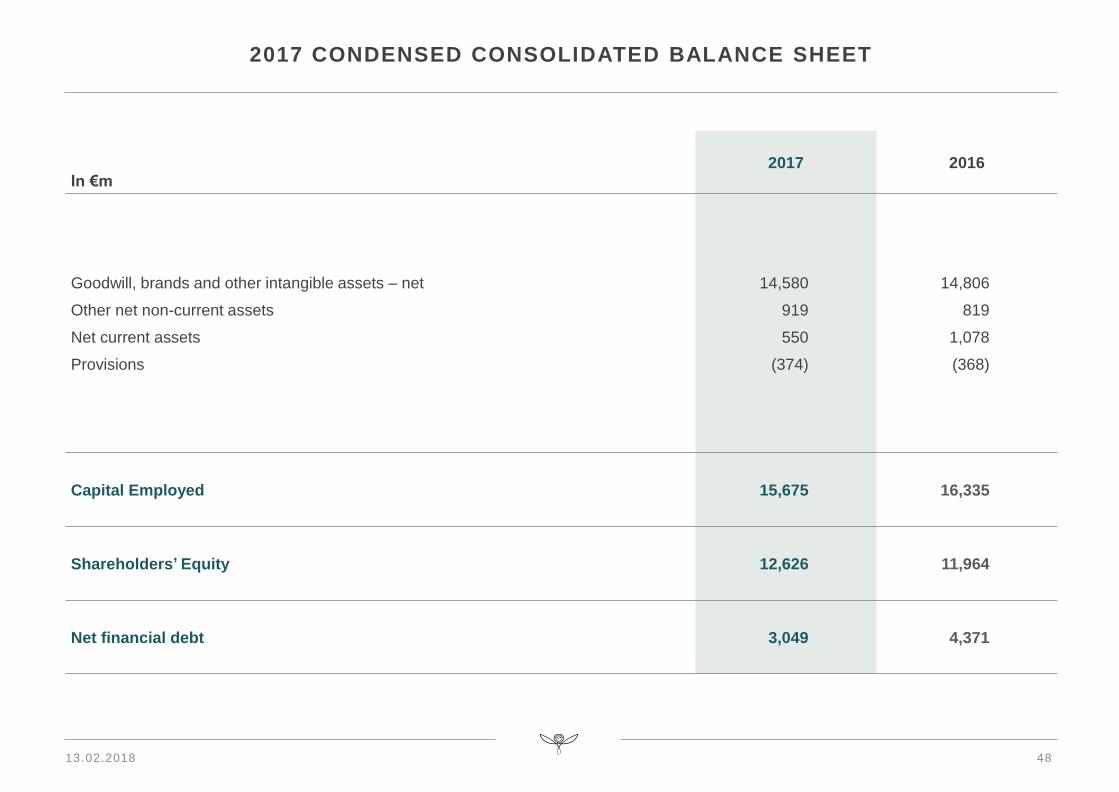

2017 CONDENSED CONSOLIDATED BALANCE SHEET

In €m2017 2016

Goodwill, brands and other intangible assets – net

Other net non-current assets

Net current assets

Provisions

14,580

919

550

(374)

14,806

819

1,078

(368)

Capital Employed 15,675 16,335

Shareholders’ Equity 12,626 11,964

Net financial debt 3,049 4,371

13.02.2018

13.02.2018

OTHER IMPACTS LINKED TO THE DISTRIBUTION*

Main impacts on

2018 financial

statements

• A capital gain or loss net of current and deferred taxes will be booked in Kering consolidated financial statements at June 30, 2018 under “Net income from discontinued operations”

• In case of capital gain, it would be subject to taxes on long-term capital gains

• No restructuring cost linked to the operation

Accounting

method in 2018

financial

statements

• Contribution of Puma until share distribution as well as capital gain or loss recorded under

“Profit (loss) from discontinued operations, net of tax” in accordance with IFRS 5

• As of the share distribution, accounting treatment to be determined based on Puma’s governance arrangements: shown either as “Available-for-sale financial assets”, or as “Investments in equity-accounted companies”

49*: Subject to Kering shareholders approval at the Annual General Meeting on

April 26, 2018. More detailed information is included in the financial report

(Subsequent events)

Gucci • Bottega Veneta • Saint Laurent • Balenciaga • Alexander McQueen • McQ

Stella McCartney • Brioni • Christopher Kane • Tomas Maier

Boucheron • Pomellato • Dodo • Qeelin • Ulysse Nardin • Girard -Perregaux

Puma • Cobra • Volcom

Kering Eyewear