DHRUVA DAILY - law.practiceleague.com

53

JULY 20 VOLUME 80 DHRUVA DAILY

Transcript of DHRUVA DAILY - law.practiceleague.com

1 Dhruva Daily Volume 80 This document is for internal purposes only

JULY 20

VOLUME 80

DHRUVA DAILY

2 Dhruva Daily Volume 80 This document is for internal purposes only

Table of Contents 1. Domestic Taxation - 1 ...................................................................................................................................................................... 3

2. Domestic Taxation – 2 ..................................................................................................................................................................... 5

3. International Taxation ..................................................................................................................................................................... 7

4. SEBI .................................................................................................................................................................................................. 8

5. GST ................................................................................................................................................................................................. 10

3 Dhruva Daily Volume 80 This document is for internal purposes only

1. Domestic Taxation - 1 Sr No

Particulars of the update

Summary of technical development

Brief comments on impact Weblink for further reading

1 Press Release dated 18 July 2020 – CBDT to start e-campaign on voluntary compliance of Income-tax for FY 2018-19 from 20 July 2020

The CBDT has issued a press release to start e-campaign on voluntary compliance of Income-tax for FY 2018-19. The e-campaign starts from today i.e. 20 July 2020 and ends on 31 July 2020. The objective is to validate the information available with the Income-tax Department and promote voluntary compliance, so that taxpayers do not get scrutiny notices. The Income-tax Department will send email/sms to identified taxpayers to verify information like specified financial transactions, TDS, TCS, foreign remittances, etc. The information will be accessible on Compliance Portal and response is to be submitted against the same.

The details of transactions provided by the Income-tax department through this e-campaign will be useful for the assessee’s in case they may be required to file/revise their return for FY 2018-19 for which time period has been extended upto 31 July 2020 Further, the information may be helpful in avoiding any re-opening of cases later on.

Weblink

2 Press Release by CBDT - New Form 26AS - the Faceless hand - holding of taxpayers, facilitates voluntary compliance, ease of e-filing returns

CBDT issues press release: “The new Form 26AS is the faceless hand-holding of the taxpayers to e-file their income tax returns quickly and correctly.” Explains that various information such as cash deposit/withdrawal from saving bank accounts, sale/purchase of immovable property, time deposits, credit card payments, purchase of shares, debentures, foreign currency, mutual funds, buy back of shares, cash payment for goods and services, etc., which was received by the Dept. w.r.t individuals having high-value financial

Weblink

4 Dhruva Daily Volume 80 This document is for internal purposes only

Sr No

Particulars of the update

Summary of technical development

Brief comments on impact Weblink for further reading

transactions since the Financial Year 2016 onwards, would now form part of the new form 26AS. Remarks that “the information being received by the IT Department from the filers of these specified SFTs is now being shown in Part E of Form 26AS to facilitate voluntary compliance, tax accountability and ease of e-filing of returns”.

3 Savita Kapila (Legal Heir of Late Shri Mohinder Paul Kapila) v. ACIT TS-343-HC-2020 (Delhi) Date of order: 16 July 2020 Notice under section 148 in name of dead person is bad in law. Legal Representatives not liable to intimate assessee’s death.

In the given case, notice under section 148 was issued in name of deceased assessee. The re-assessment order was passed in name and PAN of the legal heir The HC observed that there is no statutory requirement imposing an obligation upon legal heirs to intimate the death of the assessee. Section 292B does not cover the issuance of notice upon a dead person under the ambit of mistake, defect or omission. Section 292BB is applicable to the assessee and not to a legal representative. Accordingly, the HC held that it is settled position of law that notice under section 148 issued in name of dead person is bad in law and consequently, the proceedings need to be quashed.

Notice under section 148 issued in name of dead person is bad in law and cannot be cured by section 292B or 292BB of the Act.

Weblink

5 Dhruva Daily Volume 80 This document is for internal purposes only

2. Domestic Taxation – 2 Sr No

Name of case law and brief ratio

Summary of technical development Weblink for further reading

1 Alishan Palace Resorts Pvt Ltd V/s ITO Ward 1(3), Bhubaneswar ITA No. 114/CTK/2019 (2020 (7) TMI 393 - ITAT Cuttack) Assessee can exercise his right to choose any method for valuation of unquoted equity shares under Rule 11UA

The assessee used the DCF method for valuation of its unquoted equity shares and issued them at a premium of INR 40/- per share. The AO was of the view that the computation of FMV was not in accordance with Rule 11UA and therefore computed the FMV at INR 31.96/- using book value method and treated the differential amount received as income under Section 56(2)(viib). ITAT decide the issue in favour of the assessee and held that as per Rule 11UA the assessee has the option to choose any method either discounted or book value method for estimating the FMV of the shares. The ITAT observed that the AO has not challenged the valuation done by the assessee under the DCF but has merely compelled the assessee to change the valuation method from DCF method to book value method, which is not permissible as per Rule 11UA and other provisions of the Act.

Weblink

2 The Commissioner of Income Tax LTU, The Asst. Commissioner of Income Tax Central Circle – 19 New Delhi v/s M/s ABB Ltd ITA No. 134 of 2011 (2020 (7) TMI 398 – Karnataka High Court)

The assessee is engaged in the business of manufacture of field instrumentation and is a promoter of M/s Gujarat Instruments Ltd which is an associate company. The associate company went into liquidation and the assessee wrote off the investment made in the said concern as bad debts. The AO was of the view that the loss suffered by the assessee should be treated as capital loss. The decision was upheld by the CIT(A). The ITAT relying on the decision of the SC in case of T.R.F Ltd. V/s. CIT, held that writing off bad debt as irrecoverable in the accounts of the assessee is sufficient and therefore assessee was entitled to a deduction. The HC held that the manner of writing off of the debt was neither examined by the AO, CIT(A) nor the Tribunal. Thus the finding of ITAT that the assessee is entitled to the benefit of capital loss is set aside and matter was remitted back to the AO who shall decide the same relying on the law laid down by SC in T.R.F Ltd.

Weblink

6 Dhruva Daily Volume 80 This document is for internal purposes only

Sr No

Name of case law and brief ratio

Summary of technical development Weblink for further reading

3 Reimbursement of Expenses – A Deep Dive into Taxability Enigma (Source: Taxsutra)

In this article, the authors have covered the controversy revolving around taxability of reimbursement in hands of recipient and consequent withholding tax obligation in the hands of payer. Further the authors also discuss a few legal jurisprudences on the issue in different scenarios and consequences of not withholding taxes on the same.

Weblink

7 Dhruva Daily Volume 80 This document is for internal purposes only

3. International Taxation Sr No

Particulars of the update

Summary of technical development Weblink for further reading

1. IMS AG [ITA No.6445/Mum/2016]

The Mumbai Bench of ITAT has in the case of IMG AG, a Swiss tax resident, held that consideration for granting access to database is not royalty under Article 12(3) of India-Swiss Tax Treaty. The assessee company was engaged in providing market research report on pharmaceutical sector to its customers across the world at a predetermined subscription prices. The licence access so granted was non-exclusive and non-transferable, conferring access to the database and IMS reports (review reports). The Bench relied on the Bombay High Court’s ruling in the case of DIT Vs Dun and Breadstreet Information Services India Pvt Ltd [(2012) 20 taxmann.695 (Mum)], which dealt with India-Spain Tax Treaty, provisions of which are analogous. In the context of pronouncement of rulings after the expiry of 90 days from the date of conclusion of hearing, the Bench observed that the period of lockdown cannot be treated as an ordinary period during which the normal time limits are to remain in force. It held the period during which lockout was in force is to excluded for the purpose of time limits set out in rule 34(5) of the Appellate Tribunal Rules, 1963.

Weblink

8 Dhruva Daily Volume 80 This document is for internal purposes only

4. SEBI Sr No

Particulars of the update

Summary of technical development Brief comments on impact

Weblink for further reading

1

SEBI Informal Guidance : SEBI (Share based Employee Benefits) Regulations, 2014 (‘SBEB Regulations’)

Facts • Way to Wealth Brokers Pvt Ltd (‘ the applicant’)

is a Intermediary registered with SEBI as a stock broker.

• A listed company has approached the applicant, a registered stock broker, for cashless funding of Restricted Stock Units (‘RSUs’) being offered to their employees as a part of Employee compensation plan.

• The current market price per share is Rs 650. The RSUs are being issued to eligible employees at face value per share i.e. Rs 5. As per the approved scheme, employee is required to pay the issue price plus the applicable perquisite tax for exercise quantity of RSU.

• However, in case employees who wish to avail cashless funding, the funding amount would be credited by applicant to employee bank account and onward transfer to company account, and company would credit RSU shares directly to the DP Account of employee held with the applicant

• Within 2 working days of credit of shares to the DP account of employee, the RSU shares to the extent of cashless funding plus transaction charges would be sold and sale proceeds would be adjusted towards cashless funding made by the applicant.

Empanelled stockbrokers are permitted to fund the securities issued by a listed company under SBEB Regulations (viz. ESOP / RSU) to its employees who propose to avail cashless option under SBEB Regulations. There is no cap on amount per unit/ security that can be funded by stockbrokers.

Weblink

9 Dhruva Daily Volume 80 This document is for internal purposes only

Query • Whether registered stock broker are permitted

to fund the securities issued under SBEB Regulations (viz. ESOP / RSU) by a listed company to its employees who propose to avail cashless option?

• What is the maximum amount per unit/ security that can be funded?

SEBI Response

• As per Regulation 9(2) of the SBEB Regulations, the company may permit the empanelled stock brokers to fund the payment of exercise price which shall be adjusted against the sale proceeds of some or all the shares by the employees.

• SBEB Regulations do not prescribe for any maximum limit on amount per unit/ security that can be funded.

10 Dhruva Daily Volume 80 This document is for internal purposes only

5. GST Sr No

Particulars of the update

Summary of technical development Weblink for further reading

1 Madhya Pradesh Authority for Advance Rulings in the case of M/s Jabalpur Hotels Private Limited – Case No. 29/2019, Order No. 10/2020 dated 8 June 2020

The Applicant is in Hotel business among other businesses and the Applicant has purchased and installed lift for its hotel building. The Applicant desires to know whether he can avail ITC paid on lift.

As per the Applicant, the lift falls under the definition of “Plant and Machinery” and hence, GST paid on such lift should be restricted under Section 17(5)(d) of the CGST Act, 2017.

a) The AAR Authority held that lift is an “input” for hotel building and hotel building being an immovable property, any input or input service going into its construction shall not be available for availment of input tax credit.

Weblink

2 High Court of Gujarat at Ahmedabad – M/s. Cera Sanitaryware Limited - R/Special Civil Application NO. 8050 of 2020

The Petitioner has received notice in Form DRC-01A under Section 74(5) of the CGST Act, 2017. The Petitioner is requesting to quash or set aside the said notice on the grounds that the notice issued is illegal.

The High Court held that the request of the Petitioner is not maintainable in law, as the notice is just an intimation and it is up to the Petitioner if he wants to ignore it. If ignored, a show cause notice may follow and the Petitioner will be given an opportunity of hearing.

Weblink

3 The Authority for Advance Ruling of Madhya Pradesh in the case of M/s Methodex Systems Private Limited [Applicant] - Advance Ruling No. 08/ 2020 dated March 3, 2020

The Applicant issued a contract for supply, installation and fixing of customized furniture for newly constructed building by the government department of State Government. Intends. Accordingly, the Applicant has sought advance ruling on whether "supply, installation and fixing of customized furniture in a building" is a composite supply of goods or in the nature of works contract, and applicable rate of GST on the said supply. In this regard, the Authority observed and held as under:

Weblink

11 Dhruva Daily Volume 80 This document is for internal purposes only

Sr No

Particulars of the update

Summary of technical development Weblink for further reading

a) The supply, installation and fixing of furniture cannot be a works contract, as the items of furniture have been made or manufactured at the supplier's place which have been installed or fixed at the place of the recipient. Such installed or fixed items of furniture can be removed/ moved to any place without damage to the furniture. Thus, supply, installation and fixing of furniture cannot be covered under works contract, as it does not result in immovable property or it is not going to be part of immovable property.

b) The contract in questions conform to the "Composite Supply" as provided in section 2(30) of CGST Act. The supply made by the applicant to the govt. department consists of two taxable supplies of goods and services, which are naturally bundled and supplied in conjunction with each other where the supply of goods viz furniture is the principal supply.

c) In view of the above, the goods shall merit classification under Chapter Head 9403 of GST Tariff and shall be liable to GST at the rate applicable at the time of supply

4 The Authority for Advance Ruling of Madhya Pradesh in the case of M/s V E Commercial Vehicles Limited [Applicant] - Advance Ruling No. 09/ 2020 dated June 2, 2020

The Applicant is engaged in various busines including manufacturing of chassis trucks & buses, engines, bus body and automotive components. The Applicant has sought an advance ruling on whether supply of services in respect of activity of mounting/ fabrication of bodies on chassis provided by Customer should be treated as supply of bus or provision of services wherein the said activity of mounting/ fabrication is outsourced to the Applicant by owner/provider of chassis in following two scenarios:

• The chassis is originally manufactured by one of the unit of the Applicant registered separately as distinct person under GST Act and sold to provider of chassis receiving the chassis for fabrication of body.

• The chassis is originally manufactured by some other OEM and sold to provider of chassis before receiving the chassis for fabrication of body.

In this regard, the Authority observed that the question raised by the Applicant is essentially whether mounting of bus/ truck body by the job worker on the chassis

Weblink

12 Dhruva Daily Volume 80 This document is for internal purposes only

Sr No

Particulars of the update

Summary of technical development Weblink for further reading

supplied by the principal for which the applicant charged fabrication charges including cost of certain material that was consumed during the process of job work would be classified as supply of service under HSN 9988". Thus, the Authority held as under:

a) Circular No. 52/68/2018-GST in para 12.2 (a) clarifies with regard to bus-body builder who builds a bus working on chassis owned by them and supply the build-up bus to customer that the said supply is that of vehicle and attract GST applicable to the vehicle. Circular further clarifies in para 12.2 (b) for bus-body builder who builds body on chassis provided by principal for body building and charges fabrication charges that the said supply would merit classification as service and will attract GST at 18%. In the instant case, nature of work undertaken by the Applicant clearly falls under Para 12.2(b) of the aforementioned circular.

b) In the supply towards provision of services in respect of activity of mounting/ fabrication of bodies on chassis provided by Customer wherein the said activity of mounting/fabrication is outsourced to the Applicant by owner/provider of chassis, in no case the ownership of the chassis belongs to the Applicant. Hence, in both the scenarios mentioned in the question will be taxable under SAC 998881 - "Motor vehicle and trailer manufacturing owned by other" at the rate of 18%.

13 Dhruva Daily Volume 80 This document is for internal purposes only

END Confidential: This document is for your internal use only and may not be copied or distributed to any third party © Dhruva Advisors LLP

1 Dhruva Daily Volume 81 This document is for internal purposes only

JULY 21

VOLUME 81

DHRUVA DAILY

2 Dhruva Daily Volume 81 This document is for internal purposes only

Table of Contents 1. Domestic Taxation - 1 ...................................................................................................................................................................... 3

2. Domestic Taxation – 2 ..................................................................................................................................................................... 4

3. International Taxation ..................................................................................................................................................................... 5

4. Customs / Foreign Trade Policy ..................................................................................................................................................... 6

5. Singapore and Asian tax updates .................................................................................................................................................. 8

3 Dhruva Daily Volume 81 This document is for internal purposes only

1. Domestic Taxation - 1 Sr No

Particulars of the update

Summary of technical development

Weblink for further reading

1 Tying Up Philanthropy – A Guide To Amended Provisions For Registration Of Charitable Trusts/ Institutions Under The Income Tax Act, 1961 By: CA Pranshu Singhal Date: 10 July 2020 Source: ITAT online

The author has prepared a guide in which he has explained the various amendments ushered in by the Finance Act, 2020 to the law on registration of charitable trusts and institutions under the Income Tax Act, 1961. He has highlighted the problems that the entities are likely to face and also offered suggestions on the remedies available. The recent amendments announced by the Finance Minister in the wake of COVID-19 pandemic, as applicable to charitable entities, have been duly referred to by the author.

Weblink

4 Dhruva Daily Volume 81 This document is for internal purposes only

2. Domestic Taxation – 2 Sr No

Name of case law and brief ratio

Summary of technical development Weblink for further reading

1 ACIT v. New Delhi Young Men Christian Association 2020 (7) TMI 460 ITAT, Delhi

The Assessee is a Society registered under section 12A of the Act. Its basic aim is to promote spiritual, intellectual, physical and social interest amongst the youth. The Assessing Officer during the course of assessment proceedings observed that the Assessee is conducting several activities with an objective to maximize profits and on such basis, denied exemption under section 11 and 12 of the Act. The ITAT held that if in terms of the dominant and primary objectives of the Institution there was no desire to gain profits and the object was to promote trade and commerce not for itself but for the nation, it was to be construed as a charitable purpose and hence the Assessee qualified for exemption under section 11 and 12 of the Act.

Weblink

2 ESOPs to NR Employees - Navigating through 'Tax Complexities'. (Source: Taxsutra)

In this article, the author has broadly covered several aspects on taxation of ESOP and deals with various taxation challenges on ESOP taxation.

Weblink

5 Dhruva Daily Volume 81 This document is for internal purposes only

3. International Taxation Sr No

Particulars of the update

Summary of technical development Weblink for further reading

1. G20 finance ministers again pledge to agree on new multinational group tax rules by year-end

A virtual meeting of the G20 finance ministers was held on July 18, 2020. The G20 ministers, at their October meeting, intend to review the “blueprints” for both pillars approved by the Inclusive Framework team on BEPS. This blueprint will serve as the basis for both a public consultation, so that all stakeholders can provide their inputs and comments, followed by a final round of negotiation with a view to agreeing on a consensus based solution. The Secretary-General also noted that divergent views have been expressed by countries regarding potentially “decoupling” of pillar one and pillar two and about adopting a phased approach, starting with pillar one. While some G20/OECD Inclusive Framework members support the idea of independently agreeing and implementing the pillars, other members call for the adoption and implementation of the two pillars as a package, the Secretary-General said.

Weblink

2. FinMin rules out clarification, FAQ on ‘Google Tax’

The Finance Ministry has ruled out issuing any clarification or frequently asked questions on Equalization Levy, applicable on non-resident e-commerce companies. The total amount (without bifurcating the levy at the rate of 6 per cent on digital ad and 2 per cent on non resident e-commerce companies) collected in Equalization Levy so far this fiscal is around ₹200 crore. As per this news article, the Finance Ministry official has said that they will deal with the issues raised as and when it comes and has urged companies to work towards compliance.

Weblink

3. Ahmedabad ITAT : Web-hosting charges, not FIS under Indo-US DTAA | Esm Sys Pvt. Ltd v. ITO [TS-347-ITAT-2020(Ahd)]

The assessee made payment to non-resident for providing site promotional services like web designing, data promotion, social media management and general consulting. The non-resident person was managing and overseeing the various on page and off page activities which drive traffic to a specific website. The assessing officer treated the transaction in nature of ‘Fees for technical services’ or ‘royalty’ liable for withholding of taxes at source in India. The Tribunal relied upon judicial precedents and observed that in absence of ‘make available’ element, the transaction cannot be charged to tax as ‘Fees for Included Services’ under India-USA treaty.

Weblink

6 Dhruva Daily Volume 81 This document is for internal purposes only

4. Customs / Foreign Trade Policy Sr No

Particulars of the update

Summary of technical development Weblink for further reading

1 Foreign Trade Policy Notification No. 19/2015-2020 dated 15 July 2020 Amendment in Import Policy and Policy Conditions of items under Chapter 84 of ITC(HS), 2017, Schedule-I (Import Policy)

Import Policy of Power Tillers and its components covered under Chapter 8432 of the ITC has been amended from “Free” to “Restricted”.

Weblink

2 Foreign Trade Policy Public Notice No. 13/2015-2020 dated 15 July 2020 Procedure for allocation of Import Authorization of Power Tillers

Procedures to implement the restrictions imposed on import of power tillers and its components covered under Chapter 8432 have been notified in the Foreign Trade Policy Public Notice No. 13/2015-2020 dated 15 July 2020. This public notice inter alia prescribes conditions for issuance of authorization viz. cumulative value of authorization, past performance parameters, infrastructural requirements etc.

Weblink

3 Surat Rough Diamond Sourcing India Limited [TS-529-CESTAT-2020-CUST]

The dispute in this appeal relates to confiscation of rough diamonds imported by the assessee from its subsidiary company in UAE. The impugned diamonds were of Zimbabwe origin and were also accompanied by Kimberly Process Certificates (KPC) issued by Zimbabwe. The adjudicating authority stated that KPC Committee in its meeting (held in June 2011) had taken decision that diamonds procured from Zimbabwe prior to 17 November 2010 shall only be permitted to be imported by UAE. In the present case the subsidiary entity in UAE entered into negotiations for procuring diamonds from Zimbabwe prior to 17 November 2010 (for which KPCs

Weblink

7 Dhruva Daily Volume 81 This document is for internal purposes only

Sr No

Particulars of the update

Summary of technical development Weblink for further reading

were issued); however, sale invoice was issued on 20 January 2011 (i.e. after 17 November 2010). Accordingly, it was held by the adjudicating authority that the impugned diamonds are not permitted to be imported in India, hence are liable for confiscation. Ahmedabad bench of the CESTAT set aside the order confiscating impugned diamonds, and held that mere issuance of invoice after 17 November 2010 cannot be a ground to hold that the diamonds were banned from importation where it is undisputed that KPC were issued by Zimbabwe prior to 17 November 2010.

8 Dhruva Daily Volume 81 This document is for internal purposes only

5. Singapore and Asian tax updates Singapore: Update on Taxation of Individuals Sr No

Particulars of the update

Summary of technical development Brief comments on impact Weblink for further reading

1 Exemption for Employment Benefits for Accommodation, Food, Transport and Daily Necessities given by employer in Calendar Year 2020 due to COVID-19

Qualifying benefits that are eligible for the tax exemption

Cash allowance, reimbursement or benefits-in-kind for any of the following items:

• accommodation in Singapore (including the furniture and fittings); capped at S$75 per day per employee

• food, transport, and daily necessities for consumption in Singapore; capped at S$50 per day per employee

Due to the border restrictions imposed due to COVID-19, employees (normally residing outside Singapore e.g. Malaysia, who are required to reside in Singapore to ensure the continuity of employer’s business) receiving accommodation and related benefits will be tax exempt in Singapore subject to the satisfaction of certain conditions.

Weblink

Singapore: Income Tax Treatment of COVID-19-Related Payouts to Businesses and Individuals Sr No

Particulars of the update

Summary of technical development Weblink for further reading

1 Clarifications on tax treatment of COVID-19 related Payouts – whether taxable/ not taxable

Payouts that are not taxable: • meant to support individuals through the exceptional circumstances arising from the

COVID-19; • help employers retain their local employees by providing cashflow support • unconditional gifts Payouts to defray the operating costs of business are taxable

Weblink

9 Dhruva Daily Volume 81 This document is for internal purposes only

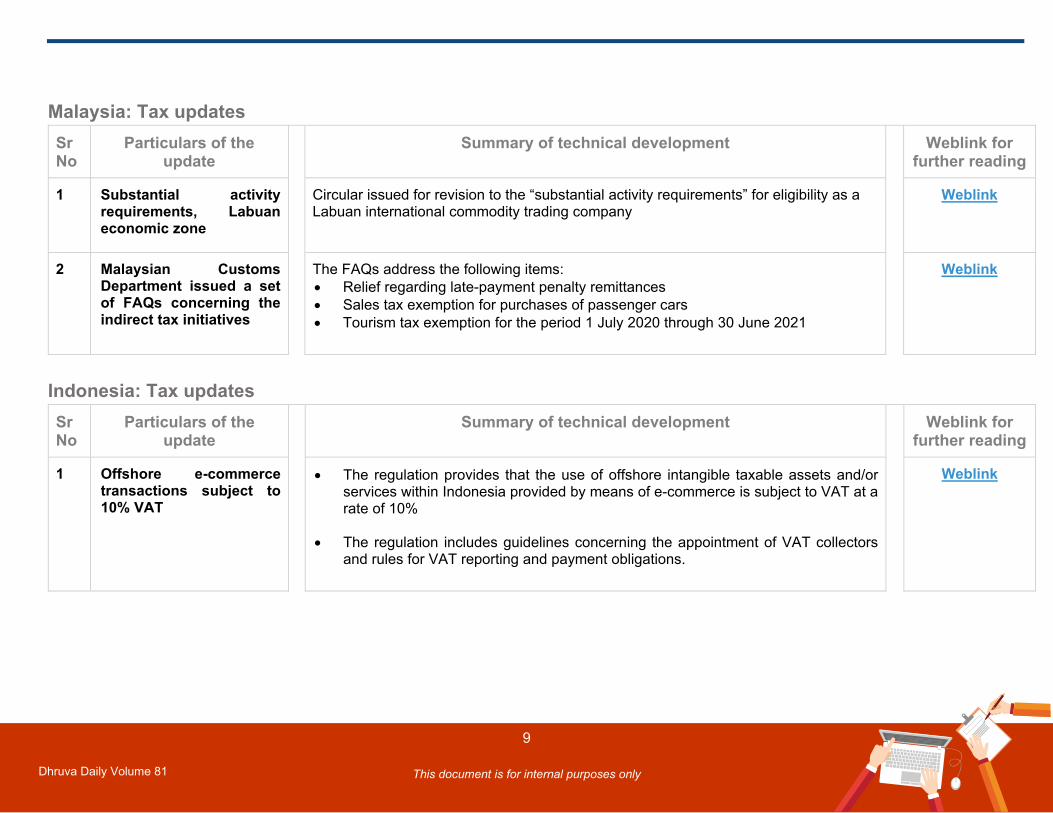

Malaysia: Tax updates Sr No

Particulars of the update

Summary of technical development Weblink for further reading

1 Substantial activity requirements, Labuan economic zone

Circular issued for revision to the “substantial activity requirements” for eligibility as a Labuan international commodity trading company

Weblink

2 Malaysian Customs Department issued a set of FAQs concerning the indirect tax initiatives

The FAQs address the following items: • Relief regarding late-payment penalty remittances • Sales tax exemption for purchases of passenger cars • Tourism tax exemption for the period 1 July 2020 through 30 June 2021

Weblink

Indonesia: Tax updates Sr No

Particulars of the update

Summary of technical development Weblink for further reading

1 Offshore e-commerce transactions subject to 10% VAT

• The regulation provides that the use of offshore intangible taxable assets and/or services within Indonesia provided by means of e-commerce is subject to VAT at a rate of 10%

• The regulation includes guidelines concerning the appointment of VAT collectors and rules for VAT reporting and payment obligations.

Weblink

10 Dhruva Daily Volume 81 This document is for internal purposes only

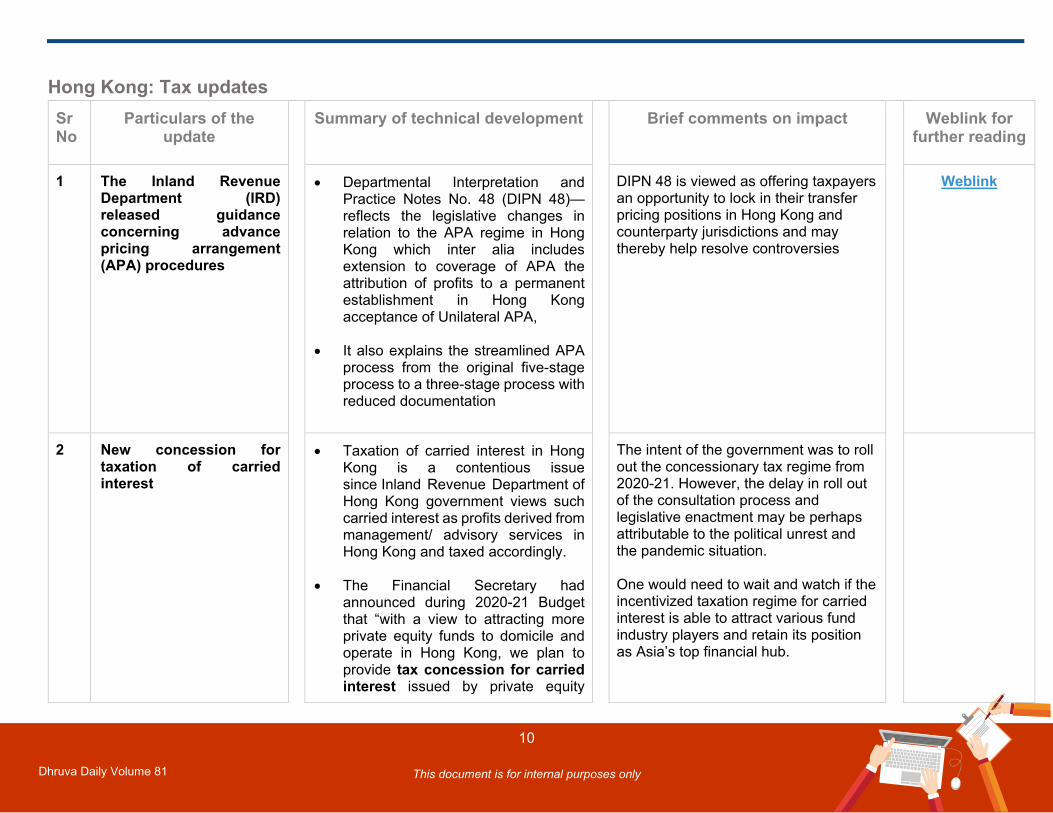

Hong Kong: Tax updates Sr No

Particulars of the update

Summary of technical development Brief comments on impact Weblink for further reading

1 The Inland Revenue Department (IRD) released guidance concerning advance pricing arrangement (APA) procedures

• Departmental Interpretation and Practice Notes No. 48 (DIPN 48)—reflects the legislative changes in relation to the APA regime in Hong Kong which inter alia includes extension to coverage of APA the attribution of profits to a permanent establishment in Hong Kong acceptance of Unilateral APA,

• It also explains the streamlined APA process from the original five-stage process to a three-stage process with reduced documentation

DIPN 48 is viewed as offering taxpayers an opportunity to lock in their transfer pricing positions in Hong Kong and counterparty jurisdictions and may thereby help resolve controversies

Weblink

2 New concession for taxation of carried interest

• Taxation of carried interest in Hong Kong is a contentious issue since Inland Revenue Department of Hong Kong government views such carried interest as profits derived from management/ advisory services in Hong Kong and taxed accordingly.

• The Financial Secretary had announced during 2020-21 Budget that “with a view to attracting more private equity funds to domicile and operate in Hong Kong, we plan to provide tax concession for carried interest issued by private equity

The intent of the government was to roll out the concessionary tax regime from 2020-21. However, the delay in roll out of the consultation process and legislative enactment may be perhaps attributable to the political unrest and the pandemic situation. One would need to wait and watch if the incentivized taxation regime for carried interest is able to attract various fund industry players and retain its position as Asia’s top financial hub.

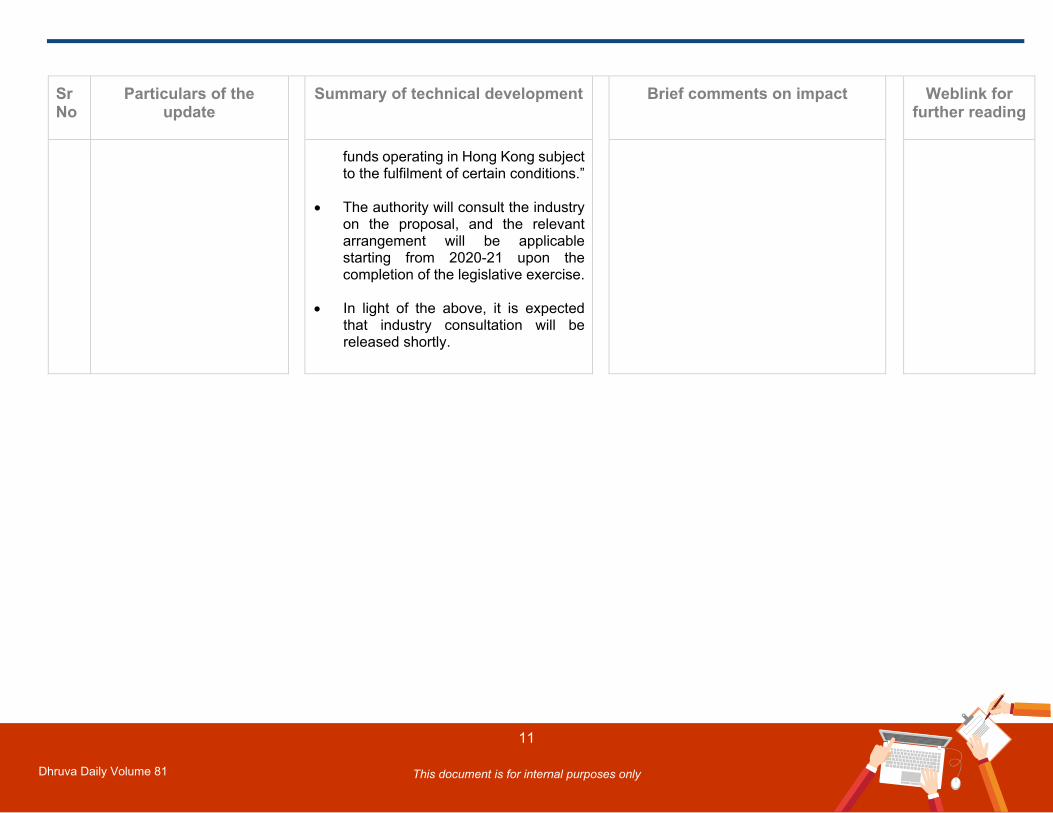

11 Dhruva Daily Volume 81 This document is for internal purposes only

Sr No

Particulars of the update

Summary of technical development Brief comments on impact Weblink for further reading

funds operating in Hong Kong subject to the fulfilment of certain conditions.”

• The authority will consult the industry on the proposal, and the relevant arrangement will be applicable starting from 2020-21 upon the completion of the legislative exercise.

• In light of the above, it is expected that industry consultation will be released shortly.

12 Dhruva Daily Volume 81 This document is for internal purposes only

END Confidential: This document is for your internal use only and may not be copied or distributed to any third party © Dhruva Advisors LLP

1 Dhruva Daily Volume 82 This document is for internal purposes only

JULY 22

VOLUME 82

DHRUVA DAILY

2 Dhruva Daily Volume 82 This document is for internal purposes only

Table of Contents 1. Domestic Taxation - 1 ...................................................................................................................................................................... 3

2. Domestic Taxation – 2 ..................................................................................................................................................................... 4

3. International Taxation ..................................................................................................................................................................... 5

4. SEBI .................................................................................................................................................................................................. 6

5. GST ................................................................................................................................................................................................... 8

3 Dhruva Daily Volume 82 This document is for internal purposes only

1. Domestic Taxation - 1 Sr No

Particulars of the update Summary of technical development

Weblink for further reading

1 Shri Pranav Kumar Rajnikantbhai Kankhara Shri Ram v. ITO [2020] 7 TMI 490 (ITAT Rajkot) Date of order: 1 June 2020 Additions made on presumption basis under section 44AD do not automatically justify levy of penalty under section 271(1)(c) if there is no conscious concealment of income or furnishing of inaccurate particulars of income.

During the course of assessment proceedings, Assessing Officer raised a query regarding deposits not being offered as business income. Consequently, assessee offered income under section 44AD of the Act and also paid tax thereon before the assessment order was passed. The Assessing Officer levied penalty on the said additions. The Tribunal held that the business income was charged to tax on presumption basis Thus it is transpired that there was no deliberate act on the part of the assessee not to disclose the business receipts in his income tax return. Besides the element of income added during the quantum proceedings, there must be some material/circumstantial evidences leading to the reasonable conclusion that there was conscious concealment or the act of furnishing of inaccurate particulars on the part of the assessee.

Weblink

2 Article: Defense Against Prosecution U/S 276B in Post Covid Era [2020] 117 taxmann.com 830 (Article) Date or article: July 21, 2020 By: Priyansh Jain and Shubham Gupta

The Author has analyzed provisions of section 276B of the Income Tax Act, 1961 in regard to launching of prosecution proceedings for non-deposit of taxes deducted at source. The Author has further highlighted principles emanating from judicial precedents which may prove as possible defense against prosecution launched under section 276B of the Act.

Weblink

4 Dhruva Daily Volume 82 This document is for internal purposes only

2. Domestic Taxation – 2 Sr No

Name of case law and brief ratio

Summary of technical development Weblink for further reading

1 Aacharan Enterprises (P.) Ltd [2020] 117 taxmann.com 745 (Rajasthan) Set off loss against income referred to in section 115BBE of the Act

Finance Act, 2016 w.e.f. 1st April 2017 has amended provisions of section 115BBE of the Act to provide that no set off of any losses shall be allowed to assessee in computing income referred to in section 115BBE (i.e. deemed income under section 68, 69, 69A, 69B, 69C, 69D). Rajasthan High Court held that the amendment to section 115BBE prohibiting set off of losses is prospective in nature and assessee is entitled to claim set off loss against income determined under section 115BBE of the Act till AY 2016-17. Also, relied on CBDT Circular No. 11/2019.

Weblink

2 Sony Pictures Networks India Pvt. Ltd. (Successor of MSM Discovery Private Ltd.) [2020] 7 TMI 494 (Mumbai-Trib.) Deduction of education cess and secondary & higher education cess

Assessee filed an additional ground of appeal for claiming deduction of education cess and secondary & higher education cess, Mumbai ITAT after going through income tax return and assessment order admitted the additional ground of appeal filed by the assessee holding that the necessary facts for adjudicating the additional ground of appeal are already available on record and no additional facts are required to the brought on record. Further, directed the Assessing Officer to verify the facts and pass the order considering decision of Bombay High Court in case of Sesa Goa Limited. [2020] 117 taxmann.com 96 (Bombay).

Weblink

5 Dhruva Daily Volume 82 This document is for internal purposes only

3. International Taxation Sr No

Particulars of the update

Summary of technical development Weblink for further reading

1. SC dismisses Revenue's appeal in Samsung's PE constitution matter

In case of Samsung Heavy Industries Co. Ltd. v. Director of Income Tax (International Taxation) [2014] 42 taxmann.com 140 (Uttarakhand), the assessee entered into a contract between O.N.G.C. on the one hand and L&T on the other hand as consortium partners. The assessee received certain amount under said contract was attributable to activities carried out within India and balance was attributable to activities outside India. The Uttarakhand High Court held that the tax liability could not be fastened without establishing that the amount received for activities carried outside India is attributable to the tax identity or permanent establishment of the enterprise situated in India. The ruling was challenged before the Supreme Court. The Taxsutra alert reports Supreme Court dismissing the revenue’s appeal on the matter. The copy of the order is yet not available.

Weblink

2. FM emphasises on consensus-based solution for digital taxation at G-20 meet

The news report cites Finance Minister Nirmala Sitharaman comments at the G-20 finance ministers meeting on the issue of taxation of digital companies. She said the solution for the issue should have a consensus and should be simple, inclusive, and based on robust economic impact assessment.

Weblink

6 Dhruva Daily Volume 82 This document is for internal purposes only

4. SEBI Sr No

Particulars of the update

Summary of technical development Brief comments on impact

Weblink for further reading

1 SEBI amends Insider trading norms; entities to maintain database on UPSI

SEBI has amended insider trading norms vide its Notification dated 17.07.2020 as under: • The Board of directors of the organization

required to handle unpublished price-sensitive information (‘UPSI’) will have to maintain a structured digital database containing nature of UPSI and the names of such persons who have shared the information and also the names of such persons with whom information is shared under the new insider trading norm along with the PAN or any other identifier authorised by law where PAN is not available.

• Such database will not be outsourced and will be maintained internally with adequate internal controls and checks such as time stamping and audit trails to ensure non-tampering of the database.

• Structured digital database will be preserved

for a period of at least 8 years after completion of the relevant transactions and in the event of receipt of any information from the regulator regarding any investigation or enforcement proceedings, the relevant information in the structured digital database will be preserved till the completion of such proceedings.

• Further, entities would have to file the non-

compliance of code of conduct with the stock

SEBI amends insider trading norms which provides for maintaining a structured digital database containing nature of (UPSI), the names of persons who have shared the information. Further, entities would have to file the non-compliance of code of conduct with the stock exchanges.

Weblink

7 Dhruva Daily Volume 82 This document is for internal purposes only

Sr No

Particulars of the update

Summary of technical development Brief comments on impact

Weblink for further reading

exchanges, and the amounts if any collected for such non-compliances would be credited to the Investor Protection Education Fund administered by SEBI.

8 Dhruva Daily Volume 82 This document is for internal purposes only

5. GST Sr No

Particulars of the update

Summary of technical development Weblink for further reading

1. High Court of Delhi at New Delhi – M/s. Pitambra Books Pvt. Ltd. – W.P. (C) 627/2020 Dated 17 July 2020

The Petitioner is requesting the High Court to direct the Respondent to process the manual refund application filed for two consecutive years, from November 2017 to March 2019 on the grounds that the High Court in its order dated 21 January 2020 issued for the Petitioner, has stayed the operations of paragraph 8 of Circular No. 125/44/2019-GST dated 18th November 2019 restricting a tax payer to file a single refund application for two consecutive years.

The High Court accepted the request and directed the Respondent to process the refund application within three working days.

Weblink

2. Maharashtra Authority for Advance Ruling in the case of M/s Sundharams Private Ltd [Applicant] - Advance Ruling No. GST-ARA-36/ 2019-20/ B-41 dated March 18, 2020

The Applicant is engaged in providing warehousing, storage and support services to the OEMs of automobile industry. The Applicant has purchased Paver Blocks which are laid in the parking area of the land to ensure efficient and safe parking of automobiles of OEMs during the contract period. The Paver Blocks are not permanently embedded on earth and capable of being removed as such without causing damage for reuse elsewhere.

The Applicant sought the advance ruling on the issue whether ITC is available on GST paid on Paver Blocks laid on land being used in the course of providing its output services to customers. As per the Applicant, laying of Paver Blocks on land does not amount to construction of Immovable property u/s.17(5)(c) of the CGST Act and are to be construed as moveable items. Further, even if it is assumed that Paver Blocks are ‘Immovable Property’, ITC should be allowed in view of the Orissa High Court's decision in the case of Safari Retreats Pvt Ltd1. In this regard, the Authority observed and held as below:

Weblink

1 Safari Retreats Pvt Ltd. Vs. Chief Commr. of CGST [105 Taxmann 324]

9 Dhruva Daily Volume 82 This document is for internal purposes only

Sr No

Particulars of the update

Summary of technical development Weblink for further reading

a) In the Supreme Court Judgments in case of T.T.G Industries Ltd.2, it was concluded that if the chattel is movable to another place as such for use, it is movable but if it has to be dismantled and reassembled or re-erected at another place for such use, such chattel would be immovable. In the instant case, the Paver Blocks have to be dismantled and disassembled from the vacant land before being erected or assembled elsewhere. Applying the test laid down in above judgment, the laying of Paver Blocks to be used for parking purpose results in immovable property

b) It cannot be disputed that such Paver Blocks are not usually shifted from one place to another, nor is it practicable to shift them frequently. The Paver Blocks, once they are erected and assembled, continue to operate from where they are positioned and actually become a part of the parking facility. Having regard to the manner in which these parking facilities are erected using Paver Blocks, they do not answer the description of “goods”.

c) The objective to use paver blocks is to keep the tyres of the vehicles in good condition with no wear and tear, to have longevity, durability and flexibility to re-use. The flexibility to re-use does not mean that blocks will be removed and re-erected frequently. They are meant to be permanently fixed to earth but whenever the need arises the applicant may remove them and re-erect. Hence, it is concluded that the applicant would not use the paver blocks with an intention to remove it and use the same as a movable property.

d) In view of the above, the subject would qualify as immovable property and Applicant cannot avail ITC on the same as per Section 17(5)(d) of the CGST Act.

e) Further, reliance cannot be placed on the High court judgment in the case of M/s. Safari Retreats Pvt. Ltd. As the same is pending with the Hon'ble Supreme Court and has not attained finality.

2 T.T.G Industries Ltd. Vs. CCE [2004 (4) SCC]

10 Dhruva Daily Volume 82 This document is for internal purposes only

11 Dhruva Daily Volume 82 This document is for internal purposes only

END Confidential: This document is for your internal use only and may not be copied or distributed to any third party © Dhruva Advisors LLP

1 Dhruva Daily Volume 83 This document is for internal purposes only

JULY 23

VOLUME 83

DHRUVA DAILY

2 Dhruva Daily Volume 83 This document is for internal purposes only

Table of Contents 1. Domestic Taxation - 1 ...................................................................................................................................................................... 3

2. Domestic Taxation – 2 ..................................................................................................................................................................... 4

3. International Taxation ..................................................................................................................................................................... 6

4. M&A – Tax related............................................................................................................................................................................ 8

5. SEBI .................................................................................................................................................................................................. 9

6. GST ................................................................................................................................................................................................. 10

3 Dhruva Daily Volume 83 This document is for internal purposes only

1. Domestic Taxation - 1 Sr No

Particulars of the update Summary of technical development

Weblink for further reading

1 PCIT v. Vodafone Idea Ltd SLP No. 8318/2020 Date of order: 22 July 2020 SC dismisses Revenue’s SLP against HC direction for release of Rs. 833 crore refund to Vodafone Idea

SC dismisses revenue’s SLP against Bombay HC order directing refund of Rs. 833 crore to Vodafone Idea Ltd for AY 2014-15. AO had issued intimation under section 245 proposing certain adjustments to the refund and also passed order under section 245 on 28th May 2020 determining the net refund of Rs. 833 Cr, however no refund was released to the assessee despite many reminders. HC had held that already having invoked powers under section 245, Revenue “cannot withheld the admitted refundable amount on the ground that the respondents may have a future demand against the petitioner arising out of the pending assessment orders”.

Weblink

2 Article: Assessment of Non - Existing Entity or Dead Person - Can the Revenue plead Oblivious? Date of article: 21 July 2020 By: Sunil Maloo Source: Taxsutra

The Author has analysed the recent judgement of Delhi High Court Savita Kapila legal heir of late Shri Mohinder Paul Kapila v. ACIT [TS-5232-HC-2020 (Delhi)-O] where revenue was pleading oblivious of death of assessee. The High Court has categorically ruled that there is no provision under the Income Tax Act, 1961 which obligates the legal heir to intimate the death of the Assessee to the department. Therefore, the revenue cannot plead oblivious. Similarly, the Karnataka High Court in the case of M/s eMudhra Ltd. v. ACIT in [TS-5948-HC-2019 (Karnataka)-O], made a speaking observation that once notice is issued by the Registrar of Companies to the Income-tax Department with respect to the proceedings of the amalgamation, then subsequently the Department cannot plea oblivious of the fact of the amalgamation.

Weblink

4 Dhruva Daily Volume 83 This document is for internal purposes only

2. Domestic Taxation – 2 Sr No

Particulars of the update

Summary of technical development Brief comments on impact Weblink for further reading

1 Shiv Raj Gupta v CIT Civil Appeal No. 12044 of 2016 Supreme Court

Assessee was the Chairman and Managing Director of a liquor manufacturing company. During the year under consideration assessee sold the controlling stake of the liquor manufacturing company. In addition to the consideration for shares, assessee also received a non – compete fees from the acquiring company given that he had an experience of 35 years and could easily join a rival company. Assessing Officer held that the compensation received as non -compete fees was a colourable device to avoid tax as there was no real competition and characterized the non – compete fees as compensation received for termination of the management of the company and taxed the same under Section 28(ii)(a). CIT(A) upheld the order of the Assessing Officer. Tribunal accepted the contentions of the assessee. Against this Revenue went into appeal before the High Court. High Court held that it is taxable as consideration received for transfer of shares. On an appeal to the Supreme Court by the assessee, SC held that commercial expediency has to be judged from the viewpoint of the assessee and Department cannot enter into the thicket of reasonableness of amounts paid. Further,

Commercial expediency has to be judged from the viewpoint of the assessee. Further, non – compete fees is a capital receipt and cannot be taxed prior to 1st April 2003.

Weblink

5 Dhruva Daily Volume 83 This document is for internal purposes only

Sr No

Particulars of the update

Summary of technical development Brief comments on impact Weblink for further reading

relying on the judgement of Guffic Chem (P.) Ltd., SC held that non-compete fees is a capital receipt and not taxable.

2 Yes Bank Ltd. v DCIT ITA No. 3497/Mum/2018 Mumbai ITAT

During the year, assessee raised funds by issuing shares to Qualified Institutional Buyers (‘QIB’). The assessee claimed the expenditure incurred on issue of shares u/s 35D. Assessing Officer disallowed the expenditure holding that QIB cannot be regarded as public. CIT(A) upheld the order of the Assessing Officer. Before the Tribunal, assessee contended that the issue is directly covered by the judgement of Hyderabad Tribunal in the case of Deccan Chronicle. Revenue contended that as per SEBI ICDR Regulations shares issued to QIB cannot be termed as public issue. Tribunal after referring to the provisions of SEBI Listing Agreement and Securities Contracts (Regulations) Rules, 1957 concluded that issue of shares to QIB is a public issue. Further, relying on the judgement of Hyderabad Tribunal in the case of Deccan Chronicle, the Tribunal allowed the deduction under section 35D of the Act.

As per the provisions of SEBI Listing Agreement and Securities Contracts (Regulations) Rules, shares issued to QIB tantamount to shares issued to public.

Weblink

6 Dhruva Daily Volume 83 This document is for internal purposes only

3. International Taxation Sr No

Particulars of the update

Summary of technical development Weblink for further reading

1. Further Details of OECD Digital Tax Plan Taking Shape

The OECD’s digital tax overhaul will reallocate corporate losses as well as profits, Grace Perez-Navarro, deputy director of the OECD’s Center for Tax Policy and Administration has said. The announcement is welcome news to the businesses that have expressed concerns that Pillar One solution may not acknowledge their losses. In the context of Dispute Resolution, he said that the OECD is developing a “two-phase process, using panels with an initial determination process,” where a second panel will make the decision if a first panel isn’t able to agree. This is expected to be a binding process. The blueprints containing technical details of features of the unified approach for Pillar One and Pillar Two is targeted by October this year.

Weblink

2. Taxsutra Eye Share : Indirect Transfers and the Indian Revenue: Are We Back to Square One?

In backdrop of recent AAR ruling in case of Tiger Global International Holdings, the article discusses provisions of tax treaty on taxability of indirect transfer. The author opines that there is an anomaly in the reasoning of the AAR where the Authority has concluded that while direct transfers were excluded from the taxing right of the source state but the indirect transfers were taxable in the source state. The Hon'ble Supreme Court in case of Vodafone, 341 ITR 1 held that domestic law, at the time, did not provide for taxing rights in an indirect transfer. The author states that it cannot be a position that pre-2012 amended Income tax Act did not provide taxing capital gains through indirect transfer in the domestic provisions, however, the treaty [always] “intended” taxing rights of an indirect transfer in the source state. This precisely is the fall out of the interpretation given by the AAR to the Treaty provisions.

Weblink

3. I SA / Sz 944/19 - Judgment of the Provincial Administrative Court in Szczecin from 2020-03-31

During the subject year 2014, the taxpayer, a Polish company issued dividends to its Cyprus based parent company (which was claimed as tax-exempt and hence no taxes withheld in terms of the Tax Treaty between Poland-Cyprus). However, the Cypriot parent on the same day issued such dividends to its parent company in Slovakia, which further issued to its shareholders (Individual Polish tax residents, who were originally the founders and shareholders of the taxpayer before restructuring made in the same year, 2014).

Weblink

7 Dhruva Daily Volume 83 This document is for internal purposes only

Sr No

Particulars of the update

Summary of technical development Weblink for further reading

Poland Provincial Administrative Court ruled that Cypriot parent company, was not the "beneficial owner" of dividends declared by the Polish entity and accordingly denied the treaty benefit claimed by the tax payer. The Polish Revenue determined that the actual beneficiaries of the dividend paid were the long-term shareholders of the taxpayer i.e., the Polish individual tax residents and hence, the dividends must be taxed at 19% (as provided under the domestic law) as against 0% (as provided under the Poland-Cyprus Treaty). The Court observed that a beneficiary is a person who actually receives the dividend and can dispose it on its own and clarified that the mere fact of being a resident of a particular country and receiving a payment is not a sufficient condition to avail treaty benefits, where the right to dispose of income is limited.

8 Dhruva Daily Volume 83 This document is for internal purposes only

4. M&A – Tax related Sr No

Particulars of the update

Summary of technical development Brief comments on impact Weblink for further reading

1 M/s Archroma India Pvt. Ltd. v. ITO [ITA No. 6919/Mum/2018] – ITAT holds that slump sale falls within the ambit of succession, restricts applicability of 5th proviso to section 32 to assets taken over from transferor company but not on goodwill

The assessee had purchased a business undertaking by under a business transfer agreement. A part of excess of the purchase consideration over the WDV was considered as towards customer distribution network and balance excess was considered as goodwill. In these facts, the Tribunal held that acquisition of business on slump sale basis qualifies as succession u/s 170 and application of 5th proviso (now 6th proviso) to section 32(1) cannot be precluded on the basis that there are separate provisions (viz. sections 50B and 2(42C)) dealing with slump sale. The Tribunal further held that invocation of 5th proviso to section 32(1) is correct for computation of depreciation on WDV of assets taken over from transferor company. The difference between slump sale value and the WDV of assets taken over would qualify as goodwill and be consequently eligible for depreciation.

This decision provides a definite view on the issue of whether slump sale of business amounts to succession under section 170, which may be useful considering that precedents on this issue are otherwise limited. Further, the decision may also be helpful in defending the claim of tax depreciation on goodwill in case of slump acquisition transaction, especially since the Tribunal has considered and ruled out the application of 5th proviso to section 32(1) on goodwill.

Weblink

9 Dhruva Daily Volume 83 This document is for internal purposes only

5. SEBI Sr No

Particulars of the update

Summary of technical development Brief comments on impact

Weblink for further reading

1 Reporting to Stock Exchange regarding violations under SEBI PIT Regulations relating to code of conduct

• The listed companies shall promptly inform the Stock exchange(s) where the concerned securities are traded, regarding violations relating to Code of Conduct (‘CoC’) under PIT Regulations in such form and manner as may be specified by the Board from time to time in terms of clause 13 of Schedule B (in case of listed companies).

• SEBI, vide circular dated July 19, 2019, had specified the standard format for reporting of violations related to CoC.

• The said format has been suitably modified

and placed at Annexure A of the SEBI Circular dated 23 July 2020. The listed companies, intermediaries and fiduciaries shall inform the violations of PIT Regulations relating to CoC as per the revised format to the Stock Exchange(s).

SEBI has prescribed revised format for reporting of violation of Code of Conduct to the Stock exchange.

Weblink

2 Trading Window Restrictions

• Trading window restrictions shall not apply in respect of Offer for Sale (‘OFS’) and Rights Entitlements (‘RE’) transactions carried out in accordance with the framework specified by the Board from time to time.

N.A. Weblink

10 Dhruva Daily Volume 83 This document is for internal purposes only

6. GST Sr No

Particulars of the update

Summary of technical development Weblink for further reading

1. Circular No. 6/2020- GST dated 16 June 2020 – Office of the Commissioner of State Tax, State Goods & Services Tax Department, Kerala

The circular highlights the issue of inadequate settlement of IGST tax from Centre to State revenue due incorrect or non-disclosure of ineligible credit under Section 17(4) (restricting ITC @ 50% for banking company and financial institutions), 17(5) (blocked credits) of the CGST Act, 2017 and reversal under Rule 42 and 43 of the CGST Rules, 2017, in GSTR-3B.

The circular has also instructed on correct table numbers, in GSTR-3B, under which such ineligible credits are required to be reported. Further, the circular has also directed taxpayers to rectify there past returns in the following manner:

a. For FY 2018-19 – Disclose ineligible credit in GSTR-9 to be filed for the said year

b. FY 2019-20 – Rectifications to be made in GSTR-3B for the period from April 2020 to September 2020

c. For GSTR-3B from April 2020 – Rectifications to be made in subsequent GSTR-3B to be filed by the taxpayer.

Weblink 1

Weblink 2

11 Dhruva Daily Volume 83 This document is for internal purposes only

END Confidential: This document is for your internal use only and may not be copied or distributed to any third party © Dhruva Advisors LLP

1 Dhruva Daily Volume 84 This document is for internal purposes only

JULY 24

VOLUME 84

DHRUVA DAILY

2 Dhruva Daily Volume 84 This document is for internal purposes only

Table of Contents 1. Domestic Taxation - 1 ...................................................................................................................................................................... 3

2. Domestic Taxation – 2 ..................................................................................................................................................................... 4

3. International Taxation ..................................................................................................................................................................... 5

3 Dhruva Daily Volume 84 This document is for internal purposes only

1. Domestic Taxation - 1 Sr No

Particulars of the update Summary of technical development

Weblink for further reading

1 Article: Whether dismissal of SLP by Hon’ble Apex Court creates a binding precedence? [2020] 117 taxmann.com 858 (Article) Date or article: July 21, 2020 By: D.C Agrawal and Y.K Gupta

The Author has analyzed the implications arising from exercise of powers of supreme court under Article 136 of the Constitution regarding grant of Special Leave. The Author has further analyzed whether binding precedence will be created in the following cases wherein: • SLP was dismissed by non – speaking order • SLP was dismissed after assigning reason • SLP was granted but dismissed without reason SLP is admitted but pending

Weblink

2 CBDT's 'Voluntary Compliance' E-campaign - A Clarion Call for Non-filers, Defaulters? Source : Taxsutra

IT Department launched the first of its kind e-campaign on voluntary compliance for filing time-barring belated/ revised returns for FY 2018-19 earlier this week, and it shall continue till the month-end, focusing on taxpayers who are either non-filers or have discrepancies or deficiency in their returns. Will this CBDT initiative promote voluntary compliance and lead to fewer high-pitched assessments and reduce litigation Mr Ameet N. Patel (Manohar Chowdhry & Associates), Pramod Achuthan (Ernst & Young LLP) and Shailesh Kumar (Nangia & Co LLP) have shared their views on the same.

Weblink

4 Dhruva Daily Volume 84 This document is for internal purposes only

2. Domestic Taxation – 2 Sr No

Particulars of the update

Summary of technical development Brief comments on impact Weblink for further reading

1 M/s. Telekon Media India Pvt. Ltd. v ITO 2020 (7) TMI 537- ITAT Delhi

During the year under consideration, the assessee has leased out workstation i.e. plant, machinery or furniture along with the building, and offered the income under the head ‘Income from House Property’. Assessing Officer held that letting out of workstation was inseparable from letting out of the building and brought the same to tax under the head ‘Income from Other sources’. CIT(A) upheld the order of the Assessing Officer. Tribunal, after referring to the agreement observed that interest has been created in the workstations as property only and not in the building. Further, Tribunal observed that rent has fixed in terms of workstations leased out. From the above, the Tribunal concluded that use of building is incidental to the letting out of workstations and the prime objective was exploitation of asset in the from of workstations. Accordingly, the appeal of the assessee was rejected.

Prime objective of letting out has to be ascertained from the lease agreement and taxability of income arising from lease shall be as per the prime objective of lease.

Weblink

5 Dhruva Daily Volume 84 This document is for internal purposes only

3. International Taxation Sr No

Particulars of the update

Summary of technical development Weblink for further reading

1. Mumbai ITAT : Software license payment for database access, not royalty under India-Singapore DTAA Reliance Corporate IT Park Limited vs DCIT [ITA No 7300/Mum/2016]

The assessee made a payment for database access to a Singapore entity. Although assessee had deducted tax at 10% while making the remittance, the assessee preferred an appeal under section 248 of the Act against the TDS liability, claiming that no tax is deductible on payment made for purchase of software license. The CIT(A) treated the payment as royalty since access to “significant proprietary database” was being allowed to the assessee by the software. The Tribunal relied on judicial precedents and held that when database access by itself does not result in taxation as royalty, such database access being coupled with software licence cannot bring the software consideration within the scope of royalty under India-Singapore DTAA.

Weblink

6 Dhruva Daily Volume 84 This document is for internal purposes only

END Confidential: This document is for your internal use only and may not be copied or distributed to any third party © Dhruva Advisors LLP