#digi2013 William Hobbs, Barclays

32

-

Upload

propellondon -

Category

Business

-

view

552 -

download

1

Transcript of #digi2013 William Hobbs, Barclays

Investment outlook 2013

William HobbsHead of Equity Strategy

January 2013

4

Outline of presentation

2013 outlook

Risk #1: the euro crisis

Risk #2: US & UK austerity

The global context

How to invest

5

2013 Outlook

Source: Google Images, Barclays

6

Clouds begin to lift

Most visible clouds:

1: The euro’s existential crisis

2: Fiscal austerity in the US and UK

Rays of sunshine?

1: The ECB (and, if needed, the BoE)

2: US New Year deal & UK history

3: The bigger picture: ‘Customer no. 1’ and Asia

7

Key barometer: manufacturing surveys stabilising

Source: Bloomberg, Datastream, Barclays Research

-5

-4

-3

-2

-1

0

1

2

Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12China US UK Germany Japan

Standard deviations from trend

8

Risk #1: the euro crisis

How to view it:

“One must imagine Sisyphus happy” – Camus

10

The ECB’s safety net at work

Source: Bloomberg, Barclays

0

1

2

3

4

5

6

7

0.0

0.5

1.0

1.5

2.0

2007 2008 2009 2010 2011 2012 2013

Euro interbank - OIS spread (lhs) Germany-Spain 10 year bond spread (rhs)

(%) (%)

11

Spain, the ECB and OMT…

Will Spain ask for a bail-out?

If the ECB’s promise is credible, it may not matter

A formal request determines who, not what

After Greece’s default, why not Spain?

Budget and debt arithmetic is better

Economy is different & reforms more credible

The troika would try harder…

12

Plausible timescale for a definitive euro fix

Source: Blackrock, Barclays Wealth Strategy

Safeguard banks, tackle

deficits & insolvent

sovereigns

Co-ordinate deposit

insurance, supervision,

rescue facilities

Greater fiscal integration, joint bond issuance

More competitive peripheral economies

Lasting solution

2012… 2017?? 2022???2013-15?

13

Risk #2: US & UK fiscal austerity

14

US fiscal cliff has been turned

New Year compromise was a big deal

‘American Taxpayer Relief Act’ keeps a lid on taxes

Tax hit in 2013: $190bn, or 1.2% GDP (cf: $650bn, 4.1%)

TBD (March?): spending cuts & debt ceiling

Spending sequestration: $90bn, or 0.6% GDP

Credit ratings matter less than ‘fundamentals’

15

Govt. borrowing (rolling 12 mths, % GDP)

Source: Datastream, Barclays Research

-6

-4

-2

0

2

4

6

8

10

12

Q1 1994 Q1 1999 Q1 2004 Q1 2009

US UK

16

Structural government deficits (IMF, % GDP)

Source: IMF WEO; Barclays

-12

-10

-8

-6

-4

-2

0

2

4

6

8

2007 2009 2011 2013F Change 2009-2013

UK Euro area US Japan

17

“How 364 economists got it totally wrong”Daily Telegraph, March 2006 – a 25th anniversary

Precedent: a brief UK history lesson

18

Sterling is competitive & real rates are low

Source: Datastream, Barclays Research

-6

-5

-4

-3

-2

-1

0

1

2

3

02/11/2002 02/11/2004 02/11/2006 02/11/2008 02/11/2010 02/11/2012

75

80

85

90

95

100

105

Real interest rates (%, LHS) Real exchange rate (index, RHS)

19

The global context

20

US housing market gathering momentum

Source: Factset, Barclays Research

400

500

600

700

800

900

1000

1100

1200

1300

Jan-08 Jan-09 Jan-10 Jan-11 Jan-12

100

150

200

250

300

350

400

450

500

550

Building permits Private housing starts Stock of new homes for sale (RHS)

21

US consumer spending: life after debt

Source: Datastream, Barclays Research

100

105

110

115

120

125

15/12/2005 15/12/2007 15/12/2009 15/12/2011

250

300

350

400

450

500

550

600

650

700

US household spending (nominal, index) Unemployment claims (000, RHS)

Index: Dec 2005=100 000s per w eek

22

Total US liabilities are large…

Source: Datastream, Federal Reserve, Barclays Research

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Q2 1962 Q2 1972 Q2 1982 Q2 1992 Q2 2002 Q2 2012

Consumer + Government

+ Non-financial business + Financial sector = Total domestic

Debt/GDP

23

… but consumer assets are larger

Source: Factset, Barclays Wealth Strategy

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Q2 1962 Q2 1972 Q2 1982 Q2 1992 Q2 2002 Q2 2012

Debt Financial assets Tangible assets Net worth

X GDP

2424

Asian growth: structural underpinnings

Source: US Bureau of Census, MSCI, Barclays

0

10

20

30

40

50

60

Stocks now Bonds now Real GDP now Population in 2041

Asia’s weight in the world, %

25

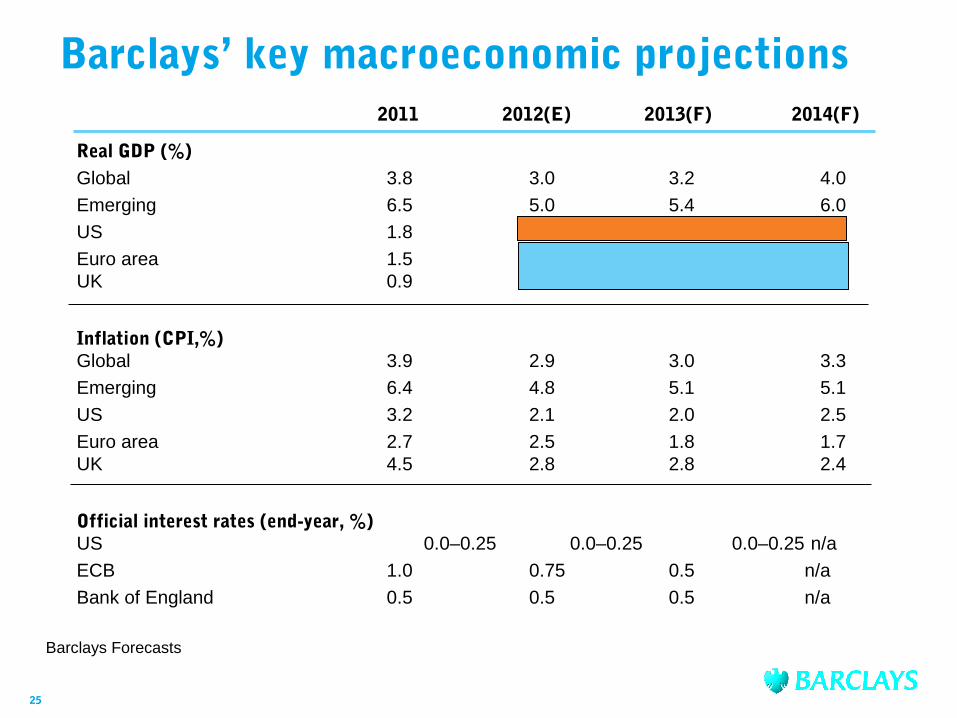

Barclays’ key macroeconomic projections

Real GDP (%)Global 3.8 3.0 3.2 4.0

Emerging 6.5 5.0 5.4 6.0

US 1.8 2.3 2.1 2.5

Euro area 1.5 -0.4 0.1 1.4UK 0.9 -0.1 1.3 2.2

Inflation (CPI,%)Global 3.9 2.9 3.0 3.3

Emerging 6.4 4.8 5.1 5.1

US 3.2 2.1 2.0 2.5

Euro area 2.7 2.5 1.8 1.7UK 4.5 2.8 2.8 2.4

Official interest rates (end-year, %)US 0.0–0.25 0.0–0.25 0.0–0.25 n/a

ECB 1.0 0.75 0.5 n/a

Bank of England 0.5 0.5 0.5 n/a

Barclays Forecasts

2011 2012(E) 2013(F) 2014(F)

26

How to invest

27

Conclusion: risk assets preferred in 2013

1. Corporate securities preferred to government

- Business cycle and collective risk appetite matter more than QE

- Credit spreads are flattered by low GB yields: High Yield preferred

2. Stocks preferred to bonds

- Analysts too optimistic, but market doesn’t believe them: valuations low

- Current: US and EUX preferred to Japan, UK, RoW; neutral EM (Asia

pref.)

- Within EUX: some core and some periphery

- Rotation ahead: ‘Income’ & recovery to switch into ‘Growth’…

3. F/X: USD becomes pro-cyclical; JPY & CHF to reverse; Asian EMs

favoured

28

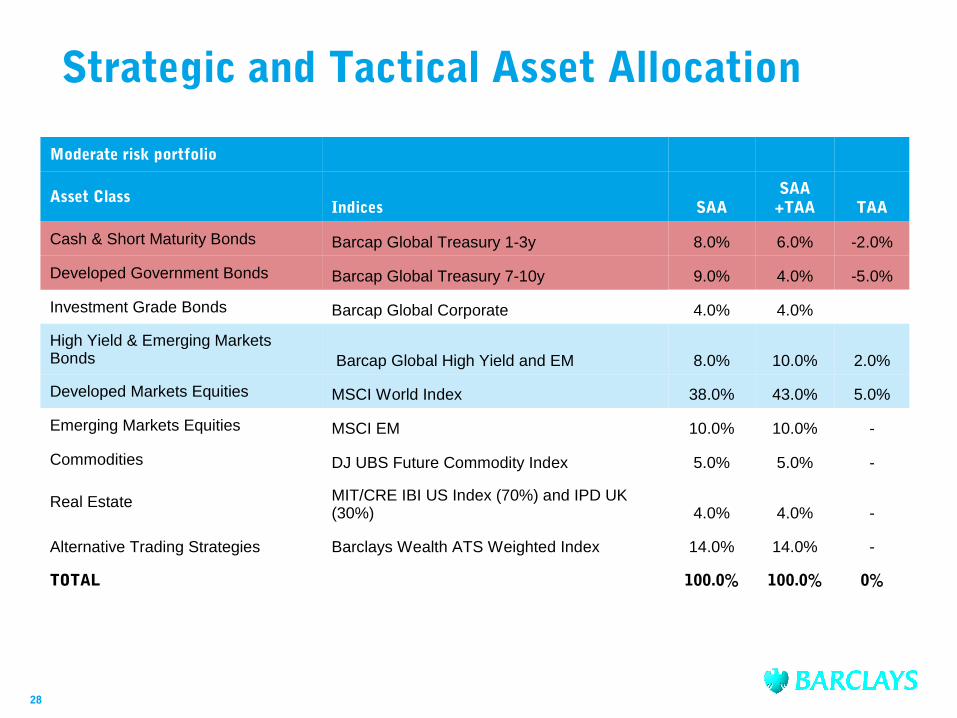

Strategic and Tactical Asset Allocation

Moderate risk portfolio

Asset ClassIndices SAA

SAA +TAA TAA

Cash & Short Maturity Bonds Barcap Global Treasury 1-3y 8.0% 6.0% -2.0%

Developed Government Bonds Barcap Global Treasury 7-10y 9.0% 4.0% -5.0%

Investment Grade Bonds Barcap Global Corporate 4.0% 4.0%

High Yield & Emerging Markets Bonds Barcap Global High Yield and EM 8.0% 10.0% 2.0%

Developed Markets Equities MSCI World Index 38.0% 43.0% 5.0%

Emerging Markets Equities MSCI EM 10.0% 10.0% -

Commodities DJ UBS Future Commodity Index 5.0% 5.0% -

Real Estate MIT/CRE IBI US Index (70%) and IPD UK (30%) 4.0% 4.0% -

Alternative Trading Strategies Barclays Wealth ATS Weighted Index 14.0% 14.0% -

TOTAL 100.0% 100.0% 0%

Developed profitability is not extreme (real ROE, %)

Source: MSCI, Datastream, FactSet, Barclays

-2

0

2

4

6

8

10

12

14

16

Dec-74 Dec-79 Dec-84 Dec-89 Dec-94 Dec-99 Dec-04 Dec-09inflation adjusted RoE 10 year moving average

Please note that past performance is not necessarily a reliable indicator of future performance

30

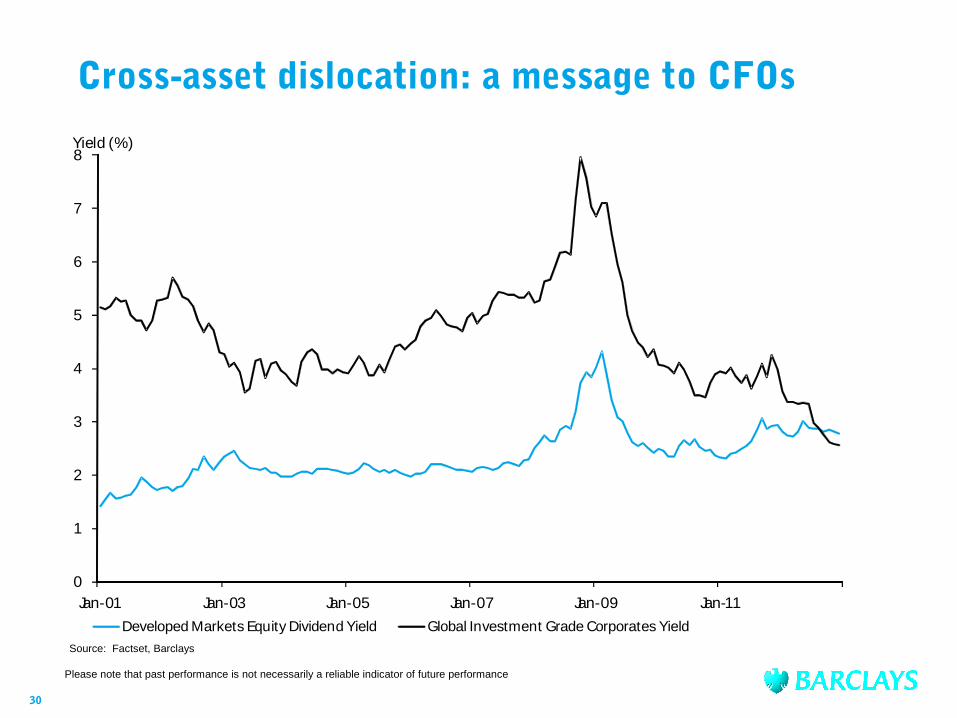

Cross-asset dislocation: a message to CFOs

Source: Factset, Barclays

0

1

2

3

4

5

6

7

8

Jan-01 Jan-03 Jan-05 Jan-07 Jan-09 Jan-11

Developed Markets Equity Dividend Yield Global Investment Grade Corporates Yield

Yield (%)

Please note that past performance is not necessarily a reliable indicator of future performance

Disclaimer

This document has been issued and approved by Barclays Bank PLC. Although information in this document has been obtained from sources believed to be reliable, we do not represent or warrant its accuracy, and such information may be incomplete or condensed. This document does not constitute a prospectus, offer, invitation or solicitation to buy or sell securities and is not intended to provide the sole basis for any evaluation of the securities or any other instrument, which may be discussed in it. All estimates and opinions included in this document constitute our judgement as of the date of the document and may be subject to change without notice. This document is not a personal recommendation and you should consider whether you can rely upon any opinion or statement contained in this document without seeking further advice tailored for your own circumstances. This document is confidential and is being submitted to selected recipients only. It may not be reproduced or disclosed (in whole or in part) to any other person without our prior written permission. Law or regulation in certain countries may restrict the manner of distribution of this document and persons who come into possession of this document are required to inform themselves of and observe such restrictions. We or our affiliates may have acted upon or have made use of material in this document prior to its publication. You should seek advice concerning any impact this investment may have on your personal tax position from your own tax adviser.

Barclays offers wealth and investment management products and services to its clients through Barclays Bank PLC and its subsidiary companies.Barclays Bank PLC is registered in England and authorised and regulated by the Financial Services Authority. Registered number is 1026167 and its registered office is 1 Churchill Place, London E14 5HP.

© Barclays Bank PLC 2012. All rights reserved. Issued for companies including Barclays Bank PLC (Reg. No. 1026167), Barclays Stockbrokers Limited (Reg. No. 1986161), a member of the London Stock Exchange and PLUS, Barclays Sharedealing (Reg. No. 2092410), Barclays Bank Trust Company Limited (Reg. No. 920880) and Gerrard Investment Management Limited (Reg No. 2752982), a member of the London Stock Exchange. All of these companies are registered in England and have their registered office at: 1 Churchill Place, London E14 5HP. All of these firms are authorised and regulated by the Financial Services Authority.