DISC O TECH - BIU...Nike : Tc: nylon, Tn: Max Air, Max chock Product Disruptive Innovation Corning...

57

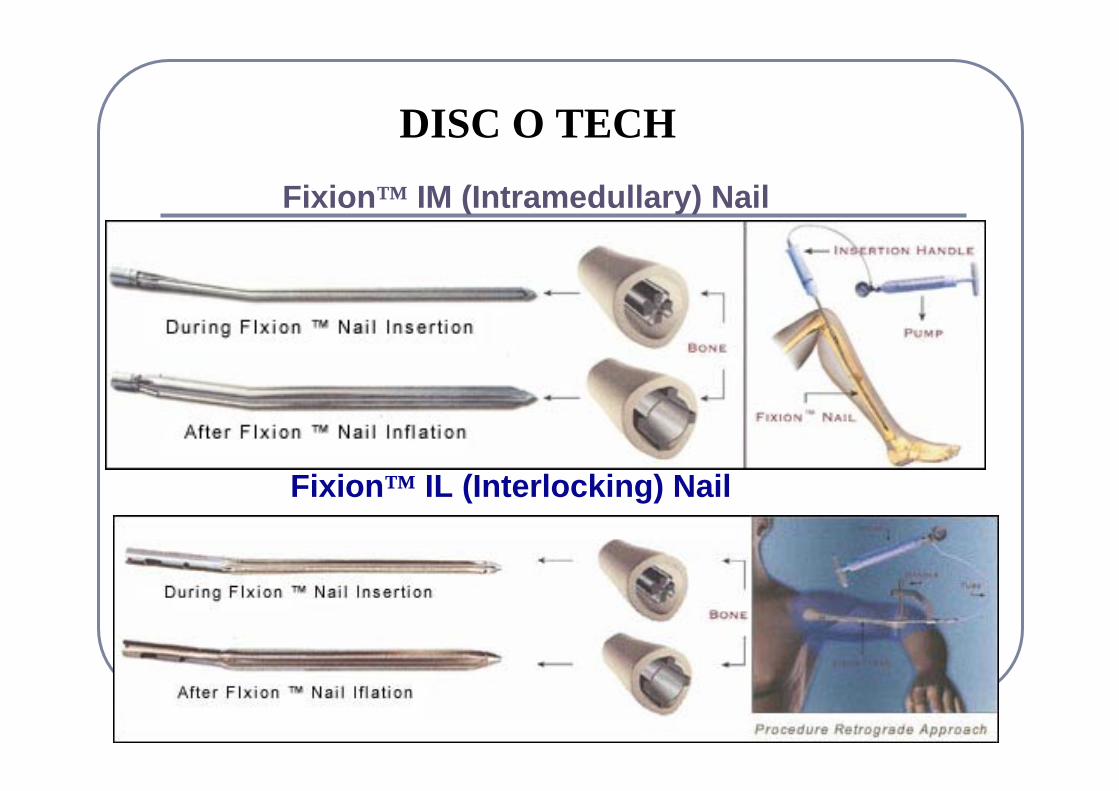

1 Fixion™ IM (Intramedullary) Nail Fixion™ IL (Interlocking) Nail DISC O TECH

Transcript of DISC O TECH - BIU...Nike : Tc: nylon, Tn: Max Air, Max chock Product Disruptive Innovation Corning...

1

Fixion™ IM (Intramedullary) Nail

Fixion™ IL (Interlocking) Nail

DISC O TECH

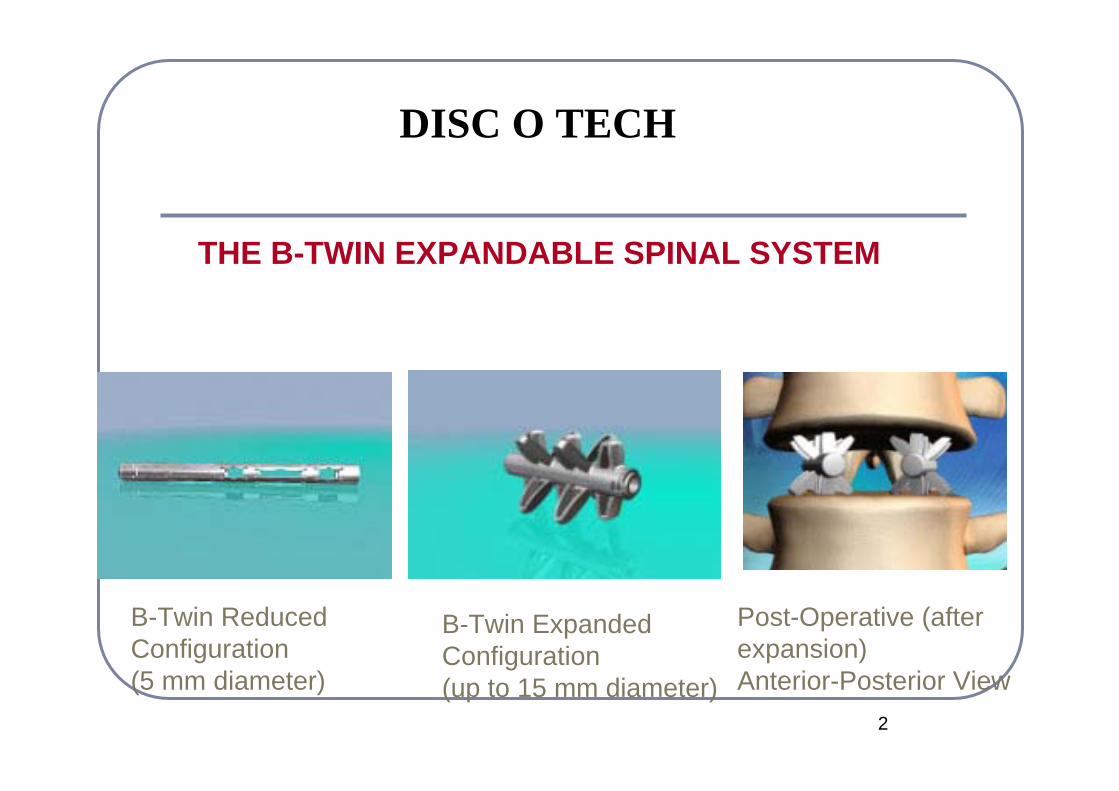

2

THE B-TWIN EXPANDABLE SPINAL SYSTEM

B-Twin Expanded Configuration(up to 15 mm diameter)

Post-Operative (after expansion)Anterior-Posterior View

B-Twin Reduced Configuration(5 mm diameter)

DISC O TECH

3

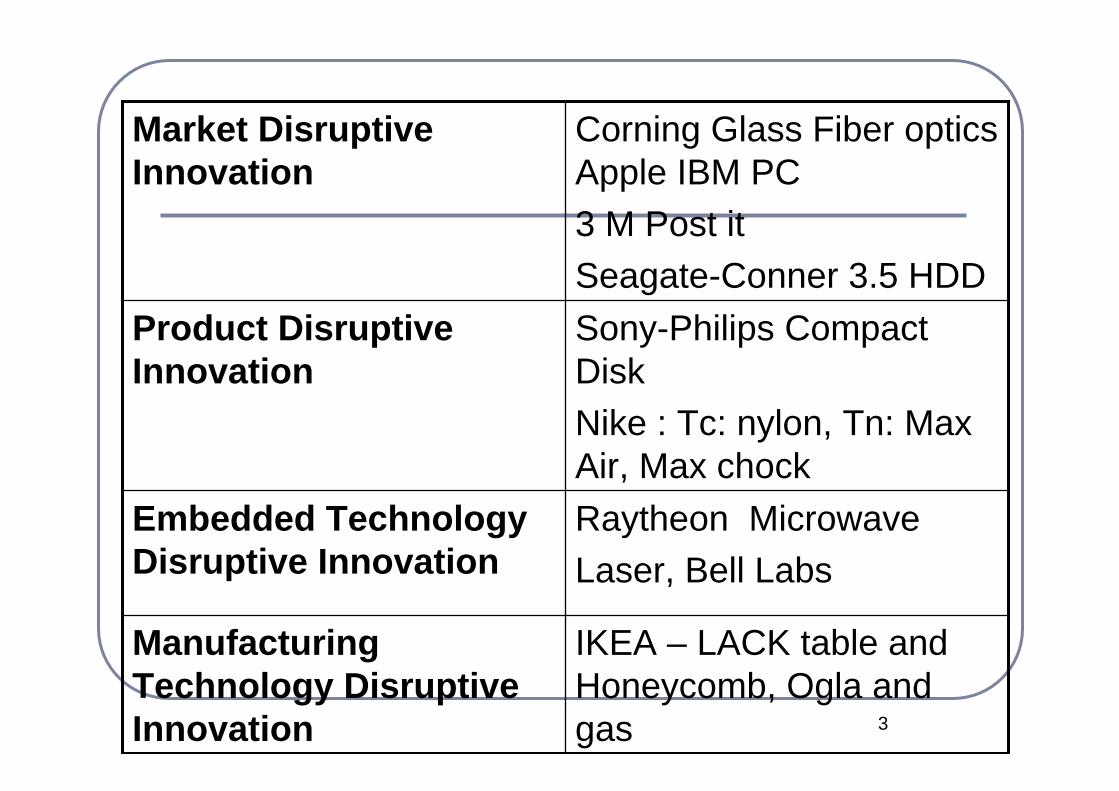

Raytheon MicrowaveLaser, Bell Labs

Embedded Technology Disruptive Innovation

IKEA – LACK table and Honeycomb, Ogla and gas

Manufacturing Technology Disruptive Innovation

Sony-Philips Compact DiskNike : Tc: nylon, Tn: Max Air, Max chock

Product Disruptive Innovation

Corning Glass Fiber optics Apple IBM PC 3 M Post itSeagate-Conner 3.5 HDD

Market Disruptive Innovation

4

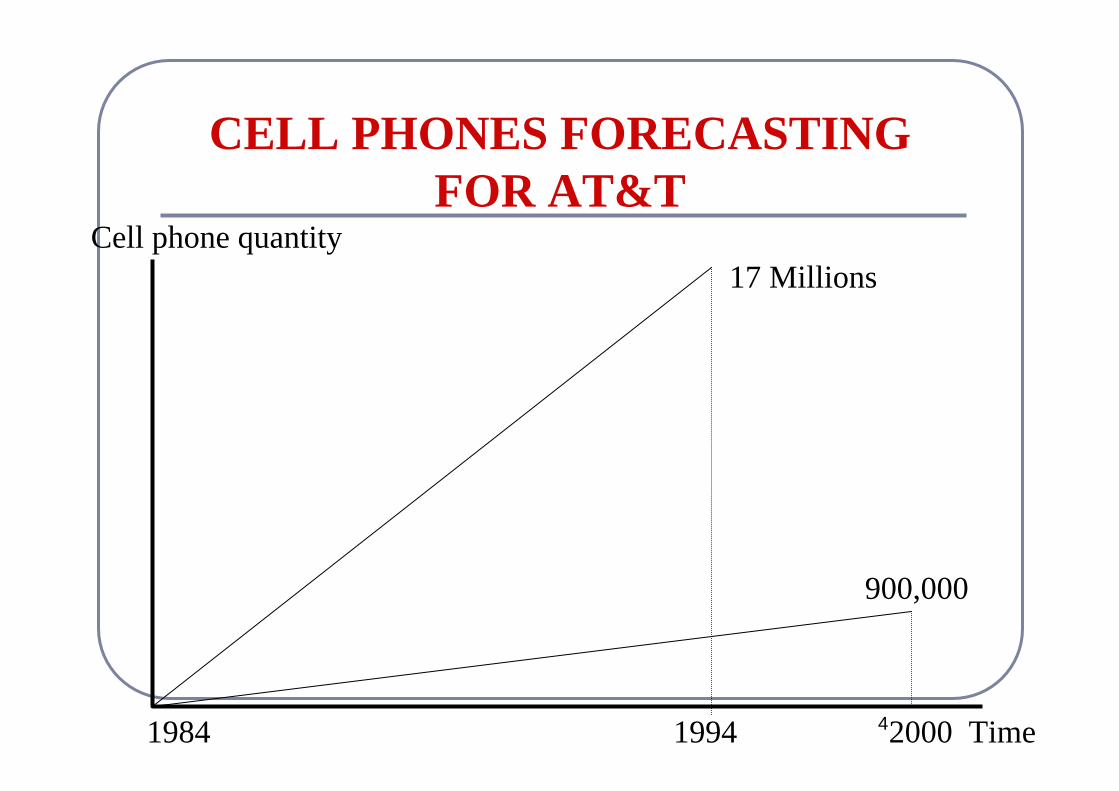

CELL PHONES FORECASTING FOR AT&T

Cell phone quantity

1984 1994 2000 Time

17 Millions

900,000

5

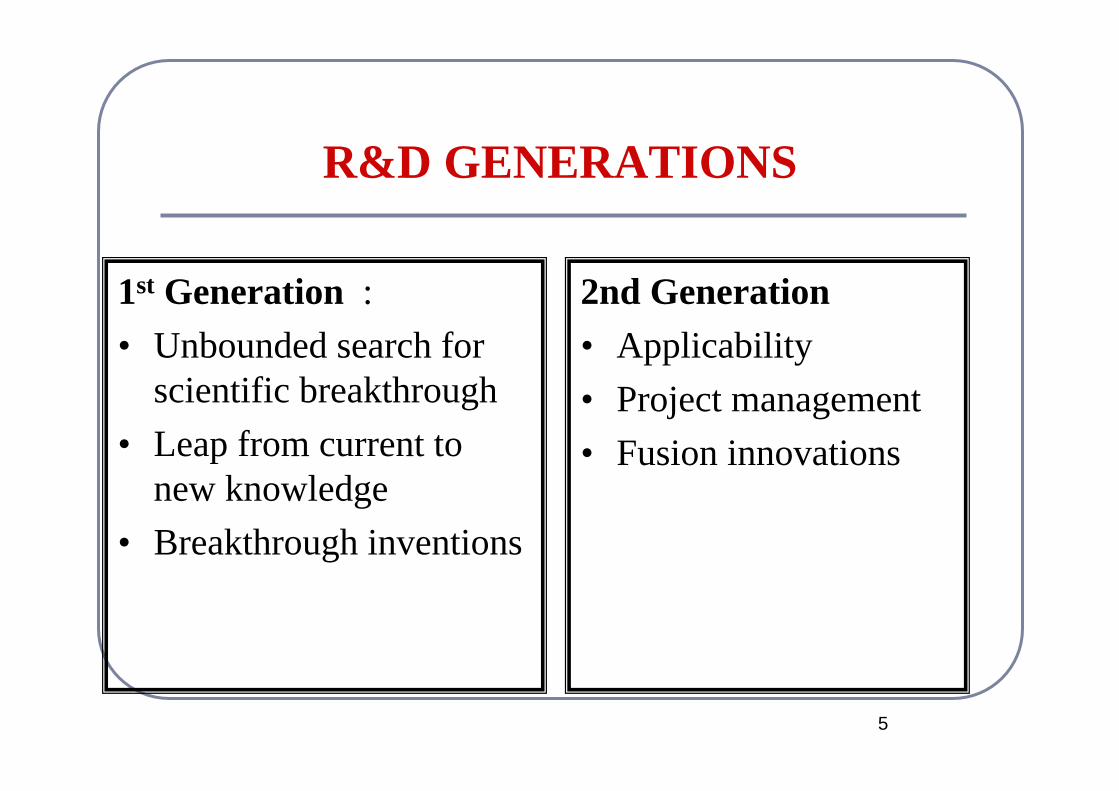

R&D GENERATIONS

1st Generation :• Unbounded search for

scientific breakthrough• Leap from current to

new knowledge• Breakthrough inventions

2nd Generation• Applicability• Project management• Fusion innovations

6

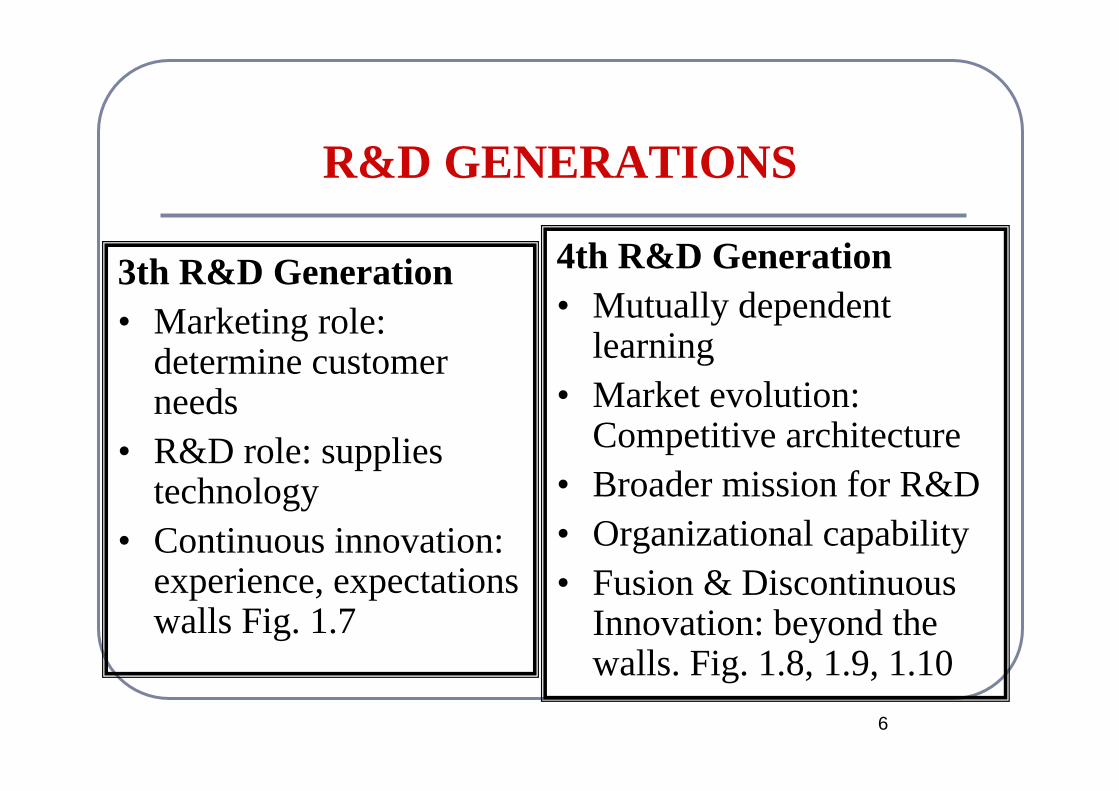

R&D GENERATIONS

3th R&D Generation • Marketing role:

determine customer needs

• R&D role: supplies technology

• Continuous innovation: experience, expectations walls Fig. 1.7

4th R&D Generation• Mutually dependent

learning• Market evolution:

Competitive architecture• Broader mission for R&D• Organizational capability• Fusion & Discontinuous

Innovation: beyond the walls. Fig. 1.8, 1.9, 1.10

7

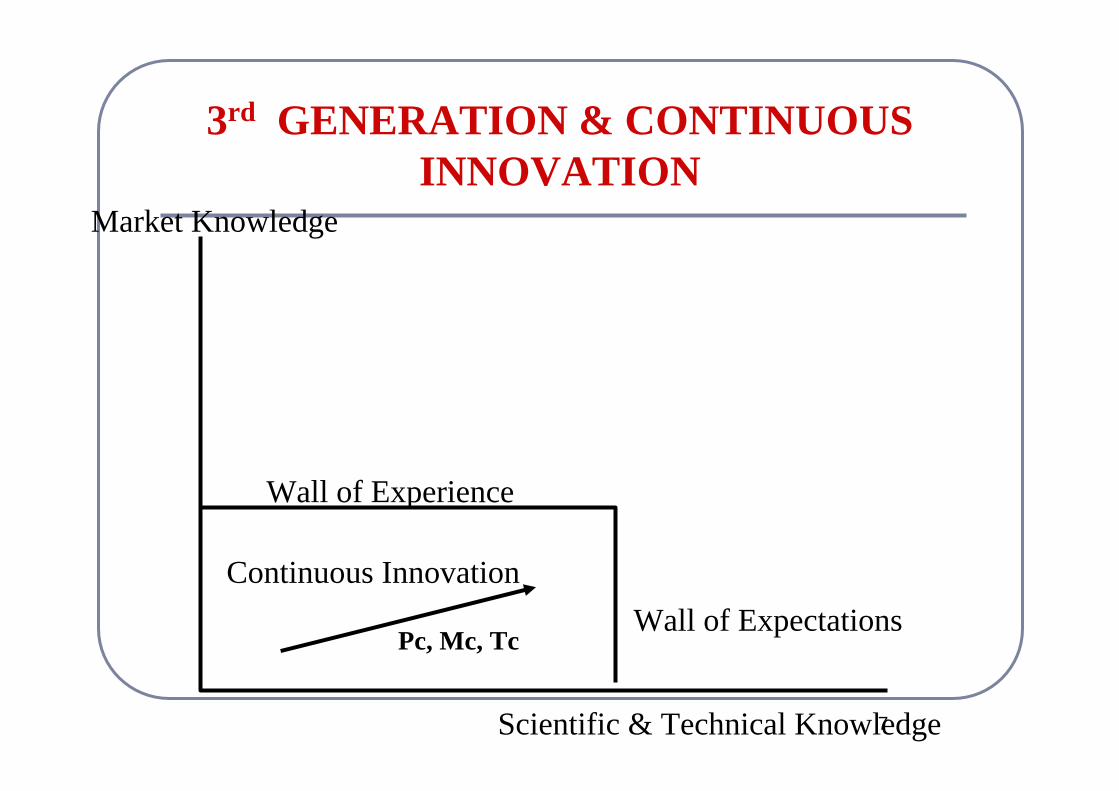

3rd GENERATION & CONTINUOUS INNOVATION

Market Knowledge

Scientific & Technical Knowledge

Wall of Experience

Wall of ExpectationsContinuous Innovation

Pc, Mc, Tc

8

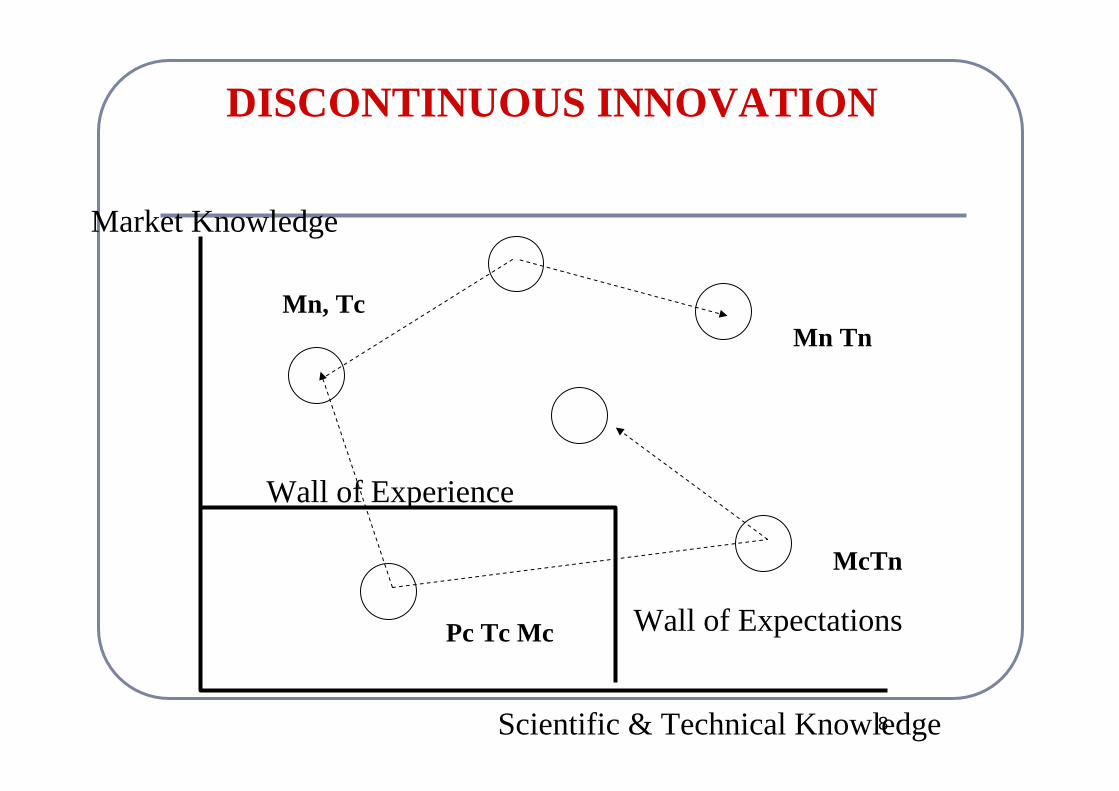

DISCONTINUOUS INNOVATION

Market Knowledge

Scientific & Technical Knowledge

Wall of Experience

Wall of Expectations

McTn

Mn TnMn, Tc

Pc Tc Mc

9

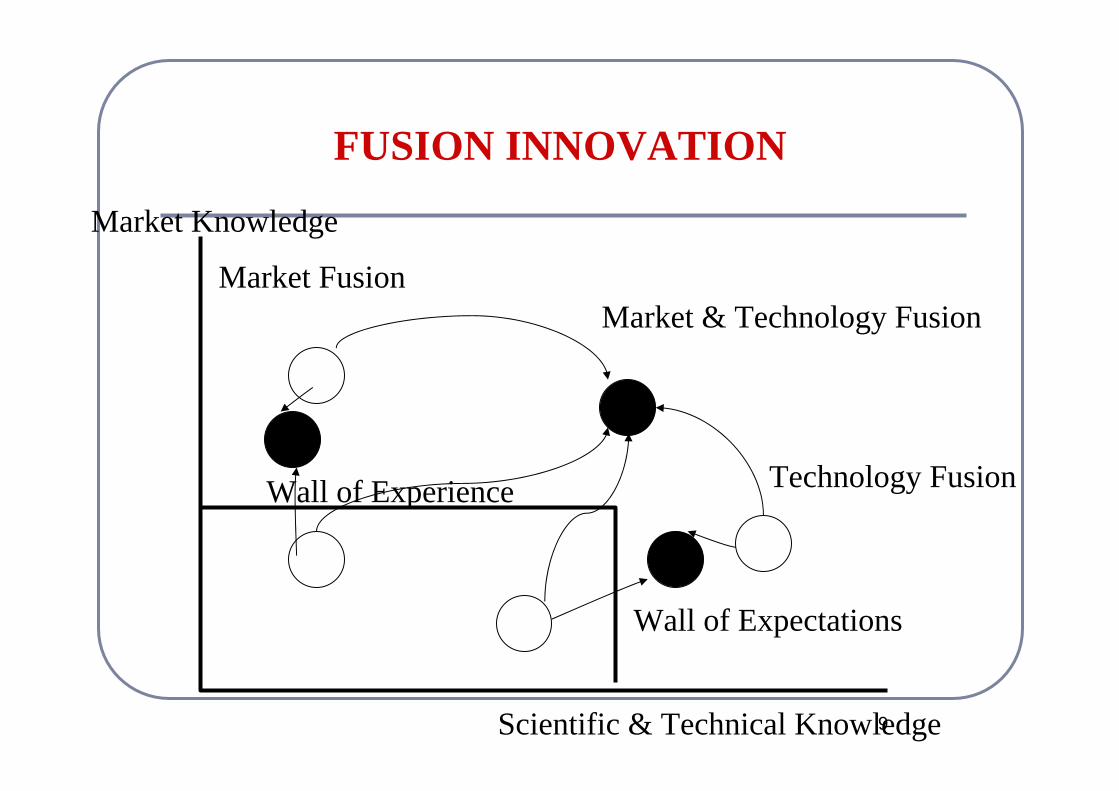

FUSION INNOVATION

Market Knowledge

Scientific & Technical Knowledge

Wall of Experience

Wall of Expectations

Market Fusion

Technology Fusion

Market & Technology Fusion

10

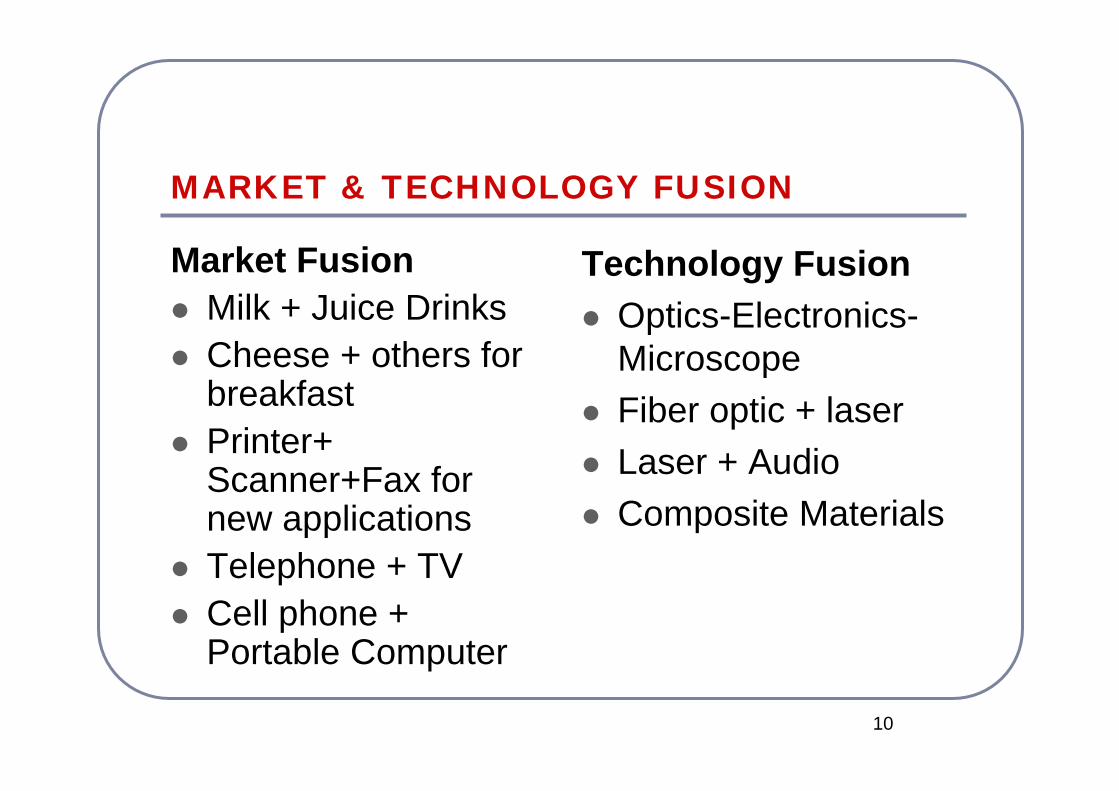

MARKET & TECHNOLOGY FUSION

Market FusionMilk + Juice DrinksCheese + others for breakfastPrinter+ Scanner+Fax for new applicationsTelephone + TVCell phone + Portable Computer

Technology FusionOptics-Electronics-MicroscopeFiber optic + laserLaser + AudioComposite Materials

11

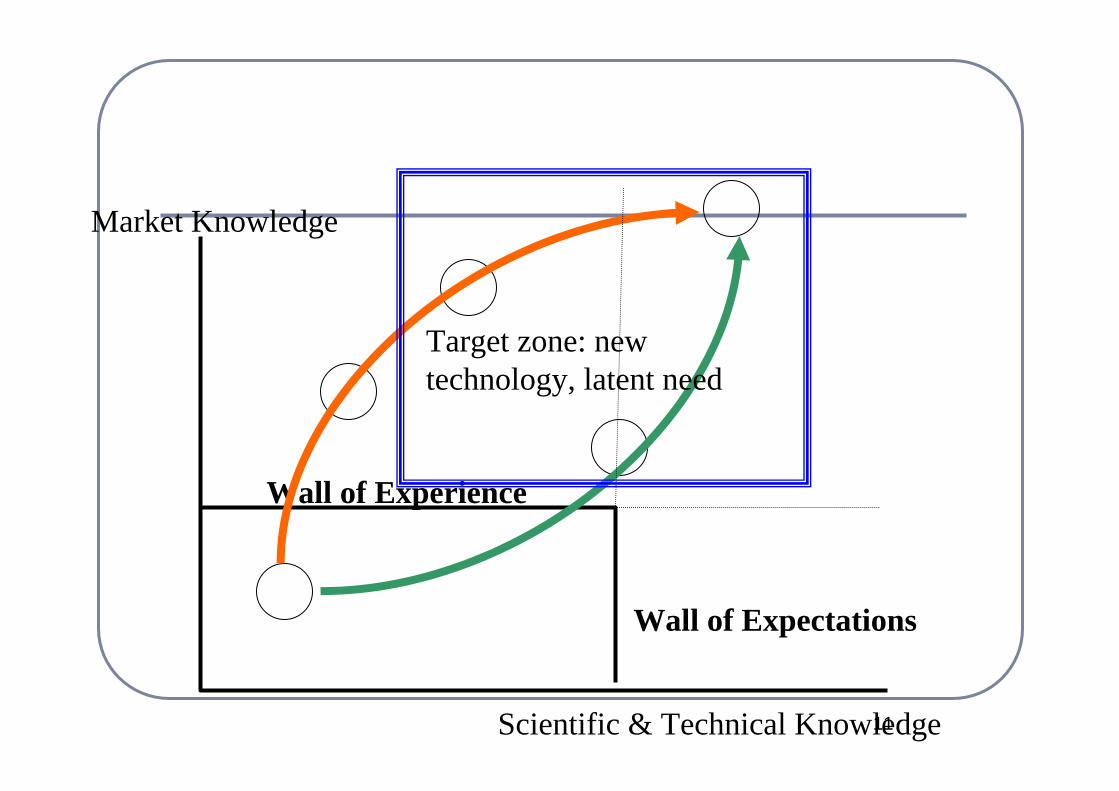

Market Knowledge

Scientific & Technical Knowledge

Wall of Experience

Wall of Expectations

Target zone: new technology, latent need

12

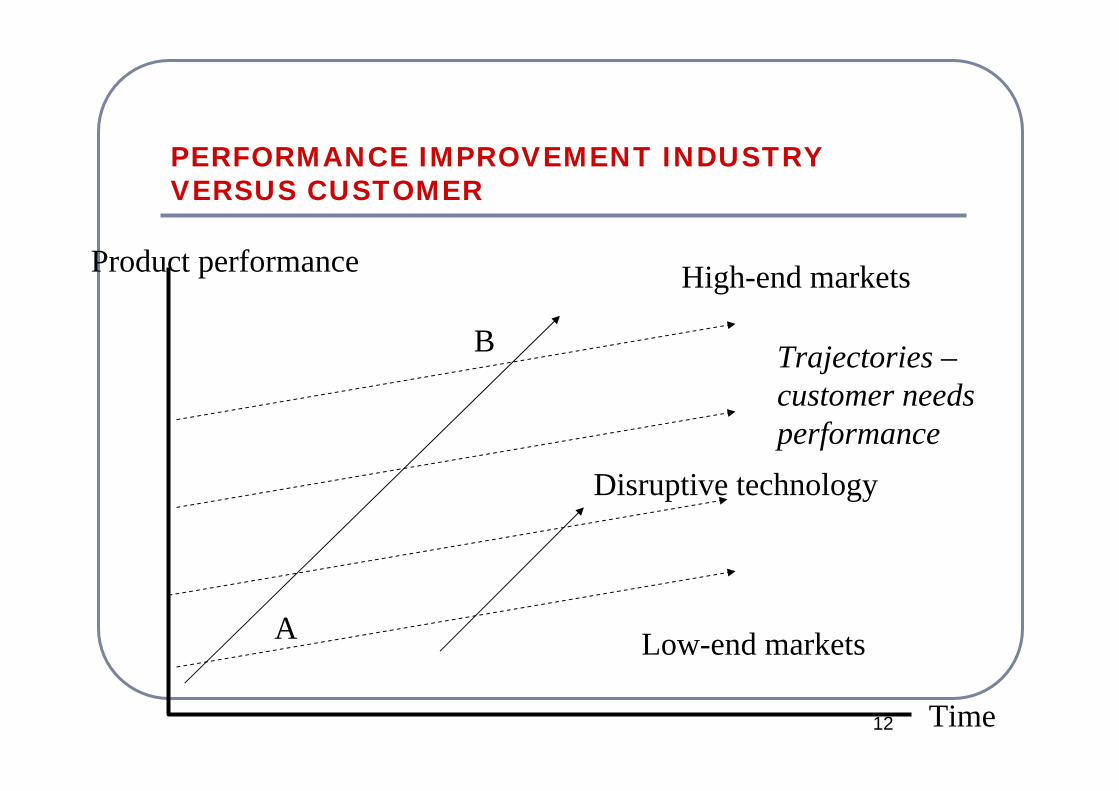

PERFORMANCE IMPROVEMENT INDUSTRY VERSUS CUSTOMER

Product performance

Time

Low-end markets

High-end markets

Disruptive technology

Trajectories –customer needs performance

A

B

13

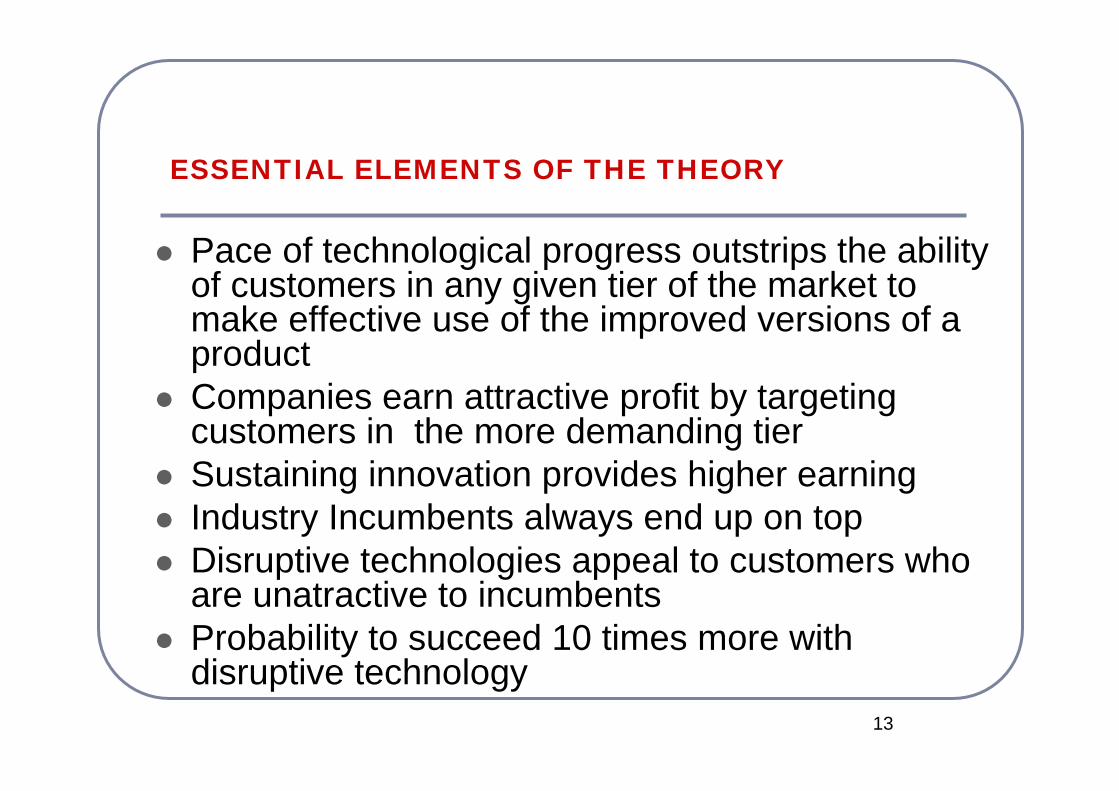

ESSENTIAL ELEMENTS OF THE THEORY

Pace of technological progress outstrips the ability of customers in any given tier of the market to make effective use of the improved versions of a productCompanies earn attractive profit by targeting customers in the more demanding tierSustaining innovation provides higher earningIndustry Incumbents always end up on topDisruptive technologies appeal to customers who are unatractive to incumbentsProbability to succeed 10 times more with disruptive technology

14

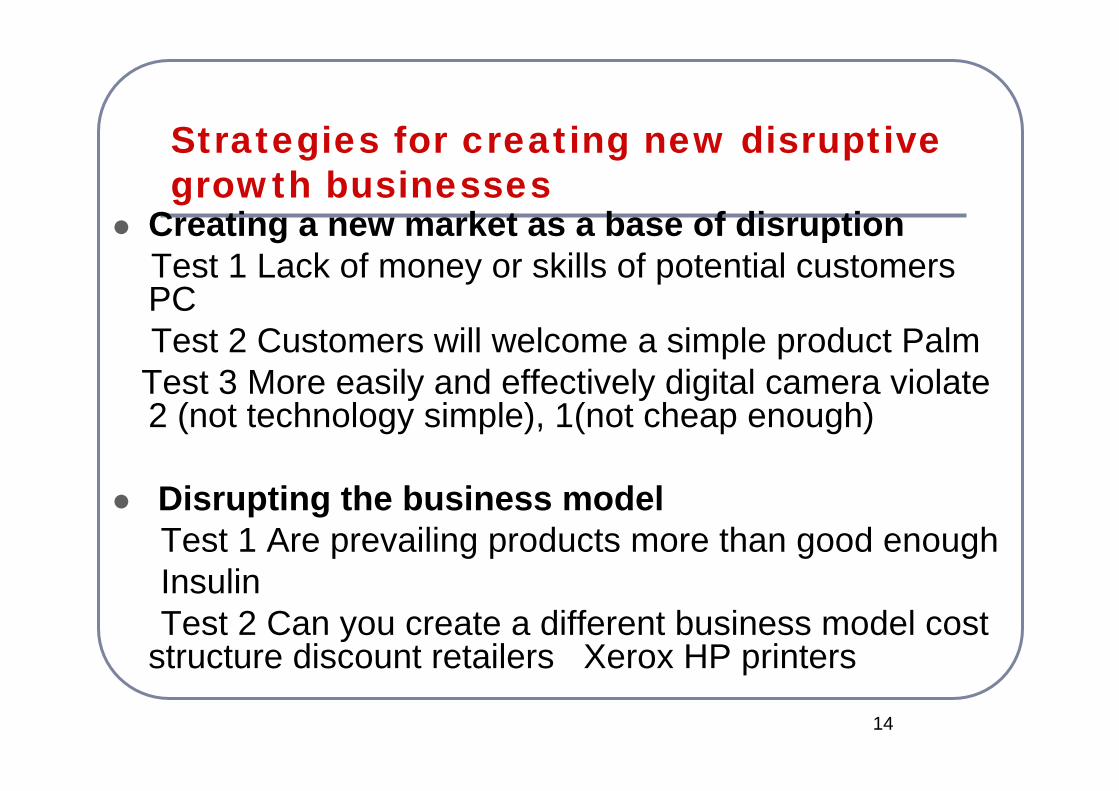

Strategies for creating new disruptive growth businesses

Creating a new market as a base of disruptionTest 1 Lack of money or skills of potential customers PCTest 2 Customers will welcome a simple product Palm

Test 3 More easily and effectively digital camera violate 2 (not technology simple), 1(not cheap enough)

Disrupting the business modelTest 1 Are prevailing products more than good enoughInsulinTest 2 Can you create a different business model cost

structure discount retailers Xerox HP printers

15

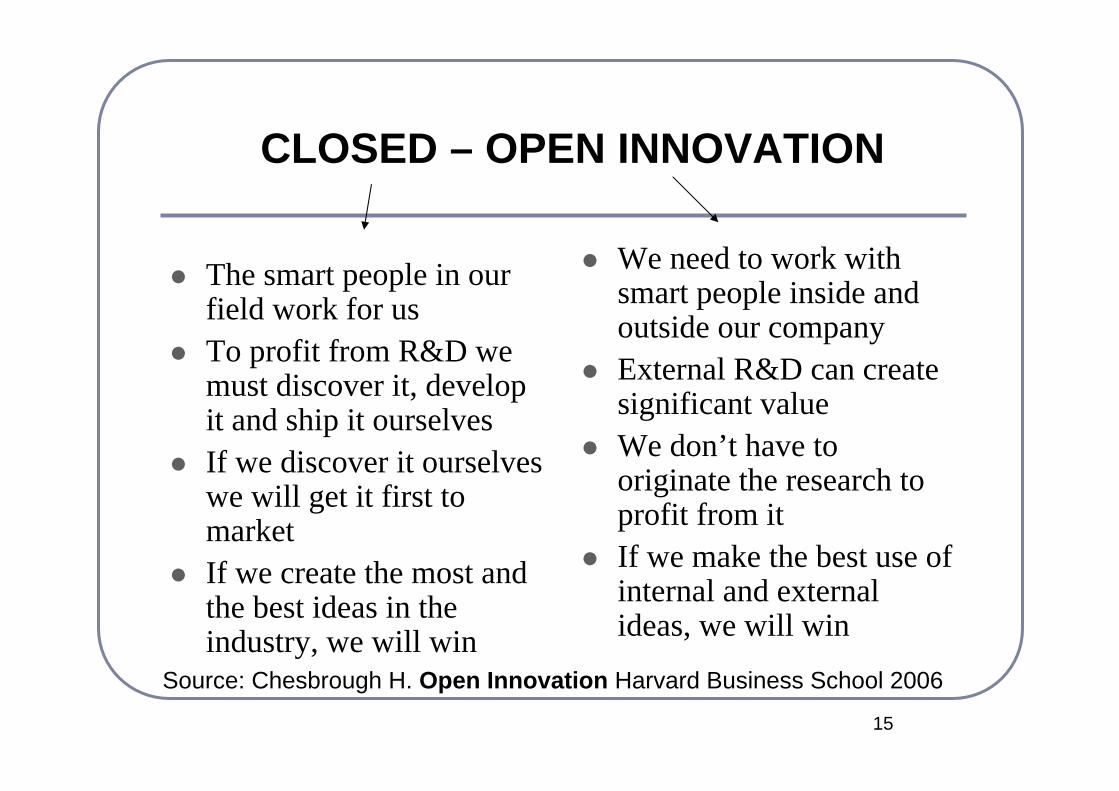

The smart people in our field work for usTo profit from R&D we must discover it, develop it and ship it ourselvesIf we discover it ourselves we will get it first to marketIf we create the most and the best ideas in the industry, we will win

We need to work with smart people inside and outside our companyExternal R&D can create significant valueWe don’t have to originate the research to profit from itIf we make the best use of internal and external ideas, we will win

CLOSED – OPEN INNOVATION

Source: Chesbrough H. Open Innovation Harvard Business School 2006

16

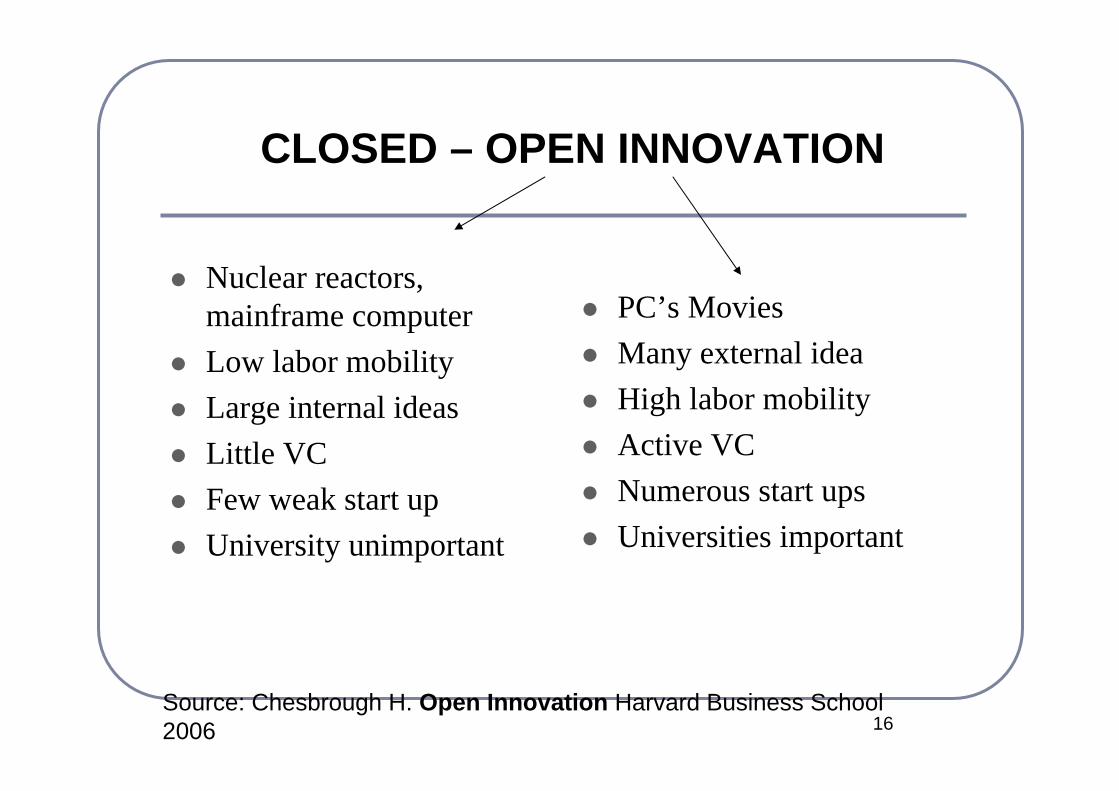

Nuclear reactors, mainframe computerLow labor mobilityLarge internal ideasLittle VCFew weak start upUniversity unimportant

PC’s MoviesMany external ideaHigh labor mobilityActive VCNumerous start upsUniversities important

CLOSED – OPEN INNOVATION

Source: Chesbrough H. Open Innovation Harvard Business School 2006

17

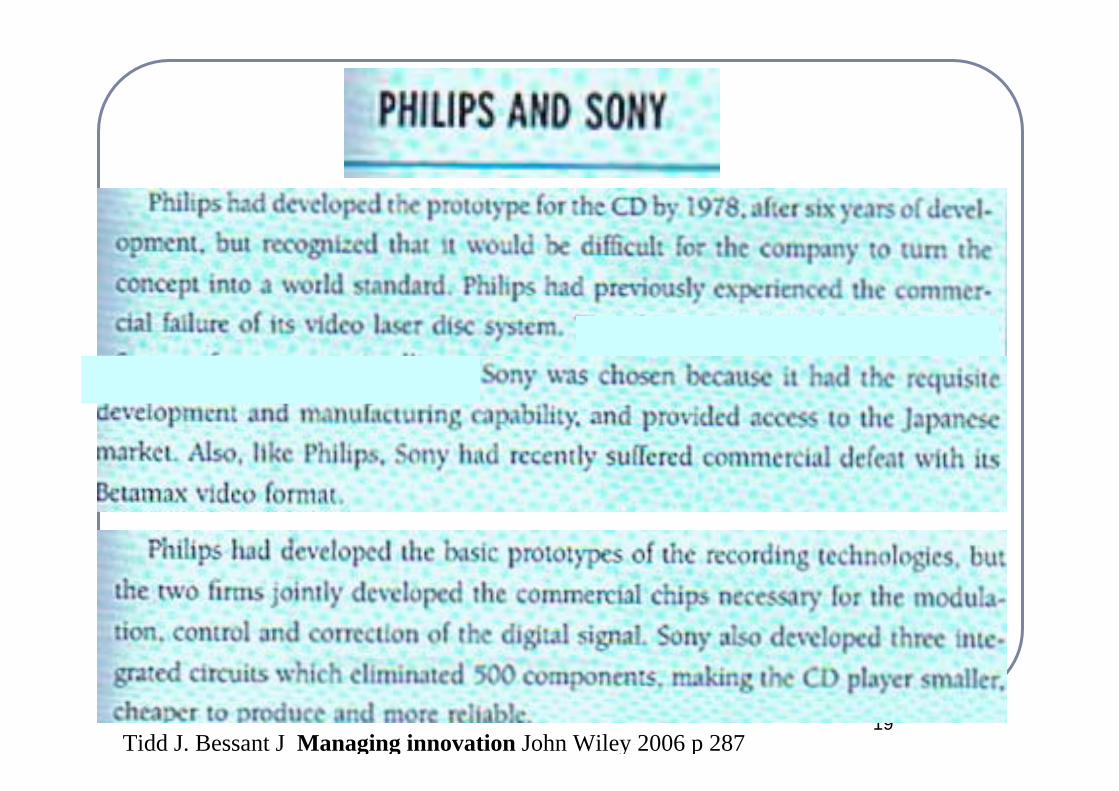

18

19Tidd J. Bessant J Managing innovation John Wiley 2006 p 287

20

21

INNOVATION STRATEGIES

Miles & Snow(78) Defenders, Prospectors, AnalyzersFreeman(82) Offensive, Defensive, Imitative,

Dependent, Traditional Opportunistic Ettlie and Bridges(87) Aggressive technology policy Long term investment in technological solutionPlanning human resources for itOpenness the environmentStructural adaptationKerin et al (92) First movers

Ettlie J.E.(2006) Managing Innovation Elsevier p 111-114

22

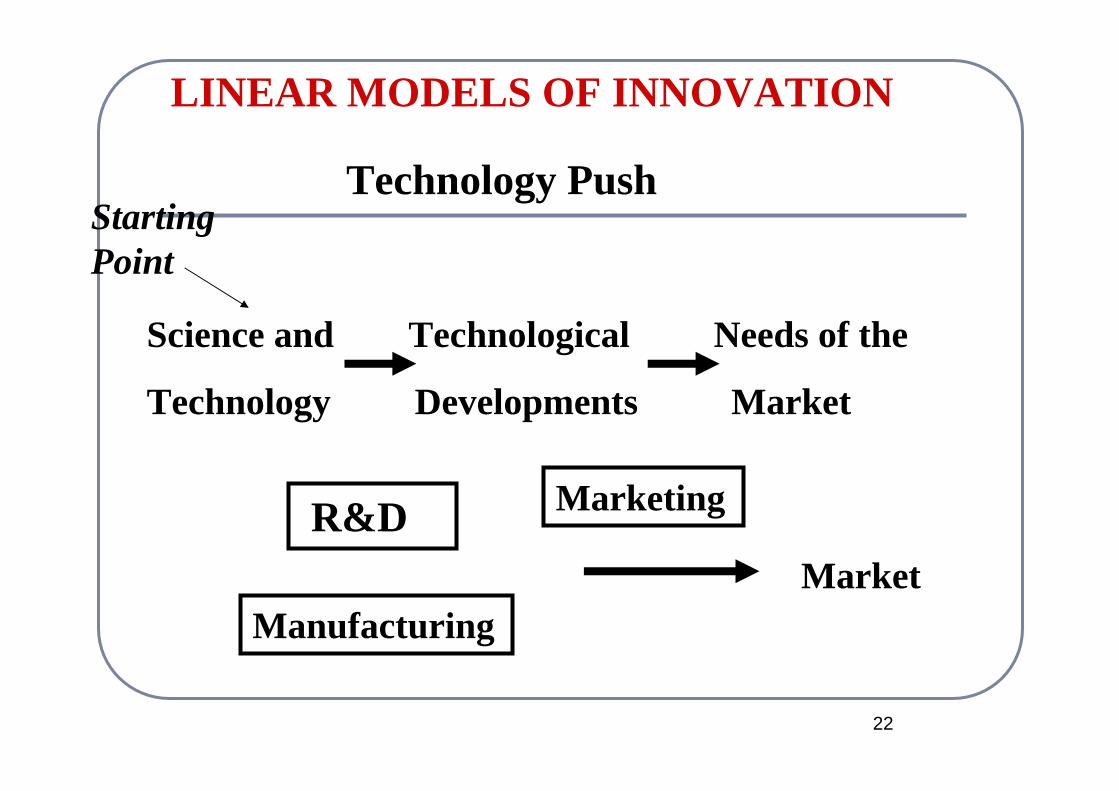

LINEAR MODELS OF INNOVATION

Science and Technological Needs of the

Technology Developments Market

R&D

Manufacturing

Marketing

Market

Technology PushStarting Point

23

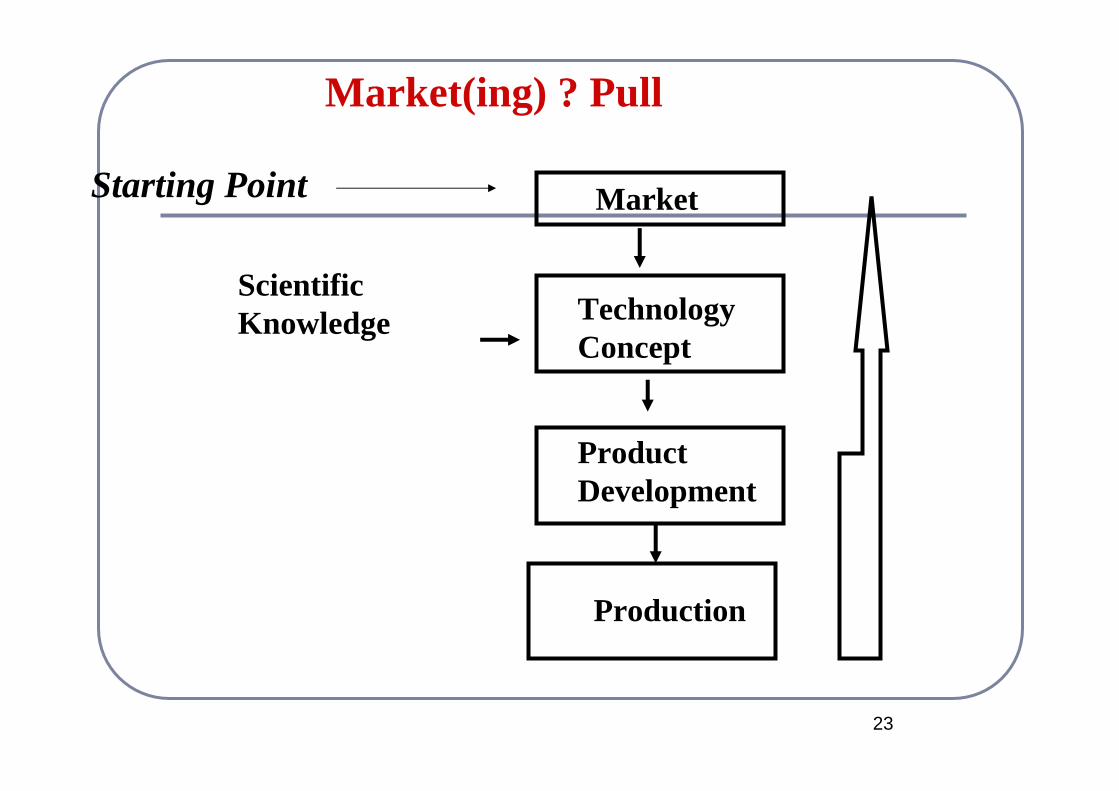

Market(ing) ? Pull

Market

Scientific Knowledge Technology

Concept

Product Development

Production

Starting Point

24

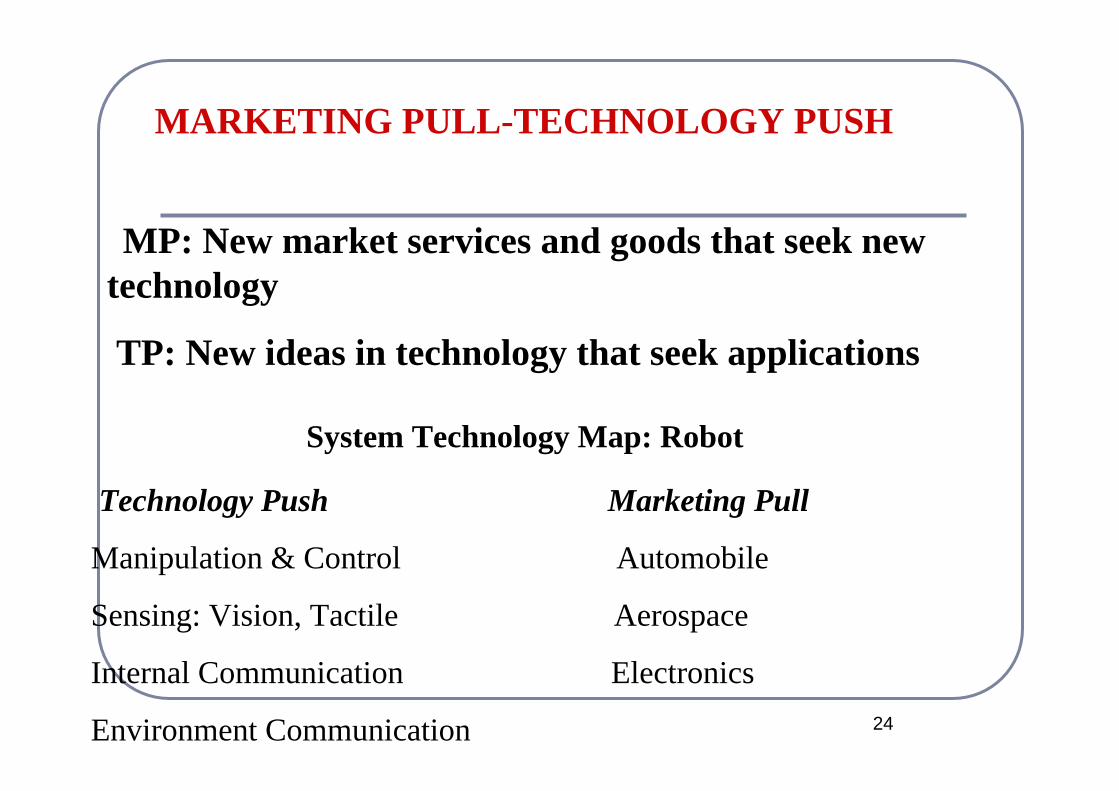

MP: New market services and goods that seek new technology

TP: New ideas in technology that seek applications

MARKETING PULL-TECHNOLOGY PUSH

System Technology Map: Robot

Technology Push Marketing Pull

Manipulation & Control Automobile

Sensing: Vision, Tactile Aerospace

Internal Communication Electronics

Environment Communication

25

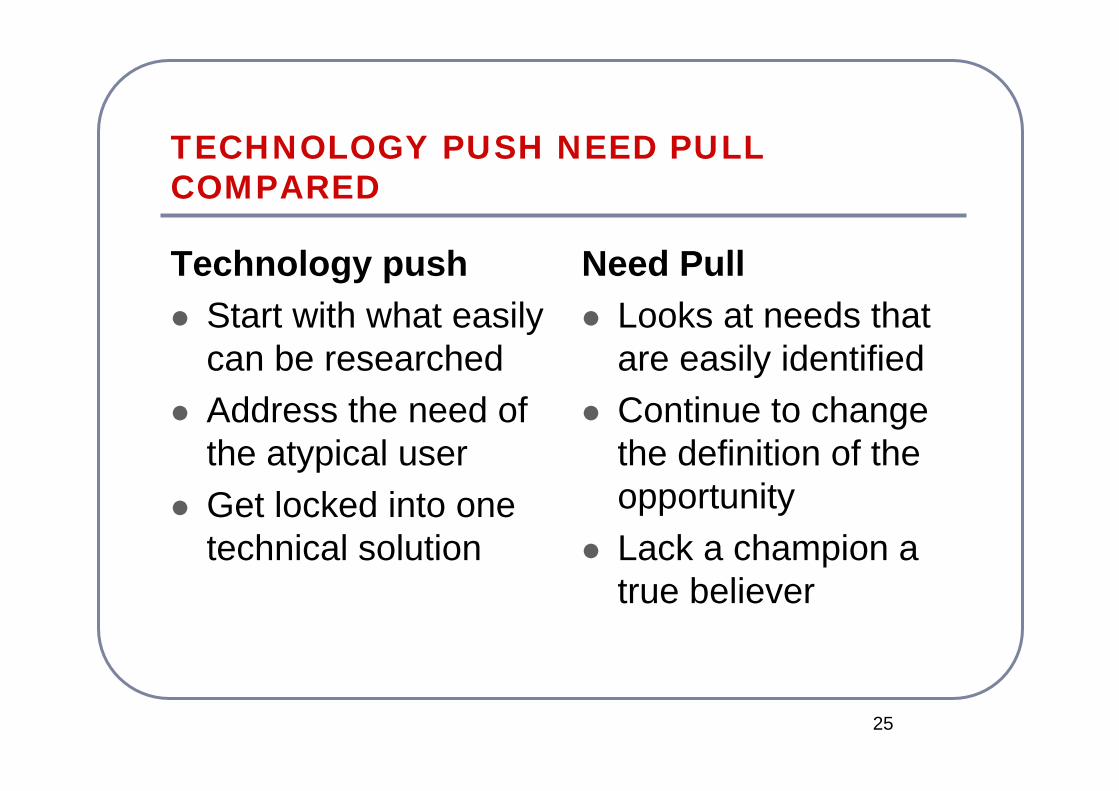

TECHNOLOGY PUSH NEED PULL COMPARED

Technology pushStart with what easily can be researchedAddress the need of the atypical userGet locked into one technical solution

Need PullLooks at needs that are easily identifiedContinue to change the definition of the opportunityLack a champion a true believer

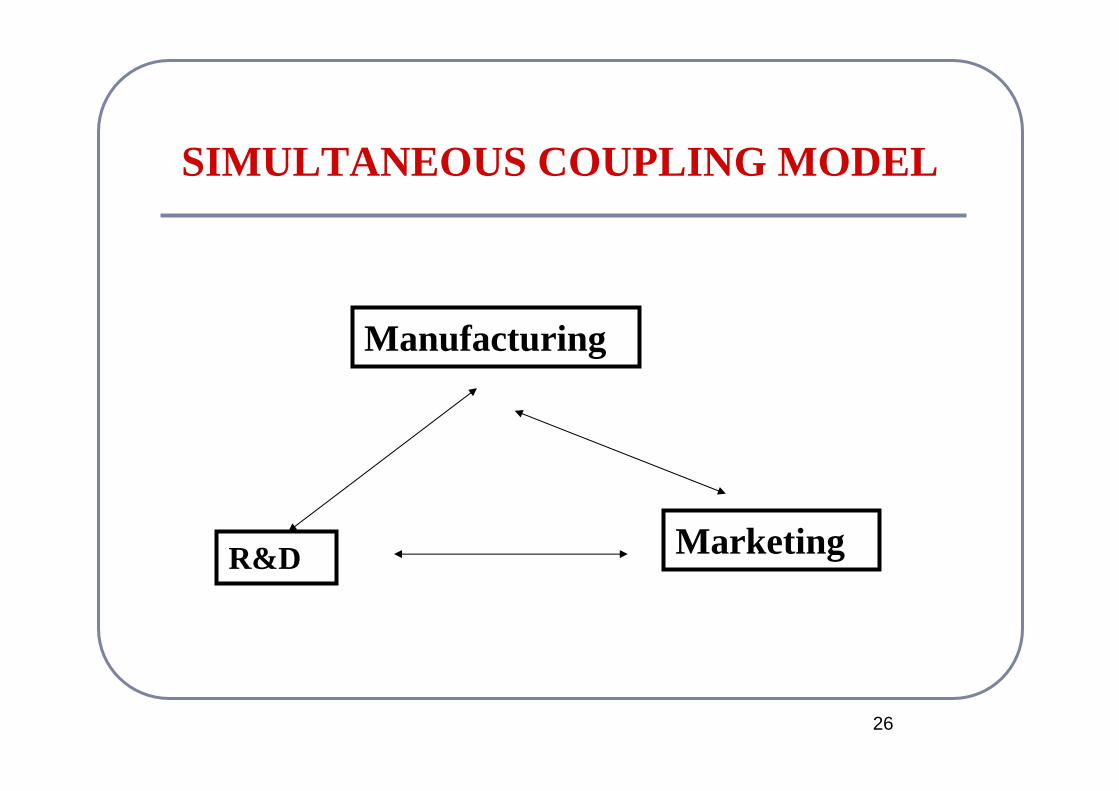

26

SIMULTANEOUS COUPLING MODEL

Manufacturing

R&D Marketing

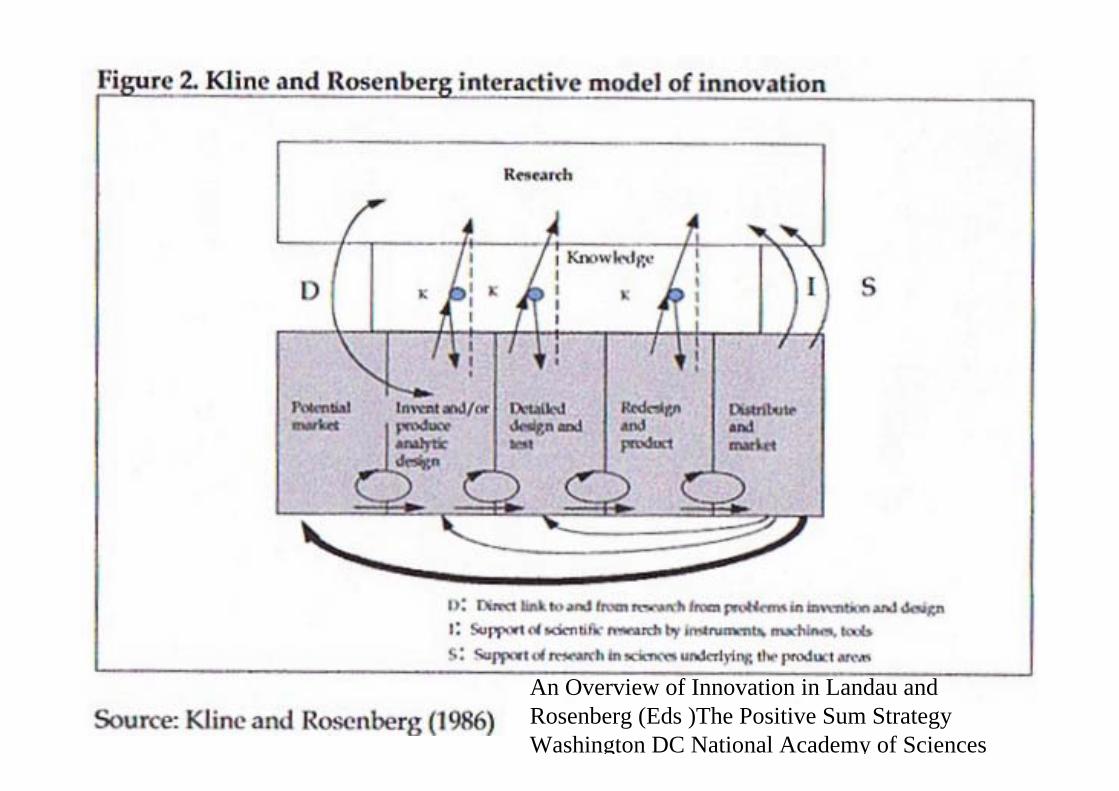

27

An Overview of Innovation in Landau and Rosenberg (Eds )The Positive Sum Strategy Washington DC National Academy of Sciences

28

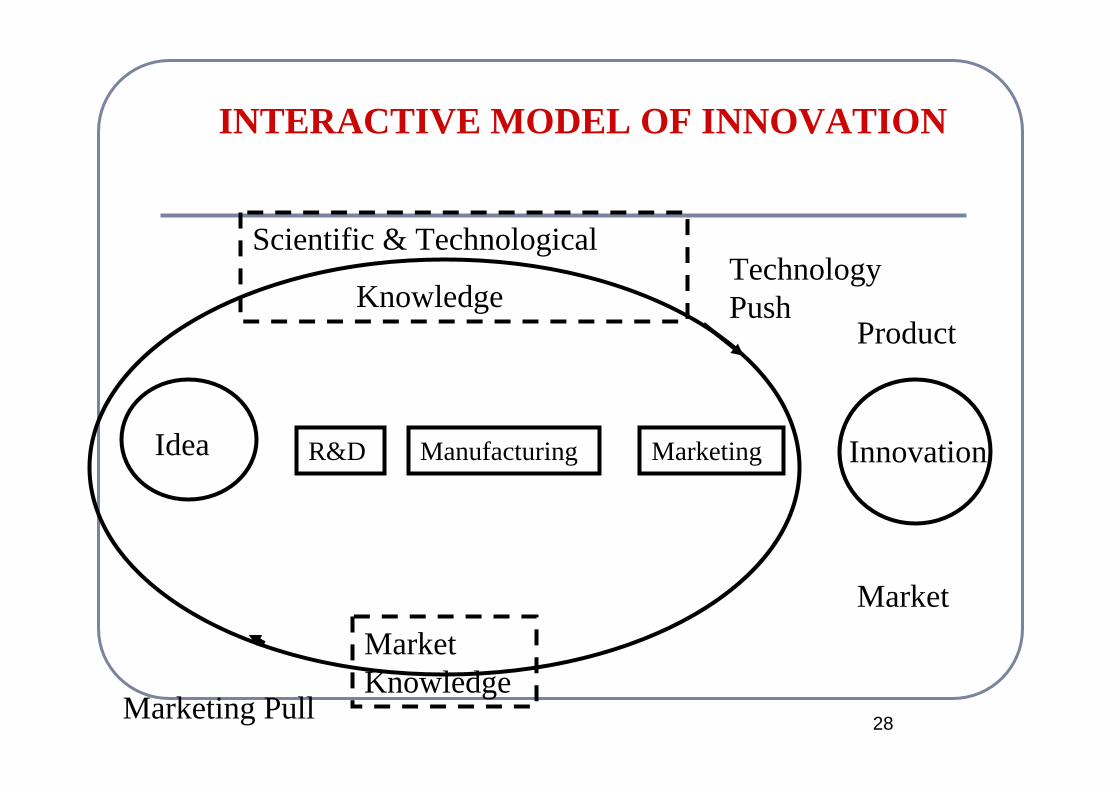

INTERACTIVE MODEL OF INNOVATION

R&D Marketing

Product

Manufacturing

Market Knowledge

Scientific & Technological

Knowledge

Idea Innovation

Technology Push

Marketing Pull

Market

29

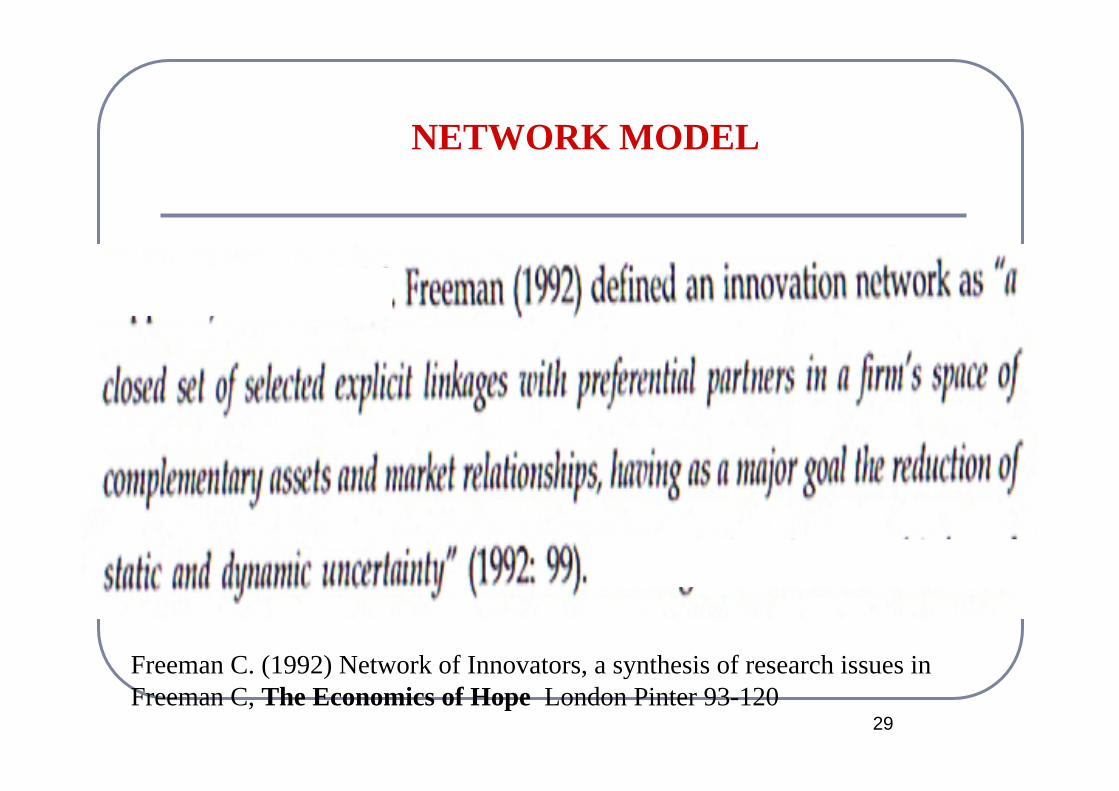

NETWORK MODEL

Freeman C. (1992) Network of Innovators, a synthesis of research issues in Freeman C, The Economics of Hope London Pinter 93-120

30

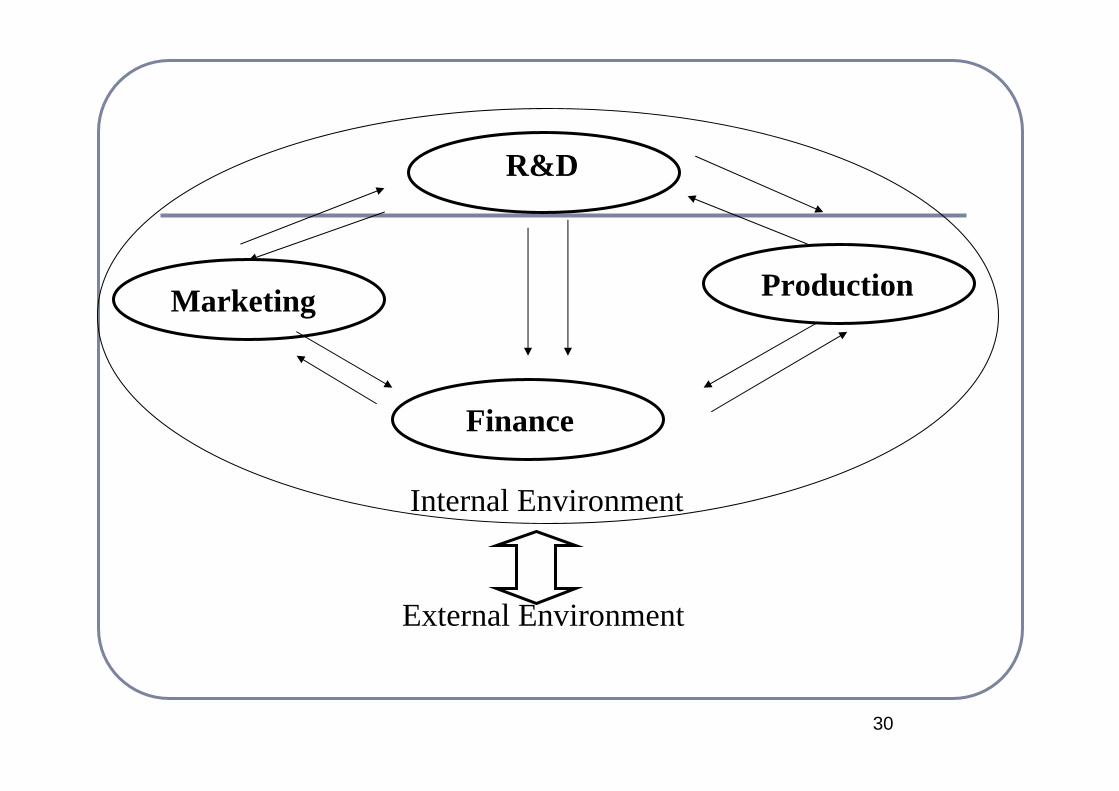

R&D

Finance

ProductionMarketing

Internal Environment

External Environment

31

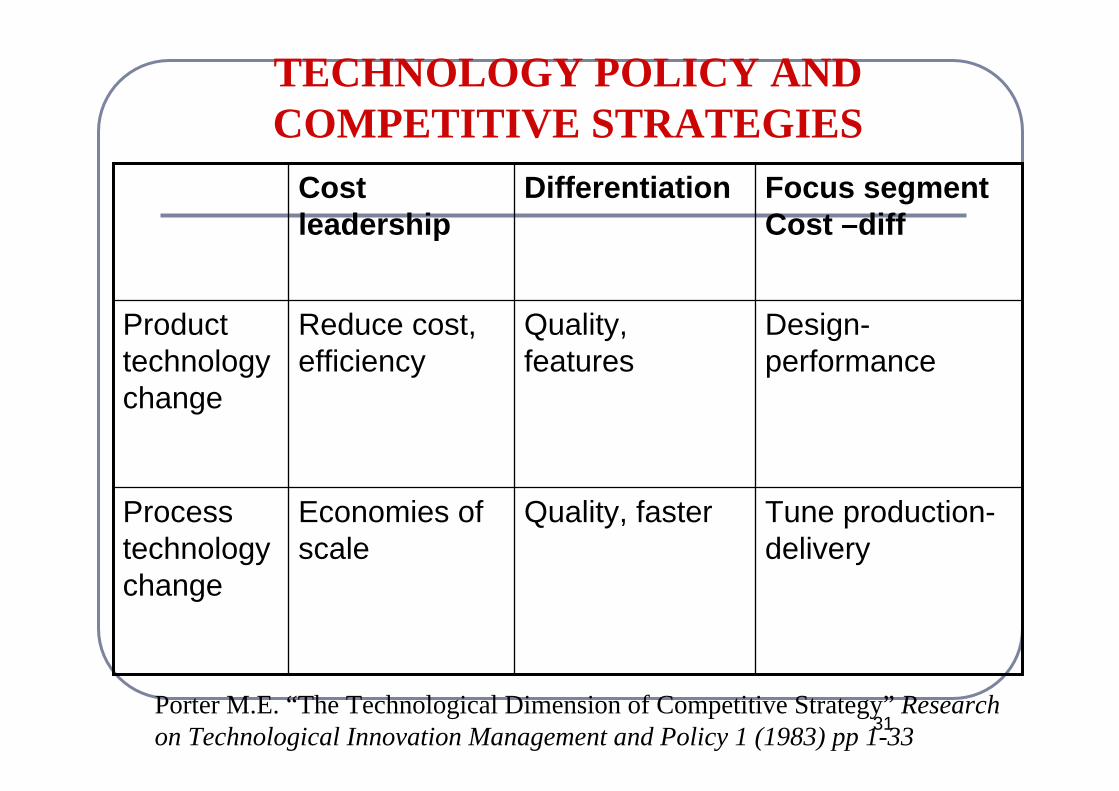

TECHNOLOGY POLICY AND COMPETITIVE STRATEGIES

Tune production-delivery

Quality, fasterEconomies of scale

Process technology change

Design-performance

Quality, features

Reduce cost, efficiency

Product technology change

Focus segment Cost –diff

DifferentiationCost leadership

Porter M.E. “The Technological Dimension of Competitive Strategy” Research on Technological Innovation Management and Policy 1 (1983) pp 1-33

32

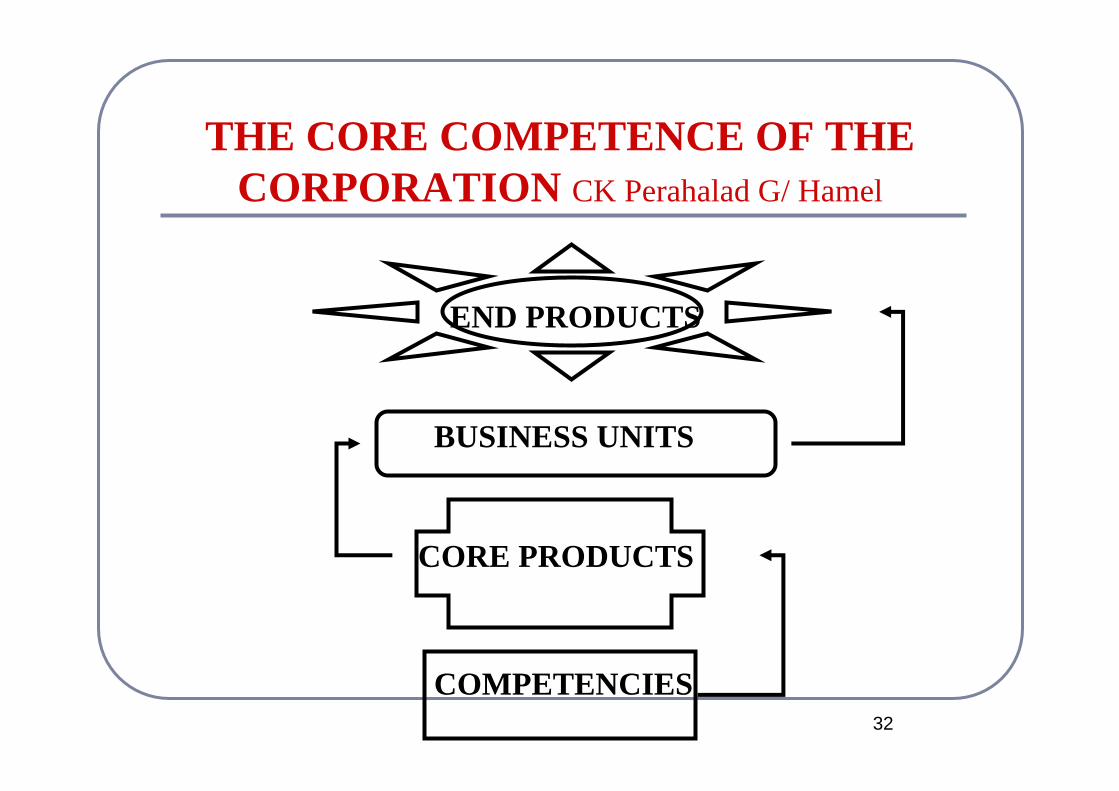

THE CORE COMPETENCE OF THE CORPORATION CK Perahalad G/ Hamel

COMPETENCIES

CORE PRODUCTS

BUSINESS UNITS

END PRODUCTS

33

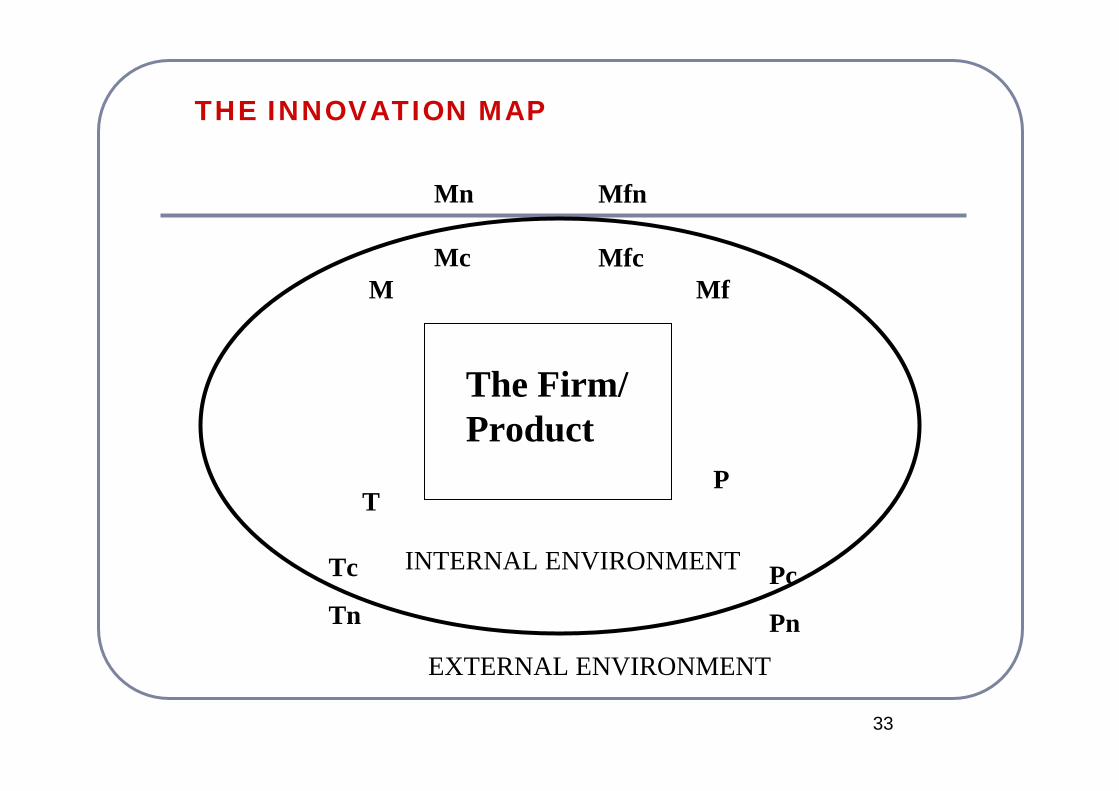

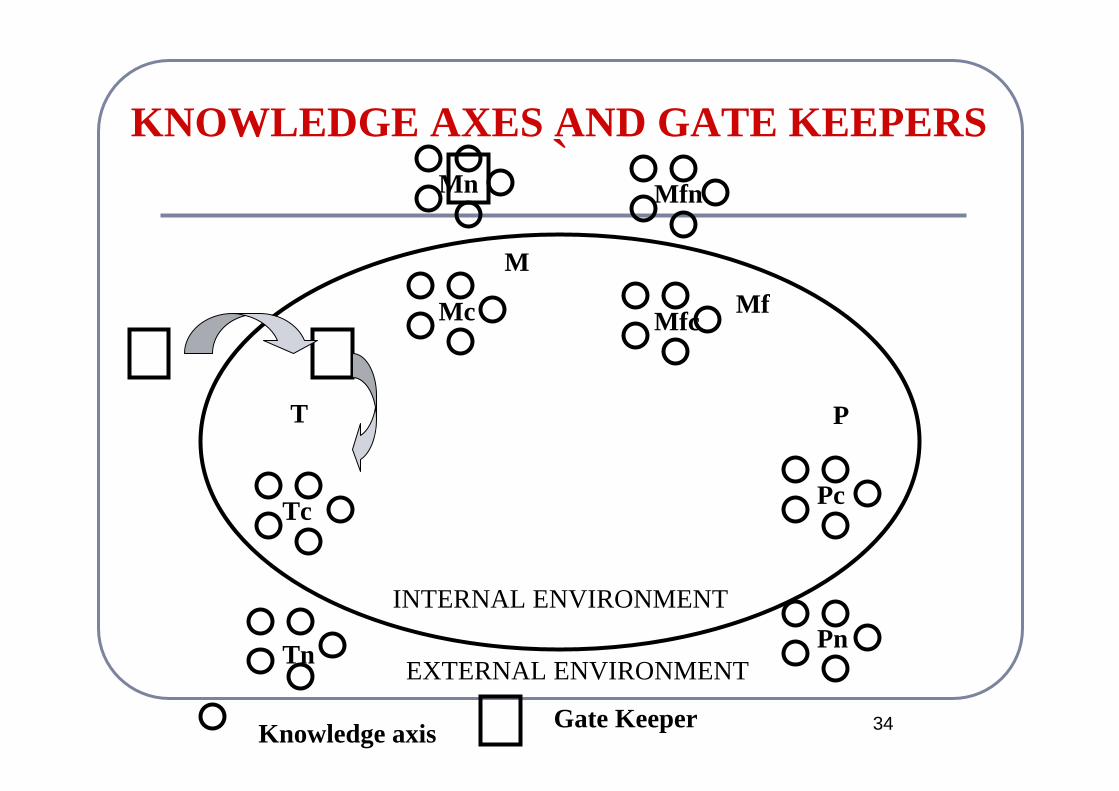

THE INNOVATION MAP

INTERNAL ENVIRONMENT

EXTERNAL ENVIRONMENT

M

TP

Tc

TnPc

Pn

Mn

McMf

Mfn

Mfc

The Firm/ Product

34

`

INTERNAL ENVIRONMENT

EXTERNAL ENVIRONMENT

M

T P

Tc

Tn

Pc

Pn

Mn

Mc

KNOWLEDGE AXES AND GATE KEEPERS

Knowledge axis Gate Keeper

Mfn

MfcMf

35

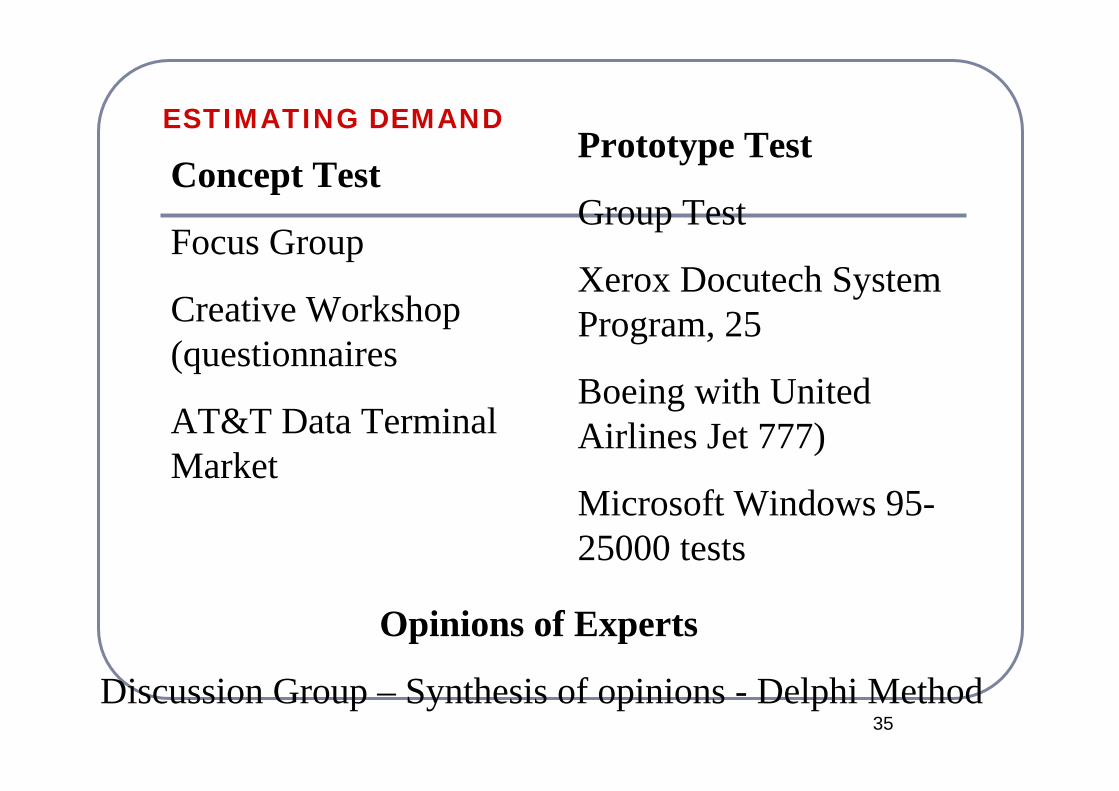

ESTIMATING DEMAND

Concept Test

Focus Group

Creative Workshop (questionnaires

AT&T Data Terminal Market

Prototype Test

Group Test

Xerox Docutech System Program, 25

Boeing with United Airlines Jet 777)

Microsoft Windows 95-25000 tests

Opinions of Experts

Discussion Group – Synthesis of opinions - Delphi Method

36

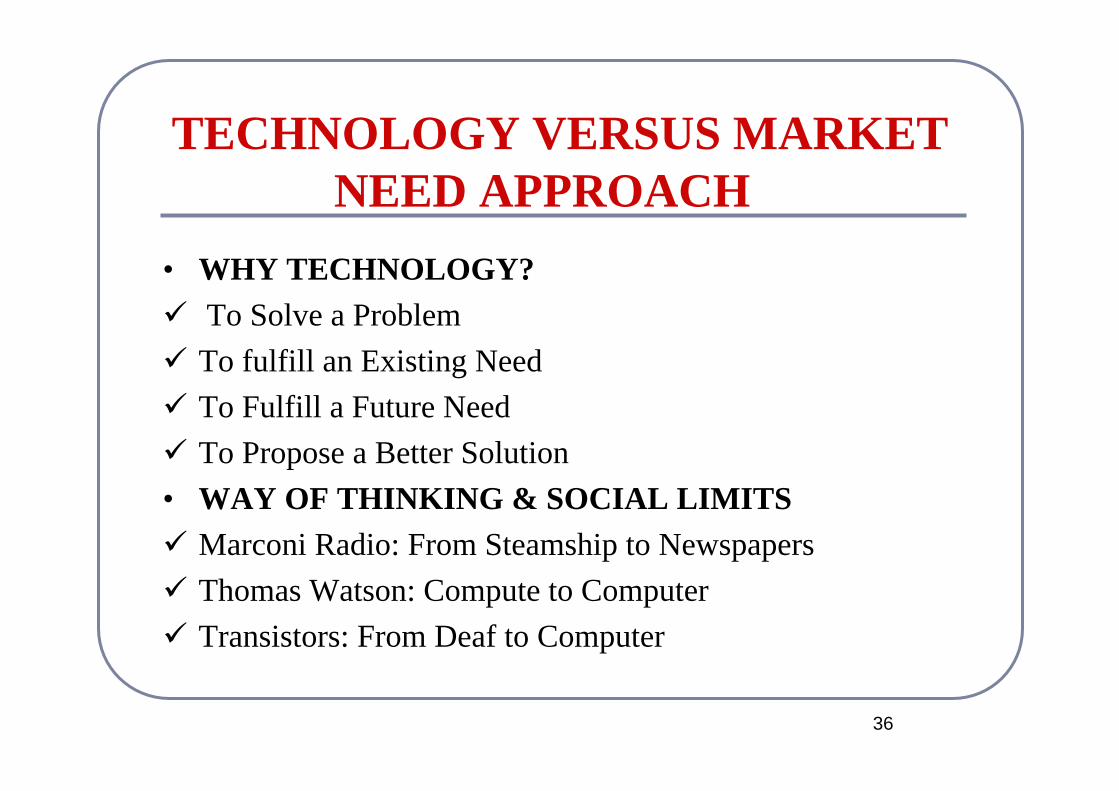

TECHNOLOGY VERSUS MARKET NEED APPROACH

• WHY TECHNOLOGY?To Solve a ProblemTo fulfill an Existing NeedTo Fulfill a Future NeedTo Propose a Better Solution

• WAY OF THINKING & SOCIAL LIMITSMarconi Radio: From Steamship to NewspapersThomas Watson: Compute to ComputerTransistors: From Deaf to Computer

37

TECHNOLOGY LIFE CYCLE (Trajectory of Technological Improvement)

Time

Application’s

Efficiency

Man hours invested

Emergence Growth Maturity Decline

38

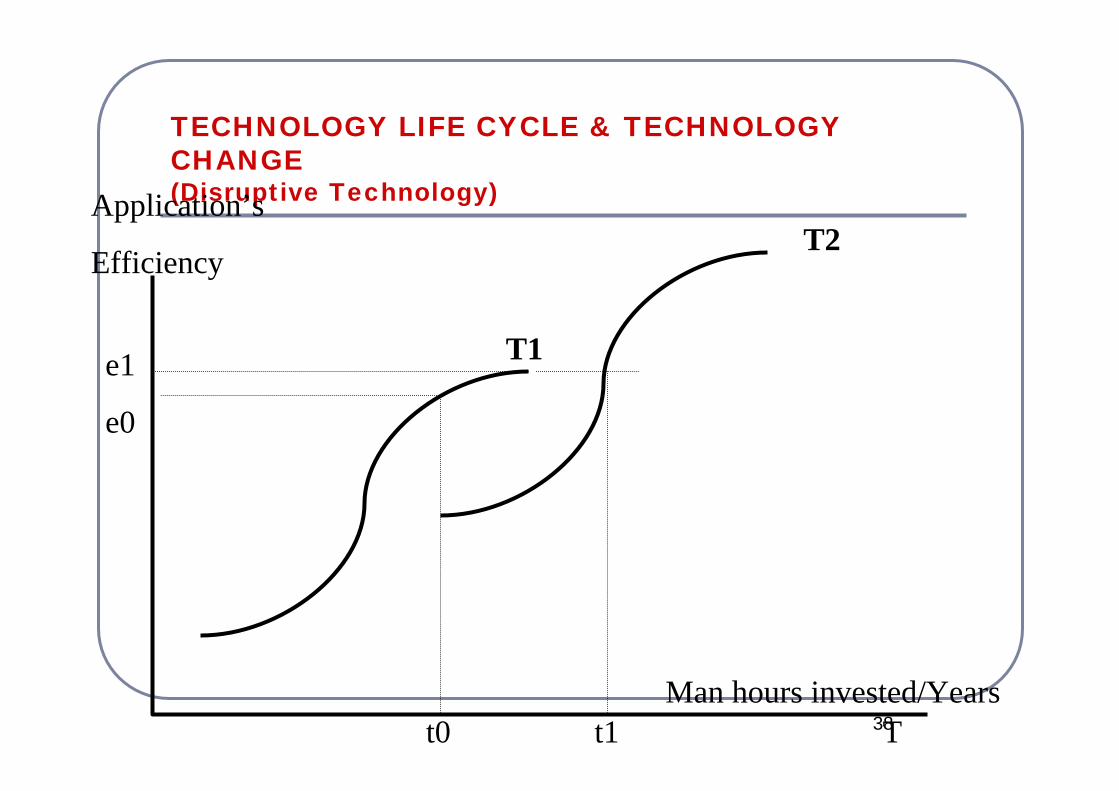

TECHNOLOGY LIFE CYCLE & TECHNOLOGY CHANGE(Disruptive Technology)

t0 t1 T

Application’s

Efficiency

e1

e0

T1

Man hours invested/Years

T2

39

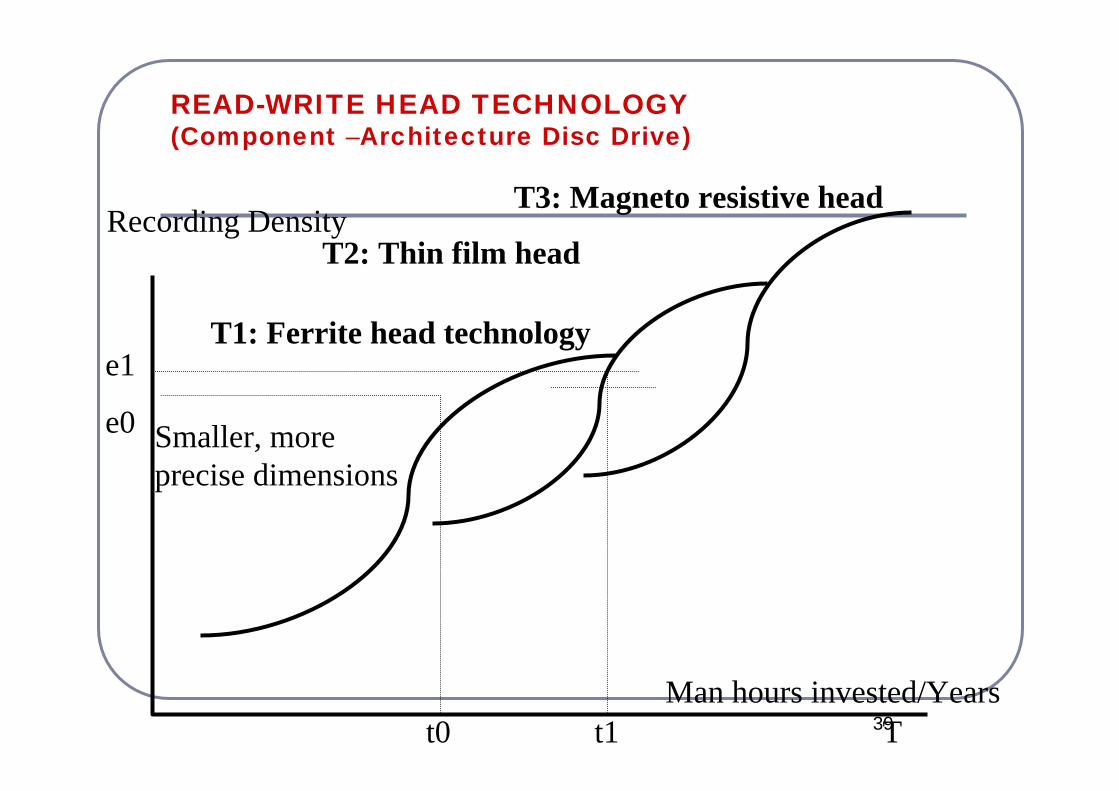

READ-WRITE HEAD TECHNOLOGY(Component –Architecture Disc Drive)

t0 t1 T

Recording Density

e1

e0

T1: Ferrite head technology

Man hours invested/Years

T3: Magneto resistive head

Smaller, more precise dimensions

T2: Thin film head

40

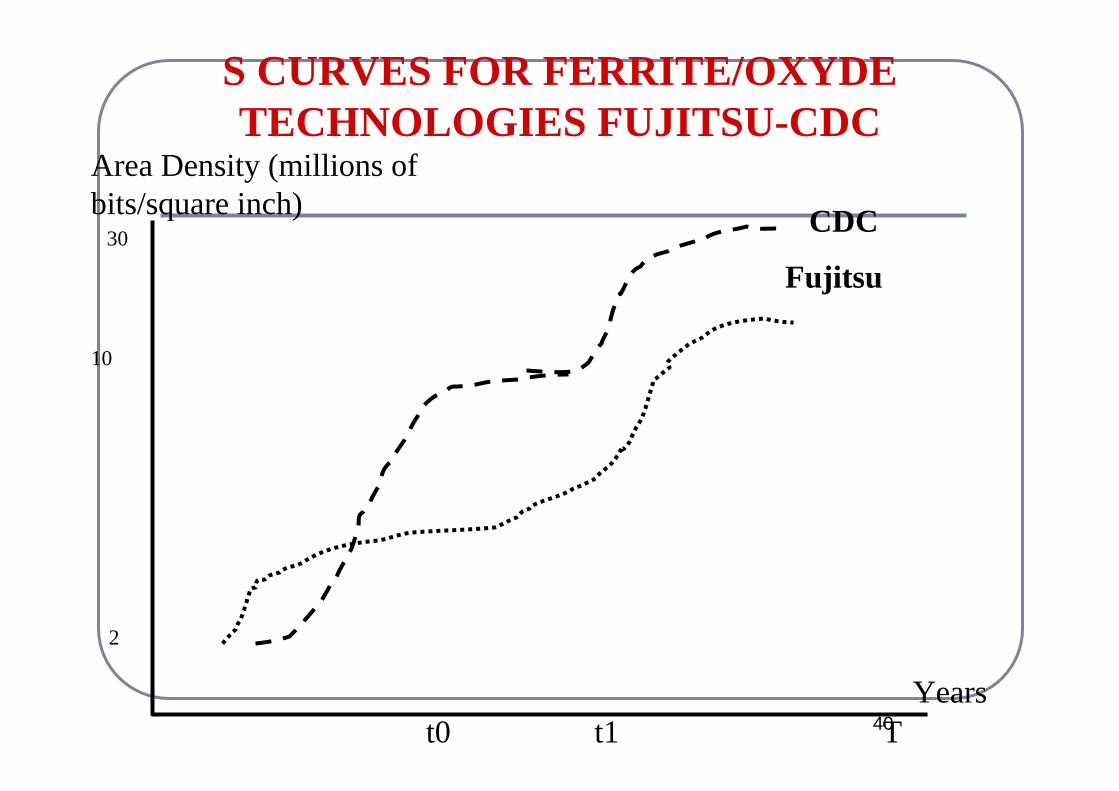

S CURVES FOR FERRITE/OXYDE TECHNOLOGIES FUJITSU-CDC

t0 t1 T

Area Density (millions of bits/square inch)

10

CDC

Fujitsu

Years

30

2

41

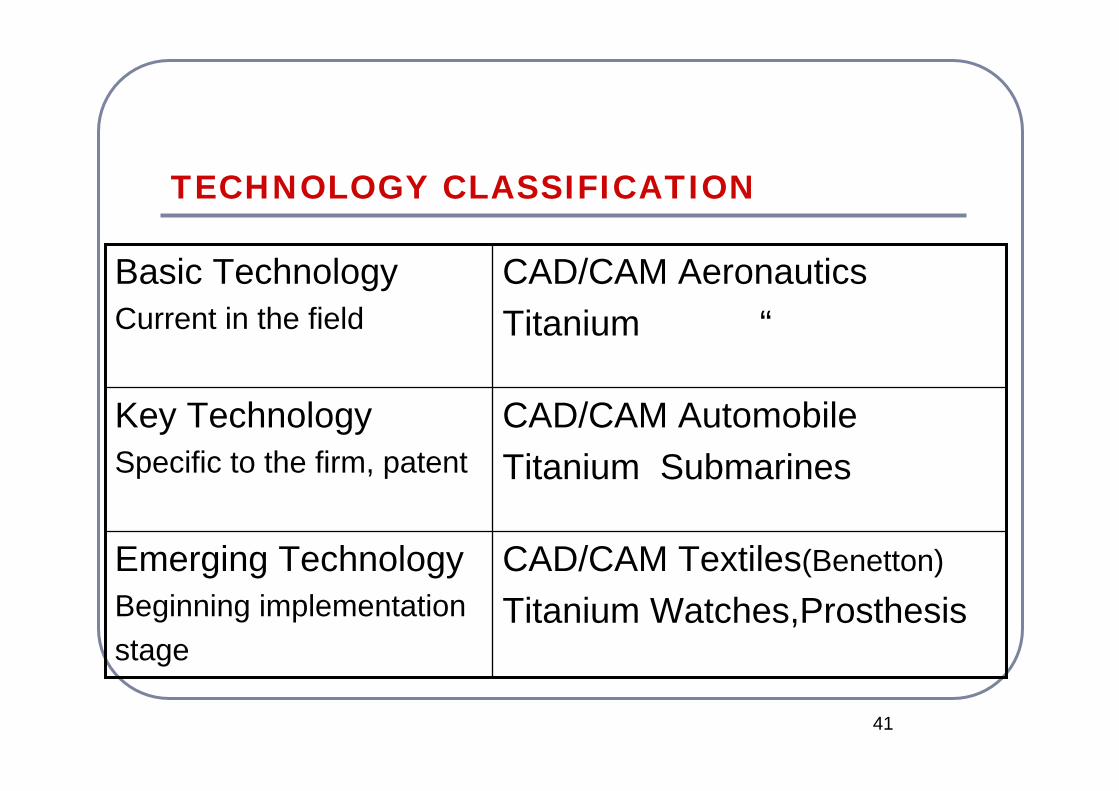

TECHNOLOGY CLASSIFICATION

CAD/CAM Textiles(Benetton)

Titanium Watches,ProsthesisEmerging TechnologyBeginning implementationstage

CAD/CAM AutomobileTitanium Submarines

Key TechnologySpecific to the firm, patent

CAD/CAM AeronauticsTitanium “

Basic TechnologyCurrent in the field

42

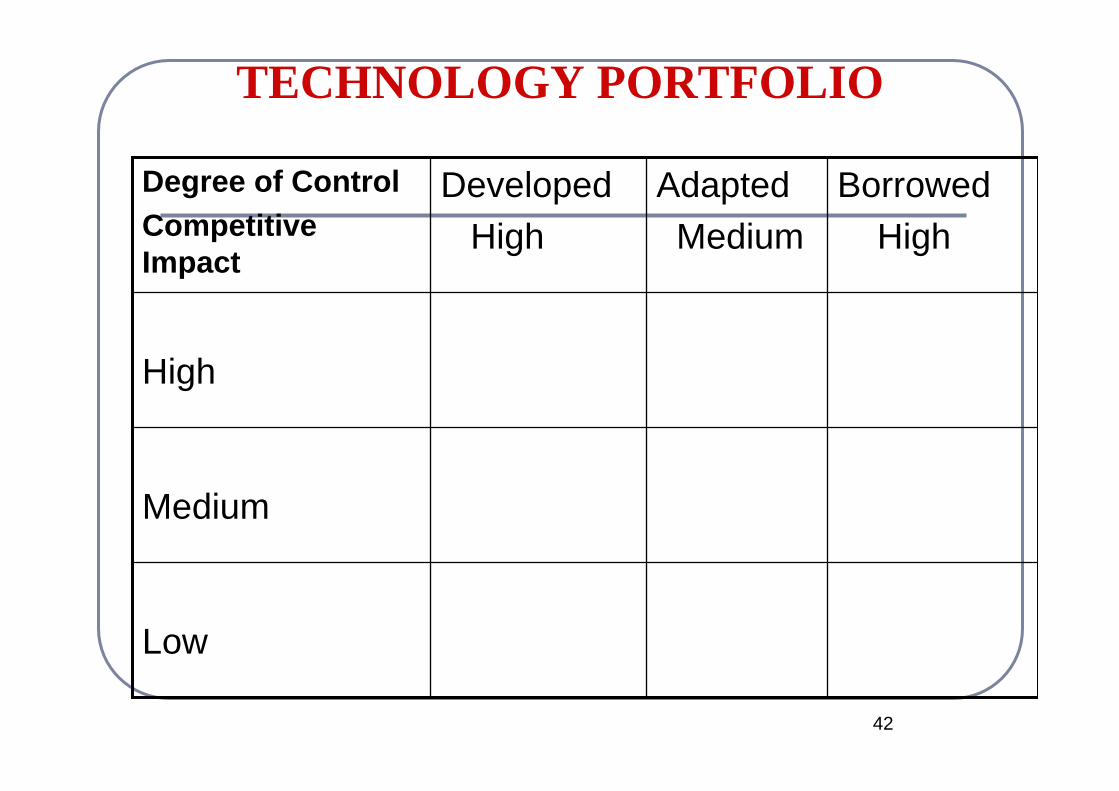

TECHNOLOGY PORTFOLIO

Low

Medium

High

BorrowedHigh

AdaptedMedium

DevelopedHigh

Degree of ControlCompetitive Impact

43

FROM MAINSTREAM MARKET TO MARKET/TECHNOLOGY INNOVATION AND BACK

Requested speed and total capacity to 8-12 disc drive : Control Data 3.5 inch Disc Drive: Conner and Quantum5.25 inch : Seagate, Tandon, Miniscribe8-12 inch using 5.25 and 3.5 inch architecture

44

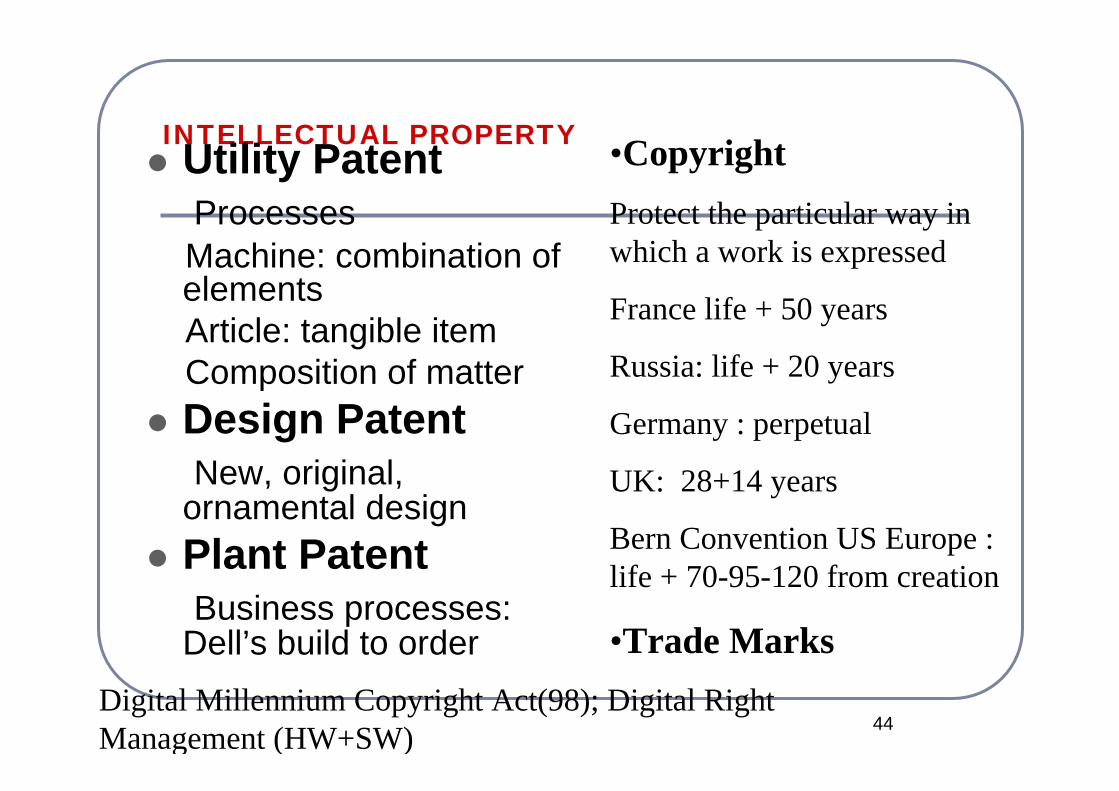

INTELLECTUAL PROPERTYUtility PatentProcessesMachine: combination of elements Article: tangible itemComposition of matterDesign PatentNew, original,

ornamental designPlant PatentBusiness processes:

Dell’s build to order

•CopyrightProtect the particular way in which a work is expressed

France life + 50 years

Russia: life + 20 years

Germany : perpetual

UK: 28+14 years

Bern Convention US Europe : life + 70-95-120 from creation

•Trade Marks Digital Millennium Copyright Act(98); Digital Right Management (HW+SW)

45

Easy of use benefit

Social-personal benefit

46

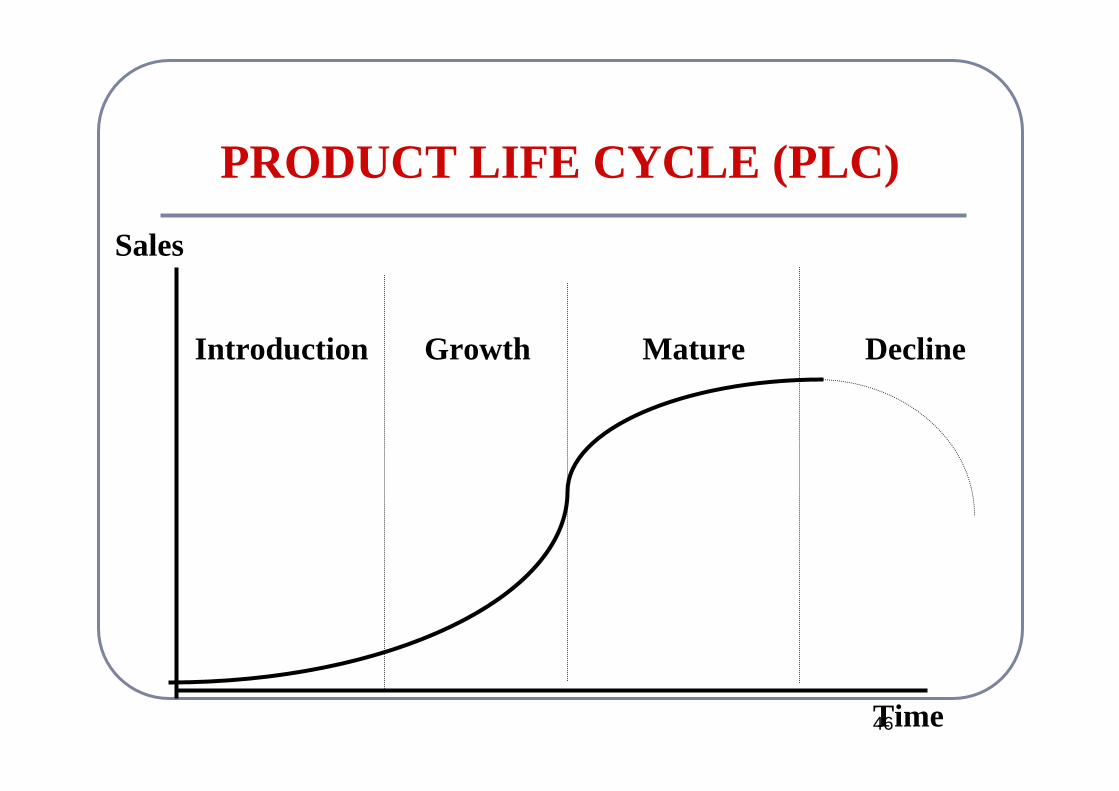

PRODUCT LIFE CYCLE (PLC)

Introduction Growth Mature Decline

Sales

Time

47

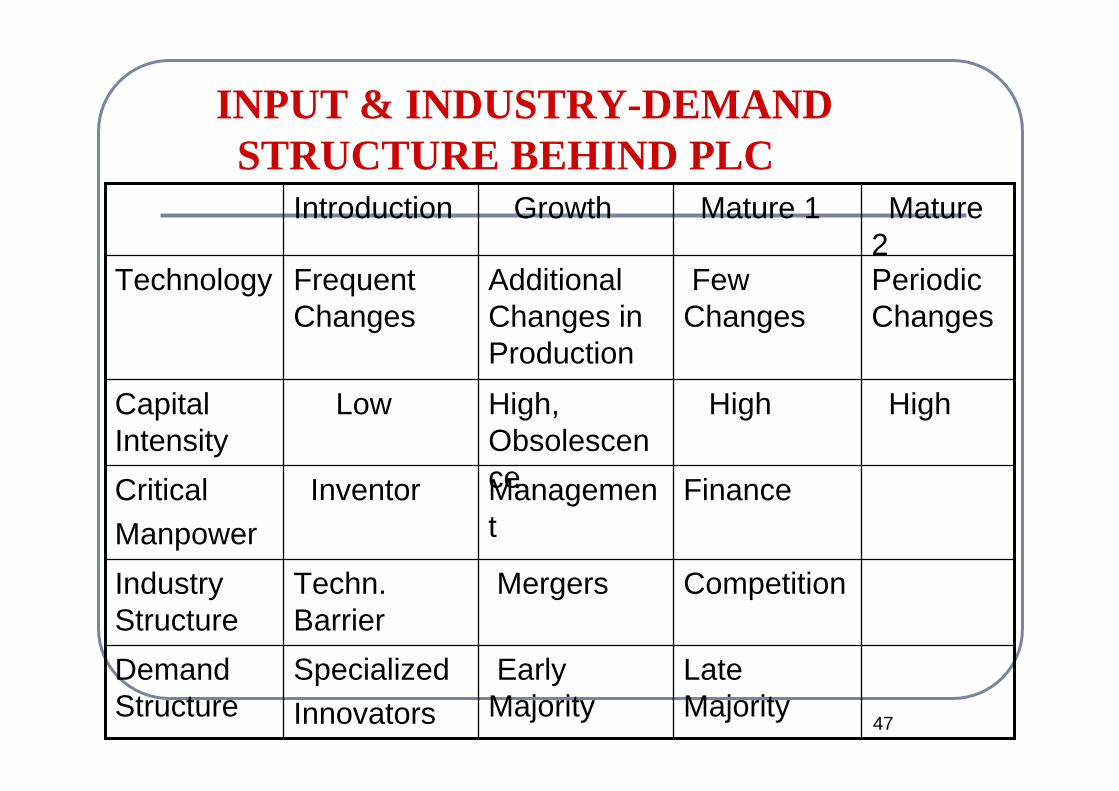

INPUT & INDUSTRY-DEMANDSTRUCTURE BEHIND PLC

Late Majority

Early Majority

SpecializedInnovators

Demand Structure

CompetitionMergersTechn. Barrier

Industry Structure

FinanceManagement

InventorCritical Manpower

HighHighHigh, Obsolescence

LowCapital Intensity

Periodic Changes

Few Changes

Additional Changes in Production

Frequent Changes

Technology

Mature 2

Mature 1GrowthIntroduction

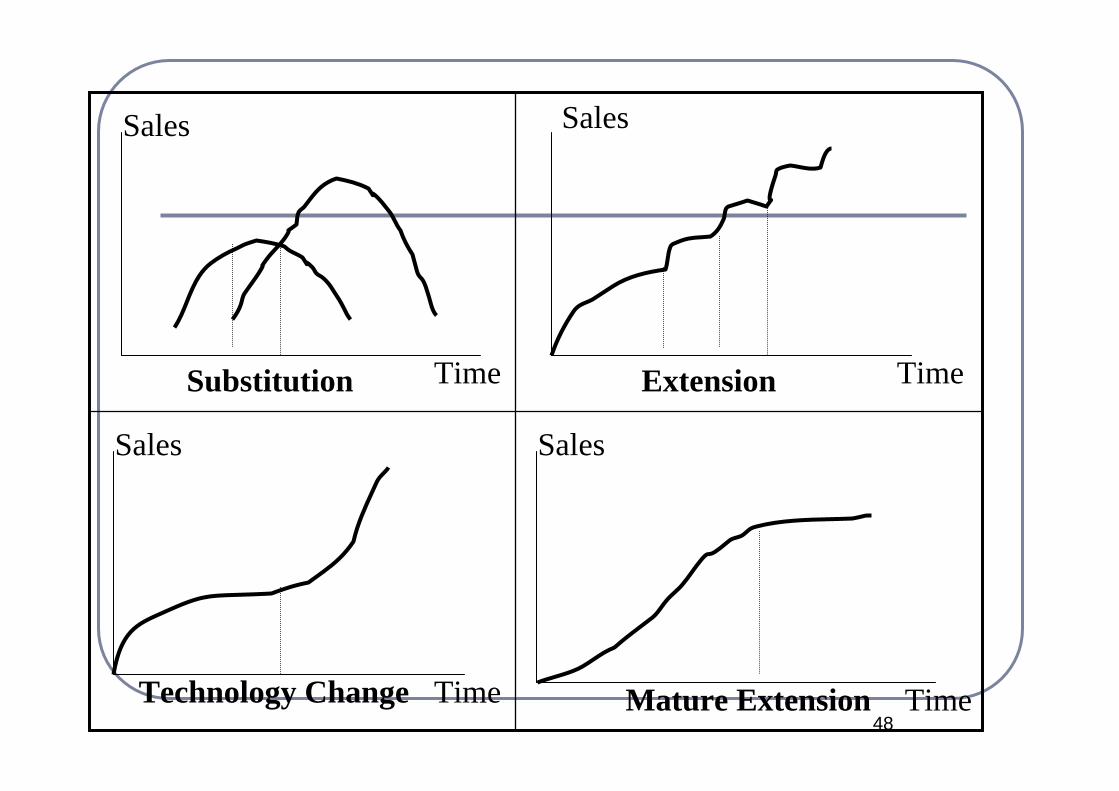

48

Sales

TimeSubstitution

Sales

TimeExtension

Sales

TimeTechnology Change

Sales

TimeMature Extension

49

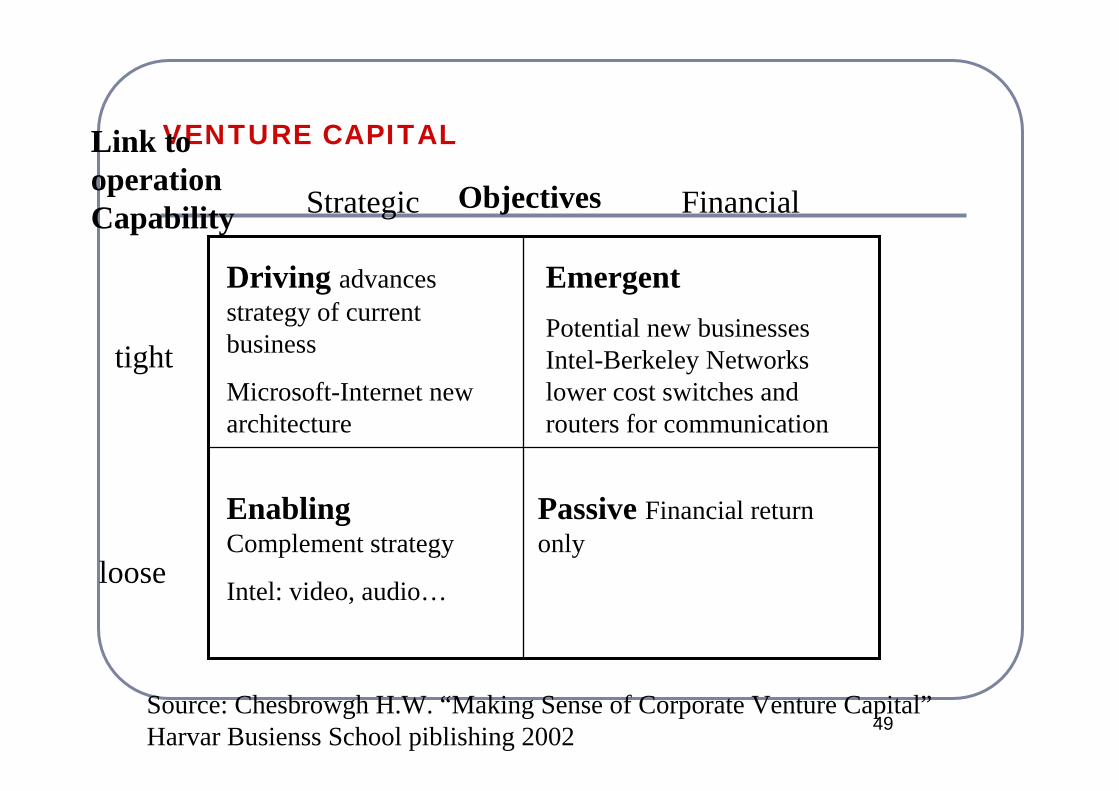

VENTURE CAPITAL

ObjectivesStrategic Financial

tight

loose

Link to operation Capability

Driving advances strategy of current business

Microsoft-Internet new architecture

Enabling Complement strategy

Intel: video, audio…

Emergent Potential new businesses Intel-Berkeley Networks lower cost switches and routers for communication

Passive Financial return only

Source: Chesbrowgh H.W. “Making Sense of Corporate Venture Capital”Harvar Busienss School piblishing 2002

50

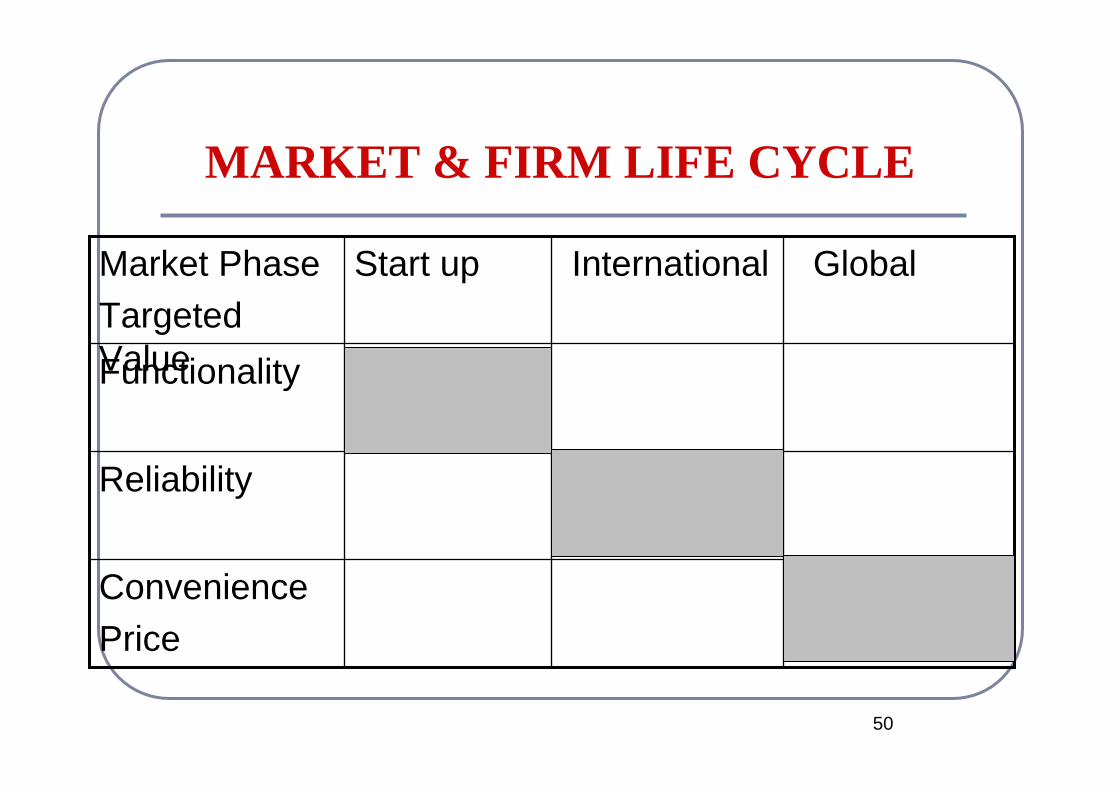

MARKET & FIRM LIFE CYCLE

ConveniencePrice

Reliability

Functionality

Global International Start upMarket PhaseTargeted Value

51

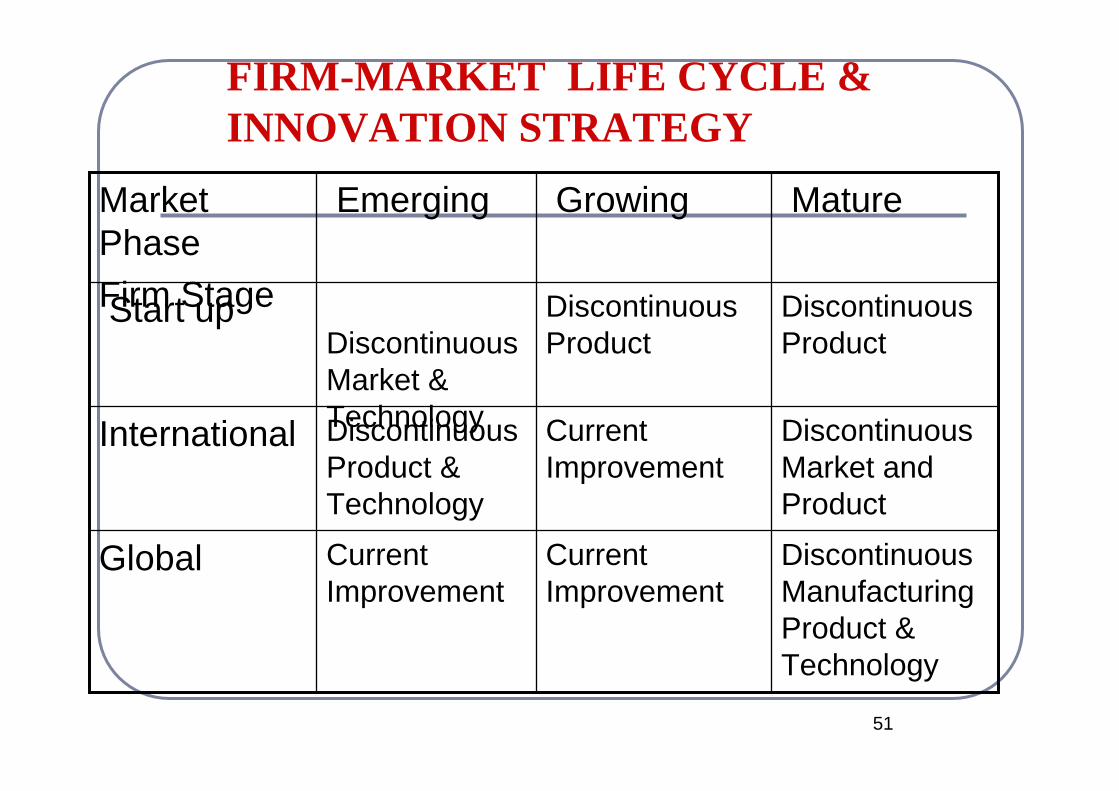

FIRM-MARKET LIFE CYCLE & INNOVATION STRATEGY

Discontinuous Manufacturing Product & Technology

Current Improvement

Current Improvement

Global

Discontinuous Market and Product

Current Improvement

Discontinuous Product & Technology

International

Discontinuous Product

Discontinuous ProductDiscontinuous

Market & Technology

Start up

MatureGrowingEmergingMarket PhaseFirm Stage

52

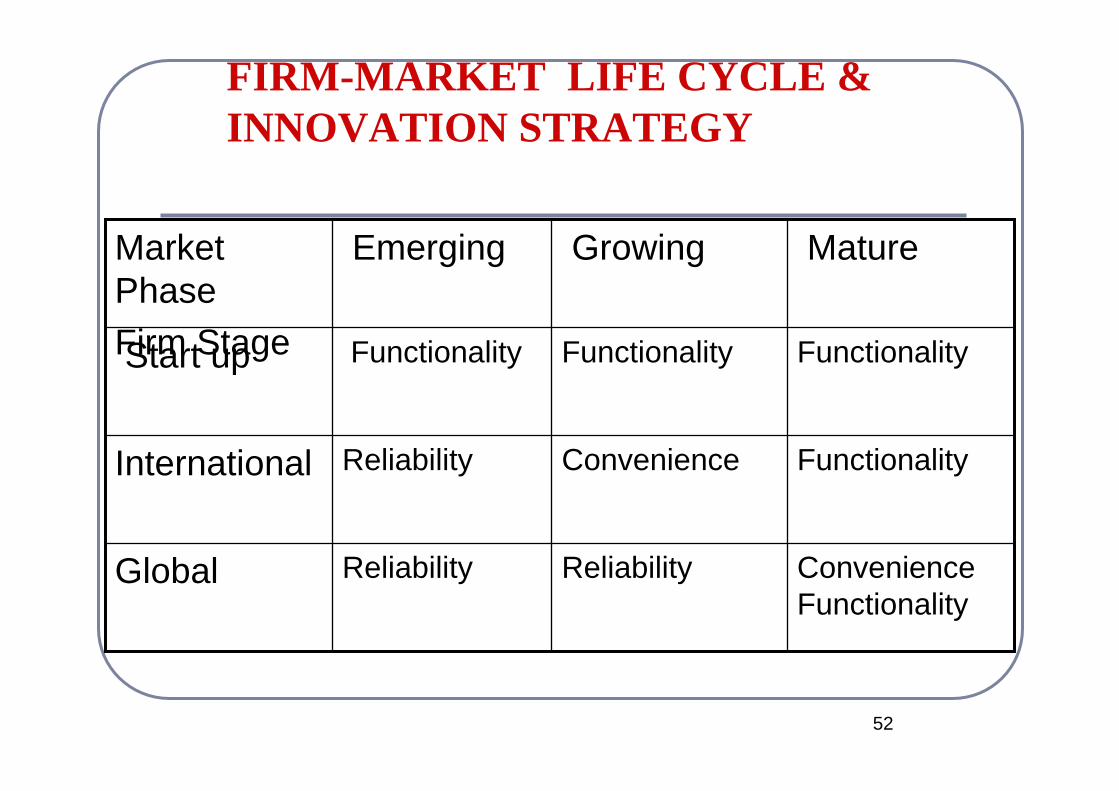

FIRM-MARKET LIFE CYCLE & INNOVATION STRATEGY

Convenience Functionality

ReliabilityReliabilityGlobal

FunctionalityConvenienceReliabilityInternational

FunctionalityFunctionalityFunctionalityStart up

MatureGrowingEmergingMarket PhaseFirm Stage

53

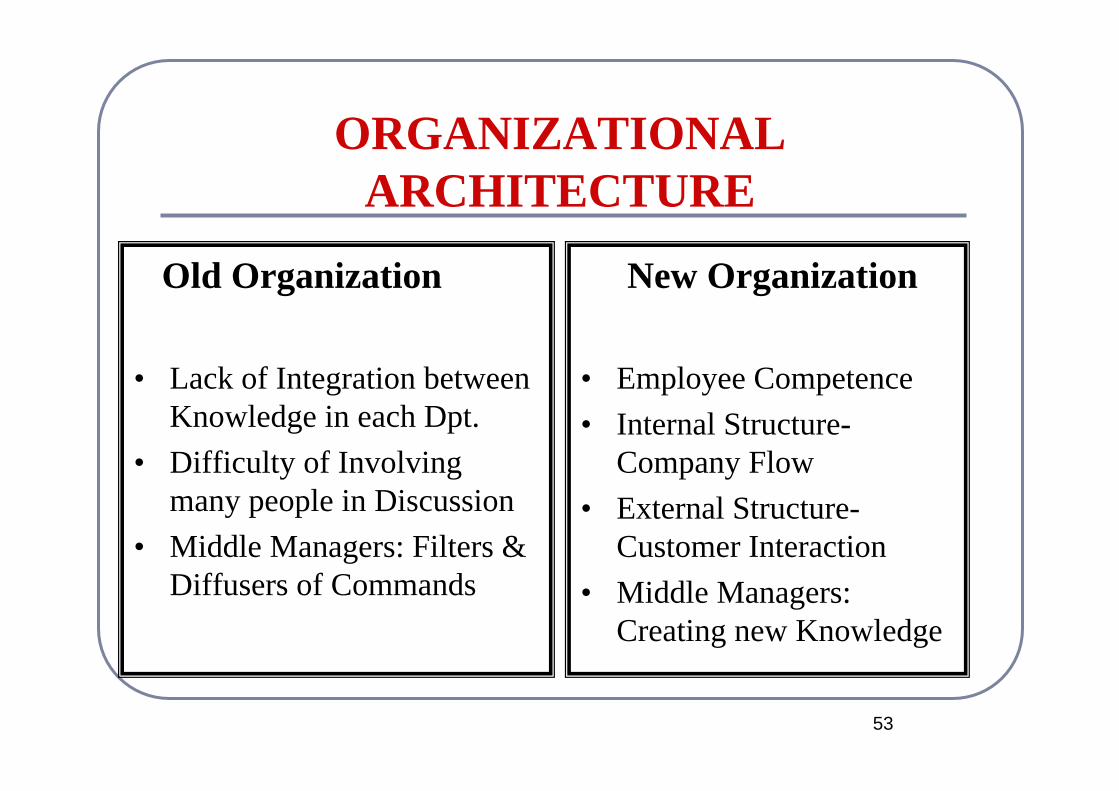

ORGANIZATIONAL ARCHITECTURE

Old Organization

• Lack of Integration between Knowledge in each Dpt.

• Difficulty of Involving many people in Discussion

• Middle Managers: Filters & Diffusers of Commands

New Organization

• Employee Competence• Internal Structure-

Company Flow• External Structure-

Customer Interaction• Middle Managers:

Creating new Knowledge

54

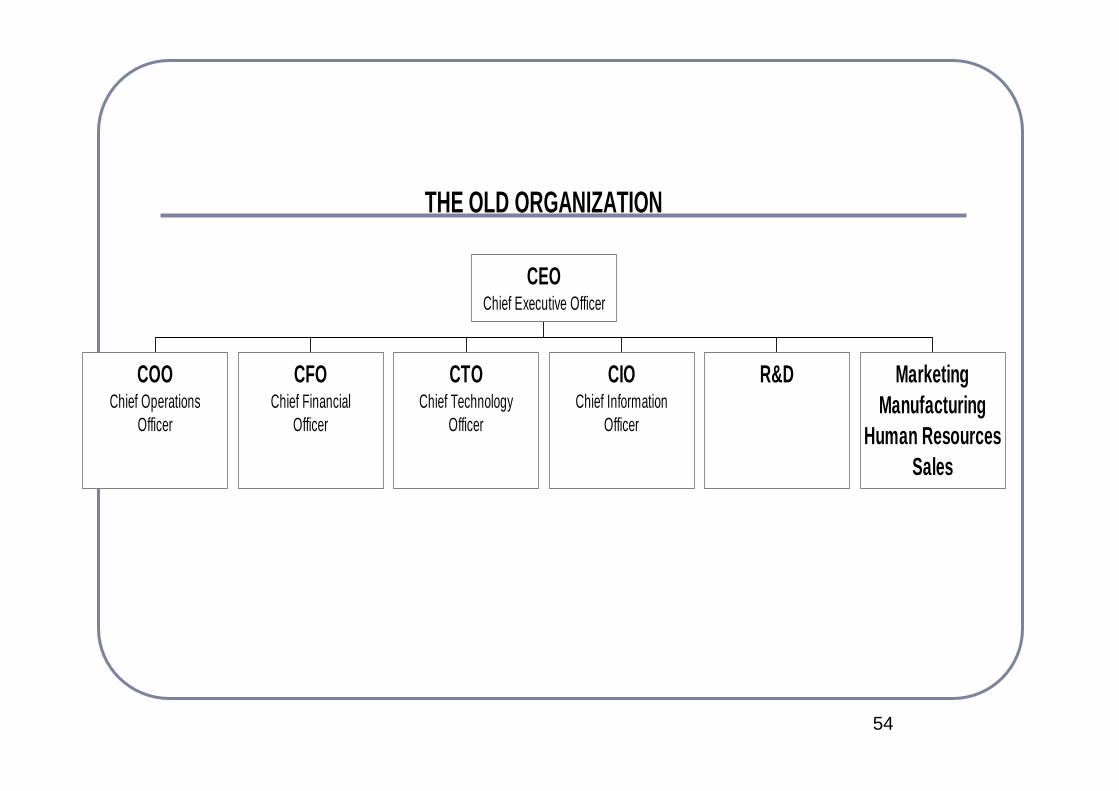

THE OLD ORGANIZATION

COOChief Operations

Officer

CFOChief Financial

Officer

CTOChief Technology

Officer

CIOChief Information

Officer

R&D MarketingManufacturing

Human ResourcesSales

CEOChief Executive Officer

55

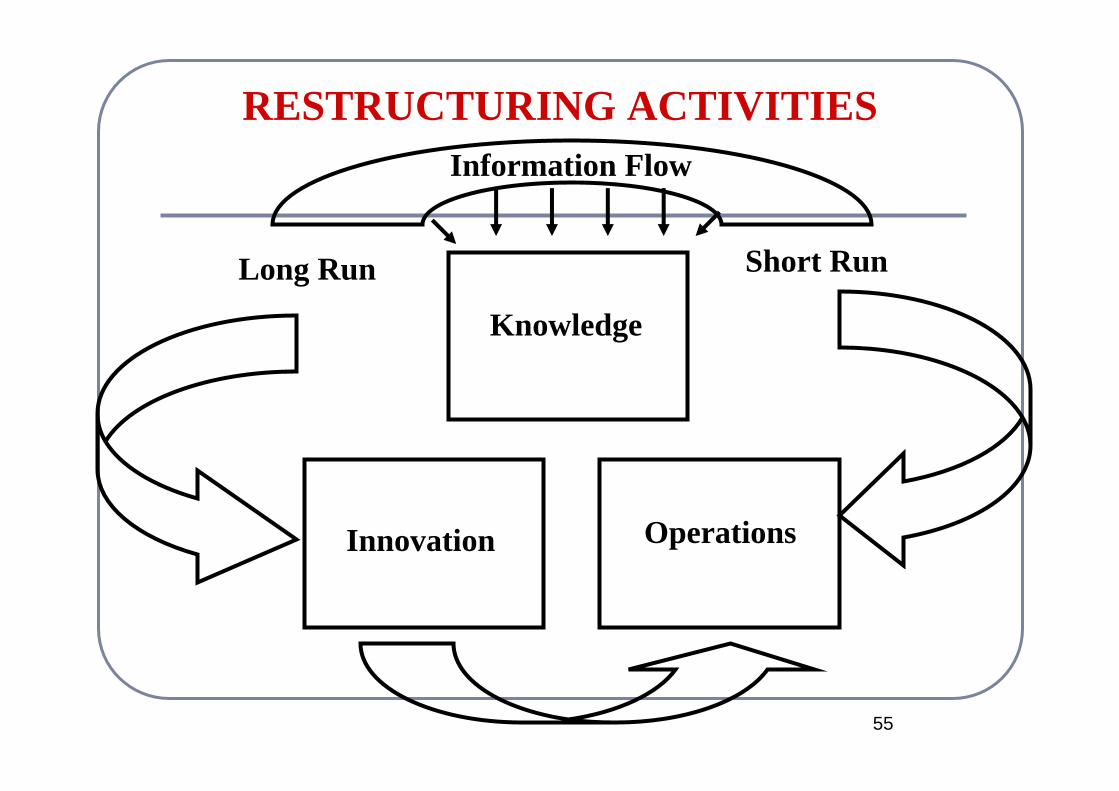

RESTRUCTURING ACTIVITIES

Innovation

Knowledge

Operations

Information Flow

Short RunLong Run

56

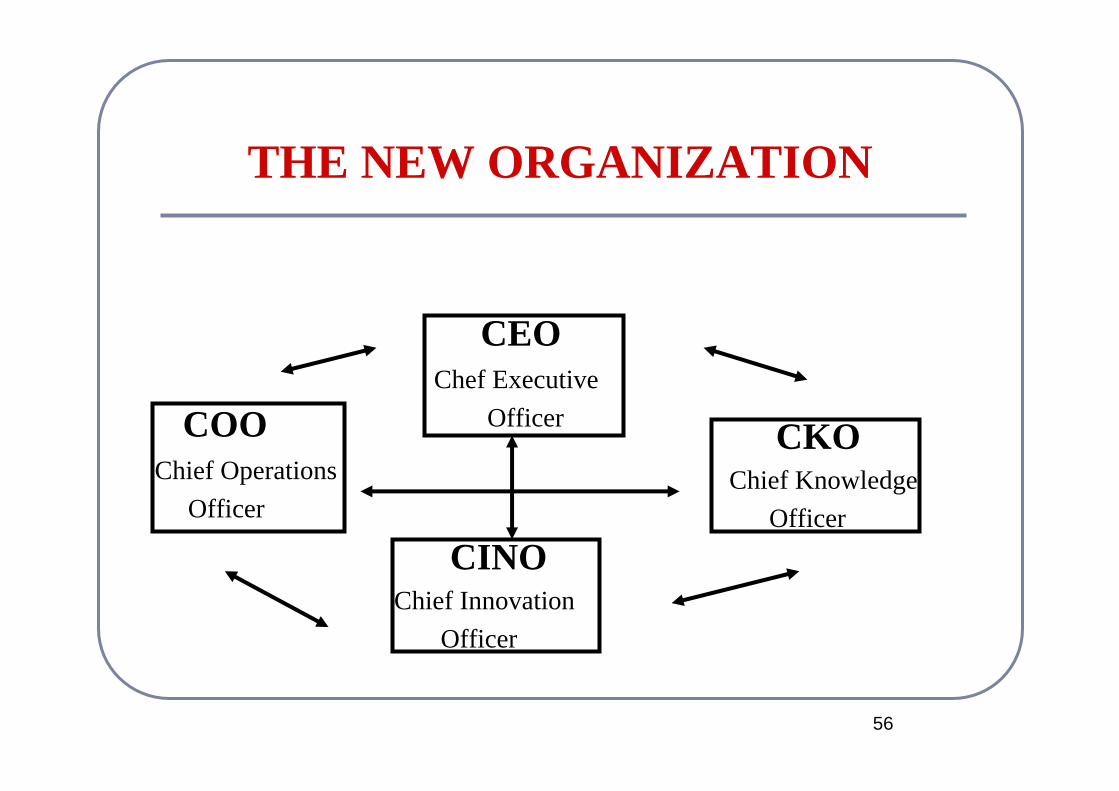

THE NEW ORGANIZATION

CEOChef Executive

Officer CKOChief Knowledge

OfficerCINO

Chief InnovationOfficer

COOChief Operations

Officer

57

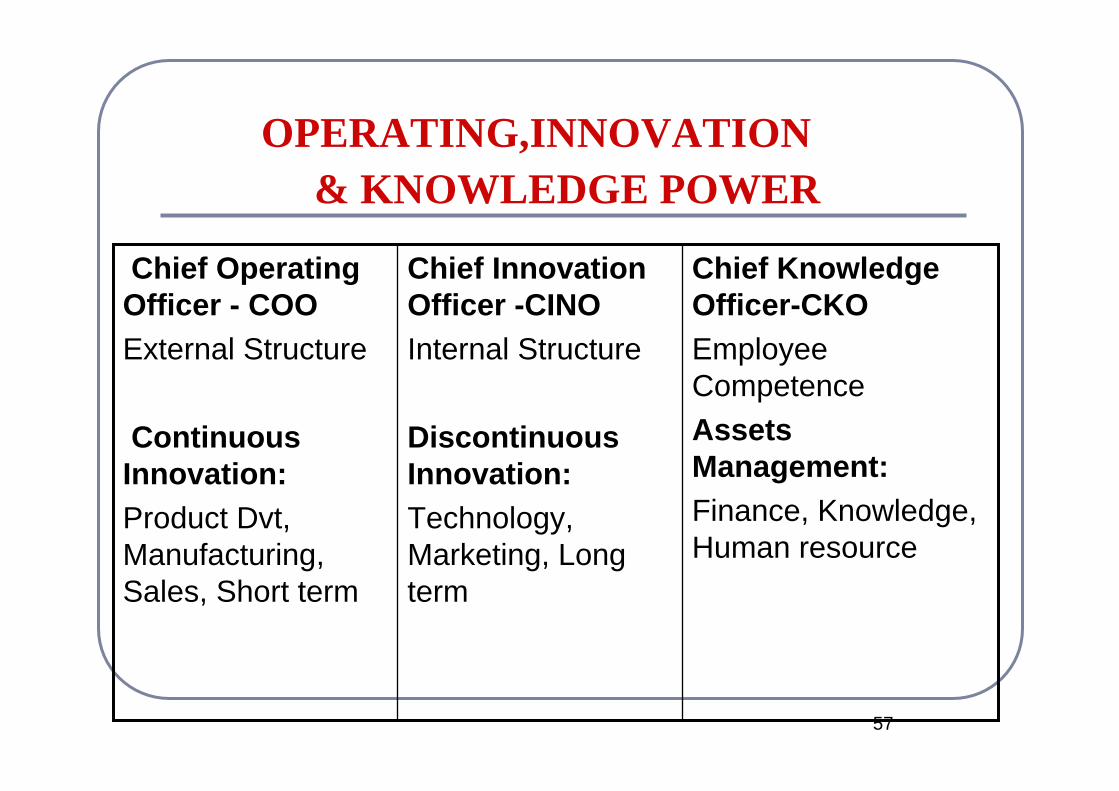

OPERATING,INNOVATION & KNOWLEDGE POWER

Chief Knowledge Officer-CKOEmployee CompetenceAssets Management:Finance, Knowledge, Human resource

Chief Innovation Officer -CINOInternal Structure

Discontinuous Innovation:Technology, Marketing, Long term

Chief Operating Officer - COOExternal Structure

Continuous Innovation:Product Dvt, Manufacturing, Sales, Short term