Karishma Pharma Machines/ Karishma International, Mumbai, Vibro Sifter

Upload

ca-karishmaCategory

view

516download

0

APPLICABLE FOR MAY 2015/NOV 2015

G K M AL I K &

AS S O C I AT E S C h a r t e r e d

Ac c o u n t a n t s

FINANCE ACT 2014

CA KARISHMA

www.cakarishma.co

m

TAX RATES

AMENDMENTS

BASIC EXEMPTION LIMIT 250000/300000/500000

SURCHARGE & MARGINALRELIEF

Same (10% if net income exceeds 1crore)

REBATE u/s 87A Same (Rs 2000- Resident Individual if NI does not exceed 5Lakhs)

GK MALIK & ASSOCIATES CA KARISHMA

Chartered Accountants www.cakarishma.co

m

INCOME FROM HOUSE PROPERTY

GK MALIK & ASSOCIATES Chartered Accountants

24(b) OLD NEW

INTEREST ON

BORROWEDCAPITAL

150000 200000

Q1.Mr. Rajesh purchased a residential house property for self-occupationat a cost of ` 30 lakh on 1.6.2013 in respect of which he took a housingloan of ` 24 lakh from Punjab National bank @ 11% p.a. on the samedate. Compute the eligible deduction in respect of interest on housingloan for A.Y. 2014-15 and A.Y.2015-16 under the provisions of the Income-tax Act, 1961, assuming that the entire loan was outstanding as on31.3.2015 and he does not own any other house property.

www.cakarishma.co

m

PROFITS AND GAINS OF BUSINESS OR PROFESSION

GK MALIK & ASSOCIATES Chartered Accountants

PARTICULARS OLD NEW

Investment

Allowance to a

Manufacturing

Company

DEDUCTION: 15%

32AC(1) 32AC(1A)

1-4-2013 to 31-03-2015

1-4-2014 to 31-03-2017

Invest more than

100 crores in new

plant and machinery

Invest more than

25 crores in new

plant and machinerywww.cakarishma.co

m

PRACTICAL QUESTION

GK MALIK & ASSOCIATES Chartered Accountants

Q2. Compute the admissible deduction under section 32AC for A.Y. 2014-15 & A.Y. 2015-16 in each of the following cases

Manufacturing

company

Investment in new plant and

machinery

(` in crores)

P.Y.2013-14 P.Y. 2014-15

A Ltd. 80 22

B Ltd. 70 25

C Ltd. 60 30

D Ltd. 75 25

E Ltd. 105 15

F Ltd. 70 30

G Ltd. 70 40www.cakarishma.co

m

CAPITAL EXPENDITURE ON SPECIFIED BUSINESS

GK MALIK & ASSOCIATES Chartered Accountants

1. Two new businesses included

Laying and operating a slurry pipeline for the transportation of iron ore.

Setting up and operating a semiconductor wafer fabrication manufacturing unit.

2. Capital asset claimed must be used for “specified business” for a period of eight years

www.cakarishma.co

m

PROFITS AND GAINS OF BUSINESS OR PROFESSION

GK MALIK & ASSOCIATES Chartered Accountants

SECTION OLD NEW

37(1) General Deduction

CSR expenditure allowed

Disallowed

40(a)(i)

Disallowance of

expenditure – Non resident

Disallowed if Tax

deducted was not

paid before the end PY

Disallowed if Tax

deducted was not

paid before the duedate of ROI

40(a)(ia)

Disallowance of

expenditure –Resident

100 % Disallowed 30% Disallowed

44AE Presumptive Income

HGV-5000 p.mOGV-4500 p.m

Any vehicle 7500 p.m

www.cakarishma.co

m

GK MALIK & ASSOCIATES Chartered Accountants

Q3. XYZ Ltd. made the following payments in the month of March 2015 to residents without deduction of tax at source. What would be the tax consequence for A.Y. 2015-16, assuming that the resident payees in all the cases mentioned below, have not paid the tax, if any, which was required to be deducted by XYZ Ltd?

Salary to its employees 1500000

Non-compete fees to Mr. X 70000

Directors’ remuneration 25000

Would your answer change if XYZ Ltd. has deducted tax on the above in April, 2015 from subsequent payments made to these persons and remitted the same in July, 2015?

PRACTICAL QUESTION

www.cakarishma.co

m

PRACTICAL QUESTION

GK MALIK & ASSOCIATES Chartered Accountants

Q4. Mr. X commenced the business of operating goods vehicles on 1.4.2014. He purchased the following vehicles during the

P/Y 2014-15. Compute his income u/s 44AE for A/Y 2015-16.Type of Vehicle Number Date of

purchase

Light Goods Vehicles

2 10-3-15

1 15-3-15

Medium Goods Vehicles

3 16-7-14

1 2-1-15

Heavy Goods Vehicles

2 29-8-14

1 23-3-15 www.cakarishma.co

m

CAPITAL GAINS

GK MALIK & ASSOCIATES Chartered Accountants

SECTION OLD NEW

54 & 54F Investment in “a residential house”

Investment in one residential house situated in India

54EC Restricts the

investment during

any financial year to 50 lakh

Restricts the investment

during Relevant PY& subsequent PY to 50 lakh

2(42A) Definition of STCA

HP <=36M Othersunlisted securities

Others

Unlisted securities

Unlisted sharesUnits of Debt oriented MF

HP <=12M Shares

Listed Securities

Listed shares

Listed Securities

www.cakarishma.co

m

TAX TREATMENT OF MF

GK MALIK & ASSOCIATES Chartered Accountants

TYPE OF MF HOLDING PERIOD TAX TREATMENT

DEBT OREINTED MF

STCA <=36M Tax at normal rates

LTCA >36M Tax at 20% with Indexation

EQUITY OREINTED MF

STCA <=12M 111A @15%

LTCA >12M

If STT is paid Exempt u/s 10(38)

If STT is not paid Option1: Indexation

+20%

Option2: www.cakarishma.co

m

PRACTICAL QUESTION

GK MALIK & ASSOCIATES Chartered Accountants

Q5. Mr. Ram working as a CEO with ABC Ltd., furnishes the following particulars of assets transferred by him during the P.Y. 2014-15

Particulars Date oftransfer

Rs.

1 A residential house in Bangalore which

he had purchased in February, 2000 at a cost of Rs.15,56,000

13/01/15 14500000

2 Listed shares of Indian companies

purchased in May 2012 at cost of Rs.1 Lakh

14/02/15 20000

3 Unlisted shares purchased in May 2012 at cost of Rs.50,000

14/02/15 75000

4 Units of equity oriented fund purchased in May 2012 at a cost of Rs.30,000

14/02/15 65000

5 Units of debt oriented fund purchased in January 2010 at a cost of Rs.31,600

14/02/15 75,000www.cakarishma.co

m

PRACTICAL QUESTION

GK MALIK & ASSOCIATES Chartered Accountants

Mr. Ram made the following investments, out of the capital gains arising on sale of residential house.

Purchased a residential flat in Pune on 21/5/2015 3500000

Purchased a residential flat in Madurai on 14/7/2015 2500000

3 years bonds of NHAI on 20/3/2015 4000000

3 years bonds of RECL on 15/5/2015 3000000

Compute the total income and tax liability of Mr. Ram for A.Y. 2015-16, if his salary income(computed) is Rs.24 lakh and interest on fixed deposits with banks is Rs.1 lakh. Assume that he has contributed Rs.1,50,000 to PPF and paid medical insurance premium of Rs.12,000 to insure his health.Cost Inflation Index of F.Y. 1999-2000: 389; F.Y.2009-10: 632; F.Y.2012-13: 852; F.Y.2014-15: 1024

www.cakarishma.co

m

IFOS

GK MALIK & ASSOCIATES Chartered Accountants

PARTICULARS OLD NEW

Advance forfeited

for transfer of a capital asset

If any amount was

forfeited upto

31.3.2014 then it

shall be deducted

from the cost of

acquisition as per

old sec. 51.

Advance forfeited

due to failure of

negotiations for

transfer of a

capital asset to be

taxable as

“Income from

other sources”

[Section 56(2)]

www.cakarishma.co

m

DEDUCTIONS

GK MALIK & ASSOCIATES Chartered Accountants

Section Particulars Ceiling limit (`)

80C Investment in specifiedinstruments

1,50,000

80CCC Contribution to certainpension funds

1,00,000

80CCD(1) Contribution to new

pension scheme ofGovernment

1,00,000

80CCE Aggregate deduction

under section 80C,80CCC & 80CCD (1)

1,50,000

www.cakarishma.co

m

PRACTICAL QUESTION

GK MALIK & ASSOCIATES Chartered Accountants

1.Mr. X invested 1,20,000 in pension plan of insurance company. How much deduction he can claim u/c VI-A?

2.Mr. Y invested total 1,20,000 in NPS. How much deduction he can claim u/c VI-A?

3.Mr. Z invested total 1,20,000 in PPF+NSC+LIP. How much deduction he can claim u/c VI-A?

4.Mr. A invested total 1,20,000 in Pension plan of insurance company and 40,000 in PPF. How much deduction he can claim u/c VI-A?

www.cakarishma.co

m

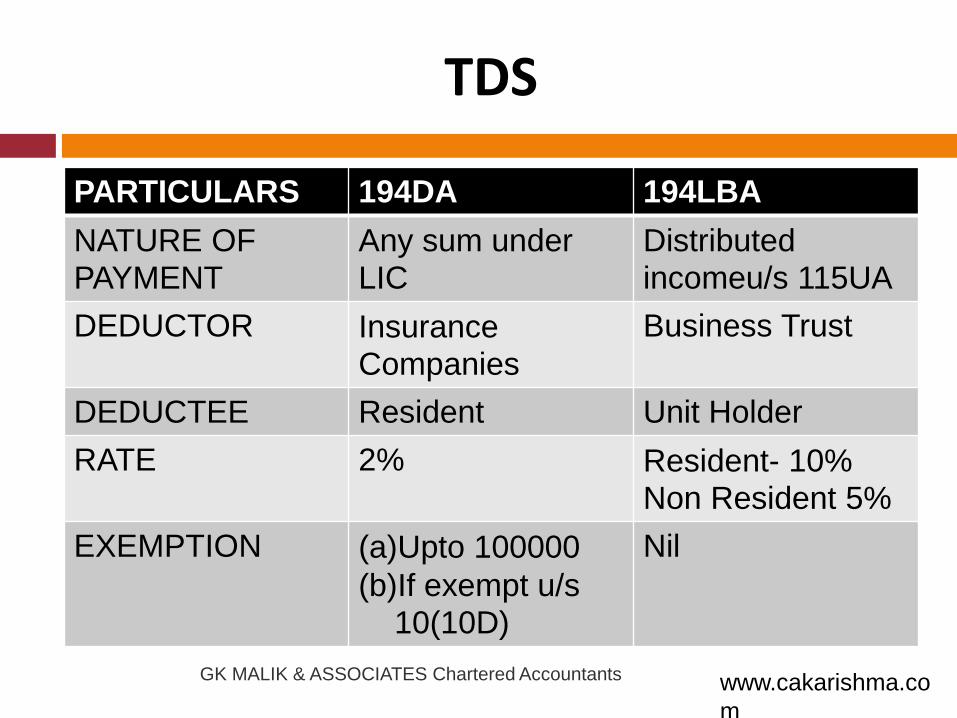

TDS

GK MALIK & ASSOCIATES Chartered Accountants

PARTICULARS 194DA 194LBA

NATURE OF PAYMENT

Any sum under LIC

Distributed incomeu/s 115UA

DEDUCTOR Insurance Companies

Business Trust

DEDUCTEE Resident Unit Holder

RATE 2% Resident- 10%Non Resident 5%

EXEMPTION (a)Upto 100000

(b)If exempt u/s 10(10D)

Nil

www.cakarishma.co

m

PRACTICAL QUESTION

GK MALIK & ASSOCIATES Chartered Accountants

Examine the applicability of the provisions for tax deduction at source under section 194DA in the above cases -

(i) Mr. X, a resident, is due to receive ` 4.50 lakhs on 31.3.2015, towards maturity proceeds of LIC policy taken on 1.4.2012, for which the sum assured is ` 4 lakhs and the annual premium is ` 1,25,000.

(ii) Mr. Y, a resident, is due to receive ` 2.20 lakhs on 31.3.2015 on LIC policy taken on 1.4.2010, for which the sum assured is ` 2 lakhs and the annual premium is ` 35,000.

(iii) Mr. Z, a resident, is due to receive ` 95,000 on 1.10.2014 towards maturity proceeds of LIC policy taken on 1.10.2010 for which the sum assured is ` 90,000 and the annual premium was ` 19,000.

www.cakarishma.co

m

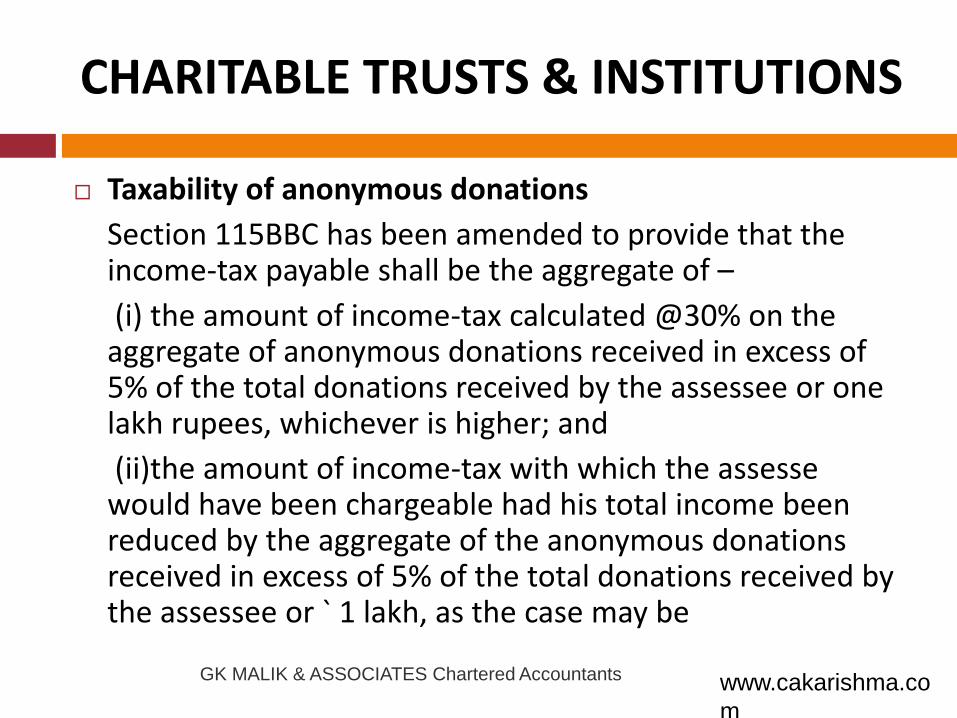

CHARITABLE TRUSTS & INSTITUTIONS

GK MALIK & ASSOCIATES Chartered Accountants

Taxability of anonymous donations

Section 115BBC has been amended to provide that the income-tax payable shall be the aggregate of –

(i) the amount of income-tax calculated @30% on the aggregate of anonymous donations received in excess of 5% of the total donations received by the assessee or one lakh rupees, whichever is higher; and

(ii)the amount of income-tax with which the assessewould have been chargeable had his total income been reduced by the aggregate of the anonymous donations received in excess of 5% of the total donations received by the assessee or ` 1 lakh, as the case may be

www.cakarishma.co

m

PRACTICAL QUESTION

GK MALIK & ASSOCIATES Chartered Accountants

Income from property held under trust is ` 6 lakh. The voluntary contributions received by a trust is ` 20 lakh, which includes anonymous donations of ` 4 lakh and corpus donations of ` 5 lakh. The trust has applied ` 10 lakh to purchase a building on 1.8.2014 for meeting its objective. Compute the tax liability of the trust for A.Y.2015-16.

www.cakarishma.co

m

THANK YOU

G K M AL I K &

AS S O C I AT E S C h a r t e r e d

Ac c o u n t a n t swww.cakarishma.co

m