Direct Capitalization

14

1 The Student Handbook to THE APPRAISAL OF REAL ESTATE Chapter 22 Direct Capitalization

-

Upload

lucas-haynes -

Category

Documents

-

view

61 -

download

1

description

Chapter 22. Direct Capitalization. Capitalization Rates The ratio of the sale price to the expected net income for the next year May be extracted from comparable sales Other methods can be used to support capitalization rate Estimating the Overall Capitalization Rate - PowerPoint PPT Presentation

Transcript of Direct Capitalization

1

The Student Handbook toTHE APPRAISAL OF REAL ESTATE

Chapter 22

Direct Capitalization

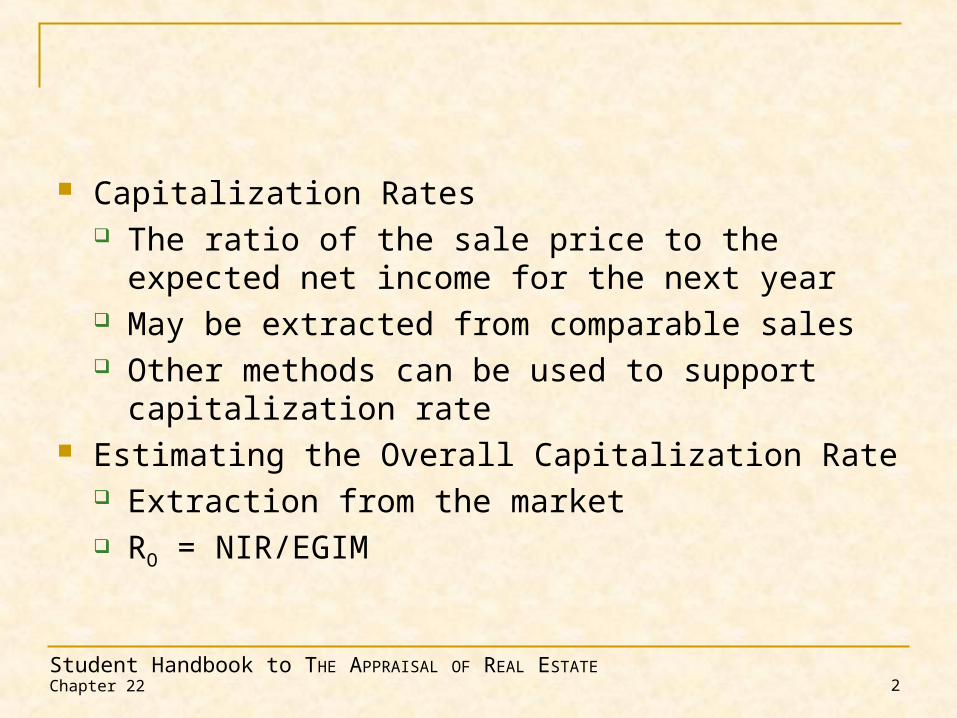

Chapter 22 2Student Handbook to THE APPRAISAL OF REAL ESTATE

Capitalization Rates The ratio of the sale price to the expected net

income for the next year May be extracted from comparable sales Other methods can be used to support

capitalization rate Estimating the Overall Capitalization Rate

Extraction from the market RO = NIR/EGIM

Chapter 22 3Student Handbook to THE APPRAISAL OF REAL ESTATE

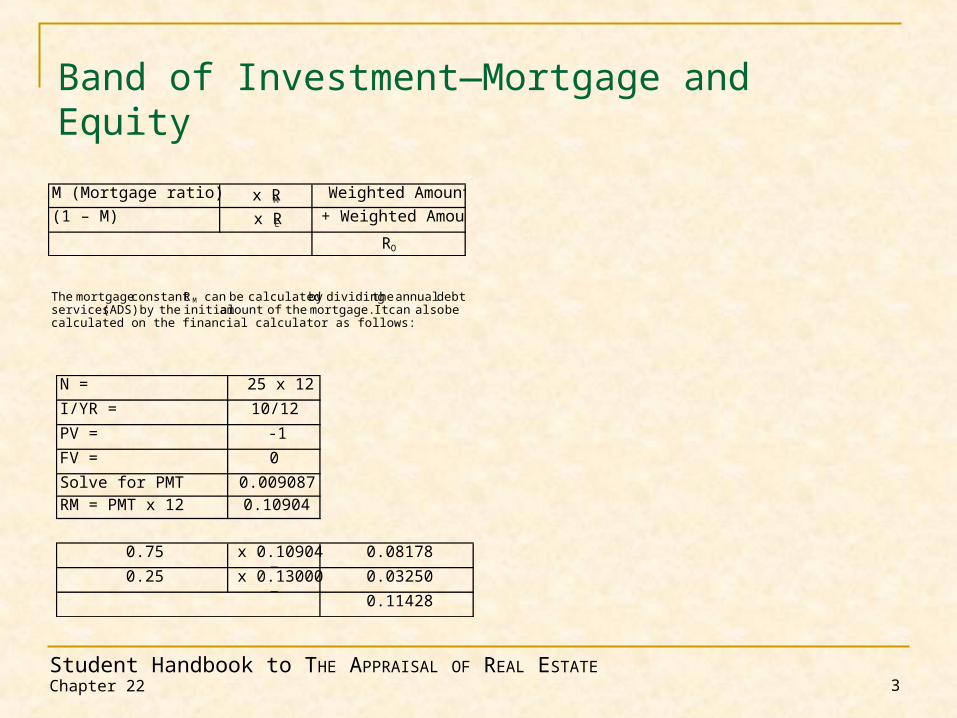

Band of Investment—Mortgage and Equity

M (Mortgage ratio) x RM Weighted Amount

(1 – M) x RE + Weighted Amount

RO

The mortgageconstantRM can be calculatedby dividingthe annualdebtservices (ADS) by the initial amountof the mortgage. It can also becalculated on the financial calculator as follows:

N = 25 x 12

I/YR = 10/12

PV = -1

FV = 0

Solve for PMT 0.009087RM = PMT x 12 0.10904

0.75 x 0.10904 =

0.08178

0.25 x 0.13000 =

0.03250

0.11428

Chapter 22 4Student Handbook to THE APPRAISAL OF REAL ESTATE

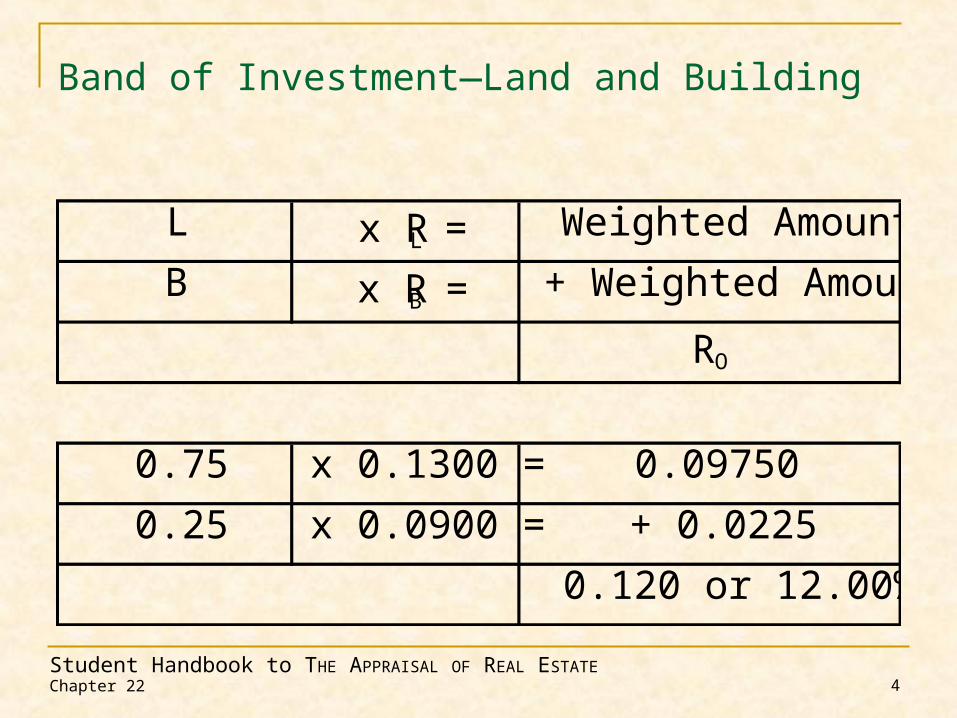

Band of Investment—Land and Building

L x RL = Weighted Amount

B x RB = + Weighted Amount

RO

0.75 x 0.1300 = 0.09750

0.25 x 0.0900 = + 0.0225

0.120 or 12.00%

Chapter 22 5Student Handbook to THE APPRAISAL OF REAL ESTATE

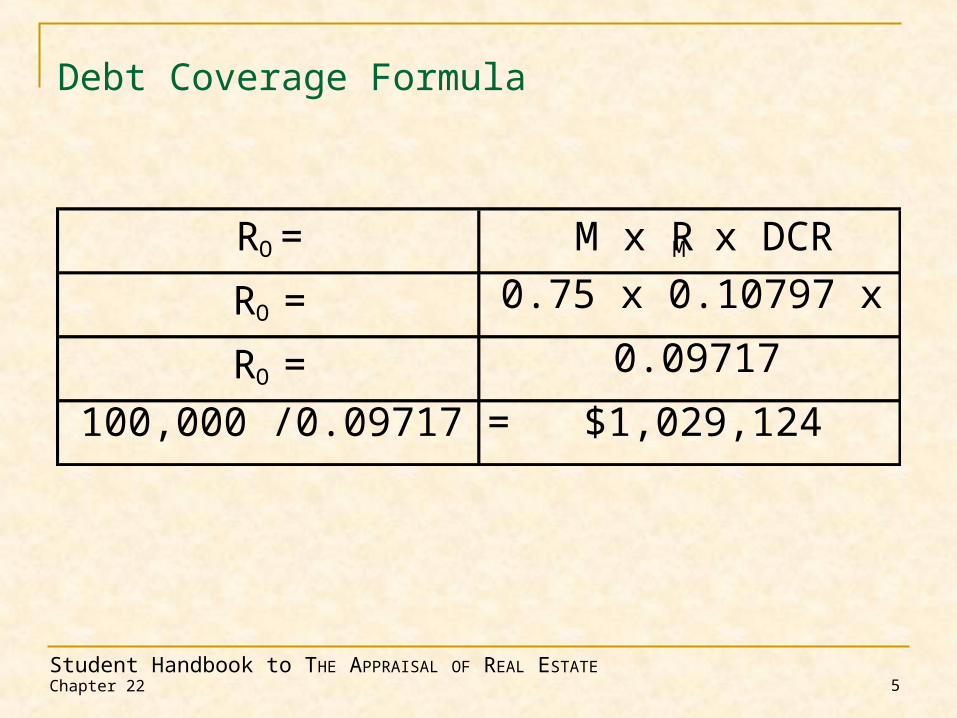

Debt Coverage Formula

RO = M x RM x DCR

RO = 0.75 x 0.10797 x 1.2

RO = 0.09717

100,000 /0.09717 = $1,029,124

Chapter 22 6Student Handbook to THE APPRAISAL OF REAL ESTATE

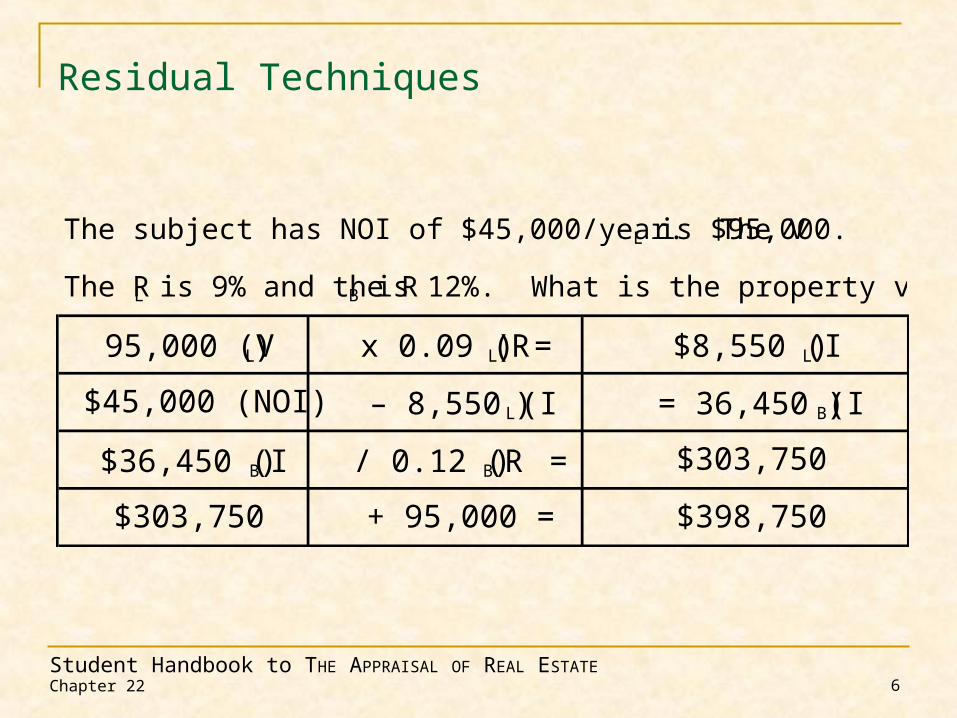

Residual Techniques

The subject has NOI of $45,000/year. The VL is $95,000.

95,000 (VL) x 0.09 (RL) = $8,550 (IL)

$45,000 (NOI) – 8,550 (IL) = 36,450 (IB)

$36,450 (IB) / 0.12 (RB) = $303,750

$303,750 + 95,000 = $398,750

The RL is 9% and the RB is 12%. What is the property value?

Chapter 22 7Student Handbook to THE APPRAISAL OF REAL ESTATE

Gross Income Multipliers Conditions

Buyers think this way Similar expense ratios Similar upside potential

Estimation of Gross Rent Multipliers

Chapter 22 8Student Handbook to THE APPRAISAL OF REAL ESTATE

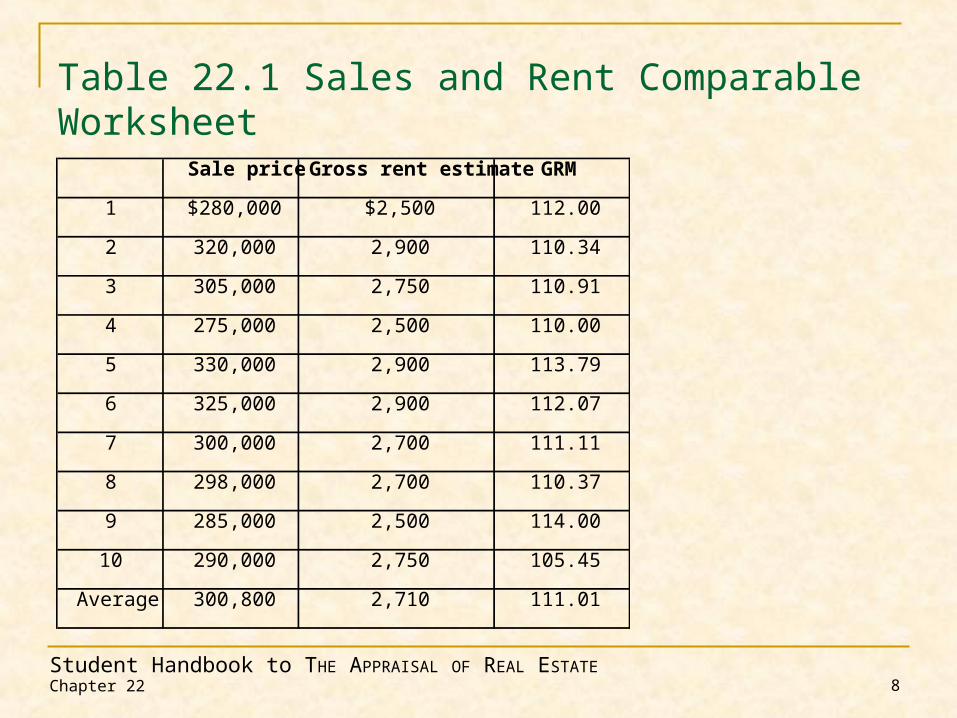

Table 22.1 Sales and Rent Comparable Worksheet

Sale price Gross rent estimate GRM

1 $280,000 $2,500 112.00

2 320,000 2,900 110.34

3 305,000 2,750 110.91

4 275,000 2,500 110.00

5 330,000 2,900 113.79

6 325,000 2,900 112.07

7 300,000 2,700 111.11

8 298,000 2,700 110.37

9 285,000 2,500 114.00

10 290,000 2,750 105.45

Average 300,800 2,710 111.01

Chapter 22 9Student Handbook to THE APPRAISAL OF REAL ESTATE

Problems

Suggested solutions begin on page 365.

Chapter 22 10Student Handbook to THE APPRAISAL OF REAL ESTATE

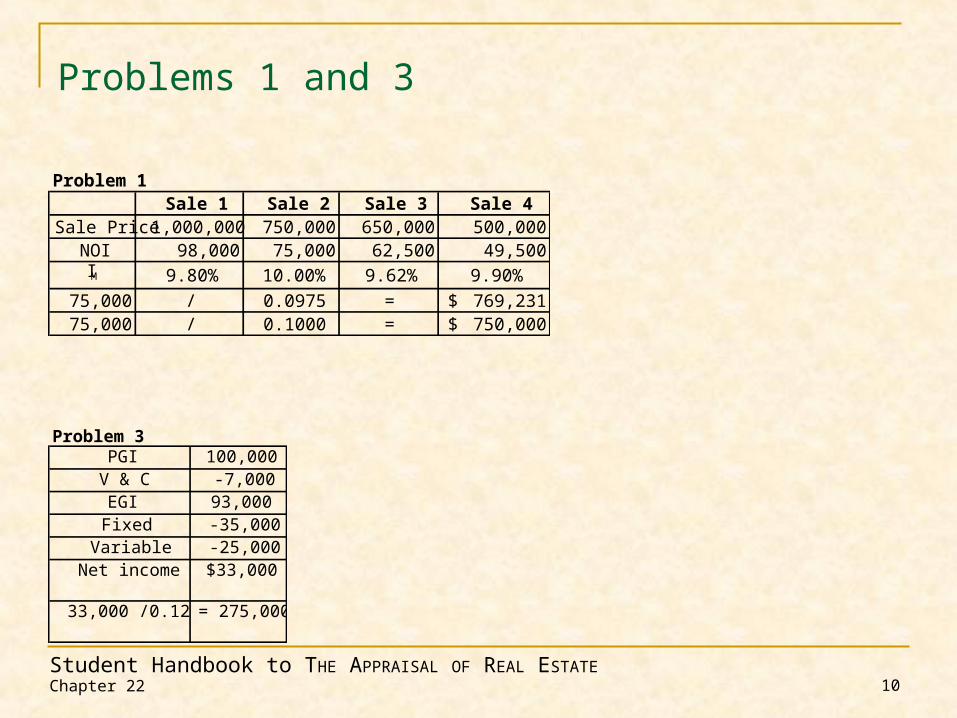

Problems 1 and 3

Problem 1Sale 1 Sale 2 Sale 3 Sale 4

Sale Price 1,000,000 750,000 650,000 500,000 NOI 98,000 75,000 62,500 49,500 IM 9.80% 10.00% 9.62% 9.90%

75,000 / 0.0975 = 769,231$ 75,000 / 0.1000 = 750,000$

PGI 100,000V & C -7,000EGI 93,000

Fixed -35,000Variable -25,000

Net income $33,000

33,000 /0.12 = 275,000

Problem 3

Chapter 22 11Student Handbook to THE APPRAISAL OF REAL ESTATE

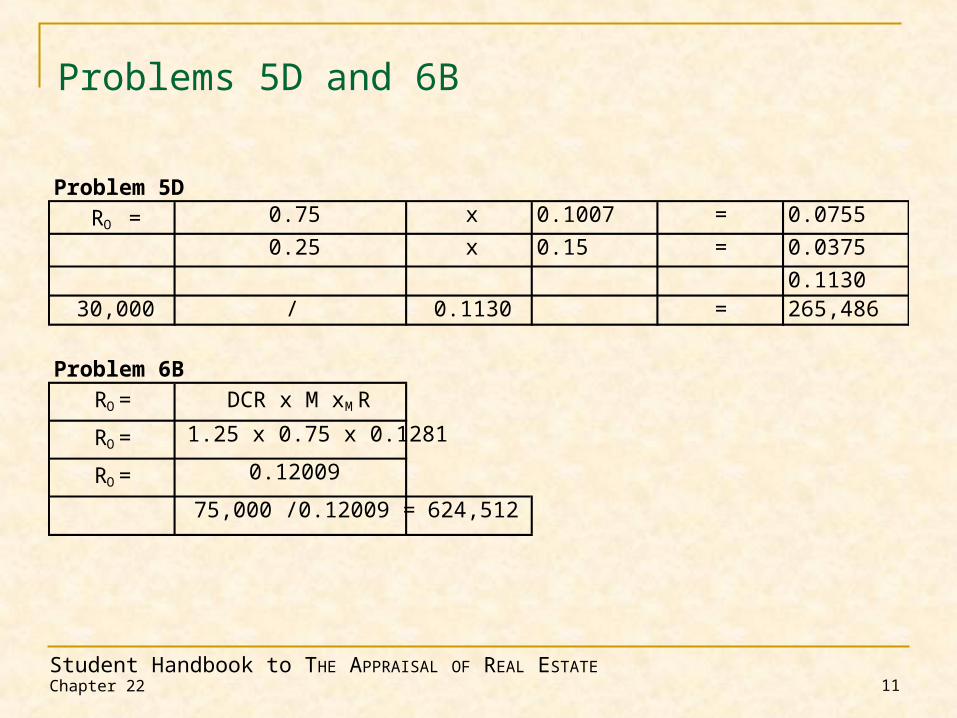

Problems 5D and 6B

Problem 5DRO = 0.75 x 0.1007 = 0.0755

0.25 x 0.15 = 0.0375

0.113030,000 / 0.1130 = 265,486

Problem 6BRO = DCR x M x RM

RO = 1.25 x 0.75 x 0.1281

RO = 0.12009

75,000 /0.12009 = 624,512

Chapter 22 12Student Handbook to THE APPRAISAL OF REAL ESTATE

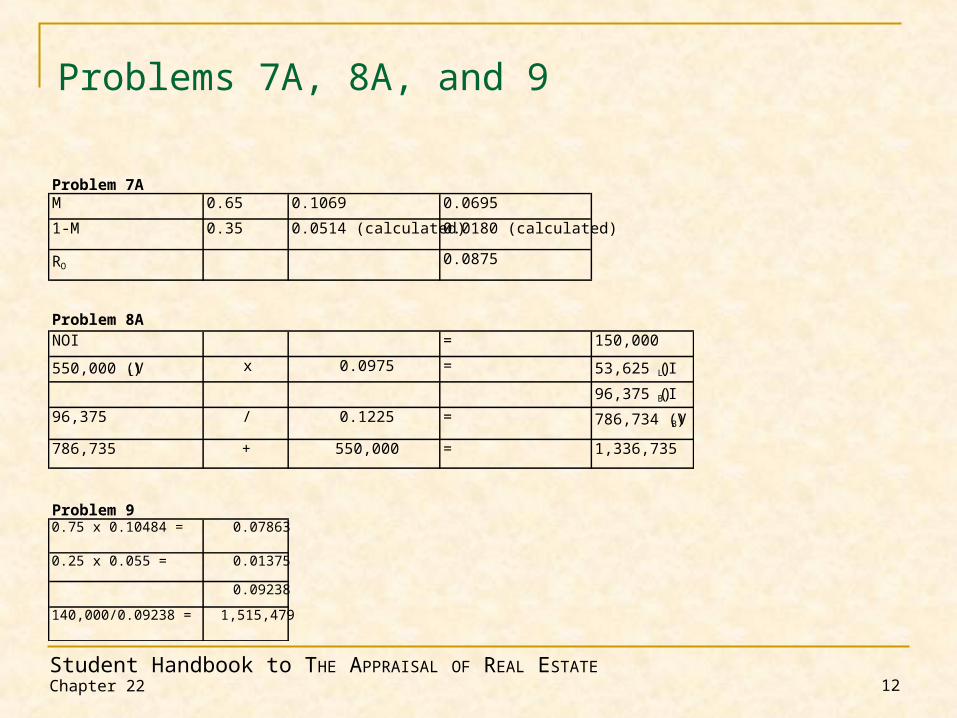

Problems 7A, 8A, and 9

M 0.65 0.1069 0.0695

1-M 0.35 0.0514 (calculated) 0.0180 (calculated)

RO 0.0875

Problem 8ANOI = 150,000

550,000 (VL) x 0.0975 = 53,625 (IL)

96,375 (IB)

96,375 / 0.1225 = 786,734 (VB)

786,735 + 550,000 = 1,336,735

0.75 x 0.10484 = 0.07863

0.25 x 0.055 = 0.01375

0.09238

140,000/0.09238 = 1,515,479

Problem 9

Problem 7A

Chapter 22 13Student Handbook to THE APPRAISAL OF REAL ESTATE

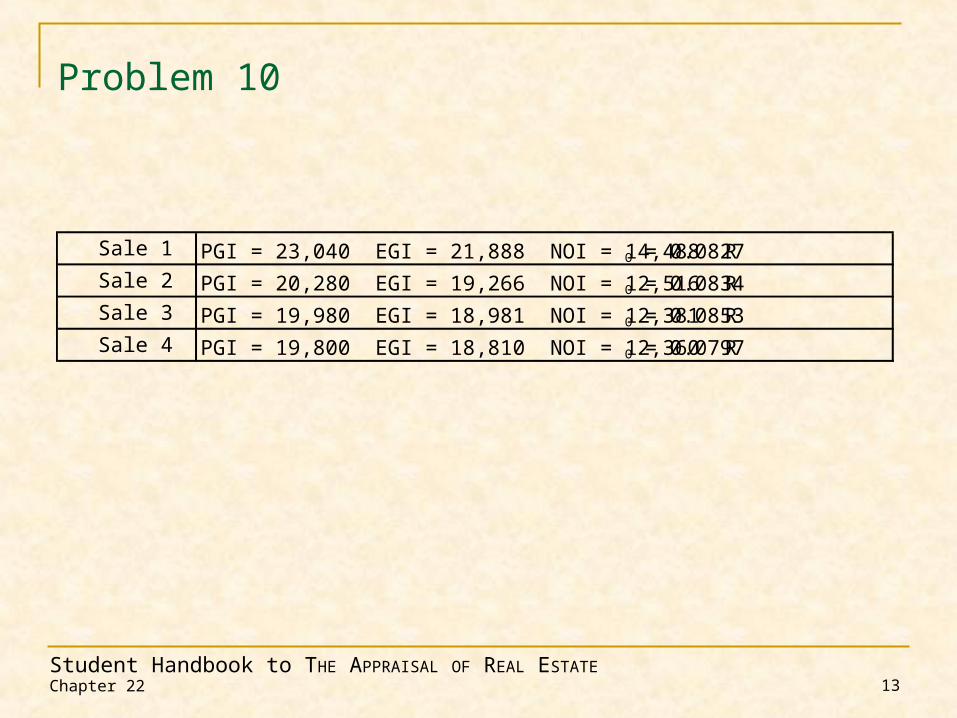

Problem 10

Sale 1

Sale 2

Sale 3

Sale 4

PGI = 23,040 EGI = 21,888 NOI = 14,488 RO = 0.0827

PGI = 20,280 EGI = 19,266 NOI = 12,516 RO = 0.0834

PGI = 19,980 EGI = 18,981 NOI = 12,381 RO = 0.0853

PGI = 19,800 EGI = 18,810 NOI = 12,360 RO = 0.0797

Chapter 22 14Student Handbook to THE APPRAISAL OF REAL ESTATE

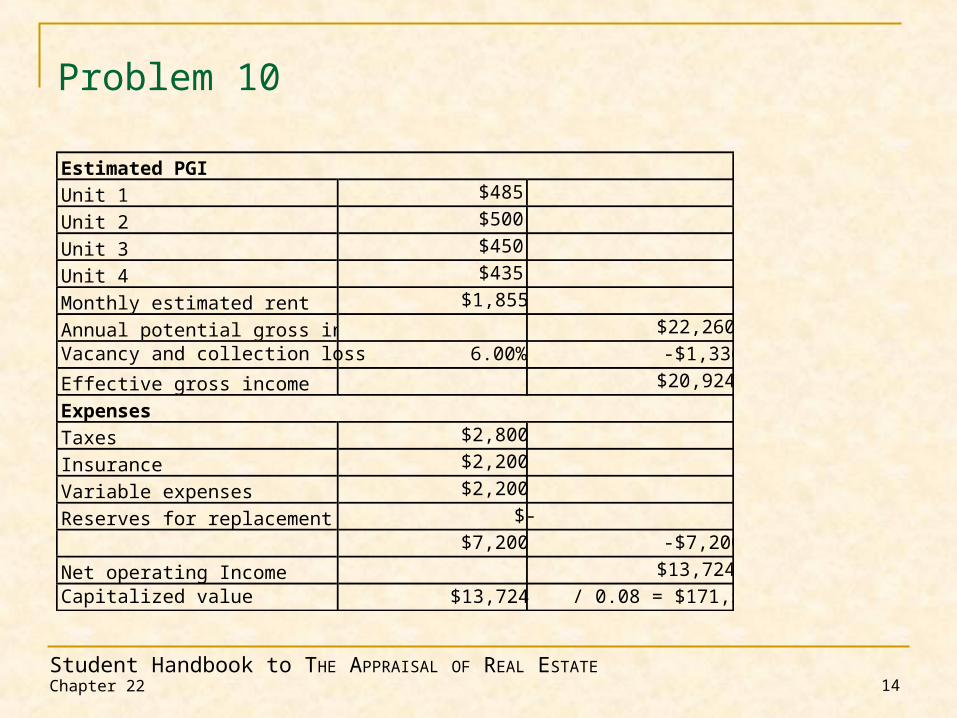

Problem 10

$485$500$450$435

$1,855$22,260

Vacancy and collection loss 6.00% -$1,336$20,924

$2,800$2,200$2,200

$-$7,200 -$7,200

$13,724Capitalized value $13,724 / 0.08 = $171,555

Expenses

Monthly estimated rentAnnual potential gross income

Effective gross income

Unit 1Unit 2Unit 3

Reserves for replacement

Net operating Income

Taxes InsuranceVariable expenses

Unit 4

Estimated PGI