Digitalized Electricity Dijitalleşen Elektrik 8 Mayıs 2014 – İstanbul ICSG.

16

Digitalized Electricity Dijitalleşen Elektrik 8 Mayıs 2014 – İstanbul ICSG

-

Upload

roger-watts -

Category

Documents

-

view

221 -

download

0

Transcript of Digitalized Electricity Dijitalleşen Elektrik 8 Mayıs 2014 – İstanbul ICSG.

Digitalized Electricity

Dijitalleşen Elektrik

8 Mayıs 2014 – İstanbul ICSG

Agenda

Copyright © 2014 Accenture All rights reserved. 2

Traditional utility model at a crossroads

Trending insights for utilities companies

Emerging smart grid business models

1

2

3

Copyright © 2014 Accenture All rights reserved.

Major energy challenges are impacting the electricity industry

3

Reliability and resilience

Energy security and independence

Rising electricity costs

Changes in demand patterns

Environmental sustainabilityEvolving technologies

Distributed generation in Germany reaches more than 1 million households, Denmark gets more than 30% of electricity from wind

Superstorm Sandy heightens US consumer concern over reliability

The last of Japan’s nuclear fleet goes offline in summer 2013

China’s electricity demand grew at more than 9.5% per year from 2006 to 2010 (EIA)

Average total energy consumption fell by 24.7% in England between 2005 and 2011 (UK ONS)

Solar PV subsidies in Germany cost €8.8 billion in 2012

Natural gas boom continues with the EIA estimating the United States to be net exporter by 2020

Electricity theft estimated to be more than 30% for some Indian utilities (World Bank)

Solar PV reaches grid parity in most of Australia

China aiming to reduce greenhouse gas emissions per unit of gross domestic product by 40% below 2005 levels by 2020

In 2012, an outage in India affected more than 620 million people—about 9% of the world’s population

Copyright © 2014 Accenture All rights reserved.

Major energy challenges are impacting the electricity industry in Turkey as well

4

Reliability and resilience

Energy security and independence

Rising electricity costs

Changes in demand patterns

Environmental sustainability

Upper limit for unlicensed generation becoming 1 MW, and increasing unlicensed generation lead to need of managing discontinuous supply and imbalances

Severe weather conditions during last winter caused gas shortages leading to electricity cuts

Constituting 38% of Turkey’s electricity generation, dependency on NG & foreign imports will continue.

Yet its share is expected to decrease by 9% by 2023

While the last year demand was relatively flat, we expect it to increase in the upcoming years again

Increasing share of renewables in energy mix will continue to secure domestic production

While improvements have been made, theft & loss is still an issue

Solar PV started to take place in the energy mix

Participating in the voluntary market, Turkey aims to reduce greenhouse gas emissions through developing renewables

Daily gas consumption incresing to 180-200 bcm, caused major problems in transporting the required amount of gas

Energy intensity (energy consumption per capita) is expected to increase by 0.1 - 2.0% acc to different scenarios

Evolving technologies

causing distribution networks to respond across three major areas

Copyright © 2014 Accenture All rights reserved. 5

Consumer

New technology threats and opportunities

Asset efficiency and performance

Increase renewables carrying capacity

Enable new load capacity(PEV, storage, etc.)

Reduce retail costs

Reduce theft

Enable demand flexibility

Enable consumer peak and demand reduction

Improve asset utilization

Improve network reliability and outage duration

O&M reduction and CAPEX optimization

Agenda

Copyright © 2014 Accenture All rights reserved. 6

Traditional utility model at a crossroads

Trending insights for utilities companies

Emerging smart grid business models

1

2

3

Copyright © 2014 Accenture All rights reserved. 7

Trending insights –Smart grid becoming mainstream

Smart grid is here to stay. It will become mainstream and a core part of utility operations

Operating models will need to evolve to support the new capabilities, processes and data

Mainstream

The adoption of smart technologies will reduce the costs of upgrading/maintaining the grid by 2030

The example: Outage management

Will smart technology solutions be part of your outage management solution by 2020?

The smart grid is a natural extension of the ongoing upgrades of the electricity network

Source: Accenture’s Digitally Enabled Grid program, 2013 executive survey.

Disagree

Disagree

Agree

Agree

Copyright © 2014 Accenture All rights reserved. 8

Trending insights –Hybrid models will dominate

Utilities will adopt a hybrid model involving traditional and smart technologies

Align smart and traditional asset investments and operating model into an integrated management strategy and investment plan

Which of the following network operating models will best characterize your network by 2030?

Source: Accenture’s Digitally Enabled Grid program, 2013 executive survey.

Copyright © 2014 Accenture All rights reserved. 9

Competition will increase – opportunities and threats

A new set of potential services, with data as a critical asset, will bring increased competition as well as new opportunities

Understand new threats and leverage these to position for growth with emerging opportunities

Competition is expected to increase Impact by 2030: Threats or opportunities?

of Utilities executives expect that energy data markets (i.e., centralized single point of access for integrated energy data, covering consumers, load types, segments etc.) will develop within the next 10 years

83%

% of Utilities executives that believe that increased competition will arise in the following areas within five years:

Beyond-the-meter solutions focused on energy efficiency and demand response

85%

Data-related services85%

Distributed generation85%

Source: Accenture’s Digitally Enabled Grid program, 2013 executive survey.

Revenues

Copyright © 2014 Accenture All rights reserved. 10

Trending insights – Regulatory strategy gains importance

Current regulatory models are increasingly under pressure due to the challenges facing distribution companies

Collaborate with regulators to help shape the regulatory models to accommodate demand reduction and competitive threats

Do you believe that regulatory or legislative changes are necessary to help you manage the grid effectively?

of Utilities executives believe that the lack of regulatory and policy support is one of the main barriers for the deployment of smart solutions for their network

56%

No.1 biggest challenge to successful full-scale smart metering deployment is the lack of supporting policy/regulation

Source: Accenture’s Digitally Enabled Grid program, 2013 executive survey.

Copyright © 2014 Accenture All rights reserved. 11

Trending insights –IT capabilities are stretched

Smart technologies will require new IT capabilities to maximize benefit realization

Address the need for new skills, tools and capability requirements without compromising on asset and financial performance. IT becomes a core competency, tightly linked with OT

The needs Current hurdles

Cyber security and privacy management will be critical or important for managing the complexity of the network

Access to the right IT skills will be critical or important to manage the increasingly large data volumes and integration

Need to improve analytical capabilities for IT/OT integration

Advanced analytical/statistical tools will be critical or important to manage the increasingly large data volumes and integration

Data management will be critical or important for managing the complexity of the network

Need to improve data governance

Need to improve analysis toolsets

Barrier for North American & European Utilities executives for deployment of smart solutions: Lack of mature technology solutions

No.1

96%

92%

90%

88%

Source: Accenture’s Digitally Enabled Grid program, 2013 executive survey.

94%

88%

100%

12

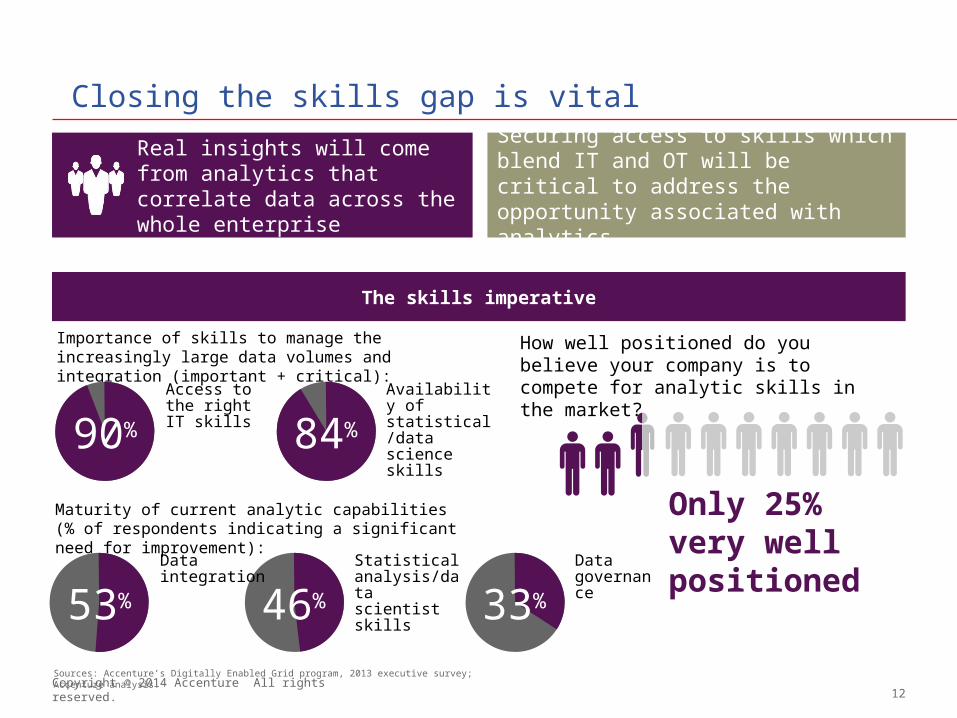

Closing the skills gap is vital

Copyright © 2014 Accenture All rights reserved.

Real insights will come from analytics that correlate data across the whole enterprise

Securing access to skills which blend IT and OT will be critical to address the opportunity associated with analytics

The skills imperative

How well positioned do you believe your company is to compete for analytic skills in the market?

Importance of skills to manage the increasingly large data volumes and integration (important + critical):

Maturity of current analytic capabilities (% of respondents indicating a significant need for improvement):

Only 25% very well positioned

Access to the right IT skills

Availability of statistical/data science skills90% 84%

Data integration

Statistical analysis/data scientist skills

Data governance53% 46% 33%

Sources: Accenture’s Digitally Enabled Grid program, 2013 executive survey; Accenture analysis.

Agenda

Copyright © 2014 Accenture All rights reserved. 13

Traditional utility model at a crossroads

Trending insights for utilities companies

Emerging smart grid business models

1

2

3

Evolving Business Model – determine the "smart" plan and timing for your strategic response

Deployment of smart grid to support external growth opportunities

Deployment of smart grid for internal operations

Copyright © 2014 Accenture All rights reserved. 14

Smart grid challengerPriorities• Funding for a portfolio of pilots and proactive support for

smart solutions• Innovate to meet consumer expectations• Build consumer relationships to support active participation • Targeted investment in key enabling capabilities (including

communications and IT/OT)• Opportunistic pursuit of new revenue streams using alliance

partners to reduce risk

Incremental traditionalistPriorities• Protect existing revenues• Maintain pace with regulatory expectation• Proven solutions with slow scaling• Avoid investment at risk of stranding• Minimize business disruption• Lowest risk approach in the short term

Smart grid embracerPriorities• Aggressively pursue new revenue streams • Make significant smart investments without

guaranteed regulated returns• Engage in major business and operating model

change including mergers and acquisitions • Actively drive change in regulation to disrupt the

status quo

Utility excellence – assumes low competitive threat

Low risk in the short term, nonsustainable long term

Utility of the future

Noneffective

Copyright © 2014 Accenture All rights reserved.

Accenture’s Digitally Enabled Grid program

15

Accenture’s Digitally Enabled Grid program provides insights and recommendations around challenges and opportunities utilities face along the path to a smarter grid, including views from utilities executives around the world

Assessment of the drivers for smart grid adoption and the approach to defining an optimal route toward a future digital grid

Investigation of the critical factors for the deployment of smart meters and the extraction of greater value through the adoption of advanced solutions

Consideration of the impacts of changing energy requirements on grid operations and the role that smart solutions can play in cost-effectively delivering reliable electricity supplies

Examination of the central role that analytics will play in extracting value from smart solutions and detailing of the key factors that utilities must address to enable this vital capability

Forging a Path toward a Digital Grid: Global perspectives on smart grid opportunities

Realizing the Full Potential of Smart Metering

Optimizing Grid Performance through Advanced Operations

Unlocking the Value of Analytics