Diamond Resorts Post Road Capital Long Case

21

At a recent Boston investment conference, a student presented a misleading and fallacious “short” presentation regarding Diamond Resorts International (DRII). Surprisingly, this presentation won the contest and has been, circulated in the investment community. Though it is not our intention to harm (reputation, career or otherwise) a student with no professional analytic experience, it is our desire to set the record straight and protect a high quality company, its founders, employees, customers and investors. We are shareholders and are sensitive to a company’s brand in the investment world; thus, we have chosen to publish a refutation (something we have not previously done) of this report to put these questions to rest. We will be following up with additional reports on the key aspects of the business. The Timeshare Industry is going through profoundly positive changes and Diamond is at the forefront. Unfortunately, this short report is inaccurate on virtually every point and conclusion . In fact, we cannot find a single page that does not contain cheap shots (to influence bias), irrelevant comments and factual inaccuracies and / or analytical fallacies. Our line-by-line to this report is posted at www.postroadcap.com/drii . Diamond Resorts is a well-run company originally financed by Soros Fund Management. Currently, Guggenheim Partners is a major investor and retains two board seats. The business is thriving and a recent securitization (November 2014) was issued with an investment grade rating and a 2.58% average interest rate, thus proving the quality of the customers and loan portfolio performance. About Post Road Capital Management, LLC: PRCM is an investment fund that utilizes a concentrated, long-term, tax efficient strategy focused on achieving outsized absolute returns. The firm was founded by David Eigen who has over 20 years of investment experience including co-portfolio manager at Iridian Asset Management. Post Road Capital has successfully vetted and invested in the timeshare space and continues to hold a position in Wyndham Worldwide (WYN). POST ROAD CAPITAL MANAGEMENT Of most relevance are the following mistaken comments: • The enterprise value is wrong; securitizations are non-recourse; cash on the balance sheet is ignored, net income is also wrong • DRII is not some sort of “scam”; in fact, they pioneered the asset-light model which results in the highest forms of FCF and returns while minimizing risk • Online agencies like Expedia are big partners, not adversaries • The report mistakes intentional churn of low quali ty acquired (in M&A) members for a long-term pattern of decline. Memberships are not in decline • Loans in Default: The report CONFUSES servicing of a portfolio of loans with securitized assets held in a portfolio. The student says that $243MM are in default. Rather, $210MM (of the $243MM) are merely being serviced and were PURCHASED out of bankruptcy in 2011. This $210MM is a company ASSET, a supply of inventory. Further , DIAMOND IS INFACT OVER RESERVED. We expect management to provide more clarity in their upcoming 10-K • Cash flow is significant, growing and sustainable – NOT declining, NOT one-time For ease of reading, we have underlined the factual and analytical errors. We remain open to questions and comments. Once again, we are not in the business of publishing reports, nor do we take any pleasure in showing the flaws in a student’s analysis. Nonetheless, we do know what can happen when a company’s reputation is harmed: investors just look the other way and say “pass.” That would be a mistake in the case of Diamond Resorts.

-

Upload

anonymous-ht0mij -

Category

Documents

-

view

213 -

download

0

Transcript of Diamond Resorts Post Road Capital Long Case

8/10/2019 Diamond Resorts Post Road Capital Long Case

http://slidepdf.com/reader/full/diamond-resorts-post-road-capital-long-case 1/22

At a recent Boston investment conference, a student presented a misleading andfallacious “short” presentation regarding Diamond Resorts International (DRII).Surprisingly, this presentation won the contest and has been, circulated in theinvestment community. Though it is not our intention to harm (reputation, career orotherwise) a student with no professional analytic experience, it is our desire to set therecord straight and protect a high quality company, its founders, employees, customersand investors.

We are shareholders and are sensitive to a company’s brand in the investment world;thus, we have chosen to publish a refutation (something we have not previously done)of this report to put these questions to rest. We will be following up with additionalreports on the key aspects of the business. The Timeshare Industry is going throughprofoundly positive changes and Diamond is at the forefront.

Unfortunately, this short report is inaccurate on virtually every point and conclusion . Infact, we cannot find a single page that does not contain cheap shots (to influencebias), irrelevant comments and factual inaccuracies and / or analytical fallacies. Ourline-by-line to this report is posted at www.postroadcap.com/drii .

Diamond Resorts is a well-run company originally financed by Soros Fund Management.Currently, Guggenheim Partners is a major investor and retains two board seats. The

business is thriving and a recent securitization (November 2014) was issued with aninvestment grade rating and a 2.58% average interest rate, thus proving the quality ofthe customers and loan portfolio performance.

About Post Road Capital Management, LLC:

PRCM is an investment fund that utilizes a concentrated, long-term, tax efficient strategy focused on achieving outsized absolute returns. The firm was fover 20 years of investment experience including co-portfolio manager at Iridian Asset Management. Post Road Capital has successfully vetted and incontinues to hold a position in Wyndham Worldwide (WYN).

POST ROAD CAPITAL MANAGEMENT

Of most relevance are the following mistaken comm

•

The enterprise value is wrong; securitizations are sheet is ignored, net income is also wrong

• DRII is not some sort of “scam”; in fact, they pionresults in the highest forms of FCF and returns wh

• Online agencies like Expedia are big partners, n•

The report mistakes intentional churn of low quaa long-term pattern of decline. Memberships are

• Loans in Default: The report CONFUSES servicing securitized assets held in a portfolio. The studenRather, $210MM (of the $243MM) are merely beiout of bankruptcy in 2011. This $210MM is a comFurther, DIAMOND IS INFACT OVER RESERVED. Wmore clarity in their upcoming 10-K

• Cash flow is significant, growing and sustainable

For ease of reading, we have underlined the factuaopen to questions and comments. Once again, we reports, nor do we take any pleasure in showing the fNonetheless, we do know what can happen when a

investors just look the other way and say “pass.” ThaDiamond Resorts.

8/10/2019 Diamond Resorts Post Road Capital Long Case

http://slidepdf.com/reader/full/diamond-resorts-post-road-capital-long-case 2/22

Disclosures:

This disclaimer is issued in connection with the website www.postroadcap.com/drii (the “Website”) maintained by Post Road Capital Management, LLC (adviser to funds that are in the business of actively buying and selling securities and other financial instruments.

Post Road currently maintains a substantial long position in the common stock of Diamond Resorts International, Inc. (“Diamond Resorts” or DRII). Post Roincreases for common shares of Diamond Resorts and will lose money if the trading price decreases for common shares of Diamond Resorts.

Post Road may change its views about or its investment positions in Diamond Resorts at any time, for any reason or no reason. Post Road may buy, sell, covor substance of any of its investments related to Diamond Resorts at any time. Post Road disclaims any obligation to notify the market or any other party oThe information and opinions contained in the Website are based on publicly available information about Diamond Resorts and other companies. Post Rnon-public information in the possession of Diamond Resorts or others that could lead Diamond Resorts or others to disagree with Post Road’s analyses and

The presentation includes forward-looking statements, estimates, projections and opinions prepared with respect to, among other things, Diamond Resortperformance, access to capital markets, market conditions, assets and liabilities . Such statements, estimates, projections and opinions may prove to be sinherently subject to significant risks and uncertainties beyond Post Road’s control.

Although Post Road believes the statements it makes in the presentation are substantially accurate in all material respects and do not omit to state materstatements not misleading, Post Road makes no representation or warranty, express or implied, as to the accuracy or completeness of those statements o

communication it makes with respect to Diamond Resorts and any other companies mentioned, and Post Road expressly disclaims any liability relating to communications (or any inaccuracies or omissions therein). Thus, shareholders and others should conduct their own independent investigation and analyscommunications and of Diamond Resorts and any other companies to which those statements or communications may be relevant.

The statements Post Road makes in the presentation or through the Website are not investment advice or a recommendation or solicitation to buy or sell aotherwise indicated, those statements speak as of the date made, and Post Road undertakes no obligation to correct, update or revise those statementsadditional materials. Post Road also undertakes no commitment to take or refrain from taking any action with respect to Diamond Resorts or any other co

All users and listeners agree and consent to exclusive jurisdiction and venue of any dispute or proceeding relating to or arising from the Website or any relaof the State of Connecticut, Fairfield County or in the Federal courts located in United States District Court for the District of Connecticut.

As used herein, except to the extent the context otherwise requires, Post Road includes its a ffiliates and funds it manages or advi ses and their respective p

NOT AN OFFERING OF SECURITIES: The information contained in this presentation is for informational purposes only and is not intended, and shall not cons

securities in any jurisdiction or of any of the investments mentioned therein. Post Road Capital Management, LLC is filed as an exempt reporting adviser w

POST ROAD CAPITAL MANAGEMENT

8/10/2019 Diamond Resorts Post Road Capital Long Case

http://slidepdf.com/reader/full/diamond-resorts-post-road-capital-long-case 3/22

Diamond Resort International

•

DRII is a timeshare company that operates on a points system. It currently has 5members under its global network. DRII sells points through “Vacation Interest S

collects an annual maintenance fee through “Management Services”

•

In April 2007, Stephen Cloobeck, acquiredSunterra Corporation by merger, which wasdelisted from NASDAQ as a result of theresignation of Sunterra Corporation's auditors andthe withdrawal of their certification of SunterraCorporation's financial statements

• Market Cap: ~$2.0B

• Enterprise Value: $2.4B + ~450M of securitizednotes

• 2014E Net Income: $43.4M

Current Price: $25.61│ P

8/10/2019 Diamond Resorts Post Road Capital Long Case

http://slidepdf.com/reader/full/diamond-resorts-post-road-capital-long-case 4/22

Diamond Resort International

•

As measured by membership, DRII is the third largest timeshareoperator (after Wyndham and Marriot) with over 515,000 members.It pioneered the asset-light business model. ALL companies nowemploy this model! While limiting capital risk, it provides highoperating margins and free cash flow as well as exponential returnson capital and equity

•

In April 2007, Stephen Cloobeck (with George Soros - laterGuggenheim), LBO’d (NOT merged) Sunterra Corporation.Sunterra’s auditors resigned (which resulted in the delisting). Thecompany was never financially insolvent. BDO performed a new

audit and all financials are up to date

•

Market Cap: ~$1.96B (at time of the report)

•

EV: < $2.3B (securitization is non-recourse; cash on the balancesheet was not subtracted); On 2015, net debt is 0.5x EBITDA

• 2014E Guided Net Income: $53-69mn; YTD at $37.6MM

Current Price: $24.18│ P

POST ROAD CAPITAL

8/10/2019 Diamond Resorts Post Road Capital Long Case

http://slidepdf.com/reader/full/diamond-resorts-post-road-capital-long-case 5/22

The Bull Case

• Inventory recapture model

•

The “genius” of this company is that DRII

recovers its inventory if the member

decides not to pay its membership fee•

This implies a ~97% retention rate

• Fast growth

• Growth through acquisitions

• High cash flow yield•

Annualizing H1’14

Imperial Capital on inventory: “Each year, 3-5% of owners fall behind on their annual abandon their interest. Diamond Resorts guarantees the annual payment (to the HOAownership

•

I asked IR how they achieve such a 97% retention rate; they responded: “they just l

8/10/2019 Diamond Resorts Post Road Capital Long Case

http://slidepdf.com/reader/full/diamond-resorts-post-road-capital-long-case 6/22

The Bull Case

•

Inventory recapture model• Imitation is the biggest form of flattery.

Wyndham and Marriot all recapture in similar

fashion to Diamond ~3% - i.e. 97% retention

•

Fast growth• Growth through tuck-in acquisitions – at 1 to 2x

EBITDA, typically in bankruptcy on favorableterms! Why is this bad???.

•

With 3% recapture, current inventory and tuck-ins., VOI sales growth is sustainable

•

High cash flow yield – savings of $60MM in interestexpense rolling in over the past two years plus cashflow from recent acquisitions provides an estimated

FCF yield of 16% (2015) and 19% (2016E)

•

Diamond Resorts has a high focus on customersatisfaction – occupancy rates (at 90%+) speakvolumes! As the only reason, “like it so much” is

farcical

Diamond hato flex recap

down to max

POST ROAD CAPITAL

8/10/2019 Diamond Resorts Post Road Capital Long Case

http://slidepdf.com/reader/full/diamond-resorts-post-road-capital-long-case 7/22

The Sales Pitch

• Had to wait an hour with a sales rep before getting a quote

• Free vacation tour as long as you come with your spouse,

make over $50,000 and bring a credit card with you. Youmust sit through a 3 hr. sales pitch

• President Obama made Cloobeck Chairman title of USCorporation for Travel Promotion (major donor)

•

Video clips of Cloobeck in ABC’s Undercover Boss

•

When compared with traditional online booking,Expedia.com and other websites were cheaper withoutpaying a VIS membership

• Most hotels and resorts can be booked online

• DRII’s customers are now aware of online travel agencies

8/10/2019 Diamond Resorts Post Road Capital Long Case

http://slidepdf.com/reader/full/diamond-resorts-post-road-capital-long-case 8/22

The Sales Pitch•

We signed up online and soon got a call. No wasted time! Roughly70% are from “existing” owners who are already at the resort. WYNand VAC percentages are similar

•

DRII does not give away free vacations, but offers mini vacations -standard industry practice. Customers can leave anytime and thepitch runs 1-2 hours. Only 14% convert. Not 100%! Minimum incomeis $60k (NOT $50k). No industry peer accepts cash

• Cloobeck’s gov’t appt.: Relevance? Same for Jeffrey Immelt,Steven Rattner, Penny Pritzker, etc. Not bad company

•

Undercover Boss appearance – Relevance??? Go see a resort and

see the maniacal focus on quality of product and experience! Wehave

• Yes: Most hotels and resorts can be booked online. Relevance???

•

Expedia.com (and other OTAs) are partners of DRII. Same for WYN,VAC et al. Many clients START as hotel-like guests but become

members. Diamond is an innovative technology focused company.We would be concerned if there was NOT an online presence

Best-in-class mDavid Palmer Alan Bentley (

Exceptional oextensive M&Aprivate equity

POST ROAD CAPITAL

8/10/2019 Diamond Resorts Post Road Capital Long Case

http://slidepdf.com/reader/full/diamond-resorts-post-road-capital-long-case 9/22

97% Retention?

•

Reviews• Owners are trying to give their timeshare away after paying $20,000 plus in

(for free). I realize now Diamond Resorts run a scam… I should have done m research before purchasing, but being a senior citizen, I was not preparedkind of overcharging.

On Yelp, comments such as:

• Diamond Resort Facebook users polled that 93.6% would not join again or reco

product to a friend.

8/10/2019 Diamond Resorts Post Road Capital Long Case

http://slidepdf.com/reader/full/diamond-resorts-post-road-capital-long-case 10/22

97% RetentionDue to historical industry practices, the timeshare industry has detractors. Every company has negative reviews. But DRII in particular, with its acquisitions of underperforming / failing resortsof naysayers who do not want to or cannot pay for a better (yet more costly) experience. DRbe well respected in the timeshare community. For questions or concerns, check www.ARDA.

POST ROAD CAPITAL

Positive Negativ

We are dri members and are very happy with them weget many hotels with them knowing accommodation isfirst class, we know how to ‘work the system’ and don’tfeel connected, I don’t understand anyone signing upand paying for ANYTHING without looking into it properly Inoticed not many of the very happy members havebeen printed, is it a conspiracy from other timeshares (yesit does happen) to print negative things

- Nov 19, 2014 tripadvisor.com

Attention all DRI owners...if your maintenplease contact the Arizona Real Estate D…and file a formal complaint. Our fees haper year for the last 3 years. We were comember of Diamond Resorts, telling us wincrease is 44.5% over what we paid in 2OUTRAGEOUS!

-Oct. 4, 2013 yelp.com

...The location to restaurants and Colonial Williamsburg isgreat.

It was a good week for us, and a memorable one. Mymom suffered a stroke and passed just 11 days after wereturned home so this vacation will have special meaningto us for years to come.

-February 3, 2012 tripadvisor.com

I purchased Wyndham Timeshares over stopped paying through the nose yet! Th

you and I was even told at one point I wmore points! This has been my greatest rrooms I want, where I want, when I wantadditional fees! It is a vicious cycle to robbetter off investing your money and/or swould not recommend this company toget out of these contracts please let me

--Aug 8, 2014 consumeraffairs.com

We are owners of this Marriott Timeshare facility and lookforward to staying here anytime we can. We especiallylike to have family or friends with us as this facility has it alland if you didn't want to go off property, you wouldn't

have to for anything. …

- January 2014, tripadvisor.com

Scam is right! Marriot runs this game andchoose. Who is to say in another 5 years another scheme that makes your points use as your weeks are now. Join the clas

in May 2014!

-July 11, 2014 tripadvisor.com

8/10/2019 Diamond Resorts Post Road Capital Long Case

http://slidepdf.com/reader/full/diamond-resorts-post-road-capital-long-case 11/22

Secondary Marketplace

• On sites such as Redweek.com and ebay.com,members are selling their time shares at literally

nothing

• DRII is threatening the users for not paying themembership fee or their loans

•

The secondary market effectively competes againstDRII’s VIS

8/10/2019 Diamond Resorts Post Road Capital Long Case

http://slidepdf.com/reader/full/diamond-resorts-post-road-capital-long-case 12/22

Secondary Marketplace - TINY

• First and foremost, though the secondary marketexists, it is de minimis and exists for all timeshareproviders

• Diamond does not threaten its members. Rather, as

with WYN et al., it sees every point of contact as anopportunity for a sale. DRII has NEVER taken amember to court

• Diamond specifically protects its primary networkand purposely makes sure the asset has limited

resale value

POST ROAD CAPITAL

8/10/2019 Diamond Resorts Post Road Capital Long Case

http://slidepdf.com/reader/full/diamond-resorts-post-road-capital-long-case 13/22

37.5% of Loans are in Default

•

According to DRII’s 10-K, as of December 31, 2013, DRII’s loan portfolio was comapproximately 72,000 loans with an outstanding aggregate loan balance of ap

$723.0 million. Approximately 45,000 of these consumer loans are loans under wconsumer was not in default, and the average balance of such loans was appr$10,663. Approximately 27,000 loans within the loan portfolio are loans that werehad not yet been foreclosed upon or canceled

8/10/2019 Diamond Resorts Post Road Capital Long Case

http://slidepdf.com/reader/full/diamond-resorts-post-road-capital-long-case 14/22

Diamond is OVER reserved on their loan portfolio

•

This student attempts to tie together two irrelevant data points from the 10-K without readfootnotes (see Note 5 and Note 16). In addition, an investor can not evaluate a loan portrandom point in time --- it must be looked at as a static pool

•

Let’s stick to the facts:

•

45k loans exist (on 515k members) = 8.9% of members have loans or 91.1% do not havoutstanding

•

The $243mn of defaulted loans has NOTHING to do with DRII’s owned or securitized loof the loan portfolio acquisition (from Tempus), $210MM was ALREADY in default. THISthat provides VERY INEXPENSIVE INVENTORY – we expect more information in the nex

•

Any loan past 180 days is immediately written off!•

Our analysis below shows DRII is 22% reserved on their cumulative portfolio…which is V

POST ROAD CAPITAL

8/10/2019 Diamond Resorts Post Road Capital Long Case

http://slidepdf.com/reader/full/diamond-resorts-post-road-capital-long-case 15/22

The Problem

• Current provision rate is only ~9% of sales

• Cost of marketing is ~50% regardless of whether

member defaults

•

Net revenues and earnings are grossly overstated

•

DRII securitizes some of its mortgages to obtaincash flow.

• Its mortgage receivable asset is not accurate and

should be written off

Key takeaway: DRII did not learn from the housingcrisis. Ability to pay is very different than willingness

to pay.

8/10/2019 Diamond Resorts Post Road Capital Long Case

http://slidepdf.com/reader/full/diamond-resorts-post-road-capital-long-case 16/22

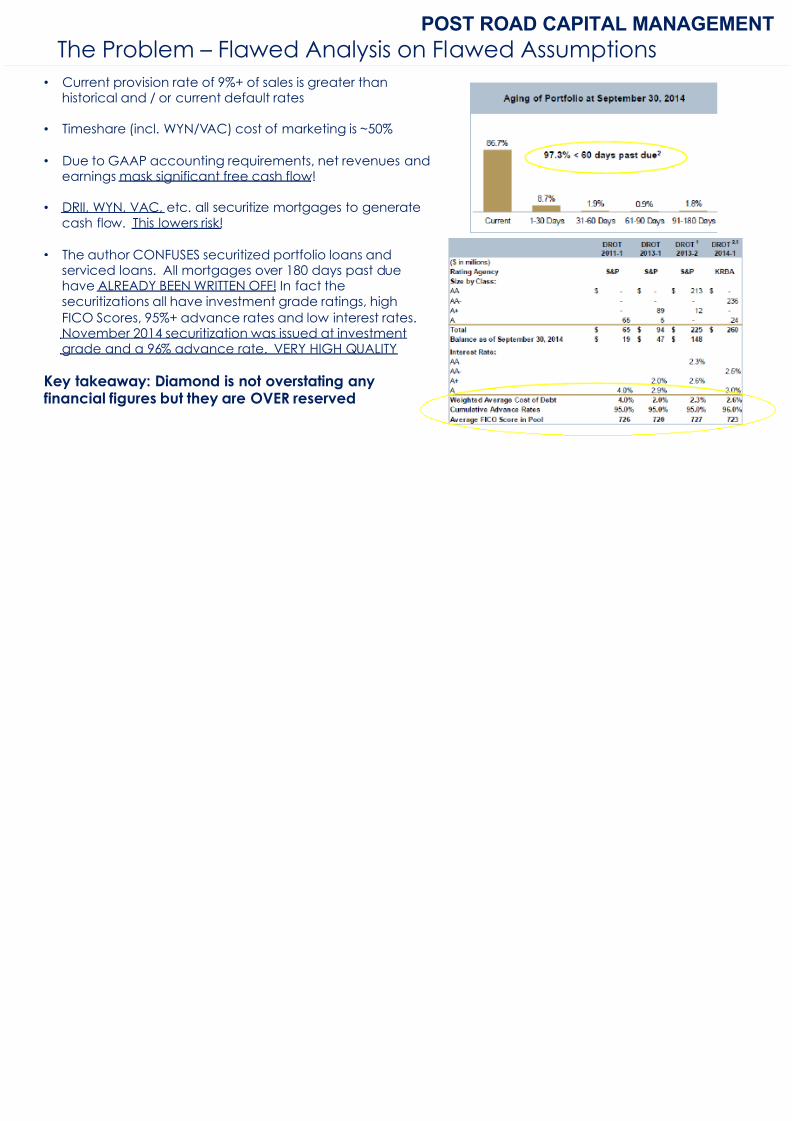

The Problem – Flawed Analysis on Flawed Assumptio

• Current provision rate of 9%+ of sales is greater thanhistorical and / or current default rates

•

Timeshare (incl. WYN/VAC) cost of marketing is ~50%

• Due to GAAP accounting requirements, net revenues andearnings mask significant free cash flow!

•

DRII, WYN, VAC, etc. all securitize mortgages to generatecash flow. This lowers risk!

•

The author CONFUSES securitized portfolio loans andserviced loans. All mortgages over 180 days past duehave ALREADY BEEN WRITTEN OFF! In fact thesecuritizations all have investment grade ratings, high

FICO Scores, 95%+ advance rates and low interest rates.November 2014 securitization was issued at investmentgrade and a 96% advance rate. VERY HIGH QUALITY

Key takeaway: Diamond is not overstating anyfinancial figures but they are OVER reserved

POST ROAD CAPITAL

8/10/2019 Diamond Resorts Post Road Capital Long Case

http://slidepdf.com/reader/full/diamond-resorts-post-road-capital-long-case 17/22

Declining Membership

• The SEC on February 22, 2013, wrote to DRII’s inregards to the confidential draft registration:

“Please balance your discussion of your strategy to increase membership in THE Club

with the fact that you experienced lowermember count in the club for the period

ended September 30, 2012”.

•

Q3 gain was after the acquisition of PMRwhere they gained ~25,000 members

•

DRII has lost approximately ~2% of its NET

members each quarter. This is very alarmingsince their VIS sales are up over 50% growth

rate for 2013 and over 15% for the past 3quarters.

POST ROAD CAPITAL

8/10/2019 Diamond Resorts Post Road Capital Long Case

http://slidepdf.com/reader/full/diamond-resorts-post-road-capital-long-case 18/22

Focus on the Relevant Key Performance Indicators!

• The SEC statement is a two year-old statement on(due to M&A) what was a rapidly changing portfolio

•

Q3 2013 gain was only partially due to acquisitions.

But investors need to know:

• In the past couple of years, management hasacquired many distressed timesharecompanies, which results in high-grading theportfolio. This will naturally increase near-termchurn since a portion of acquired owners were

of lower quality (and in many cases were indefault) This is good churn, not bad! Average

transactions size is up (over several years) from~ $10,500 to over $19,000!

• The 2% quarterly churn figure is WRONG! Postexpected churn, we think organic growth is around0-4% with regular volatility/seasonality in timing. Thisis very in line with industry peers and allows for

significant revenue and earnings growth

POST ROAD CAPITAL

8/10/2019 Diamond Resorts Post Road Capital Long Case

http://slidepdf.com/reader/full/diamond-resorts-post-road-capital-long-case 19/22

Valuation

•

After adjusting DRII’s earnings with aprovision rate reflective of the state of

the business, DRII trades at 91x 2015Eand 107x 2016E

• DRII will point out at cash flow growth.There are two problems: (1) 2014 cashflow growth comes frommanagement fees at the expense of

very large investments in previous

years, and (2) $50M of that cash flowis from savings from financing throughsecuritization, already reflecting aone-time gain

!"# $%&&' $%&$' $%&('

-./00 !23245/6 "647.704 #2870 ! "" #$! " $ "% #& && & '( #! %$

,-./0 10 .2 ")#&)! !&#*&+ **#)+'

45 -67 80 29 5 2: .8;7 - <.1 81 +"#+$+ "&+#$'( !&%#"'!

=>? @-.11 ,-.A08 "!$#'!! "$&#+%( !')#&""

452597B728 ?7-/0<71 C7/72D7 E "* %#(+ + E "+ +#$) * E !' %#"$ "

F.1 8 .A B5 2597B728 1 7-/0<71 !+#"!& $&#$$' $+#('+

45 25 97 B7 28 @- .1 1 , -. A0 8 E (* #') ( E "" "# +!$ E "$ &# %( "

G.85 H F.-I.-5 87 JKI7 21 71 "$*#!(& "&!#'!! !&'#&!*

9:7.2456; "63/<7 =$>?@, @+>)@% @&>=?=

>287-718 7KI7217 %!#'"' ()#"&+ %%#)!)

J5-20291 L7A.-7 85K71 +%) M))+N $#!&!

G5K71 M(#&"+N M"*#$"'N &#+++

A74 "63/<7 B&%>(%( B&(>,)( CB$>+$+D

!"#$%&%#' )& * #+ ,"#&& &)-.& /01* 102* 101*

!"#$ &'() *"'+",-(. /0112 /01/2 /0132 !"#$ &'() &*(+ ,-.*"/0(1# 23424 453677 893572:

!" -. ? " 1@ (/ $. * A 1B. #/ +. 1/ # 8< 72 3> 77 : 86 23 ;; >: 89 =3 24 9:

C*.. D"#$ &'() 8<77397>: 8553=;>: 86;3;;5:

!"! $%&'(

A required 8% cash flow rate in 2015 in a declining cash flow business (since VIS havvalues DRII ~$12. However these cash flows are a result from earlier investments and

underlying business economics. A P/E multiple places the stock much lower.

POST ROAD CAPITAL

8/10/2019 Diamond Resorts Post Road Capital Long Case

http://slidepdf.com/reader/full/diamond-resorts-post-road-capital-long-case 20/22

Valuation•

Due to the faulty default rate analysis, the report has outsized provision coststhat are nonsensical. The student’s EPS is irrelevant

•

Cash flow growth comes only partially from a vastly lower interest rate oncorporate debt as well as recently acquired (2013) properties at 1 to 2x

EBITDA. The “$50M of that cash flow” is nowhere to be found in any of thefinancial statements. As shown to the right, the free cash flow inflection ispowerful and sustainable

•

VOI sales have NOT started to peak. The statement is wholly inaccurate!

• An asset-light quality, real estate based business should trade at a 6% to 8%free cash flow yield. At this multiple, DRII would trade at at $48 to $64 on2015 figures and materially higher on 2016. ALL OF THIS ignores that debt /

EBITDA will be under 1x by year-end 2015! We need only be half right on ourexpectations for this stock to be at least a double

•

ALL competitors trade on EBITDA and free cash flow multiples making the“P/E” multiple less relevant though better than what his report implies

POST ROAD CAPITAL

8/10/2019 Diamond Resorts Post Road Capital Long Case

http://slidepdf.com/reader/full/diamond-resorts-post-road-capital-long-case 21/22

Insider Selling and Deceiving Investor Community

•

Stephen Cloobeck and other investors announced to sale some of their sharesbeen especially active trying to attract investors

•

Management mentions in its latest roadshows: “For the first six months of 2014 w$81.5 million in cash…The primary source of cash generated during the six-monfrom earnings”.

• Not true. It was through an increase in due to related parties (~$45M) and cash flow from financing (~$38M)

• Misleading with its 3.5% inventory recapture rate

•

The company hides facts about their declining membership status or its defaul

mangelo@Wha

POST ROAD CAPITAL

8/10/2019 Diamond Resorts Post Road Capital Long Case

http://slidepdf.com/reader/full/diamond-resorts-post-road-capital-long-case 22/22

Shareholder Friendly and Aligned Management Tea

• Stephen Cloobeck and other insiders are hesitant to sell shares at these levels. 10b5-1). Insiders/Executive Management own over 30% of the shares outstand

and his senior team have ZERO intention of selling stock in the near future

• The student is analytically WRONG in regard to free cash flow, which we legitimOVER $200 million in 2014 and a run-rate of over $250 million going into 2015

•

DRII has entered a period of massive free cash flow growth, which makes it a munder-levered company

•

The company trades at a material valuation gap (relative and absolute) to its its superior economic returns and comparable product offering

•

Multiple ways to win a) valuation gap closes, b) returning capital to shareholde

announced $100mn buyback), c) make accretive acquisitions (with leverage)private equity or other strategic will buy Diamond

David Eigen -- [email protected] Nat Brogadir -- NGB@po

POST ROAD CAPITAL